Strategic%20 innovation%20new%20game%20strategies%20for%20competitive%20advantage

503

-

Upload

mitesh-take -

Category

Design

-

view

77 -

download

0

Transcript of Strategic%20 innovation%20new%20game%20strategies%20for%20competitive%20advantage

Strategic Innovation

In today’s fast-changing business environment, those firms that want to remaincompetitive must also be innovative. Innovation is not simply developing newtechnologies into new products or services, but in many cases finding newmodels for doing business in the face of change. It often entails changing therules of the game.

From the late 1990s to today, the dominant themes in the strategy literaturehave been strategic innovation, the impact of information and communicationstechnologies on commerce, and globalization. The primary issues have beenand continue to be how to gain a competitive advantage through strategicinnovation using new game strategies, and how to compete in a world withrapid technological change and increasing globalization. Strategic Innovationdemonstrates to students how to create and appropriate value using these “newgame” strategies. Beginning with a summary of the major strategic frameworksshowing the origins of strategic innovation, Afuah gives a thorough examin-ation of contemporary strategy from an innovation standpoint with several keyadvantages:

• Focus on developing strategy in the face of change.• A wealth of quantitative examples of successful strategies, as well as

descriptive cases.• Emphasis on the analysis of strategy, not just descriptions of strategies.• A detailed, change-inclusive framework for assessing the profitability

potential of a strategy or product, the AVAC (activities, value, appropri-ability, and change) model.

• Emphasis on the aspects of strategy that can be linked to the determinantsof profitability.

• Consideration of how both for-profit and non-profit organizations canbenefit from new game strategies.

Allan Afuah is Associate Professor of Strategy and International Business at theStephen M. Ross School of Business, University of Michigan.

Strategic Innovation

New Game Strategies forCompetitive Advantage

Allan Afuah

Stephen M. Ross School of Business

University of Michigan

First published 2009by Routledge270 Madison Ave, New York, NY 10016

Simultaneously published in the UKby Routledge2 Park Square, Milton Park, Abingdon, Oxon OX14 4RN

Routledge is an imprint of the Taylor & Francis Group,an informa business

© 2009 Allan Afuah

All rights reserved. No part of this book may be reprinted orreproduced or utilized in any form or by any electronic, mechanicalor other means, now known or hereafter invented, includingphotocopying and recording, or in any information storage orretrieval system, without permission in writing from the publishers.

Trademark Notice: Product or corporate names may betrademarks or registered trademarks, and are used only foridentification and explanation without intent to infringe.

Library of Congress Cataloging-in-Publication DataAfuah, Allan.Strategic innovation: new game strategies for competitiveadvantage / by Allan Afuah.

p. cm.Includes index.1. Strategic planning. 2. Originality. 3. Resourcefulness.4. Technological innovations. 5. Competition. I. Title.HD30.28.A3473 2009658.4′063—dc222008034812

ISBN10: 0–415–99781–X (hbk)ISBN10: 0–415–99782–8 (pbk)ISBN10: 0–203–88324–1 (ebk)

ISBN13: 978–0–415–99781–2 (hbk)ISBN13: 978–0–415–99782–9 (pbk)ISBN13: 978–0–203–88324–2 (ebk)

This edition published in the Taylor & Francis e-Library, 2009.

“To purchase your own copy of this or any of Taylor & Francis or Routledge’scollection of thousands of eBooks please go to www.eBookstore.tandf.co.uk.”

ISBN 0-203-88324-1 Master e-book ISBN

To my grandmother, Veronica Masang-Namang Nkweta, and theBamboutos highlands which she tilled to feed me.

To every family that has been kind enough to welcome a foreignstudent to its home.

Contents

List of Figures ixList of Tables xiList of Exhibits for Cases xiiiPreface xvAcknowledgments xix

PART IIntroduction 1

1 Introduction and Overview 3

2 Assessing the Profitability Potential of a Strategy 35

3 The Long Tail and New Games 67

PART IIStrengths and Weaknesses 89

4 Creating and Appropriating Value Using New GameStrategies 91

5 Resources and Capabilities in the Face of New Games 117

6 First-mover Advantages/Disadvantages andCompetitors’ Handicaps 145

7 Implementing New Game Strategies 178

PART IIIOpportunities and Threats 197

8 Disruptive Technologies as New Games 199

9 Globalization and New Games 223

10 New Game Environments and the Role of Governments 252

11 Coopetition and Game Theory 275

PART IVApplications 301

12 Entering a New Business Using New Games 303

13 Strategy Frameworks and Measures 323

PART VCases 371

Case 1 The New World Invades France’s Terroir 373

Case 2 Sephora Takes on America 377

Case 3 Netflix: Responding to Blockbuster, Again 383

Case 4 Threadless in Chicago 391

Case 5 Pixar Changes the Rules of the Game 393

Case 6 Lipitor: The World’s Best-selling Drug (2008) 401

Case 7 New Belgium: Brewing a New Game 405

Case 8 Botox: How Long Would the Smile Last? 411

Case 9 IKEA Lands in the New World 417

Case 10 Esperion: Drano for Your Arteries? 422

Case 11 Xbox 360: Will the Second Time be Better? 434

Case 12 Nintendo Wii: A Game-changing Move 442

Notes 447Author Index 469Subject Index 473

viii Contents

Figures

1.1 Business System and Options for New Games 81.2 Components of a New Game Strategy 181.3 Types of New Game 241.4 Flow of the Book 302.1 Components of an AVAC Analysis 392.2 Drivers of the Components of an AVAC Analysis 413.1 A Long Tail Distribution 683.2 Impact of the Internet on a Long Tail Distribution 713.3 Value System of Long Tail Potential Coopetitors 714.1 Value Creation and Appropriation 924.2 A Book Value Chain 984.3 New Game Activities and Value Creation and Capture 1105.1 The Role of Complementary Assets 1255.2 Strategies for Exploiting Complementary Assets 1266.1 Types of Player 1636.2 Different New Game Product Strategies 1676.3 Player Types in Different Countries 1676.4 A Firm’s Evolution from Explorer to Exploiter 1687.1 Strategy, Structure, Systems, People, and

Environment (S3PE) Framework 1797.2 What Should a Firm Do? 1868.1 S-curves Showing Physical Limits of Technologies 2018.2 PC versus Mainframes and Minicomputers 2048.3 Disruptive Technologies and Value Creation and

Appropriation 2118.4 Disruptiveness of Disruptive Technologies 2198.5 Examples of Degrees of Disruptiveness 2199.1 Who Appropriates How Much from Nigerian Oil? 2289.2 Effect of Taxes on Value Appropriation 2299.3 Effect of Subsidies on Value Appropriation 2309.4 Who Appropriates More Value than It Creates? 2319.5 Types of Multinational 2339.6 Different Global Strategies 239

10.1 The Macroenvironment 25310.2 Determinants of Environments that are Conducive to

Profitable New Games 25710.3 A PESTN Analysis 271

11.1 A Payoff Matrix 27711.2 Dominant Strategy 27811.3 Nash Equilibrium 27911.4 Prisoner’s Dilemma 28111.5 A Sequential Game 28211.6 Players in a Value Creation and Appropriation Game 29011.7 For Question 1 30013.1 SWOT Framework 32613.2 Elements of a PESTN Framework 32913.3 BCG’s Growth/Share Matrix 33113.4 Illustration of Growth/Share Matrix 33313.5 GE/McKinsey Matrix 33513.6 Porter’s Five Competitive Forces 33713.7 Components of Porter’s Five Forces 33913.8 Business System for a Technology Firm 34413.9 An Automobile Maker’s Business System 34513.10 A Generic Value Chain 34613.11 A Value System 34713.12 A Value Network 34913.13 A Value Shop 35013.14 Elements of the Balanced Scorecard 35113.15 Elements of the S3PE 35813.16 Elements of the 4Ps 35913.17 Components of an AVAC Framework 362

x Figures

Tables

1.1 Competitive Consequences of New Game Strategy 191.2 Costs, Retail, and Wholesale Prices 211.3 Forecasted Console and Games Sales 211.4 Estimates of the Profitability of Three Different Strategies 222.1 Applications of AVAC Analysis 522.2 Selected Financials 542.3 Customer Service for Year Ending March 2005 552.4 Industry Leading Margins for Year Ending March 2005 552.5 Back-of-the-envelope Estimates of the Contribution

of Some Activities to Low Cost and Revenues 583.1 The Activities Component of an iTunes AVAC Analysis 813.2 The Value Component of an iTunes AVAC Analysis 823.3 The Appropriability Component of an iTunes AVAC

Analysis 833.4 The Change Component of an iTunes AVAC Analysis 853.5 Strategic Consequences of an AVAC analysis of

Apple’s iTunes Activities 864.1 Some Estimated Costs for the iPhone in 2007 994.2 October 2005 Top 8 Most Expensive Components/

Inputs of a 30GB iPod 1165.1 Rank Ordering Resources/Capabilities by

Competitive Consequence 1295.2 Strategic Consequence for Google’s Search Engine

Capabilities 1355.3 Rank Ordering Complementary Assets 1365.4 Is a Strength from a Previous Game a Strength or

Handicap in a New Game? 1375.5 Sample Values of Intangible Resources (all numbers,

except rations, in $ billion) 1406.1 First-mover Advantages (FMAs) 1466.2 Rank Ordering First-mover Advantages 1586.3 Lipitor’s Projected Sales 1736.4 NPVs for the Different Revenue Flows 1737.1 Is an S2P Component from a Previous Game a

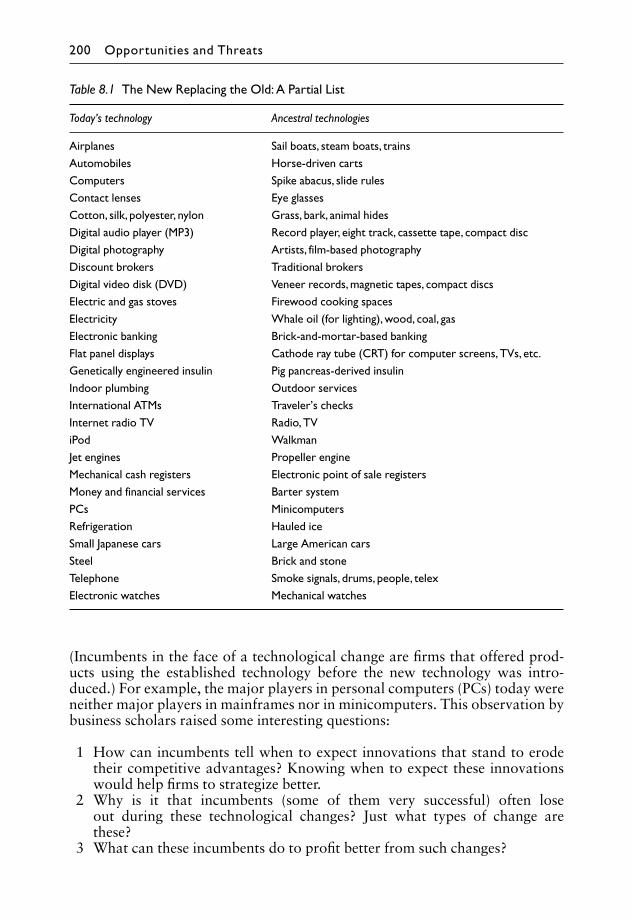

Strength or Handicap in a New Game? 1918.1 The New Replacing the Old: A Partial List 2008.2 The Disrupted and Disruptors? 205

8.3 To What Extent is Technological Change Disruptiveto an Established Technology? 207

8.4 Are Previous Strengths Still Strengths or Have theyBecome Handicaps in the Face of a Disruptive Technology? 211

9.1 June 2007 OECD Gasoline Prices and Taxes 2259.2 Oil Joint Ventures in Nigeria 2259.3 What Each Player Gets 2269.4 How Much Does each OECD Member Appropriate

from a Gallon of Gasoline? 2279.5 What Each Player Appropriates 251

11.1 A Mapping of Coalitions into Value Created 28811.2 Coalitions (submarkets) and Value Created 29211.3 Value Added and Guaranteed Minimum 29312.1 Type of New Game to Pursue When Entering a New

Business 31913.1 Elements of a VIDE Analysis 35513.2 Strategic Management Frameworks: A Comparison 36513.3 Summary of Some Financial Measures 368

xii Tables

Exhibits for Cases

1.1 Hierarchy of French Wines 3741.2 World Wine Exports in 1999 and 2007 3762.1 Comparison of Industry Competitors in 2007 3813.1 Summary of Netflix’s Income Statements

($US millions, except where indicated) 3853.2 Summary of Netflix’s Movie Rental Plans 3863.3 Summary of Blockbuster’s Income Statements

($US millions, except where indicated) 3883.4 Summary of Blockbuster Total Access Movie Rental Plans 3885.1 An Animation Movie Value Chain 3955.2 Pixar Full-length Animation Movies 3995.3 Top 12 Grossing Animation Movies 4005.4 Competing Animation Movies 4006.1 US Market Shares of Cholesterol-lowering Drugs,

January 1997 4026.2 The Drug Development Process in the USA 4036.3 Statin Average Prescription Pricing Structure 4046.4 1997 Lipitor Worldwide Sales Projections 4047.1 Average Cost of Goods Sold for United States Brewery 4057.2 Cost Implications of Generator Purchase 4088.1 2008 Plastic Surgery Fees 4138.2 Allergan’s Product Areas 4158.3 Allergan’s Products in 2008 4159.1 IKEA Sales 4179.2 Purchasing 4199.3 Top Sales Countries in 2007 4199.4 Where the Money Goes 421

10.1 Selected Disease Statistics—USA 2003 42310.2 Drug Development Process 42510.3 Drug Trial Expenses per Approved Compound 42610.4 Total Hypolipemic Market Sales and Expectations 42610.5 2002 Select Pharmaceutical Company Financial

Information ($000s) 42710.6 Nominal and Real Cost-of-Capital (COC) for the

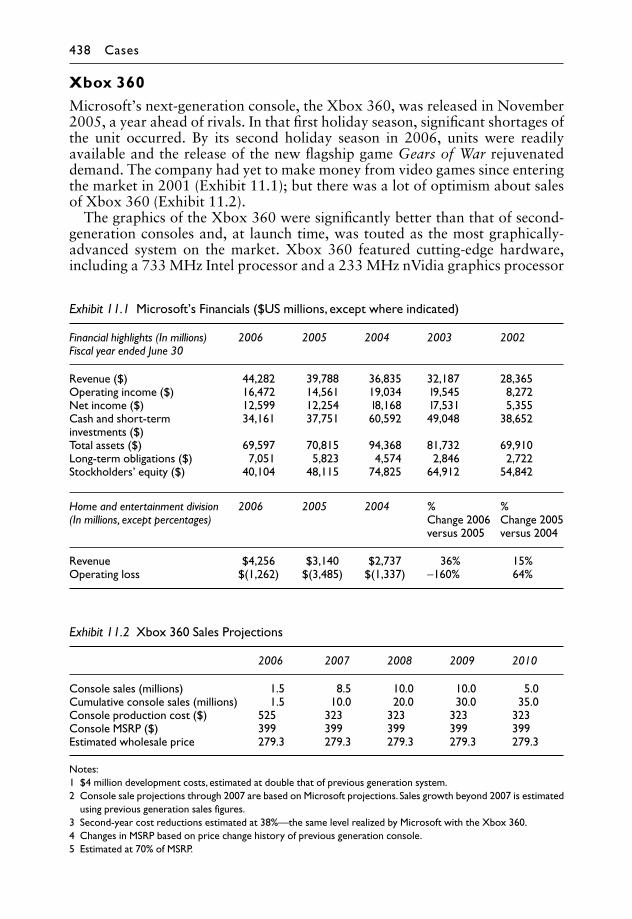

Pharmaceutical Industry, 1985–2000 42711.1 Microsoft’s Financials

($US millions, except where indicated) 438

11.2 Xbox 360 Sales Projections 43811.3 Playstation 3 Sales Projections 43911.4 Sony’s Summary Financials

($US millions, except where indicated) 44011.5 Game Sales Information 44112.1 Xbox 2001 Forecast Sales, Costs, and Prices 44312.2 Costs, Retail, and Wholesale Prices 44512.3 Forecasted Console and Games Sales 446

xiv Exhibits for Cases

Preface

The first question that potential readers might be tempted to ask is, whyanother book on strategy? Strategic Innovation: New Game Strategies forCompetitive Advantage has many of the same features that existing textbookshave. It draws on the latest research in strategic management and innovation, itis peppered with the latest examples from key business cases, it is easy to read,and so on. However, it has six distinctive features that give it a unique positionvis-à-vis existing strategy and innovation books.

Distinctive FeaturesFirst, Strategic Innovation: New Game Strategies for Competitive Advantage isabout change. While existing textbooks acknowledge the importance ofchange, especially in an ever-changing world, they devote very little or no atten-tion to the subject of change. All the chapters in New Game Strategies are aboutchange and strategic management—about how to create and appropriate valuein the face of new games. Second, existing strategic management texts tend tohave very few or no numerical examples. This lack of numerical examples doeslittle to reinforce the growing consensus that strategy is about winning butrather, it might be promoting the “anything goes in strategy” attitude that is notuncommon to students who are new to the field of strategic management. Nineof the thirteen chapters in the book have numerical examples that link elementsof the balance sheet to components of the income statement. Of course, thebook is also full of case examples. Third, while other texts are more descriptivethan analytical, this book is more analytical than descriptive. It is largely aboutthe why and how of things, and less about the what of things. Fourth, the bookincludes a detailed framework for assessing the profitability potential of a strat-egy, resource, business unit, brand, product, etc. Called the AVAC (activities,value, appropriability, and change), the framework is distinctive in that itincludes not only both firm-specific and industry-specific factors that impactfirm profitability, but also a change component. Fifth, the book’s emphasis is onthose activities that can be linked to the determinants of profitability; that is, thebook focuses on those aspects of strategy that can be logically linked to elem-ents of the balance sheet and income statement. Sixth, the book summarizes themajor strategic management frameworks that are otherwise scattered in othertexts. This is a useful one-stop reference for many students.

The Dawn of Strategic InnovationTo understand why a book with these six features is needed today in the field ofstrategic management, it is important to take a quick look at the evolution ofthe field. In the 1960s, the dominant theme in the field of strategic managementwas corporate planning and managers were largely concerned with planning forthe growth that had been spurred by reconstruction of Europe and Japan, andthe Cold War, following World War II. The SWOT (Strength, Weaknesses,Opportunities, and Threats) framework became popular as the tool of choicefor identifying and analyzing those internal and external factors that werefavorable or unfavorable to achieving firm objectives. In the late 1960s andearly 1970s, the primary theme had shifted to corporate strategy and the issuesof the day were dominated by diversification and portfolio planning. Tools suchas BCG’s Growth/Share matrix, and the McKinsey/GE matrix enjoyed a lot ofpopularity as analysis tools. In the late 1970s and early 1980s, the theme shiftedto industry and competitive analysis, and the primary issues became the choiceof which industries, markets, and market segments in which to compete, andwhere within each industry or market to position oneself. Porter’s Five Forcesand business system (value chain) were the analytical tools of the day. In the late1980s and early 1990s, the theme had evolved into the pursuit of competitiveadvantage and its sources within a firm. Professors C.K. Prahalad and GaryHamel’s core competence of the firm and the resource-based view of the firmemerged as the dominant themes.

From the late 1990s to today, the dominant themes have been strategicinnovation, globalization, and the impact of information and communicationstechnologies on value-adding activities. The primary issues have been and con-tinue to be how to gain a competitive advantage through strategic innovationusing new game strategies, and how to compete in a world with rapid techno-logical change and increasing globalization. A strategic innovation is a game-changing innovation in products/services, business models, business processes,and/or positioning vis-à-vis coopetitors to improve performance. A firm’s newgame strategy is what enables it to perform well or not so well in the face of astrategic innovation. Thus, to perform better than its competitors in the face ofa new game, a firm needs to have the right new game strategies. This book isabout the new game strategies that firms use to exploit strategic innovations. Itis about change. It is about how to create and appropriate value using new gamestrategies. These new game strategies can be revolutionary or incremental, orsomewhere in-between. This book is not only about a firm using new gameactivities to offer customers new value (from new products/services) that theyprefer to that from competitors, but also about how the firm can better positionitself to appropriate the value created in the face of change or no change, and totranslate the value and position to money. It is also about some of the morerecent issues about the digital economy such as the Long Tail, and the not-so-recent issues such as disruptive technologies. Firms that initiate new games, andare therefore first movers, can make a lot of money; but so can firms that followthe first movers. It all depends on the new game strategy that each firm pursues.

xvi Preface

Some Strategic Innovation QuestionsNew game strategies often overturn the way value is created and appropri-ated. They can create new markets and industries, destroy or reinforce exist-ing product-market positions, and most important of all, they can be veryprofitable for some firms. This raises some very interesting questions. Whatexactly are new game strategies? What do we mean by creation and appropri-ation of value? Which new game strategies are likely to be most profitable fora firm—to give a firm a competitive advantage? If resources are really thecornerstones of competitive advantage, what is the role of resources duringnew games? Since, in playing new games, firms often move first, what reallyare first-mover advantages and disadvantages, and how can one take advan-tage of them? What are competitor’s handicaps and how can a first movertake advantage of them? How can the profitability potential of a strategy—new game or non-new game—be analyzed? Is entering a new business usingnew game strategies any better than entering using non-new game strategies?Does game theory have anything to do with new game strategies? What islikely to be the reaction of competitors when a firm pursues a new gamestrategy? Given competitors’ likely reaction, what should a firm do in pursu-ing new game strategies? Does implementing new game strategies requiremore precaution than implementing any other strategy? What are the sourcesof new game strategies? What is the role of globalization and a firm’smacroenvironment in its ability to create and appropriate value using new gamestrategies? Are some environments more conducive to new game strategiesthan others? What is the role of government in new games? How many ofthe new game concepts and tools detailed for for-profit firms applicable tononprofit organizations?

This book explores these questions, or provides the concepts and tools toexplore them. The book takes the perspective of a general manager who hasoverall responsibility for the performance of his or her firm, for a business unitwithin the firm, or for any organization for which performance is important.Such a manager needs to understand the basis for the firm’s performance in theface of change. The manager needs to know what determines the performance,what other change might erode that performance, and when and what the firmcould do to gain and maintain a competitive advantage. The manager must thenuse the firm’s resources to formulate and implement a strategy that will give it acompetitive advantage. Thus, the book should be useful in courses whose goalis to challenge students to think strategically when confronting day-to-dayactivities. It should also be useful to managers who want to challenge them-selves to think strategically, irrespective of their functional role within theirorganization.

The seeds of the book were sowed in the period from 1997 to 2006 when Itaught the Strategy Core Course at the Stephen M. Ross School of Business atthe University of Michigan. During that time, I also taught an elective in Innov-ation Management. In 2003/2004 when I was on academic sabbatical leavefrom Michigan, I also taught the core course in strategy at The Wharton Schoolof the University of Pennsylvania in the USA, and at INSEAD, in Fontainebleau,France. The ideas that most of my students in these schools found fascinatinghad a common theme—changing the rules of the game. Students could not have

Preface xvii

enough of the concepts and cases about strategic innovation, and the associatednew game strategies for a competitive advantage.

Intended AudienceThe book is written for courses in strategic management, entrepreneurship, ormarketing that emphasize strategic innovation or change in a graduate orundergraduate curriculum. It should also be useful to managers who want tochallenge themselves to think strategically, irrespective of their functional rolewithin their organization. Managers and scholars who are interested in explor-ing any of the questions raised above would also find the book useful; so shouldthose managers who are in positions that have a direct impact on firm profit-ability, or who are in consulting, entrepreneurship, or venture capital. It shouldalso be of interest to those functional specialists (finance, marketing, HRM,engineering) who must participate in game-changing activities.

xviii Preface

Acknowledgments

I continue to owe a huge debt of gratitude to my Professors and mentors at theMassachusetts Institute of Technology (MIT); in particular, Professors RebeccaHenderson, James M. Utterback, and Thomas Allen. They introduced me to thesubject of strategic innovation, and to the virtues of patience and tolerance.When I arrived at the University of Michigan from MIT, I was lucky that theDean of the Business School at the time, B. Joseph White (now the President ofthe University of Illinois) had created an environment in which we could thriveas researchers and teachers. That meant a lot to me and I am forever grateful! Iwould also like to thank three anonymous reviewers for their suggestions andhelp in reshaping this book. Some of my students at the Stephen M. Ross Schoolof Business at the University of Michigan gave me very useful feedback when Ipre-tested the concepts of the book, at the formative stage. Some of the cases inPart V of the book were written by some of these students under my super-vision. I am grateful to all of them. I would also like to thank Joseph Lui, whoread through some of the chapters and gave me useful feedback. Katie Changprovided me with dependable research assistance. Finally, I would like to thankMichael and Mary Kay Hallman for the funding that enabled me to explore thetopic of strategic innovation with a little more freedom.

I would like to thank Nancy Hale, Routledge editor for business books,whose professionalism convinced me to work with Routledge.

Allan AfuahAnn Arbor, MichiganJuly 29, 2008

Introduction

Chapter 1: Introduction and Overview

Chapter 2: Assessing the Profitability Potential of aStrategy

Chapter 3: The Long Tail and New Games

Part I

Introduction and Overview

Reading this chapter should provide you with the conceptual and analyticaltools to:

• Define strategy, new games, new game strategies, value creation and valueappropriation, and strategic innovation.

• Understand the characteristics of new games and how a firm can exploitthem to gain and prolong a competitive advantage.

• Begin to understand how to use an AVAC analysis to evaluate the profit-ability potential of a new game strategy.

• Describe types of new game (regular, resource-building, position-building,and revolutionary).

IntroductionConsider the following business performances:

With a market value of over $160 billion for most of 2008, Google was oneof the most valuable companies in the world. Its net income in 2007 was$4.2 billion on sales of $16.6 billion, giving it a net profit margin of 25.4%,one of the highest of any company of its size. This was a remarkable per-formance for a company that only four years earlier, in 2002, had revenuesof $439 million and a net income of $99 million in a struggling dotcomindustry.

In 2006, Threadless, an online T-shirt company founded in 2000, hadprofits of $6 million on revenues of $18 million, from T-shirts that had beendesigned, marketed, and bought by members of the public.1 This made thefirm one of the most profitable in the clothing retail business.

In 2007, Pfizer’s Lipitor was the world’s best-selling drug with sales of$12.7 billion, more than twice its nearest competitor’s sales (Plavix, with$5.9 billion). This was the third year in a row that Lipitor had topped thebest-seller list. One of the most remarkable things about Lipitor is that itwas the fifth cholesterol drug in its category (statins) in a pharmaceuticalsindustry where the third or fourth product in a category usually has littlechance of surviving, let alone of becoming the best seller in the industry.

During the 2007 Christmas season, demand for the Nintendo Wii was sostrong that Nintendo was forced to issue rain checks to customers. On eBay,bids for the $249 machine were in the thousands of dollars. What was even

Chapter 1

more remarkable was that each Wii console was sold at a profit, unlikecompeting consoles from Microsoft and Sony that were being sold at a loss.

Goldcorp, a Canadian gold mining company, offered prizes totalling$575,000 to anyone who would analyze its banks of geological survey dataand suggest where, in its Red Lake, Canada, property gold could be found.2

Fractal Graphics, an Australian company, won the top prize of $105,000.More importantly, the contest yielded targets that were so productive thatGoldcorp was said to have mined eight million ounces of gold worth morethan $3 billion in the six years following the launch.3

Between 1994 and 1998, Dell’s sales increased by five times, its profitsincreased by ten times, its stock shot up by 5,600%, its revenue growth wastwice as fast as that of its rivals while its operating earnings were greaterthan the combined operating earnings of all of its major rivals.4

From 2000 to 2005, Ryanair posted after-tax profit margins of 20–28%in an airline industry where most firms were losing hundreds of millions ofdollars. These record high after-tax profit margins made Ryanair not onlythe most profitable major airline company in the world over that period, butalso one of the most profitable European companies!

Definitions

New Game Strategies

At the core of each of these remarkable performances are strategic innovations,and new game strategies. A strategic innovation is a game-changing innovationin products/services, business models, business processes, and/or positioningvis-à-vis coopetitors to improve performance. A new game strategy is a set ofactivities that creates and/or appropriates value in new ways.5 It is what deter-mines a firm’s performance in the face of a strategic innovation. It entails per-forming new value chain activities or existing ones differently from the waythey have been performed in the past, to create value and/or position a firm toappropriate (capture) value.6 It is about not only creating value in differentways, but also about putting a firm in a position to profit from the value cre-ated. It is often about rewriting the rules of the game, overturning existing waysof creating and appropriating value. For example, rather than keep its data-banks of geological survey data on its Red Lake, Ontario property secret, andstruggle to find where gold might be located, Goldcorp made the data availableto the public and challenged it to locate the gold. Goldcorp was looking to thepublic, rather than to its employees or a contractor, to solve its problem. Onlythe winners, those who produced desirable results, would be paid. Contrast thiswith employees who would be paid whether or not they succeeded in locatinggold. Rather than design and market its own T-shirts, Threadless had membersof its registered users design and submit designs to the firm each week. Mem-bers of the community then voted for the best design, and winners wereawarded prizes. The winning design was then produced and sold to members ofthe community. Effectively, the firm did not perform many of the activities thatT-shirt companies traditionally performed, or did so differently.

The winner of a new game can be a first mover or follower; that is, the winnerof a new game can be the firm that moved first to change the rules of the game,

4 Introduction

or a firm that came in later and played the game better. The important thing isthat a firm pursues the right new game strategy to create and capture value.Google was not the first to introduce search engines but it played the new gamevery well—it was better at monetizing search engines. Its new game strategy inthe early 2000s included undertaking paid listings rather than pop-ups orbanner advertising for monetizing searches, developing those algorithmsthat delivered more relevant searches to its customers than competitors’search engines, and placing the paid-listing ads on its website as well as onthird-party sites.

New games are not always about product innovation. In fact, some of themore interesting cases of new games have nothing to do with new products orservices. Rather, they have been about changing the rules of the game in gettingan existing product to customers or in positioning a firm to appropriate existingvalue better. Take the case of Dell. It introduced direct sales to end-customers,bypassing distributors. It also established build-to-order manufacturing andbusiness processes in which each customer’s computer was built to the cus-tomer’s specification and only after the customer had ordered and paid for thecomputer. Both activities gave Dell some advantages over its competitors. Bybypassing distributors, for example, it was moving away from having to con-front the more concentrated and powerful distributors to dealing directly withthe more fragmented end-customers where it could build switching costs, brandidentity, and identify other sources of revenue such as services.

New games do not always have to be about leapfrogging competitors withproducts that have better product characteristics than competitors’. In fact,some of the more interesting new game strategies are those in which firms cutback some product/service characteristics that had come to be considered sac-red cows, but at the same time, they add a few new features. For example, whenNintendo offered its Wii, it deliberately used much cheaper three-year-oldmicroprocessor and graphics technologies, rather than trying to outmuscleMicrosoft and Sony, which used the latest and fastest but much more expensivetechnologies which many avid gamers had come to expect in each new gener-ation of game consoles. The Wii had other features that appealed more tononavid gamers, such as the ability to play games that enabled people also to getsome physical exercise.

Both first movers and followers can also make money during new games. Forexample, Merck revolutionized the cholesterol-lowering drug market when itpioneered the statin cholesterol drug category, and made lots of money. WarnerLambert, which came into the new game late when it introduced Lipitor (astatin), was able to make even more money using its own new game strategies. Itentered an alliance with Pfizer to gain access to Pfizer’s large sales force andmarketing might, to sell the drug to doctors and conduct direct-to-consumer(DTC) marketing.

Finally, what is a new game in one industry or country, may not be a newgame in another. Take the case of Ryanair. In addition to performing some ofthe activities that had set Southwest Airlines apart from its US competitors—such as flying only one type of airplane model (Boeing 737s for Southwest andA320s for Ryanair) and operating largely out of secondary airports—Ryanairwent further. It sold snacks, advertised inside as well as on its planes, andcollected commissions on the proceeds made from hotel and car rental sales

Introduction and Overview 5

made through its website. It also forged lucrative relationships with localauthorities of the secondary airports where it established operations.

Usually, a new game strategy entails some type of commitment that is madeby the firm pursuing the strategy.7 It also involves tradeoffs.8 For example,Google invested a lot of money in research and development (R&D) to keepimproving the relevance of its searches; and by committing to paid listing ads, itwas foregoing banner and pop-up ads and associated benefits and costs.

Value Creation and Appropriation

Since we have defined a new game strategy as the set of activities that createsand/or captures value in new ways, it is only appropriate that we define valuecreation and value appropriation. A firm creates value when it offers customersproducts or services whose perceived benefits to customers exceed the cost ofproviding the benefits.9 A firm appropriates (captures) value when it profitsfrom it. For example, if a musician writes, composes, and produces a song thatcustomers want, the musician has created value, provided that the cost of offer-ing the music does not exceed the benefits perceived by customers. The profitsthat the musician receives from his or her music are the value that he or shecaptures. As the case of many a musician would suggest, value captured isnot always equal to the value created. Before the Internet, recording studiomanagers and distribution channels usually had the bargaining power overmusicians and therefore captured more value from each record sold than theycreated. Musicians usually appropriated less value than they created, ten centsof every dollar.

Cooperating to Create Value and Competing toAppropriate it

When a customer buys a product, the value that it perceives in the product is notonly a function of the value created by the maker of the product, it is also afunction of the components that go into the product, the complements thatwork with the product, and of what the customer puts into using the product.Effectively, the value that a customer perceives in a product is a function of thecontribution of coopetitors—of the suppliers, customers, rivals, complemen-tors, and other actors with whom a firm cooperates and competes to create andappropriate value. For example, the value that a customer perceives in aniPhone is not only a function of what Apple puts into designing and getting theproduct produced, but also a function of the contribution of the suppliers ofthe chips, LCDs, and other components that go into the product. It is also afunction of the quality and availability of the type of phone service on it, of themusic and other content that can be played on the machine, and of how wellthe user can use the product.

Thus, firms cooperate with suppliers, customers, complementors, and some-times rivals to create value and compete with them to capture the value.Cooperation can be direct as is the case with strategic alliances, joint ventures,and long-term contracts; but often, “cooperation” is indirect as in supplierscontracting with firms to supply products to a firm’s specifications. “Competi-tion” exists not only when a firm has to select a supplier and bargain with the

6 Introduction

supplier but also when the firm has to bargain with buyers over the price of itsproducts. More importantly, competition also exists in an indirect way duringdirect cooperation. When firms are in an alliance or joint venture to coopera-tively create value, they also have to compete to determine who incurs whatcosts and who will capture what fraction of the value created. Thus, wherethere is cooperation to create value, there is nearly always competition toappropriate the value; and where there is competition to capture value, there isprobably some cooperation to create the value. Even competition among rivalsoften has elements that could benefit from cooperation. For example, rivalsstand to benefit when their market grows and therefore can cooperate to growthe market where such cooperation is legal. They also stand to profit whenthey do not get into unnecessary price wars, or get entangled in governmentoverregulation or taxation.

New Games

New Game Activities

Recall that a new game strategy is the set of activities that creates and/or cap-tures value in new ways. The cornerstones of this set are new game activities. Anew game activity is an activity that is performed differently from the wayexisting industry value chain activities have been performed to create or capturevalue.10 The activity can be completely new or it can be an existing activity thatis being performed differently. The important thing is that, (1) the way theactivity is performed is different from the way existing value chain activitieshave been performed, and (2) the activity contributes to creating or capturingvalue. For example, recall that Google’s new game strategy in the early 2000sincluded undertaking paid listings rather than pop-ups or banner advertisingfor monetizing searches, developing those algorithms that delivered morerelevant searches to its customers, and placing the paid-listing ads on its websiteas well as on third-party sites. Undertaking paid listings was a new gameactivity to firms in the search engine industry. So was developing thealgorithms to deliver more relevant searches to customers; and so was placingpaid listing adds on third-party sites. Because a set can have only one member,there will be times when a firm’s new game strategy consists of one new gameactivity, thereby making the activity a strategy. In fact, very often people refer toa new game activity as a new game strategy. Finally, strategic innovations arenew games.

Value Systems and Options for New Game Strategies—Which, Where, When, What, and How?

To understand the options that each firm has for pursuing new game strategies,consider the business system (value chain) of Figure 1.1. At each stage of thechain, a firm has many options for performing the activities needed to add valueat that stage to create and deliver products to end-customers.11 For example, atthe technology stage, a firm has many options for sourcing the technology. Itcan develop the technology internally using its own R&D resources, license thetechnology from another firm, form a strategic alliance with partners to develop

Introduction and Overview 7

the technology, or decide to wait for the next-generation technology. If itdecides to develop the technology, the firm can patent aggressively to protect itstechnology, or give away the technology. Suppose firms in an industry developtheir technologies internally and keep them proprietary; then a firm that givesaway its own technology to anyone who wants it is pursuing a new gamestrategy. That is what Sun Microsystems did when it gave away its SPARCworkstation computer technology in the early 1990s. Of course, a firm isalso pursuing a new game strategy if it decides to use a radically differenttechnology.

At the distribution level, a firm also has many choices. It can use all thechannels available to it for distribution, or use only a few. It can also decide tosell directly to customers or depend completely on distributors. It can decide tobuild products and warehouse lots of finished goods inventory, or have a build-to-order system with little or no finished goods inventory. Again, suppose firmsin a market all depend on distributors to deliver products to end-customers. Afirm that decides to sell directly to end-customers is effectively performing anew game activity. This is what Dell did when it decided to start selling directlyto end-customers. At the manufacturing level, a firm can be vertically integratedinto producing its components or buy the components; it can produce thecomponents at home or in foreign countries; it can locate all its plants in onecountry or in different countries; it can perform its own purchasing or have anagent do it, etc.

Effectively, since there are many options for performing value chain activitiesat every stage of the value chain, there also exist options for performing newgame activities at all stages of a value chain. Thus, the opportunity to gain astrategic advantage is not limited to product innovation (new game strategiesat the technology and product design stages). Opportunities for a strategicadvantage through new game strategies exist at all the stages of a value chain—manufacturing, marketing, distribution, and service included. They also exist invertically integrating backwards to supply one’s inputs, integrating verticallyforwards to dispose of one’s outputs, and integrating horizontally into com-plements or other related segments.

Moreover, options also exist as to which activities to perform, when to per-form them, how to perform them, where to perform them, and what to expectas the output. At the R&D stage, for example, a firm may decide to performbasic R&D and not applied R&D while its competitors perform both. It might

Figure 1.1 Business System and Options for New Games.

8 Introduction

decide to perform that R&D in the USA, China, and South Africa while itscompetitors do so only in Europe. It might decide to be the first mover ratherthan a follower in the R&D activities that it performs. It might also decide topatent religiously while its competitors depend on trade secrets.

In any case, new game activities can create new customer value for existing ornew customers, address newer and more valuable market segments, better pos-ition a firm to capture value created in its value system, or generate new rev-enues from existing or new revenue sources. They constitute the cornerstones ofnew game strategies.

Finally, note that although new game activities are the cornerstones of newgame strategies, the latter often contain some non-new game activities. Forexample, not all the activities that Google performed to be profitable were newgame; but the cornerstones of its new game strategy are new game activities.

From Activities to ProfitsHow do activities become profits? When a firm performs business systems activ-ities, (1) it produces a product with benefits that customers value, (2) it betterpositions itself vis-à-vis its coopetitors, or (3) it does both. The product, or theposition attained then has to be converted to profits. Although each category ofactivities sometimes takes a different path to profits, activities often comple-ment each other. Let us examine both.

Product with Benefits that Customers Value

Many firms perform activities to offer products that customers want. R&D,product development, purchasing, and manufacturing are examples of activi-ties that are designed largely to add value along a value chain so as to offercustomers products that they value. If a firm’s product offers benefits that cus-tomers perceive as unique—e.g. low-cost or differentiated products—customersare more likely to gravitate towards the firm rather than its competitors. Offer-ing customers low-cost or differentiated products is just one step, albeit a veryimportant one, for a firm to profit from performing value-adding activities. Thefirm must also price the product well since too high a price drives away somecustomers while too low a price leaves money on the table. It must seek out asmany customers as possible, since customers usually do not come knocking ata firm’s door. It could also seek different profitable sources of revenue thatexploit the product. For example, many US car dealers make more money fromservicing cars than from selling new ones. A firm could also locate its product ina market with few or no competitors such as a new market segment, a differentregion of a country, or another country.

Effectively, when value-adding activities produce low-cost or differentiatedproducts, the products must still be translated into money—they still have to bepriced well, the number of customers that perceive value in the productsincreased, profitable sources of revenues sought, and the product also posi-tioned in the right market spaces to profit more fully from it.

Introduction and Overview 9

Better Positioning vis-à-vis Coopetitors

A firm can also perform activities to position itself better vis-à-vis its coopetitorsin order to profit from the value that the firm or its coopetitors have created. Afirm has a superior position vis-à-vis a coopetitor if the coopetitor needs thefirm more than the firm needs the coopetitor. For example, when a firm pur-chases its rivals, it increases its power over customers since there are now fewerfirms (competitors) for a customer to play against each other. Buyers now needthe firm more than they did before the firm purchased its rivals. Such a firm canuse its increased power to raise its prices, or extract other concessions fromcustomers. This is a practice that Tyco International pursued profitably formany years. If a firm integrates vertically forwards to sell directly to consumers,it is bypassing the more concentrated distributors to deal directly with the morefragmented consumers. In addition to saving on the sales commissions that areusually paid to distributors, such a firm can also build switching costs at cus-tomers (see Chapters 4 and 6) and seek other sources of revenues. It also has thefreedom and flexibility to introduce more innovative products to customers. If afirm instead integrates vertically backwards to produce its own critical inputs, itincreases its bargaining power over suppliers. The firm can use such power toencourage suppliers to provide second sources for its inputs. Doing so can allowa firm to extract concessions from suppliers, including lower prices and higherquality, both of which can increase the firm’s profits.

Value Creation and Better Positioning

Some activities result in value creation and better positioning vis-à-vis coopeti-tors. For example, by offering a differentiated product, a firm is not onlycreating value but also positioning better itself vis-à-vis customers, rivals, andpotential new entrants since differentiation reduces rivalry, power of suppliers,and the threat of new entry.12 By marketing a product in a location with nocompetition, one is introducing value to customers in the location. At the sametime, since there are no competitors, the firm has a monopolistic position in thespace and is therefore well-positioned vis-à-vis some coopetitors.

In any case, when a firm performs a value-adding activity, the activity con-tributes to value creation and capture in one or more of the following ways. Theactivity:

a Lowers the cost of, or adds to the differentiation of a product—it contrib-utes to value creation, and customer benefits.

b Positions the firm better vis-à-vis its coopetitors.c Transforms the value created into profits.d Exploits the position vis-à-vis coopetitors to profit from the value created

by the firm and that created by its coopetitors.

Characteristics of New GamesWhen firms perform new value chain activities, or existing ones differently, theyare playing new games. (Each firm’s strategy is then the set of activities, includ-ing non-new game activities, that it pursues to create and appropriate value in

10 Introduction

the face of the new game.) Since the activities that underpin new games are newor existing ones that are performed differently, new games create new value orgenerate new ways of capturing value; and since performing activities requiresresources/capabilities, performing new game activities may require newresources/capabilities that build on a firm’s existing resources/capabilities orrequire very different ones. Because, in pursuing a new game, a firm may bemoving first, such a firm has an opportunity to build and take advantage of first-mover advantages. Moreover, when a firm pursues a new game strategy, itscompetitors are likely to react to the strategy. Therefore a firm is better offanticipating and taking into consideration the likely reaction of competitorswhen it pursues a new game strategy; and since firms usually pursue new gamestrategies within the context of their industry, macro, or global environments, afirm is also better off identifying and responding to the opportunities andthreats of these environments. Effectively, new games exhibit several character-istics of which firms can take advantage. New games:

1 Generate new ways of creating and appropriating new value.2 Offer opportunity to build new resources/capabilities or translate existing

ones in new ways into value.3 Create the potential to build and exploit first-mover advantages and

disadvantages.4 Attract reactions from new and existing competitors.5 Have their roots in the opportunities and threats of the firm’s environments.

The first three characteristics are about a firm’s internal environment—theactivities, resources, and capabilities that it can use to exploit the opportunitiesand threats of its external environment. The fourth and fifth characteristics areabout the external threats and opportunities. We explore each of these charac-teristics of new games.

Generate New Ways of Creating and Appropriating Value

As we have seen above, a firm creates value when it offers customers benefitsthat they perceive as being valuable to them and the firm’s cost of providingthe benefits does not exceed the benefits. Innovation (product or businessprocess) is a good example of value creation by new games, since it entailsdoing things differently and results in differentiated and/or low-cost newproducts.

New games give a firm an opportunity to create unique benefits for a valuableset of customers, and/or uniquely position the firm vis-à-vis its coopetitors toappropriate the value created. In choosing which new game strategy to pursue,a firm can opt for those activities that enable it to offer unique benefits that meetthe needs of customers with a high willingness to pay. In so doing, the firm isavoiding head-on competition, thereby keeping down the profit-sapping effectsof rivalry. For example, when Ryanair decided to expand its activities intosouthern Europe, it did not try to fight established airlines head-on at largercongested airports and try to outdo them at what they had been doing fordecades. Rather, it went for the less congested secondary airports where it didnot have to compete head-on with incumbent big airlines. Because the value is

Introduction and Overview 11

unique, a firm also has more power over its customers than it would have if thebenefits were not unique; and if customers have a high willingness to pay, a firmcan afford to set its prices closer to customers’ reservation prices without driv-ing the customers away, since the customers need the unique benefits from thefirm’s products. (A customer’s reservation price for a product is the highestprice that the customer is willing to pay for the product.) A firm can offerunique benefits to such valuable customers by working with them to help themdiscover their latent needs for a new product that it has invented or discovered,leapfrogging existing needs through innovation, reaching out for a market seg-ment that had never been served with the benefits in question, or following so-called reverse positioning in which the firm strips some of the benefits that somecustomers have come to expect but which other customers have no need forwhile adding some new ones.13

Offering a select group of customers unique benefits can dampen the powerof the customers and the effects of rivalry as well as the threat of substitutes andpotential new entries, but it may not do much about suppliers and some com-plementors. Thus, beyond pursuing activities that offer unique customer bene-fits, a firm may also want to pursue the kinds of activity that dampen or reversethe power of its suppliers. For example, by making sure that there are secondsources for all its key components, a firm can considerably dampen the powerof suppliers for the particular component. Cooperation with other coopetitors,not just suppliers, can also dampen their power vis-à-vis a firm. Effectively, anew game offers a firm an opportunity to build a system of activities that isdifficult to imitate and that enables the firm to create unique benefits for valu-able customers and uniquely position it vis-à-vis its coopetitors to appropriatethe value.14

The change element side of new game activities suggests that the new ways ofcreating and capturing value can render existing ways obsolete or can build onthem. It also suggests that the value created or the new position attained can beso superior to existing ones that the products that embody them render existingproducts noncompetitive or can be moderate enough to allow existing productsto remain in the market. For example, the activities that are performed to createand appropriate value in online auctions are so different from those for offlineauctions that the latter are largely obsolete as far as online auctions are con-cerned. The value created is also so superior that for most items, offline auctionshave been completely displaced by online auctions.

The change element also suggests that new games may result in an industrythat is more or less attractive than before the games. An industry is more attract-ive after change if the competitive forces that impinge on industry firms aremore friendly than before—that is, if rivalry, the bargaining power of suppliers,the bargaining power of customers, the threat of potential new entry and ofsubstitutes are low. If the industry is more attractive, industry firms are, onaverage, more profitable. As we will see when we explore disruptive technolo-gies, many new games increase the competitive forces on incumbents as barriersto entry drop, and rivalry increases.

12 Introduction

Offer Opportunity to Build New Resources/Capabilities orTranslate Existing Ones in New Ways

New games also offer a firm an opportunity to build scarce distinctiveresources/capabilities for use in creating and appropriating value, or to useexisting resources/capabilities in new ways to create and appropriate value. Toperform the activities that enable a firm to create and/or appropriate value, afirm needs resources (assets). These can be tangible (physical assets such asplants, equipment, patents, and cash), intangible (the nonphysical ones such asbrand-name reputation, technological know-how, and client relations), ororganizational (routines, processes, structure, systems, and culture).15 A firm’scapabilities or competences are its ability to integrate resources and/or translatethem into products.16 New game strategies can be used to build resources/cap-abilities and/or translate existing ones into value that customers want. The caseof eBay serves as a good example. By taking a series of measures to make itsonline auction market feel safe, building a brand, and increasing the number ofmembers in its community of registered users, eBay was able to build a largeand safe community—a critical resource—that attracted even more membersevery year. It was then able to use this large base of buyers and sellers to movefrom an auctions format into a multiformat that included fixed pricing andauction formats, and from collectibles to many other categories.

Again, the change side of new games suggests that the resources/capabilitiesthat are needed to perform new game activities can build on existing resources/capabilities or be so different that existing resources/capabilities are renderedobsolete. For example, the resources/capabilities needed by eBay are so differentfrom those needed for an offline auction that offline resources such as offlinephysical locations, bidding systems, etc., are obsolete as far as online auctionsare concerned. This has strategic implications that we will explore in laterchapters.

Create the Potential to Build and Exploit First-moverAdvantages and Disadvantages

A first-mover advantage is an advantage that a firm gains by being the first tocarry out a value creation and/or value appropriation activity or strategy.17

Since, in pursuing a new game, a firm may be effectively moving first, such afirm has an opportunity to earn first-mover advantages. If a firm performs theright activities to enable it to attain first-mover advantages, it can take advan-tage of them to build or consolidate its competitive advantage. For example,when a firm introduces a new product, moves into a new market, or performsany other new game activity that can allow it to create or appropriate value innew ways, the firm has an opportunity to build and exploit first-mover advan-tages. For example, a firm that introduces a new product first can build switch-ing costs or establish a large installed customer base before its competitorsintroduce competing products. In such a case, the switching costs or installedbase is said to be the firm’s first-mover advantage. Perhaps one of the mostpopular examples of a firm that built and exploited first-mover advantages isWal-Mart. When it first started building its stores in the Southwestern USA,large powerful suppliers refused to give it goods on consignment. Wal-Mart

Introduction and Overview 13

turned things around in its favor when it grew big by pursuing the right activ-ities: it saturated contiguous towns with stores and built associated distributioncenters, logistics, information technology infrastructure, and relevant “Wal-Mart culture.” By scaling up its efficient activities, Wal-Mart became very largeand effectively reversed the direction of power between it and its supplier—withWal-Mart now having the power over suppliers. Effectively, a firm that usesnew games to offer unique value to customers and uniquely position itself toappropriate the value, can use first-mover advantages to solidify its advantagein value creation and appropriation.

The more counterintuitive a new game strategy, the more opportunities thatthe first-mover has to build advantages before followers move in. As we willargue in Chapter 6, first-mover advantages are usually not automaticallyendowed on whoever moves first. They have to be earned. Of course, whereverthere are first-mover advantages, there are usually also first-mover disadvan-tages that can give followers an advantage. Competitors that follow, rather thanmove first, can take advantage of first-mover disadvantages (also called follow-er’s advantages). For example, when a firm is the first to pursue a new game, it islikely to incur the cost of resolving technological and marketing uncertaintiessuch as proving that the product works and that there is a market for it. Follow-ers can free-ride on first movers’ investments to resolve these uncertainties andbe spared these extra expenses. If the technology and market are changing, thefirst mover may make commitments in the early stages of the technology andmarket that reduce its flexibility in some later decisions. This again opens upopportunities for followers. We will also explore first-mover disadvantages inmore detail in Chapter 6.

Attract Reactions from New and Existing Competitors

If a firm pursues a new game first, the chances are that competitors are not likelyto sit by and watch the firm make money alone. They are likely to react to thefirm’s actions. Thus, it is important to try to anticipate competitors’ likelyreactions to one’s actions. In fact, business history suggests that many firms thatultimately made the most money from innovations were not the first to intro-duce the innovations. So-called followers, not first movers, won. One reason isbecause followers often can exploit first-mover’s disadvantages (also called fol-lowers’ advantages). However, a first mover can have three things going for it.First, it can build and exploit first-mover advantages. Second, it can take advan-tage of the fact that new games are often counterintuitive, making it difficult forfollowers to understand the rationale behind the utility of the new games. Themore that the idea behind a new game strategy is counter to the prevailingdominant industry logic about how to perform activities to make money in theindustry, the more that a first mover will not be followed immediately by poten-tial competitors; and if a firm follows a first mover, its dominant logic mayhandicap it from effectively replicating the first mover’s activities. While poten-tial followers are still getting over their industry’s dominant logic to understandthe potential of the new game, a first mover can preemptively accumulate valu-able important resources/capabilities that are needed to profit from theactivities.

Third, a firm that pursues a new game strategy can take advantage of the fact

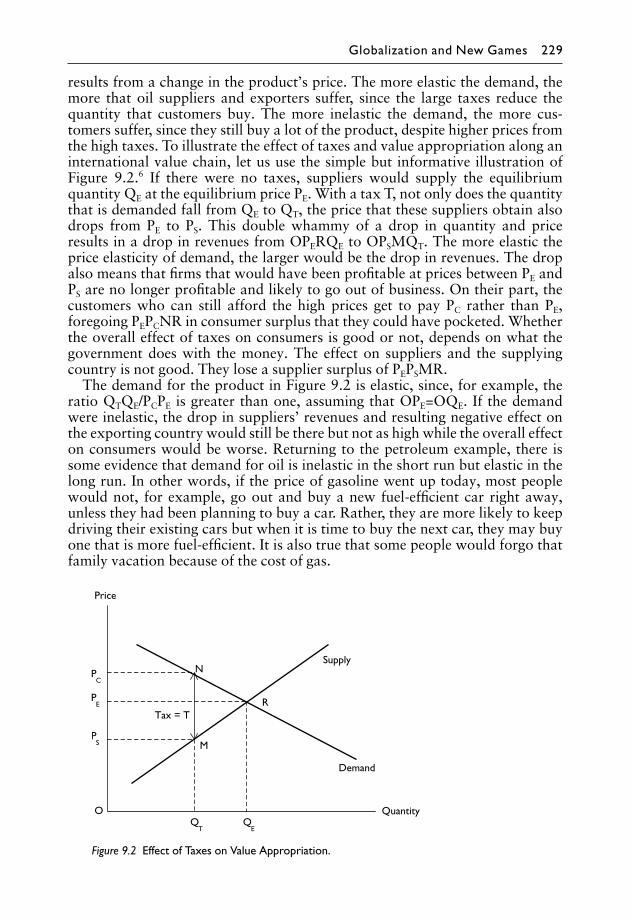

14 Introduction

that when a pioneer pursues a new game strategy, some of its competitors mayhave prior commitments or other inseparabilities that handicap them when theytry to react to the pioneer’s actions. The role of prior commitments is bestillustrated by the case of Compaq when it tried to react to Dell’s direct sales andbuild-to-order new game strategy. Compaq decided to incorporate the sametwo activities into its business model. Citing previous contracts, Compaq’s dis-tributors refused Compaq from selling directly to end-customers and the firmhad to abandon its proposed new business model. Some firms may decide not tofollow a first mover for fear of cannibalizing their existing products. In somecases, the inertia of large firms may prevent them from moving to compete withfirst movers.

In any case, an important part of profiting from a new game is in anticipatingand proactively trying to respond to the likely reaction of competitors. Thisentails asking questions such as: if I offer that new product, raise my prices,invest more in R&D, adopt that new technology, advertise more, launch thatproduct promotion, form the strategic alliance, etc., what is likely to be thereaction of my competitors? This also entails obtaining competitive intelligencenot only on competitors’ handicaps but also on their goals, resources/capabil-ities and past behavior to help in making judgments about competitors’ likelyreactions. With such information, a firm can better anticipate competitors’likely reactions and incorporate counter-measures in formulating and executingnew game strategies. Of course, the likely reaction of suppliers, complementors,and customers should also be taken into consideration.

Have their Roots in the Opportunities and Threats of aFirm’s Environments

Firms that pursue new games do not do so in a vacuum. They operate in theirindustry, macro, and global environments. In fact, many of the new game activ-ities that are performed to create value or improve a firm’s ability to appropri-ate value are triggered by opportunities or threats from both their industry,macro, and global environments. An industry environment consists of the act-ors and activities such as supply and demand that take place among suppliers,rivals, complementors, substitutes, and buyers. A firm may offer a new productbecause it wants to occupy some white space that it has identified in the marketsthat it serves. Airbus’ offering of the A380 super jumbo plane falls in thiscategory. Sometimes, new games can be a result of a hostile competitiveenvironment. Dell’s decision to sell directly to customers rather than passthrough distributors was actually because the distributors would not carry itsproducts at the time. It was a fledgling startup and many distributors were busyselling products for the IBMs and the Compaqs. The macroenvironment ismade up of the political-legal, economic, socio-cultural, technological, and nat-ural environments (PESTN) in which firms and industries operate. A firm mayenter a market because it fears that a disruptive technology will erode its com-petitive advantage. Another may use the same disruptive technology to attackincumbents that have been successful at using an existing technology. Yetanother firm may be responding to opportunities in its political-legal environ-ment. For example, Ryanair’s expansion into secondary airports in the Euro-pean Union followed the union’s deregulation of the airline industry. The drop

Introduction and Overview 15

in its profits in 2008 was largely attributable to the sharp rise in the cost of oil tomore than three times what it had been paying for in earlier years.

The global environment consists of a world in which countries and theirindustries and firms are increasingly interconnected, interdependent, and moreintegrated, thereby moving towards having similar political-legal, economic,socio-cultural, technological, and natural environments (PESTN). Theopportunities and threats of the global environment are exhibited throughglobalization. Globalization is the interdependence and integration of people,firms, and governments to produce and exchange products and services.18

Globalization creates opportunities for some firms and individuals but createsthreats for others. There are opportunities to market products to, outsourcework to export to, or import from foreign countries in new ways.

In any case, external environments differ from one industry to the other, andfrom one country or region to another. In the carbonated soft drinks industry,for example, regular and diet colas have been the major sellers for decades. Infact, when coke tried to change the formula for its regular coke, customers didnot like it and the company had to revert to the old product. Other industriesare relatively less stable. Rapid technological change, globalization, changingcustomer tastes, and more availability of skilled human resources in differentcountries make some industries very turbulent. In such industries, firms oftenhave to cannibalize their own products before someone else does. Effectively,how firms need to interact with or react to environments can differ considerablyfrom one industry to the other, or from one country to the other, and canconstitute opportunities and threats that firms can exploit through new games.

Concern for the natural environment also creates many opportunities to useinnovation to build better cars, build better power plants, better dispose ofwaste, and reduce carbon emissions. Understanding these opportunities andthreats not only helps a firm to make better choices about which activities toperform, but when to perform them and how to perform them.

Multigames and DynamicsA new game usually does not take place in isolation. It usually takes place in thecontext of other games and is usually preceded by, followed by, or played inparallel with other games. When a firm introduces a new game, it often does soin response to another game. For example, when Dell decided to sell its built-to-order PCs directly to businesses and consumers, it did so in the context of alarger new game—the introduction of PCs that were disrupting minicomputers.When Google developed its search engine and pursued paid listings to monetizethe engine, it was doing so in the context of the Internet, a much larger newgame. When Wal-Mart initially located its stores in small towns in parts of theSouthwestern USA, it was doing so in the context of the larger game of discountretailing that was challenging the standard department store. Each firm usuallyplays multigames over a period. For example, Wal-Mart started out selling onlygoods at discount prices in its discount stores but in 1988, it introduced itsversion of superstores, selling both food and goods in its Wal-Mart Supercent-ers. This multigame and dynamic nature of new games has implications that wewill encounter when we explore first-mover advantages and disadvantages, andcompetitors’ handicaps in Chapter 6.

16 Introduction

Competitive Advantage from New GamesMany firms pursue new game strategies in search of a competitive advantage,or just to make money. A firm’s competitive advantage is its ability to earn ahigher rate of profits than the average rate of profits of the market in which itcompetes. Since revenues come from customers, any firm that wants to makemoney must offer customers benefits that they perceive as valuable comparedto what competitors offer. Thus, an important step in gaining a competitiveadvantage is to create unique benefits for customers without exceeding thecost of the benefits—creating unique value; but to create value, a firm has toperform the relevant value-adding activities; and for a firm to perform value-adding activities effectively, it needs to have the relevant resources and cap-abilities. Since, as we saw earlier, not even unique value can guarantee thatone will profit from it, the activities that a firm performs should also positionit to appropriate the value created. If the activities are a new game, then thereis a change element in the creation and appropriation of value since newgames generate new ways of creating and appropriating value, offer opportun-ities to build new resources or translate existing ones in new ways, create thepotential to build and exploit first-mover advantages, attract reactions fromcoopetitors, or identify and respond to the opportunities and threats of theenvironment. Effectively, competitive advantage is about creating andappropriating value better than competitors; but creating and appropriatingvalue requires the right activities and the underpinning of resources andcapabilities. Moreover, there is always the element of change from the newgame component of activities—either from a firm or from the actors in itsexternal environment.

Components of a New Game Strategy

In effect, when a firm pursues a new game strategy, the extent to which thestrategy can give the firm a competitive advantage is a function of the activitiesthat the firm performs, the value that it creates, how much value it captures, andhow much it is able to take advantage of change. It is a function of the fourcomponents: Activities, Value, Appropriability, and Change (AVAC) (Figure1.2). Thus, one can estimate the extent to which a new game strategy stands togive a firm a competitive advantage by answering the following four questions:

1 Activities: is the firm performing the right activities? Does it have what ittakes to perform them?

2 Value: do customers perceive the value created by the strategy as unique?3 Appropriability: does the firm make money from the value created?4 Change: does the strategy take advantage of change (present or future) to

create unique value and/or position itself to appropriate the value?

Answering these four questions constitutes an AVAC analysis. The AVAC analy-sis can be used to estimate the profitability potential of a strategy or the extentto which a strategy is likely to give a firm a competitive advantage. The morethat the answers to these question are Yes rather than No, the more that thestrategy is likely to give the firm a competitive advantage. Although a detailed

Introduction and Overview 17

exploration of the AVAC analysis is postponed until Chapter 2, the analysis issimple and fundamental enough for us to start using it below.

Competitive Consequences of Strategies

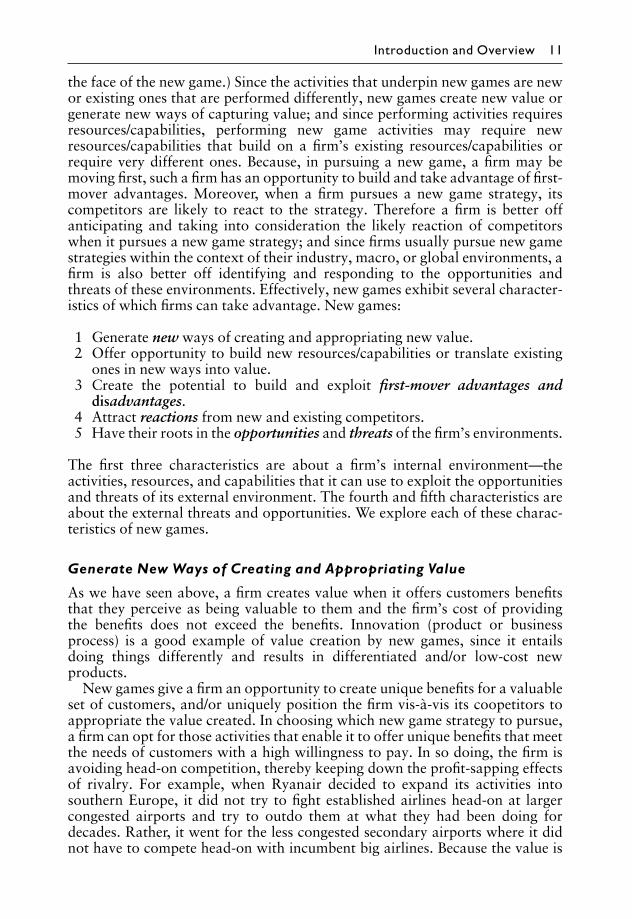

Each strategy—new game or otherwise—has competitive consequences.Depending on the strategy that a firm pursues, the firm may have a sustainablecompetitive advantage, temporary competitive advantage, competitive parity,or competitive disadvantage (Table 1.1). An AVAC analysis enables a firm toidentify and rank strategies by their competitive consequences. Table 1.1 showssix different strategies and the competitive consequence for each. In Strategy 1,the set of activities that the firm performs creates value that customers perceiveas unique and the firm is able to appropriate the value so created. The firm alsohas the resources and capabilities needed to perform the activities. Moreover,the strategy takes advantage of change (present or future) to create and/orappropriate value better. All the answers to the questions are Yes, and the firm isthus said to have a sustainable competitive advantage.

In many industries, however, the more common cases are Strategy 2 andStrategy 3, which give a firm a temporary competitive advantage. In Strategy 2,the firm has a set of activities that enables it to create value that customersperceive as unique, and put it in a position to appropriate the value. It also haswhat it takes to perform the activities; but the strategy is such that the firmcannot take advantage of change. During the period before the change, the firmhas a temporary competitive advantage. In Strategy 3, the set of activities thatthe firm performs enables it to create value and take advantage of change, butcan appropriate the value created only for the short period that it takes com-petitors to imitate it. It has the resources and capabilities to perform the value-creating activities. Thus, the firm also has a temporary competitive advantage.In pharmaceuticals, for example, strategies are often anchored on patents whichusually give their owners a competitive advantage for the duration of thepatent. When a patent expires, however, many imitators produce generic ver-sions of the drug, eroding the advantage of the original patent owners. In Strat-egy 4, the firm can neither appropriate the value created nor take advantage ofchange, even though it creates value and has what it takes to perform the

Figure 1.2 Components of a New Game Strategy.

18 Introduction

activities. Such a strategy is also said to give the firm competitive parity. Mostproducers of commodity products have comparative parity. In Strategy 5, thefirm has what it takes to perform some activities but not others. It can appropri-ate some of the value created, even though the value is not unique. It is vulner-able to change. A firm that pursues such a strategy also has competitive paritywith competitors. In Strategy 6, the set of activities that a firm performs neithercreates unique value nor puts the firm in a position to appropriate value createdby others; nor does the firm have what it takes to perform the activities. Thefirm is said to have a competitive disadvantage.

Thus, the more that the answers to these question are Yes rather than No, themore that the strategy is likely to give the firm a competitive advantage. Whatshould a firm do if an AVAC analysis shows that it has a temporary competitiveadvantage, competitive parity, or a competitive disadvantage? Such a firm candecide whether to perform the types of activity that will enable it to turn theNoes to Yesses or at least dampen them, thereby giving it a more sustainablecompetitive advantage or something closer to it. It may also decide to abandonthe strategy.

Table 1.1 Competitive Consequences of New Game Strategy

First-moveradvantage

Activities: Is thefirm performingthe right activities?Does it have whatit takes (resourcesand capabilities) toperform theactivities?

Value: Is the valuecreated by thestrategy unique, asperceived bycustomers,compared to thatfrom competitors?

Appropriability:Does the firmmake money fromthe value created?

Change: Doesthe strategy takeadvantage ofchange (present orfuture) to createunique value and/or position itself toappropriate thevalue?

Competitiveconsequence

Strategy 1 Yes Yes Yes Yes Sustainablecompetitiveadvantage

Strategy 2 Yes Yes Yes No Temporarycompetitiveadvantage

Strategy 3 Yes Yes Yes/No Yes Temporarycompetitiveadvantage

Strategy 4 Yes Yes No No Competitiveparity

Strategy 5 No/Yes No Yes No Competitiveparity

Strategy 6 No No No No Competitivedisadvantage

Strategicaction

What can a firm do to reinforce the Yesses and reverse or dampen theNoes, and what is the impact of doing so?

Introduction and Overview 19

Illustrative ExampleWe illustrate the significance of a good new game strategy using the example ofNintendo’s introduction of its Wii video game console.

Estimating the Value of a New Game Strategy: The Case ofVideo Consoles

Nintendo introduced its Wii video console in the Americas on November 19,2006, only about a week after Sony had introduced its PS3 console on Novem-ber 11. Microsoft’s Xbox had been available for purchase about a year earlieron November 22, 2005. Game developers, such as Electronic Arts, developedthe video games that customers bought to play on their consoles. For everyvideo game that a game developer sold to be played on a particular console, thegame developer paid the console-maker a royalty. This aspect of the gameconsole business model differed from the PC business model where softwaredevelopers did not pay any royalties to PC makers. Console-makers alsodeveloped some games in-house. Each console-maker, on average, collected0.415 of every game sold.19 The average wholesale price of Xbox 360/PS3-generation games was about $43.20