Second Quarter Results 2021

34

Second Quarter Results 2021 July 2021

Transcript of Second Quarter Results 2021

Second Quarter Results 2021July 2021

Disclaimer

Disclaimer

This presentation may contain forward-looking information and statements

2

Company OverviewAbout the Company | Value Proposition | Historical Performance | Corporate Governance | Shareholders' Structure | Sustainability | COVID-19 Impact

Aeronautical Business (AR)Passenger Flow 6M21 | Passenger Traffic | Airline Participation 6M21 | Aeronautical Revenue 2Q21

Non-Aeronautical Business (NAR)Commercial Revenues 2Q21 | Diversification Revenues 2Q21 | Historical NAR Growth

MDP & Maximum TariffsMDP Investments 2021-2025 | Airport Expansions | Maximum Tariffs

Financial ResultsHighlights 2Q21 | Cost & Efficiency | Balance Sheet | Profitability Indicators | Value Distribution

Outlook & IndustryIndustry Trends | Airlines Fleet

Table of Contents

3

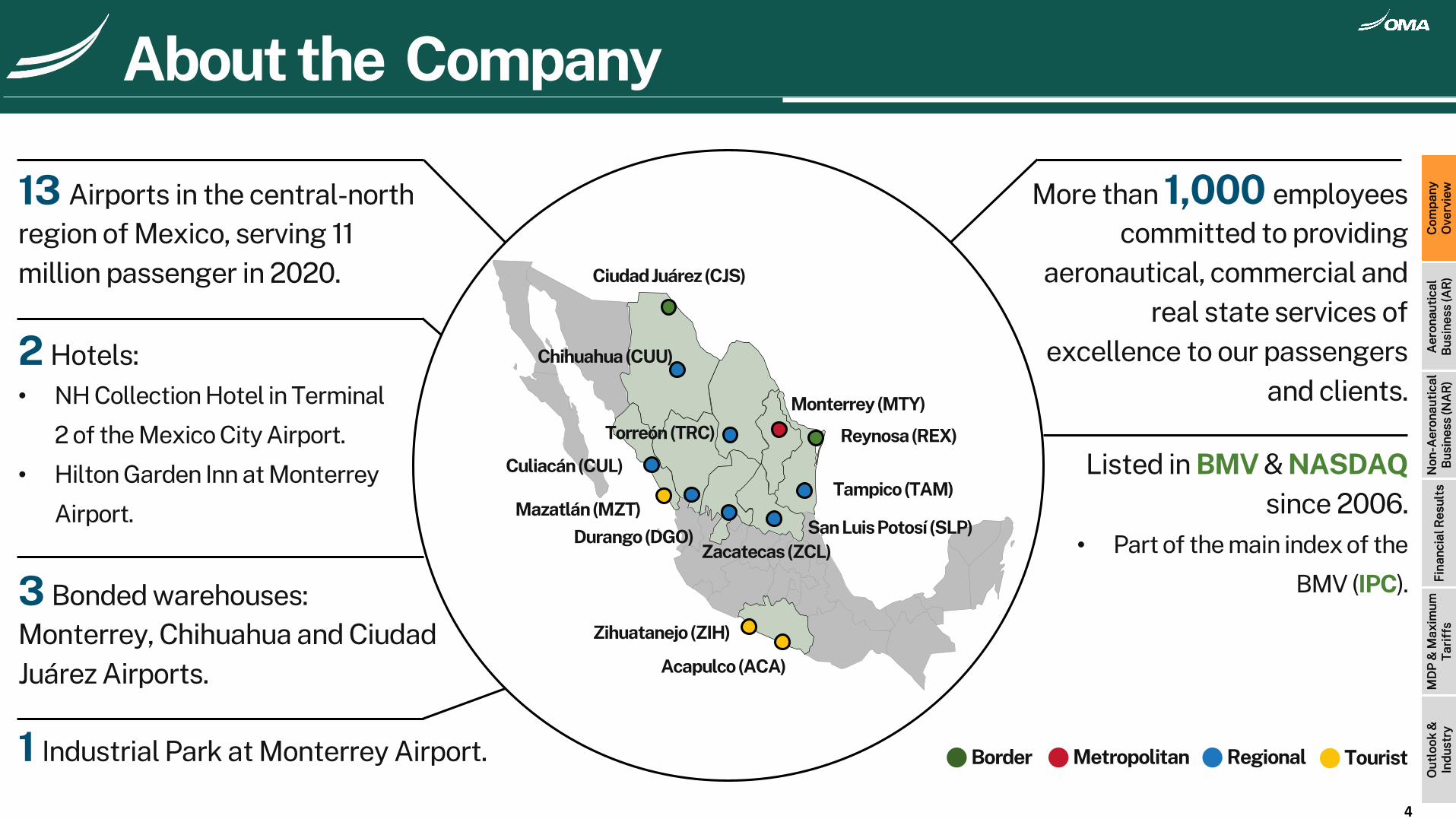

13 Airports in the central-north region of Mexico, serving 11 million passenger in 2020. Ciudad Juárez (CJS)

Chihuahua (CUU)

Culiacán (CUL)

Durango (DGO)Zacatecas (ZCL)

Torreón (TRC)

Monterrey (MTY)

Reynosa (REX)

Tampico (TAM)

San Luis Potosí (SLP)

Acapulco (ACA)

Zihuatanejo (ZIH)

Mazatlán (MZT)

2 Hotels: • NH Collection Hotel in Terminal

2 of the Mexico City Airport.

• Hilton Garden Inn at Monterrey

Airport.

3 Bonded warehouses: Monterrey, Chihuahua and Ciudad Juárez Airports.

1 Industrial Park at Monterrey Airport.

More than 1,000 employees committed to providing

aeronautical, commercial and real state services of

excellence to our passengers and clients.

Listed in BMV & NASDAQsince 2006.

• Part of the main index of the

BMV (IPC).

About the Company

RegionalBorder Metropolitan Tourist

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

4

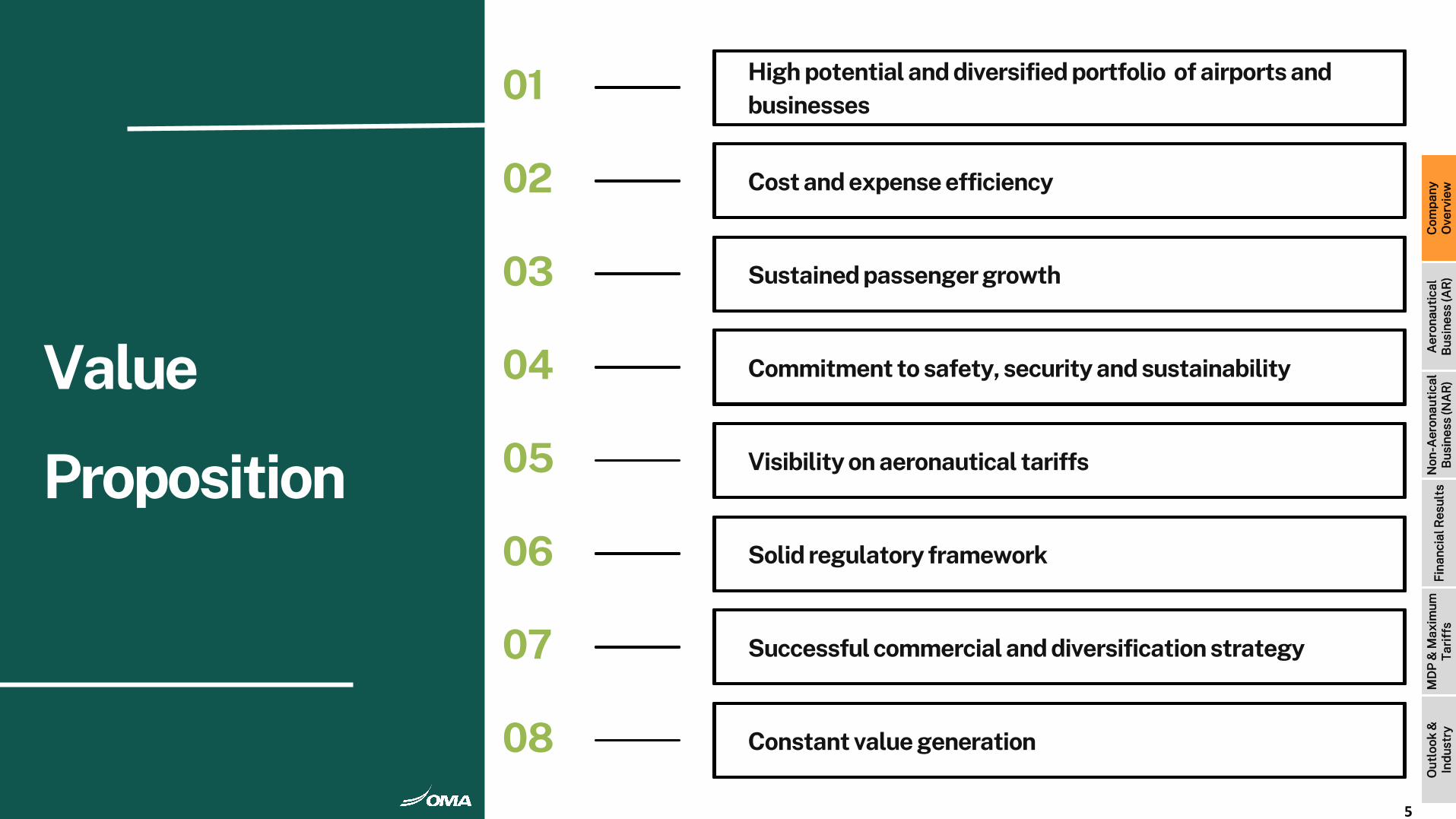

Value

Proposition

01 High potential and diversified portfolio of airports and businesses

02 Cost and expense efficiency

03 Sustained passenger growth

04 Commitment to safety, security and sustainability

05 Visibility on aeronautical tariffs

06 Solid regulatory framework

07 Successful commercial and diversification strategy

08 Constant value generation

5

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

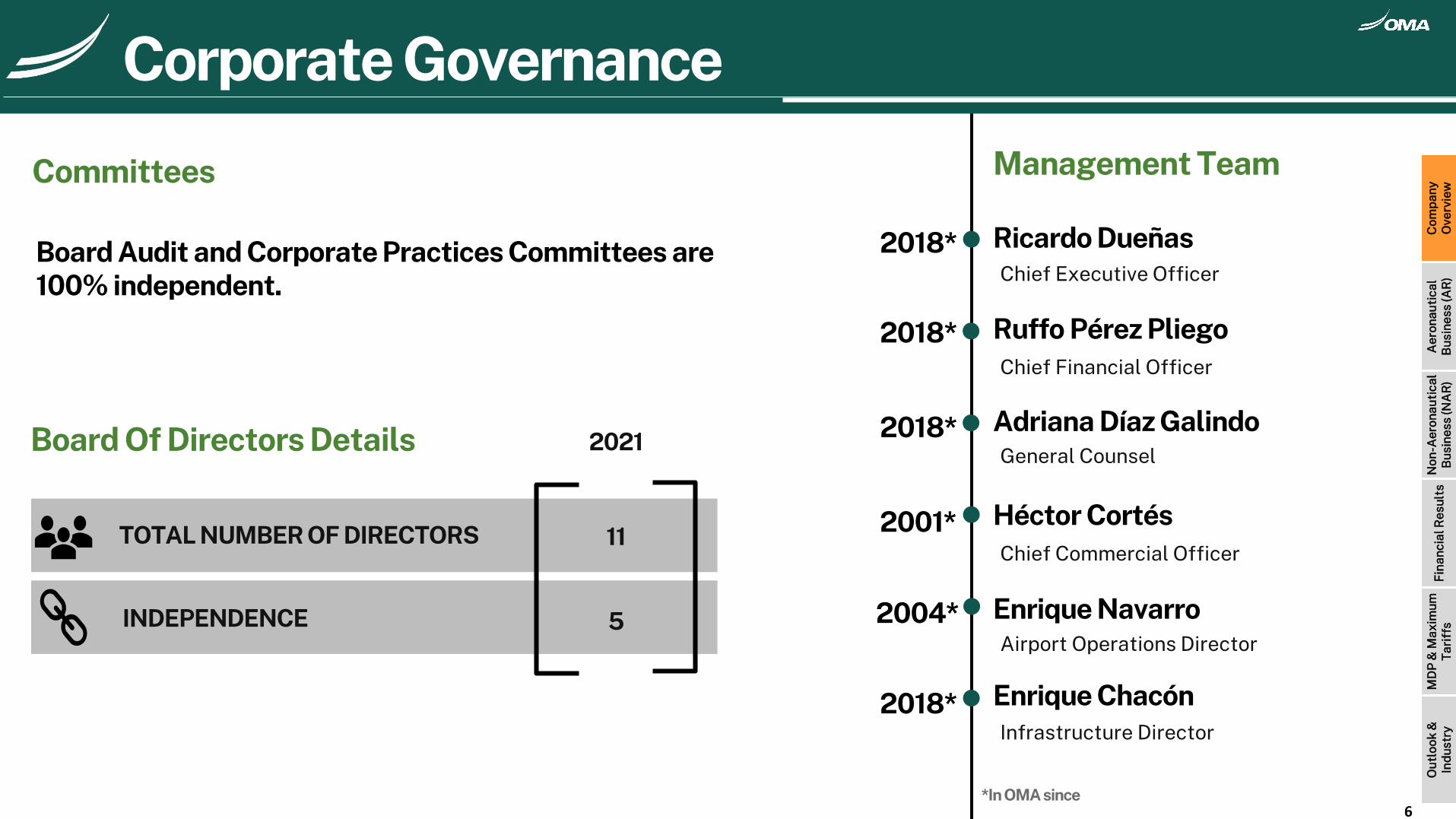

TOTAL NUMBER OF DIRECTORS

INDEPENDENCE

11

5

2021Board Of Directors Details

Management TeamCommittees

Ricardo Dueñas

Ruffo Pérez Pliego

Adriana Díaz Galindo

Héctor Cortés

Enrique Navarro

Enrique Chacón

Board Audit and Corporate Practices Committees are 100% independent. Chief Executive Officer

Chief Financial Officer

General Counsel

Chief Commercial Officer

Airport Operations Director

Infrastructure Director

2018*

2018*

2018*

2001*

2004*

2018*

*In OMA since

Historical PerformanceCorporate Governance

6

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

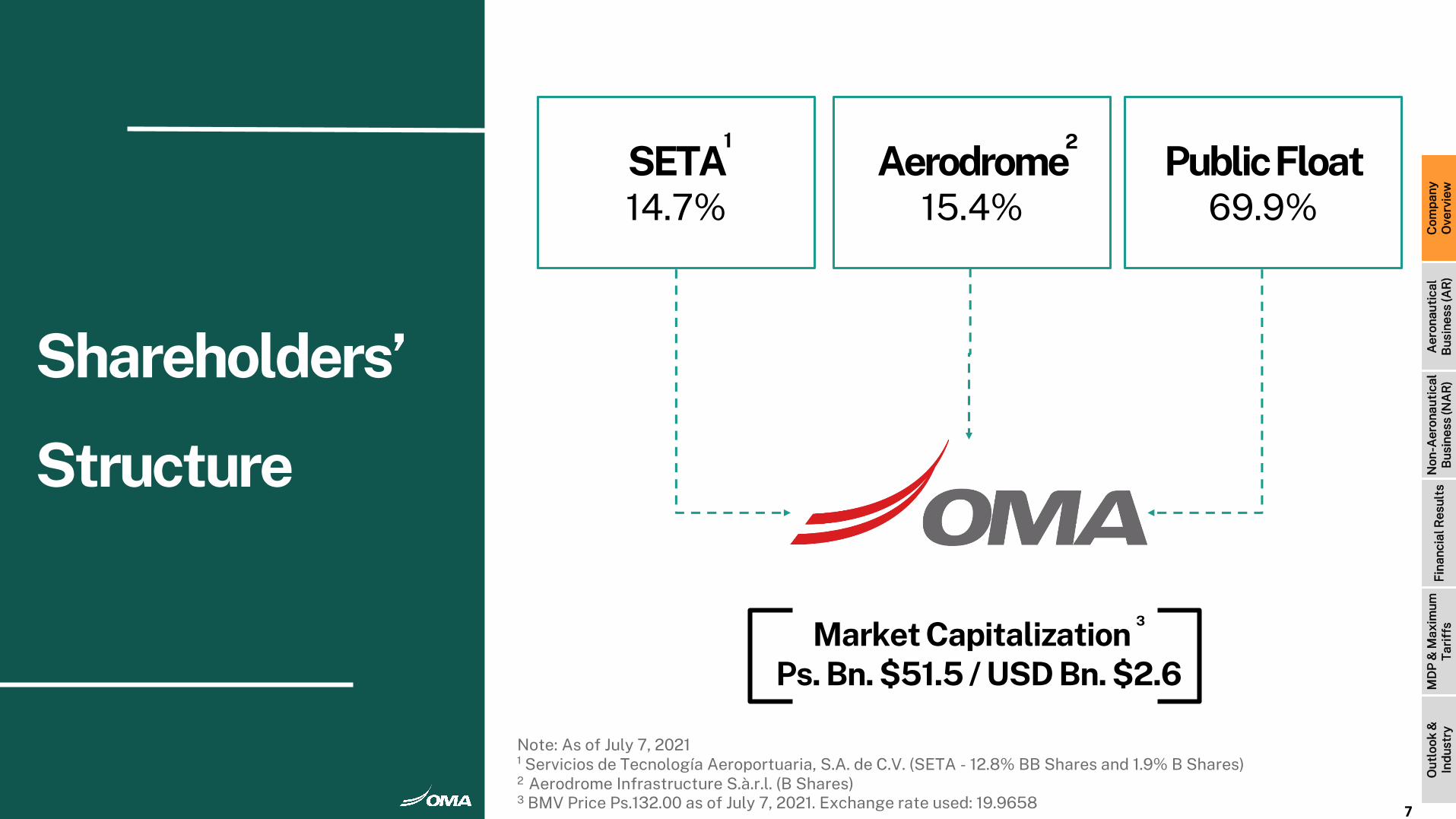

Shareholders’ Structure

Shareholders’

Structure

Shareholders’

Structure

Market Capitalization 3

Ps. Bn. $51.5 / USD Bn. $2.6

PublicFloat69.9%

Note: As of July 7, 2021¹ Servicios de Tecnología Aeroportuaria, S.A. de C.V. (SETA - 12.8% BB Shares and 1.9% B Shares)2 Aerodrome Infrastructure S.à.r.l. (B Shares)3 BMV Price Ps.132.00 as of July 7, 2021. Exchange rate used: 19.9658

Aerodrome15.4%

SETA14.7%

1 2

7

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

Historical PerformanceNon-Aeronautical Revenue

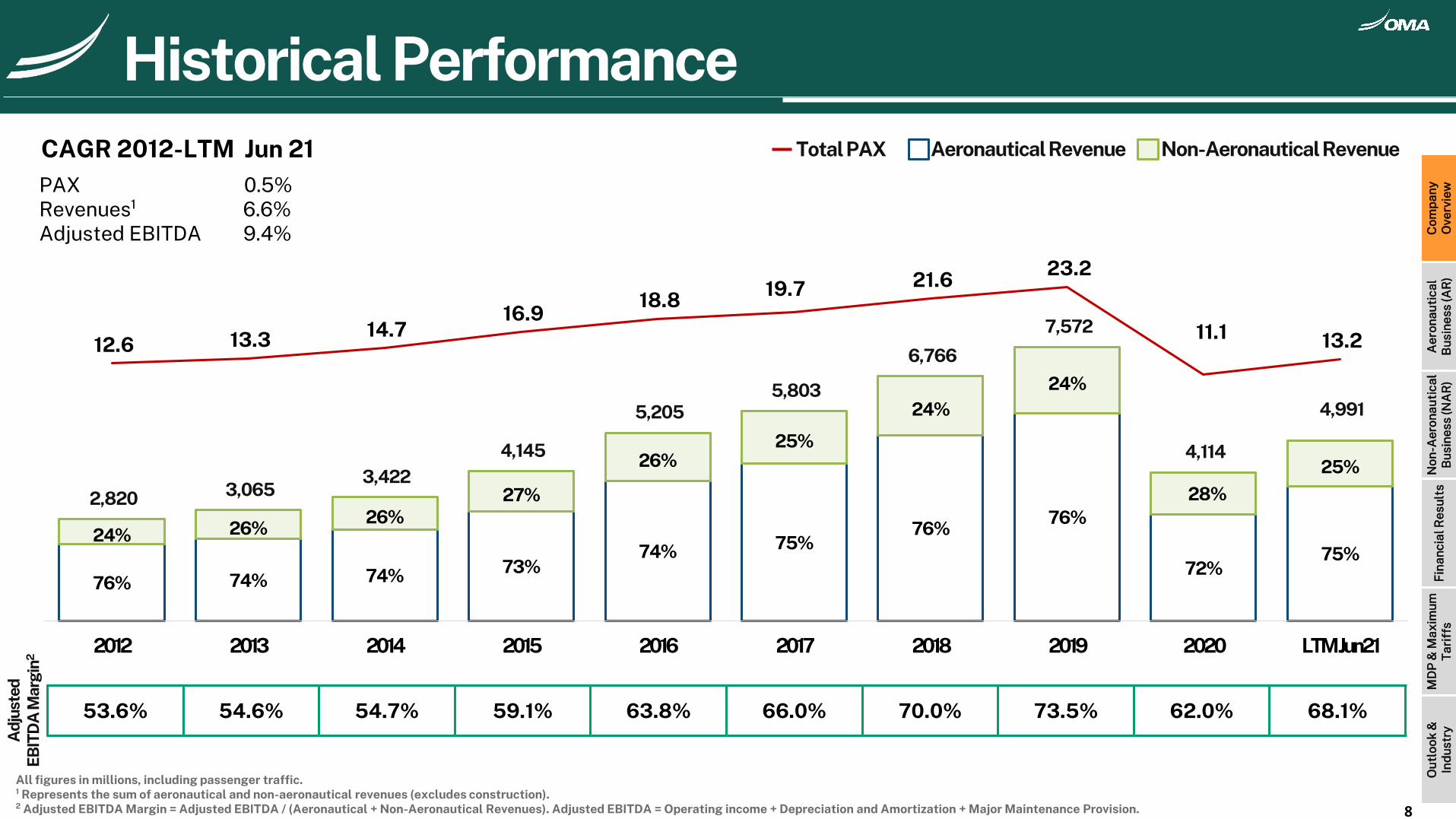

PAX 0.5%Revenues¹ 6.6% Adjusted EBITDA 9.4%

All figures in millions, including passenger traffic.¹ Represents the sum of aeronautical and non-aeronautical revenues (excludes construction).² Adjusted EBITDA Margin = Adjusted EBITDA / (Aeronautical + Non-Aeronautical Revenues). Adjusted EBITDA = Operating income + Depreciation and Amortization + Major Maintenance Provision.

CAGR 2012-LTM Jun 21

53.6% 54.6% 54.7% 59.1% 63.8% 66.0% 70.0% 73.5% 62.0% 68.1%

Total PAX Aeronautical Revenue

Historical Performance

8

76% 74% 74% 73%74% 75%

76%76%

72%75%

24% 26%26%

27%

26%25%

24%24%

28%

25%

2,820 3,065 3,422

4,145

5,205 5,803

6,766

7,572

4,114

4,991

12.6 13.3 14.7 16.9

18.8 19.7 21.6 23.2

11.1 13.2

-23.0

-21.0

-19.0

-17.0

-15.0

-13.0

-11.0

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

19.0

21.0

23.0

25.0

27.0

-

2,000

4,000

6,000

8,000

10,000

2012 2013 2014 2015 2016 2017 2018 2019 2020 LTMJun21

Adj

uste

d EB

ITD

A M

argi

n2

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

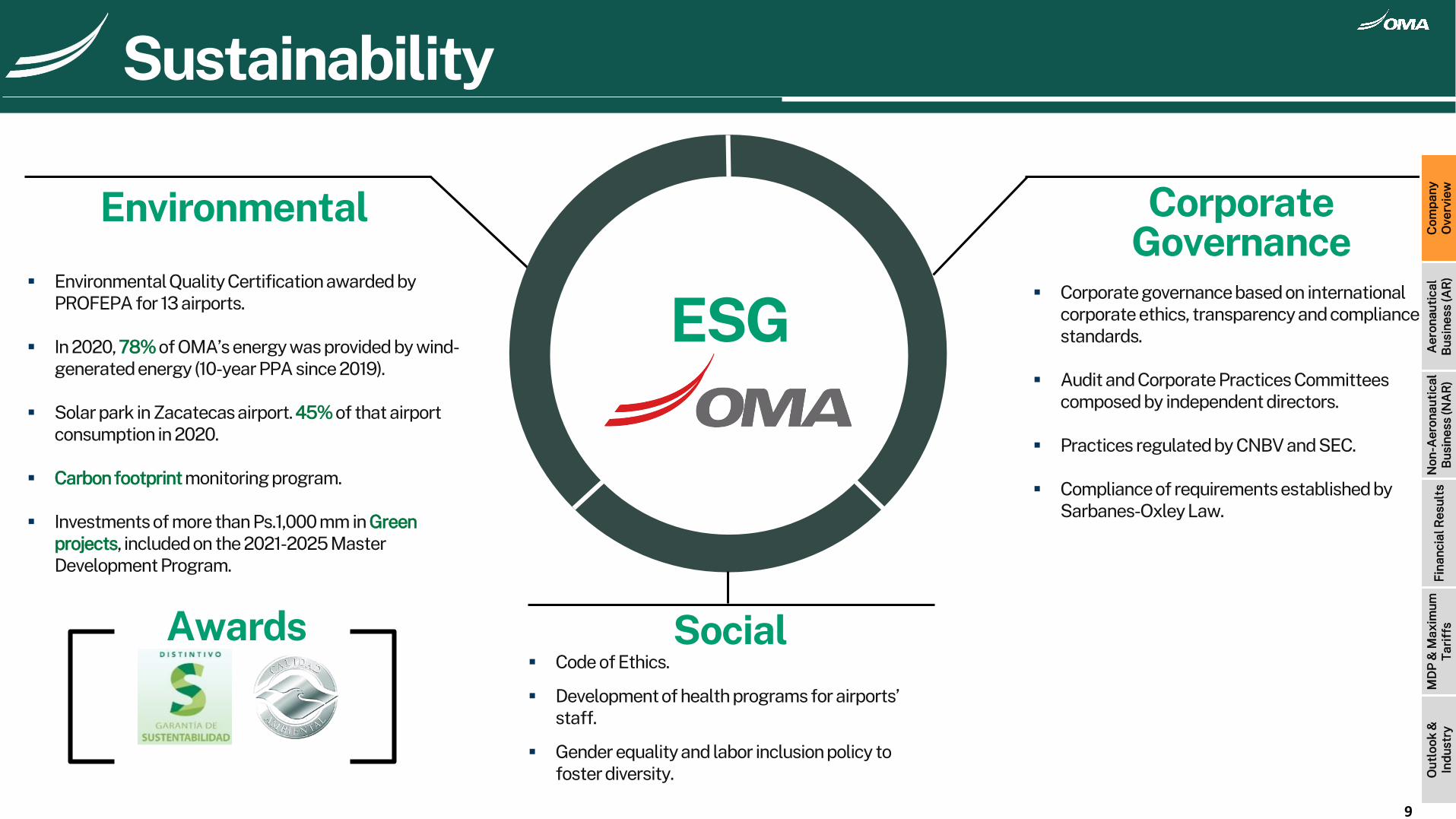

ESG

Environmental Corporate Governance

Social

▪ Environmental Quality Certification awarded by PROFEPA for 13 airports.

▪ In 2020, 78%of OMA’s energy was provided by wind-generated energy (10-year PPA since 2019).

▪ Solar park in Zacatecas airport. 45% of that airport consumption in 2020.

▪ Carbon footprint monitoring program.

▪ Investments of more than Ps.1,000 mm in Green projects, included on the 2021-2025 Master Development Program.

▪ Corporate governance based on international corporate ethics, transparency and compliance standards.

▪ Audit and Corporate Practices Committees composed by independent directors.

▪ Practices regulated by CNBV and SEC.

▪ Compliance of requirements established by Sarbanes-Oxley Law.

▪ Code of Ethics.

▪ Development of health programs for airports’ staff.

▪ Gender equality and labor inclusion policy to foster diversity.

Awards

Sustainability

9

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

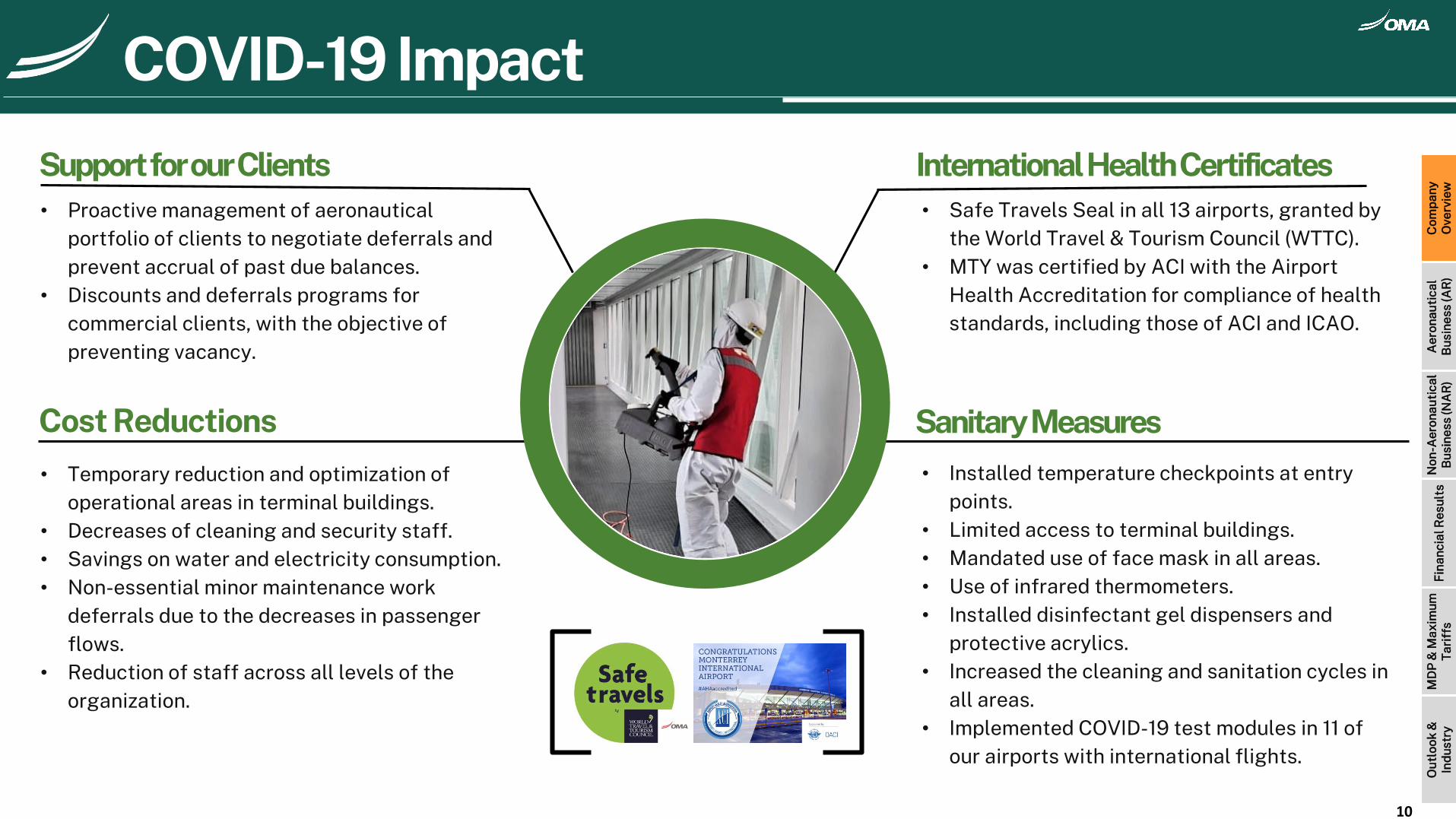

• Installed temperature checkpoints at entry points.

• Limited access to terminal buildings.• Mandated use of face mask in all areas.• Use of infrared thermometers.• Installed disinfectant gel dispensers and

protective acrylics.• Increased the cleaning and sanitation cycles in

all areas.• Implemented COVID-19 test modules in 11 of

our airports with international flights.

• Safe Travels Seal in all 13 airports, granted by the World Travel & Tourism Council (WTTC).

• MTY was certified by ACI with the Airport Health Accreditation for compliance of health standards, including those of ACI and ICAO.

Sanitary MeasuresCost Reductions

Support for our Clients International Health Certificates• Proactive management of aeronautical

portfolio of clients to negotiate deferrals and prevent accrual of past due balances.

• Discounts and deferrals programs for commercial clients, with the objective of preventing vacancy.

• Temporary reduction and optimization of operational areas in terminal buildings.

• Decreases of cleaning and security staff.• Savings on water and electricity consumption.• Non-essential minor maintenance work

deferrals due to the decreases in passenger flows.

• Reduction of staff across all levels of the organization.

COVID-19

Historical PerformanceCOVID-19 Impact

10

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

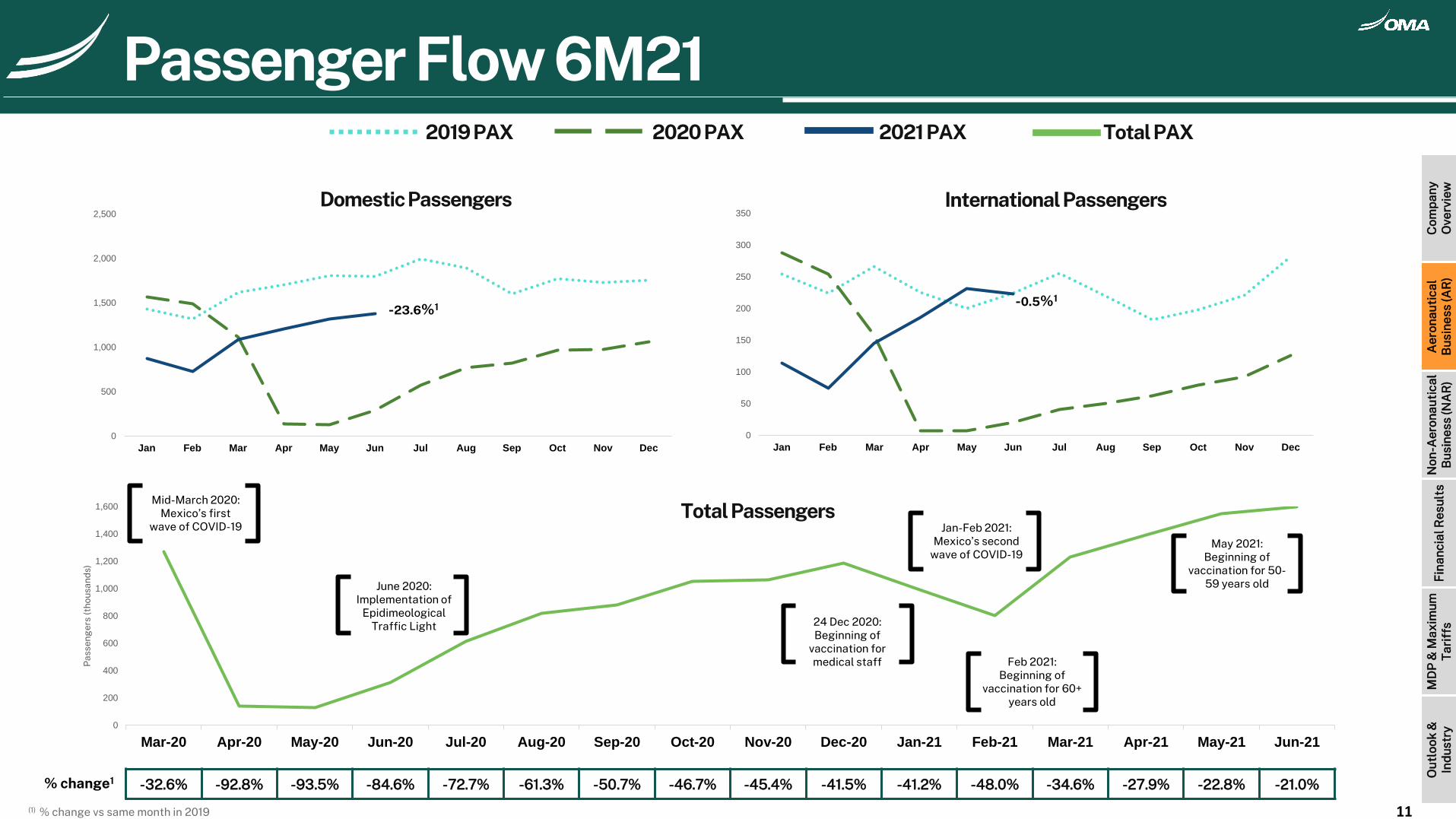

0

200

400

600

800

1,000

1,200

1,400

1,600

Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21

Pas

seng

ers

(tho

usan

ds)

Passenger Flows and Top Routes 5M21

Domestic Passengers

-32.6% -92.8% -93.5% -84.6% -72.7% -61.3% -50.7% -46.7% -45.4% -41.5% -41.2% -48.0% -34.6% -27.9% -22.8% -21.0%

Mid-March 2020: Mexico’s first

wave of COVID-19 Jan-Feb 2021: Mexico’s second

wave of COVID-19

June 2020: Implementation of

EpidimeologicalTraffic Light

Historical PerformancePassenger Flow 5M210

500

1,000

1,500

2,000

2,500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

0

50

100

150

200

250

300

350

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

International Passengers

Total Passengers

24 Dec 2020: Beginning of

vaccination formedical staff Feb 2021:

Beginning ofvaccination for 60+

years old

May 2021: Beginning of

vaccination for 50-59 years old

Passenger Flow 6M21

11

-23.6%1 -0.5%1

% change1

(1) % change vs same month in 2019

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

Total PAX 2019 PAX 2020 PAX 2021 PAX

Passenger Flows and Top Routes 5M21Top 5 Routes %*

Seat Capacity

-31.7%Terminal

Passengers

-29.5%

Historical PerformancePassenger Traffic

*Based on the number of passengers 6M21variation 6M21vs6M19

Δ% vs 6M19

3.4%

3.6%

5.6%

8.1%

11.9%

CJS-MEX

CUU-MEX

CUL-TIJ

MTY-CUN

MTY-MEX

12

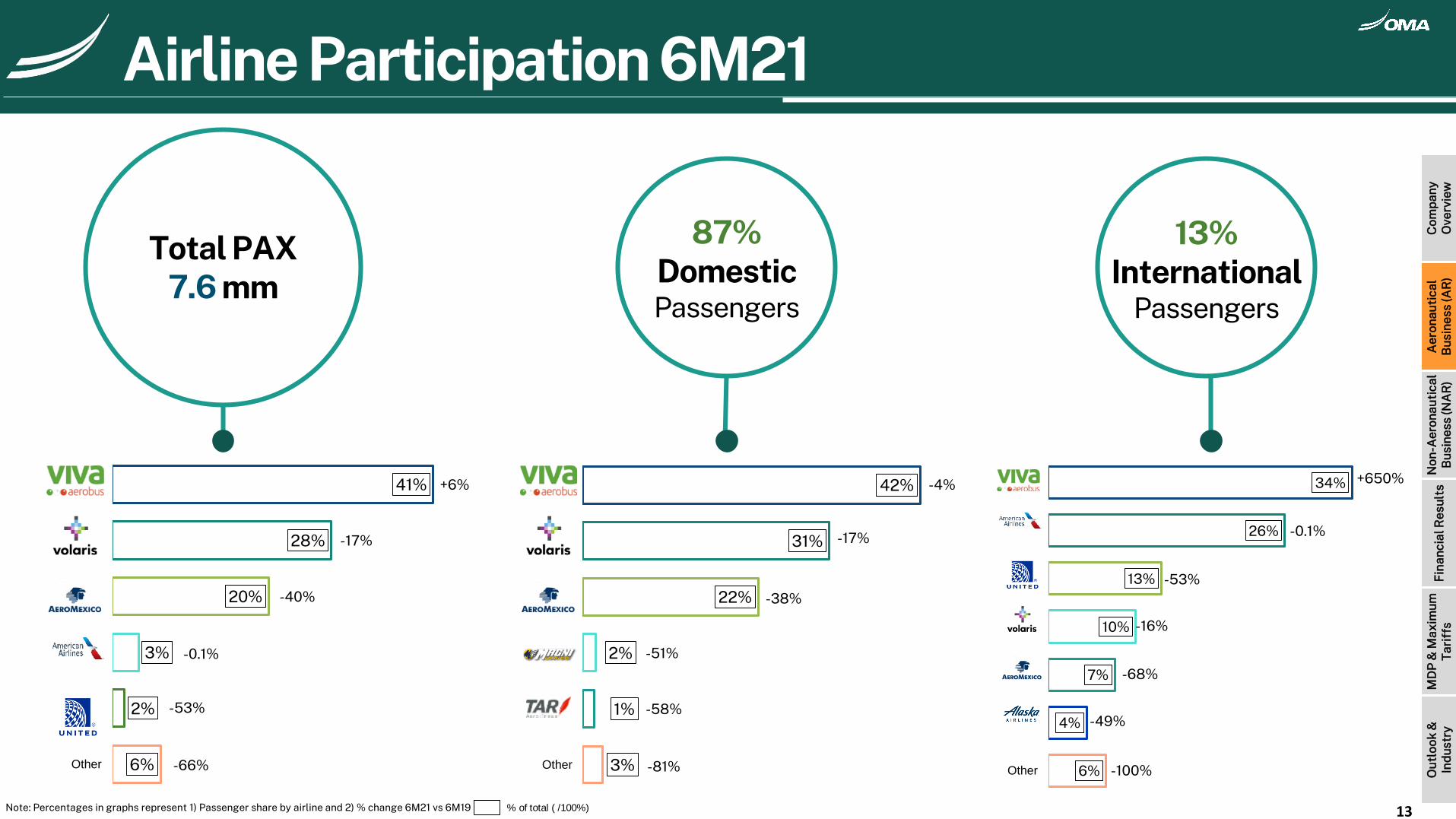

Highlights 6M21 vs 6M19Total PAX Domestic PAX International PAX

7.6 million

-31.7%

6.6 million

-31.9%

1.0 million

-30.1%

Airport% PAX/Total

6M2021Passenger

Variation 6M21 vs 6M19

MTY 44% -36%

CUL 12% -23%

CJS 8% -23%

CUU 7% -28%

MZT 7% -14%

ACA 4% -30%

TRC 3% -35%

SLP 3% -29%

ZIH 3% -46%

DGO 3% -13%

REX 2% -24%

TAM 2% -53%

ZCL 2% -31%

Passengers by Airport

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

-49%

+1%

-7%

-31%

-21%

6%

4%

7%

10%

13%

26%

34%

Other

Alaska Airlines

GrupoAeroméxico

Volaris

United Airlines

AmericanAirlines

Viva Aerobus

3%

1%

2%

22%

31%

42%

Other

TAR Aerolíneas

Magnicharters

GrupoAeroméxico

Volaris

Viva Aerobus

Note: Percentages in graphs represent 1) Passenger share by airline and 2) % change 6M21 vs 6M19 % of total ( /100%)

-4%

-17%

-38%

-51%

-58%

-81%

+650%

-0.1%

-53%

-16%

-68%

-49%

-100%

87%DomesticPassengers

13%International

Passengers

Total PAX7.6 mm

6%

2%

3%

20%

28%

41%

Other

UnitedAirlines

AmericanAirlines

GrupoAeroméxico

Volaris

Viva Aerobus +6%

-40%

-17%

-0.1%

-53%

-66%

13

Passenger Flows and Top Routes 5M21Historical PerformanceAirline Participation 6M21

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

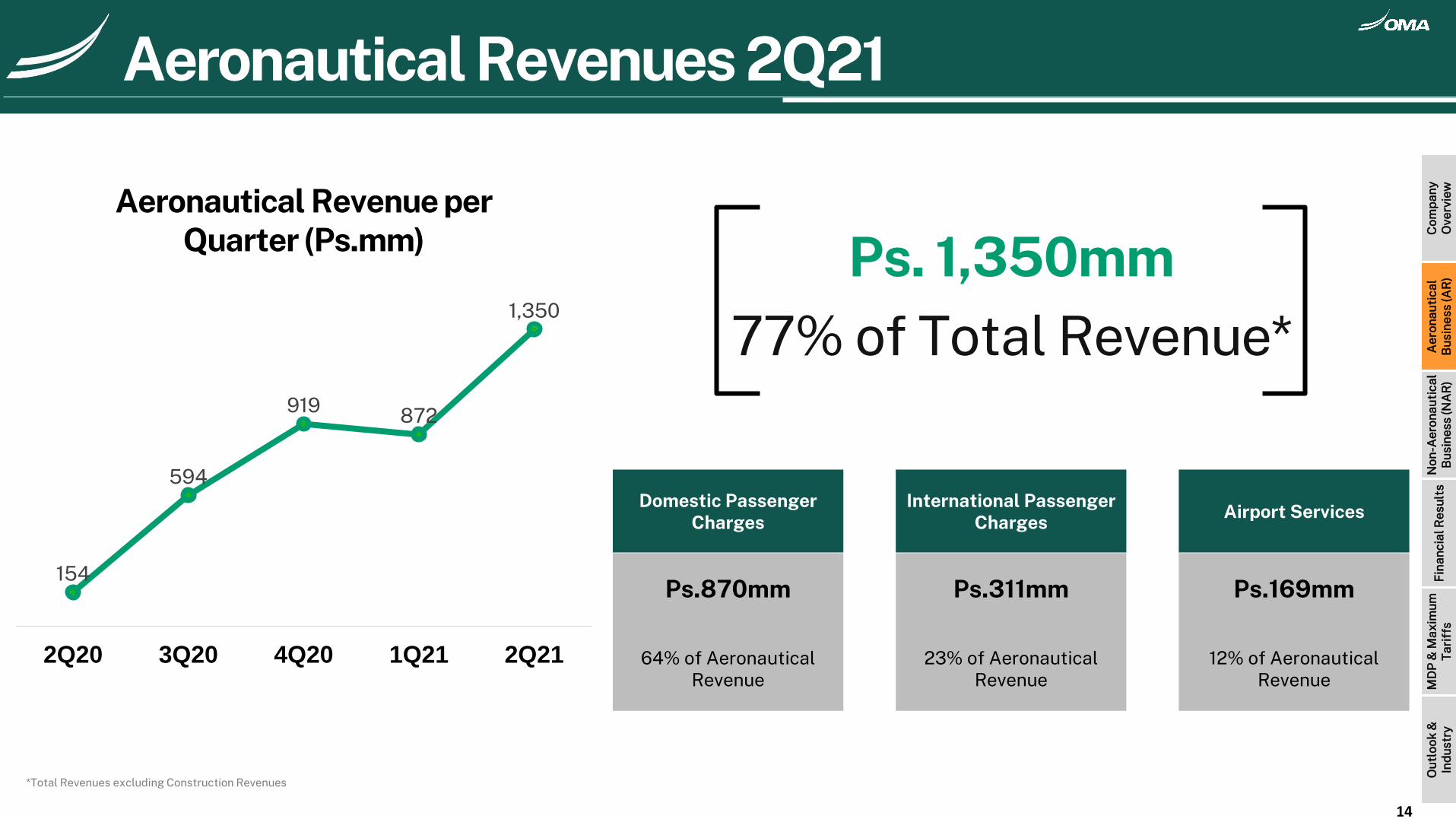

Ps. 1,350mm77% of Total Revenue*

Domestic Passenger Charges

International Passenger Charges

Airport Services

Ps.870mm

64% of Aeronautical Revenue

Ps.311mm

23% of AeronauticalRevenue

Ps.169mm

12% of Aeronautical Revenue

154

594

919 872

1,350

2Q20 3Q20 4Q20 1Q21 2Q21

*Total Revenues excluding Construction Revenues

Aeronautical Revenue per Quarter (Ps.mm)

Aeronautical Revenues 2Q21

14

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

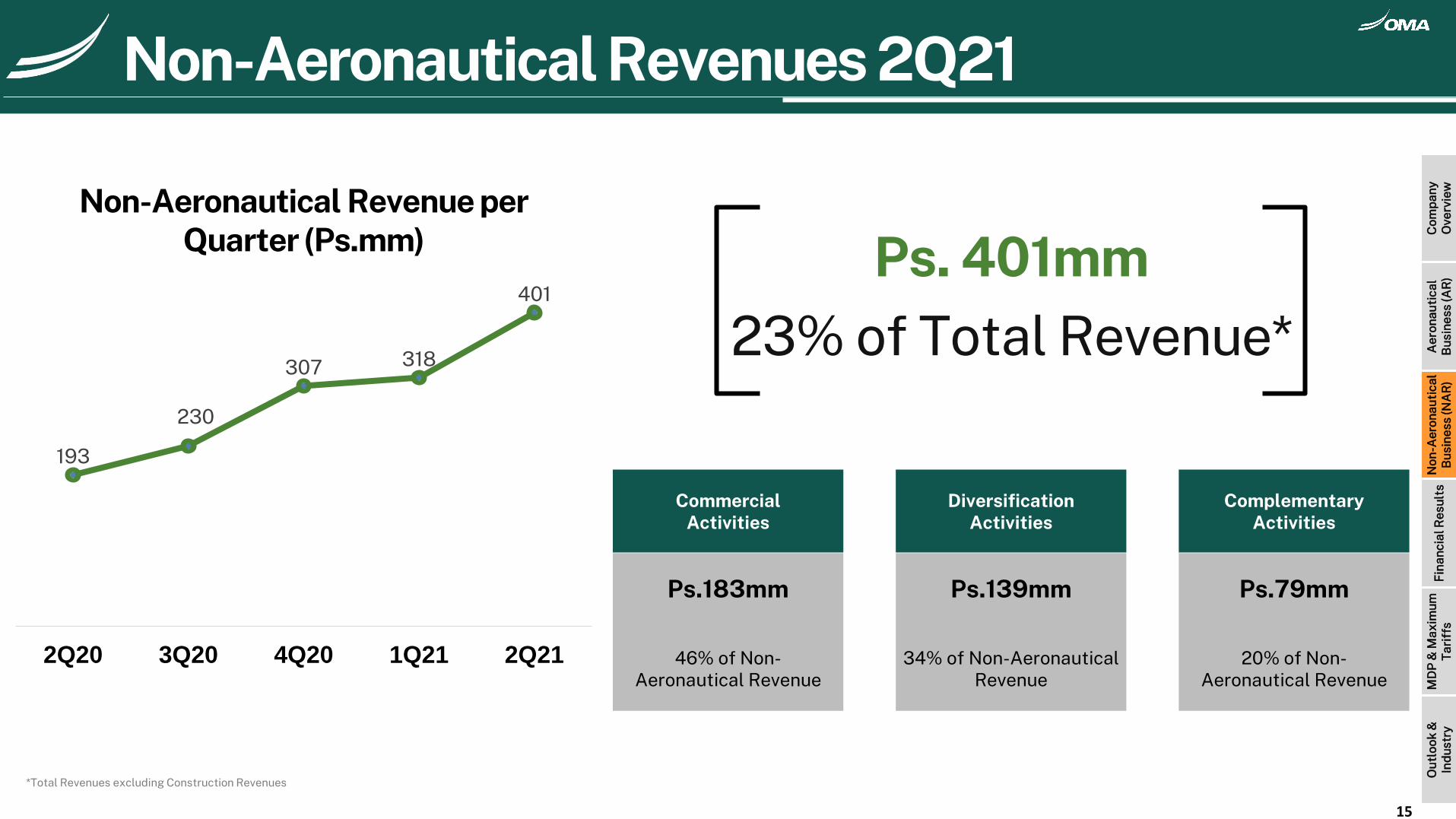

193

230

307 318

401

2Q20 3Q20 4Q20 1Q21 2Q21

Ps. 401mm23% of Total Revenue*

CommercialActivities

DiversificationActivities

ComplementaryActivities

Ps.183mm

46% of Non-Aeronautical Revenue

Ps.139mm

34% of Non-AeronauticalRevenue

Ps.79mm

20% of Non-Aeronautical Revenue

*Total Revenues excluding Construction Revenues

Non-Aeronautical Revenue per Quarter (Ps.mm)

Non-Aeronautical Revenues 2Q21

15

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

.

30% CommercialRevenues

Direct operation and management of parking

areas across our airports.

Parking

18% CommercialRevenues

+250 spaces for reservations, VIP

services, delivery offices and vehicle shelter

spaces.

Car Rental

11% CommercialRevenues

+200 spaces for retail.7,000 m2

Retail & Duty Free

.

9% CommercialRevenues

Along with advertising providers, we

commercialize +900 advertising spaces.

Advertising15% Commercial

Revenues

+120 spaces for local and

International franchises.9,300 m2

Restaurants

6% CommercialRevenues

11 lounges in 2,400 m2, of which 8 are OMA Premium Lounges.

VIP Lounges

11% CommercialRevenues

Includes communications and

networks, shared time, hotel promotion,

financial services andpassenger services.

Other

Commercial Revenues 2Q21

16

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

10% of NAR | 287 Rooms

Avg. Room Rate:Ps.2,053 per night

Occupancy Rate: 55.8%(42.8% in 2Q20)

EBITDA Margin: 43.9%

NHT2 Collection

3% of NAR | 134 Rooms

Avg. Room Rate:Ps.1,886 per night

Occupancy Rate: 45.8%(0.8% in 2Q20)

EBITDA Margin: 41.0%

Hilton Garden Inn

16% of NAR

+69.3% revenues vs 2Q20

Tons handled 2Q21: 9,667(+102.2%)

OMA Carga

4% of NAR

+25.6% revenues vs 2Q209 warehouses leased

(59,000 m2)1 warehouse available for

rent

MTY Industrial Park

1% of NAR

+10.7% revenues vs 2Q20

Real Estate

Diversification Revenues 2Q21

17

NAR: Non-Aeronautical Revenues

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

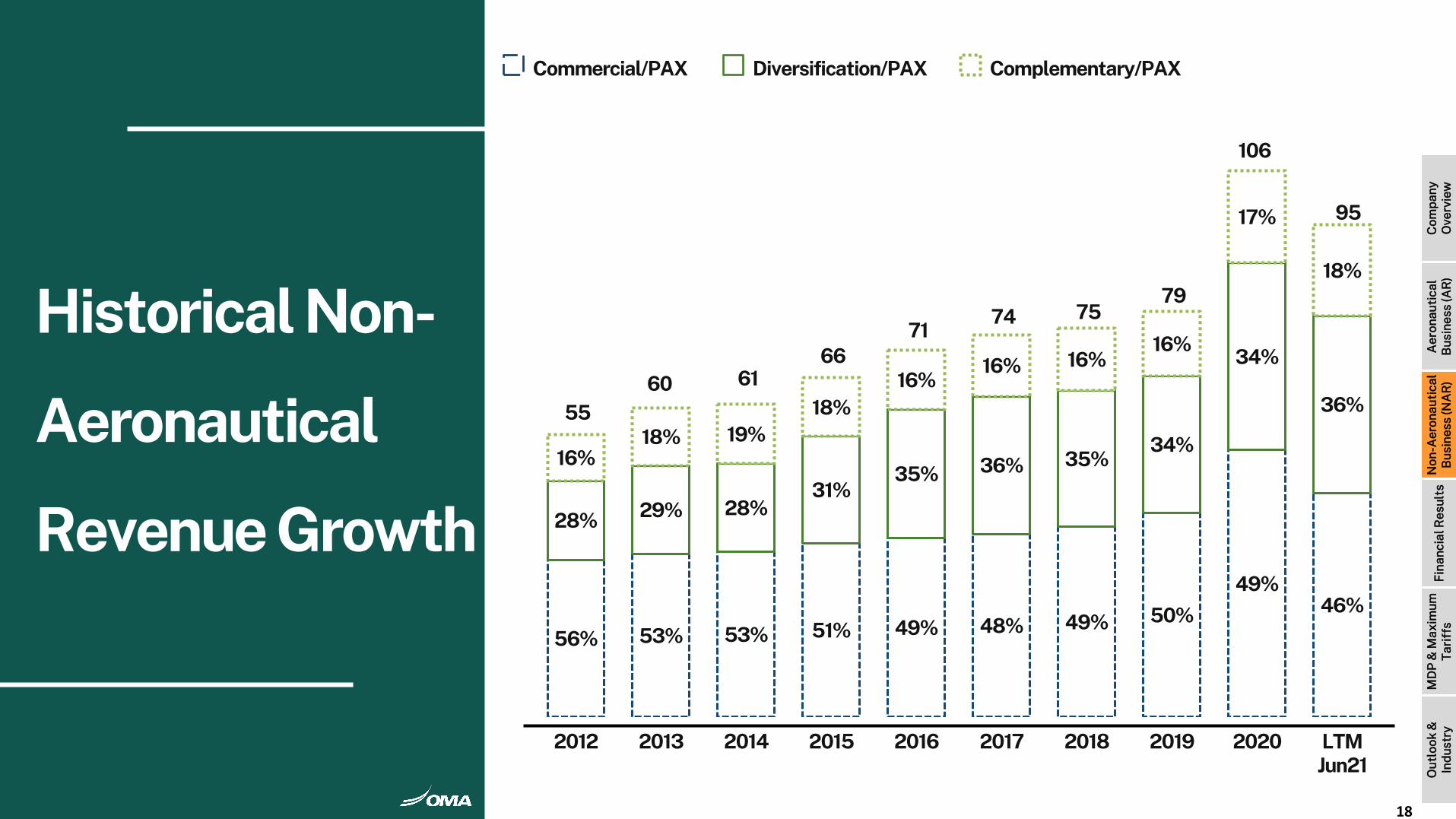

56% 53% 53% 51% 49% 48% 49% 50%

49%46%

28% 29% 28%31%

35% 36% 35%34%

34%

36%

16%18% 19%

18%16%

16% 16%16%

17%

18%

55 60 61

66 71

74 75 79

106

95

2012 2013 2014 2015 2016 2017 2018 2019 2020 LTM Jun21

Historical Non-

Aeronautical

Revenue Growth

Commercial/PAX Diversification/PAX Complementary/PAX

18

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

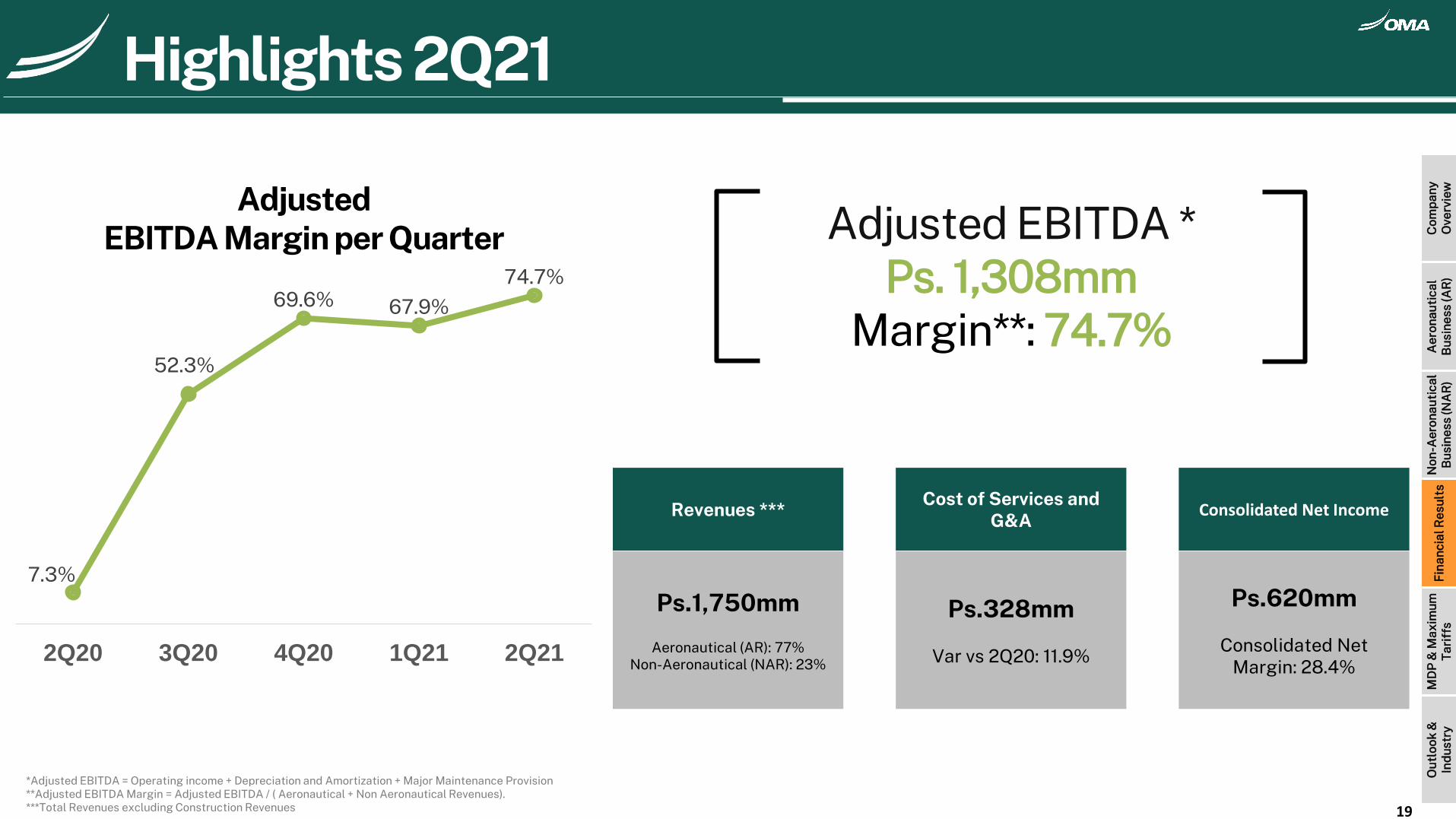

Adjusted EBITDA *Ps. 1,308mm

Margin**: 74.7%

Revenues ***Cost of Services and

G&AConsolidated Net Income

Ps.1,750mm

Aeronautical (AR): 77%Non-Aeronautical (NAR): 23%

Ps.328mm

Var vs 2Q20: 11.9%

Ps.620mm

Consolidated Net Margin: 28.4%

*Adjusted EBITDA = Operating income + Depreciation and Amortization + Major Maintenance Provision**Adjusted EBITDA Margin = Adjusted EBITDA / ( Aeronautical + Non Aeronautical Revenues).***Total Revenues excluding Construction Revenues

AdjustedEBITDA Margin per Quarter

7.3%

52.3%

69.6% 67.9%

74.7%

2Q20 3Q20 4Q20 1Q21 2Q21

Highlights 2Q21

19

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

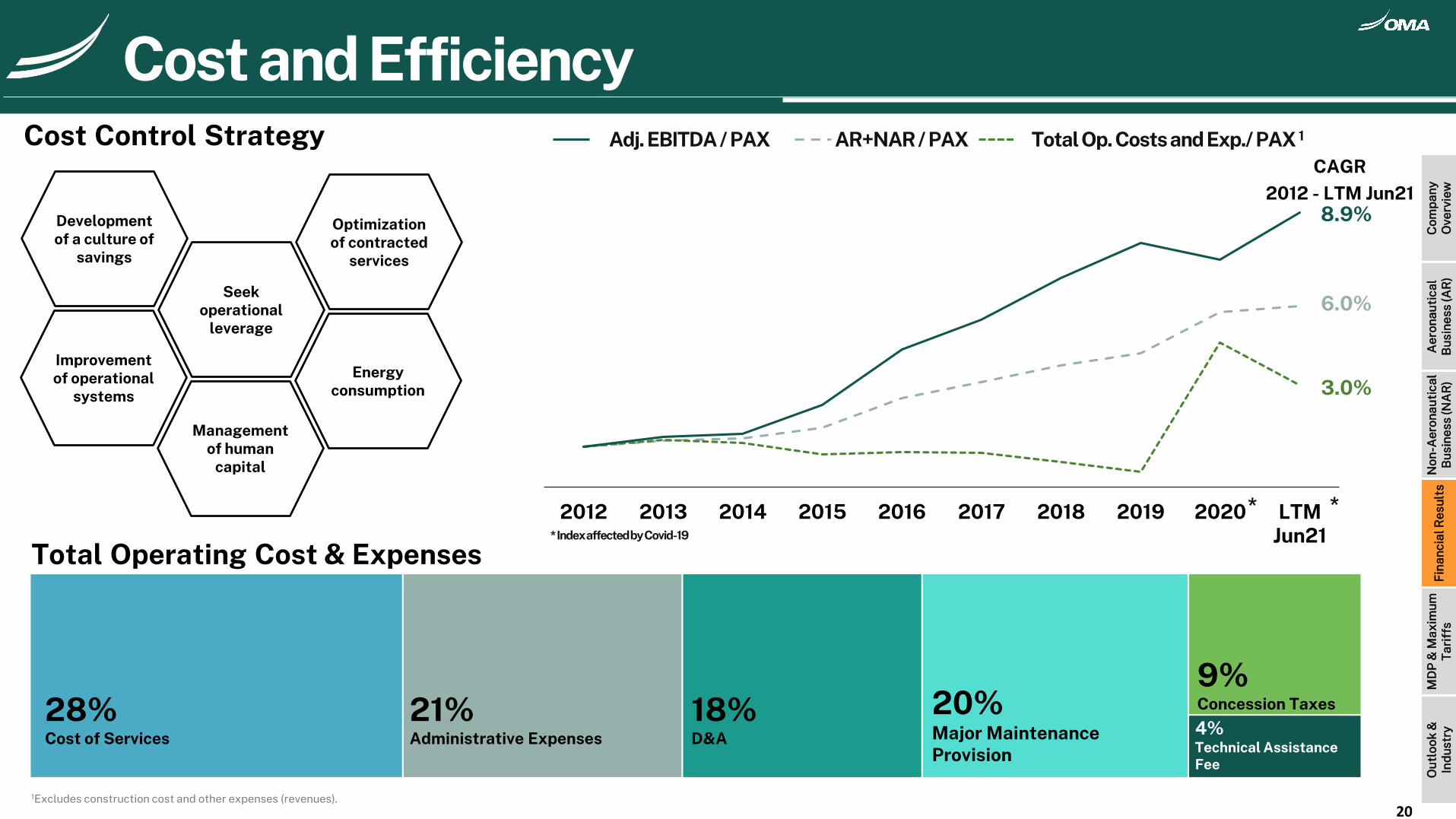

Seekoperational

leverage

Development of a culture of

savings

Improvement of operational

systems

Energy consumption

Optimizationof contracted

services

Management of human

capital 80.0 0

100 .00

120 .00

140 .00

160 .00

180 .00

200 .00

220 .00

240 .00

2012 2013 2014 2015 2016 2017 2018 2019 2020 LTM Jun21

CAGR

2012 - LTM Jun21

6.0%

8.9%

3.0%

Cost Control Strategy

Total Operating Cost & Expenses

AR+NAR / PAXAdj. EBITDA / PAX Total Op. Costs and Exp./ PAX 1

1Excludes construction cost and other expenses (revenues).

Cost and Efficiency

* ** Index affected by Covid-19

20

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

28%Cost of Services

21%Administrative Expenses

18%D&A

20%Major Maintenance Provision

9%Concession Taxes

4%Technical Assistance Fee

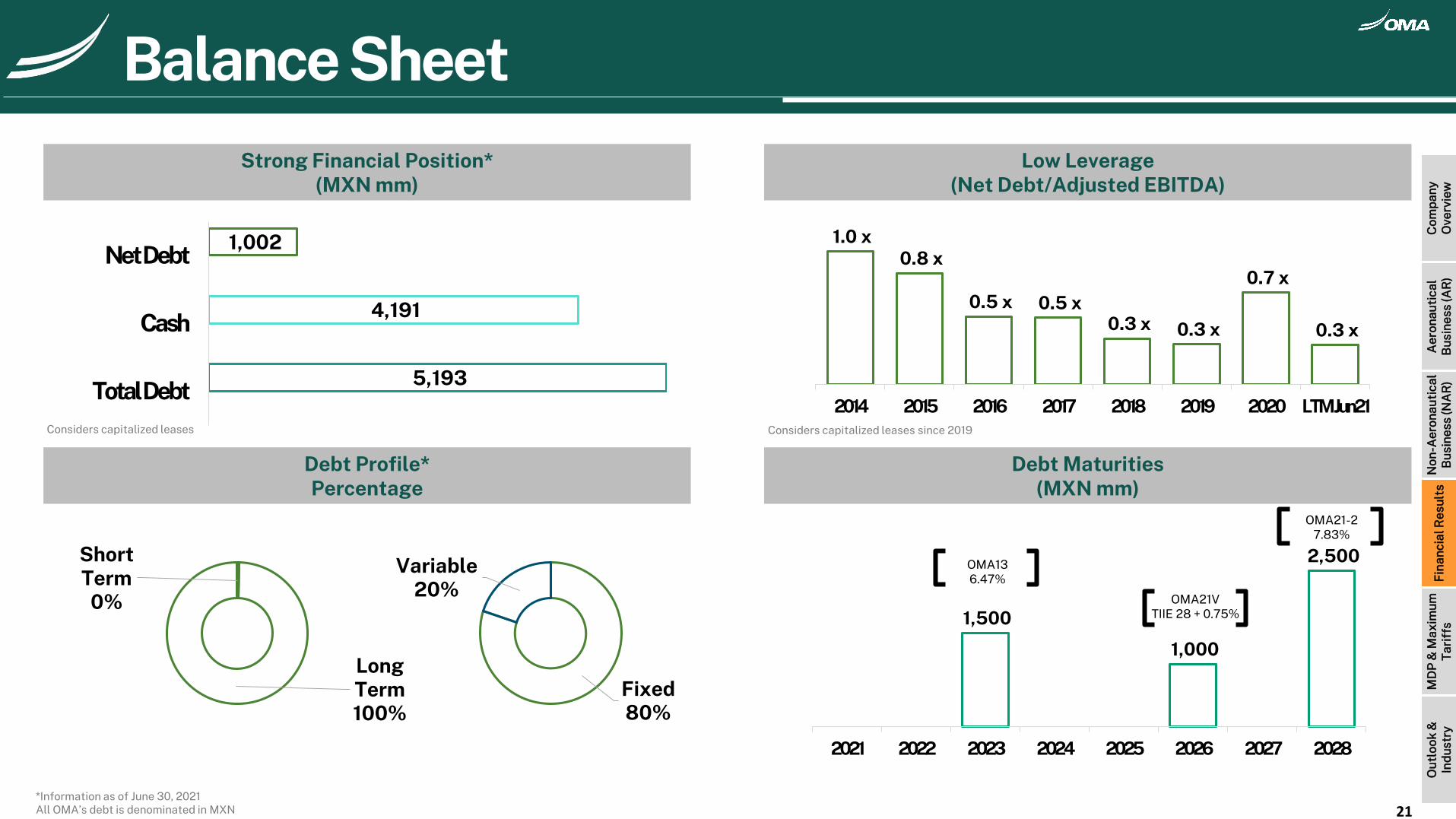

Strong Financial Position*(MXN mm)

Low Leverage(Net Debt/Adjusted EBITDA)

Debt Profile*Percentage

Debt Maturities(MXN mm)

5,193

4,191

1,002

Total Debt

Cash

Net Debt

Short Term

0%

Long Term100%

1.0 x0.8 x

0.5 x 0.5 x0.3 x 0.3 x

0.7 x

0.3 x

2014 2015 2016 2017 2018 2019 2020 LTM Jun21

1,500

1,000

2,500

2021 2022 2023 2024 2025 2026 2027 2028

*Information as of June 30, 2021All OMA’s debt is denominated in MXN

Considers capitalized leases since 2019

Balance Sheet

OMA136.47%

OMA21VTIIE 28 + 0.75%

OMA21-27.83%

Fixed80%

Variable20%

21

Considers capitalized leases

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

Value Distribution

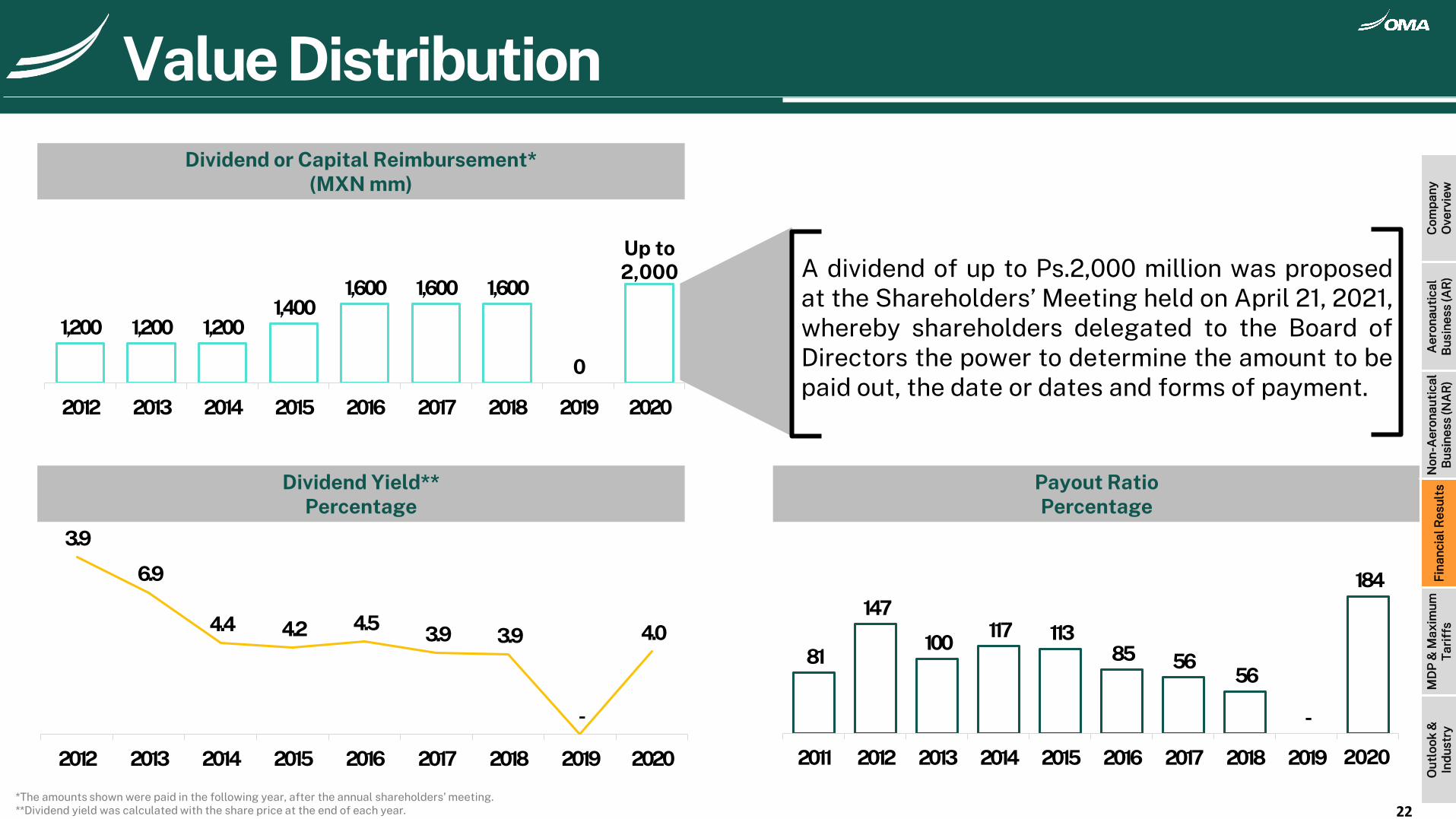

1,200 1,200 1,2001,400

1,600 1,600 1,600

0

Up to 2,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

Dividend or Capital Reimbursement*(MXN mm)

Dividend Yield**Percentage

3.9

6.9

4.4 4.2 4.5 3.9 3.9

-

4.0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Payout Ratio Percentage

A dividend of up to Ps.2,000 million was proposedat the Shareholders’ Meeting held on April 21, 2021,whereby shareholders delegated to the Board ofDirectors the power to determine the amount to bepaid out, the date or dates and forms of payment.

81

147

100 117 113

85 5656

-

184

2011 2012 2013 2014 2015 2016 2017 2018 2019

*The amounts shown were paid in the following year, after the annual shareholders’ meeting.**Dividend yield was calculated with the share price at the end of each year.

2020

22

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

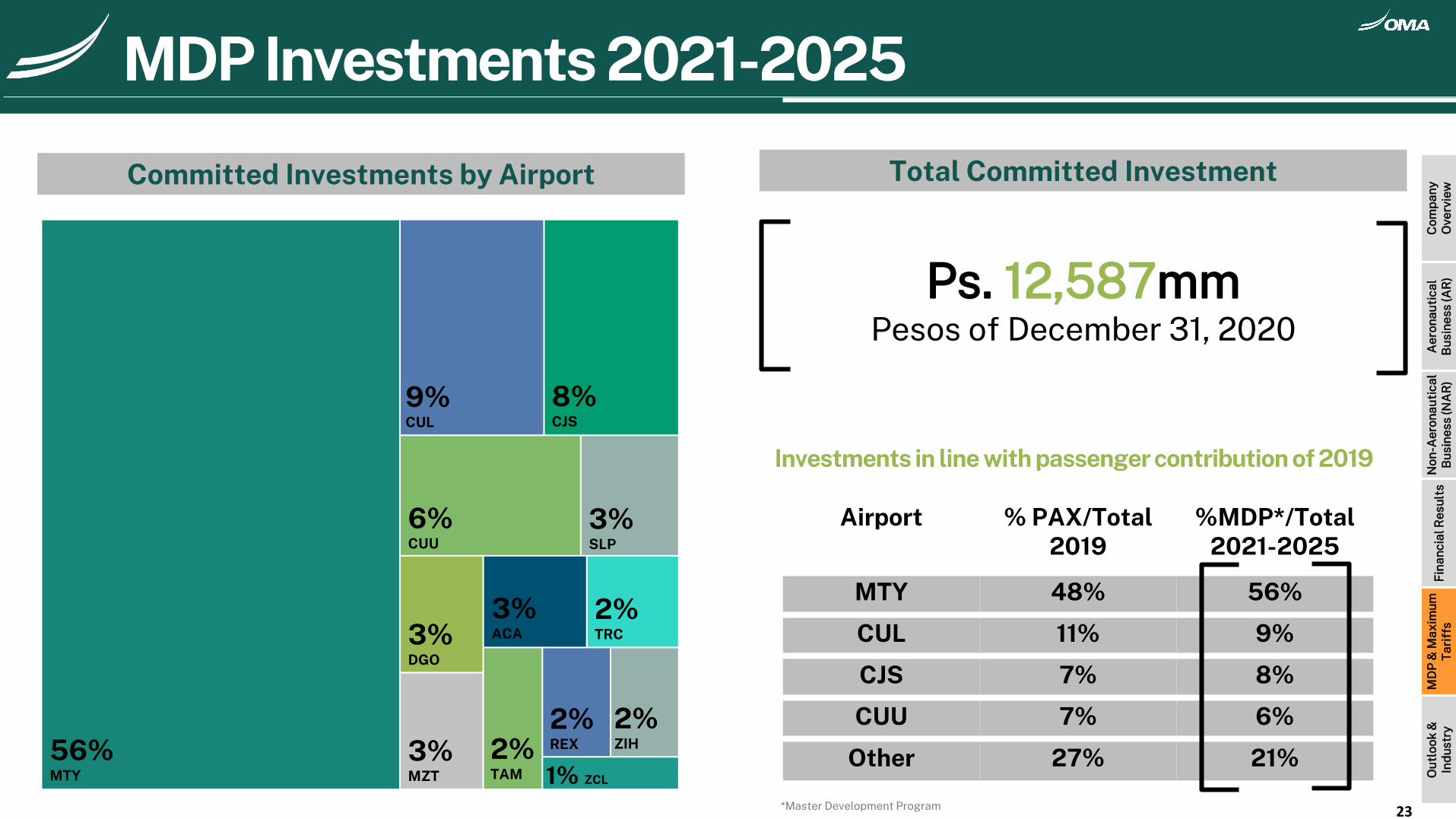

Investments in line with passenger contribution of 2019

MDP Investments 2021-2025

Airport % PAX/Total 2019

%MDP*/Total2021-2025

MTY 48% 56%

CUL 11% 9%

CJS 7% 8%

CUU 7% 6%

Other 27% 21%

Total Committed InvestmentCommitted Investments by Airport

Ps. 12,587mmPesos of December 31, 2020

56%MTY

9%CUL

8%CJS

6%CUU

3%SLP

3%DGO

3%ACA

2%TRC

3%MZT

2%TAM

2%REX

2%ZIH

1% ZCL

23*Master Development Program

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

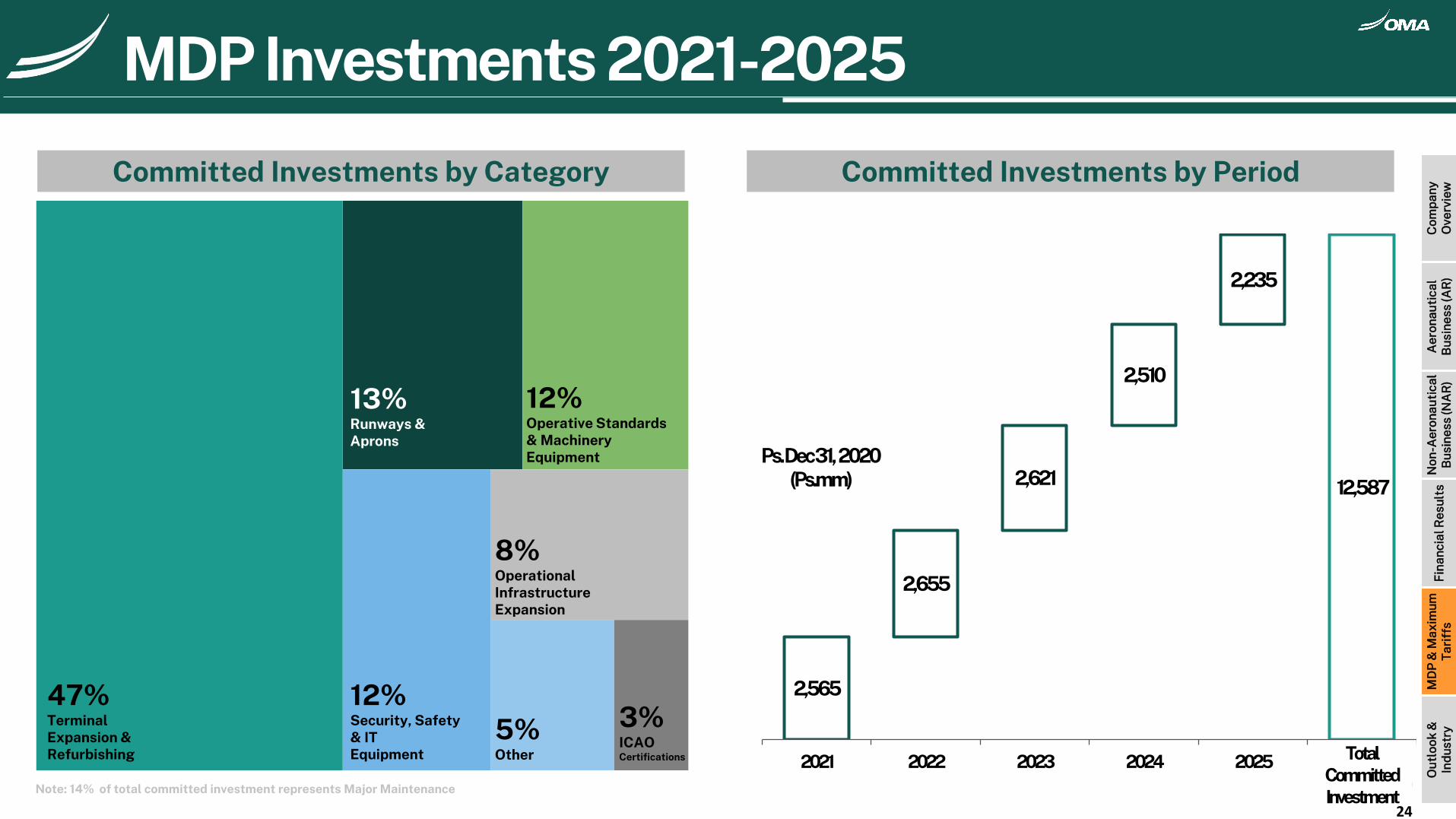

Note: 14% of total committed investment represents Major Maintenance

2,565

2,655

2,621

2,510

2,235

12,587

2021 2022 2023 2024 2025 Total Comprometido

Ps. Dec 31, 2020 (Ps.mm)

Total Committed Investment

MDP Investments 2021-2025

Committed Investments by Category

47%TerminalExpansion &Refurbishing

13%Runways &Aprons

12%Operative Standards & Machinery Equipment

8%Operational Infrastructure Expansion

12%Security, Safety & ITEquipment

5%Other

3%ICAO Certifications

Committed Investments by Period

24

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

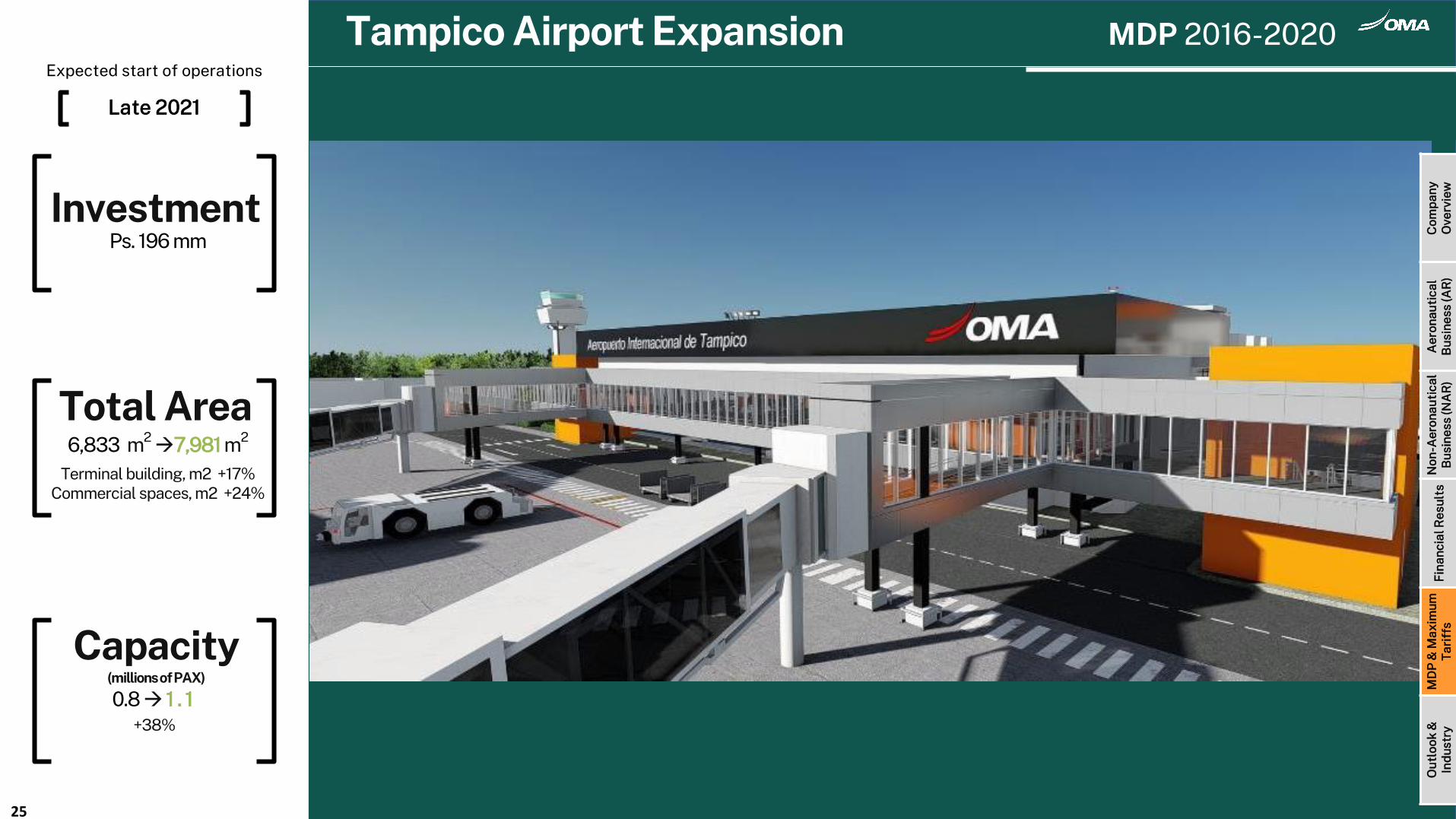

Tampico Airport Expansion MDP 2016-2020

25

Expected start of operations

Late 2021

Total Area6,833 m2

→7,981 m2

Terminal building, m2 +17% Commercial spaces, m2 +24%

0.8→ 1 . 1+38%

InvestmentPs. 196 mm

Capacity(millions of PAX)

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

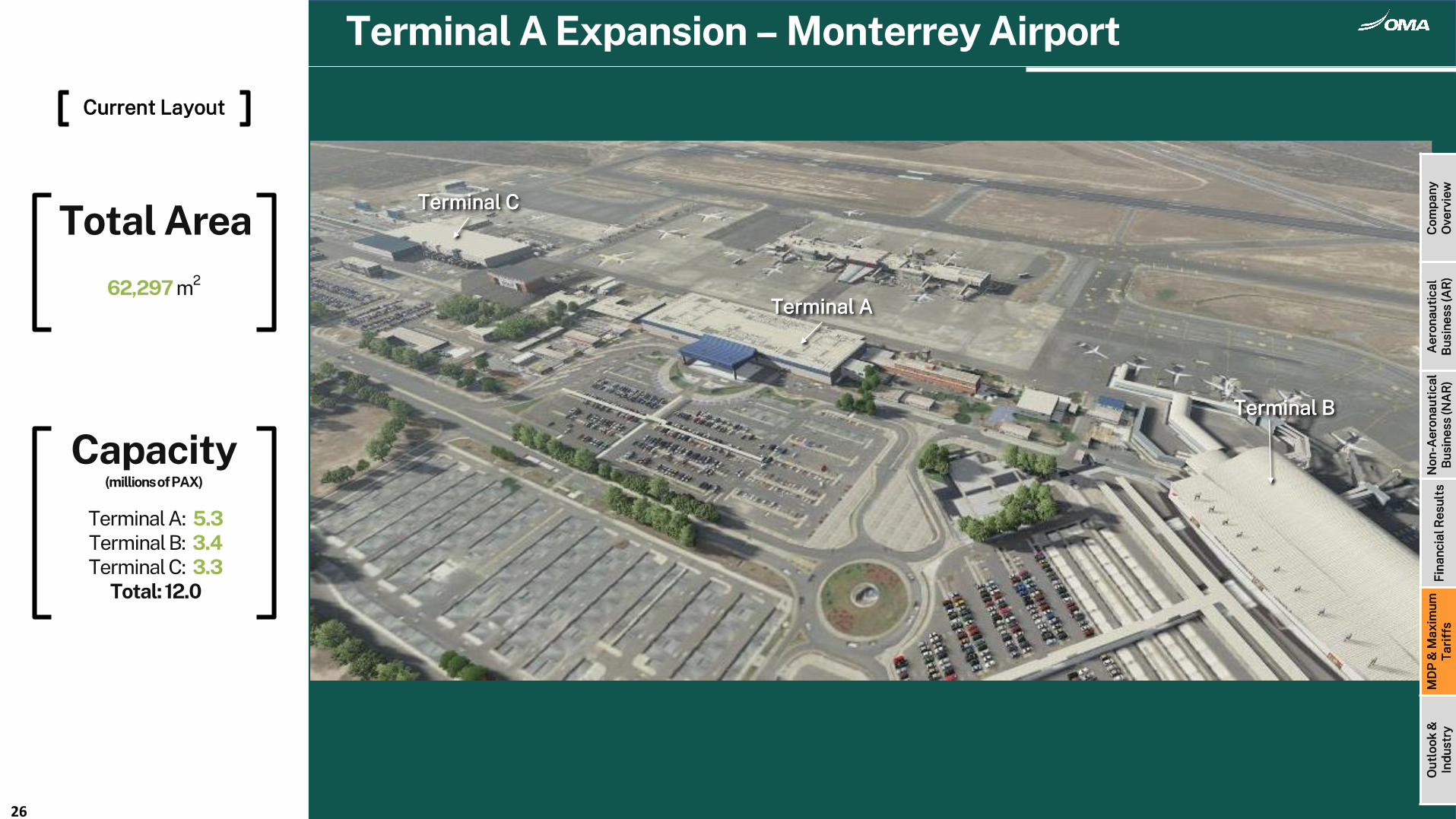

Total Area

62,297 m2

Capacity(millions of PAX)

Terminal A: 5.3Terminal B: 3.4Terminal C: 3.3

Total: 12.0

Terminal A Expansion – Monterrey Airport

Terminal C

Terminal A

Terminal B

26

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

Current Layout

Terminal A Expansion – Monterrey Airport

Terminal C

Terminal A

Terminal B

Wing #1

Public Area of TA

Terminal A

Terminal B

27

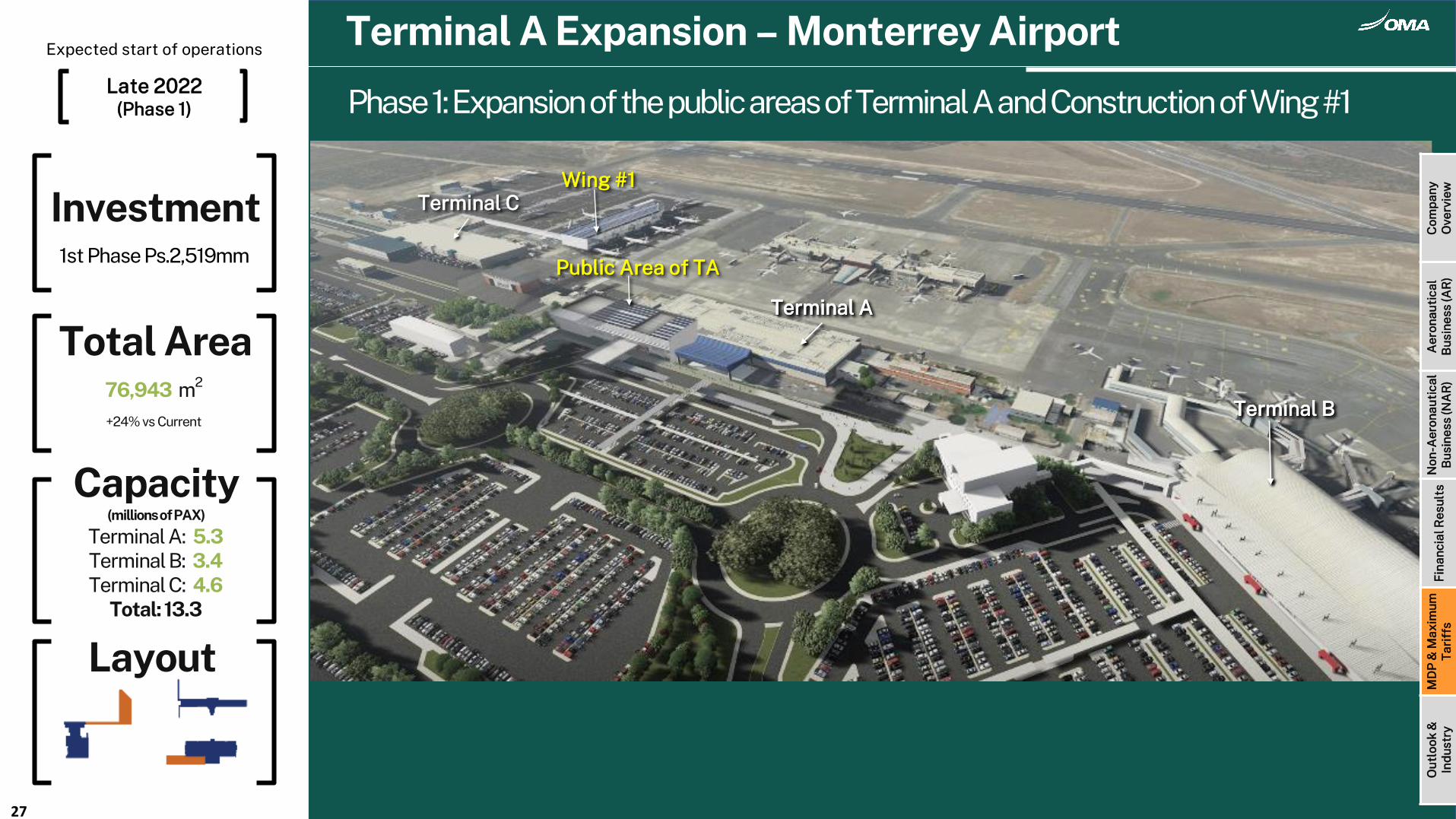

Phase 1: Expansion of the public areas of Terminal A and Construction of Wing #1

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

Total Area76,943 m2

+24% vs Current

Investment1st Phase Ps.2,519mm

Layout

Terminal A: 5.3Terminal B: 3.4Terminal C: 4.6

Total: 13.3

Capacity(millions of PAX)

Expected start of operations

Late 2022(Phase 1)

Terminal A Expansion – Monterrey Airport

Terminal A

Terminal B

Terminal A

Terminal B

Wing #2

General Expansion of

Terminal A

Wing #1

28

Phase 2: Construction of Wing #2 and Expansion of Both Public and Restricted Areas

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

Total Area91,696 m2

+19% vs Phase 1

Investment2nd Phase Ps.2,286mm

Layout

Terminal A: 12.9Terminal B: 3.4

Total: 16.3

Capacity(millions of PAX)

Expected start of operations

Late 2025(Phase 2)

Expansion and Remodeling – Culiacán Airport

29

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

2024

Total Area12,128 m2

→24,330 m2

Terminal building, m2 +101% Commercial spaces, m2

+107%

2.1→3 . 3+57%

InvestmentPs. 454 mm

Capacity(millions of PAX)

Expansion and Remodeling – Ciudad Juárez Airport

30

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

Expected start of operations

End 2022

Total Area6,210 m2

→12,470 m2

Terminal building, m2 +101% Commercial spaces, m2 +111%

0.96→ 1 . 9+111%

InvestmentPs. 493 mm

Capacity(millions of PAX)

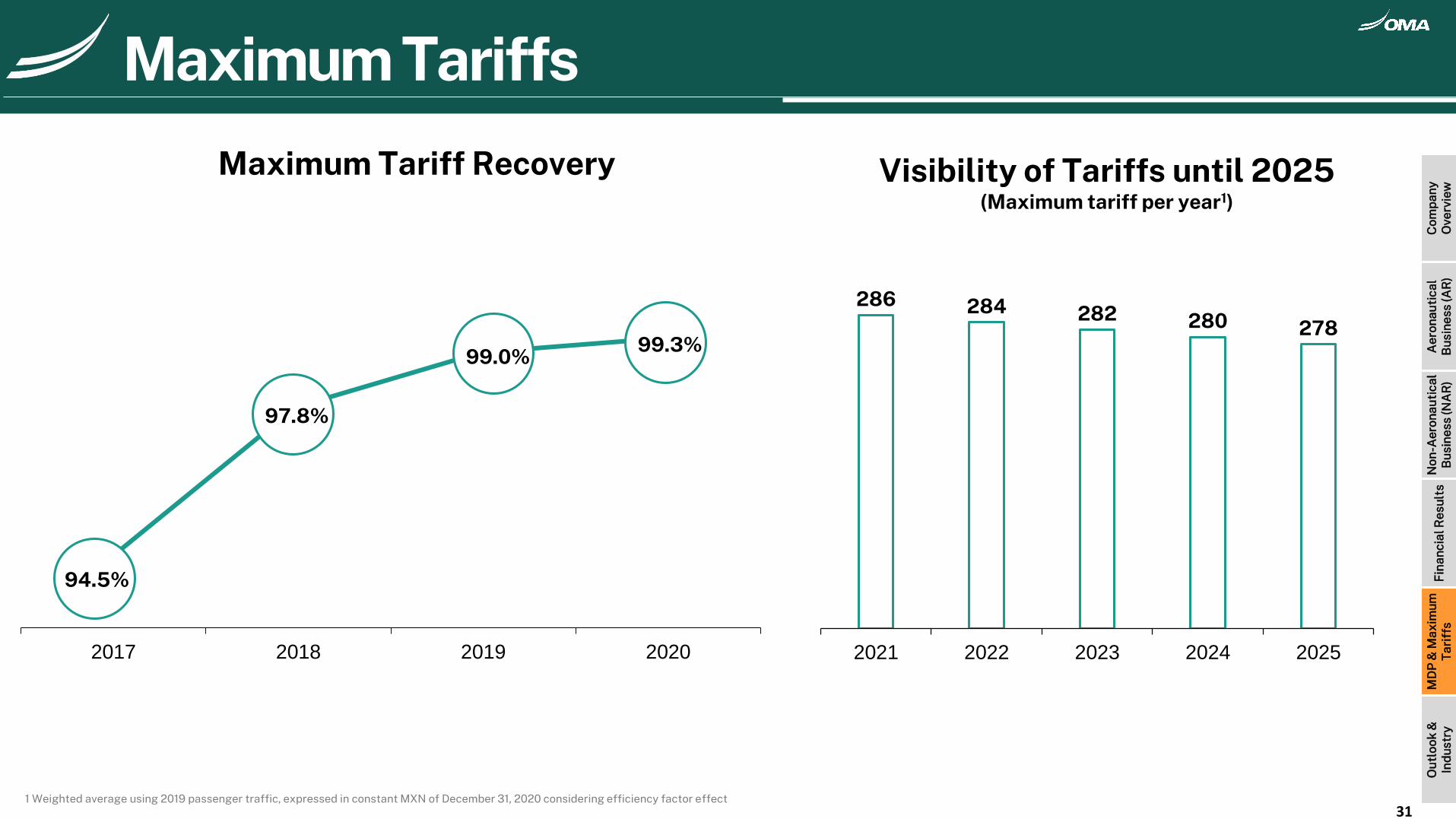

94.5%

97.8%

99.0%99.3%

2017 2018 2019 2020

Maximum Tariff Recovery

1 Weighted average using 2019 passenger traffic, expressed in constant MXN of December 31, 2020 considering efficiency factor effect

Maximum Tariffs

31

286 284 282 280 278

2021 2022 2023 2024 2025

Visibility of Tariffs until 2025(Maximum tariff per year1)

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

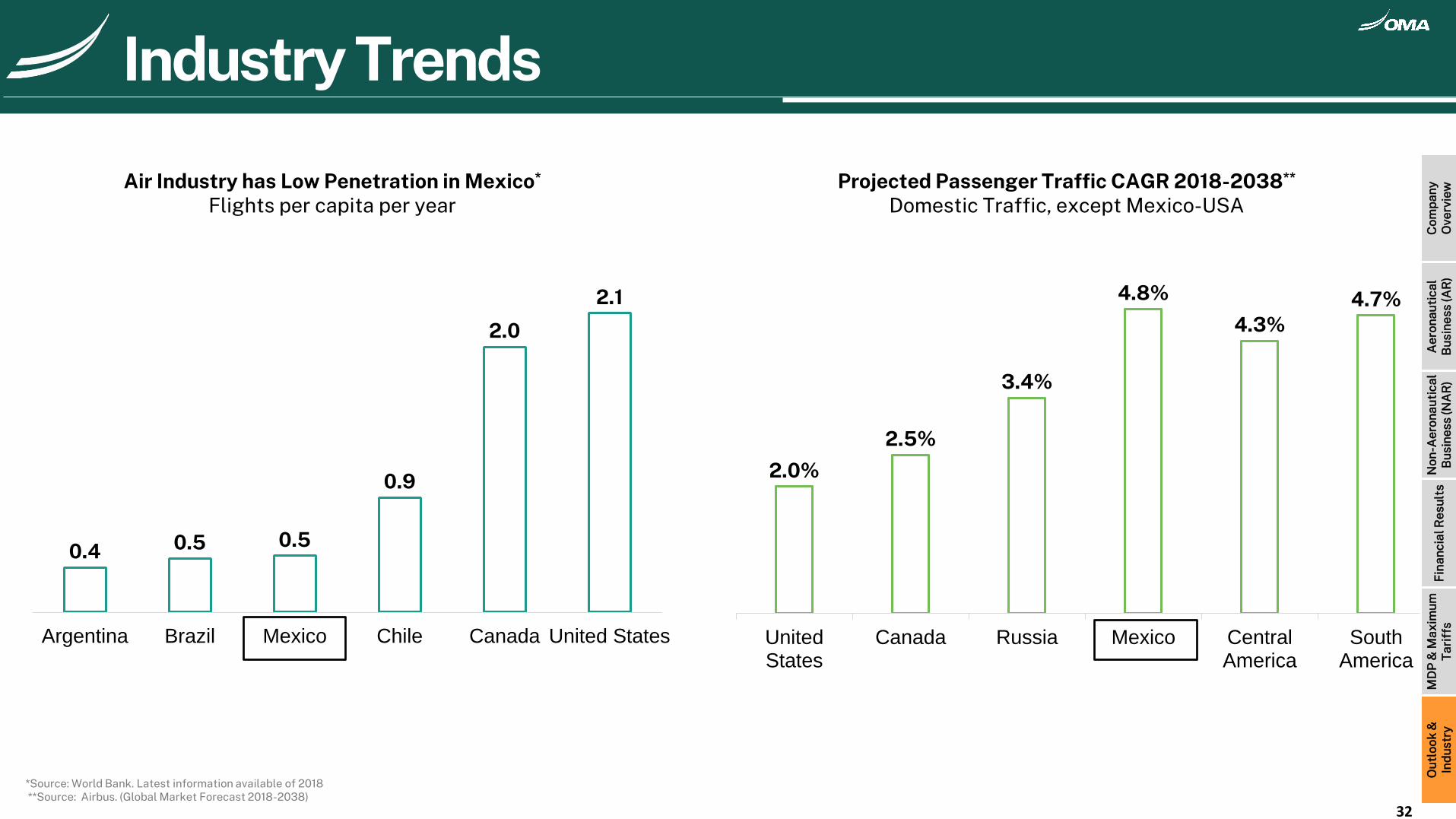

Air Industry has Low Penetration in Mexico*

Flights per capita per yearProjected Passenger Traffic CAGR 2018-2038**

Domestic Traffic, except Mexico-USA

*Source: World Bank. Latest information available of 2018**Source: Airbus. (Global Market Forecast 2018-2038)

0.4 0.5 0.5

0.9

2.0

2.1

Argentina Brazil Mexico Chile Canada United States

Industry Trends

2.0%

2.5%

3.4%

4.8%

4.3%4.7%

UnitedStates

Canada Russia Mexico CentralAmerica

SouthAmerica

32

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

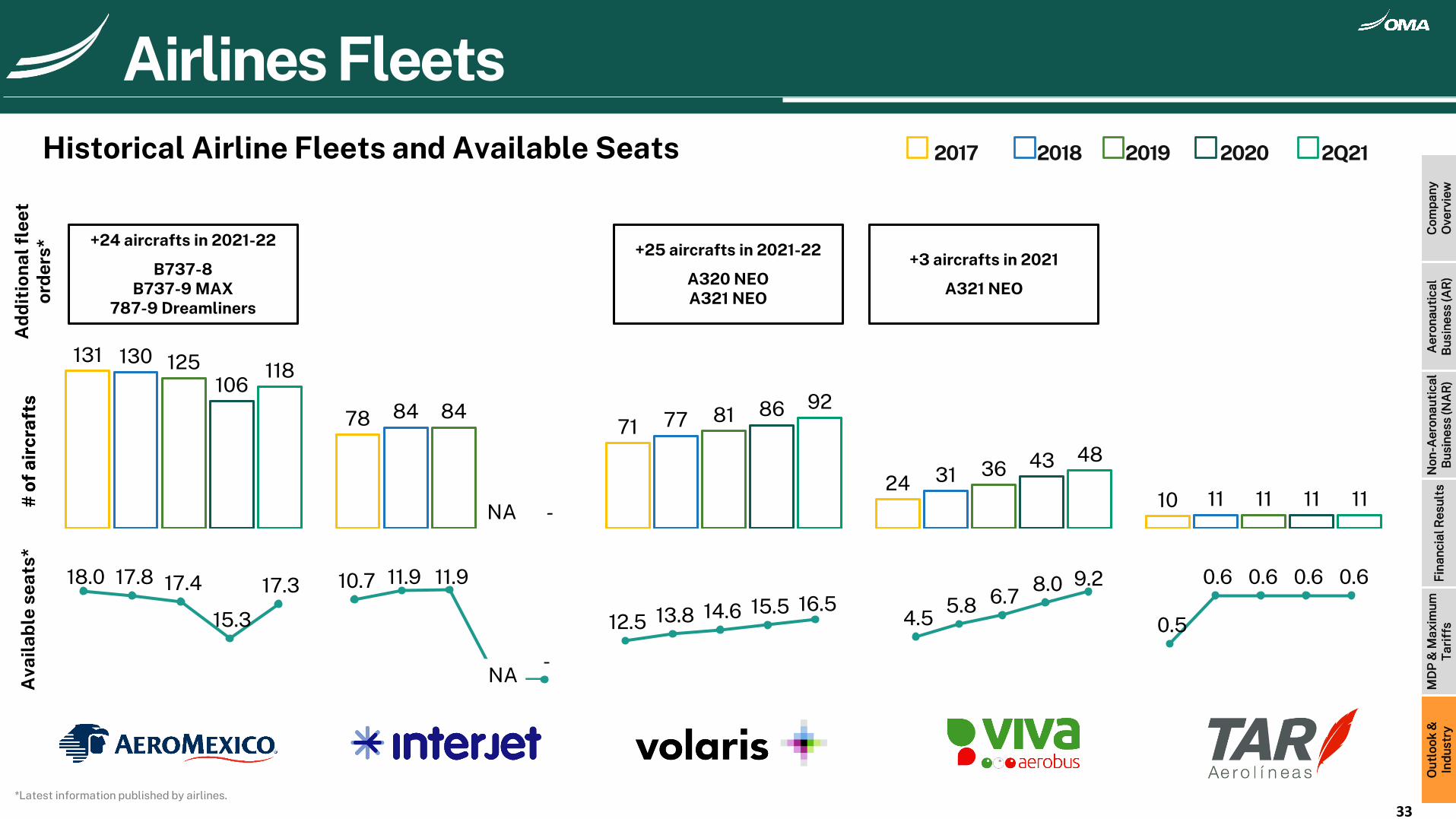

Historical Airline Fleets and Available Seats

131

78 71

2410

130

84 77

3111

125

84 81

36

11

106

NA

86

43

11

118

-

92

48

11

2017 2018 2019 2020 2Q21

Ava

ilab

lese

ats*

10.7 11.9 11.9

- -

18.0 17.8 17.4

15.3

17.3

12.5 13.8 14.6 15.5 16.5 4.5

5.8 6.7 8.0 9.2

-

2.0

4.0

6.0

8.0

10.0

0.5

0.6 0.6 0.6 0.6

NA

Airlines Fleets

+25 aircrafts in 2021-22

A320 NEOA321 NEO

+24 aircrafts in 2021-22

B737-8B737-9 MAX

787-9 Dreamliners

+3 aircrafts in 2021

A321 NEO

*Latest information published by airlines.

33

# o

fai

rcra

fts

# o

fai

rcra

fts

Ad

dit

ion

alfl

eet

ord

ers*

Com

pan

yO

verv

iew

Aer

onau

tica

lB

usin

ess

(AR

)N

on-A

eron

auti

cal

Bus

ines

s (N

AR

)F

inan

cial

Res

ults

MD

P &

Max

imum

Tar

iffs

Out

look

&In

dus

try

Chief Financial OfficerRuffoPérez Pliego del Castillo

[email protected]+52.81.8625.4300

Investor RelationsLuis Emmanuel Camacho Thierry

[email protected]+52.81.8625.4308

Follow us on:

Contact

GRUPO AEROPORTUARIO DEL CENTRO NORTE, S.A.B. DE C.V.