2015 Second Quarter Update

12

2015 Second Quarter Update August 5, 2015

-

Upload

company-spotlight -

Category

Investor Relations

-

view

360 -

download

0

Transcript of 2015 Second Quarter Update

2015 Second Quarter Update

August 5, 2015

2015 SECOND QUARTER UPDATE |

Safe Harbor Statement

Some of what we’ll discuss today concerning future company performance

will be forward-looking information within the meanings of the securities

laws. Actual results may materially differ from those discussed in these

forward-looking statements, and you should refer to the additional

information contained in Spectra Energy and Spectra Energy Partners’ Forms

10-K and other filings made with the SEC concerning factors that could cause

those results to differ from those contemplated in today’s discussion. As this

is a joint presentation, the terms “we,” “our,” and “us” refer to Spectra Energy

and/or Spectra Energy Partners, as appropriate.

Reg G Disclosure

In addition, today’s discussion includes certain non-GAAP financial measures

as defined under SEC Regulation G. A reconciliation of those measures to the

most directly comparable GAAP measures is available on our website.

2

2015 SECOND QUARTER UPDATE |

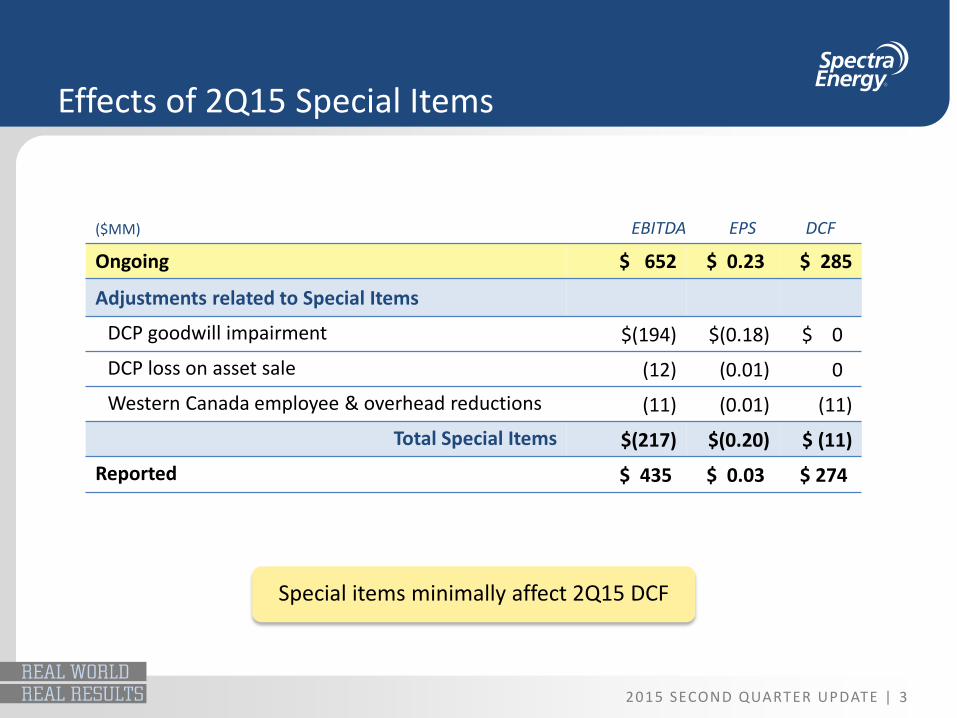

Effects of 2Q15 Special Items

3

($MM) EBITDA EPS DCF

Ongoing $ 652 $ 0.23 $ 285

Adjustments related to Special Items

DCP goodwill impairment $(194) $(0.18) $ 0

DCP loss on asset sale (12) (0.01) 0

Western Canada employee & overhead reductions (11) (0.01) (11)

Total Special Items $(217) $(0.20) $ (11)

Reported $ 435 $ 0.03 $ 274

Special items minimally affect 2Q15 DCF

2015 SECOND QUARTER UPDATE |

2Q15 Results – Ongoing EBITDA

4

Spectra Energy Partners Distribution Western Canada Field Services

U.S. Transmission • Increased earnings from

expansions previously placed into service (TEAM 2014, TEAM South and Kingsport)

Liquids • Higher crude transportation

revenues, mainly due to higher volumes and increased tariff rates on Express

• Higher volumes on Sand Hills

• Decreased earnings from lower Canadian dollar

• Higher Empress earnings • Partially offset by lower

Canadian dollar

• Decreased earnings from lower commodity prices

• Partially offset by increased earnings from asset growth, improved operating efficiencies and other initiatives

PERFORMANCE DRIVERS FOR THE QUARTER:

Ongoing SE EBITDA ($MM) 2Q15 2Q14

YTD 2Q15

YTD 2Q14

Spectra Energy Partners(2) $478 $374 $942 $803

Distribution 98 112 290 338

Western Canada 115 111 276 348

Field Services(1) (27) 54 (41) 184

Other (12) (24) (27) (41)

Ongoing SE EBITDA $652 $627 $1,440 $1,632 (1) Represents equity earnings of DCP + gains from DPM equity issuances. (2) EBITDA for SEP is different than the EBITDA reported for the Spectra Energy Partners segment

within SE. The primary difference is because SEP standalone reports its own Corporate Other.

Ongoing SEP EBITDA ($MM) 2Q15 2Q14

YTD 2Q15

YTD 2Q14

U.S. Transmission $396 $320 $794 $694

Liquids 78 51 142 109

Other(2) (18) (18) (35) (37)

Ongoing SEP EBITDA(2) $456 $353 $901 $766

2015 SECOND QUARTER UPDATE |

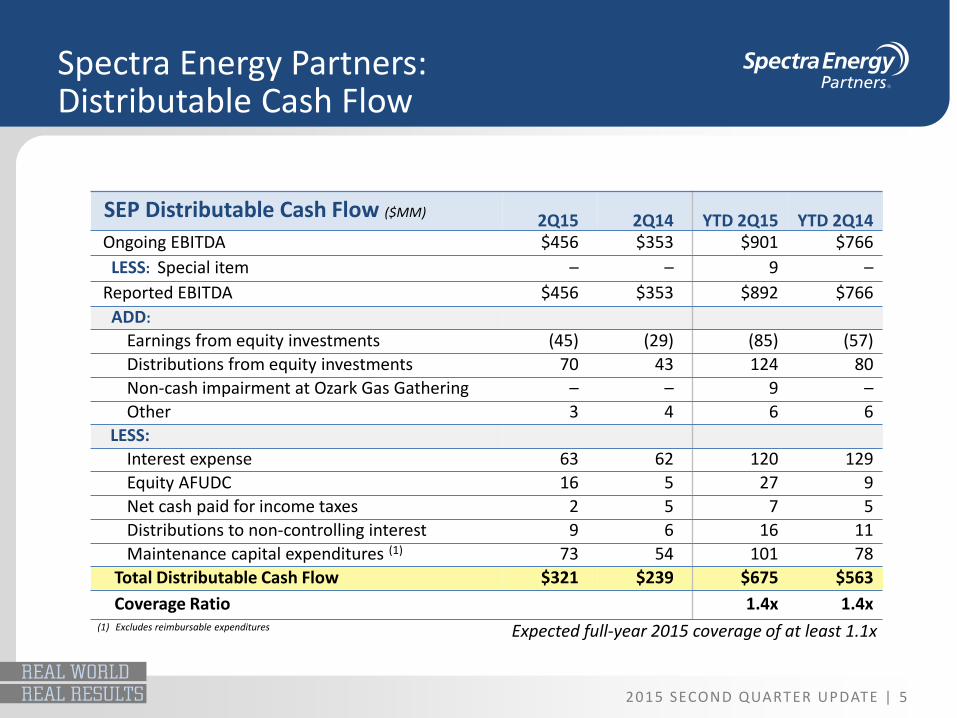

Spectra Energy Partners: Distributable Cash Flow

5

SEP Distributable Cash Flow ($MM) 2Q15 2Q14 YTD 2Q15 YTD 2Q14

Ongoing EBITDA $456 $353 $901 $766

LESS: Special item – – 9 –

Reported EBITDA $456 $353 $892 $766

ADD:

Earnings from equity investments (45) (29) (85) (57)

Distributions from equity investments 70 43 124 80

Non-cash impairment at Ozark Gas Gathering – – 9 –

Other 3 4 6 6

LESS:

Interest expense 63 62 120 129

Equity AFUDC 16 5 27 9

Net cash paid for income taxes 2 5 7 5

Distributions to non-controlling interest 9 6 16 11

Maintenance capital expenditures (1) 73 54 101 78

Total Distributable Cash Flow $321 $239 $675 $563

Coverage Ratio 1.4x 1.4x (1) Excludes reimbursable expenditures Expected full-year 2015 coverage of at least 1.1x

2015 SECOND QUARTER UPDATE |

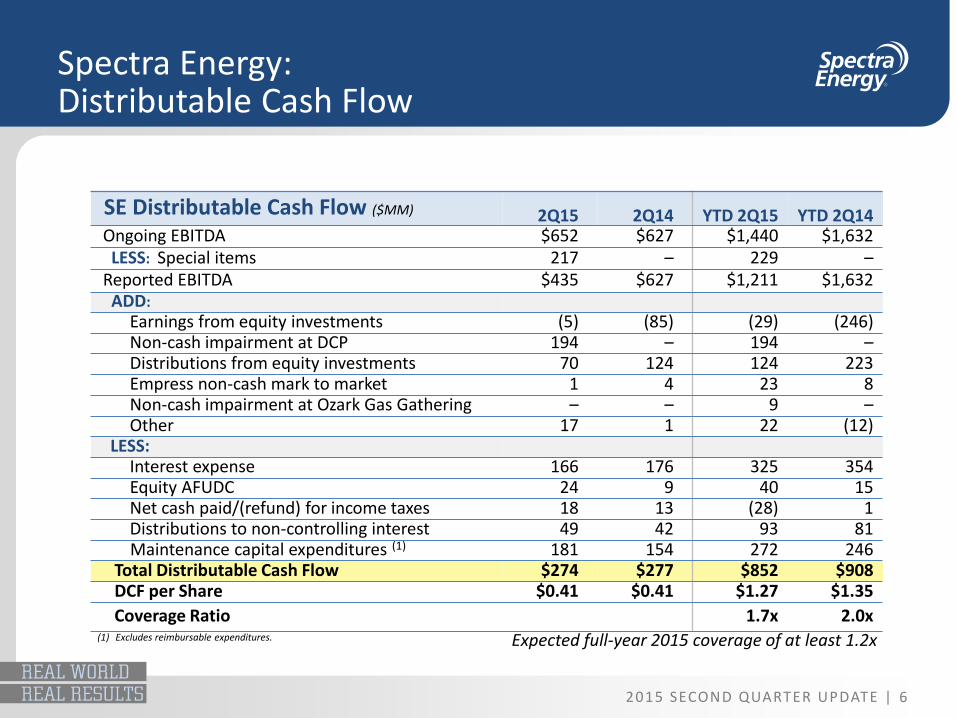

SE Distributable Cash Flow ($MM) 2Q15 2Q14 YTD 2Q15 YTD 2Q14 Ongoing EBITDA $652 $627 $1,440 $1,632 LESS: Special items 217 – 229 – Reported EBITDA $435 $627 $1,211 $1,632 ADD:

Earnings from equity investments (5) (85) (29) (246) Non-cash impairment at DCP 194 – 194 – Distributions from equity investments 70 124 124 223 Empress non-cash mark to market 1 4 23 8 Non-cash impairment at Ozark Gas Gathering – – 9 – Other 17 1 22 (12)

LESS: Interest expense 166 176 325 354 Equity AFUDC 24 9 40 15 Net cash paid/(refund) for income taxes 18 13 (28) 1 Distributions to non-controlling interest 49 42 93 81 Maintenance capital expenditures (1) 181 154 272 246

Total Distributable Cash Flow $274 $277 $852 $908 DCF per Share $0.41 $0.41 $1.27 $1.35

Coverage Ratio 1.7x 2.0x

6

Spectra Energy: Distributable Cash Flow

(1) Excludes reimbursable expenditures. Expected full-year 2015 coverage of at least 1.2x

2015 SECOND QUARTER UPDATE |

CEO Priorities

7

Operate assets safely and reliably

Continue to facilitate growth and increase shareholder returns • Execute on secured project backlog

• Secure projects in development

• Structure DCP Midstream for the long-term

• Participate in industry consolidation

2015 SECOND QUARTER UPDATE |

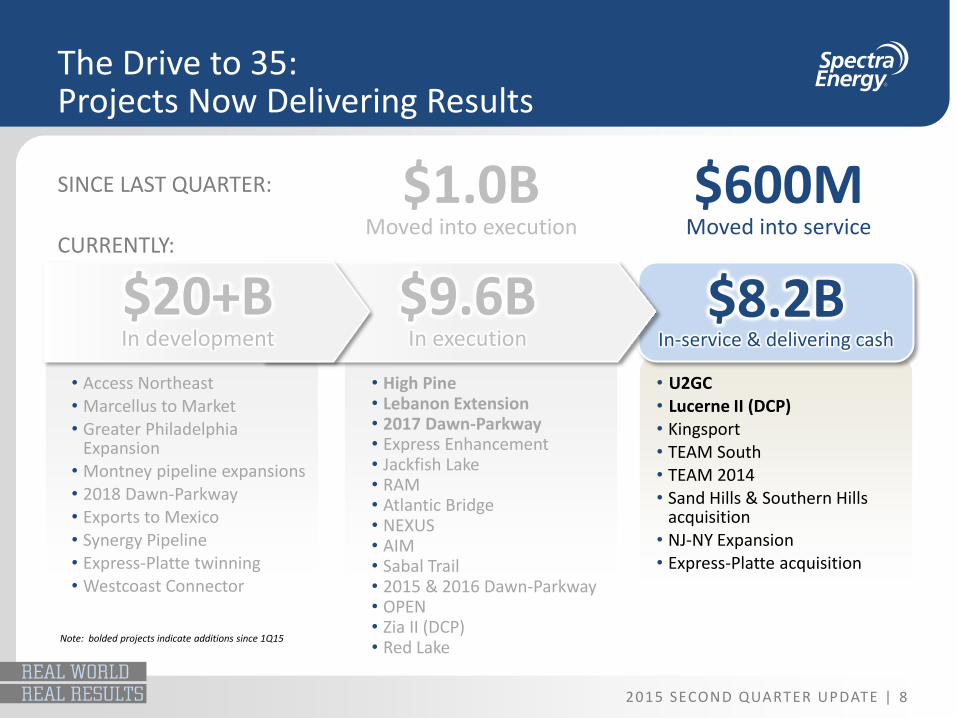

The Drive to 35: Projects Now Delivering Results

8

• Access Northeast • Marcellus to Market • Greater Philadelphia

Expansion • Montney pipeline expansions • 2018 Dawn-Parkway • Exports to Mexico • Synergy Pipeline • Express-Platte twinning • Westcoast Connector

SINCE LAST QUARTER: $1.0B Moved into execution

$600M Moved into service

$8.2B In-service & delivering cash

$9.6B In execution

$20+B In development

CURRENTLY:

• U2GC • Lucerne II (DCP) • Kingsport • TEAM South • TEAM 2014 • Sand Hills & Southern Hills

acquisition • NJ-NY Expansion • Express-Platte acquisition

• High Pine • Lebanon Extension • 2017 Dawn-Parkway • Express Enhancement • Jackfish Lake • RAM • Atlantic Bridge • NEXUS • AIM • Sabal Trail • 2015 & 2016 Dawn-Parkway • OPEN • Zia II (DCP) • Red Lake

Note: bolded projects indicate additions since 1Q15

2015 SECOND QUARTER UPDATE |

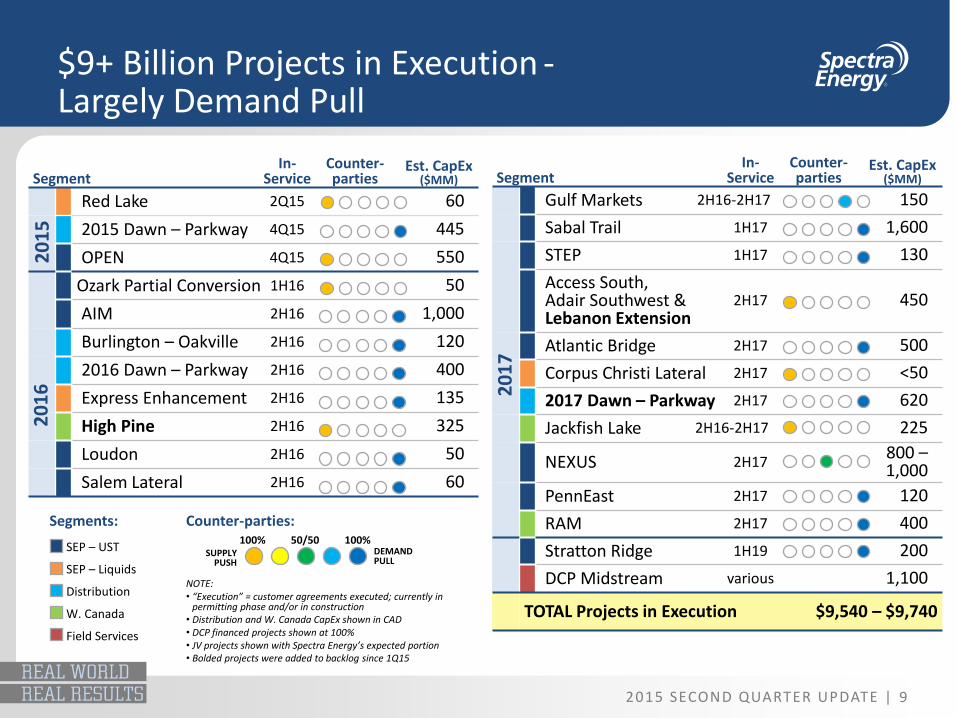

Segment In-

Service Counter- parties

Est. CapEx ($MM)

Gulf Markets 2H16-2H17 150

Sabal Trail 1H17 1,600

STEP 1H17 130

Access South, Adair Southwest & Lebanon Extension

2H17 450

Atlantic Bridge 2H17 500

Corpus Christi Lateral 2H17 <50

2017 Dawn – Parkway 2H17 620

Jackfish Lake 2H16-2H17 225

NEXUS 2H17 800 – 1,000

PennEast 2H17 120

RAM 2H17 400

Stratton Ridge 1H19 200

DCP Midstream various 1,100

TOTAL Projects in Execution $9,540 – $9,740

Segment In-

Service Counter- parties

Est. CapEx ($MM)

Red Lake 2Q15 60

2015 Dawn – Parkway 4Q15 445

OPEN 4Q15 550

Ozark Partial Conversion 1H16 50

AIM 2H16 1,000

Burlington – Oakville 2H16 120

2016 Dawn – Parkway 2H16 400

Express Enhancement 2H16 135

High Pine 2H16 325

Loudon 2H16 50

Salem Lateral 2H16 60

$9+ Billion Projects in Execution - Largely Demand Pull

9

20

15

2

01

6

SEP – UST

SEP – Liquids

Distribution

W. Canada

Field Services

SUPPLY PUSH

100% 100%50/50DEMAND PULL

20

17

Segments: Counter-parties:

NOTE: • “Execution” = customer agreements executed; currently in

permitting phase and/or in construction • Distribution and W. Canada CapEx shown in CAD • DCP financed projects shown at 100% • JV projects shown with Spectra Energy’s expected portion • Bolded projects were added to backlog since 1Q15

2015 SECOND QUARTER UPDATE |

The Drive to 35: Securing Projects for Future Growth

10

• Access Northeast • Marcellus to Market • Greater Philadelphia

Expansion • Montney pipeline expansions • 2018 Dawn-Parkway • Exports to Mexico • Synergy Pipeline • Express-Platte twinning • Westcoast Connector

• U2GC • Lucerne II (DCP) • Kingsport • TEAM South • TEAM 2014 • Sand Hills & Southern Hills

acquisition • NJ-NY Expansion • Express-Platte acquisition

$1.0B Moved into execution

$600M Moved into service

$8.2B In-service & delivering cash

$9.6B In execution

$20+B In development

SINCE LAST QUARTER:

CURRENTLY:

• High Pine • Lebanon Extension • 2017 Dawn-Parkway • Express Enhancement • Jackfish Lake • RAM • Atlantic Bridge • NEXUS • AIM • Sabal Trail • 2015 & 2016 Dawn-Parkway • OPEN • Zia II (DCP) • Red Lake

Note: bolded projects indicate additions since 1Q15

2015 SECOND QUARTER UPDATE | 11

Spectra Energy & Spectra Energy Partners offer best-in-class investment opportunities

Spectra Energy Partners

1. Strong portfolio Scale, diversity, strategically located assets

• Transportation, storage, LDC, G&P • Natural gas, crude, NGLs • US & Canadian operations

Connecting diverse supplies with growing demand markets

2. Stable cash flows Visible, contracted cash flows with little commodity exposure

2015e – 2017e ongoing EBITDA 99% fee-based

UST: 95% reservation-based revenue with no commodity or volume exposure

3. Robust growth profile Organic growth projects with attractive returns

Projects in execution provide incremental EBITDA of ~$1B by 2020

Projects in execution provide incremental EBITDA of ~$800M by 2020

4. Healthy financials Solid balance sheet and liquidity

• Disciplined financial management • Commitment to investment grade

balance sheet

• Majority of growth funded at SEP • ATM program

5. Solid track record Ability to execute and deliver on commitments

70+ projects totaling ~$9B placed into service since 2007

31 consecutive quarters of distribution increases

6. Attractive returns Sustainable, reliable dividend & distribution growth

• 9% dividend CAGR • 14 cent/year dividend increase

through 2017

• 8%-9% distribution CAGR • $0.0125/quarter distribution

increase through 2017

Investor Value Propositions

Spectra Energy 6 QUALITIES of PREMIER INVESTMENTS:

INVEST IN: