Overview EU-wide Stress Test 2014 Mario Quagliariello – Head of the Risk Analysis Unit 24/07/2014...

16

Overview EU-wide Stress Test 2014 Mario Quagliariello – Head of the Risk Analysis Unit 24/07/2014 - PRUEBAS DE ESTRÉS - La Visión del Regulador y el Impacto en la Banca JORNADA DEL CLUB DE GESTIÓN DE RIESGOS - Madrid

-

Upload

shawn-greer -

Category

Documents

-

view

214 -

download

1

Transcript of Overview EU-wide Stress Test 2014 Mario Quagliariello – Head of the Risk Analysis Unit 24/07/2014...

Overview EU-wide Stress Test 2014Mario Quagliariello – Head of the Risk Analysis Unit

24/07/2014 - PRUEBAS DE ESTRÉS - La Visión del Regulador y el Impacto en la Banca

JORNADA DEL CLUB DE GESTIÓN DE RIESGOS - Madrid

2

Agenda

Context

Key features

Process and timeline

1

2

3

3

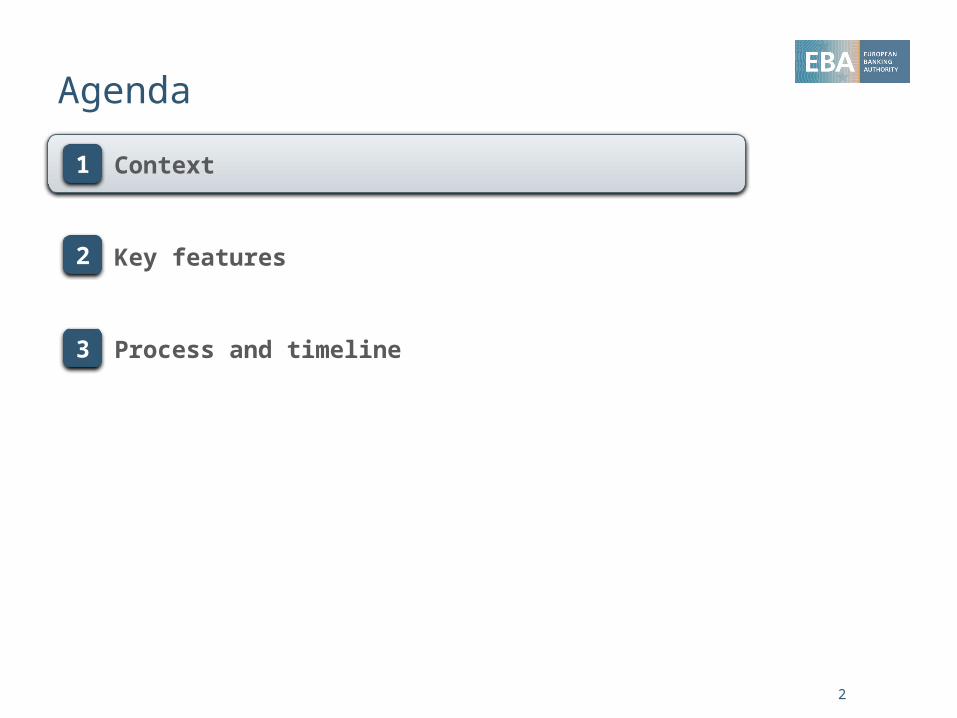

It's a long way to the ST … It's a long way to go…

Pre-emptive capital raising

Credit sensitivities Disclosure (capital

and sovereign)

EU-widestress test 2011

9% after sovereign buffer

EUR 204bn capital strengthening

CT1 ratio of 11.7% comparable to US

EU CT1 sufficient if RWA can be trusted

EU-widerecapitali-

sation

EBA recommendation Common definition of

NPL and forbearance CAs responsibility PIT assessment of

capital, with minimum threshold

AQRs

Forward looking assessment and reaction function

Significant frontloading

EU-widestress test

2014

Ongoing, leading to supervisory consistency, transparency and benchmarking

RWA consistency

4

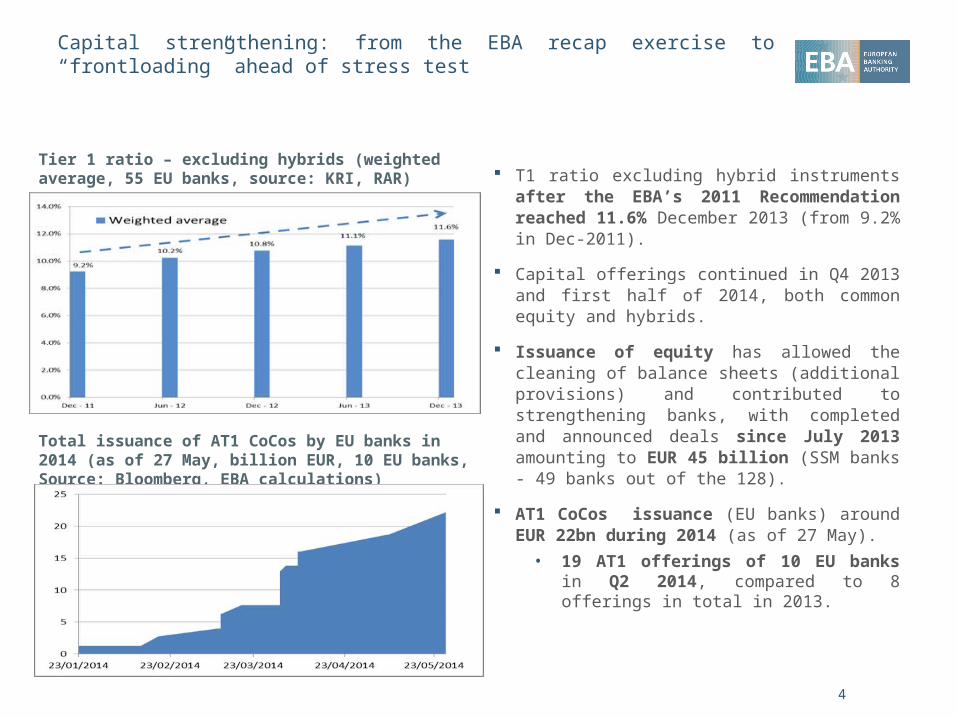

Capital strengthening: from the EBA recap exercise to “frontloading” ahead of stress test

T1 ratio excluding hybrid instruments after the EBA’s 2011 Recommendation reached 11.6% December 2013 (from 9.2% in Dec-2011).

Capital offerings continued in Q4 2013 and first half of 2014, both common equity and hybrids.

Issuance of equity has allowed the cleaning of balance sheets (additional provisions) and contributed to strengthening banks, with completed and announced deals since July 2013 amounting to EUR 45 billion (SSM banks - 49 banks out of the 128).

AT1 CoCos issuance (EU banks) around EUR 22bn during 2014 (as of 27 May).• 19 AT1 offerings of 10 EU banks in Q2

2014, compared to 8 offerings in total in 2013.

Tier 1 ratio – excluding hybrids (weighted average, 55 EU banks, source: KRI, RAR)

Total issuance of AT1 CoCos by EU banks in 2014 (as of 27 May, billion EUR, 10 EU banks, Source: Bloomberg, EBA calculations)

5

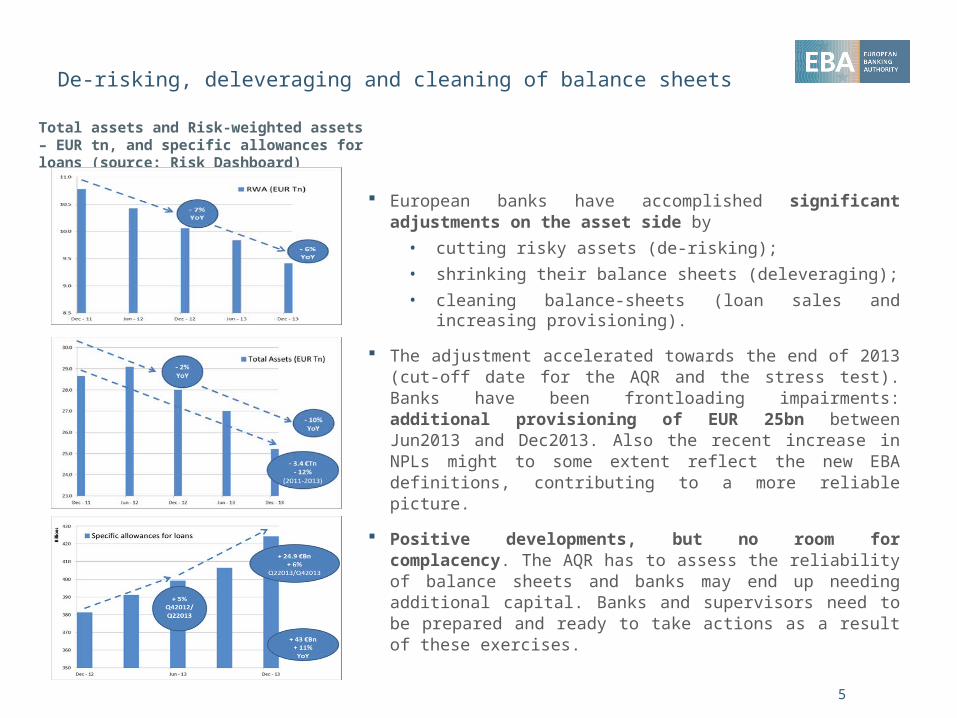

De-risking, deleveraging and cleaning of balance sheets

European banks have accomplished significant adjustments on the asset side by• cutting risky assets (de-risking);• shrinking their balance sheets (deleveraging);• cleaning balance-sheets (loan sales and increasing

provisioning).

The adjustment accelerated towards the end of 2013 (cut-off date for the AQR and the stress test). Banks have been frontloading impairments: additional provisioning of EUR 25bn between Jun2013 and Dec2013. Also the recent increase in NPLs might to some extent reflect the new EBA definitions, contributing to a more reliable picture.

Positive developments, but no room for complacency. The AQR has to assess the reliability of balance sheets and banks may end up needing additional capital. Banks and supervisors need to be prepared and ready to take actions as a result of these exercises.

Total assets and Risk-weighted assets – EUR tn, and specific allowances for loans (source: Risk Dashboard)

6

Agenda

Context

Key features

Process and time line

1

2

3

7

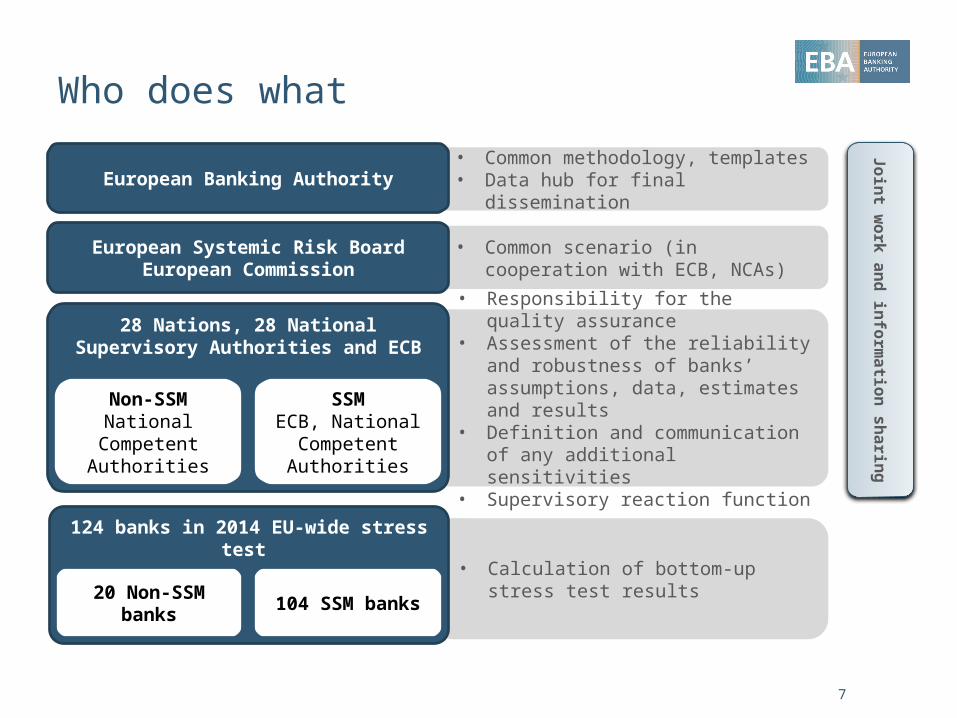

• Common methodology, templates • Data hub for final dissemination

• Common scenario (in cooperation with ECB, NCAs)

• Responsibility for the quality assurance• Assessment of the reliability and

robustness of banks’ assumptions, data, estimates and results

• Definition and communication of any additional sensitivities

• Supervisory reaction function

• Calculation of bottom-up stress test results

124 banks in 2014 EU-wide stress test

28 Nations, 28 National Supervisory Authorities and ECB

Who does what

European Systemic Risk BoardEuropean Commission

European Banking Authority

Non-SSMNational Competent

Authorities

SSMECB, National

Competent Authorities

20 Non-SSM banks 104 SSM banks

Joint work and inform

ation sharing

8

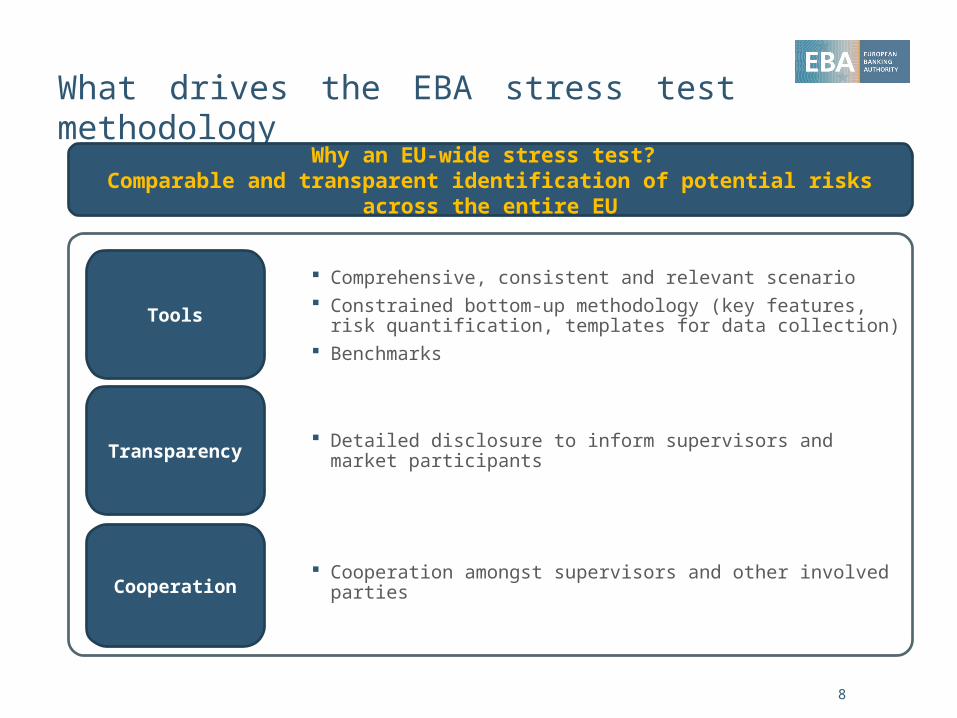

What drives the EBA stress test methodology

Why an EU-wide stress test? Comparable and transparent identification of potential risks across the entire EU

Tools

Transparency

Cooperation

Comprehensive, consistent and relevant scenario Constrained bottom-up methodology (key features, risk quantification,

templates for data collection) Benchmarks

Detailed disclosure to inform supervisors and market participants

Cooperation amongst supervisors and other involved parties

9

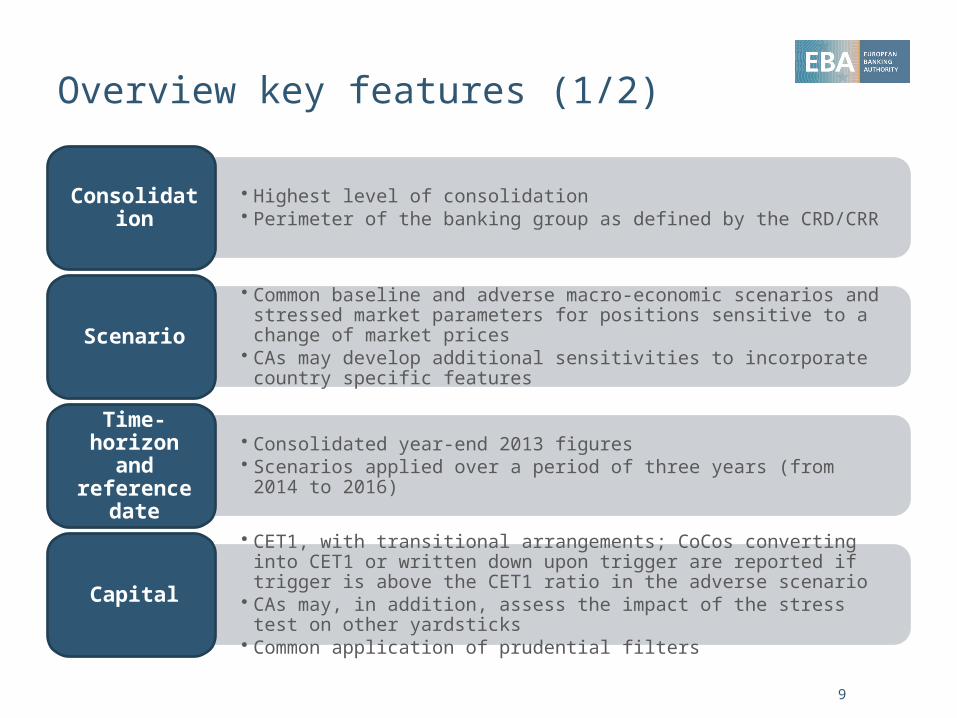

Overview key features (1/2)

• Highest level of consolidation• Perimeter of the banking group as defined by the CRD/CRRConsolidation

• Common baseline and adverse macro-economic scenarios and stressed market parameters for positions sensitive to a change of market prices

• CAs may develop additional sensitivities to incorporate country specific featuresScenario

• Consolidated year-end 2013 figures• Scenarios applied over a period of three years (from 2014 to 2016)

Time-horizon and reference

date

• CET1, with transitional arrangements; CoCos converting into CET1 or written down upon trigger are reported if trigger is above the CET1 ratio in the adverse scenario

• CAs may, in addition, assess the impact of the stress test on other yardsticks• Common application of prudential filters

Capital

10

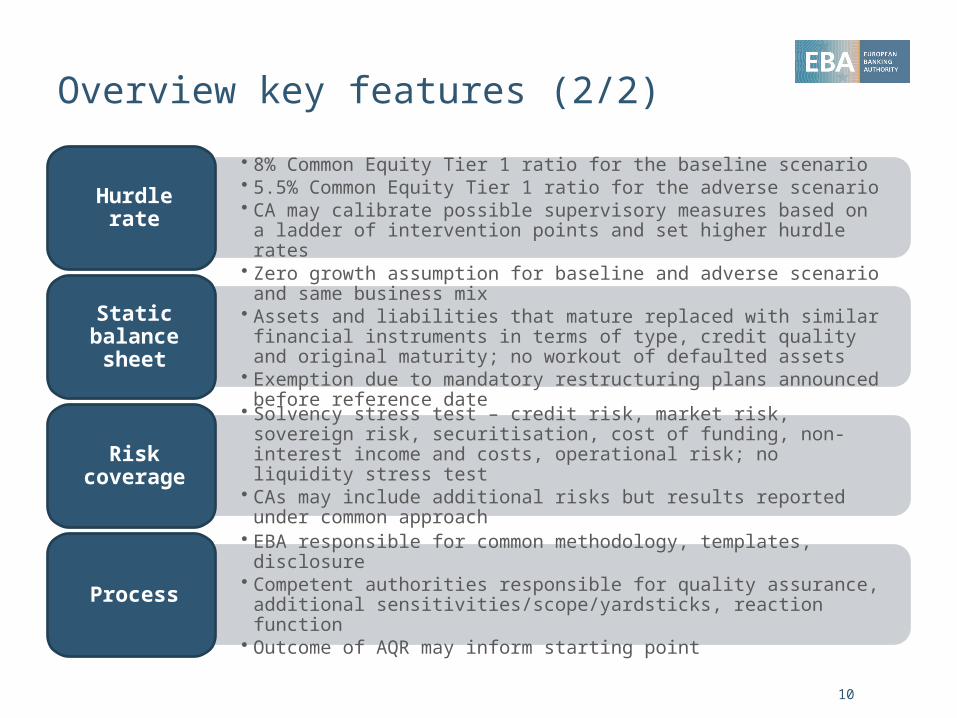

Overview key features (2/2)

• 8% Common Equity Tier 1 ratio for the baseline scenario• 5.5% Common Equity Tier 1 ratio for the adverse scenario• CA may calibrate possible supervisory measures based on a ladder of intervention

points and set higher hurdle rates

Hurdle rate

• Zero growth assumption for baseline and adverse scenario and same business mix• Assets and liabilities that mature replaced with similar financial instruments in

terms of type, credit quality and original maturity; no workout of defaulted assets• Exemption due to mandatory restructuring plans announced before reference date

Static balance sheet

• Solvency stress test – credit risk, market risk, sovereign risk, securitisation, cost of funding, non-interest income and costs, operational risk; no liquidity stress test

• CAs may include additional risks but results reported under common approachRisk coverage

• EBA responsible for common methodology, templates, disclosure• Competent authorities responsible for quality assurance, additional

sensitivities/scope/yardsticks, reaction function• Outcome of AQR may inform starting point

Process

11

Overview disclosure: 9 templates, 12k data points

• Main P&L items like net interest income, net trading income, impairments for financial assets and other comprehensive incomeP&L

• Exposure, RWA, value adjustments, provisions, default and loss rates• No disclosure of credit risk parameterCredit risk

• Market risk position by main risk typesMarket risk

• Securitisation exposure, RWA and impairmentsSecuritisation

• Sovereign exposure by country, maturity and accounting treatmentSovereign

• RWA by risk typeRWA

• Capital position, components, adequacy including, stressed• Capital restructuringCapital

~130

~6,500

~40

~50

~4,930

~50

~310

12

Agenda

Context

Key features

Process and time line

1

2

3

13

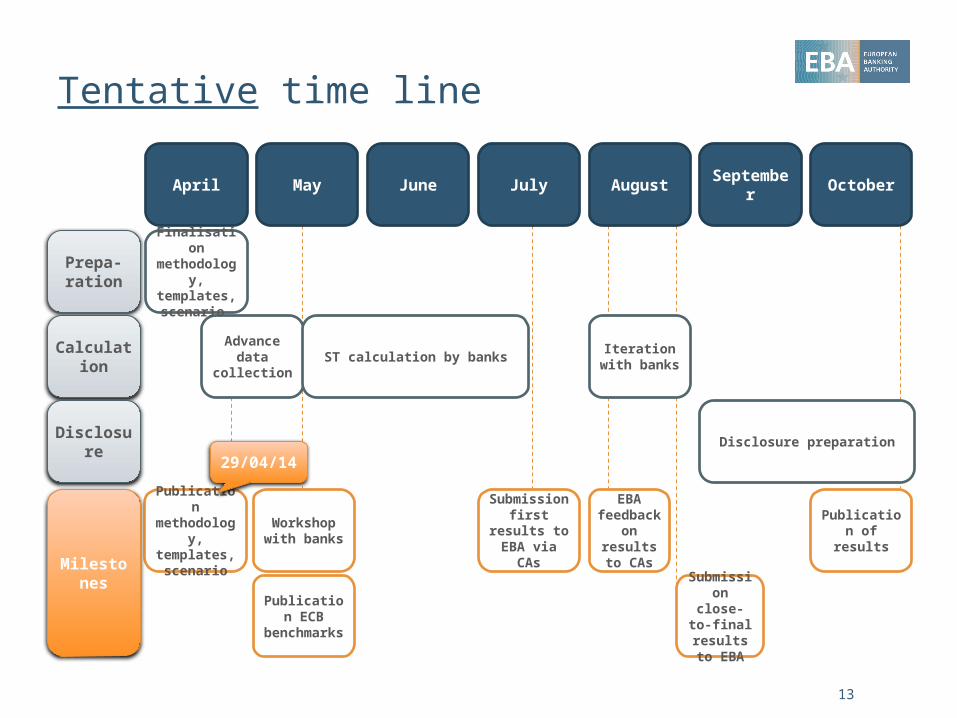

Tentative time line

April May June July August September October

Advance data collection ST calculation by banks Iteration with

banks

Publication ECB benchmarks

Submission close-to-

final results to EBA

Publication methodology,

templates, scenario

Workshop with banks

Submission first results to

EBA via CAs

EBA feedback on results

to CAs

Publication of results

Disclosure preparation

Prepa-ration

Calculation

Disclosure

Milestones

Finalisation methodology,

templates, scenario

29/04/14

14

Process is ongoing and on track (1/2)

The publication of the stress test methodology and scenarios took place on 29 April 2014.

An EBA “Q&A” process is in place to ensure immediate support to banks and supervisors. • We have received more than 1000 questions from banks and published on the EBA extranet. • The EBA QA team is liaising with the ECB as well as NCAs for more complex or controversial issues.

Banks have submitted the data for the advance data collection and preliminary results.• The EBA has run statistical quality checks and provided feedback to NCAs• The EBA distributed benchmarks on the stress test starting point in June to NCAs as originally planned

and currently working on “deltas”.• Benchmarks to be used as part of the quality assurance process NCAs and ECB are carrying out

15

Process is ongoing and on track (2/2)

The EBA is currently discussing details of communication in liaison with SSM colleagues as well as non SSM countries.• Including disclosure of additional national sensitivities, and• Stress test outcome for subsidiaries• Possible additional yardsticks/metrics to be disclosed • Interaction with banks

EBA is facilitating the cooperation and coordination between home and host authorities in the stress test as well as in the AQR

Quality assurance and join-up of AQR and ST, led by competent authorities, are key for the success of the exercise.

EUROPEAN BANKING AUTHORITY

Tower 42, 25 Old Broad StreetLondon EC2N 1HQ

Tel: +44 2073821770Fax: +44 207382177-1/2

E-mail: [email protected]://www.eba.europa.eu