Merk Presentation

18

LARGE ASIAN MANUFACTURERS IN THE GARMENT INDUSTRY: NEW CHALLENGES FOR LABOUR RIGHTS ADVOCATES BY JEROEN MERK [email protected]

-

Upload

brett-wright -

Category

Documents

-

view

221 -

download

0

Transcript of Merk Presentation

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 1/18

LARGE ASIAN

MANUFACTURERS IN THE

GARMENT INDUSTRY:NEW CHALLENGES FOR LABOUR RIGHTS

ADVOCATES

BY JEROEN MERK

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 2/18

INTRODUCTION

• Background and status of the research

• Labour rights advocates

• Growing importance of large Asian garmentmanufacturers

• Field research by AFW alliance and CCC inCambodia, India, Indonesia, and Sri Lanka

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 3/18

GLOBAL

OUTSOURCING

• Rising powers. Rising labour forces…?

• Labour geography (Herod, Wills, Cumbers) – the role of labour

• Global outsourcing, the transational

fragmentation of production,

• Consequences of labour (working conditions,

possibilities for reregulation, collective action)

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 4/18

SUBCONTRACTED

CAPITALISM

Spatial fragmentation of production processes throughoutsourcing arrangements makes it possible for one type ofcompanies to escape direct control over mass labor processes.

The organising of labour-intensive processes becomes“somebody‟s else problem”

It has drastically transformed the relation between capital andlabor.

The outsourcing system creates a „social distance between the

worker –the actual producer – and „the entity for which theproductive activity is ultimately performed‟ (McIntyre, 2008: 34-5).

Subcontacted capitalism‟ (Wills, 2009).

challenge for labour (unions et al)

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 5/18

FUNCTIONAL SPLIT

Global buyers (r etailers & brand-named

companies)

• Focus on end-consumer through

branding/retailing

• Outsource all (labour-intensive)

production

• Target of anti-sweatshop campaigns sinceearly 1990s - responded by adopting

ethical standards

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 6/18

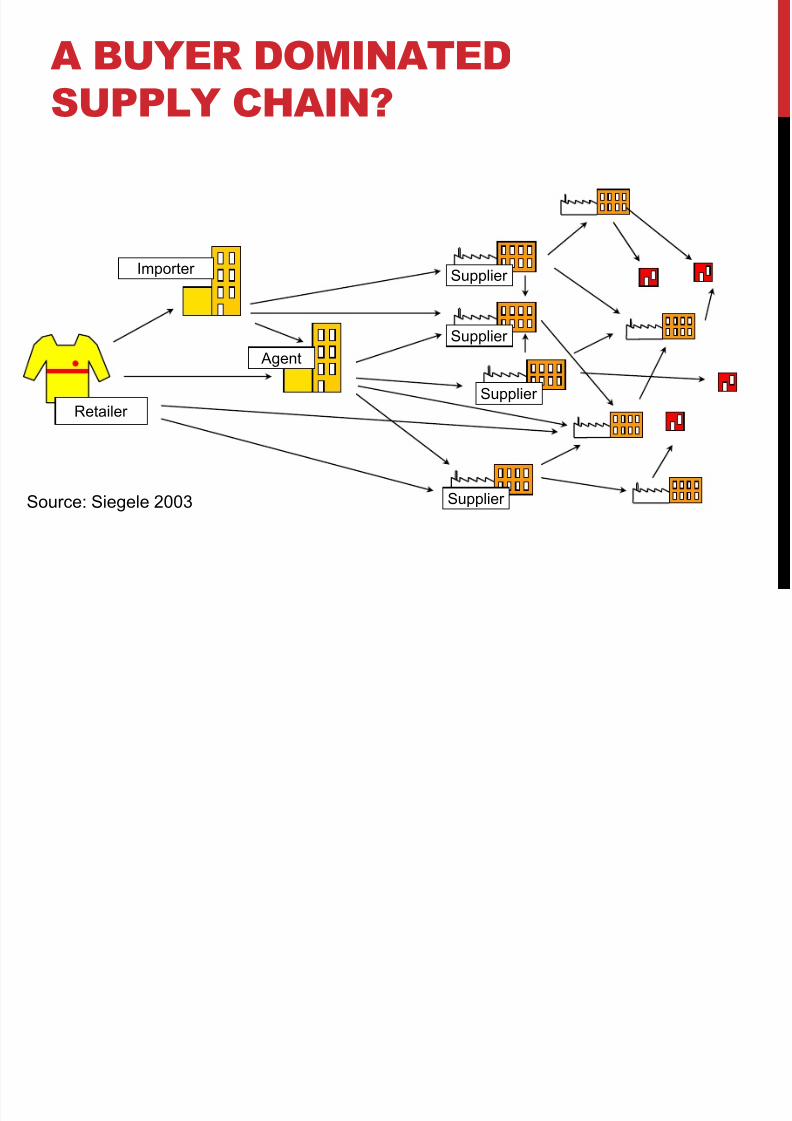

A BUYER DOMINATED

SUPPLY CHAIN?

Agent

Importer

Supplier

Supplier

Supplier

Supplier

Retailer

Source: Siegele 2003

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 7/18

CAPTIVE SUPPLIERS…AND/ OR

EMERGING GIANTS?

Many argue that labour-intensive manufacturing represents a„lower order‟ or „dead end‟ factor in competitiveness.

Supplier remains subordinated to agents that control „higher -order‟ factors like proprietary technology, product differentiation,

brand reputation, consumer relations and constant industrialupgrading (see Raikes et al. 2000: 5-6).

Some manufacturers, however, are doing very

well… Definition: Tier1 companies are large producers who have direct

supply relations with major brands and retailers. Some areTNCs themselves - while productive operations are dispersedthrough Asia and beyond. Other represent large national firms

that produce large volumes for export.

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 8/18

A FEW EXAMPLES

Dada Corporations: Korean cap manufacturer (25% of the world market), operatesfacilities in Bangladesh, China, Vietnam and Indonesia, from which it exports to theUnited States.

Esquel Group, which supplies companies like Tommy Hilfiger, Hugo Boss, Marks &

Spencer, Nordstrom, and Next. The company employs 47,000 employees dispersed over17 factories in nine countries.

Nien Hsing: The world‟s largest jean producer). While its plants in Taiwan only employs700 people, its facilities in Lesotho and Central America employ thousands of workers.

Ramatex: Malaysian manufacturing giant that operates plants in China, Namibia,Cambodia and Mauritius. The company employs 25,000 workers.

Similar trends in other labour-intensive sectors: athletic footwear (Yue Yuen),Electronics (Foxconn)

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 9/18

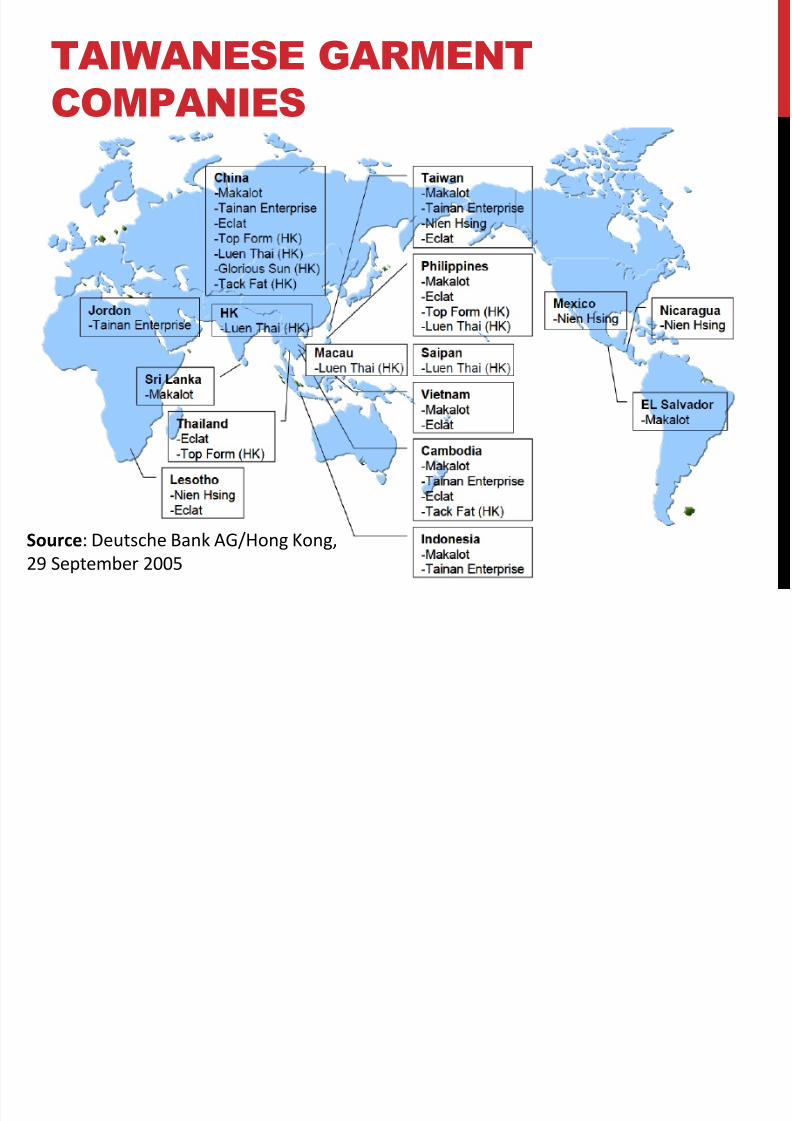

TAIWANESE GARMENT

COMPANIES

Source: Deutsche Bank AG/Hong Kong,

29 September 2005

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 10/18

HOW TO EXPLAIN

THEIR SUCCESS?

Centralisation/ consolidation tendencies

• Triangle manufacturing

MFA phase out (2005)

• Global buyers reduce number of suppliers to save costs,

reduce logistics issues, shortening lead times.

CSR…?

• Some indications that global buyers consolidate production at

larger suppliers to

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 11/18

WHO IS THE LEAD

FIRM?

With the increase of Asian production MNCs the questionemerges: who is the “lead firm”?

Some Asian MNCs are highly profitable operations, whoseearnings sometimes outstrip those of their EU or US-basedclients.

The policies and practices of which company within thesupply network are actually the most influential when itcomes to shaping the working conditions where goods areproduced?

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 12/18

HOW IMPORTANT ARE

LARGE GARMENT

MANUFACTURERS?

In Sri Lanka the four leading garment manufacturers account for24.34% of total Sri Lankan apparel export earnings. The industryprovides about 230,000 workers employment, about 70.000working these Tier 1 firms.

Majority of garment workers employed by smallcompanies:

• India’s apparel industry consists of an estimated 27,000

domestic manufacturers, 48,000 fabricators (jobcontractors) and about 1000 manufacturer exporters.

Only 6% of the overall garment industry is controlled by

large organized players.

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 13/18

CHARACTERISTICS

• Find and train, and discipline large workforces

• Often operate production sites with thousands of

workers,

• Must organise labor-intensive labour processes

• maintaining a technical division of labour

• Impose discipline with regard to speed and quality

of work

• Deal with worker resistance

• Working conditions

• Generally poor working conditins, but better than

2nd, 3rd, 4rd tier factories

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 14/18

CHARACTERISTICS

• Upgrading/vertical integration

• One-stop shop - They offer a full range of service to its customers,

spanning design, product development, sourcing, manufacturing and

delivery. Vertical reintegration

• No or little access to end-markets• These manufacturers produce garments that are distributed and sold

under the name of the contractor. Little control is exercised over

(retail) market outlets in Western countries.

• Relatively stable relations with global buyers

• These manufacturers have established long-term, relatively stable,

relationships with global buyers, often five years or longer.

• CSR programs

• These manufacturer have (much) experience with CSR programs driven by

global buyers, who have often prioritized implementation at core suppliers

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 15/18

WORKER AGENCY AT

TIER 1 FACTORIES

Three day mass strike for a living wage of 93US$

Followed by mass dismissals

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 16/18

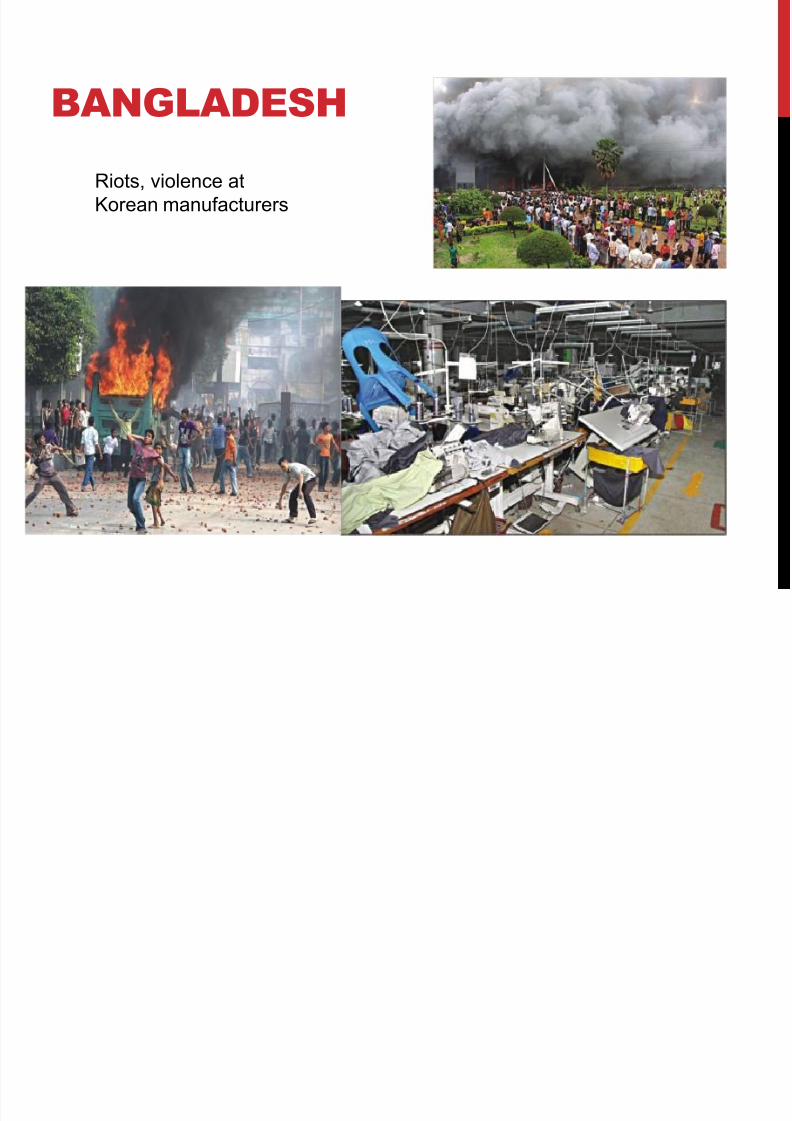

BANGLADESH

Riots, violence at

Korean manufacturers

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 17/18

CHALLENGES FOR LABOUR

RIGHTS ADVOCATES

These companies typically resist unionization drives

Their growing power might question to what degreecommercial purchasers are still able to control theirsuppliers.

Asian garment TNCs are more difficult to target as they arelargely invisible to end-consumers

OPPORTUNITIES FOR

7/29/2019 Merk Presentation

http://slidepdf.com/reader/full/merk-presentation 18/18

OPPORTUNITIES FOR

LABOUR RIGHTS

ADVOCATES

Consolidation, large workforces provides opportunities fororganising

Longer-term relations with brands/ retailers

Higher investment, make relocation-strategies moreexpensive

More profitable companies… make wage agreementspossible