Uber, Inc. Investment Briefing Deck August 2008 – Confidential –

Upload

aaron-bishopCategory

view

152download

0

(Source: Foundation Capital)

*A Trillion Dollar MarketBy the People, For the People

WhereCrowdfundingmeets marketplacelending

2

TABLE OF CONTENTS

p.3 The Opportunity

Elevator Pitch p.4

p.5 The Marketplace

Industry Background p.6

p.7 Numbers At A Glance

The Borrower p.8

p.9 Cost Of Credit

p.11 Marketing Strategy

Executive Team p.12

p.13 Contact Information

Key Financials And Projections p.10

3

THE OPPORTUNITY

ExtraFunds is seeking a minumum of $1 million in investment capital,which will be used for operating capital, including the hiring ofadditional call center employees and expenses related to lead

acquisition and marketing. None of the investor capital will be usedto pay salaries of executive team members.

We are offering investors convertible notes, which carry annuallycompounding interest of 10%. The minimum investment is 12

months.

ExtraFunds is currently owned by Ottawa Capital, LLC, which hasinvested nearly $1M into the company.

$1M 10%compoundingannual interest

4

ELEVATOR PITCH

ExtraFunds is your link to Marketplace Lending!

MARKETPLACE LENDING

Borrower Investors

ExtraFunds is a loan servicing company in the online lending marketplace. We provide expertise in marketing, real-time underwriting, verification and collection

services for marketplace lenders and borrowers alike.

Crowdfunding investors can now enjoy impressive returns on their small or large investments, while borrowers benefit from a direct lending relationship.

5

THE MARKETPLACE

And where we fit!

ExtraFunds competes directly with other short-term consumer lenders andpayday lenders and indirectly with other online lenders in the emerging lending

marketplace.

Consumer

Small DollarLoans

PurchaseFinance

EducationFinancing

Real Estate

MerchantCash Advance

SMB Credit

6

INDUSTRY BACKGROUND

MARKETPLACE LENDING

MARKETPLACE LENDING

Borrower Investors

Source: Lending Club, J.P. Morgan

TRADITIONAL RETAIL LENDING

$$

Package

rB eo wrroBank ss e/S icerv

estv on rI s ancr hT es

Source: Lending Club, J.P. Morgan

MARKETPLACE LENDING IS DISINTERMEDIATINGTHE BORROWING AND INVESTING EXPERIENCE

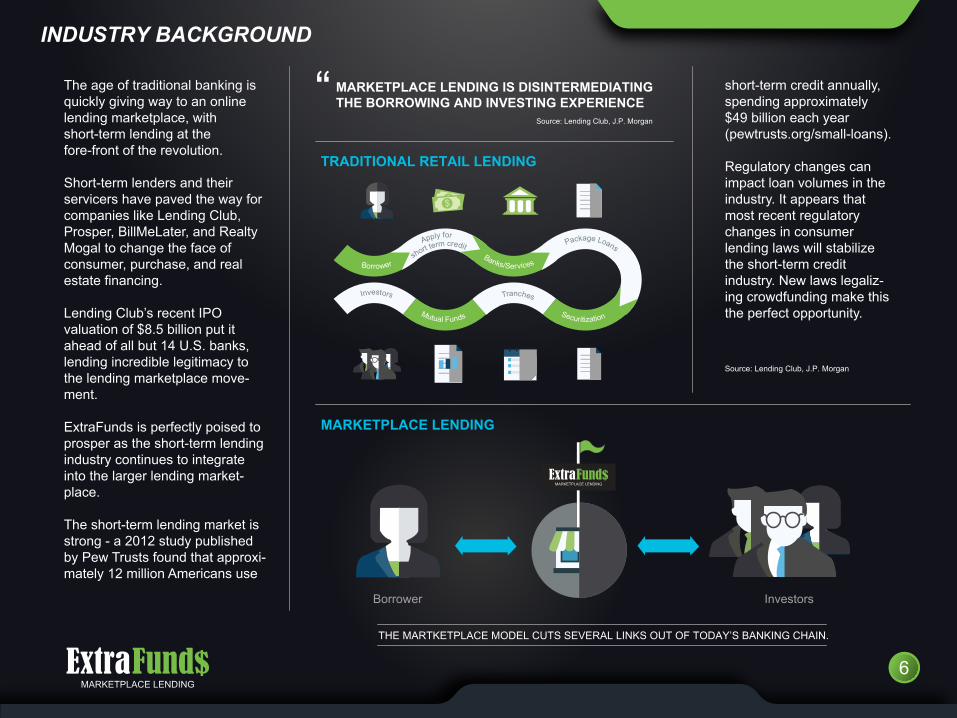

The age of traditional banking is quickly giving way to an online lending marketplace, with short-term lending at the fore-front of the revolution.

Short-term lenders and their servicers have paved the way for companies like Lending Club, Prosper, BillMeLater, and Realty Mogal to change the face of consumer, purchase, and real estate financing.

Lending Club’s recent IPO valuation of $8.5 billion put it ahead of all but 14 U.S. banks, lending incredible legitimacy to the lending marketplace move-ment.

ExtraFunds is perfectly poised to prosper as the short-term lending industry continues to integrate into the larger lending market-place.

The short-term lending market is strong - a 2012 study published by Pew Trusts found that approxi-mately 12 million Americans use

short-term credit annually, spending approximately $49 billion each year (pewtrusts.org/small-loans).

Regulatory changes can impact loan volumes in the industry. It appears that most recent regulatory changes in consumer lending laws will stabilize the short-term credit industry. New laws legaliz-ing crowdfunding make this the perfect opportunity.

THE MARTKETPLACE MODEL CUTS SEVERAL LINKS OUT OF TODAY’S BANKING CHAIN.

7

NUMBERS AT A GLANCE

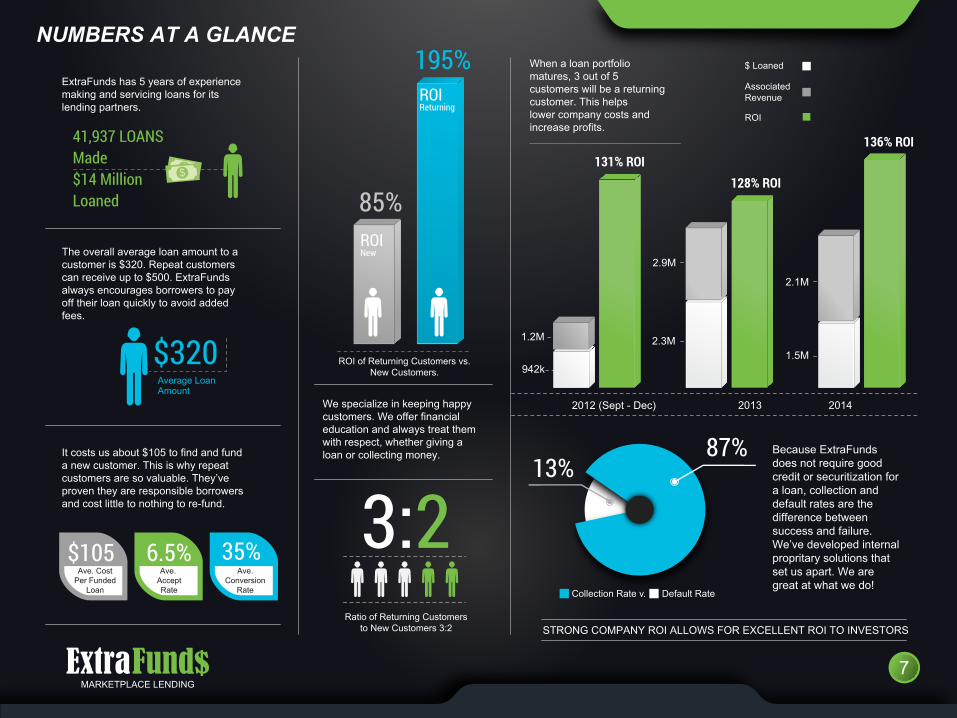

41,937 LOANSMade$14 MillionLoaned

ExtraFunds has 5 years of experiencemaking and servicing loans for its lending partners.

ROI of Returning Customers vs.New Customers.

85%

195%

ROINew

ROIReturning

The overall average loan amount to acustomer is $320. Repeat customerscan receive up to $500. ExtraFundsalways encourages borrowers to payoff their loan quickly to avoid addedfees.

Average LoanAmount

$320

It costs us about $105 to find and funda new customer. This is why repeatcustomers are so valuable. They’veproven they are responsible borrowersand cost little to nothing to re-fund.

$105 6.5% 35%Ave.

AcceptRate

Ave.Conversion

Rate

Ave. CostPer Funded

Loan

3:2Ratio of Returning Customers

to New Customers 3:2

We specialize in keeping happycustomers. We offer financialeducation and always treat themwith respect, whether giving aloan or collecting money. 87%

13%Because ExtraFundsdoes not require goodcredit or securitization fora loan, collection anddefault rates are thedifference betweensuccess and failure.We’ve developed internalpropritary solutions thatset us apart. We aregreat at what we do!

STRONG COMPANY ROI ALLOWS FOR EXCELLENT ROI TO INVESTORS

Collection Rate v. Default Rate

2.1M

1.5M

2.9M

2.3M

2012 (Sept - Dec) 2013 2014

131% ROI

942k

1.2M

128% ROI

136% ROI

$ Loaned

AssociatedRevenue

ROI

When a loan portfoliomatures, 3 out of 5customers will be a returningcustomer. This helpslower company costs andincrease profits.

8

THE BORROWERA STUDY BY DONE BY GWU SCHOOL OF BUSINESS

2% 2% of all U.S. adultsuse small dollarloans

Short-term credit is a multi-billion dollar industry in the U.S.Borrowers all have one thing in common - They havea short-term need for quick credit and often have no othercredit options.

63%have children athome

41% Earn between$25,000 and $50,000 /yr.39% earn over $40,000 /yr.

54% have a high school degree.54% have gone to collegeor have a college degree.

“Most payday loans are used to pay unexpected expenses or expenses that couldnot be postponed…If payday loan customers live from paycheck to paycheck withvery little discretionary income, even small expenses may cause financial problemsand make emergencies a frequent event. In such cases, even frequent use ofpayday loans may be better than the alternatives.”

Gregory ElliehausenDivision of Research and StatisticsBoard of Governors of the Federal Reserve System and Financial Services Research ProgramThe George Washington University School of Business

The study concluded borrowers:

• Have limited liquid assets and savings, most use other forms of credit;

• Have characteristics that may limit their access to credit;

• Use payday loans moderately, as intended for short-term use;

• Are aware of the cost of their most recent payday loan;

• Consider the alternatives, are satisfied with their decision;

• Benefit by having access to payday loans.

9

COST OF CREDIT

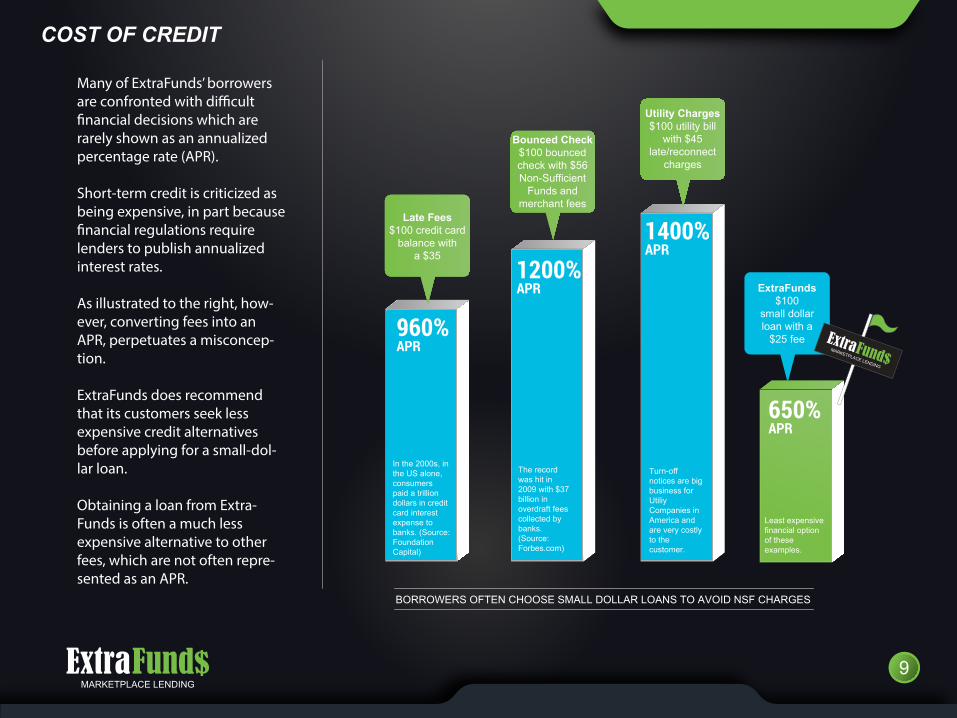

Many of ExtraFunds’ borrowers are confronted with di�cult �nancial decisions which are rarely shown as an annualized percentage rate (APR).

Short-term credit is criticized as being expensive, in part because �nancial regulations require lenders to publish annualized interest rates.

As illustrated to the right, how-ever, converting fees into an APR, perpetuates a misconcep-tion.

ExtraFunds does recommend that its customers seek less expensive credit alternatives before applying for a small-dol-lar loan.

Obtaining a loan from Extra-Funds is often a much less expensive alternative to other fees, which are not often repre-sented as an APR.

1200%APR

1400%APR

650%APR

960%APR

Late Fees$100 credit card

balance witha $35

Bounced Check$100 bouncedcheck with $56Non-Sufficient

Funds andmerchant fees

Utility Charges$100 utility bill

with $45late/reconnect

charges

ExtraFunds$100

small dollarloan with a

$25 fee

The record was hit in 2009 with $37 billion in overdraft fees collected by banks. (Source: Forbes.com)

Turn-off notices are big business for Utiliy Companies in America and are very costly to the customer.

Least expensivefinancial optionof these examples.

In the 2000s, in the US alone, consumers paid a trillion dollars in credit card interestexpense to banks. (Source: Foundation Capital)

BORROWERS OFTEN CHOOSE SMALL DOLLAR LOANS TO AVOID NSF CHARGES

MARKETPLACE LENDING

10

KEY FINANCIALS AND PROJECTIONS

Money Loaned

Associated Revenues

1. Figures for 2014 were calculated using average daily loan volume during final quarter of the year.2. ROI percentage for 2014 was calculated using money loaned and associated revenues statistics over the entire year.

2,3M

3,1M

7,50

0,00

010

,500

,000

11,2

50,0

0016

,312

,500

18,7

50,0

0028

,125

,000

30

135%2

15

100

140%

40

150

145%

60

250

150%

115

Average loansper business day:

ROI percentage:

Call centerrepresentatives:

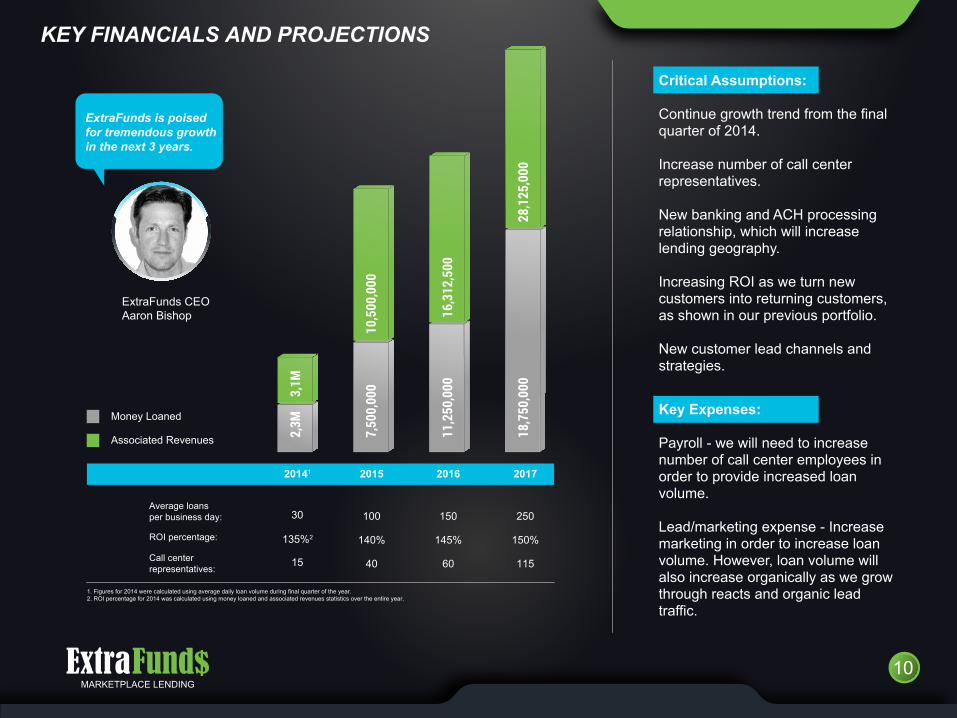

ExtraFunds is poisedfor tremendous growthin the next 3 years.

ExtraFunds CEOAaron Bishop

Critical Assumptions:

Continue growth trend from the finalquarter of 2014.

Increase number of call center representatives.

New banking and ACH processing relationship, which will increase lending geography.

Increasing ROI as we turn new customers into returning customers, as shown in our previous portfolio.

New customer lead channels and strategies.

Key Expenses:

Payroll - we will need to increase number of call center employees in order to provide increased loan volume.

Lead/marketing expense - Increase marketing in order to increase loan volume. However, loan volume will also increase organically as we grow through reacts and organic lead traffic.

20141 2015 2016 2017

11

MARKETING STRATEGY

Money Money Produced by ExtraFunds, 2013

ExtraFunds solicits new and returning customers using traditional, creative and trending marketing techniques.

Lead buying: ExtraFunds’ partners with trusted lead generation compa-nies.

Viral Marketing: ExtraFunds attracts customers with clever viral marketing campaigns such as its Money Money video.

SEO and PPC: ExtraFunds continues to establish organic and paid relevance online.

Social Media: Facebook, Twitter, Instagram, Pinterest, YouTube, Vine.

Email: ExtraFunds uses Opt-in email campaigns to market to its internal customer database.

Mail: ExtraFunds still believes there is value in good old fashioned mail to make both new and repeat customers aware of exciting offers!

12

EXECUTIVE TEAM

Aaron W. BishopChief Executive Officer

Founder of ExtraFunds.Oversees all business andinvestment activities. 20 yearsof experience as a small- andmedium-sized business owner.Expertise includes privateequity, real estate, marketing/branding, and customproduct development. Companiesfounded include Reminderbandd/b/a iFrogz, OttawaCapital, and Bishop Properties.B.A. from Ottawa University.M.A. from Johns HopkinsUniversity.

Brian ZangChief Technology Officer

Has successfully organizedproduction, shipping, sales,marketing, accounting, andtraining efforts in severalstart-up ventures and establishedbusinesses, maximizingefficiency and sustaininggrowth. Oversees the developmentand use of companytechnology, including websites,software, and infrastructure.B.A. in History from TowsonUniversity. M.S. in InstructionalTechnology from Utah StateUniversity.

Bryce SorensenDirector of Lending Operations

Implements lending strategiesdesigned to minimizedefaults and maximize portfolioefficiency. Oversees preventativetroubleshooting for theworkforce organization anddevelopment in the lendingoperations. Consults on thedevelopment and testing ofinnovative methods of leadacquisition and underwriting.Marketing degree from UtahState University.

Michael JewellGeneral Counsel

Licensed attorney withexperience in lending andbanking compliance, as wellas corporate and securitieslaw. Oversees securitiescompliance as well as internalcompliance with lending lawsand regulations. B.A. inEnglish and Political Sciencefrom Utah State University.J.D. from the University ofSan Diego with an emphasisin business and corporate law.

13

CONTACT INFORMATION

ExtraFunds, LLC33 N. Main St., Suite 101

Logan, UT 84321

www.extrafunds.com

435-787-9500