Auditing Stands Clubbing 1-33

31

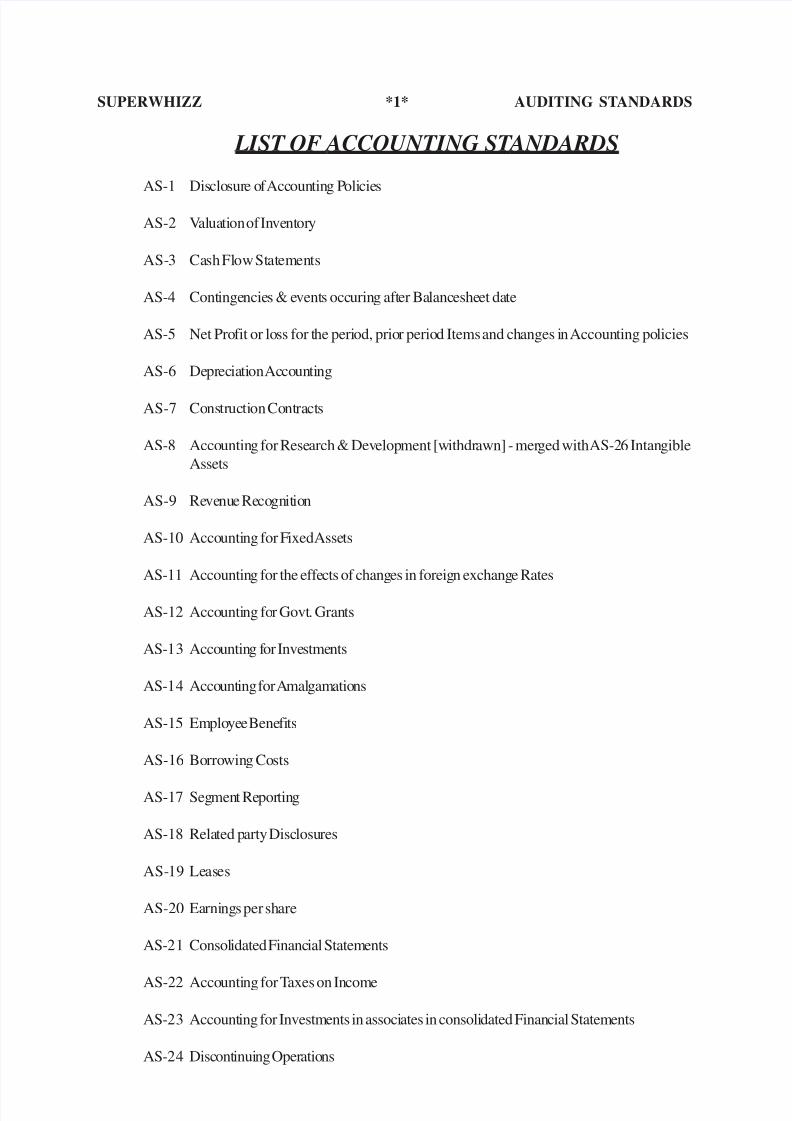

SUPERWHIZZ *1* AUDITING ST ANDARDS LIST OF ACCOUNTING ST ANDARDS AS-1 Dis clo sur e o f Acc oun tin g P oli cie s AS-2 V al ua ti on of In ve nt or y AS- 3 Ca sh Fl ow Statem en ts AS-4 Cont inge ncie s & e vent s occ urin g aft er Ba lanc eshe et da te AS-5 Net Pro fit or lo ss for t he peri od, prio r perio d Items and ch anges i n Accoun ting po licies AS-6 De pr ec ia ti on Ac co un ti ng AS-7 Co ns tr uc ti on Co nt ra cts AS-8 Acco untin g for Rese arch & Dev elop ment [w ithdr awn] - mer ged with AS-2 6 Intan gible Assets AS-9 Re ve nu e Re co gn it ion AS-10 Acco unti ng for F ixed Asse ts AS-11 Accounting for the effe cts of chang es in foreig n exchang e Rates AS-12 Acco unti ng fo r Govt . Gran ts AS-13 Acco untin g f or Inve stments AS-14 Acco unt ing for A mal gam atio ns AS-15 Em plo ye e Bene fi ts AS-16 Borrowin g Co sts AS-17 Seg men t Re por tin g AS-18 Rela ted p arty Disc losu res AS- 19 Leases AS-20 Ea rni ng s per sh are AS-21 Consol idated Financ ial Statem ents AS-22 Acco unti ng for T axes on In com e AS-23 Account ing for Investm ents in associates in consoli dated Finan cial Statem ents AS-24 Disc ont inui ng Oper atio ns

-

Upload

priyadhaarshan-p-nagesh -

Category

Documents

-

view

220 -

download

0

Transcript of Auditing Stands Clubbing 1-33

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 1/30

SUPERWHIZZ *1* AUDITING STANDARDS

LIST OF ACCOUNTING STANDARDS

AS-1 Disclosure of Accounting Policies

AS-2 Valuation of Inventory

AS-3 Cash Flow Statements

AS-4 Contingencies & events occuring after Balancesheet date

AS-5 Net Profit or loss for the period, prior period Items and changes in Accounting policies

AS-6 Depreciation Accounting

AS-7 Construction Contracts

AS-8 Accounting for Research & Development [withdrawn] - merged with AS-26 Intangible

Assets

AS-9 Revenue Recognition

AS-10 Accounting for Fixed Assets

AS-11 Accounting for the effects of changes in foreign exchange Rates

AS-12 Accounting for Govt. Grants

AS-13 Accounting for Investments

AS-14 Accounting for Amalgamations

AS-15 Employee Benefits

AS-16 Borrowing Costs

AS-17 Segment Reporting

AS-18 Related party Disclosures

AS-19 Leases

AS-20 Earnings per share

AS-21 Consolidated Financial Statements

AS-22 Accounting for Taxes on Income

AS-23 Accounting for Investments in associates in consolidated Financial Statements

AS-24 Discontinuing Operations

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 2/30

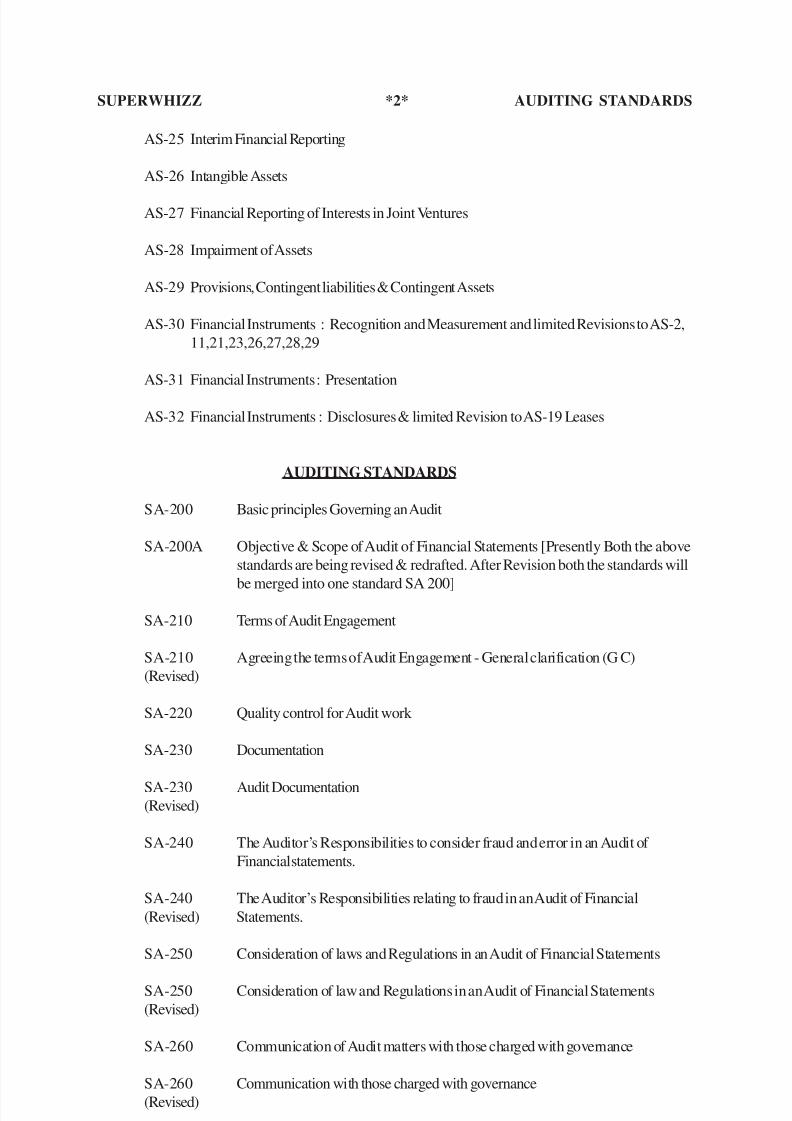

SUPERWHIZZ *2* AUDITING STANDARDS

AS-25 Interim Financial Reporting

AS-26 Intangible Assets

AS-27 Financial Reporting of Interests in Joint Ventures

AS-28 Impairment of Assets

AS-29 Provisions, Contingent liabilities & Contingent Assets

AS-30 Financial Instruments : Recognition and Measurement and limited Revisions to AS-2,

11,21,23,26,27,28,29

AS-31 Financial Instruments : Presentation

AS-32 Financial Instruments : Disclosures & limited Revision to AS-19 Leases

AUDITING STANDARDS

SA-200 Basic principles Governing an Audit

SA-200A Objective & Scope of Audit of Financial Statements [Presently Both the above

standards are being revised & redrafted. After Revision both the standards will

be merged into one standard SA 200]

SA-210 Terms of Audit Engagement

SA-210 Agreeing the terms of Audit Engagement - General clarification (G C)

(Revised)

SA-220 Quality control for Audit work

SA-230 Documentation

SA-230 Audit Documentation(Revised)

SA-240 The Auditor’s Responsibilities to consider fraud and error in an Audit of

Financial statements.

SA-240 The Auditor’s Responsibilities relating to fraud in an Audit of Financial

(Revised) Statements.

SA-250 Consideration of laws and Regulations in an Audit of Financial Statements

SA-250 Consideration of law and Regulations in an Audit of Financial Statements

(Revised)

SA-260 Communication of Audit matters with those charged with governance

SA-260 Communication with those charged with governance

(Revised)

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 3/30

SUPERWHIZZ *3* AUDITING STANDARDS

SA-265 Communicating Deficiencies in Internal Control to those charged with

governance & management

SA-299 Responsibility of Joint Auditors

SA-300 Audit Planning

SA-300 Planning & Audit of Financial Statements

(Revised)

SA-315 Identifying & Assessing the risk of material misstatements through understanding

the entity and it’s environment

SA-320 Audit Materiality

SA-320 Materiality in planning & performing an Audit

(Revised)

SA-330 The Auditors Responses to assessed Risks

SA-402 Audit Considerations relating to entities using Service Organization

SA-402 Audit Considerations relating to an entity using a Service Organization

(Revised)

SA-450 Evaluation of Mis-statements identified during the Audit.

SA-500 Audit Evidence

SA-500 Audit Evidence

(Revised)

SA-501 Audit Evidence - Additional Considerations for specific items

SA-505 External Confirmations

SA-510 Initial engagements - Opening balances

SA-510 Initial Audit engagements - Opening balances

(Revised)

SA-520 Analytical Procedure

SA-530 Audit Sampling

SA-530 Audit Sampling(Revised)

SA-540 Audit of Accounting estimates

SA-540 Auditing accounting estimates, including fair value accounting estimates &

(Revised) related disclosures

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 4/30

SUPERWHIZZ *4* AUDITING STANDARDS

SA-550 Related parties

SA-550 Related parties

(Revised)

SA-560 Subsequent events

SA-560 Subsequent events

(Revised)

SA-570 Going Concern

SA-570 Going Concern

(Revised)

SA-580 Representations by Management

SA-580 Written Representations

(Revised)

SA-600 Using the work of another Auditor

SA-610 Relying upon the work of an Internal Auditor

SA-610 Using the work of Internal Auditors(Revised)

SA-620 Using the work of an expert - General clarification

SA-700 The Auditor’s Report on Financial Statements

SA-710 Comparatives

SA-720 The Auditor’s responsibility in relation to other Information in documents

containing Audited Financial Statement

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 5/30

SUPERWHIZZ *5* AUDITING STANDARDS

SA-200 - Basic Principles Governing An Audit

w.e.f. 1-4-1985

Introduction:-

(1) This standard describes the Basic principles which govern the Auditor’s professional responsibi-

lities & which should be complied with whenever an Independent Statutory Audit is carried out.

(2) Other standards on Auditing issued by the ICAI will elaborate these Basic principles to give

guidence on Auditing procedures & reporting practices.

(3) Complaince with the Basic principles requires the application of Auditing procedures & report

ing practices appropriate to the particular circumstances.

Basic principles :-

(1) Integrity, Objectivity & Independence

(2) Confidentiality

(3) Skills & Competence

(4) Work performed by others

(5) Documentation

(6) Planning

(7) Audit evidence

(8) Accounting system & Internal Control

(9) Audit Conclusions & Reporting

(1) Integrity, Objectivity & Independence :-

(a) The Auditor should be straight forward, honest & sincere in his approach to his professional

work.

(b) He must be fair and must not allow prejudice or bais to override his objectivity. He should

maintain an impartiable attitude.

(c) The Auditor must not only be actually Independent but also appear to be independent to allreasonable minded persons.

(2) Confidentiality :-

(a) The Auditor should respect the confidentiality of information acquired in the course of his work.

(b) He should not disclose any information to a third party.

(c) He must disclose only in the following three circumstances.

(i) When he has obtained the specific authority of the client in writing

(ii) When there is a professional duty to disclose

eg:- To any committee authorised by ICAI

(iii) When there is a legal obligation to disclose

eg:- To any court/Tribunal but not to any govt. officer or Income Tax officer.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 6/30

SUPERWHIZZ *6* AUDITING STANDARDS

(3) Skills & Competence :-

(a) The Audit should be performed & the report should be prepared with due professional care by

persons who have adequate training, experience & competence in Auditing.

(b) The Auditor acquires specialized skills & competence through a combination of General

education, Study, passing the qualifying examination & practical experience under proper

supervision.

(c) The Auditor requires a continuing awareness of all developments on Accounting & Auditing

matters, pronouncements of the ICAI, relevant regulations & statutory requirements.

(4) Work performed by others :-

(a) When the auditor deligate work to assistants or uses the work performed by other Auditors &

experts, he will continue to be responsible for forming and expressing his opinion on the financial

information.

(b) The Auditor should obtain reasonable Assurance that the work performed by other Auditor or

experts is adequate for his purpose.

(c) Where the Auditor has used the report of the Branch Auditors, his Audit report should expressly

state the fact of such Reliance

(d) The Auditor should carefully direct, superwise & Review the work delegated to his assistants.

(5) Documentation:-

The Audit should document matters which are important in providing evidence that the Audit

was carried out in accordance with the Basic principles.

(6) Planning :-

(a) The Auditor should plan his work which will enable him to perform the Audit efficiently,

effectively and in a timely manner.

(b) Plans should be based on knowledge of clients Business, Internal Control, Procedures,

Accounting system, Accounting policies, the nature, timing & extent of Audit procedure to be

performed, co-ordinating the work to be performed etc.,

(c) Plans should be further developed & revised as necessary during the course of Audit.

(7) Audit Evidence:-

(a) The Auditor should obtain sufficient appropriate Audit evidence by performing complaince &

substantive procedure. This will enable him to arrive at reasonable conclusions on which he canbase his opinion on financial information.

(b) Complaince procedures are tests which are designed to obtain reasonable Assurance about the

Internal Control System. The Auditor examines the Internal Control System in terms of

existence, effectiveness & Continuity.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 7/30

SUPERWHIZZ *7* AUDITING STANDARDS

(c) Substantive procedures are tests which are designed to obtain reasonable Assurance about the

data produced by the Accounting System. The Auditor examines the data of produced by

Accounting System in terms of Completeness, Accuracy & Validity.

(8) Accounting System & Internal Control:-

(a) Management is responsible for maintaining an adequate accounting system by incorporating

various Internal Controls which are appropriate to size & nature of Business.

(b) The Auditor should reasonably assure himself that the Accounting System is adequate & all the

Accounting information has been recorded

(c) The Auditor should gain an understanding of the Accounting System & related Internal Controls

for determining the nature, timing & extent of Audit procedures.

(d) Where the Auditor concludes that he can rely on Internal Controls, then his substantive

procedures would be less extentive than would otherwise be required & they may also differ in

terms of their nature & timing.

(9) Audit Conclusions & Reporting :-

(a) The Auditor should review & assess the conlcusions drawn from the Audit evidence

obtained. This will be the basis for his expression of opinion on the financial information.

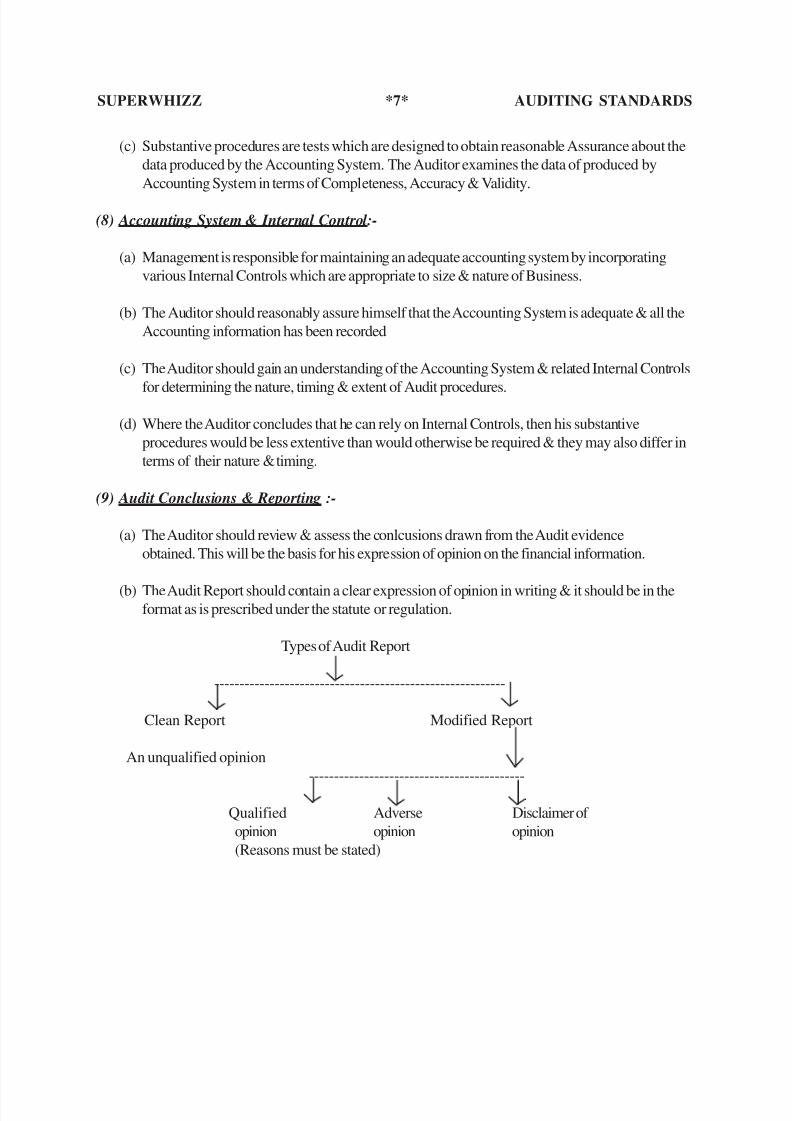

(b) The Audit Report should contain a clear expression of opinion in writing & it should be in theformat as is prescribed under the statute or regulation.

Types of Audit Report

----------------------------------------------------------

Clean Report Modified Report

An unqualified opinion

-------------------------------------------

Qualified Adverse Disclaimer of

opinion opinion opinion

(Reasons must be stated)

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 8/30

SUPERWHIZZ *8* AUDITING STANDARDS

SA 200A - Objectives & Scope of the Audit of Financial statements

w.e.f - 1-4-95

Introduction:-

(1) This standard describes the overall objective & scope of the Audit of General purpose

Financial statements of an Enterprise by an Independent Auditor.

(2) The term General purpose Financial Statement include B/S, Statement of profit & loss, other

statements & explanatory notes which form part thereof, and which are issued for the use of

share holders, members, creditors, employees & public at large (General public)

Objective of an Audit:-

(a) The Objective of an Audit of Financial Statements prepared in accordance with recognized

Accounting policies & statutory requirements, is to enable the Auditor to express his opinion on

the Financial Statements

(b) The Auditor’s opinion helps in the determination of the true & fair view of the financial position

& operating results of an enterprise.

(c) The Auditor’s opinion does not contain any guarantee or Assurance about the future financial

viability of the enterprise or the efficiency or effective with which the management may have

conducted the affairs of the enterprise.

Responsibility for the Financial Statements :-

(1) The responsibility for the preparation and presentation of Financial Statements is that of the

management of the enterprise. Therefore managements responsibilities include maintaince of

Accounting records, Internal controls, Selection & application of Accounting policies &

safeguarding the assets of the enterprise.

(2) The Auditor is responsible for forming and expressing his opinion on the financial statements.

(3) The Audit of Financial Statements does not relieve the management of it’s responsibilities.

Scope of an Audit :-

(1) The scope of an Audit of Financial Statements will be determined by the Auditor after taking

into account the following.

(a) The terms of the engagement

(b) The requirements of relevant legislation &

(c) The official pronouncements of the ICAI.

(2) The terms of engagement cannot restrict the scope of an Audit when it is prescribed by the

legislation or ICAI pronouncements

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 9/30

SUPERWHIZZ *9* AUDITING STANDARDS

(3) The Audit should be organized to cover adequately all aspects of the enterprise which are

relevant to the financial statements being Audited

(4) The Auditor’s work involves exercise of Judgement in deciding the Audit procedures & in

assessing the estimates made in the preparation of Financial Statements. Much of the Audit

evidence available to the Auditor can only enable him to arrive at reasonable conclusions.

Therefore absolute certainity in Auditing is rarely attainable.

(5) Because of test nature of Audit, Inherent limitations of Audit & Inherent limitations of Internal

Control System, there is an unavoidable risk that some material misstatements in the financial

statement may remain undiscovered.

(6) Discovery of material mis-statements is not the main objective of Audit. Therefore the Auditor

cannot be relaid upon to discover all errors and frauds.

(7) Where the auditor has any indication that some error or fraud may have occured, then he must

extend his Audit procedures until his suspicious are either confirmed or dispelled.

(8) The Auditor is not expected to perform duties which fall outside the scope of his professional

competence. For eg:- He is not a technical expert for determining the physical condition of

certain assets

(9) If there are any constraints which are placed on the scope of Audit which impair the Auditor’s

ability, then the Auditor must issue his report containing a qualified opinion or disclaimer of

opinion as may be appropriate.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 10/30

SUPERWHIZZ *10* AUDITING STANDARDS

SA 240- Auditors responsibilities relating to Fraud in an Audit of

Financial Statement.

w.e.f:- 1-4-2009.

Introduction:-

(1) This standard deals with the auditor’s responsibility relating to Fraud in an Audit of Financial

Statement.

(2) This standard expands how SA-315 and SA-330 are to be applied in relation to risks of

material mis-statement due to fraud.

Characteristics of Fraud:-

(1) Misstatements in the Financial Statement can arise either from fraud or from error. Fraud is

intentional but error is unintentional.

(a) Fraud - This is an intentional act by one or more individuals among management those

charged with governance, employees or third parties, involving the use of deception to obtain

an unjust or illegal advantage

(b)Fraud Risk Factor - These are events or conditions that indicate an incentive or pressure to

commit fraud or provide an opportunity to commit fraud.

(2) There are two types of Intentional misstatements that are relevant to auditor & they are fradulantfinancial reporting & mis appropriation of Assets.

Responsibility for the prevention & detection of Fraud :-

(1) The primary responsibility for the prevention & detection of fraud is that of both those charged

with governance of the entity & the management

(2) This involves a commitment to creating a culture of honesty and ethical behaviour which can be

reinforced by an active oversight by those charged with governance.

Responsibilities of the Auditor:-

(1) According to SA-200A, on account of inherent limitations of Audit, there is an unavoidable risk

that some material misstatements of the financial statements will not be detected, eventhough the

Audit is properly planned & performed in accordance with the essays.

(2) The risk of not detecting a material mis statements resulting from fraud is higher than the risk of

not detecting an error. This is because fraud involves sophisticated and carefully organized

schemes, forgery, collusion etc..,

(3) The auditor’s ability to detect a fraud depends on many factors such as skillfulness of theperpetrator, the frequency of manipulation, the degree of collusion, the Amount involved and the

seniority of the individuals involved.

(4) The risk of the Auditor not detecting a material mis-statement resulting from Management fraud

is greater than employee fraud because management is in a position to manipulate accounting

records, over ride control procedure.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 11/30

SUPERWHIZZ *11* AUDITING STANDARDS

(5) The Auditor is responsible for maintaing an attitude of professional skepticism throughout the

Audit.

Professional skepticism is an attitude that includes a questioning mind and a critical Assessment of

Audit evidence.

(6) The Auditor may accept recods & documents as genuine, except in those circumstances where he

has reasons to believe the contrary.

(7) During the course of Audit , if the Auditor has a cause to believe that a document may not be

authentic, than he shall investigate further.

(8) Wher the Auditor encounters exceptional circumstances where he either identifies a fraud or

suspected froud ,then

a) He should determine his professional & legal responsibilities and consider whether it is

appropriate to withdraw from the engagement &

b) Discuss with the appropriate level of of management & those charged with governance, the

resons for his withdrawn, and determine whether these is any professional or legal requirement

to report to regulatory authorities.

(9) The Audiror shall document communications about fraud made to management , these charged with

governance , regulators and others.

(10) In exceptional circumstances whether the Auditor has doubts about the Integrity or honesty of management or those charged with governance, he should consider seeking legal advice to

determine the approprite course of Action.

(11) The Auditor’s Professional duty to maintain the confidentiality of client information may prevent

him from reporting the fraud to any party outside the client entity.

(12) In the case of Audit of Banks, the Auditor has a statutory duty to report the occurence of fraud

to the RBI.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 12/30

SUPERWHIZZ *12* AUDITING STANDARDS

Audit Evidence

SA – 500 W.e.f 1-4-2009

1) The objective of the Auditor is to design & perform Audit procedures which will enable him

to obtain sufficient appropriate Audit evidence . This will allow him to arrived at reasonable

conclusion on which he can base his opinion.

2) Appropriateness of Audit Evidence:-

This refers to the quality of Audit evidence, i.e., the relevance and reliability in providing

support for the conclusion.

3) Audit Evidence :-

This refers to the information used by the Auditor in arriving at conclusions on which his

opinion is based. It includes both information contained in the Accounting records /

Financial statement and other information.

4) Sufficiency of Audit Evidence :-

This refers to the measure of the quantity of Audit evidence. The quantity of the Audit

evidence needed. It will depends on two factors namely the risks of material misstatement

& the quality of evidence.

5) The Auditor shall design & perform Audit procedures that are appropriate in the

circumstances for the purpose of obtaining sufficient appropriate Audit evidence.

6) When designing and performing Audit procedures, the Auditor should consider the

relevance & reliability of the information to be used as audit evidence.

7) When information to be used as Audit evidence has been prepared using the work of a

management’s expert, the Auditor shall consider the significance of that experts work.

The term Management expert refers to an individual or organisation possessing expertise in

a field other than Accounting or Auditing & whose work is used by the entity in thepreparation of financial statements.

8) When using information produced by the entity, the Auditor shall evaluate whether the

information is sufficiently reliable, accurate , complete, precise, detailed etc…,

9) If the Audit evidence obtained from one source is inconsistent with the evidence obtained

from another source or the Auditor has doubt regarding the reliability of information to be

used as Audit evidence, then he shall determine whether any modification or additions to

Audit procedures are necessary to resolve the matter.

10) The Auditor should obtain sufficient appropriate Audit evidence to reduce Audit risk to an

acceptably lower level.

Audit risk is that risk which refers to the Auditor expressing an inappropriate opinion when

the financial statements are materially misstated

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 13/30

SUPERWHIZZ *13* AUDITING STANDARDS

11) The sufficiency and Appropriateness of Audit evidence are interrelated. Sufficiency refers to

the Quantity of Audit evidence & Appropriateness refers to quality of Audit evidence.

12) Corroborative Evidence: This refers to the Auditor obtaining evidence from differentsources regarding the same assertion (Basis of evidence). The Auditor will have more

assurance only when the corroborative evidence obtained is consistent in nature.

13) Audit procedures for obtaining Audit Evidence ( 7 methods) :-

a) Inspection :- This refers to the Auditor examining the records or documents ,

whether Internal or External in paper form, electronic form, (or) other media, (or)

physical examination of an Asset.

Eg:- Inspection of Financial Instruments like stock or bond.

Inspection of documents may not necessary provide Audit evidence aboutownership or value.

Inspection of tangible Assets may provide reliable

Audit evidence with respect to their existence but not about the entities rights &

obligations (or) valuation of Assets.

b) Observation :-

This refers to the Auditor looking at a process or procedure being performed by

others

Eg:- Auditor observing the Annual physical stock taking undertaken by the clientspersonnel (or) implementation of Internal control Activities.

c) External Confirmation :-

This refers to the Auditor obtaining Audit evidence in writing from any third

party in paper form or Electronic form or other medium

Eg :- Direct confirmation of balances from debtors, creditor, bankers etc..,

d) Recalculation:-

This refers to the Auditor checking the mathematical Accuracy of documents orrecords. This may be performed manually or electronically .

e) Reperformance : -

This involves the Auditor’s independent execution of procedures or controls that were

originally performed as part of the entities Internal control.

f) Analytical procedures : -

This refers to the evaluation of Financial information made by a study of possible

relationships among both Financial and non- financial data. This involves the

investigation of

a) Fluctuations

b) Inconsistent relationships & ( G.P. , N.L )

c) Deviations from predicate Amounts (Variance )

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 14/30

SUPERWHIZZ *14* AUDITING STANDARDS

g) Inquiry : -

This refers to the Auditor seeking information from knowledgable persons, both financial and

non financial , either within the entity or outside the intity.Responses to inquires may provide

the Auditor with information which he did not previously possess or with corroborative Auditevidence. Inquires may be made either orally or in writing.

14. The quality of Audit evidence will be effected by its relavance and Reliability. Relevance relates

to the logical connection and reliability will be influenced by its source, nature and circumstances

under which it is obtained .

Possible -> reasonable / Inquiry X response

SA - 320 - Materiality in planning and performing an Audit.

w.e.f. : - 1-4-2010.

1) Mis- statements , including omissions, are considered to be material if they ,individually

or in the aggregate, could reasonably be expected to influence the economic decisions

taken by the users of Financial statements.

2) Judgements about Materiality will depend on the size of the item or its nature or a

combination of both.

3) The Auditor’s determination of Materiality is a matter of professional Judgement, and

will be affected by his perception of the needs of the users of Financial Statements.

4) The concept of Materiality will be applied by the Auditor in the following aspects.

a)Both in planning & performing the Audit.

b)Evaluating the affect of identified misstatements on the Audit.c)Evaluating the effect of uncorrected mis-statements on financial statements &

d)Forming the opinion in the Audit makes.

5) In planning the Audit, the Auditor makes Judgements about the size of mis-statements

that will be considered material.

6) The objective of the Auditor is to apply the concept of Materiality appropriately in

planning & performing the Audit.

7) Performance Materiality : -

Performance Materiality means the Amount (s) set by the auditor at less than

materiality for the financial statements as a whole to reduce to an appropriately

low level the probability that the aggregate of uncorrected & undetected mis -statements

exceeds Materiality for the Financial Statements as a whole.

8) When establishing the overall Audit strategy, the Auditor shall determine materiality for

the Financial statements as a whole . In specific circumstances, the Auditor shall also

determine the materiality levels to be applied to particular classes of transaction, account

balances or disclosure.

9) During the course of Audit, the Auditor may have to revise Materiality for the financial

statements as a whole & also the performance materiality.

10) The Auditor obtains reasonable assurance and depends on sufficient appropriate Audit

evidence to reduce Audit risk to an acceptably lower level.

Audit risk is the risk where the Auditor expresses an inappropriate Audit opinion when

the Financial statements are materially mis - stated.11) Determining Materiality involves the exercise of professional judgement. A choosen Bench

Mark will be the starting point in determining materiality for the Financial statements as

a whole. Examples of Bench Marks are profit after Tax (PAT).Total revenue, Gross profit,

Total expenses , Total equity , Net Asset Value etc..,

12) In the case of certain entities like Central govt, State govt, and govt. related entities,

materiality for the Financial statements may be influenced by legislative and regulatory

requirements, Public utility programs such as PMGSY, AIBP (Accelerated Irrigated

Development programme)

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 15/30

SUPERWHIZZ *15* AUDITING STANDARDS

SA 210 – Agreeing the Terms of Audit Engagement

W e f. – 1-4-2010.

(1) This deals with the Auditor’s responsibilities in agreeing the terms of the Audit Engagement with

the management & where appropriate with those charged with governance.

(2) The objective of the Auditor is to accept or continue an Audit Engagement only when the basis

upon which it has to be performed has been agreed as given below.

(a) Establishing the pre-conditions for an Audit and

(b) Confirming a common understanding between the Auditor and the management / those

charged with governance.

(3) Preconditions for an Audit :-

The use by the management of an acceptable Financial reporting framework in thepreparation of Financial Statement & the agreement of management/those charged with

governance to the premise on which an Audit is conducted.

(4) Requirements/Pre-conditions for an Audit :-

In order to establish whether the pre-conditions for an Audit are present, the Auditor

shall ensure the following aspects.

(a) Determine whether the Financial Reporting framework to be applied in the preparation of the

Financial Statement is acceptable.

(b) Obtain the agreement of management that it acknowledges and understands it’s responsibility

for the preparation of the Financial Statements and their fair presentation , implementing the

Internal Control free from fraud or error, provide the Auditor with access to all records and

documents, additional information as may be requested by the Auditor & unrestricted access to

persons within the entity to enable the Auditor to obtain Audit evidence.

(5) Limitation on scope prior to Audit Engagement Acceptance :-

If the management/those charged with governance impose any limitation on the scope of

Auditor’s work, and the Auditor believes that he can only express a disclaimer of opinion, then

the Auditor shall not accept such a limited engagement unless he is required to do so under any

law or regulation.

(6) If the pre-conditions for an Audit are not present, then the Auditor shall not accept the proposedAudit Engagement.

(7) The Auditor shall agree the terms of the Audit Engagement with the management or those

charged with governance, as may be appropriate.

(8) The agreed terms of the Audit Engagement shall be recorded in an Audit Engagement letter or

other suitable form of written agreement & shall include the following aspects.

(a) The objective & scope of Audit of Financial Statements

(b) Responsibilities of the Auditor

(c) Responsibilities of Management

(d) Identification of the applicable Financial reporting framework for the preparation of Financial Statements &

(e) The form and content of reports to be issued by the Auditor and the circumstances in

which the form & content may differ.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 16/30

SUPERWHIZZ *16* AUDITING STANDARDS

(9) If any law or Regulation prescribes insufficient detail the terms of Audit Engagement, then the

Auditor need not record them in a written agreement, except the fact that the law or regulation

applies & the management acknowledges and understands it’s responsibilities.

(10) In the case of recurring Audits, the Auditor should consider whether the terms of Audit

Engagement are to be revised or to remind the client about the existing terms of Audit

Engagement.

(11) The Auditor shall not agree to a change in terms of Audit Engagement when there is no

reasonable Justification for doing so.

(12) Prior to completing the Audit Engagement, if the Auditor is requested to change the Audit

Engagement to an Engagement that conveys a lower level of Assurance, then the Auditor should

consider whether there is any reasonable Justification for doing so.

(13) If the terms of the Audit Engagement are changed, the Auditor and the management shall agree

& record the new terms of the Engagement either in the form of Audit Engagement letter or any

other suitable form of Written Engagement.

(14) If the Auditor is unable to agree to a change of the terms of Audit Engagement and the

management does not permit him to continue the Original Engagement, then the auditor shall

withdraw from the engagement. He should also determine whether there is any obligation to

report to management, those charged with governance, owners or regulators.

Note :-There may be certain engagements where the objective & scope of the engagement and theAuditor’s obligations are not laid down in the statute or regulation. In that situation, the Auditors

should prepare an Audit Engagement letter & request the client to acknowledge it. This will

establish the understanding between the Auditor and the client.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 17/30

SUPERWHIZZ *17* AUDITING STANDARDS

SA – 300 Planning & Performing an Audit of Financial Statements w.e.f -1-4-08

1. This SA deals with the Auditor’s responsibility to plan an Audit of Financial Statement.

This SA is framed in the context of Recurring Audits.2. The objective of the Auditor is to plan the Audit so that it will be performed in an effective

manner.

3. The Engagement partner and other key members of the Enagagement team shall be involved in

planning the Audit, including planning & participating in the discussion among engagement team

members.

4. The Auditor shall establish an overall Audit strategy that takes into Account, the scope, timing &

direction of the Audit, and that guides the development of the Audit plan.

5. In Establishing the overall Audit strategy the Auditor shall ensure the following aspects.

(a) Identify the characteristics of the scope of the engagement.

(b) Ascertain the reporting objectives of the Engagement.(c) Consider the factors which are significant in directing the engagement teams efforts.

Eg. Working

(d) Consider the results of preliminary engagement activities.

(e) Ascertain the nature,timing and extent of resources necessary to perform the

engagement.

6. Eg:- No.of Audit staff members, capability of computer systems etc.,

7. The Auditor shall develop an Audit plan which includes the nature, timing and extent of Audit

procedure.

8. The Auditor shall update & change the overall Audit strategy & the Audit plan as necessary

during the course of Audit.

9. The Auditor shall plan the nature, timing & extent of direction & supervision of engagement teammembers and the review of their work.

10. The Auditor shall document –

(a) The overall Audit strategy

(b) The Audit plan &

(c) Any significant changes made during the Audit engagement to the overall Audit

strategy or the Audit plan & the reasons for such changes.

11. The Auditor shall undertake the following activities prior to starting an initial Audit.

(a) Perform procedures regarding the acceptance of the client relationship and

(b) Communicate with the predecessor Auditor, where there is a change of Auditors

in compliance with the relevant ethical requirement.

12. Benefits of Audit Planning :-

(1) Planning an Audit involves establishing the overall Audit strategy for the Engagement &

developing an Audit plan. Planning benefits in several ways including the following.

(a) Helping the Auditor to devote appropriate attention to important areas of Audit.

(b) Helping the Auditor to identify & resolve potential problems on a timely basis.

(c) Helping the Auditor to properly organize & perform the Audit Engagement in an

efficient & effective manner.

(d) Assisting the Auditor in the selection of engagement team members on the basis

of capabilities, competence to respond to anticipated risks & the assignment of

proper work team to them.

(e) Facilitating the direction & supervision of Engagement team members & thereview of their work.

(f) Assisting in the co-ordination of work done by Auditors of components &

experts.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 18/30

SUPERWHIZZ *18* AUDITING STANDARDS

SA – 520 Analytical Procedure w.e.f – 1-4-97

1) The Auditor should apply Analytical Procedures at the planning and overall Review

stages of Audit.Analytical Procedure may also be applied at other stages of Audit.2) Analytical Procedures means the analysis of significant Ratios and trends, including the

investigation of fluctuations, inconsistent relationships and deviations from predicted

Amounts.

3) Examples of Analytical Procedures.

(a) Comparision of current years information with prior period information.

(b) Comparision of Budgeted figures with Actual figures.

(c) Comparision of Entity’s information with industry information.

(d) Comparision between Financial information with non-financial information.

Eg:- Payroll costs with no.of employees.

4) The extent of Reliance that the Auditor places on the results of Analytical Procedures

depends on the following factors.

(a) Materiality of the items involved.

(b) Other Audit Procedures directed towards the same Audit objectives.

(c) The Accuracy with which the expected result of the Analytical Procedures can

be predicted &

(d) Assessments of Inherent & Control risks.

5) When Analytical procedures identify significant fluctuations or inconsistent relationships

or deviations from predicted Amounts, then the Auditor should investigate & obtain

adequate explanations and appropriate correlative evidence.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 19/30

SUPERWHIZZ *19* AUDITING STANDARDS

S.A – 530 - Audit Sampling

w.e.f – 1 – 4 – 2009

1) This SA applies when the Auditor has decided to use Audit Sampling in performing AuditProcedures. It deals with the Auditor’s use of Statistical and Non- statistical Sampling when

(a) Designing and selecting the Audit Sample

(b) Performing tests of controls & tests of details and

(c) Evaluating the results from the sample.

2) The objective of the Auditor when using Audit sampling is to provide a reasonable basis for the

Auditor to arrive at conclusions about the population from which the sample is selected.

3) Audit Sampling:-

The application of Audit procedures to less than 100% of items with in a population.

4) Sampling Risk:-

This is the risk that the Auditor’s conclusion based on a sample may be different if the entire

population were subjected to the same Audit procedure.

5) Non – Sampling Risk:-

This is the risk that the Auditor reaches an erroneous conclusion for any reason not related to

Sampling Risk.

6) Anomaly :- (Idle)

This is a mis-statement or deviation that is demonstrably not representative of mis-statement

or deviation in a population.

7) Stratification: -

This is the process of dividing a population into sub population of each which is a

group of sampling units having similar characteristics.

8) The Auditor shall evaluate

a) The results of the sample &

b) Whether the use of Audit sampling has provided a reasonable basis for conclusions

about the population that has been tested.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 20/30

SUPERWHIZZ *20* AUDITING STANDARDS

SA-230 –Audit DocumentationW.e.f. 1-4-2009

1) Audit Evidence provides

a) Evidence of the Auditors basis for a conclusion about the achievement of the overall objective

of the Auditor &

b) Evidence that the Audit was planned & performed in accordance with SAs and applicable legal

and regulatory requirements.

2) Audit documentation serves a no of purposes including the following.

a) Assisting the engagement team to plan & perform the Audit.

b) Assisting members of the engagement team to direct, supervise the Audit work performed by

other.c) Enabling the engagement team to be Accountable for its work.

d) Retaining a record of matters of continuing significance to future Audits.

e) Enabling the conduct of quality control reviews & inspections.

f) Enabling the conduct of external inspections in accordance with applicable, legal, regulatory

or other requirements.

3) Audit Documentation :

These are also known as working papers or work papers and they refer to the record of Audit

procedures performed, relevant Audit Evidence obtained and conclusions reached by the

Auditor.

4) Audit File:

One or more folders or other storage media, in physical or electronic form, containing the

records that comprise the Audit Documentation for a specific engagement.

5) Experienced Auditor:

An Individual, whether Internal or External to firm, who has practical Audit Experience & a

reasonable understanding of

a) Audit processes -(11 Aspects)

b) SAs and Applicable legal & regulatory requirements.

c) The Business environment in which the entity operates &

d) Auditing & financial reporting issues relevant to the Entity’s industry.

6) The Auditor shall prepare Audit Documentation on a timely basis.

7) Form Content & Extent of Audit Documentation:

The Auditor shall prepare Audit Documentation that is sufficient to enable an experienced

Auditor having no previous connection with the Audit, to understand.

a) The nature timing & extent of the Audit procedures performed to comply with the SAs and

applicable legal and regulatory requirements.

b) The results of the Audit procedures performed and the Audit Evidence obtained &

c) Significant matters arising during the Audit, the conclusion reached thereon and significant

professional Judgement made in reaching those conclusions.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 21/30

SUPERWHIZZ *21* AUDITING STANDARDS

8) In documenting the nature, timing & extent of Audit procedures performed the Auditor shall

record

a) The identifying characteristics of the specific items or matters tested.b) Who performed the Audit work & the date on which that work was completed.

c) Who received the Audit work performed & the date and extent of such review.

9) Matters arising after the date of Auditors report:

In exceptional circumstances if the Auditor performs new or additional Audit procedures or

draws new conclusions after the date of the Auditors report then the Auditor shall document.

a) The circumstances encountered

b) The New or additional Audit procedures performed Audit evidence obtained, conclusions

reached & their effect on Auditors Report &c) When & by whom the resulting changes to Audit documentation were made reviewed.

10) The Auditor shall assemble the Audit Documentation in an Audit File & complete the

administrative process on a timely basis i.e., not more than 60 days after the date of Auditor’s

Report.

11) After the assembly of the Final Audit file has been completed, the Auditor shall not delete or

discard. Audit documentation of any nature before the end of retention period which is not

shorter than 10yrs from the date of the Auditor’s Report.

SA-580 - Written Representationsw.e.f. - 1-4-2009.

(1) Audit Evidence is all the information used by the Auditor in arriving at the conclusions on

which his opinion will be based Written Representations are also Audit Evidence & they provide

the Auditor with all the necessary information relating to the entity’s Financial statements.

(2) Written Representations do not provide sufficient appropriate Audit Evidence on their

own about any of the matters.

(3) Written Representations :-

These are written statements provided by the management to the Auditor to confirm

certain matters or to support other Audit Evidence. They do not include Financial Statements,

supporting books, records or financial statement assertions.

(4) The Auditor shall request Written Representations from management with appropriate

responsibilities for the Financial Statement & Knowledge of the matters concerned.

(5) The Auditor shall request the management to provide a written representation that it has

fulfilled it’s responsibility for the preparation & presentation of the Financial Statements in acco-

rdance with the applicable Financial reporting framework.

(Sec. 211 S-VI)

(6) The Auditor shall request the management to provide a written representation that it has

provided the Auditor with all relevant information as agreed in the terms of the Audit

Engage ment.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 22/30

SUPERWHIZZ *22* AUDITING STANDARDS

(7) The date of the Written Representations shall be as practicably near to the date of the

Auditors report but not there after.

(8) If Written Representations are inconsistent with other Audit Evidence, the Auditor shallperform Audit procedures to resolve the matter if the matter remains unresolved, the Auditor

shall consider the competence, Integrity, Ethical values, deligence, Commitment & Reliability of

Representations and Audit Evidence in general.

(9) The Written Representations shall be in the form of a Representation letter adressed to

the Auditor.

(10) Disclaimer of Opinion :-

In the following two circumstances the Auditor shall issue an Audit Report containing adisclaimer of opinion.

(a) If the Auditor Concludes that the Written Representations are not Reliable & Written

Representation are not Reliable &

(b) If the management does not provide written representations as requested by the Auditor

SA-220 - Quality Control for Audit Work

w.e.f. :- 1-4-1999

1. The purpose of SA-220 is to establish standards on -

(a) The Quality Control policies & procedures of an Audit Firm regarding Audit Work generally &

(b) The Quality Control procedures regarding the work delegated to assistants on an

Individual Audit.

2. (a) The Auditor - Means the person with final responsibility for Audit

(b) Audit Firm - Means either the partners of a firm providing Audit Services (OR)

a sole practitioner providing Audit Services as may be appropriate

(c) Personnel - Means all partners & professional staff engaged in the Audit practice

of the firm , &

(d) Assistants - Means personnel involved in an individual Audit other than the Auditor.

3. Audit Firm :-

(a) The Audit Firm should implement Quality Control policies & procedures which are

designed to ensure that all Audits are conducted in accordance with SAs.

(b) The Firm’s general Quality Control policies & procedures should be communicated to

the personnel such that they are understood and implemented.

4. In dividual Audits :-

(a) The Auditor should implement Quality Control procedures which are appropriate to theIndividual Audit.

(b) The Auditor should carefully direct, supervise & review the work delegated to his

Assistants & also consider their professional competence.

(c) In the case of large Complex Audits, the process of reviewing an Audit may

include requesting personnel not otherwise involved in the Audit to perform certain

additional procedures before issuing the Auditor’s Report.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 23/30

SUPERWHIZZ *23* AUDITING STANDARDS

SA-315 - Identifying & Assessing the risk of material

misstatements through understanding entity & it’s environment

w.e.f. 1-4-2008.

(1) The objective of the Auditor is to identity & assess the risks of material misstatement, whether

due to fraud or error, both at the Financial Statement & assertion levels through understanding

the entity & it’s environment, including the Entity’s Internal Control, there by providing a basis

for designing and implementing responses. This will help the Auditor to reduce the risk of mate-

rial mis-statement to an acceptably lower level.

(2) Assertions :-

Representations by management, explicit or otherwise that are embodied in the financial

statements, as used by the Auditor to consider the different types of potential mis-statements

that may occur.

(3) Business Risk :-

A Risk resulting from significant conditions, events, circumstances, actions or inactions

that could adversly affect an Entity’s ability to achieve it’s objectives & execute it’s strategy or

from the setting of inappropriate objectives and strategies.

(4) Risk Assessment Procedures :-

The Audit procedures performed to obtain an understanding of the Entity & it’s envi-

ronment including the Entity’s Internal Control, to identify & assess the risks of material mis-

statement, whether due to fraud or error, both at the Financial Statement & assertion levels.

(5) Significant Risk :-

An identified and assessed Risk of material mis-statement that requires special Audit

consideration according to Auditor’s judgement.

(6) Material Weakness :-

A Weakness in Internal Control that could have a material effect on the Financial Statements.

(7) Risk Assessment Procedure & Related Activities :-

They include the following

→Making enquires of management

→Analytical procedures

→Observation & Inspection

(8) The Auditor shall obtain an understanding of the following

(a)Relevant Industry & applicable Financial reporting framework.

(b)Nature of the entity

(c)The ownership, governance structure &

(d)The operations of the Entity

(e)The selection & application of Accounting policies.

(f)The objectives, strategies & related Business risks

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 24/30

SUPERWHIZZ *24* AUDITING STANDARDS

(9) The Auditor shall obtain an understanding of Internal Control relevant to the Audit. It is

a matter of Auditor’s professional Judgement.

(10) The Auditor shall communicate material weaknesses in Internal Control identified duringthe Audit on a timely basis both to the management & those charged with governance of the

Entity.

SA-330 – The Auditor’s Responses to Assessed Risk.

w.e.f – 1-4-2008.

(1) The objective of the Auditor is to obtain, sufficient appropriate Audit Evidence about the

assessed Risks of material mis-statement, through designing & implementing appropriate

responses to those risks.

(2) Substantive procedure :-

An Audit procedure designed to detect material mis-statements at the assertion level substantive

procedures comprise of

(a) Tests of details, i.e., transactions, Account balances & disclosures &

(b) Analytical procedures

(3) Tests of Control :-

An Audit procedure designed to evaluate the operating effectiveness of controls in preventing,

detecting and correcting material mis-statement at the assertion level .

(4) The Auditor shall design and implement overall responses to address the assessed risks of

material mis-statement at the Financial Statement level.

(5) The Auditor shall design & perform further Audit procedures whose nature, timing & extent are

based on & are response to the assessed Risks of Material mis-statement at the Assertion level.

(6) The Auditor shall design & perform substantive procedure for each material class of

transactions, account balances & disclosures.

(7) The Auditor shall evaluate whether the assessments of the risks of material misstatement at the

assertion level remain appropriate, before the conclusion of the Audit.

(8) If the Auditor has not obtained sufficient appropriate Audit Evidence regarding a material

financial statement assertion, then the Auditor shall express a qualified opinion or a disclaimer of

opinion.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 25/30

SUPERWHIZZ *25* AUDITING STANDARDS

SA-600 – Using the work of another Auditor (Branch Auditor)

w.e.f -1-4-2002.

(1) When the principal Auditor uses the work of another Auditor, the principal Auditor shoulddetermine how the work of the other Auditor will affect the Audit.

(2) (a) Principal Auditor :-

It means the Auditor with responsibility for reporting on the Financial Information of

an Entity which includes the Financial information of one or more components audited by

another Auditor.

(b) Other Auditor:-

It means the Auditor with the responsibility of reporting on the Financial Information of a

component which is included in the Financial information audited by the principal Auditor.

(c) Component :-

It means a division, branch, subsidiary, joint venture, associated enterprise or other entity whose

financial information is included in the Financial Information audited by the principal Auditor.

(3) The Auditor should consider whether his participation alone is sufficient to act as principal

Auditor.

(4) When using the work of another Auditor the principal Auditor should consider the professionalcompetence of the other auditor particularly if he is not a member of the ICAI.

(5) The principal auditor should perform procedures to obtain sufficient appropriate Audit Evidence

that the work of other Auditor is adequate for the specific assignment.

(6) The principal auditor should consider the significant finding of the other auditor.

(7) There should be sufficient liaison beetween the principal Auditor and the other Auditor.

(8) The other auditor should co-ordinate with the principal auditor because his work will be used by

the principal auditor.(9) Where the principal auditor concludes that the work of the other auditor cannot be used by him,

then he should consider it as a limitation on the scope of his Audit work, & he should express a

qualified opinion or disclaimer of opinion as may be appropriate.

(10) Where the principal Auditor relies on the reports of the other auditors, then his Audit report

should clearly state the division of Responsibility.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 26/30

SUPERWHIZZ *26* AUDITING STANDARDS

SA-610 – Using the Work of Internal Auditor

w.e.f : - 1-4-2010.

(1) The objective of the External Auditor is to determine the extent of the specific work performedby the Internal Auditor & whether such work is adequate for the purposes of his Audit.

(2) Internal Audit Function :-

An appraisal activity established or provided as a service to the entity. It’s functions include

examining, evaluating & monitoring the adequacy & effectiveness of Internal Control, among

various other things.

(3) Internal Auditors:-

The Individuals who perform the activities of Internal Audit Function. They may belong to an

Internal Audit Dept. or equivalent function.

(4) For determining whether the work of Internal Auditors is adequate for his Audit, the external

Audit shall evaluate the following aspects.

(a) The objectivity of the Internal Audit Function.

(b) The technical competence of the Internal Auditors.

(c) Whether the work was carried out with due professional care.

(d) Whether there is an affective communication between the external Auditor and the

Internal Auditor.(e) The nature and scope of the specific work performed by the Internal Auditors.

(f) Whether the work was performed by Internal Auditors having adequate technical

training & proficiency (aptitude)

(g) Whether adequate Audit Evidence was obtained by the Internal Auditors to draw

reasonable conclusions.

(h) Whether the Internal Auditor’s work was properly supervised, reviewed &

documented.

(i) Whether the conclusions reached by the Internal Auditor are consistent with the results

of the work performed

(j) Whether any exceptions or unusual matters found by the Internal Auditors are properly

resolved.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 27/30

SUPERWHIZZ *27* AUDITING STANDARDS

SA-620 – Using the work of an Expert

w.e.f. – 1-4-1991

(1) The Auditor’s education & experience will enable him to be knowledgeable about business

matters in general, but he is not expected to have the expertise of another professional such as

an actuary or an Engineer.

(2) An Expert is a specialist who may be an individual or firm or a AOP possessing specialized skill,

knowledge & Experience in any field other than Accounting & Auditing.

(3) An Expert may be –

(a) Engaged by the Client or

(b) Engaged by the Auditor or(c) Employed by the Client or

(d) Employed by the Auditor

(4) When the Auditor uses the work of an expert employed by him, he is using his work in the

capacity as an expert & not as an assistant. Therefore, the Auditor need not enquire into the

skills & competence of that expert.

(5) When the Auditor plans to use the experts work as Audit Evidence, he should satisfy himself

about the Expert’s skills & competence by considering his professional qualifications,

membership in an appropriate professional body, experience, reputation in the field etc….,

(6) The auditor should also consider the objectivity of the Expert. There is a risk that the objectivity

of the Expert may be impaired when the expertise either employed by the client or related in

some other manner to the client.

(7) After performing audit procedures, if the Auditor concludes that the work of the expert is

inconsistent or does not constitute sufficient appropriate Audit Evidence, then the Audit should

express a qualified opinion or a disclaimer of opinion or an adverse opinion, as may be

appropriate.

(8) When expressing an unqualified opinion, the Auditor should not refer to the work of an Expert inhis report.

(9) If the Auditor decides to express other than an unqualified opinion, he may refer or describe the

work of the expert. If the Auditor decides to disclose the identity of the Expert, then he should

obtain the prior consent of that expert (in writing).

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 28/30

SUPERWHIZZ *28* AUDITING STANDARDS

SA-250 – Consideration of laws & regulations in an Audit of

Financial Statement w.e.f . – 1-4-2009.

(1) It is the responsibility of the management with the oversight of those charged with governance,

to ensure that the entity’s operations are conducted in accordance with all applicable laws &

regulations

(2) The Auditor is not responsible for preventing non-compliance & he cannot be expected to

detect non-compliance with all laws & regulations

(3) Whether an act constitutes non-compliance is ultimately a matter for legal determination by

account of law.

(4) Non-compliance :-

Acts of omission or commission by the entity either intentional or unintentional, which are

contrary to the prevailing laws or regulations, Such acts include transactions entered into in the

name of the Entity by the management or those charged with governance or employees. Non-

compliance does not include personal mis-conduct, i.e., unrelated to the Business activities of

the Entity.

(5) The Auditor shall obtain sufficient appropriate Audit Evidence regarding compliance with laws &

regulations which have a direct affect on material Financial Statement assertions.

(6) During the course of Audit, the Auditor shall remain alert to the possibility that there will be

instances of non-compliance or suspected non-compliances with laws & regulations.

(7) If the Auditor suspects that the management or those charged with governance are involved in

non-compliance then he should communicate the matter to an Audit committee or supervisory

board & obtain legal advice.

(8) If the Auditor concludes that the non-compliance has a material affect on the Financial

Statements, then he should express a qualified opinion or Adverse opinion as may be

appropriate.

(9) The Auditor shall document all the identified or suspected non-compliances with laws &

regulations & also all the discussions that he had with the management, those charged with

governance & other parties outside the Entity.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 29/30

SUPERWHIZZ *29* AUDITING STANDARDS

SA-260 – Communication with those charged with Governance

w.e.f. – 1-4-2009.

(1) Those charged with governance :-

The persons with responsibility for overseeing the strategic direction of the Entity &

obligations related to the accountability of the Entity. This includes overseeing the

financial reporting process.

Eg:- Executive members of the Governance boards, Corporate trustees,

owner-manager, persons responsible for approving the Entity’s financial

statements.

(2) Management :-

The persons with executive responsibility for the conduct of the Entity’s operations. Insome Entity’s management includes owner-manager, those charged with governance

& executive members of the governance board.

(3) The Auditor shall communicate with those charged with governance an over view of

the planned scope & timing of the Audit. His communication should include the

Entity’s accounting practices, applicable financial reporting framework, significant

difficulties encountered during Audit, material weaknesses of Internal Control, other

matters as considered important according to Auditor’s professional judgement

etc…,

(4) The Auditor shall communicate with those charged with governance on a timely basis.

He should document when & to whom they were communicated. If any

communication was made orally, the Auditor shall also document then.

SA-265- Communicating Deficiencies of Internal Control to

Management & those charged with governance

w.e.f – 1-4-2010.

(1) The objective of the Auditor is to communicate appropriately to those charged with

governance & management deficiencies in Internal control that the Auditor has

identified during the Audit & that are of sufficient importance in the Auditor’s

professional judgement.

(2) Deficiency in Internal Control :-

This exists when a control is designed, implemented or operated in such a way it is

unable to prevent, detect, & correct material mis-statements in the Financial

Statement on a timely basis.

(3) Significant Deficiency in Internal Control :-

A Deficiency or a combination of Deficiencies in Internal Control that are of sufficientimportance & that must be communicated to those charged with governance,

according to Auditor’s professional judgement.

8/8/2019 Auditing Stands Clubbing 1-33

http://slidepdf.com/reader/full/auditing-stands-clubbing-1-33 30/30

SUPERWHIZZ *30* AUDITING STANDARDS

4) The Auditor shall determine whether he has identified one or more deficiencies in Internal

control, on the basis of the Audit work performed.

5) If the Auditor has identified one or more deficiencies in Internal Control ,

Whether Individually or in combination, he should consider whether, they constitute significant

deficiency.

6) The Auditor shall communicate in writing to those charged with governance & to management

on a timely basis, all the significant deficiencies in Internal control identified during the Audit.

7) The Auditor shall include in his written communication to those charged with governance, the

following aspects

(a) A description of significant deficiency & an explanation of their potential affects(b) Sufficient information to enable those charged with governance & Management to

understand the context of the

(c) A Statement that the purpose of the Audit was to express an opinion on the financial

statement & the audit was conducted not for the purpose Of expressing an opinion on the

effectiveness of Internal control.