White Paper - Merk Fund

10

Emerging Market Currencies: Asian Currencies Resilient, Better Value ? Merk Investments LLC ® | Research | July 2013 White Paper FUNDS TM The Authority on Currencies ™

Transcript of White Paper - Merk Fund

Emerging Market Currencies:

Asian Currencies Resilient,

Better Value ?

FUNDSTM

The Authority on Currencies™

Merk Investments LLC® | Research | July 2013

White Paper

FUNDSTM

The Authority on Currencies™

© 2013 Merk Investments LLC® | (866) MERK FUNDS | www.merkfunds.com | Page 2

®

Merk Investments LLC | White Paper | July 2013

Watemark as of 2011-12-08. COPY/PASTE for material in InDesign format.(FYI: The irregular blue frame around the Owl and Text is normal...)

Year-to-date through June 2013, we have experienced unusually high volatility in emerging market currencies, stemming from the speculation around the Federal Reserve Board’s tapering, spillover of the Bank of Japan’s recent easing, geopolitical instability, and slower growth in major emerging market economies. To protect them-selves, should U.S.-based investors abandon their emerging market currency exposures? Are there any emerging market currencies that might weather the storm better than others? In this report, we attempt to answer these timely and relevant questions through analyzing 21 emerging market currencies (Figure 1).1

While we expect high volatility to continue in the near term, our analysis suggests that a select number of emerg-ing Asian currencies may be more resilient to this round of shocks, given respective countries’ strong external positions. More fundamentally, we maintain a positive long-term outlook on these Asian currencies. In particular, we believe countries with strong economic fundamentals, increasing pricing power, and low correlation with U.S. markets, may continue to provide U.S.-based investors diversification benefits and liquid access to emerging market growth.

Figure 1. Currencies of 21 Emerging Markets

Separating Winners From Losers

After the 2008-2009 financial crisis, emerging markets across the board witnessed large investment inflows and emerging market currencies in general benefited from the trend. Investors in the developed world were attracted to the higher expected nominal yields of emerging market currencies, as central banks of major developed econo-mies unveiled massive monetary easing and pushed nominal interest rates to ultra-low levels.

121 countries classified by MSCI as EM countries by May 2013. Greece, the UAE and Qatar (recently reclassified to emerging markets by MSCI) are not included in this whitepaper, as the reclassifications will take effect in November 2013 for Greece and in 2014 for the UAE and Qatar. In addition, Morocco is downgraded to frontier market status in June 2013.

ASIA! EMEA (Europe, Middle-East, Africa)!

LATAM (Latin America)!

Chinese Yuan (CNY)! Czech Republic Koruna (CZK)! Brazilian Real (BRL)!

Indonesian Rupiah (IDR)! Egyptian Pound (EGP)! Chilean Peso (CLP)!

Indian Rupee (INR)! Hungarian Forint (HUF)! Colombian Peso (COP)!

South Korean Won (KRW)! Moroccan Dirham (MAD)! Mexican Peso (MXN)!

Malaysian Ringgit (MYR)! Polish Zloty (PLN)! Peruvian Nuevo Sol (PEN)!

Philippine Peso (PHP)! Russian Ruble (RUB)!

Thai Baht (THB)! Turkish Lira (TRY)!

New Taiwan Dollar (TWD)! South African Rand (ZAR)!

Watemark as of 2011-12-08. COPY/PASTE for material in InDesign format.(FYI: The irregular blue frame around the Owl and Text is normal...)

© 2013 Merk Investments LLC® | (866) MERK FUNDS | www.merkfunds.com | Page 3

®

Merk Investments LLC | White Paper | July 2013

However, not all the emerging market currencies generated positive returns for U.S.-based investors. During the three-year period from 2009 to 2012, only 10 out of the 21 emerging market currencies studied in the report ap-preciated against the U.S. dollar on a cumulative basis (Figure 2). In addition, high-yielding emerging market currencies are often associated with additional risks, stemming from market segmentation, political instability, and competitive devaluation. Therefore, a contained level of volatility, or a high risk-adjusted return, may be very valuable for investors seeking investments in emerging market currencies.

Figure 2. Cumulative Returns Against the U.S. Dollar from 2009/12/31 – 2012/12/31

Past performance does not predict future returns. Source: Merk Investments, Bloomberg

Figure 3 depicts the risk-return profiles of emerging market currencies for the same three-year period ending De-cember 31, 2012. As highlighted in navy blue in the chart, Asian currencies as a group not only led the post-crisis appreciation but also presented the most favorable risk-return profiles. Most Asian currencies, except the Indo-nesian rupiah (IDR) and the Indian rupee (INR), recorded an annualized return between 2-4% and an annualized risk, measured by standard deviation of daily returns, below or around 10%. In contrast, most Latin American and EMEA currencies posted higher standard deviations and lower or negative returns during the same time period.

! ASIA! EMEA! LATAM!

Appreciation Against USD!

PHP! 12.57%! ! ! COP! 15.66%!

MYR! 12.05%! ! ! PEN! 13.19%!

TWD! 10.17%! ! ! CLP! 5.90%!

CNY! 9.57%! ! ! MXN! 1.85%!

KRW! 9.36%! ! ! ! !

THB! 9.09%! ! ! ! !

Depreciation Against USD!

IDR! -3.97%! RUB! -1.61%! BRL! -14.97%!

INR! -15.40%! CZK! -2.88%! !

! ! MAD! -6.64%! !

! ! PLN! -7.46%! !

! ! ZAR! -12.69%! !

! ! EGP! -13.82%! !

! ! HUF! -14.43%! !

! ! TRY! -15.98%! ! !

Watemark as of 2011-12-08. COPY/PASTE for material in InDesign format.(FYI: The irregular blue frame around the Owl and Text is normal...)

®

Merk Investments LLC | White Paper | July 2013

© 2013 Merk Investments LLC® | (866) MERK FUNDS | www.merkfunds.com | Page 4

Asian currencies outperformed, especially on a risk-adjusted basis, their peer emerging market currencies in the post-crisis period likely as a result of: • Economic strength: Asian economies led the world’s post-crisis recovery. According to the IMF World Economic Outlook Database, developing Asian countries as a group enjoyed annual growth rates from 6.6%-10.0% between 2009 and 2012, while growth in Latin American countries and emerging European countries were between 3.0%-6.1% and 1.6%-4.6%, respectively. • Inflation contained: Most Asian countries except India placed high priority on taming inflation during the recovery. Several Asian central banks acted aggressively in 2011 when inflation accelerated, and refrained from easing too soon when inflation slowed in 2012. Unlike Brazil and India where year-over-year inflation reached 7% and 10% during 2011, respectively, most Asian countries kept inflation largely in line with respective central banks’ inflation target range. • Credit ratings higher: Despite the downgrade of many EMEA developing countries, Asian countries re-ceived upgrades or maintained stable local currency sovereign debt ratings. Latin American countries studied in the report also received upgrades, but Asian countries on average started with higher sovereign ratings.

“Strong economic recovery, relatively contained inflationary pressure, and higher sovereign ratings boosted investor confidence and curbed volatility in Asian currencies.”

In addition, Asian currencies demonstrated low correlations with U.S. equity markets, providing potential port-folio diversification benefits for U.S.-based investors. As shown in Figure 4, all of the Asian currencies studied in the report posted three-year correlations less than 0.35, among the lowest in all emerging market currencies. This low correlation could be particularly attributed to growing intra-Asian investment and trade flows and lower dependence on U.S. funding compared to other emerging markets.

-8.0%!

-6.0%!

-4.0%!

-2.0%!

0.0%!

2.0%!

4.0%!

6.0%!

0.0%! 2.0%! 4.0%! 6.0%! 8.0%! 10.0%! 12.0%! 14.0%! 16.0%! 18.0%! 20.0%!

3-Ye

ar A

nnua

lized

Ret

urns

Rel

ativ

e to

the

U.S

. Dol

lar!

3-Year Annualized Standard Deviation of Daily Returns!

Figure 3. Emerging Markets Currencies 3-Year Risk-Return! (2009/12/31 - 2012/12/31)!

ASIA! LATAM! EMEA!

CNY!

Source: Merk Investments, Bloomberg! © Merk Investments LLC!

TWD!

THB!

PHP! MYR!

IDR!

INR!

KRW!

COP!

CLP!

MXN!

BRL!ZAR!

PEN!

EGP!

MAD!

TRY!

RUB! CZK!PLN!

HUF!

®

Merk Investments LLC | White Paper | July 2013

© 2013 Merk Investments LLC® | (866) MERK FUNDS | www.merkfunds.com | Page 5

Which Currencies May Weather the Storm Better?

The sentiment has turned unfavorable for emerging markets this year. In recent months, emerging market curren-cies have come under pressure and volatility has risen across the board. Several reasons have contributed to the underperformance and rising volatility, including domestic political turmoil (the Turkish lira and the Brazilian real), substantially deteriorated growth outlook (the South African rand), fresh tensions around currency wars, and spillover effects from the massive weakening of the Japanese yen (the South Korean won and the New Taiwan dollar).

However, the major source of volatility, for emerging market currencies across the spectrum, may have been the uncertainty surrounding the tapering of Fed stimulus. Anticipating rising interest rates domestically, U.S.-based investors might further pull out money from emerging markets – a reversal of capital flows into these markets in the past few years. In our analysis, this uncertainty exposes currencies of emerging market countries with weak external positions to the greatest risks of capital outflows.

Currencies of emerging market countries running large current account deficits are particularly vulnerable in this environment. In a normal period, large current account deficits mean these emerging market countries rely on foreign investors to finance their economic growth or budget deficits. In a period of high volatility (akin to what we are experiencing currently), countries with large current account deficits are more likely to lose investor confi-dence and suffer from capital outflows. Such outflows mean downward pressure on the local currency as foreign investors convert their local currency proceeds from asset sales into their home currency or other hard currencies in the global foreign exchange market.

-0.1!

0.0!

0.1!

0.2!

0.3!

0.4!

0.5!

0.6!

0.7!

0.8!

EGP! CNY! IDR! TWD!KRW! PHP! MYR! INR! PEN! THB! COP! CLP! RUB! MAD! CZK! TRY! BRL! HUF! ZAR! PLN! MXN!

Figure 4. Three-Year Correlation of Daily Returns with S&P 500 Index!(2010/01/01 - 2012/12/31)!

Source: Merk Investments, Bloomberg! © Merk Investments LLC!

®

Merk Investments LLC | White Paper | July 2013

© 2013 Merk Investments LLC® | (866) MERK FUNDS | www.merkfunds.com | Page 6

Among the 21 emerging market economies analyzed in the report, most Asian countries except Indonesia and India are currently running modest to high current account surpluses, while all Latin American countries and most EMEA countries are currently running deficits. Figure 5 below shows the IMF’s estimates of these countries’ current account balance as a percentage of Gross Domestic Product by the end of 2012. Asian countries are high-lighted in navy blue while EMEA and Latin American currencies are depicted in grey.

Largely in line with the chart, currencies of countries with wide current account deficits (more than 5% of GDP) suffered the most in May 2013 from the erosion of investor confidence triggered by tapering talk. These curren-cies included the South African rand (ZAR), the Turkish lira (TRY), and the Indian rupee (INR). While several factors had affected the performance and, as always, past performance does not predict the future, we expect the current account deficit to remain an issue of concern among investors in these markets.

Additionally, most Asian countries are armed with stronger external positions, making respective currencies less vulnerable to capital outflows. In addition to having current account surplus, most Asian countries have accumu-lated sizeable official foreign reserves after the 1997-98 Asian financial crisis. Figure 6 shows Asian countries’ vast reserve assets as a percentage of GDP in comparison to other emerging market countries (Asian countries are highlighted in navy blue while EMEA and Latin American currencies are depicted in grey). In the current market turbulence, foreign reserves provide emerging market countries a valuable buffer in dealing with volatile capital flows and enhance investor confidence in the countries’ ability to repay short-term external debt, usually denominated in hard currencies. Sufficient foreign reserve assets also enhance an emerging market central bank’s capability in currency intervention when needed (usually by selling FX and buying domestic currency). In June

-12.0%!

-8.0%!

-4.0%!

0.0%!

4.0%!

8.0%!

12.0%!

TWD!MYR!

RUB!KRW! PHP!

CNY!HUF!

THB!MXN!

BRL!CZK!

IDR!

EGP!COP!

CLP!PLN!

PEN!IN

R!TRY!

ZAR!MAD!

Figure 5. Current Account Balance as Percentage of GDP*!

Source: Merk Investments, IMF World Economic Outlook April 2013!*IMF estimate for 2012! © Merk Investments LLC!

© 2013 Merk Investments LLC® | (866) MERK FUNDS | www.merkfunds.com | Page 6

®

Merk Investments LLC | White Paper | July 2013

© 2013 Merk Investments LLC® | (866) MERK FUNDS | www.merkfunds.com | Page 7

2013, central banks from Poland, Turkey, Brazil, Indonesia and India intervened in the currency markets to sup-port their respective currencies. Perhaps worth noting, relatively low reserve-to-GDP ratios make Turkey and Indonesia more vulnerable to the risk of running out of firepower.

“While not immune to the near-term risk-aversion, Asian countries’ strong external positions (cur-rent account surplus and large foreign reserves) may make Asian currencies more resillent to capital outflows”.

Which Currencies Will Thrive In the Long Term?

Despite recent underperformance and volatility, we maintain our positive outlook on emerging market currencies vs the U.S. dollar in the long term. Our view is primarily driven by emerging markets’ higher growth and lower indebtedness, the convergence of purchasing power parity with developed countries, and further liberalization of capital accounts and development of local currency debt markets.

In particular, we expect a number of Asian currencies to outperform other emerging market currencies in the long term supported by the following factors:

0.0%! 10.0%! 20.0%! 30.0%! 40.0%! 50.0%! 60.0%! 70.0%! 80.0%! 90.0%!

TWD!HUF!THB!

MYR!CNY!PHP!PEN!

KRW!RUB!PLN!

MAD!CZK!CLP!INR!BRL!ZAR!

MXN!IDR!TRY!COP!EGP!

Figure 6. Official Foreign Reserve as Percentage of GDP* !

Source: Merk Investments, CIA World Factbook, IMF!* Dec. 31, 2012 estimate! © Merk Investments LLC!

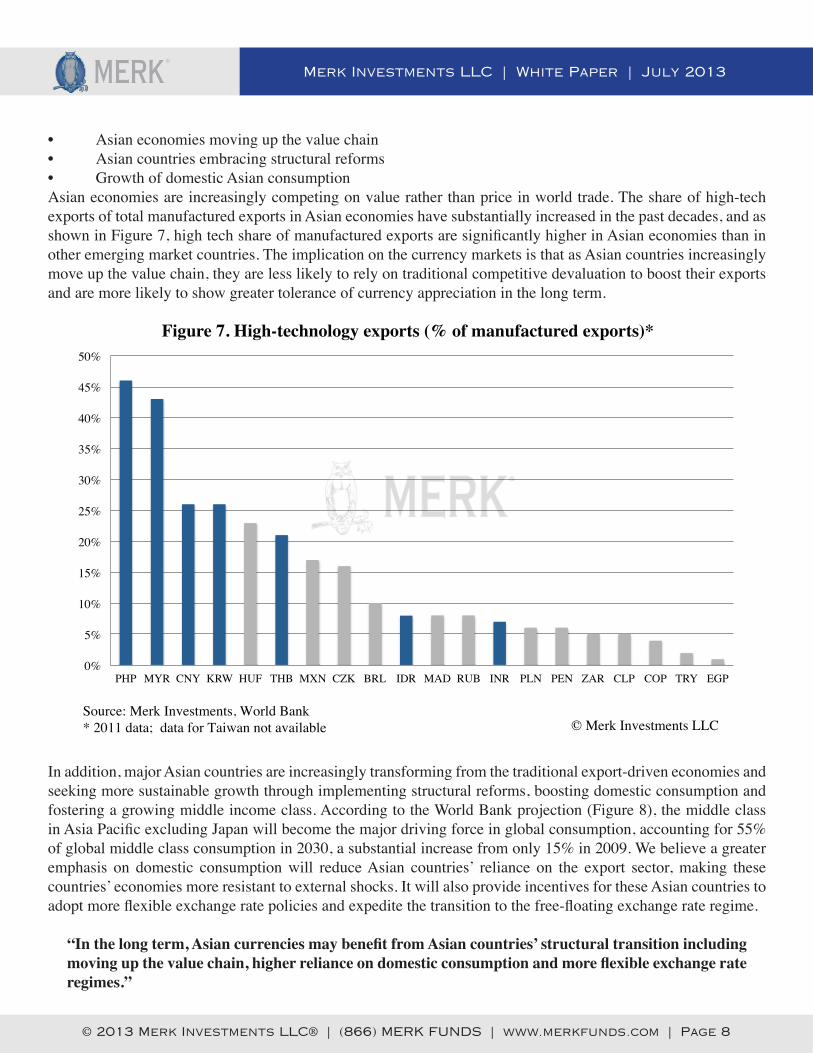

• Asian economies moving up the value chain• Asian countries embracing structural reforms• Growth of domestic Asian consumptionAsian economies are increasingly competing on value rather than price in world trade. The share of high-tech exports of total manufactured exports in Asian economies have substantially increased in the past decades, and as shown in Figure 7, high tech share of manufactured exports are significantly higher in Asian economies than in other emerging market countries. The implication on the currency markets is that as Asian countries increasingly move up the value chain, they are less likely to rely on traditional competitive devaluation to boost their exports and are more likely to show greater tolerance of currency appreciation in the long term.

In addition, major Asian countries are increasingly transforming from the traditional export-driven economies and seeking more sustainable growth through implementing structural reforms, boosting domestic consumption and fostering a growing middle income class. According to the World Bank projection (Figure 8), the middle class in Asia Pacific excluding Japan will become the major driving force in global consumption, accounting for 55% of global middle class consumption in 2030, a substantial increase from only 15% in 2009. We believe a greater emphasis on domestic consumption will reduce Asian countries’ reliance on the export sector, making these countries’ economies more resistant to external shocks. It will also provide incentives for these Asian countries to adopt more flexible exchange rate policies and expedite the transition to the free-floating exchange rate regime.

“In the long term, Asian currencies may benefit from Asian countries’ structural transition including moving up the value chain, higher reliance on domestic consumption and more flexible exchange rate regimes.”

®

Merk Investments LLC | White Paper | July 2013

© 2013 Merk Investments LLC® | (866) MERK FUNDS | www.merkfunds.com | Page 8

0%!

5%!

10%!

15%!

20%!

25%!

30%!

35%!

40%!

45%!

50%!

PHP! MYR! CNY! KRW! HUF! THB! MXN! CZK! BRL! IDR! MAD! RUB! INR! PLN! PEN! ZAR! CLP! COP! TRY! EGP!

Figure 7. High-technology exports (% of manufactured exports)*!

Source: Merk Investments, World Bank!* 2011 data; data for Taiwan not available! © Merk Investments LLC!

®

Merk Investments LLC | White Paper | July 2013

Conclusion

Within the emerging market currencies, Asian currencies have demonstrated favorable risk-return profiles for U.S.-based investors with what we believe are comparably attractive risk-adjusted returns, low volatility, and low correlation with U.S. equities. Despite recent risk aversion, we believe Asian currencies may weather increased volatility triggered by speculation surrounding Fed policy better than other EM currencies. Furthermore, over the longer term, we believe Asian currencies may outperform other emerging market currencies as a result of Asian countries’ transition to a higher value added and more consumption-oriented growth model.

The currency asset class allows investors to gain liquid (not risk free) exposure to emerging market growth. Com-pared to emerging market equities and local debt, emerging market currencies historically exhibit lower volatility. Compared to emerging market debt, a pure play in emerging market currencies may provide investors with lower interest rate and credit risks. Indeed, an upcoming Merk whitepaper will dive into the questions of whether inves-tors are fairly rewarded for the interest rate risk they are bearing in emerging market bonds and whether emerging market currencies might provide investors better risk-adjusted returns in the current market environment.

© 2013 Merk Investments LLC® | (866) MERK FUNDS | www.merkfunds.com | Page 9

About the Authors

Axel Merk is the President and CIO of Merk Investments, manager of the Merk Funds. An authority on currencies, he is a pioneer in the use of strategic currency investing to seek diversification. Axel Merk is a sought after speaker and author on topics ranging from the economy, gold and currencies to sustainable wealth and personal finance, as well as a regular guest and contributor to the business media around the world.

Yuan Fang is a Financial Analyst at Merk Investments and a member of the portfolio management group. She focuses on macro-economic research, security selection and portfolio analytics.

Asia Pacific ex. Japan,

15%!

North America, Europe &

Japan, 72%!

Other, 13%!

2009!

Asia Pacific ex. Japan,

55%!

North America, Europe &

Japan, 34%!

Other, 11%!

2030F!

Source: Merk Investments, World Bank, Brookings Institution!Forcasts are inherently limited and should not be relied upon as an indicator of future performance!

© Merk Investments LLC!

Figure 8. Asia's Rising Middle Class and Growing Consumption Share!Share of Global Middle Class Consumption (%)!

FOR MORE INFORMATION, PLEASE CONTACT US:

(866) MERK FUNDS | www.merkfunds.com

© 2013 Merk Investments LLC®FUNDS

The Authority on Currencies™

Fed: The “Fed” is the central bank of the United States and controls the money supply.Standard Deviation: a measure of historical volatility of the returns of the investment.Correlation: a measure, ranging in value from 1.00 to -1.00, of the historical association between returns of two investments.S&P 500 Index: a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. Performance figures assume that all dividends are reinvested. An investor cannot invest directly in an index.MSCI Emerging Markets (EM) Index: a free float-adjusted market capitalization index that is designed to measure equity market per-formance of emerging markets.GDP: Gross domestic product (GDP) is the market value of all officially recognized final goods and services produced within a country in a given period of time. * * *The Merk Mutual Funds (“Funds”) may be appropriate for you if you are pursuing a long-term goal with a currency component to your portfolio; are willing to tolerate the risks associated with investments in foreign currencies; or are looking for a way to potentially mitigate downside risk in or profit from a secular bear market. For more information on the Funds and to download a prospectus, please visit www.merkfunds.com.

Investors should consider the investment objectives, risks and charges and expenses of the Funds carefully before in-vesting. This and other information is in the prospectus, a copy of which may be obtained by visiting the Funds’ website at www.merkfunds.com or calling 866-MERK FUND. Please read the prospectus carefully before you invest.

Since the Funds primarily invest in foreign currencies, changes in currency exchange rates affect the value of what the Funds own and the price of the Funds’ shares. Investing in foreign instruments bears a greater risk than investing in domestic instruments for reasons such as volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, emerging market risk, and relatively illiquid markets. The Funds are subject to interest rate risk, which is the risk that debt securities in the Funds’ portfo-lio will decline in value because of increases in market interest rates. The Funds may also invest in derivative securities, such as forward contracts, which can be volatile and involve various types and degrees of risk. If the U.S. dollar fluctuates in value against currencies the Funds are exposed to, your investment may also fluctuate in value. The Merk Currency Enhanced U.S. Equity Fund may invest in exchange traded funds (“ETFs”). Like stocks, ETFs are subject to fluctuations in market value, may trade at prices above or below net asset value and are subject to direct, as well as indirect fees and expenses. As a non-diversified fund, the Merk Hard Currency Fund will be subject to more investment risk and potential for volatility than a diversified fund because its port-folio may, at times, focus on a limited number of issuers

This report was prepared by Merk Investments LLC, and reflects the current opinion of the authors. It is based upon sources and data believed to be accurate and reliable. Merk Investments LLC makes no representation regarding the advisability of investing in the products herein. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute investment advice. Foreside Fund Services, LLC, distribu-tor.

Explicit permission must be obtained from Merk Investments LLC in order to replicate, copy, distribute or quote from this document or any portion thereof.

Published by Merk Investments LLC, July 2013

© 2013 Merk Investments LLC

®

Merk Investments LLC | White Paper | July 2013