The World Bank FOR OFFICIAL USE...

109

Document of The World Bank FOR OFFICIAL USE ONLY Report No: 52142-MX PROJECT APPRAISAL DOCUMENT ON A PROPOSED LOAN IN THE AMOUNT OF US$1,250 MILLION TO THE UNITED MEXICAN STATES FOR A SOCIAL PROTECTION SYSTEM IN HEALTH PROJECT February 23, 2010 Human Development Sector Management Unit Mexico and Colombia Country Management Unit Latin America and the Caribbean Region This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of The World Bank FOR OFFICIAL USE...

Document of

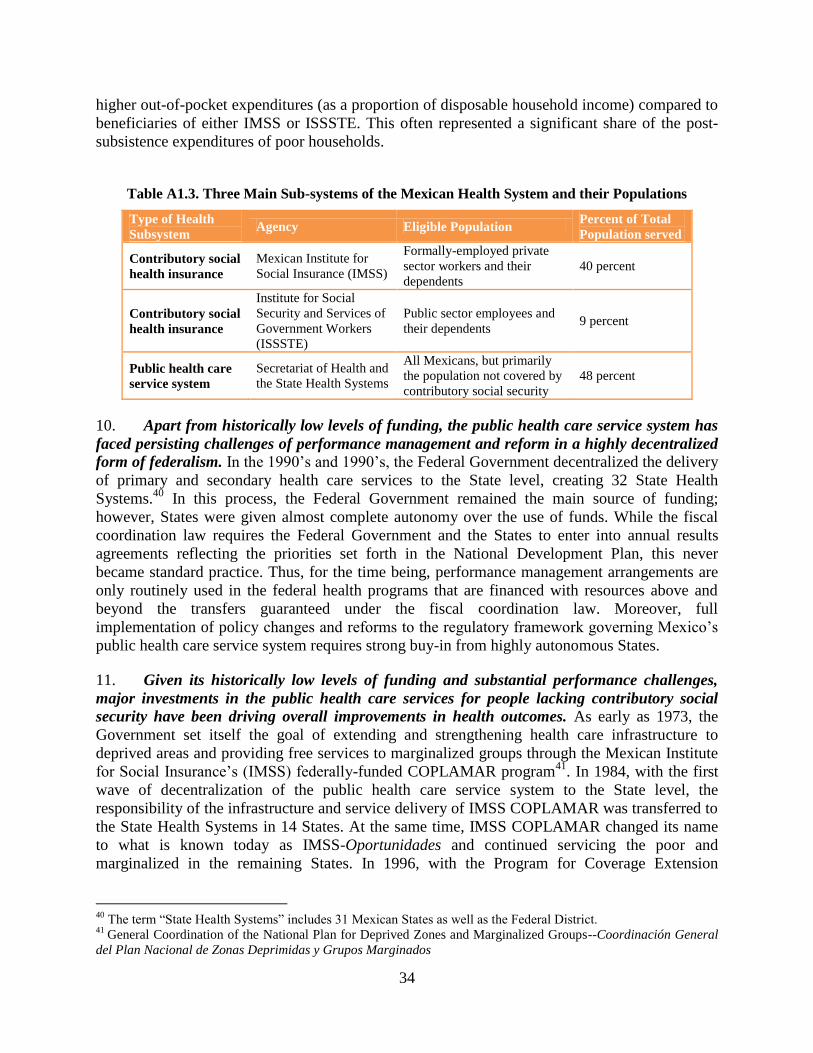

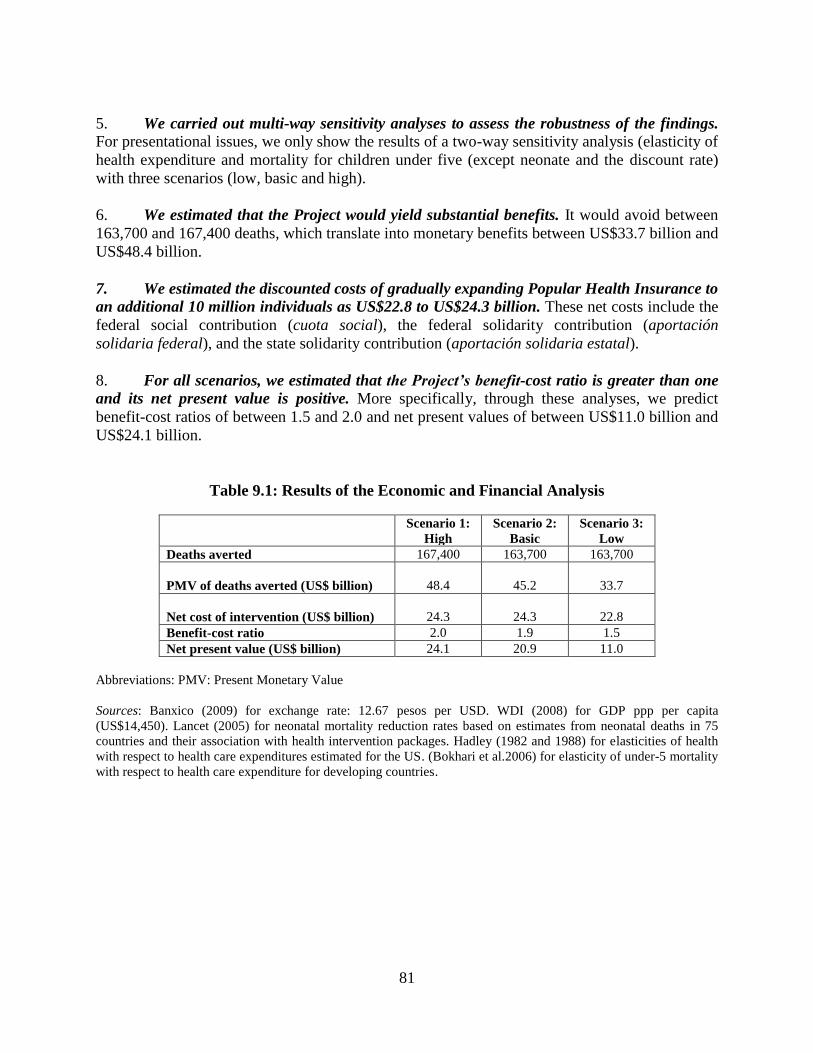

The World Bank

FOR OFFICIAL USE ONLY

Report No: 52142-MX

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED LOAN

IN THE AMOUNT OF US$1,250 MILLION

TO THE

UNITED MEXICAN STATES

FOR A

SOCIAL PROTECTION SYSTEM IN HEALTH PROJECT

February 23, 2010

Human Development Sector Management Unit

Mexico and Colombia Country Management Unit

Latin America and the Caribbean Region

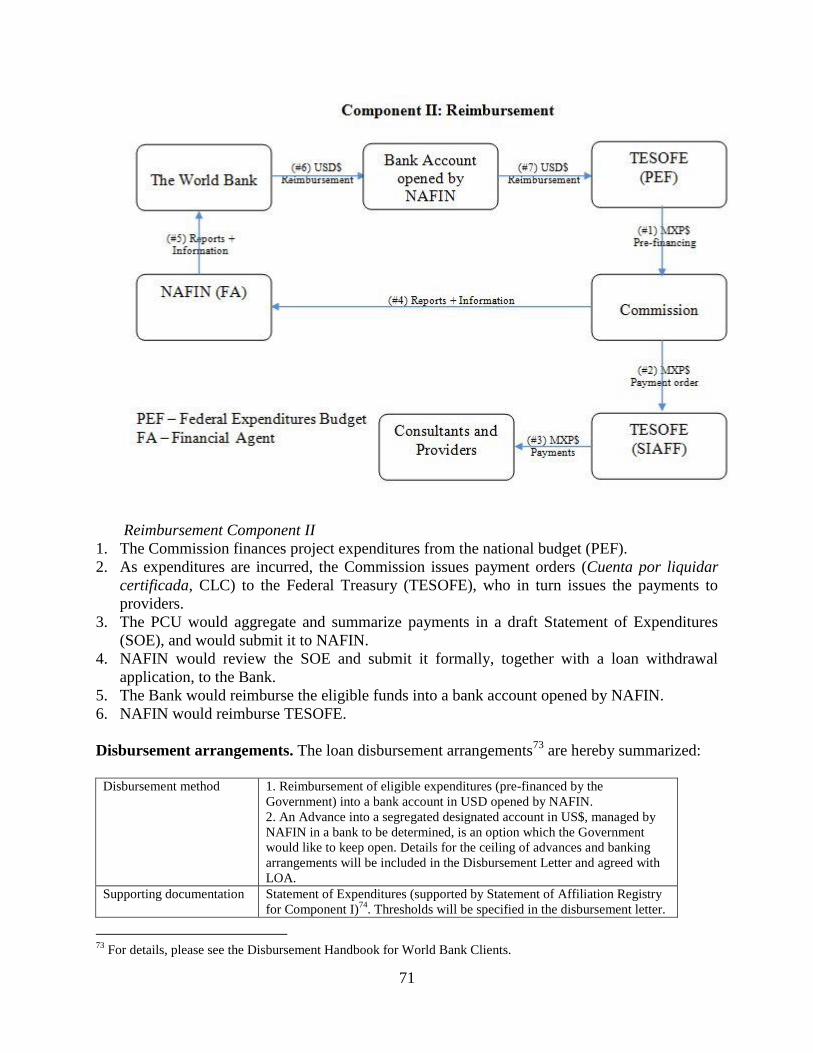

This document has a restricted distribution and may be used by recipients only in the

performance of their official duties. Its contents may not otherwise be disclosed without World

Bank authorization.

Pub

lic D

iscl

osur

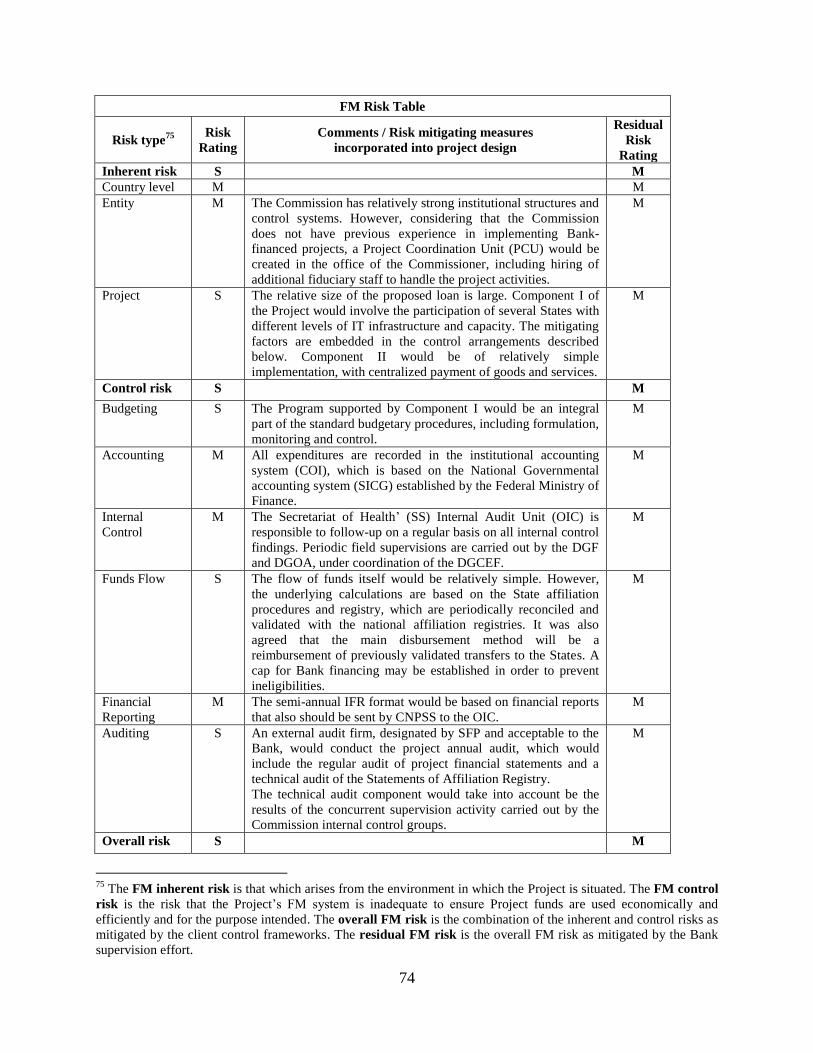

e A

utho

rized

Pub

lic D

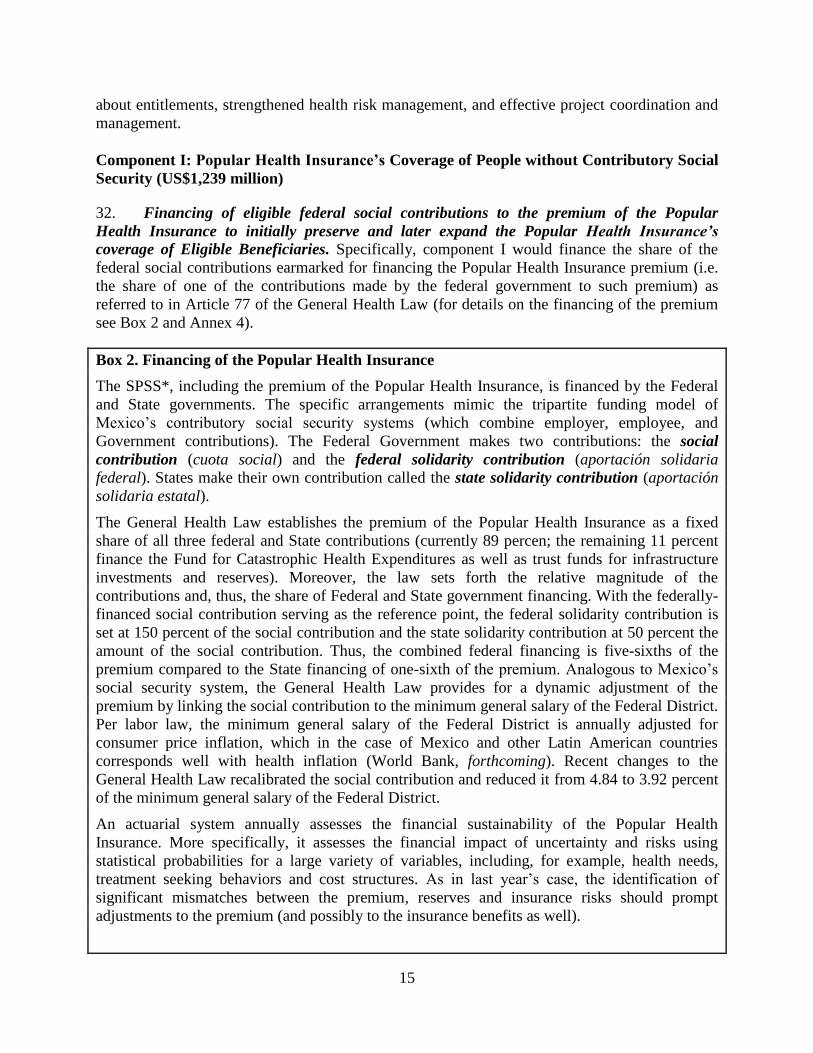

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective February 23, 2010)

Currency Unit = Mexican Peso (MXN)

12.8148 MXN = US$1

US$0.0780 = 1 MXN

FISCAL YEAR

January 1 – December 31

ABBREVIATIONS AND ACRONYMS

AIDS Acquired Immune Deficiency Syndrome

ASE State Solidary Contribution (Aportación Solidaria Estatal)

ASF Federal Solidary Contribution (Aportación Solidaria Federal)

BP Bank Procedure

CDI Commission for Indigenous Development (Comisión de Desarrollo de

los Pueblos Indígena)

CLC Payment Orders (Cuenta por Liquidar Certificada)

CNPSS or

Commission

The National Commission of Social Protection in Health (Comisión

Nacional de Protección Social en Salud)

COI Uniform Accounting System (Contabilidad Integral)

CONAPO National Population Council (Consejo Nacional de Población)

CONEVAL National Council for the Evaluation of Social Development Policy

(Consejo Nacional de Evaluación de la Política de Desarrollo Social)

COPLAMAR General Coordination of the National Plan for Deprived Zones and

Marginalized Groups (Coordinación General del Plan Nacional de

Zonas Deprimidas y Grupos Marginados)

CPS Country Partnership Strategy

CS Social Contribution (Cuota Social)

DGAF General Directorate of Administration and Finance (Dirección General

de Administración y Finanzas)

DGAO General Directorate of Affiliation and Operation (Dirección General de

Afiliación y Operación)

DGCEF General Directorate of Coordination with Federal Entities (Dirección

General de Coordinación con Entidades Federativas)

DGF General Directorate of Finance (Dirección General de Finanzas)

DGGSS General Directorate of Health Service Management (Dirección General

de Gestión de Servicios de Salud)

ENIGH Survey on Household Income and Expenditures (Encuesta de Ingresos y

Gastos de los Hogares)

ENSANUT National Health and Nutrition Survey (Encuesta Nacional de Salud y

Nutrición)

FA Financial Agent

FBS Fixed Budget Selection

FM Financial Management

FPGC Fund for the Protection Against Catastrophic Expenditures (Fondo de

Protección contra Gastos Catastróficos)

FPP Budgetary Contingency Fund (Fondo de Previsión Presupuestal)

FY Fiscal Year

GDP Gross Domestic Product

GET Global Expert Team

GHL General Health Law

GoM Government of Mexico

HDI Human Development Index

HDR Human Development Report

HIV Human Immunodeficiency Virus

IBRD International Bank for Reconstruction and Development

IDA International Development Association

IFR Interim Financial Reports

IMSS Mexican Social Insurance Institute (Instituto Mexicano del Seguro

Social)

INEGI National Institute for Statistics, Geography and Informatics (Instituto

Nacional de Estadística Geografía e Informática)

IP Implementation Process

IPP Indigenous Peoples Plan

ISDS Information Safeguards Data Sheet

ISSSTE National Institute for the Social Security of Government Workers

(Instituto de Seguridad y Servicios Sociales de los Trabajadores del

Estado)

LAC Latin America and the Caribbean Region

LCS Least Cost Selection

MDGs Millennium Development Goals

NAFIN National Finance Agent (Nacional Financiera)

NDP National Development Plan

OECD Organization for Economic Co-operation and Development

OIC Internal Control Unit (Organo Interno de Control)

OM Operational Manual

OP Operational Policy

PAC Program for Coverage Extension (Programa de Ampliación de

Cobertura de salud)

PASSPA Health Service Assistance Program for the Open Population (Programa

de Apoyo a los Servicios de Salud para Población Abierta)

PCU Project Coordination Unit

PDO Project Development Objective

PEF Federal Expenditure Budget (Presupuesto de Egresos de la Federación)

PIC Public Information Center

PID Project Information Document

PND National Development Plan (Plan Nacional de Desarrollo)

PPP Purchasing Power Parity

PROSESA Programa Sectorial de Salud

QBS Quality Based Selection

QCBS Quality and Cost Based Selection Method

REPSS Regímenes Estatales de Protección Social en Salud

RFP Request for Proposals

RVP Regional Vice-President

SAI The Supreme Audit Institution

SEED Epidemiological and Statistical System for the recording of Deaths

(Sistema Epidemiológico y Estadístico de Defunciones)

SEPA System for the Execution of Procurement Plans (Sistema de Ejecución de

Planes de Adquisiciones)

SFB Selection under a Fixed Budget

SFP Public Administration Secretariat (Secretaría de la Función Pública)

SHCP Federal Secretariat of Finance (Secretaría de Hacienda y Crédito

Público)

SINAIS National Health Information System (Sistema Nacional de Información

en Salud)

SOE Statements of Expenditures

SPSS Social Protection System in Health (Sistema de Protección Social en

Salud)

TA Technical Assistance

TESOFE Federal Treasury (Tesorería de la Federación)

UNDP United Nations Development Program

WBG The World Bank Group

WDI World Development Indicators

WHO World Health Organization

Vice President: Pamela Cox

Country Director: Gloria Grandolini

Sector Director: Evangeline Javier

Sector Manager: Keith Hansen

Task Team Leader: Christoph Kurowski

MEXICO

Social Protection System in Health

CONTENTS

Page

I. STRATEGIC CONTEXT AND RATIONALE ................................................................. 1

A. Country and sector issues.................................................................................................... 1

B. Rationale for Bank involvement ....................................................................................... 10

C. Higher level objectives to which the project contributes .................................................. 13

II. PROJECT DESCRIPTION ............................................................................................... 13

A. Lending instrument ........................................................................................................... 13

B. Project development objective .......................................................................................... 13

C. Project Key Performance Indicators ................................................................................. 13

D. Project components ........................................................................................................... 14

E. Lessons learned and reflected in the project design .......................................................... 17

F. Alternatives considered and reasons for rejection ............................................................ 18

III. IMPLEMENTATION .................................................................................................... 19

A. Institutional and implementation arrangements ................................................................ 19

B. Monitoring and evaluation of outcomes/results ................................................................ 20

C. Sustainability..................................................................................................................... 20

D. Critical risks and possible controversial aspects ............................................................... 21

E. Loan conditions and covenants ......................................................................................... 23

IV. APPRAISAL SUMMARY ............................................................................................. 23

A. Economic and financial analyses ...................................................................................... 23

B. Technical ........................................................................................................................... 24

C. Fiduciary ........................................................................................................................... 25

D. Social................................................................................................................................. 26

E. Environment ...................................................................................................................... 27

F. Safeguard policies ............................................................................................................. 28

G. Policy Exceptions and Readiness...................................................................................... 29

Annex 1: Country and Sector or Program Background ......................................................... 30

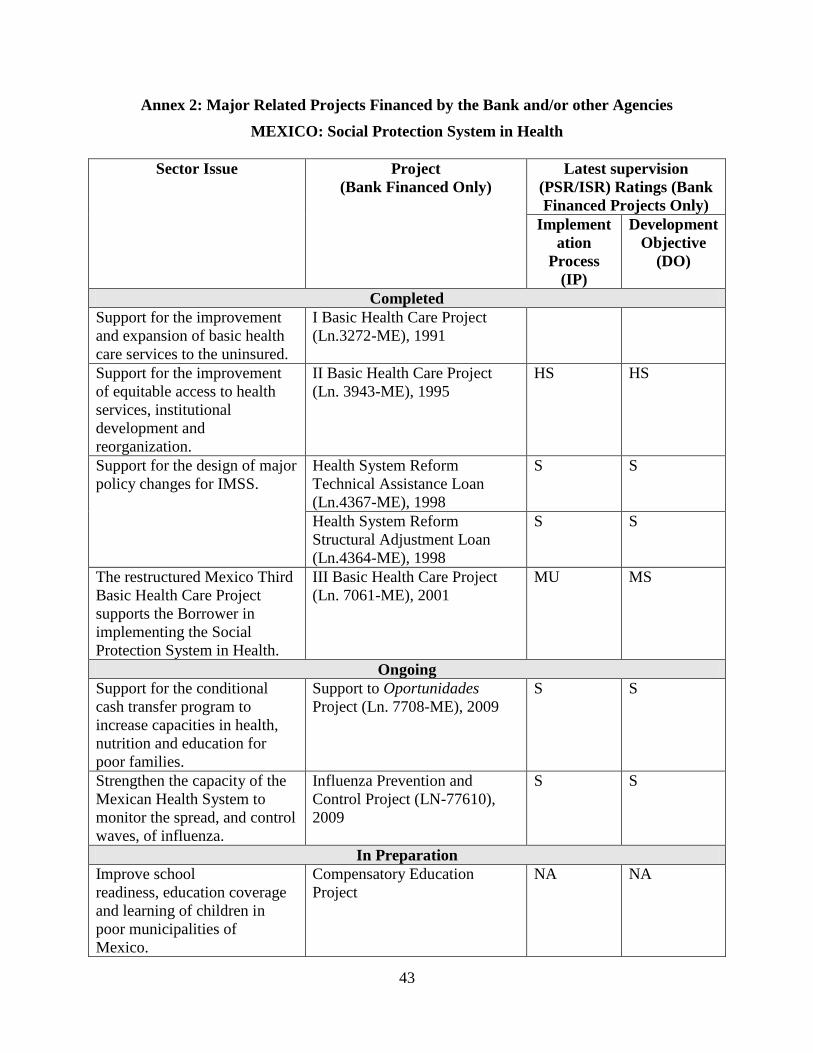

Annex 2: Major Related Projects Financed by the Bank and/or other Agencies ................. 43

Annex 3: Results Framework and Monitoring ........................................................................ 45

Annex 4: Detailed Project Description ...................................................................................... 52

Annex 5: Project Costs ............................................................................................................... 59

Annex 6: Implementation Arrangements ................................................................................. 60

Annex 7: Financial Management and Disbursement Arrangements ..................................... 66

Annex 8: Procurement Arrangements ...................................................................................... 76

Annex 9: Economic and Financial Analysis ............................................................................. 80

Annex 10: Safeguard Policy Issues ............................................................................................ 82

Annex 11: Project Preparation and Supervision ..................................................................... 89

Annex 12: Documents in the Project File ................................................................................. 90

Annex 13: Statement of Loans and Credits .............................................................................. 91

Annex 14: Country at a Glance ................................................................................................. 93

Annex 15: Map 33447R .............................................................................................................. 96

Annex 16: References ................................................................................................................. 97

MEXICO

SUPPORT TO THE SOCIAL PROTECTION SYSTEM IN HEALTH

PROJECT APPRAISAL DOCUMENT

LATIN AMERICA AND CARIBBEAN

LCSHH

Date: February, 23, 2010 Team Leader: Christoph Kurowski

Country Director: Gloria M. Grandolini

Sector Manager/Director: Keith E. Hansen

Sectors: Health (100%)

Themes: Health system performance (80%);

Indigenous peoples (10%); Social safety nets

(10%)

Project ID: P116226 Environmental category: C - Not Required

Lending Instrument: Specific Investment Loan Joint IFC:

Joint Level:

Project Financing Data

[X] Loan [ ] Credit [ ] Grant [ ] Guarantee [ ] Other:

For Loans/Credits/Others:

Total Bank financing (US$m.): 1,250.00

Proposed terms: IBRD Flexible loan, with a variable-spread, all conversion options, a bullet

repayment on January 15, 2028 and interest payments made each January 15 and July 15.

Financing Plan (US$m)

Source Local Foreign Total

Borrower 25,607.00 4.00 25,611.00

International Bank for Reconstruction and

Development

1,243.00 7.00 1,250.00

Total: 26,850.00 11.00 26,861.00

Borrower:

United Mexican States

Mexico

Responsible Agency: Secretariat of Health

Lieja No. 7, Piso 1

Colonia Juarez

DF

Mexico

06696

Tel: (52-55) 5553-0758

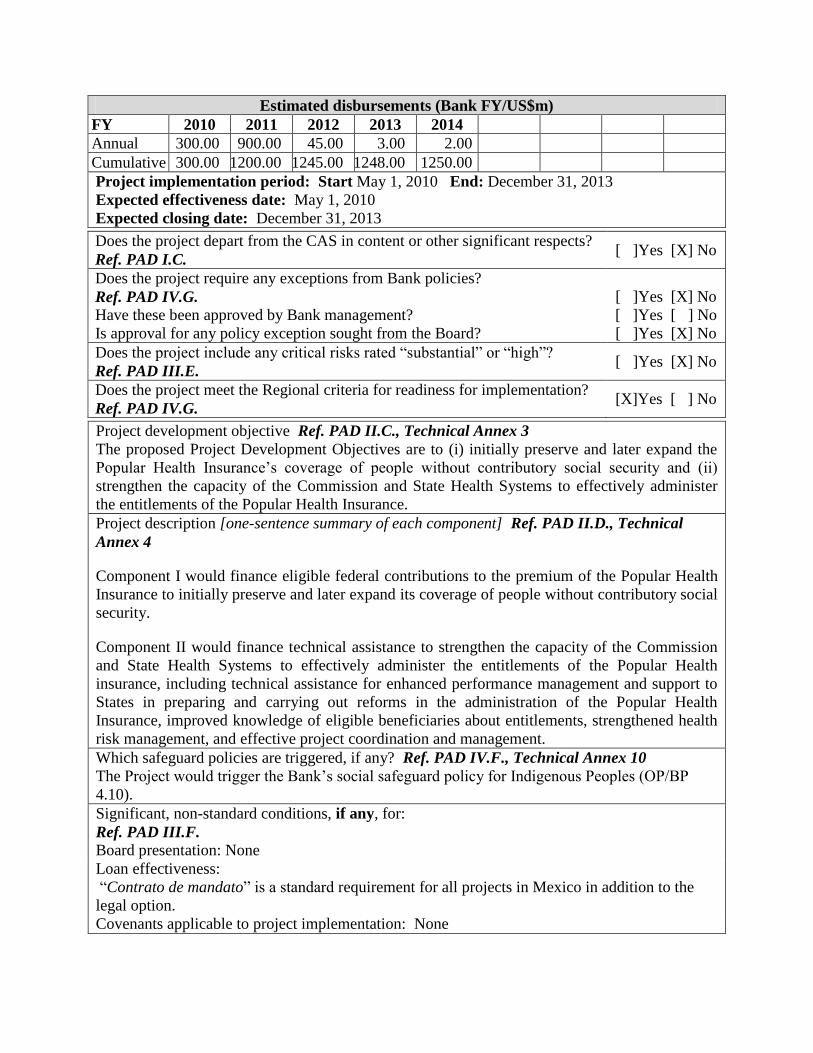

Estimated disbursements (Bank FY/US$m)

FY 2010 2011 2012 2013 2014

Annual 300.00 900.00 45.00 3.00 2.00

Cumulative 300.00 1200.00 1245.00 1248.00 1250.00

Project implementation period: Start May 1, 2010 End: December 31, 2013

Expected effectiveness date: May 1, 2010

Expected closing date: December 31, 2013

Does the project depart from the CAS in content or other significant respects?

Ref. PAD I.C. [ ]Yes [X] No

Does the project require any exceptions from Bank policies?

Ref. PAD IV.G. Have these been approved by Bank management?

[ ]Yes [X] No

[ ]Yes [ ] No

Is approval for any policy exception sought from the Board? [ ]Yes [X] No

Does the project include any critical risks rated ―substantial‖ or ―high‖?

Ref. PAD III.E. [ ]Yes [X] No

Does the project meet the Regional criteria for readiness for implementation?

Ref. PAD IV.G. [X]Yes [ ] No

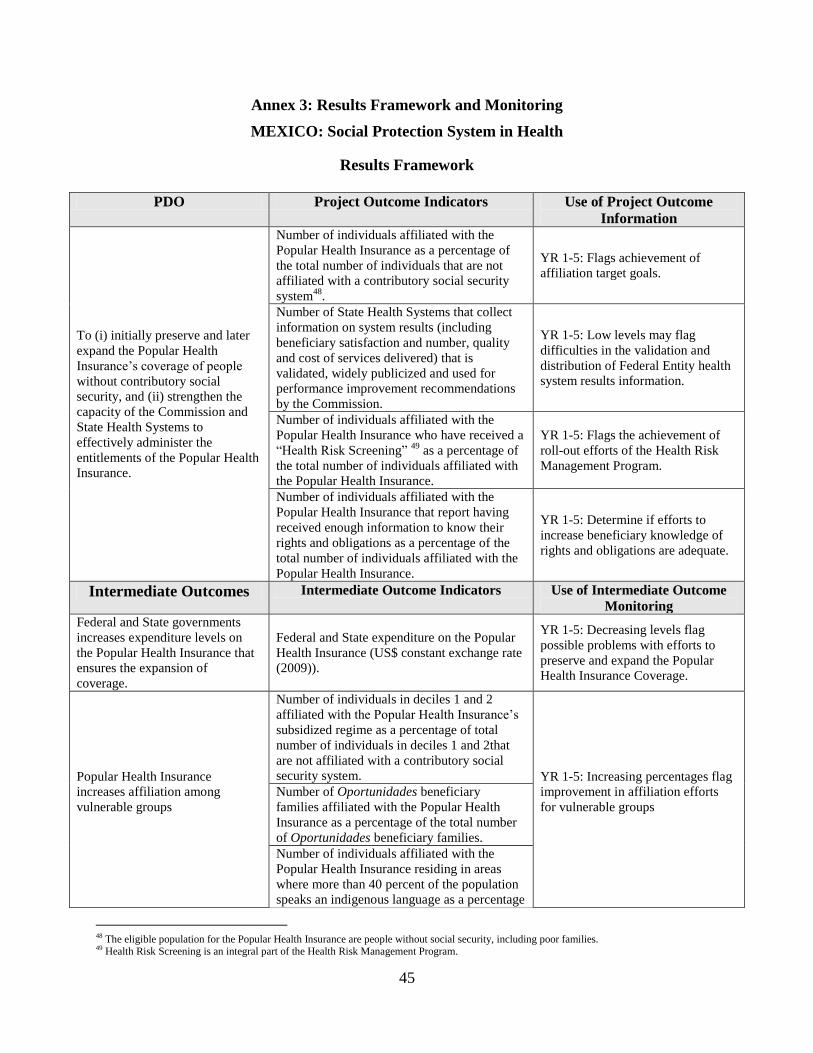

Project development objective Ref. PAD II.C., Technical Annex 3

The proposed Project Development Objectives are to (i) initially preserve and later expand the

Popular Health Insurance‘s coverage of people without contributory social security and (ii)

strengthen the capacity of the Commission and State Health Systems to effectively administer

the entitlements of the Popular Health Insurance.

Project description [one-sentence summary of each component] Ref. PAD II.D., Technical

Annex 4

Component I would finance eligible federal contributions to the premium of the Popular Health

Insurance to initially preserve and later expand its coverage of people without contributory social

security.

Component II would finance technical assistance to strengthen the capacity of the Commission

and State Health Systems to effectively administer the entitlements of the Popular Health

insurance, including technical assistance for enhanced performance management and support to

States in preparing and carrying out reforms in the administration of the Popular Health

Insurance, improved knowledge of eligible beneficiaries about entitlements, strengthened health

risk management, and effective project coordination and management.

Which safeguard policies are triggered, if any? Ref. PAD IV.F., Technical Annex 10

The Project would trigger the Bank‘s social safeguard policy for Indigenous Peoples (OP/BP

4.10).

Significant, non-standard conditions, if any, for:

Ref. PAD III.F.

Board presentation: None

Loan effectiveness:

―Contrato de mandato‖ is a standard requirement for all projects in Mexico in addition to the

legal option.

Covenants applicable to project implementation: None

1

I. STRATEGIC CONTEXT AND RATIONALE

A. Country and sector issues

Trends in Socioeconomic Development

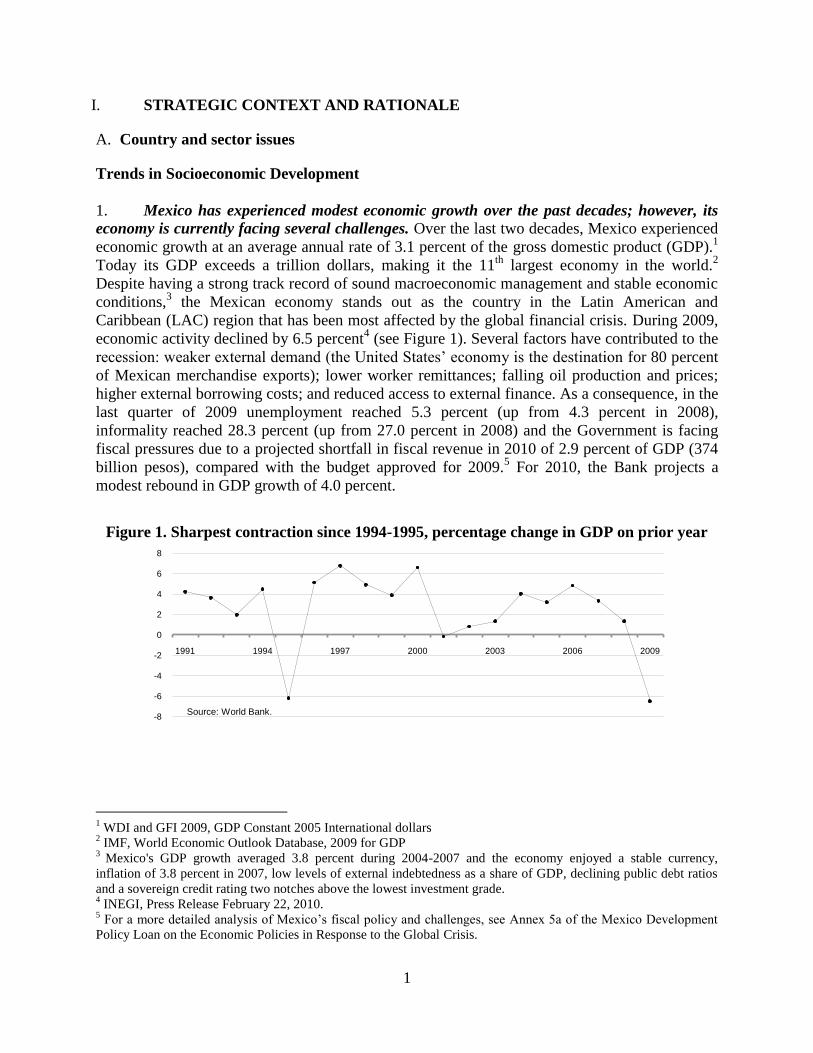

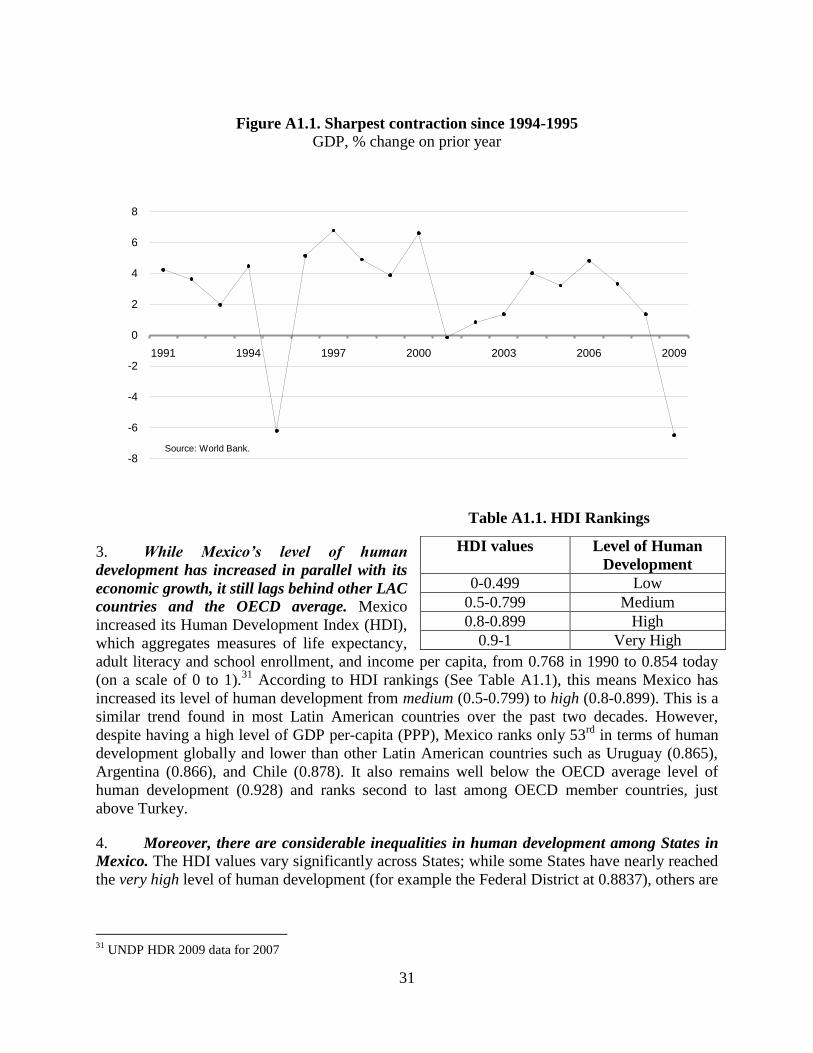

1. Mexico has experienced modest economic growth over the past decades; however, its

economy is currently facing several challenges. Over the last two decades, Mexico experienced

economic growth at an average annual rate of 3.1 percent of the gross domestic product (GDP).1

Today its GDP exceeds a trillion dollars, making it the 11th

largest economy in the world.2

Despite having a strong track record of sound macroeconomic management and stable economic

conditions,3 the Mexican economy stands out as the country in the Latin American and

Caribbean (LAC) region that has been most affected by the global financial crisis. During 2009,

economic activity declined by 6.5 percent4 (see Figure 1). Several factors have contributed to the

recession: weaker external demand (the United States‘ economy is the destination for 80 percent

of Mexican merchandise exports); lower worker remittances; falling oil production and prices;

higher external borrowing costs; and reduced access to external finance. As a consequence, in the

last quarter of 2009 unemployment reached 5.3 percent (up from 4.3 percent in 2008),

informality reached 28.3 percent (up from 27.0 percent in 2008) and the Government is facing

fiscal pressures due to a projected shortfall in fiscal revenue in 2010 of 2.9 percent of GDP (374

billion pesos), compared with the budget approved for 2009.5 For 2010, the Bank projects a

modest rebound in GDP growth of 4.0 percent.

1 WDI and GFI 2009, GDP Constant 2005 International dollars

2 IMF, World Economic Outlook Database, 2009 for GDP

3 Mexico's GDP growth averaged 3.8 percent during 2004-2007 and the economy enjoyed a stable currency,

inflation of 3.8 percent in 2007, low levels of external indebtedness as a share of GDP, declining public debt ratios

and a sovereign credit rating two notches above the lowest investment grade. 4 INEGI, Press Release February 22, 2010.

5 For a more detailed analysis of Mexico‘s fiscal policy and challenges, see Annex 5a of the Mexico Development

Policy Loan on the Economic Policies in Response to the Global Crisis.

-8

-6

-4

-2

0

2

4

6

8

1991 1994 1997 2000 2003 2006 2009

Source: World Bank.

Figure 1. Sharpest contraction since 1994-1995, percentage change in GDP on prior year

2

Table 1. HDI Rankings

2. While Mexico’s level of human

development has increased in parallel with its

economic growth, it still lags behind other LAC

countries and the OECD average, and HDI

values vary significantly across States6. Mexico

increased its Human Development Index (HDI),

which aggregates measures of life expectancy,

adult literacy and school enrollment, and income per capita, from 0.768 in 1990 to 0.854 today

(on a scale of 0 to 1).7 According to HDI rankings (see Table 1), this means Mexico has

increased its level of human development from medium to high. Despite its high level of GDP

per capita (PPP) and improvements in the HDI, however, Mexico ranks only 53rd

in terms of

human development globally and lower than other Latin American countries such as Uruguay

(0.865), Argentina (0.866), and Chile (0.878). It also remains well below the OECD average

level of human development (0.928) and ranks second to last among OECD countries, just above

Turkey. Moreover, there are considerable inequalities in human development among the States in

Mexico. While some States have nearly reached the very high level (for example the Federal

District at 0.8837), others are only at the medium level (for example Chiapas at 0.7185).8

Health Sector Issues

3. Since the 1990s, Mexico has significantly improved its health outcomes and is on track

to achieve the health-related Millennium Development Goals (MDGs), but with increasing

rates of non-communicable diseases, the country is now facing a “dual burden of disease.” As

part of the MDGs, in 2001, countries such as Mexico agreed to improve specific health outcomes

in their population by reducing under-5 child mortality and infant mortality (MDG 4) by two-

thirds and reducing maternal mortality (MDG 5) by three-quarters between 1990 and 2015.

Today, Mexico is one of the few countries in the world that is on track to achieve these Goals.

Between 1990 and 2007, it had reduced under-5 child mortality by over 55 percent and infant

mortality by 62 percent and had nearly halved its maternal mortality rate.9 Likewise, life

expectancy at birth has increased from 71 years to 75 years.10

These continuous achievements

have resulted in what is commonly referred to as a ―dual burden of disease.‖ At the same time as

the extreme poor and other marginalized groups continue to be plagued by high maternal and

child mortality —mainly from infectious diseases and perinatal conditions— an aging population

and unhealthy lifestyles produce a rapidly growing population segment that is increasingly

suffering from non-communicable diseases, such as diabetes and cancer. Today 16 percent of

Mexico‘s burden of disease is due to communicable diseases while 72 percent is due to non-

communicable diseases.11

6 The term ―States‖ refers to the 31 States and the Federal District in Mexico

7 UNDP HDR 2009 data for 2007

8 Values from the Informe sobre Desarollo Humano Mexico 2006-7.

9 UNDP 2009 and World Bank HNP Stats, 1995 and 2007 data.

10 WDI 2009, last figure for 2007.

11 WHO Global Burden of Disease database, estimates for 2004 using age-standardized DALYs, last updated in

February 2009.

HDI values Level of Human

Development

0-0.499 Low

0.5-0.799 Medium

0.8-0.899 High

0.9-1 Very High

3

4. As the HDI data and the dual burden of disease suggest, overall achievements in

health outcomes mask substantial disparities across population groups. These disparities are

closely linked to the level of socioeconomic development. The populations in the Mexican States

that have lower human and economic development, like Chiapas, Guerrero and Oaxaca, suffer

from dramatically higher mortality rates than those in States with higher human and economic

development, like Nuevo León and the Federal District. For example, in 2008, the maternal

mortality rate (maternal deaths per 100,000 live births) was 81.0 in Chiapas, while it was 23.6 in

Nuevo León (see Table 2).

Table 2. Maternal Mortality, HDI and GDP per capita by State, latest available data12

Maternal

Mortality, 2008

HDI, 2007 GDP per capita in

PPP $US, 2004

Chiapas 81.0 0.7185 $3,693

Guerrero 87.2 0.7390 $4,952

Oaxaca 97.3 0.7336 $3,978

Nuevo León 23.6 0.8513 $16,585

Federal District 55.2 0.8837 $23,029

5. In addition to broader socioeconomic determinants, Mexico’s disparities in health

outcomes, including financial protection, are associated with the fragmentation of its health

systems and, more specifically, with the historical underfunding of the public health care

service system for people without contributory social security. The Mexican health system

actually comprises several parallel sub-systems. Each of the three main sub-systems serves a

separate, specified population (as shown in Table 3), with their access being dependent on their

employment status. Two of these are ―contributory‖ social security schemes, meaning that

individuals and their employers each contribute to the cost of several benefits including health

insurance. IMSS covers workers in the formal sector and their dependents. ISSSTE covers public

sector employees and their dependents. The third sub-system, which serves the rest of the

population, is a public health care service system. The boundaries among sub-systems are not

merely administrative. The sub-systems each have their own service networks, and there is little

or no risk-pooling, information-sharing, or portability of benefits among them. These sub-

systems have been drawing on significantly different levels of funding. Between 1995 and 2000,

for the social health insurance systems of IMSS and ISSSTE, spending reached US$270 and

US$330 per capita per year, respectively. By contrast, it was a meager US$52 per capita for the

public health care service system.13

The chronically lower spending on the public health care

service system resulted in lower service quality, 20 percent lower utilization rates and ultimately

poorer health outcomes. For example, in 2000, the maternal mortality rate was nearly three times

as high among those with access only to the public health care service system as among those

with contributory social health insurance (75.8 versus 27.5 deaths per 100,000 live births). In

addition, for those dependent on the public health care service system, the added expenses of

user fees, paying for medicines, and frequent recourse to private services in lieu of low-quality

public service providers resulted in 40 percent higher out-of-pocket expenditures (as a proportion

12

Data for maternal mortality: own estimates based on INEGI/SS: 2000-2007; SEED preliminary 2008; Data for

HDI: UNDP HDR 2009 data for 2007; Data for GDP per capita in PPP $US: World Development Indicators 2006. 13

Parker & John Scott 2008, using a 1.00MXN to 0.205540971 USD exchange rate from January 2000.

4

of disposable household income) compared to beneficiaries of either IMSS or ISSSTE. This

often represented a significant share of the post-subsistence expenditures of poor households.

Table 3. Three Main Sub-systems of the Mexican Health System and their Populations

6. Apart from historically low levels of funding, the public health care service system has

faced persisting challenges of performance management and reform in a highly decentralized

form of federalism. In the 1980‘s and 1990‘s, the Federal Government14

decentralized the

delivery of primary and secondary health care services to States, thus creating 32 State Health

Systems15

. In this process, the Federal Government remained the main source of funding;

however, States were given almost complete autonomy over the use of funds. While the fiscal

coordination law requires the Federal Government and States to enter into annual results

agreements reflecting the priorities set forth in the National Development Plan, this never

became standard practice. Thus, for the time being, performance management arrangements are

only routinely used in federal health programs financed with resources above and beyond the

transfers guaranteed under the fiscal coordination law. Moreover, full implementation of policy

changes and reforms to the regulatory framework governing Mexico‘s public health care service

system requires strong buy-in from the highly autonomous States.

7. Given its historical low levels of funding and substantial performance challenges,

major investments in the public health care services for people lacking contributory social

security have been driving overall improvements in health outcomes. As early as 1973, the

Government set itself the goal of extending and strengthening health care infrastructure to

deprived areas and providing free services to marginalized groups through the program known

today as IMSS-Oportunidades. In 1996, with the Program for Coverage Extension (PAC), the

Secretariat of Health further boosted the geographic coverage of infrastructure within the public

health care service system and introduced a basic package of 34 mainly preventive health

interventions. By 2005, this package covered 89.2 percent of the rural population, with 29.3

percent of the total managed by IMSS-Oportunidades and 73.0 percent by the public health care

service (García Lopez 2009).16

Complementary to these programs, the Government implemented

14

The term ―Federal Government‖ refers to the Government of Mexico 15

The term ―State Health Systems‖ refers to the different administrative units, departments and individuals that

coordinate and administer health services in the 31 Mexican States as well as the Federal District. 16

The two programs overlap 3.2 percent of the total coverage area.

Type of Health

Subsystem Agency Eligible Population

Percent of Total

Population served

Contributory social

health insurance

Mexican Institute for

Social Insurance (IMSS)

Formally-employed private

sector workers and their

dependents

40 percent

Contributory social

health insurance

Institute for Social

Security and Services of

Government Workers

(ISSSTE)

Public sector employees and

their dependents 9 percent

Public health care

service system

Secretariat of Health and

the State Health Systems

All Mexicans, but primarily

the population not covered by

contributory social security

48 percent

5

the conditional cash transfer program Oportunidades, which targets the poor (all of them lacking

contributory social security) and holds its beneficiaries co-responsible for the regular use of

preventive health services (see Annex 1 for more details). Moreover, Mexico made great efforts

to scale up disease-specific programs for communicable diseases, which typically affect the poor

disproportionately; for example, vaccination programs, oral rehydration therapy, micronutrient

supplementation and anti-helminthic therapy (Sepúlveda et al. 2007).

8. To further invest in the health of people without contributory social security and to

reduce their persistently high out-of-pocket expenditures on health care, in 2003 Mexico

decided to transform the public health care service system into a public health insurance

system. Historically, policymakers assumed that inequalities across health subsystems were only

a transitional problem, as they expected the formal labor market to expand and automatically

make more people eligible for contributory social health insurance. However, in Mexico as in

other Latin American countries, this process has stalled. For example, between 1996 and 2006,

coverage of contributory social security stagnated at around 33-34 percent of the total workforce

(see Figure A2 in Annex 1). Drawing on the successful experiences of other countries with non-

contributory health insurance systems (see Table A4.1 in Annex 4), Mexican policymakers

decided to introduce a public health insurance scheme for people lacking contributory social

security, who tend to be mostly poor.

9. The introduction of the public health insurance scheme in 2003 brought three

fundamental changes to the public health care service system:

It replaced budgets with premiums. Prior to the reform, the Federal Government set the

federal budget envelope for the financing of State Health Systems based on expenditures

in the previous year, adjusted for inflation. It determined allocations to States based on the

payroll and infrastructure of each State Health System, with minor adjustments for

mortality rates. These rigid rules perpetuated low levels of funding for the public health

care system, ingrained large funding disparities across the States, and discouraged quality

improvements or innovation. Today, under the public health insurance, the Federal

Government bases the budget envelope and allocations to the States on an actuarially-

calculated premium; that is, a statistically determined payment based on the expected

costs of ensuring, providing, and overseeing a wide range of services and supporting

activities for the enrolled population. In turn, State Health Systems, in their role as the

administrators of the insurance, guarantee health benefits free of charge to those enrolled

in the insurance. The Federal Government finances close to 83 percent of this premium,

with States financing the remaining portion (See Box 2). These rules linked the funding of

State Health Systems to explicitly defined rights of beneficiaries. The rules were expected

to increase the resource envelope of the public health care service system and to reduce

financing disparities across States.

It eliminated user fees but, at the same time, introduced beneficiary contributions. Prior

to the reform, people without contributory social health insurance paid fees to access

health services. While these fees constituted an additional source of revenue for the

system, they created barriers to access health services, were highly regressive and

contributed to the high levels of out-of-pocket expenditures and their impoverishing

effects. Today, under the public health insurance, access to services is free at the time of

use. However, beneficiary households pay an annual contribution that States reinvest in

6

health services or use to build up reserves for the insurance scheme. This contribution is

proportional to each family‘s ability to pay, according to an income assessment. Families

belonging to the two lowest income deciles are exempted from contributing, as are low- or

middle-income families with children younger than five years old.17

The elimination of

user fees combined with the introduction of beneficiary contributions was expected to

increase health service utilization and reduce out-of-pocket expenditures among

beneficiaries. This promotes both inter-temporal risk pooling and consumption smoothing,

two of the chief objectives of a health insurance.

It introduced explicitly defined entitlements. Prior to the reform, the mandate of the

public health care service system was ambiguous. While State Health Systems aimed to

provide all citizens as needed with at least 34 primarily preventive interventions, access to

these and additional services was largely dependent on the availability of financial

resources in each State. Moreover, the system often lacked the resources to ensure service

quality, including the completeness of services. In contrast, the Public Health Insurance

explicitly defines beneficiary entitlements, disclosed in a letter to beneficiary families

along with an insurance policy; introduced an accreditation system for health facilities and

established mechanisms such as patient management, mediation and arbitration systems

that ensure that beneficiary rights are enforced. Along with the increase in resources and

the elimination of user fees, these mechanisms were expected to increase the utilization

and quality of health services and lead to better health outcomes for people without

contributory social security.

10. The public health insurance, named after a first pilot Seguro Popular (Popular Health

Insurance), has been quickly brought to scale. Since 2004, the Popular Health Insurance has

rapidly expanded health insurance coverage to eligible beneficiaries (adding on average

approximately 10 percent of the target population each year and in some years close to the

maximum annual rate of 14.3 percent set forth in the General Health Law) (Knaul et al. 2005).

At the end of 2009, there were more than 31 million individuals enrolled, more than half of the

approximately 48 million total eligible individuals. Likewise, the benefits covered by the Popular

Health Insurance have expanded significantly, from 76 health interventions at its inception to

266 interventions today. Thus, the Popular Health Insurance is the largest health insurance both

in terms of coverage and benefits for people lacking contributory social security in Latin

America (see Table A4.1 in Annex 4).

11. Even without achieving universal coverage, the Popular Health Insurance has already

improved the performance of the publicly-funded health care service system. Since its

inception, the Popular Health Insurance has been subject not only to its own internal control and

auditing systems but also internal and external evaluations (see Annex 3). Most importantly,

these evaluations found that the Popular Health Insurance has resulted in:

Increases in the spending on the health of people without contributory social security;

from, for example, US$52 per capita per year in 2001 to US$154 per capita per year in

17

Article 10 Bis 2 of Chapter 5 of the Guidelines for Affiliation, Operation, Integration of the National Beneficiary

Registry and the Determination of Family Contributions to the Social Protection System in Health States that, at the

time of affiliation, those families with at least on family member that is less than 5 years old and that is in at least

income decile III are exempt from contributing to the system.

7

2004 (González-Pier et al. 2007). This has begun to correct the financing inequalities

across health subsystems and State Health Systems. For example, the ratio of public

expenditures for IMSS compared with those on the publicly-funded health care service

changed from 5:1 to 3:1, and expenditure inequalities across State Health Systems

changed from 5:1 to 4:1.

The effective removal of financial barriers to access health services, resulting in increases

in the utilization of health services (compared with the uninsured), which in turn are

expected to translate into better health over the coming years. For example, the utilization

of health services was significantly higher for Popular Health Insurance beneficiaries

(63.6 percent) compared to the uninsured (58.3 percent) (Gakidou et al. 2006; Bleich et al.

2007; Hernández-Torres et al. 2008).

Reductions in the likelihood of suffering from catastrophic18

and impoverishing health

expenditures (compared with the uninsured). For example, from 2005 to 2006, the Popular

Health Insurance reduced the proportion of those experiencing catastrophic expenditures

by 23 percent (Knaul et al. 2005; King et al. 2009); likewise, the probability of incurring

catastrophic health expenditures was estimated as 8 percent less for households with

Popular Health Insurance affiliates than for uninsured households (Hernández-Torres et al.

2008). In addition, opinion surveys show that Popular Health Insurance beneficiaries are

satisfied with the scheme. More than 95 percent of beneficiaries are ―very satisfied‖ or

―relatively satisfied‖ with the insurance; moreover, 95 percent of health service users are

―very satisfied‖ or ―somewhat satisfied‖ with the health services provided.

12. The Popular Health Insurance constitutes the key pillar of Mexico’s Social Protection

System in Health serving people without contributory social security. It is administered by

State Health Systems. In addition to the Popular Health Insurance, the SPSS includes the Fund

for Protection against Catastrophic Health Expenditures (the Fund), which finances complex,

mostly tertiary health care interventions. Moreover, in 2006 the Federal Government established

the Health Insurance for a New Generation, a federal program, which complements the benefits

of the Popular Health Insurance and finances 116 complex maternal and child health

interventions (for example open-heart surgery for children). The 32 State Health Systems

administer the Popular Health Insurance; while in contrast, the National Commission for Social

Protection in Health (the Commission) and the State Health Systems jointly administer the

Health Insurance for a New Generation and the Commission solely administers the Fund. The

Commission also provides the general oversight for the SPSS.

Current Challenges to the System

13. With seven years of implementation, the Popular Health Insurance has produced

dramatic results for the health and social protection of families without coverage by

contributory social security (see paragraph 11); however, at the same time, it faces some

important challenges. These challenges fall into the broad categories of expanding coverage and

effectively administering the entitlements of the insurance.

18

Catastrophic expenditures are defined as out-of-pocket health expenses greater than 30 percent of post-subsistence

income.

8

14. The current recession calls for an accelerated expansion of Popular Health Insurance

coverage but, at the same time, may hamper it. Policymakers introduced the Popular Health

Insurance with the goal of achieving universal health insurance coverage. They hoped to achieve

this goal by 2010. The current Government reconfirmed the goal of universal health insurance

coverage and, based on earlier affiliation patterns, set the firm target date of 2012. However, the

current crisis calls for an accelerated expansion of the Popular Health Insurance and, at the same

time, poses a threat to the short-term goal of universal coverage. International evidence,

including Mexico‘s experience during the 1994-95 and 2000-01 crises, demonstrates the

importance of securing and, if possible, increasing financial protection in health to safeguard

health gains during downturns. As household income drops, families tend to invest less in their

health. For example, they use health services (and in particular preventive services) less

frequently, and poor and vulnerable households also cut back on food expenditures (A. Ávila &

Shamah Levy 2006). At the same time, however, with informal employment and unemployment

on the rise, fewer people have access to coverage through contributory social security systems,

which means that more people become dependent on subsidized public health insurance or the

public health care service systems. Moreover, fiscal revenues drop, forcing governments to

reduce their spending across social programs, including subsidized public health insurance

schemes and public health care service systems (Gobierno de México 2008).

15. In late 2009, Mexico took a bold step to substantially expand Popular Health

Insurance coverage during the economic crisis. In December of 2009, the Government

proposed and Congress unanimously approved changes to the General Health Law to refine the

premium system. These changes entailed a reduction of the premium level. This reduction

rectified an earlier design shortcoming; that is, a discrepancy between the information on family

size that fed into the original calculation of the premium (4.3 members per family based on

census data) and the actual average size of beneficiary families (3.1 members per family). The

adjustment of the premium level will allow the enrollment of more than 6 million additional

beneficiaries within current State health system budgets. Furthermore, the Federal and State

Governments are committed to create the necessary fiscal space to provide financial protection in

health to all Mexicans by 2012.As a consequence, the Commission will have to shift its focus

from limiting affiliation to the poor and most vulnerable (which prevailed during the early stages

of scaling-up the Popular Health Insurance) to stimulating demand for affiliation across all

eligible population groups, but while maintaining a focus on hard-to-reach groups. The changes

introduced into the General Health Law also entailed the switch from a per-family to a per-capita

premium. The originally adopted per-family premium system discriminated against States with

larger average family sizes, which tend to have less developed health systems and lower health

budgets. Hence, the switch to a per-capita system will help further alleviate the reductions in

financial imbalances resulting from the introduction of the Popular Health Insurance. At the

same time, however, the affiliation of beneficiaries will remain family-based.

16. The second major challenge is to effectively administer the entitlements of the Popular

Health Insurance. Since its inception, the policies of Popular Health Insurance have been geared

toward rapid enrollment. Having overcome many obstacles in this endeavor and moving rapidly

towards universal coverage, policymakers have shifted their attention towards the effective

administration of Popular Health Insurance entitlements. Pursuing this shift, the Commission has

identified three priorities for the coming three years: (i) strengthening performance management

9

while accelerating structural reforms of State Health Systems; (ii) improving beneficiaries‘

awareness of their rights; and (iii) fostering health promotion and disease prevention.

17. The design of the Popular Health Insurance foresees fundamental changes to the

organization and management of State Health Systems, including the development of critical

health insurance functions; yet, the implementation of these reforms has been slower than

anticipated. When health service delivery was decentralized to the States in the 1980‘s and

1990‘s, State Health Systems adopted a vertically-integrated organizational model in which the

functions of oversight (stewardship), financing and service provision were centralized in State

ministries of health. With the introduction of the Popular Health Insurance, the regulatory

framework for the State Health Systems stipulates an organizational separation of these

functions, most importantly, the creation of insurance agencies, so-called Regímenes Estatales de

Protección Social en Salud or REPSS. This separation would pave the way for stronger

accountability mechanisms between the insurance agencies and service providers and new

financing arrangements for service providers. These changes would reap further benefits; most

importantly, the possibility to purchase health services from all existing provider networks

(including the networks of IMSS and ISSSTE), which would in turn enhance access to services,

make the use of existing service infrastructure more efficient, and facilitate the portability of

insurance coverage (across State Health Systems). The above would constitute a major step

towards overcoming the fragmentation of the Mexican health system. To date, all States have

established the REPSS, eighteen have joined forces under the Commission for the Organizational

Restructuring of State Health Systems to further advance the organizational and institutional

reforms, and two have adopted the strategic purchasing of services. Further progress along this

reform path in all States will depend on the effective transfer of knowledge across States as well

as enhanced technical assistance from the Federal Government.

18. As the organizational reform of State Health Systems advances, refined and stronger

performance management arrangements between the Commission and State Health Systems

can enhance the effective administration of the Popular Health Insurance’s entitlements. As

State Health Systems continue to develop and strengthening REPSS, the onus is on the

Commission to establish incentives that promote the efficient delivery of the entitlements and

specifically the benefit package of the Popular Health Insurance. With the exception of the 1.25

percent of the federal solidarity contribution that is dependent on State Health System

performance, financial incentives currently remain geared toward affiliation, not performance

improvements. Furthermore, the regulation of responsibilities remains patchy. This weakness is

compounded by the limited capacity of State Health Systems to comprehensively collect and

analyze service delivery data. Hence, limited information flows from State Health Systems as

well as surveys carried out jointly by the Commission and State Health Systems. Also the

capacity of the Commission to comprehensively corroborate information reported by State

Health Systems requires strengthening. As such, the monitoring of the administration of

entitlements remains incomplete, which hampers an effective performance benchmarking of

State Health Systems. While a worthy goal in itself, an enhanced performance management

arrangement between the Commission and State Health Systems would also goad organizational

and management reforms in State Health Systems.

19. Improving the effective administration of Popular Health Insurance entitlements also

hinges on an improved understanding of these rights by beneficiaries. Entitlements under the

10

Popular Health Insurance (and for families with small children under the Health Insurance for a

New Generation) include a multitude of health care services, which are defined in detail through

protocols and guidelines. While surveys suggest that the beneficiaries of these insurances are

generally satisfied with the health care services they receive, there is evidence that they have

only a limited knowledge of entitlements.19

This impairs the use of preventive services in

particular, since demand for such services depends on households understanding their

importance; that is, health literacy rather than acute health needs. It also undermines efforts to

protect beneficiary rights through patient management, mediation and arbitration systems.

Efforts to improve the understanding of entitlements and more broadly the benefits of insurance

also have to go beyond current beneficiaries. They have to reach out to the broader target

population of the Popular Health Insurance – that is, those without contributory social security –

to ensure that there is sufficient demand for affiliation. These efforts need to reach marginalized

municipalities with large indigenous populations and those living in poverty, which tend to have

far below average educational levels and face other structural barriers to demand affiliation.

20. Effectively administering entitlements will also depend on promoting demand for

health promotion and disease prevention services. Currently, beneficiaries frequently seek care

for curative services. In contrast, demand for interventions that promote health and prevent

diseases—some of the most cost-effective interventions—remains relatively low in Mexico. This

lessens the overall (allocative) efficiency of the system, especially in the context of an increasing

burden of non-communicable diseases. Preventing many non-communicable diseases and their

complications is inexpensive, while treating them is costly (and sometimes impossible). Regular

contacts with the health system for disease prevention and health promotion would also allow the

Commission to establish a comprehensive epidemiological profile of the beneficiary population,

which would further help to comprehensively assess the financial risks facing the system.

B. Rationale for Bank involvement

21. The World Bank Group’s (WBG) Country Partnership Strategy (CPS) for Mexico

(Report No. 42846-MXY March 4, 2008) identified several principles of engagement including

flexibility, fast response, and selectivity driven by the key long term development challenges of

Mexico. The proposed operation demonstrates the Bank‘s flexibility and fast response capacity

to Mexico's changing financing and development needs in the context of the economic crisis. It

is closely aligned with two of the strategic development challenges identified in the CPS:

sustainable growth through investment in human capital and strengthening institutions. Toward

the former, the proposed Project (henceforth the Project) would help to remove barriers to access

health services and would strengthen financial protection for people lacking contributory social

security, mostly poor families. Toward the latter, the proposed Project would help to improve the

organizational and institutional arrangements and, ultimately, the performance of the Popular

Health Insurance.

22. The Mexican Government has requested Bank support in tackling the challenges

facing the Popular Health Insurance. The rationale for its involvement is three-fold. First,

19

This phenomenon is well documented for non-contributory health insurance schemes in the Latin American and

Caribbean region. Possible explanations include the rather short implementation periods of the schemes, moreover,

the generally low educational attainments of its target populations.

11

Bank support would be productive as it would build on two decades of successful experience

supporting the development of Mexico‘s health sector. Since the preparation of the First Basic

Health Care Project in the late 1980s, a series of Bank projects have supported the expansion and

improvement of quality health services, institutional reforms of State Health Systems for the

effective administration of the Popular Health Insurance, and improvements in monitoring

reform progress. In addition, the Influenza Preparation and Control Project, approved by the

Board in November, aims among other objectives to strengthen the national disease surveillance

system. Furthermore, ongoing programmatic analytical and advisory activities assess options to

improve the performance of the Popular Health Insurance and advance its integration with the

contributory social health insurance systems (see Box 1).

23. Second, the Bank has extensive experience in designing, implementing and

strengthening of health insurance programs to expand coverage to the poor, informal worker

families and other vulnerable groups. Globally, the Bank has been supporting more than forty

countries in the introduction and scaling up of non-contributory or subsidized-contributory health

insurance schemes, including in Argentina, the Dominican Republic, Honduras, Panama,

Nicaragua, and Paraguay. These countries have implemented non-contributory health insurance

schemes with the same broad benefits and target populations as the Popular Health Insurance in

Mexico or, for example, the “Plan Nacer” program in Argentina providing limited benefits to

mothers and children.

24. Finally, the Bank is supporting Mexico in strengthening social programs that face

similar challenges and/or contribute to the same goals of the Popular Health Insurance—

most importantly, Mexico’s conditional cash transfer program, Oportunidades—and,

therefore, can facilitate exploiting synergies. The Commission and the management of the

Oportunidades program are working towards a joint strategy with the help of the Bank. A first

successful step in this endeavor was the rapid scale-up of the Popular Health Insurance, which

will eliminate a perverse financial incentive for State Health Systems to give the affiliation of

Oportunidades beneficiaries less priority than they deserve. In addition, there is scope for

significant efficiency gains across the reform priority areas identified for the Popular Health

Insurance. For example, enhanced monitoring of State Health System performance needs to

capture information for Oportunidades beneficiaries and can use Oportunidades databases.

Efforts to empower and educate Popular Health Insurance beneficiaries can use Oportunidades

information and communication platforms. Finally, the Popular Health Insurance will be able to

draw on strategies to promote health and prevent diseases as well as general lessons learned from

the Oportunidades program.

12

Box 1: More than 20 Years of Successful Cooperation in Health System Strengthening

For more than 20 years, Mexico and the Bank have been working jointly to strengthen the

health system and improve health by expanding basic health services to the poor. In 1990, with

the First Basic Health Care Project, the Government requested the Bank support in its efforts to

strengthen the health sector. The First and Second Basic Health Care Projects supported

Government efforts to expand health service coverage to approximately 10 million people in

rural and remote areas, coming close to attaining full geographic coverage. The Third Basic

Health Care Project has further contributed to improving access to quality primary and hospital

care for 22 million poor Mexicans.

Currently the Bank is implementing two health projects that are highly relevant to the current

project: the Third Basic Health Care project and the Influenza Prevention and Control

project. The Third Basic Health Care Project has provided key support to the implementation

and expansion of the SPSS for more than seven years. This experience is essential to the

activities undertaken by the Popular Health Insurance, particularly in the areas of service

delivery and the reform efforts. Furthermore, the project builds on 5 years of programmatic

sector work (analytical and advisory services), examining options for reform of the system‘s

financing as well as functional integration. The Influenza Prevention and Control project aims to

strengthen the national surveillance system responsible for collecting the country‘s

epidemiological data on a regular basis, which is essential for the development of a benefits

package that targets high-frequency, high-cost pathologies in the population and for the better

alignment of Popular Health Insurance‘s benefit package.

The Bank is also carrying out a three-year programmatic analytical and advisory activity in

support of the functional integration of the Mexican health system. While the fragmentation of

the system is not a problem per se; design issues within this approach, such as incentive

incompatibility and a lack of cooperation impede the performance of the health system.

Functional integration aims to overcome these design issues without merging health sector

organizations. The analytical and advisory activity helps to (i) identify priorities among the many

challenges of functional integration, (ii) assess the readiness and facilitate the development of

objectives for functional integration in priority areas, and (iii) support sub-systems in developing

reforms consistent with these objectives.

The Bank also has supported Mexican Government’s efforts to improve the efficiency of

contributory social health insurance programs, IMSS and ISSSTE. When the financial

sustainability of Government insurance programs was threatened in 1998, the Bank worked with

it to design and implement critical policy changes. An adjustment loan combined with a

technical assistance loan supported the Government in developing a sound, long-term strategy to

manage liabilities, introduce user choice and competition, develop purchasing mechanisms and

strengthen health service delivery networks.

13

C. Higher level objectives to which the project contributes

25. The Project would support strategies and objectives outlined in the Government’s

National Health Sector Program (Programa Sectorial de Salud, PROSESA) 2007-2012 and

aligned with the health-related MDGs and the National Development Plan (NDP) 2007-

2012. It would directly support four of the ten strategies outlined in PROSESA: (i) consolidating

the financing reform for effective, universal access to essential health care interventions; (ii)

improving the planning, organization, development and accountability mechanisms of the health

system; (iii) developing systems, technologies and processes that improve the efficiency and

promote the integration of the sector; and (iv) strengthening health promotion and disease

prevention. Furthermore, it would contribute to central objectives of the PROSESA, including

increases in health service utilization and reductions of mortality and out-of-pocket expenditures.

As such, it would help to sustain and accelerate progress towards the health-related MDGs in the

context of the economic crisis, particularly reducing infant and maternal mortality. Likewise, the

Project would contribute to the goals and principles of the NDP; specifically, the goal of creating

equal opportunities and the principle of targeting resources to programs that have demonstrated

their effectiveness in reaching the poor.

II. PROJECT DESCRIPTION

A. Lending instrument

26. The proposed/selected lending instrument is a specific investment loan of US$1,250

million.

B. Project development objective

27. The proposed Project Development Objectives are to (i) initially preserve and later

expand the Popular Health Insurance’s coverage of people without contributory social

security and (ii) strengthen the capacity of the Commission and State Health Systems to

effectively administer the entitlements of the Popular Health Insurance.

C. Project Key Performance Indicators

28. The key performance outcome indicators for the Project are as follows:

Number of individuals affiliated with the Popular Health Insurance as a percentage of the

total number of individuals that are not affiliated with a contributory social security

system.

Number of State Health Systems that collect information on system results (including

beneficiary satisfaction and number, quality and cost of services delivered) that is

validated, widely publicized and used for performance improvement recommendations by

the Commission20

.

20

Information would be made available through State Secretariat of Health internet portal, through the press and/or

radio announcements.

14

Number of individuals affiliated with the Popular Health Insurance who have received a

―Health Risk Screening‖21

as a percentage of the total number of individuals affiliated

with the Popular Health Insurance.

Number of individuals affiliated with the Popular Health Insurance that report having

received enough information to know their rights and obligations as a percentage of the

total number of individuals affiliated with the Popular Health Insurance.

29. The proposed key intermediate outcome indicators for the Project are as follows:

Federal and State expenditure on the Popular Health Insurance (US$ constant exchange

rate (2009)).

Number of State Health Systems that collect information on system results (including

beneficiary satisfaction and number, quality and cost of services delivered) that is

validated by the Commission.

Health risk management program guidelines have been designed and rolled out.

Number of individuals affiliated with the Popular Health Insurance who report having

received a bill of rights and responsibilities at the time of affiliation as a percentage of the

total number of individuals affiliated with the Popular Health Insurance.

Expected Outcomes

30. The Project is expected to contribute to the extension of health insurance coverage and

the effective administration of entitlements and to produce four major outcomes. First, the

Popular Health Insurance coverage of people without contributory health insurance would be

gradually expanded from 31.1 million (64 percent) to 41.1 million (85 percent). Second, the

Commission would have ramped up its activities to capture, benchmark, and widely disseminate

information on the service delivery of the State Health Systems as well as to issue

recommendations to improve performance. Third, the percentage of Popular Health Insurance

beneficiaries who consider the information provided to them about their rights under the Popular

Health Insurance as adequate is expected to increase from 71 to 80 percent. Finally, 10 million

Popular Health Insurance beneficiaries would have received a health risk screening.

D. Project components

31. The Project would consist of two components. Component I would finance eligible

federal ―social contributions‖ (see Box 2) to the premium of the Popular Health Insurance to

initially preserve and later expand the Popular Health Insurance‘s coverage of people without

contributory social security. Across the globe, Bank projects have started to co-finance insurance

and in particular health insurance premiums. The proposed Project would be a logical extension

of this practice insofar that it would finance the insurance premium of the developing world‘s

largest (both in terms of population and benefits) and highly scrutinized health insurance for

people without contributory social security. Component II would finance technical assistance to

strengthen the capacity of the Commission and State Health Systems to effectively administer

the entitlements of the Popular Health Insurance, including technical assistance for enhanced

performance management and support to States in preparing and carrying out reforms in the

administration of the Popular Health Insurance, improved knowledge of eligible beneficiaries

21

Health Risk Screening is an integral part of the Health Risk Management Program.

15

about entitlements, strengthened health risk management, and effective project coordination and

management.

Component I: Popular Health Insurance’s Coverage of People without Contributory Social

Security (US$1,239 million)

32. Financing of eligible federal social contributions to the premium of the Popular

Health Insurance to initially preserve and later expand the Popular Health Insurance’s

coverage of Eligible Beneficiaries. Specifically, component I would finance the share of the

federal social contributions earmarked for financing the Popular Health Insurance premium (i.e.

the share of one of the contributions made by the federal government to such premium) as

referred to in Article 77 of the General Health Law (for details on the financing of the premium

see Box 2 and Annex 4).

Box 2. Financing of the Popular Health Insurance

The SPSS*, including the premium of the Popular Health Insurance, is financed by the Federal

and State governments. The specific arrangements mimic the tripartite funding model of

Mexico‘s contributory social security systems (which combine employer, employee, and

Government contributions). The Federal Government makes two contributions: the social

contribution (cuota social) and the federal solidarity contribution (aportación solidaria

federal). States make their own contribution called the state solidarity contribution (aportación

solidaria estatal).

The General Health Law establishes the premium of the Popular Health Insurance as a fixed

share of all three federal and State contributions (currently 89 percen; the remaining 11 percent

finance the Fund for Catastrophic Health Expenditures as well as trust funds for infrastructure

investments and reserves). Moreover, the law sets forth the relative magnitude of the

contributions and, thus, the share of Federal and State government financing. With the federally-

financed social contribution serving as the reference point, the federal solidarity contribution is

set at 150 percent of the social contribution and the state solidarity contribution at 50 percent the

amount of the social contribution. Thus, the combined federal financing is five-sixths of the

premium compared to the State financing of one-sixth of the premium. Analogous to Mexico‘s

social security system, the General Health Law provides for a dynamic adjustment of the

premium by linking the social contribution to the minimum general salary of the Federal District.

Per labor law, the minimum general salary of the Federal District is annually adjusted for

consumer price inflation, which in the case of Mexico and other Latin American countries

corresponds well with health inflation (World Bank, forthcoming). Recent changes to the

General Health Law recalibrated the social contribution and reduced it from 4.84 to 3.92 percent

of the minimum general salary of the Federal District.

An actuarial system annually assesses the financial sustainability of the Popular Health

Insurance. More specifically, it assesses the financial impact of uncertainty and risks using

statistical probabilities for a large variety of variables, including, for example, health needs,

treatment seeking behaviors and cost structures. As in last year‘s case, the identification of

significant mismatches between the premium, reserves and insurance risks should prompt

adjustments to the premium (and possibly to the insurance benefits as well).

16

The SPSS also provides for a beneficiary contribution that is set as a progressive proportion of

household income. In general, it is the responsibility of the States to collect the beneficiary

contribution. Under federal rules and supervision, State Health Systems can use these funds to

invest into service delivery improvements of their provider networks.

* This includes the Popular Health Insurance, the Fund for Catastrophic Health Expenditures and several Trust

Funds. The Health Insurance for a New Generation is financed separately and exclusively from federal

contributions.

Component II: Capacity of the Commission and of State Health Systems to Administer the

Popular Health Insurance Entitlements (US$7.875 million)

Financing of technical assistance to the Commission and to State Health Systems to (i)

support enhancements in performance management in the administration of the Popular

Health Insurance, and (ii) support State Health Systems in preparing and carrying out

reforms in the administration of the Popular Health Insurance; said technical assistance to

include, inter alia, the review and refinement of the federal monitoring and audit system,

(including Coordination Agreements), assessments of the capacity of State Health

Systems to monitor the delivery of health services to different groups of beneficiaries

(including vulnerable groups), the development of instruments to capture and validate

information, the development of performance benchmarks, the design of a disclosure

policy for the Popular Health Insurance, the development of platforms to transfer

experiences and knowledge across State Health Systems, and the development of

financing mechanisms for technical assistance to State Health Systems to effectively carry

out key health system functions, specially, their responsibilities as the administrators of

the Popular Health Insurance.

Figure 2. Financing Flows of the Popular Health Insurance Premium

17

Financing of technical assistance to the Commission and to State Health Systems to

improve the knowledge of Eligible Beneficiaries about their entitlements under the

Popular Health Insurance; said technical assistance to include, inter alia, the design of a

communication strategy with a focus on vulnerable groups, consultations with

stakeholders, the development of communication tools, implementation support to State

Health Systems, including training and supervision of the implementation of said

communication strategy, the evaluation of communication pilots as well as evaluation of

said communication pilots and communication strategy, including the review and

development of surveys, data collection and data analysis.

Financing of technical assistance to the Commission and to State Health Systems to

strengthen their capacity to manage health risks; said technical assistance to include, inter

alia, the design of a health risk management program, consultations with stakeholders,

training and implementation support to State Health Systems, including the supervision of

the implementation of said health risk management program, the evaluation of health risk

management pilots and said health risk management program, including the design of

surveys, data collection, and data analysis.

Financing of technical assistance to allow the Commission coordinate and manage the

Project; said technical assistance to include, inter alia, the training of staff in fiduciary and

safeguard matters, the carrying out of annual external audits, and the carrying out of the

activities included in the Indigenous Peoples Plan (IPP).

E. Lessons learned and reflected in the project design

33. A number of lessons have been gleaned from the Bank’s experience in Mexico during

the past two decades as well as from the implementation of similar projects around the world. Several of these lessons informed the selection of the lending instrument, the identification of

risks and the design of the risk mitigation measures; these lessons are discussed in the

corresponding sections of this document. In addition, two essential lessons have been

incorporated into the design of the Project: the need for comprehensive incentive and support

systems to foster reform in highly decentralized contexts, and the importance of empowering

beneficiaries of insurance systems serving the poor and vulnerable.

34. In highly decentralized systems, for comprehensive health sector reforms to be

implemented successfully at the local level (which can take as long as two decades), the

central authority must develop incentive and support systems to help local agencies to

implement the reforms. The Bank‘s experience in the Dominican Republic, Hungary,

Germany, and many other countries around the globe suggest that legislative reform is just the

beginning of the reform process. Therefore, Component II would support the Commission in

developing a comprehensive incentive and support system to enhance the performance of State

Health Systems and drive the pace of reform. This system would combine good practices from

countries such as Argentina, China, Indonesia, Poland, and Turkey, including closer monitoring,

the publicizing of the results of this monitoring, setting benchmarks, making financing

conditional on results, creating platforms for the exchange of experiences and innovations, and

building capacity. Even with such incentives and support, the experience of Mexico itself as well

as that of other countries suggests that reforms take a long time to implement in very

18

decentralized health systems. Therefore, the Project‘s targets are ambitious but realistic and have

been drawn from the experiences of the Mexico Third Basic Health Care Project.

35. The introduction of health insurance can yield major improvements in the

performance of a health system, but the full potential impact will only be realized if

beneficiaries are empowered. Health insurance systems for the poor and other vulnerable

groups have been emerging in many developing countries over the past two decades and have

increasingly become a focus of the Bank‘s support to the health sector. This focus of the Bank‘s

reflects its recognition that, if properly designed and implemented, health insurance can yield

significant improvements in health system performance, including making the system more

accountable, bringing it higher levels of funding, making it more efficient, increasing people‘s

awareness of their health, empowering them and giving them more choice among providers,

increasing consumer satisfaction, widening financial protection, and improving health outcomes.

While the positive impact of health insurance in terms of increasing the use of health services