The Future of EVs in the U.S. - Home - Transport Energy ...

18

The Future of EVs in the U.S. A Base Case Projection to 2040 August 2019 Monthly Report Tammy Klein Principal [email protected] / +1.703.625.1072 (M) / futurefuelstrategies.com

Transcript of The Future of EVs in the U.S. - Home - Transport Energy ...

The Future of EVs in the U.S. A Base Case Projection to 2040

August 2019 Monthly Report

Tammy Klein Principal

[email protected] / +1.703.625.1072 (M) / futurefuelstrategies.com

Key Points in This Report: • My view is that EVs will remain a small part of overall

vehicle sales through 2040, representing 10% of all newsales that will be largely BEVs with small numbers ofhybrids, FCEVs and PHEVs. Most of these sales will bein California and the Section 177 states; ZEV programtargets will not be met by 2025.

• Other projections assume a policy future that I find verycircumspect and not based in our present political andpolicy reality: super stringent federal fuel economystandards, car bans, federal ZEV targets, etc. and ageneral strong commitment to battling transport-relatedair pollution and climate change. This is the case in theEU and China, but not in the U.S. where the currentAdministration is focused on a deregulatory pathway.

• To facilitate high sales of EVs in 2040 requires strongpolicy frameworks that need to be put into place now orover the next few years, and that will most likely nothappen.

• Many analyses miss a critical (and unfortunate) reality:most Americans are not doing well financially now. Theysimply cannot afford an EV, and this trend is likely tostay in place through at least the end of the 2020s andbeyond.

Introduction This report, continuing the summer's focus on electric vehicles (EVs), ends with a first: my own projection for EV sales in the U.S. through 2040. I will do the same for the EU and China in the coming months. In summary, my view is that EVs will remain a small part of overall vehicle sales through 2040, representing 10% of all new sales that will be largely BEVs with small numbers of hybrids, FCEVs and PHEVs. My EV estimate is lower for several reasons that will be explored in more depth in this report. First, and in summary, there is no strong federal policy commitment and push for these vehicles, as is happening in China and the EU. I expect this to remain the case until at least 2021and perhaps longer. California, through its ZEV program, and the Section 177 states1 will largely continue to lead on setting favorable policies for EV uptake and other states already offer different types of incentives that favor EVs.2 Cities across the U.S. are taking a range of actions on EVs as well as noted in recent posts.3 (See posts Aug. 8, 2019 and July 23, 2019) But the smattering of state and local policies are not likely to be enough to really push

1 Section 177 is a reference to a section of the Clean Air Act that essentially allows under certain conditions, states to follow California regulations. The states in this case are Connecticut, Delaware, Maine, Maryland, Massachusetts, New Jersey, New York, Oregon, Pennsylvania, Rhode Island, Vermont, Washington. These are generally the states with the highest level of EV penetration in the U.S.

2 See e.g. National Conference of State Legislatures, "State Efforts To Promote Hybrid and Electric Vehicles," Sept. 26, 2017 available at http://www.ncsl.org/research/energy/state-electric-vehicle-incentives-state-chart.aspx#additional.

3 These kinds of policies range from fleet-related (procurement, charging infrastructure), parking benefits, to including EV chargers in revised building codes, to charging infrastructure incentives. See also, Slowik and Lutsey, ICCT," The Continued Transition to Electric Vehicles in U.S. Cities," July 2018 available at https://www.theicct.org/publications/continued-EV-transition-us-cities-2018. "Nine of the top 10 major metropolitan areas with the highest electric vehicle uptake offered consumer incentives typically worth $2,000 to $5,000. Consumers in California markets, Denver, and Seattle have benefited from substantial purchase incentives. Counterexamples with the removal of such incentives and/or imposition of electric vehicle fees (e.g., Atlanta, Detroit, Indianapolis, Memphis, Nashville, Salt Lake City) stand out as rare markets with declining 2017 electric vehicle uptake."

2

uptake to the levels projected in many EV studies.

The 10% projection is based on other factors discussed in this report, including:

• The current political situation and potential outcome of the U.S. presidential election;• The fact that there is no strong national vision in place or even being contemplated which will have

ripple effects for years;• The demographics of U.S. consumers. Many simply cannot afford EVs at the current price threshold,

but I show that even when prices decline, many still will not be able to afford them.

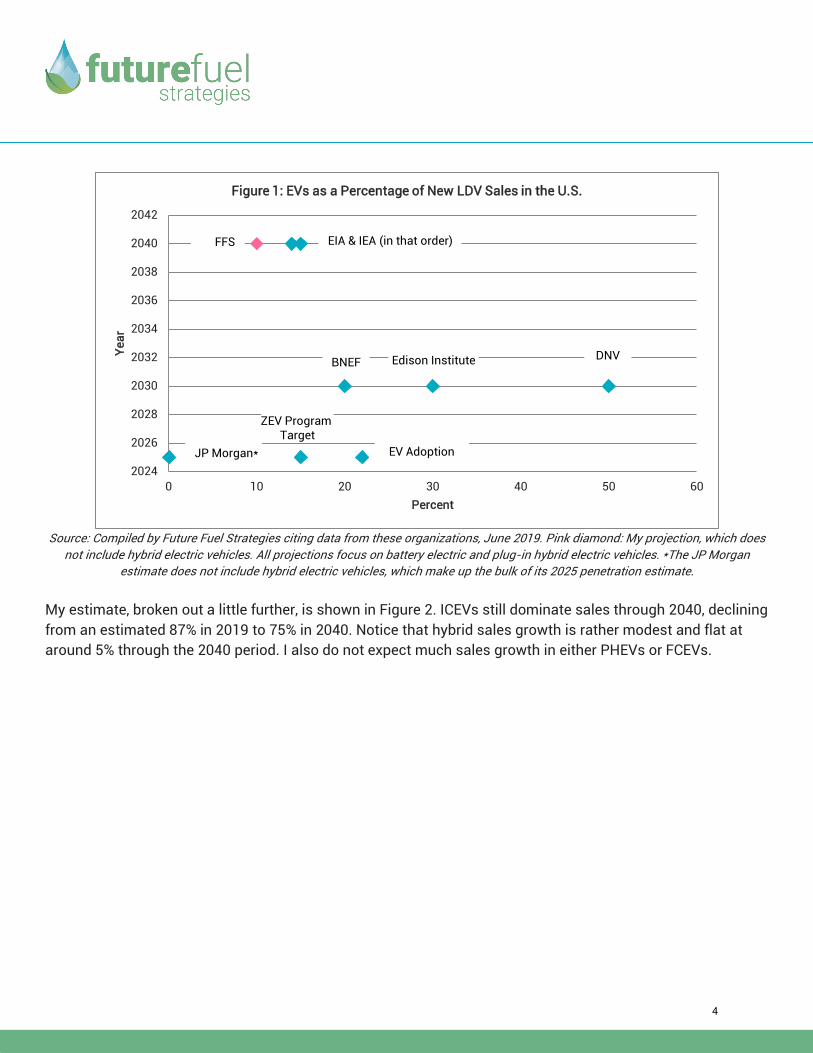

My Projection: EV Sales in the U.S. through 2040 I project that EVs will remain a small part of overall vehicle sales through 2040, estimating 10% of all new sales will be largely battery electric (BEV) and some plug-in hybrid electric vehicles (PHEVs) by 2040. Accepting the U.S. Energy Information Administration (EIA's) light-duty vehicle (LDV) sales numbers for 2040 at a little over 16 million, that would mean sales of about 1.6 million EVs in 2040.4 As Figure 1 shows, my estimate is the most conservative of analyses shown for the U.S. just under EIA's (14% by 2040) and IEA's New Policies Scenario (15% by 2040), but not by that much.5 I expect that the bulk6 of EV sales will be in California as per its Zero Emission Vehicle (ZEV) program and the Section 177 states following that program. My 2040 projection assumes by extension that the 15.4% sales target under the ZEV program put into place by California will not be met in 2025 and would be delayed significantly. I also assume the bulk of sales will be BEV, not PHEV.

4 Energy Information Administration, Annual Energy Outlook 2019, available at https://www.eia.gov/outlooks/aeo/.

5 MIT Professor John Heywood estimates 15% by 2050, to provide additional perspective. Norman Meyersohn, New York Times, "The Internal Combustion Engine Is Not Dead Yet," Aug. 17, 2017 at https://www.nytimes.com/2017/08/17/automobiles/wheels/internal-combustion-engine.html.

6 Two-thirds of ZEVs are sold in California now. See Nicholas Lutsey, et al., ICCT, "Quantifying the Electric Vehicle Charging Infrastructure Gap Across U.S. Markets," January 2019 available at https://www.theicct.org/sites/default/files/publications/US_charging_Gap_20190124.pdf (hereinafter "ICCT EV Charging").

3

Source: Compiled by Future Fuel Strategies citing data from these organizations, June 2019. Pink diamond: My projection, which does not include hybrid electric vehicles. All projections focus on battery electric and plug-in hybrid electric vehicles. *The JP Morgan

estimate does not include hybrid electric vehicles, which make up the bulk of its 2025 penetration estimate.

My estimate, broken out a little further, is shown in Figure 2. ICEVs still dominate sales through 2040, declining from an estimated 87% in 2019 to 75% in 2040. Notice that hybrid sales growth is rather modest and flat at around 5% through the 2040 period. I also do not expect much sales growth in either PHEVs or FCEVs.

2024

2026

2028

2030

2032

2034

2036

2038

2040

2042

0 10 20 30 40 50 60

Year

Percent

Figure 1: EVs as a Percentage of New LDV Sales in the U.S.

JP Morgan*

EIA & IEA (in that order)

DNV

EV Adoption

FFS

ZEV Program Target

BNEF Edison Institute

4

Figure 2: Klein Outlook for EVs as a Percentage of New LDV Sales 2019-2040

Source: Future Fuel Strategies with base data from U.S. EIA, August 2019 Note: "Other" is generally diesel, natural gas LDVs, E85 FFVs and small sales of hydrogen fuel-cell vehicles.

Reducing air pollution and greenhouse gas (GHG) emissions in line with Paris Agreement goals are primary policy drivers in other countries/regions such as China and the EU. By contrast, neither policy driver is a priority for the current Administration or for most consumers.7 The EU, for example, is strongly focused on decarbonization. The U.S., by contrast, is currently focused on deregulation. Every EV analysis featured for comparison appears to bank on strong national policies to drive the market such as stringent fuel economy standards, car bans, ZEV mandates, tax incentives and infrastructure targets. But, with the exception of the ZEV tax credit, there are no such federal policy drivers at this time.8 This could certainly change post 2021 or 2026, but the lack of policy commitment and strong national vision now will have ripple effects reaching into the 2030s and beyond, especially as people are holding on to their vehicles for longer periods of time and the legacy fleet continues to age. Other studies do not appear to account for this effect.

7 The same in not true in the EU and China, where many cities are experiencing poor air quality related to mobile source emissions, especially NOx and PM.

8 For example, IEA notes in its World Energy Outlook that "[EV] shares are lower in regions lacking a strong policy push and with relatively low taxes on fuel and consumer preferences for bigger cars. In the United States and Middle East, the market of electric cars reaches around 15% and around 1% by 2040, respectively."

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2019 2020 2025 2030 2035 2040

Gasoline BEV Hybrid PHEV Other

5

In fact, these analyses appear to completely ignore the political, policy and demographic/consumer realities that are happening right now in the U.S.9 For example, consider this quote from a recent National Renewable Energy Laboratory (NREL) report:

"Continued advancements in battery technologies help lower electric vehicle costs while smart vehicle charging complements friendly electricity rate structures and low electricity rates. A large network of public, workplace, and/or utility-owned charging stations reduces range anxiety while fast and efficient charging technologies (e.g., induction-based, DC-based, and catenary technologies) reduce inconveniences, even for longer trips or larger vehicles. Optimal smart routing and urban planning further reduce infrastructure needs and costs. With favorable economics for PEVs, fleet managers—for passenger and freight services—can implement a rapid turnover. Expansion of car-sharing services, perhaps enabled by automation, would enhance this fleet impact. Vehicle manufacturers follow these trends and develop and market a diverse set of model options serving nearly all consumer preferences for design, convenience, and performance. A combination of local, state, and federal policies—such as air pollution standards, efficiency standards, and gasoline taxes—lead to economic incentives and/or mandates for PEVs. Furthermore, drivers recognize or perceive the possible noise, acceleration, and convenience benefits of electric vehicles leading to greater adoption."10

There are some huge assumptions here across the board, but particularly with respect to policy and consumer acceptance and uptake. In the subsections that follow, I present a qualitative analysis that supports the 10% projection and is connected with the present political, policy and demographic realities in the U.S.

Political Reality: Republicans May Retain the Presidency and the Senate

In the June report on national EV policies, I made the point that the current presidential political situation in the U.S. will be the single largest determinant of the EV market over the next 10 years. I said that "If President Trump wins another term, all bets are off: a pathway toward dismantling and deregulation that impacts the fuels/vehicles markets generally and EVs critically will continue until 2025-2026." Another strong determinant will be the conservative make up of the U.S. Supreme Court, set in 2018 with the controversial appointment of Justice Brett Kavanaugh. Will such a court strike down:

9 The JP Morgan analyst Michael Cembalest notes, "Forecasters are now jockeying for position with geometric projections. However, the transition to EVs is likely to be gradual, once again confounding the expectations of futurists... [Past EV forecasts are] still useful as a reminder that many forecasters vote with their hearts instead of their minds, and often don’t incorporate real-life barriers to product displacement. Cars are not smartphones: they have higher upfront and ongoing maintenance costs, complex supply chains, refueling requirements and higher standards for performance and safety. The EV revolution is now upon us, but the important question for investors is the pace. The median forecast is ~125 million EVs by 2030; I’m taking the 'under' rather than the 'over'."

10 Mai, Trieu, Paige Jadun, Jeffrey Logan, Colin McMillan, Matteo Muratori, Daniel Steinberg, Laura Vimmerstedt, Ryan Jones, Benjamin Haley, and Brent Nelson. 2018. Electrification Futures Study: Scenarios of Electric Technology Adoption and Power Consumption for the United States. Golden, CO: National Renewable Energy Laboratory. NREL/TP-6A20-71500. https://www.nrel.gov/docs/fy18osti/71500.pdf. To be fair, the authors caution that their work is not a projection or prediction. However, they do estimate a low, medium and high EV sales projection case for 2050. Low=10%, medium=60% and high=90%.

6

• Future progressive fuel economy policies?• California's ability to set its own fuel economy or other fuel/vehicle policies?• Future climate change policies (e.g. carbon tax) that may drive the EV market?• Progressive electrification policies (ZEV mandates and targets)?• Cities' abilities to diverge from state and federal policy setting in the area of transport?

To really see significant uptake of EVs in the U.S. (or any) LDV market the way some analysts predict in Figure 1, a national vision or policies really have to be set now. Such policies need to be comprehensive, such as what Norway has done (see post Apr. 4, 2019). China is another example through its NEV program. I see no such pathway for the U.S. right now.

With respect to the presidential race, I believe it is possible that the president could win another term. Right now Republicans hold 219 of 270 electoral votes from secure states that Democrats will be unlikely to flip.11 President Trump (or potentially another Republican) could also pick up red-leaning states such as Florida and Arizona in 2020, bringing the total to 259. At this point, he would need to win some combination of Wisconsin (10 votes), Michigan (16 votes) and/or Pennsylvania (20 votes) to reach 270. Notably, much of Michigan and Pennsylvania voted Republican in the 2018 elections. The path for Democrats is challenging.

What's more, policies that Congress could enact to better lay the groundwork for a robust EV market in the 2020s and beyond will not likely be supported by Republicans and thus are not expected to materialize until 2025 (or even after). The bottom line is that the political situation now does matter in assessing future EV sales and penetration in the 2040 time period. By and large, Republicans are not supportive of the kinds of policies it will take to create a robust EV market, discussed in the next section.

EV analyses appear to ignore our present political reality as if there is no connection from the present to the future (in this case, 2040). Not only do those analyses ignore the present political reality, but they assume there will be some other kind of alternate reality where a robust Congress takes far-reaching, visionary and bipartisan public policy actions to tackle thorny issues such as energy and climate change. However, and perhaps unfortunately, Congress has taken no such visionary legislative action in years. For example, the last comprehensive energy legislation was enacted in 2007 (the Energy Independence and Security Act (EISA)).12

In any event, assume the most progressive political scenario: a progressive Democrat takes the White House in 2021and 2025 and there is sustained Democratic control of both chambers of Congress through much of the 2020s. The Congress enacts a "New Green Deal" and/or other progressive legislation that would impose a national ZEV mandate, super stringent fuel economy standards, additional consumer incentives for EVs, a

11 270 to Win, "2020 President: Consensus Electoral Map," Mar. 9, 2019, available at https://www.270towin.com/maps/consensus-2020-electoral-map-forecast.

12 And, I could argue EISA was hardly visionary.

7

carbon tax or other similar scheme, internal combustion engine (ICEV) bans/limitations or other sorts of fuel-limiting measures to promote EVs. These kinds of measures would most likely be stricken down13 by the conservative majority in the Supreme Court.14 Even "outside deals" the federal government could reach in the future with the auto industry where they would voluntarily comply with ZEV or ICEV requirements, similar to the deal just struck between the state of California and Honda, BMW, Volkswagen and Ford, could be subject to challenge.

Policy Reality: Supportive Policies Will Most Likely Not Materialize Until 2030 (Or Beyond)

Fuel Economy Standards Delayed

If Trump (or another Republican) wins in 2020, it is my view the fuel economy standards contemplated under the Obama Administration are not going to be implemented ― at least not until the post-2025 timeframe ― if ever at all. The previous and proposed revised standards proposed under the Safer Affordable Fuel-Efficient (SAFE) Vehicles Rule for Model Years 2021-2026 Passenger Cars and Light Trucks will be tied up in litigation between California and the federal government for years. I do not believe the Trump Administration will succeed in litigation to revoke the state's waiver15, but they may well succeed in the effort to set a lesser standard and its argument in the draft SAFE rulemaking respecting consumer preferences is a strong one.

Litigation and setting a lesser standard will hamper EV development because parity with ICEVs will be delayed. This is a huge assumption other organizations rely on in doing their forecasts: ICEVs will become more

13 It would not be difficult to find constitutional grounds upon which to challenge these kinds of progressive laws/regulations.

14 See e.g., Matt Ford, New Republic, "Would the Green New Deal Survive the Supreme Court?, Mar. 18, 2019 at https://newrepublic.com/article/153334/green-new-deal-survive-supreme-court. "Kavanaugh also appears set to take part in a mini-revolution on the court that could have far-reaching effects. Most of the EPA’s regulatory power comes from its interpretation of broad statutes like the Clean Air Act and the Clean Water Act. When federal courts interpret how agencies implement acts of Congress, they typically use what’s known as Chevron deference, so named for a 1980s case involving the oil giant. Generally speaking, the Chevron doctrine instructs judges to defer to a federal agency’s interpretation of federal law when deciding whether the agency is exceeding its authority under that law. Over the past 30 years, Chevron deference evolved into a pillar of federal administrative law. It’s also recently become a target of ire among conservative legal scholars, who partially blame it for expanding the federal government’s regulatory powers. Justice Neil Gorsuch, a frequent critic of the doctrine, tilted the court’s balance on the subject when he replaced Scalia, who generally accepted it. Kavanaugh does not go quite as far as Gorsuch in his critiques, but his rulings and academic writings strongly suggest he’d vote to narrow the doctrine if given the opportunity. That could constrain Green New Deal–related regulations if the justices read the legislation more narrowly than the EPA staff does."

15 I do not believe the Administration has a strong justification for revoking the California waiver. First, there is nothing in the relevant law that gives EPA the authority to revoke. It can either grant or deny a waiver, not revoke. Second, there is a strong reliance interest at stake here. This means that the California Air Resources Board (CARB), the auto industry and other stakeholders relied upon the original waiver and developed a whole regulatory regime as a result. To revoke now after five-six years will not be well received in federal courts. Third, the Administration tries to use another statute, the Energy Policy and Conservation Act of 1975 (EPCA) to argue that this preempts California's ability to set its own standards under the Clean Air Act (CAA). However, this is not a correct interpretation of the CAA and EPCA.

8

expensive than EVs because of stringent fuel economy policies and that ultimately will push consumers toward EVs. Notably, analyses such as BNEF's16, IEA's and JP Morgan's assume parity will be reached in the 2020s because of these standards and also declining battery prices. But with respect to fuel economy, if standards are not tightened sufficiently, a major lever for EV (including hybrids) commercialization disappears.

By comparison, I do see EV uptake increasing in the EU (see report July 11, 2019) and China, driven in part by very stringent fuel economy standards agreed by the EU institutions in 2018 and in China because of its New Energy Vehicle policy. But it will not happen in the U.S. for a number of years. If we assume (1) option 1 or 2 under the SAFE rule are put into place (2) they survive legal challenge by California (3) a Republican retains the White House in 2021, which I noted above is a very real possibility, the earliest a new Administration could even propose a new, more stringent regulation would be 2026, assuming that it is even a political priority for the incoming Administration (either Republican or Democrat). The proposal to implementation process, if we assume no litigation, would be about three to four years, so 2029 or 2030. Litigation would further delay fuel economy standard setting, and could push back standards another five years at the very least, 2034-2035.

No National ZEV Mandate

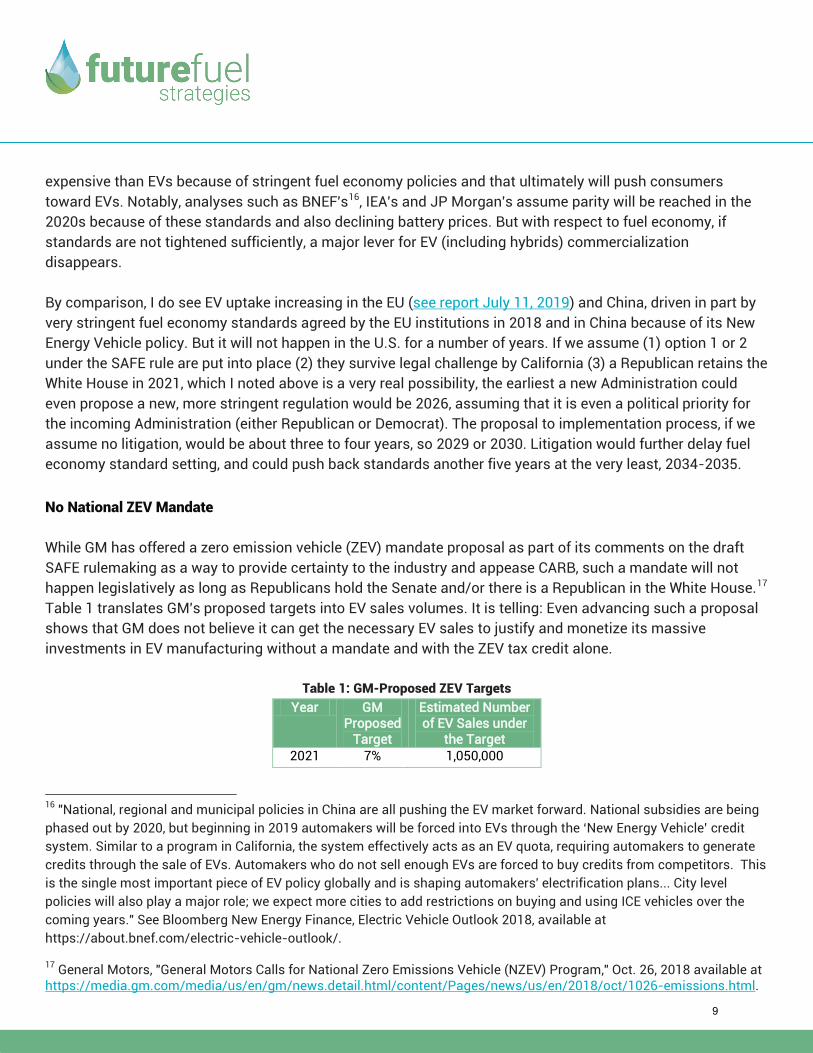

While GM has offered a zero emission vehicle (ZEV) mandate proposal as part of its comments on the draft SAFE rulemaking as a way to provide certainty to the industry and appease CARB, such a mandate will not happen legislatively as long as Republicans hold the Senate and/or there is a Republican in the White House.17 Table 1 translates GM's proposed targets into EV sales volumes. It is telling: Even advancing such a proposal shows that GM does not believe it can get the necessary EV sales to justify and monetize its massive investments in EV manufacturing without a mandate and with the ZEV tax credit alone.

Table 1: GM-Proposed ZEV Targets Year GM

Proposed Target

Estimated Number of EV Sales under

the Target 2021 7% 1,050,000

16 "National, regional and municipal policies in China are all pushing the EV market forward. National subsidies are being phased out by 2020, but beginning in 2019 automakers will be forced into EVs through the ‘New Energy Vehicle’ credit system. Similar to a program in California, the system effectively acts as an EV quota, requiring automakers to generate credits through the sale of EVs. Automakers who do not sell enough EVs are forced to buy credits from competitors. This is the single most important piece of EV policy globally and is shaping automakers' electrification plans... City level policies will also play a major role; we expect more cities to add restrictions on buying and using ICE vehicles over the coming years." See Bloomberg New Energy Finance, Electric Vehicle Outlook 2018, available at https://about.bnef.com/electric-vehicle-outlook/.

17 General Motors, "General Motors Calls for National Zero Emissions Vehicle (NZEV) Program," Oct. 26, 2018 available at https://media.gm.com/media/us/en/gm/news.detail.html/content/Pages/news/us/en/2018/oct/1026-emissions.html.

9

Year GM Proposed

Target

Estimated Number of EV Sales under

the Target 2022 9% 1,350,000 2023 11% 1,650,000 2024 13% 1,950,000 2025 15% 2,250,000 2030 25% 3,750,000

Source: Compiled by Future Fuel Strategies citing data from General Motors. *Estimate based on average sales of 15 million a year from EIA Annual Energy Outlook projections.

ZEV Tax Credit Caps Could Be Raised

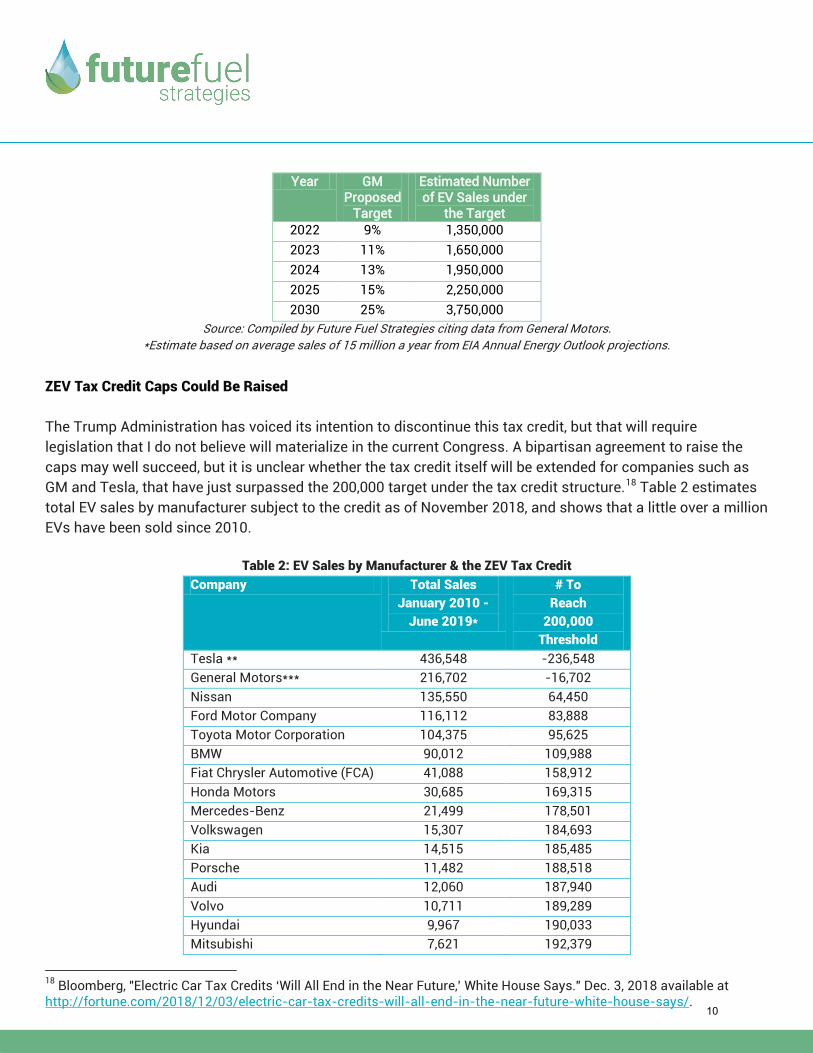

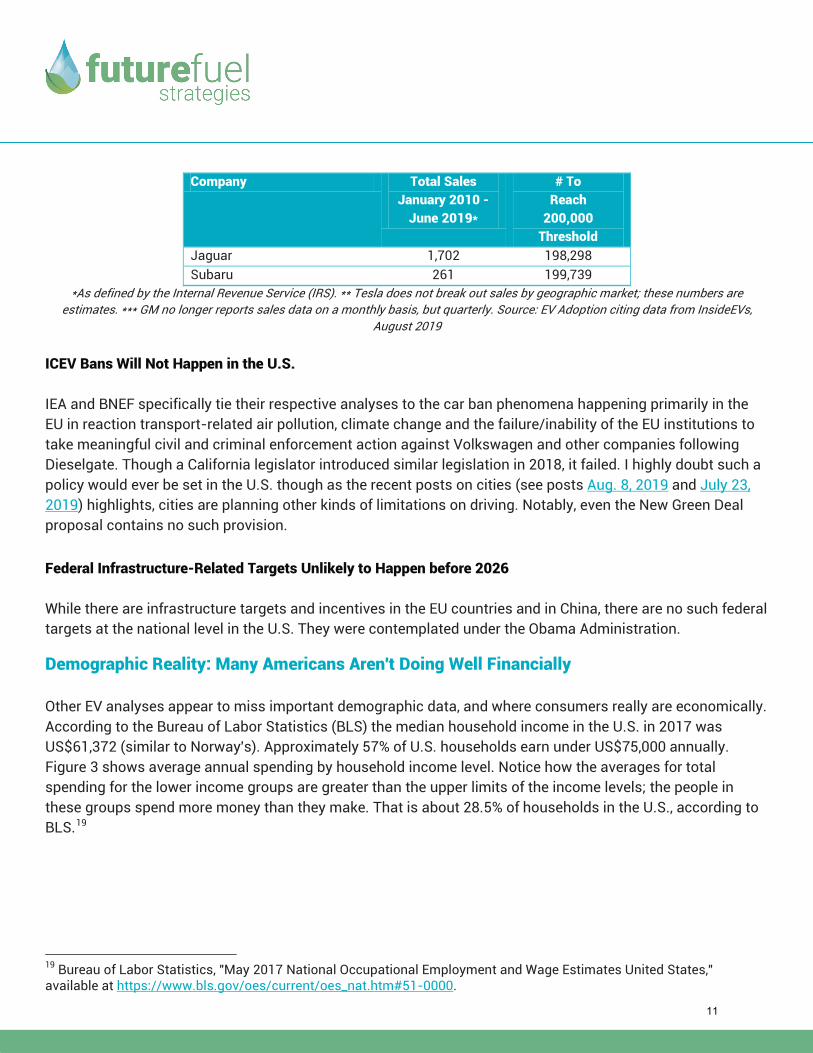

The Trump Administration has voiced its intention to discontinue this tax credit, but that will require legislation that I do not believe will materialize in the current Congress. A bipartisan agreement to raise the caps may well succeed, but it is unclear whether the tax credit itself will be extended for companies such as GM and Tesla, that have just surpassed the 200,000 target under the tax credit structure.18 Table 2 estimates total EV sales by manufacturer subject to the credit as of November 2018, and shows that a little over a million EVs have been sold since 2010.

Table 2: EV Sales by Manufacturer & the ZEV Tax Credit Company Total Sales

January 2010 -June 2019*

# To Reach

200,000 Threshold

Tesla ** 436,548 -236,548General Motors*** 216,702 -16,702Nissan 135,550 64,450 Ford Motor Company 116,112 83,888 Toyota Motor Corporation 104,375 95,625 BMW 90,012 109,988 Fiat Chrysler Automotive (FCA) 41,088 158,912 Honda Motors 30,685 169,315 Mercedes-Benz 21,499 178,501 Volkswagen 15,307 184,693 Kia 14,515 185,485 Porsche 11,482 188,518 Audi 12,060 187,940 Volvo 10,711 189,289 Hyundai 9,967 190,033 Mitsubishi 7,621 192,379

18 Bloomberg, "Electric Car Tax Credits ‘Will All End in the Near Future,’ White House Says." Dec. 3, 2018 available at http://fortune.com/2018/12/03/electric-car-tax-credits-will-all-end-in-the-near-future-white-house-says/.

10

Company Total Sales January 2010 -

June 2019*

# To Reach

200,000 Threshold

Jaguar 1,702 198,298 Subaru 261 199,739 *As defined by the Internal Revenue Service (IRS). ** Tesla does not break out sales by geographic market; these numbers are

estimates. *** GM no longer reports sales data on a monthly basis, but quarterly. Source: EV Adoption citing data from InsideEVs, August 2019

ICEV Bans Will Not Happen in the U.S.

IEA and BNEF specifically tie their respective analyses to the car ban phenomena happening primarily in the EU in reaction transport-related air pollution, climate change and the failure/inability of the EU institutions to take meaningful civil and criminal enforcement action against Volkswagen and other companies following Dieselgate. Though a California legislator introduced similar legislation in 2018, it failed. I highly doubt such a policy would ever be set in the U.S. though as the recent posts on cities (see posts Aug. 8, 2019 and July 23, 2019) highlights, cities are planning other kinds of limitations on driving. Notably, even the New Green Deal proposal contains no such provision.

Federal Infrastructure-Related Targets Unlikely to Happen before 2026

While there are infrastructure targets and incentives in the EU countries and in China, there are no such federal targets at the national level in the U.S. They were contemplated under the Obama Administration.

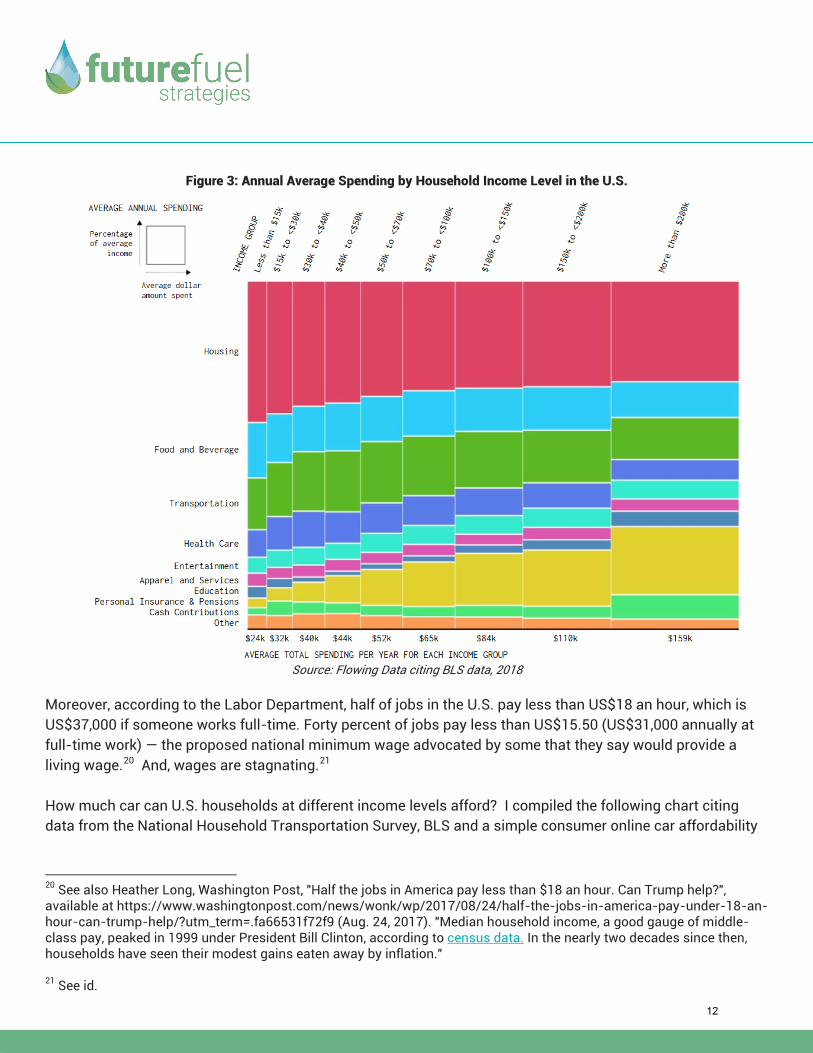

Demographic Reality: Many Americans Aren't Doing Well Financially

Other EV analyses appear to miss important demographic data, and where consumers really are economically. According to the Bureau of Labor Statistics (BLS) the median household income in the U.S. in 2017 was US$61,372 (similar to Norway's). Approximately 57% of U.S. households earn under US$75,000 annually. Figure 3 shows average annual spending by household income level. Notice how the averages for total spending for the lower income groups are greater than the upper limits of the income levels; the people in these groups spend more money than they make. That is about 28.5% of households in the U.S., according to BLS.19

19 Bureau of Labor Statistics, "May 2017 National Occupational Employment and Wage Estimates United States," available at https://www.bls.gov/oes/current/oes_nat.htm#51-0000.

11

Figure 3: Annual Average Spending by Household Income Level in the U.S.

Source: Flowing Data citing BLS data, 2018

Moreover, according to the Labor Department, half of jobs in the U.S. pay less than US$18 an hour, which is US$37,000 if someone works full-time. Forty percent of jobs pay less than US$15.50 (US$31,000 annually at full-time work) ― the proposed national minimum wage advocated by some that they say would provide a living wage.20 And, wages are stagnating.21

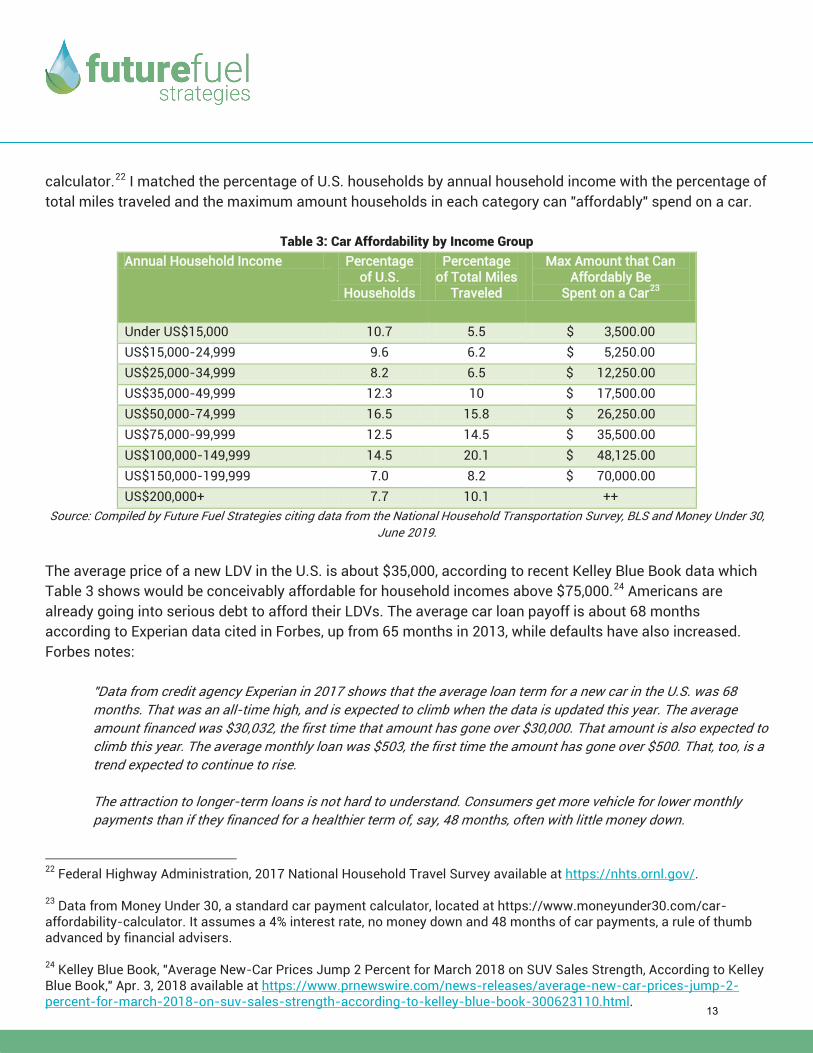

How much car can U.S. households at different income levels afford? I compiled the following chart citing data from the National Household Transportation Survey, BLS and a simple consumer online car affordability

20 See also Heather Long, Washington Post, "Half the jobs in America pay less than $18 an hour. Can Trump help?", available at https://www.washingtonpost.com/news/wonk/wp/2017/08/24/half-the-jobs-in-america-pay-under-18-an-hour-can-trump-help/?utm_term=.fa66531f72f9 (Aug. 24, 2017). "Median household income, a good gauge of middle-class pay, peaked in 1999 under President Bill Clinton, according to census data. In the nearly two decades since then, households have seen their modest gains eaten away by inflation."

21 See id.

12

calculator.22 I matched the percentage of U.S. households by annual household income with the percentage of total miles traveled and the maximum amount households in each category can "affordably" spend on a car.

Table 3: Car Affordability by Income Group Annual Household Income Percentage

of U.S. Households

Percentage of Total Miles

Traveled

Max Amount that Can Affordably Be

Spent on a Car23

Under US$15,000 10.7 5.5 $ 3,500.00 US$15,000-24,999 9.6 6.2 $ 5,250.00 US$25,000-34,999 8.2 6.5 $ 12,250.00 US$35,000-49,999 12.3 10 $ 17,500.00 US$50,000-74,999 16.5 15.8 $ 26,250.00 US$75,000-99,999 12.5 14.5 $ 35,500.00 US$100,000-149,999 14.5 20.1 $ 48,125.00 US$150,000-199,999 7.0 8.2 $ 70,000.00 US$200,000+ 7.7 10.1 ++

Source: Compiled by Future Fuel Strategies citing data from the National Household Transportation Survey, BLS and Money Under 30, June 2019.

The average price of a new LDV in the U.S. is about $35,000, according to recent Kelley Blue Book data which Table 3 shows would be conceivably affordable for household incomes above $75,000.24 Americans are already going into serious debt to afford their LDVs. The average car loan payoff is about 68 months according to Experian data cited in Forbes, up from 65 months in 2013, while defaults have also increased. Forbes notes:

"Data from credit agency Experian in 2017 shows that the average loan term for a new car in the U.S. was 68 months. That was an all-time high, and is expected to climb when the data is updated this year. The average amount financed was $30,032, the first time that amount has gone over $30,000. That amount is also expected to climb this year. The average monthly loan was $503, the first time the amount has gone over $500. That, too, is a trend expected to continue to rise.

The attraction to longer-term loans is not hard to understand. Consumers get more vehicle for lower monthly payments than if they financed for a healthier term of, say, 48 months, often with little money down.

22 Federal Highway Administration, 2017 National Household Travel Survey available at https://nhts.ornl.gov/.

23 Data from Money Under 30, a standard car payment calculator, located at https://www.moneyunder30.com/car-affordability-calculator. It assumes a 4% interest rate, no money down and 48 months of car payments, a rule of thumb advanced by financial advisers.

24 Kelley Blue Book, "Average New-Car Prices Jump 2 Percent for March 2018 on SUV Sales Strength, According to Kelley Blue Book," Apr. 3, 2018 available at https://www.prnewswire.com/news-releases/average-new-car-prices-jump-2-percent-for-march-2018-on-suv-sales-strength-according-to-kelley-blue-book-300623110.html.

13

A key economic trend influencing the longer loan terms is wage stagnation in the U.S. and the ever increasing cost of the average-priced car. And as consumers follow their wants for SUVs and crossovers, typically more expensive than sedans they used to buy, they want what they want in a new vehicle–damn the cost."25

By comparison, the average price of an electric vehicle (BEV/PHEV) is over US$50,000, according to data from the EV enthusiast site evrater.26 According to a survey of 22,000 EV owners by PlugInsights, 45% of EV buyers who bought long-range EVs (Teslas and the Chevy Bolt) make more than US$200,000 a year.27 Nearly all of these vehicles are small compact cars or sedans with an range just over 200 miles.

Figure 4 shows that most of the EVs that will be introduced in the next few years will be over US$60,000, though several such as the Rivian, Porsche, two Kia models and Volvo (the three yellow dots that are obscured in the chart) will be small cross-over vehicles (CUVs). The two Kia models (Kia Soul and Niro) and the Volvo XC40 are all small CUVs28 prices at around US$40,000.29 These prices are pre-tax credit. But by and large, it will be more affluent households purchasing these vehicles for the foreseeable future ― into the 2020s and beyond. The reality is that they are the only group that both want and can afford them.30

25 David Kiley, Forbes, "Average New Vehicle Cost is $36,000+ And Loan Delinquencies Are Up," May 30, 2018 available at https://www.forbes.com/sites/davidkiley5/2018/05/30/average-new-vehicle-cost-is-36000-and-loan-delinquencies-are-up/#6cb0c8991e84.

26 evrater, "The Electric Vehicle List," available at https://evrater.com/evs.

27 Bradley Berman, InsideEVs, "The Biggest Challenge Facing Electric Cars Is Still Affordability," Jan. 22, 2019 available at https://insideevs.com/electric-cars-affordability/ (hereinafter Berman). Data presented by CARB has shown that it is affluent households that are purchasing EVs in California. See Tammy Klein, Guess Who's Buying ZEVs in California, Future Fuel Strategies, Sept. 13, 2017 available at http://futurefuelstrategies.com/2017/09/13/socioeconomics-drive-zev-purchases-california.

28 Electric CUV sales will be key to watch to monitor how mainstream the EV market is becoming in the U.S.

29 A friend from ARPA-E said to me recently, "Car companies and others keep saying that the cost of these EVs will go down as battery prices decline. But battery prices have declined ― a lot. And the vehicles are not that much cheaper though there are more of them. Have you noticed that?" Battery prices have declined 75% between 2010-2016. See Claire Curry, “Lithium-ion Battery Costs and Market: Squeezed margins seek technology improvements & new business models,” Bloomberg New Energy Finance, 2017, available at https://data.bloomberglp.com/bnef/sites/14/2017/07/BNEF-Lithium-ion-battery-costs-and-market.pdf.

30 Even VW CEO Hans Dieter Pötsch admitted as much. "The current price level cannot stay the same if these cars are equipped with electric motors. Therefore, it will inevitably lead to significant price increases in the small car segment...[as a result EVs could remain] unaffordable for people on low incomes.” See Berman at footnote 24. Navigant has projected the price of EVs will remain constant for the next five years.

14

Figure 4: Current and Future U.S. EV Model Prices v. Range

Source: evrater, 2019

The foregoing analysis shows that many Americans are buying bigger LDVs that they can't afford already at an average price of US$35,000. EVs at the current average price of US$50,000 are simply out of reach for 84% of households (if we accept the data in Table 3), even with a tax credit. With the tax credit, EVs are only within reach for the six-figure income bracket and above, but not the other 69% of households. These are the primary buyers of EVs in the U.S. right now. If prices were to come down to the US$35,000 level as promised by Tesla with its Model 3 and other EV manufacturers, still only 43% of households could afford them.31 The ZEV tax credit may help. But still, producing a wide range of vehicles, particularly cross-over utility vehicles (CUVs) that are priced at the US$35,000 level will take years to happen, most likely the mid to late 2020s.32 This would also assume consumers would want to buy something like an EV CUV instead of an ICEV CUV.

31 See Alex Beyman, Medium, "What Good is the Electric Car if Nobody Can Afford It? Cheap Electric Cars on the Horizon," Nov. 23, 2018 available at https://medium.com/predict/what-good-is-the-electric-car-if-nobody-can-afford-it-cheap-electric-cars-on-the-horizon-a90c540dc355. "I don’t mean upcoming big name electric cars like the Bolt, which offer 200 mile range at around $30,000 after subsidy. That is not really affordable for most people. I know almost nobody who has ever bought a brand new car for example. Many seemingly well to do Americans can’t even afford an unexpected $500 expense. A $30,000 car is out of the question for them." Beyman makes the case in this article for microEVs, but I can't see how these vehicles would ever meet stringent federal safety standards or more importantly, that they would be acceptable for most American drivers.

32 See id. at 14. See also McKinsey & Company, "Electrifying insights: How Automakers Can Drive Electrified Vehicle Sales and Profitability," January 2017 available online here. "Current projections put EV battery pack prices below $190/kWh by the end of the decade, and suggest the potential for pack prices to fall below $100/kWh by 2030. Lower costs for battery packs could potentially bring base versions of the Chevy Bolt below $30,000, and base versions of the Tesla Model 3 below $40,000 after the $7,500 federal tax subsidy is applied. However, the unsubsidized price of these EVs is still above the average price of around $35,000 for a new vehicle purchase in the U.S."

15

That will take years to happen, at least in the mid to late 2020s, and even then a wide swath of the public would not be able to afford these vehicles, even if they wanted them. This is the demographic reality that these analyses are missing. They focus on the total cost of ownership (TCO) and how much lower that will be with an EV than an ICEV. However, this is not how consumers make purchasing decisions.33

One other fact to point out: the households that can only afford a US$35,000 priced or less vehicle also represent 59% of all vehicle miles traveled (VMT) in the U.S. So these households not only would have to have an EV that best fits their lifestyle at a price they could conceivably afford (or be willing to go into debt for) but would need the maximum range and charging speed (at least Level 2 or DC) as well because they are driving the most. Notice that the two highest income levels at US$150,000 and above in Table 2 represents 18% of VMT.

Conclusion What would it take to achieve a 40% sales penetration by 2040, more in line with other analysts? In contrast to my base case, there would have to be:

• Strong Federal Policy Vision and Regulatory Certainty: What I mean is that there may be a policy orsuite of policies the federal government may promulgate to promote EV uptake (e.g. New Green Deal,ZEV mandate, infrastructure support, continued/expanded consumer incentives, stringent fueleconomy, raising gas taxes, etc.) that will either have to be carefully crafted to avoid legal challenge(e.g. perhaps the incentives) or such policies would be litigated and settled in favor of the progressivepolicy in question. Increasing the caps under the existing EV incentive program and expanding the taxcredit to support lower-income buyers (below US$75,000 in annual income) could be two policies thatcould have a significant impact and potentially avoid legal challenge. It would also send a clear andcertain signal to the auto industry.

The federal government could also step in to more actively promote infrastructure development:workplace, public and even home charging for consumers. It could potentially avoid the minefield of anational ZEV mandate, fuel economy setting and even overarching climate legislation in favor of thesekinds of targeted interventions. But to do this, there would either need to be bipartisan agreement atthe executive and legislative branch level, or one party would have to control both branches. Anotheroption would be to sidestep the legislative process altogether and cut a deal with the auto industry onissue such as fuel economy and ZEVs as we saw in 2012 in the Obama Administration and this month

33 For a great visualization, see Jeff Desjardins, "Visualizing Household Income Distribution in the U.S. by State," Nov. 6, 2017 available at https://www.visualcapitalist.com/household-income-distribution-u-s-state/.

16

with the California Air Resources Board (CARB) and the four automakers.34 Such a deal could still be challenged on various legal grounds and may not withstand judicial scrutiny.

• Strong State Support: In addition to the federal government, the EV-supportive states (generallyCalifornia and the Section 177 states) would have to maintain their respective ZEV mandate/EVprograms and potentially increase their financial support to consumers as well. They will also need tofocus on expand charging infrastructure, particularly in and around cities.

• Mainstream Consumers Actually Want EVs: The auto industry follows through on its promises toproduce more affordable EVs in a range of different models, including CUV and SUVs, by 2025-2030.And, mainstream (non-coastal affluent) consumers will want to buy these vehicles, especially withfederal and some state subsidies offered. Whether battery prices decline or not, or whether there is trueparity with ICEVs, automakers may price EVs competitively anyway through the 2020s and into the2030s to create and grow the market. Once the inflection point occurs where EVs become cheaper thanICEVs (around 2030), they may back off such a strategy. This also means that enough consumersovercome another key objection to EVs in addition to price: range anxiety. This could be possible withrange expected to increase in future models and with battery improvements. The expansion ofinfrastructure will help.

• The Role of Cities: While cities are not able to, by and large, offer subsidies to consumers, they can doother things to help encourage EVs that are meaningful (see posts Aug. 8, 2019 and July 23, 2019).This includes priority or preferential parking, HOV lane access and installing free public and workplacecharging. These measures seem small, but recall that one of the major drivers for the development ofNorway's market are these kinds of measures coupled with the NOx/GHG vehicle pricing scheme.Similar types of measures in EU cities and in China are helping to drive EV uptake. If cities take furtheractions to limit ICEVs, such as Los Angeles' proposed future "fossil-free zone" or even congestionmitigation pricing that applies to ICEVs but not EVs, that could help spur the market as well.

There are two key questions here in my view:

• Can an EV market develop in the absence of a strong national vision and without strong policies,signals and certainty?

• In this absence, will U.S. consumers find their way to EVs over traditional ICEVs?

My view on the first question is that it has not been done to date. Every county with any degree of EV penetration currently has a suite of policies in place to support uptake. It may be possible to develop an EV market without any supportive policies, but my guess (in line with my base case) is that the uptake would begin slowly. Real EV sales penetration would not begin until the mid-2030s. This would be consistent with

34 See e.g. Eric D. Lawrence, USA Today, "Ford, VW, BMW, Honda Reach Emissions Deal with California, Bucking Rollback," July 25, 2019 at https://www.usatoday.com/story/money/cars/2019/07/25/ford-vw-honda-bmw-emissions-deal-california/1827079001/.

17

the introduction of other new vehicle technologies over time, such as anti-lock brakes or power steering. Several auto industry representatives have reminded me that it takes at least 20 years, maybe more, to gain consumer acceptance and the tipping point where we see integration of new technologies into the vehicle market. If we mark 2010 as the start date, the first year that EVs were reintroduced on a mass scale, that would mean 2030 as the year when EVs begin to gain more mass acceptance in the U.S. consumer market. The uptake would begin slowly and real penetration would not begin until after 2035-2040, in line with my base case analysis. Notably, the year 2030 could be a pivotal year for other reasons such as the introduction of more efficient, cheaper, resilient batteries that deliver better performance and range for EVs. (See post Mar. 25, 2019)

Along with federal policy and consumer movements toward or away from EVs, another key guidepost to watch is the auto industry. What will it do if the tax incentive stays in place as it is or is even removed? And what if there is no other federal support policy or vision for EVs? The industry is spending a conservative US$400 billion on EV investments in the next few years alone. Much of that is targeted to the China market, but some is directed to the EU and the U.S. as well. The U.S. is a huge potential market for them. Will it take other actions to ensure the market grows in the U.S.? What would that look like? Options could be favorable pricing and incentives to consumers for their vehicles, installing infrastructure (home and public), free service, upgraded features in the vehicles, among the potential actions it could take.

18