Tax Matters August 16 2006 · 2018-04-04 · ¾ New Mexico Taxation & Revenue Department Proposes...

17

Tax Matters The Newsletter of the New Mexico Tax Research Institute Issue No. 2006-9 August 16, 2006 New Mexico Tax Research Institute 505-797-6667 P.O. Box 91657 [email protected] Albuquerque, New Mexico 87199-1657 www.nmtri.org Views expressed in this publication are those of the editorial staff unless otherwise indicated. They do not necessarily reflect the views of any member or members of the New Mexico Tax Research Institute. Nothing in this publication is intended to be nor should be constued as offering tax advice. No tax planning decision should be made without consulting your professional tax advisor. All rights reserved. No material in this publication may be reproduced or redistributed without the express written permission of the New Mexico Tax Research Institute. © 2006 NMTRI IN THIS ISSUE OF TAX MATTERS: New Mexico Taxation & Revenue Department Proposes Royalty Income Settlement. New Mexico Tax & Revenue Department Suggests Law Changes. NMTRI Hosts Discussion of Business Activity Tax Simplification Act. Where Does New Mexico Rank? Does It Matter? Voting for Dollars in Arizona? Whatchmacallit in Texas? New Office Location for NMTRI. Coming Attractions! New Mexico Taxation & Revenue Department Proposes Settlement re Intangible Property Royalty Income. The New Mexico Taxation and Revenue Department has apparently just concluded a window of opportunity for an industry-wide settlement concerning the taxation of companies having income from licensing intangible property to related entities operating in New Mexico. The settlement proposal is a result of the recent decision in Kmart Corporation v. Taxation and Revenue Department of the State of New Mexico, N.M. S. Ct., Dkt. No. 27,269, 12/29/2005, reported in the December 2005 issue of Tax Matters. Attorney Bruce Fort coordinated the negotiations for the Department. A document outlining the settlement will be posted on the NMTRI website, www.nmtri.org .

Transcript of Tax Matters August 16 2006 · 2018-04-04 · ¾ New Mexico Taxation & Revenue Department Proposes...

Tax Matters The Newsletter of the New Mexico Tax Research Institute

Issue No. 2006-9 August 16, 2006

New Mexico Tax Research Institute 505-797-6667 P.O. Box 91657 [email protected] Albuquerque, New Mexico 87199-1657 www.nmtri.org Views expressed in this publication are those of the editorial staff unless otherwise indicated. They do not necessarily reflect the views of any member or members of the New Mexico Tax Research Institute. Nothing in this publication is intended to be nor should be constued as offering tax advice. No tax planning decision should be made without consulting your professional tax advisor. All rights reserved. No material in this publication may be reproduced or redistributed without the express written permission of the New Mexico Tax Research Institute.

© 2006 NMTRI

IN THIS ISSUE OF TAX MATTERS:

New Mexico Taxation & Revenue Department Proposes Royalty Income Settlement. New Mexico Tax & Revenue Department Suggests Law Changes. NMTRI Hosts Discussion of Business Activity Tax Simplification Act. Where Does New Mexico Rank? Does It Matter? Voting for Dollars in Arizona? Whatchmacallit in Texas? New Office Location for NMTRI. Coming Attractions!

New Mexico Taxation & Revenue Department Proposes Settlement re Intangible Property Royalty Income. The New Mexico Taxation and Revenue Department has apparently just concluded a window of opportunity for an industry-wide settlement concerning the taxation of companies having income from licensing intangible property to related entities operating in New Mexico. The settlement proposal is a result of the recent decision in Kmart Corporation v. Taxation and Revenue Department of the State of New Mexico, N.M. S. Ct., Dkt. No. 27,269, 12/29/2005, reported in the December 2005 issue of Tax Matters. Attorney Bruce Fort coordinated the negotiations for the Department. A document outlining the settlement will be posted on the NMTRI website, www.nmtri.org.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

2

New Mexico Taxation & Revenue Department Suggests Law Changes. The NMTRD presented a list of legislative suggestions to the New Mexico Legislature Revenue Stabilization and Tax

Policy Interim Committee at its meeting in Deming in July. See our earlier report in the August 3 issue of Tax Matters. The full list is below. NMTRD is said to be still working on some of these recommendations and may have changes or additions to the list. The Committee had several questions about some of the items and NMTRD representatives promised more information at subsequent meetings of the Committee. If any NMTRI members have questions about these suggested changes, please contact the NMTRI office.

NM Taxation and Revenue Department

Proposed Legislation, July 28, 2006 1. Technical Corrections

Statute Affected

Legislative Proposal

Purpose of Change

7-1-4

Technical Corrections to Section 7-1-4 The technical correction is to Subsection E to recognize that the secretary of Taxation and Revenue Department issues the administrative subpoena pursuant to Section 7-1-4. This proposal was introduced during the 2006 session as HB 828. Location of HB 828: [11]nt prntd-HRC API

The purpose of Subsection E of Section 7-1-4 is to toll, or suspend, the running of the statute of limitations in the event that a taxpayer filed an action in court to quash an administrative subpoena that was issued pursuant to Section 7-1-4. Section 7-1-4E, as passed in 2005, refers to a “…. subpoena or summons issued by that court pursuant to this section….”. Section 7-1-4E should read, “…. subpoena or summons issued by the secretary or the court pursuant to this section….”, since a subpoena or summons issued pursuant to Section 7-1-4 is issued by the Secretary.

7-2-5.8

Apportionment of Exemptions vs. Apportionment of Tax 1) This proposal would amend Section 7-2-5.8 to remove the apportionment language in Subsection A. 2) This change would delete Subsection E relating to the definition of “federal extension”.

1) Currently, Section 7-2-11 allows for the apportionment of tax when a taxpayer has income from New Mexico and non-New Mexico sources. It is not necessary to have this additional language in the statute. 2) The removal of this language will eliminate challenges to the exemption on constitutionality grounds.

7-2C-5

Allow corporate income tax intercepts A technical correction is needed to implement provisions of HB 478 and SB 226 from the 2006 Session. The change will add the Corporate Income and Franchise Tax Act to the language in section 7-2C-5 permitting the Department to intercept tax refunds.

HB 478/SB 226 authorized the Department to intercept corporate income tax refunds to offset worker’s compensation fee payments that are due. The bills failed to make a “tracking” change in Section 7-2C-5 to permit the Department to intercept corporate income tax refunds.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

3

Statute Affected

Legislative Proposal

Purpose of Change

9-11-4

Reconcile Multiple Amendments to Section 9-11-4 (Laws 2005) During the 2005 Legislative Session Section 9-11-4 was amended by HB-411 and HB-747. This proposal would simply reconcile the two amendments and assist with the implementation of the Legislature’s intent.

Reconciling will clarify the Legislature’s intent and make it clear that the Tax Fraud Division is an official division of the Taxation and Revenue Department.

2. Tax Administrative Act Provisions

Statute Affected

Legislative Proposal

Purpose of Change

7-1-2

Tax Credits Under the Tax Administration Act This proposal would list all tax credits, including the Film Tax Credits, under the Tax Administration Act.

This proposal would clarify that the various tax credits administered by the Taxation and Revenue Department are governed by the Tax Administration Act. This will provide consistency in administration of the various tax credits and will ensure that taxpayer information related to these credits is covered by the confidentiality statute (Section 7-1-8).

3. Tri-Agency Portal Provisions

Statute Affected

Legislative Proposal

Purpose of Change

New 7-3-2 7-3-12

Tri-Agency Information and Penalties 1) Require employers, payors, withholders and pass-through entities that do not have a Department of Labor (DOL) filing requirement to file an informational return with the Taxation and Revenue Department (TRD) on a quarterly basis. Failure to file the informational return would result in a penalty. 2) Require that all employers with more than fifty employees file electronically. This proposal would also establish a penalty for failure to do so. NOTE: The TRD legislation will also include language from Department of Labor legislative proposals.

These proposals will ensure that all three agencies (TRD, DOL and Worker’s Comp Administration) receive identical information from filers.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

4

4. Processing Provisions

Statute Affected

Legislative Proposal

Purpose of Change

New

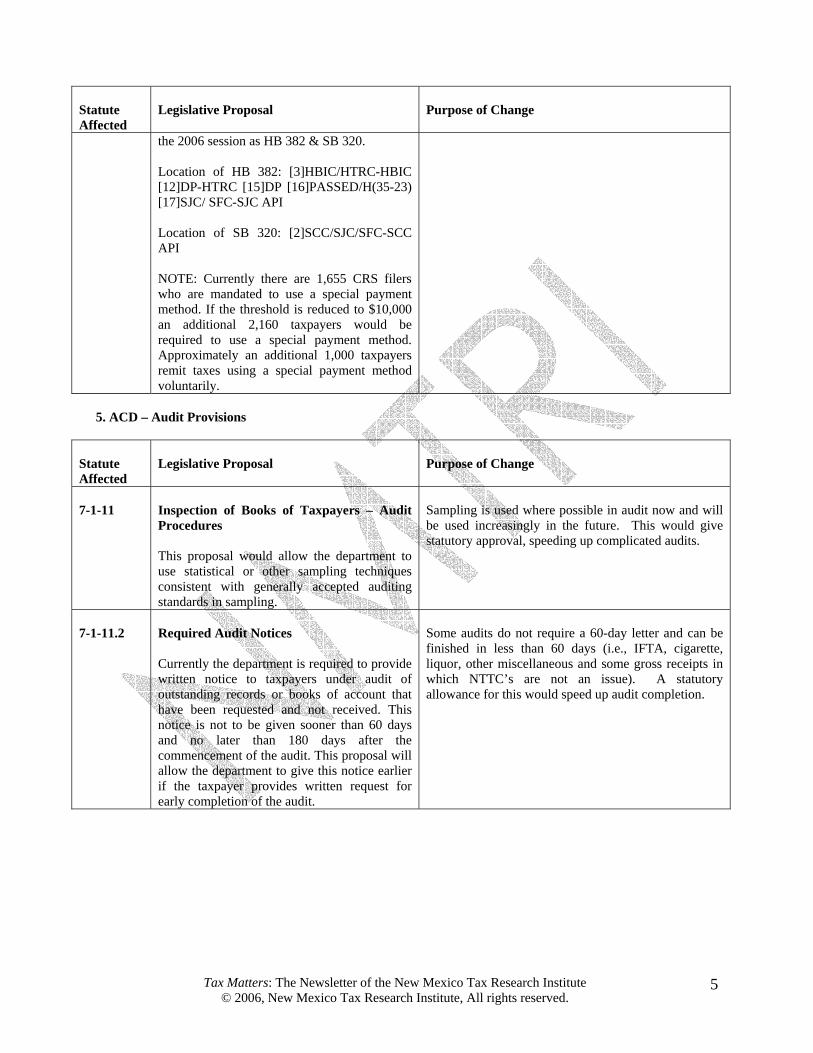

Mandatory E-filing of PIT Returns Personal income tax preparers who file more than 25 income tax returns will be required to file electronically unless the taxpayer has indicated in writing that they do not want their return filed electronically. Tax preparers who do not comply with this requirement will be subject to a penalty, not to exceed $5 per return. This proposal was introduced during the 2006 session as HB 382 & SB 320. Location of HB 382: [3]HBIC/HTRC-HBIC [12]DP-HTRC [15]DP [16]PASSED/H(35-23) [17]SJC/ SFC-SJC API Location of SB 320: [2]SCC/SJC/SFC-SCC API NOTE: Other states that have implemented similar mandates show a 20% increase in e-filed returns.

Electronic filing decreases the costs associated with filing paper returns and paper checks. This proposal would allow the department to encourage tax preparers to electronically file, but also provides minimal penalties and a way out if the taxpayer is adverse to e-filing.

7-1-13

Automatic Federal Extensions Currently the Taxation and Revenue Department honors automatic federal extensions for personal income tax purposes. In 2005 the IRS changed the period of time for which they grant an automatic federal extension from 4 to 6 months. This proposal was introduced during the 2006 session as HB 384 & SB 319. Location of HB 384: [3]HBIC/HTRC-HBIC [12]DP-HTRC [15]DP [16]PASSED/H(59-0) [17]SJC/SFC- SJC API Location of SB 319: [2]SCC/SJC/SFC-SCC [3]germane-SJC [6]DP-SFC [11]DP/a [13]PASSED/S (32-0) [15]HBIC/HJC-HBIC [22]DP-HJC API

This proposal will make the state language track with the federal changes and eliminate confusion for taxpayers and tax preparers.

7-1-13.1

Tax Threshold for Mandating a Special Payment Method Currently taxpayers who are liable for taxes in excess of $25,000 are required to remit their taxes using a special payment method. This proposal would reduce the tax threshold to $10,000. This proposal was introduced during

Expands the number of taxpayers required to make payment of certain taxes through special payment procedures, thereby encouraging e-filing and electronic payments.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

5

Statute Affected

Legislative Proposal

Purpose of Change

the 2006 session as HB 382 & SB 320. Location of HB 382: [3]HBIC/HTRC-HBIC [12]DP-HTRC [15]DP [16]PASSED/H(35-23) [17]SJC/ SFC-SJC API Location of SB 320: [2]SCC/SJC/SFC-SCC API NOTE: Currently there are 1,655 CRS filers who are mandated to use a special payment method. If the threshold is reduced to $10,000 an additional 2,160 taxpayers would be required to use a special payment method. Approximately an additional 1,000 taxpayers remit taxes using a special payment method voluntarily.

5. ACD – Audit Provisions

Statute Affected

Legislative Proposal

Purpose of Change

7-1-11

Inspection of Books of Taxpayers – Audit Procedures This proposal would allow the department to use statistical or other sampling techniques consistent with generally accepted auditing standards in sampling.

Sampling is used where possible in audit now and will be used increasingly in the future. This would give statutory approval, speeding up complicated audits.

7-1-11.2

Required Audit Notices Currently the department is required to provide written notice to taxpayers under audit of outstanding records or books of account that have been requested and not received. This notice is not to be given sooner than 60 days and no later than 180 days after the commencement of the audit. This proposal will allow the department to give this notice earlier if the taxpayer provides written request for early completion of the audit.

Some audits do not require a 60-day letter and can be finished in less than 60 days (i.e., IFTA, cigarette, liquor, other miscellaneous and some gross receipts in which NTTC’s are not an issue). A statutory allowance for this would speed up audit completion.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

6

7-1-67

Change Managed Audit Provisions A taxpayer who has entered into a managed audit agreement with the department currently has 30 days after the mailing of an assessment to remit payment in order to avoid the accrual of interest. This proposal would extend that time period to 180 days. This proposal was introduced during the 2006 session as HB 384 & SB 319. Location of HB 384: [3]HBIC/HTRC-HBIC [12]DP-HTRC [15]DP [16]PASSED/H(59-0) [17]SJC/SFC- SJC API Location of SB 319: [2]SCC/SJC/SFC-SCC [3]germane-SJC [6]DP-SFC [11]DP/a [13]PASSED/S (32-0) [15]HBIC/HJC-HBIC [22]DP-HJC API

This proposal should expand the pool of taxpayers who qualify for the managed audit program by increasing the time for payment. Current managed audit processing time, including review and assessment, can be up to 210 days. With the current 30 days to pay, the total time before a payment must be made can be 240 days. This change increases that time to about 390 days (or 1 year and one month) allowing the taxpayer more time to obtain the monies necessary to pay the tax liability.

6. Penalty/Interest & Assessment Provisions

Statute Affected

Legislative Proposal

Purpose of Change

7-1-17

Increase the minimum assessment amount. This proposal would increase the minimum amount assessed by the Department from $10.00 to $25.00.

This proposed change would equalize minimum assessment amounts, raise the amounts to make them more meaningful and provide greater cost effectiveness for the Department’s billing and collection efforts.

7-1-67 7-1-68

Decrease of Interest Rate – Deficiencies and Overpayments 1) The interest rate on underpayments and overpayments of tax is decreased from the current 15 percent to the rate established by the IRS for individual income tax purposes. The current IRS rate is 8 percent. The IRS updates its rates quarterly. This proposal was introduced during the 2006 session as HB 390 & SB 318. Location of HB 390: [3]HJC/HTRC-HJC [9]DP-HTRC [20]DNP-CS/DP (Succeeding entries: H 82) Location of SB 318: [2]SCC/SJC/SFC-SCC [3]germane-SJC [6]DP-SFC [11]DP [13]PASSED/S (29-4) [15]HTRC/HJC-HTRC [22]DP-HJC API 2) No interest would be paid by the Department on claims for refund of oil and gas or hard minerals taxes if the refund is made

1) A reduction of the department’s interest rate will bring the rate more closely in line with market interest rates. The federal government adjusts their interest rate regularly for this same purpose. This bill would bring the state into conformity with that policy. This proposal also places the penalty for failure to pay tax and file more equally on the penalty assessment. In the past the department has been criticized that interest assessments are more punitive than our penalty assessments. 2) Oil and Gas and hard mineral refunds can be very complex with significant detail that requires a thorough review before a determination can be made on the refund request. Increasing the time from 60 to 120 days before the department starts paying interest allows the department time to request and review additional information it may require. Because many taxpayers wait until December 30 each year to file refund requests, the extended time relieves the pressure on the department to just approve the refund request so it doesn’t have to pay interest.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

7

Statute Affected

Legislative Proposal

Purpose of Change

within one hundred and twenty days of the date of the claim for refund.

7-1-69

Increase of Penalty Rate – Failure to Pay Tax or File The maximum penalty for failure to pay tax or to file a return due to negligence is increased from 10 percent to 20 percent of the tax due. As under present law, the penalty would be imposed at a rate of 2 percent per month up to the maximum. A similar proposal, increasing the penalty rate to 16 percent, was introduced during the 2006 session as HB 390 & SB 318. Provisions are effective for penalties assessed. Location of HB 390: [3]HJC/HTRC-HJC [9]DP-HTRC [20]DNP-CS/DP (Succeeding entries: H 82) Location of SB 318: [2]SCC/SJC/SFC-SCC [3]germane-SJC [6]DP-SFC [11]DP [13]PASSED/S (29-4) [15]HTRC/HJC-HTRC [22]DP-HJC API

The state’s authority to impose penalty is meant to penalize taxpayers for failure to pay tax or file a return due to negligence. The increase in penalty helps neutralize the revenue loss resulting from the decrease in the interest rate.

7-1-69.1

Penalty for failure to file fuel tax returns All persons required to file information returns under the Gasoline Tax Act and the Special Fuels Supplier Tax Act are subject to a $50 penalty per missed return. Present law imposes the penalty on taxpayers who fail to file returns. Both acts require information returns from persons who are not directly liable for the tax. These include wholesale and retail operators who purchase already-taxed fuel from distributors. Information returns are needed from these parties to track sales of taxable and non-taxable fuel as they pass through the chain of commerce.

Present law imposes the penalty upon taxpayers who fail to file returns. Both the Gasoline Tax Act and the Special Fuels Supplier Tax Act require information returns from persons who are not directly liable for the tax. These are the wholesale and retail operators who purchase already-taxed fuel from distributors. Information returns are needed from these parties to track the sales of taxable and non-taxable fuel as they pass through the chain of commerce.

7-1-71.2

Double Local Option Penalty 1) Additional penalty for inaccurate reporting of the food or medical gross receipts deduction would be reduced. Under present law, penalty is imposed at a rate of 200 percent of local option tax rates times the difference between the incorrect deduction amount and the correct deduction amount. Penalty is imposed for both under- and over-reported deductions. The proposal would reduce the penalty rate to 2 percent per month up to a maximum of 20 percent of the misreported deduction amount

1) This change will encourage taxpayers who had reported the food or medical deduction incorrectly to amend their reports, which in turn will adjust the distributions to the counties and municipalities. Currently there is no incentive to amend these reporting errors. 2) Currently we have provisions that allow us not to assess regular penalty and interest on a managed audit assessment but there is no similar provision for the double local option penalty. This provision will encourage taxpayers who have incorrectly reported the food or medical deduction pursuant to Sections 7-9-92

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

8

Statute Affected

Legislative Proposal

Purpose of Change

times the local option tax rates. Penalty would be imposed only in cases where deductions are overreported. As under present law, this penalty is in addition to any other penalties that apply. This proposal was introduced during the 2006 session as HB 380 & SB 323. Location of HB 380: [3]HJC/HTRC-HJC [9]DP-HTRC [20]DNP-CS/DP (Succeeding entries: H 82) Location of SB 323: [2]SCC/SJC/SFC-SCC API 2) A taxpayer who has entered into a managed audit agreement with the department and who has incorrectly reported the gross receipts tax deduction for food sales or for sales of medical services would not be subject to the double local option penalty. This proposal was introduced during the 2006 session as HB 384 & SB 319. Location of HB 384: [3]HBIC/HTRC-HBIC [12]DP-HTRC [15]DP [16]PASSED/H(59-0) [17]SJC/SFC- SJC API Location of SB 319: [2]SCC/SJC/SFC-SCC [3]germane-SJC [6]DP-SFC [11]DP/a [13]PASSED/S (32-0) [15]HBIC/HJC-HBIC [22]DP-HJC API

and 7-9-93 NMSA 1978, to correct their reporting errors through a managed audit without being penalized.

7. Oil & Gas Provisions

Statute Affected

Legislative Proposal

Purpose of Change

7-1-10

Records Required by Statute Change wording of Subsection E to read as follows: Upon the written application of a taxpayer and at the sole discretion of the secretary or the secretary’s delegate, the secretary or the secretary’s delegate may enter into an agreement with a taxpayer allowing the taxpayer to report gross values, gross receipts, deductions or the value of the property on an estimated basis for gross receipts tax, compensating tax, oil and gas severance tax, oil and gas conservation tax, oil and gas emergency school tax and oil and gas ad valorem production tax for a limited time

This would give the Department the flexibility to negotiate alternative valuation methods under the oil and gas tax programs. The industry is very complex and the sale of production can occur throughout North America. To require them to trace their production to the ultimate sales point and to recognize all costs associated to transportation is very cumbersome and difficult. Other alternative valuations should be available by agreement on a going-forward basis. This change would also support the department’s ability to negotiate a reasonable valuation application rather than spending a significant amount of time in the court system. These recommended changes track with what the federal government recognizes in their regulation and have been discussed with the Legal Bureau who

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

9

period not to exceed four years. As used in this section, “estimated basis” means a methodology that is reasonably expected to approximate the tax that will be due over the period of time of the agreement using summary rather than detail data or alternate valuation applications or methods.

believe this would allow some flexibility and negotiating tools.

7-1-26

Claim for Refund 1) Subsection I of this statute references the term “oil and gas tax return” and the natural resources reported on the return. This proposal would include helium or a non-hydrocarbon gas in the listing of natural resources. 2) In Subsection J, add the following to the last sentence: An oil and gas tax return that incorporates an amended tax due line is recognized as a request for refund.

1) This definition change will incorporate the definition changes made to the Oil and Gas tax programs in the 2005 session. 2) Oil and Gas taxpayers report amendments on a return that incorporates both the current tax detail and amendments. In the amendments, taxpayers may submit a credit tax due amount that needs to pass through the evaluation process. If the credit line does not pass the edits for distribution, this change codifies historic practices of denying this refund amount.

7-25-3

Rate and Measure of Tax Add to the definition of “natural resource” helium or a non-hydrocarbon gas.

This definition change will incorporate the definition changes made to the Oil and Gas tax programs in the 2005 session.

7-29-4 7-30-4 7-32-4

Imposition of Oil and Gas Severance Tax In Subsection A, remove the word “sold” and replace with “removed from the production unit”. Section 7-29-4 B. (1): Remove the word “sold” and replace with “removed from the production unit”. Section 7-30-4 A: In the first sentence remove the word “sold” and replace with “removed from the production unit”. In the second sentence, remove the word “sold” and replace with “removed products from the production unit”. Section 7-32-4: Remove the word “sold” and replace with the word “removed”.

Not all oil and gas produced in the state is “sold”. Oil is refined into gasoline products and is not physically sold. Natural gas is sometimes not sold but used in co-generation facilities to generate electricity. These recommended changes would clear this issue and relieve the department of litigation risks in court. The term “sold” is currently under litigation and the Legal Bureau agrees with this recommendation to change the term.

8. ACD Collection Provisions

Statute Affected

Legislative Proposal

Purpose of Change

New

Lottery Offsets Allow the offset of winnings from the New Mexico Lottery for an individual’s state tax liability.

Many other states that operate a lottery have the ability to offset lottery winnings and are generating revenue from this process.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

10

9. MVD – NAFTA Registration

Statute Affected

Legislative Proposal

Purpose of Change

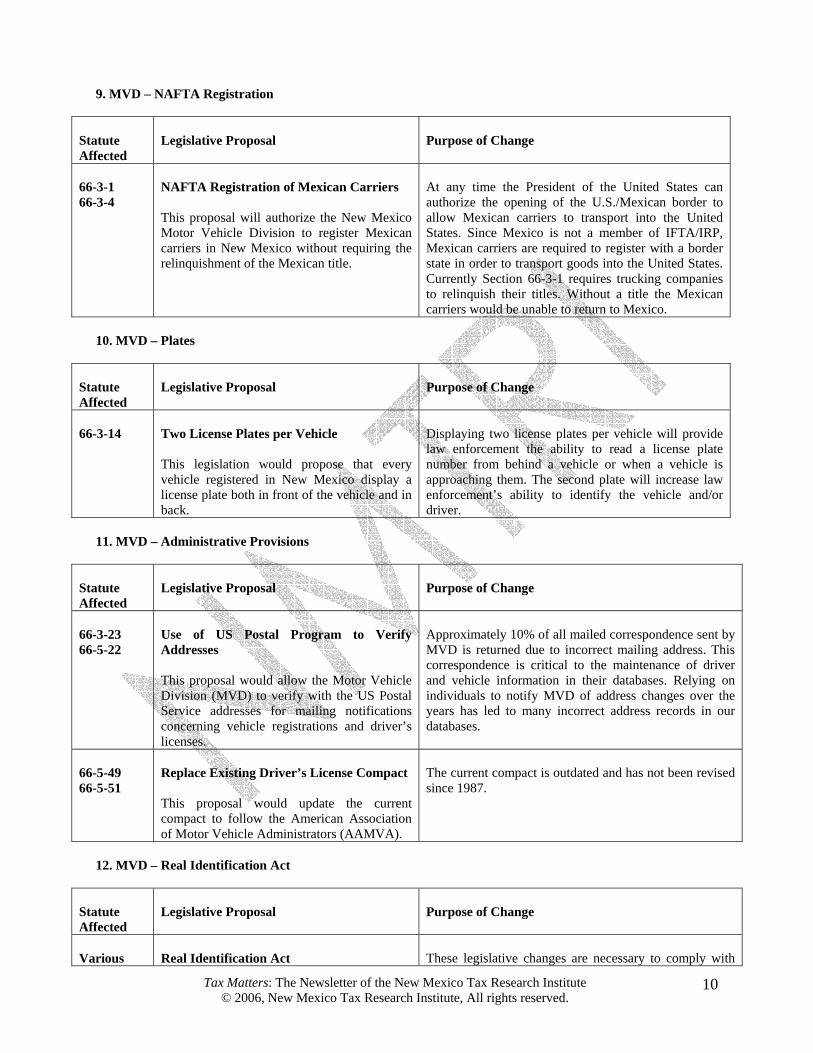

66-3-1 66-3-4

NAFTA Registration of Mexican Carriers This proposal will authorize the New Mexico Motor Vehicle Division to register Mexican carriers in New Mexico without requiring the relinquishment of the Mexican title.

At any time the President of the United States can authorize the opening of the U.S./Mexican border to allow Mexican carriers to transport into the United States. Since Mexico is not a member of IFTA/IRP, Mexican carriers are required to register with a border state in order to transport goods into the United States. Currently Section 66-3-1 requires trucking companies to relinquish their titles. Without a title the Mexican carriers would be unable to return to Mexico.

10. MVD – Plates

Statute Affected

Legislative Proposal

Purpose of Change

66-3-14

Two License Plates per Vehicle This legislation would propose that every vehicle registered in New Mexico display a license plate both in front of the vehicle and in back.

Displaying two license plates per vehicle will provide law enforcement the ability to read a license plate number from behind a vehicle or when a vehicle is approaching them. The second plate will increase law enforcement’s ability to identify the vehicle and/or driver.

11. MVD – Administrative Provisions

Statute Affected

Legislative Proposal

Purpose of Change

66-3-23 66-5-22

Use of US Postal Program to Verify Addresses This proposal would allow the Motor Vehicle Division (MVD) to verify with the US Postal Service addresses for mailing notifications concerning vehicle registrations and driver’s licenses.

Approximately 10% of all mailed correspondence sent by MVD is returned due to incorrect mailing address. This correspondence is critical to the maintenance of driver and vehicle information in their databases. Relying on individuals to notify MVD of address changes over the years has led to many incorrect address records in our databases.

66-5-49 66-5-51

Replace Existing Driver’s License Compact This proposal would update the current compact to follow the American Association of Motor Vehicle Administrators (AAMVA).

The current compact is outdated and has not been revised since 1987.

12. MVD – Real Identification Act

Statute Affected

Legislative Proposal

Purpose of Change

Various

Real Identification Act

These legislative changes are necessary to comply with

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

11

Various statutes within the Motor Vehicle Code would need to be amended in order to comply with recent federal legislation. These changes would include minimum documentation requirements, verification of principal residence and digital facial images.

federal mandates imposed on all states and will assist in the federal government’s maintenance of national security.

13. CDL Provisions

Statute Affected

Legislative Proposal

Purpose of Change

New 66-1-4.16 66-5-4 66-5-65 66-5-68 66-8-135

Commercial Driver’s License Amendments This bill would address the following federal mandates: 1) Masking of traffic violations - Masking occurs when a judge enters a deferred adjudication for traffic citations and the violation is reported to MVD as a dismissal. 2) Federal Motor Carrier Safety Act (“FMCSA”) regulations demand that all violations be reported. The bill includes a broader definition for “state of domicile” to also comply with FMCSA Regulations. 3) Section 66-1-4.16 definition of conviction needs to match the federal definition word-for-word. 4) Section 66-1-4.16(M) needs to include Mexico: "state" means a state, territory or possession of the United States, the District of Columbia, Mexico, or a province of the Dominion of Canada. 5) Section 66-5-4 needs to exempt from licensure military personnel when driving a vehicle owned or leased by the Department of Defense. 6) Section 66-5-68 - delete throughout paragraphs B through E language requiring the offense be committed in a commercial vehicle. 7) Section 66-5-68 - include language that the disqualification period will run consecutively to any revocation period for the same offense. 8) Section 66-8-135 - record of traffic cases – all convictions on record for 55 years. 9) Adopt language that NM will treat a

Any State found to be in substantial noncompliance with the Motor Carrier Safety Act is subject to withholding of 5 percent of Federal-aid highway funds the first fiscal year and 10% the second and subsequent year(s) of noncompliance. FMCSA may also decertify the State’s CDL program and prohibit the issuance of CDLs if a determination is made that the deficiencies affect a substantial number of either CDL applicants or drivers. NM Department of Transportation estimates the Road Fund could lose $10 million under the 5 percent penalty and $20 million under the 10% penalty.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

12

Statute Affected

Legislative Proposal

Purpose of Change

conviction received in another state the same as if received here. 10) Section 66-5-65(E) - HazMat endorsement on a transfer CDL: NM will require re-testing if applicant has not tested within past two years. Require all applicants renewing for HazMat endorsement to re-test for that endorsement. The masking and “state of domicile” proposals were introduced during the 2006 session as HB 317. Location of HB 317: [3]HJC/HTRC-HJC [13]DNP-CS/DP-HTRC [17]DP [19]PASSED/H(58-0)-SJC/ SFC-SJC [21]w/drn-SFC [22]DP [24]fl/a-PASSED/S(37-0) API

14. MVD – Technical Corrections

Statute Affected

Legislative Proposal

Purpose of Change

66-3-1004 66-3-1004.1

All Terrain Vehicle Clean-Up 66-3-1004 – Subsection G imposed a fee of $1.00 on registration certificates and nonresident permit for the NM Clean and Beautiful Program. 66-3-1004.1 - Paragraph (5) of subsection A provides for the disposition of fees to the NM Clean and Beautiful Program. One or both of these statutes should be amended to refer to the Litter Control and Beautification Fund instead of the NM Clean and Beautiful Program. The alternative is to create a NM Clean and Beautiful Program.

Currently there is no NM Clean and Beautiful Program. The Motor Vehicle Division does not have a way to dispose of the $1.00 fee collected on vehicle registrations and permits.

66-6-23

Mandatory Financial Responsibility Act Fee The Motor Vehicle Division (MVD) currently collects a $2.00 registration fee used to enforce the provisions of the Mandatory Financial Responsibility Act and for creating and maintaining a multi-language noncommercial driver’s license testing program. This proposal would allow MVD to

MVD has received permission from the Legislative Finance Committee to use the $2.00 fee to support commercial knowledge testing and other operational functions where vehicle insurance is a part of the operation. This proposal would formalize this permission statutorily.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

13

Statute Affected

Legislative Proposal

Purpose of Change

use this fee to support day-to-day operations. 15. Cigarette Tax Act Provisions

Statute Affected

Legislative Proposal

Purpose of Change

Various

This proposal will address various concerns with HB 617 passed during the 2006 Legislative Session. After numerous discussions with industry it has become clear that the current language needs to be amended to address inconsistencies and clarify the intent of the legislation. The following is a brief description of the proposed changes:

• Remove “or importer of cigarettes that posses a valid and current permit pursuant to 26 U.S.C. 57-13” [Section 7-12-5(C)]. This is in conflict with Section 7-12-9.2. • Change the word “any” Indian nation… to “that” Indian nation [Section 7-12-4(A)(2)]. This change will clarify that an Indian must on own land to qualify for exemption, not land owned by another tribe, nation, etc. and to bring into agreemet with other statutes in other tax acts. • Address packaging requirements for “small cigars”. Current language requires cigarettes in lots of 20 or 25. Small cigars are usually sold in packs of less than 20 sticks. • Modify the definition of “cigarette” to include language from the federal definition of a small cigar. “Any roll of tobacco or any substitute for tobacco wrapped in anything that is not 100 percent tobacco and weighs three pounds or less per thousand.” • Amend the definition of “contraband cigarettes” to state that “any labeling which is required by federal law shall not be considered to constitute “false or fraudulent labeling. “” A similar change is made to Section 7-12-9.1(G)(5).

This legislation is necessary to assist the Taxation and Revenue Department with administration of the Cigarette Tax Act and to provide clear guidance to the cigarette and cigar industries.

7-12-4

Exemptions for Cigarette Tax The proposal would clarify that the exemption for the sale of cigarettes to an enrolled member be licensed by their Indian nation, tribe or pueblo. Current language allows an

This will clarify that sales to an enrolled member must occur on their tribal land to qualify for the exemption and not on land of another nation, tribe or pueblo.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

14

Statute Affected

Legislative Proposal

Purpose of Change

exemption for sales to an enrolled member licensed by the governing body of any Indian nation, tribe or pueblo for use or sale on that reservation or pueblo grant.

7-12-5

Affixing Stamps 1) This proposal would remove from Subsection C the language “or importer of cigarettes that possesses a valid and current permit pursuant to 26 U.S.C. 57-13”. 2) Removal of the following language in Subsection D is also proposed: “Packages shall contain cigarettes in lots of 20 or 25.“ Instead the language similar to the following should be included: “Packages to which a stamp is required to be affixed and which contain less than 20 cigarettes shall have affixed a twenty-stick stamp.”

1) The current language is in conflict with Section 7-12-9.2 which only authorizes a distributor to buy from a manufacturer, not an importer. This will clarify who a distributor may purchase cigarettes from. 2) Small cigars (Prime Time, Tiparillos, etc.) are defined as cigarettes. They are usually sold in packs of less than 20 sticks. To avoid another stamp denomination, distributors would use the stamps already available.

16. Gasoline and Special Fuels Supplier Tax Act Provisions

Statute Affected

Legislative Proposal

Purpose of Change

7-13-4 7-16A-10

Gasoline & Special Fuels Tax Remitted by an Out-of-State Distributor Allows an out-of-state distributor to remit the gasoline or special fuel excise tax imposed on fuel imported into New Mexico on behalf of the importer.

Avoids requiring importers to pay the tax twice until they can claim a refund of the tax paid in the other state.

New

Bonding Requirement for Mexican Truckers This proposal would require truckers who are not based in an IFTA jurisdiction (i.e., Mexican truckers) who have been adopted by New Mexico to furnish a surety bond to ensure the payment of the weight distance or special fuel excise tax.

This proposal would ensure payment of tax from truckers over whom we do not have any enforcement/collection authority when the trucker returns to their home country.

Federal State Tax Issues: Business Activity Tax Nexus. On August 15 a group of NMTRI members and guests met with state officials and Joshua Baca, Legislative Aide to U.S. Representative Heather

Wilson, to discuss the issues involved in the Business Activity Simplification Act, H.R. 1956,

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

15

currently pending in the Congress. A companion bill, S. 2721, has been introduced in the Senate. The bill would set standards the states would have to meet before they could assess business activity taxes, including corporate income taxes. The effort is designed to blunt the use of “economic presence” practiced by many states, including New Mexico, in asserting corporate income tax liability. The states have mounted a vigorous defense of their prerogative to assess taxes under existing constitutional, federal legislative and court interpretations. Many muti-state businesses have been just as vigorous in saying that one national rule that limits the states would facilitate interstate business operation, investment and development. An existing limitation on the states’ ability to assert corporate income tax liability against a multi-state corporation is 15 U.S.C. § 381, popularly known as Public Law 86-272. This limitation was adopted by the Congress to answer complaints from the business community in response to the 1959 Supreme Court decision in Northwestern States Portland Cement Co. v. Minnesota, 358 U.S. 450 (1959) that expanded the authority of states to impose apportioned net income taxes on interstate businesses. Public Law 86-272 prohibits a state from imposing its net income tax on a business whose only activity within the state is the solicitation of orders of tangible property, provided that the orders are approved and the goods are shipped to the purchasers from outside the taxing state. One of the more significant changes that would be made by H.R. 1956 would be to extend protection to all kinds of business activity. In addition to the technical tax issues presented by the legislation, the question of whether the legislation is an “unfunded mandate” has slowed consideration of the bill. If it is it would be subject to more stringent procedural rules in the Congressional debate. The discussion was spirited, sincere and comprehensive and Mr. Baca thanked NMTRI and all of the participants for illuminating the competing issues for him and Congresswoman Wilson.

VOTING FOR DOLLARS? USAToday (7/17/2006) reports that “In an effort to improve voter turnout in Arizona, Tucson political activist Mark Osterloh gathered more than 185,000 signatures to put his Arizona Voter Reward Act on the state ballot this November as Proposition 200. If Arizona's voters approved, one lucky voter would win a million dollars, financed by unclaimed prize money from the state's existing lottery. Citizens

would qualify by voting in the primary or general election. If they vote in both, they would be entered twice. Osterloh's slogan is "Who wants to be a millionaire? Vote." What do NMTRI members think of this idea?

WHATCHAMACALLIT? DOES IT QUACK? The Houston Chronicle (8/10/06) reports that the campaign for Governor of Texas has been impacted by a pronouncement from the Financial Accounting Standard Board on taxes. The decision by the FASB,

saying the state's new business tax is an income tax for reporting purposes, embraced a label rejected by tax proponents, including Gov. Rick Perry. The newspaper opines that the designation gives fresh fodder to Perry challengers Carole Keeton Strayhorn, currently the state comptroller; Kinky Friedman; and Chris Bell. Strayhorn spokesman Mark Sanders said

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

16

the ruling makes Perry the first governor in Texas history to sign into law an income tax. Chief economist Dale Craymer of the Texas Taxpayers and Research Association said, "This is one of those things where it may be considered an income tax for financial reporting purposes, but that doesn't necessarily mean that it's an income tax for the purposes of the Texas Constitution. They have different definitions."

Where Does New Mexico Rank? Does It Matter? Members will soon receive a copy of the latest study done by Dr. Manuel del Valle, Research Director of NMTRI, on various state rankings studies. Dr. del Valle examines the studies, looks at their underlying assumptions and tries to determine if they are verifiable and actually relate to economic prosperity. The study, State Rankings as Tax Policy Tools, will be mailed to members and later will be posted on the NMTRI website: www.nmtri.org. We hope you see the value of this study and will be pleased to answer questions if you desire after reading the study.

MARK YOUR CALENDARS! THE DATES HAVE BEEN SET FOR THE 2007 FOURTH ANNUAL NEW MEXICO TAX POLICY CONFERENCE.

THIS PREMIER EVENT WILL BE HELD ON APRIL 30-MAY 1, 2007 AT THE LA FONDA ON THE PLAZA HOTEL IN SANTA FE. WATCH THIS SPACE FOR THE TERRIFIC LINE-UP OF

SPEAKERS.

NMTRI Office: Effective August 21, 2006, NMTRI will be located in new office space located at 9400 Holy Avenue NE, Building 2, in Albuquerque. Our mailing address remains the same, P.O. Box 91657, Albuquerque, NM 87199-1657. You may contact us at our new office number 505-797-6664 for President and Executive Director Jim Eads and 505-797-6667 for Research Director Dr. Manuel del Valle. Our mobile numbers remain the same, 505-228-7129 for Eads and 505-238-

2086 for del Valle. Faxes may be sent to 505-797-6666. We have been using space generously provided to us by the Bank of America in downtown Albuquerque, but the decision was made to relocate to space in far northeast Albuquerque more convenient to the staff and to members coming in from Santa Fe. NMTRI extends our sincere thanks to Rick Wadley and Matt Schaefer at the Bank of America for their generous allowance of use of their space for the last three years.

Tax Matters: The Newsletter of the New Mexico Tax Research Institute © 2006, New Mexico Tax Research Institute, All rights reserved.

17

COMING SOON in Tax Matters: The Newsletter of the New Mexico Tax Research Institute

Distinguished Lectures Series: More speakers are coming Tax News Makers: Interviews with tax policy thought leaders

Report: Effort to update New Mexico’s tax regulations Combined Reporting: What should New Mexico do? Oil and Gas Prices: What do they mean to New Mexico’s revenues?

COMMENTS: Your suggestions and comments on this newsletter, the annual meeting (past or future), the Distinguished Lectures Series, our research or any aspect of NMTRI’s operation and programs are welcome. Please send them to [email protected], call 505-228-7129 or mail them to P.O. Box 91657, Albuquerque, New Mexico 871990-1657. We genuinely solicit your input and thank you for your support.

“The power to tax is the power to destroy.” You have an interest in the tax policy of New Mexico.

Join NMTRI today.