STATEMENT OF ACCOUNTS - Milton Keynes

162

STATEMENT OF ACCOUNTS 2011/12 For the year ended 31 st March 2012

Transcript of STATEMENT OF ACCOUNTS - Milton Keynes

STATEMENT OF ACCOUNTS

2011/12

For the year ended 31st March 2012

Contents

Page No

1 Explanatory Foreword

13 Statement of Auditors Opinion

16 Statement of Responsibilities

17 Accounting Policies

Core Financial Statements

42 Movement in Reserves Statement

44 Comprehensive Income and Expenditure Statement

45 Balance Sheet

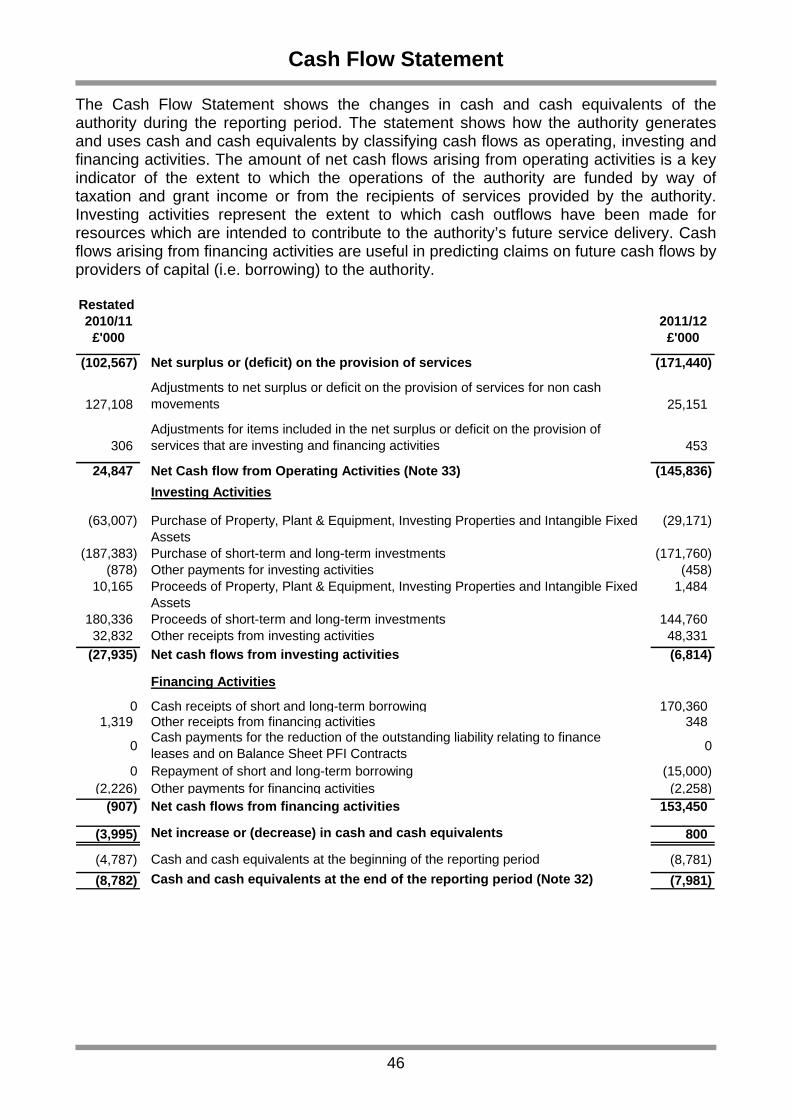

46 Cash Flow Statement

47 Notes to the Accounts (Index on following page)

Supplementary Financial Statements

142 Housing Revenue Account

152 Collection Fund

155 Glossary

Contents

Index of Notes to the Financial Statements Page No

Note No

47 1 2010/11 Comparator Restatements

48 2 Accounting Standards that have been Issued but not yet Adopted

48 3 Assumptions about the future, other major sources of estimation uncertainty and critical judgements in applying Accounting Policies.

52 4 Material Items of Income and Expense 52 5 Material Events after the Balance Sheet Date

54 6 Adjustments between Accounting Basis and Funding Basis under Regulation

61 7 Transfers to/from Earmarked Reserves 68 8 Exceptional Items 68 9 Trading Operations 70 10 Acquired and Discontinued Operations 70 11 Agency Services 70 12 Members Allowances 71 13 External Audit Costs 72 14 Road Charging Schemes under the Transport Act 2000 73 15 Pooled Budgets 76 16 Officers Remuneration 78 17 Dedicated Schools Grants 79 18 Grant Income 81 19 Landfill Allowance Trading Scheme 81 20 Property, Plant and Equipment 84 ~ Depreciation 84 ~ Capital Commitments 85 ~ Valuation of Non-Current Assets 87 ~ Re-Valuation of Non-Current Assets 87 ~ Foundation School Asset Values 87 ~ Effects of Changes in Estimates 88 ~ Impairment 89 ~ Material Impairment Losses 90 21 Heritage Assets 94 22 Investment Properties 96 23 Capital Expenditure and Capital Financing

Contents

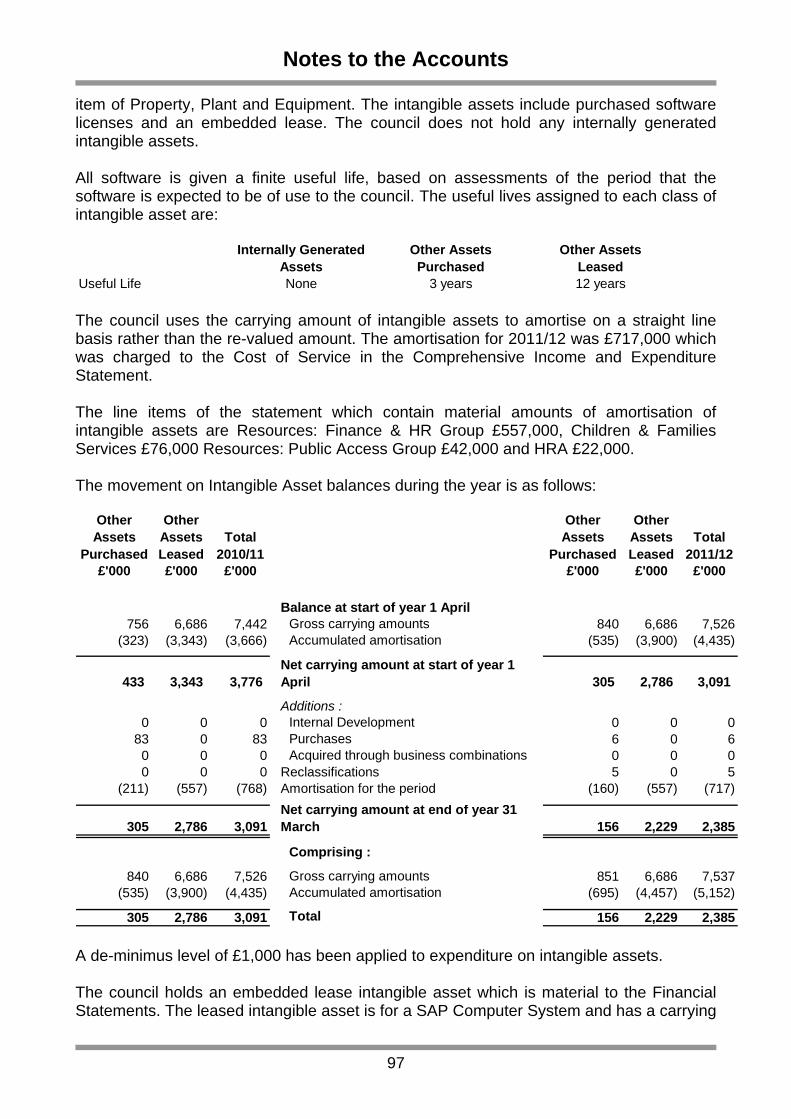

96 24 Intangible Assets 98 25 Current Assets Held for Sale 98 26 Debtors 99 27 Work in Progress and Inventories 100 28 Creditors 100 29 Borrowing Repayable 101 30 Provisions 105 31 Reserves 105 ~ Capital Adjustment Account 107 ~ Revaluation Reserve 107 ~ Financial Instrument Adjustment Account 108 ~ Pension Reserve 109 ~ Collection Fund Adjustment Account 109 ~ Deferred Capital Receipts Reserve 110 ~ Accumulated Absence Account 110 32 Cash and Cash Equivalents 111 33 Net Cash Flow from Operating Activities 112 34 Amounts Reported for Resource Allocation Decisions 118 35 Financial Instruments 125 36 Leases 127 37 Long Term Contracts 129 38 Related Party Transactions 135 39 Group Accounts 135 40 Trust Funds 136 41 Contingent Gains and Losses 137 42 Retirement Benefits 141 43 Pension Schemes Accounted for as Defined Contribution Schemes

Explanatory Foreword

1

1. INTRODUCTION

The financial performance for 2011/12 for the activities undertaken by the council is set out in the Financial Statements as reported in the Statement of Accounts. The Statement of Accounts contains the following:

a. Accounting Policies Details the legislation and principles against which the Statement of Accounts has been prepared;

b. Financial Statements

The Movement in Reserves Statement, incorporating the movement in year

on all the different reserves held by the council;

The council’s Comprehensive Income and Expenditure Statement which summarises resources which have been applied and generated in providing services and managing the council during the last year;

The Balance Sheet which sets out the assets and liabilities recognised by the council as at 31st March 2012, and;

The Cash Flow Statement, which summarises the changes in cash and cash equivalents of the council during the reporting period.

c. Notes to the Financial Statements

The notes to support the financial statements have three main purposes: To present information about the basis of preparation of the financial

statements and the specific accounting policies used;

To disclose the information required by the International Financial Reporting Standards Code of Practice that is not presented elsewhere in the financial statements, and;

To provide information that is not presented elsewhere in the financial statements, but is relevant to the understanding of them.

d. Housing Revenue Account

The Housing Revenue Account Income and Expenditure Statement shows the economic costs in the year of providing housing services in accordance with generally accepted accounting practices rather than the amount to be funded from rents and government grants;

e. Collection Fund

The Collection Fund Statement shows the transactions of the billing authority in relation to the collection from tax payers and distribution to local authorities and the Government of Council Tax and Non-Domestic Rates.

Explanatory Foreword

2

2. SERVICE EXPENDITURE

The service expenditure comprises the day-to-day service running expenses and general income of the council and includes expenses such as salaries, heating, lighting, rent, rates, stationery and depreciation, plus income relating to the services provided. For 2011/12 the council developed its budget options, within the resources available, by reference to its Corporate Plan and strategic objectives. It also drew on information from formal budget consultations with the public and other interested parties. The council approved a net budget of £196,209,000 for 2011/12 on 22nd February 2011, and chose to freeze its Council Tax. a. General Fund Revenue Outturn The General Fund outturn is a (£0.282m) underspend and a contribution of (£1.500m) to the General Fund as budgeted, which has been achieved against a backdrop of reductions in Government funding in year as well as pressures identified during the year. This shows the council has addressed the savings requirement and delivered a small underspend, with some opportunity to create reserves for specific future financial issues. This creates a solid basis for the delivery of the 2012/13 budget and the confirmed challenge of addressing the future years budget pressures. The overall impact of this outturn position produces a closing position of £8.796m on General Fund Balance as at 31st March 2012. The Housing Revenue Account is reporting an outturn in year of (£1.421m). The overall position for the year, including the balance brought forward from 2010/11, is an underspend of (£0.123m), which results in a reserve balance at the end of March 2012 of £5.511m. The outturn position for the Dedicated Schools Grant is an underspend of (£2.302m). The Capital outturn is (£6.824m) against the latest spend approval, £6.854m is due to delays in projects, resources and project delivery will be rephased into 2012/13, leaving a small overspend of £0.030m on the capital programme. The table overleaf details the over and underspends by Service Group:

Explanatory Foreword

3

RevisedBudget£'000 £'000 £'000 %

Resources: Finance and Human Resources 8,707 8,406 (301) (3.5%)Resources: Public Access 95 75 (20) (21.1%)Adult Social Care and Health 57,299 56,489 (810) (1.4%)Housing and Community 2,355 3,133 778 33.0%Regulatory Unit 3,440 3,384 (56) (1.6%)Community Facilities Unit 12,812 12,661 (151) (1.2%)Integrated Support and Social Care 30,741 30,608 (133) (0.4%)Education, Effectiveness and Participation 35,520 34,529 (991) (2.8%)Planning, Economy and Development 2,100 2,434 334 15.9%Highways and Transportation 19,544 19,575 31 0.2%Neighbourhood Services 27,887 28,200 313 1.1%Organisational Transformation Programme 472 520 48 10.2%Corporate Core 4,139 4,057 (82) (2.0%)Net Operating Expenditure 205,111 204,071 (1,040)

Corporate ItemsLevies 439 439 0 0.0%Debt Financing and Interest Charges 22,501 21,539 (962) (4.3%)Sustainability Items 779 779 0 0.0%Corporate Savings & One Off Pressures 1,204 2,924 1,720 142.9%Asset Rental (33,825) (33,825) 0 0.0%Projected Outturn Position 196,209 195,927 (282)

ResourcesFormula Grant (88,491) (88,491) 0 0.0%Early Intervention Grant (10,172) (10,172) 0 0.0%Council Tax (Including Freeze Grant) (94,807) (94,807) 0 0.0%Reserves (2,739) (2,739) 0 0.0%Total Resources Available (196,209) (196,209) 0

(Addition)/Reduction in General Fund 0 (282) (282)

General Fund Balance 1st April 2011 (7,014)General Fund (Under)/Overspend 2011/12 (282)Budgeted Contribution to General Fund Balance (1,500)

General Fund Balance 31st March 2012 (8,796)

Outturn (Under)\Overspends

Significant variations for each Service Group are detailed in the paragraphs that follow. Resources - Finance and Human Resources The significant variations in Resources - Finance and Human Resources are increased income from Housing Benefit overpayment debts of (£306,000), additional recovery of council tax benefit overpayments of (£345,000) and improved recovery of Housing Benefit payments of (£344,000). These savings were offset by £235,000 to provide for funding for future potential liabilities arising from central government changes to both Council Tax benefits and Housing Benefit

Explanatory Foreword

4

Reform and a contribution of £300,000 to the Insurance Reserve due to an increase in the expected level of claims. An unachievable Procurement savings target of £283,000 was partially offset by Procurement restructure savings of (£114,000). Resources - Public Access Facilities and Administration Buildings were unable to achieve hospitality catering and room hire income £144,000 but incurred lower utility costs (£84,000) than budgeted. Further savings were achieved in costs for office rationalisation (£55,000), lower cleaning and catering costs (£57,000), repairs & maintenance costs (£63,000), and additional rent income and savings (£60,000). Property shows an underspend of (£159,000) due to the release of a Property creditor which is offset by a contribution to the office accommodation Reserve £200,000. Adult Social Care and Health Joint Commissioning and Contracts budgets under spent by (£370,000) including pressures on the joint equipment budget with the Primary Care Trust of £120,000 which have been offset by grant savings and the maintenance of vacancies (£222,000). There is also an under spend within Adult Social Care Training of (£268,000). Adult Social Care is under spent by (£475,000). Overspends within Physical Disability external homecare were more than offset by reductions in Learning Disability transition placements and efficiency savings in the Mental Health Pooled Budget. There were also favourable variances in Community Alarms and Sheltered Housing due to staffing vacancies within sheltered schemes and equipment savings within the Alarm Service. Additional savings were made across Other Adult Services including Supported Employment, Emergency Social Work, Alcohol Abuse Placements and Delayed Discharges. Housing and Community The variance against Revised Budget includes the creation of reserves totalling £639,000 including £200,000 for the compulsory purchase of two properties at Peartree Bridge, £200,000 for legal fees linked to compulsory purchase and a dispute over Calverton Travellers Site and £100,000 for Bed and Breakfast costs arising from homelessness. There was also a loss of income and future abortive capital costs related to travellers’ sites of £154,000. Regulatory Unit The Regulatory Unit received additional income of (£148,000) in Licensing and Cemeteries and Crematoria, which offsets reduced income in Building Control and Sustainability. Additional legal costs for the Casino of £137,000 combined with legal and professional fees in Licensing of £90,000 and tribunal costs £60,000 are partially offset by savings in utility costs (£246,000).

Explanatory Foreword

5

Community Facilities Unit Savings within Leisure and Community in respect of the Leisure Partnership Contract were (£133,000), and the Library Service achieved savings of (£143,000). These are offset by additional costs in respect of Woughton Leisure Centre and Woughton on the Green Sports Ground of £180,000. Integrated Support and Social Care Staff identified in the Special Education Needs Disability and Inclusion Service (SENDIS) team who were budgeted to be charged to General Fund have been charged to Dedicated Schools Grant creating an underspend of (£213,000). £113,000 contribution has been made to Earmarked Reserves to offset the anticipated shortfall in Youth Services income in 2012/13, while restructuring of the service takes place. There were pressures within Children’s Social Care, because of the increasing number of children in care, and in-house fostering placements resulting in an overspend of £326,000. There were overspends of £98,000 in Special Guardianship Orders and £111,000 supported accommodation for 16/17 year olds. These pressures were offset by increased use of better value placements to reduce expenditure on external fostering and residential placements (£329,000). Family Support staffing underspent by (£224,000) due to reduced use of agency staff. A Demand reserve of £420,000 was created at the start of the year for increases in numbers of children in care; however, it was not necessary to draw down on this reserve and £200,000 was added to it in year to mitigate against the risks of an increase in provision. Education, Effectiveness and Participation Key variations include project management costs for Day Nurseries and adjustments to senior posts within Universal Services £194,000 and an overspend of £107,000 in Day Nurseries due to reduced income and the use of agency staff. In addition, a contribution to reserves of £400,000 has been made to fund redundancy, reorganisation and running costs for the Organisational Transformation Programme. These costs are offset by underspends across Children’s Centres (£103,000), lower use of the Improvement Fund than anticipated (£132,000), an underspend on Home to College Transport following the introduction of eligibility changes (£102,000), an underspend on Short Breaks (£344,000) and a saving on recommissioned services of (£307,000). In addition, increased buy back of the Music Service (£88,000) and Children and Adolescent Mental Health Services (CAMHS) staffing vacancies of (£65,000) combined with lower take up of Early Years Provision projects and workforce training (£126,000) further improved the service group position.

Explanatory Foreword

6

Planning, Economy and Development Urban Design was unable to achieve £56,000 of the income target. This was income previously chargeable to the Homes and Community Agency (HCA), but the transfer of the HCA development control function to the council meant this could no longer be achieved. Development Management had additional legal costs of £56,000 from appeals and Housing in Multiple Occupation (HIMO) appeal costs awarded and an £88,000 shortfall in fee income. In Spatial Planning a number of studies and surveys that had been planned to take place during the year could not be carried out due to delays in the Core Strategy, saving (£76,000). Restructuring of services resulted in pension strain and redundancy costs of £144,000 in Economic Development and £52,000 in Spatial Planning. This was partially offset by (£87,000) savings realised from the Planning Restructure. Highways and Transportation Energy costs in street lighting were £395,000 over the budget due to the delays in savings implementation together with the energy increase in October. Fees from charging capital projects were overachieved by (£165,000), although abortive costs from the Station Square capital project of £69,000 had to be recharged to revenue. A provision of £143,000 was made in relation to the potential shortfall on the Secklow Gate insurance claim and £126,000 was spent on principal bridge inspections. Concessionary fare reimbursement costs were £276,000 greater than budget due to increased ridership levels but there were savings on bus subsidies (£412,000) as a result of increased revenues; pursuing cross boundary income due from other authorities and savings on the contracts when they were tendered early in the year. Community transport costs were (£67,000) less than budget and additional highways adoption income of (£260,000) was achieved. Neighbourhood Services Savings of £150,000 were planned in the budget for the introduction of a four day week in waste collection. This could not be achieved due to operational restrictions at depot, landfill and other sites. Savings of £100,000 were also planned from staffing on the Joint Waste Project which has since ceased. These pressures are offset by Landfill tonnage savings of (£645,000), a reduction in Hazardous Waste tonnage (£93,000), a reduction in costs from the Carbon Reduction Commitment contract resultant from the new ways of working (£257,000) and additional income from the Materials Recycling Facility profit share of (£110,000). A decrease in the amount of fleet hire of £131,000 meant the savings anticipated for increased trading account charges in Fleet were not achieved. In addition a £200,000 provision was made for potential liabilities arising from ongoing fleet investigations. Building services had £108,000 more pay costs than budgeted because of a change from

Explanatory Foreword

7

temporary to permanent staff during the year. These costs were not fully recovered through income. In Landscape, fleet costs were £242,000 more than budgeted and a reduction in salaries of (£295,000) from reduced Agency and Overtime usage was offset by contractor/professional services of £411,000. Adoptions income has fallen significantly from previous years because of no residual land transfers from the HCA, income was £113,000 less than budget and Environmental Services Development under achieved its salary recovery by £120,000. Organisational Transformation Programme Additional staffing costs required for the delivery of the Organisation Transformation Programme were partially funded from savings in supplies and services. Corporate Core There were a number of underspends in Democratic Services including (£119,000) on Member Services for salary cost savings, reduced transport and catering costs and savings on supplies and services. In Local Elections there were savings of (£46,000) on staff costs due to the ability to charge costs against the Referendum, £100,000 was contributed to the Events Reserve and the Portfolio Office saved (£61,000) due to maternity leave and staff vacancies. Variations between latest outturns and latest approved budgets are monitored on a monthly basis and are reported to Members throughout the year. Further information on the overall financial performance of the council in 2011/12 is disclosed in the Comprehensive Income and Expenditure Statement and the notes to the Financial Statements. Corporate Items An opportunity to purchase Microsoft Office upgrades earlier than anticipated resulted in a cost of £550,000 in 2011/12, releasing savings for future financial years and avoiding price increases. There was also an additional contribution of £200,000 to the Redundancy and Reorganisation Reserve. Under accounting regulations the Council must provide for potential costs as at 31st March. Debt Financing The movement in debt financing was to provide for potential future treasury management cash flow costs linked to the ongoing discussions with the Homes and Communities Agency.

Explanatory Foreword

8

b. Housing Revenue Account Outturn The outturn position for the HRA shows an in year underspend of (£1.421m) at 31st March 2012. Significant variations include (£798,000) net savings in repairs expenditure which offsets £256,000 reduction in rent due to longer re-let periods as a result of changes in the asbestos management process leading to a higher number of empty properties undergoing works. Other notable savings include (£321,000) resulting from vacancies and restructuring, (£305,000) from release of uncommitted special services works budgets (block improvements, landscaping and cleaning), (£106,000) from capitalisation of building services (including WBT share), (£290,000) savings in utility costs from the milder winter, (£189,000) fall in debt charges and (£286,000) from anticipated recovery of leasehold service charge costs. A deficit of £660,000 was recognised in the Leasehold Major Works Recharge account as less work was carried out for leaseholders and on communal areas than had been anticipated in the budget. Review of Leasehold bad debt reserves and budgets highlighted an excess of (£130,000) above current provision requirements and was released accordingly to part fund the leasehold major works recharge gap. Services required for the Working Better Together programme incurred costs of £500,000. However, this resulted in a lower contribution to the Revenue Contributions to Capital Outlay Account, achieving a saving of (£190,000). In 2011/12 an earmarked reserve of £310,000 was created within the HRA to fund the HRA element of demolition costs relating to three units at Waterside due to take place in 2012/13. The level of HRA Reserve at the end of 2010/11 was £1,298,000 less than budgeted due to necessary additional contributions made towards MKC regeneration (CESP Community Energy Saving Programme) and major works capital projects. Therefore, overall, the underspend at 31st March 2012 was (£123,000). This results in the level of the reserve carry forward being (£5,511,000) compared to a budget of (£5,388,000) at 31st March 2012. Further information on the overall financial performance of the Housing Revenue Account in 2011/12 is disclosed in the notes to the Supplementary Financial Statements. c. Income from Grants, Local Tax Payers and Other Sources The net budget requirement was financed from four main sources:

• Redistributed Non-Domestic Rates (£67.596m) NNDR is the amount raised from businesses collected locally but re-distributed

nationally;

Explanatory Foreword

9

• Revenue Support Grant (RSG) (£20.894m) RSG is one of the two main non-specific grants from central government;

• Early Intervention Grant (EIG) (£10.219m)

EIG is the other main non-specific grant from Central Government;

• Council Tax (£98.599m) This is the means of raising money locally, based upon the value of domestic property and is adjusted for the previous year’s surplus or deficit on collection.

In addition, some services receive specific grants, which are included in their separate budgets. There are conditions attached to many of these grants, which set out how, when and on what service or activity the grant may be spent. Since 1st April 2007 Schools services have been funded through the Dedicated Schools Grant (DSG). For 2011/12 the council received £158.6m in DSG funding. This funding was previously provided through the RSG and NNDR. A list of the grants the council received in 2011/12 can be found at note 18 to the Financial Statements. 3. PENSION LIABILITY

The council is a member of the Local Government Pension Scheme administered by Buckinghamshire County Council. The council’s financial statements in accordance with the proper accounting practice show a pension liability at 31st March 2012 of (£263.933m), which is an increase of (£121.768m) since 2010/11. In practice, statutory arrangements for funding the deficit mean that the financial position of the authority remains healthy. The deficit will be funded through reassessment of employer’s contributions as a result of the three-yearly fund valuations by the actuary. This is done in accordance with the appropriate International Financial Reporting Standard (IAS) 19. Full details of the Local Government Pension Scheme can be found in note 42 to the Financial Statements.

Explanatory Foreword

10

4. MATERIAL OR UNUSUAL CHARGES OR CREDITS TO THE ACCOUNTS, ASSETS ACQUIRED OR LIABILITIES INCURRED

The following transactions are considered to be material or unusual charges or credits within the 2011/12 Statement of Accounts:

a) The council’s pension liability has increased by (£121.768m). Further details can

be found in the Local Government Pension Scheme note 42 to the Financial Statements;

b) Major non-current asset disposals during the year include the transfer of the

Tickford Park and Green Park Schools to Foundation status along with a parcel of land which should have been transferred when Walton High moved to Foundation Status. These transfers totalled £7.207m. Details of major non-current asset disposals can be found in note 4 to the Financial Statements;

c) Milton Keynes Council has disclosed one item as exceptional in the Comprehensive

Income and Expenditure Accounts for the HRA Self Financing Scheme due to the degree of prominence required to provide a fair view of the accounts. Details of this Exceptional item can be found in note 8 to the Financial Statements.

5. SIGNIFICANT CHANGE IN ACCOUNTING POLICY

The Code of Practice on Local Authority Accounting in the United Kingdom 2011/12 introduced a change to the treatment in accounting for Heritage assets held by the Council. Heritage Assets are required to be recognised as a separate class of assets for the first time in the 2011/12 financial statements. Previously, heritage assets were either recognised as community assets (at cost) in the Property, Plant and Equipment classification in the Balance Sheet or were not recognised in the Balance Sheet as it was not possible to obtain cost information on the assets. Full details of the Heritage Assets held by the council can be found in the Notes to the Financial Statements (Property, Plant and Equipment note 20). 6. BORROWING FACILITIES

During 2011/12 ten new Public Works Loan Board loans totalling (£170.360m) were taken out to fund the HRA Self-Financing settlement payment in order to exit the Housing Subsidy system (classified as capital expenditure). Furthermore, one existing long term loan (£15.0m) was repaid upon maturity to the Public Works Loan Board during the year.

Explanatory Foreword

11

At the end of the financial year the council had outstanding borrowing in respect of the funding of capital projects of (£457.387m) including accrued interest. Further details of the composition of this sum can be found in the note 29 to the Financial Statements. It was not necessary during the year for the council to borrow temporary funds for cash flow purposes. Consequently, there were no temporary loans outstanding at 31st March 2012. At the 31st March 2012, the council had £101.880m invested with various financial institutions, of this amount £2.233m has been classified as cash equivalents as per the Accounting Policy note 6. 7. INTERNAL AND EXTERNAL SOURCES OF FINANCE TO FUND CAPITAL

EXPENDITURE PLANS AND FINANCIAL COMMITMENTS

The council’s total capital expenditure for 2011/12 including amounts accrued for works completed but not paid for at 31st March 2012 was £35,056,000 (£62,718,000 in 2010/11). The sources of finance to fund this expenditure included Government grants and contributions of £27,210,000 (£37,684,000 in 2010/11) which includes £8,092,000 Major Repairs Allowance, supported borrowing of £4,242,000 (£14,956,000 in 2010/11). The balance of £3,604,000 (£10,079,000 in 2010/11) came from capital receipts, revenue contributions prudential borrowing and finance leases. Full details of capital expenditure and financing can be found in note 23 to the Financial Statements. Capital commitments total £10,500,000 and include a new swimming pool and facilities at Wolverton swimming pool and a new Community Pavilion in Broughton. Full details of the council’s capital commitments can be found in note 20 to the Financial Statements. 8. SIGNIFICANT PROVISIONS, CONTINGENCIES AND WRITE-OFFS

The Council has three significant provisions held on the Balance Sheet as at 31st March 2012: • Heating and Utilities Provision – This has been set aside to cover the cost of potential

refunds to sheltered area tenants and leaseholders in respect of over recovered utility costs;

• Overpaid Benefit Provision – The council has created this provision to meet the cost of

any overpaid housing benefits currently recovered through a reduction in ongoing benefit payments, which become unrecoverable due to a change in tenant circumstances, and:

Explanatory Foreword

12

• Secklow Gate Bridge - Following a fire under the bridge during 2010, a provision was created to account for the possibility that the third party insurance company would not pay the full costs incurred for the repair work.

Further details of the provisions can be found in Note 30 to the financial statements. The council discloses a number of contingent gains and losses in note 41 to the financial statements. The most significant disclosure relates to the overage due to the council as and when properties built on the Radcliffe School land are sold. There have been no significant write offs during 2011/12. 9. IMPACT OF CURRENT ECONOMIC CLIMATE

Two key areas affected by the economic downturn are housing asset valuations and a decline in the growth of the Council Tax base. The reduction in Housing Asset Valuations was recognised in an 18.9% deflation adjustment to 2008/09 based upon Housing Price Index data for Milton Keynes. A review of the same data indicates that land values have stabilised and that no further adjustment is necessary for 2011/12. The process for calculating the tax base for forthcoming years has been revised since 2009 to take prudent account of the decline in the level of house-building. In addition, the level of balances held in both the General Fund and Housing Revenue Account are reviewed annually as part of the budget setting process to ensure that they are adequate to meet possible fluctuations in income and expenditure during the forthcoming year. Reserves have been created to mitigate the possible impact of change programmes agreed by the council to meet shortfalls in funding or changes in government funding streams. 10. PROCUREMENT OF SERVICES

The council entered into a long term (twelve year) contract with Hyder Business Services (HBS), now trading as Mouchel Business Services, with effect from 1st January 2004 to provide a wide range of functions across eighteen service streams including Finance, Human Resources, IT, Revenues and Benefits. The council has retained a client/core team for these functions and a team has been created to monitor the overall performance of the contract. Full details of all long term contracts, including further details of the contract with Mouchel, can be found in note 37 to the Financial Statements.

Accounting Policies

13

INDEPENDENT AUDITOR’S REPORT TO THE MEMBERS OF MILTON KEYNES COUNCIL Opinion on the Authority financial statements I have audited the financial statements of Milton Keynes Council for the year ended 31 March 2012 under the Audit Commission Act 1998. The financial statements comprise the Movement in Reserves Statement, the Comprehensive Income and Expenditure Statement, the Balance Sheet, the Cash Flow Statement, the Housing Revenue Account Income and Expenditure Statement, the Movement on the Housing Revenue Account Statement and Collection Fund and the related notes. The financial reporting framework that has been applied in their preparation is applicable law and the CIPFA/LASAAC Code of Practice on Local Authority Accounting in the United Kingdom 2011/12. This report is made solely to the members of Milton Keynes Council in accordance with Part II of the Audit Commission Act 1998 and for no other purpose, as set out in paragraph 48 of the Statement of Responsibilities of Auditors and Audited Bodies published by the Audit Commission in March 2010. Respective responsibilities of the Chief Finance Officer and auditor As explained more fully in the Statement of Responsibilities, the Chief Finance Officer is responsible for the preparation of the Statement of Accounts, which includes the financial statements, in accordance with proper practices as set out in the CIPFA/LASAAC Code of Practice on Local Authority Accounting in the United Kingdom, and for being satisfied that they give a true and fair view. My responsibility is to audit and express an opinion on the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require me to comply with the Auditing Practices Board’s Ethical Standards for Auditors. Scope of the audit of the financial statements An audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the Authority’s circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the Chief Finance Officer; and the overall presentation of the financial statements. In addition, I read all the financial and non-financial information in the explanatory foreword to identify material inconsistencies with the audited financial statements. If I become aware of any apparent material misstatements or inconsistencies I consider the implications for my report. Opinion on financial statements In my opinion the financial statements: • give a true and fair view of the financial position of Milton Keynes Council as at 31 March 2012 and of its expenditure and income for the year then ended; and • have been prepared properly in accordance with the CIPFA/LASAAC Code of Practice on Local Authority Accounting in the United Kingdom 2011/12.

Accounting Policies

14

Opinion on other matters In my opinion, the information given in the explanatory foreword for the financial year for which the financial statements are prepared is consistent with the financial statements. Matters on which I report by exception I report to you if: • in my opinion the annual governance statement does not reflect compliance with ‘Delivering Good Governance in Local Government: a Framework’ published by CIPFA/SOLACE in June 2007; • I issue a report in the public interest under section 8 of the Audit Commission Act 1998; • I designate under section 11 of the Audit Commission Act 1998 any recommendation as one that requires the Authority to consider it at a public meeting and to decide what action to take in response; or • I exercise any other special powers of the auditor under the Audit Commission Act 1998. I have nothing to report in these respects. Conclusion on Authority’s arrangements for securing economy, efficiency and effectiveness in the use of resources Respective responsibilities of the Authority and the auditor The Authority is responsible for putting in place proper arrangements to secure economy, efficiency and effectiveness in its use of resources, to ensure proper stewardship and governance, and to review regularly the adequacy and effectiveness of these arrangements. I am required under Section 5 of the Audit Commission Act 1998 to satisfy myself that the Authority has made proper arrangements for securing economy, efficiency and effectiveness in its use of resources. The Code of Audit Practice issued by the Audit Commission requires me to report to you my conclusion relating to proper arrangements, having regard to relevant criteria specified by the Audit Commission. I report if significant matters have come to my attention which prevent me from concluding that the Authority has put in place proper arrangements for securing economy, efficiency and effectiveness in its use of resources. I am not required to consider, nor have I considered, whether all aspects of the Authority’s arrangements for securing economy, efficiency and effectiveness in its use of resources are operating effectively. Scope of the review of arrangements for securing economy, efficiency and effectiveness in the use of resources I have undertaken my audit in accordance with the Code of Audit Practice, having regard to the guidance on the specified criteria, published by the Audit Commission in October 2011, as to whether the Authority has proper arrangements for: • securing financial resilience; and • challenging how it secures economy, efficiency and effectiveness. The Audit Commission has determined these two criteria as those necessary for me to consider under the Code of Audit Practice in satisfying myself whether the Authority put in place proper arrangements for securing economy, efficiency and effectiveness in its use of resources for the year ended 31 March 2012.

Accounting Policies

15

I planned my work in accordance with the Code of Audit Practice. Based on my risk assessment, I undertook such work as I considered necessary to form a view on whether, in all significant respects, the Authority had put in place proper arrangements to secure economy, efficiency and effectiveness in its use of resources. Conclusion On the basis of my work, having regard to the guidance on the specified criteria published by the Audit Commission in October 2011, I am satisfied that, in all significant respects, Milton Keynes Council put in place proper arrangements to secure economy, efficiency and effectiveness in its use of resources for the year ended 31 March 2012. Certificate I certify that I have completed the audit of the accounts of Milton Keynes Council in accordance with the requirements of the Audit Commission Act 1988 and the Code of Audit Practice issued by the Audit Commission. Mick West District Auditor Audit Commission Unit 5, Isis Business Centre Horspath Road Cowley, Oxford OX4 2RD 26 September 2012

Accounting Policies

16

1. THE COUNCIL’S RESPONSIBILITIES

The council is required: a) to make arrangements for the proper administration of its financial affairs and to

secure that one of its officers has the responsibility for the administration of those affairs. In this council, that officer is the Chief Finance Officer;

b) to manage its affairs to secure economic, efficient and effective use of resources and safeguard its assets;

c) to approve a statement of accounts.

On behalf of the council:

2. THE RESPONSIBILITIES OF THE CHIEF FINANCE OFFICER

The Chief Finance Officer is responsible for the preparation of the council’s Statement of Accounts in accordance with proper practices as set out in the CIPFA/LASAAC Code of Practice on Local Authority Accounting in the United Kingdom (“the Code”). In preparing this Statement of Accounts, the Chief Finance Officer has: a) selected suitable accounting policies and then applied them consistently; b) made judgements and estimates that were reasonable and prudent; c) complied with the Local Authority Code.

The Chief Finance Officer has also: a) kept proper accounting records which are up to date; b) taken reasonable steps for the prevention and detection of fraud and other

irregularities. The Statement of Accounts provides a true and fair view of the council’s financial position of the authority at the reporting date, and of its income and expenditure for the year ended 31st March 2012.

Accounting Policies

17

1. GENERAL PRINCIPLES

The Statement of Accounts summarises the council’s transactions for the 2011/12 financial year and its position at the year-end of 31st March 2012. The authority is required to prepare an annual Statement of Accounts by the Accounts and Audit Regulations 2011 which those regulations require to be prepared in accordance with proper accounting practices. These practices primarily comprise the Code of Practice on Local Authority Accounting in the United Kingdom 2011/12 and the Service Reporting Code of Practice (SeRCOP) 2011/12 supported by International Financial Reporting Standards (IFRS) and statutory guidance issued under section 12 of the 2011 Act. The accounting policies have been applied consistently in dealing with items considered material to present a true and fair view of the financial position and transactions of the council. 2. ACCRUALS OF INCOME AND EXPENDITURE

Activity is accounted for in the year that it takes place, not simply when cash payments are made or received. In particular:

• Revenue from the sale of goods is recognised when the authority transfers the

significant risks and rewards of ownership to the purchaser and it is probable that economic benefits or service potential associated with the transaction will flow to the authority;

• Revenue from the provision of services is recognised when the authority can measure reliably the percentage of completion of the transaction and it is probable that economic benefits or service potential associated with the transaction will flow to the authority;

• Supplies are recorded as expenditure when they are consumed – where there is a gap between the date supplies are received and their consumption; they are carried as inventories on the Balance Sheet;

• Works are charged as expenditure when they are completed, before which they are carried as works in progress on the Balance Sheet;

• Interest payable on borrowings and receivable on investments is accounted for on the basis of the effective interest rate for the relevant financial instrument rather than the cash flows fixed or determined by the contract;

• Where income and expenditure have been recognised but cash has not been received or paid, a debtor or creditor for the relevant amount is recorded in the Balance Sheet. Where it is doubtful that debts will be settled, the balance of debtors is written down and a charge made to revenue for the income that might not be collected;

• Payment of wages to weekly paid employees is included in the accounts on the basis of a 52-week year, except in the case of Homecare staff where wages have been accrued. This accounting treatment, other than in respect of Homecare staff, is not in accordance with the Code of Practice, although any difference is not considered material. Similarly, issues from the council’s stores and all other internal recharging systems have been treated in the same way;

Accounting Policies

18

• Annual leave and flexi-time that has not been taken at 1st March is accrued and full details can be found in Accounting Policy note 9 – Employee Benefits.

3. ACQUIRED AND DISCONTINUED OPERATIONS

IFRS5 defines a discontinued operation as a component of an entity that either has been disposed of or is classified as held for sale, and: • represents either a separate major line of business or a geographical area of

operations, and; • is part of a single co-ordinated plan to dispose of a separate major line of business or

geographical area of operations, or; • is a subsidiary acquired exclusively with a view to resale and the disposal involves loss

of control. The surplus or deficit on discontinuing the operation is presented as a single amount on the face of the Comprehensive Income and Expenditure Statement where applicable. Detailed disclosure of revenue, expenses, surplus or deficit and related items is presented as a note to the Financial Statements where applicable, however, there were no operations discontinued or acquired during 2011/12 and therefore no disclosures are required.

4. BACK PAY ARISING FROM UNEQUAL PAY CLAIMS

The council has no current claims in respect of Equal Pay legislations, and therefore no provision has been made. However, the issue is disclosed as a contingent liability in Note 41 to the Financial Statements. 5. CAPITAL RECEIPTS

Receipts from the sale of assets are recorded in the accounts in accordance with normal accounting practice. Under regulations introduced from April 2004 the council is required to pay a percentage of receipts from the sale of housing assets to the Department for Communities and Local Government. This percentage is 75% for dwellings and 50% for any other interest in housing land.

Accounting Policies

19

6. CASH AND CASH EQUIVALENTS

Cash is represented by cash in hand and deposits with any financial institution repayable without penalty on notice of not more than 24 hours. Cash equivalents are investments held for cash flow purposes that mature in three months or less from the date of acquisition and that are readily convertible to known amounts of cash with insignificant risk of change in value. In the Cash Flow Statement, cash and cash equivalents are shown net of bank overdrafts that are repayable on demand and that form an integral part of the council’s cash management.

7. CHARGES TO REVENUE FOR THE USE OF NON-CURRENT ASSETS

Service revenue accounts and support services are debited with the following amounts for all fixed assets used in the provision of their services to record the real cost of holding those assets during the year: • Depreciation attributable to the assets used by the relevant service; • Impairment losses attributable to the clear consumption of economic benefits on

tangible fixed assets used by the service and other losses where there are no accumulated gains in the Revaluation Reserve against which they can be written off;

• Amortisation of intangible fixed assets attributable to the service.

The charge made to the Housing Revenue Account is calculated in accordance with the Item 8 Credit and Item 8 Debit (General) Determination 2011/12. In addition, in March 2012 the council completed the necessary transaction under the move to HRA Self Financing in 2012/13. This transaction was treated in accordance with guidance issued by CIPFA in LAAP Bulletin 92. External interest payable is charged to the Financing and Investment Income and Expenditure section of the Comprehensive Income and Expenditure Statement. The council is not required to raise Council Tax to cover depreciation, impairment losses or amortisations; however, it is required to make an annual provision from revenue to contribute towards the reduction in its overall borrowing requirement calculated in accordance with statutory guidance. Depreciation, impairment and amortisations are therefore replaced by a revenue provision in the Movement in Reserves Statement so there is no impact on the level of Council Tax.

Accounting Policies

20

8. DONATED ASSETS

Donated assets transferred for nil consideration are recognised immediately at fair value as an asset on the Balance Sheet, unless any conditions of the transfer have not been met and the asset is credited to a Donated Assets Account. 9. EMPLOYEE BENEFITS

Short Term Employee Benefits Payable during Employment

Salaries, wages and employee related payments are recognised in the period in which the service is received from employees. The cost of annual leave entitlement earned but not taken by employees at the end of the period is recognised in the Financial Statements to the extent that employees are permitted to carry forward leave into the following period. Untaken leave is accrued on the basis of actual leave untaken at 31st March 2012 for non-school staff and a calculation of the accrued benefit for schools staff based on the number of days in each term. Employees are also entitled to flexi-time and any accrued hours at 31st March have been reflected in the accounts on the basis of actual hours accumulated by each employee.

Termination Benefits

Termination benefits are amounts payable as a result of a decision by the authority to terminate an officer’s employment before the normal retirement date or an officer’s decision to accept voluntary redundancy. Benefits are charged on an accruals basis to the Comprehensive Income and Expenditure Statement when the authority is demonstrably committed to the termination of the employment of an officer or group of officers or making an offer to encourage voluntary redundancy.

Post Employment Benefits - Local Government Pension Scheme

Employees of the council are entitled to become members of one of two separate pension schemes according to the terms of their employment: • The Teachers’ Pension Scheme, administered by Capita Teachers’ Pensions on behalf

of the Department for Children, Schools and Families (DCSF); • The Local Government Pension Scheme, administered by Buckinghamshire County

Council. Both schemes provide defined benefits to members (retirement lump sums and pensions), earned as employees worked for the council. However, the arrangements for the teachers’ scheme mean that liabilities for these benefits cannot be identified to the council. The teachers’ scheme is therefore accounted for as if it were a defined contributions scheme; no liability for future payments of benefits is recognised in the Balance Sheet and the Children and Education Services revenue account in the Comprehensive Income and

Accounting Policies

21

Expenditure Statement is charged with the employer’s contributions payable to teachers’ pensions in the year. The Local Government Scheme is accounted for as a defined benefits scheme. The liabilities of the Buckinghamshire pension scheme attributable to the council are included in the Balance Sheet on an actuarial basis using the projected unit method (i.e. an assessment of the future payments that will be made in relation to retirement benefits earned to date by employees, based on assumptions about mortality rates, employee turnover rates, etc, and projected earnings for current employees).

Liabilities are discounted to their value at current prices, using a discount rate of 1.6% (1.3% real). The discount rate for pension’s liabilities is calculated using the AA Corporate Bond Rate. The assets of the Local Government Pension Fund attributable to the council are included in the Balance Sheet at their fair value:

• Quoted Securities – Current Bid Price; • Unquoted Securities – Professional Estimate; • Unitised Securities – Current Bid Price; • Property – Market Value.

The change in the net pension’s liability is analysed into seven components:

• Current Service Cost – the increase in liabilities as result of years of service earned this

year, allocated in the Comprehensive Income and Expenditure Statement to the revenue accounts of services for which the employees worked;

• Past Service Cost – the increase in liabilities arising from current year decisions whose effect relates to years of service earned in earlier years, charged to the Net Cost of Services in the Comprehensive Income and Expenditure Statement as part of Non Distributed Costs;

• Interest Cost – the expected increase in the present value of liabilities during the year as they move one year closer to being paid, charged to Financing and Investment Income and Expenditure in the Comprehensive Income and Expenditure Statement;

• Expected Return on Assets – the annual investment return on the fund assets attributable to the council, based on an average of the expected long-term return, credited to Financing and Investment Income and Expenditure in the Comprehensive Income and Expenditure Statement;

• Gains/Losses on Settlements and Curtailments – the result of actions to relieve the council of liabilities or events that reduce the expected future service or accrual of benefits of employees, charged to the Cost of Services in the Comprehensive Income and Expenditure Statement as part of Non Distributed Costs;

• Actuarial Gains and Losses – changes in the net pensions liability that arise because events have not coincided with assumptions made at the last actuarial valuation or because the actuary has updated its assumptions, shown as a gain or loss in the Other Comprehensive Income and Expenditure section of the Comprehensive Income and Expenditure Statement;

• Contributions paid to the Buckinghamshire Pension Fund – cash paid as employer’s contributions to the pension fund.

Accounting Policies

22

The accounting treatment for pensions benefits is in accordance with International Financial Reporting Standard (IAS) 19. This is a complex accounting standard, but it is based on a simple principle – that the council has to account for accumulated retirement benefits earned at the Balance Sheet date, even if the actual benefits are paid out over many years into the future. These policies reflect the council’s commitment in the long term to increase contributions to make up any shortfall in attributable net assets in the pension fund.

In relation to retirement benefits, statutory provisions require the General Fund Balance to be charged with the amount payable by the council to the pension fund in year, not the amount calculated according to the relevant accounting standards. This means that there are appropriations to and from the Pensions Reserve to remove the notional debits and credits for retirement benefits and replace them with debits for the cash paid to the pension fund and any amounts payable to the fund but unpaid at the year end. Full disclosures in respect of the Local Government Pension Scheme can be found in note 42 to the Financial Statements.

Discretionary Benefits

The council also has restricted powers to make discretionary awards of retirement benefits in the event of any early retirements. Any liabilities estimated to arise as a result of an award to any member of staff (including teachers) are accrued in the year of the decision to make the award and accounted for using the same policies as are applied to the Local Government Pension Scheme.

10. EVENTS AFTER THE BALANCE SHEET DATE

Events after the Balance Sheet date are defined as events, which could be favourable or unfavourable, that occur between the end of the reporting period and the date that the Financial Statements are authorised for issue. Events can be classified as adjusting or non-adjusting, with definitions as follows: • Adjusting - An event after the reporting period that provides further evidence of

conditions that existed at the end of the reporting period, including an event that indicates that the going concern assumption in relation to the whole or part of the council is not appropriate;

• Non-Adjusting - An event which takes place after the reporting period that is indicative of a condition that arose after the end of the reporting period.

The council discloses details of any such events at Note 5 to the Financial Statements.

Accounting Policies

23

11. EXCEPTIONAL ITEMS AND PRIOR PERIOD ADJUSTMENTS

Exceptional items are included in the cost of the service to which they relate or on the face of the Comprehensive Income and Expenditure Statement if such a degree of prominence is required for a fair view of the accounts. A disclosure note is provided where the authority has any exceptional items in the Accounts. Prior period adjustments that are the result of corrections and adjustments arising from the use of estimates inherent in the accounting process are adjusted in the accounts in the year that they are identified. However, prior period adjustments arising from changes in accounting policies or from the correction of fundamental errors are accounted for by restating the comparative figures for the preceding period in the Statement of Accounts and notes and by adjusting the opening balance of reserves for the cumulative effect. Details of any Prior Period Adjustments are fully explained as a note to the accounts where applicable.

12. FINANCIAL INSTRUMENTS

Financial Liabilities:

Financial liabilities are initially measured at fair value and carried at amortised cost. Annual charges to the Comprehensive Income and Expenditure Statement for interest payable are based on the carrying amount of the liability, multiplied by the effective interest rate for the instrument. For most of the borrowings that the council has, this means that the amount presented in the Balance Sheet is the outstanding principal repayable and any accrued interest and interest charged to the Comprehensive Income and Expenditure Statement is the amount payable for the year in the loan agreement. Gains and losses on the repurchase or early settlement of borrowing are credited and debited to Financing and Investment Income and Expenditure in the Comprehensive Income and Expenditure Statement in the year of repurchase or settlement. Where a repurchase has taken place as part of the restructuring of the loan portfolio that involves the modification or exchange of existing instruments, the premium or discount is respectively deducted from or added to the amortised cost of the new or modified loan, and the write down to the Comprehensive Income and Expenditure Statement is spread over the life of the loan by an adjustment to the effective interest rate. Where premiums and discounts have been charged to the Comprehensive Income and Expenditure Statement, regulations allow the impact on the General Fund Balance to be spread over future years. The council has a policy of spreading the gain or loss over the term that was remaining on the loan against which the premium was payable or discount receivable when it was repaid. The reconciliation of amounts charged to the Comprehensive Income and Expenditure Statement to the net charge required against the General Fund Balance is managed by a transfer to or from the Movement in Reserves Statement, taken to or from the Financial Instrument Adjustment Account.

Accounting Policies

24

Debt Redemption:

The council sets aside a statutory amount each year from its General Fund revenue account for debt redemption, in the form of a Minimum Revenue Provision, as required by the Local Authority (Capital Finance and Accounting) regulations.

Minimum Revenue Provision

The council has charged 2011/12 statutory General Fund Minimum Revenue Provision (MRP) at 4% of the opening Capital Financing Requirement for all capital expenditure financed by borrowing incurred before 2008/09 and for all subsequent capital expenditure financed by supported borrowing. This is in line with Regulations implemented under the Local Government Act 2003. These Regulations have been supplemented by statutory guidance issued alongside the Local Authorities (Capital Finance and Accounting) (England) (Amendment) Regulations 2008. The Regulations place a duty on local authorities to make a prudent provision for debt redemption. The guidance sets out four options for the calculation of a prudent provision, with the first two being available only for supported expenditure. The other two options set out the methods for accounting for self-financed borrowing. The MRP for self-financed capital expenditure incurred in 2008/09 and beyond is calculated in accordance with Option 3 under which MRP is made in equal instalments over the expected life of the asset. The MRP calculation also provides for: • the repayment of capitalisation directions issued by the Secretary of State in respect of

expenditure incurred at Local Government Reorganisation; and • an adjustment in respect of commuted payments made to or for the benefit of the

council in 1992-1993. The one exception to this is that where assets are purchased for future development and it is anticipated that future sale proceeds will offset the cost, the repayment of debt will be funded from future capital receipts. In such cases MRP will not be applied.

Additional Debt Redemption:

In accordance with the Local Government Act 2003, the council may also choose to further redeem its outstanding loan debt by means of:

• additional revenue contributions; • use of capital receipts; • use of the Major Repairs Allowance.

Debt Restructuring:

The council has, on occasions when satisfactory market conditions prevail, restructured certain long term loans with the Public Works Loan Board. This results in either a premium being paid or a discount received and these are written down in accordance with current legislation (currently the Local Authorities (Capital Finance and Accounting) (Amendment)

Accounting Policies

25

(England) Regulations 2007 (Statutory Instrument 2007 No. 573) as amended by the Local Authorities (Capital Finance and Accounting) (England) (Amendment) Regulations 2008 (Statutory Instrument 2008 No. 414)).

Financial Assets:

Financial Assets are classified into two types:

• Loans and receivables – assets that have fixed or determinable payments but are not quoted in an active market;

• Available for Sale Assets – assets that have a quoted market price and/or do not have fixed or determinable payments:

• Financial assets at fair value through profit or loss – assets classed as derivatives.

Loans and Receivables:

Loans and receivables are initially measured at fair value and carried at amortised cost. Annual credits to the Comprehensive Income and Expenditure Statement for interest receivable are based on the carrying amount of the asset multiplied by the effective rate of interest for the instrument. For all of the loans the council has made, this means that the amount presented in the Balance Sheet is the outstanding principal receivable and any accrued interest and interest credited to the Comprehensive Income and Expenditure Statement is the amount receivable for the year in the loan agreement. Where interest relates to 2011/12 which has not been paid by the 31st March 2012 this amount has been accrued and can be seen as part of the borrowing repayment on demand or within excess of 12 months.

Available for sale assets:

The council does not hold any available for sale financial assets.

Impairment of Financial Assets:

Where assets are identified as being impaired because of a likelihood arising from a past event then the payment due under contract will not be made, the asset is written down and a charge made to the Comprehensive Income and Expenditure Statement. Any gains or losses that arise on the derecognising of the asset are credited or debited to the Comprehensive Income and Expenditure Statement.

Accounting Policies

26

13. FOREIGN CURRENCY TRANSLATION

Where the authority has entered into a transaction denominated in a foreign currency, the transaction is converted into sterling at the exchange rate applicable on the date the transaction was effective. Where material amounts in foreign currency are outstanding at the year-end, they would be reconverted at the spot exchange rate at 31st March. Resulting gains or losses would be recognised in the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement. However, in 2011/12 foreign currency transactions of the council are not considered to be material.

14. GOVERNMENT GRANTS AND OTHER CONTRIBUTIONS

Whether paid on account, by instalments or in arrears, government grants and third party contributions and donations are recognised as income at the date that the authority satisfies the conditions of entitlement to the grant/contribution, there is reasonable assurance that:

• The authority will comply with the conditions attached to the payments; and • The grants or contributions will be received.

Amounts recognised as due to the council are not credited to the Comprehensive Income and Expenditure Statement until conditions attached to the grant or contribution have been satisfied. Conditions are stipulations that specify that the future economic benefits or service potential embodied in the asset acquired using the grant or contribution are required to be consumed by the recipient as specified, or future economic benefits or service potential must be returned to the transferor. Monies advanced as grants and contributions for which conditions have not been satisfied are carried in the Balance Sheet as creditors. When conditions are satisfied, the grant or contribution is credited to the relevant service line (for attributable revenue grants and contributions) or Taxation and Non-Specific Grant Income line (for non-ring fenced revenue grants and all capital grants) in the Comprehensive Income and Expenditure Statement. Where capital grants are credited to the Comprehensive Income and Expenditure Statement, they are reversed out of the General Fund Balance in the Movement in Reserves Statement. Where the grant has yet to be used to finance capital expenditure, it is posted to the Capital Grant Unapplied Reserve. Where it has been applied, it is posted to the Capital Adjustment Account. Amounts in the Capital Grants Unapplied Reserve are transferred to the Capital Adjustment Account once they have been applied to fund capital expenditure.

Accounting Policies

27

15. HERITAGE AND COMMUNITY ASSETS

The council’s collection of Heritage Assets is identified under the following categories: • Historical Buildings & Archaeological Sites • Museum & Archive Collections • Arts Collection • Civic Insignia These are assets with historical, artistic, scientific, technological, geophysical or environmental qualities that are held and maintained principally for their contribution to knowledge and culture. Heritage Assets acquired or constructed in 2011/12 are recognised and measured (including the treatment of revaluation gains and losses) in accordance with the council’s accounting policy on Property, Plant and Equipment. However, the measurement bases in relation to each category of Heritage Assets held prior to 2011/12 are detailed below. The accounting policies for Heritage Assets that are deemed to include elements of intangible heritage assets are also presented below. The council’s collection of Heritage Assets is accounted for as follows: Historical Buildings & Archaeological Sites The council owns a variety of Historical Buildings and Archaeological Sites. Many of these are ‘designated heritage assets’ e.g. scheduled ancient monuments, listed buildings or assets within conservation areas and are of national significance. In addition to this, there are others that are ‘non-designated heritage assets’, i.e. those which have a degree of significance meriting consideration in planning decisions but are of local significance rather than national. The nature, scale and significance of these assets is not confined to a particular type or size and incorporates a range of listed buildings. Scheduled ancient monuments also involve a similarly broad range, including public infrastructure such as road bridges. Historical Buildings and Archaeological Sites are assessed by the Property Services Department with regards to meeting the CIPFA Code of Practice definition of Heritage Assets and donated assets. Insurance valuations are considered to establish whether their application would be appropriate and also whether a market value exists for each asset. The council undertakes a valuation where the information is available and appropriate. In most cases the council does not consider that comparable market value information can be obtained for its historical buildings and archaeological sites or that insurance valuations

Accounting Policies

28

can be used in order for values to be established. This is because of the nature of the assets held. Museum & Archive Collections The Museum collection consists of just less than 5,000 collection items and relates to the significant history of Milton Keynes from pre-historic to present day. The Museum collection is held at Buckinghamshire’s County Museum. The Archive collection consists of deposited council and predecessor collections which constitutes a rich archival history of the area. The archives are held at the Centre for Buckinghamshire Studies, Aylesbury. The council currently adheres to the collecting policies of Buckinghamshire County Museum and the Centre for Buckinghamshire Studies (County Archives) who collect on the council’s behalf. The council does not consider that reliable cost or valuation information can be obtained for its museum and archive collections and would involve a disproportionate cost in comparison to the benefits to the users of the council’s financial statements. This is because of the diverse nature of the assets held and lack of comparable market values. Consequently the council does not recognise the assets on the Balance Sheet. Museum objects are usually donated and information is held at the Buckinghamshire County Museum. Archive material is generally deposited, not donated and relevant data is held on accession registers. Arts Collection The council’s public art collection is made up of in the region of 100 items of works of art. The collection includes sculptures, paintings, prints and artists designs integrated in public spaces and buildings. Reliable cost or valuation information is not readily available, the council believes that obtaining valuations for these items requires significant investment and currently the cost is prohibitive. However, the council acknowledges the need for a valuation review and plans are in place to undertake this work in the future. Consequently the council does not recognise these assets on the balance sheet this financial year but wishes to do so in future years. The council does not have any items in its arts collection which it can verify as being donated. Civic Insignia The council’s Mayoral Insignia comprises assets which are pertinent to the council’s position as a Borough i.e. chains of office for the Mayor, Deputy Mayor and respective consorts.

Accounting Policies

29

Reliable cost or valuation information is not readily available and the council believes that the costs involved in obtaining this information are not commensurate with the benefits to the users of the financial statements. Consequently the council does not recognise these assets on the balance sheet. The council does not have any items in its civic Insignia collection which it can verify as being donated. 16. INSURANCE

To obtain insurance cover in the most cost effective manner the council arranges its insurance with a system of internal financing of claims (a substantial policy excess applies) and external cover with a recognised insurance market. Internal funds have been maintained to cover those claims that fall below the policy excess. These funds are based on the total potential liability that could accrue up to 31st March 2012. Some risks carry a lower policy excess and claims that fall below this amount are met from revenue as they arise. External cover is provided by way of premiums paid to the council’s Insurers. The nature of risks covered by the internal arrangements is shown below.

Risk Maximum Cover per Claim

Employers Liability £50,000 - Amounts in excess of this are covered externally.

Third Party £50,000 - Amounts in excess of this are covered externally.

Fire Damage £50,000 - Amounts in excess of this are covered externally.

Loss of School Contents £50,000 - Amounts in excess of this are covered externally.

Cash Loss The first £100 is met by the service concerned - amounts in excess of this are covered externally.

Loss of Computers The first £100 is met by the service concerned - amounts in excess of this are covered externally.

17. INTANGIBLE FIXED ASSETS

Expenditure on assets that do not have physical substance but are identifiable and controlled by the council (e.g. software licences) is capitalised when it will bring benefits to the council for more than one financial year. All intangible assets are recognised if it is probable that the expected future benefits attributable to the asset will flow to the council. Internally generated assets are recognised where the required criteria are met in line with the International Financial Reporting Standards Code of Practice.

Accounting Policies

30

All Intangible Fixed Assets are included at historic cost and amortised on a straight line basis, over their economic lives from the year following acquisition. The economic lives are reviewed at the end of each reporting period and revised if necessary.

18. INTEREST IN COMPANIES

The Comprehensive Income and Expenditure Statement reflects all of the council’s revenue activities. The Balance Sheet has been prepared by aggregating the account balances of all of the council’s services and funds.

The council has considered whether or not Group Accounts should be prepared and has concluded that it has no material interest in companies and other entities that could be regarded as subsidiaries, associates or joint controlled entities and would require the council to prepare group accounts.

The council is invited to appoint Members to many entities of local, regional and national significance. These appointments have been examined; together with Members own declarations of interest, along with those of all Assistant Directors, Heads of Service and Corporate Leadership Team. No material reportable interests were identified. Minority interests in companies are detailed in note 38 to the Financial Statements.

Significant contractual relationships are disclosed in note 37 to the Financial Statements.

19. INVENTORIES, WORK IN PROGRESS AND LONG TERM CONTRACTS

Inventories are included in the Balance Sheet at the lower of cost and net realisable value. The cost of inventories is assigned using the (First In, First Out/Weighted Average) costing formula.

Long term contracts are accounted for on the basis of charging the surplus or deficit on the provision of services with the value of works and services received under the contract during the financial year.

Certain repair works undertaken by the council are rechargeable to private concerns and individuals. Incomplete works and works not yet recharged are accounted for at cost. 20. INVESTMENT PROPERTIES

Investment property is property (land or a building, or part of a building, or both) that is held solely to earn rentals or for capital appreciation or both. An investment property is recognised as an asset when and only when:

Accounting Policies

31

• It is probable that the future economic benefits that are associated with the investment property will flow to the entity, and;

• The cost or fair value of the investment property can be measured reliably.

Investment properties are measured at cost initially. The cost of an investment property includes its purchase price, transaction costs and directly attributable expenditure. After initial recognition, investment properties are measured at fair value. The fair value of an investment property reflects market conditions at the Balance Sheet date. Investment properties are not depreciated but are revalued annually according to market conditions at the end of each year. 21. LANDFILL ALLOWANCE SCHEMES

The Waste and Emissions Trading Act 2003 places a duty on waste disposal authorities to reduce the amount of biodegradable municipal waste (BMW) disposed to landfill. In April 2005 it introduced a trading scheme, which allocates tradable landfill allowances. The Landfill Allowances Trading Scheme gives rise to an asset for allowances held; grant income and a liability for actual BMW landfill usage. Full details of the Landfill Allowances Trading Scheme can be found in Note 19 to the Financial Statements. 22. LEASES

Leases are classified as finance leases where the terms of the lease transfer substantially all of the risks and rewards incidental to ownership of the property, plant or equipment from the lessor to the lessee. All other leases are classified as operating leases. Where a lease covers both land and buildings, the land and buildings elements are considered separately for classification. Arrangements that do not have the legal status of a lease but convey a right to use to use an asset in return for payment are accounted for under this policy where fulfilment of the arrangement is dependant on the use of specific assets. The Authority as Lessee Finance Leases Property, plant and equipment held under finance leases is recognised on the Balance Sheet at the commencement of the lease at its fair value measured at the lease’s inception (or the present value of the minimum lease payments, if lower). The asset recognised is matched by a liability for the obligation to pay the Lessor. Initial direct costs of the authority are added to the carrying amount of the asset. Premiums paid on entry into a lease are applied to writing down the lease liability. Contingent rents (where applicable) are charged as expenses in the periods in which they are incurred.

Accounting Policies

32

Lease payments are apportioned between:

• A charge for the acquisition of the interest in the property, plant or equipment – applied to write down the lease liability, and:

• A finance charge (debited to the Financing and Investment Income and Expenditure line in the Comprehensive Income and Expenditure Statement).