OECD CONFERENCE ON CORPORATE RESPONSIBILITY Paris, 15 th March 2009 Bruno Levesque, Principal...

19

OECD CONFERENCE OECD CONFERENCE ON CORPORATE ON CORPORATE RESPONSIBILITY RESPONSIBILITY Paris, 15 Paris, 15 th th March 2009 March 2009 Bruno Levesque, Principal Administrator, Financial Bruno Levesque, Principal Administrator, Financial Education Education 1

-

Upload

alannah-ramsey -

Category

Documents

-

view

218 -

download

0

Transcript of OECD CONFERENCE ON CORPORATE RESPONSIBILITY Paris, 15 th March 2009 Bruno Levesque, Principal...

OECD CONFERENCEOECD CONFERENCEON CORPORATE ON CORPORATE RESPONSIBILITYRESPONSIBILITY

Paris, 15Paris, 15thth March 2009 March 2009

Bruno Levesque, Principal Administrator, Financial Bruno Levesque, Principal Administrator, Financial EducationEducation

1

OECD programme on financial education

• Recognising the need for policymakers and other relevant stakeholders to meet the objective of improving financial education, the OECD launched in 2oo3 its “international programme on financial education”

• Under the aegis of the OECD Committee on Financial Markets and the OECD Insurance and Private Pensions Committee

2

OECD Financial Education Programme

--Tree pillars--1. Analytical

– Surveys, reports and publications on a broad range of financial education issues and topics

2. Standard setting- OECD Principles and Good Practices for Financial Education

and Awareness (2005)- Good Practices for Enhanced Risk Awareness and Education

on Insurance Issues (2008)- Good Practices for Financial Education Relating to Private

Pensions (2008)- Good Practices on Financial Education and Awareness

Relating to Credit (May 2009)

3. International cooperation– Conferences and events – International Network and Gateway

3

www.financial-education.org

4

What is financial What is financial education?education?

5

Financial Education

6

Why is financial Why is financial education and education and awareness so awareness so

important?important?7

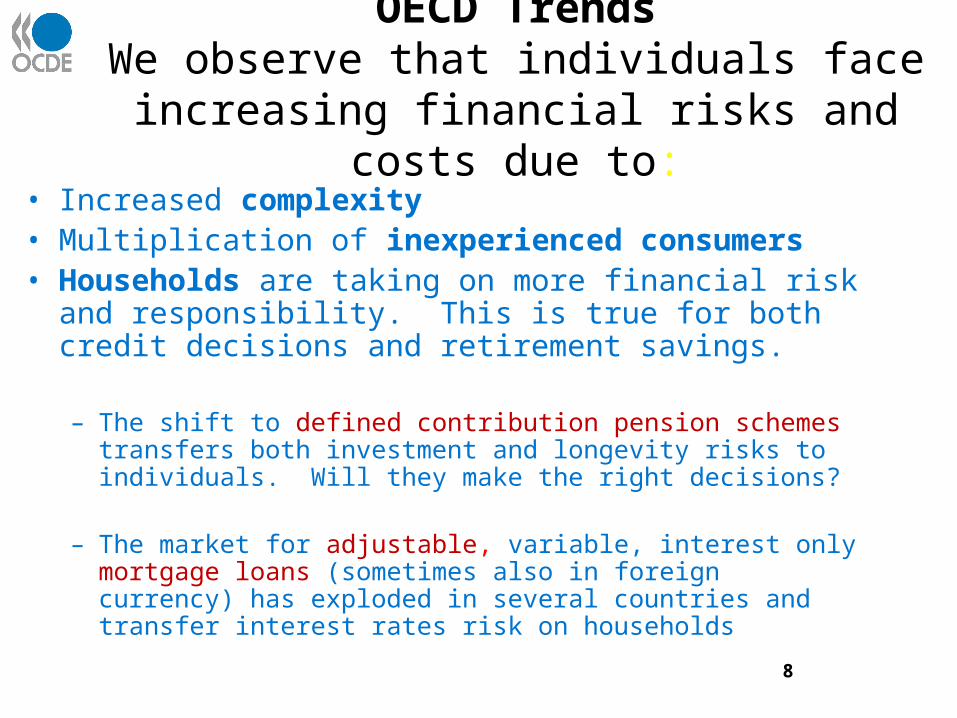

OECD TrendsWe observe that individuals face increasing

financial risks and costs due to:

• Increased complexity• Multiplication of inexperienced consumers• Households are taking on more financial risk

and responsibility. This is true for both credit decisions and retirement savings.

– The shift to defined contribution pension schemes transfers both investment and longevity risks to individuals. Will they make the right decisions?

– The market for adjustable, variable, interest only mortgage loans (sometimes also in foreign currency) has exploded in several countries and transfer interest rates risk on households

8

Consumers are clearly not prepared to face these challenges and risks

• Worldwide surveys show the level of financial literacy is low in all countries, including in developed countries.

• Worse: consumers often overestimate their financial understanding and thus do not seek to improve it

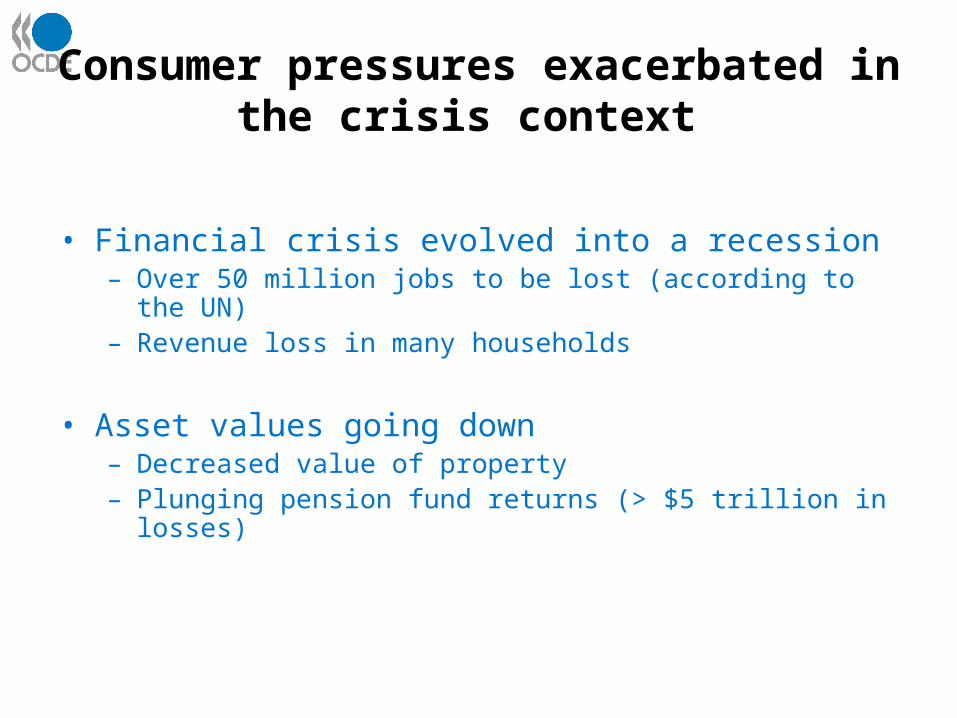

Consumer pressures exacerbated in the crisis context

• Financial crisis evolved into a recession– Over 50 million jobs to be lost (according to the UN)– Revenue loss in many households

• Asset values going down– Decreased value of property– Plunging pension fund returns (> $5 trillion in losses)

The crisis• Causes are multifaceted:

--solvency-- accounting rules--deleveraging-- regulatory arbitrage-- liquidity --securitisation--rating agencies-- etc…

11

Responses• Resulting initiatives are multidimensional:

-- Incentives

-- Macro-prudential reforms

-- Corporate governance

-- Taxation -- Business environment and competition policy

-- Trade and investment

-- Macroeconomic, fiscal and labour market policies• Particularity of OECD’s strategic response :

– Recognizes the lack of financial education and awareness of both individuals and institutions

– Proposes consumer protection and education policy actions

12

OECD strategic response to the crisis

Two key consumer-related deliverables:1. Survey on financial education and the crisis

conducted within the INFE framework2. OECD Recommendation on Good Practices on

Financial Education and Awareness Relating to Credit

1. Results of the survey on financial education and the crisis

• Lack of financial literacy is one of the contributors to the crisis and in particular of its aggravation

• The crisis and its consequences have highlighted the need for enhanced level of accountability of financial institutions vis-à-vis their clients and consumers

• They have also raised awareness on the need for increased financial literacy and capability of households and policymakers – The crisis as a « teachable moment »– The crisis as a trigger for policy actions in the financial education

areaFinancial literacy and capability is now considered as :• one of the pillars of financial stability• an essential life-skill for households

A series of financial awareness and education policy measures have been introduced to address the effects of the crisis

2. OECD Good Practices on Financial Education and

Awareness Relating to Credit

• Adopted in May 2009 as a Council Recommendation

• Covers main stakeholders’ roles and responsibilities in enhancing public awareness and capability on credit issues, including roles of:– OECD– Governments and other Authorities – Other social and business partners NGOs– Credit market players

15

Role of credit market players

1. Role should be well defined and part of their good governance

2. Liable for ensuring staff’s training, qualification and competence

3. Use of “due diligence” standards to assess consumers’ profiles should be mandatory for all credit providers as part of the underwriting process

16

Role of credit market players (cont’d)

4. Information disclosed should be distinguished from advertising and promotion.

5. Responsible for ensuring consumers’ understanding of products they purchase

6. Should ensure suitable and easily accessible consumer information about their right to recourse.

7. Intermediaries or third parties should have same liabilities and obligations as any credit market participant.

17

Conclusion

• This crisis represents a unique teachable moment for all stakeholders on the importance of financial education and awareness.

• Financial education sits alongside effective regulation as a consumer protection measure and is not a replacement for a safe and fair market or for effective regulation.

• The OECD will continue to play a leadership role in informing policy development in the area of financial education and awareness. A significant area of research will focus on the roles and responsibilities of financial service providers, especially intermediaries.

18