HOLD - Ascendas REIT - Investor Relations: IR Homeir.ascendas-reit.com/misc/Ascendas...

30

MITA No. 013/06/2009 Please refer to the important disclosures at the back of this document. Ascendas REIT Strong asset portfolio. Ascendas REIT (A-REIT) is Singapore's first and largest business space and industrial REIT, with a portfolio of 90 properties and book value of about S$4.7 billion. The key strength of A-REIT lies in its strong asset portfolio. We like A-REIT for its balance exposure to different groups of industrial properties, balance mix of single and multi-tenanted properties and diversified base of quality tenants. Growth via property development. A-REIT's expertise and engagement in industrial property development can also enhance shareholder value and further strengthen its asset portfolio. With just one ongoing development project at the moment, this leaves A-REIT with significant headroom of S$280.6m for new development projects. Limited impact from negative rental reversions. Even though some of A- REIT's assets could face negative rental reversions going forward, we believe that the impact on its portfolio as a whole would not be significant because the NLA of expiring leases is small compared to the total NLA of A-REIT's portfolio and the average existing rents of these expiring leases are not significantly higher than current market rents. Gearing level remains comfortable. Its balance sheet has been strengthened after two fund raising exercises this year. A-REIT successfully lowered its gearing level to 30.5% at the end of Sep 2009. The current gearing ratio provides a comfortable buffer from management's target gearing ratio of 40%. DPU to fall due to placement dilution. We expect A-REIT to deliver DPU of 12.86 S-cents for FY09/10. This is 15.3% lower than the FY08/09 DPU due to the dilution impact from the two placement exercises in 2009. For FY10/11, we expect DPU to remain steady and turn in marginal growth of 0.3% YoY to 12.9 S-cents. These translate to DPU yields of 6.84% and 6.86% for FY09/10 and FY10/11, respectively. Re-initiate A-REIT with HOLD; fair value estimate of S$1.76. We derive a fair value estimate of S$1.76 for A-REIT, which is pegged at par to our RNAV estimate. We like A-REIT for its stable dividend yield, diversified tenant base, long term leases and property development capability. Nevertheless, we re- initiate coverage on A-REIT with a HOLD rating on valuation ground. We advise investors to accumulate A-REIT at more attractive price levels around the range of S$1.60 to S$1.70. An undeniable leader in industrial space SINGAPORE Company Report 24 November 2009 Re-initiating Coverage HOLD S$1.88 Fair Value: S$1.76 Stock Code: Reuters: AEMN.SI ISIN Code A17U Bloomberg: AREIT SP Event: Re-initiate Coverage General Data Issued Capital (m) 1,870 Mkt Cap (S$m/US$m) 3515 / 2538 Major Shareholder Ascendas Land (19.23%) Free Float (%) 71.73 NTA per share (S$) 1.60 Daily Vol 3-mth (‘000) 7,523 52Wk High (S$) 1.950 52Wk Low (S$) 1.008 Foo Sze Ming (65) 6531 9810 e-mail: [email protected] Year to Gross Revenue Net Pty Income Distri Income DPU NAV Price/NAV Net Div Yield 31 Mar (S$m) (S$m) (S$m) (cents) (S$) (x) (%) FY 08 322.3 243.5 187.3 14.1 1.8 1.0 7.5 FY 09 396.5 296.6 210.9 15.2 1.6 1.2 8.1 FY 10F 413.4 322.5 240.4 12.9 1.6 1.2 6.8 FY 11F 416.4 324.8 241.1 12.9 1.6 1.2 6.9

Transcript of HOLD - Ascendas REIT - Investor Relations: IR Homeir.ascendas-reit.com/misc/Ascendas...

MITA No. 013/06/2009

Please refer to the important disclosures at the back of this document.

Ascendas REIT

Strong asset portfolio. Ascendas REIT (A-REIT) is Singapore's first and

largest business space and industrial REIT, with a portfolio of 90 properties

and book value of about S$4.7 billion. The key strength of A-REIT lies in its

strong asset portfolio. We like A-REIT for its balance exposure to different

groups of industrial properties, balance mix of single and multi-tenanted

properties and diversified base of quality tenants.

Growth via property development. A-REIT's expertise and engagement in

industrial property development can also enhance shareholder value and further

strengthen its asset portfolio. With just one ongoing development project at

the moment, this leaves A-REIT with significant headroom of S$280.6m for

new development projects.

Limited impact from negative rental reversions. Even though some of A-

REIT's assets could face negative rental reversions going forward, we believe

that the impact on its portfolio as a whole would not be significant because

the NLA of expiring leases is small compared to the total NLA of A-REIT's

portfolio and the average existing rents of these expiring leases are not

significantly higher than current market rents.

Gearing level remains comfortable. Its balance sheet has been

strengthened after two fund raising exercises this year. A-REIT successfully

lowered its gearing level to 30.5% at the end of Sep 2009. The current gearing

ratio provides a comfortable buffer from management's target gearing ratio of

40%.

DPU to fall due to placement dilution. We expect A-REIT to deliver DPU of

12.86 S-cents for FY09/10. This is 15.3% lower than the FY08/09 DPU due to

the dilution impact from the two placement exercises in 2009. For FY10/11,

we expect DPU to remain steady and turn in marginal growth of 0.3% YoY to

12.9 S-cents. These translate to DPU yields of 6.84% and 6.86% for FY09/10

and FY10/11, respectively.

Re-initiate A-REIT with HOLD; fair value estimate of S$1.76. We derive a

fair value estimate of S$1.76 for A-REIT, which is pegged at par to our RNAV

estimate. We like A-REIT for its stable dividend yield, diversified tenant base,

long term leases and property development capability. Nevertheless, we re-

initiate coverage on A-REIT with a HOLD rating on valuation ground. We advise

investors to accumulate A-REIT at more attractive price levels around the

range of S$1.60 to S$1.70.

An undeniable leader in industrial space

SINGAPORE Company Report

24 November 2009

Re-initiating Coverage

HOLD

S$1.88

Fair Value: S$1.76

Stock Code:Reuters: AEMN.SIISIN Code A17UBloomberg: AREIT SP

Event: Re-initiate Coverage

General Data

Issued Capital (m) 1,870

Mkt Cap (S$m/US$m) 3515 / 2538

Major Shareholder

Ascendas Land (19.23%)

Free Float (%) 71.73

NTA per share (S$) 1.60

Daily Vol 3-mth (‘000) 7,523

52Wk High (S$) 1.950

52Wk Low (S$) 1.008

Foo Sze Ming(65) 6531 9810e-mail: [email protected]

Year to Gross Revenue Net Pty Income Distri Income DPU NAV Price/NAV Net Div Yield

31 Mar (S$m) (S$m) (S$m) (cents) (S$) (x) (%)

FY 08 322.3 243.5 187.3 14.1 1.8 1.0 7.5

FY 09 396.5 296.6 210.9 15.2 1.6 1.2 8.1

FY 10F 413.4 322.5 240.4 12.9 1.6 1.2 6.8

FY 11F 416.4 324.8 241.1 12.9 1.6 1.2 6.9

Page 2 24 November 2009

Ascendas REIT

Section A Investment Highlights 3

Section B Sector Outlook 5

Section C Asset Portfolio Analysis 8

Section D Capital Management 14

Section E Financials 16

Section F Peers Comparison 18

Section G Valuation 20

Section H Risk factors 23

Appendix 1 Background on A-REIT 24

Appendix 2 Trust Structure 25

Appendix 3 Asset Portfolio Summary 26

Table of Content

Page 3 24 November 2009

Ascendas REIT

Section A: Investment Highlights

Re-initiate A-REIT with HOLD; fair value estimate of S$1.76. We are

re-initiating coverage on A-REIT with a HOLD rating and fair value estimate

of S$1.76, which is pegged at par to our RNAV estimate. We like A-REIT

for its stable dividend yield, diversified tenant base, long term leases and

property development capability. Nevertheless, we re-initiate coverage on

A-REIT with a HOLD rating on valuation ground. We advise investors to

accumulate A-REIT at more attractive price levels around the range of S$1.60

to S$1.70.

Strong asset portfolio. One of the key strengths of A-REIT is its strong

asset portfolio. We like A-REIT for its balance exposure to different groups

of industrial properties, balance mix of single and multi-tenanted properties

and diversified base of quality tenants. A-REIT also holds security deposits

from tenants. On a portfolio basis, the weighted average security deposit

is 7 months of A-REIT's gross rental income. This protects A-REIT from

any defaults or early lease termination by tenants.

Growth via property development. A-REIT's expertise and engagement

in industrial property development can also enhance shareholder value and

further strengthen its asset portfolio. With just one ongoing development

project at the moment - the Built-to-Suit (BTS) for SingTel with an expected

development cost of S$175.4m, this leaves A-REIT with significant headroom

of S$280.6m for new development projects.

Limited impact from negative rental reversions in FY09/10 and FY10/

11. Even though negative rental reversions could affect A-REIT's portfolio of

flatted factories and logistics and distribution centres in FY09/10 and FY10/

11, we believe that the impact on A-REIT's portfolio as a whole would not

be significant because the NLA of expiring leases is small when compared

to the total NLA of A-REIT's portfolio and the average existing rents of

these expiring leases are not significantly higher than the current market

rents.

Gearing level remains comfortable. With the two fund raising exercises,

A-REIT has successfully lowered its gearing level from 42.2% at the end of

2008 to 30.5% at the end of Sep 2009. The current gearing ratio also

provides a comfortable buffer from management's target gearing ratio of

40%. A-REIT is able to tolerate a further 23.9% decline (S$1,120m) in the

valuation of its property portfolio before breaching its target gearing level.

This provides a very comfortable buffer, in our view.

DPU to fall due to placement dilution. We expect A-REIT to deliver

DPU of 12.86 S-cents for FY09/10. This is 15.3% lower than the FY08/09

DPU and is due to the dilution impact from the two placement exercises in

2009. For FY10/11, we expect DPU to remain steady and turn in marginal

growth of 0.3% YoY to 12.9 S-cents. These translate to DPU yields of

6.84% and 6.86% for FY09/10 and FY10/11, respectively.

Page 4 24 November 2009

Ascendas REIT

Key risk factors. Some of the key risk factors in investing in A-REIT include

its exposure to the economic conditions and government policy in Singapore,

competition in a highly fragmented industrial property market and potential

conflict of interests between A-REIT and the Ascendas Group.

Page 5 24 November 2009

Ascendas REIT

Section B: Sector Outlook

Industrial property prices had fallen 15%-24% from peak. According

to URA data, median prices and rents of multiple user factories had already

fallen sharply by 21.2% and 15.3% respectively since peaking in 3Q08.

For multiple user warehouses, prices and rents had also fallen by 24.3%

and 20.6% respectively over the same period. The credit crisis and slowdown

in economic activities had resulted in the decline in demand for industrial

space, which fell to the lowest since 2007, as corporates scaled back on

expansion plans in light of the uncertain outlook. However, as global

economies emerged out of the crisis, the pace of decline in industrial property

prices and rents had slowed down since 1Q09.

Exhibit 2: Median price and median rent for warehousing space

Source: URA

350

370

390

410

430

450

470

490

510

530

550

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

3Q

Pri

ce

(S

$ p

sf)

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

Re

nta

l (S

$ p

sf

pm

)

Median price (LHS) Median rent (RHS)

Exhibit 1: Median price and median rent for factory space

Source: URA

250

270

290

310

330

350

370

390

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

3Q

Pri

ce

(S

$ p

sf)

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

Re

nta

l (S

$ p

sf

pm

)

Median price (LHS) Median rent (RHS)

Page 6 24 November 2009

Ascendas REIT

Supply outlook for factory space remains a concern. According to

URA, there will be 24.9m sq ft of factory space completing between 2010

and 2013, out of which 13.3m sq ft will be entering the market in 2010.

Although the oncoming supply of factory in 2010 will be lower than that in

2009, this figure is still significantly higher in comparison to the annual

supply of factory space between 2003 and 2008. On a positive note, as

much as 43% and 84% of the new supply of business and science park

space and industrial space have already been pre-committed. However,

the take-up rate of the remaining uncommitted space could still remain

slow unless there is a sustainable recovery in the global economy. We

estimate that vacancy rate for factory space could reach a peak of 9.2% in

2010, after which we expect to see a decline in vacancy rate on the back of

the decline in the pipeline of new factory space. For warehousing space,

we are more optimistic on this sector as the oncoming supply of new

warehousing space is expected to decline sharply in 2010 and 2011.

Exhibit 3: Supply and demand outlook for factory space

Source: URA, OIR estimates

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

F

20

10

F

20

11

F

20

12

F

20

13

F

GF

A (

mil

lio

n s

q f

t)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Va

ca

nc

y r

ate

(%

)Supply Demand Vacancy rate

Page 7 24 November 2009

Ascendas REIT

Exhibit 4: Supply and demand outlook for warehousing space

Source: URA, OIR estimates

0.0

1.0

2.0

3.0

4.0

5.0

6.0

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

F

20

10

F

20

11

F

20

12

F

20

13

F

GF

A (

mil

lio

n s

q f

t)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Va

ca

nc

y r

ate

(%

)

Supply Demand Vacancy rate

Page 8 24 November 2009

Ascendas REIT

Exhibit 5: A-REIT's exposure to different groups of industrial properties

Source: Company, OIR

Valuation as

at 31 Mar 09

(S$m)

% of total

portfolio Description

Business & Science Park* 1,441.6 31.7 Suburban office, corporate HQ buildings and R&D space

Hi-tech Industrial 946.7 20.8 High office content combined with high specifications industrial mixed-use space

Light Industrial & Flatted Factories 830.6 18.3 Low office content combined with manufacturing space

Logistics & Distribution Centres* 1,193.5 26.2 Warehousing and distribution centres

Warehouse Retail Facilities 137.0 3.0 Single-user retail and warehouse space

4,549.4 100.0

* Includes the development costs for the newly completed Expeditors Building and Plaza 8

Section C: Asset Portfolio Analysis

Balance exposure within different groups of industrial properties.

Within the industrial property group, there are different groups of industrial

properties that cater to different needs of the users (refer to Exhibit 5).

While the conventional industrial space is usually related to manufacturing

and storage uses, there are also industrial spaces that cater to research

and development purposes and also some with high office content that

acts as a substitute to the conventional office space. A-REIT's portfolio of

assets is well-diversified among the different groups of industrial properties

and this mitigates the risk of a slowdown in demand for any particular

group of industrial properties.

Balance mix of single and multi-tenanted properties improves

income stability. Single-tenanted buildings typically have long term leases

with stepped rental increases which provide greater income stability to A-

REIT. On the other hand, multi-tenanted buildings have shorter lease terms

and have more volatile income streams due to rental reversions which are

largely dependent on the economic cycle. Within A-REIT's asset portfolio,

46% of its portfolio value is attributable to single-tenanted sale-&-leaseback

buildings while the remaining 54% is attributable to multi-tenanted buildings.

This balance provides A-REIT with a component of income stability and

also a component of potential income growth from rental reversions.

Page 9 24 November 2009

Ascendas REIT

Exhibit 6: Balance mix of single and multi-tenanted properties

Source: Company

Mix of Sale-&-Leaseback vs Multi-tenanted Buildings

(% of total portfolio value)

Sale-&-

Leaseback, 46%Multi-tenanted

Buildings, 54%

Diversified base of strong tenants mitigates tenancy risk. A-REIT has

a diversified tenant base with about 900 tenants that include well-established

companies such as SingTel, Siemens, Hewlett Packard and Toll Asia. With

the exception of SingTel which contributes 5.9% of A-REIT's portfolio income,

no other single tenant account for more than 5% of A-REIT's total portfolio

income and the top 10 tenants account for about 26.5% of A-REIT's total

portfolio income. While tenancy risk for industrial landlord has heightened

in light of the weak manufacturing and global trade, A-REIT's strong tenant

base, coupled with its limited rental exposure to a single tenant, should

help to mitigate its tenancy risk profile.

Exhibit 7: Top 10 tenants

Source: Company

Sector % of portfolio income

Singtel Telecommunication 5.9

C&P Logistics 4.5

Creative Electronics 3.6

Cold Storage Retail 2.0

Siemens Multi-industry 2.0

SenKee Logistics Logistics 2.0

TT International Electronics, Logistics 1.8

Hewlett Packard Electronics 1.6

Toll Asia Logistics 1.6

Courts Megastore Retail 1.5

26.5

Page 10 24 November 2009

Ascendas REIT

Exhibit 8: Security deposit for sale & leaseback (SLB) properties

Source: Company

No of SLB properties

Weighted average no of

months rent as security

deposit*

Business & Science Parks 3 14

Hi-Tech Properties 7 7

Light Industrial 26 11

Logistics & Distribution Centres 14 9

Warehouse Retail Facilities 2 11

52 9.4

* Excluding cases where rental is paid upfront

Security deposits provide cushion against tenants default. For its sale-

&-leaseback properties, A-REIT holds security deposits ranging from 7 to

14 months (weighted average: 10 months). On a portfolio basis, the weighted

average security deposit is 7 months of A-REIT's gross rental income. The

higher amount of security deposits held for sale-&-leaseback properties

could protect A-REIT from any potential default by its sale-&-leaseback

tenants, which will have a greater impact on A-REIT's income (due to its

larger quantum) than a potential default by a tenant in a multi-tenanted

property. In the event of a default, rental income can be sustained by the

security deposit over the short term as A-REIT seeks new tenants for its

property.

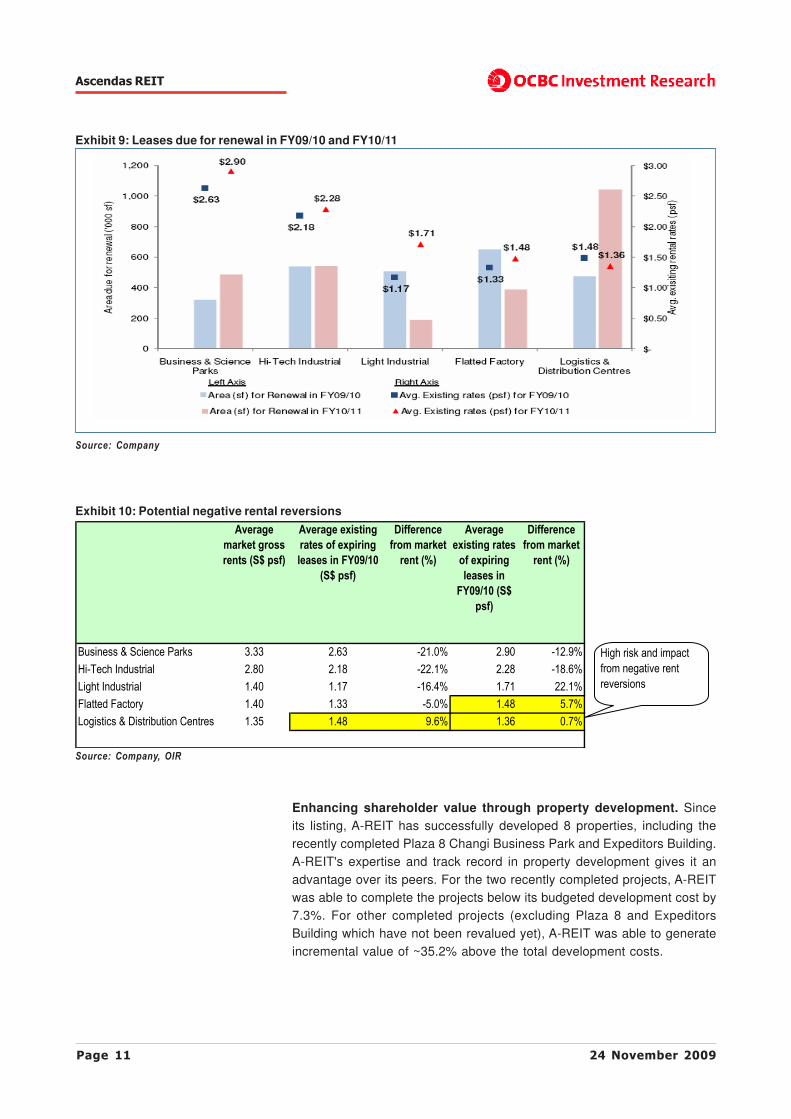

Limited impact from negative rental reversions in FY09/10 and FY10/

11. For the leases expiring in FY09/10 and FY10/11, we do not foresee

significant impact from negative rental reversions on A-REIT. The average

existing rents of expiring leases in its business and science parks and hi-

tech industrial properties are still 12.9% to 22.1% below the current market

asking rents, which provide a comfortable margin of safety to accommodate

any further decline in market rents. For the light industrial properties, expiring

leases in FY10/11 could face significant negative rental reversion as average

existing rent of expiring leases is currently 22.1% higher than market asking

rents but the overall impact on A-REIT's portfolio income will be limited as

the area is just ~1% of the total NLA of A-REIT's portfolio. Negative rental

reversion could also affect A-REIT's flatted factories in FY10/11 and logistics

and distribution centres in FY09/10 and FY10/11 but the impact should be

manageable as average existing rents of these expiring leases are not

significantly higher than the current market rents.

Page 11 24 November 2009

Ascendas REIT

Exhibit 9: Leases due for renewal in FY09/10 and FY10/11

Source: Company

Average

market gross

rents (S$ psf)

Average existing

rates of expiring

leases in FY09/10

(S$ psf)

Difference

from market

rent (%)

Average

existing rates

of expiring

leases in

FY09/10 (S$

psf)

Difference

from market

rent (%)

Business & Science Parks 3.33 2.63 -21.0% 2.90 -12.9%

Hi-Tech Industrial 2.80 2.18 -22.1% 2.28 -18.6%

Light Industrial 1.40 1.17 -16.4% 1.71 22.1%

Flatted Factory 1.40 1.33 -5.0% 1.48 5.7%

Logistics & Distribution Centres 1.35 1.48 9.6% 1.36 0.7%

High risk and impact

from negative rent

reversions

Exhibit 10: Potential negative rental reversions

Source: Company, OIR

Enhancing shareholder value through property development. Since

its listing, A-REIT has successfully developed 8 properties, including the

recently completed Plaza 8 Changi Business Park and Expeditors Building.

A-REIT's expertise and track record in property development gives it an

advantage over its peers. For the two recently completed projects, A-REIT

was able to complete the projects below its budgeted development cost by

7.3%. For other completed projects (excluding Plaza 8 and Expeditors

Building which have not been revalued yet), A-REIT was able to generate

incremental value of ~35.2% above the total development costs.

Page 12 24 November 2009

Ascendas REIT

Exhibit 11: Completed development projects

Source: Company

Completed Development

Development

Cost (S$m)

Book value as at

31 Mar 09 (S$m) Value-add (%)

Courts Megastore 46.0 60.9 32.4

Giant Hypermart 65.4 76.1 16.4

HansaPoint@CBP* 26.1 80.9 210.0

15 Changi North Way 36.2 40.9 13.0

Pioneer Hub 79.3 90.0 13.5

3 Changi Business Park Crescent 59.0 72.9 23.6

Plaza 8 Changi Business Park# 98.8 98.8 NA

Expeditors Building# 24.2 24.2 NA

Total 435.0 421.7 35.2

* CBP - Changi Business Park

computation of the value-add %

# Revaluations of Plaza 8 and Expeditors Building have not been done yet; Excluded in the

Source: Company

Exhibit 12: Development projects in progress

Development-in-progress

Expected

Development

Cost (S$m)

Expected

Completion Date

BTS Hi-Tech Industrial building for Singtel 175.4 4Q FY09/10

Total 175.4

Amount funded 100.5

Development cost to be funded 74.9

Appetite for more development projects. Based on A-REIT's deposited

property value of S$4,559.7m, it has the capacity to take on as much as

S$456m worth of development projects in accordance to the maximum

10% exposure limit of the property fund's deposited property to property

development under the MAS guidelines for property fund. With just one

ongoing development project at the moment - Built-to-Suit (BTS) for SingTel

with an expected development cost of S$175.4m, this leaves A-REIT with

significant headroom of S$280.6m for new development projects.

Page 13 24 November 2009

Ascendas REIT

Backing from a strong sponsor - Ascendas. A-REIT is sponsored by the

Ascendas Group, which holds a deemed interest of 20.66% through

Ascendas Land and Ascendas Funds Management. Ascendas, a subsidiary

of JTC Corporation, has an excellent track record as Asia's premier developer

and manager of business space. It manages S$9b of assets, with presence

in more than 30 cities in 10 countries. We believe that having a strong

sponsor in Ascendas could provide financial support and instill greater investor

confidence in A-REIT, especially during challenging times. Even though A-

REIT's right of first refusal on its sponsor's assets have expired, it is still

able to leverage on its sponsor's portfolio of assets for acquisition, as

demonstrated in its acquisitions of the Science Hub & Rutherford and CGG

Veritas Hub.

Page 14 24 November 2009

Ascendas REIT

Exhibit 13: Significant buffer to breach target gearing level

Source: Company, OIR

in S$ m

Total assets 4,695

Aggregate leverage (include deferred payments) 1,430

Gearing 30.50%

Target gearing (a) 40.00%

Aggregate leverage (include deferred payments) (b) 1,430

Total assets (=b/a) 3,575

Buffer to asset devaluation 1,120

- % of current asset value 23.90%

Section D: Capital Management

Completed two fund raising exercises in CY09. For the year to date,

A-REIT had successfully raised a total of S$709.6m from two fund raising

exercises. Gross proceeds of S$408m were raised from a private placement

and preferential offering exercise in January and another S$301.6m were

raised from a private placement exercise in August. The successful book

closure of its private placement in January that came within a day of launch

amid the challenging market condition was a good demonstration of A-

REIT's capability in the capital market.

Gearing level remains comfortable. With the two fund raising exercises,

A-REIT successfully lowered its gearing level from 42.2% at the end of

2008 to 30.5% at the end of Sep 2009. The current gearing ratio provides a

comfortable buffer from management's target gearing ratio of 40%. A-REIT

is able to tolerate a further 23.9% decline (S$1,120m) in the valuation of its

property portfolio before breaching its target gearing level. This provides a

very comfortable buffer, in our view.

Well spread out debt maturity profile eases refinancing strain. Near

term refinancing risk for A-REIT is limited as it has already completed its

refinancing exercise for 2009. For the S$300m term loan facility due in

2010, A-REIT has already received offer to extend the loan. The maturity

profile of A-REIT's borrowings is also well spread out, with less than 30% of

total borrowings due for refinancing in each of the next 5 years. Its diversified

funding sources from untapped portion of its Multicurrency Medium Term

Note (MTN) programme (~S$725m) and various bilateral banking credit

facilities also provide financial flexibility for A-REIT's refinancing needs.

Page 15 24 November 2009

Ascendas REIT

Exhibit 14: Debt maturity profile

Source: Company

350395

300

150 125

87

0

50

100

150

200

250

300

350

400

450

2010 2011 2012 2013 2014

in S

$m

CMBS Term loan MTN Revolving credit facilities

% of total

borrowings 21.3% 16.8% 24.9% 8.9% 28.1%

Page 16 24 November 2009

Ascendas REIT

Section E: Financials

Key revenue driver coming from development projects. We expect

A-REIT to deliver revenue growth of 4.3% YoY to S$413.4m in FY09/10 as

newly completed projects such as Plaza 8 (CBP Phase 2) and Expeditors

Building will contribute positively from 3Q FY09/10 onwards. Other completed

development projects such as 3 Changi Business Park Crescent (CBP

Phase 1), Pioneer Hub and 15 Changi North Way will also make their

maiden full year contribution in FY09/10. For FY10/11, we expect revenue

growth to slow down to 0.7% YoY as we expect negative rental reversions

to offset the incremental revenue growth from new development projects.

The BTS for SingTel at Kim Chuan will start contributing to A-REIT's top-

line from FY10/11 onwards.

Exhibit 15: Revenue forecasts

Source: Company, OIR estimates

413.4 416.4

396.5

322.3

300

320

340

360

380

400

420

440

FY2007/08 FY2008/09 FY2009/10F FY2010/11F

in S$m

Additional

income from

CBP Phase

1& 2,

Pioneer

Hub, 15

Changi

North Way

&

Ex peditors

Building

Full y ear

contribution

from

Ex peditors

Building,

CBP Phase

2 and

Singtel BTS.

Lower property expenses drive NPI growth rate higher. For FY09/10,

we expect A-REIT to deliver stronger NPI growth rate of 8.7% relative to its

revenue growth, with an expected NPI of S$322.5m. Stronger NPI growth is

aided by property tax rebate and lower utilities charges. For FY10/11, we

expect A-REIT to deliver NPI of S$324.8m and NPI growth is expected to

slow down to 0.7% YoY, which is in line with A-REIT's revenue growth.

Page 17 24 November 2009

Ascendas REIT

Exhibit 17: DPU forecasts and yields

Source: Company, OIR estimates

12.9012.86

15.18

14.13

8.21

6.976.95

7.64

10.00

11.00

12.00

13.00

14.00

15.00

16.00

FY2007/08 FY2008/09 FY2009/10F FY2010/11F

in S-cents

5.00

5.50

6.00

6.50

7.00

7.50

8.00

8.50

in %

DPU (LHS) Yield (RHS)

Exhibit 16: NPI forecasts

Source: Company, OIR estimates

324.8322.5

296.6

243.5

200

220

240

260

280

300

320

340

FY2007/08 FY2008/09 FY2009/10F FY2010/11F

in S$m

Higher

rev enue,

Property

tax rebate

and lower

utilities

charges

Higher

rev enue

DPU to fall due to placement dilution. We expect A-REIT to deliver

DPU of 12.86 S-cents for FY09/10. This is 15.3% lower than FY08/09 DPU

and is attributable to the dilution impact from the two placement exercises

in 2009. Putting aside the dilution impact, we expect A-REIT's distributable

income to grow by 14% YoY in FY09/10. For FY10/11, we expect DPU to

remain steady and turn in marginal growth of 0.3% YoY to 12.9 S-cents.

These translate to DPU yields of 6.84% and 6.86% for FY09/10 and FY10/

11, respectively.

Page 18 24 November 2009

Ascendas REIT

Source: Bloomberg, OIR

Section F: Peers Comparison

Exhibit 18: Comparables Table

Bloomberg

TickerLast Price

OIR/ Cons

FY09 DPU

(in S$)

OIR/ Cons

FY10 DPU

(in S$)

FY09

Yield

(%)

FY10

Yield

(%)

Gearing

ratio (%)

Bk value

per share

(in S$)

Price-to-

book (x)

Office

Frasers Commercial Trust FCOT SP 0.145 SGD 439.9 0.015 0.011 10.3 7.6 38.9 0.27 0.54

CapitaCommercial Trust* CCT SP 1.110 SGD 3,123.4 0.067 0.064 6.0 5.8 30.9 1.51 0.73

K-REIT Asia KREIT SP 0.995 SGD 1,329.3 0.078 0.070 7.8 7.0 9.1 1.48 0.67

Suntec REIT* SUN SP 1.280 SGD 2,091.9 0.113 0.091 8.8 7.1 34.3 1.97 0.65

Office Average 8.3 6.9 28.3 1.31 0.65

Retail

CapitaMall Trust* CT SP 1.730 SGD 5,500.1 0.090 0.093 5.2 5.4 29.5 1.57 1.10

Frasers Centerpoint Trust* FCT SP 1.200 SGD 751.9 0.081 0.081 6.8 6.8 29.9 1.22 0.98

Starhill Global REIT SGREIT SP 0.530 SGD 1,024.2 0.054 0.039 10.2 7.4 27.1 0.81 0.65

Retail Average 7.4 6.5 28.8 1.20 0.91

Healthcare

Parkway Life REIT PREIT SP 1.190 SGD 718.4 0.076 0.083 6.4 7.0 28.7 1.34 0.89

Healthcare Average 6.4 7.0 28.7 1.34 0.89

Hospitality

Ascott Residence Trust* ART SP 1.050 SGD 646.3 0.074 0.072 7.0 6.9 39.7 1.32 0.79

CDL Hospitality REIT CDREIT SP 1.480 SGD 1,238.1 0.078 0.091 5.3 6.1 20.2 1.41 1.05

Hospitality Average 6.2 6.5 29.9 1.36 0.92

Industrial

Ascendas REIT* AREIT SP 1.880 SGD 3,515.5 0.129 0.129 6.8 6.9 30.5 1.60 1.18

Cambridge Industrial Trust CREIT SP 0.415 SGD 360.0 0.052 0.050 12.5 12.0 40.7 0.60 0.69

Macarthurcook Industrial REIT MIREIT SP 0.350 SGD 93.2 0.049 0.019 14.0 5.4 44.6 0.94 0.37

Mapletree Logistics Trust* MLT SP 0.700 SGD 1,438.0 0.059 0.055 8.4 7.9 38.7 0.88 0.80

Industrial Average 10.4 8.0 38.6 1.00 0.76

Overseas

Ascendas India Trust AIT SP 0.860 SGD 654.8 0.068 0.073 7.9 8.5 10.9 0.84 1.02

CapitaRetail China Trust CRCT SP 1.150 SGD 716.3 0.082 0.085 7.1 7.4 33.5 1.12 1.03

First REIT FIRT SP 0.755 SGD 208.0 NA NA NA NA 14.8 0.93 0.81

Fortune REIT (in HK$) FRT SP 2.850 HKD 4,727.5 0.315 0.293 11.1 10.3 25.7 4.88 0.58

Lippo-Mapletree Indonesia* LMRT SP 0.470 SGD 506.5 0.050 0.052 10.6 11.1 11.1 0.74 0.63

Saizen REIT SZREIT SP 0.150 SGD 142.9 NA NA NA NA 44.4 0.41 0.37

Overseas Average 9.2 9.3 23.4 1.49 0.74

S-REITs Average 8.5 7.6 29.2 1.29 0.78

* DPU and Yields are based on OIR forecast

Updated as at 23rd Nov 09

Market Cap (in

S$m)

Page 19 24 November 2009

Ascendas REIT

Highest Price/Book valuation within S-REITs universe. A-REIT is

currently trading at Price/Book of 1.18x and this is the highest within the

S-REITs universe. On average, S-REITs are trading at an average Price/

Book of 0.78x. Industrial REITs are trading at Price/Book of 0.76x and its

closest peer (base on sector and market cap), Mapletree Logistics Trust,

is currently priced at Price/Book of 0.8x. Among the large-cap S-REITs,

peers such as CapitaMall Trust, CapitaCommercial Trust and Suntec REIT

are trading at Price/Book of 1.1x, 0.73x and 0.65x, respectively.

Lowest gearing among industrial peers. A-REIT has gearing ratio of

30.5% as at the end of September and this is the lowest among other

REITs in the industry property market. As a whole, industrial REITs have

an average gearing level of 38.6%, which is higher than the 29.2% gearing

level of the S-REITs universe.

Page 20 24 November 2009

Ascendas REIT

Section G: Valuation

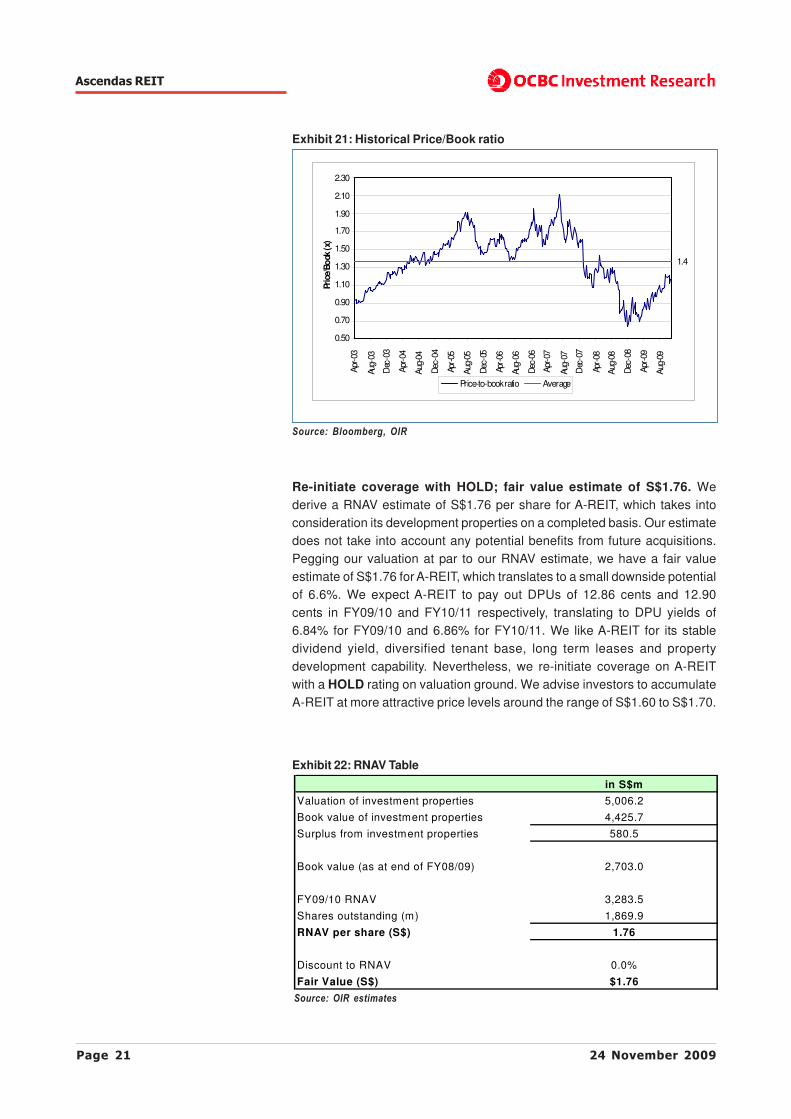

Valuation back to normalize range. Since bottoming in March, A-REIT's

share price had recovered from the low of S$1.05 (after adjusting for

placement dilution) and gained 79% to close at S$1.88 (yesterday's closing).

Despite the surge in share price, valuation has not reached a demanding

level yet. The current valuation of A-REIT is still within the normalized

historical valuation range. Several key valuation matrices such as yield

spread over SGS 10-yr bond yield, forward DPU yield and Price/Book ratio

are now close to the historical average (refer to Exhibits 19 to 21).

Exhibit 19: Historical DPU yield vs SGS 10-yr bond yield

Source: Bloomberg, OIR

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Apr-

03

Aug-0

3

De

c-0

3

Ap

r-0

4

Aug-0

4

De

c-0

4

Ap

r-05

Aug-

05

Dec-0

5

Ap

r-0

6

Aug-0

6

De

c-0

6

Ap

r-07

Aug-0

7

Dec-0

7

Apr-

08

Aug-0

8

De

c-0

8

Ap

r-0

9

Aug-0

9

in %

A-REIT's DPU yield SGS 10yr bond yield

Exhibit 20: Historical yield spread

Source: Bloomberg, OIR

3.8

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Apr-

03

Aug-

03

Dec

-03

Apr

-04

Aug

-04

Dec

-04

Apr

-05

Aug

-05

Dec

-05

Apr

-06

Aug

-06

Dec

-06

Apr-

07

Aug-

07

Dec

-07

Apr-

08

Aug-

08

Dec

-08

Apr

-09

Aug

-09

in %

Yield spread Average

Page 21 24 November 2009

Ascendas REIT

Exhibit 21: Historical Price/Book ratio

Source: Bloomberg, OIR

1.4

0.50

0.70

0.90

1.10

1.30

1.50

1.70

1.90

2.10

2.30

Apr

-03

Aug-

03

Dec

-03

Apr

-04

Aug

-04

Dec

-04

Apr-

05

Aug

-05

Dec

-05

Apr-

06

Aug-

06

Dec

-06

Apr

-07

Aug-

07

Dec

-07

Apr-

08

Aug

-08

Dec

-08

Apr

-09

Aug

-09

Pric

e/Bo

ok (x)

Price-to-book ratio Average

Re-initiate coverage with HOLD; fair value estimate of S$1.76. We

derive a RNAV estimate of S$1.76 per share for A-REIT, which takes into

consideration its development properties on a completed basis. Our estimate

does not take into account any potential benefits from future acquisitions.

Pegging our valuation at par to our RNAV estimate, we have a fair value

estimate of S$1.76 for A-REIT, which translates to a small downside potential

of 6.6%. We expect A-REIT to pay out DPUs of 12.86 cents and 12.90

cents in FY09/10 and FY10/11 respectively, translating to DPU yields of

6.84% for FY09/10 and 6.86% for FY10/11. We like A-REIT for its stable

dividend yield, diversified tenant base, long term leases and property

development capability. Nevertheless, we re-initiate coverage on A-REIT

with a HOLD rating on valuation ground. We advise investors to accumulate

A-REIT at more attractive price levels around the range of S$1.60 to S$1.70.

Exhibit 22: RNAV Table

Source: OIR estimates

in S$m

Valuation of investment properties 5,006.2

Book value of investment properties 4,425.7

Surplus from investment properties 580.5

Book value (as at end of FY08/09) 2,703.0

FY09/10 RNAV 3,283.5

Shares outstanding (m) 1,869.9

RNAV per share (S$) 1.76

Discount to RNAV 0.0%

Fair Value (S$) $1.76

Page 22 24 November 2009

Ascendas REIT

Exhibit 23: Key valuation assumptions

Source: OIR estimates

Risk-free rate 2.40%

Beta 1

Market risk premium 6.50%

Cost of debt 4.20%

Cap rate 6.16%

Terminal growth rate 3.00%

Page 23 24 November 2009

Ascendas REIT

Section H: Risk Factors

Some of the key risk factors in investing in A-REIT include:

1) Highly exposed to the economic conditions and government policy

in Singapore. A-REIT's property assets are all located in Singapore and

its performance is highly reliant on the economic conditions and government

policy in Singapore. In the event where Singapore's economy deteriorates,

vacancy rates and rents could be adversely affected. In addition, any

unfavorable change in government policy towards businesses could also

affect foreign investments and reduce the demand for industrial space in

Singapore.

2) Competition in a highly fragmented industrial property market.

The industry property market in Singapore is highly fragmented and

competition among industrial landlords for tenants could depress the rents

in the industrial property market and thus adversely affect A-REIT's financial

performance.

3) Potential conflict of interests between A-REIT and the Ascendas

Group. The Ascendas Group holds a deemed interest of 20.66% in A-REIT

and the manager and the property manager of A-REIT are 100% directly

owned by the Ascendas Group. The Ascendas Group is involved in a similar

scope of business as A-REIT which includes investing, acquiring, developing

and managing of industrial properties in Singapore. A-REIT may have to

compete with the Ascendas Group for tenants in the Singapore market.

Page 24 24 November 2009

Ascendas REIT

Appendix 1: Background on A-REIT

A-REIT, Singapore's first and largest business space and industrial REIT,

was listed on 19 November 2002 with a portfolio of 8 properties worth S$545

million. It has since increased its properties to 90 with a book value of

about S$4.7 billion.

It owns a diversified property portfolio in Singapore comprising business

and science parks, hi-tech industrial properties, light industrial properties,

logistics and distribution centres as well as warehouse retail facilities. These

properties house a tenant base of over 900 international and local companies

from a wide range of industries and activities, including research and

development, life sciences, information technology, electronics, engineering,

light manufacturing, telecommunications, logistics service providers,

manufacturing services and back-room office support in service industries.

A-REIT is listed in several indices including the Morgan Stanley Capital

International, Inc (MSCI) Index, the European Public Real Estate Association

/ National Association of Real Estate Investment Trusts (EPRA/NAREIT)

Global Real Estate Index and Global Property Research (GPR) Asia 250. A

corporate family credit rating of "Baa1" was assigned to A-REIT by Moody's

Investors Service.

A-REIT's objective is to achieve income stability and long-term growth in

the portfolio. Potential growth in the existing portfolio would be through a

proactive approach to fund and asset management, and acquisition of

strategically located premium properties to deliver consistent returns to

unitholders.

Page 25 24 November 2009

Ascendas REIT

Source: Company

Appendix 2: Trust Structure

Page 26 24 November 2009

Ascendas REIT

Appendix 3: Asset Portfolio Summary

Source: Company

Page 27 24 November 2009

Ascendas REIT

Ascendas Real Estate Investment Trust's Key Financial Data

EARNINGS FORECAST

Year Ended 31 Mar (S$m) FY08 FY09 FY010F FY11F

Gross revenue 322.3 396.5 413.4 416.4

Property service fees -9.7 -12.1 -12.4 -12.5

Property tax -18.8 -26.4 -24.8 -24.4

Other property operating expenses -50.3 -61.4 -53.7 -54.7

Property operating expenses -78.8 -99.9 -91.0 -91.6

Net property income 243.5 296.6 322.5 324.8

Interest income 0.1 0.0 0.0 0.0

Manager's fee -17.2 -22.6 -23.5 -23.6

Performance fee -8.4 -9.1 -4.7 -4.7

Trust expenses -2.5 -4.7 -3.7 -3.7

Borrowing costs -40.5 -59.5 -60.7 -62.2

Non property expenses -68.5 -95.9 -92.6 -94.3

Net income 175.0 200.7 229.9 230.5

Net change on revaluation of investment properties 494.1 -115.4 0.0 0.0

Total return for the period 669.1 85.3 229.9 230.5

Non-tax deductible expenses 12.3 10.2 10.5 10.7

Net change on revaluation of investment properties -494.1 115.4 0.0 0.0

Income available for distribution 187.3 210.9 240.4 241.1

DPU (S cents) 14.1 15.2 12.9 12.9

Page 28 24 November 2009

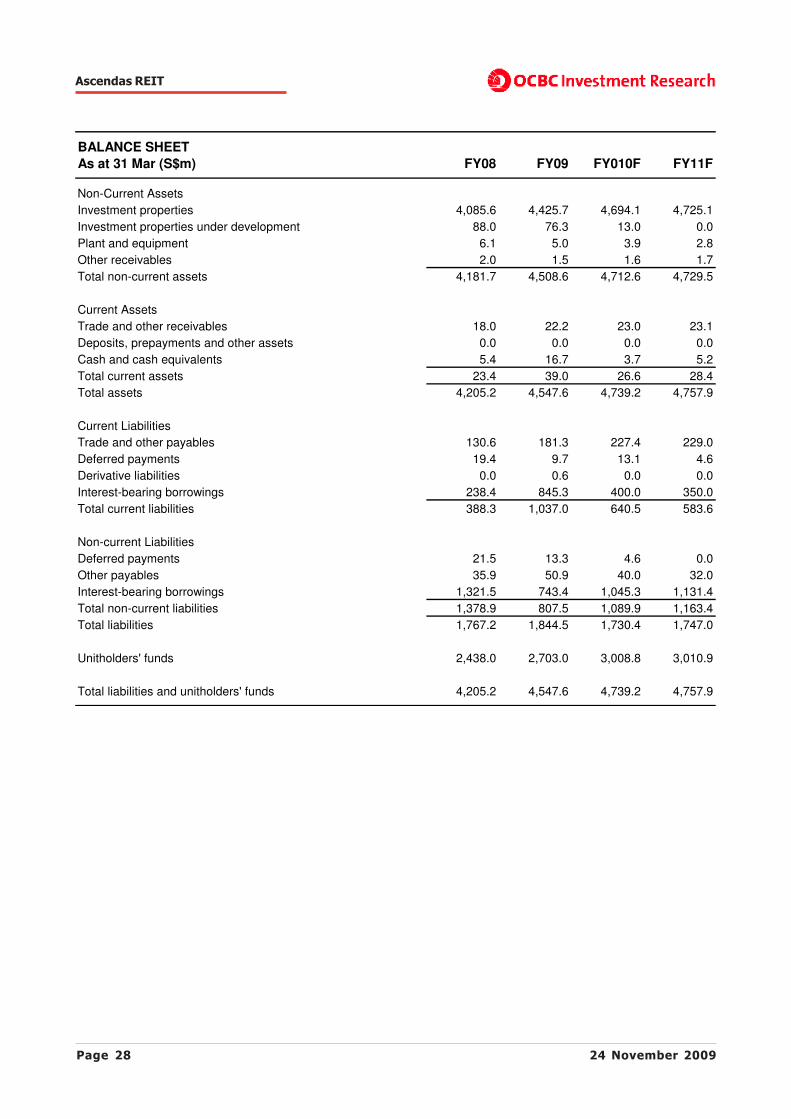

Ascendas REIT

BALANCE SHEET

As at 31 Mar (S$m) FY08 FY09 FY010F FY11F

Non-Current Assets

Investment properties 4,085.6 4,425.7 4,694.1 4,725.1

Investment properties under development 88.0 76.3 13.0 0.0

Plant and equipment 6.1 5.0 3.9 2.8

Other receivables 2.0 1.5 1.6 1.7

Total non-current assets 4,181.7 4,508.6 4,712.6 4,729.5

Current Assets

Trade and other receivables 18.0 22.2 23.0 23.1

Deposits, prepayments and other assets 0.0 0.0 0.0 0.0

Cash and cash equivalents 5.4 16.7 3.7 5.2

Total current assets 23.4 39.0 26.6 28.4

Total assets 4,205.2 4,547.6 4,739.2 4,757.9

Current Liabilities

Trade and other payables 130.6 181.3 227.4 229.0

Deferred payments 19.4 9.7 13.1 4.6

Derivative liabilities 0.0 0.6 0.0 0.0

Interest-bearing borrowings 238.4 845.3 400.0 350.0

Total current liabilities 388.3 1,037.0 640.5 583.6

Non-current Liabilities

Deferred payments 21.5 13.3 4.6 0.0

Other payables 35.9 50.9 40.0 32.0

Interest-bearing borrowings 1,321.5 743.4 1,045.3 1,131.4

Total non-current liabilities 1,378.9 807.5 1,089.9 1,163.4

Total liabilities 1,767.2 1,844.5 1,730.4 1,747.0

Unitholders' funds 2,438.0 2,703.0 3,008.8 3,010.9

Total liabilities and unitholders' funds 4,205.2 4,547.6 4,739.2 4,757.9

Page 29 24 November 2009

Ascendas REIT

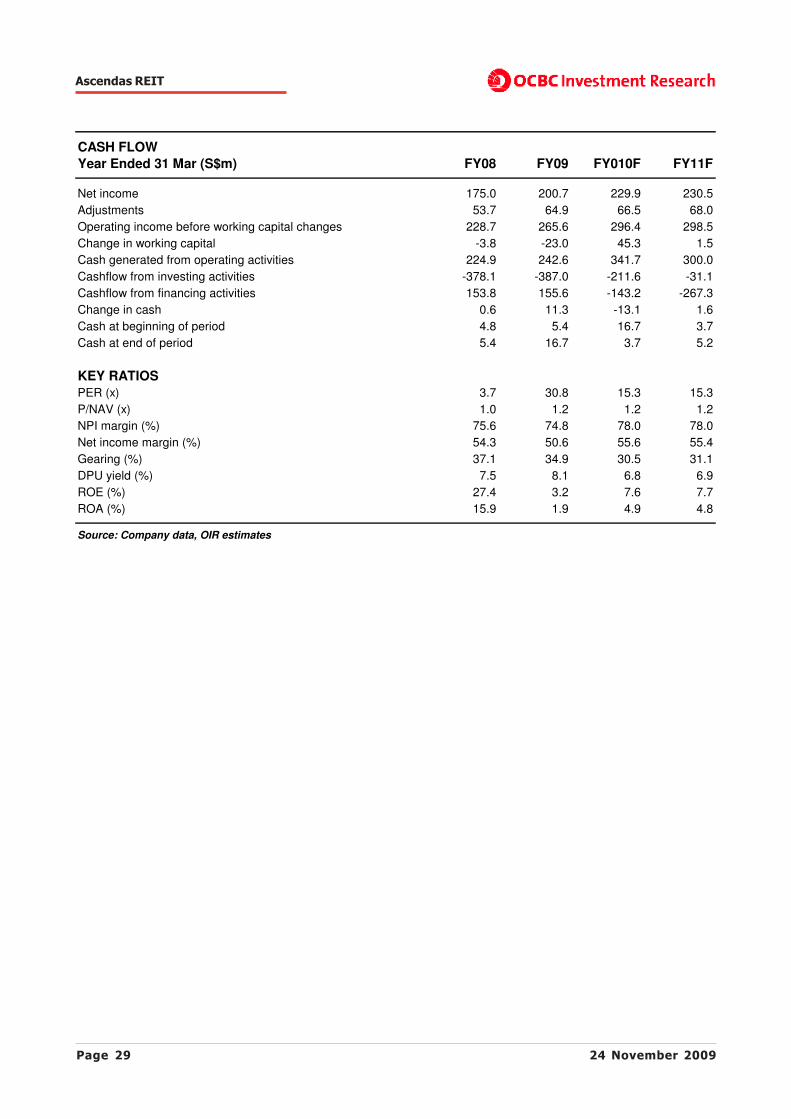

CASH FLOW

Year Ended 31 Mar (S$m) FY08 FY09 FY010F FY11F

Net income 175.0 200.7 229.9 230.5

Adjustments 53.7 64.9 66.5 68.0

Operating income before working capital changes 228.7 265.6 296.4 298.5

Change in working capital -3.8 -23.0 45.3 1.5

Cash generated from operating activities 224.9 242.6 341.7 300.0

Cashflow from investing activities -378.1 -387.0 -211.6 -31.1

Cashflow from financing activities 153.8 155.6 -143.2 -267.3

Change in cash 0.6 11.3 -13.1 1.6

Cash at beginning of period 4.8 5.4 16.7 3.7

Cash at end of period 5.4 16.7 3.7 5.2

KEY RATIOS

PER (x) 3.7 30.8 15.3 15.3

P/NAV (x) 1.0 1.2 1.2 1.2

NPI margin (%) 75.6 74.8 78.0 78.0

Net income margin (%) 54.3 50.6 55.6 55.4

Gearing (%) 37.1 34.9 30.5 31.1

DPU yield (%) 7.5 8.1 6.8 6.9

ROE (%) 27.4 3.2 7.6 7.7

ROA (%) 15.9 1.9 4.9 4.8

Source: Company data, OIR estimates

Page 30 24 November 2009

Ascendas REIT

SHAREHOLDING DECLARATION:The analyst/analysts who wrote this report holds NIL shares in the above security.

RATINGS AND RECOMMENDATIONS:OCBC Investment Research’s (OIR) technical comments and recommendations are short-term and tradingoriented.- However, OIR’s fundamental views and ratings (Buy, Hold, Sell) are medium-term calls within a 12-monthinvestment horizon. OIR’s Buy = More than 10% upside from the current price; Hold = Trade within +/-10%from the current price; Sell = More than 10% downside from the current price.- For companies with less than S$150m market capitalization, OIR’s Buy = More than 30% upside from thecurrent price; Hold = Trade within +/- 30% from the current price; Sell = More than 30% downside from thecurrent price.

DISCLAIMER FOR RESEARCH REPORTThis report is solely for information and general circulation only and may not be published, circulated,reproduced or distributed in whole or in part to any other person without our written consent. This reportshould not be construed as an offer or solicitation for the subscription, purchase or sale of the securitiesmentioned herein. Whilst we have taken all reasonable care to ensure that the information contained in thispublication is not untrue or misleading at the time of publication, we cannot guarantee its accuracy orcompleteness, and you should not act on it without first independently verifying its contents. Any opinion orestimate contained in this report is subject to change without notice. We have not given any considerationto and we have not made any investigation of the investment objectives, financial situation or particularneeds of the recipient or any class of persons, and accordingly, no warranty whatsoever is given and noliability whatsoever is accepted for any loss arising whether directly or indirectly as a result of the recipientor any class of persons acting on such information or opinion or estimate. You may wish to seek advicefrom a financial adviser regarding the suitability of the securities mentioned herein, taking into considerationyour investment objectives, financial situation or particular needs, before making a commitment to invest inthe securities. OCBC Investment Research Pte Ltd, OCBC Securities Pte Ltd and their respective connectedand associated corporations together with their respective directors and officers may have or take positionsin the securities mentioned in this report and may also perform or seek to perform broking and otherinvestment or securities related services for the corporations whose securities are mentioned in this reportas well as other parties generally.

Privileged/Confidential information may be contained in this message. If you are not the addressee indicatedin this message (or responsible for delivery of this message to such person), you may not copy or deliverthis message to anyone. Opinions, conclusions and other information in this message that do not relate tothe official business of my company shall not be understood as neither given nor endorsed by it.

Co.Reg.no.: 198301152E For OCBC Investment Research Pte Ltd

Carmen LeeHead of ResearchPublished by OCBC Investment Research Pte Ltd