A FINE BALANCE - Ascendas REIT

152

A FINE BALANCE A-REIT 7TH ANNUAL REPORT FY2008/09

Transcript of A FINE BALANCE - Ascendas REIT

A FINE BALANCE

A-REIT 7TH ANNUAL REPORT FY2008/09

04 About A-REIT

06 A-REIT Structure

08 Significant Events

10 Financial Highlights

16 Chairman’s Statement

20 Manager’s Report

36 Board of Directors

38 The A-REIT Team

42 The Property Manager

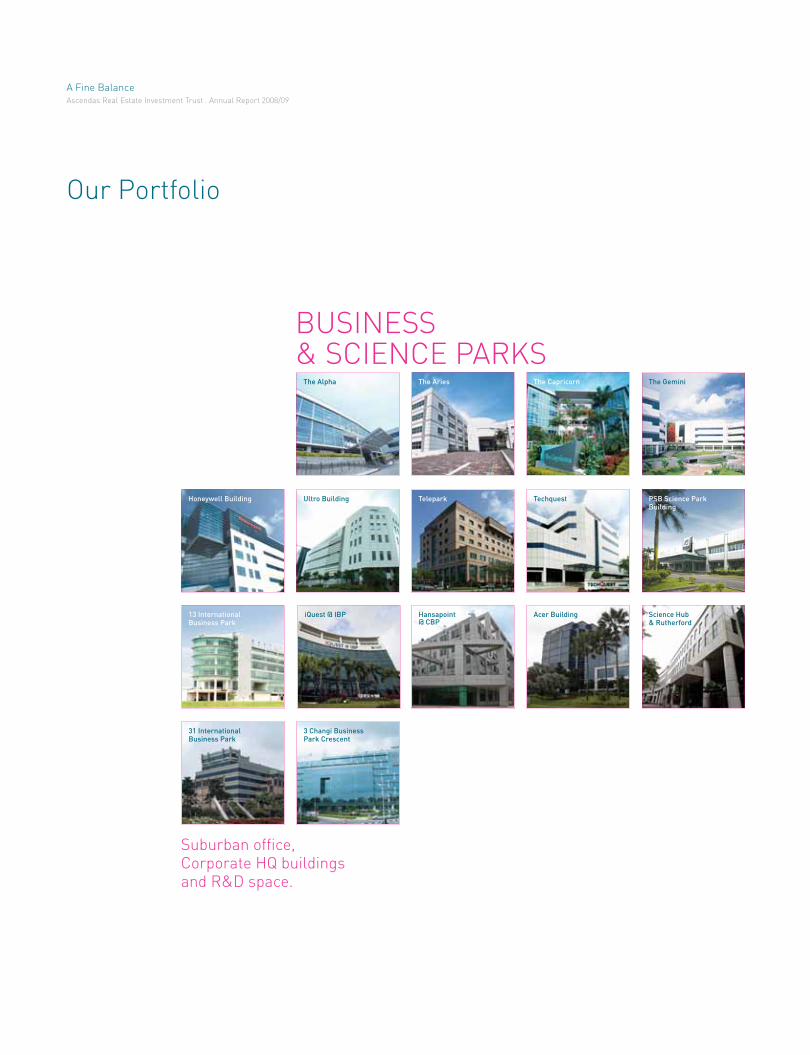

48 Investment Property Portfolio

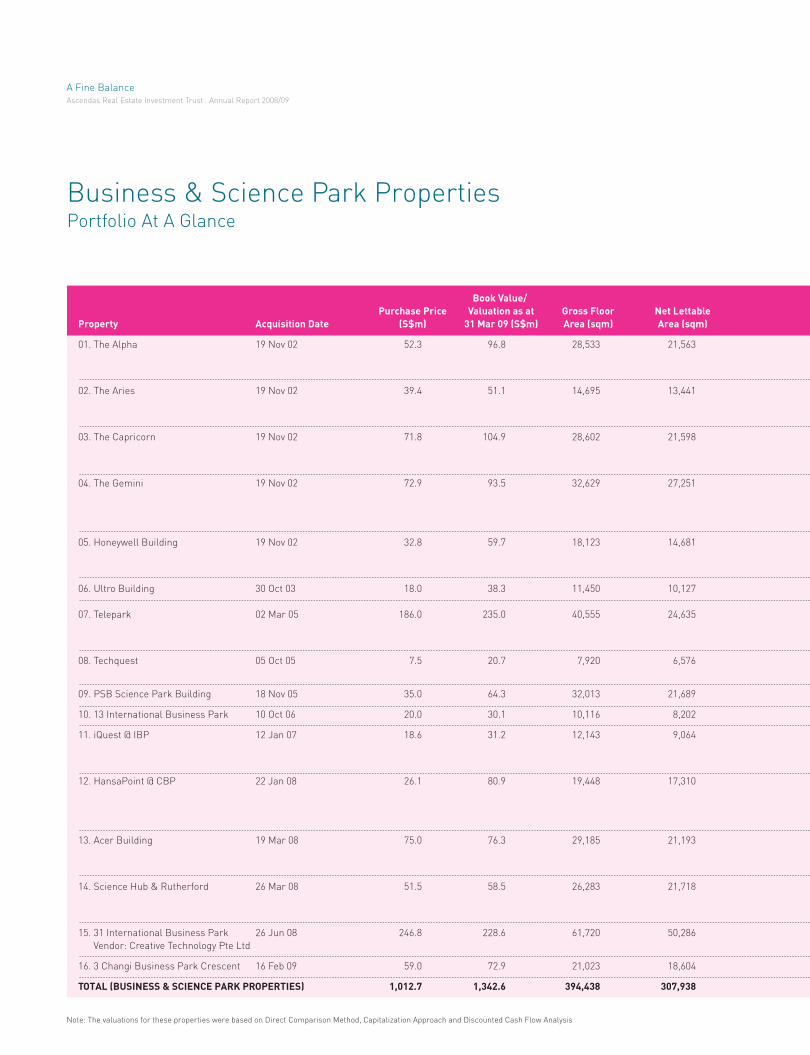

54 Business & Science Park Properties

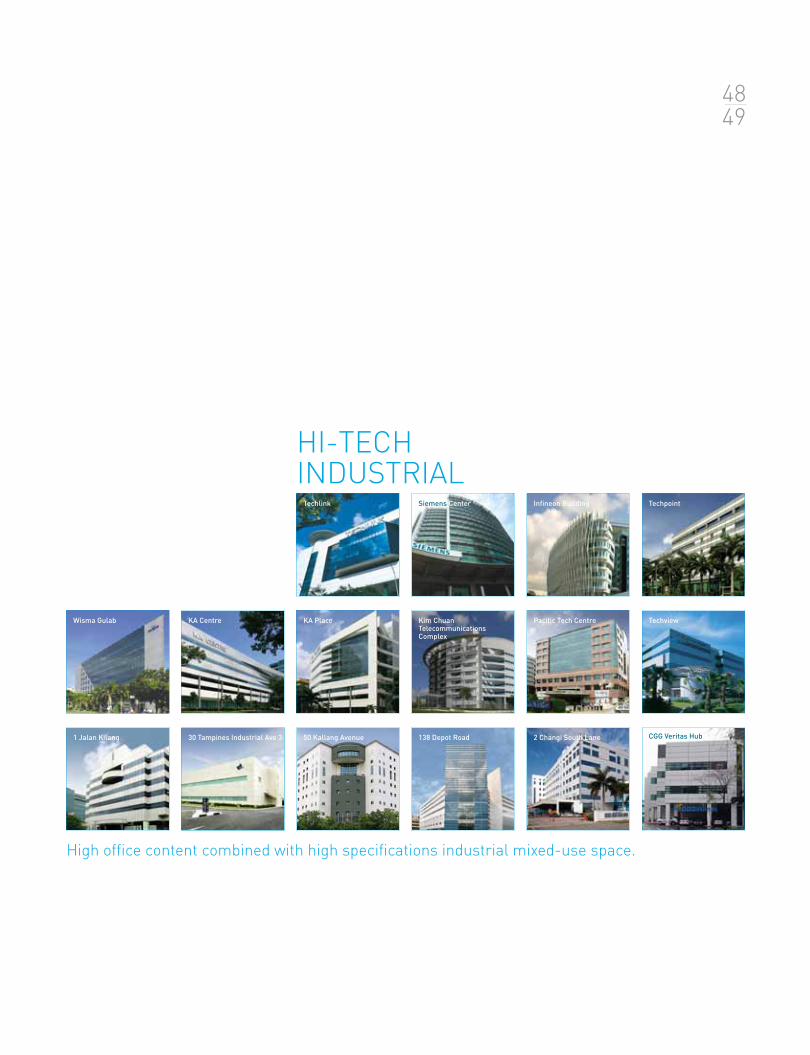

58 Hi-Tech Industrial Properties

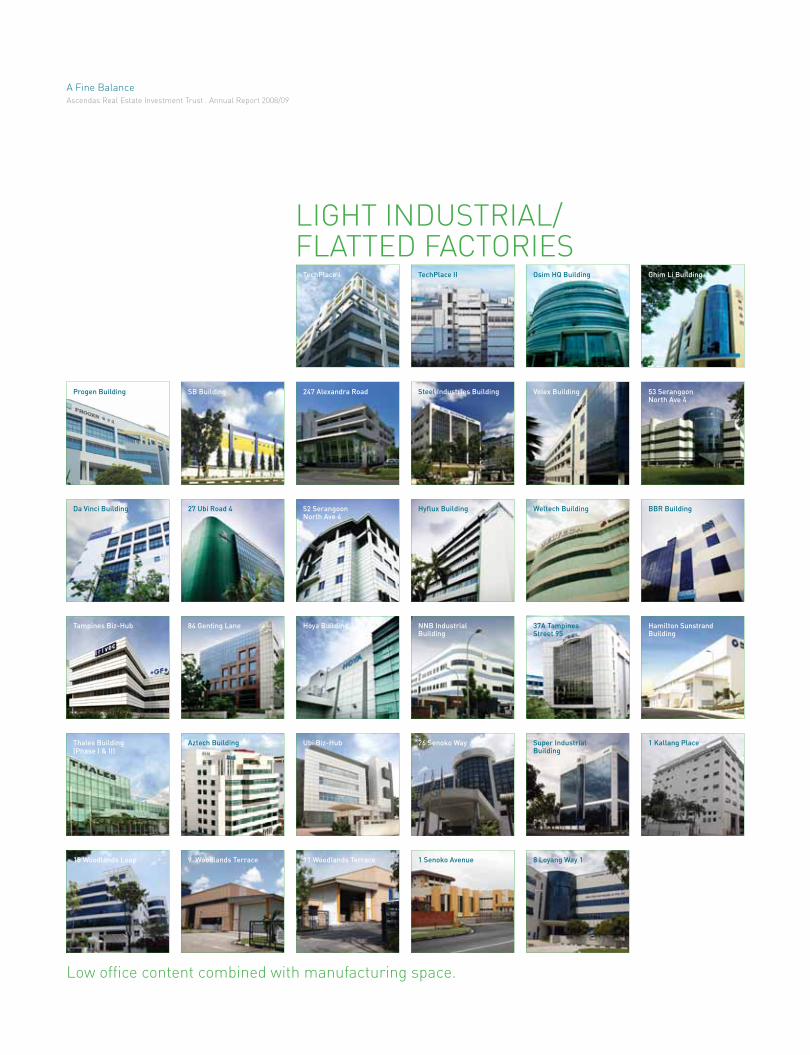

62 Light Industrial/

Flatted Factories Properties

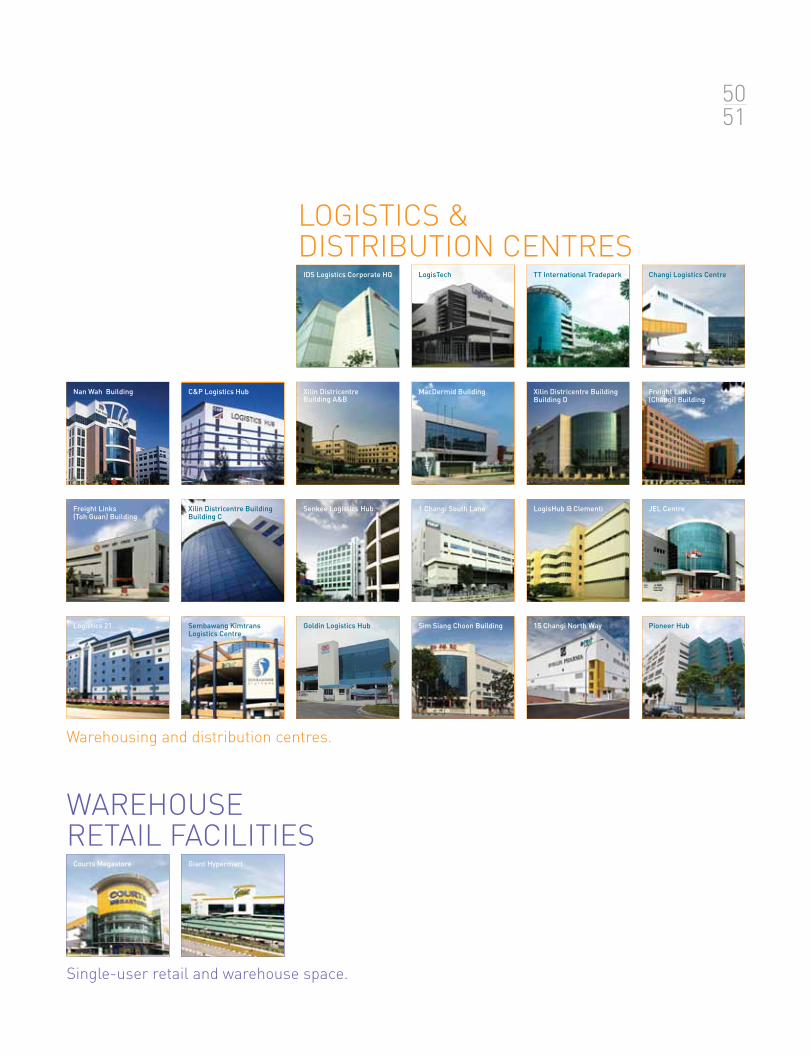

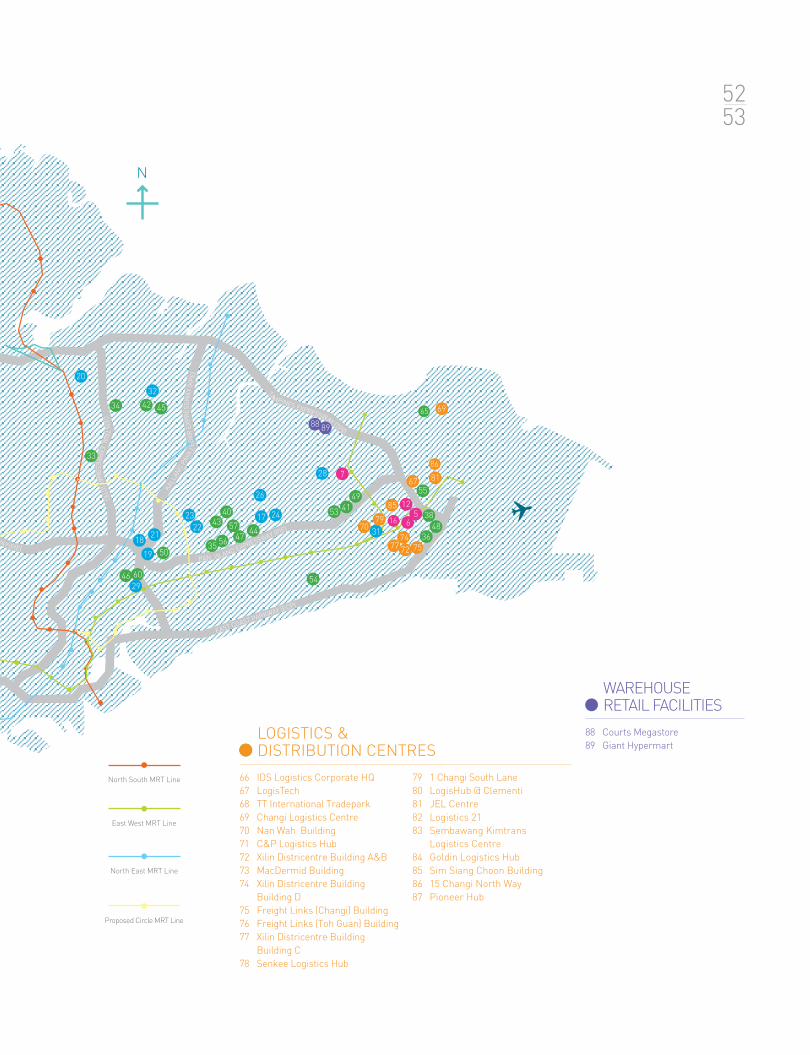

68 Logistics & Distribution Centres

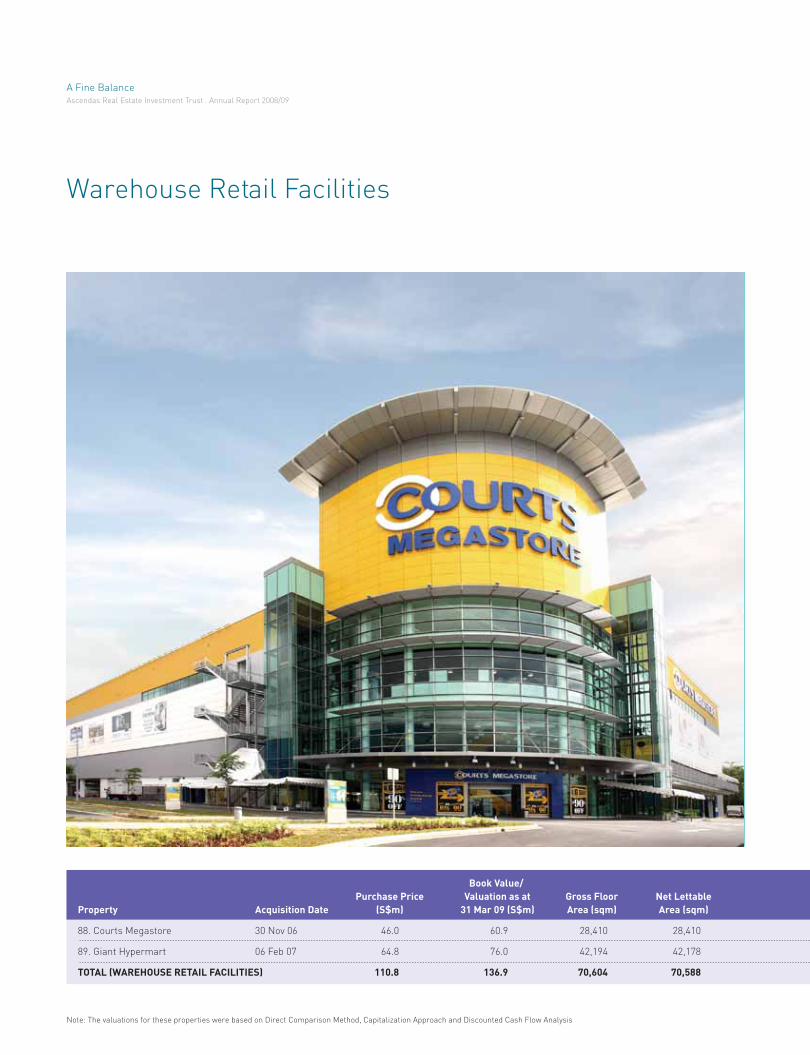

72 Warehouse Retail Facilities

74 Enhancing Corporate

Social Responsibilities

76 Investor Relations

77 CBRE Market Study

84 Corporate Governance

94 Financial Statements

144 Statistics of Unitholdings

146 Additional Information

149 Glossary

CONTENTS

A-REIT was voted as Singapore’s 7th best

managed company (after SingTel, SIA, OCBC,

Capitaland, DBS and UOB) in FinanceAsia’s 2009

annual poll of Asia’s best managed companies.

Any discrepancies in the tables and charts between the listed figures and totals thereof are due to rounding.Where applicable, figures and percentages are rounded to one decimal place.

Every system requires some form of self-balancing mechanism to cleanse itself of

excesses, which may build up from time to time, so as to sustain its health and vigour.

Managing a business is also all about balancing. And it was a fine balancing act that

has brought us to where we are today, and will take us further tomorrow. It is an ever

evolving art that requires us to weigh carefully the many priorities that often pull a

business in opposite directions: the long-term interests of the business versus the

short-term impulses of the market; the indivisible, yet divergent interests of its

customers, investors and employees; the drive to pursue profits without sacrificing

ethics; and the need to seek progress without compromising the environment.

A-REIT is a business that is not only driven to grow and prosper, but one that seeks

long-lasting success and resilience by always maintaining a fine balance of the forces

within its operating sphere. It is precisely this balance of the “hardware” and the

“heart-ware” that sets us apart not just as a sustainable business, but one with a soul.

To deliver predictable distributionsand achieve long term

capital stability for unitholders.

A-REIT’s Mission

About A-REIT

A-REIT owns a diversified portfolio of properties in Singapore comprising:

• Business & Science Parks

Suburban office, corporate HQ buildings and R&D space.

• Hi-Tech Industrial

High office content combined with high specifications mixed-use

industrial space.

• Light Industrial / Flatted Factories

Low office content combined with manufacturing space.

• Logistics & Distribution Centres

Warehousing and distribution centres.

• Warehouse Retail Facilities

Single-user retail and warehouse space.

These properties house a tenant base of about 900 international and

local companies from a range of industries and activities, including

research and development, life sciences, information technology,

engineering, light manufacturing, logistics service providers, electronics,

telecommunications, manufacturing services and back-room office

support in service industries.

Ascendas Funds Management (S) Limited (“AFM”) is the manager of

A-REIT (the “Manager”).

The Manager is committed to delivering long-term sustainable

distributions and capital stability to unitholders through a three-pronged

strategy of:

• Yield accretive investments comprising developments as well as

acquisitions of income-producing properties with strong underlying

real estate fundamentals

• Organic portfolio growth through proactive asset management

• Prudent capital & risk management

Ascendas Real Estate Investment Trust (“A-REIT”) is the first and largest

business space and industrial Real Estate Investment Trust (“REIT”)

listed on Singapore Exchange Securities Trading Limited (“SGX-ST”).

0405

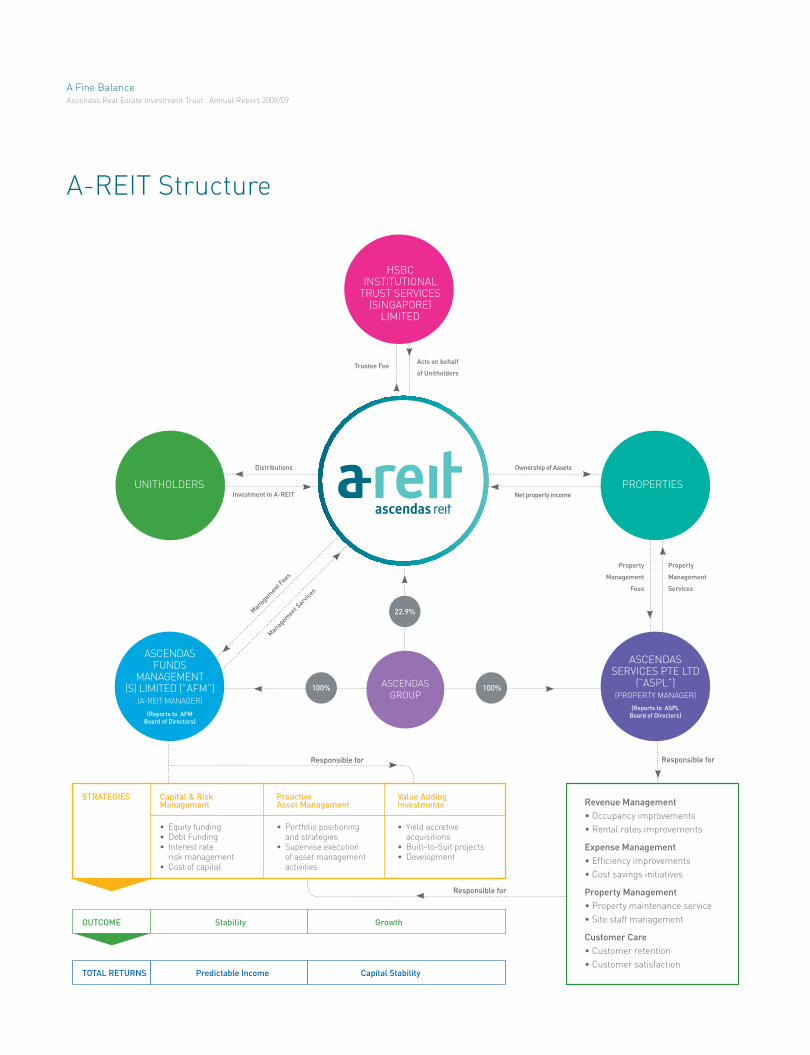

A-REIT Structure

22.9%

100% 100%

Distributions

Investment in A-REIT

Ownership of Assets

Net property income

Acts on behalf

of UnitholdersTrustee Fee

Managem

ent Fees

Managem

ent Serv

ices

Property

Management

Fees

Property

Management

Services

STRATEGIES Capital & RiskManagement

ProactiveAsset Management

Value AddingInvestments

• Equity funding• Debt Funding• Interest rate

risk management• Cost of capital

• Portfolio positioning and strategies

• Supervise execution of asset managementactivities

• Yield accretive acquisitions

• Built-to-Suit projects• Development

OUTCOME Stability Growth

TOTAL RETURNS Predictable Income Capital Stability

Revenue Management

• Occupancy improvements

• Rental rates improvements

Expense Management

• Efficiency improvements

• Cost savings initiatives

Property Management

• Property maintenance service

• Site staff management

Customer Care

• Customer retention

• Customer satisfaction

Responsible for Responsible for

Responsible for

HSBCINSTITUTIONAL

TRUST SERVICES(SINGAPORE)

LIMITED

PROPERTIESUNITHOLDERS

ASCENDASSERVICES PTE LTD

(”ASPL”)(PROPERTY MANAGER)

(Reports to ASPL

Board of Directors)

ASCENDASFUNDS

MANAGEMENT(S) LIMITED (”AFM”)

(A-REIT MANAGER)

(Reports to AFM

Board of Directors)

ASCENDAS

GROUP

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

A-REIT’s Competitive Edge

Stability & Growth

A-REIT’s value offering is stability and

predictability built on a fine balance

of three solid cornerstones of prudent

capital and risk management,

disciplined and value-adding

investment and proactive asset

management. We continue to build

upon our strengths to create a

competitive edge to differentiate

ourselves, to facilitate growth,

resilence and enhance sustainability

and stability in our portfolio.

Diversity & Depth

We are the largest business space

and industrial REIT in Singapore

spanning across six property asset

classes. The portfolio of properties

is well-located, of high quality and is

well-diversified in terms of tenants’

industries and country of origin.

There is a good balance of long-term

and short-term leases which

provides stability and predictability. Customer Focus

We have a track record of customers

growing with us with a high customer

retention ratio of 80% in FY2008/09.

Size Advantage

A-REIT accounted for 15% of the

S-REIT sector and 8% of Asian

REIT (ex-Japan) sector. In 2008,

it accounted for about 11% of the

trading volume for S-REIT on the

SGX-ST, making it one of the more

liquid REITs in the Singapore market.

Market Leader

A-REIT is the established market

leader in most of the sectors that

it operates in.

We are focused on the business

space and industrial property sector

with a committed sponsor. Ascendas

Group has a track record of more

than 20 years in this sector.

Development Capability

We are the only REIT in Singapore to

offer our development capability to

create greater value and returns for

our Unitholders by taking advantage

of the development capacity allowed

under the S-REIT regulations.

Established Operational Platform

Our Property Manager, Ascendas

Services Pte Ltd (”ASPL”), has a

dedicated sales/marketing, leasing

and property management team

of over 80 people, all of whom

possess in-depth understanding of

this property sector and its

customers’ needs.

0607

2008

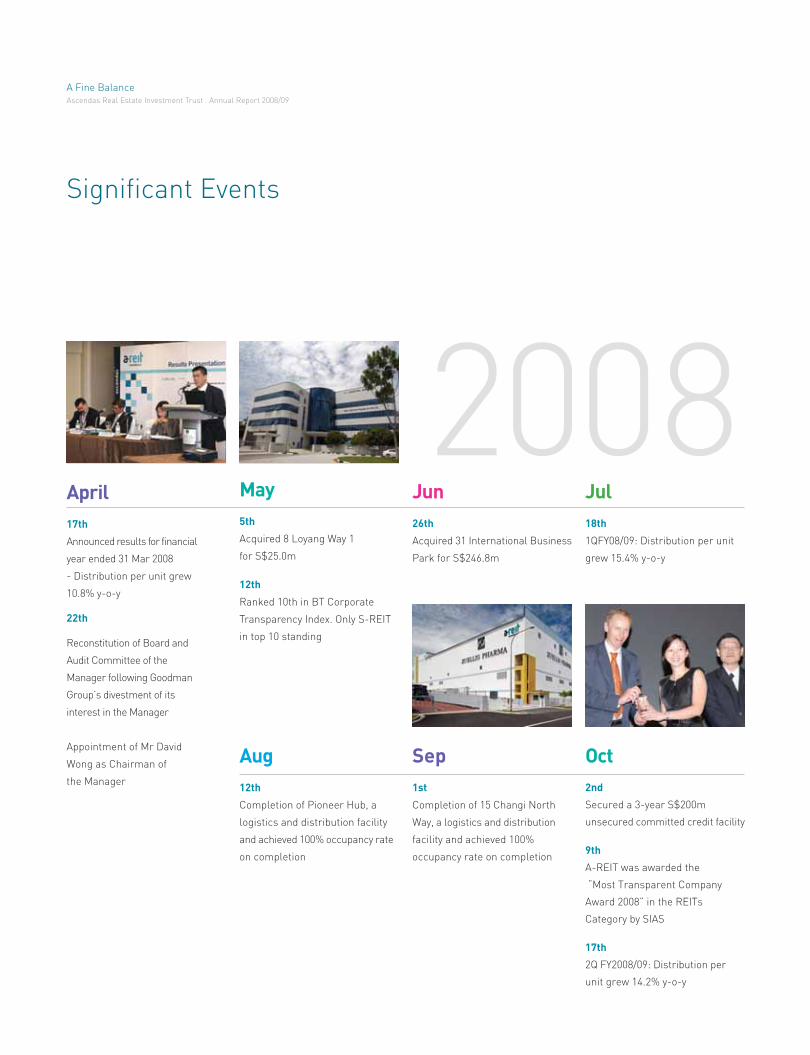

Significant Events

April

17th

Announced results for financial

year ended 31 Mar 2008

- Distribution per unit grew

10.8% y-o-y

22th

Reconstitution of Board and

Audit Committee of the

Manager following Goodman

Group’s divestment of its

interest in the Manager

Appointment of Mr David

Wong as Chairman of

the Manager

May

5th

Acquired 8 Loyang Way 1

for S$25.0m

12th

Ranked 10th in BT Corporate

Transparency Index. Only S-REIT

in top 10 standing

Jun

26th

Acquired 31 International Business

Park for S$246.8m

Jul

18th

1QFY08/09: Distribution per unit

grew 15.4% y-o-y

Aug

12th

Completion of Pioneer Hub, a

logistics and distribution facility

and achieved 100% occupancy rate

on completion

Sep

1st

Completion of 15 Changi North

Way, a logistics and distribution

facility and achieved 100%

occupancy rate on completion

Oct

2nd

Secured a 3-year S$200m

unsecured committed credit facility

9th

A-REIT was awarded the

“Most Transparent Company

Award 2008” in the REITs

Category by SIAS

17th

2Q FY2008/09: Distribution per

unit grew 14.2% y-o-y

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

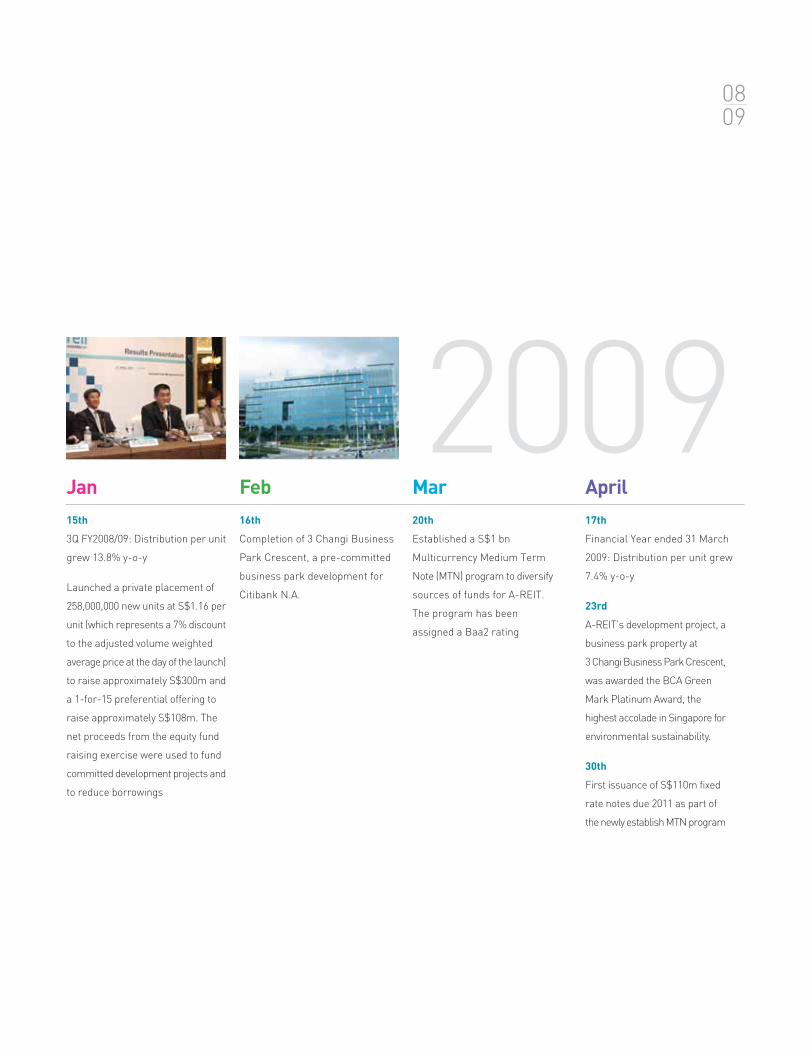

Jan

15th

3Q FY2008/09: Distribution per unit

grew 13.8% y-o-y

Launched a private placement of

258,000,000 new units at S$1.16 per

unit (which represents a 7% discount

to the adjusted volume weighted

average price at the day of the launch)

to raise approximately S$300m and

a 1-for-15 preferential offering to

raise approximately S$108m. The

net proceeds from the equity fund

raising exercise were used to fund

committed development projects and

to reduce borrowings

Feb

16th

Completion of 3 Changi Business

Park Crescent, a pre-committed

business park development for

Citibank N.A.

Mar

20th

Established a S$1 bn

Multicurrency Medium Term

Note (MTN) program to diversify

sources of funds for A-REIT.

The program has been

assigned a Baa2 rating

April

17th

Financial Year ended 31 March

2009: Distribution per unit grew

7.4% y-o-y

23rd

A-REIT’s development project, a

business park property at

3 Changi Business Park Crescent,

was awarded the BCA Green

Mark Platinum Award, the

highest accolade in Singapore for

environmental sustainability.

30th

First issuance of S$110m fixed

rate notes due 2011 as part of

the newly establish MTN program

2009

0809

Financial Highlights

FY 08/0907/0806/0705/0604/0503/0402/03FY 08/0907/0806/0705/0604/0503/0402/03

FY 08/0907/0806/0705/0604/0503/0402/03 FY 08/0907/0806/0705/0604/0503/0402/03

NET INCOME (S$m) NET INCOME AVAILABLE

FOR DISTRIBUTION (S$m)

EARNINGS PER UNIT

(”EPU”) (cents)(2)

DISTRIBUTION PER UNIT

(”DPU”) (cents)

200.7

175.0

148.4

132.0

75.2

40.6

14.3

210.9

187.3

163.8

142.6

84.2

45.5

15.2

15.1

8

14.1

3

12.7

5

11.6

8

9.5

6

8.1

6

7.6

3(1

)

6.1

1

18.3

6(1

)

50.3

1

26.1

3

11.8

4

10.9

8

8.6

5

Notes:

(1) Annualised based on restated EPU of 6.69 cents and actual DPU of 2.78 cents for the 133 days ended 31 Mar 03

(2) The EPU has been calculated using total return for the period and the weighted average number of units on issue during the period. In accordance to FRS 33, comparative EPUs and weighted

average number of units for calculation of EPU have been restated to account for the effects of the rights issue in February 2009

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

As at

31 March 09080706050403 09080706050403 09080706050403

89

84

77

64

36

16

8

4,5

47.6

4,2

05.2

3,3

07.0

2,8

07.5

2112.3

1,0

20.7

636.4

1.6

1

1.8

4

1.4

9

1.3

4

1.2

3

0.9

8

0.9

1

NUMBER OF PROPERTIES

IN PORTFOLIO

TOTAL ASSETS (S$m) NET ASSET

VALUE PER UNIT (S$)

Notes:

(1) Before adjustment for distributable income not yet distributed.

(2) Based on respective closing prices on 31 Mar.

(3) Includes total borrowings and deferred payments on acquistion of properties.

As at

31 March

As at

31 March

FINANCIAL YEAR 02/03 03/04 04/05 05/06 06/07 07/08 08/09

Total net borrowings (S$m) 125.0 263.8 553.9 969.8 1,183.5 1,559.9 1,588.7

Total Unitholders' funds (S$m) (1) 498.2 691.6 1,425.5 1,708.4 1,970.0 2,438.0 2,703.0

Market capitalisation (S$m) (2) 444.2 898.2 2,181.8 2,663.0 3,158.6 3,154.8 2,053.8

Aggregate leverage (3) 19.6% 28.9% 30.2% 36.8% 37.3% 38.2% 35.5%

Unit price (2) (S$) 0.82 1.27 1.88 2.17 2.39 2.38 1.22

Number of Units in issue (m) 545.0 707.2 1,160.6 1,227.2 1,321.6 1,325.6 1,683.5

1011

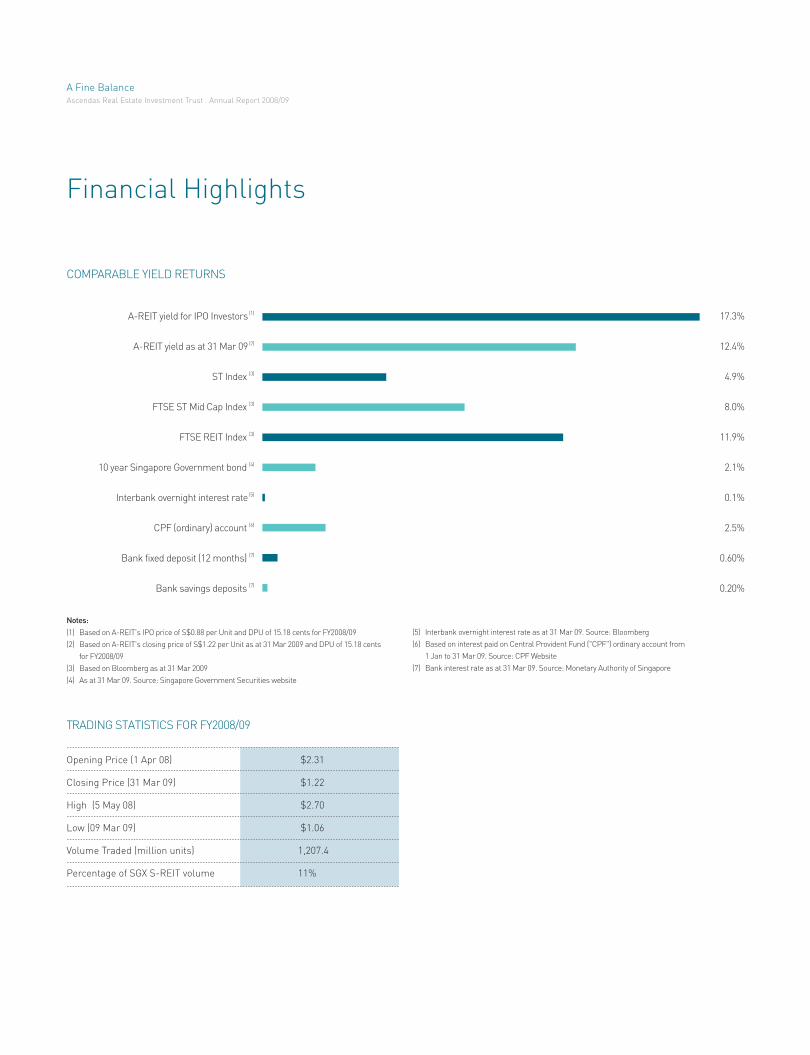

17.3%

12.4%

4.9%

8.0%

11.9%

2.1%

0.1%

2.5%

0.60%

0.20%

A-REIT yield for IPO Investors (1)

A-REIT yield as at 31 Mar 09 (2)

ST Index (3)

FTSE ST Mid Cap Index (3)

FTSE REIT Index (3)

10 year Singapore Government bond (4)

Interbank overnight interest rate (5)

CPF (ordinary) account (6)

Bank fixed deposit (12 months) (7)

Bank savings deposits (7)

Notes:

(1) Based on A-REIT's IPO price of S$0.88 per Unit and DPU of 15.18 cents for FY2008/09

(2) Based on A-REIT's closing price of S$1.22 per Unit as at 31 Mar 2009 and DPU of 15.18 cents

for FY2008/09

(3) Based on Bloomberg as at 31 Mar 2009

(4) As at 31 Mar 09. Source: Singapore Government Securities website

COMPARABLE YIELD RETURNS

(5) Interbank overnight interest rate as at 31 Mar 09. Source: Bloomberg

(6) Based on interest paid on Central Provident Fund ("CPF") ordinary account from

1 Jan to 31 Mar 09. Source: CPF Website

(7) Bank interest rate as at 31 Mar 09. Source: Monetary Authority of Singapore

TRADING STATISTICS FOR FY2008/09

Opening Price (1 Apr 08) $2.31

Closing Price (31 Mar 09) $1.22

High (5 May 08) $2.70

Low (09 Mar 09) $1.06

Volume Traded (million units) 1,207.4

Percentage of SGX S-REIT volume 11%

Financial Highlights

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

% CHANGE (unit price / index value)

1,400

1,200

1,000

800

600

400

200

0

$3.50

$3.00

$2.50

$2.00

$1.50

$1.00

$0.50

$0.00

MONTHLY TRADING PERFORMANCE SINCE IPO TURNOVER

Nov 02 (IPO) FY2002/03 FY2003/04 FY2004/05 FY2005/06 FY2006/07 FY2007/08 APR 08 MAY 08 JUN 08 JUL 08 AUG 08 SEP 08 OCT 08 NOV 08 DEC 08 JAN 09 FEB 09 MAR 09

Volume traded (’m) Unit Price

1213

120

110

100

90

80

70

60

50

40

30

April 08 May 08 Jun 08 Jul 08 Aug 08 Sep 08 Oct 08 Nov 08 Dec 08 Jan 09 Feb 09 Mar 09

STI

A-REIT

IND S-REIT

FTSE S-REIT

A-REIT unit price performance versus Singapore Market

Base: April 2008

(million units)Unit Price

(S$)

DONG

moveto advance or progress

MOVING BOLDLY, TREADING WISELY.

Taking quick and big strides doesn’t necessarily get you to your desired destination,

unless you are moving in the right direction. Corporate moves should not be made

just to be the biggest or fastest. Strategic decisions should always be well contemplated

and evaluated to ensure that they are made in a wise and sensible manner.

JING

reposedignified calmness;

composure

Chairman’s Message

FY2008/09 was challenging with the

implosion of the global financial

market and its consequent impact

on economic activities as aggregate

demand rapidly declined in the major

developed markets. Singapore, being

one of the world’s most open

economies, was not spared the

tumult. However, A-REIT continued

to focus on its core competencies

and re-calibrated its three-pronged

strategies to adapt to the changing

market conditions and delivered a

commendable set of financial results

for the year.

On behalf of the Board, I am pleased

to present A-REIT’s 7th annual

report for the financial year ended

31 Mar 2009. I am glad to report a

very successful year in which the

strategies pursued by the Manager

have delivered stable and predictable

distributions for the Unitholders of

A-REIT. This achievement is

remarkable especially in the light of

the global economic turbulence in

the second half of the financial year.

A-REIT’s distribution per unit (DPU)

increased by 7.4% to 15.18 cents as

compared to 14.13 cents in the

previous financial year after taking

its performance fees in cash instead

of units. The Manager opted to

receive its performance fees in cash

in order to close the gap between

earnings per unit and DPU, i.e. to

avoid paying distribution out of

capital and also not to further dilute

Unitholders’ interest as units are

currently trading at a discount to

its NAV. The portfolio grew to 89

properties versus 84 properties last

year, and total assets were S$4.5bn

as at 31 Mar 2009, up from S$4.2bn

a year ago, an increase of about 8%

despite a devaluation of S$115m on

the portfolio upon its regulatory

annual revaluation.

A Balanced Portfolio Performance

As at 31 Mar 2009, overall portfolio

occupancy stands at a healthy 97.8%,

with 95.3% occupancy for multi-

tenanted properties. The portfolio

continues to see positive rental

reversion in renewal rates across all

sub-sectors as a result of active

leasing management and the market

rental rates being higher than

existing rental rates of those leases

in A-REIT’s portfolio due for renewal.

This is particularly true for the

Business & Science Parks and Hi-

Tech Industrial sectors. However,

due to the deteriorating economic

situation, market spot rates have

been declining and the Manager has

shifted its strategic focus to

"Maintaining Occupancy, Retaining

Customers". As a result, positive

rental reversion, if any, for FY 2009/10

is expected to be relatively muted

compared to the last financial year.

The Manager’s disciplined

investment strategy has resulted in

enhanced returns per investment

dollar from development activities

and selective quality acquisition of

income producing properties which

resulted in a healthy and strong

balance sheet. During the financial

year, A-REIT completed two

acquisitions worth S$271.8m and

completed three development

projects worth about S$174.5m.

The three development projects:

Pioneer Hub, 15 Changi North Way

and 3 Changi Business Park

Crescent, were completed on

schedule and within budget and

achieved 100% occupancy on

completion. Since commencing its

development strategy in 2006,

A-REIT has achieved an unrealized

capital gain of $109.7m

(approximately 35.2% over

development cost) on the six

development projects undertaken

so far.

In addition, A-REIT commenced

construction of a 100% pre-

committed built-to-suit logistics

facility at the Airport Logistics Park

located in the east of Singapore.

A multi-tenanted business park

building cum amenity centre is also

currently under construction at

3 Changi Business Park Crescent.

These projects are expected to be

completed in 4Q2009. In May 2009,

A-REIT announced a built-to-suit

development of a Hi-Tech industrial

property for Singapore

Telecommunications Limited. This

development is expected to be

completed in 1Q2010.

A-REIT will continue to pursue quality

and sustainable yield accretive

acquisitions and, at the same time,

engage in development (especially

built-to-suit) opportunities for

enhanced returns.

Balancing the Finances

We persist in proactive capital and

risk management of A-REIT’s

finances in order to optimize its

capital structure. When the market

turned abruptly in the second half

of the financial year, a healthy capital

structure became the focal point of

the investing community.

A 3-year S$200 m committed credit

facility was secured in October 2008

to increase A-REIT’s funding capacity.

In Jan 2009, A-REIT launched an

equity fund raising exercise and

raised approximately S$408 m (at a

7% discount to the adjusted volume

weighted adjusted price at the day of

the launch) to fund committed

development projects, as well as to

to reduce borrowings. Aggregate

leverage as at 31 Mar 2009 was 35.5%

with 90.0% of A-REIT’s total debt

hedged into fixed rate for the next

3.4 years at an all-in cost of

borrowing of 3.67%. However,

refinancing cost and cost for new

borrowings are expected to be higher

over the next 12 months.

To further diversify A-REIT’s sources

of funding, a medium term note

(MTN) programme was established

and issuance of a 2-year note for

S$150m was completed in

Apr and May 2009.

The proactive management of

A-REIT’s capital structure has

enabled us to further enhance our

balance sheet. We will continue to

balance between certainty in our

capital structure and the cost of

debt to attain optimal returns for

our Unitholders.

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

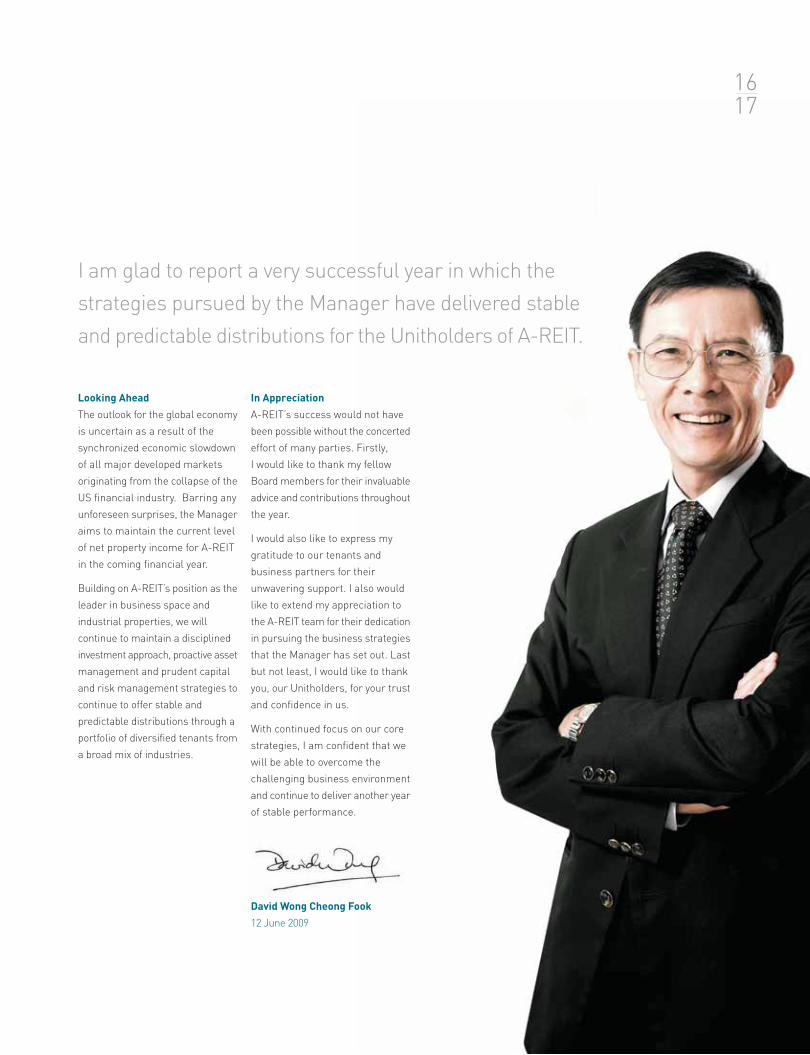

I am glad to report a very successful year in which the

strategies pursued by the Manager have delivered stable

and predictable distributions for the Unitholders of A-REIT.

1617

Looking Ahead

The outlook for the global economy

is uncertain as a result of the

synchronized economic slowdown

of all major developed markets

originating from the collapse of the

US financial industry. Barring any

unforeseen surprises, the Manager

aims to maintain the current level

of net property income for A-REIT

in the coming financial year.

Building on A-REIT’s position as the

leader in business space and

industrial properties, we will

continue to maintain a disciplined

investment approach, proactive asset

management and prudent capital

and risk management strategies to

continue to offer stable and

predictable distributions through a

portfolio of diversified tenants from

a broad mix of industries.

In Appreciation

A-REIT’s success would not have

been possible without the concerted

effort of many parties. Firstly,

I would like to thank my fellow

Board members for their invaluable

advice and contributions throughout

the year.

I would also like to express my

gratitude to our tenants and

business partners for their

unwavering support. I also would

like to extend my appreciation to

the A-REIT team for their dedication

in pursuing the business strategies

that the Manager has set out. Last

but not least, I would like to thank

you, our Unitholders, for your trust

and confidence in us.

With continued focus on our core

strategies, I am confident that we

will be able to overcome the

challenging business environment

and continue to deliver another year

of stable performance.

David Wong Cheong Fook

12 June 2009

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

1819

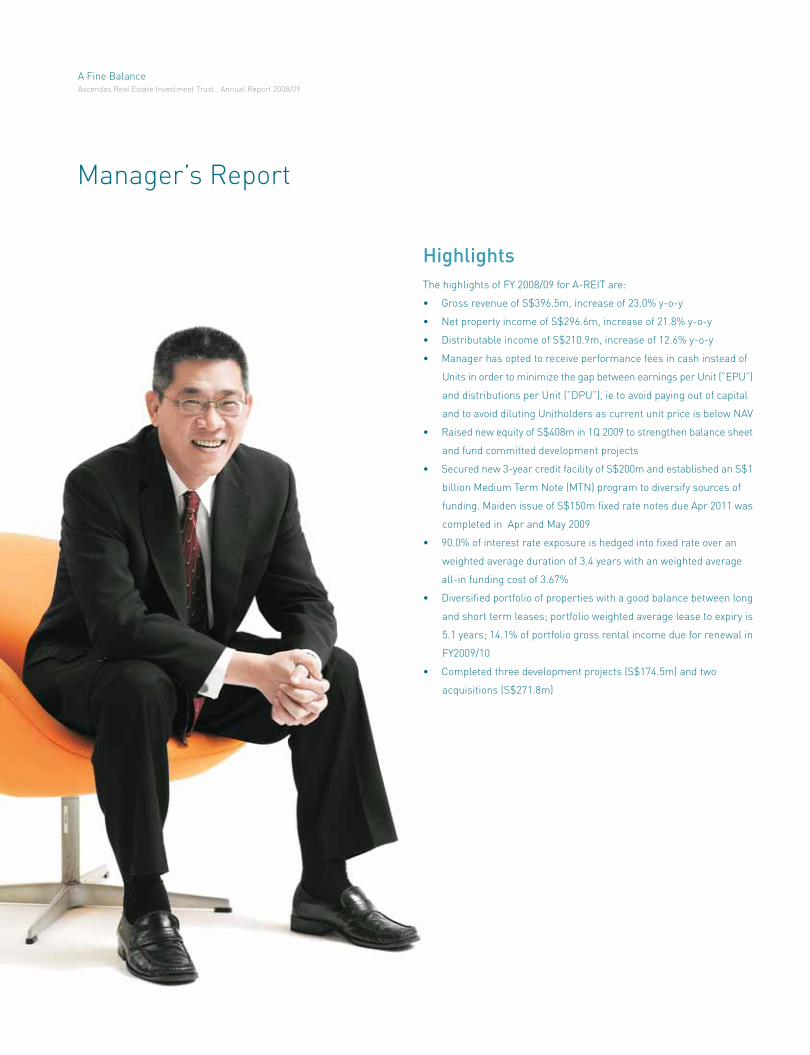

Manager’s Report

Highlights

The highlights of FY 2008/09 for A-REIT are:

• Gross revenue of S$396.5m, increase of 23.0% y-o-y

• Net property income of S$296.6m, increase of 21.8% y-o-y

• Distributable income of S$210.9m, increase of 12.6% y-o-y

• Manager has opted to receive performance fees in cash instead of

Units in order to minimize the gap between earnings per Unit (”EPU”)

and distributions per Unit (”DPU”), ie to avoid paying out of capital

and to avoid diluting Unitholders as current unit price is below NAV

• Raised new equity of S$408m in 1Q 2009 to strengthen balance sheet

and fund committed development projects

• Secured new 3-year credit facility of S$200m and established an S$1

billion Medium Term Note (MTN) program to diversify sources of

funding. Maiden issue of S$150m fixed rate notes due Apr 2011 was

completed in Apr and May 2009

• 90.0% of interest rate exposure is hedged into fixed rate over an

weighted average duration of 3.4 years with an weighted average

all-in funding cost of 3.67%

• Diversified portfolio of properties with a good balance between long

and short term leases; portfolio weighted average lease to expiry is

5.1 years; 14.1% of portfolio gross rental income due for renewal in

FY2009/10

• Completed three development projects (S$174.5m) and two

acquisitions (S$271.8m)

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

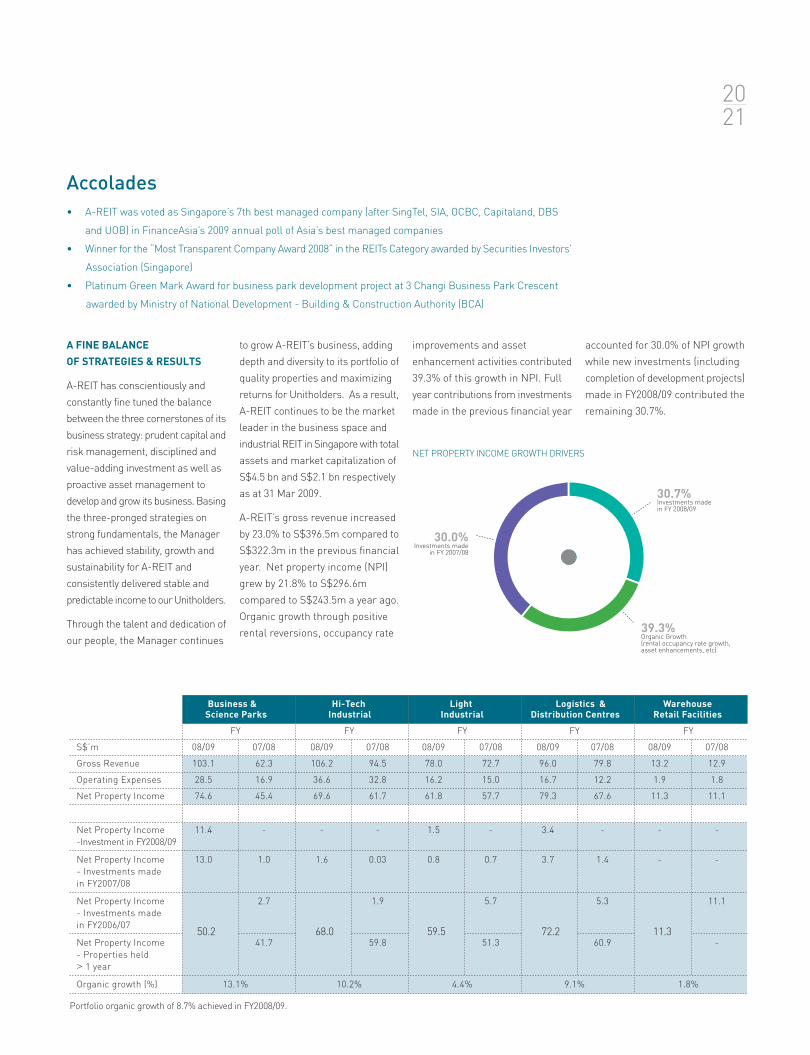

Business & Hi-Tech Light Logistics & Warehouse

Science Parks Industrial Industrial Distribution Centres Retail Facilities

FY FY FY FY FY

S$’m 08/09 07/08 08/09 07/08 08/09 07/08 08/09 07/08 08/09 07/08

Gross Revenue 103.1 62.3 106.2 94.5 78.0 72.7 96.0 79.8 13.2 12.9

Operating Expenses 28.5 16.9 36.6 32.8 16.2 15.0 16.7 12.2 1.9 1.8

Net Property Income 74.6 45.4 69.6 61.7 61.8 57.7 79.3 67.6 11.3 11.1

Net Property Income 11.4 - - - 1.5 - 3.4 - - -

-Investment in FY2008/09

Net Property Income 13.0 1.0 1.6 0.03 0.8 0.7 3.7 1.4 - -

- Investments made

in FY2007/08

Net Property Income 2.7 1.9 5.7 5.3 11.1

- Investments made

in FY2006/07

Net Property Income 41.7 59.8 51.3 60.9 -

- Properties held

> 1 year

Organic growth (%) 13.1% 10.2% 4.4% 9.1% 1.8%

50.2 68.0 59.5 72.2 11.3

Portfolio organic growth of 8.7% achieved in FY2008/09.

2021

30.7%Investments madein FY 2008/09

39.3%Organic Growth(rental occupancy rate growth,asset enhancements, etc)

30.0%Investments made

in FY 2007/08

NET PROPERTY INCOME GROWTH DRIVERS

A FINE BALANCE

OF STRATEGIES & RESULTS

A-REIT has conscientiously and

constantly fine tuned the balance

between the three cornerstones of its

business strategy: prudent capital and

risk management, disciplined and

value-adding investment as well as

proactive asset management to

develop and grow its business. Basing

the three-pronged strategies on

strong fundamentals, the Manager

has achieved stability, growth and

sustainability for A-REIT and

consistently delivered stable and

predictable income to our Unitholders.

Through the talent and dedication of

our people, the Manager continues

to grow A-REIT’s business, adding

depth and diversity to its portfolio of

quality properties and maximizing

returns for Unitholders. As a result,

A-REIT continues to be the market

leader in the business space and

industrial REIT in Singapore with total

assets and market capitalization of

S$4.5 bn and S$2.1 bn respectively

as at 31 Mar 2009.

A-REIT’s gross revenue increased

by 23.0% to S$396.5m compared to

S$322.3m in the previous financial

year. Net property income (NPI)

grew by 21.8% to S$296.6m

compared to S$243.5m a year ago.

Organic growth through positive

rental reversions, occupancy rate

Accolades

• A-REIT was voted as Singapore’s 7th best managed company (after SingTel, SIA, OCBC, Capitaland, DBS

and UOB) in FinanceAsia’s 2009 annual poll of Asia’s best managed companies

• Winner for the “Most Transparent Company Award 2008” in the REITs Category awarded by Securities Investors’

Association (Singapore)

• Platinum Green Mark Award for business park development project at 3 Changi Business Park Crescent

awarded by Ministry of National Development - Building & Construction Authority (BCA)

improvements and asset

enhancement activities contributed

39.3% of this growth in NPI. Full

year contributions from investments

made in the previous financial year

accounted for 30.0% of NPI growth

while new investments (including

completion of development projects)

made in FY2008/09 contributed the

remaining 30.7%.

Manager’s Report

April 08 May 08 Jun 08 Jul 08 Aug 08 Sep 08 Oct 08 Nov 08 Dec 08 Jan 09 Feb 09 Mar 09

140

120

100

80

60

40

20

0

-20

A-REIT

AMB Property

Prologis

Goodman Group

Brixton PLC

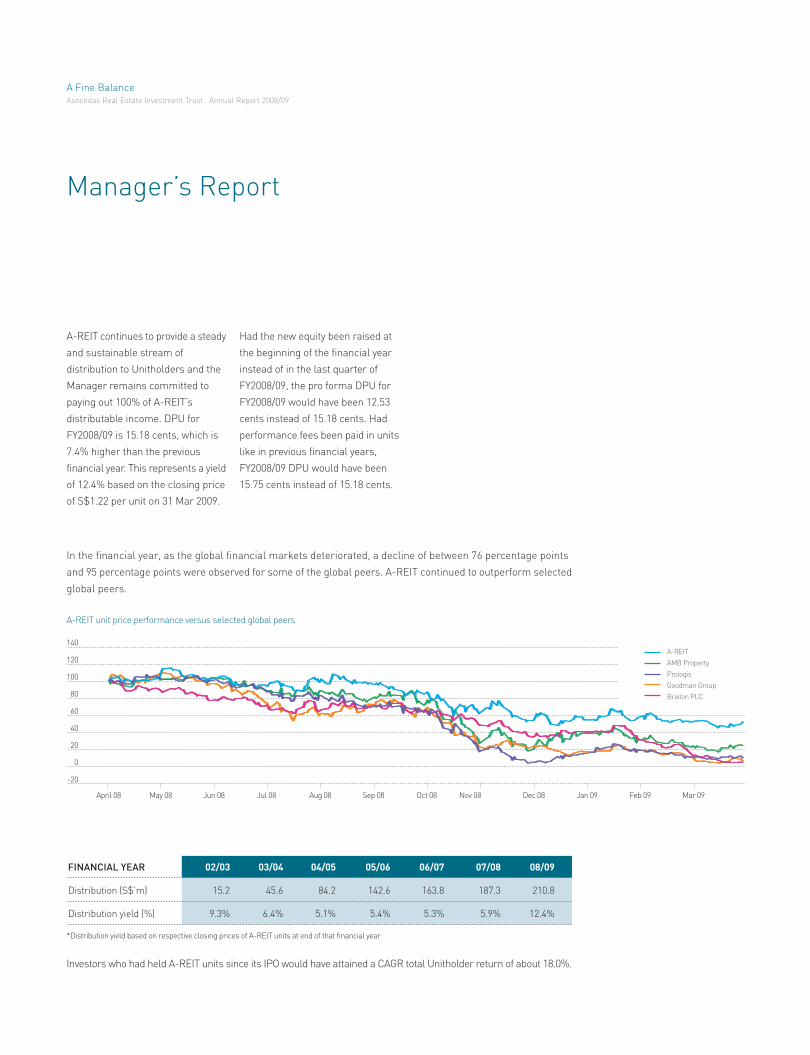

A-REIT unit price performance versus selected global peers

In the financial year, as the global financial markets deteriorated, a decline of between 76 percentage points

and 95 percentage points were observed for some of the global peers. A-REIT continued to outperform selected

global peers.

FINANCIAL YEAR 02/03 03/04 04/05 05/06 06/07 07/08 08/09

Distribution (S$’m) 15.2 45.6 84.2 142.6 163.8 187.3 210.8

Distribution yield (%) 9.3% 6.4% 5.1% 5.4% 5.3% 5.9% 12.4%

Investors who had held A-REIT units since its IPO would have attained a CAGR total Unitholder return of about 18.0%.

A-REIT continues to provide a steady

and sustainable stream of

distribution to Unitholders and the

Manager remains committed to

paying out 100% of A-REIT’s

distributable income. DPU for

FY2008/09 is 15.18 cents, which is

7.4% higher than the previous

financial year. This represents a yield

of 12.4% based on the closing price

of S$1.22 per unit on 31 Mar 2009.

Had the new equity been raised at

the beginning of the financial year

instead of in the last quarter of

FY2008/09, the pro forma DPU for

FY2008/09 would have been 12.53

cents instead of 15.18 cents. Had

performance fees been paid in units

like in previous financial years,

FY2008/09 DPU would have been

15.75 cents instead of 15.18 cents.

*Distribution yield based on respective closing prices of A-REIT units at end of that financial year

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

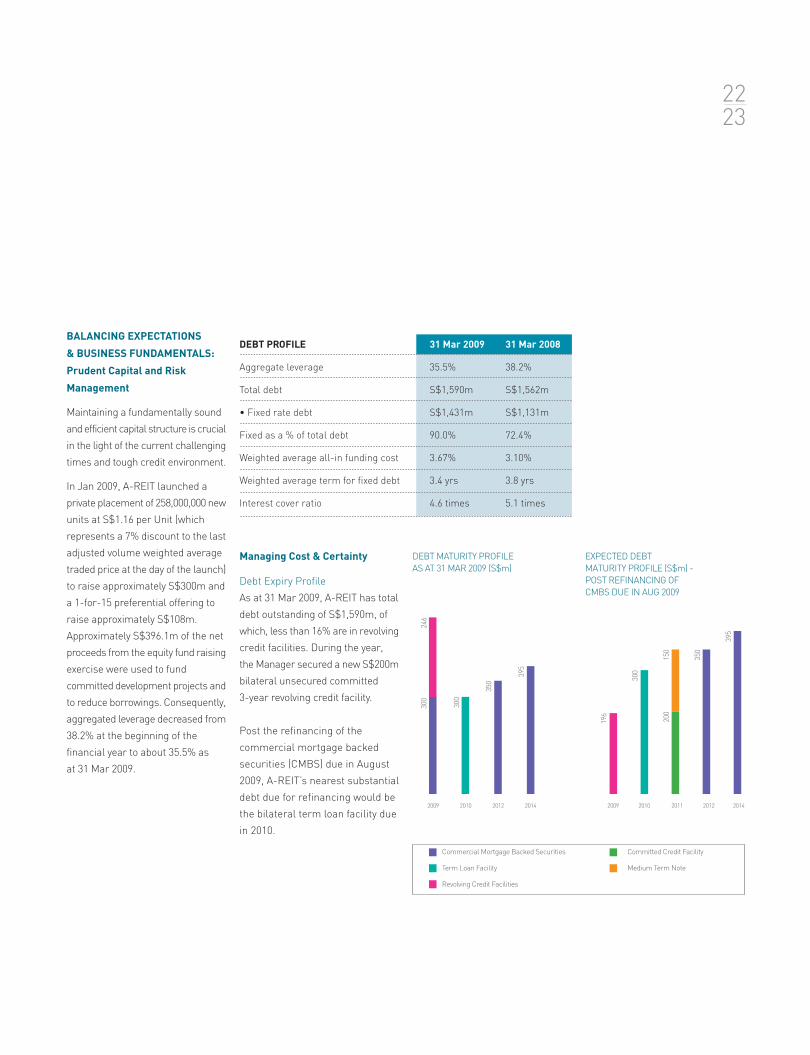

DEBT MATURITY PROFILE

AS AT 31 MAR 2009 (S$m)

BALANCING EXPECTATIONS

& BUSINESS FUNDAMENTALS:

Prudent Capital and Risk

Management

Maintaining a fundamentally sound

and efficient capital structure is crucial

in the light of the current challenging

times and tough credit environment.

In Jan 2009, A-REIT launched a

private placement of 258,000,000 new

units at S$1.16 per Unit (which

represents a 7% discount to the last

adjusted volume weighted average

traded price at the day of the launch)

to raise approximately S$300m and

a 1-for-15 preferential offering to

raise approximately S$108m.

Approximately S$396.1m of the net

proceeds from the equity fund raising

exercise were used to fund

committed development projects and

to reduce borrowings. Consequently,

aggregated leverage decreased from

38.2% at the beginning of the

financial year to about 35.5% as

at 31 Mar 2009.

Managing Cost & Certainty

Debt Expiry Profile

As at 31 Mar 2009, A-REIT has total

debt outstanding of S$1,590m, of

which, less than 16% are in revolving

credit facilities. During the year,

the Manager secured a new S$200m

bilateral unsecured committed

3-year revolving credit facility.

Post the refinancing of the

commercial mortgage backed

securities (CMBS) due in August

2009, A-REIT’s nearest substantial

debt due for refinancing would be

the bilateral term loan facility due

in 2010.

EXPECTED DEBT

MATURITY PROFILE (S$m) -

POST REFINANCING OF

CMBS DUE IN AUG 2009

2014201220102009

300

300

350

395

246

2009 2010 2011 2012 2014

Commercial Mortgage Backed Securities

Term Loan Facility

Revolving Credit Facilities

196

300

150

350

395

200

DEBT PROFILE 31 Mar 2009 31 Mar 2008

Aggregate leverage 35.5% 38.2%

Total debt S$1,590m S$1,562m

• Fixed rate debt S$1,431m S$1,131m

Fixed as a % of total debt 90.0% 72.4%

Weighted average all-in funding cost 3.67% 3.10%

Weighted average term for fixed debt 3.4 yrs 3.8 yrs

Interest cover ratio 4.6 times 5.1 times

2223

Committed Credit Facility

Medium Term Note

Liquidity Risk

To address the tight credit market

environment, the Manager has

diversified A-REIT’s sources of debt

funding by establishing an S$1bn

multi-currency Medium Term Note

(”MTN”) program on 20 Mar 2009.

The issues of 2-year fixed rate

notes for S$150m was completed

in April and May 2009. The Manager

will continue to explore various

funding options and tenure whilst

balancing them with an acceptable

cost of interest to ensure a

sustainable stream of distributions

to Unitholders.

Interest Rate Risk

Adopting a prudent stance on

interest rate exposure management,

the Manager has established a policy

to hedge at least 50% of A-REIT’s

interest rate risk exposure using

interest rate swaps. As of

31 Mar 2009, A-REIT maintained

about 90% of its interest rate

exposure in fixed rates over a

weighted average duration of 3.4

years. The overall portfolio weighted

average cost of borrowings is 3.67%.

The overall portfolio weighted

average cost of borrowings is

expected to increase to about 4%

post refinancing of the CMBS due

in Aug 2009 as cost of new

borrowings is expected to be higher.

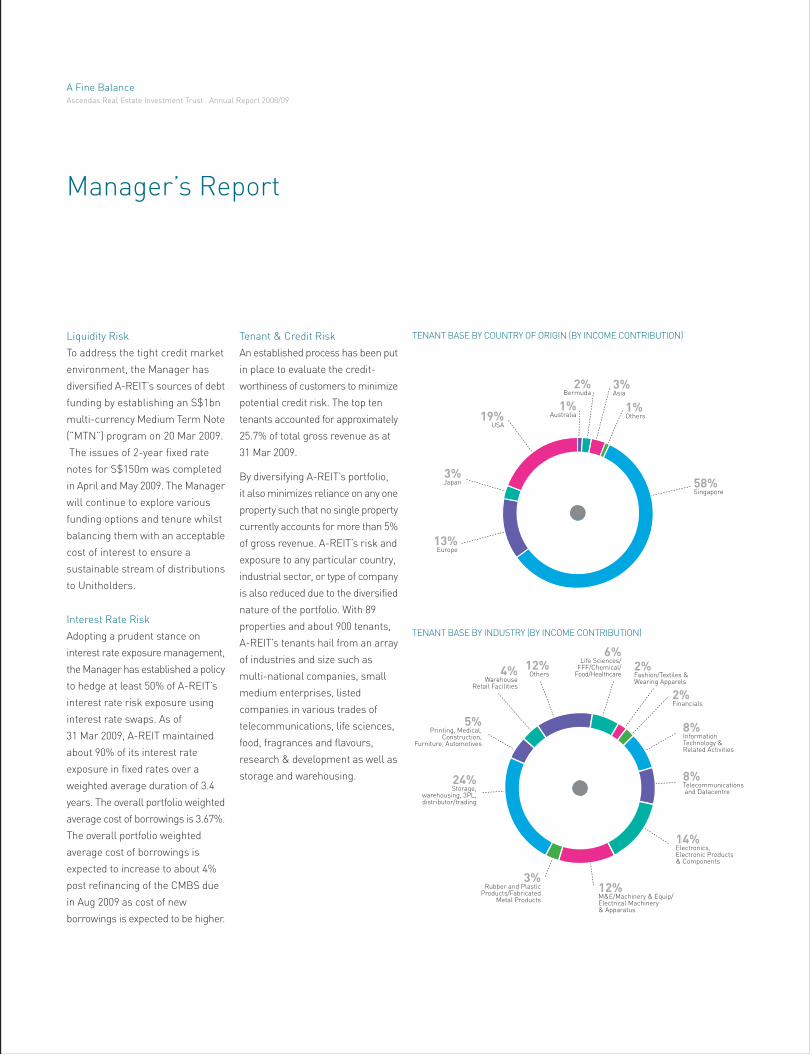

Tenant & Credit Risk

An established process has been put

in place to evaluate the credit-

worthiness of customers to minimize

potential credit risk. The top ten

tenants accounted for approximately

25.7% of total gross revenue as at

31 Mar 2009.

By diversifying A-REIT’s portfolio,

it also minimizes reliance on any one

property such that no single property

currently accounts for more than 5%

of gross revenue. A-REIT’s risk and

exposure to any particular country,

industrial sector, or type of company

is also reduced due to the diversified

nature of the portfolio. With 89

properties and about 900 tenants,

A-REIT’s tenants hail from an array

of industries and size such as

multi-national companies, small

medium enterprises, listed

companies in various trades of

telecommunications, life sciences,

food, fragrances and flavours,

research & development as well as

storage and warehousing.

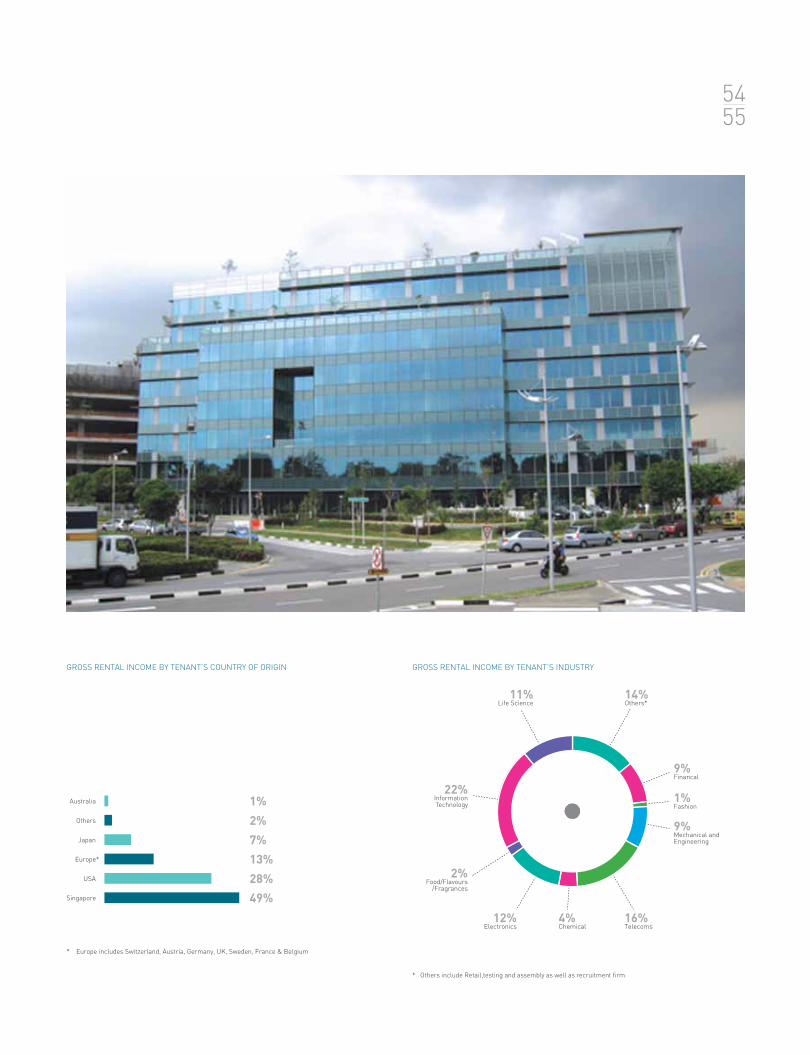

19%USA

1%Australia

2%Bermuda

3%Asia

1%Others

58%Singapore

13%Europe

3%Japan

TENANT BASE BY COUNTRY OF ORIGIN (BY INCOME CONTRIBUTION)

TENANT BASE BY INDUSTRY (BY INCOME CONTRIBUTION)

12%Others

6%Life Sciences/

FFF/Chemical/Food/Healthcare

2%Fashion/Textiles &Wearing Apparels

2%Financials

8%InformationTechnology &Related Activities

8%Telecommunications and Datacentre

14%Electronics,Electronic Products& Components

12%M&E/Machinery & Equip/Electrical Machinery& Apparatus

3%Rubber and Plastic

Products/FabricatedMetal Products

24%Storage,

warehousing, 3PL,distributor/trading

5%Printing, Medical,

Construction,Furniture, Automotives

4%Warehouse

Retail Facilities

Manager’s Report

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

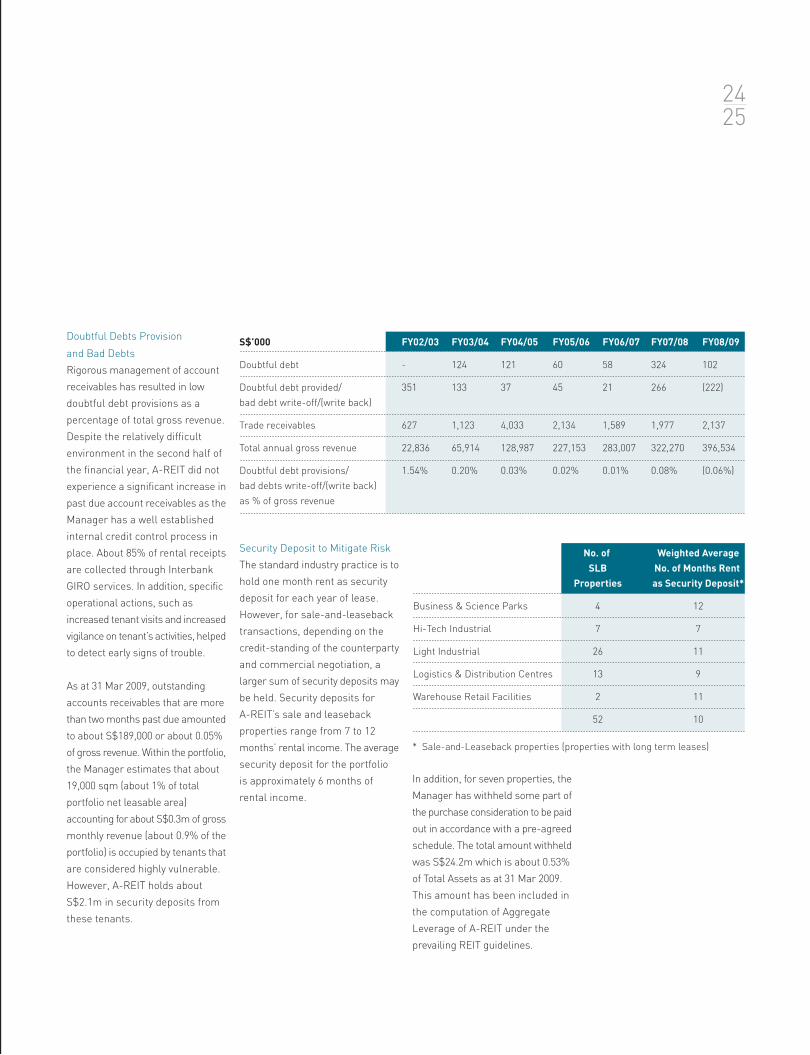

Doubtful Debts Provision

and Bad Debts

Rigorous management of account

receivables has resulted in low

doubtful debt provisions as a

percentage of total gross revenue.

Despite the relatively difficult

environment in the second half of

the financial year, A-REIT did not

experience a significant increase in

past due account receivables as the

Manager has a well established

internal credit control process in

place. About 85% of rental receipts

are collected through Interbank

GIRO services. In addition, specific

operational actions, such as

increased tenant visits and increased

vigilance on tenant’s activities, helped

to detect early signs of trouble.

As at 31 Mar 2009, outstanding

accounts receivables that are more

than two months past due amounted

to about S$189,000 or about 0.05%

of gross revenue. Within the portfolio,

the Manager estimates that about

19,000 sqm (about 1% of total

portfolio net leasable area)

accounting for about S$0.3m of gross

monthly revenue (about 0.9% of the

portfolio) is occupied by tenants that

are considered highly vulnerable.

However, A-REIT holds about

S$2.1m in security deposits from

these tenants.

S$’000 FY02/03 FY03/04 FY04/05 FY05/06 FY06/07 FY07/08 FY08/09

Doubtful debt - 124 121 60 58 324 102

Doubtful debt provided/ 351 133 37 45 21 266 (222)

bad debt write-off/(write back)

Trade receivables 627 1,123 4,033 2,134 1,589 1,977 2,137

Total annual gross revenue 22,836 65,914 128,987 227,153 283,007 322,270 396,534

Doubtful debt provisions/ 1.54% 0.20% 0.03% 0.02% 0.01% 0.08% (0.06%)

bad debts write-off/(write back)

as % of gross revenue

Security Deposit to Mitigate Risk

The standard industry practice is to

hold one month rent as security

deposit for each year of lease.

However, for sale-and-leaseback

transactions, depending on the

credit-standing of the counterparty

and commercial negotiation, a

larger sum of security deposits may

be held. Security deposits for

A-REIT’s sale and leaseback

properties range from 7 to 12

months’ rental income. The average

security deposit for the portfolio

is approximately 6 months of

rental income.

No. of Weighted Average

SLB No. of Months Rent

Properties as Security Deposit*

Business & Science Parks 4 12

Hi-Tech Industrial 7 7

Light Industrial 26 11

Logistics & Distribution Centres 13 9

Warehouse Retail Facilities 2 11

52 10

* Sale-and-Leaseback properties (properties with long term leases)

In addition, for seven properties, the

Manager has withheld some part of

the purchase consideration to be paid

out in accordance with a pre-agreed

schedule. The total amount withheld

was S$24.2m which is about 0.53%

of Total Assets as at 31 Mar 2009.

This amount has been included in

the computation of Aggregate

Leverage of A-REIT under the

prevailing REIT guidelines.

2425

Manager’s Report

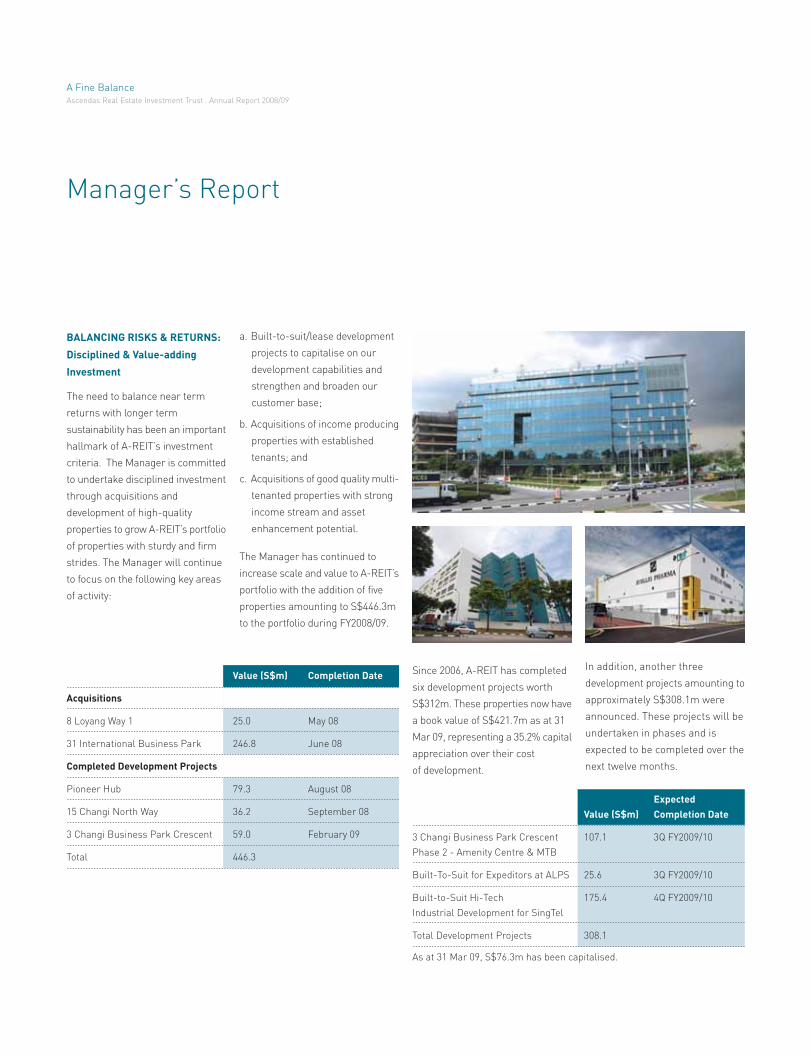

BALANCING RISKS & RETURNS:

Disciplined & Value-adding

Investment

The need to balance near term

returns with longer term

sustainability has been an important

hallmark of A-REIT’s investment

criteria. The Manager is committed

to undertake disciplined investment

through acquisitions and

development of high-quality

properties to grow A-REIT’s portfolio

of properties with sturdy and firm

strides. The Manager will continue

to focus on the following key areas

of activity:

Value (S$m) Completion Date

Acquisitions

8 Loyang Way 1 25.0 May 08

31 International Business Park 246.8 June 08

Completed Development Projects

Pioneer Hub 79.3 August 08

15 Changi North Way 36.2 September 08

3 Changi Business Park Crescent 59.0 February 09

Total 446.3

a. Built-to-suit/lease development

projects to capitalise on our

development capabilities and

strengthen and broaden our

customer base;

b. Acquisitions of income producing

properties with established

tenants; and

c. Acquisitions of good quality multi-

tenanted properties with strong

income stream and asset

enhancement potential.

The Manager has continued to

increase scale and value to A-REIT’s

portfolio with the addition of five

properties amounting to S$446.3m

to the portfolio during FY2008/09.

Since 2006, A-REIT has completed

six development projects worth

S$312m. These properties now have

a book value of S$421.7m as at 31

Mar 09, representing a 35.2% capital

appreciation over their cost

of development.

In addition, another three

development projects amounting to

approximately S$308.1m were

announced. These projects will be

undertaken in phases and is

expected to be completed over the

next twelve months.

Expected

Value (S$m) Completion Date

3 Changi Business Park Crescent 107.1 3Q FY2009/10

Phase 2 - Amenity Centre & MTB

Built-To-Suit for Expeditors at ALPS 25.6 3Q FY2009/10

Built-to-Suit Hi-Tech 175.4 4Q FY2009/10

Industrial Development for SingTel

Total Development Projects 308.1

As at 31 Mar 09, S$76.3m has been capitalised.

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

Development in progress:

3 Changi Business Park Crescent

To be developed over three phases,

the development at 3 Changi

Business Park Crescent comprises

three business park buildings and

an amenity podium. These buildings

will be sited on a land area of 29,864

sqm with a 60-year lease tenure and

will have a combined gross floor area

of 74,660 sqm.

This project is strategically located

at Changi Business Park, within a

short walking distance to the

Singapore Expo and Expo MRT

station and is easily accessible to

other parts of Singapore via major

expressways, namely, ECP, PIE

and TPE.

The first phase of the business park

buildings, with a gross floor area of

21,023 sqm is fully pre-committed

to Citibank NA for a lease term of 7

years with an option to extend for

another 3+3 years upon lease expiry.

It was completed in February 2009

and Citibank NA will be consolidating

its operations, technology and

support service to this building to

provide for greater synergies,

as well as cater for future

business growth.

The second building is a multi-

tenanted facility with gross floor area

of approximately 33,000 sqm of which

about 8,000 sqm is amenity space to

cater to the needs of the increasing

population at the Changi Business

Park. Expected date of completion

is in the second half of 2009.

Development in progress:

Built-to-Suit for Expeditors Pte Ltd

A new built-to-suit project for

Expeditors Singapore Pte Ltd was

committed during the financial year.

This investment comprises a part 2-

storey / part 4-storey logistics facility

at Plot 6 of the Airport Logistics Park

of Singapore which is strategically

located within the Airport Free Trade

Zone. Upon completion in the second

half of 2009, the development is

expected to have a gross floor area

of 12,707 sqm and a net lettable area

of 11,430 sqm and will be leased to

Expeditors Singapore Pte Ltd for a

period of five years with an option to

renew for another five years.

Development in progress:

Built-to-Suit Hi-Tech Industrial

Property for SingTel

A built-to-suit 9-storey Hi-Tech

Industrial building at Kim Chuan

Road for SingTel is in progress. Upon

completion in 1Q 2010, SingTel will

lease the building for 20 years with

annual rental escalation and with an

option to renew the lease for another

10 years. The investment, with a

gross floor area of approximately

32,862 sqm, is next to Kim Chuan

Telecommunications Complex, an

existing building owned by A-REIT

which is currently leased to SingTel.

This is a testament of the positive

working relationship with A-REIT’s

tenants and its ability to leverage on

existing tenants to further grow

its portfolio.

2627

Manager’s Report

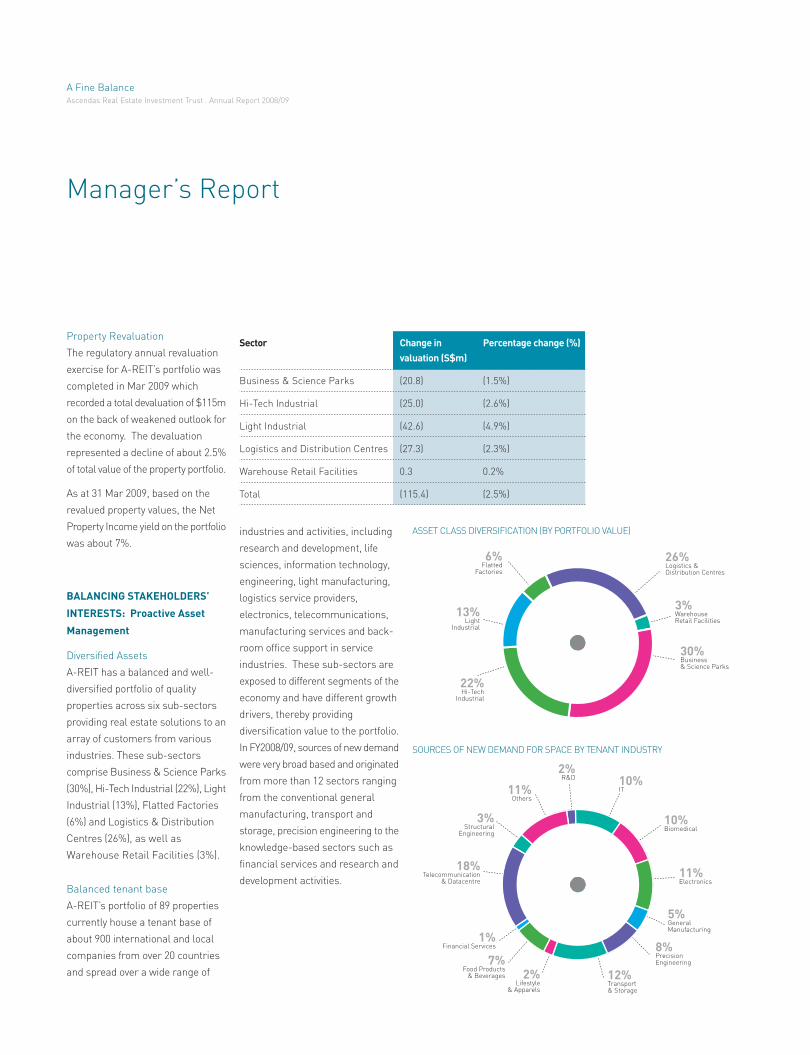

Property Revaluation

The regulatory annual revaluation

exercise for A-REIT’s portfolio was

completed in Mar 2009 which

recorded a total devaluation of $115m

on the back of weakened outlook for

the economy. The devaluation

represented a decline of about 2.5%

of total value of the property portfolio.

As at 31 Mar 2009, based on the

revalued property values, the Net

Property Income yield on the portfolio

was about 7%.

BALANCING STAKEHOLDERS’

INTERESTS: Proactive Asset

Management

Diversified Assets

A-REIT has a balanced and well-

diversified portfolio of quality

properties across six sub-sectors

providing real estate solutions to an

array of customers from various

industries. These sub-sectors

comprise Business & Science Parks

(30%), Hi-Tech Industrial (22%), Light

Industrial (13%), Flatted Factories

(6%) and Logistics & Distribution

Centres (26%), as well as

Warehouse Retail Facilities (3%).

Balanced tenant base

A-REIT’s portfolio of 89 properties

currently house a tenant base of

about 900 international and local

companies from over 20 countries

and spread over a wide range of

Sector Change in Percentage change (%)

valuation (S$m)

Business & Science Parks (20.8) (1.5%)

Hi-Tech Industrial (25.0) (2.6%)

Light Industrial (42.6) (4.9%)

Logistics and Distribution Centres (27.3) (2.3%)

Warehouse Retail Facilities 0.3 0.2%

Total (115.4) (2.5%)

industries and activities, including

research and development, life

sciences, information technology,

engineering, light manufacturing,

logistics service providers,

electronics, telecommunications,

manufacturing services and back-

room office support in service

industries. These sub-sectors are

exposed to different segments of the

economy and have different growth

drivers, thereby providing

diversification value to the portfolio.

In FY2008/09, sources of new demand

were very broad based and originated

from more than 12 sectors ranging

from the conventional general

manufacturing, transport and

storage, precision engineering to the

knowledge-based sectors such as

financial services and research and

development activities.

ASSET CLASS DIVERSIFICATION (BY PORTFOLIO VALUE)

SOURCES OF NEW DEMAND FOR SPACE BY TENANT INDUSTRY

3%Structural

Engineering

11%Others

2%R&D 10%

IT

10%Biomedical

11%Electronics

5%GeneralManufacturing

8%PrecisionEngineering

12%Transport& Storage

2%Lifestyle

& Apparels

7%Food Products

& Beverages

1%Financial Services

18%Telecommunication

& Datacentre

3%WarehouseRetail Facilities

13%Light

Industrial

30%Business& Science Parks

22%Hi-Tech

Industrial

6%Flatted

Factories

26%Logistics &Distribution Centres

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

29.3%

70.7%

Business And Science Parks (By NLA)

SHORT TERM & LONG TERM LEASES

BY SECTOR

Multi tenanted/Short term Leases

Sale-and-Leaseback/Long Term Leases

A-REIT has a high quality and

well-diversified tenant base. As of

31 Mar 2009, the top 10 tenants

account for 25.7% of total gross

revenue vis-á-vis 27.9% a year ago.

In addition, no single property

accounts for more than 5.0% of

gross revenue.

Well-balanced lease tenure

A-REIT has a mix of sale-and-

leaseback properties (48%) with long

term leases and multi-tenanted

properties (52%) with short term

leases. Sale-and-leaseback long

term leases typically have annual

stepped rental increases which

provide stable growth for the portfolio.

Majority of the leases in the Business

& Science Parks as well as High-

Tech industrial properties are on

short term basis. More than two-

third of the Logistic & Distribution

sector and the Light Industrial sector

are long term leases.

Singt

el

TOP 10 TENANTS BY GROSS REVENUE

(% of Gross Revenue)

5.8

%

C&P

Creat

ive

Cold

Stora

ge

Siem

ens

SENKEE L

ogist

ics

TT In

tern

ationa

l

Hewle

tt Pac

kard

Courts M

egas

tore

Toll

Asia

4.5

%

3.5

%

1.9

%

1.9

%

1.9

%

1.7

%

1.6

%

1.5

%

1.4

%

48%Sale-and-

Leaseback

52%Multi-tenantedBuildings

2829

38.9%

61.1%

Hi-tech Industrial (by NLA)

16.7%

83.3%

Ligh Industrial (by NLA)

39.1%

60.9%

Logistic and Distribution Centres (by NLA)

Manager’s Report

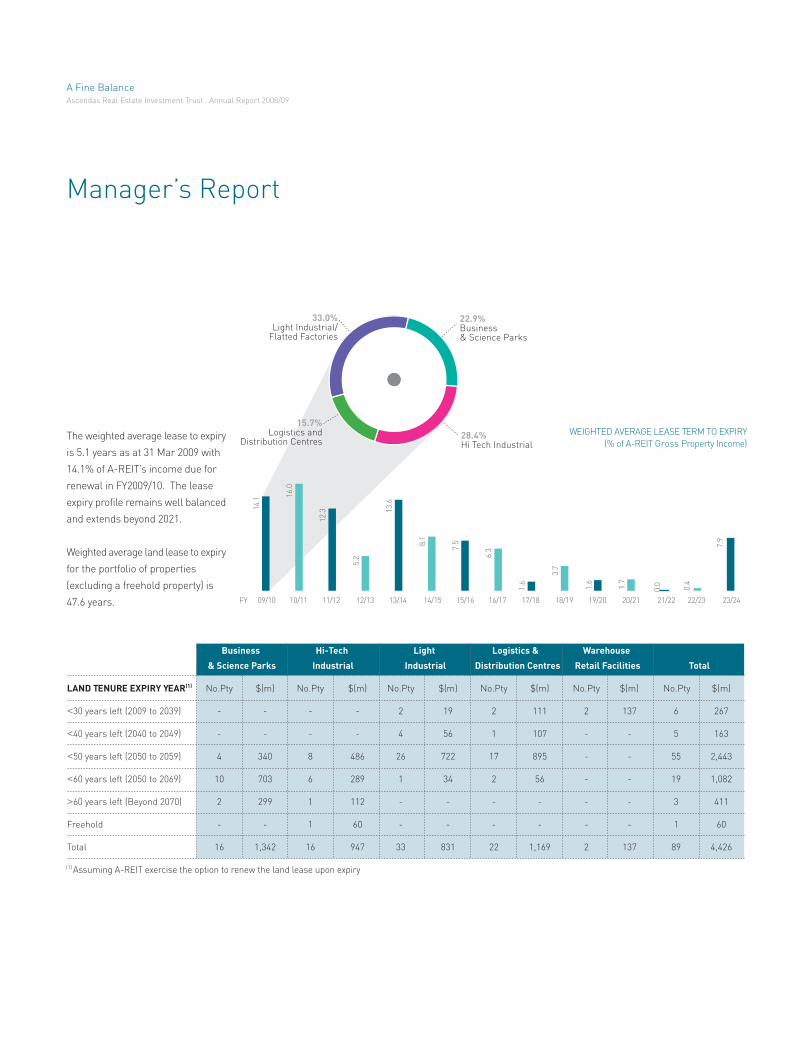

The weighted average lease to expiry

is 5.1 years as at 31 Mar 2009 with

14.1% of A-REIT’s income due for

renewal in FY2009/10. The lease

expiry profile remains well balanced

and extends beyond 2021.

Weighted average land lease to expiry

for the portfolio of properties

(excluding a freehold property) is

47.6 years.

Business Hi-Tech Light Logistics & Warehouse

& Science Parks Industrial Industrial Distribution Centres Retail Facilities Total

LAND TENURE EXPIRY YEAR(1) No.Pty $(m) No.Pty $(m) No.Pty $(m) No.Pty $(m) No.Pty $(m) No.Pty $(m)

<30 years left (2009 to 2039) - - - - 2 19 2 111 2 137 6 267

<40 years left (2040 to 2049) - - - - 4 56 1 107 - - 5 163

<50 years left (2050 to 2059) 4 340 8 486 26 722 17 895 - - 55 2,443

<60 years left (2050 to 2069) 10 703 6 289 1 34 2 56 - - 19 1,082

>60 years left (Beyond 2070) 2 299 1 112 - - - - - - 3 411

Freehold - - 1 60 - - - - - - 1 60

Total 16 1,342 16 947 33 831 22 1,169 2 137 89 4,426

(1) Assuming A-REIT exercise the option to renew the land lease upon expiry

WEIGHTED AVERAGE LEASE TERM TO EXPIRY

(% of A-REIT Gross Property Income)

FY 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23 23/24

14.1

16.0

12.3

5.2

13.6

8.1

7.5

6.3

1.6

3.7

1.6 1.7

0.0 0.4

7.9

22.9%Business& Science Parks

28.4%Hi Tech Industrial

33.0%Light Industrial/

Flatted Factories

15.7%Logistics and

Distribution Centres

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

About 75% of the properties in

A-REIT’s portfolio are on land rent

basis. This implies that the properties

do not have a land value accorded to

its valuation.

Maintaining Stability in

Challenging Times through

Proactive Asset Management

(delivered by the Property Manager,

Ascendas Services Pte Ltd)

A-REIT’s asset management function

is outsourced to its Property

Manager, Ascendas Services Pte Ltd

(ASPL), which has a dedicated and

proactive asset management team

who is constantly exploring

opportunities to optimize value within

the portfolio.

A demonstration of our active leasing

strategy and our positive relations

with our customers, A-REIT leased

and renewed a total of 185,929 sqm

of space within the portfolio in

FY2008/09, of which, 114,897 sqm

are renewal of leases. Our customer

retention rate stands at 80%,

signifying a large majority of

customers renewed their tenancy

with A-REIT upon expiration of their

existing leases.

PROPERTIES ON LAND RENT BASIS A-REIT’S PORTFOLIO OCCUPANCY RATE VS INDUSTRY

Active Leasing: Maintaining

Occupancy, Retaining Customers

Occupancy of the portfolio declined

marginally to 97.8% from 98.4% a

year ago in the face of the global

economic crisis. The occupancy

rate for multi-tenanted buildings

also decreased to 95.3% from 96.4%

a year ago. A notable observation

is that A-REIT’s portfolio occupancy

has consistently exceeded the

Urban Redevelopment Authority’s

(”URA”) island-wide occupancy

rates and despite the weak market

conditions, continues to maintain

this lead by between 2.6 and 7.9

percentage points.

96.4

%

93.8

%

95.3

%

91.0

% 98.9

%

91.0

% 98.7

%

92.8

%

Business Park Hi Tech Industrial Light Industrial Logistics

A-REIT

URA (Industry average)

3031

Percentage

of Portfolio

Property No. of Properties on Land Rent

Value on Land Rent Basis (by

Sector (S$m) Basis Property Value)

Business & Science Parks 1,342 8 30.5%

Hi-Tech Industrial 947 7 34.3%

Light Industrial/ Flatted Factories 831 30 64.0%

Logistics & Distribution Centres 1,169 22 100.0%

Warehouse Retail Facilities 137 0 0.0%

Total 4,426 67 55.0%

Manager’s Report

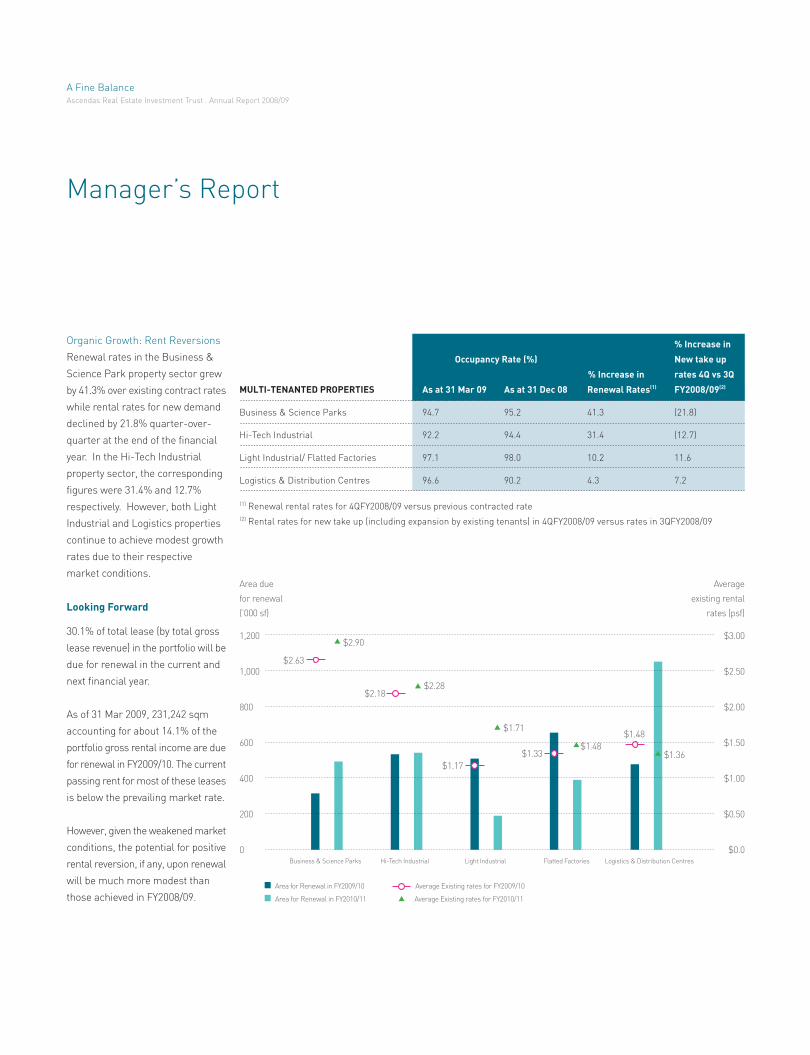

Organic Growth: Rent Reversions

Renewal rates in the Business &

Science Park property sector grew

by 41.3% over existing contract rates

while rental rates for new demand

declined by 21.8% quarter-over-

quarter at the end of the financial

year. In the Hi-Tech Industrial

property sector, the corresponding

figures were 31.4% and 12.7%

respectively. However, both Light

Industrial and Logistics properties

continue to achieve modest growth

rates due to their respective

market conditions.

Looking Forward

30.1% of total lease (by total gross

lease revenue) in the portfolio will be

due for renewal in the current and

next financial year.

As of 31 Mar 2009, 231,242 sqm

accounting for about 14.1% of the

portfolio gross rental income are due

for renewal in FY2009/10. The current

passing rent for most of these leases

is below the prevailing market rate.

However, given the weakened market

conditions, the potential for positive

rental reversion, if any, upon renewal

will be much more modest than

those achieved in FY2008/09.

% Increase in

Occupancy Rate (%) New take up

% Increase in rates 4Q vs 3Q

MULTI-TENANTED PROPERTIES As at 31 Mar 09 As at 31 Dec 08 Renewal Rates(1) FY2008/09(2)

Business & Science Parks 94.7 95.2 41.3 (21.8)

Hi-Tech Industrial 92.2 94.4 31.4 (12.7)

Light Industrial/ Flatted Factories 97.1 98.0 10.2 11.6

Logistics & Distribution Centres 96.6 90.2 4.3 7.2

(1) Renewal rental rates for 4QFY2008/09 versus previous contracted rate

(2) Rental rates for new take up (including expansion by existing tenants) in 4QFY2008/09 versus rates in 3QFY2008/09

$2.63

$2.90

$2.18$2.28

$1.17

$1.71

$1.33$1.48

$1.48

$1.36

1,200

1,000

800

600

400

200

0

$3.00

$2.50

$2.00

$1.50

$1.00

$0.50

$0.0Business & Science Parks Hi-Tech Industrial Light Industrial Flatted Factories Logistics & Distribution Centres

Area due

for renewal

(’000 sf)

Average

existing rental

rates (psf)

Area for Renewal in FY2009/10

Area for Renewal in FY2010/11

Average Existing rates for FY2009/10

Average Existing rates for FY2010/11

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

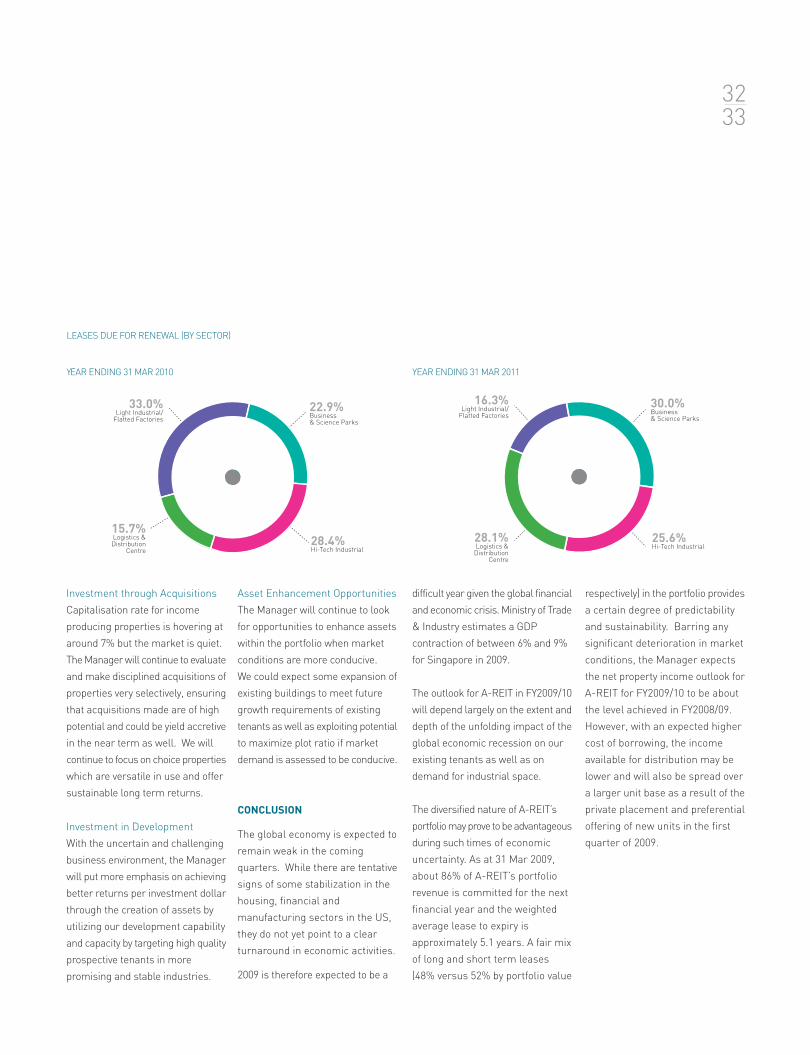

Investment through Acquisitions

Capitalisation rate for income

producing properties is hovering at

around 7% but the market is quiet.

The Manager will continue to evaluate

and make disciplined acquisitions of

properties very selectively, ensuring

that acquisitions made are of high

potential and could be yield accretive

in the near term as well. We will

continue to focus on choice properties

which are versatile in use and offer

sustainable long term returns.

Investment in Development

With the uncertain and challenging

business environment, the Manager

will put more emphasis on achieving

better returns per investment dollar

through the creation of assets by

utilizing our development capability

and capacity by targeting high quality

prospective tenants in more

promising and stable industries.

Asset Enhancement Opportunities

The Manager will continue to look

for opportunities to enhance assets

within the portfolio when market

conditions are more conducive.

We could expect some expansion of

existing buildings to meet future

growth requirements of existing

tenants as well as exploiting potential

to maximize plot ratio if market

demand is assessed to be conducive.

CONCLUSION

The global economy is expected to

remain weak in the coming

quarters. While there are tentative

signs of some stabilization in the

housing, financial and

manufacturing sectors in the US,

they do not yet point to a clear

turnaround in economic activities.

2009 is therefore expected to be a

difficult year given the global financial

and economic crisis. Ministry of Trade

& Industry estimates a GDP

contraction of between 6% and 9%

for Singapore in 2009.

The outlook for A-REIT in FY2009/10

will depend largely on the extent and

depth of the unfolding impact of the

global economic recession on our

existing tenants as well as on

demand for industrial space.

The diversified nature of A-REIT’s

portfolio may prove to be advantageous

during such times of economic

uncertainty. As at 31 Mar 2009,

about 86% of A-REIT’s portfolio

revenue is committed for the next

financial year and the weighted

average lease to expiry is

approximately 5.1 years. A fair mix

of long and short term leases

(48% versus 52% by portfolio value

respectively) in the portfolio provides

a certain degree of predictability

and sustainability. Barring any

significant deterioration in market

conditions, the Manager expects

the net property income outlook for

A-REIT for FY2009/10 to be about

the level achieved in FY2008/09.

However, with an expected higher

cost of borrowing, the income

available for distribution may be

lower and will also be spread over

a larger unit base as a result of the

private placement and preferential

offering of new units in the first

quarter of 2009.

22.9%Business& Science Parks

28.4%Hi-Tech Industrial

33.0%Light Industrial/

Flatted Factories

15.7%Logistics &Distribution

Centre

16.3%Light Industrial/

Flatted Factories

30.0%Business& Science Parks

25.6%Hi-Tech Industrial

28.1%Logistics &

DistributionCentre

YEAR ENDING 31 MAR 2010 YEAR ENDING 31 MAR 2011

3233

LEASES DUE FOR RENEWAL (BY SECTOR)

QUAN

authoritya power or right delegated or given

ZE

responsibiltya particular burden of obligation

upon one who is responsible;accountability

AUTHORITY TO EXECUTE, RESPONSIBILITIES TO ACCOUNT FOR.

Authority is the foundation to discharge responsibilities. Working towards a common goal,

the varied interests of various stakeholders: investors, customers and business partners

must be balanced. Responsibilities, Authority and Accountability are the three inseparable

legs of a balanced tripod upon which good execution is possible. People must be accountable

for the outcomes for which they have been empowered with the authority to deliver.

Board of Directors

Mr David Wong Cheong Fook

Chairman, Independent Director

Mr Wong is a Director on the boards

of LMA International NV, PacificMas

Bhd, Banking Computer Services

Pte Ltd, Jurong International

Holdings Pte Ltd, OCBC Bank

(Malaysia) Bhd and Teva

Pharmaceutical Investments

(Singapore) Pte Ltd. He is also a

Member of the Casino Regulatory

Authority and is a board member

of the National Environment

Agency. He is a Fellow of the

Institute of Certified Public

Accountants in Singapore, and a

member of the Institute of

Chartered Accountants in England

and Wales.

Mr Swee Kee Siong

Non-executive Director

Mr Swee is the Chairman of the

Investment Committee for

Ascendas India Development Trust,

Ascendas China Industrial &

Business Parks Fund and Ascendas

China Commercial Fund. He is a

Fellow of the Royal Institution of

Chartered Surveyors and Fellow of

the Singapore Institute of Surveyors

and Valuers. He has over 30 years

of experience in planning,

developing, marketing and

managing industrial estates,

business and science parks in

Singapore. Mr Swee was a member

of URA Master Plan Committee

from 1995 to 1998, the Chief

Executive Officer of Ascendas

Singapore operations and the

Singapore Science Park, and the

Deputy Chief Executive Officer of

Jurong Town Corporation.

Ms Chong Siak Ching

Vice Chairman,

Non-executive Director

Ms Chong is the President and

Chief Executive Officer of Ascendas

Pte Ltd. She sits on the boards of

Ascendas Pte Ltd and its

subsidiaries. Ascendas pioneered

Singapore’s first business space

trust, A-REIT in Nov 2002, and

Singapore’s first India-based

properties business trust, Ascendas

India Trust in August 2008. She is

also a Board Director on the

Singapore Tourism Board and the

Deputy Chairman of Spring

Singapore, the enterprise

development agency of Singapore.

She is also a Management Board

member of the Institute of Real

Estate Studies at the National

University of Singapore and the

Nanyang Business School’s

Graduate Board Member. Previously

Jurong Town Corporation’s Deputy

Chief Executive Officer, she has

extensive experience in business

space management.

Mr Benedict Kwek Gim Song

Independent Director

Chairman, Audit Committee

Mr Kwek is the Chairman of PST

Management Pte Ltd which is the

manager and trustee of SGX listed

Pacific Shipping Trust. He also

serves on the boards of Delmonte

Pacific Ltd and NTUC ChoiceHomes

Cooperative and NTUC Club, where

he is the Audit Committee

Chairman of the two former

companies. Mr Kwek, with over 32

years of banking experience, was

formerly the President and CEO of

Keppel TatLee Bank Ltd. He was

previously a Board Member of JTC

and a director of Jurong Port

Pte Ltd.

01

02

03

04

01 Mr David Wong Cheong Fook

02 Ms Chong Siak Ching

03 Mr Benedict Kwek Gim Song

04 Mr Swee Kee Siong

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

05 Mr Chia Kim Huat

06 Mr Joseph Chen Seow Chan

07 Mr Tan Ser Ping

Mr Chia Kim Huat

Independent Director

Mr Chia is presently a partner of

Rajah & Tann LLP and heads its

Corporate and China Practice

Group. Mr Chia has more than 16

years experience as a practicing

lawyer and his main areas of

practice include capital market

transactions, cross-border joint

ventures, private equity investments,

mergers and acquisitions, corporate

and banking transactions. He

graduated from National University

of Singapore with a Bachelor of

Laws (Honours) degree in 1992 and

is a member of the Singapore

Academy of Law and The Law

Society of Singapore.

Mr Tan Ser Ping

Executive Director, CEO

Mr Tan is responsible for the overall

management and operations of A-

REIT. He works with the Board

members to determine the

business strategies and plans for

the strategic development of

A-REIT. He works closely with the

A-REIT team to ensure that the

operations of A-REIT are in

accordance with the stated

business strategies. Prior to joining

the Manager, he was the Executive

Vice President of Real Estate

Development & Investment (REDI)

of Ascendas Pte Ltd where he was

responsible for formulating REDI

policies, strategies and plans

across all country operations and

developing new product offerings

and markets for Ascendas. He

headed the task force for the

establishment of A-REIT prior to

its listing.

Mr Joseph Chen Seow Chan

Independent Director

Mr Chen has 29 years of experience

in the treasury and fixed income

business. He worked in a number

of major foreign banks and the

Monetary Authority of Singapore,

prior to joining United Overseas

Bank (”UOB”), where he worked for

17 years. He was Managing

Director, Global Treasury of UOB

when he retired in November 2005.

He was also a Director of UOB

Bullion & Futures, a subsidiary of

UOB, until retirement. Mr Chen was

also a member of the UOB

Management Committee and the

Assets & Liabilities Committee.

Before joining Ascendas in 2001,

Mr Tan was Senior General

Manager for the Singapore Suzhou

Industrial Park Development

Company Ltd, Residential &

Commercial Business Group. In his

over 20 years of working experience,

he also held senior positions in

various banks including the Bank

of America, Standard Chartered

Bank and United Overseas Bank.

Mr Tan graduated from the National

University of Singapore with a

Bachelor of Accountancy (Honours)

degree. He obtained his Masters in

Business Administration from the

University of Leicester, UK.

05

06

07

3637

The A-REIT Team

The A-REIT Team

01 02 03

04 05 06 07 08 09 10 11 12

Tan Ser Ping

Chief Executive Officer

Executive Director

Please refer to page 37.

Tan Shu Lin

Head, Capital Markets

As Head of Capital Markets for the

Manager, Shu Lin is responsible for

managing the capital structure of

A-REIT as well as to oversee and

manage both equity and debt capital

markets transactions and other

capital market related activities.

She is also responsible for liaising

with analysts as well as potential

and existing investors.

Prior to joining the Manager, Shu Lin

was Assistant Vice President of Real

Estate Fund Management at Ascendas

Pte Ltd where she was responsible for

developing property fund management

activities in the region. She was also

responsible for sourcing and

evaluating potential investment

opportunities in the region. Before

joining Ascendas, Shu Lin has had

more than six years of working

experience with various financial

institutions. She graduated with a

First Class Honours degree in

Economics from University of

Portsmouth, United Kingdom and is

a Chartered Financial Analyst.

Kevin Lee

Foo Pei Teng

Co-Head, Business Development

& Investment

Kevin and Pei Teng are jointly

responsible for developing and

executing A-REIT’s business

development and investment

strategy. Their team is responsible

for generating and evaluating

opportunities for acquisition and

development, structuring deals,

negotiating and closing such

transactions.

Tan Tuan Hong

Head, Corporate Services

& Risk Management

Tuan Hong is responsible for

accounting, financial reporting

and analysis, taxation, risk

management and compliance

execution. Tuan Hong has over 20

years of experience in the areas of

financial control and planning for

companies in the manufacturing,

retail & distribution as well as

services industries.

Prior to joining the Manager,

Tuan Hong served as the Asia

Pacific Financial Controller of a

NASDAQ-listed company with

principal activities in operating

network-neutral data centres and

Internet exchange services.

Tuan Hong holds a Bachelor of

Accountancy degree from the

National University of Singapore

and a Master degree in Business

Administration from Manchester

Business School (UK). He is a

Fellow member of the Institute of

Certified Public Accountants of

Singapore and a member of the

British Computer Society.

01 Rina Ang

02 Tan Shu Lin

03 Tan Ser Ping

04 Mary De Souza

05 Roy Teo

06 Sharon Seet

07 Joanne Neo

08 Kevin Lee

09 Yong Kok Fong

10 Ryan Tan

11 Sabrina Tay

12 Stefanie Tan

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

13 14 15

16 17 18 19 20 21 22 23 24

Kevin Lee

Head, Industrial Properties Portfolio

As Portfolio Manager (Industrial

Properties), Kevin oversees the

Property Manager, ASPL, in its

asset management strategies and

execution for A-REIT’s portfolio of

Hi-Tech Industrial and Light

Industrial properties.

Prior to joining the Manager, Kevin

was Director at an international

property consultant where he has

served corporate clients and banks

involving assets appraisal and also

investment advisory. Kevin is a

licensed valuer and also a member

of the Royal Institution of Chartered

Surveyors. He holds a Bachelor of

Science degree in Land

Management from University of

Reading, United Kingdom.

Maria Theresa Belmonte

Legal Counsel

& Compliance Manager

Assistant Company Secretary

Theresa’s responsibilities include

providing legal advice in all areas

within A-REIT including legal

documentation for acquisitions.

She also serves as the Compliance

Manager for A-REIT and assists in

A-REIT’s corporate secretarial

matters. She was formerly an in-

house legal counsel in a SGX-listed

company and prior to that was a

practicing lawyer. She has previous

experience in the areas of real

property law, general corporate law

and corporate secretarial work.

Theresa was called to the Singapore

Bar after graduating with an LL.B

(Hons) from the National University

of Singapore.

Roy Teo

Head, Logistics Properties Portfolio

Coordinator, Asset Management

Roy oversees ASPL in its asset

management strategies and

execution for A-REIT’s portfolio of

logistics properties. As Coordinator

for the Asset Management function,

he is a crucial link between the

Manager (AFM) and the Property

Manager (ASPL) to ensure that the

optimal level of service and the best

possible outcome are delivered for

the A-REIT properties.

Prior to his current role with the

Manager, Roy was the Assistant

Manager for Business Development at

Keppel Logistics Pte Ltd. He has over

eight years of experience in the

logistics industry in areas including

finance, accounting, project

management and business

development in Singapore and

regionally. Roy holds a Bachelor of

Science (Honours) degree in Applied

Accountancy from Oxford Brookes

University and is an Affiliate

member of the Association of

Chartered Certified Accountants.

Foo Pei Teng

Head, Business & Science Park

and Warehouse Retail

Facilities Portfolio

As Portfolio Manager (Business &

Science Park and Warehouse Retail

Properties), Pei Teng oversees ASPL,

in its asset management strategies

and execution for A-REIT’s portfolio

of Business & Science Park and

Warehouse Retail properties.

Prior to joining the Manager, Pei

Teng was a Business Development

Manager with Ascendas Pte Ltd.

She was involved in the evaluation

of several regional real estate

development and investment deals

in Korea, Australia and the

Philippines. Pei Teng graduated

with a Bachelor of Business

(Honours) degree in Financial

Analysis from Nanyang Technological

University and a Master of Science

degree in Real Estate from

National University of Singapore.

19 Patricia Goh

20 Foo Pei Teng

21 Calvin Tay

22 Maria Theresa Belmonte

23 Ho Sok Teng

24 Crystal Koh

13 Chan Lai Kuan

14 Ng Kok Hua

15 Tan Tuan Hong

16 Carol Ng

17 Lee Yong Kian

18 Leong Sai Keong

Not in picture: Cassie Ang, Jeffrey Toh

4041

The Property Manager(Ascendas Services Pte Ltd)

The asset management function of A-REIT is outsourced to its Property Manager,

Ascendas Services Pte Ltd (ASPL), a 100% owned subsidiary of the Ascendas Group.

Under the leadership of its CEO, Mr Thomas Teo, the ASPL team is committed to provide proactive and

professional services by working closely with the Manager to enhance the market positioning and

attractiveness of our properties and services to maximize returns for A-REIT’s unitholders.

A Fine BalanceAscendas Real Estate Investment Trust . Annual Report 2008/09

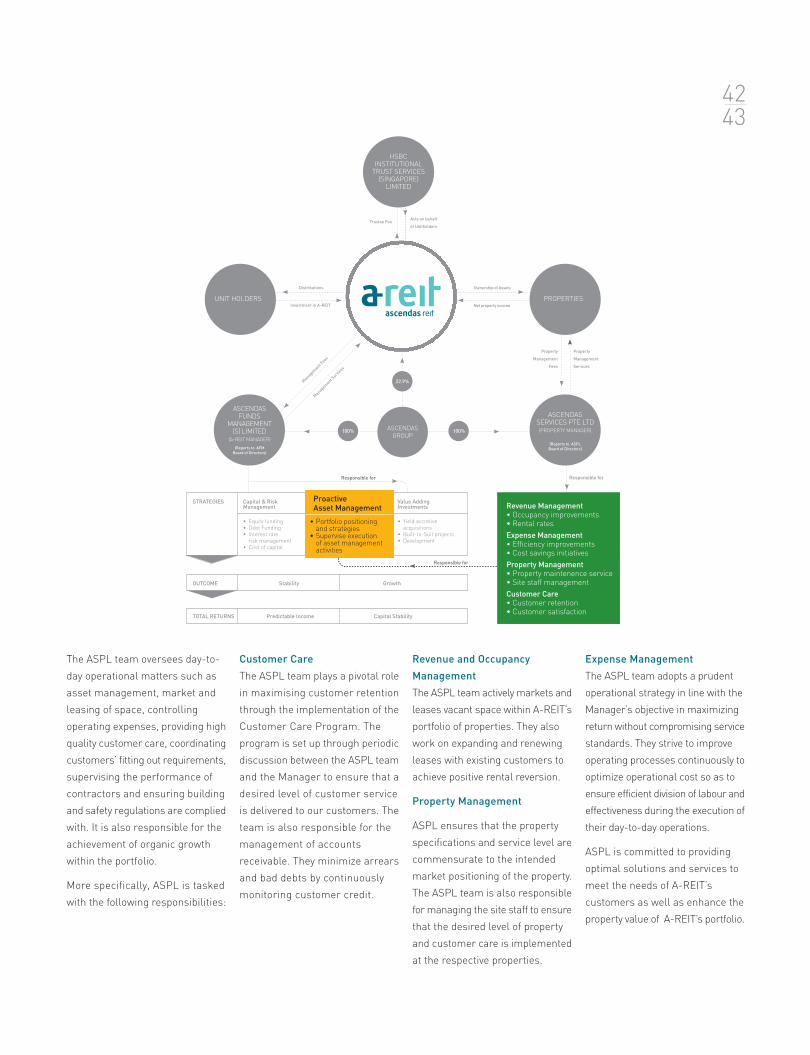

22.9%

100% 100%

Distributions

Investment in A-REIT

Ownership of Assets

Net property income

Acts on behalf

of UnitholdersTrustee Fee

Managem

ent Fees

Managem

ent Serv

ices

Property

Management

Fees

Property

Management

Services

STRATEGIES Capital & RiskManagement

ProactiveAsset Management

Value AddingInvestments

• Equity funding• Debt Funding• Interest rate

risk management• Cost of capital

• Portfolio positioning and strategies

• Supervise execution of asset managementactivities

• Yield accretive acquisitions

• Built-to-Suit projects• Development

OUTCOME Stability Growth

Revenue Management

• Occupancy improvements

• Rental rates

Expense Management

• Effi ciency improvements

• Cost savings initiatives

Property Management

• Property maintenence service

• Site staff management

Customer Care

• Customer retention

• Customer satisfaction

Responsible for Responsible for

Responsible for