Energy Technology Perspectives 2010eneken.ieej.or.jp/data/3481.pdf · ©OECD/IEA -2010 Energy...

32

© OECD/IEA - 2010 Energy Technology Perspectives 2010 IEEJ, Tokyo 4 November 2010 Dr Peter Taylor Head, Energy Technology Policy Division IEEJ: November 2010

Transcript of Energy Technology Perspectives 2010eneken.ieej.or.jp/data/3481.pdf · ©OECD/IEA -2010 Energy...

© OECD/IEA - 2010

Energy Technology Perspectives 2010

IEEJ, Tokyo4 November 2010

Dr Peter TaylorHead, Energy Technology Policy Division

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

The context

Need a global energy technology revolution to meet climate change and energy security challenges.

Some early signs of progress, but much more needs to be done.

Which technologies can play a role?

What are the costs and benefits?

What policies are needed?

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

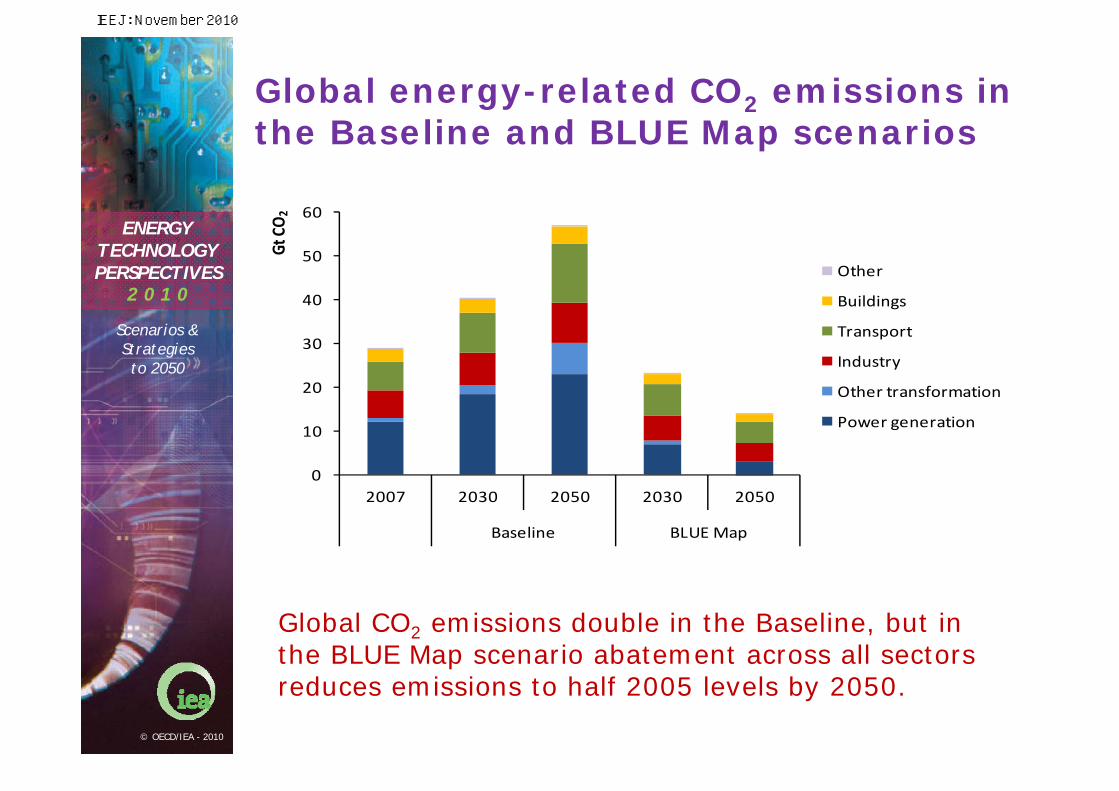

Global energy-related CO2 emissions in the Baseline and BLUE Map scenarios

0

10

20

30

40

50

60

2007 2030 2050 2030 2050

Baseline BLUE Map

Gt CO2

Other

Buildings

Transport

Industry

Other transformation

Power generation

Global CO2 emissions double in the Baseline, but in the BLUE Map scenario abatement across all sectors reduces emissions to half 2005 levels by 2050.

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

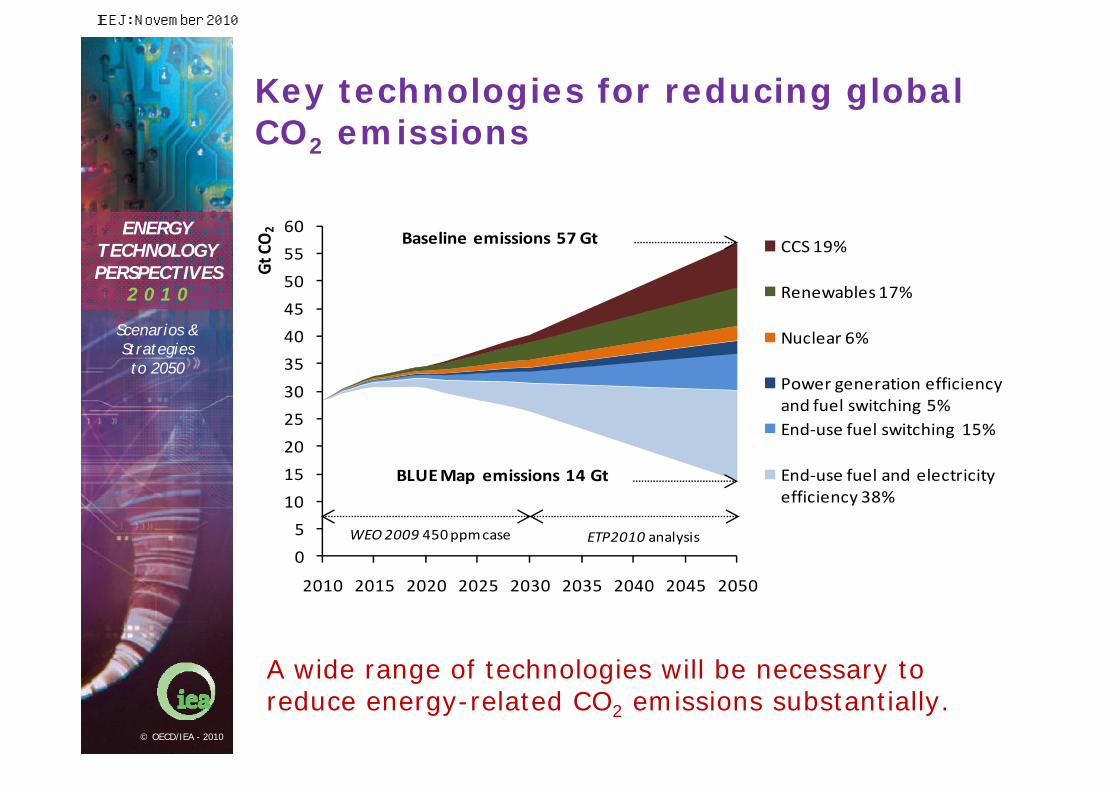

Key technologies for reducing global CO2 emissions

A wide range of technologies will be necessary to reduce energy-related CO2 emissions substantially.

0

5

10

15

20

25

30

35

40

45

50

55

60

2010 2015 2020 2025 2030 2035 2040 2045 2050

Gt CO2

CCS 19%

Renewables 17%

Nuclear 6%

Power generation efficiency and fuel switching 5%End‐use fuel switching 15%

End‐use fuel and electricity efficiency 38%

BLUE Map emissions 14 Gt

Baseline emissions 57 Gt

WEO 2009 450 ppmcase ETP2010 analysis

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Primary energy demand by fuel and by scenario

By 2050, coal, oil and gas demand are all lower than today under the BLUE Map scenario.

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

Mtoe 2007 Baseline 2050 BLUE Map 2050

‐27%

‐36%

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

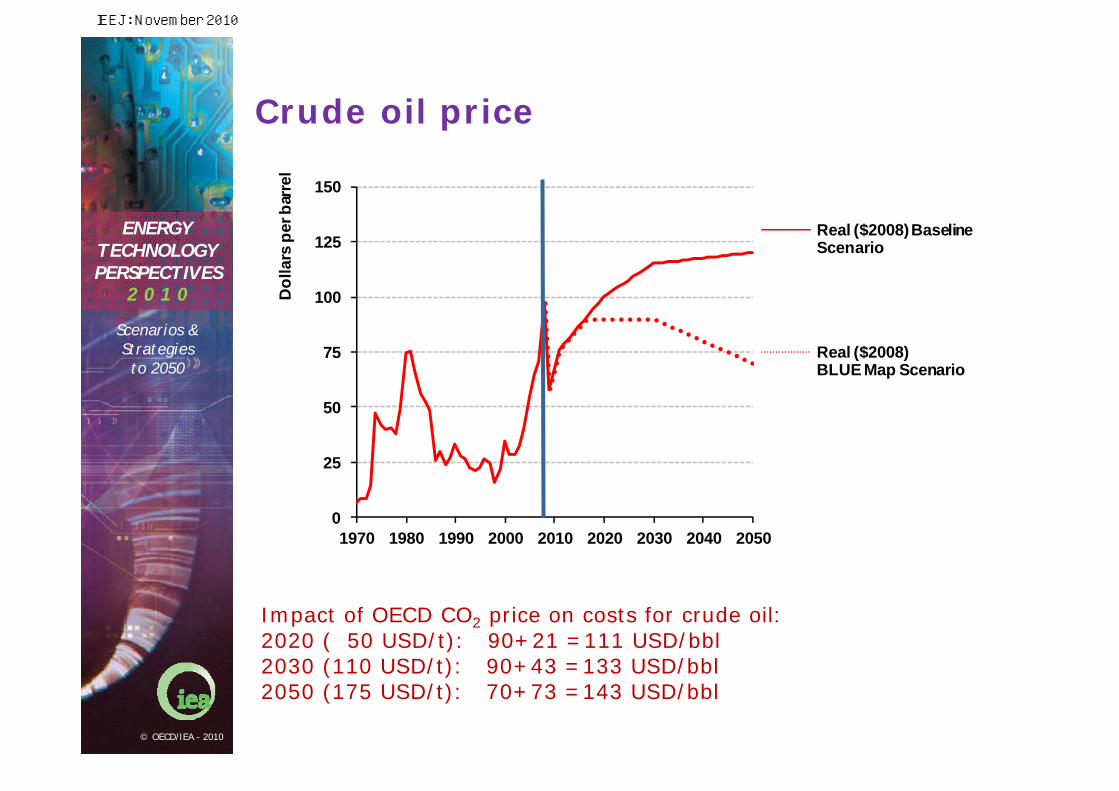

Crude oil price

Impact of OECD CO2 price on costs for crude oil:2020 ( 50 USD/t): 90+21 =111 USD/bbl 2030 (110 USD/t): 90+43 =133 USD/bbl2050 (175 USD/t): 70+73 =143 USD/bbl

0

25

50

75

100

125

150

1970 1980 1990 2000 2010 2020 2030 2040 2050

Dol

lars

per

bar

rel

Real ($2008) Baseline Scenario

Real ($2008) BLUE Map Scenario

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

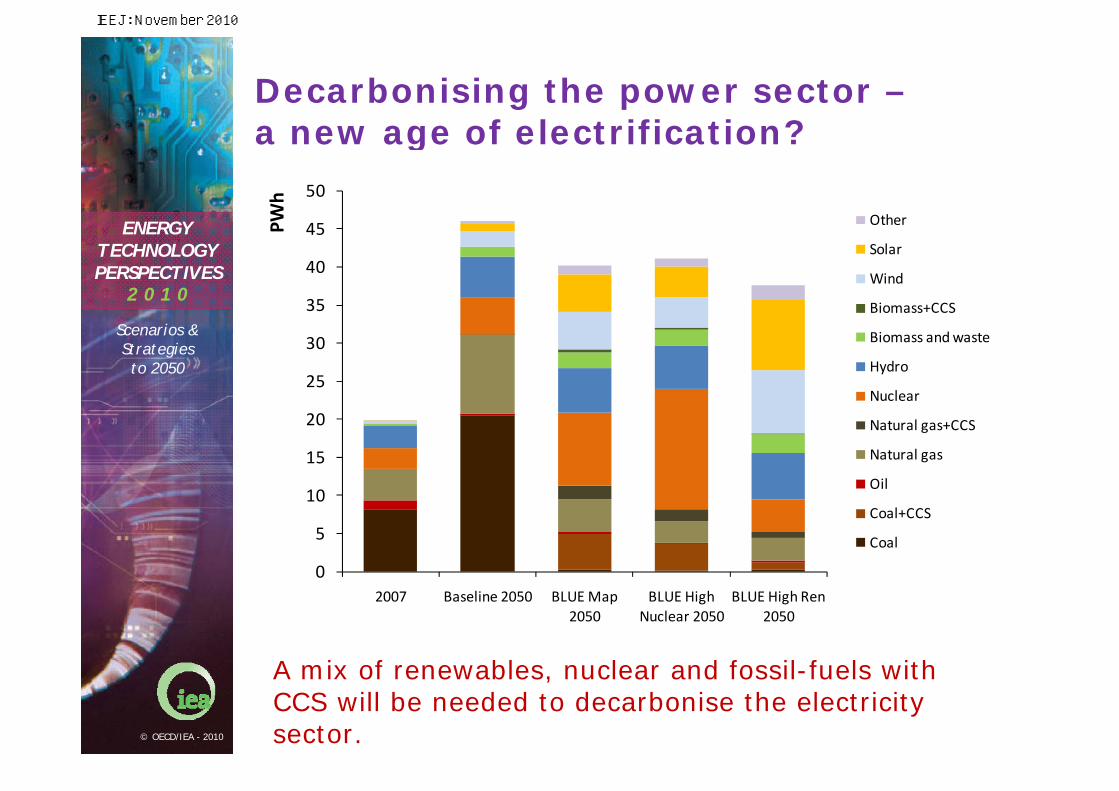

Decarbonising the power sector –a new age of electrification?

A mix of renewables, nuclear and fossil-fuels with CCS will be needed to decarbonise the electricity sector.

0

5

10

15

20

25

30

35

40

45

50

2007 Baseline 2050 BLUE Map 2050

BLUE High Nuclear 2050

BLUE High Ren 2050

PWh

Other

Solar

Wind

Biomass+CCS

Biomass and waste

Hydro

Nuclear

Natural gas+CCS

Natural gas

Oil

Coal+CCS

Coal

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

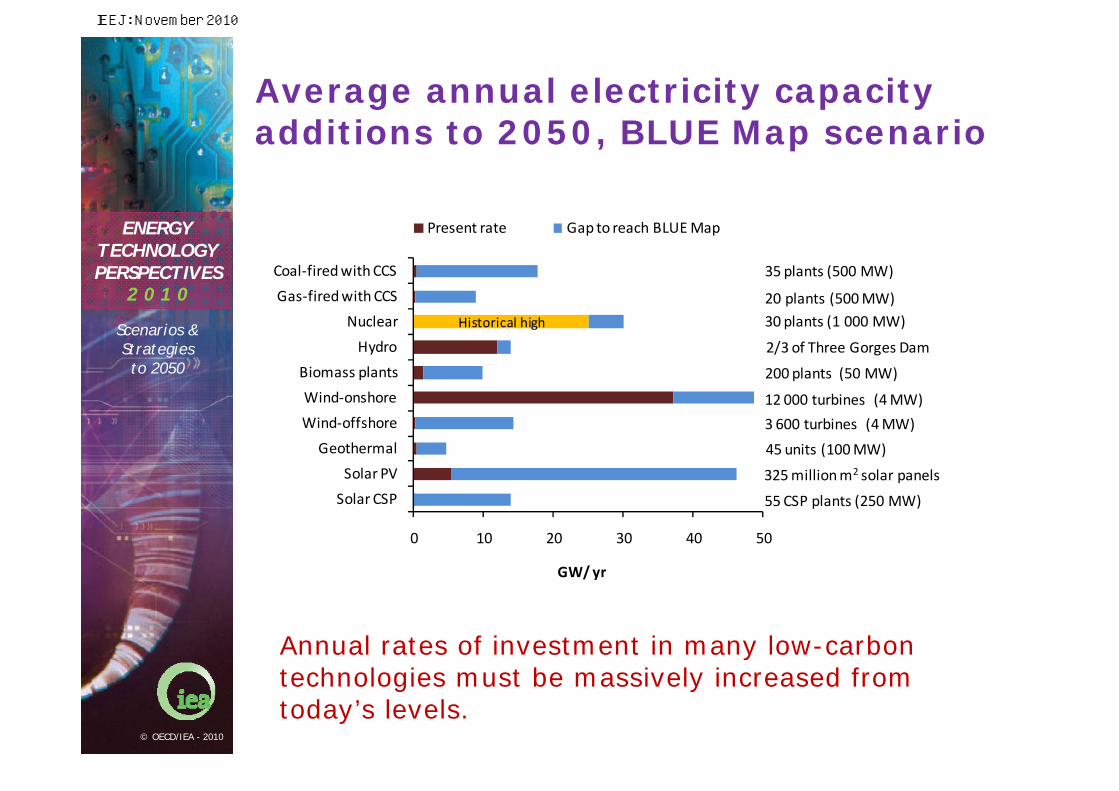

Average annual electricity capacity additions to 2050, BLUE Map scenario

Annual rates of investment in many low-carbon technologies must be massively increased from today’s levels.

0 10 20 30 40 50

Solar CSP

Solar PV

Geothermal

Wind‐offshore

Wind‐onshore

Biomass plants

Hydro

Nuclear

Gas‐fired with CCS

Coal‐fired with CCS

GW/ yr

Present rate Gap to reach BLUE Map

30 plants (1 000 MW)

200 plants (50 MW)

12 000 turbines (4 MW)

3 600 turbines (4 MW)

45 units (100 MW)

55 CSP plants (250 MW)

325 million m2 solar panels

2/3 of Three Gorges Dam

35 plants (500 MW)

20 plants (500 MW)

Historical high

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

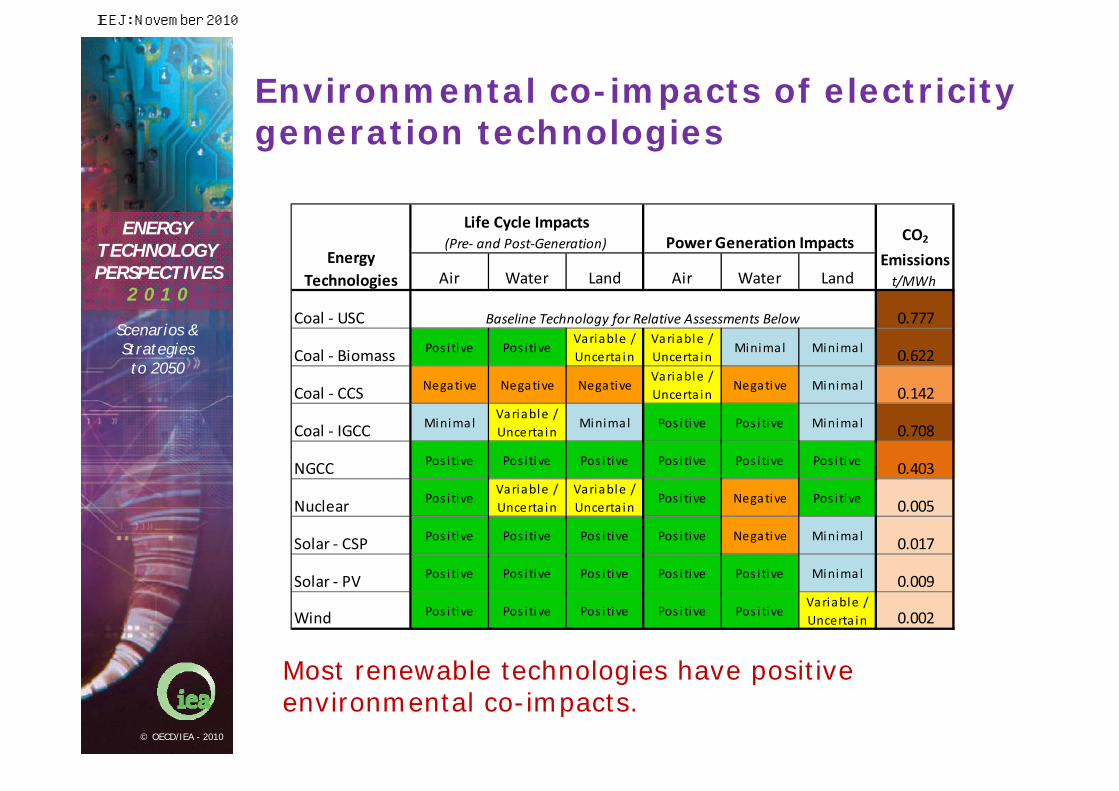

Environmental co-impacts of electricity generation technologies

Most renewable technologies have positive environmental co-impacts.

Air Water Land Air Water Land

Coal ‐ USC 0.777

Coal ‐ Biomass Pos i tive Pos i tiveVariable /Uncerta in

Variable /Uncerta in

Minimal Minimal 0.622

Coal ‐ CCS Negative Negative NegativeVariable /Uncerta in

Negative Minimal 0.142

Coal ‐ IGCC MinimalVariable /Uncerta in

Minimal Pos i tive Pos i tive Minimal 0.708

NGCC Pos itive Pos i tive Pos i tive Pos i tive Pos i tive Pos i tive 0.403

Nuclear Pos i tiveVariable /Uncerta in

Variable /Uncerta in

Pos i tive Negative Pos i tive 0.005

Solar ‐ CSP Pos itive Pos i tive Pos i tive Pos i tive Negative Minimal 0.017

Solar ‐ PV Pos itive Pos i tive Pos i tive Pos i tive Pos i tive Minimal 0.009

Wind Pos itive Pos i tive Pos i tive Pos i tive Pos i tiveVariable /Uncerta in 0.002

CO2

Emissionst/MWh

Energy Technologies

Baseline Technology for Relative Assessments Below

Life Cycle Impacts(Pre‐ and Post‐Generation) Power Generation Impacts

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Smart grid CO2 reductions in 2050

Smart grids allow better management of the grid and can facilitate the deployment of low-carbon technologies, such as renewables and electric vehicles.

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

Direct reductions Enabled reductions

Greater integration of renewables

Facilitation of electric vehicles and plug‐in electric vehicles

Energy savings from peak load management

Continuous commissioning of service sector loads

Accelerated deployment of energy efficiency programs

Reduced line losses (voltage control)

Direct feedback on energy usage

0.34‐ 0.69

0.31‐ 0.62

0.09‐ 0.27

0.03‐ 0.25

0.01‐ 0.05

0.00‐ 0.01

0.07‐ 0.27

Gt CO

2/ yr

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Additional investment and fuel savings, 2010-2050

Even using a 10% discount rate, fuel savings in the BLUE Map scenario more than offset the additional investment required.

‐140

‐120

‐100

‐80

‐60

‐40

‐20

0

20

40

60

Investmen

t

Fuel savings

USD

trillion (2010‐2050)

Commercial

Residential

Transport

Industry

Power distribution

Power transmission

Power generation

Biomass and waste

Natural gas

Oil

CoalUnd

iscoun

ted

3% discoun

t

10% discoun

t

Total

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

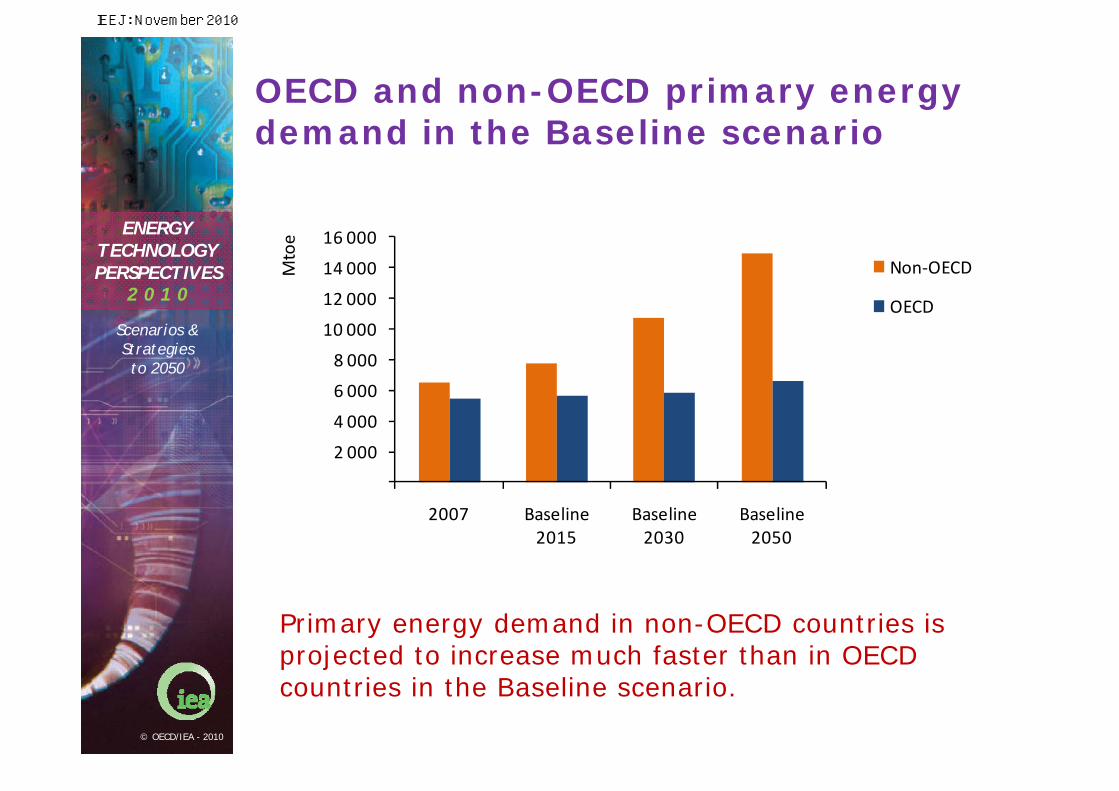

OECD and non-OECD primary energy demand in the Baseline scenario

Primary energy demand in non-OECD countries is projected to increase much faster than in OECD countries in the Baseline scenario.

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

2007 Baseline 2015

Baseline 2030

Baseline 2050

Mtoe

Non‐OECD

OECD

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

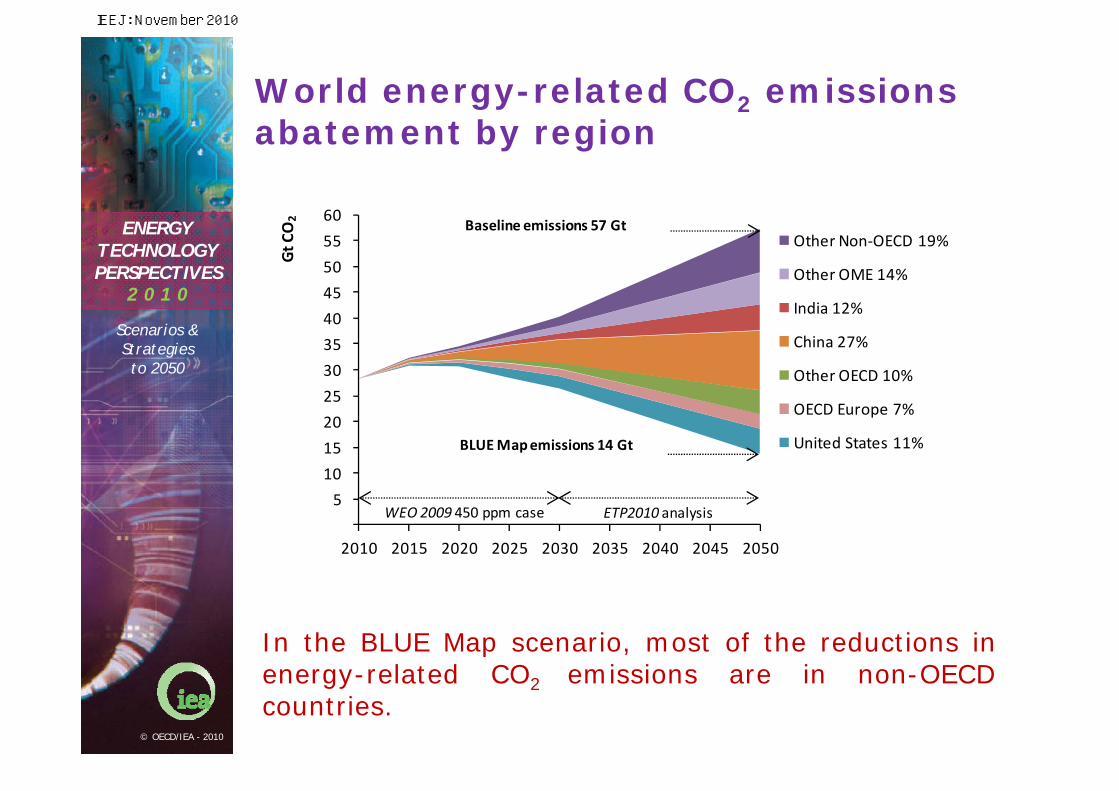

World energy-related CO2 emissions abatement by region

In the BLUE Map scenario, most of the reductions in energy-related CO2 emissions are in non-OECD countries.

5

10

15

20

25

30

35

40

45

50

55

60

2010 2015 2020 2025 2030 2035 2040 2045 2050

Gt C

O2

Other Non‐OECD 19%

Other OME 14%

India 12%

China 27%

Other OECD 10%

OECD Europe 7%

United States 11%BLUE Map emissions 14 Gt

Baseline emissions 57 Gt

ETP2010 analysis WEO 2009 450 ppm case

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Regional Implications

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

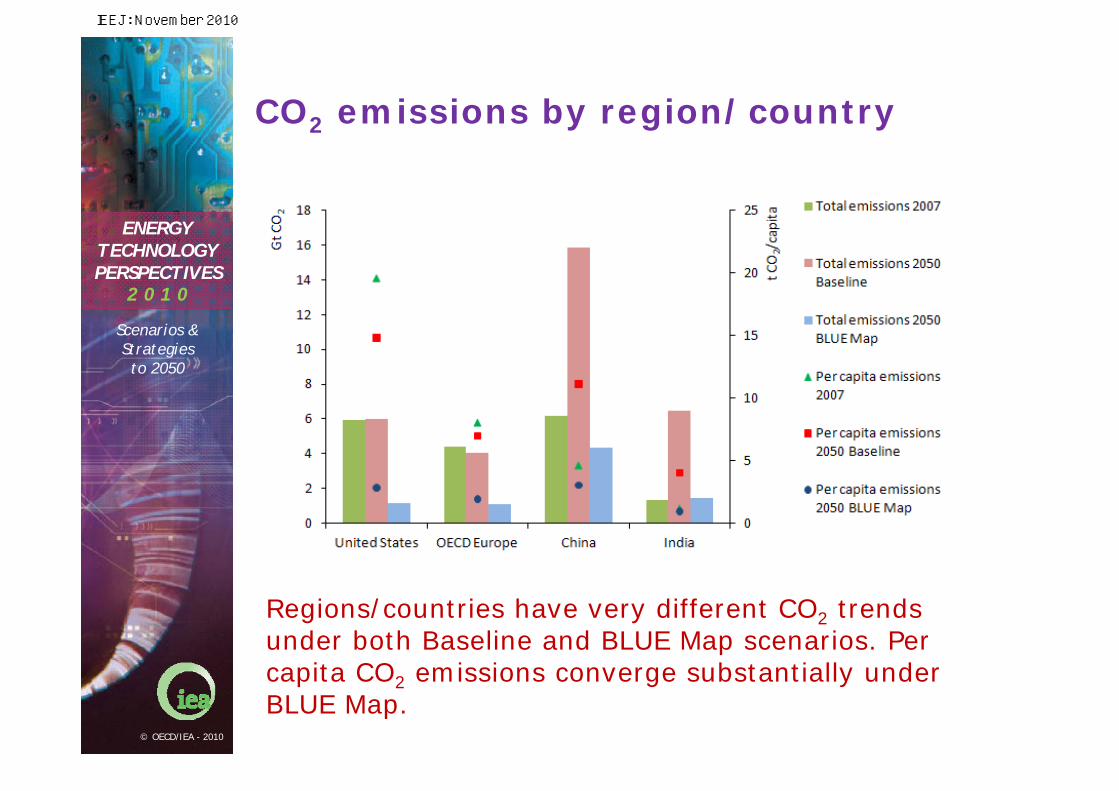

CO2 emissions by region/country

Regions/countries have very different CO2 trends under both Baseline and BLUE Map scenarios. Per capita CO2 emissions converge substantially under BLUE Map.

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Primary energy demand by fuel and by scenario

Under the BLUE Map scenario fossil fuel demand growth is offset by the growth in nuclear power and the use of renewable energy.

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Decarbonisation of power generation

Decarbonising the power sector requires all countries to dramatically change their generation mix.

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Direct energy and process CO2emissions in industry by sector

Energy efficiency and CCS are the two most important abatement options in industry.

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

CO2 emissions reduction in the buildings sector

Decarbonisation of the electricity sector contributes two-thirds to emissions reduction in the buildings sector.

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

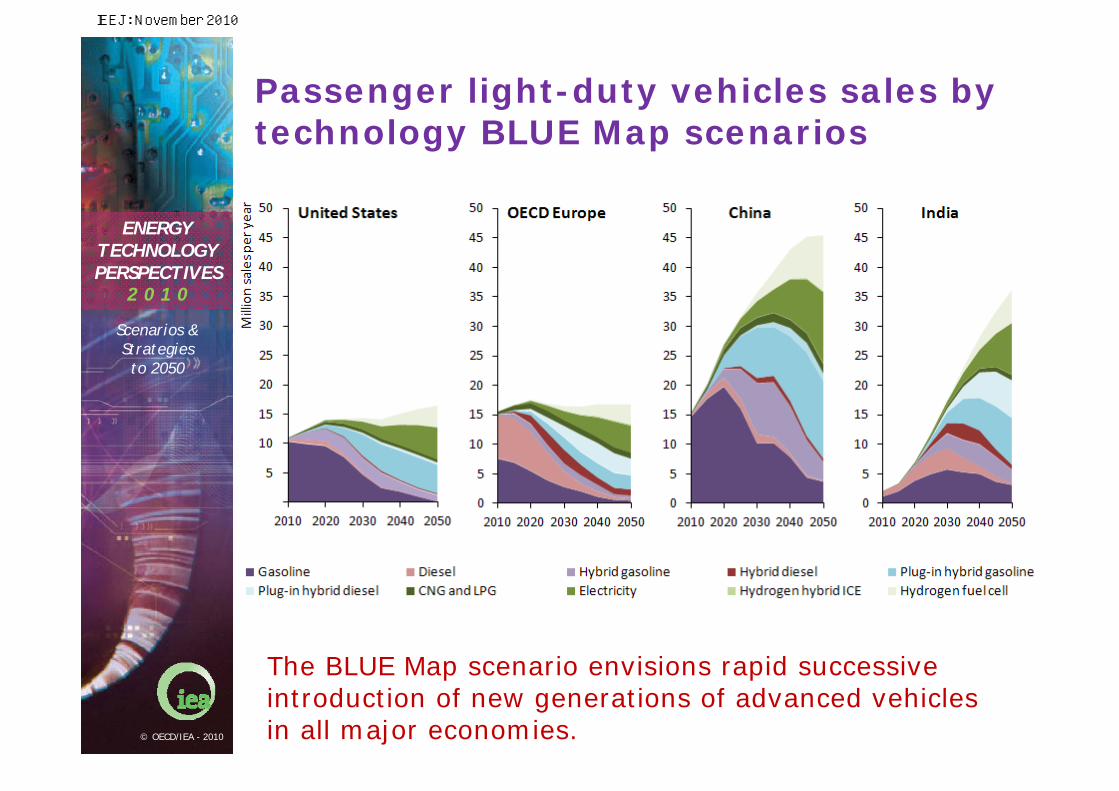

Passenger light-duty vehicles sales by technology BLUE Map scenarios

The BLUE Map scenario envisions rapid successive introduction of new generations of advanced vehicles in all major economies.

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Technology policies

Carbon pricing is important, but should be complemented by other policies

Policies must be tailored to the technology’s stage of development and reflect good design principles

Public RD&D spending must at least double

Governments need to implement best practices in energy RD&D

A number of enabling actions are also needed:

Private sector leadership Expanded human capacity Greater government outreach and planning on

infrastructure needs Expanded, more effective international

collaboration

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Policies for supporting low-carbon technologies

Government support policies need to be appropriately tailored to the stage(s) of technological development.

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

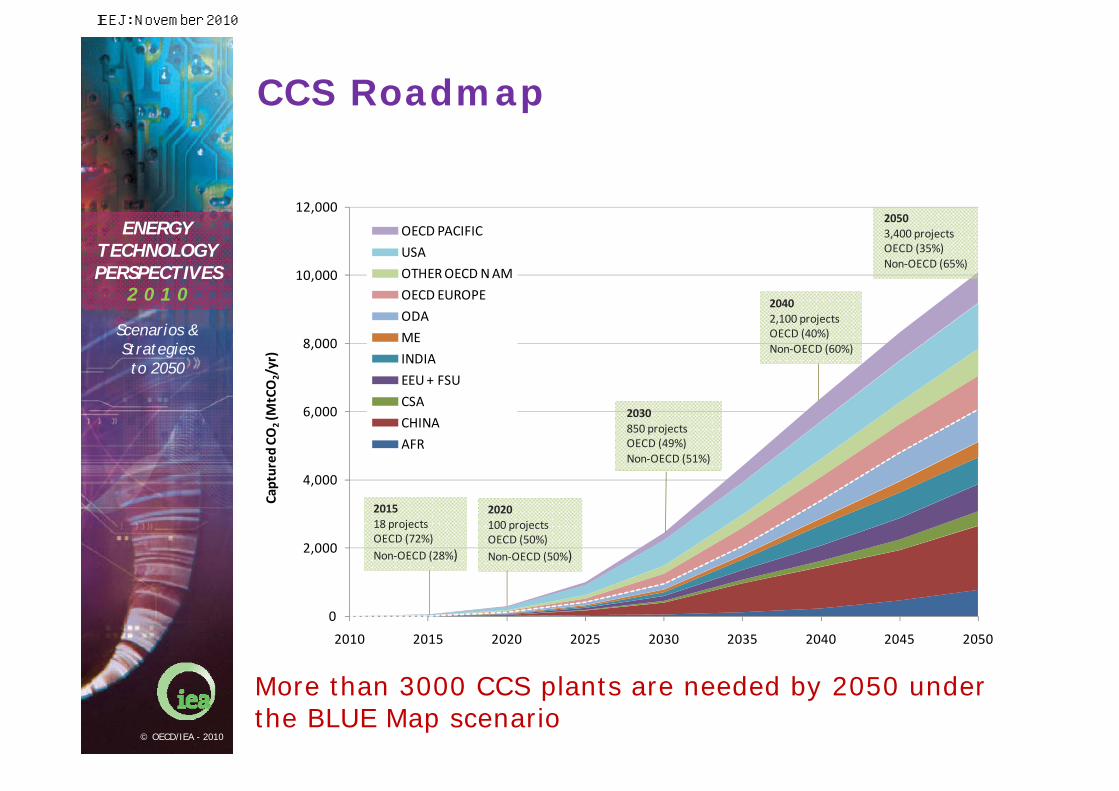

CCS Roadmap

0

2,000

4,000

6,000

8,000

10,000

12,000

2010 2015 2020 2025 2030 2035 2040 2045 2050

Captured

CO

2(M

tCO

2/yr)

OECD PACIFIC

USA

OTHER OECD N AM

OECD EUROPE

ODA

ME

INDIA

EEU + FSU

CSA

CHINA

AFR

2020100 projectsOECD (50%)Non‐OECD (50%)

2030850 projectsOECD (49%)Non‐OECD (51%)

20503,400 projectsOECD (35%)Non‐OECD (65%)

20402,100 projectsOECD (40%)Non‐OECD (60%)

201518 projectsOECD (72%)Non‐OECD (28%)

More than 3000 CCS plants are needed by 2050 under the BLUE Map scenario

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

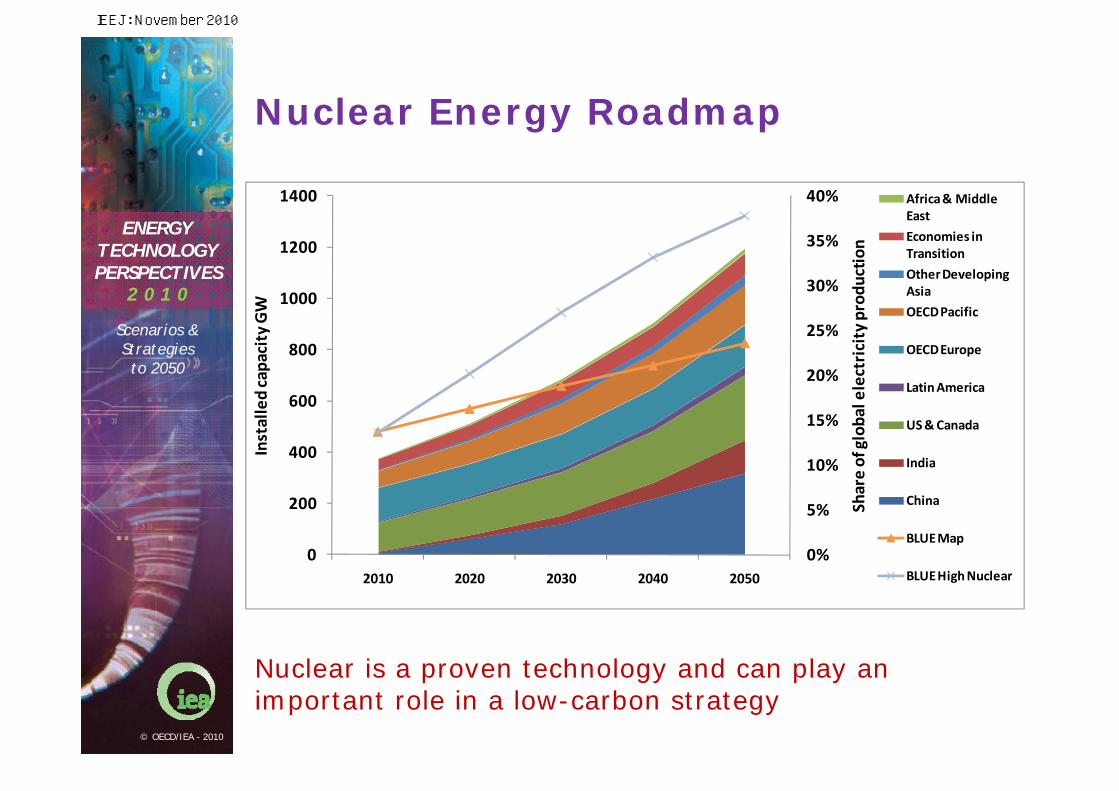

Nuclear is a proven technology and can play an important role in a low-carbon strategy

Nuclear Energy Roadmap

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

200

400

600

800

1000

1200

1400

2010 2020 2030 2040 2050

Share of global electricity produ

ction

Installed capacity GW

Africa & Middle East

Economies in Transition

Other Developing Asia

OECD Pacific

OECD Europe

Latin America

US & Canada

India

China

BLUE Map

BLUE High Nuclear

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

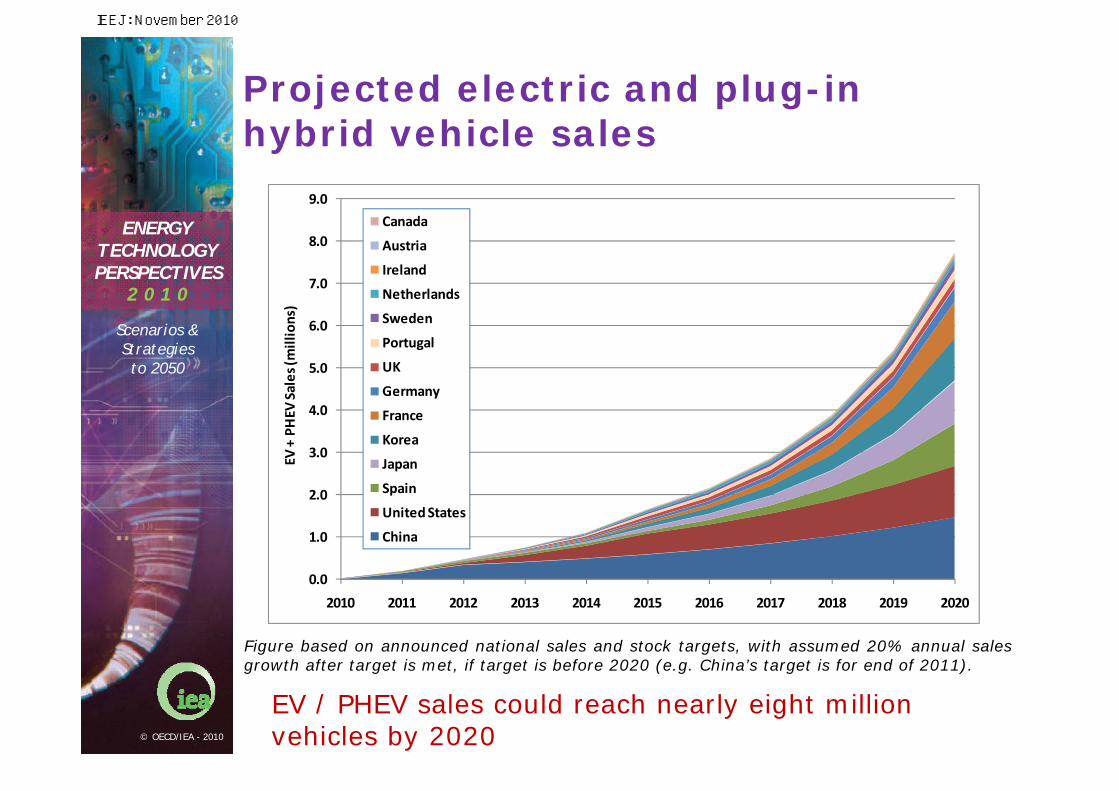

Projected electric and plug-in hybrid vehicle sales

EV / PHEV sales could reach nearly eight million vehicles by 2020

Figure based on announced national sales and stock targets, with assumed 20% annual sales growth after target is met, if target is before 2020 (e.g. China’s target is for end of 2011).

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

EV + PHEV

Sales (m

illions)

Canada

Austria

Ireland

Netherlands

Sweden

Portugal

UK

Germany

France

Korea

Japan

Spain

United States

China

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

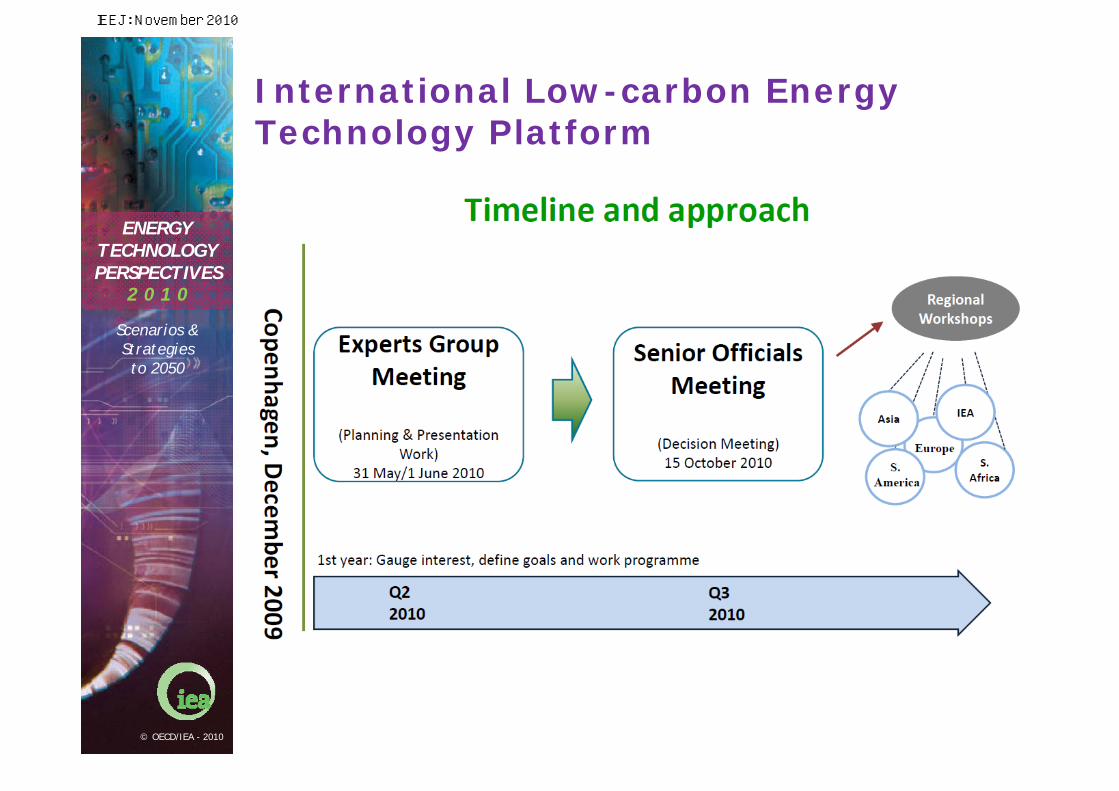

International Low-carbon Energy Technology Platform

IEEJ: November 2010

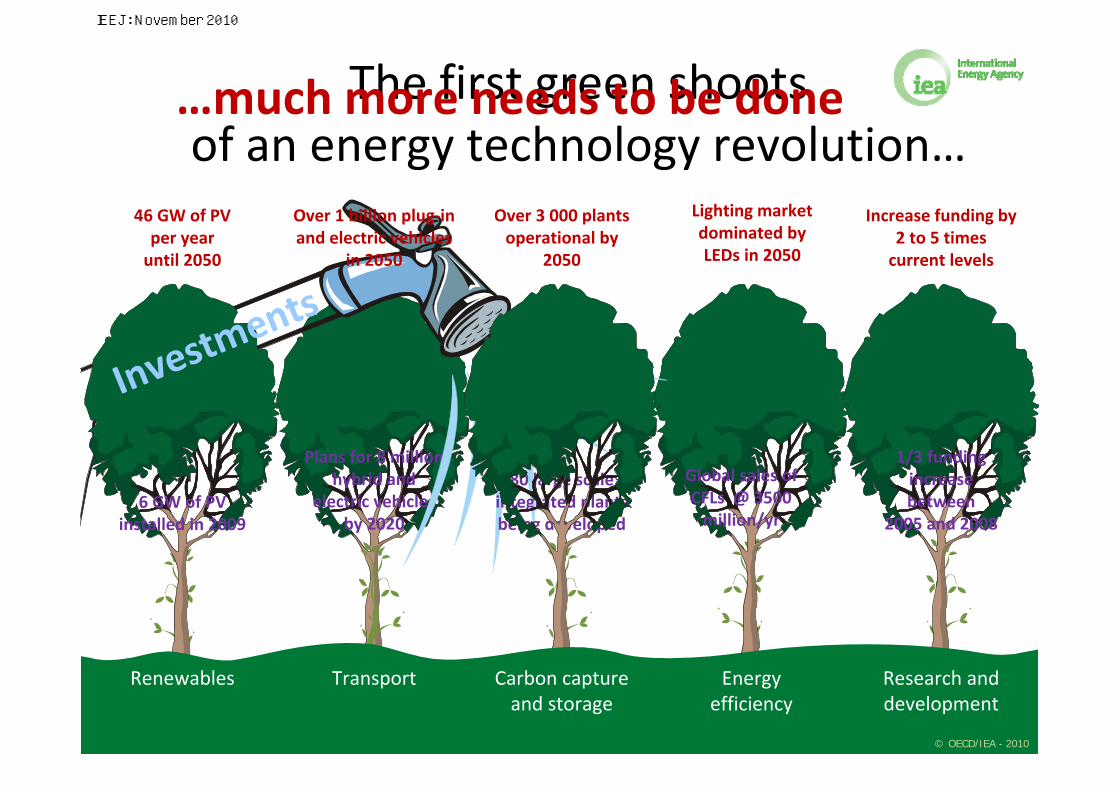

Plans for 8 million hybrid and

electric vehiclesby 2020

The first green shootsof an energy technology revolution……much more needs to be done

6 GW of PVinstalled in 2009

1/3 funding increasebetween

2005 and 2008

80 large scaleintegrated plantsbeing developed

Investm

ents

46 GW of PVper yearuntil 2050

Over 1 billion plug‐in and electric vehicles

in 2050

Increase funding by2 to 5 timescurrent levels

Over 3 000 plantsoperational by

2050

Renewables Transport Energyefficiency

Research anddevelopment

Carbon captureand storage

© OECD/IEA - 2010

Global sales of CFLs @ 3500 million/yr

Lighting market dominated by LEDs in 2050

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Thank You

www.iea.org/techno/etp/index.asp

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

ANNEX

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

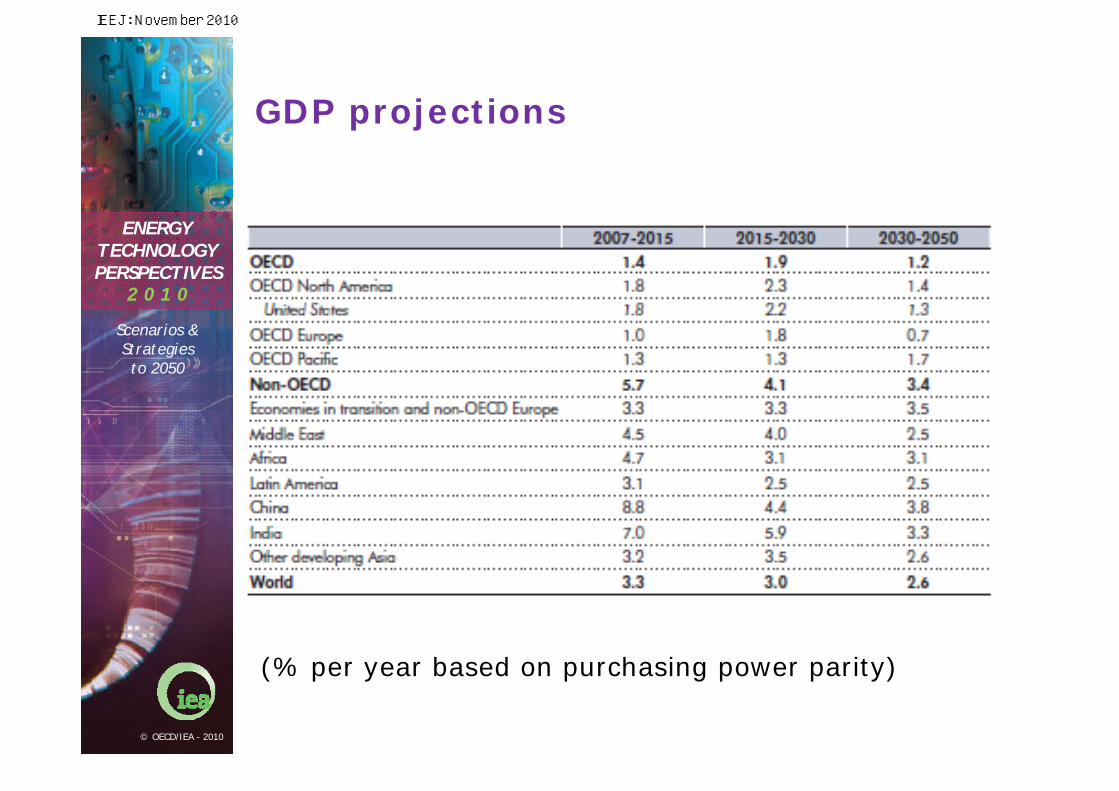

GDP projections

(% per year based on purchasing power parity)

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

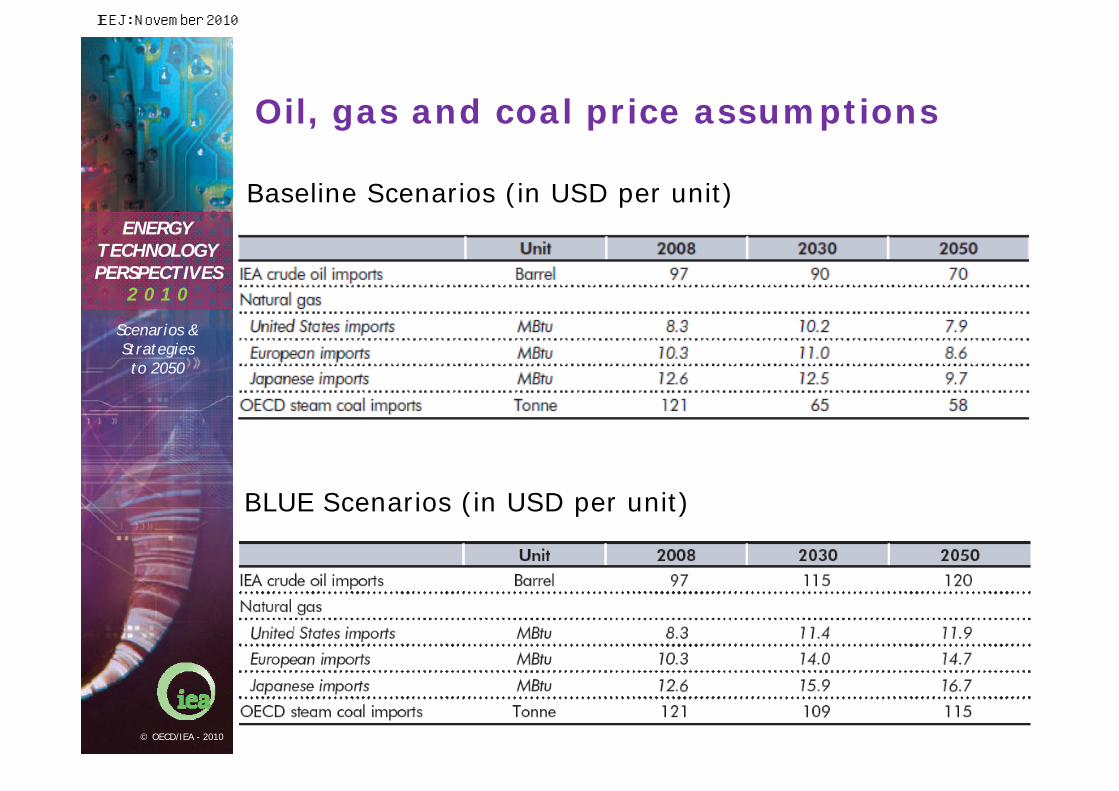

Oil, gas and coal price assumptions

Baseline Scenarios (in USD per unit)

BLUE Scenarios (in USD per unit)

IEEJ: November 2010

2 0 1 0

ENERGYTECHNOLOGYPERSPECTIVES

Scenarios &Strategiesto 2050

© OECD/IEA - 2010

Carbon prices in the BLUE Map scenario

USD / t CO2 2020 2030 2050

OECD 50 110 175

Non-OECD 0 65 175

IEEJ: November 2010

Contact: [email protected]