Energy Technology Perspectives 2017 - OECD€¦ · Energy Technology Perspectives 2017 - OECD ......

33

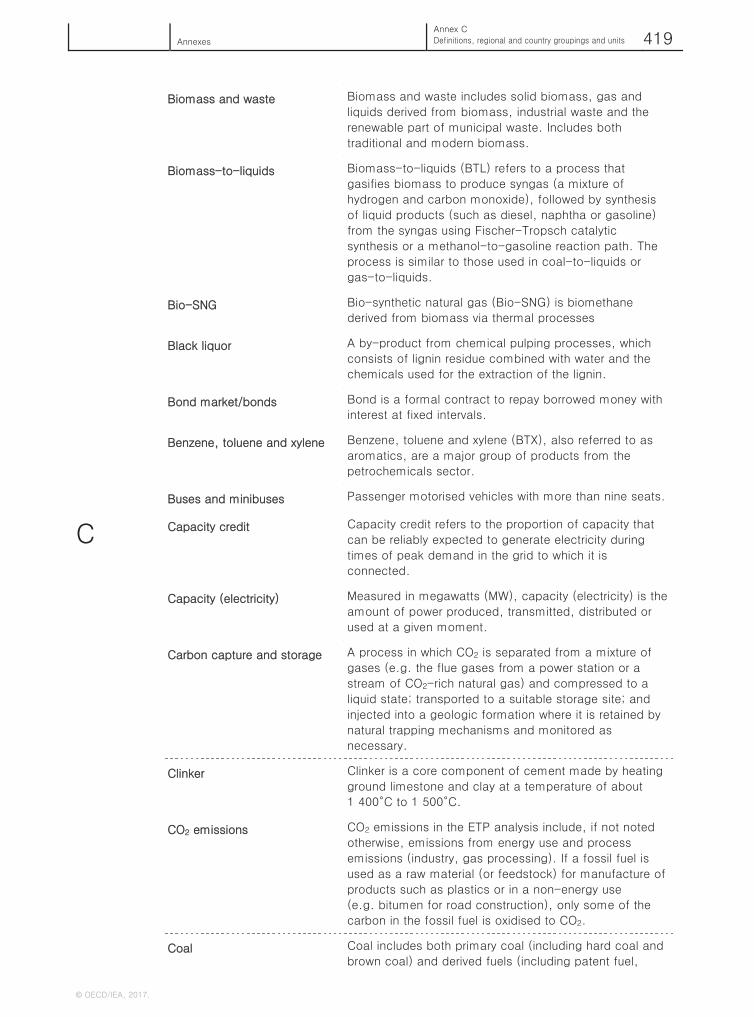

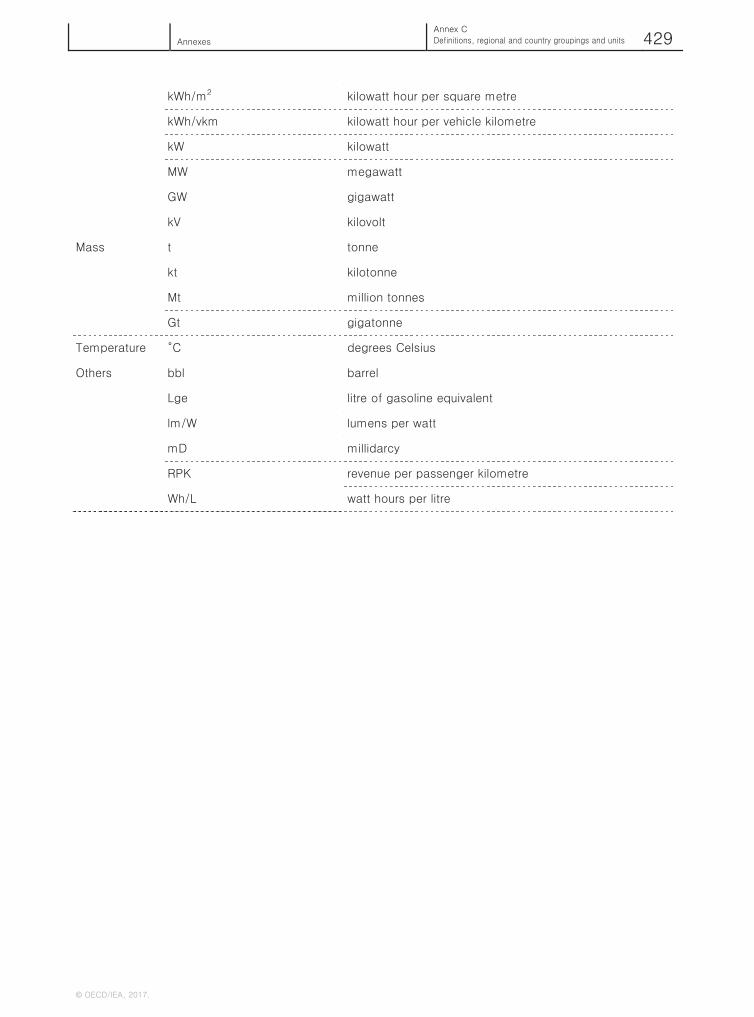

Energy Technology Perspectives 2017 Catalysing Energy Technology Transformations Together Secure Sustainable Energy Technology Perspectives 2017 http://dx.doi.org/10.1787/energy_tech-2017-en ISBN: 9789264275973(online) ISBN: 9789264270503 (print) © OECD/IEA 2017 Corrigendum Please note that despite our best efforts to ensure quality control, errors have slipped into Energy Technology Perspectives 2017. The text in pages 10, 13, 14, 15, 37, 90, 91, 96, 97, 104, 105, 106, 107, 108, 109, 110, 111, 120, 139, 144, 165, 169, 179, 208, 371, 372, 397, 418, 419, 426, 428, 429 has changed. It should be replaced by the following pages.

Transcript of Energy Technology Perspectives 2017 - OECD€¦ · Energy Technology Perspectives 2017 - OECD ......

Energy TechnologyPerspectives 2017Catalysing Energy Technology Transformations

Together

SecureSustainable

Energy Technology Perspectives 2017http://dx.doi.org/10.1787/energy_tech-2017-enISBN: 9789264275973(online)ISBN: 9789264270503 (print)© OECD/IEA 2017

CorrigendumPlease note that despite our best efforts to ensure quality control, errors have slipped into Energy Technology Perspectives 2017.The text in pages 10, 13, 14, 15, 37, 90, 91, 96, 97, 104, 105, 106, 107, 108, 109, 110, 111, 120, 139, 144, 165, 169, 179, 208, 371, 372, 397, 418, 419, 426, 428, 429 has changed. It should be replaced by the following pages.

Narrow cost and

performance gap

Compe��ve without

financial support

Time

RD&D

Se

co

nd

wa

ve

Th

ird

wa

ve

Niche

markets

Continual

incremental

improvements

Spillovers

Widespread

deployment

Inn

ova

tio

n s

tag

es

First

commercial

project

Second

generation

(learning from

early projects)Third generation

(performance improvement

from ongoing R&D)

Prototype and

demo stage

Wide cost and

performance gap

Fir

st

wa

ve

Learning: learning by doing, scaling up

Learning: learning by doing, scaling up

Learning: demonstra�on, knowledge

exchange, scale

Learning: R&D, knowledge exchange

Public support: strategically

directed R&D

Private ac�ons: angel investors,

corporate R&D

Public support: market crea�on,

technology-specific support

Private ac�ons: PPPs, ,venture capital

corporate debt, equity investors

Public support: declining,

technology-neutral, holis�c support

Private ac�ons: project ac�ons,

corporate debt

Public support: accelerate adop�on, market

pull policies, system integra�on

Private ac�ons: corporate and

household budgets; bond markets

Part 1

Setting the scene Chapter 1

The global outlook 37

© OECD/IEA, 2017.

The share of electricity in final energy demand across all end-use sectors almost doubles from 18% today to 35% in the 2DS in 2060, and 41% in the B2DS. The shift is particularly notable in transport, where electricity becomes the primary fuel for on-road vehicles in the B2DS (Figure 1.11). The additional electricity consumption by end-use sectors in the B2DS in 2060 is about 1 700 terawatt hours (TWh) more than the 2DS, equivalent to the combined annual electricity consumption of India and the Russian Federation today.

Decarbonisation of power generation The shift to electrification in the B2DS increases the pressure on the power sector, not only to accommodate additional generation but to do so while rapidly decarbonising and becoming a source of negative emissions. This transformation will require a considerable change in the traditional trends in power sector investment, with the carbon intensity of electricity generation declining at an average rate of -3.9% in the next decade for the 2DS or -4.5% for the B2DS, compared with -0.5% over the past decade.

In the 2DS, renewables deliver around two-thirds of the emissions reductions achieved in the power sector, with CCS providing 18% and nuclear 16% of reductions. By 2060, 98% of electricity generation is from low-carbon sources (Figure 1.12), with the carbon intensity of generation approaching zero — a colossal effort relative to today’s level of around 520 grammes of CO2 per kilowatt hour (gCO2/kWh) and the 254 gCO2/kWh achieved in the RTS. In the B2DS, the carbon intensity of electricity generation falls below zero, to -10 gCO2/kWh in 2060, effectively making the power sector a source of negative emissionsto offset residual emissions in industry and in transport.

Figure Power generation fuel mix by scenario, 2014 and 2060

Key point The fuel mix to generate electricity in the 2DS and B2DS would be vastly different from today’s mix.

Increased development and use of sustainable bioenergy A significant contribution from sustainably sourced bioenergy is needed as part of the transition to a clean energy future in both the 2DS and the B2DS. Bioenergy can play an important role across the energy sector: in electricity production, in heating for buildings, for industrial uses and in transport.

The role of bioenergy will largely be defined by the availability of sustainably sourced bioenergy feedstock. Its supply will need to grow from 55 EJ today to almost 100 EJ in 2060 in the RTS and to around 145 EJ in both the 2DS and B2DS. While this is within

0%

20%

40%

60%

80%

100%

RTS 2DS B2DS2014 2060

Elec

trici

ty m

ix

Fossil w/o CCS Fossil with CCS Nuclear Bioenergy with CCS Renewables

8

8

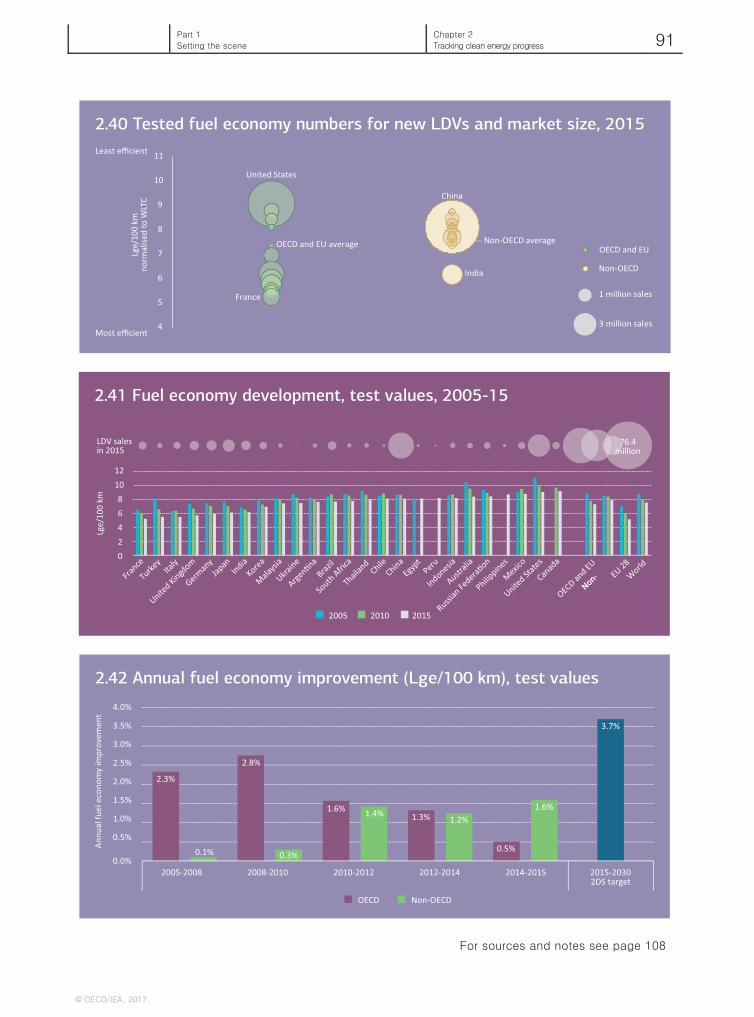

2.40 Tested fuel economy numbers for new LDVs and market size, 2015

2.41 Fuel economy development, test values, 2005-15

2.42 Annual fuel economy improvement (Lge/100 km), test values

2.3%

2.8%

1.6%

1.3%

0.5%

3.7%

0.1%0.3%

1.4%1.2%

1.6%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2005-2008 2008-2010 2010-2012 2012-2014 2014-2015 2015-2030

2DS target

An

nu

alfu

el

eco

no

my

imp

ro

ve

me

nt

OECD Non-OECD

2.49 Building energy codes

2.50 Change in building envelope performance

0

20

40

60

80

100

120

1990 1995 2000 2005 2010 2015 2020 2025

Ind

ex

19

90

=1

00

AfricaLa�n AmericaOECD EuropeOECD AmericasWorld

ChinaEurasiaMiddle EastOther AsiaIndia

0%

20%

40%

60%

80%

2.51 Efficiency policy progress, 2005-15100%

Germany France niU ted

States

United

Kingdom

China Korea Italy Canada paS in

Residen�al progress

Non-residen�al progress

Residen�al proximity totarget

Non-residen�al proximity to target

No informa�on

Code in development

Voluntary energy codes

for part of sector

Mandatory energy codes

for part of sector

Mandatory energy codes

for the whole sector

Billion square metres in

floor area addi�ons to 2025

1

This map is without prejudice o the status of or sovereignty over any territory,t to the delimita�on of interna�onal fron�ers and boundaries, and to the name of any territory, city or area.

North

America

La�n America

and Caribbean

Africa

Western

Europe China

India

Eurasia

Japan and

Korea

Australia and

New Zealand

Other Asia

Middle

East

5.3

2.6

4.1

7.1

2.2

1.5

13.9

12.18.5

0.5

1.5

ONLY

1/3OF COUNTRIES HAVE MANDATORY ENERGY CODES FOR THE ENTIRE BUILDINGS SECTOR

2/3OF NEW

BUILDINGS NEED

TO BE COVERED

BY MANDATORY

BUILDING

ENERGY CODES

BY 2025

0 20 40 60 80

100 120 140 160 180 200

lm/W

Incandescent Halogen CFL LFL LED - RTS LED - 2DS LED - B2DS

0%10%20%30%40%50%60%70%80%90%

100%Sh

are

of re

siden

tial L

ED sa

les

Part 2

Catalysing energy technology transformations Chapter 4

Advancing the low-carbon transition in industry 165

© OECD/IEA, 2017

Decarbonisation pathways The levels of climate change ambition expressed in the Paris Agreement require a much more ambitious pathway for the energy system than the current and announced policies and targets in the RTS imply. The energy demand and CO2 emissions reduction needed to reach the 2DS pathway or a more ambitious climate target are significantly deeper. The annual improvements in aggregated energy intensity in the industry sector since 2000 would need to triple to meet a 2DS trajectory and almost quadruple to meet the more ambitious B2DS pathway through 2030 (Figure 4.2). The contribution of fossil fuels to the overall energy mix in industry, which has remained nearly flat since 2000, would need to fall by 4-7% over the next 15 years to avoid the more costly 2DS or B2DS trajectories in the long term, which would require much more drastic technological and structural changes to reduce CO2 emissions in the post‐2030 period. Without early action, as more carbon‐intensive capacity in industry is installed, stranded assets or costly retrofits are likely in order to shift to a less carbon‐intensive industry sector and compensate for early CO2 emissions by reducing more dramatically in later time periods.

Figure Energy use and aggregated energy intensity in industry per

value added by scenario

Notes: Final industrial energy use includes blast furnaces (BFs), coke ovens (COs) and petrochemical feedstocks. Energy intensity is

given in gigajoules (GJ) per thousand United States dollars (USD) of aggregated industrial value added.

Source: IEA (2016), World Energy Balances 2016.

Key point Final industry energy intensity decreases dramatically by 2060 in the low‐carbon scenarios.

In the 2DS, global direct CO2 emissions from industry are reduced by 44% by 2050 and halved by 2060 compared with the RTS. However, to reach net‐zero CO2 emissions at the system level, by 2060, which is required for the B2DS, industry would need to further reduce its carbon emissions by 69% by 2050 and 80% by 2060 compared with the RTS (Figure 4.3). These reductions would have to include efforts to address process CO2 emissions, generated in industrial processes from the use of carbon-based raw materials, which accounted for 23% of total CO2 emissions in industry in 2014, in addition to emissions from fuel combustion. Such an ambitious change in the direct CO2 intensity of industrial activity will need to occur along with development of new infrastructure and sustainable consumer products, which will require considerable amounts of material commodities to be produced and adapted to new applications.

0

50

100

150

200

250

2000 2005 2010 2014

Historical

EJ

0

1

2

3

4

5

2030 2030 2030 2060 2060 2060

RTS 2DS B2DS RTS 2DS B2DS

GJ/U

SD t

hous

and

Other renewables

Waste

Biomass

Heat

Electricity

Natural gas

Oil

Coal

Global aggregate energyintensity

Part 2

Catalysing energy technology transformations Chapter 4

Advancing the low-carbon transition in industry 169

© OECD/IEA, 2017

rates include the cost and time to develop infrastructure, stimulating behavioural change and technical issues related to the quality of scrap.

Figure Global material production projections in the RTS and B2DS

Notes: HVC = high-value chemicals. HVC refer to ethylene, propylene and BTX (benzene, toluene and xylene). Crude steel and aluminium

production levels are expressed in liquid metal terms.

Key point Production levels are decreased for crude steel, aluminium and primary chemicals in the B2DS due to material efficiency strategies.

Table Material efficiency strategies by subsector and scenario

RTS 2DS B2DS

Iron and steel Post‐consumer scrap

recycling – continue current

trends.

Post‐consumer scrap

recycling – improved

collection rates.

Same strategy as 2DS.

Improved manufacturing

and semi‐manufacturing

yields.

Post‐consumer scrap

reuse.

Cement Clinker substitution –

continue current trends.

Maximised clinker

substitution ratios.

Same strategy as 2DS.

0 150 300 450 600 750

2014

RTS 2060

B2DS 2060

2014

RTS 2060

B2DS 2060

Pulp

Alu

min

ium

Product (Mt)Primary

Recycled

Recovered fibrepulp

Virgin wood pulp

0 1 000 2 000 3 000 4 000 5 000

2014

RTS 2060

B2DS 2060

2014

RTS 2060

B2DS 2060

2014

RTS 2060

B2DS 2060

Chem

ical

sCr

ude

stee

lCe

men

t

Cement

Clinker additives

Primary

Secondary

HVC

Ammonia

Methanol

Product (Mt)

Part 2

Catalysing energy technology transformations Chapter 4

Advancing the low-carbon transition in industry 179

© OECD/IEA, 2017

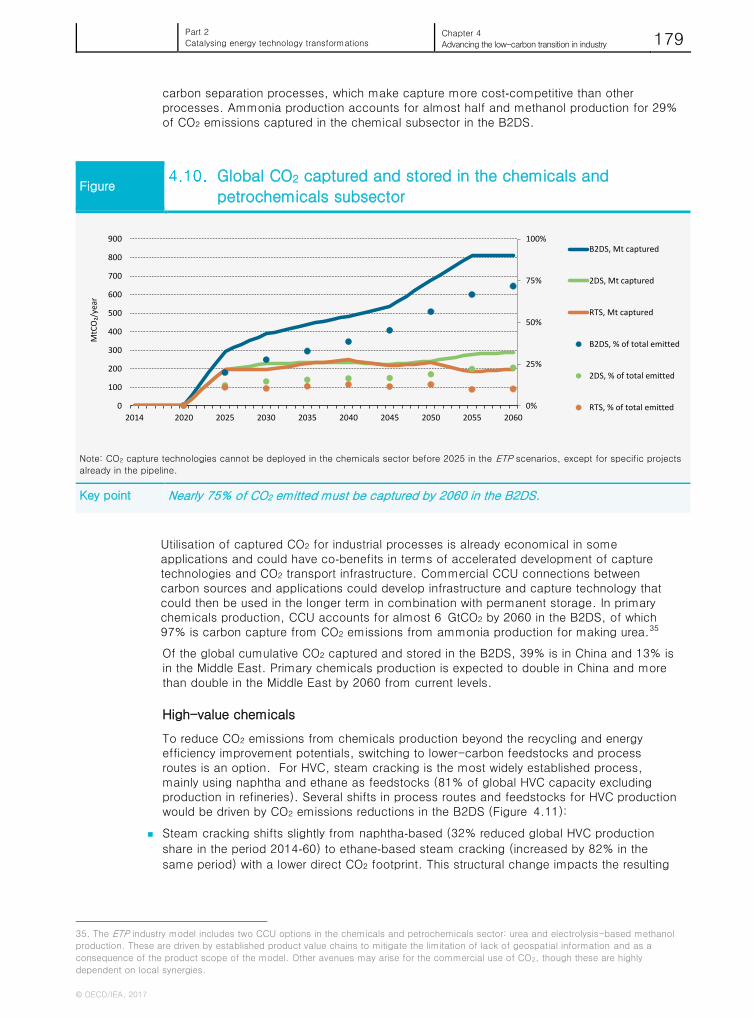

carbon separation processes, which make capture more cost‐competitive than other processes. Ammonia production accounts for almost half and methanol production for 29% of CO2 emissions captured in the chemical subsector in the B2DS.

Figure Global CO2 captured and stored in the chemicals and

petrochemicals subsector

Note: CO2 capture technologies cannot be deployed in the chemicals sector before 2025 in the ETP scenarios, except for specific projects

already in the pipeline.

Key point Nearly 75% of CO2 emitted must be captured by 2060 in the B2DS.

Utilisation of captured CO2 for industrial processes is already economical in some applications and could have co‐benefits in terms of accelerated development of capture technologies and CO2 transport infrastructure. Commercial CCU connections between carbon sources and applications could develop infrastructure and capture technology that could then be used in the longer term in combination with permanent storage. In primary chemicals production, CCU accounts for almost 6 GtCO2 by 2060 in the B2DS, of which 97% is carbon capture from CO2 emissions from ammonia production for making urea.35

Of the global cumulative CO2 captured and stored in the B2DS, 39% is in China and 13% is in the Middle East. Primary chemicals production is expected to double in China and more than double in the Middle East by 2060 from current levels.

High-value chemicals

To reduce CO2 emissions from chemicals production beyond the recycling and energy efficiency improvement potentials, switching to lower-carbon feedstocks and process routes is an option. For HVC, steam cracking is the most widely established process, mainly using naphtha and ethane as feedstocks (81% of global HVC capacity excluding production in refineries). Several shifts in process routes and feedstocks for HVC production would be driven by CO2 emissions reductions in the B2DS (Figure 4.11):

Steam cracking shifts slightly from naphtha‐based (32% reduced global HVC production

share in the period 2014‐60) to ethane‐based steam cracking (increased by 82% in the

same period) with a lower direct CO2 footprint. This structural change impacts the resulting

35. The ETP industry model includes two CCU options in the chemicals and petrochemicals sector: urea and electrolysis-based methanol

production. These are driven by established product value chains to mitigate the limitation of lack of geospatial information and as a

consequence of the product scope of the model. Other avenues may arise for the commercial use of CO2, though these are highly

dependent on local synergies.

0%

25%

50%

75%

100%

0

100

200

300

400

500

600

700

800

900

2014 2020 2025 2030 2035 2040 2045 2050 2055 2060

MtCO₂/year

B2DS, Mt captured

2DS, Mt captured

RTS, Mt captured

B2DS, % of total emitted

2DS, % of total emitted

RTS, % of total emitted

--

-- --

- --

--

-

0%

20%

40%

60%

80%

100%

2015 2025 2035 2045 2055

Shar

e of

pro

duct

ion

with

CCS

Steel

RTS 2DS B2DS Share of production which is not low carbon through other routes

0%

20%

40%

60%

80%

100%

2015 2025 2035 2045 2055

Cement

0%

20%

40%

60%

80%

100%

2015 2025 2035 2045 2055

Primary chemicals

- 4- 2 0 2 4 6 8

10

2030 2045 2060 2030 2045 2060 2030 2045 2060Low concentration,

smallLow concentration,

largeHigh concentration

GtCO

2/yr

2DS

CO captured Total net CO produced

- 4- 2 0 2 4 6 8

10

2030 2045 2060 2030 2045 2060 2030 2045 2060Low concentration,

smallLow concentration,

largeHigh concentration

B2DS

Coal

Natural gas

Oil products

Electricity

District heating

and cooling

Solid biomass

Solar thermal

energy

Geothermal

energy

Final energy

demand

Biofuels

Hydrogen

Coal

Primary

energy supply

Oil

Natural gas

Nuclear

Biomass

Hydro

Wind

Solar

Geothermal

Ocean

Refineries

Alternative fuel

production

Gas processing

Coal upgrading

Electricity plants

Co-generation plants

Heat plants

Electricity sector

Electricity storage

Gas pipelines, LNG

Electricity transmission

and distribution

District heat grid

Hydrogen

infrastructure

Conversion Transport and distribution

Energy flows

CO emissions2

New capacity additions Electricity prices

Overall costs of supply sideResults

Technical and

economic characteristics

Input assumptions

Demand load

curves

Resources, potentials

Supply costs

CO prices2