Editor: Frankie Wong Tel: (852) 2277 6765 Email ...

10

Transcript of Editor: Frankie Wong Tel: (852) 2277 6765 Email ...

denniswu

Typewriter

denniswu

Typewriter

THAILAND EQUITY RESEARCH

Page | 1 | PHILLIP SECURITIES (THAILAND)

IRPC

FY15 earnings recover from previous loss

THAILAND | SET | ENERG | COMPANY RESULTS BLOOMBERG IRPC TB l REUTERS IRPC.BK

FY15 net profit achieved at Bt9,402mn IRPC reported the stronger than expected results in 2015. Net profit came in Bt9,402mn, beating our forecast of Bt9,298mn due to 4QFY15 lower than expect of stock loss. FY15 earnings recovered from a year‐earlier loss of Bt5,235mn as oil stock loss and LCM allowance of Bt2,239mn was offset by wider gross margin, a reversal of TPI Aromatics’ doubtful debt provision of Bt2,823mn IRPC set in 1QFY15 and insurance claims of Bt1,313mn. Wider gross margin benefitted from a stronger market GIM, up from US$7.6/barrel to US$14.6/barrel, as a slump in crude oil price helped reduce fuel cost; and higher market GIM proportion in petroleum unit, from 39% to 44%, as a result of lower cost, thanks to Delta project, and a significant increase in petroleum spreads. FY15 DPS is declared at Bt0.22 and the stock will trade ex‐dividend on February 18 and payment to be made on April 22. Figure 1: Market GIM breakdown Source: IRPC,PSR

Commencement of UHV unit to boost FY16 earnings Gross refining margin is likely to remain high as Singapore GRM increased from US$8/barrel reported in 4QFY15 to US$9 in quarter to date and Dubai crude price gradually picked up to US$28/barrel as the world’s large crude oil producers, both OPEC and non‐OPEC members, are widely expected to cut their output. Additionally, IRPC is expected to benefit from a startup of UHV unit (a part of Phoenix project) in early 2QFY16, which will add value to its products with propylene capacity to increase by 320k ton/year by using fuel oil as feedstock. The UHV commencement would increase profit by US$0.5/barrel from an average US$14.1 in 2015. ‘BUY’ rating with Bt4.80 target price IRPC shares currently trade near its book value after a sharp pullback. We thus rate the stock a ‘BUY’ with a target price of Bt4.80, down from Bt4.90 due to higher than expect FY15 dividend payout.

Closing Price(Bt) 4.24

Target Price(Bt) 4.80 (+16.04%)

COMPANY DATA

O/S Shares (mn) : 20,434

Market Cap. (Btmn) :

Market Cap. (USDmn) :

52‐WK Hi/Lo (Bt) : 4.82/3.2

3M Average Daily T/O (mn) : 99.14

Par Value (Bt) : 1.00

MAJOR SHAREHOLDERS (%)

1. PTT PCL 38.5

2. GOVERNMENT SAVINGS BANK 9.5

3. GOVERNMENT PERSION FUND 4.9

PRICE PERFORMANCE (%)

1MTH 3MTH 1YR

ABS ‐4% 5% 5%

REL TO SET INDEX ‐9% 13% 28%

PRICE VS SET INDEX

Source: Bloomberg, PSR

KEY FINANCIALS

FYE Dec FY14 FY15 FY16E FY17E

Sales(Btmn) 281,589 214,172 143,449 161,266

Net Profit(Btmn) ‐5,235 9,402 9,746 10,242

EPS (Bt) ‐0.26 0.46 0.48 0.50

P/E (X) n.m. 9.2 8.9 8.5

BVPS (Bt) 3.32 3.71 3.97 4.35

P/B (X) 1.3 1.1 1.1 1.0

DPS (Bt) 0.08 0.22 0.12 0.13

Dividend Yield (%) 1.9 5.2 2.8 3.1

ROE (%) n.m. 13.12 13.57 13.06

Debt/Equity (X) 1.15 1.40 1.15 0.87

Source: Company, PSR Est.

**Multiples and yields are based on latest closing price

VALUATION METHOD

P/B'16 (1.2x)

Ornmongkol Tantitanatorn

Capital Market Investment Analyst # 34100

Tel: 66 2 635 1700 # 491

10 February 2016

86,642

2,447

26 February 2015

Buy (Upgraded from Trading Buy)

0

2

4

6

8

Feb‐14 Feb‐15 Feb‐16

IRPC TB EQUITY SETI (rebased)

THAILAND EQUITY RESEARCH

PHILLIP SECURITIESS (THAILAND) | 2 | P a g e

IRPC COMPANY RESULTS Income Statement

Btmn 4Q15 3Q15 4Q14 q‐q+/‐ y‐y+/‐ 2015 2014 y‐y+/‐

Sales and services 49,024 52,070 63,873 ‐6% ‐23% 214,172 281,589 ‐24%

Costs of sales 46,032 49,339 70,198 ‐7% ‐34% 197,913 287,930 ‐31%

Gross profit 2,992 2,731 ‐6,325 10% 147% 16,258 ‐6,341 356%

Selling expenses 300 289 274 4% 9% 1,207 1,103 9%

Administrative expenses 1,480 1,072 1,177 38% 26% 4,965 4,341 14%

Operating profit 1,212 1,370 ‐7,776 ‐12% 116% 10,086 ‐11,785 186%

Other income ‐583 1,046 1,297 ‐156% ‐145% 4,348 5,806 ‐25%

Gain/loss from affiliates ‐29 ‐47 ‐105 37% 72% ‐184 ‐139 ‐33%

EBIT 599 2,370 ‐6,584 ‐75% 109% 14,250 ‐6,118 333%

Interest expense 117 1,268 582 ‐91% ‐80% 2,481 1,494 66%

EBT 482 1,101 ‐7,166 ‐56% 107% 11,769 ‐7,611 255%

Taxation 31 210 ‐1,393 ‐85% 102% 2,346 ‐2,398 198%

EAT 452 892 ‐5,774 ‐49% 108% 9,423 ‐5,213 281%

Minority ‐4 ‐4 ‐5 ‐6% 8% ‐21 ‐21 ‐1%

Net profit 447 887 ‐5,779 ‐50% 108% 9,402 ‐5,235 280%

EPS (Bt) 0.02 0.04 ‐0.28 ‐50% 108% 0.46 ‐0.26 280%

Total Crude Intake (Mbbl) 17 16 16 67 63

Market GIM (US$/bbl) 14.7 14.1 10.4 14.0 7.6

Petroleum (GRM) 7.1 4.8 4.7 6.2 3.0

Petrochemical (PTF) 6.6 8.2 4.6 6.7 3.5

Power and Utilities 1.0 1.2 1.1 1.1 1.2

StockGain/Loss (US$/bbl) ‐3.3 ‐2.8 ‐10.7 ‐2.3 ‐3.4

Lower of Cost or Market (US$/bbl) ‐0.2 ‐0.3 ‐5.4 1.3 ‐1.6

Oil Hedging Gain/Loss (US$/bbl) ‐1.3 ‐0.7 ‐0.4 ‐0.5 0.8

Market GIM (Btmn) 8,804 8,161 5,688 32,156 15,788

StockGain/Loss (Btmn) ‐1,985 ‐1,597 ‐5,839 ‐5,208 ‐7,008

Lower of Cost or Market (Btmn) ‐99 ‐191 ‐2,946 2,969 ‐3,267

Oil Hedging Gain/Loss (Btmn) ‐774 ‐407 ‐206 ‐1,176 1,725

Key Financial Ratio

% 4Q15 3Q15 4Q14 q‐q+/‐ y‐y+/‐ 2015 2014 y‐y+/‐

Cost of sales/sales 93.90% 94.75% 109.90% ‐1% ‐15% 92.41% 102.25% ‐10%

SG&A exp/sales 3.63% 2.61% 2.27% 39% 60% 2.88% 1.93% 49%

Gross margin 6.10% 5.25% ‐9.90% 16% 162% 7.59% ‐2.25% 437%

Operating profit margin 2.47% 2.63% ‐12.17% ‐6% 120% 4.71% ‐4.19% 213%

Net profit margin 0.91% 1.70% ‐9.05% ‐46% 110% 4.39% ‐1.86% 336%

Balance Sheet

Btmn 4Q15 3Q15 4Q14 q‐q+/‐ y‐y+/‐ 2015 2014 y‐y+/‐

Assets 163,174 175,135 162,798 ‐7% 0% 163,174 162,798 0%

Liabilities 87,296 101,329 94,894 ‐14% ‐8% 87,296 94,894 ‐8%

Paid‐up (mn shrs) ‐ Par Bt1 20,434 20,434 20,434 0% 0% 20,434 20,434 0%

Equities 75,804 73,741 67,834 3% 12% 75,804 67,834 12%

BVPS (Bt) 3.71 3.61 3.32 3% 12% 3.71 3.32 12%

Debt/equity (x) 1.2 1.4 1.4 ‐16% ‐18% 1.2 1.4 ‐18%

THAILAND EQUITY RESEARCH

PHILLIP SECURITIESS (THAILAND) | 3 | P a g e

Corporate Governance ‐2015

ADVANC BAFS BCP BIGC BTS CK CPN DRT DTAC DTC

EASTW EGCO GRAMMY HANA HMPRO INTUCH IRPC IVL KBANK KCE

KKP KTB LHBANK LPN MCOT MINT MONO NKI PHOL PPS

PS PSL PTT PTTEP PTTGC QTC RATCH ROBINS SAMART SAMTEL

SAT SC SCB SCC SE‐ED SIM SNC SPALI THCOM TISCO

TKT TMB TOP VGI WACOAL

AAV ACAP AGE AHC AKP AMATA ANAN AOT APCS ARIP

ASIMAR ASK ASP BANPU BAY BBL BDMS BECL BKI BLA

BMCL BOL BROOK BWG CENTEL CFRESH CHO CIMBT CM CNT

COL CPF CPI CSL DCC DELTA DEMCO ECF EE ERW

GBX GC GFPT GLOBAL GUNKUL HEMRAJ HOTPOT HYDRO ICC ICHI

INET IRC KSL KTC LANNA LH LOXLEY LRH MACO MBK

MC MEGA MFEC NBC NCH NINE NSI NTV OCC OGC

OISHI OTO PAP PDI PE PG PJW PM PPP PR

PRANDA PREB PT PTG Q‐CON QH RS S & J SABINA SAMCO

SCG SEAFCO SFP SIAM SINGER SIS SITHAI SMK SMPC SMT

SNP SPI SSF SSI SSSC SST STA STEC SVI SWC

SYMC SYNTEC TASCO TBSP TCAP TF TGCI THAI THANA THANI

THIP THRE THREL TICON TIP TIPCO TK TKS TMI TMILL

TMT TNDT TNITY TNL TOG TPC TPCORP TRC TRU TRUE

TSC TSTE TSTH TTA TTCL TTW TU TVD TVO TWFP

TWS UAC UT UV VNT WAVE WINNER YUASA ZMICO

2S AEC AEONTS AF AH AIRA AIT AJ AKR AMANAH

AMARIN AP APCO AQUA AS ASIA AUCT AYUD BA BEAUTY

BEC BFIT BH BIG BJC BJCHI BKD BTNC CBG CGD

CHG CHOW CI CITY CKP CNS CPALL CPL CSC CSP

CSS CTW DNA EARTH EASON ECL EFORL ESSO FE FIRE

FOCUS FORTH FPI FSMART FSS FVC GCAP GENCO GL GLAND

GLOW GOLD GYT HTC HTECH IEC IFEC IFS IHL IRCP

ITD JSP JTS JUBILE KASET KBS KCAR KGI KKC KTIS

KWC KYE L&E LALIN LHK LIT LIVE LST M MAJOR

MAKRO MATCH MATI MBKET M‐CHAI MFC MILL MJD MK MODERN

MOONG MPG MSC MTI MTLS NC NOK NUSA NWR NYT

OCEAN PACE PATO PB PCA PCSGH PDG PF PICO PL

PLANB PLAT PPM PRG PRIN PSTC PTL PYLON QLT RCI

RCL RICHY RML RPC S SALEE SAPPE SAWAD SCCC SCN

SCP SEAOIL SIRI SKR SMG SOLAR SORKON SPA SPC SPCG

SPPT SPVI SRICHA SSC STANLY STPI SUC SUSCO SUTHA SYNEX

TAE TAKUNI TCC TCCC TCJ TEAM TFD TFI TIC TIW

TLUXE TMC TMD TOPP TPCH TPIPL TRT TSE TSR UMI

UP UPF UPOIC UREKA UWC VIBHA VIH VPO WHA WIN

XO

Score Range

< 50%

50‐59%

60‐69%

70‐79%

80‐89%

90‐100%

The disclosure of the survey result of the Thai Institute of Directors Association (IOD)

regarding corporate governance is made pursuant to the Office of the Securities and

Exchange Commission. The survey of the IOD is based on the information of a company

l isted on the Stock Exchange of Thailand and the Market for Alternative disclosure to the

public and able to be accessed by a general public investor. The results, therefore, is from

the perspective of a third party. It is not an evaluation of operation and is not based on

inside information.

The survey result is as of the date appearing in the Corporate Governance Report of Thai

Listed Companies. As a result, the survey result may be changed after that data. Phil l ip

Securities (Thailand) of securities company does not confirm nor certify the accuracy of

such survey result.

No logo given

Number of Logo

Results Presentation

THAILAND EQUITY RESEARCH

PHILLIP SECURITIESS (THAILAND) | 4 | P a g e

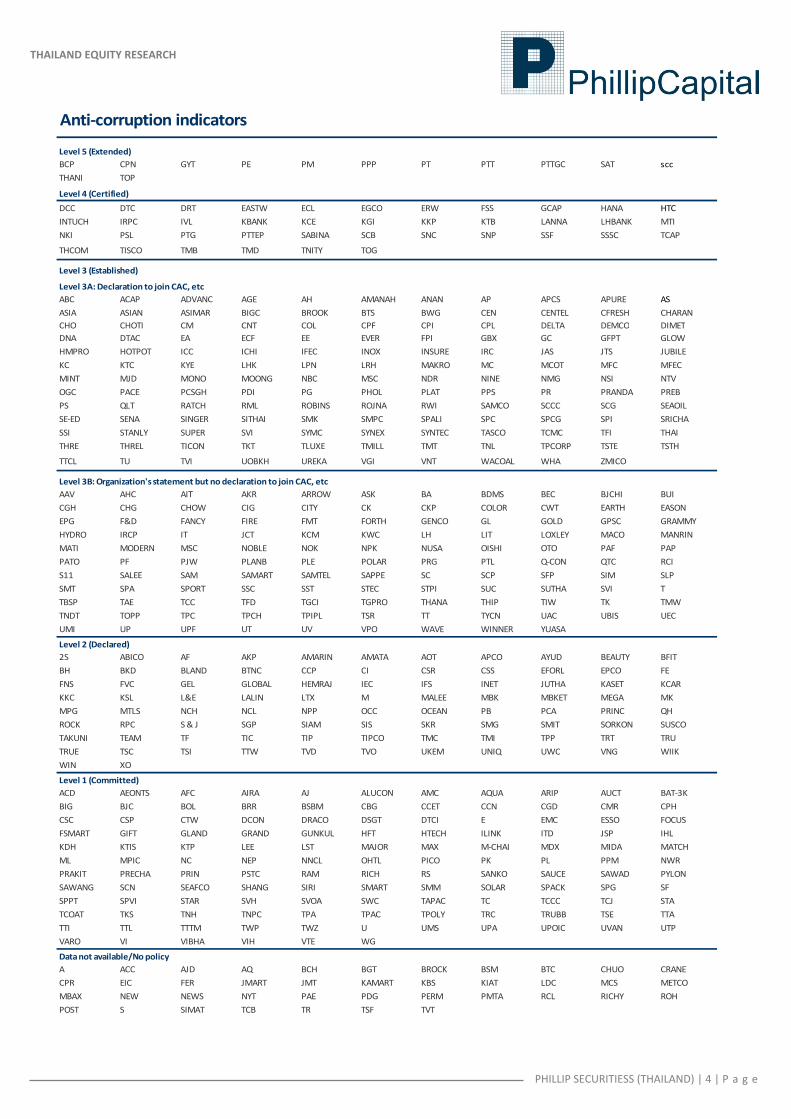

Anti‐corruption indicators

Level 5 (Extended)

BCP CPN GYT PE PM PPP PT PTT PTTGC SAT scc

THANI TOP

Level 4 (Certified)

DCC DTC DRT EASTW ECL EGCO ERW FSS GCAP HANA HTC

INTUCH IRPC IVL KBANK KCE KGI KKP KTB LANNA LHBANK MTI

NKI PSL PTG PTTEP SABINA SCB SNC SNP SSF SSSC TCAP

THCOM TISCO TMB TMD TNITY TOG

Level 3 (Established)

Level 3A: Declaration to join CAC, etc

ABC ACAP ADVANC AGE AH AMANAH ANAN AP APCS APURE AS

ASIA ASIAN ASIMAR BIGC BROOK BTS BWG CEN CENTEL CFRESH CHARAN

CHO CHOTI CM CNT COL CPF CPI CPL DELTA DEMCO DIMET

DNA DTAC EA ECF EE EVER FPI GBX GC GFPT GLOW

HMPRO HOTPOT ICC ICHI IFEC INOX INSURE IRC JAS JTS JUBILE

KC KTC KYE LHK LPN LRH MAKRO MC MCOT MFC MFEC

MINT MJD MONO MOONG NBC MSC NDR NINE NMG NSI NTV

OGC PACE PCSGH PDI PG PHOL PLAT PPS PR PRANDA PREB

PS QLT RATCH RML ROBINS ROJNA RWI SAMCO SCCC SCG SEAOIL

SE‐ED SENA SINGER SITHAI SMK SMPC SPALI SPC SPCG SPI SRICHA

SSI STANLY SUPER SVI SYMC SYNEX SYNTEC TASCO TCMC TFI THAI

THRE THREL TICON TKT TLUXE TMILL TMT TNL TPCORP TSTE TSTH

TTCL TU TVI UOBKH UREKA VGI VNT WACOAL WHA ZMICO

Level 3B: Organization's statement but no declaration to join CAC, etc

AAV AHC AIT AKR ARROW ASK BA BDMS BEC BJCHI BUI

CGH CHG CHOW CIG CITY CK CKP COLOR CWT EARTH EASON

EPG F&D FANCY FIRE FMT FORTH GENCO GL GOLD GPSC GRAMMY

HYDRO IRCP IT JCT KCM KWC LH LIT LOXLEY MACO MANRIN

MATI MODERN MSC NOBLE NOK NPK NUSA OISHI OTO PAF PAP

PATO PF PJW PLANB PLE POLAR PRG PTL Q‐CON QTC RCI

S11 SALEE SAM SAMART SAMTEL SAPPE SC SCP SFP SIM SLP

SMT SPA SPORT SSC SST STEC STPI SUC SUTHA SVI T

TBSP TAE TCC TFD TGCI TGPRO THANA THIP TIW TK TMW

TNDT TOPP TPC TPCH TPIPL TSR TT TYCN UAC UBIS UEC

UMI UP UPF UT UV VPO WAVE WINNER YUASA

Level 2 (Declared)

2S ABICO AF AKP AMARIN AMATA AOT APCO AYUD BEAUTY BFIT

BH BKD BLAND BTNC CCP CI CSR CSS EFORL EPCO FE

FNS FVC GEL GLOBAL HEMRAJ IEC IFS INET JUTHA KASET KCAR

KKC KSL L&E LALIN LTX M MALEE MBK MBKET MEGA MK

MPG MTLS NCH NCL NPP OCC OCEAN PB PCA PRINC QH

ROCK RPC S & J SGP SIAM SIS SKR SMG SMIT SORKON SUSCO

TAKUNI TEAM TF TIC TIP TIPCO TMC TMI TPP TRT TRU

TRUE TSC TSI TTW TVD TVO UKEM UNIQ UWC VNG WIIK

WIN XO

Level 1 (Committed)

ACD AEONTS AFC AIRA AJ ALUCON AMC AQUA ARIP AUCT BAT‐3K

BIG BJC BOL BRR BSBM CBG CCET CCN CGD CMR CPH

CSC CSP CTW DCON DRACO DSGT DTCI E EMC ESSO FOCUS

FSMART GIFT GLAND GRAND GUNKUL HFT HTECH ILINK ITD JSP IHL

KDH KTIS KTP LEE LST MAJOR MAX M‐CHAI MDX MIDA MATCH

ML MPIC NC NEP NNCL OHTL PICO PK PL PPM NWR

PRAKIT PRECHA PRIN PSTC RAM RICH RS SANKO SAUCE SAWAD PYLON

SAWANG SCN SEAFCO SHANG SIRI SMART SMM SOLAR SPACK SPG SF

SPPT SPVI STAR SVH SVOA SWC TAPAC TC TCCC TCJ STA

TCOAT TKS TNH TNPC TPA TPAC TPOLY TRC TRUBB TSE TTA

TTI TTL TTTM TWP TWZ U UMS UPA UPOIC UVAN UTP

VARO VI VIBHA VIH VTE WG

Data not available/No policy

A ACC AJD AQ BCH BGT BROCK BSM BTC CHUO CRANE

CPR EIC FER JMART JMT KAMART KBS KIAT LDC MCS METCO

MBAX NEW NEWS NYT PAE PDG PERM PMTA RCL RICHY ROH

POST S SIMAT TCB TR TSF TVT

THAILAND EQUITY RESEARCH

PHILLIP SECURITIESS (THAILAND) | 5 | P a g e

Anti‐corruption indicators

Level 5 : Extended

Anti‐corruption policies extend to business partners, dealers, and distributors.

Level 4 : Certified

Anti‐corruption policies can be engaged by audit committee and auditors approved by the SEC.

Anti‐corruption policies are certified by CAC and independent assurance providers.

Level 3 : Established

Anti‐corruption corruption policies cover anti‐bribery, and communications and educating all employees anti‐corruption policies.

Level 3A Public out statement to join CAC, etc.

Level 3B Declare statement and organization’s anti‐corruption policies but no intention to join CAC, etc.

Level 2 : Declared

Declare statement to participate CAC against corruption.

Level 1 : Committed

Organization and Board of Directors’ statements against corruption and not getting involve in any malpractices.

Assessment

Anti‐corruption progress indicator for listed companies is a part of SEC’s commitment to create sustainability in anti‐corruption and to become a role model to any

related business. The progress indicators comprise of five levels: 1) Committed, 2) Declared, 3) Established, 4) Certified, and 5) Extended. These indicators will

encourage listed firms to formulate anti‐corruption policies to opt out of corruption, and investors can determine their investment based on anti‐corruption indicator

or avoid investment in listed firms that could get involve in corruption.

THAILAND EQUITY RESEARCH

PHILLIP SECURITIESS (THAILAND) | 6 | P a g e

Industry Group Name Sector Name Sector Index

Agro & Food Industry[AGRO] Agribusiness AGRI

Food & Beverage FOOD

Consumer Products[CONSUMP] Fashion FASHION

Home & Office Products HOME

Personal Products & Pharmaceuticals PERSON

Financials [FINCIAL] Banking BANK

Finance & Securities FIN

Insurance INSUR

Industrials [INDUS] Automotive AUTO

Industrial Materials & Machinery IMM

Packaging PKG

Paper & Printing Materials PAPER

Petrochemicals & Chemicals PETRO

Steel STEEL

Property & Construction[PROPCON] Construction Materials CONMAT

Construction Services CONS

Property Development PROP

Property Fund & REITs PF&REIT

Resources [RESOURC] Energy & Util ities ENERG

Mining MINE

Services [SERVICE] Commerce COMM

Media & Publishing MEDIA

Health Care Services HELTH

Tourism & Leisure TOURISM

Professional Services PROF

Transportation & Logistics TRANS

Technology [TECH] Electronic Components ETRON

Information & Communication Technology ICT

PSR Rating SystemCapital Gain Recommendation

> 15% BUY

> 5% ‐ 15% ACCUMULATE / TRADING BUY

> 0% ‐ 5% NEUTRAL

0 <= SELL

Remarks

We do not base our recommendations entirely on the above quantitative return bands. We consider qualitative factors l ike (but

not l imited to) a stock's risk reward profi le, market sentiment, recent rate of share price appreciation, presence or absence of

stock price catalysts, and speculative undertones surrounding the stock, before making our final recommendation

22776846