Econ 240 C Lecture 13 1. 2 Re-Visit Santa Barbara South Coast House Price Santa Barbara South Coast...

111

Econ 240 C Econ 240 C Lecture 13 Lecture 13 1

-

date post

21-Dec-2015 -

Category

Documents

-

view

214 -

download

0

Transcript of Econ 240 C Lecture 13 1. 2 Re-Visit Santa Barbara South Coast House Price Santa Barbara South Coast...

Econ 240 CEcon 240 C

Lecture 13Lecture 13

1

2

Re-VisitRe-Visit

Santa Barbara South Coast House Santa Barbara South Coast House PricePrice

UC Budget, General FundUC Budget, General FundExponential Smoothing, p.43-Exponential Smoothing, p.43------------------------------------------------------------------------- Intervention AnalysisIntervention Analysis

3

0

500

1000

1500

1970 1980 1990 2000 2010

YEAR

HS

EP

RC

Santa Barbara South Coast Median House Price, 1974-2008

Thousands of Nominal DollarsThousands of Nominal Dollars

4

3

4

5

6

7

8

1970 1980 1990 2000 2010

YEAR

LNH

SE

PR

C

SB South Coast Median House Price, Log Scale

5

0

500

1000

1500

1970 1980 1990 2000 2010

YEAR

HS

EP

RC

08

Santa Barbara South Coast Median House Price, 2008$

6

5.0

5.5

6.0

6.5

7.0

7.5

1970 1980 1990 2000 2010

YEAR

LNH

SE

PR

C08

Santa Barbara South Coast LN Median House Price 2008 $

71996-20051996-2005

8

-0.05

0.00

0.05

0.10

5.8

6.0

6.2

6.4

6.6

6.8

7.0

7.2

22 23 24 25 26 27 28 29 30 31

Residual Actual Fitted

Actual, Fitted and residual from Regression, 1996-2005

9

UC Budget, General Fund Vs. CA Personal Income in $B, 1968-69 Through 2009-10

0

0.5

1

1.5

2

2.5

3

3.5

4

0 200 400 600 800 1000 1200 1400 1600 1800

CA Personal Income $B

UC

Bu

dg

et, G

ener

al F

un

d $

BUC Budget Vs. CA Personal UC Budget Vs. CA Personal

IncomeIncome

10

CA General Fund Expenditures Vs. Personal Income 1968-69 through 2009-10

2009-10

1968-69

0

20

40

60

80

100

120

0 200 400 600 800 1000 1200 1400 1600 1800

CA Personal Income $B

CA

Gen

eral

Fu

nd

Exp

end

itu

res

$BCA General Fund Expenditures Vs. CA General Fund Expenditures Vs. Personal IncomePersonal Income

11

Relative Size of CA Government, 1968-69 through 2009-10

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

68-6

9

70-7

1

72-7

3

74-7

5

76-7

7

78-7

9

80-8

1

82-8

3

84-8

5

86-8

7

88-8

9

90-9

1

92-9

3

94-9

5

96-9

7

98-9

9

00-0

1

02-0

3

04-0

5

06-0

7

08-0

9

Fiscal Year

Per

cen

tRelative Size of CA Relative Size of CA

GovernmentGovernment

12

4

5

6

7

8

70 75 80 85 90 95 00 05

LNCAPY

Log of California Personal Income in Nominal Dollars, 1968-69 through 2009-10

CA Personal Income, Nominal CA Personal Income, Nominal $$

13

OutlineOutline

Exponential SmoothingExponential SmoothingBack of the envelope formula: geometric Back of the envelope formula: geometric

distributed lag: L(t) = a*y(t-1) + (1-a)*L(t-1); distributed lag: L(t) = a*y(t-1) + (1-a)*L(t-1); F(t) = L(t)F(t) = L(t)

ARIMA (p,d,q) = (0,1,1); ARIMA (p,d,q) = (0,1,1); ∆y(t) = e(t) –(1-a)e(t-∆y(t) = e(t) –(1-a)e(t-1)1)

Error correction: L(t) =L(t-1) + a*e(t)Error correction: L(t) =L(t-1) + a*e(t) Intervention AnalysisIntervention Analysis

14

Part I: Exponential SmoothingPart I: Exponential Smoothing

Exponential smoothing is a technique Exponential smoothing is a technique that is useful for forecasting short that is useful for forecasting short time series where there may not be time series where there may not be enough observations to estimate a enough observations to estimate a Box-Jenkins modelBox-Jenkins model

Exponential smoothing can be Exponential smoothing can be understood from many perspectives; understood from many perspectives; one perspective is a formula that one perspective is a formula that could be calculated by handcould be calculated by hand

15

0

200

400

600

800

1000

1970 1980 1990 2000 2010

YEAR

HS

EP

RC

Santa Barbara South Coast Median House Price in Nominal Thousands

16

3

4

5

6

7

1970 1980 1990 2000 2010

YEAR

LN

HS

EP

RC

Three Rates of Growth

17

0

200

400

600

800

1000

1970 1980 1990 2000 2010

YEAR

HS

EP

RC

04

Santa Barbara South Coast House Price, 000 04 $

18Simple exponential Simple exponential smoothingsmoothing

Simple exponential smoothing, also Simple exponential smoothing, also known as single exponential smoothing, known as single exponential smoothing, is most appropriate for a time series is most appropriate for a time series that is a random walk with first order that is a random walk with first order moving average error structuremoving average error structure

The levels term, L(t), is a weighted The levels term, L(t), is a weighted average of the observation lagged one, average of the observation lagged one, y(t-1) plus the previous levels, L(t-1):y(t-1) plus the previous levels, L(t-1):

L(t) = a*y(t-1) + (1-a)*L(t-1)L(t) = a*y(t-1) + (1-a)*L(t-1)

19

Single exponential smoothingSingle exponential smoothing

The parameter a is chosen to minimize The parameter a is chosen to minimize the sum of squared errors where the the sum of squared errors where the error is the difference between the error is the difference between the observation and the levels term: e(t) = observation and the levels term: e(t) = y(t) – L(t)y(t) – L(t)

The forecast for period t+1 is given by The forecast for period t+1 is given by the formula: L(t+1) = a*y(t) + (1-a)*L(t)the formula: L(t+1) = a*y(t) + (1-a)*L(t)

Example from John Heinke and Arthur Example from John Heinke and Arthur Reitsch, Reitsch, Business Forecasting, 6Business Forecasting, 6thth Ed. Ed.

20observations Sales

1 500

2 350

3 250

4 400

5 450

6 350

7 200

8 300

9 350

10 200

11 150

12 400

13 550

14 350

15 250

16 550

17 550

18 400

19 350

20 600

21 750

22 500

23 400

24 650

21

Single exponential smoothingSingle exponential smoothing

For observation #1, set L(1) = For observation #1, set L(1) = Sales(1) = 500, as an initial conditionSales(1) = 500, as an initial condition

As a trial value use a = 0.1As a trial value use a = 0.1So L(2) = 0.1*Sales(1) + 0.9*Level(1) So L(2) = 0.1*Sales(1) + 0.9*Level(1)

L(2) = 0.1*500 + 0.9*500 = 500 L(2) = 0.1*500 + 0.9*500 = 500And L(3) = 0.1*Sales(2) + And L(3) = 0.1*Sales(2) +

0.9*Level(2) L(3) = 0.1*350 + 0.9*Level(2) L(3) = 0.1*350 + 0.9*500 = 4850.9*500 = 485

22observations Sales Level

1 500 500

2 350

3 250

4 400

5 450

6 350

7 200

8 300

9 350

10 200

11 150

12 400

13 550

14 350

15 250

16 550

17 550

18 400

19 350

20 600

21 750

22 500

23 400

24 650

23observations Sales Level

1 500 500

2 350 500

3 250 485

4 400

5 450

6 350

7 200

8 300

9 350

10 200

11 150

12 400

13 550

14 350

15 250

16 550

17 550

18 400

19 350

20 600

21 750

22 500

23 400

24 650

a = 0.1

24

Single exponential smoothingSingle exponential smoothing

So the formula can be used to So the formula can be used to calculate the rest of the levels calculate the rest of the levels values, observation #4-#24values, observation #4-#24

This can be set up on a spread-sheetThis can be set up on a spread-sheet

25observations Sales Level

1 500 500

2 350 500

3 250 485

4 400 461.5

5 450 455.4

6 350 454.8

7 200 444.3

8 300 419.9

9 350 407.9

10 200 402.1

11 150 381.9

12 400 358.7

13 550 362.8

14 350 381.6

15 250 378.4

16 550 365.6

17 550 384.0

18 400 400.6

19 350 400.5

20 600 395.5

21 750 415.9

22 500 449.3

23 400 454.4

24 650 449.0

a = 0.1

26

Single exponential smoothingSingle exponential smoothing

The forecast for observation #25 is: The forecast for observation #25 is: L(25) = 0.1*sales(24)+0.9*L(24)L(25) = 0.1*sales(24)+0.9*L(24)

Forecast(25)=Levels(25)=0.1*650+0.9Forecast(25)=Levels(25)=0.1*650+0.9*449*449

Forecast(25) = 469.1Forecast(25) = 469.1

Single Exponential Smoothing

0

100

200

300

400

500

600

700

800

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Observation

Val

ue Sales

Levels

28Single exponential Single exponential distributiondistribution

The errors can now be calculated: The errors can now be calculated: e(t) = sales(t) – levels(t) e(t) = sales(t) – levels(t)

29observations Sales Level error

1 500 500 0

2 350 500 -150

3 250 485 -235

4 400 461.5 -61.5

5 450 455.4 -5.35

6 350 454.8 -104.8

7 200 444.3 -244.3

8 300 419.9 -119.9

9 350 407.9 -57.9

10 200 402.1 -202.1

11 150 381.9 -231.9

12 400 358.7 41.3

13 550 362.8 187.2

14 350 381.6 -31.6

15 250 378.4 -128.4

16 550 365.6 184.4

17 550 384.0 166.0

18 400 400.6 -0.6

19 350 400.5 -50.5

20 600 395.5 204.5

21 750 415.9 334.1

22 500 449.3 50.7

23 400 454.4 -54.4

24 650 449.0 201.0

a = 0.1

30observations Sales Level error

error squared

1 500 500 0 0

2 350 500 -150 22500

3 250 485 -235 55225

4 400 461.5 -61.5 3782.25

5 450 455.4 -5.35 28.62

6 350 454.8 -104.8 10986.18

7 200 444.3 -244.3 59698.86

8 300 419.9 -119.9 14376.05

9 350 407.9 -57.9 3353.58

10 200 402.1 -202.1 40852.14

11 150 381.9 -231.9 53780.95

12 400 358.7 41.3 1704.33

13 550 362.8 187.2 35027.05

14 350 381.6 -31.6 996.06

15 250 378.4 -128.4 16487.67

16 550 365.6 184.4 34016.68

17 550 384.0 166.0 27553.51

18 400 400.6 -0.6 0.37

19 350 400.5 -50.5 2554.91

20 600 395.5 204.5 41823.74

21 750 415.9 334.1 111594.53

22 500 449.3 50.7 2565.62

23 400 454.4 -54.4 2960.80

24 650 449.0 201.0 40412.28

a = 0.1

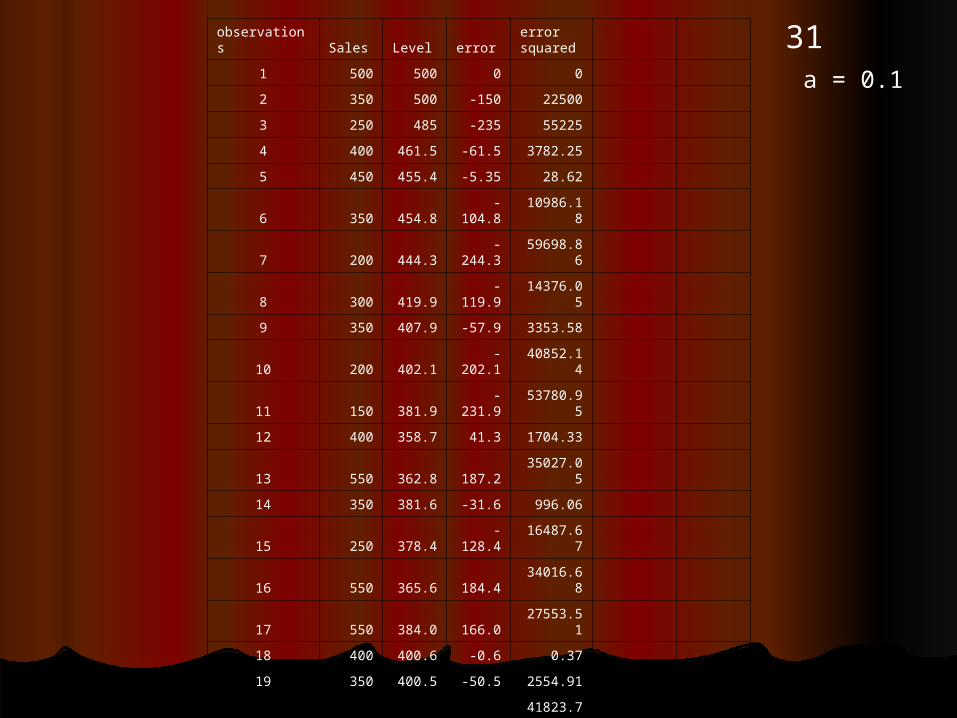

31observations Sales Level errorerror squared

1 500 500 0 0

2 350 500 -150 22500

3 250 485 -235 55225

4 400 461.5 -61.5 3782.25

5 450 455.4 -5.35 28.62

6 350 454.8 -104.8 10986.18

7 200 444.3 -244.3 59698.86

8 300 419.9 -119.9 14376.05

9 350 407.9 -57.9 3353.58

10 200 402.1 -202.1 40852.14

11 150 381.9 -231.9 53780.95

12 400 358.7 41.3 1704.33

13 550 362.8 187.2 35027.05

14 350 381.6 -31.6 996.06

15 250 378.4 -128.4 16487.67

16 550 365.6 184.4 34016.68

17 550 384.0 166.0 27553.51

18 400 400.6 -0.6 0.37

19 350 400.5 -50.5 2554.91

20 600 395.5 204.5 41823.74

21 750 415.9 334.1 111594.53

22 500 449.3 50.7 2565.62

23 400 454.4 -54.4 2960.80

24 650 449.0 201.0 40412.28

sum sq res 582281.2

a = 0.1

32

Single exponential smoothingSingle exponential smoothing

For a = 0.1, the sum of squared For a = 0.1, the sum of squared errors is: errors is: errors)errors)2 2 = 582,281.2= 582,281.2

A grid search can be conducted for A grid search can be conducted for the parameter value a, to find the the parameter value a, to find the value between 0 and 1 that value between 0 and 1 that minimizes the sum of squared errorsminimizes the sum of squared errors

The calculations of levels, L(t), and The calculations of levels, L(t), and errors, e(t) = sales(t) – L(t) for a =0.6errors, e(t) = sales(t) – L(t) for a =0.6

33observations Sales Levels

1 500 500

2 350 500

3 250 410

4 400 314

5 450 365.6

6 350 416.2

7 200 376.5

8 300 270.6

9 350 288.2

10 200 325.3

11 150 250.1

12 400 190.0

13 550 316.0

14 350 456.4

15 250 392.6

16 550 307.0

17 550 452.8

18 400 511.1

19 350 444.4

20 600 387.8

21 750 515.1

22 500 656.0

23 400 562.4

24 650 465.0

a = 0.6

34

Single exponential smoothingSingle exponential smoothing

Forecast(25) = Levels(25) = Forecast(25) = Levels(25) = 0.6*sales(24) + 0.4*levels(24) = 0.6*sales(24) + 0.4*levels(24) = 0.6*650 + 0.4*465 = 7760.6*650 + 0.4*465 = 776

35observations Sales Levels error

error square

1 500 500 0 0

2 350 500 -150 22500

3 250 410 -160 25600

4 400 314 86 7396

5 450 365.6 84.4 7123.36

6 350 416.2 -66.2 4387.74

7 200 376.5 -176.5 31150.84

8 300 270.6 29.4 864.45

9 350 288.2 61.8 3814.38

10 200 325.3 -125.3 15699.02

11 150 250.1 -100.1 10023.67

12 400 190.0 210.0 44080.13

13 550 316.0 234.0 54747.14

14 350 456.4 -106.4 11322.57

15 250 392.6 -142.6 20324.22

16 550 307.0 243.0 59036.75

17 550 452.8 97.2 9445.88

18 400 511.1 -111.1 12348.55

19 350 444.4 -94.4 8920.73

20 600 387.8 212.2 45037.39

21 750 515.1 234.9 55172.40

22 500 656.0 -156.0 24349.97

23 400 562.4 -162.4 26379.58

24 650 465.0 185.0 34237.15

Sum of Sq Res 533961.9

a = 0.6

36

Single exponential smoothingSingle exponential smoothing

Grid search plotGrid search plot

Grid Search for Smoothing Parameter

490000

500000

510000

520000

530000

540000

550000

560000

570000

580000

590000

0 0.2 0.4 0.6 0.8 1 1.2

Smoothing Parameter

Su

m o

f S

qu

ared

Res

idu

als

38

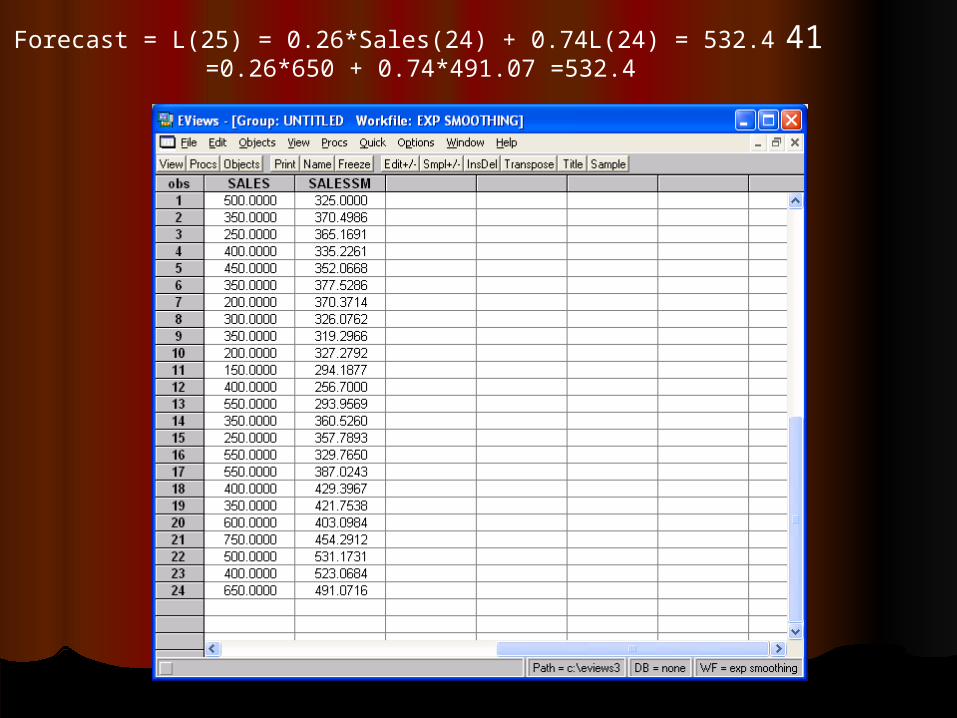

Single Exponential SmoothingSingle Exponential Smoothing EVIEWS: Algorithmic search for the EVIEWS: Algorithmic search for the

smoothing parameter asmoothing parameter a In EVIEWS, select time series sales(t), and In EVIEWS, select time series sales(t), and

openopen In the sales window, go to the PROCS menu and In the sales window, go to the PROCS menu and

select exponential smoothingselect exponential smoothing Select singleSelect single the best parameter a = 0.26 with sum of squared the best parameter a = 0.26 with sum of squared

errors = 472982.1 and root mean square error = errors = 472982.1 and root mean square error = 140.4 = (472982.1/24)140.4 = (472982.1/24)1/21/2

The forecast, or end of period levels mean = 532.4The forecast, or end of period levels mean = 532.4

39

40

41Forecast = L(25) = 0.26*Sales(24) + 0.74L(24) = 532.4=0.26*650 + 0.74*491.07 =532.4

42

43Part II. Three Perspectives on Part II. Three Perspectives on Single Exponential SmoothingSingle Exponential SmoothingThe formula perspectiveThe formula perspective

L(t) = a*y(t-1) + (1 - a)*L(t-1)L(t) = a*y(t-1) + (1 - a)*L(t-1)e(t) = y(t) - L(t)e(t) = y(t) - L(t)

The Box-Jenkins PerspectiveThe Box-Jenkins PerspectiveThe Updating Forecasts PerspectiveThe Updating Forecasts Perspective

44

Box Jenkins PerspectiveBox Jenkins PerspectiveUse the error equation to substitute for L(t) Use the error equation to substitute for L(t)

in the formula, L(t) = a*y(t-1) + (1 - a)*L(t-in the formula, L(t) = a*y(t-1) + (1 - a)*L(t-1)1)L(t) = y(t) - e(t)L(t) = y(t) - e(t)y(t) - e(t) = a*y(t-1) + (1 - a)*[y(t-1) - e(t-1)] y(t) - e(t) = a*y(t-1) + (1 - a)*[y(t-1) - e(t-1)]

y(t) = e(t) + y(t-1) - (1-a)*e(t-1)y(t) = e(t) + y(t-1) - (1-a)*e(t-1)or or y(t) = y(t) - y(t-1) = e(t) - (1-a) e(t-1)y(t) = y(t) - y(t-1) = e(t) - (1-a) e(t-1)

So y(t) is a random walk plus MAONE noise, So y(t) is a random walk plus MAONE noise, i.e y(t) is a (0,1,1) process where (p,d,q) are i.e y(t) is a (0,1,1) process where (p,d,q) are the orders of AR, differencing, and MA.the orders of AR, differencing, and MA.

45

Box-Jenkins PerspectiveBox-Jenkins Perspective

In Lab Seven, we will apply simple In Lab Seven, we will apply simple exponential smoothing to retail sales, exponential smoothing to retail sales, and which can be modeled as (0,1,1).and which can be modeled as (0,1,1).

46

47

48

130000

140000

150000

160000

170000

90 91 92 93 94 95 96

RETAIL RETAILSM

Retail Sales: Simple Exponential Smoothing

50

51

Box-Jenkins PerspectiveBox-Jenkins Perspective

If the smoothing parameter approaches If the smoothing parameter approaches one, then y(t) is a random walk:one, then y(t) is a random walk:y(t) = y(t) - y(t-1) = e(t) - (1-a) e(t-1)y(t) = y(t) - y(t-1) = e(t) - (1-a) e(t-1)if a = 1, then if a = 1, then y(t) = y(t) - y(t-1) = e(t) y(t) = y(t) - y(t-1) = e(t)

In Lab Seven, we will use the price of In Lab Seven, we will use the price of gold to make this pointgold to make this point

52

360

380

400

420

440

460

10 20 30 40 50 60 70

GOLD

Weekly Closing Price of Gold , Nov. 14, 2003-April 29, 2005

53

54

55

56Box-Jenkins PerspectiveBox-Jenkins PerspectiveThe levels or forecast, L(t), is a The levels or forecast, L(t), is a

geometric distributed lag of past geometric distributed lag of past observations of the series, y(t), hence observations of the series, y(t), hence the name “exponential” smoothingthe name “exponential” smoothingL(t) = a*y(t-1) + (1 - a)*L(t-1)L(t) = a*y(t-1) + (1 - a)*L(t-1)L(t) = a*y(t-1) + (1 - a)*ZL(t)L(t) = a*y(t-1) + (1 - a)*ZL(t)L(t) - (1 - a)*ZL(t) = a*y(t-1) L(t) - (1 - a)*ZL(t) = a*y(t-1) [1 - (1-a)Z] L(t) = a*y(t-1) [1 - (1-a)Z] L(t) = a*y(t-1) L(t) = {1/ [1 - (1-a)Z]} a*y(t-1) L(t) = {1/ [1 - (1-a)Z]} a*y(t-1) L(t) = [1 +(1-a)Z + (1-a)L(t) = [1 +(1-a)Z + (1-a)2 2 ZZ2 2 + …] a*y(t-1)+ …] a*y(t-1)L(t) = a*y(t-1) + (1-a)*a*y(t-2) + (1-L(t) = a*y(t-1) + (1-a)*a*y(t-2) + (1-

a)a)22a*y(t-3) + ….a*y(t-3) + ….

57

58The Updating Forecasts The Updating Forecasts PerspectivePerspective

Use the error equation to substitute for Use the error equation to substitute for y(t) in the formula, L(t) = a*y(t-1) + (1 - y(t) in the formula, L(t) = a*y(t-1) + (1 - a)*L(t-1)a)*L(t-1)y(t) = L(t) + e(t)y(t) = L(t) + e(t)L(t) = a*[L(t-1) + e(t-1)] + (1 - a)*L(t-1)L(t) = a*[L(t-1) + e(t-1)] + (1 - a)*L(t-1)

So L(t) = L(t-1) + a*e(t-1), So L(t) = L(t-1) + a*e(t-1), i.e. the forecast for period t is equal to the i.e. the forecast for period t is equal to the

forecast for period t-1 plus a fraction a of the forecast for period t-1 plus a fraction a of the forecast error from period t-1.forecast error from period t-1.

59Part III. Double Exponential Part III. Double Exponential

Smoothing Smoothing With double exponential smoothing, one With double exponential smoothing, one

estimates a “trend” term, R(t), as well estimates a “trend” term, R(t), as well as a levels term, L(t), so it is possible to as a levels term, L(t), so it is possible to forecast, f(t), out more than one periodforecast, f(t), out more than one period

f(t+k) = L(t) + k*R(t), k>=1f(t+k) = L(t) + k*R(t), k>=1L(t) = a*y(t) + (1-a)*[L(t-1) + R(t-1)]L(t) = a*y(t) + (1-a)*[L(t-1) + R(t-1)]R(t) = b*[L(t) - L(t-1)] + (1-b)*R(t-1)R(t) = b*[L(t) - L(t-1)] + (1-b)*R(t-1)

so the trend, R(t), is a geometric distributed so the trend, R(t), is a geometric distributed lag of the change in levels, lag of the change in levels, L(t)L(t)

1k 1k 1k

1k

60

If the smoothing parameters a = b, If the smoothing parameters a = b, then we have double exponential then we have double exponential smoothingsmoothing

If the smoothing parameters are If the smoothing parameters are different, then it is the simplest different, then it is the simplest version of Holt-Winters smoothingversion of Holt-Winters smoothing

Part III. Double Exponential Part III. Double Exponential SmoothingSmoothing

61Part III. Double Exponential Part III. Double Exponential SmoothingSmoothing

Holt- Winters can also be used to forecast Holt- Winters can also be used to forecast seasonal time series, e.g. monthlyseasonal time series, e.g. monthly

f(t+k) = L(t) + k*R(t) + S(t+k-12) k>=1f(t+k) = L(t) + k*R(t) + S(t+k-12) k>=1L(t) = a*[y(t)-S(t-12)]+ (1-a)*[L(t-1) + R(t-L(t) = a*[y(t)-S(t-12)]+ (1-a)*[L(t-1) + R(t-

1)]1)]R(t) = b*[L(t) - L(t-1)] + (1-b)*R(t-1)R(t) = b*[L(t) - L(t-1)] + (1-b)*R(t-1)S(t) = c*[y(t) - L(t)] + (1-c)*S(t-12)S(t) = c*[y(t) - L(t)] + (1-c)*S(t-12)

62

Part V. Intervention AnalysisPart V. Intervention Analysis

63

Intervention AnalysisIntervention Analysis

The approach to intervention The approach to intervention analysis parallels Box-Jenkins in that analysis parallels Box-Jenkins in that the actual estimation is conducted the actual estimation is conducted after pre-whitening, to the extent after pre-whitening, to the extent that non-stationarity such as trend that non-stationarity such as trend and seasonality are removedand seasonality are removed

Example: preview of Lab 7Example: preview of Lab 7

64Telephone Directory Telephone Directory AssistanceAssistance

A telephone company was receiving A telephone company was receiving increased demand for free directory increased demand for free directory assistance, i.e. subscribers asking assistance, i.e. subscribers asking operators to look up numbers. This operators to look up numbers. This was increasing costs and the was increasing costs and the company changed policy, providing a company changed policy, providing a number of free assisted calls to number of free assisted calls to subscribers per month, but charging subscribers per month, but charging a price per call after that number. a price per call after that number.

65Telephone Directory Telephone Directory AssistanceAssistance

This policy change occurred at a This policy change occurred at a known time, March 1974known time, March 1974

The time series is for calls with The time series is for calls with directory assistance per monthdirectory assistance per month

Did the policy change make a Did the policy change make a difference?difference?

66

67

The simple-minded approachThe simple-minded approach

=549 - 162

=387

68

69

70

71

PrinciplePrinciple

The event may cause a change, and The event may cause a change, and affect time series characteristicsaffect time series characteristics

Consequently, consider the pre-event Consequently, consider the pre-event period, January 1962 through period, January 1962 through February 1974, the event March February 1974, the event March 1974, and the post-event period, 1974, and the post-event period, April 1974 through December 1976April 1974 through December 1976

First difference and then seasonally First difference and then seasonally difference the entire seriesdifference the entire series

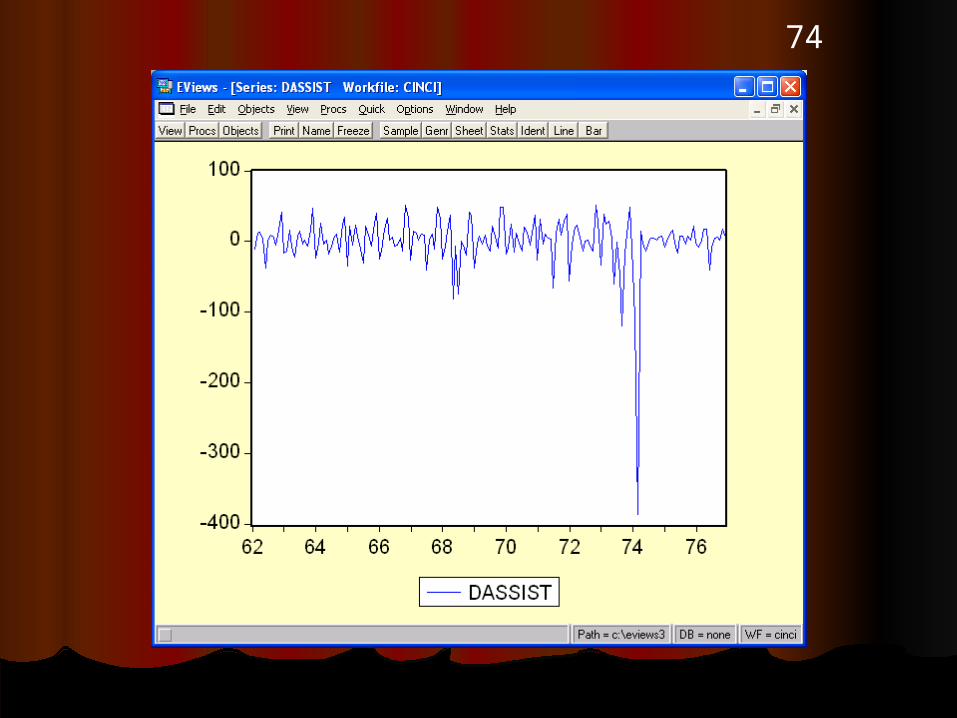

72Analysis: Entire Differenced Analysis: Entire Differenced SeriesSeries

73

74

75

76

77Analysis: Pre-Event Analysis: Pre-Event DifferencesDifferences

78

79

80

81

So Seasonal NonstationaritySo Seasonal Nonstationarity

It was masked in the entire sample It was masked in the entire sample by the variance caused by the by the variance caused by the difference from the eventdifference from the event

The seasonality was revealed in the The seasonality was revealed in the pre-event differenced series pre-event differenced series

82

83

Pre-Event AnalysisPre-Event Analysis

Seasonally differenced, differenced Seasonally differenced, differenced series series

84

85

86

87

88

Pre-Event Box-Jenkins ModelPre-Event Box-Jenkins Model

[1-Z[1-Z12 12 ][1 –Z]Assist(t) = WN(t) – a*WN(t-][1 –Z]Assist(t) = WN(t) – a*WN(t-12)12)

89

90

91

92

Modeling the EventModeling the Event

Step functionStep function

93

Entire SeriesEntire Series

Assist and StepAssist and StepDassist and DstepDassist and DstepSddast sddstepSddast sddstep

94

95

96

97

Model of Series and EventModel of Series and Event

Pre-Event Model: [1-ZPre-Event Model: [1-Z12 12 ][1 –Z]Assist(t) = ][1 –Z]Assist(t) = WN(t) – a*WN(t-12)WN(t) – a*WN(t-12)

In Levels Plus Event: Assist(t)=[WN(t) – In Levels Plus Event: Assist(t)=[WN(t) – a*WN(t-12)]/[1-Z]*[1-Za*WN(t-12)]/[1-Z]*[1-Z1212] + (-b)*step] + (-b)*step

Estimate: [1-ZEstimate: [1-Z12 12 ][1 –Z]Assist(t) = WN(t) ][1 –Z]Assist(t) = WN(t) – a*WN(t-12) + (-b)* [1-Z– a*WN(t-12) + (-b)* [1-Z12 12 ][1 –Z]*step][1 –Z]*step

98

99

100

Policy Change EffectPolicy Change Effect

Simple: decrease of 387 (thousand) Simple: decrease of 387 (thousand) calls per monthcalls per month

Intervention model: decrease of 397 Intervention model: decrease of 397 with a standard error of 22with a standard error of 22

101

102Stochastic Trends: Random Stochastic Trends: Random

Walks with DriftWalks with DriftWe have discussed earlier in the We have discussed earlier in the

course how to model the Total Return course how to model the Total Return to the Standard and Poor’s 500 Indexto the Standard and Poor’s 500 Index

One possibility is this time series could One possibility is this time series could be a random walk around a be a random walk around a deterministic trend”deterministic trend”

Sp500(t) = exp{a + d*t +WN(t)/[1-Z]}Sp500(t) = exp{a + d*t +WN(t)/[1-Z]}And taking logarithms,And taking logarithms,

103Stochastic Trends: Random Stochastic Trends: Random

Walks with DriftWalks with Drift Lnsp500(t) = a + d*t + WN(t)/[1-Z]Lnsp500(t) = a + d*t + WN(t)/[1-Z] Lnsp500(t) –a –d*t = WN(t)/[1-Z]Lnsp500(t) –a –d*t = WN(t)/[1-Z] Multiplying through by the difference Multiplying through by the difference

operator, operator, = [1-Z]= [1-Z] [1-Z][Lnsp500(t) –a –d*t] = WN(t-1)[1-Z][Lnsp500(t) –a –d*t] = WN(t-1)

[LnSp500(t) – a –d*t] - [LnSp500(t-1) – a –[LnSp500(t) – a –d*t] - [LnSp500(t-1) – a –d*(t-1)] = WN(t)d*(t-1)] = WN(t)

Lnsp500(t) = d + WN(t)Lnsp500(t) = d + WN(t)

104

So the fractional change in the total return So the fractional change in the total return to the S&P 500 is drift, d, plus white noiseto the S&P 500 is drift, d, plus white noise

More generally, More generally, y(t) = a + d*t + {1/[1-Z]}*WN(t)y(t) = a + d*t + {1/[1-Z]}*WN(t)[y(t) –a –d*t] = {1/[1-Z]}*WN(t)[y(t) –a –d*t] = {1/[1-Z]}*WN(t)[y(t) –a –d*t]- [y(t-1) –a –d*(t-1)] = WN(t)[y(t) –a –d*t]- [y(t-1) –a –d*(t-1)] = WN(t)[y(t) –a –d*t]= [y(t-1) –a –d*(t-1)] + WN(t)[y(t) –a –d*t]= [y(t-1) –a –d*(t-1)] + WN(t)Versus the possibility of an ARONE:Versus the possibility of an ARONE:

105

[y(t) –a –d*t]=b*[y(t-1)–a–d*(t-1)]+WN(t)[y(t) –a –d*t]=b*[y(t-1)–a–d*(t-1)]+WN(t) Y(t) = a + d*t + b*[y(t-1)–a–d*(t-1)]+WN(t)Y(t) = a + d*t + b*[y(t-1)–a–d*(t-1)]+WN(t) Or y(t) = [a*(1-b)+b*d]+[d*(1-b)]*t+b*y(t-1) Or y(t) = [a*(1-b)+b*d]+[d*(1-b)]*t+b*y(t-1)

+wn(t)+wn(t) Subtracting y(t-1) from both sides’Subtracting y(t-1) from both sides’ y(t) = [a*(1-b)+b*d] + [d*(1-b)]*t + (b-1)*y(t-1) y(t) = [a*(1-b)+b*d] + [d*(1-b)]*t + (b-1)*y(t-1)

+wn(t)+wn(t) So the coefficient on y(t-1) is once again So the coefficient on y(t-1) is once again

interpreted as b-1, and we can test the null that interpreted as b-1, and we can test the null that this is zero against the alternative it is this is zero against the alternative it is significantly negative. Note that we specify the significantly negative. Note that we specify the equation with both a constant, equation with both a constant,

[a*(1-b)+b*d] and a trend [d*(1-b)]*t [a*(1-b)+b*d] and a trend [d*(1-b)]*t

106Part IV. Dickey Fuller Tests: Part IV. Dickey Fuller Tests: TrendTrend

107

ExampleExample

Lnsp500(t) from Lab 2Lnsp500(t) from Lab 2

108

109

110

111