Berenberg Specialty Chemicals & Food Ingredients...

46

Public Patrick Jany, CFO 30 September 2014 Berenberg Specialty Chemicals & Food Ingredients Conference LONDON, 30 SEPTEMBER 2014

-

Upload

truongcong -

Category

Documents

-

view

219 -

download

1

Transcript of Berenberg Specialty Chemicals & Food Ingredients...

Public

Patrick Jany, CFO30 September 2014

Berenberg Specialty Chemicals & Food Ingredients ConferenceLONDON, 30 SEPTEMBER 2014

Public

Patrick Jany, CFO30 September 2014

Strategy and goals

Patrick Jany, CFO, 30 September 2014

PROFITABLE GROWTHPROFITABLE GROWTH

Continuous improvement

Clariant’s roadmap to increased performance

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London3

THREE PHASES OF STRATEGY IMPLEMENTATION SINCE 2009

2009 2010 2011 2012 2013 2014 2015

Comprehensive restructuring

Clariant Excellence (CLNX) for continuous improvement

* before exceptional items

Increase Profitability

5 PILLARS STRATEGY

1

Foster Innovation and R&D

2

Intensify Growth

4

Reposition Portfolio

5

Add value with Sustainability

3

TARGETS− Sales growth > global GDP

growth (approx. 5%)

− EBITDA* margin 16-19%

− Above-average peer group return on invested capital (ROIC)

Patrick Jany, CFO, 30 September 2014

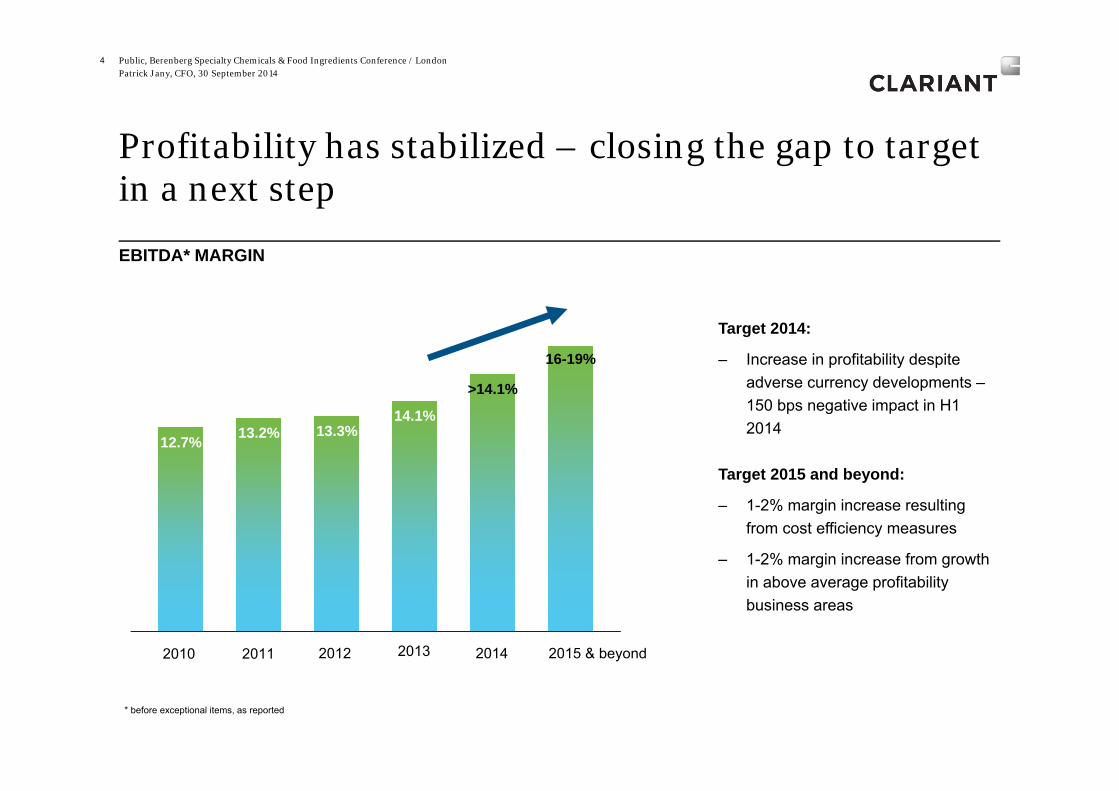

12.7% 13.2% 13.3%14.1%

>14.1%

16-19%

4

2012 2013 2014 2015 & beyond2011

* before exceptional items, as reported

EBITDA* MARGIN

2010

Profitability has stabilized – closing the gap to target in a next step

Target 2014:

– Increase in profitability despite adverse currency developments –150 bps negative impact in H1 2014

Target 2015 and beyond:

– 1-2% margin increase resulting from cost efficiency measures

– 1-2% margin increase from growth in above average profitability business areas

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Public

Patrick Jany, CFO30 September 2014

Business Areas

Patrick Jany, CFO, 30 September 2014

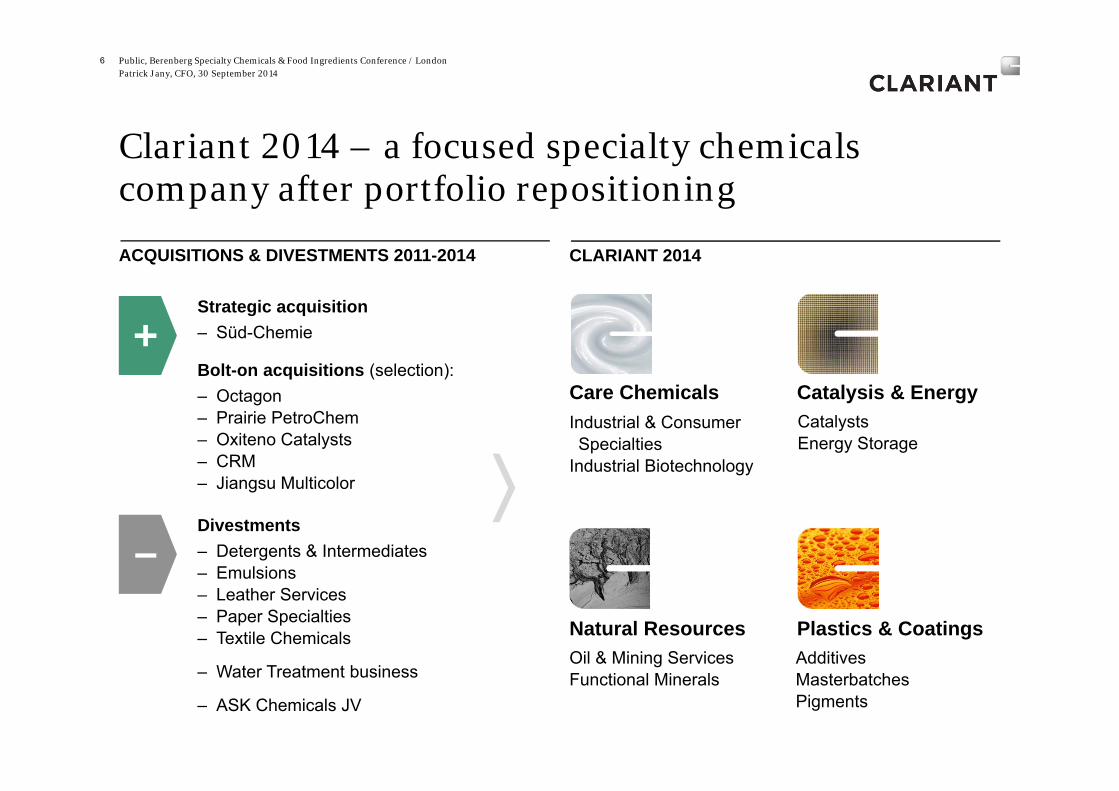

Clariant 2014 – a focused specialty chemicals company after portfolio repositioning

Strategic acquisition– Süd-Chemie

Bolt-on acquisitions (selection):– Octagon– Prairie PetroChem– Oxiteno Catalysts– CRM– Jiangsu Multicolor

6

Divestments– Detergents & Intermediates– Emulsions– Leather Services– Paper Specialties– Textile Chemicals

– Water Treatment business

– ASK Chemicals JV

–

Care ChemicalsIndustrial & Consumer Specialties

Industrial Biotechnology

Catalysis & Energy

Natural ResourcesOil & Mining Services Functional Minerals

Plastics & CoatingsAdditivesMasterbatchesPigments

CLARIANT 2014

+

CatalystsEnergy Storage

ACQUISITIONS & DIVESTMENTS 2011-2014

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

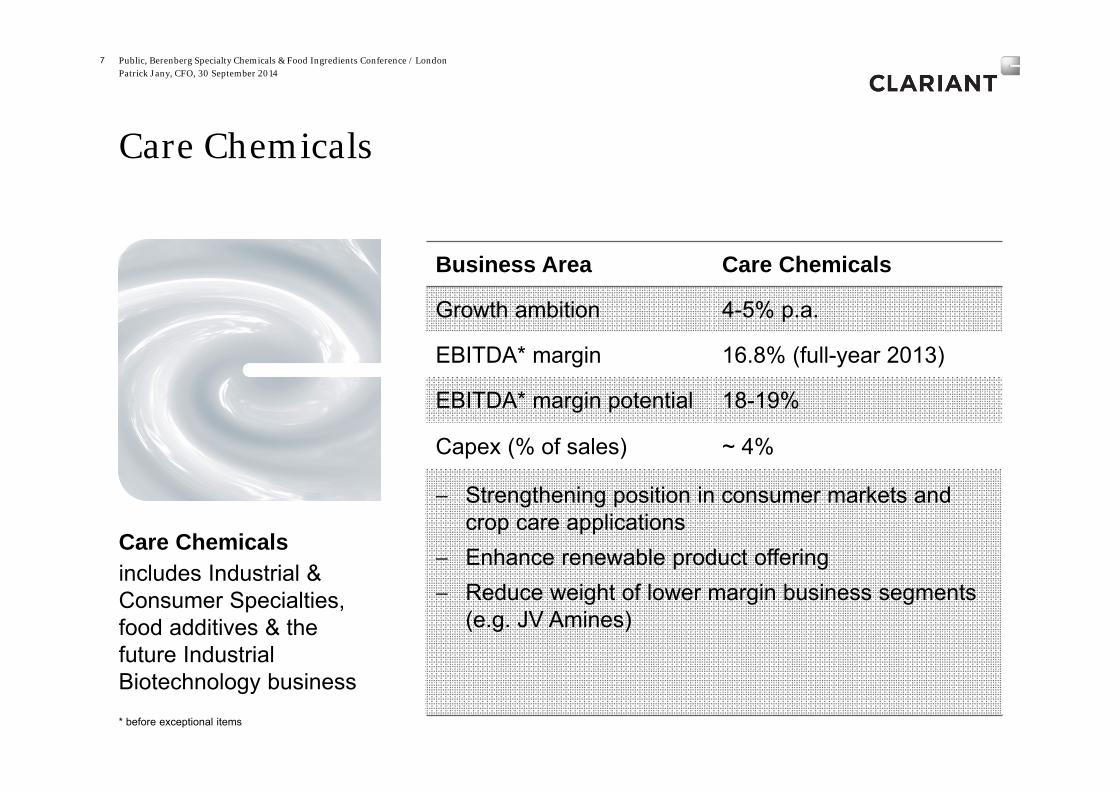

Care Chemicals

Business Area Care Chemicals

Growth ambition 4-5% p.a.

EBITDA* margin 16.8% (full-year 2013)

EBITDA* margin potential 18-19%

Capex (% of sales) ~ 4%

− Strengthening position in consumer markets and crop care applications

− Enhance renewable product offering− Reduce weight of lower margin business segments

(e.g. JV Amines)

7

* before exceptional items

Care Chemicalsincludes Industrial & Consumer Specialties, food additives & the future Industrial Biotechnology business

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

Catalysis & Energy

8

Business Area Catalysis & Energy

Growth ambition 6-7% p.a.

EBITDA* margin 22.3% (full-year 2013)

EBITDA* margin potential 24-26%

Capex (% of sales) ~ 6% of sales

− Strengthen position in various product segments via organic growth and innovation (Catofin for propylene/butylene production, OleMax®, selective hydrogenation catalyst, catalysts for PP production)

− achieve break-even in Li-battery materials and accelerate market penetration

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

* before exceptional items

Catalysis & Energyincludes Catalysts and Energy Storage businesses

Patrick Jany, CFO, 30 September 2014

Natural Resources

9

Business Area Natural Resources

Growth ambition 6-7% p.a

EBITDA* margin 15.2% (full-year 2013)

EBITDA* margin potential 15-17%

Capex (% of sales) 3-4%

− Grow with megatrends e.g. deep-water, EOR or Unconventional Oil and leverage structure

− Grow in North America− Expand in core Floating expertise in Mining Services − Improve low margin Functional Mineral businesses

(Europe, water)

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

* before exceptional items

Natural Resourcesincludes Oil & Mining Services and Functional Minerals businesses

Patrick Jany, CFO, 30 September 2014

Plastics & Coatings

10

Business Area Plastics & Coatings

Growth ambition Global GDP

EBITDA* margin 14.1% (full-year 2013)

EBITDA* margin potential 16-19%

Capex (% of sales) 3-4%

− Above average growth in emerging markets and end-user segments in Pigments

− Reduce dependency of Masterbatches and Pigments on Europe

− Broaden market presence in flame retardants

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

* before exceptional items

Plastics & Coatingsincludes Additives, Pigments and Masterbatchesbusinesses

Public

Patrick Jany, CFO30 September 2014

Performance, Growth, Innovation

Patrick Jany, CFO, 30 September 2014

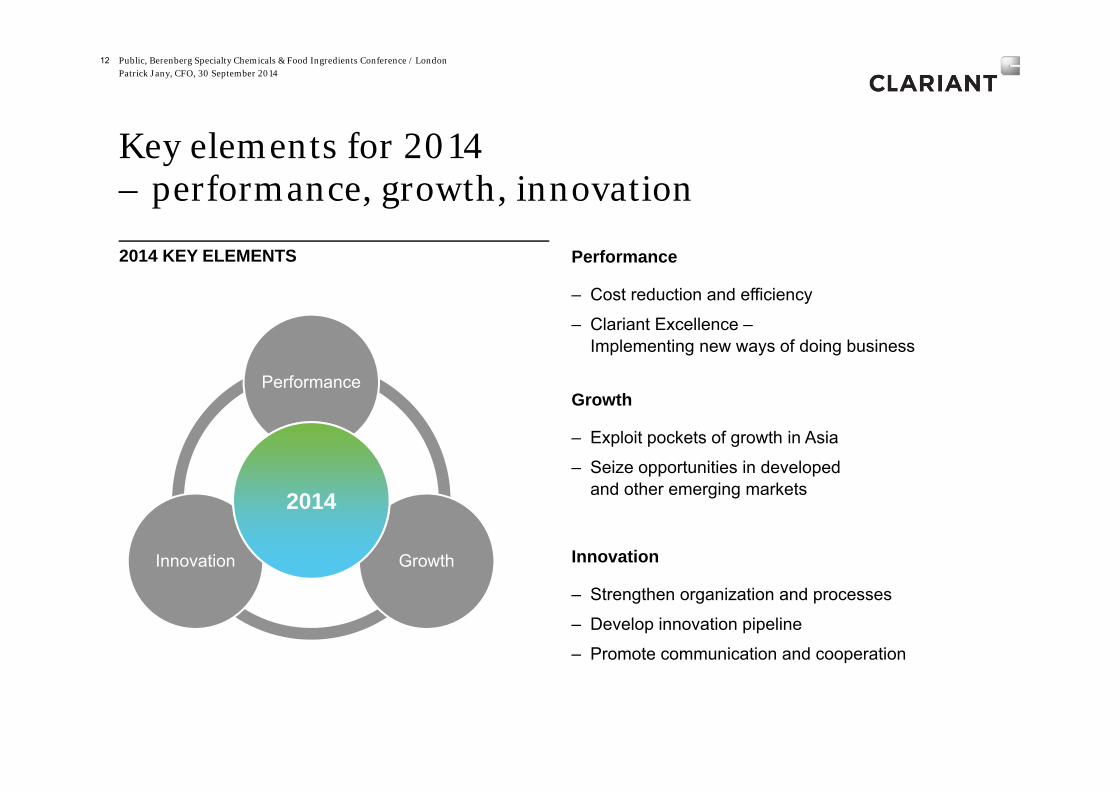

Key elements for 2014 – performance, growth, innovation

12

GrowthInnovation

Performance

2014

Performance

– Cost reduction and efficiency

– Clariant Excellence –Implementing new ways of doing business

Growth

– Exploit pockets of growth in Asia

– Seize opportunities in developed and other emerging markets

Innovation

– Strengthen organization and processes

– Develop innovation pipeline

– Promote communication and cooperation

2014 KEY ELEMENTS

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

Performance – higher profitability expected from cost efficiency and growth investments

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London13

– Cost discipline across the company

– Efficient delivery of business services

– Avoiding remnant costs from divestments

– Investments into innovation and capexprojects

Clariant Excellence initiative:

Connecting the dots – operational improvements by systematically linking all Functional Excellence Programs (Innovation, Commercial and Operational Excellence)

Intesifiy Lean

Operational Excellence Commercial Excellence Innovation Excellence

Explore growth

Accelerate business transformation

12

3

KEY METRICS IMPROVED

Patrick Jany, CFO, 30 September 2014

Growth – differentiated business steering: investment geared towards attractive markets …

14

COMPETITIVE POSITION% Share of revenues 2013

INDUSTRY ATTRACTIVENESS

Harvest

Watch List Improve

Grow39%

6%

34%

21%

25% of 2014 investments*

52% of 2014 investments*

23% of 2014 investments*

* Distribution of growth capex 2014E

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Focus investments on key growth businesses

– Catalysts

– Crop Solutions

– Mining Solutions

– Oil Services

– Personal Care

– Bio-based Chemicals

Patrick Jany, CFO, 30 September 2014

… and growth regions

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London15

62% of investments in emerging markets and North America in 2014 vs. 36% in 2013

Patrick Jany, CFO, 30 September 2014

Growth – Major investment projects coming on stream in the next 1-2 years

– Focused investments on growth areas and niches to avoid overcapacities

16

PROJECT BUSINESS LOCATION INVESTMENT (M CHF)

ON STREAM

Polypropylene Catalyst production Catalysts Louisville (KY), USA > 100 2015

Glucamide production Consumer Care Gendorf, Germany 25-50 2015

Industrial Home Care expansion Ind. & Cons. Spec. Clear Lake, USA 25-50 2015

Licocene Performance Polymer Additives Höchst, Germany < 25 2016

Industrial Home Care expansion Ind. & Cons. Spec. Dayabay, China < 25 2016

High performance pigments Pigments Zhenjiang, China 25-50 2016

Additives project Additives Zhenjiang, China 25-50 2016

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

Innovation and R&D for profitable growth

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London17

950People in R&D (end of 2013)

12Global R&D Centers

>7 000Patents

3.3%of Group sales 2013

>50Technical Application Centersaround the world

>130Scientific collaborations

Innovation figures Megatrends as drivers for innovation

ENVIRONMENTPROTECTION

GLOBALIZATION & URBANIZATION

RESOURCES & ENERGY

Patrick Jany, CFO, 30 September 2014

Innovation focuses on attractive segments linked to megatrends

18 Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

ATTRACTIVE MARKET SEGMENTS

Shale Oil & GasBio-based Chemicals

Functional Packaging

Oil Production and Mining

Coal-to-Gas/Chemicals

Nutrition & Health

Public

Patrick Jany, CFO30 September 2014

Financial Targets

Patrick Jany, CFO, 30 September 2014

Priority on cash generation and a conservative financing policy

Solid cash profile and increased focus on cash generation:

– in 2014 through CHF 200-250 million cash proceeds from disposals

– 2014/15 through improved profitability and cash focused incentives

– 2015 onwards through high-margin innovation driven growth

20

0 0

0.30 0.33 0.36

2009 2010 2011 2012 2013

SOLID MATURITY PROFILE* – POTENTIAL TO REDUCE DEBTin CHF million

ESTABLISHING A TRACK RECORDDividend per share (CHF)

820

20099

249 284174

605

324150

8

16 16

12

266

13 7

2 12

2

0100200300400500600700800900

Cash* 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

DerivativesUncommitted & other loans / NWC facilitiesLong-term loansCertificate of IndebtednessEUR BondCHF BondCash*

Liquidity Maturities of Financial Debt

* including near cash assets and financial instruments with positive fair values reported under other current assets, status end of June 2014

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

Delivering on the next performance steps and preparing for sustainable value creation

– Profitability increase – implementation of business-specific strategies, cost efficiency

– Focus on cash generation: significantly improved free cash flow in 2015

– Long-term, conservative financing policy allows financial flexibility

– Financial flexibility – basis for investments into growth i.e. innovation, growth opportunities, bolt-on acquisitions

– Based on improved profitability, solid cash generation, and a shortened balance sheet, focus will shift to sustainable ROIC-improvement

21

PROFITABLE GROWTH

EBITDA improvement

2011 2012 2013 2014 2015

ROIC improvementFree cash flow generation

2016

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Public

Patrick Jany, CFO30 September 2014

First Half-Year 2014

Patrick Jany, CFO, 30 September 201423 Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

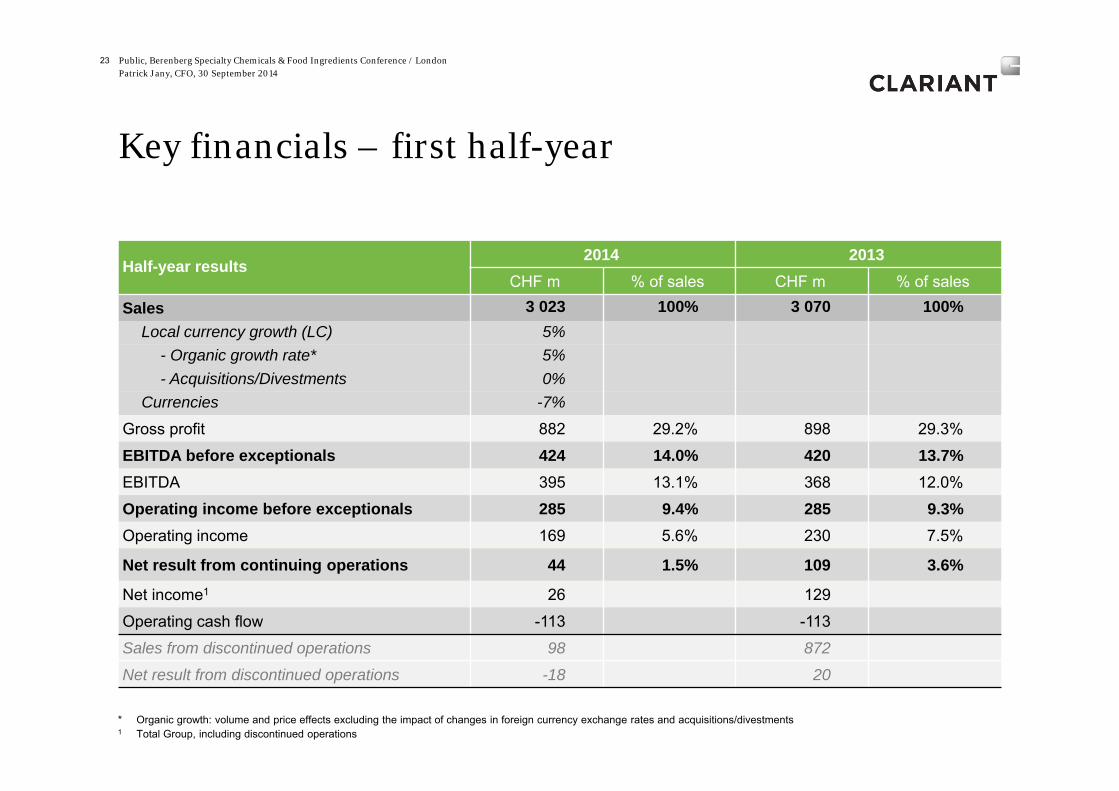

Key financials – first half-year

Half-year results2014 2013

CHF m % of sales CHF m % of sales

Sales 3 023 100% 3 070 100%Local currency growth (LC) 5%

- Organic growth rate* 5%- Acquisitions/Divestments 0%

Currencies -7%

Gross profit 882 29.2% 898 29.3%

EBITDA before exceptionals 424 14.0% 420 13.7%EBITDA 395 13.1% 368 12.0%

Operating income before exceptionals 285 9.4% 285 9.3%Operating income 169 5.6% 230 7.5%

Net result from continuing operations 44 1.5% 109 3.6%

Net income1 26 129

Operating cash flow -113 -113

Sales from discontinued operations 98 872

Net result from discontinued operations -18 20

* Organic growth: volume and price effects excluding the impact of changes in foreign currency exchange rates and acquisitions/divestments1 Total Group, including discontinued operations

Patrick Jany, CFO, 30 September 2014

Sales in CHF m

H1 2014

Change (LC)

H12013

315 316

24 Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Business Area performance – first half-year

Sales in CHF m

H1 2014

Change (LC)

H12013

775 811

Sales in CHF m

H1 2014

Change (LC)

H12013

621 634

EBITDA bef. exc. in CHF m

H1 2014

Change (LC)

H12013

12215.7%

13817.0%

EBITDA bef. exc. in CHF m

H1 2014

Change (LC)

H12013

8613.8%

7111.2%

Care Chemicals

Natural Resources

EBITDA bef. exc. in CHF m

H1 2014

Change (LC)

H12013

7925.1%

7022.2%

Catalysis & Energy

+2% +23%

Sales in CHF m

H1 2014

Change (LC)

H12013

1 312 1 309

EBITDA bef. exc. in CHF m

H1 2014

Change (LC)

H12013

19114.6%

19114.6%

Plastics & Coatings

–5%

+6% +6%+8%

+6%

+36%

Patrick Jany, CFO, 30 September 2014

First Half-Year – solidity in challenging market conditions

● Significant sales growth in the first six months- Robust sales growth in all four Business Areas

- Mixed and volatile development across portfolio and regions, driven by regional- and segment-specific factors

- Ability to absorb ongoing market volatility over the course of the quarters

● Improved level of performance- Margin improvement based on strong market positions and efficiency gains

- Soft economic conditions in Europe continue to impact profitability

- Progress in profitability masked by negative currency developments and seasonal effects

● Foster growth and manage efficiency – targeting the next level- Cost discipline across the company

- Major investment projects approved, operation starting in 2015/2016

- Promote innovation and commercial orientation

25 Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

Sales growth driven by volumes – headwinds from FX in the first half-year

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London26

Sales mix H1 2014 Sales growth in local currencies

Volume4%

Price1% Acq./Div.

0%

Currency-7%

Sales H1 2014: CHF 3 023 m

Latin America448 / +14%

Europe1173 / -1%

North America 485 / +3% Asia / Pacific

679 / +10%

Middle East& Africa 238 / +12%

Germany 431 / −3%

China 253/ +22%

Brazil 194 / +4%

all figures continuing operations

Emerging Markets Mature Markets

− Good LC sales growth driven by 4% higher volumes and 1% higher prices, overcompensated by unfavorable currency developments

− Double-digit sales growth in the emerging markets, weaker growth in Brazil

− Persistent weakness in Europe; Germany and Eastern Europe softened

Public

Patrick Jany, CFO30 September 2014

Second Quarter 2014

Patrick Jany, CFO, 30 September 201428 Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Key financials – second quarter

Second Quarter2014 2013

CHF m % of sales CHF m % of sales

Sales 1 531 100% 1 544 100%Local currency growth (LC) 6%

- Organic growth rate* 6%- Acquisitions/Divestments 0%

Currencies -7%

Gross profit 451 29.5% 453 29.3%

EBITDA before exceptionals 214 14.0% 211 13.7%EBITDA 197 12.9% 180 11.7%

Operating income before exceptionals 145 9.5% 144 9.3%Operating income 128 8.4% 111 7.2%

Net result from continuing operations 83 5.4% 71 4.6%

Net income1 74 79

Operating cash flow -62 -41

Sales from discontinued operations 32 451

Net result from discontinued operations -9 8

* Organic growth: volume and price effects excluding the impact of changes in foreign currency exchange rates and acquisitions/divestments1 Total Group, including discontinued operations

Patrick Jany, CFO, 30 September 2014

Sales in CHF m

Q2 2014

Change (LC)

Q22013

195 197

29 Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Business Area performance – second quarter

Sales in CHF m

Q2 2014

Change (LC)

Q22013

359 370

Sales in CHF m

Q2 2014

Change (LC)

Q22013

307 309

EBITDA bef. exc. in CHF m

Q2 2014

Change (LC)

Q22013

5515.3%

5915.9%

EBITDA bef. exc. in CHF m

Q2 2014

Change (LC)

Q22013

3912.7%

299.4%

Care Chemicals

Natural Resources

EBITDA bef. exc. in CHF m

Q2 2014

Change (LC)

Q22013

5528.2%

5125.9%

Catalysis & Energy

3% 14%

Sales in CHF m

Q2 2014

Change (LC)

Q22013

670 668

EBITDA bef. exc. in CHF m

Q2 2014

Change (LC)

Q22013

9414.0%

9614.4%

Plastics & Coatings

– 1%

5%9%

5%

55% 6%

Patrick Jany, CFO, 30 September 2014

Sales growth driven by volumes – headwinds from FX

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London30

Sales mix Q2 2014 Sales growth in local currenciesVolume

5%

Price1% Acq./Div.

0%

Currency-7%

− Organic sales growth in LC driven by 5% higher volumes and 1% higher prices

− Double-digit sales growth in the emerging markets China, MEA and LATAM; solid growth in North America

− Brazil with further slowing growth (+5% in Q1)

− Europe slightly weaker, due to negative growth in Germany and Eastern Europe

Sales Q2 2014: CHF 1 531 m

Latin America240 / +13%

Europe565 / –1%

North America 229 / +6% Asia / Pacific

365 / +9%

Middle East& Africa 132 / +15%

Germany 204 / −2%

China 144/ +16%

Brazil 103/ +3%

all figures continuing operations

Emerging Markets Mature Markets

Patrick Jany, CFO, 30 September 2014

LC sales growth EBITDA* margin

Care Chemicals• Industrial Applications and Consumer Care businesses achieved

solid growth, the latter driven by continuing double-digit growth in the Crop Solution segment

• EBITDA* margin at 15.3% compared to 15.9% due to an unfavorable currency effect, weak market prices for mono-ethylene-glycol (MEG) and lower de-icing sales

+3% 15.3%

Catalysis & Energy• Particularly good sales growth in the Middle East

• Strong sales growth in the Petrochemicals business; beneficial re-fill cycle

• Sales in Energy Storage significantly above prior-year level

• EBITDA* margin increased due to lower production costs and less dilution from Energy Storage

+5% 28.2%

31

Strong margins in Catalysis & Energy, solid sales growth in Care Chemicals

* before exceptional items

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

LC sales growth EBITDA* margin

Natural Resources• Oil & Mining Services business with double-digit sales growth

• Mining Services reported good double-digit sales growth: market share gains, mainly in Latin America and Australia

• EBITDA* margin increased significantly on higher volumes and sales prices, a lower cost base and a better product mix, more than offsetting a significant currency impact

+9% 12.7%

Plastics & Coatings• All three businesses Pigments, Masterbatches, and Additives

contributed to growth

• Heterogeneous regional development from business to business

• EBITDA* margin below previous-year level as higher volumes could not compensate for unfavorable currency developments

+6% 14.0%

32

EBITDA* margin improvement in Natural Resources, volumes recovered in Plastics & Coatings

* before exceptional items

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Public

Patrick Jany, CFO30 September 2014

Summary & Outlook

Patrick Jany, CFO, 30 September 2014

Summary

34

Achievements

Priorities 2014 –moving along the profitable growth path

− Performance: more profitable portfolio and improved operational efficiency

− Innovation: 260 innovation projects with more than CHF 1.6 billion sales potential in total

− Sustainability introduced as 5th strategic pillar – essential to achieve company targets

− Increase profitability – on the basis of a competitive cost position

− Improve free cash flow generation – manage EBITDA conversion into free cash flow

− Intensify organic growth – investments in short-term business opportunities and developing the long-term innovation pipeline

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

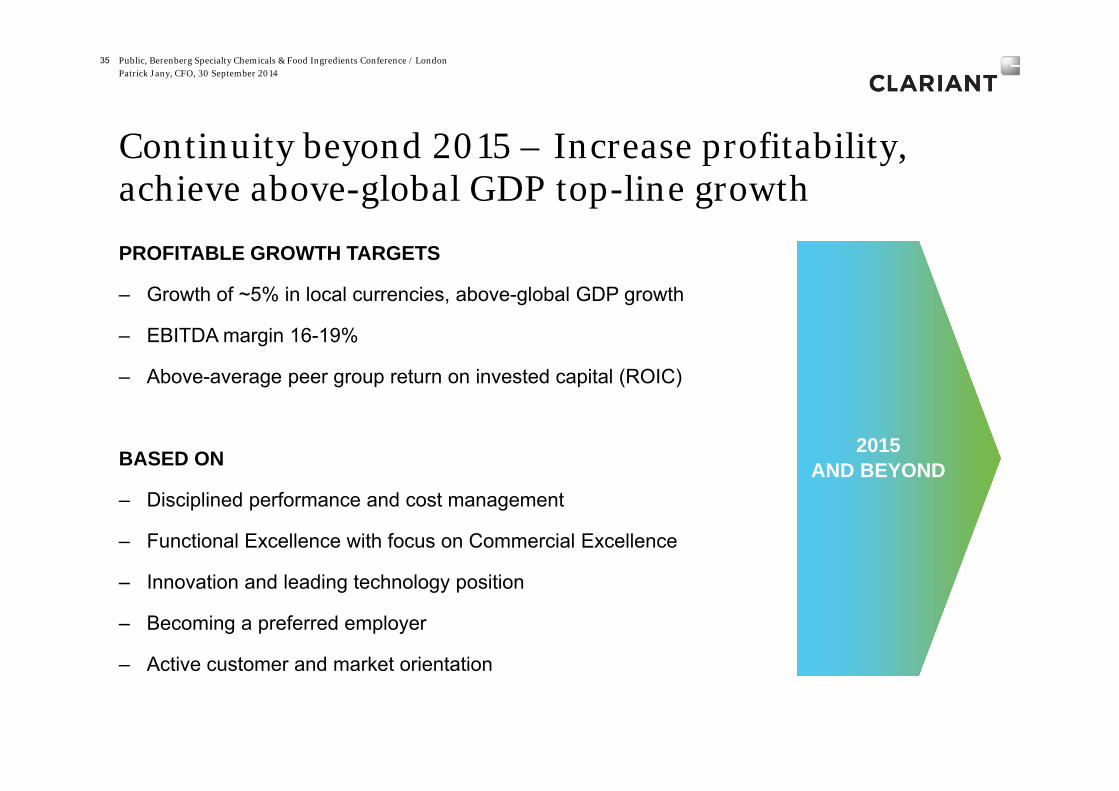

Continuity beyond 2015 – Increase profitability, achieve above-global GDP top-line growth

35

PROFITABLE GROWTH TARGETS

– Growth of ~5% in local currencies, above-global GDP growth

– EBITDA margin 16-19%

– Above-average peer group return on invested capital (ROIC)

BASED ON

– Disciplined performance and cost management

– Functional Excellence with focus on Commercial Excellence

– Innovation and leading technology position

– Becoming a preferred employer

– Active customer and market orientation

2015 AND BEYOND

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

Clariant’s macroeconomic view

− A challenging business environment similar to the first half-year, characterized by a heterogeneous development in the different regions

− Favorable but mixed emerging market economies, with volatile currencies

− Europe flat, moderate growth in the United States

Outlook 2014 – Clariant will further progress in sales and profitability

− Focus on profitably growing the four Business Areas, on cost efficiency and on promoting innovation

− Full-year 2014: low to mid single-digit sales growth in local currencies and an EBITDA margin before exceptional items above full-year 2013

2015 and beyond

− Target to reach the top tier of the specialty chemicals industry by 2015, i.e. an EBITDA margin before exceptional items range of 16% to 19% and a return on invested capital (ROIC) above peer group average

36

Challenging trading conditions to persist through the remainder of the year

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Public

Patrick Jany, CFO30 September 2014

Backup Slides

Patrick Jany, CFO, 30 September 201438

Sales and cost structure*

Global cost distribution in %

* These distributions represent an approximation to total cash in- and out-flows and are closely linked to transaction exposures for H1 2014. Including discontinued operations

EUR49%

USD31%

CHF4%

JPY2%

Emerging markets

14%

EUR43%

USD37%

CHF0% JPY

3%

Emerging markets

17%

Global sales distribution in %

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

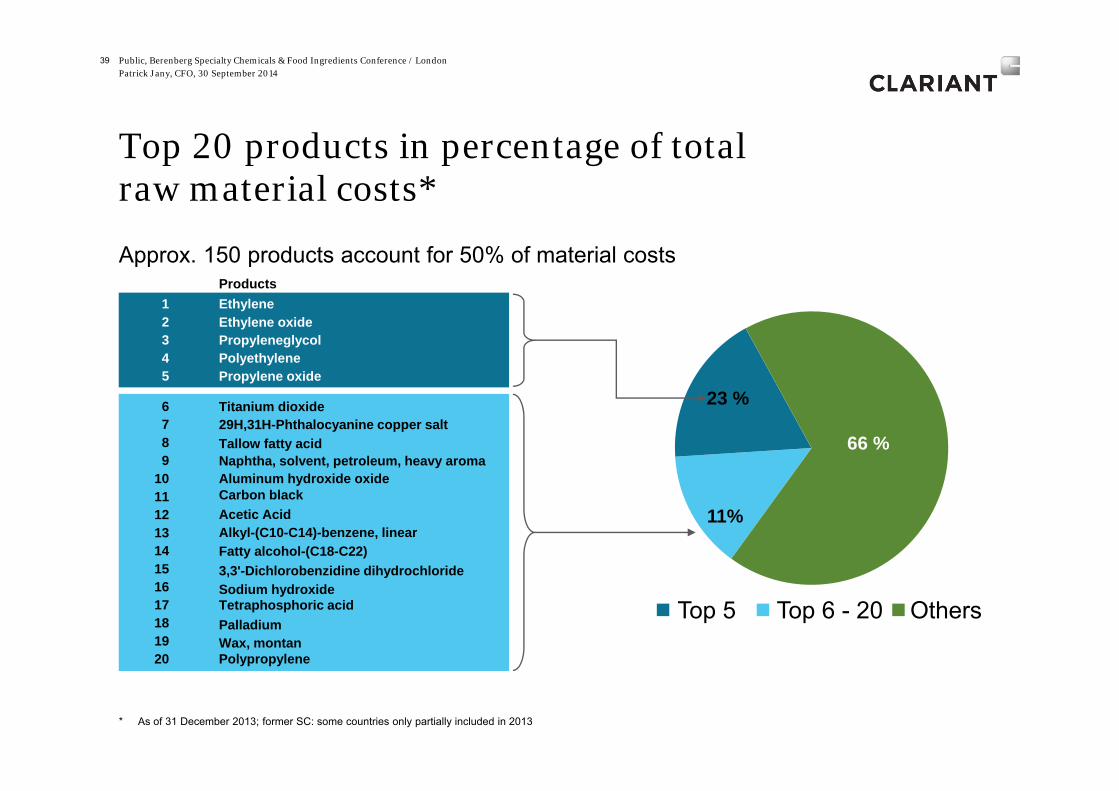

Approx. 150 products account for 50% of material costs

39

Top 20 products in percentage of total raw material costs*

11%

23 %

1 Ethylene2 Ethylene oxide3 Propyleneglycol4 Polyethylene5 Propylene oxide

6 Titanium dioxide7

Tallow fatty acid8

3,3'-Dichlorobenzidine dihydrochloride

9

29H,31H-Phthalocyanine copper salt

10 Aluminum hydroxide oxide11

Naphtha, solvent, petroleum, heavy aroma

12Alkyl-(C10-C14)-benzene, linear13

Wax, montan

14

Carbon black

15

Acetic Acid

16 Sodium hydroxide17 Tetraphosphoric acid18 Palladium19

Fatty alcohol-(C18-C22)

20 Polypropylene

66 %

Top 5 Top 6 - 20 Others

Products

* As of 31 December 2013; former SC: some countries only partially included in 2013

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

Regional distribution of Clariant’s shareholder baseas of 31 December 2013

40

Switzerland 38%

Germany 17%

United Kingdom 9%

Rest of Europe 10%

Europe Total 74%

Americas Total 7%

Rest of the World 2%

Unidentified Shareholdings 17%

Switzerland38%

Germany17%

United Kingdom9%

Rest of Europe10%

Americas7%

Rest of the World2%

Unidentified Shareholdings

17%

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

,1.3

,2.1

,2.3

,3.0

,3.6

,3.8

,5.3

,5.9

,6.0

,6.3

,6.3

,6.7

,6.7

,7.0

,7.1

,7.1

,7.2

,7.4

,7.7

,7.8

,8.1

,8.2

,9.0

,9.5

9.5

,9.6

,9.7

,9.7

,10.

2,1

0.6

,11.

2,1

1.7

,11.

7,1

2.3

,12.

6,1

2.7

,12.

9,1

2.9

,13.

0,1

3.3

,14.

1,1

4.5

,15.

1,1

6.2

,16.

3,1

6.6

,17.

2,2

0.4

,23.

8,2

9.3

41

Improved ROIC in relation to peers

ROIC 2013 by peer (in %)

2013 Median 9.5%

Clariant ROIC2013: 9.5%

Source: Annual Reports; Corporate Controlling2012: Clariant ROIC: 8.5%, Median 10.5%, WACC 8.2%

Cro

daEM

SLy

onde

ll Ba

sell

Hon

eyw

ell

Alb

emar

leIC

LC

elan

ese

East

man

Ferr

oS

herw

in W

illiam

sPP

GVa

lspa

rH

B F

ulle

rD

u P

ont

John

son

Mat

they

Cyt

ecBA

SFS

ymris

ePo

lyon

eE

voni

kA

ltana

Axi

all

Um

icor

eW

est L

ake

Che

mAk

zo

Cla

riant

LG C

hem

ical

sR

ockw

ood

Om

nova

AZ

Ele

ctro

nics

Bras

kem

Shin

etsu

Dow

Bor

ealis

DS

MH

unts

man

nS

chul

man

Sol

vay

Ashl

and

Lonz

aC

hem

tura

Cab

otH

& R

DIC

Kem

iraW

acke

rK

rato

nLa

nxes

sM

itsub

ishi

Mits

ui

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

9.7%

7.5%

12.7%13.2% 13.5%

14.1%

6%

8%

10%

12%

14%

16%

18%

20%

2008 2009 2010 2011 2012 2013

42

Historic EBITDA* Development

* before exceptional items, as reported

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

30 October 2014 Nine Months 2014 Results

18 February 2015 Full-Year 2014 Results

31 March 2015 Annual General Meeting

43

Calendar of upcoming corporate events

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

IR contacts

44

Dr. Ulrich SteinerHead of Investor Relations

Phone +41 (0) 61 469 67 45Mobile +41 (0) 79 297 27 07E-mail [email protected]

Dr. Siegfried SchwirzerDeputy Head Investor Relations

Phone +41 (0) 61 469 67 49Mobile +41 (0) 79 718 45 98 E-mail [email protected]

Marco FerraroInvestor Relations Officer

Phone +41 (0) 61 469 64 11Mobile +41 (0) 79 931 03 98E-mail [email protected]

Edith Schwab

Phone +41 (0) 61 469 67 48E-mail [email protected]

Mirjam Grieder

Phone +41 (0) 61 469 67 66E-mail [email protected]

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London

Patrick Jany, CFO, 30 September 2014

Our Publications

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London45

iPad App: www.clariant.com/IRapp Factbook: www.clariant.com/factbook

Patrick Jany, CFO, 30 September 2014

This presentation contains certain statements that are neither reported financial results nor other historical information. This presentation also includes forward-looking statements.

Because these forward-looking statements are subject to risks and uncertainties, actual future results may differ materially from those expressed in or implied by the statements. Many of these risks and uncertainties relate to factors that are beyond Clariant’s ability to control or estimate precisely, such as future market conditions, currency fluctuations, the behavior of other market participants, the actions of governmental regulators and other risk factors such as: the timing and strength of new product offerings; pricing strategies of competitors; the Company's ability to continue to receive adequate products from its vendors on acceptable terms, or at all, and to continue to obtain sufficient financing to meet its liquidity needs; and changes in the political, social and regulatory framework in which the Company operates or in economic or technological trends or conditions, including currency fluctuations, inflation and consumer confidence, on a global, regional or national basis.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this document. Clariant does not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date of these materials.

46

Disclaimer

Public, Berenberg Specialty Chemicals & Food Ingredients Conference / London