Mining machinery - Berenberg

38

BERENBERG EQUITY RESEARCH Mining machinery Process plant exposure preferable to mining operations Alexander Virgo Analyst +44 20 3207 7856 [email protected] Chris Armstrong Specialist Sales +44 20 3207 7809 [email protected] Kaj Alftan Specialist Sales +44 20 3207 7879 [email protected] 2 July 2013 Capital Goods & Industrial Engineering

Transcript of Mining machinery - Berenberg

BERENBERG EQUITY RESEARCH

Mining machinery

Process plant exposure preferable to mining operations

Alexander Virgo

Analyst

+44 20 3207 7856

Chris Armstrong

Specialist Sales

+44 20 3207 7809

Kaj Alftan

Specialist Sales

+44 20 3207 7879

2 July 2013

Capital Goods & Industrial Engineering

What is Berenberg THOUGHT LEADERSHIP?

Berenberg’s analysts are recognised by investors and by corporates for their in-depth research into the industries they cover.

Our THOUGHT LEADERSHIP brand will highlight the deep-dive fundamental industry research that we feel is most important to informing our forecasts and ratings.

For our disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG) and our disclaimer please see the end of this document. Please note that the use of this research report is subject to the conditions and restrictions set forth in the disclosures and the disclaimer at the end of this document.

Mining machinery Capital Goods & Industrial Engineering

Table of contents

Process plant exposure preferable to mining operations 4

The changing face of mining investment 7

Focus on brownfield investment favours mining equipment 11

Opex budgets favour process plant exposure 16

Equipment characteristics: consumables vs spares and service 20

Assessing portfolio exposure 25

Atlas Copco: Good aftermarket exposure, but fool’s gold? 29

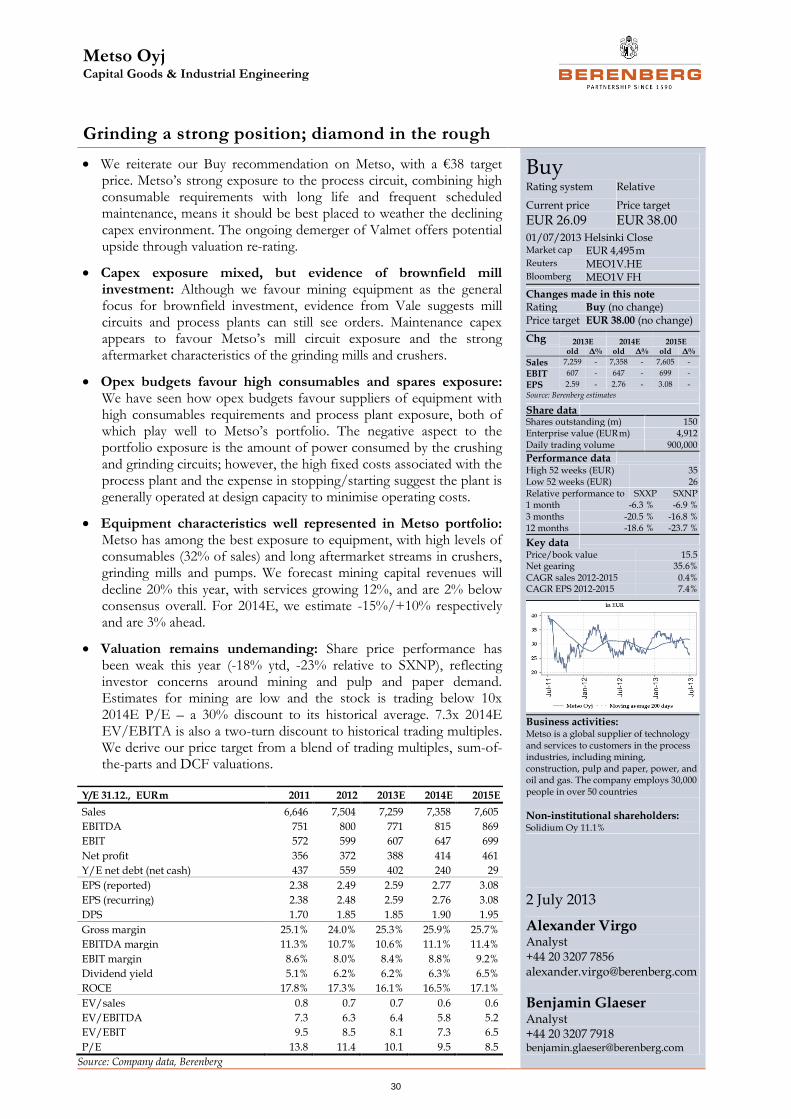

Metso: Grinding a strong position; diamond in the rough 30

Sandvik: Underperformance belies breadth of portfolio 31

Weir: Strongest aftermarket revenue exposure 32

Disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG) 33

Contacts: Investment Banking 37

Mining machinery Capital Goods & Industrial Engineering

4

Process plant exposure preferable to mining operations

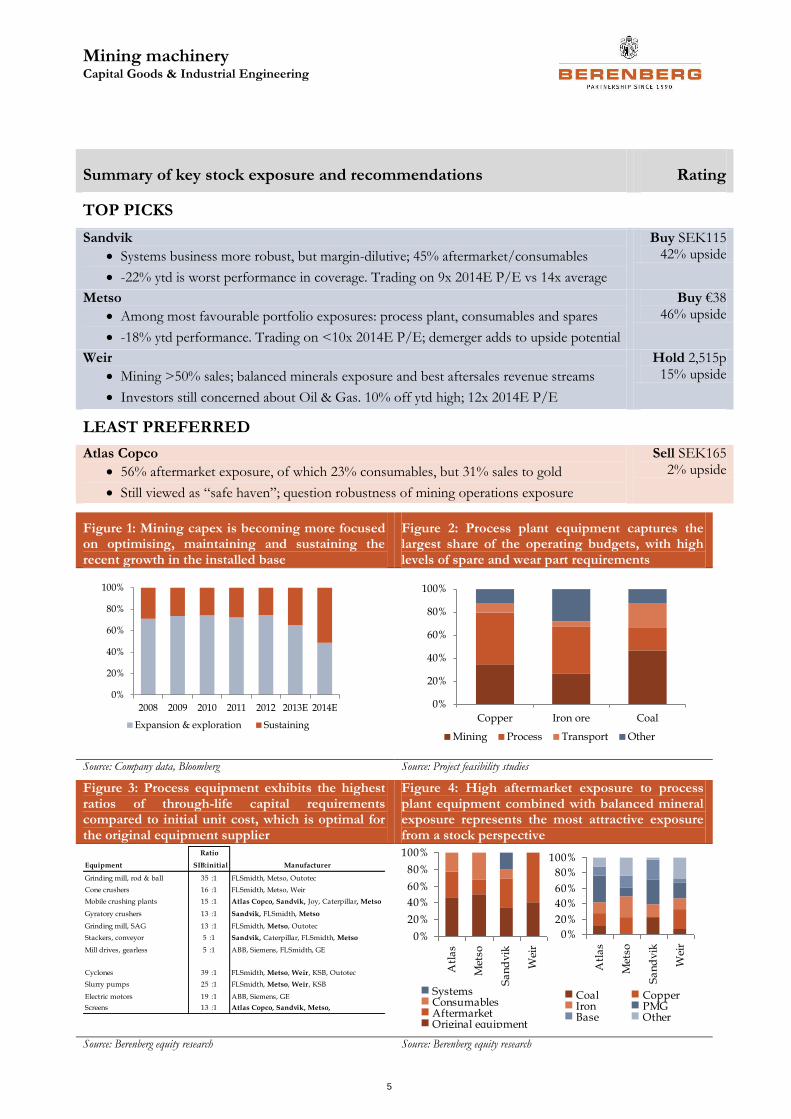

Investors should seek exposure to mining equipment suppliers with ●high exposure to the fast-growing maintenance capex budgets of the miners. Process plant equipment offers more high-margin aftermarket business and greater stability than mining operations. In this light, we reiterate our Buy recommendations on Metso and Sandvik and highlight Weir as favourably exposed. We retain concerns over investors’ faith in the robustness of Atlas Copco’s business. Analysis of feasibility studies and equipment operating costs supports our preference for process plant exposure.

Mining capex emphasis shifting fast to maintenance: ●Maintenance capex has grown at a 29% CAGR since 2009 and is expected to grow at a 27% CAGR 2012-14E as capex budgets are refocused towards maintenance capex and away from expansion projects. Expansion capex is expected to decline 23% and 38% in 2013E and 2014E. Greenfield investment over the last 5-8 years has seen significant growth in the installed base of equipment, which miners now need to optimise and maintain, to the benefit of both revenue growth and profitability of the original equipment suppliers.

Shift from greenfield to brownfield expansion more beneficial ●for mining equipment suppliers: The likes of Sandvik and Atlas Copco can still see original equipment orders as brownfield expansion projects generally focus on extending mining operations for existing processing plants. Despite brownfield investment typically being 20-25% of the greenfield capex required for equivalent mine production, mining equipment procurement can be similar in absolute terms, reflecting no need for new infrastructure or process plant.

Opex budgets favour process plant exposure: High utilisation rates ●(90%+) and consequent requirements for equipment availability (95%+) mean the process plant generally offers more favourable aftermarket revenue streams for equipment suppliers – Metso and Weir are best positioned. Process plant equipment on average requires 2x the level of wear parts of mining equipment in normal production, while spare parts (ie maintenance) are also typically 2x mining equipment requirements through the life of the mine. Low headcount and high fixed costs of process plants make mining operations the first point of focus for miners in terms of cost savings, suggesting Atlas Copco’s portfolio could actually be at greater risk in the near term.

Preference for process equipment exposure supported by ●analysis of equipment operating characteristics: Equipment with the highest ratio of stay-in-business capital (defined as spare parts, wear parts and replacement capex) to initial capex is the most attractive from a product portfolio standpoint. Pumps, cyclones and grinding mills exhibit the best characteristics, favouring Metso and Weir; Sandvik, too, though to a lesser degree.

Portfolio assessment points to Weir and Metso as best positioned ●in terms of high-margin aftermarket business and exposure to process plant equipment across balanced minerals exposure. Sandvik benefits from some exposure to process equipment, while its Systems business offers stability, albeit at lower margins. Atlas Copco has the highest product exposure to mining operations, particularly gold, but benefits from high aftermarket exposure and a broad non-mining portfolio.

Atlas Copco AB

Sell Current price

SEK 162.50 Price target

SEK 165.00 01/07/2013 Stockholm Close

Metso Oyj

Buy Current price

EUR 26.09 Price target

EUR 38.00 01/07/2013 Helsinki Close

Sandvik AB

Buy Current price

SEK 80.90 Price target

SEK 115.00 01/07/2013 Stockholm Close

Weir Group plc

Hold Current price

GBp 2,187 Price target

GBp 2,515 01/07/2013 London Close

Rating system: Relative

2 July 2013

Alexander Virgo Analyst +44 20 3207 7856 [email protected]

Chris Armstrong Specialist Sales +44 20 3207 7809 [email protected]

Mining machinery Capital Goods & Industrial Engineering

5

Summary of key stock exposure and recommendations Rating

TOP PICKS

Sandvik

Systems business more robust, but margin-dilutive; 45% aftermarket/consumables

-22% ytd is worst performance in coverage. Trading on 9x 2014E P/E vs 14x average

Buy SEK115 42% upside

Metso

Among most favourable portfolio exposures: process plant, consumables and spares

-18% ytd performance. Trading on <10x 2014E P/E; demerger adds to upside potential

Buy €38 46% upside

Weir

Mining >50% sales; balanced minerals exposure and best aftersales revenue streams

Investors still concerned about Oil & Gas. 10% off ytd high; 12x 2014E P/E

Hold 2,515p 15% upside

LEAST PREFERRED

Atlas Copco

56% aftermarket exposure, of which 23% consumables, but 31% sales to gold

Still viewed as “safe haven”; question robustness of mining operations exposure

Sell SEK165 2% upside

Figure 1: Mining capex is becoming more focused on optimising, maintaining and sustaining the recent growth in the installed base

Figure 2: Process plant equipment captures the largest share of the operating budgets, with high levels of spare and wear part requirements

Source: Company data, Bloomberg Source: Project feasibility studies

Figure 3: Process equipment exhibits the highest ratios of through-life capital requirements compared to initial unit cost, which is optimal for the original equipment supplier

Figure 4: High aftermarket exposure to process plant equipment combined with balanced mineral exposure represents the most attractive exposure from a stock perspective

Source: Berenberg equity research Source: Berenberg equity research

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013E 2014E

Expansion & exploration Sustaining

0%

20%

40%

60%

80%

100%

Copper Iron ore Coal

Mining Process Transport Other

Ratio

Equipment SIB:initial Manufacturer

Grinding mill, rod & ball 35 :1 FLSmidth, Metso, Outotec

Cone crushers 16 :1 FLSmidth, Metso, Weir

Mobile crushing plants 15 :1 Atlas Copco, Sandvik, Joy, Caterpillar, Metso

Gyratory crushers 13 :1 Sandvik, FLSmidth, Metso

Grinding mill, SAG 13 :1 FLSmidth, Metso, Outotec

Stackers, conveyor 5 :1 Sandvik, Caterpillar, FLSmidth, Metso

Mill drives, gearless 5 :1 ABB, Siemens, FLSmidth, GE

Cyclones 39 :1 FLSmidth, Metso, Weir, KSB, Outotec

Slurry pumps 25 :1 FLSmidth, Metso, Weir, KSB

Electric motors 19 :1 ABB, Siemens, GE

Screens 13 :1 Atlas Copco, Sandvik, Metso,

0%

20%

40%

60%

80%

100%

Atl

as

Met

so

Sa

nd

vik

Wei

r

SystemsConsumablesAftermarketOriginal equipment

0%

20%

40%

60%

80%

100%

Atl

as

Met

so

Sa

nd

vik

Wei

r

Coal CopperIron PMGBase Other

Mining machinery Capital Goods & Industrial Engineering

6

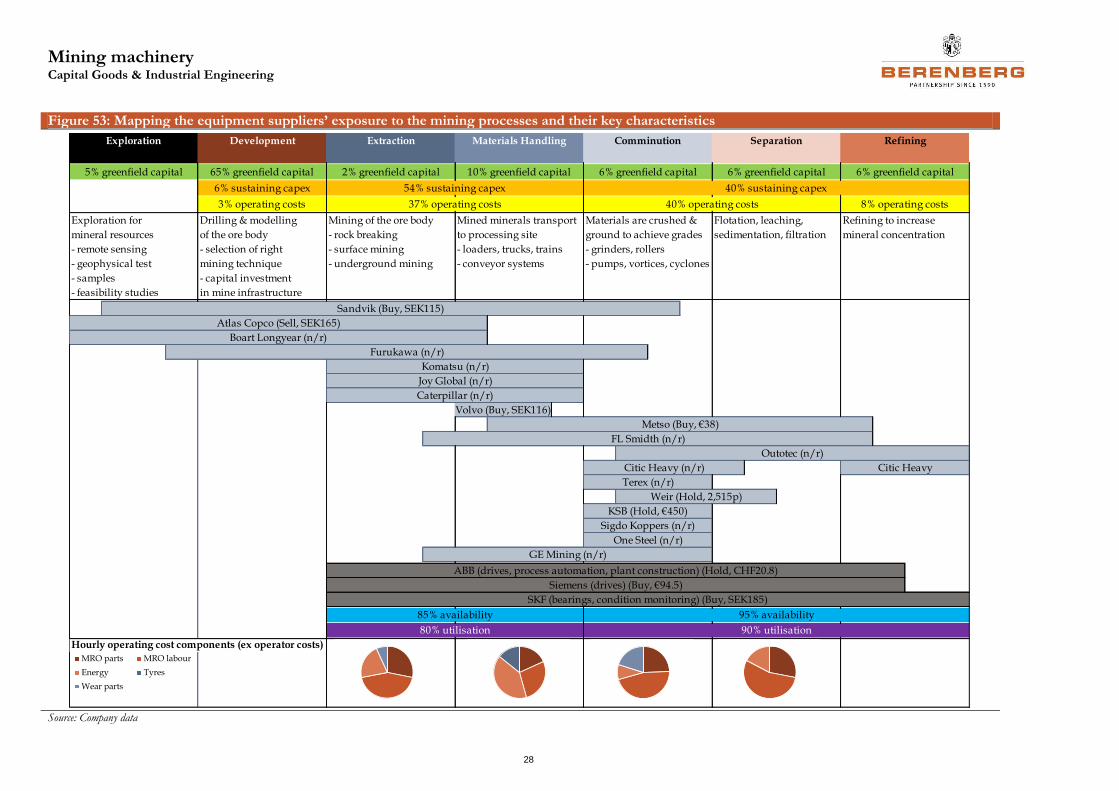

Figure 5: Mapping the equipment suppliers’ exposure to the mining processes and their key characteristics

Source: Company data; for disclosures, historical price targets and rating changes pertaining to the companies included in this table, please visit our disclosure listing page on our website at: https://www.berenberg.de/cgi-bin/compliance.cgi?rm=comp_start&lang=englisch

Exploration Development Extraction Materials Handling Comminution Separation Refining

5% greenfield capital 65% greenfield capital 2% greenfield capital 10% greenfield capital 6% greenfield capital 6% greenfield capital 6% greenfield capital

6% sustaining capex 54% sustaining capex 40% sustaining capex

3% operating costs 37% operating costs 40% operating costs 8% operating costs

Exploration for Drilling & modelling Mining of the ore body Mined minerals transport Materials are crushed & Flotation, leaching, Refining to increase

mineral resources of the ore body - rock breaking to processing site ground to achieve grades sedimentation, filtration mineral concentration

- remote sensing - selection of right - surface mining - loaders, trucks, trains - grinders, rollers

- geophysical test mining technique - underground mining - conveyor systems - pumps, vortices, cyclones

- samples - capital investment

- feasibility studies in mine infrastructure

Sandvik (Buy, SEK115)

Atlas Copco (Sell, SEK165)

Boart Longyear (n/r)

Furukawa (n/r)

Komatsu (n/r)

Joy Global (n/r)

Caterpillar (n/r)

Volvo (Buy, SEK116)

Metso (Buy, €38)

FL Smidth (n/r)

Outotec (n/r)

Citic Heavy (n/r) Citic Heavy

Terex (n/r)

Weir (Hold, 2,515p)

KSB (Hold, €450)

Sigdo Koppers (n/r)

One Steel (n/r)

GE Mining (n/r)

ABB (drives, process automation, plant construction) (Hold, CHF20.8)

Siemens (drives) (Buy, €94.5)

SKF (bearings, condition monitoring) (Buy, SEK185)

85% availability 95% availability

80% utilisation 90% utilisation

Hourly operating cost components (ex operator costs)

MRO parts MRO labour

Energy Tyres

Wear parts

Mining machinery Capital Goods & Industrial Engineering

7

The changing face of mining investment

Focus on maintenance capex and brownfield expansion

Debottlenecking or expanding existing mining operations is cheaper and more capital-efficient than starting from scratch, and miners’ capex guidance reflects a more cautious approach to capital allocation in the medium term than we have seen since the 2008/09 recovery. Since the middle of 2012, miners have been returning to an enduring theme of asset efficiency and process optimisation – brownfield investment.

Significant headwinds for new orders for equipment suppliers but this is well known

The significant investment made in new mining projects over the last 5-8 years has had a consequent effect on the capital required to sustain that investment, meaning operating budgets and maintenance capital requirements have increased. This should provide a larger addressable wallet for equipment suppliers in terms of aftersales support. Company guidance would suggest maintenance capex growth of 35% and 24% in 2013E and 2014E respectively.

Positive implications for suppliers with high aftermarket exposure and offering ways to improve operational efficiency

Investors have been focused on the end of the mining super-cycle for some time, but expectations are now low in terms of capex development. Consensus is 6-7% below company capex guidance for 2013E/14E, but assuming scepticism is reserved for expansion plans (and maintenance capex guidance is accepted), expectations for expansion capex declines in 2013E and 2014E are more than 20% and 40% respectively.

Consensus expectations for capex growth are already low

Shift from expansion to asset optimisation

With the return of uncertainty to the macro environment, falling commodity prices and questions being raised in the near term around Chinese growth in particular, miners are scaling back expansion plans and focusing on maximising the efficiency of their existing assets. Expansion, where it comes, is being pursued through brownfield investment in existing assets, rather than breaking new ground in greenfield projects. Maintenance – or stay-in-business (SIB) – capex continues to grow, driven in part by the significant investment in expansion and new assets over the last 5-8 years.

Following the huge government stimulus in China in 2010 and the strong rebound in the resources sector, miners returned to significant capital investment (Figure 6). The top five1 alone spent over $165bn of expansionary capex over the 2010-12 period. As the macro environment became more uncertain through 2012 and commodity prices began to fall, questions were raised over the extent of expansion on the supply side. Calls from shareholders for tighter capital management have been backed up with changes in top management at a number of the major miners. Capital allocation has become focused on reducing the operating cost per tonne rather than developing new assets.

Greenfield expansion is expensive: it typically requires significant investment in infrastructure such as roads, railways and ports as well as considerable time spent building and constructing the mine before it can even begin production. Technical

1 BHP Billiton, Rio Tinto, Anglo American, Vale and GlencoreXstrata.

Top 5 miners: expansion capex (US$bn)

Source: Company data inc. guidance

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013E 2014E

Total Anglo American Xstrata

Rio Tinto Vale BHP

Top 5 miners: maintenance capex (US$bn)

Source: Company data inc. guidance

0

5

10

15

20

25

30

35

2008 2009 2010 2011 2012 2013E 2014E

Total Anglo American Xstrata

Rio Tinto Vale BHP

Capex growth expectations (yoy)

Source: Company data inc. guidance

-60%

-40%

-20%

0%

20%

40%

60%

2009 2010 2011 2012 2013E 2014E 2015E

Expansion & exploration Sustaining

Top 5 consensus Global listed capex

Expansion, where it is happening, is being pursued through brownfield projects, while maintenance capex continues to grow, servicing an increased installed base and targeting asset efficiency

Mining machinery Capital Goods & Industrial Engineering

8

reports, pre-feasibility studies, bankable feasibility studies (on the basis of which “go/no-go” decisions are made) and planning/permitting often taken 3-5 years before ground can even be broken on a new mine. It might take another 2-4 years before the first product is shipped from the mine and revenue begins to come in. Brownfield investment is often less than 20% of the costs of a new mine of equivalent capacity.

SIB investment can be made to optimise the method of mining, from investing in new, more efficient drilling, loading and hauling equipment, automating the hauling process (Rio Tinto’s autonomous trucks in the Pilbara save more than AUD100,000 per year, per truck in driver costs – there are over 150 trucks in the system and drivers are typically hired on a 2.25:1 ratio to account for double shifts and changeover efficiency) or shortening the haulage distance (to reduce fuel costs).

On the process side, optimising the crushing system, ensuring correct and efficient screens are in place and improving the wear life of the plant equipment can considerably enhance the throughput of the mill circuit and reduce the cost per tonne. Brownfield and maintenance investment typically sees much quicker payback – often within 12-18 months. Significant recent new mine development has led to an increase in the installed base of equipment and equipment waiting commissioning, suggesting the requirement for SIB capex is higher, and miners’ guidance reflects this shift (Figure 7).

Figure 6: Annual capex – top five miners ($m) Figure 7: Expansion vs maintenance capex

Source: Company data, including guidance Source: Company data, including guidance

The last three years have seen significant increases in expansion capex, from the top five miners (Figure 8) and from the mining industry as a whole. Capex grew at a 30% CAGR from 2009-12, but guidance suggests it is likely to shrink considerably over the next two years. On the maintenance side, growth since 2009 has also been strong (29% CAGR), and is expected to continue to develop over the next two years, reflecting the greater focus on brownfield investment, SIB capex and the larger installed base (Figure 9).

Figure 8: Expansion capex – top five ($bn) Figure 9: Maintenance capex – top five ($bn)

Source: Company data Source: Company data

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2008 2009 2010 2011 2012 2013E 2014E

BHP Vale Rio Tinto Xstrata Anglo American

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013E 2014E

Expansion & exploration Sustaining

0

20

40

60

2008 2009 2010 2011 2012 2013E 2014E

BHP ValeRio Tinto XstrataAnglo American Total

0

10

20

30

40

2008 2009 2010 2011 2012 2013E 2014E

BHP ValeRio Tinto XstrataAnglo American Total

Mining machinery Capital Goods & Industrial Engineering

9

Much of the focus on brownfield investment is a result of the escalation in costs of both starting a new project and operating the assets once they are in place. The cost of new projects combined with the falling commodity prices forces miners to consider new options for capital deployment and they look for the quicker, more certain returns that are available from plant optimisation and operational efficiencies.

Figure 10: Capital intensity ($/t) Figure 11: Mine capital cost escalation (yoy)

Source: Xstrata Source: Xstrata

Consensus expectations have already adjusted

Declines in mining capex have been consensus for some time now, though the magnitude has varied. At the beginning of 2012, consensus expected mining capex to decline by 9% in the year and actually it ended up growing by almost 20%. Expectations for 2013E and 2014E have been for around a 7-8% decline in each year for most of the last 18 months; however, consensus remains, on average, 6-7% below company guidance (top five miners). Assuming the scepticism is connected with expansionary rather than maintenance capex, consensus is already discounting significant declines.

The top five miners currently guide for $72bn capex in 2013E and another $61bn in 2014E, which compares to consensus expectations of $68bn and $56bn respectively (Figure 12). On average, consensus expectations are 6-7% below company guidance for both years, except for Rio Tinto, with 2014E showing a marginally larger differential overall (Figure 13). This suggests the capex of the top five miners will decline by between 17% (company guidance) and 23% (consensus) over the next two years (2014 versus 2012).

Figure 12: Capex guidance vs consensus ($m) Figure 13: Capex guidance vs consensus (%)

Source: Company data, Bloomberg Source: Company data, Bloomberg

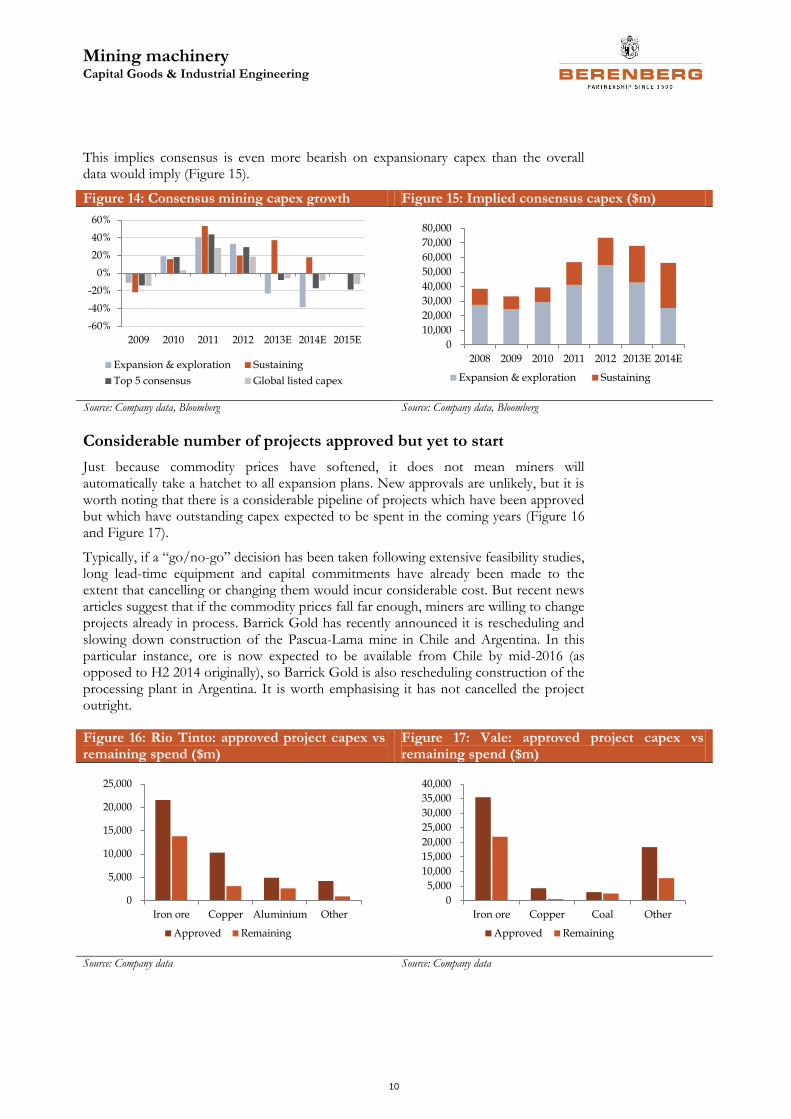

If we look beyond the top five at the broader group of listed companies, consensus expects overall capex to decline 6%/8% in 2013E/14E and 12% in 2015E (Figure 14). The evolution of that expectation has also not changed significantly in the last 12 months, suggesting that consensus is already bearish on expansionary capex.

We do not know the split in consensus expectations between expansion and maintenance capex, but it seems more likely that company guidance on maintenance capex will be taken as accurate, with scepticism largely retained for expansion plans.

Capital intensity - copper 2011 $/t

1985-2011 green & brownfield projects 7,700

2012-2015 greenfield projects in construction 14,970

2016-2020 greenfield unapproved 18,600

Xstrata brownfield 8,920

Xstrata greenfield 13,315 0%

10%

20%

30%

40%

2004 2005 2006 2007 2008 2009 2010 2011

010,00020,00030,00040,00050,00060,00070,00080,000

2013E 2014E 2013E 2014E

Guidance Consensus

BHP Vale Rio Tinto Xstrata Anglo American

-20%

-15%

-10%

-5%

0%

5%

10%

BHP VLE RTO XTA AA Total

2013E 2014E

Mining machinery Capital Goods & Industrial Engineering

10

This implies consensus is even more bearish on expansionary capex than the overall data would imply (Figure 15).

Figure 14: Consensus mining capex growth Figure 15: Implied consensus capex ($m)

Source: Company data, Bloomberg Source: Company data, Bloomberg

Considerable number of projects approved but yet to start

Just because commodity prices have softened, it does not mean miners will automatically take a hatchet to all expansion plans. New approvals are unlikely, but it is worth noting that there is a considerable pipeline of projects which have been approved but which have outstanding capex expected to be spent in the coming years (Figure 16 and Figure 17).

Typically, if a “go/no-go” decision has been taken following extensive feasibility studies, long lead-time equipment and capital commitments have already been made to the extent that cancelling or changing them would incur considerable cost. But recent news articles suggest that if the commodity prices fall far enough, miners are willing to change projects already in process. Barrick Gold has recently announced it is rescheduling and slowing down construction of the Pascua-Lama mine in Chile and Argentina. In this particular instance, ore is now expected to be available from Chile by mid-2016 (as opposed to H2 2014 originally), so Barrick Gold is also rescheduling construction of the processing plant in Argentina. It is worth emphasising it has not cancelled the project outright.

Figure 16: Rio Tinto: approved project capex vs remaining spend ($m)

Figure 17: Vale: approved project capex vs remaining spend ($m)

Source: Company data Source: Company data

-60%

-40%

-20%

0%

20%

40%

60%

2009 2010 2011 2012 2013E 2014E 2015E

Expansion & exploration Sustaining

Top 5 consensus Global listed capex

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2008 2009 2010 2011 2012 2013E 2014E

Expansion & exploration Sustaining

0

5,000

10,000

15,000

20,000

25,000

Iron ore Copper Aluminium Other

Approved Remaining

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Iron ore Copper Coal Other

Approved Remaining

Mining machinery Capital Goods & Industrial Engineering

11

Focus on brownfield investment favours mining equipment

Mining operations often capture more of brownfield investment; maintenance benefits both mining and process

Mining operations (drills, shovels, trucks etc) often account for more of the budget for brownfield investment, when expansion plans are driven by the need to sustain throughput for existing processing plants. Mining operation capex also tends to continue beyond the initial outlay, as truck fleets etc are built up, whereas the process plant is built prior to production commencing.

The current focus on brownfield investment is more likely to favour mining equipment suppliers, particularly hauling and conveying, rather than process equipment suppliers

Moving underground generally requires more mining equipment and infrastructure investment in both greenfield and brownfield projects. If the underground mine is a development of an existing open pit mine site, then the process plant is already in place and virtually all the capital is allocated to mining equipment and bulk material handling systems.

Large-scale brownfield capex can still generate new equipment orders for suppliers such as Atlas Copco, Sandvik and Caterpillar

SIB capex can take a number of forms and appears to focus as much on equipment replacement as it does on operational enhancements. Projects can be very specific (replacement or addition of a ball mill, for example) or focused much more generally on process systems and infrastructure.

Companies that can offer quick payback on upgraded equipment or which can help capture process efficiency savings should benefit from this trend; eg Weir, Metso, ABB

Focus on brownfield changes the dynamics for equipment demand

The nature of brownfield investment, focused on sustaining and developing existing mine sites, means infrastructure and overheads account for less of the budget and more of the capital is focused on equipment, particularly mining equipment.

Figure 18: Greenfield copper investment split Figure 19: Brownfield copper investment split

Source: Project feasibility studies Source: Project feasibility studies

Brownfield capex might be some 20% of the cost of greenfield investment, but the proportion allocated to equipment could be 50% in mining operations and another 20-25% in the mill circuit.

We have examined feasibility studies, which are conducted for up to three years prior to the “go/no-go” decision on a new mining investment, to understand where the capital is

Capex budget: greenfield vs. brownfield

Source: Project feasibility studies

0%

20%

40%

60%

80%

100%

Copper Iron ore Copper

Greenfield BrownfieldContingency Owner costsIndirect costs InfrastructureProcess Mining

Capex budget: greenfield vs. brownfield

Source: Project feasibility studies

0%

20%

40%

60%

80%

100%

Open pit U/ground

Owner costs Indirect costsInfrastructure ProcessMining

Vale 2013 SIB capex composition (US$m)

Source: Company data

0

500

1000

1500

2000

2500

3000

Iron ore Base metals Coal

Other Equipment replacement Ops enhancement

Mining Process Infrastructure

Indirect costs Owner costs Contingency Mining Process Infrastructure Indirect costs

Mining machinery Capital Goods & Industrial Engineering

12

allocated across different types of mine (open pit versus underground), different minerals (copper, iron ore, coal) and different levels of investment (greenfield versus brownfield).

Starting with copper, the difference in scale between greenfield and brownfield investment is clear from the data in Figure 20, and underpins the data displayed in the pie charts in the previous two figures. The annual production intended at each of the three greenfield projects cited here ranges from 300ktpa to 84mtpa (thousand or million tonnes per annum), and initial investment is between $5.5bn and $6.5bn. By contrast, brownfield investment in the two projects examined came to less than $1bn. What is most striking from a mining equipment supplier’s perspective (such as that of Atlas Copco or Sandvik) is that the capex budget allocated to mining equipment in brownfield projects can in some cases exceed a greenfield opportunity (compare the first US project to the Alaskan and South American projects in Figure 20).

On the process equipment side, the proportion of the capital outlay allocated does not appear to change significantly (about 25%), which means brownfield investment does not necessarily favour process equipment suppliers. However, miners do not need to undertake feasibility studies on the same scale to add a grinding circuit, optimise a process plant or invest in concentration plants as they would when looking to break new ground and develop new mining operations.

Figure 20: Sample copper mine capex budgets ($m)

Source: Project feasibility studies

Looking at iron ore projects, a similar picture emerges to that described above for copper. Mining equipment can account for almost double the proportion of the budget for brownfield iron ore projects (Figure 22) compared to greenfield (Figure 21). On the process side, again, proportions remain relatively similar. A process plant is designed for a certain level of throughput, and brownfield investment typically involves expanding the mining operations to sustain that level of design throughput for the existing plant.

Only if the expansion plans are likely to significantly improve the output of the mine would the miner consider adding to the mill circuit. Instead, brownfield investment from a process standpoint focuses more on plant optimisation, ensuring equipment is up to date, well maintained and operating efficiently. This capital is smaller and frequently related to the operating cost budget, which we will discuss in greater detail in the next section.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Mongolia Alaska S America US US

Greenfield BrownfieldContingency Owner costsIndirect costs InfrastructureProcess Mining

Despite a smaller overall capital outlay, more of a brownfield project’s capital can be allocated to mining equipment, favouring suppliers such as Caterpillar, Komatsu, Atlas Copco and Sandvik

2012 capex by mineral

Sources: McKinsey

Mining machinery Capital Goods & Industrial Engineering

13

Figure 21: Greenfield iron ore investment split Figure 22: Brownfield iron ore investment split

Source: Project feasibility studies Source: Project feasibility studies

The iron ore projects for which we found details were smaller in scale than the copper projects examined earlier, but still provide a good cross-section (although we could not find sufficient details on brownfield projects). From a greenfield perspective, the process plant for iron ore projects accounts for a much larger share than mine equipment (compared to copper) in the projects we examined. The intended production of each project ranged from 10mtpa to 68mtpa (Figure 23). Mining equipment budgets appear largely to vary in proportion to the scale of the project.

Figure 23: Sample iron ore mine capex budgets ($m)

Source: Project feasibility studies

Moving underground certainly favours extraction and haulage

Coal was the only mineral for which we were able to obtain good comparable details for both open pit and underground mining projects. Moving mining operations underground is intuitively a more expensive business than open cast mining, and the project data we found supports this intuition. In fact, for the projects we looked at, the mining equipment share of the capex budget essentially doubled with underground mining (Figure 24).

Looking at brownfield investment for underground coal operations shows mining equipment accounting for up to 50% of the capital outlay, with process plant investment accounting for 20-25% (Figure 25). The reasons for this have been discussed with respect to iron ore and copper, but the additional factor is that coal tends to be much harder and more abrasive to mine, so the equipment required at the mine face has to be able to cope with the harsher environment, which inevitably means greater expense per unit.

Mining Process Infrastructure

Indirect costs Owner costs Contingency

Mining Process Infrastructure

Indirect costs Contingency

0

500

1,000

1,500

2,000

2,500

3,000

3,500

S Africa Finland Australia Canada

GreenfieldContingency Owner costsIndirect costs InfrastructureProcess Mining

Mining machinery Capital Goods & Industrial Engineering

14

Figure 24: Greenfield coal investment split Figure 25: Brownfield underground coal investment split

Source: Project feasibility studies Source: Project feasibility studies

Mining equipment capex is concentrated on trucks

The bulk of the cost in mining operations lies with the loading and haulage system, whether that is traditional shovel and truck operations or in-pit crushing and conveying (IPCC). As can be seen from examining the equipment procurement list for the two largest projects we examined – the new copper mine at Oyu Tolgoi in Mongolia and the potential Pebble mine, also copper, in Alaska (Figure 26) – over 50% of the capex budget for mining equipment lies with trucks, and another 10-20% with shovels. A good proportion of the balance lies with ancillary trucks, excavators, dozers and graders, with perhaps 5% associated with drills. This mix is relatively consistent if we examine brownfield expansion projects as well.

Figure 26: Composition of mining equipment spend at two open cast copper mines ($m)

Figure 27: Composition of process plant procurement at Oyu Tolgoi and Pebble ($m)

Source: Company data, feasibility studies Source: Company data, feasibility studies

Looking at the composition of the process plant at both projects shows a much more fragmented bill of materials (Figure 27). Typically, the cost of building a new process plant is about equally weighted between procurement, steel and labour. The individual equipment – such as crushers, mills, pumps and drives – can still be expensive (primary crushers or semi-autogenous grinding (SAG) mills can cost $15m or more) but there are fewer of them; or in the case of pumps and drives, there can be high volumes, but prices are below $1m each.

The initial outlay on mining truck fleets may be relatively limited (to, say, 10-12 trucks) and the fleet is built up over time, whereas the process plant has to be finished and commissioned before product can be shipped from the mine. This means that mining equipment capex can be extended over a longer time period and delivery schedules can

0%

20%

40%

60%

80%

100%

Open pit U/ground

Mining Process Infrastructure

Indirect costs Owner costs

Mining Process Infrastructure

Indirect costs Owner costs

0

100

200

300

400

500

Oyu Tolgoi Pebble

Drills Shovels

Trucks Ancillary trucks

Excavators Other

0

200

400

600

Oyu Tolgoi Pebble

Crushers Mills

Flotation circuit Pumps & cyclones

Drives Other

Mining equipment capital outlay is dominated by trucks and loading equipment – favouring Caterpillar, Komatsu and Joy Global

Process plant bill of materials is much more fragmented and the more expensive items are fewer in volume

Mining machinery Capital Goods & Industrial Engineering

15

provide good visibility for the equipment suppliers. Process equipment is generally associated with longer lead times and takes longer to deliver and install.

Because of the size of the outlay on trucks and the cost of transporting the ore to the mill circuit, the option of IPCC systems is being considered. This generally includes a semi-mobile crusher and then long conveyor belt systems to transport the crushed ore to the mill circuit; however, IPCC systems tend to be suitable only if the crusher can stay in place for extended periods of time – moving it and the associated conveyor belts is expensive (can be over 30% of initial capex).

Sustaining capex focuses on both equipment replacement and operations enhancement

Examining specific examples of sustaining capex shows that the replacement of equipment and operational enhancement are the two main drivers, both of which offer scope for equipment suppliers to generate orders in a market where overall capex is declining.

Vale’s main initiatives for its sustaining capex in 2013 have been summarised in Figure 28. The company is expecting to spend $2.4bn on projects in iron ore, of which $600m is allocated to operational enhancements and c$1bn is allocated to equipment replacement, or 25% and 40% of the total respectively. For base metals, Vale expects to spend $1.4bn in sustaining capex this year, of which 35% is on operational enhancements and 15% on equipment replacement. Clearly, the various allocations are driven by the needs of the assets in operation in those minerals, but it is helpful to think about the magnitudes of investment that will be undertaken even in a declining capex environment.

Freeport McMoRan (FCX) has been even more specific about its brownfield development projects (Figure 29), illustrating how the lines are somewhat blurred between brownfield and maintenance, but the combined investment of c$7bn is expected to increase production by over 40% (from 2012) by 2016. The sulphur dioxide furnace rebuild would fall more into maintenance or SIB capex, but is expected to increase annual copper production at the Tenke mine by 50% as it also includes the addition of a second sulphuric acid plant. The Cerro Verde project earthworks are a more typical brownfield investment, focused on adding 600m lbs (from c400m lbs currently) to annual production by developing new open pit mining operations for the existing plant.

Figure 28: Vale: focus of sustaining capex ($m) Figure 29: Freeport McMoRan brownfield investment to 2016 ($m)

Source: Company data Source: Company data, feasibility studies

The last brownfield investment project for FCX flies in the face of the brownfield project analysis conducted earlier in the section as it is totally focused on adding a new ball mill and flotation circuit to the existing plant at the Morenci mine, which will increase production by c50%.

0

500

1000

1500

2000

2500

3000

Iron ore Base metals Coal

Ops enhancement Equipment replacement Other

0

1000

2000

3000

4000

5000

SulphurDioxide furnace

Earthworks Ball mill

To date Outstanding

Mining machinery Capital Goods & Industrial Engineering

16

Opex budgets favour process plant exposure

Operating budgets favour suppliers exposed to the process plant, due to high utilisation rates and availability needs

Although the proportion of operating costs associated with mining operations and processing appear similar, the reality is that fuel and labour account for the greatest portions of the operating budget. Longer life, greater utilisation rates and higher availability requirements make process equipment more appealing in terms of both consumables and spares exposure.

This favours Weir and Metso over Atlas Copco and Sandvik within our coverage universe, with their greater exposure to the mill circuit

Mining operation costs are driven by fuel, labour and a concentration of large equipment with high initial costs. Draglines, shovels and trucks have high initial costs and expensive annual maintenance, while the consumables component associated with drilling and loading is relatively low.

High headcount (equipment operators) and intensive maintenance schedules offer scope for cost savings. Consumables are a relatively low proportion of the budget, which means price sensitivity should be low

Process costs are characterised by high energy demands but maintenance-intensive equipment that is required to run at 95% availability to sustain 90% utilisation rates. The expense incurred in not running at design capacity or switching on and off tends to mean cost savings are sought elsewhere.

Underlines the strong positioning of the portfolios of Weir and Metso

Energy costs mask true share of operating costs; availability is key

Although clearly the mineral, the grade, the mining system, the location and many other factors affect the set-up of a mine, the operating budgets for mining operations and process operations appear relatively similar (Figure 30), except when mining operations are underground. However, energy and labour (operation and maintenance) account for more of the costs of mining operations than they do for processing.

Figure 30: Typical operating budget split (open cast mines)

Figure 31: Operating cost per tonne ($/t) and proportion of life of mine costs (copper mine)

Source: Project feasibility studies Source: Project feasibility studies

High utilisation rates in the process plant, which demand higher equipment availability, drive a different mix of operating costs within the process plant. With coal, the harder

Typical operating costs by process

Source: Project feasibility studies

0%

20%

40%

60%

80%

100%

Copper Iron ore Coal

Mining Process Transport Other

Mining process: operating cost breakdown

Source: Project feasibility studies

0%

20%

40%

60%

80%

100%

Copper Coal

Hauling Haulage support

Loading Blasting

Drilling Other

Processing: operating cost breakdown

Source: Project feasibility studies

0%

20%

40%

60%

80%

100%

Copper Iron ore Coal

Energy Labour

Consumables - mech Consumables - chem

Repairs Other

0%

20%

40%

60%

80%

100%

Copper Iron ore Coal

Mining Process Transport Other

0%5%10%15%20%25%30%35%40%

0

5

10

15

20

25

30

Mining machinery Capital Goods & Industrial Engineering

17

and more abrasive environment means the mining process accounts for a greater proportion of the costs, while for copper and iron ore the material needs to be processed (rather than washed, as with coal) and refined before it can be shipped, meaning the process costs are a greater proportion of the operating budget. Labour and transport of the product to port clearly also command a reasonable share of the operating costs.

Looking in more detail at some of the components of the Pumpkin Hollow copper project in the US, which has both open pit and underground operations, the cost of underground mining is some 5-6x more than open pit, though in this case the lower volumes mined underground mean the latter accounts for a lower proportion of costs than the open pit operations through the life of mine (LoM; see Figure 31). On a per tonne basis, therefore, the process and mining costs are still relatively similar.

One critical element where the processing and mining do differ, though, is in utilisation and availability. The former represents the utilisation rates of the equipment – essentially how many hours a year it operates. Typically, mining equipment operates on a 12-hour shift basis, with two shifts a day, and for 350-360 days a year, to account for holidays, weather and scheduled maintenance, which implies utilisation rates of c80%. A process plant operates 365 days a year, 24 hours a day, and utilisation rates are typically 90%. Availability is defined as whether a piece of equipment is serviceable and able to be used. The higher utilisation requirements in process plants mean the equipment has to run at c95% availability, while mining equipment tends to run at availability rates of c85%. The expense of unscheduled failure in the process plant (where the feed is relatively constant and the rest of the plant has to stop) is much greater than if, perhaps, a drill or truck is non-operational for slightly longer than anticipated. The stockpile of ore-to-be-processed provides a buffer between the mining operations and the process plant.

Intuitively, this means process plant equipment is more critical from a maintenance and uptime standpoint, which should favour the equipment suppliers most exposed to it, such as Weir and Metso.

Opex budgets of mining operations dominated by fuel and labour

The most striking (and again, somewhat intuitive) conclusion from examining the detailed cost components of the operating budgets is that energy is the largest cost, whether in the form of electrical drives to run the shovels or diesel to run the trucks. Spares (6% of costs) and maintenance (25%) are clearly important components of mining operating costs, but labour and other overheads also account for meaningful proportions (Figure 32). Our research suggested that there is scope to lengthen maintenance schedules, shorten shifts and cut headcount in mining operations as a way of mitigating price declines in the refined product. This has been confirmed by recent announcements in the Australian mining sector, with GlencoreXstrata, Peabody and Aquila announcing a combined 1,000 job cuts as well as production reductions in the last couple of weeks.

Looking at the mining operations in a different way, and breaking the costs down by the different operations (Figure 33), we can see that haulage (ie trucks) accounts for the largest share of the costs, driven by the fuel required. Drilling (4-5% of operating costs) is a relatively small proportion, though clearly has a high proportion of consumables associated with it.

Mining equipment life, as we shall see in the next section in more detail, varies between 12,000 and 72,000 hours (or c2-6 years) before full rebuild is required, though this depends on the individual mine characteristics, abrasiveness and hardness etc of the ore. Scheduled maintenance typically happens once a year, where the equipment may be out of use for up to a couple of days. Mines employ maintenance personnel specialising in some of the more complex equipment, typically employing 1-2 maintenance engineers

Mining machinery Capital Goods & Industrial Engineering

18

for every 2-3 operators (Pebble plans for 1:1 operators:mechanics in open pit operations), as the labour content of the maintenance costs of these machines is also a large component of the operating costs (Figure 32).

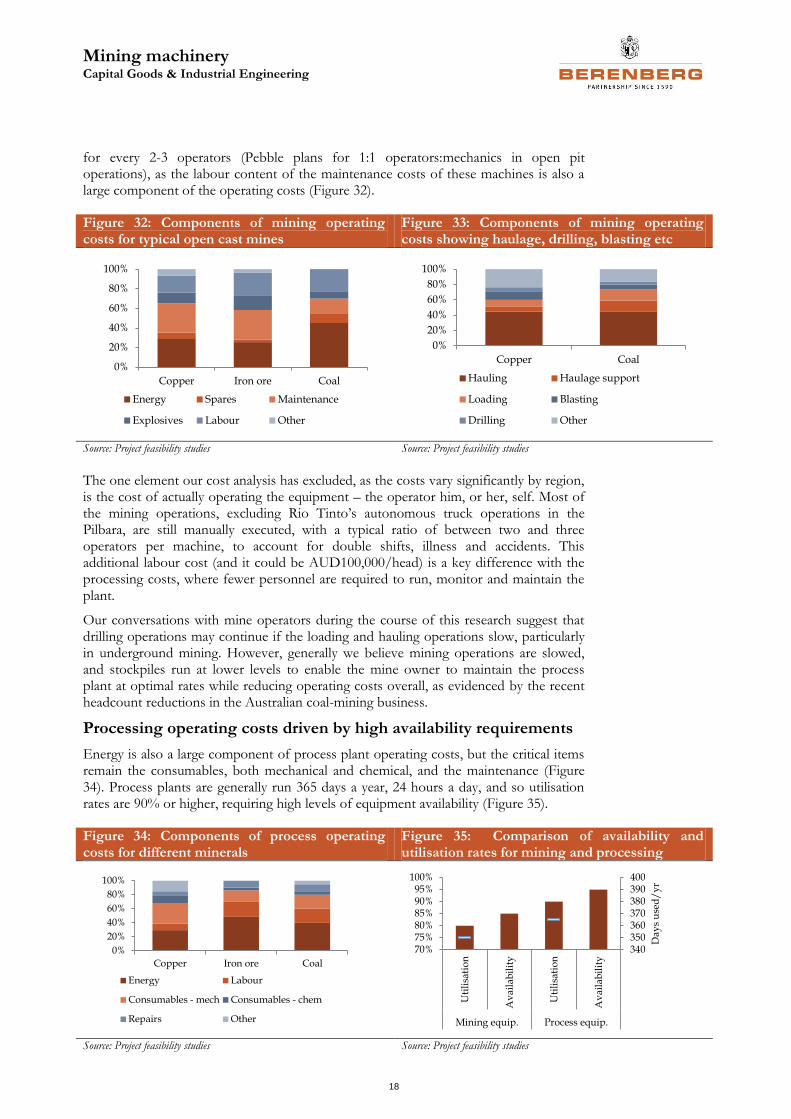

Figure 32: Components of mining operating costs for typical open cast mines

Figure 33: Components of mining operating costs showing haulage, drilling, blasting etc

Source: Project feasibility studies Source: Project feasibility studies

The one element our cost analysis has excluded, as the costs vary significantly by region, is the cost of actually operating the equipment – the operator him, or her, self. Most of the mining operations, excluding Rio Tinto’s autonomous truck operations in the Pilbara, are still manually executed, with a typical ratio of between two and three operators per machine, to account for double shifts, illness and accidents. This additional labour cost (and it could be AUD100,000/head) is a key difference with the processing costs, where fewer personnel are required to run, monitor and maintain the plant.

Our conversations with mine operators during the course of this research suggest that drilling operations may continue if the loading and hauling operations slow, particularly in underground mining. However, generally we believe mining operations are slowed, and stockpiles run at lower levels to enable the mine owner to maintain the process plant at optimal rates while reducing operating costs overall, as evidenced by the recent headcount reductions in the Australian coal-mining business.

Processing operating costs driven by high availability requirements

Energy is also a large component of process plant operating costs, but the critical items remain the consumables, both mechanical and chemical, and the maintenance (Figure 34). Process plants are generally run 365 days a year, 24 hours a day, and so utilisation rates are 90% or higher, requiring high levels of equipment availability (Figure 35).

Figure 34: Components of process operating costs for different minerals

Figure 35: Comparison of availability and utilisation rates for mining and processing

Source: Project feasibility studies Source: Project feasibility studies

0%

20%

40%

60%

80%

100%

Copper Iron ore Coal

Energy Spares Maintenance

Explosives Labour Other

0%

20%

40%

60%

80%

100%

Copper Coal

Hauling Haulage support

Loading Blasting

Drilling Other

0%

20%

40%

60%

80%

100%

Copper Iron ore Coal

Energy Labour

Consumables - mech Consumables - chem

Repairs Other

340350360370380390400

70%75%80%85%90%95%

100%

Uti

lisa

tio

n

Av

aila

bil

ity

Uti

lisa

tio

n

Av

aila

bil

ity

Mining equip. Process equip.

Da

ys

use

d/

yr

Mining machinery Capital Goods & Industrial Engineering

19

While all assets are better operating than not, from a cost effectiveness standpoint, process plants have such a high fixed cost base that generally the optimal situation for them to be generating the best cost per tonne milled or processed is for them to be operating at design capacity. Coal plants, which generally simply wash the product, are perhaps the exception to this, but iron, copper, gold and other metals where there is a continuous process make it difficult to vary either the speed or the volume of the process, which would generally require a similar energy input almost regardless of the volume throughput. The energy saved by running a mill slightly slower is insignificant compared to that required to overcome the inertia in stopping and starting.

In running the plant, consumables take different forms, all of which provide a more or less continuous stream of aftermarket business for the equipment suppliers:

grinding media inside the mills (steel rods, balls etc), the use of which is driven by the abrasiveness of the ore and the throughput of the mill;

liners for the inside of the mills and slurry pumps, which are also subject to the abrasiveness of the ore and the plant throughput; and

chemicals (flocculants), which are used as catalysts or reagents in the refining process and which are also calculated on a per tonne basis.

On top of this is the cost of maintaining and repairing (both scheduled and on an ad hoc basis) the equipment to ensure the high availability and utilisation rates are sustained. The manpower required to implement, monitor and sustain the plant is much lower, per tonne processed and in absolute terms, than that required for the mining operations – the employee base associated with the processing operations of an integrated copper mine and plant, processing perhaps 70,000 tonnes per day, might be less than 15% of the manpower required to drill, load and haul the required feed tonnage of ore. The Alaskan Pebble project plans for over 500 open pit operations employees (50:50 operators:mechanics) compared to c75 process plant personnel.

Our examination of the cost saving plans of the major miners and our conversations during the course of this research show that there are certainly savings to be made in terms of negotiating with suppliers of consumables, running lower inventories and ensuring automation is used where possible. However, the scope for making immediate, and reversible, savings in the processing plant is more limited compared to the mining operations, supporting our thesis that the more defensive exposure lies here rather than closer to the mine face.

Mining machinery Capital Goods & Industrial Engineering

20

Equipment characteristics: consumables vs spares and service

Longevity of service, high requirements for consumables, spares and maintenance favour process equipment

Mining equipment demonstrates lower spare and wear part requirements as a proportion of the overall operating costs, though this can be higher for individual pieces of equipment. The serviceable life tends to be shorter. Generally, the ratio of capital required to operate the equipment over its serviceable life is lower compared to process equipment.

Much of the operating cost is associated with fuel and energy, while there is also the cost of the operator to consider. Higher individual capital cost makes mining equipment more vulnerable in periods of declining expenditure

Process equipment tends to have longer serviceable life, but requires high volumes of spare and wear parts and frequent maintenance to deliver that life and operate throughout it. This translates to a higher ratio of through-life costs to initial capital cost per unit compared to mining equipment.

Long life and high aftermarket content offer more stable, high-margin aftermarket revenue streams for equipment suppliers

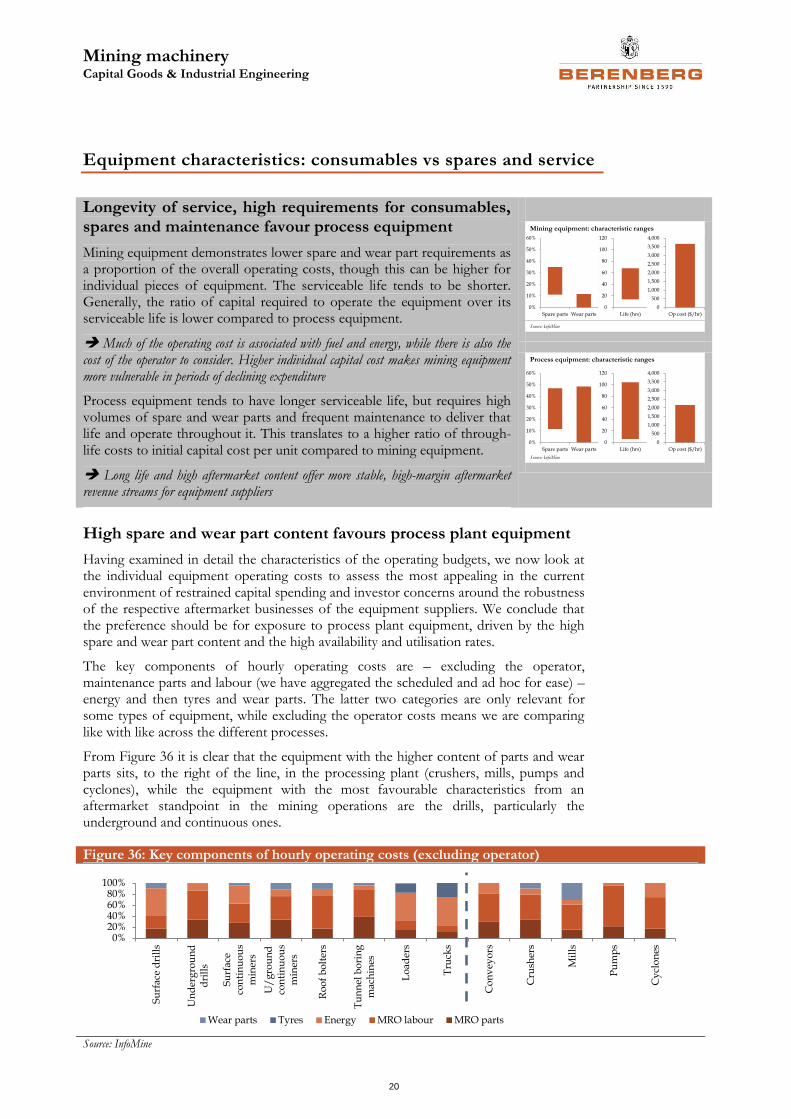

High spare and wear part content favours process plant equipment

Having examined in detail the characteristics of the operating budgets, we now look at the individual equipment operating costs to assess the most appealing in the current environment of restrained capital spending and investor concerns around the robustness of the respective aftermarket businesses of the equipment suppliers. We conclude that the preference should be for exposure to process plant equipment, driven by the high spare and wear part content and the high availability and utilisation rates.

The key components of hourly operating costs are – excluding the operator, maintenance parts and labour (we have aggregated the scheduled and ad hoc for ease) – energy and then tyres and wear parts. The latter two categories are only relevant for some types of equipment, while excluding the operator costs means we are comparing like with like across the different processes.

From Figure 36 it is clear that the equipment with the higher content of parts and wear parts sits, to the right of the line, in the processing plant (crushers, mills, pumps and cyclones), while the equipment with the most favourable characteristics from an aftermarket standpoint in the mining operations are the drills, particularly the underground and continuous ones.

Figure 36: Key components of hourly operating costs (excluding operator)

Source: InfoMine

0%

10%

20%

30%

40%

50%

60%

Spare parts Wear parts

0

20

40

60

80

100

120

Life (hrs)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Op cost ($/hr)

Mining equipment: characteristic ranges

Source: InfoMine

Process equipment: characteristic ranges

Source: InfoMine

0%

10%

20%

30%

40%

50%

60%

Spare parts Wear parts

0

20

40

60

80

100

120

Life (hrs)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Op cost ($/hr)

0%20%40%60%80%

100%

Su

rfac

e d

rill

s

Un

der

gro

un

dd

rill

s

Su

rfac

eco

nti

nu

ou

sm

iner

s

U/

gro

un

dco

nti

nu

ou

sm

iner

s

Ro

of

bo

lter

s

Tu

nn

el b

ori

ng

mac

hin

es

Lo

ader

s

Tru

cks

Co

nv

eyo

rs

Cru

sher

s

Mil

ls

Pu

mp

s

Cy

clo

nes

Wear parts Tyres Energy MRO labour MRO parts

Mining machinery Capital Goods & Industrial Engineering

21

Mining equipment: pick your spot carefully for aftermarket business

Our analysis suggests that while mining equipment can be very expensive and may require high levels of sustaining capital (the capital required to rebuild or replace the equipment) and operating costs, the aftermarket opportunity associated with the initial sale can vary from low (eg draglines) to relatively high (eg shovels or tunnel boring machines).

Assuming a mine life of 30 years, we calculated the initial capital cost, sustaining capital cost and operating capital cost (the latter two combined to define stay-in-business capital, or SIB capital) on a per unit basis for each of the key pieces of equipment in mining and process operations. We then compared the ratio of SIB capital to initial capital on a per unit basis to establish the SIB ratio, to identify what equipment generated the most attractive aftermarket sales opportunity (Figure 37). Using the feasibility studies we have examined, mining operations are typically modelled on 350-360 days per year, two shifts of 12 hours each, with 80% utilisation rates and 85% equipment availability, resulting in c5,700 hours of operation per year, or 171,000 over a 30-year LoM.

Items of mining equipment with the most appealing SIB ratios are drilling rigs and continuous mining machines (including tunnel boring machines), while shovels and backhoe excavators also demonstrate appealing aftermarket characteristics.

Figure 37: Mining operations: SIB capital vs initial capital

Source: InfoMine, Berenberg equity research

Mining operations encompass some of the largest pieces of mechanical equipment manufactured and the operating costs are of similar magnitude, with the likes of draglines, hydraulic shovels and large-scale hydraulic backhoe excavators costing $2,000 to $3,000 per hour to operate (excluding the actual operator!). The smaller equipment generally costs less than $500 per hour to operate (Figure 37).

Spare parts and wear parts, on average, account for c25% and 5% respectively of operating costs, though this does vary by equipment, sometimes significantly. A drill or continuous miner will require 10-12% of the hourly operating costs allocated to wear parts and also figures highly (35%+) in terms of spare part requirements. The larger equipment may also generate 5x to 6x the initial capital cost in maintenance labour costs over the life of a mine, suggesting that suppliers which can improve this aspect of the

Capital invested ($m) Ratio

Initial Sustaining Operating Total SIB SIB:initial

Underground loaders (LHDs) 1.9 14.3 12.7 27.0 14 :1

Shovels, hydraulic 15.9 117.0 62.3 179.3 11 :1

Continuous miners, u/ground 3.2 13.8 22.1 35.9 11 :1

Roof bolters 1.4 7.7 8.8 16.5 11 :1

Tunnel boring machines 19.0 48.3 162.5 210.9 11 :1

Rotary blasthole drill rigs 3.0 17.0 13.2 30.3 10 :1

Continuous miners, surface 4.9 20.1 29.6 49.7 10 :1

Backhoes, hydraulic 17.0 124.7 40.2 164.9 9 :1

Bucketwheel excavators 7.1 25.1 31.1 56.1 7 :1

Wheel loaders 7.7 44.0 14.9 58.9 7 :1

Shovels, cable 23.0 94.6 32.9 127.5 5 :1

Underground ore & coal haulers 1.6 3.8 4.6 8.4 5 :1

Draglines, crawler 5.5 12.5 12.1 24.5 4 :1

Trucks, rear-dump (40t-400t) 6.5 17.8 11.8 29.6 4 :1

Draglines, walking 184.5 279.6 243.9 523.5 2 :1

Mining machinery Capital Goods & Industrial Engineering

22

operational performance of their equipment will be offering considerable cost saving potential to their customers.

Figure 38: Mining equipment: key operating cost characteristics

Source: InfoMine

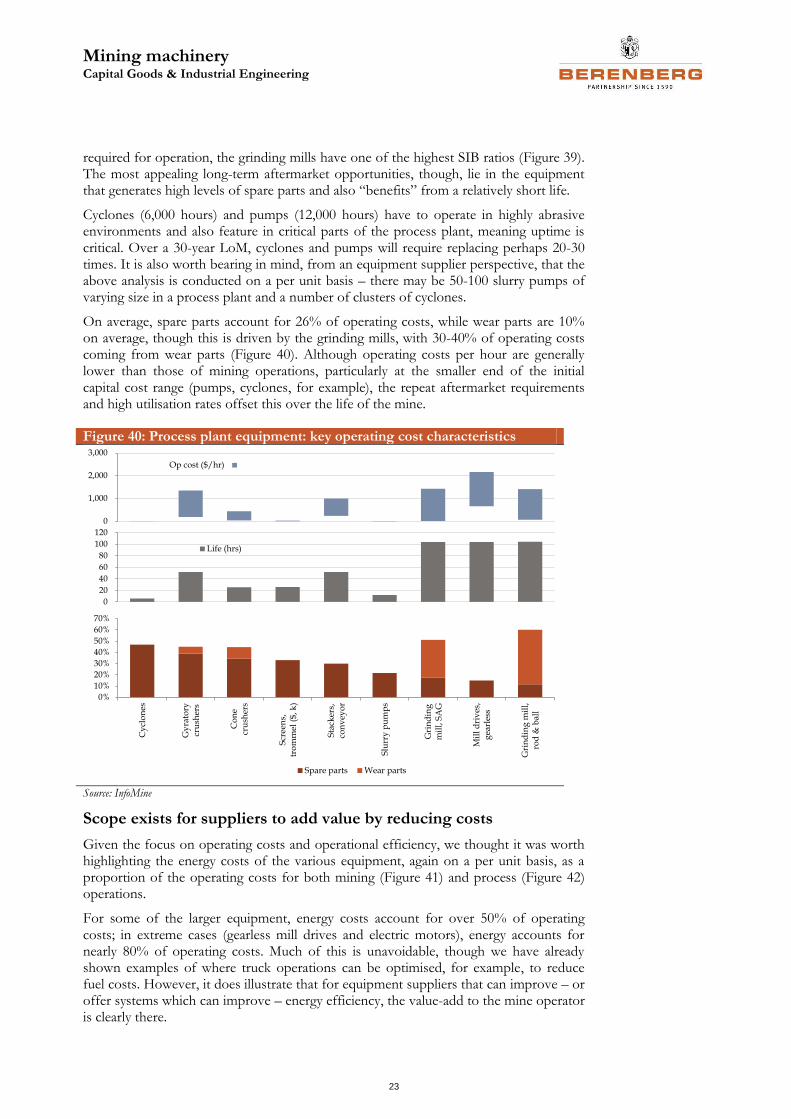

Process equipment: longevity and high SIB capex appeal

Using the same simple assumptions to calculate the SIB ratios for process equipment shows a considerable advantage from an aftermarket perspective for suppliers of equipment into the process plant. The SIB ratios are, on average, over twice those of mining equipment (18:1 average versus 8:1), while the higher availability and utilisation rates could see process equipment operating for up to one-third longer over the life of the mine (225,000 hours versus 171,000 hours).

Figure 39: Processing plant: SIB capital vs initial capital

Source: InfoMine, Berenberg equity research

The feasibility studies show that process plant modelling typically assumes two shifts of 12 hours per day operating 365 days per year, with 90% utilisation rates and 95% equipment availability. This translates to c7,500 hours per year and c225,000 hours over a 30-year LoM. From an equipment perspective, due to the grinding media and liners

0

1,000

2,000

3,000

Op cost ($/hr)

0

20

40

60

80

100

120

Life (hrs)

0%

10%

20%

30%

40%

50%

Dra

gli

nes

,w

alk

ing

Co

nti

nu

ou

s m

iner

s,u

/g

rou

nd

Sh

ov

els,

cab

le

Bu

cket

wh

eel

exca

vat

ors

Co

nti

nu

ou

s m

iner

s,su

rfac

e Sh

ov

els,

hy

dra

uli

c

Dra

gli

nes

,cr

awle

r

Bac

kh

oes

,h

yd

rau

lic

Ro

tary

bla

sth

ole

dri

ll r

igs

Ro

of

bo

lter

s

Wh

eel

load

ers

Du

mp

tru

cks

Wear parts Spare parts

Capital invested ($m) Ratio

Initial Sustaining Operating Total SIB SIB:initial

Grinding mill, rod & ball 5.5 7.1 190.5 197.6 35 :1

Cone crushers 4.0 21.2 43.8 65.0 16 :1

Mobile crushing plants 1.2 8.8 9.0 17.7 15 :1

Gyratory crushers 13.0 33.5 136.5 170.0 13 :1

Grinding mill, SAG 13.5 17.6 164.2 181.7 13 :1

Stackers, conveyor 20.5 53.1 67.2 120.4 5 :1

Mill drives, gearless 18.8 24.3 72.7 97.0 5 :1

$, 000s

Cyclones 26 1.0 0.0 1.0 39 :1

Slurry pumps 84 1.6 0.6 2.1 25 :1

Electric motors 185 1.9 1.7 3.6 19 :1

Screens 403 3.5 1.9 5.4 13 :1

Mining machinery Capital Goods & Industrial Engineering

23

required for operation, the grinding mills have one of the highest SIB ratios (Figure 39). The most appealing long-term aftermarket opportunities, though, lie in the equipment that generates high levels of spare parts and also “benefits” from a relatively short life.

Cyclones (6,000 hours) and pumps (12,000 hours) have to operate in highly abrasive environments and also feature in critical parts of the process plant, meaning uptime is critical. Over a 30-year LoM, cyclones and pumps will require replacing perhaps 20-30 times. It is also worth bearing in mind, from an equipment supplier perspective, that the above analysis is conducted on a per unit basis – there may be 50-100 slurry pumps of varying size in a process plant and a number of clusters of cyclones.

On average, spare parts account for 26% of operating costs, while wear parts are 10% on average, though this is driven by the grinding mills, with 30-40% of operating costs coming from wear parts (Figure 40). Although operating costs per hour are generally lower than those of mining operations, particularly at the smaller end of the initial capital cost range (pumps, cyclones, for example), the repeat aftermarket requirements and high utilisation rates offset this over the life of the mine.

Figure 40: Process plant equipment: key operating cost characteristics

Source: InfoMine

Scope exists for suppliers to add value by reducing costs

Given the focus on operating costs and operational efficiency, we thought it was worth highlighting the energy costs of the various equipment, again on a per unit basis, as a proportion of the operating costs for both mining (Figure 41) and process (Figure 42) operations.

For some of the larger equipment, energy costs account for over 50% of operating costs; in extreme cases (gearless mill drives and electric motors), energy accounts for nearly 80% of operating costs. Much of this is unavoidable, though we have already shown examples of where truck operations can be optimised, for example, to reduce fuel costs. However, it does illustrate that for equipment suppliers that can improve – or offer systems which can improve – energy efficiency, the value-add to the mine operator is clearly there.

0

1,000

2,000

3,000

Op cost ($/hr)

0

20

40

60

80

100

120

Life (hrs)

0%

10%

20%

30%

40%

50%

60%

70%

Cy

clo

nes

Gy

rato

rycr

ush

ers

Co

ne

cru

sher

s

Scr

een

s,tr

om

mel

($,

k)

Sta

cker

s,co

nv

eyo

r

Slu

rry

pu

mp

s

Gri

nd

ing

mil

l, S

AG

Mil

l d

riv

es,

gea

rles

s

Gri

nd

ing

mil

l,ro

d &

bal

l

Spare parts Wear parts

Mining machinery Capital Goods & Industrial Engineering

24

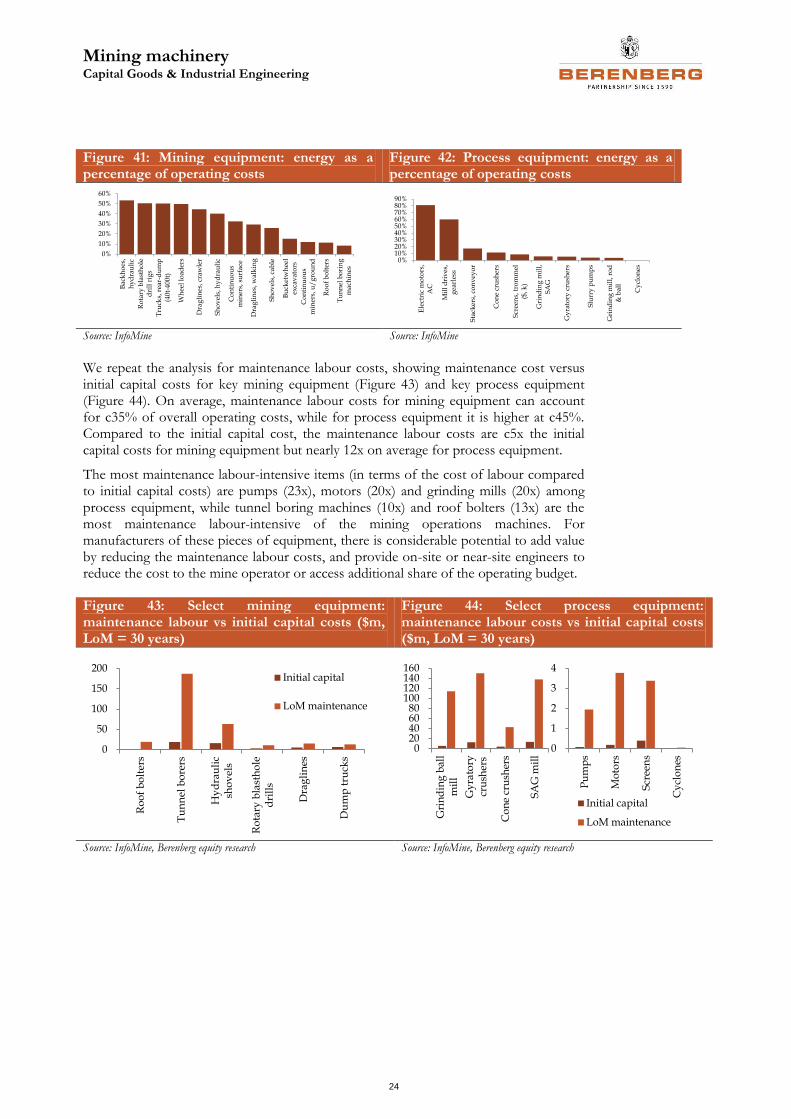

Figure 41: Mining equipment: energy as a percentage of operating costs

Figure 42: Process equipment: energy as a percentage of operating costs

Source: InfoMine Source: InfoMine

We repeat the analysis for maintenance labour costs, showing maintenance cost versus initial capital costs for key mining equipment (Figure 43) and key process equipment (Figure 44). On average, maintenance labour costs for mining equipment can account for c35% of overall operating costs, while for process equipment it is higher at c45%. Compared to the initial capital cost, the maintenance labour costs are c5x the initial capital costs for mining equipment but nearly 12x on average for process equipment.

The most maintenance labour-intensive items (in terms of the cost of labour compared to initial capital costs) are pumps (23x), motors (20x) and grinding mills (20x) among process equipment, while tunnel boring machines (10x) and roof bolters (13x) are the most maintenance labour-intensive of the mining operations machines. For manufacturers of these pieces of equipment, there is considerable potential to add value by reducing the maintenance labour costs, and provide on-site or near-site engineers to reduce the cost to the mine operator or access additional share of the operating budget.

Figure 43: Select mining equipment: maintenance labour vs initial capital costs ($m, LoM = 30 years)

Figure 44: Select process equipment: maintenance labour costs vs initial capital costs ($m, LoM = 30 years)

Source: InfoMine, Berenberg equity research Source: InfoMine, Berenberg equity research

0%

10%

20%

30%

40%

50%

60%

Bac

kh

oes

,h

yd

rau

lic

Ro

tary

bla

sth

ole

dri

ll r

igs

Tru

cks,

rea

r-d

um

p(4

0t-

400

t)

Wh

eel

load

ers

Dra

gli

nes

, cra

wle

r

Sh

ov

els,

hy

dra

uli

c

Co

nti

nu

ou

sm

iner

s, s

urf

ace

Dra

gli

nes

, wal

kin

g

Sh

ov

els,

cab

le

Bu

cket

wh

eel

exca

vat

ors

Co

nti

nu

ou

sm

iner

s, u

/g

rou

nd

Ro

of

bo

lter

s

Tu

nn

el b

ori

ng

ma

chin

es

0%10%20%30%40%50%60%70%80%90%

Ele

ctri

c m

oto

rs,

AC

Mil

l d

riv

es,

gea

rles

s

Sta

cker

s, c

on

vey

or

Co

ne

cru

sher

s

Scr

een

s, t

rom

mel

($, k

)

Gri

nd

ing

mil

l,S

AG

Gy

rato

ry c

rush

ers

Slu

rry

pu

mp

s

Gri

nd

ing

mil

l, r

od

& b

all

Cy

clo

nes

0

50

100

150

200

Ro

of

bo

lter

s

Tu

nn

el b

ore

rs

Hy

dra

uli

csh

ov

els

Ro

tary

bla

sth

ole

dri

lls

Dra

gli

nes

Du

mp

tru

cks

Initial capital

LoM maintenance

020406080

100120140160

Gri

nd

ing

bal

lm

ill

Gy

rato

rycr

ush

ers

Co

ne

cru

sher

s

SA

G m

ill

0

1

2

3

4

Pu

mp

s

Mo

tors

Scr

een

s

Cy

clo

nes

Initial capital

LoM maintenance

Mining machinery Capital Goods & Industrial Engineering

25

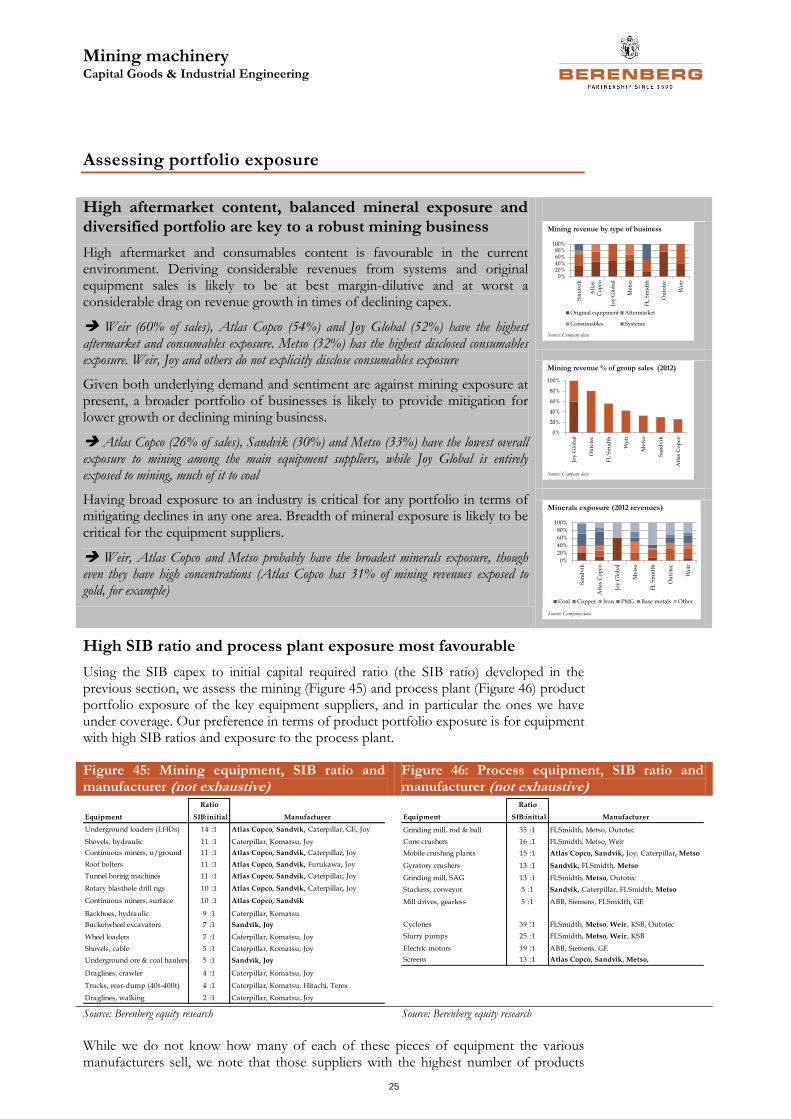

Assessing portfolio exposure

High aftermarket content, balanced mineral exposure and diversified portfolio are key to a robust mining business

High aftermarket and consumables content is favourable in the current environment. Deriving considerable revenues from systems and original equipment sales is likely to be at best margin-dilutive and at worst a considerable drag on revenue growth in times of declining capex.

Weir (60% of sales), Atlas Copco (54%) and Joy Global (52%) have the highest aftermarket and consumables exposure. Metso (32%) has the highest disclosed consumables exposure. Weir, Joy and others do not explicitly disclose consumables exposure

Given both underlying demand and sentiment are against mining exposure at present, a broader portfolio of businesses is likely to provide mitigation for lower growth or declining mining business.

Atlas Copco (26% of sales), Sandvik (30%) and Metso (33%) have the lowest overall exposure to mining among the main equipment suppliers, while Joy Global is entirely exposed to mining, much of it to coal

Having broad exposure to an industry is critical for any portfolio in terms of mitigating declines in any one area. Breadth of mineral exposure is likely to be critical for the equipment suppliers.

Weir, Atlas Copco and Metso probably have the broadest minerals exposure, though even they have high concentrations (Atlas Copco has 31% of mining revenues exposed to gold, for example)

High SIB ratio and process plant exposure most favourable

Using the SIB capex to initial capital required ratio (the SIB ratio) developed in the previous section, we assess the mining (Figure 45) and process plant (Figure 46) product portfolio exposure of the key equipment suppliers, and in particular the ones we have under coverage. Our preference in terms of product portfolio exposure is for equipment with high SIB ratios and exposure to the process plant.

Figure 45: Mining equipment, SIB ratio and manufacturer (not exhaustive)

Figure 46: Process equipment, SIB ratio and manufacturer (not exhaustive)

Source: Berenberg equity research Source: Berenberg equity research

While we do not know how many of each of these pieces of equipment the various manufacturers sell, we note that those suppliers with the highest number of products

Mining revenue by type of business

Source: Company data

0%20%40%60%80%

100%

San

dv

ik

Atl

as

Co

pco

Joy

Glo

bal

Met

so

FL

Sm

idth

Ou

tote

c

Wei

r

Original equipment Aftermarket

Consumables Systems

Mining revenue % of group sales (2012)

Source: Company data

0%

20%

40%

60%

80%

100%

Joy

Glo

bal

Ou

tote

c

FL

Sm

idth

Wei

r

Met

so

San

dv

ik

Atl

as C

op

co

Minerals exposure (2012 revenues)

Source: Company data

0%

20%

40%

60%

80%

100%

San

dv

ik

Atl

as C

op

co

Joy

Glo

bal

Met

so

FL

Sm

idth

Ou

tote

c

Wei

r

Coal Copper Iron PMG Base metals Other

Ratio

Equipment SIB:initial Manufacturer

Underground loaders (LHDs) 14 :1 Atlas Copco, Sandvik, Caterpillar, GE, Joy

Shovels, hydraulic 11 :1 Caterpillar, Komatsu, Joy

Continuous miners, u/ground 11 :1 Atlas Copco, Sandvik, Caterpillar, Joy

Roof bolters 11 :1 Atlas Copco, Sandvik, Furukawa, Joy

Tunnel boring machines 11 :1 Atlas Copco, Sandvik, Caterpillar, Joy

Rotary blasthole drill rigs 10 :1 Atlas Copco, Sandvik, Caterpillar, Joy

Continuous miners, surface 10 :1 Atlas Copco, Sandvik

Backhoes, hydraulic 9 :1 Caterpillar, Komatsu

Bucketwheel excavators 7 :1 Sandvik, Joy

Wheel loaders 7 :1 Caterpillar, Komatsu, Joy

Shovels, cable 5 :1 Caterpillar, Komatsu, Joy

Underground ore & coal haulers 5 :1 Sandvik, Joy

Draglines, crawler 4 :1 Caterpillar, Komatsu, Joy

Trucks, rear-dump (40t-400t) 4 :1 Caterpillar, Komatsu, Hitachi, Terex

Draglines, walking 2 :1 Caterpillar, Komatsu, Joy

Ratio

Equipment SIB:initial Manufacturer

Grinding mill, rod & ball 35 :1 FLSmidth, Metso, Outotec

Cone crushers 16 :1 FLSmidth, Metso, Weir

Mobile crushing plants 15 :1 Atlas Copco, Sandvik, Joy, Caterpillar, Metso

Gyratory crushers 13 :1 Sandvik, FLSmidth, Metso

Grinding mill, SAG 13 :1 FLSmidth, Metso, Outotec

Stackers, conveyor 5 :1 Sandvik, Caterpillar, FLSmidth, Metso

Mill drives, gearless 5 :1 ABB, Siemens, FLSmidth, GE

Cyclones 39 :1 FLSmidth, Metso, Weir, KSB, Outotec

Slurry pumps 25 :1 FLSmidth, Metso, Weir, KSB

Electric motors 19 :1 ABB, Siemens, GE

Screens 13 :1 Atlas Copco, Sandvik, Metso,

Mining machinery Capital Goods & Industrial Engineering

26

with high SIB ratios and process plant exposure are Metso and Weir, while among the more mining operations-focused suppliers, Atlas Copco and Sandvik products rank most consistently with high SIB ratios. When translating this into the individual company exposures, we find only Metso (32% of sales), Atlas Copco (23%) and Sandvik (11%) break out explicitly the revenues they derive from consumables. The reality is that Joy Global and Weir, Outotec and FLSmidth must generate revenue from consumables and it could be quite a high proportion when one considers the portfolio exposure (continuous miners at Joy, pumps and liners and Weir, grinding mills at Outotec and FLSmidth).

Overall, the suppliers with the highest levels of aftermarket and consumables revenues are Weir (60% of sales), Atlas Copco (54%) and Joy Global (52%), with Outotec (23%) generating the lowest levels (Figure 47). The high process exposure at Weir should also be of benefit given the more limited flexibility in that part of operations with respect to operating budgets.

High levels of systems business (FLSmidth, 49%; Sandvik 20%) are a mixed blessing. Long installation periods and considerable investment costs mean current projects are unlikely to be significantly curtailed, though Barrick Gold’s recent actions highlight that build schedules can still be changed. The turnkey nature of the systems business means margins are generally lower than in the rest of the mining equipment portfolio. If the balance of the business is in decline, the more stable, lower-margin systems business is likely to be margin-dilutive.

Figure 47: Mining revenue by type – key equipment suppliers

Source: Company data

Balanced portfolio exposure is key to a robust business

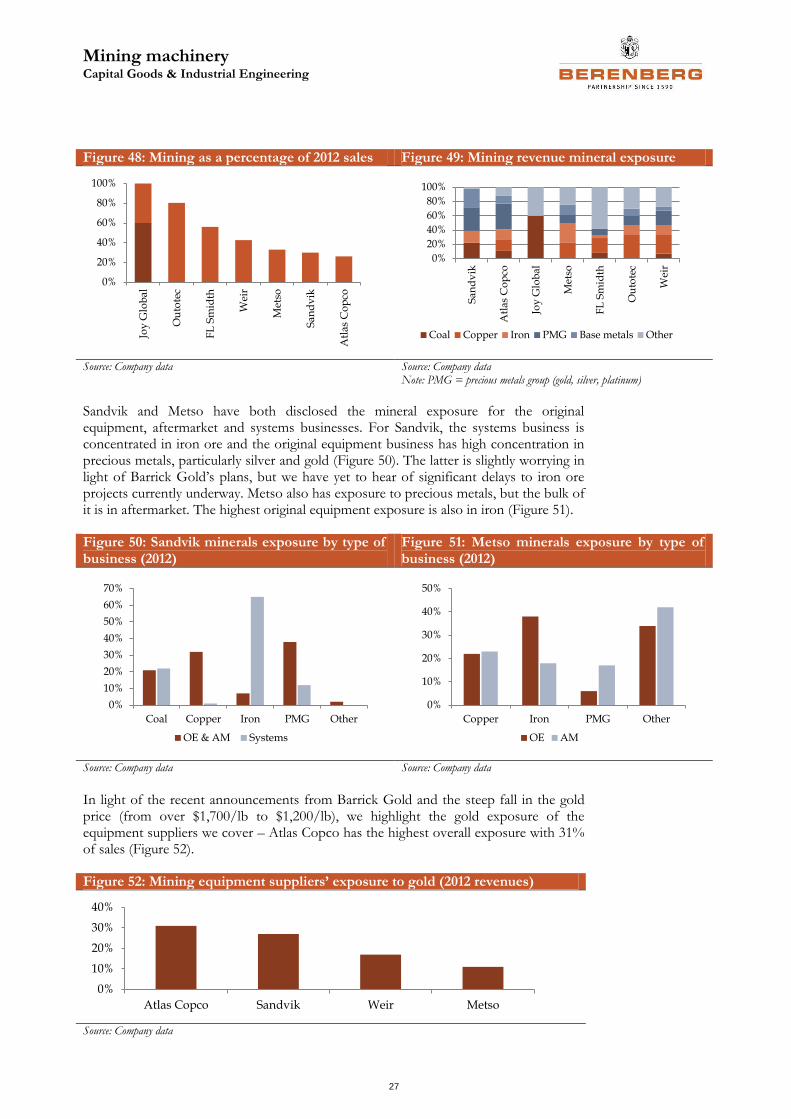

This is something of a truism and relevant for any business, industry or portfolio. In mining, clearly companies with mining accounting for a lower proportion of their overall sales will be better positioned with respect to both end market demand dynamics and investor sentiment. Atlas Copco (26% of group sales), Sandvik (30%) and Metso (33%) have the lowest overall exposure of the mining equipment suppliers we are examining, while Joy Global has the highest (Figure 48).

Balanced mineral exposure should help mitigate the decline of one commodity in particular. The suppliers with the most balanced exposures are Atlas Copco, Weir and Metso, while Joy Global is clearly very dependent on coal (Figure 49). FLSmidth has high exposure to fertilisers and aggregates, which is why the “other” component of its revenue exposure is so large.

0%

20%

40%

60%

80%

100%

Sa

nd

vik

Atl

as C

op

co

Joy

Glo

bal

Met

so

FL

Sm

idth

Ou

tote

c

Wei

r

Original equipment Aftermarket Consumables Systems