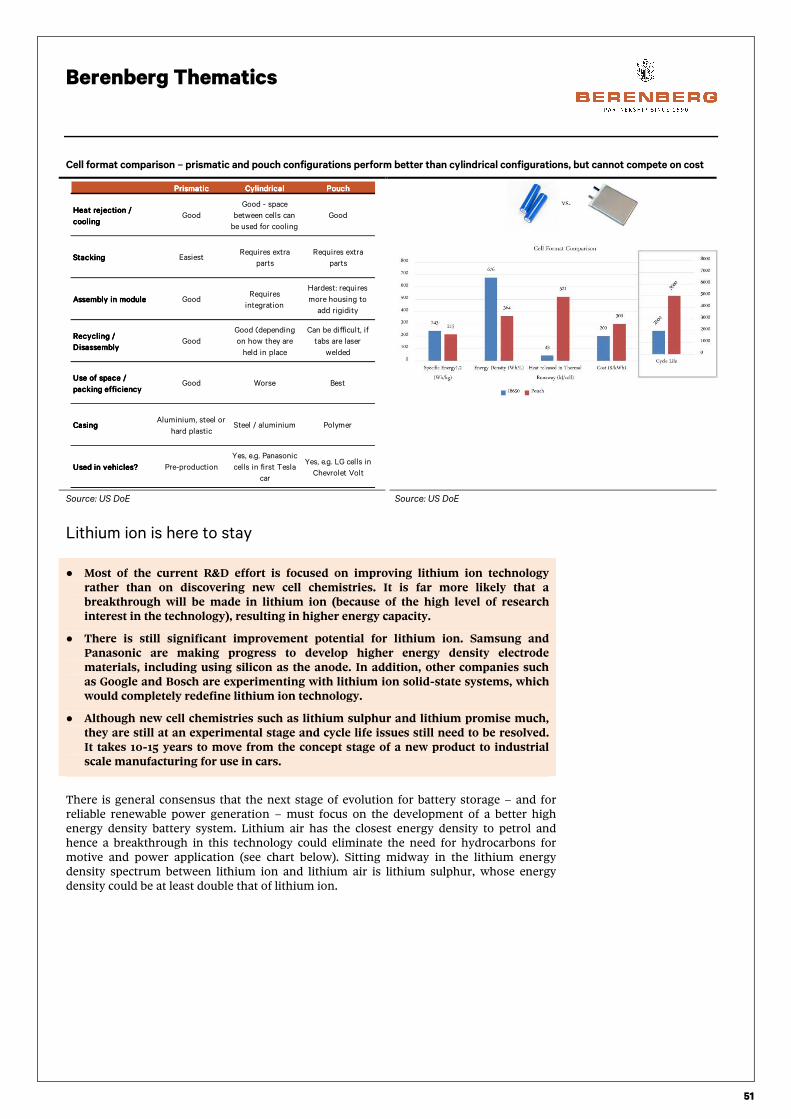

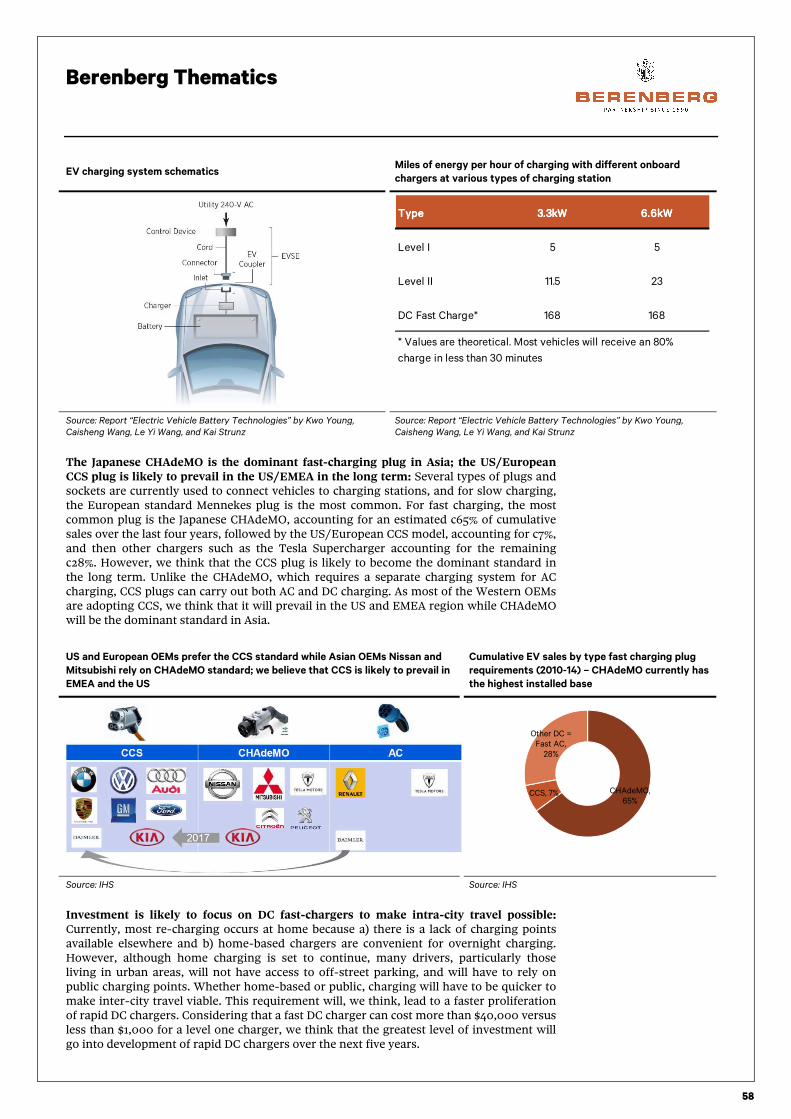

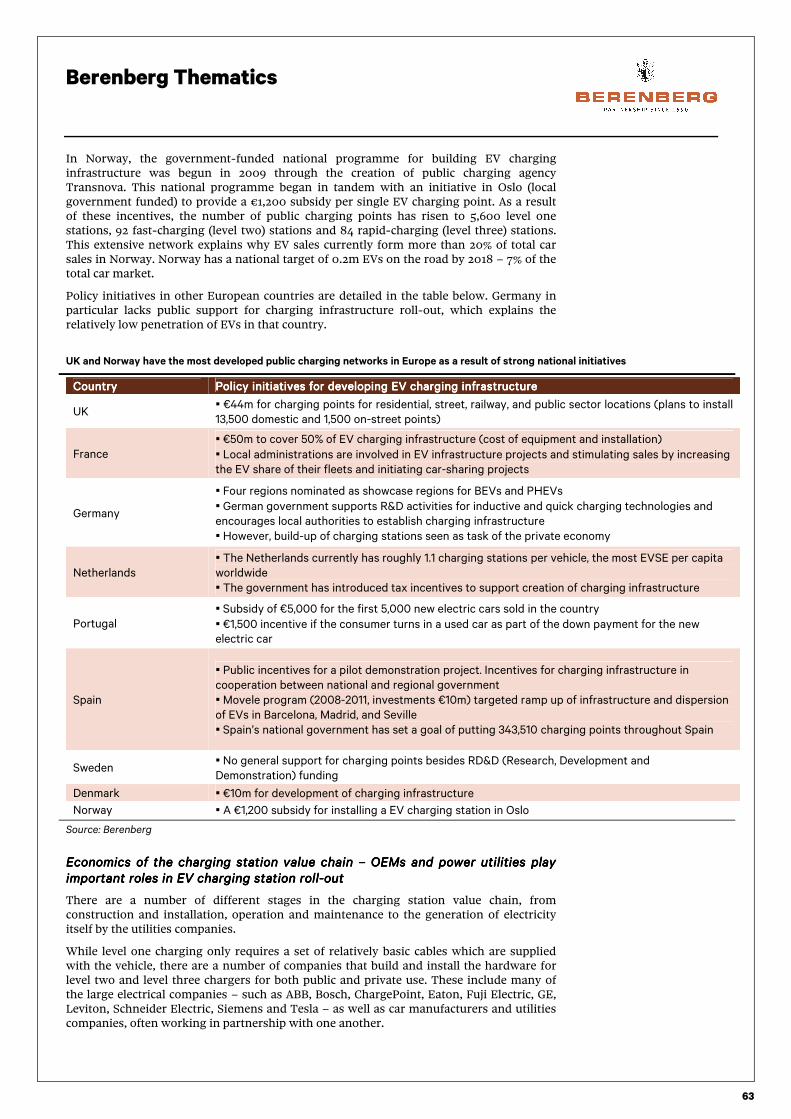

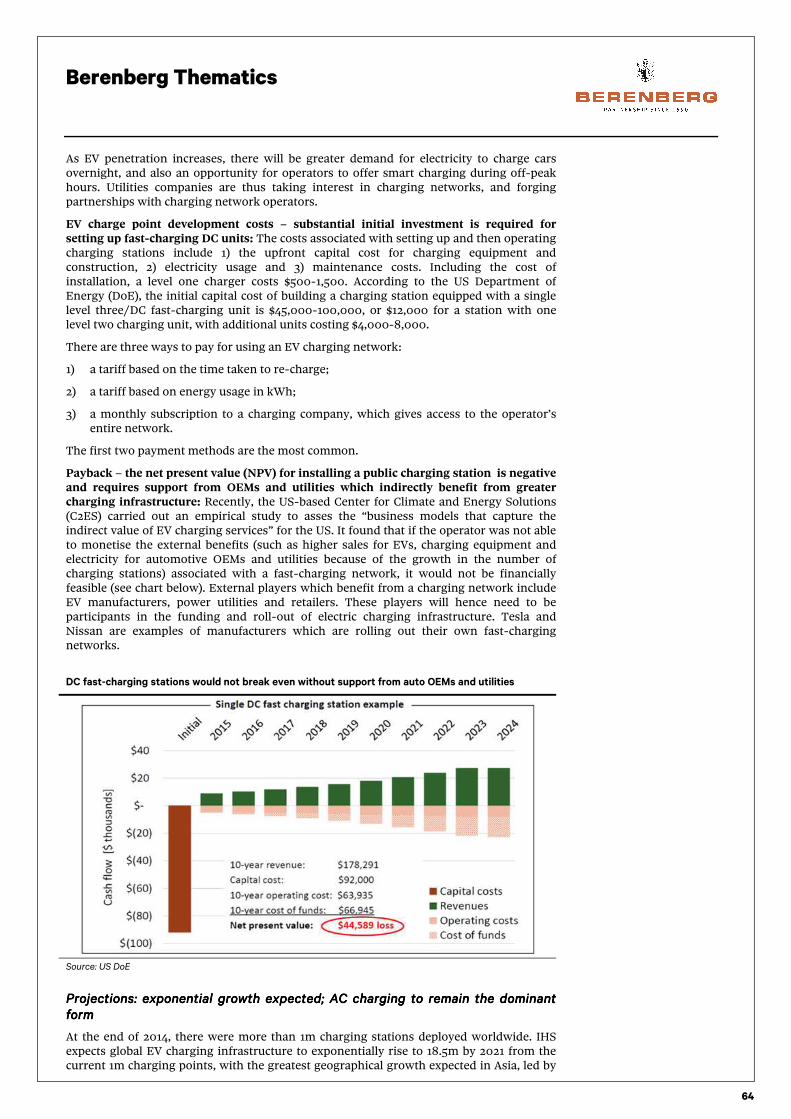

Berenberg Thematics - Battery Technology

174

ATLAS ALPHA • THOUGHT LEADERSHIP • ACCESS • SERVICE Berenberg Thematics Battery adoption at the tipping point 10 February 2016 Asad Farid, CFA Analyst +44 20 3207 7932 [email protected] Nick Anderson Analyst +44 20 3207 7838 [email protected] Jamie Rosser Analyst +44 20 3465 2732 [email protected] Chris Armstrong Specialist Sales +44 20 3207 7809 [email protected]

-

Upload

jamie-rosser -

Category

Documents

-

view

345 -

download

25

Transcript of Berenberg Thematics - Battery Technology

ATLAS ALPHA • THOUGHT LEADERSHIP • ACCESS • SERVICE

Berenberg Thematics

Battery adoption at the tipping point

10 February 2016

Asad Farid, CFA Analyst

+44 20 3207 7932 [email protected]

Nick Anderson Analyst

+44 20 3207 7838 [email protected]

Jamie Rosser Analyst

+44 20 3465 2732 [email protected]

Chris Armstrong Specialist Sales

+44 20 3207 7809 [email protected]

Berenberg Thematics

What is Berenberg Thematics?

Under our Thematics brand, we will focus on big, longer-term themes --- specifically, disruptive technologies, demographics and corporate governance issues --- which we feel investors should be looking at. Within each note, we will highlight trends and issues that we believe to be of interest to investors, and the effect of these on sectors and stocks which we view as beneficiaries or at risk from the specific theme. The companies that we will consider will include those already under coverage, those not covered, and also relevant privately-owned

businesses, which we believe will be affected.

THE TEAM

Asad Farid has been working at Berenberg for the past four years. His previous focus was

on the oil and gas sector where he was the lead analyst for oil field services. Before joining Berenberg, he worked as an economist and banking analyst at AKD Securities and has eight years of sell-side research experience. Asad is an MBA from University of Cambridge and is a CFA charter holder. As apart of his MBA programme, Asad completed internships at Google and with Berenberg’s Technology Hardware team.

Nick Anderson joined the Thematics team in 2016 having previously built up and led the

banking team; he joined Berenberg in 2010. Nick has over 20 years’ experience as a top-ranked sell-side equity analyst including spells as co-head of the Lehman Brothers European banks team and as a transport analyst at both Lehman Brothers and HSBC James Capel. In addition, he has worked as a management consultant at McKinsey. Nick

has degrees in economics and management studies from the University of Cambridge and in wine production from the University of Brighton.

Jamie Rosser joined Berenberg in September 2014 on the graduate scheme. Having

successfully completed the programme, he joined the Thematics team in November 2015. Prior to this, Jamie gained experience through internships with Grant Thornton, Ignis Asset

Management and the Phoenix Group. Jamie graduated from the University of Bath with a BSc in Mathematics and has passed the CFA level I exam.

Chris Armstrong has 20 years of experience on both the buy-side (as an analyst and

portfolio manager) and on the sell-side, most recently as industrial specialist sales. Chris joined Berenberg as a Swiss equity salesman in 2006, before specialising in industrials in 2009. He has previously been a portfolio manager/analyst at Axa Framlington, Bank of Tokyo-Mitsubishi and NatWest, and holds a BA in Economics from Durham University.

For our disclosures in respect of section 34b of the German Securities Trading Act (Wertpapierhandelsgesetz – WpHG) and our disclaimer please see the end of this document.

Please note that the use of this research report is subject to the conditions and restrictions set forth in the disclosures and the disclaimer at the end of this document.

Berenberg Thematics

3

Table of contents

Battery adoption at the tipping point 4

Battery technology – drivers and implications 5

Section 1: Batteries – market overview 18

Cost evolution for lithium ion 23

Section 2: Energy storage for autos – mass adoption is nearing 32

EV uptake – impressive growth but mass adoption yet to be achieved 36

Regulatory incentives – a key growth driver for energy storage in autos 54

Charging infrastructure 57

Mass transit 70

Implications for autos – identifying the winners 76

Section 3: Energy storage for renewables/utilities 98

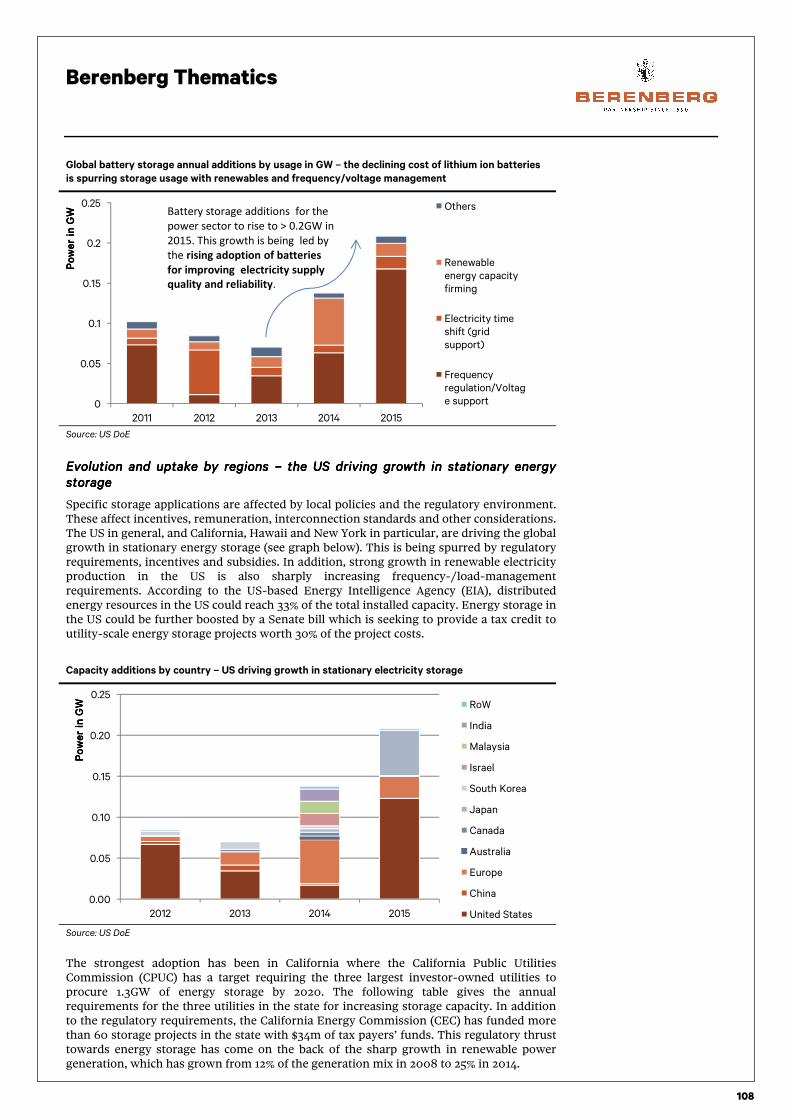

Uptake of utility-scale battery storage by the power sector 107

Outlook and implications: structural growth guaranteed; storage likely to replace gas-fired peaker plants 121

Implications for utilities – battery storage is more of an opportunity than an “existential” threat 124

Section 4: Implications of the growth in lithium ion batteries for the lithium sector 141

Lithium supply outlook 2015-2025 146

Lithium demand outlook 2015-25: strong structural growth driven by automotive and power sectors 149

Lithium market headed towards supply demand imbalance – prices are headed upwards 152

Risk to thesis 165

Disclosures in respect of section 34b of the German Securities Trading Act

(Wertpapierhandelsgesetz – WpHG) 168

Berenberg Thematics

Battery adoption at the tipping point

● Disruptive technologies cannot be ignored by investors. In this, our first Berenberg Thematics report, we explore potential disruption to the automotive and utilities industries (7% of Europe’s market cap), among others, from the mass adoption of new battery technologies. We forecast the combined market for electric passenger vehicles (EVs), electric buses (EBs) and battery storage to increase eight-fold to over $200bn by 2020, a five-year CAGR of more than 50%. The tipping point is nearing as battery economics become cost-effective, helped by favourable regulation, expanding product offerings and infrastructure, and surging renewable generation. Many automotive OEMs will survive (those with scale and vision) but some incumbent utilities are at risk (especially those focused on a centralised distribution model). We also identify nine stocks to watch within the extended lithium ion battery value chain.

● Introducing Berenberg Thematics: Our new Thematics product will focus on major, five-year themes that have a material impact across several sectors. A collaborative effort involving all of Berenberg’s sector teams, reports will combine a deep-dive on the theme with a detailed stock analysis of the winners and losers. Our initial focus is on three sub-themes: disruptive technology, demographics and corporate governance.

● Why read this report? Disruptive technologies matter: In 1980, McKinsey forecast that the size of the US mobile phone market would reach 900,000 handsets by 2000. The actual number was 109m. Such new technologies can be “sustaining”, which favour incumbent producers, or “disruptive”, which allow new entrants, after an initial slow rate of adoption, to unexpectedly replace established ones. Digital cameras and mobile phones are recent examples; we think batteries come next. Investors must engage in the debate as transformational change is likely.

● Why now? Battery technology is coming of age: There have been many false dawns in the mass adoption of batteries in the automotive and utilities industries in the last 20 years. But as the comparative cost of batteries finally moves towards parity with incumbent hydrocarbon solutions, mass market adoption is close to tipping point.

● Automotive disruption – the EV market will grow 14-fold to $140bn by 2020: Favourable regulation, falling battery/EV costs, improving product range and expansion in charging infrastructure will drive rapid growth. Scale and vision will separate winners from losers. We think Daimler (Buy), BMW (Hold), Renault (Buy), Volkswagen (Buy) and GM will transition successfully to join Tesla (Sell). Toyota and Peugeot (Sell), in contrast, are challenged. EBs offer an additional $60bn market by 2020 – three-fold growth.

● Utilities disruption – battery storage will be a $14bn market by 2020 – a 28-fold growth: Demand will be driven by renewables investment (creating unpredictable generation), a reduction in battery costs and regulation. Distributed power generation and micro grids threaten the centralised distribution model. Incumbent utilities will be disrupted, but in Europe, RWE (Sell), E.ON (Sell) and Enel (Buy) will be the least threatened given their renewable/storage exposure.

● The lithium ion battery industry offers opportunities: We expect lithium ion to be the dominant battery technology. Consolidation and barriers to entry key to sustained returns for suppliers. Well-placed suppliers within an extended value chain include: low-cost lithium miners, energy storage battery producers, renewables/micro grid equipment suppliers, selected semiconductor manufacturers, and suppliers of next-generation lithium ion batteries.

● Nine stocks to watch: Stocks well placed to benefit from the battery revolution include: Infineon Technologies (Buy), Umicore (Sell), Albemarle, Maxwell, Orocobre, RedT, SMA, BYD and Solar City.

10 February 2016

Asad Farid, CFA Analyst +44 20 3207 7932 [email protected]

Nick Anderson Analyst +44 20 3207 7838 [email protected]

Jamie Rosser Analyst +44 20 3465 2732 [email protected]

Chris Armstrong Specialist Sales +44 20 3207 7809 [email protected]

Berenberg Thematics

5

Battery technology – drivers and implications

Source: Berenberg

Berenberg Thematics

6

Battery adoption at the tipping point

“Mastery itself was the prize” was how Churchill described his initially controversial decision to change the Royal Navy’s fuel from locally-sourced coal to insecure petroleum supplies from Persia (now Iran). History might have unfolded quite differently had the UK delayed this transformative shift to a superior technology prior to the outbreak of World War I. Today, regulatory bodies, automotive companies, power utilities and a diverse array of other sectors are again faced with the question of how to deal with a prospective disruptive shift to battery energy storage which is still considered by many market participants as economically unviable. For the forerunners investing heavily in battery storage, mastery again is the prize.

There have, however, been a number of false dawns in the adoption of rechargeable batteries, leading to classic failures such as GM’s EV1 electric vehicle in 1996. Similarly, over the last decade, the euphoria about the anticipated demand for raw materials required for batteries created expectations of a sharp spike in lithium prices along with price increases for other minerals, too, such as graphite, nickel and cobalt. This led to a number of lithium mining project failures for the smaller mining companies when the price increase failed to materialise.

The Achilles heel of rechargeable batteries has always been their comparative cost versus hydrocarbon-based power generation, whether for automotive propulsion or electricity generation/storage for utilities. We think that this disadvantage is close to being bridged and that battery technology adoption is at the tipping point. Over the next three years, we believe that batteries will break into the automotive and stationary storage mass markets. Three sectors – automotive, utilities and mass transport – will drive the market for batteries. We expect lithium ion to be the dominant battery technology for the next five years.

Automotives – size of the EV market set to grow from $10bn in 2014

to $140bn by 2020

We expect sales of plug-in electric vehicles (PEVs) to grow from ~0.3m cars in 2014 to 4m by 2020 – a 4% market penetration rate, split equally between all-electric battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs). Assuming an average EV price of $35,000, this translates into EV market/sales growing from $10bn in 2014 to $140bn by 2020. This growth will be driven by regulatory requirements for emissions reduction, EV price reduction due to economies of scale in battery manufacturing, wider availability of charging infrastructure and greater diversity of EV offerings by OEMs over the next five years.

In our view, there are four factors that will drive electrification of the automotive sector.

Factor #1 Factor #1 Factor #1 Factor #1 –––– high regulatory support for EVs to reduce the air high regulatory support for EVs to reduce the air high regulatory support for EVs to reduce the air high regulatory support for EVs to reduce the air pollution that is pollution that is pollution that is pollution that is plaguing urban centresplaguing urban centresplaguing urban centresplaguing urban centres

Transport-related air pollution is responsible for $0.9tn of economic losses in OECD countries, according to OECD research: Air pollution causes 0.5m premature deaths per annum in OECD countries and 1.6m deaths per annum in China. Economic loss from transport-based air pollution is estimated at $0.9tn per annum in OECD countries (50% of air pollution is attributable to transport, according to the OECD) and $0.6tn for China (assuming transport is responsible for 40% of air pollution in China).

Electrification of transportation is a priority for major OECD countries and China in order to reduce transport-related air pollution: Direct purchase subsidies form more than 20% of a car’s purchase price in larger economies. However, the level of direct subsidies for EVs across different countries pales in comparison to the economic loss from air pollution (see chart below). Hence, despite some market concerns, we do not think that the risk of an abrupt end to EV subsidies is very high. We expect subsidies for PHEVs to be phased out sooner than those for BEVs. Continued subsidies for BEVs will provide an impetus to their adoption as manufacturing costs for batteries come down. There is also a possibility that there will be a shift from direct EV subsidies to subsidies for building infrastructure.

Berenberg Thematics

7

EV purchase subsidies – 20% of an EV’s purchase price is subsidised

Source: WHO, OECD, US Department of Energy (DoE), CAAM, Berenberg

FactorFactorFactorFactor #2 #2 #2 #2 –––– the economics of mass production: battery costs are to decline by the economics of mass production: battery costs are to decline by the economics of mass production: battery costs are to decline by the economics of mass production: battery costs are to decline by $130/kWh (down by 43%) to reach $170/kWh by 2020$130/kWh (down by 43%) to reach $170/kWh by 2020$130/kWh (down by 43%) to reach $170/kWh by 2020$130/kWh (down by 43%) to reach $170/kWh by 2020

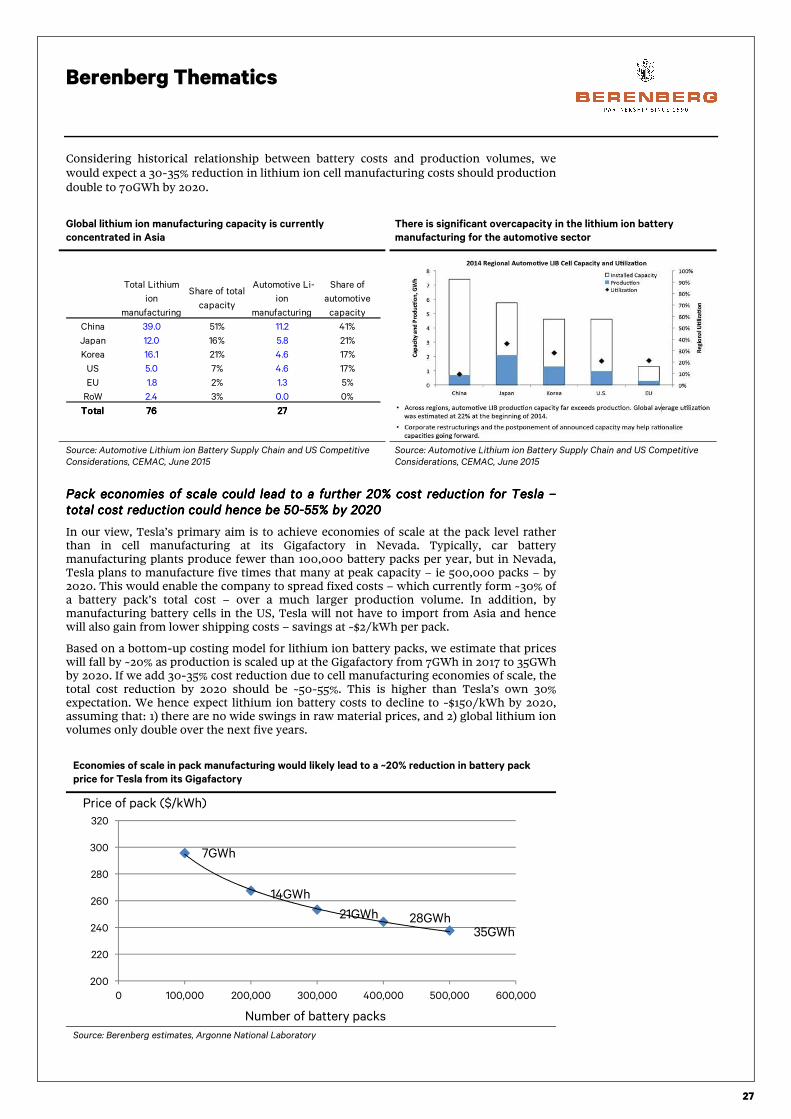

Cell level economies of scale – cost reduction of $70/kWh: Battery manufacturing plans announced by Tesla (in partnership with Panasonic), BYD, LG and Samsung will increase global automotive lithium ion battery manufacturing capacity (currently at ~27GWh) by 4x to 110GWh over 2015-2020. Assuming that global production of lithium ion cells (including automotive) doubles by 2020, this should lead to cost savings of 35% (ie $70/kWh) in cell manufacturing.

Pack level economies of scale of $60/kWh: Currently, battery pack manufacturing per plant is well below 100,000 packs per annum. However, Tesla’s battery pack manufacturing capacity at its new Gigafactory facility in Nevada will increase from 100,000 packs in 2017/18 to 500,000 packs by 2020/21. We estimate that this will lead to cost savings of 20-25% at the pack level, ie $60/kWh.

If battery pack costs decline to $170/kWh by 2020, then the price premium which EVs have versus ICVs will end

Source: Berenberg

Factor #3 Factor #3 Factor #3 Factor #3 –––– a vast improvement in EV product offering by traditional OEMs: at a vast improvement in EV product offering by traditional OEMs: at a vast improvement in EV product offering by traditional OEMs: at a vast improvement in EV product offering by traditional OEMs: at least 13 BEV and 25 PHEV models will be introduced over 2016least 13 BEV and 25 PHEV models will be introduced over 2016least 13 BEV and 25 PHEV models will be introduced over 2016least 13 BEV and 25 PHEV models will be introduced over 2016----20202020

Traditional OEMs are entering the EV space, led by Volkswagen, Daimler, GM and Ford: Currently, there are only a few BEV models available in the US and Europe, produced by three main manufacturers: Tesla, BMW and Renault-Nissan. The competitive environment and the number of EV options available to consumers are set to radically alter over the next five years. Traditional OEMs such as Volkswagen, Daimler, GM and Ford have aggressive medium-term EV roll-out plans. Based on their officially announced plans, at least 13 new BEV models and 25 PHEV models across the entire price spectrum (mass market to luxury) will be launched by 2020.

No . o f de a t hs

from a ir

po llu t ion 2 0 12

E c onomic

loss

($ bn)

US 114804 568

China 1600000 1400

G e rma ny 72000 277

UK 52430 202

Fra nc e 52600 185

6975

7700

0

6600

6500

0 10000

USUSUSUS

ChinaChinaChinaChina

GermanyGermanyGermanyGermany

UKUKUKUK

FranceFranceFranceFrance

Direct purchase subsidies on new EV (EUR)

300

170

70

60

0

50

100

150

200

250

300

350

Battery packcost 2015

Cell leveleconomies of

scale

Pack leveleconomies of

scale

Battery packcost 2020

$/kWh

Price premium vs Price premium vs Price premium vs Price premium vs

battery cost savingsbattery cost savingsbattery cost savingsbattery cost savings$'000$'000$'000$'000

Tesla S (70kWh) price

premium over Jaguar

XJ Saloon excl. subsidy

5

Battery price reduction

(2015-20)-9

21

12

49

49

0 20 40 60 80

2015

2020

Battery pack cost $'000 Others

Berenberg Thematics

8

The mass market is where the war will be fought: The main growth market which is likely to open up for EV manufacturers as a result of reduction in battery costs will be the mass market (ie cars priced under $35,000). Although currently the Nissan Leaf and the Renault Zoe are targeted at the mass market, adoption is significantly hindered by their low effective range of below 100 miles. This is set to change in 2016 and 2017, with the launch of two prominent new models – the $35,000 Chevrolet Bolt and the $35,000 Tesla Model 3, both of which will offer a range of ~200 miles. We think that falling battery costs and rising range for smaller EVs will open the mass market for electrification.

The number of EV models available to consumers will rise to 58

by 2020

A 200-mile range (ie the Bolt and Model 3 EVs) will significantly

lower “range anxiety” among mass market EV owners

Source: Berenberg, Company press releases and news reports Source: Berenberg

Factor #4 Factor #4 Factor #4 Factor #4 –––– rapid expansion in charging infrastructure to cut range anxiety rapid expansion in charging infrastructure to cut range anxiety rapid expansion in charging infrastructure to cut range anxiety rapid expansion in charging infrastructure to cut range anxiety –––– China is targeting 5m charging points by 2020China is targeting 5m charging points by 2020China is targeting 5m charging points by 2020China is targeting 5m charging points by 2020

The level of investment in EV charging infrastructure has increased sharply: Global annual spending on EV charging infrastructure rose by more than 3x in 2013-14 versus the prior four years. National, state and city administrations along with automotive OEMs, utilities and charging equipment manufacturers are financing the ongoing investment in charging infrastructure. In countries such as the US, the UK, France and Norway), financial support is available for both residential and high power inter-/intra-city charging points.

The global EV charging network is fast expanding: As a result of the high level of investment, the global EV charging network has more than doubled in terms of the number of slow-charging points and risen by 8x for fast-charging points since end-2012. The US is currently leading in the deployment of public EV charging. However, China has announced plans to set up 5m charging points by 2020 in its attempt to raise EV sales to 5m cars by then. This would likely to ease charging network constraints in its main cities, such as Shanghai and Beijing.

National and state level support resulting in strong growth in public EV charging network

Source: IHS, China 13th five-year development plan, US DoE, Berenberg estimates

0

10

20

30

40

50

60

70

2015 2020BEV PHEV

20202020

58585858

Number

Number

Number

Numberof available EV models

of available EV models

of available EV models

of available EV models

No. o f E V

c ha rg ing

po in t s re la t ive

t o pe t ro l

st a t ions ra t io

Na t iona l support a nd t a rge t s

Ch ina 0.3National target to install 5mn charging

points by 2020

US 0.3

US DoE has invested >0.4bn in

elec trification of the t ransportat ion sec tor.

Numerous state level funding schemes for

charging infrast ruc ture

G e rma ny 0.9 No national support apart from R&D

UK 2.0

EUR44mn spent on set t ing up charging

infrast ruc ture. Subsidy on resident ial

equipment at £700.

Fra nc e 2.0EUR50m allocated to finance 50% of EV

infrast ruc ture charging costs

34,504

Berenberg Thematics

9

Utilities – battery storage to grow from ~$0.5bn to a ~$14bn market

by 2020

In 2015, ~0.5GW of storage was added globally. With an energy to power ratio of ~2x, this translates into ~1GWh of storage capacity added. We expect the energy to power ratio for energy storage systems to rise to 4-5x by 2020 as more load shifting storage systems are installed to integrate renewables. We expect both grid scale and residential/commercial storage to more than double per annum over 2016-2020 as power networks move from being centralised to distributed interconnected systems. By 2020, we expect annual storage installations to rise to 10GW, which translates into ~45GWh of annual storage. Assuming all-in battery costs of ~$300/kWh, this will translate into a market size of ~$14bn by 2020. Rising renewable generation, reduction in battery costs and regulatory requirements will be the main growth drivers.

We believe there are three factors which will drive stationary storage uptake by utilities, the commercial sector and households over the next five years.

Factor #1 Factor #1 Factor #1 Factor #1 –––– rising renewable investment leading to unpredictable generation; rising renewable investment leading to unpredictable generation; rising renewable investment leading to unpredictable generation; rising renewable investment leading to unpredictable generation; there is an increased need for storage for load/frequency management there is an increased need for storage for load/frequency management there is an increased need for storage for load/frequency management there is an increased need for storage for load/frequency management

Battery storage market for frequency smoothing has emerged as renewable generation has increased: Solar and wind power generation as a percentage of total electricity has more than doubled in large economies since 2010. Rising renewables in the electricity mix are making generation more unpredictable and grid balancing more difficult. As a result, battery storage requirements at grid level for frequency smoothing have been increasing globally, led by the US. We expect lithium ion batteries to remain the dominant technology for frequency regulation and other high-power applications.

Renewables integration will require battery storage for load shifting: Currently, the global share of wind and solar as a percentage of electricity generation is ~5% (up from 2% in 2010). In the OECD region, it is relatively higher at ~7% (3.2% in 2010), although it is lower (ie 3%) in China and India. The International Renewable Agency (IRENA) expects a 4x increase in the share of renewables by 2030. This radical jump in variable renewable generation will increase the need for storage in our view, especially for load shifting. Flow batteries could potentially be the preferred technology for load shifting applications.

Stationary energy storage is headed towards strong long-term structural growth

Source: Navigant Research (Jaffe and Adamson, 2014)

Factor #2 Factor #2 Factor #2 Factor #2 –––– the economics of residential “storage plus solar” are improving: the economics of residential “storage plus solar” are improving: the economics of residential “storage plus solar” are improving: the economics of residential “storage plus solar” are improving: microgrids/electricity trading platforms will emergemicrogrids/electricity trading platforms will emergemicrogrids/electricity trading platforms will emergemicrogrids/electricity trading platforms will emerge

Solar and storage costs are fast declining as the scale of manufacturing rises: Battery storage is at the same position of the learning curve as solar PVs were 10-15 years ago. As the scale of manufacturing increases for batteries, we expect the cost of small-scale residential and commercial battery storage to decline from $900/kWh to $500/kWh by 2020E. We also expect the cost of solar PVs to decline by 35% by 2020, in line with its current ongoing downward price trajectory.

Global forecast for utility scale battery storage (MW)

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

0

2000

4000

6000

8000

10000

12000

14000

16000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Annual revenue (USD thousands)

Annual revenue (USD thousands)

Annual revenue (USD thousands)

Annual revenue (USD thousands)

MW

MWMWMW

Annual Capacity (MW) Annual Revenue (USD Thousands)

Berenberg Thematics

10

We expect the cost of electricity for solar PV and storage to fall below retail tariffs in a number of countries: Currently, residential solar generation plus storage is close to breakeven with retail electricity tariff rate only in Germany. Based on the ongoing reduction in battery costs as well as in solar PVs, we estimate the levelised cost (the cost in $/kWh of building and operating the facility over its lifetime) of electricity (LCOE) for solar generation plus storage to fall below the retail electricity tariff in Germany, Australia, the UK and in a number of states in the US by 2020. We expect microgrids – which allow for electricity trading – to emerge in these countries on the back of rising battery adoption.

Batteries plus solar to become cost-effective by 2020 Lithium ion battery costs have more than halved over the last

five years as production has increased

Source: Berenberg, Company press releases and news reports Source: Berenberg

Factor #3 Factor #3 Factor #3 Factor #3 –––– regulatory requirements are bosting storageregulatory requirements are bosting storageregulatory requirements are bosting storageregulatory requirements are bosting storage

Aggressive renewable energy generation targets: High renewable energy targets in Europe and the US are driving uptake of grid scale storage. The state of New York is aiming to produce 50% of its electricity through renewables by 2030. Hawaii is targeting 100% through renewable generation by 2030. Europe has an ambitious target of 20% renewables by 2020.

High regulatory requirements for grid storage in California: The California state authorities have issued direct requirements for grid scale storage; its three largest utilities are required to add more than 1.3GW storage by 2020.

The state of California requires its three largest utilities to add 1.3GW of grid scale storage by 2020

Source: US DoE

US

(California)

US

(average)

Australia

Germany

UK

France

China

0.0

0.1

0.2

0.3

0.4

0.0 0.1 0.2 0.3 0.4

2015 Residential2015 Residential2015 Residential2015 Residential retail tariff rates ($/kWh)retail tariff rates ($/kWh)retail tariff rates ($/kWh)retail tariff rates ($/kWh)

2020 Residential

2020 Residential

2020 Residential

2020 ResidentialSolar plus Storage

Solar plus Storage

Solar plus Storage

Solar plus Storage

LCOE ($/kWh)

LCOE ($/kWh)

LCOE ($/kWh)

LCOE ($/kWh)

2001

2002

2003

2004

2005

2006 2007 20082009

20102011 2012

201320142015y = -15.6x + 718

R² = 89%

0

100

200

300

400

500

600

700

800

900

0 5 10 15 20 25 30 35 40

Production (GWh)

Price ($/kWh)

Renewable target Renewable target Renewable target Renewable target

as % of total by as % of total by as % of total by as % of total by

2030203020302030

New York 50%

Hawaii 100%

Vermont 75%

Europe20% of total

generation by 2020

0 100 200 300 400 500

2014

2016

2018

2020

Southern California Edison

Pacific Gas & Electric

San Diego & Electric

Sorage requirement (MW)Sorage requirement (MW)Sorage requirement (MW)Sorage requirement (MW)

Berenberg Thematics

11

Mass transport – electric bus market to grow from $18bn to $60bn

by 2020

We expect the number of hybrid and pure (battery-only) electric buses (PEBs) to grow on the back of regulatory requirements, a decline in costs and the introduction of new battery and charging technology which will increase their range. Chinese bus manufacturers, led by BYD, are going to drive this growth. Lithium iron phosphate (LFP)-based technology is likely to dominate in the medium term. Similar to our house view on Tesla (see our Great start but sleepy giants are waking up report, dated 2 February 2016), the bus manufacturing “giants” have small to non-existent pure electric bus offerings, which has given smaller OEMs (such as Wright Bus) a head start. This is soon to change, with Daimler’s offering set to enter production after 2018 and MAN’s by 2020. We see Volvo and BYD as the best plays on electric transit – Volvo because of its first-mover advantage relative to other large European OEMs (it is currently testing its pure electric offering in Gothenburg) and BYD because its scale, international success and ability to partner with other OEMs such as ADL to break into new markets.

We dislike smaller OEMs and producers which outsource their electric drivetrains as they will suffer from pricing pressure (unable to sacrifice margin to reduce pricing unlike larger OEMs) and lower margins (giving away too much margin to drivetrain manufacturers in a low margin business) respectively.

We see three reasons for the expected growth in the number of EBs.

Reason #1 Reason #1 Reason #1 Reason #1 –––– regulatory support in China, Europe and US, encouraging electric regulatory support in China, Europe and US, encouraging electric regulatory support in China, Europe and US, encouraging electric regulatory support in China, Europe and US, encouraging electric bus adoption to reduce air pollution blighting urban centresbus adoption to reduce air pollution blighting urban centresbus adoption to reduce air pollution blighting urban centresbus adoption to reduce air pollution blighting urban centres

National funding schemes are financing the electrification of mass transit sector: National funding schemes in the US, Europe and China are supporting the hybridisation of the mass transit sector. China is also providing a hefty purchase subsidy of $75,000 on new EBs.

City/state authorities are taking an active role in phasing out traditional buses: In London, all single-decker buses passing through its ultra emission zone are required to be zero emission by 2020. The city authorities in Copenhagen are aiming for all city buses to be zero emission by 2025, while in California all buses will need to be zero-emission by 2040.

Significant national/local government funding is being provided

for the electrification of mass transit

China’s production has grown by 858% yoy, Yutong has emerged

as a market leader

Source: Berenberg Source: chinabuses.org

Reason #2 Reason #2 Reason #2 Reason #2 –––– EB and charging infrastructure costs are declining with mass EB and charging infrastructure costs are declining with mass EB and charging infrastructure costs are declining with mass EB and charging infrastructure costs are declining with mass adoptionadoptionadoptionadoption

Ongoing reductions in battery costs are making EBs more affordable: Battery pack costs for EBs have declined markedly from c$1,200/kWh in 2009 to c$250-350/kWh today. This has resulted in PEB prices – ie the Proterra – falling from c$1.2m in 2010 to closer to $750,000 today.

Cost of fast-charging equipment for buses is also declining with increased adoption: The cost of a Proterra 500kW charger declined from c$1m in 2010 to c$350k in 2015.

Targets and Targets and Targets and Targets and

subsidiessubsidiessubsidiessubsidies

ChinaChinaChinaChina

Targetting to raise share of new energy buses to 80% by 2019. Purchase subsidy of $75k on an all electric bus

LondonLondonLondonLondon

UKUKUKUK

All single decker vehicles passing through London's ultra low emission zone must be zero emission.

ParisParisParisParis

FranceFranceFranceFrance

RATP Paris to replace its entire 4,800 bus fleet with zero emission vehicles by 2025

55

24

25

135

0 50 100 150

US

Low/No Emission Vehicle

deployment prog.

California

Zero Emission Truck &

Bus P ilot Project

Europe

Zero Emission Urban Bus

projec t

UK

Green Bus fund

US$ m

Berenberg Thematics

12

The cost of EBs and charging infrastructure has more than halved since 2010

Source: Berenberg

Reason #3 Reason #3 Reason #3 Reason #3 –––– new battery and charging new battery and charging new battery and charging new battery and charging technology will reduce range problemstechnology will reduce range problemstechnology will reduce range problemstechnology will reduce range problems

Adoption of LTO-based batteries: Lithium titanate (LTO)-based batteries are able to charge at 10-20x the speed of other lithium-ion-based cells. The adoption of LTO-based cells in mass transport could significantly reduce “range anxiety” by allowing for quick charging at bus stops.

Adoption of high-power electric charging equipment as well as inductive charging reduces recharging times: Proterra and ABB are introducing very high-power charging equipment. Bombardier and Conductix Wampfler offer inductive charging technology.

High-power fast-charging technologies can improve bus

range

Source: Berenberg

We identify six sub-sectors and 18 interesting companies which will

be benefit from greater battery adoption over the next five years

We expect lithium ion batteries to be the dominant technology over the next five years. We believe that a number of sectors across the battery value chain will benefit from strong demand growth for batteries in the power and automotive sectors.

SubSubSubSub----sector #1 sector #1 sector #1 sector #1 –––– automotive/bus OEMs that are focusing on electrification of automotive/bus OEMs that are focusing on electrification of automotive/bus OEMs that are focusing on electrification of automotive/bus OEMs that are focusing on electrification of their product portfoliotheir product portfoliotheir product portfoliotheir product portfolio

We expect rapid expansion in EV penetration over the next five years led by China, the US and Europe. In the US and Europe, Tesla, the Nissan-Renault alliance and BMW are spearheading the electrification of the automotive sector, especially in the BEV space. In China, the EV market is dominated by four local players, led by BYD. These four players have invested strongly over the last five years in 1) lithium ion battery technology, 2)

0

0.2

0.4

0.6

0.8

1

1.2

All electric bus Cost of high power charging point (500kW)

2010 2015

US$ m

$260k costof diesel bus

TechnologyTechnologyTechnologyTechnology Charging powerCharging powerCharging powerCharging power

Charging Charging Charging Charging

time for time for time for time for

300kWh 300kWh 300kWh 300kWh

batterybatterybatterybattery

Proterra Conductive 500kW 36min

ABB Conductive200kW; 400kW

(15s)45-90min

Bombardier Inductive 200kW 45 min

Conductix

WampflerInductive 60-180kW

100-

300min

Berenberg Thematics

13

upgrading their manufacturing facilities to accommodate EVs and 3) setting up their own battery manufacturing facilities or striking partnerships with dominant battery suppliers. We expect them to benefit from the structural demand growth for the next 5-10 years.

We think that the automotive OEMs with the scale and the strongest EV offering will prevail. Traditional OEMS led by Volkswagen, Daimler, GM and Ford have impressive plans for launching new EV models over the next 3-5 years. Their manufacturing scale and strong operating cash flows from their established internal combustion vehicle (ICV) business lines should help finance the investment required to build EV product portfolio while absorbing the associated losses/margin dilution in the mid-term. We discuss the automotive OEMs that we expect to lose out on this growth in the next section.

Autos ranking grid – Tesla in the US and Europe along with BYD in China are likely to retain a significant market share while

traditional OEMs will catch up in the EV space

Source: Berenberg

SubSubSubSub----sector #2 sector #2 sector #2 sector #2 –––– lithium miners: lowlithium miners: lowlithium miners: lowlithium miners: low----cost players will benefit from continued cost players will benefit from continued cost players will benefit from continued cost players will benefit from continued structural increases in structural increases in structural increases in structural increases in lithium prices in the medium termlithium prices in the medium termlithium prices in the medium termlithium prices in the medium term

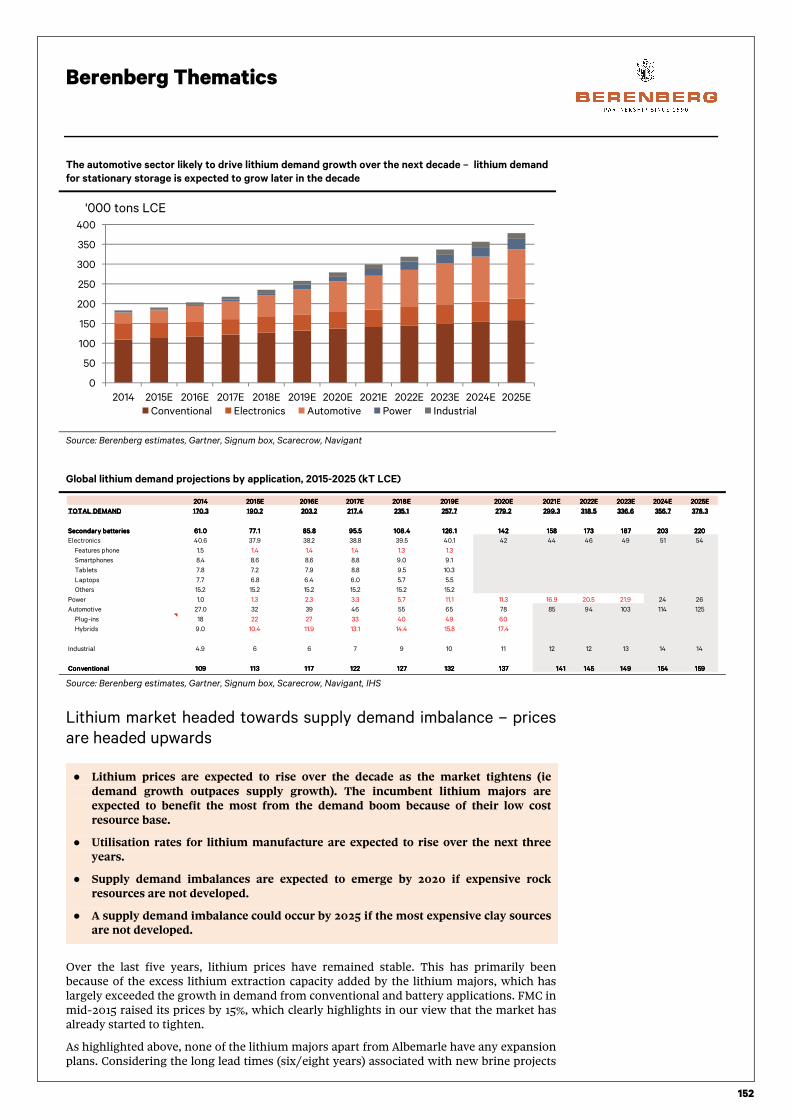

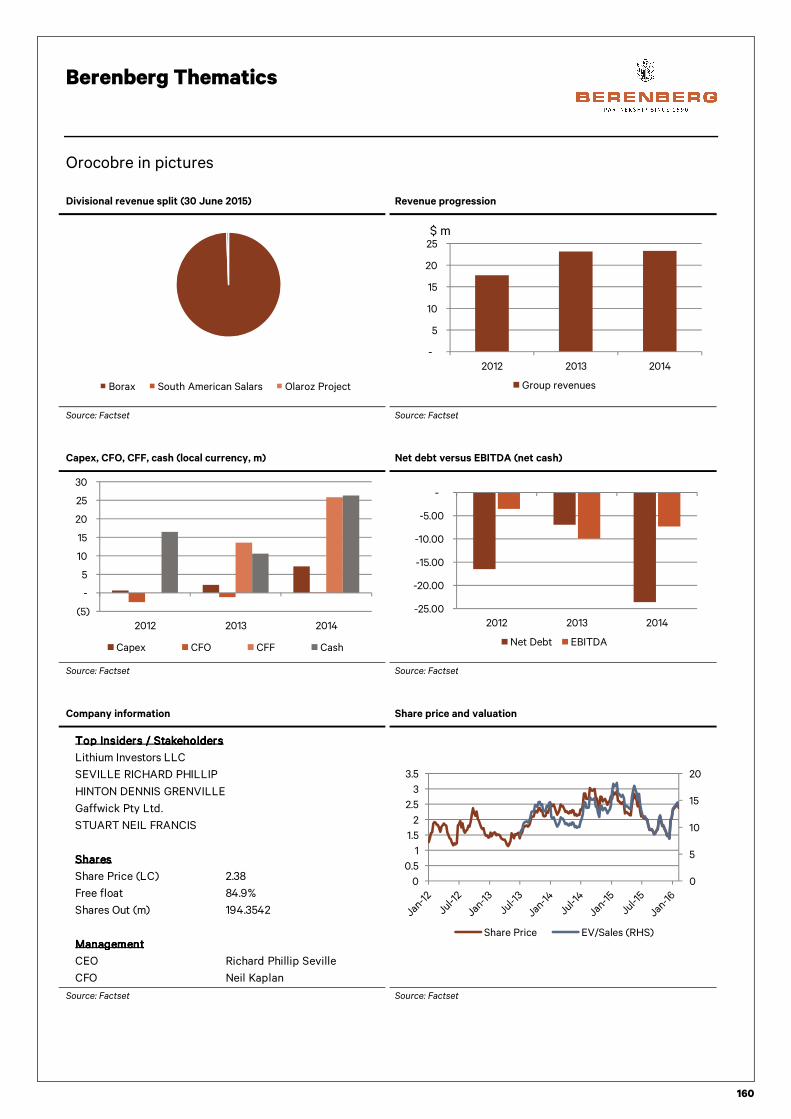

Lithium prices are headed for a structural bull run, with demand from the automotive and power sectors to exceed supply, even under conservative assumptions for EV penetration rates and stationary storage uptake by utilities. We expect global lithium demand to increase by ~60% by 2020. Supply constraints in the medium term due to the long five- to 10-year project development lead times and stringent regulatory requirements are likely to exacerbate the supply demand imbalance. We expect the lithium majors, especially Albemarle, to benefit from the positive price momentum due to the low-cost profile of its projects. Lithium mining “juniors” such as Orocobre and Western Lithium will play a central role in bringing relatively higher-cost resources into the market. Under our base case scenario, we estimate that global supply of lithium will rise by ~25% by 2020. Hence, we expect a structural increase in lithium prices over the next five years.

Lithium miners ranking grid: lithium major Albemarle and minors Orocobre and Western Lithium are bringing 57.5kT (25% of current

capacity) of new lithium manufacturing capacity over the next five years

Source: Berenberg

CompanyCompanyCompanyCompany

(Country, Market cap)

Lithium ion battery and EV Lithium ion battery and EV Lithium ion battery and EV Lithium ion battery and EV

power train technology power train technology power train technology power train technology Charging infrastructureCharging infrastructureCharging infrastructureCharging infrastructure Battery manufacturingBattery manufacturingBattery manufacturingBattery manufacturing

Depth of EV offering Depth of EV offering Depth of EV offering Depth of EV offering

(current/target over 2016-20)(current/target over 2016-20)(current/target over 2016-20)(current/target over 2016-20)Mass transportMass transportMass transportMass transport

Overall exposure to Overall exposure to Overall exposure to Overall exposure to

growth in batteriesgrowth in batteriesgrowth in batteriesgrowth in batteries

TeslaTeslaTeslaTesla

US - USD 21.3bn

VERY HIGHVERY HIGHVERY HIGHVERY HIGH

BYDBYDBYDBYD

China - HKD 125.8bn

VERY HIGHVERY HIGHVERY HIGHVERY HIGH

BMWBMWBMWBMW

Germany - EUR 45.5bn

MEDIUM-HIGHMEDIUM-HIGHMEDIUM-HIGHMEDIUM-HIGH

Renault-NissanRenault-NissanRenault-NissanRenault-Nissan

France - EUR 20.8bn

Japan - JPY 4.9tn

HIGHHIGHHIGHHIGH

VWVWVWVW

Germany - EUR 53.9bn

HIGHHIGHHIGHHIGH

GMGMGMGM

US - USD 44.1bn

HIGHHIGHHIGHHIGH

DaimlerDaimlerDaimlerDaimler

Germany - EUR 64.1bn

HIGHHIGHHIGHHIGH

FordFordFordFord

US - USD 45.4bn

MEDIUMMEDIUMMEDIUMMEDIUM

Note: Level of exposure ranking. 5 Stars= VERY HIGH, 4 Stars = HIGH, 3 stars= MEDIUM, 2 Stars= LOW-MEDIUM,1 Star=LOW

CompanyCompanyCompanyCompany

(Country, Market cap)

Cost profile of the Cost profile of the Cost profile of the Cost profile of the

projectsprojectsprojectsprojects

Status of expansion Status of expansion Status of expansion Status of expansion

projectsprojectsprojectsprojectsPast experiencePast experiencePast experiencePast experience ScaleScaleScaleScale

Share of Lithium in Share of Lithium in Share of Lithium in Share of Lithium in

EarningsEarningsEarningsEarnings

Overall exposure to Overall exposure to Overall exposure to Overall exposure to

growth in batteriesgrowth in batteriesgrowth in batteriesgrowth in batteries

AlbemarleAlbemarleAlbemarleAlbemarle

US - USD 5.8bn

VERY HIGHVERY HIGHVERY HIGHVERY HIGH

OrocobreOrocobreOrocobreOrocobre

Australia - AUD 0.5bn

HIGHHIGHHIGHHIGH

Western LithiumWestern LithiumWestern LithiumWestern Lithium

Canada - CAD 0.1bn

MEDIUMMEDIUMMEDIUMMEDIUM

Note: Level of exposure ranking. 5 Stars= VERY HIGH, 4 Stars = HIGH, 3 stars= MEDIUM, 2 Stars= LOW-MEDIUM,1 Star=LOW

Berenberg Thematics

14

SubSubSubSub----sector #3 sector #3 sector #3 sector #3 –––– cathode manufacturerscathode manufacturerscathode manufacturerscathode manufacturers

The chemicals required for manufacturing lithium ion cells are the main determinants of a battery pack’s performance (ie in terms of storage capacity, life, safety). They are hence the most value added components of the battery storage system and f0rm the bulk of its cost. This is especially true for the active cathode material which forms more than half of the lithium ion cell cost. Specific cathode chemistries have been perfected after years of R&D and are protected by patents. As a result, we believe that speciality chemical companies such as Umicore and BASF hold a significant pricing advantage in an environment where demand for cathode materials is rapidly rising on the back growth in EVs and stationary storage.

We expect that chemical companies with the IPs for the cathode materials such as nickel manganese cobalt (NMC) and nickel cobalt aluminium (NCA) (which are important for automotive applications) to experience the strongest pricing improvement because only a few companies can manufacture battery grade NMC and NCA cathode materials. In contrast, a number of companies in Asia manufacture LFP and LCO (lithium cobalt oxide) cathodes. While demand from storage and EBs is likely to grow strongly for LFP over the next five years, the increasing levels of competition between these players are likely to limit any pricing increase.

Umicore and BASF are the market leaders in NMC- and NCA-based cathode materials and are likely to benefit as rising EV penetration

leads to demand growth over the next five years

Source: Berenberg

SubSubSubSub----sector #4 sector #4 sector #4 sector #4 –––– energy storage battery providersenergy storage battery providersenergy storage battery providersenergy storage battery providers

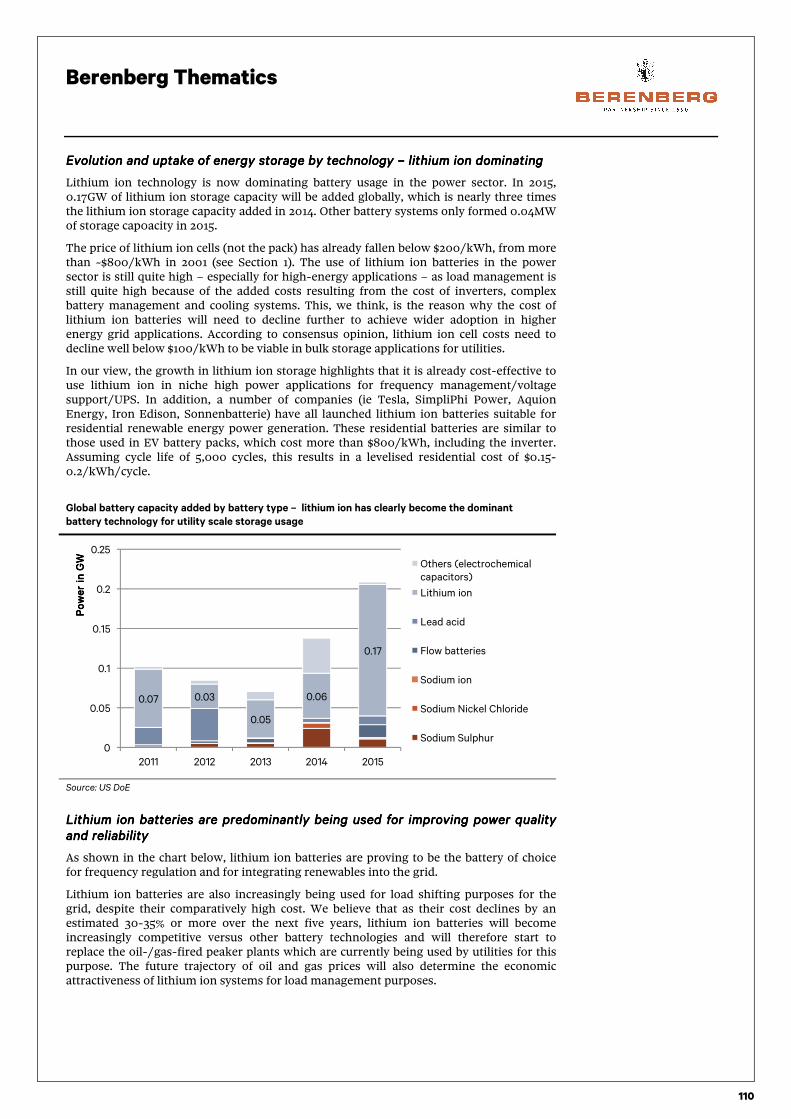

There has been robust growth in the stationary storage segment (yearly installations have doubled since 2010), driven by frequency smoothing requirements. Lithium ion technology is hence dominating because of its high power density. We expect that there will be strong growth in storage for load shifting purposes in order to integrate renewables. IHS expects grid storage to grow to 40GW by 2020 from only 538MW in 2015. We think that flow batteries could prove ideal for load management purposes while lithium ion will continue to dominate the frequency management space. Companies that provide low-cost stationary storage systems are likely to experience strong growth in earnings.

ElectronicsElectronicsElectronicsElectronics EVsEVsEVsEVs BusesBusesBusesBuses Stationary storageStationary storageStationary storageStationary storage

Umicore: Umicore: Umicore: Umicore: Belgium - EUR 3.7bn LCO, NMC, NCA, LFPLCO, NMC, NCA, LFPLCO, NMC, NCA, LFPLCO, NMC, NCA, LFP

JMAT: JMAT: JMAT: JMAT: UK - GBP 4.4bn LFP

BASF: BASF: BASF: BASF: Germany - EUR 52.9bn NMC, LFP

Nichia: Nichia: Nichia: Nichia: Japan - Private LCO, NCM, LMO

Toda Kogyo: Toda Kogyo: Toda Kogyo: Toda Kogyo: Japan - JPY 16.4bn LCO, LMO, LFP

Sumitomo Chemicals: Sumitomo Chemicals: Sumitomo Chemicals: Sumitomo Chemicals: Japan - JPY 917.1bn LMO

Tanaka Chemicals: Tanaka Chemicals: Tanaka Chemicals: Tanaka Chemicals: Japan - JPY 12.2bn NMC

Nippon Chemicals: Nippon Chemicals: Nippon Chemicals: Nippon Chemicals: Japan - JPY 20.5bn LCO, NMC

3M: 3M: 3M: 3M: US - USD 94.5bn NMC

AGC Seimi Chemicals: AGC Seimi Chemicals: AGC Seimi Chemicals: AGC Seimi Chemicals: Japan - Private NMC

Targray: Targray: Targray: Targray: Canada - Private LCO, LFP, NCM, NCA

Merck KGaA: Merck KGaA: Merck KGaA: Merck KGaA: Germany - EUR 32.1bn LCO, LFP

L&F Material: L&F Material: L&F Material: L&F Material: South Korea - Private LCO, LFP

Fuji Pigment: Fuji Pigment: Fuji Pigment: Fuji Pigment: Japan - Private LCO, LFP

Honjo ChemicaHonjo ChemicaHonjo ChemicaHonjo Chemical: Japan - Private LCO, LFP

Citic Guoan Mengguli: Citic Guoan Mengguli: Citic Guoan Mengguli: Citic Guoan Mengguli: China - Private LCO, LFP

Reshine New Material: Reshine New Material: Reshine New Material: Reshine New Material: China - Private LCO, LFP

Pulead Technology: Pulead Technology: Pulead Technology: Pulead Technology: China - Private LCO, LFP

Seimi Tongda Lithium Energy: Seimi Tongda Lithium Energy: Seimi Tongda Lithium Energy: Seimi Tongda Lithium Energy: China - Private LCO, LFP

Shanshan Tech: Shanshan Tech: Shanshan Tech: Shanshan Tech: China - Private LCO, LFP

B&M Science and Technology: B&M Science and Technology: B&M Science and Technology: B&M Science and Technology: China - Private LCO, LFP

Henan Kelong New Energy Co: Henan Kelong New Energy Co: Henan Kelong New Energy Co: Henan Kelong New Energy Co: China - Private NCM

NEI Corp: NEI Corp: NEI Corp: NEI Corp: US - Private LTO, LMNO, LMO, NCA

Target marketTarget marketTarget marketTarget marketType of Cathode Type of Cathode Type of Cathode Type of Cathode

MaterialsMaterialsMaterialsMaterials

CompanyCompanyCompanyCompany

(Country, Market cap)(Country, Market cap)(Country, Market cap)(Country, Market cap)

Berenberg Thematics

15

Exposure by key market – Maxwell, RedT, Leclanché, Ceres and Intelligent Energy all represent potentially attractive technology

acquisitions for larger automotive OEMs and battery manufacturers

Source: Berenberg

SubSubSubSub----sector #5sector #5sector #5sector #5 –––– solar integrators, power management, residential storage solar integrators, power management, residential storage solar integrators, power management, residential storage solar integrators, power management, residential storage vendors and microvendors and microvendors and microvendors and micro----grid operatorsgrid operatorsgrid operatorsgrid operators

We think that the ongoing reduction in the cost of batteries and solar panels will expedite the move towards distributed power generation and distribution. We think that micro grids and energy trading platforms will develop in countries with high electricity retail tariffs and fixed grid charges such as Germany, Australia, the UK and a number of states in the US. Solar PV providers, residential storage and other important equipment suppliers such as invertors are expected to benefit.

Exposure by key market

Source: Berenberg

SubSubSubSub----sector #6sector #6sector #6sector #6 –––– nextnextnextnext----generation lgeneration lgeneration lgeneration lithium ion technology providersithium ion technology providersithium ion technology providersithium ion technology providers

We think that the next stage in the evolution of battery technology will follow on from the intensive R&D currently being carried out to develop advanced lithium ion batteries, which have a higher proportion of active materials than other battery types and hence greater energy storage capacity. At the same time, the development of new cell chemistries which can simplify manufacturing methods and reduce costs could be a game-changer in terms of battery adoption. There are promising signs that ongoing R&D into semi-solid and solid-state lithium ion batteries could deliver the next step-up in energy density for batteries.

CompanyCompanyCompanyCompany

(Country, Market cap)

Grid scale Grid scale Grid scale Grid scale

storage/generationstorage/generationstorage/generationstorage/generation

Residential/commeResidential/commeResidential/commeResidential/comme

rcial storage/ rcial storage/ rcial storage/ rcial storage/

generationgenerationgenerationgeneration

Transportation - Transportation - Transportation - Transportation -

Electric Electric Electric Electric

cars/buses/truckscars/buses/truckscars/buses/truckscars/buses/trucks

Overall exposure to Overall exposure to Overall exposure to Overall exposure to

transport electrification, transport electrification, transport electrification, transport electrification,

distributed distributed distributed distributed

generation/storagegeneration/storagegeneration/storagegeneration/storage

DetailsDetailsDetailsDetails

Maxwell TechnologiesMaxwell TechnologiesMaxwell TechnologiesMaxwell Technologies

US - USD 0.2bn

VERY HIGHVERY HIGHVERY HIGHVERY HIGH

Leading supplier of ultracapacitors ideal for the start stop car

market to grow from 22m to 56m vehicles by 2020. Other target

growth market is for ultracapacitors are renewable energy capacity

firming at the grid level, wind turbine (pitch control) etc

Johnson ControlJohnson ControlJohnson ControlJohnson Control

US - USD 23.2bn

MEDIUMMEDIUMMEDIUMMEDIUM

Johnson Control is investing $555m in increasing its capacity to

manufacture advanced lead-acid batteries to be used in the start

stop market for cars and buses. The company also sees the

possibility of targeting stationary storage market

Saft Saft Saft Saft

France - EUR 0.6bn

VERY HIGHVERY HIGHVERY HIGHVERY HIGH Major Li-ion battery manufacturer supplying industrial, aerospace

and stationary storage application at grid and residential level.

RedT EnergyRedT EnergyRedT EnergyRedT Energy

UK - GBP 35m

VERY HIGHVERY HIGHVERY HIGHVERY HIGH

RedT is one of the leading companies working on flow batteries for

large scale load management purposes. The demand for load

management is expected to see strong growth as renewable

generation continues to rise

LeclancheLeclancheLeclancheLeclanche

Switzerland - CHF 90m

VERY HIGHVERY HIGHVERY HIGHVERY HIGH Lithium ion battery manufacturer for stationary storage (grid and

residential scale) and automotiove applications.

CeresCeresCeresCeres

UK - GBP 50m

HIGHHIGHHIGHHIGHDeveloper of low cost fuel cells able to run on natural gas.The key

markets for its fuel cells are residential electricity and heat

generation units and back up power for the commercial market.

Intellligent EnergyIntellligent EnergyIntellligent EnergyIntellligent Energy

UK - GBP 55m

HIGHHIGHHIGHHIGH

Leading developer of hydrogen fuel cells for automotive, back up

power and electronics. The company has won an important power

management contract to provide backup electricity to Telecom

stations in India

Note: Level of exposure ranking. 5 Stars= VERY HIGH, 4 Stars = HIGH, 3 stars= MEDIUM, 2 Stars= LOW-MEDIUM,1 Star=LOW

CompanyCompanyCompanyCompany

(Country, Market cap)

Renewable Renewable Renewable Renewable

generationgenerationgenerationgenerationResidential storageResidential storageResidential storageResidential storage

Microgrid-electrity Microgrid-electrity Microgrid-electrity Microgrid-electrity

trading platformtrading platformtrading platformtrading platform

Battery management Battery management Battery management Battery management

systemssystemssystemssystems

Overall exposure to Overall exposure to Overall exposure to Overall exposure to

renewable generation & renewable generation & renewable generation & renewable generation &

storagestoragestoragestorage

DetailsDetailsDetailsDetails

Solar City Solar City Solar City Solar City

US - USD 2.9bn

HIGHHIGHHIGHHIGHSolar City is the leading seller, Installer and financier of solar panale in US

and has 33% of the residential market. It now be selling/leasing Tesla's

storage products together with its solar panels in the US market.

SMA SMA SMA SMA

Germany - EUR 1.3bn

HIGHHIGHHIGHHIGHSMA is globally the largest proider of inverters for residential solar

generation. It also has an extyensive product portfolio of inverters for

residential and commercial storage market.

InfineonInfineonInfineonInfineon

Germany - EUR 11.9bn

HIGHHIGHHIGHHIGH

Infineon is the third largest supplier of semiconductors for the automotive

sector. These are used in the power train, battrey management systems

and sensors within the vehicle. EVs have more than double semi content

versus an ICV. Rising EV penetration should benefit Infineon.

Note: Level of exposure ranking. 5 Stars= VERY HIGH, 4 Stars = HIGH, 3 stars= MEDIUM, 2 Stars= LOW-MEDIUM,1 Star=LOW

Berenberg Thematics

16

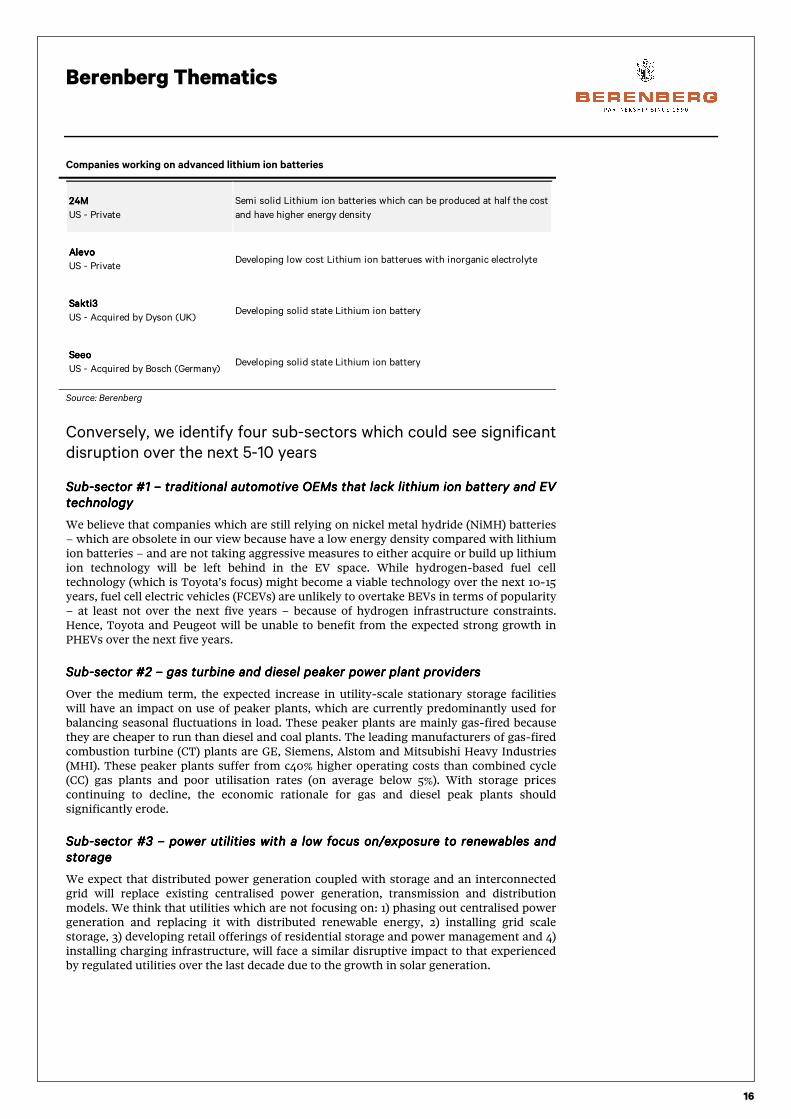

Companies working on advanced lithium ion batteries

Source: Berenberg

Conversely, we identify four sub-sectors which could see significant

disruption over the next 5-10 years

SubSubSubSub----sector #1 sector #1 sector #1 sector #1 –––– traditional automotive OEMs that lack lithium ion battery and EV traditional automotive OEMs that lack lithium ion battery and EV traditional automotive OEMs that lack lithium ion battery and EV traditional automotive OEMs that lack lithium ion battery and EV technologytechnologytechnologytechnology

We believe that companies which are still relying on nickel metal hydride (NiMH) batteries – which are obsolete in our view because have a low energy density compared with lithium ion batteries – and are not taking aggressive measures to either acquire or build up lithium ion technology will be left behind in the EV space. While hydrogen-based fuel cell technology (which is Toyota’s focus) might become a viable technology over the next 10-15 years, fuel cell electric vehicles (FCEVs) are unlikely to overtake BEVs in terms of popularity – at least not over the next five years – because of hydrogen infrastructure constraints. Hence, Toyota and Peugeot will be unable to benefit from the expected strong growth in PHEVs over the next five years.

SubSubSubSub----sector #2 sector #2 sector #2 sector #2 –––– gas turbine and diesel peaker power plant providersgas turbine and diesel peaker power plant providersgas turbine and diesel peaker power plant providersgas turbine and diesel peaker power plant providers

Over the medium term, the expected increase in utility-scale stationary storage facilities will have an impact on use of peaker plants, which are currently predominantly used for balancing seasonal fluctuations in load. These peaker plants are mainly gas-fired because they are cheaper to run than diesel and coal plants. The leading manufacturers of gas-fired combustion turbine (CT) plants are GE, Siemens, Alstom and Mitsubishi Heavy Industries (MHI). These peaker plants suffer from c40% higher operating costs than combined cycle (CC) gas plants and poor utilisation rates (on average below 5%). With storage prices continuing to decline, the economic rationale for gas and diesel peak plants should significantly erode.

SubSubSubSub----sector #3 sector #3 sector #3 sector #3 –––– power utilities with a low power utilities with a low power utilities with a low power utilities with a low focusfocusfocusfocus on/exposure to renewables and on/exposure to renewables and on/exposure to renewables and on/exposure to renewables and storagestoragestoragestorage

We expect that distributed power generation coupled with storage and an interconnected grid will replace existing centralised power generation, transmission and distribution models. We think that utilities which are not focusing on: 1) phasing out centralised power generation and replacing it with distributed renewable energy, 2) installing grid scale storage, 3) developing retail offerings of residential storage and power management and 4) installing charging infrastructure, will face a similar disruptive impact to that experienced by regulated utilities over the last decade due to the growth in solar generation.

24M 24M 24M 24M

US - Private

Semi solid Lithium ion batteries which can be produced at half the cost

and have higher energy density

Alevo Alevo Alevo Alevo

US - PrivateDeveloping low cost Lithium ion batterues with inorganic electrolyte

Sakti3Sakti3Sakti3Sakti3

US - Acquired by Dyson (UK)Developing solid state Lithium ion battery

Seeo Seeo Seeo Seeo

US - Acquired by Bosch (Germany)Developing solid state Lithium ion battery

Berenberg Thematics

17

Utilities ranking grid – RWE, E.ON and Enel have the lowest risk of disruption among European utilities because of their exposure to

renewables and storage

Source: Berenberg

SubSubSubSub----sector sector sector sector #4 #4 #4 #4 –––– largelargelargelarge----scale lithium ion battery manufacturers scale lithium ion battery manufacturers scale lithium ion battery manufacturers scale lithium ion battery manufacturers are are are are likely to suffer likely to suffer likely to suffer likely to suffer from capacity overhang anfrom capacity overhang anfrom capacity overhang anfrom capacity overhang andddd weak battery pricing weak battery pricing weak battery pricing weak battery pricing

There continues to be 40-50% overcapacity in lithium ion battery manufacturing for both the electronics and automotive sectors. Continued capacity expansion by Asian players such as LG Chem, Samsung and Panasonic over the last decade have commoditised the market. The level of competition and capacity overhang should rise further as a result of the giant battery manufacturing facilities being set up by the likes of Tesla/Panasonic and BYD. Margins for battery manufacturers are likely to remain under pressure in the mid-term.

Risk to thesis

The risks associated with the growth of lithium ion batteries in automotive and stationary storage relate to regulation, incentives, environmental impacts and security of supply for critical materials. These are long-term risks and can negatively affect the cost trajectory for batteries and their adoption in the transportation and power sectors.

1) Regulatory risk: Any abrupt elimination or lowering of subsidies/incentives on EVs or continued restrictions on stationary storage at grid level in Europe could impede growth in batteries.

2) Security of supply: Cobalt and natural graphite have high supply risk, according to the European Commission. This is because supply of both materials is highly concentrated, 56% of global cobalt production comes from the Congo and 69% of natural graphite from China. Both materials are critical for lithium ion battery manufacturing.

3) Environmental: Only 1% of lithium ion batteries are recycled. Virgin manufacturing of cathode materials for batteries is more pollutive than recycled cathode materials.

CompanyCompanyCompanyCompany

(Country, Market cap)

Distributed renewable Distributed renewable Distributed renewable Distributed renewable

generation (excl. generation (excl. generation (excl. generation (excl.

hydro)hydro)hydro)hydro)

Grid scale storageGrid scale storageGrid scale storageGrid scale storageRetail residential Retail residential Retail residential Retail residential

storage offeringstorage offeringstorage offeringstorage offering

Charging infrastructure Charging infrastructure Charging infrastructure Charging infrastructure

deploymentdeploymentdeploymentdeployment

RISK OF RISK OF RISK OF RISK OF

DISRUPTIONDISRUPTIONDISRUPTIONDISRUPTION

RWERWERWERWE

Germany - EUR 7.4bnLOWLOWLOWLOW

E.ONE.ONE.ONE.ON

Germany - EUR 18.1bnLOWLOWLOWLOW

EnelEnelEnelEnel

Italy - EUR 33.1bnLOWLOWLOWLOW

FortumFortumFortumFortum

Finland - EUR 10.8bnHIGHHIGHHIGHHIGH

GDF Suez - EngieGDF Suez - EngieGDF Suez - EngieGDF Suez - Engie

France - EUR 34.0bnHIGHHIGHHIGHHIGH

IberdrolaIberdrolaIberdrolaIberdrola

Spain - EUR 39.5bnMEDIUMMEDIUMMEDIUMMEDIUM

VerbundVerbundVerbundVerbund

Austria - EUR 3.7bnHIGHHIGHHIGHHIGH

CentricaCentricaCentricaCentrica

UK - GBP 9.7bnVery HIGHVery HIGHVery HIGHVery HIGH

Red ElectricaRed ElectricaRed ElectricaRed Electrica

Spain - EUR 9.9bnVery HIGHVery HIGHVery HIGHVery HIGH

EDFEDFEDFEDF

France - EUR 22.4bnHIGHHIGHHIGHHIGH

SSESSESSESSE

UK - GBP 13.8bnMEDIUMMEDIUMMEDIUMMEDIUM

TernaTernaTernaTerna

Spain - EUR 9.3bnLOW-MEDIUMLOW-MEDIUMLOW-MEDIUMLOW-MEDIUM

National GridNational GridNational GridNational Grid

UK - GBP 35.7bnLOW-MEDIUMLOW-MEDIUMLOW-MEDIUMLOW-MEDIUM

Note: Level of exposure ranking. 5 Stars= VERY HIGH, 4 Stars = HIGH, 3 stars= MEDIUM, 2 Stars= LOW-MEDIUM,1 Star=LOW

Berenberg Thematics

18

Section 1: Batteries – market overview

“The Stone Age did not end due to the scarcity of stones; the oil age will not end with the scarcity of oil.”

Sheik Yamani – former oil minister, Saudi Arabia

● The evolution of battery technology has accelerated in recent years with the discovery of new cell chemistries. Lead times for new technology development from discovery to mass adoption can be 10-15 years.

● We believe that lithium ion will dominate and will provide the next leg of growth for rechargeable batteries. This is due to the rapid reduction in its cost over the last five years as well as continued improvement storage capacity (energy density). There are other new technologies which hold promise (ie lithium sulphur and lithium air) but which are still at the concept stage.

● Rechargeable batteries are moving closer to mass adoption in the automotive and power sector over the next five years due to:

o tightening emission and fuel consumption requirements for the automotive sector, aimed at encouraging OEMs to focus on their EV offerings (CO2 emission target by regulators 2021: Europe – 95g/km from 130g/km in 2015; the US – 106.9g/km from 140g/km in 2016; China – the 2020 fuel consumption requirement: 5litres/100km from 6.9L/100km in 2015);

o rising renewable power generation (at 22% of global power generation in 2013), which is making electricity generation unpredictable and hence would encourage utilities to adopt stationary storage for frequency and load management purposes – further, demand for utility scale storage to intensify with the International Energy Agency (IEA) projecting that non-hydro renewable sources will form ~half (ie 600GW) of all global capacity additions over 2014-20;

o lithium ion battery development following a similar learning curve as electronics and solar PVs – battery cell costs have halved in just the last five years from $440/kWh to $200/kWh in 2015.

o a fall in lithium ion battery costs by 40-45% by 2020 resulting from a 30-35% cost reduction from economies of scale at the cell level economies of scale and a 20% cost reduction from economies of scale at the pack level.

Energy storage has long appealed to our imagination in ways it can potentially transform the way we live. However, technological limitations and high costs have meant that their use in automotive and power applications have been limited. As a result, our reliance on traditional and more reliable energy sources, predominantly fossil fuels, remains. Increasing adoption of renewable power over the last decade has increased volatility in electricity generation. As a result, the need to develop better and more cost-effective battery systems to make power distribution systems more efficient has increased. At the same time, tightening regulatory limits on car emissions have prompted OEMs to increase their focus on EV offerings to consumers. The recent scandal at Volkswagen, when the company was caught using cheat devices manipulating car emission results, has undermined the credibility of the diesel engine as the right technology to meet future emission requirements and should further enhance OEMs’ R&D focus on EVs. The ongoing steep decline in battery prices should spur adoption of battery storage for power and automotive applications.

How does a battery work?

There are a number of different components to a battery, each made from a material which performs a specific function to trigger the electrochemical reaction that converts stored chemical energy into electrical energy. The chemical reaction in a battery involves the transfer of electrons through the movement of ions and is known as an oxidation-reduction reaction, or “redox” reaction.

Berenberg Thematics

19

Key parts of a battery, their function and the materials used

Source: Berenberg CGGC

How does a battery work? Batteries work via redox reactions Structure of a cylindrical battery

Source: Berenberg, epg.eng.ox.ac.uk

Introduction to energy storage technologies

Battery storage systems’ evolution has been marked by jumps in performance through the discovery of new materials, followed by long periods of efficiency improvements through experimentation with battery composition/structure.

The timeline below illustrates the development of battery storage systems since the creation of the early form of lead acid battery in 1859. Of note:

1) new battery technologies have generally not replaced but complemented the older

systems;

2) there has been no major breakthrough in battery technology for more than two

decades since the introduction of lithium ion batteries in the 1990s.

The first point can be explained by the varying attributes of different battery storage systems such as cost, weight, thermal stability, product life and energy to power requirements. These differences determine the applications for which each battery technology is suitable.

PartPartPartPart FunctionFunctionFunctionFunction MaterialsMaterialsMaterialsMaterials

Anode

(Negative Electrode)

Receives Lithium-ions from the Cathode when charging and emits

to Cathode when discharging.

Made from metals/compounds with very few electrons in their

valence shells

Cathode

(Positive Electrode)

Receives Lithium-ions from the Anode when discharging and emits

to Anode when charging.

Made from metals/compounds that have nearly full valence shells

such as compounds including oxygen, chlorine or both.

ElectrolyteIonic conductor and electric insulator that allows Lithium-ions to

pass between Anode and Cathode

Typically an acid/base (alkaline) or salt solution e.g. Lithium salts

or an organic solvent

SeparatorProvides insultaion between the Anode and Cathode. If the Anode

and Cathode were not separated, the battery would short circuit.Micro-porous membranes

Can The outer container for the chemicals inside Metal

Berenberg Thematics

20

Battery technology timeline Energy storage characteristics

Source: Continental Source: Berenberg estimates

There are four mainstream secondary/rechargeable battery technologies – lead acid, sodium sulphur, NiMH and lithium ion. Lead acid batteries are predominantly used as common car batteries, for uninterrupted power systems (UPS) back-up power and grid support for utilities. NiMH is predominantly used in electronics and in hybrid EVs. However, it is increasingly being replaced by high density lithium ion as the latter’s cost declines. Sodium sulphur batteries, also called molten salt batteries, have been used for peak power management, especially in Japan; however, they have suffered from serious operational and safety issues. Utilities are increasingly using lithium ion storage systems for grid support, as they perform better and cost less. However, utility scale applications will always require a mix of battery systems as each type has its own relative advantages.

Energy density, cost and stage of development for different battery technologies

Source: Thermodynamic analysis on energy density of batteries, DOE/EPRI Electricity Storage Handbook in Collaboration with NRECA Continental, Berenberg estimates

Specific EV battery Specific EV battery Specific EV battery Specific EV battery

requirementsrequirementsrequirementsrequirementsMetricMetricMetricMetric

1. Energy densityAlso called volumetric energy density.

kWh per unit volume i.e. kWh/l

2. Specific Energy kWh/kg

3. Power DensityPeak power per unit of battery volume i.e.

W/l

4. Cost $/kWh

5. Durability Cycle life

0

100

200

300

400

500

600

700

800

900

1000

Lead acid SodiumSulphur

NiMH Li-ion AdvancedLi-ion

Sodium ion SodiumNickelChloride

Li-Sulphur Li air Sodium air

Energy density (Wh/kg)

Price ($/kWh) 269 270 900 300 <200 <200 400 380 n.a. n.a.

MainstreamUnder

DevelopmentR&D

High temperature batteries

Berenberg Thematics

21

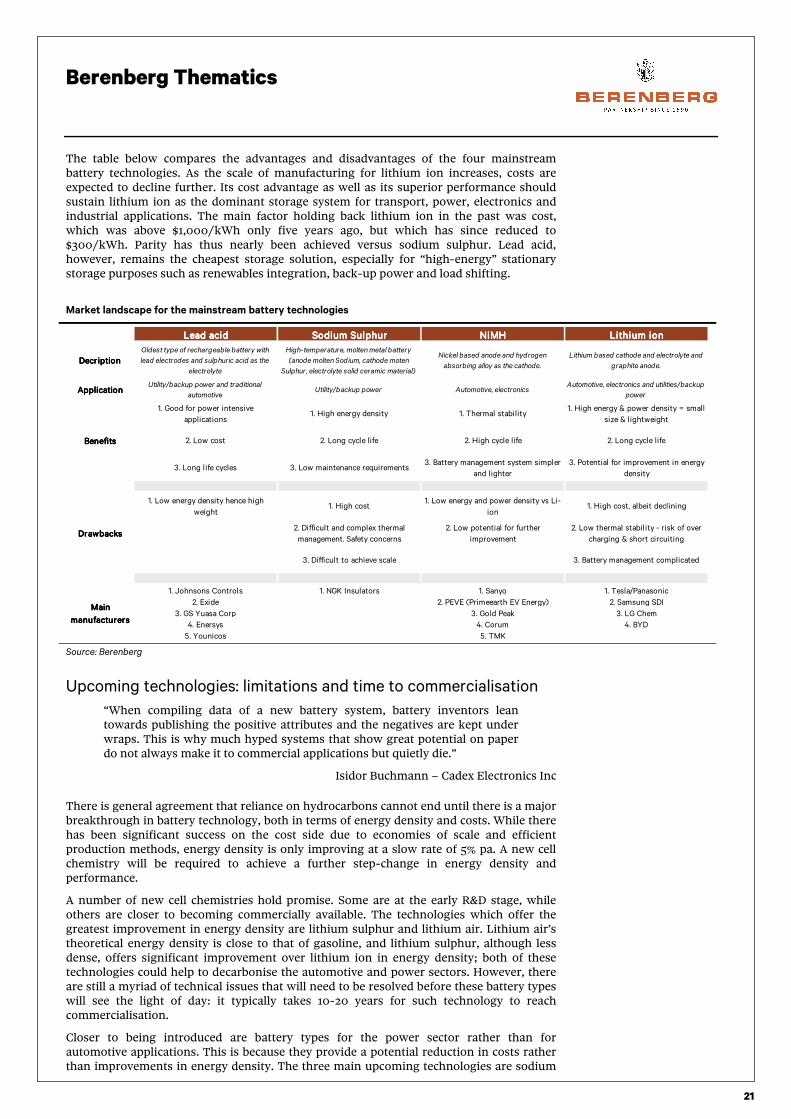

The table below compares the advantages and disadvantages of the four mainstream battery technologies. As the scale of manufacturing for lithium ion increases, costs are expected to decline further. Its cost advantage as well as its superior performance should sustain lithium ion as the dominant storage system for transport, power, electronics and industrial applications. The main factor holding back lithium ion in the past was cost, which was above $1,000/kWh only five years ago, but which has since reduced to $300/kWh. Parity has thus nearly been achieved versus sodium sulphur. Lead acid, however, remains the cheapest storage solution, especially for “high-energy” stationary storage purposes such as renewables integration, back-up power and load shifting.

Market landscape for the mainstream battery technologies

Source: Berenberg

Upcoming technologies: limitations and time to commercialisation

“When compiling data of a new battery system, battery inventors lean towards publishing the positive attributes and the negatives are kept under wraps. This is why much hyped systems that show great potential on paper do not always make it to commercial applications but quietly die.”

Isidor Buchmann – Cadex Electronics Inc

There is general agreement that reliance on hydrocarbons cannot end until there is a major breakthrough in battery technology, both in terms of energy density and costs. While there has been significant success on the cost side due to economies of scale and efficient production methods, energy density is only improving at a slow rate of 5% pa. A new cell chemistry will be required to achieve a further step-change in energy density and performance.

A number of new cell chemistries hold promise. Some are at the early R&D stage, while others are closer to becoming commercially available. The technologies which offer the greatest improvement in energy density are lithium sulphur and lithium air. Lithium air’s theoretical energy density is close to that of gasoline, and lithium sulphur, although less dense, offers significant improvement over lithium ion in energy density; both of these technologies could help to decarbonise the automotive and power sectors. However, there are still a myriad of technical issues that will need to be resolved before these battery types will see the light of day: it typically takes 10-20 years for such technology to reach commercialisation.

Closer to being introduced are battery types for the power sector rather than for automotive applications. This is because they provide a potential reduction in costs rather than improvements in energy density. The three main upcoming technologies are sodium

Lead acidLead acidLead acidLead acid Sodium SulphurSodium SulphurSodium SulphurSodium Sulphur NiMHNiMHNiMHNiMH Lithium ionLithium ionLithium ionLithium ion

ApplicationApplicationApplicationApplicationUtility/backup power and traditional

automotiveUtility/backup power Automotive, electronics

Automotive, electronics and utilities/backup

power

1. Good for power intensive

applications1. High energy density 1. Thermal stability

1. High energy & power density = small

size & lightweight

2. Low cost 2. Long cycle life 2. High cycle life 2. Long cycle life

3. Long life cycles 3. Low maintenance requirements3. Battery management system simpler

and lighter

3. Potential for improvement in energy

density

1. Low energy density hence high

weight1. High cost

1. Low energy and power density vs Li-

ion1. High cost, albeit declining

2. Difficult and complex thermal

management. Safety concerns

2. Low potential for further

improvement

2. Low thermal stability - risk of over

charging & short circuiting

3. Difficult to achieve scale 3. Battery management complicated

1. Johnsons Controls 1. NGK Insulators 1. Sanyo 1. Tesla/Panasonic

2. Exide 2. PEVE (Primeearth EV Energy) 2. Samsung SDI

3. GS Yuasa Corp 3. Gold Peak 3. LG Chem

4. Enersys 4. Corum 4. BYD

5. Younicos 5. TMK

High-temperature, molten metal battery

(anode molten Sodium, cathode moten

Sulphur, electrolyte solid ceramic material)

Nickel based anode and hydrogen

absorbing alloy as the cathode.

Lithium based cathode and electrolyte and

graphite anode.

BenefitsBenefitsBenefitsBenefits

DrawbacksDrawbacksDrawbacksDrawbacks

Main Main Main Main

manufacturersmanufacturersmanufacturersmanufacturers

DecriptionDecriptionDecriptionDecription

Oldest type of rechargeable battery with

lead electrodes and sulphuric acid as the

electrolyte

Berenberg Thematics

22

ion, sodium nickel chloride and flow batteries, which could open up bulk storage opportunities for utilities in the power sector, provided that storage costs can be reduced below $100/kWh.

However, in our view, the batteries that offer the most scope for commercial success over the next five years are advanced lithium ion batteries. Advanced lithium ion batteries are the next evolutionary step for traditional lithium ion, and could potentially double energy density and be cheaper to operate. Measures to increase the energy density of traditional lithium ion include:

1) doping the graphite anode with silicon to increase its charge carrying capacity;

2) experimenting with lithium-based cathode material;

3) reducing the inactive materials used in cell construction;

4) moving towards semi-solid and solid-state lithium ion batteries.

The following table outlines the upcoming battery technologies and their key benefits and drawbacks.

Market overview of upcoming battery technologies

Source: Berenberg estimates

Sodium ionSodium ionSodium ionSodium ionSodium Nickel Sodium Nickel Sodium Nickel Sodium Nickel

ChlorideChlorideChlorideChlorideFlow batterriesFlow batterriesFlow batterriesFlow batterries

Semi solid/solid state Semi solid/solid state Semi solid/solid state Semi solid/solid state

Lithium ionLithium ionLithium ionLithium ionLithium SulphurLithium SulphurLithium SulphurLithium Sulphur Lithium airLithium airLithium airLithium air

Based on molten Sodium

and nickel electrodes

A solid state battery with

oxidation of Lithium at the

anode and oxygen reduction

at cathode to generate

current

ApplicationsApplicationsApplicationsApplications Utilitity/backup power Utility/backup power

and automotiveUtility/backup power

Automotive and

utility/backup power

Initially niche applications:

Military, aerospace etc

Initially niche applications:

Military, aerospace etc

1. Low cost (<

$200/kWh)

1. Good for long duration

energy storage

applications

1. Costs lower versus

traditional lithium ion

batteries

1. 5x theoretical energy

density as Li-ion

1. Theoretical energy

approaching that for

gasoline

2. Thermal stability.

Relatively safe versus

Lithium ion