BDC Basics: What Every New BDC Must Know Before Launching · What Every New BDC Must Know Before...

56

BDC Basics: What Every New BDC Must Know Before Launching January 30, 2013

-

Upload

duongtuyen -

Category

Documents

-

view

218 -

download

0

Transcript of BDC Basics: What Every New BDC Must Know Before Launching · What Every New BDC Must Know Before...

BDC Basics:What Every New BDC Must Know Before Launching

January 30, 2013

©2013 Sutherland Asbill & Brennan LLP2

BDC Basics

• Part I: History and Overview of the BDC Model

• Part II: Regulatory and Reporting Requirements

• Part III: Management and Operational Considerations

• Part IV: BDC Structures

©2013 Sutherland Asbill & Brennan LLP3

Part I:History and Overview

of the BDC Model

©2013 Sutherland Asbill & Brennan LLP4

Overview

• Created by Congress in 1980 to promote financing to small, growing businesses.

• Special type of closed-end fund regulated under the Investment Company Act of 1940 (the “1940 Act”): Provides small, growing companies access to capital

Enables private equity funds to access public capital markets

Enables retail investors to participate in the upside of pre-IPO investing with complete liquidity

Traditional listed BDC may sell to all retail investors

Non-listed BDC enables accredited retail investors to participate in the upside of pre-IPO investing, but with limited liquidity

• Typically structured as Regulated Investment Company (“RIC”) for tax purposes

• Hybrid between an operating company and an investment company

©2013 Sutherland Asbill & Brennan LLP5

Benefits of the BDC Model

• Access to public capital markets

• Shares may be traded on national exchanges

• Flow-through tax treatment as a RIC

• Reduced burden under 1940 Act, as compared to registered closed-end funds Restrictions on leverage Restrictions on affiliated transactions

• External model permits management fee and “carried interest” incentive fee structure

• Publicly available financial information through quarterly reporting

• Portfolio is diversified to comply with RIC tax requirements Reduces risk typically associated with private equity investments

©2013 Sutherland Asbill & Brennan LLP6

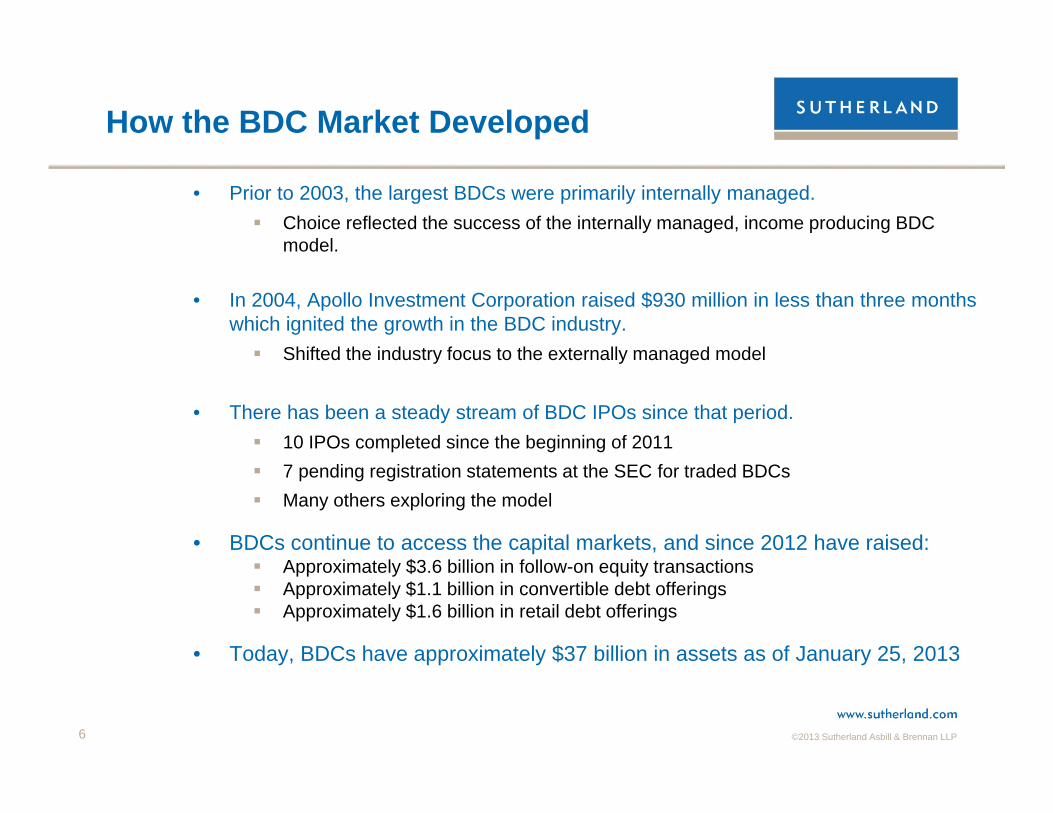

How the BDC Market Developed

• Prior to 2003, the largest BDCs were primarily internally managed. Choice reflected the success of the internally managed, income producing BDC

model.

• In 2004, Apollo Investment Corporation raised $930 million in less than three months which ignited the growth in the BDC industry. Shifted the industry focus to the externally managed model

• There has been a steady stream of BDC IPOs since that period. 10 IPOs completed since the beginning of 2011 7 pending registration statements at the SEC for traded BDCs Many others exploring the model

• BDCs continue to access the capital markets, and since 2012 have raised: Approximately $3.6 billion in follow-on equity transactions Approximately $1.1 billion in convertible debt offerings Approximately $1.6 billion in retail debt offerings

• Today, BDCs have approximately $37 billion in assets as of January 25, 2013

©2013 Sutherland Asbill & Brennan LLP7

Typical BDC Structure

©2013 Sutherland Asbill & Brennan LLP8

Part II:Regulatory and

Reporting Requirements

©2013 Sutherland Asbill & Brennan LLP

• Organize the BDC as a Delaware or a Maryland corporation

• Register a class of securities under the 1934 Act

• Make an election to be a BDC- file a Form N-54A (Notification of election to be subject to sections 55 through 65 of the 1940 Act)

• Register a class of securities on Form N-2

• List securities on the New York Stock Exchange (NYSE), the Nasdaq Stock Market, Inc. (Nasdaq), or the NYSE MKT, or the BDC can be a non-traded BDC

• Comply with the Sarbanes-Oxley Act of 2002 and Dodd-Frank Act

• Comply with regulatory requirements of the 1940 Act

9

How Does a Company Become a BDC?

©2013 Sutherland Asbill & Brennan LLP10

• A BDC must invest 70% of its assets in “good” BDC assets.

• 70% basket includes securities issued by an “eligible portfolio company,” as defined in Section 2(a)(46), which includes: U.S. issuers that are neither an investment company as defined in section 3 (other than

a wholly-owned SBIC) nor a company which would be an investment company except for the exclusion from the definition of investment company in section 3(c) and (i) do not have any class of securities listed on a national securities exchange; or (ii) have a class of securities listed on a national securities exchange, but have an

aggregate market value of outstanding voting and non-voting common equity of less than $ 250 million.

• A BDC can generally invest with flexibility in “bad” assets that do not fall within the “70% basket”. The SEC Staff has never been called upon to consider whether utilizing a specific

strategy for the entire “30% basket,” e.g., investing solely in foreign companies, might run afoul of the intent of Section 55(a)

“Good” vs. “Bad” BDC Assets

©2013 Sutherland Asbill & Brennan LLP

What are BDCs Investing In?

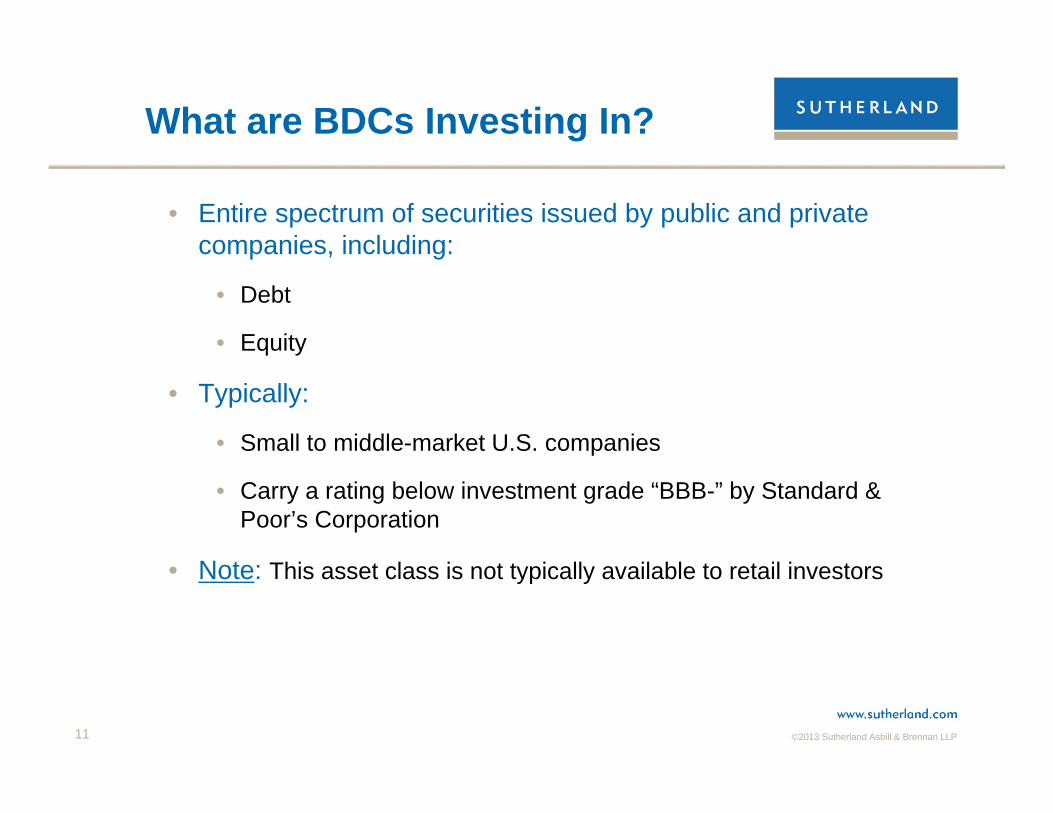

• Entire spectrum of securities issued by public and private companies, including:

• Debt

• Equity

• Typically:

• Small to middle-market U.S. companies

• Carry a rating below investment grade “BBB-” by Standard & Poor’s Corporation

• Note: This asset class is not typically available to retail investors

11

©2013 Sutherland Asbill & Brennan LLP

Investing Across the Capital Structure

12

Senior Secured Debt

Second Lien Secured Debt

Mezzanine Debt & Equity Warrants

Preferred Equity

Common EquityLower

HigherB

alan

ce S

heet

©2013 Sutherland Asbill & Brennan LLP13

• BDCs must have 200% asset coverage (Total Assets/Total Debt). For example, a BDC with $50 in equity can borrow up to $50 A BDC would be able to invest $100 in growing businesses

• Other investment companies are restricted to a 300% asset coverage requirement with respect to issuing debt.

• BDCs may exclude leverage at the SBIC level if the SEC grants exemptive relief, which many have received.

• Legislation currently pending in Congress that would increase the amount of funds BDCs may borrow by reducing the asset-to-debt coverage requirement from 2:1 to 1.5:1

$50 Equity

$50Debt

$50 Equity

$50 Equity

$25Debt

$50Equity

Limitations on Borrowings

©2013 Sutherland Asbill & Brennan LLP14

• Section 57 addresses the ability of BDCs to engage in certain types of transactions with affiliates: Section 57 is less onerous than its counterpart for registered investment companies

(Section 17).

• Depending on the nature of the affiliation with the BDC, transactions involving a BDC and one or more of its affiliates require either: Authorization by the required majority of the board of directors, which consists of a

majority of the board, including a majority of disinterested board members; or An order of the Commission.

• Co-investment between a BDC and an affiliated fund generally requires SEC exemptive relief Mass Mutual exception (i.e., no terms negotiated other than price)

Limitations on Transactions with Affiliates

©2013 Sutherland Asbill & Brennan LLP15

• BDC must have a majority of independent directors - persons who are not “interested persons” as defined in Section 2(a)(19) of the 1940 Act.

• Custodian Agreement A BDC generally must place and maintain its securities and similar investments in

the custody of a bank qualified under Section 26(a)(1) of the 1940 Act or a broker dealer, or be subject to additional audit and operational procedures related to securities held in safekeeping.

• Fidelity Bond A BDC must maintain a bond issued by a reputable fidelity insurance company, in

an amount prescribed by the 1940 Act, to protect the BDC against larceny and embezzlement. The bond must cover each officer and employee with access to securities and funds of the BDC.

• Requirement to maintain and enforce a Code of Ethics for officers of the BDC Includes reporting of all securities holdings and transactions.

1940 Act Requirements

©2013 Sutherland Asbill & Brennan LLP

• Restrictions on investing in other investment companies. May not invest: In more than 3% of the outstanding voting stock of a registered investment company or

BDC; or More than 5% of the value of its total assets in a registered investment company or

BDC; or More than an aggregate of 10% of its total assets in registered investment companies

or BDCs.

• Restrictions on investment funds investing in a BDC. Neither a public (i.e. registered) or private investment fund may own more than 3% of

the outstanding voting stock of a BDC

• Limitations on indemnification. A BDC is prohibited from protecting any director or officer against any liability to the

company, or its security holders, arising from willful misfeasance, bad faith, gross negligence or reckless disregard of the duties involved in the conduct of such person’s office.

• Bookkeeping and records requirements. A BDC must maintain and make available for inspection prescribed books and records.

• BDCs must make available significant managerial assistance to their portfolio companies.

1940 Act Requirements (cont.)

16

©2013 Sutherland Asbill & Brennan LLP17

• Must appoint a chief compliance officer.

• Must maintain a compliance program compliant with Rule 38a-1 of the 1940 Act, which requires: Adoption and implementation of policies and procedures designed to prevent

violation of the federal securities laws. Review of these policies and procedures annually for their adequacy and the

effectiveness of their implementation.

• Compliance polices and procedures for the registered investment adviser under Rule 206(4)-7 of the Investment Advisers Act of 1940. Requires an investment adviser of a BDC to adopt and implement policies and

procedures. Requires maintenance and enforcement of a code of ethics for advisor’s employees.

• Subject to regular examinations by the SEC.

1940 Act Requirements (cont.)

©2013 Sutherland Asbill & Brennan LLP18

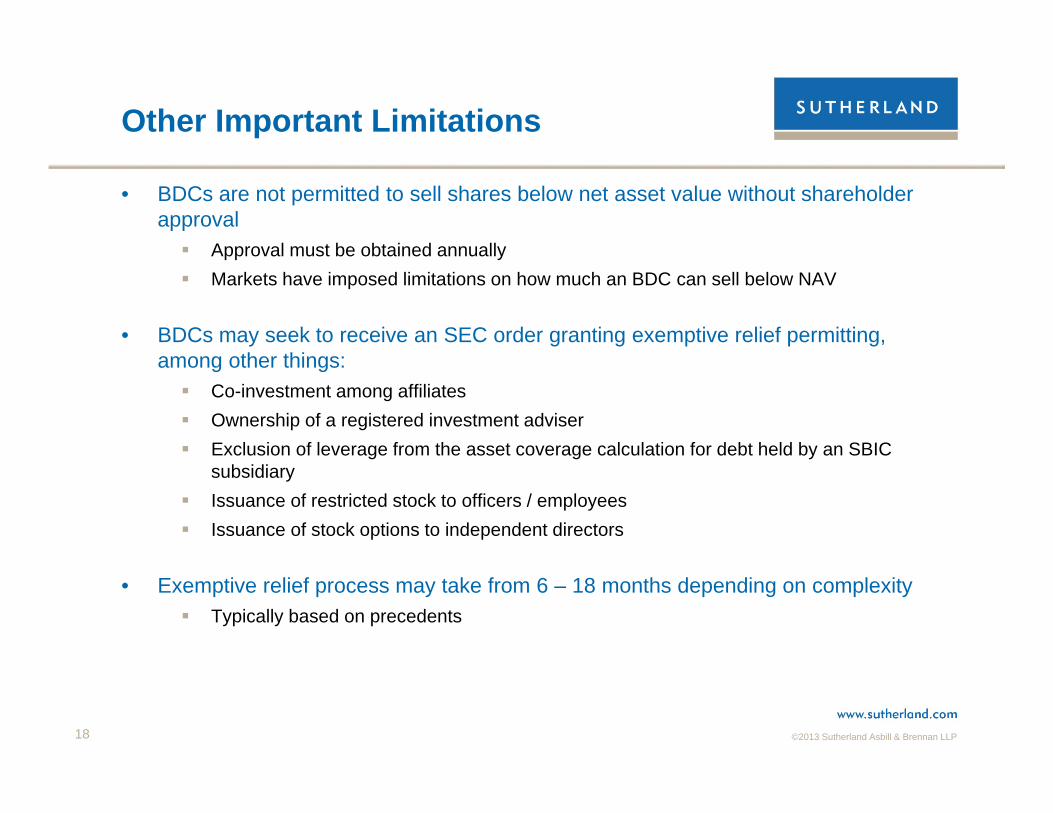

• BDCs are not permitted to sell shares below net asset value without shareholder approval Approval must be obtained annually Markets have imposed limitations on how much an BDC can sell below NAV

• BDCs may seek to receive an SEC order granting exemptive relief permitting, among other things: Co-investment among affiliates Ownership of a registered investment adviser Exclusion of leverage from the asset coverage calculation for debt held by an SBIC

subsidiary Issuance of restricted stock to officers / employees Issuance of stock options to independent directors

• Exemptive relief process may take from 6 – 18 months depending on complexity Typically based on precedents

Other Important Limitations

©2013 Sutherland Asbill & Brennan LLP19

• Form 10-K (Annual Report)

• Form 10-Q (Quarterly Report)

• Form 8-K (Current Report)

• Proxy Statements

• Sections 13 and 16 Filings Forms 3, 4 or 5 for reporting beneficial ownership by insiders Schedules 13D and 13G for reporting beneficial ownership by others

• Regulation G and Regulation FD

• Comply with the Sarbanes-Oxley Act of 2002

• Disclosure Controls and Procedures

• Internal Control over Financial Reporting/Attestation

SEC Reporting Requirements for BDCs

©2013 Sutherland Asbill & Brennan LLP20

• Consolidation of subsidiaries vs. portfolio companies

• Valuation policy, including description of valuation process and methodologies

• Control investments, investments in affiliates, and investment in non-affiliates

• Schedule of investments Disclose non-income producing investments Disclose assets held in securitized vehicles Interest rate and maturity date on debt investments

• Fair value and Level 3 reconciliation tables

• Concentration – Geography and industry sectors

Financial Statement Disclosures

©2013 Sutherland Asbill & Brennan LLP21

• BDCs that have their securities listed or traded on NASDAQ or NYSE must comply with the corporate governance listing standards, including, among other things: A listed BDC must have an audit committee composed solely of “independent

directors” (as defined by the applicable exchange or association).

Director nominees of a listed BDC must be selected or recommended for the Board’s selection by a nominating committee or the vote of a majority of the BDC’sindependent directors (depending on the exchange).

The non-management, or “independent directors”, of the BDC must hold regularly scheduled executive sessions.

The BDC must adopt a code of business conduct and ethics, various committee charters and, in the case of NYSE-listed BDCs, corporate governance guidelines. All such documents must be posted on the company’s website.

Exchange Listing Standards

©2013 Sutherland Asbill & Brennan LLP22

Part III:Management and

Operational Considerations

©2013 Sutherland Asbill & Brennan LLP23

• BDC is managed internally by executive officers (i.e., no external adviser) 9 of the 39 actively traded BDCs are internally managed

• Must comply with SEC executive compensation disclosure requirements

• Certain performance-based compensation is permitted, including: Issuance of at-the market options, warrant, or rights pursuant to an executive

compensation plan; or Maintenance of a profit sharing plan

• Otherwise, the BDC must use cash assets as compensation

• Exemptive orders permitting the issuance of restricted stock have been issued in a number of circumstances including: Hercules Technology Growth Capital MCG Capital Corporation Main Street Capital Corporation

Internally Managed Structure

©2013 Sutherland Asbill & Brennan LLP24

• Portfolio managed by external investment adviser 30 of the 39 actively traded BDCs are externally managed

• Investment adviser of a BDC must be registered under the Advisers Act

• May utilize an external administrator for expense reimbursement purposes

• Adviser is permitted to charge a base management fee, as well as an incentive fee on both: Investment income Realized capital gains

• Contrasts with most registered closed-end funds, which are typically prohibited from taking an incentive fee on capital gains

• Incentive fees are often subject to hurdle/catch-up features

Externally Managed Structure

©2013 Sutherland Asbill & Brennan LLP25

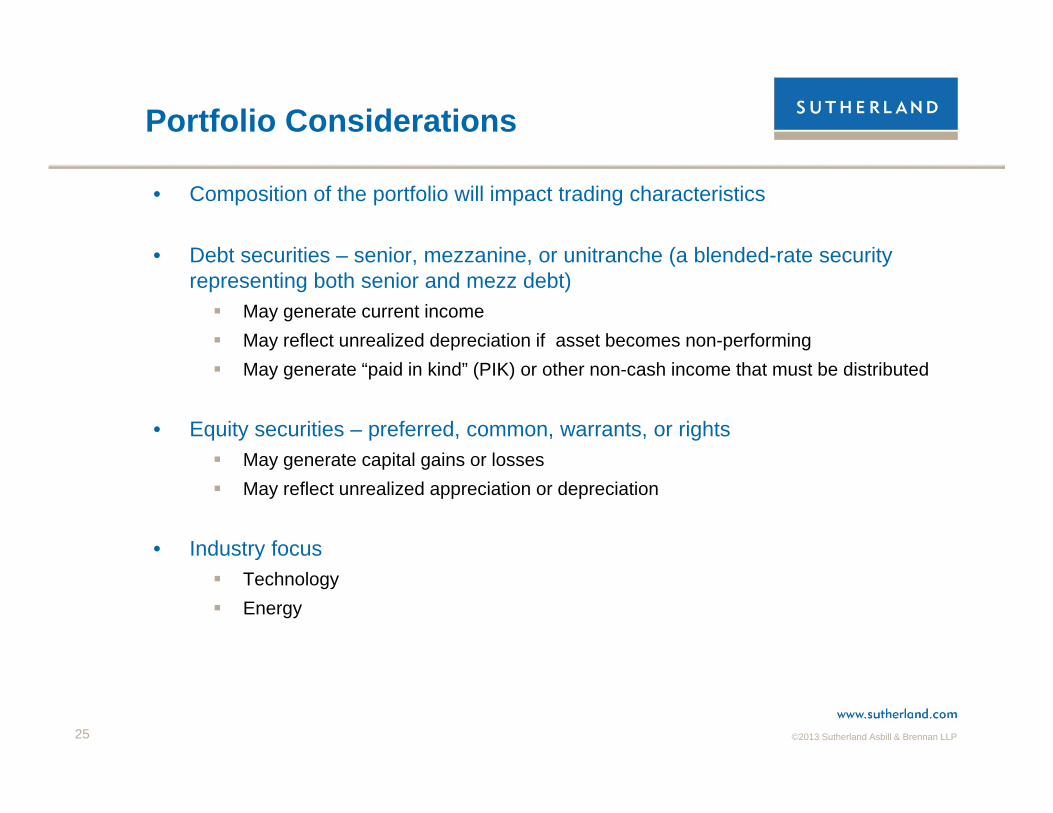

• Composition of the portfolio will impact trading characteristics

• Debt securities – senior, mezzanine, or unitranche (a blended-rate security representing both senior and mezz debt) May generate current income May reflect unrealized depreciation if asset becomes non-performing May generate “paid in kind” (PIK) or other non-cash income that must be distributed

• Equity securities – preferred, common, warrants, or rights May generate capital gains or losses May reflect unrealized appreciation or depreciation

• Industry focus Technology Energy

Portfolio Considerations

©2013 Sutherland Asbill & Brennan LLP26

• SEC Staff has taken no formal position on the calculation of the fee but requires BDCs to include extensive disclosure in registration statements regarding the manner in which the fee will be calculated in varying scenarios.

• Section 205(b)(3) of the Advisers Act permits external investment advisers to BDCs to receive incentive fees, provided that the BDCs do not have outstanding any equity-based compensation arrangement or profit-sharing plan. Section 205(b)(3) provides an exception from the general prohibition on an investment

adviser charging an incentive fee based on a share of capital gains. May assess an incentive performance fee of up to 20% on a BDC’s realized capital

gains net of all realized capital losses and unrealized capital depreciation over a specified period.

• Section 205(b)(3) of the Advisers Act makes no reference to whether the unrealized capital depreciation by which the fee must be reduced includes: Only depreciation below the original cost of the security in question, or Whether it includes a decrease in value in a security above the original cost but below

the point of a previous unrealized capital appreciation.

Calculation of Adviser’s Incentive Fee

©2013 Sutherland Asbill & Brennan LLP27

• Investments are reported at fair value, as determined in good faith by the board of directors.

• ASC 820 – Fair Value Measurements and Disclosures (formerly FAS 157).

• “Fair value” – Price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at measurement date.

• Key Controls in the Valuation Process: Documented approval of trades Controls over inputs in valuation write-ups Segregation between preparation and review of valuations Identified and monitored problem loans High level analytical reviews Completeness of disclosures All controls evidence Sarbanes-Oxley 404 readiness

Portfolio Valuation Process

©2013 Sutherland Asbill & Brennan LLP28

• Investments classified into three levels: Level 1: Inputs are unadjusted, quoted prices in active markets for identical financial

instruments at the measurement date.

Level 2: Inputs include quoted prices for similar financial instruments in active markets and inputs that are observable for the financial instruments, either directly or indirectly, for substantially the full term of the financial instrument.

Level 3: Inputs include significant unobservable inputs for the financial instruments and include situations where there is little, if any, market activity for the investment. The inputs into the determination of fair value are based upon the best information available and may require significant management judgment or estimation.

• Majority of BDCs classify debt and equity investments as Level 3 instruments.

• Debt investments with broker quotes may be considered a Level 2 instrument (broadly syndicated loans).

General Principles of Valuation

©2013 Sutherland Asbill & Brennan LLP29

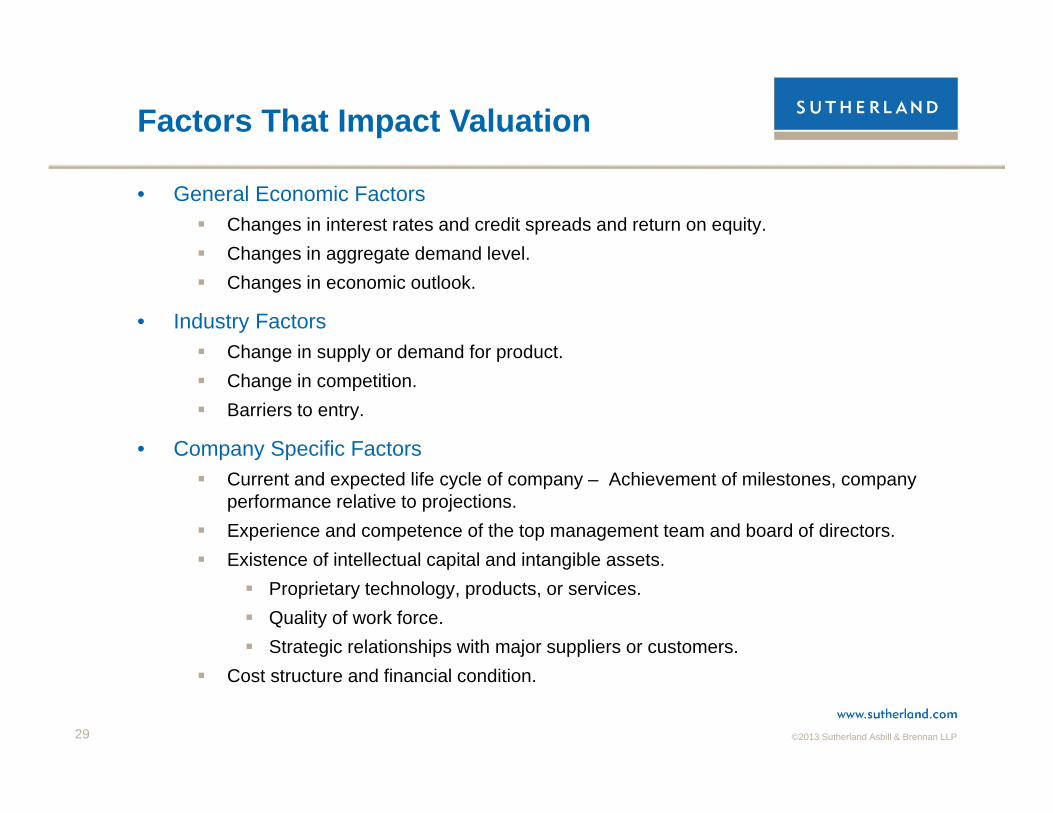

• General Economic Factors Changes in interest rates and credit spreads and return on equity. Changes in aggregate demand level. Changes in economic outlook.

• Industry Factors Change in supply or demand for product. Change in competition. Barriers to entry.

• Company Specific Factors Current and expected life cycle of company – Achievement of milestones, company

performance relative to projections. Experience and competence of the top management team and board of directors. Existence of intellectual capital and intangible assets.

Proprietary technology, products, or services. Quality of work force. Strategic relationships with major suppliers or customers.

Cost structure and financial condition.

Factors That Impact Valuation

©2013 Sutherland Asbill & Brennan LLP30

• BDCs are regulated by the SEC’s Division of Investment Management

• Rule 38a-1 of the 1940 Act requires the BDC to have a comprehensive compliance program Oversight of compliance with all federal securities laws Quarterly testing and documentation intended to ensure program

effectiveness Chief Compliance Officer reports directly to the board of directors Management expected to set tone at the top

• Rule 206(4)-7 of the Advisers Act requires the investment adviser to have a comprehensive compliance program

• SEC’s Office of Compliance, Inspections and Examinations have examination authority Risk-based exams may occur at any time – be prepared

Compliance Considerations

©2013 Sutherland Asbill & Brennan LLP31

• A BDC may elect to be taxed as a “regulated investment company,” or RIC, under the Internal Revenue Code. Allows “pass through” tax treatment for income and capital gains that are distributed to

shareholders – no taxation at BDC. Must distribute at least 90% of its investment income to shareholders annually.

May retain, distribute or “deem distribute” capital gains.• Annually, at least 90% of gross income must be generated from investment

company taxable income (generally interest, dividends and capital gains)• Quarterly, at least 50% of assets (at fair value) must be:

Cash, cash equivalents, or government securities Securities of other RICs Securities that, with respect to any one issuer, both (1) represents an amount 5% or

less of the RIC’s total assets and (2) is not more than 10% of the outstanding voting securities of the issuer

• Quarterly, not more than 25% of the RIC’s total assets can be invested in: Securities of any one issuer (excluding other RICs or government securities) Securities of two or more issuers controlled by the RIC and engaged in the same trade

or business Securities of qualified publicly traded partnerships

Taxation as a RIC

©2013 Sutherland Asbill & Brennan LLP32

Part IV:BDC Structures

©2013 Sutherland Asbill & Brennan LLP33

• Publicly-traded BDCs Listed on NASDAQ/NYSE Formed either as a blind-pool vehicle, or through the acquisition of an existing portfolio

or conversion of SBIC funds IPO through traditional firm commitment underwritten offering

• Non-Traded BDCs Shares are not listed on any exchange IPO through continuous offering of shares up to preset maximum amount Liquidity offering through periodic repurchase offers Typically have fixed 5-7 year period before exchange listing or traditional IPO

• Private BDCs Shares are not listed on any exchange Shares are sold through private placement offering Intention to conduct IPO in near term Funding may be effected through a capital call model Generally no liquidity prior to a qualifying IPO

Types of BDC Structures

©2013 Sutherland Asbill & Brennan LLP34

Publicly Traded BDCs

©2013 Sutherland Asbill & Brennan LLP35

• Typically 6 – 8 months to complete IPO depending on: Market Conditions SEC review process

• Consider formation / structuring issues Portfolio acquisition / manage any built-in gain Form of consideration

• Consider any necessary exemptive relief Co-investment with sister funds

• Prepare registration of investment adviser (if externally-managed)

• Develop compliance / corporate governance programs

• Establish independent Board of Directors

• Select service providers Public accountants, valuation assistance, custodian, etc.

IPO Process Overview

©2013 Sutherland Asbill & Brennan LLP36

• Organize the entity - typically as a Delaware or a Maryland corporation

• File an IPO registration statement on Form N-2 under the Securities Act

• Register a class of securities under the Exchange Act

• Apply to list securities on the NASDAQ or NYSE

• Make an election to be regulated as a BDC by filing a Form N-54A

• Have N-2 registration statement declared effective by the SEC

• Comply with regulatory requirements of the 1940 Act

• Comply with reporting requirements including the Exchange Act, Sarbanes-Oxley Act, etc.

IPO Process Overview (cont.)

©2013 Sutherland Asbill & Brennan LLP37

• Can start with or without an initial portfolio Market has generally favored vehicles with existing portfolios Some blind-pool vehicles have completed IPOs recently, though

• Initial portfolio can be acquired from an affiliated fund on a pre-IPO basis

• Considerations in connection with the acquisition of an initial portfolio: Consider required approvals at the private fund level Consider funding issues on a pre-BDC basis

Use of a bridge facility or notes Equity may be issued, provided that no fund will hold greater than 3% of the BDC

post-transaction Consider tax implications

Timing and recognition of accrued but unrealized appreciation/depreciation in initial portfolio

• Disclosure requirements for initial portfolio Typically an audited schedule of investments is required More fulsome financial statements may also be acquired in certain cases

Initial Portfolio Acquisitions

©2013 Sutherland Asbill & Brennan LLP38

Non-Traded BDCs

©2013 Sutherland Asbill & Brennan LLP39

• REITs have successfully used the non-traded model for years.

• In January 2009, FS Investment Corporation launched the first non-traded BDC IPO of $1.5 billion and follow-on offering of $1.0 billion fully subscribed

• Eleven non-listed BDCs have launched public offerings (nearly $15.5 billion target fund size) and approximately four non-listed BDCs are in registration.

• Non-listed BDCs have collectively raised nearly $4.3 billion since 2008.

• Most of the non-traded BDCs combine an investment platform with an existing distribution network. For example, FS Investment Corporation, FS Energy and Power Fund and FS Investment

Corporation II combines the distribution network of FS2 Capital Partners with investment personnel of GSO/Blackstone

KKR Asset Management is the investment sub-adviser for Corporate Capital Trust, while CNL Fund Advisors serves as the dealer manager

CION Investment Corp. combines the distribution network of ICON with the investment personnel of Apollo

HMS Income Fund combines the distribution network of Hines with the investment personnel of Main Street

Sierra Income Corp. combines the distribution network of SC Distributors with the investment personnel of Medley

Development of Non-Traded BDCs

©2013 Sutherland Asbill & Brennan LLP40

• A Non-Traded BDC enables retail investors to receive stable income and potentially receive capital appreciation in the event of a liquidity event, such as a listing, liquidation or merger. Shares not listed on any exchange Raise capital through continuous private offerings Eliminates price volatility through the ability to adjust net offering price so that it remains

at or below NAV Limited liquidity

Most Non-Traded BDCs have a mechanism that provides liquidity after a certain holding period (such as periodic repurchase offers to their shareholders)

Subject to the individual state registration requirements for public offerings

• All the non-traded BDCs that are currently offering and in registration are externally managed

Non-Traded BDC Structures

©2013 Sutherland Asbill & Brennan LLP41

• Suitability requirements May only be sold to investors that meet certain state suitability requirements

• FINRA review

• State blue sky review Must be approved to sell securities in each state where solicitations will occur, requiring

compliance with the “Omnibus Guidelines” published by the National Association of State Securities Administrators (“NASAA”)

Completing blue sky process can take up to a year

• Continuous offering over a period of time 497 is filed periodically to report sales, update portfolio and keep prospectus current

• Liquidity Event Typically complete liquidity event within five to seven years following completion of

offering Liquidity event could include: (1) sale of all or substantially all of company’s assets

either on a complete portfolio basis or individually followed by a liquidation, (2) listing of company’s common shares on a national exchange, or (3) merger or another transaction approved by company’s board of directors in which shareholders receive cash or shares of a publicly traded company

Additional Characteristics ofNon-Traded BDCs

©2013 Sutherland Asbill & Brennan LLP

• Redemptions/Repurchases Non-listed issuers typically offer to redeem or repurchase portion of outstanding

shares on quarterly basis Periodic tender offers by closed-end funds, including BDCs, excepted from Regulation

M under the Securities Exchange Act of 1934 if made at net asset value or if the comply with Rule 23c-3 of the Investment Company Act of 1940

REITs received class exemption from Regulation M from the SEC for certain redemption plans BDCs may receive similar relief

Additional Characteristics ofNon-Traded BDCs (Con’t)

42

©2013 Sutherland Asbill & Brennan LLP43

• Sponsor Requirements Sponsor must have adequate experience and net worth Limited indemnification of Sponsor, which may affect bylaws and/or charter of an issuer

• Suitability of Investors Default minimum suitability standards of either $70,000 gross income and $70,000 net

worth or $250,000 net worth Enhanced suitability standards may be imposed by various states Minimum investment amounts

• Fees, Compensation and Expenses Sponsor’s compensation must be “reasonable”

For BDCs, compensation presumptively reasonable if limited to “participation in net gains” of the issuer

For Sponsor providing services to the issuer, fees must be competitive as compared to independent third-parties

Offering document must estimate and itemize fees and expenses

NASAA Omnibus Guidelines: Compliance with “Blue Sky Laws”

©2013 Sutherland Asbill & Brennan LLP44

• Conflicts of Interest Issuer may only invest in joint ventures or general partnerships with non-affiliates so long

has “controlling interest” Issuer may only invest in joint ventures or general partnerships with affiliated entities

provided there are no duplication of fees and each investor has right of first refusal to buy the affiliates’ interests in the venture

Limited ability to invest in joint ventures or general partnerships with non publicly registered affiliates

Multi-tiered arrangements permissible so long not designed to circumvent the Guidelines, there are no duplication of fees, no decrease in the voting rights of stockholders and the fiduciary obligations of the various parties are adjusted

NASAA Omnibus Guidelines: Compliance with “Blue Sky Laws” (cont.)

©2013 Sutherland Asbill & Brennan LLP45

• Rights and Obligations of Participants (i.e. Stockholders) 10% holders have right to call stockholders meetings Majority approval of stockholders required to amend entity charter, dissolve the

company, remove the Sponsor, elect a new Sponsor or approve the sale of substantially all of the assets of the company

Stockholder right to inspect and copy the company’s records, including stockholder list Reports to stockholders (e.g.,10-Qs and 10-Ks) Distribution Reinvestment Plans (“DRPs”) may not charge sales commissions for shares

issued under the DRP Stockholders must be able to elect or revoke participation in the DRP Stockholders participating in the DRP must receive “current” copy of the

prospectus each time shares under the DRP are issued Broker-dealers responsible for ensuring participants in the DRP remain “suitable” to

invest in the issuer

NASAA Omnibus Guidelines: Compliance with “Blue Sky Laws” (cont.)

©2013 Sutherland Asbill & Brennan LLP46

Private BDCs

©2013 Sutherland Asbill & Brennan LLP

Capital Raise

• Typically sponsored by large private equity firms with an existing investor base TPG Specialty Lending, Inc. registered on Form 10 and has raised approximately $360 million

through private offerings.

• Typically draws down capital via a capital call model, similar to a private fund structure

Private Offering

• Shares are offered through a private placement offering to the sponsor’s existing investor base, rather than via a continuous public offering

• Private placement structure eliminates need to be declared effective by each state in which offering shares

Regulatory Structure

• BDC/RIC structure helps mitigate need for offshore feeder fund structure for foreign/tax exempt investors

Exit

• Generally target an initial public offering and exchange listing, similar to the non-traded BDC structure

47

What is a Private BDC?

©2013 Sutherland Asbill & Brennan LLP48

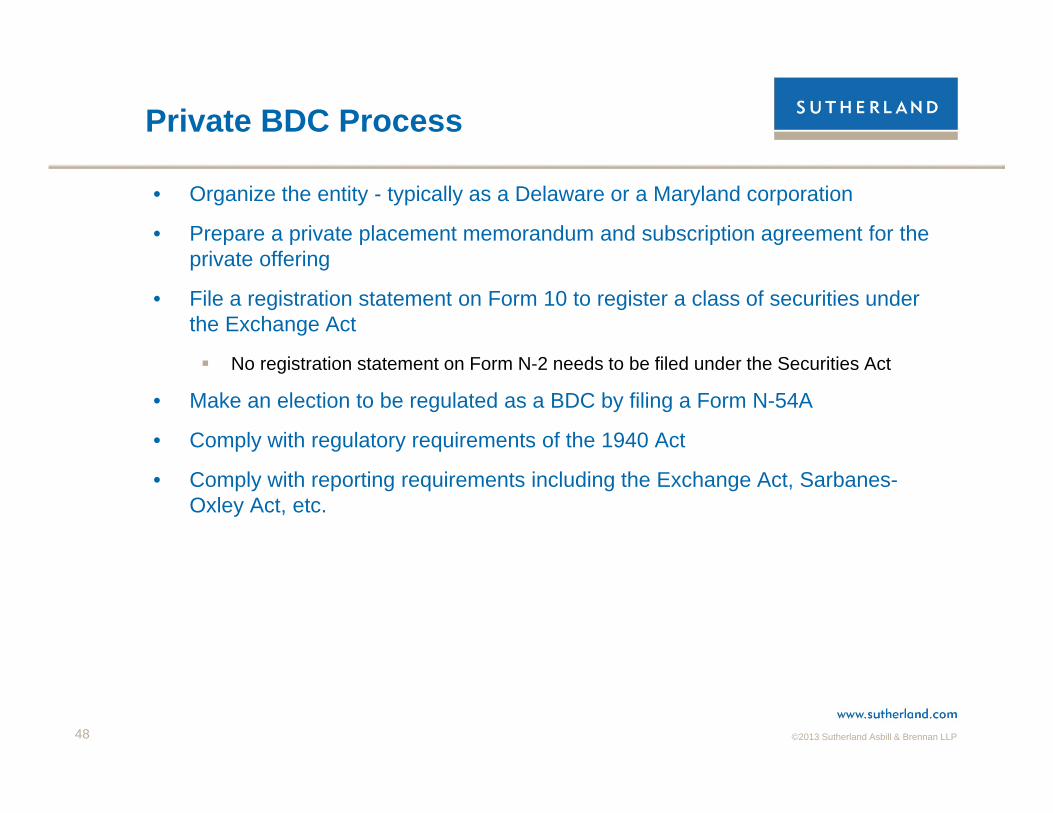

• Organize the entity - typically as a Delaware or a Maryland corporation

• Prepare a private placement memorandum and subscription agreement for the private offering

• File a registration statement on Form 10 to register a class of securities under the Exchange Act

No registration statement on Form N-2 needs to be filed under the Securities Act

• Make an election to be regulated as a BDC by filing a Form N-54A

• Comply with regulatory requirements of the 1940 Act

• Comply with reporting requirements including the Exchange Act, Sarbanes-Oxley Act, etc.

Private BDC Process

©2013 Sutherland Asbill & Brennan LLP

SBICs

49

©2013 Sutherland Asbill & Brennan LLP

BDC SBIC Trends

• SBIC Subsidiaries Twelve BDCs have SBIC subsidiaries. Provides access to low-cost debt (a fully funded SBIC with $75

million in regulatory capital can access up to $150 million in leverage from the SBA with an option for a second license for an additional $75 million). SBICs under common control can access up to $225 million in

leverage, which Congress may increase to $350 million.• Fund Formation

Some BDCs are using BDCs as asset managers. The benefit of this structure is the fee income received.

• Fund Platforms Some BDCs are building a platform of funds that complement the

BDC’s business.

50

©2013 Sutherland Asbill & Brennan LLP

• Three (3) SBICs elected to become BDCs and conducted successful IPOs

Main Street Capital Corporation / $64,500,000 Triangle Capital Corporation / $71,550,000 Fidus Investment Corporation / $70,050,000

• BDCs that have received an SBIC license for a wholly-owned subsidiary:

Fifth Street Finance Corp. Hercules Technology Growth Capital, Inc. Medallion Financial Corp. MCG Capital Corporation PennantPark Investment Corporation Rand Capital Corporation Saratoga Investment Corporation OFS Capital Corporation Golub Capital BDC, Inc.51

Are There BDCs That Have SBIC Subsidiaries?

©2013 Sutherland Asbill & Brennan LLP

• Conversion Transaction Approval of LPs in advance of valuation and merger Merger of SBIC into subsidiary of BDC Amend limited partnership agreement SBA approval

• SEC Review Affiliate transaction issues Compensation issues Disclosure issues

52

How Does an SBIC Convert to a BDC?

©2013 Sutherland Asbill & Brennan LLP

BDC/SBIC Structure

• Exemptive Relief

• Relief to get SBIC leverage treatment at BDC level

• Section 18(a):

Question of whether BDC with an SBIC subsidiary must comply with the asset coverage requirements of Section 18(a) (as modified by Section 61(a) for BDCs) on a consolidated basis.

The senior securities issued by the SBIC Subsidiary would be excluded from the SBIC Subsidiary’s individual asset coverage ratio by Section 18(k) if the SBIC Subsidiary were a BDC.

Exemption requested- senior securities representing indebtedness issued by the SBIC Subsidiary may be excluded from the BDC’sconsolidated asset coverage ratio.

The SEC regularly provides this exemptive relief, which generally does not take as long as other forms of relief.

53

©2013 Sutherland Asbill & Brennan LLP

What are the Incentives for an SBIC to Convert to a BDC?

• Why Are BDCs Attractive to SBICs? Ability to access public market Flexibility in funding portfolio investments Permanent capital base Additional compensation incentives

• Why Are SBICs Attractive to the BDC Market? Existing portfolio – not blind pool Existing management team with track record Market niche – lower middle market Additional leverage capacity

54

©2013 Sutherland Asbill & Brennan LLP55

Contact Information

For more information, please visit our practice site at www.publiclytradedprivateequity.com and our corporate site at

www.sutherland.com.

John J. [email protected]

Harry S. [email protected]

Cynthia M. [email protected]

Steve B. [email protected]

©2013 Sutherland Asbill & Brennan LLP56

Disclaimer

All Rights Reserved. This communication is for general informational purposes only and is not intended to constitute legal advice or a recommended course of action in any given situation. This communication is not intended to be, and should not be, relied upon by the recipient in making decisions of a legal nature with respect to the issues discussed herein. The recipient is encouraged to consult independent counsel before making any decisions or taking any action concerning the matters in this communication. This communication does not create an attorney-client relationship between Sutherland and the recipient.