Bdc 101 06

17

© 2010 Cosmopoint FINANCIAL ACCOUNTING I CHAPTER 6: Cash Book & Petty Cash Book © 2010 Cosmopoint

-

Upload

asia-green -

Category

Economy & Finance

-

view

34 -

download

1

Transcript of Bdc 101 06

FINANCIAL ACCOUNTING I

CHAPTER 6:

Cash Book & Petty Cash Book

© 2010 Cosmopoint

Slide 2 of 15© 2010 Cosmopoint

Learning Objectives :

Define cash book

Explain the importance of cash book

Describe cash discount

Illustrate three columns cash book

Define Petty Cash Book

Explain Imprest system / cash float system

Slide 3 of 15© 2010 Cosmopoint

1.0 CASH BOOK

• Cash Book is a book of original entry for cash transactions.

• Cash Book consists of:

• Cash paid into the bank is any cheque received and deposited into business bank account.

CASH BOOK

Cash Acc Bank Acc

Slide 4 of 15© 2010 Cosmopoint

1.1 IMPORTANCE OF CASH BOOK

• The importance of Cash Book are:– Safeguards assets from employee theft, robbery and

unauthorised used– Ensure the accuracy and reliability of accounting records– Adherences to company policies– Monitor operational efficiency– Cash Book provides instant access to your bank balances

and makes reconciliation fast and easy.• Therefore, a business with many cash and cheques

transactions would require to :– Bank in daily cash receipts on the same day– Use cheque or electronic transfer for all cash payments

Slide 5 of 15© 2010 Cosmopoint

1.1.1 EXAMPLE OF TWO COLUMN CASH BOOK

Sept 20X9 Details

1 Put capital in bank account RM10,940

2 Received cheque from Boon RM315

3 Cash Sales RM802

4 Paid rent by cash RM135

5 Banked RM50

CASH BOOK

Sep 09 Details Fol Cash Bank Sep 09 Details Fol Cash Bank

1 Capital 10,940 4 Rent 135

2 Boon 315 5 Bank C 50

3 Sales 802 30 Bal c/d 617 11,305

5 Cash C 50

802 11,305 802 11,305

Oct 1 Bal b/d 617 11,305

Slide 6 of 15© 2010 Cosmopoint

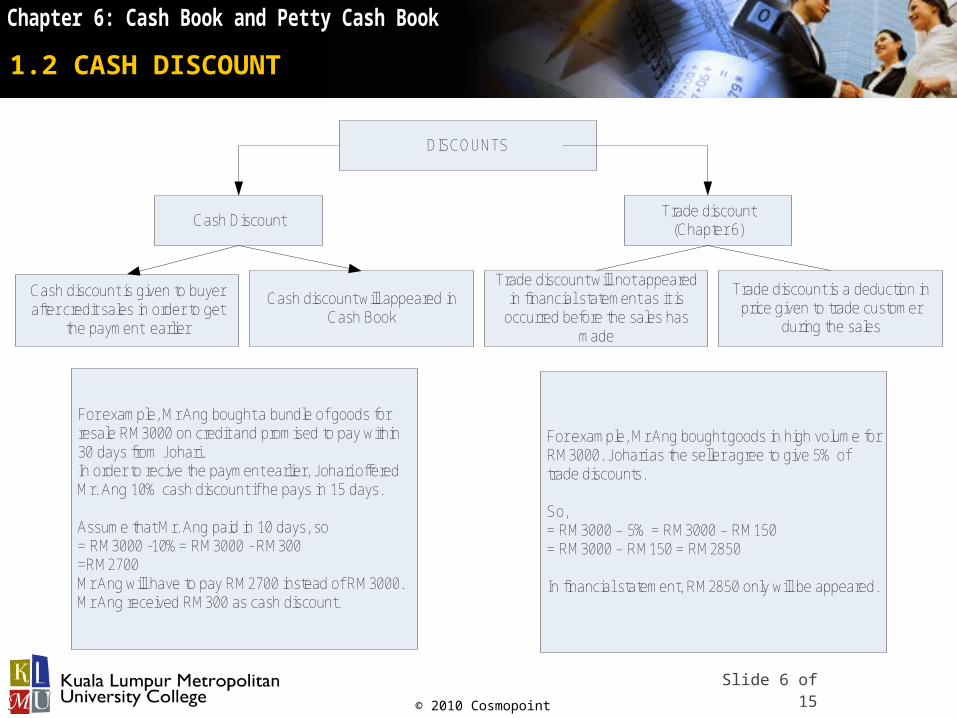

1.2 CASH DISCOUNT

Cash DiscountTrade discount

(Chapter 6)

Cash discount is given to buyer after credit sales in order to get

the payment earlier

For example, Mr Ang bought a bundle of goods for resale RM3000 on credit and promised to pay within 30 days from Johari. In order to recive the payment earlier, Johari offered Mr. Ang 10% cash discount if he pays in 15 days.

Assume that Mr. Ang paid in 10 days, so = RM3000 -10%= RM3000 - RM300=RM2700Mr Ang will have to pay RM2700 instead of RM3000. Mr Ang received RM300 as cash discount.

Trade discount is a deduction in price given to trade customer

during the sales

Cash discount will appeared in Cash Book

Trade discount will not appeared in financial statement as it is

occurred before the sales has made

For example, Mr Ang bought goods in high volume for RM3000. Johari as the seller agree to give 5% of trade discounts.

So,= RM3000 – 5% = RM3000 – RM150= RM3000 – RM150 = RM2850

In financial statement, RM2850 only will be appeared.

DISCOUNTS

Slide 7 of 15© 2010 Cosmopoint

1.3 THREE COLUMN CASH BOOK

• Three columns cash book is a cash book that consists of discounts columns.

• There are two types of discounts columns:

-Discounts allowed are cash discounts by a business to its customer when they pay their debt quickly

-Discounts received are cash discounts by a business from its suppliers when it pays what it owes them quickly.

3 COLUMNS CASH BOOKDiscount Allowed

Discount Received

Slide 8 of 15© 2010 Cosmopoint

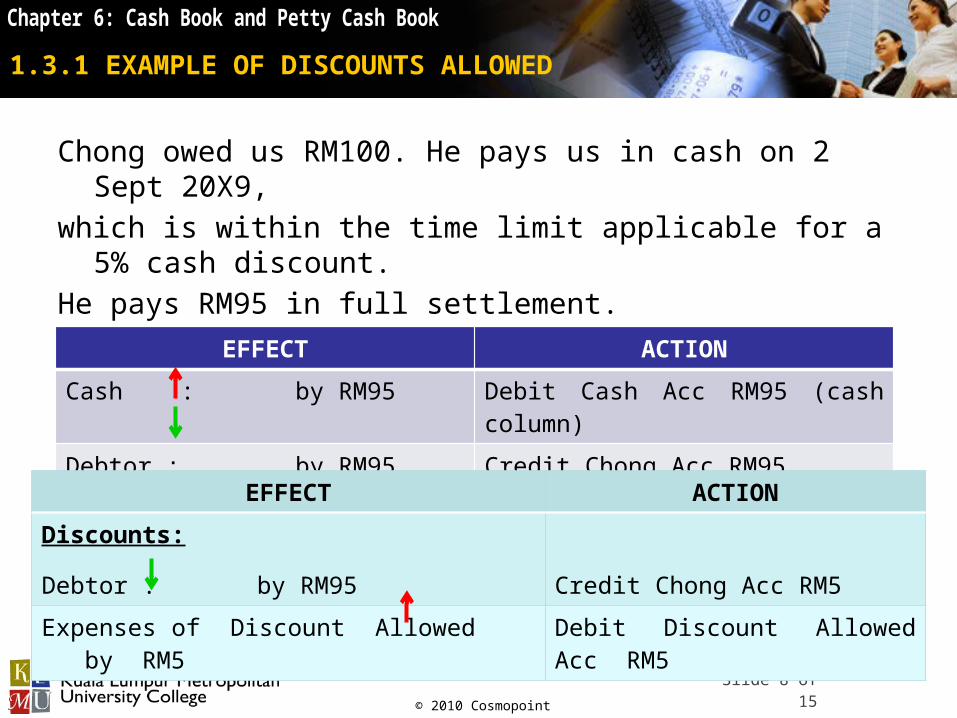

1.3.1 EXAMPLE OF DISCOUNTS ALLOWED

Chong owed us RM100. He pays us in cash on 2 Sept 20X9,

which is within the time limit applicable for a 5% cash discount.

He pays RM95 in full settlement.

(RM100 – RM5 = RM95)

EFFECT ACTION

Cash : by RM95 Debit Cash Acc RM95 (cash column)

Debtor : by RM95 Credit Chong Acc RM95

EFFECT ACTION

Discounts:

Debtor : by RM95 Credit Chong Acc RM5

Expenses of Discount Allowed by RM5 Debit Discount Allowed Acc RM5

Slide 9 of 15© 2010 Cosmopoint

1.3.2 EXAMPLE OF DISCOUNTS RECEIVED

The business owed Sunny RM400. It pays him by cheque on 3

Sept 20X9, which is within the time limit laid down by him for a

3% cash discount.

The business will pay RM388 in full settlement.

(RM400 – RM12 = RM388)

EFFECT ACTION

ChequeBank : by RM388

Credit Bank Acc RM388 (bank column)

Creditor : by RM388 Debit Sunny Acc RM388

EFFECT ACTION

Discounts:

Creditor : by RM12 Debit Sunny Acc RM12

Revenues of Discount received by RM12 Credit Discount Received Acc RM12

Slide 10 of 15© 2010 Cosmopoint

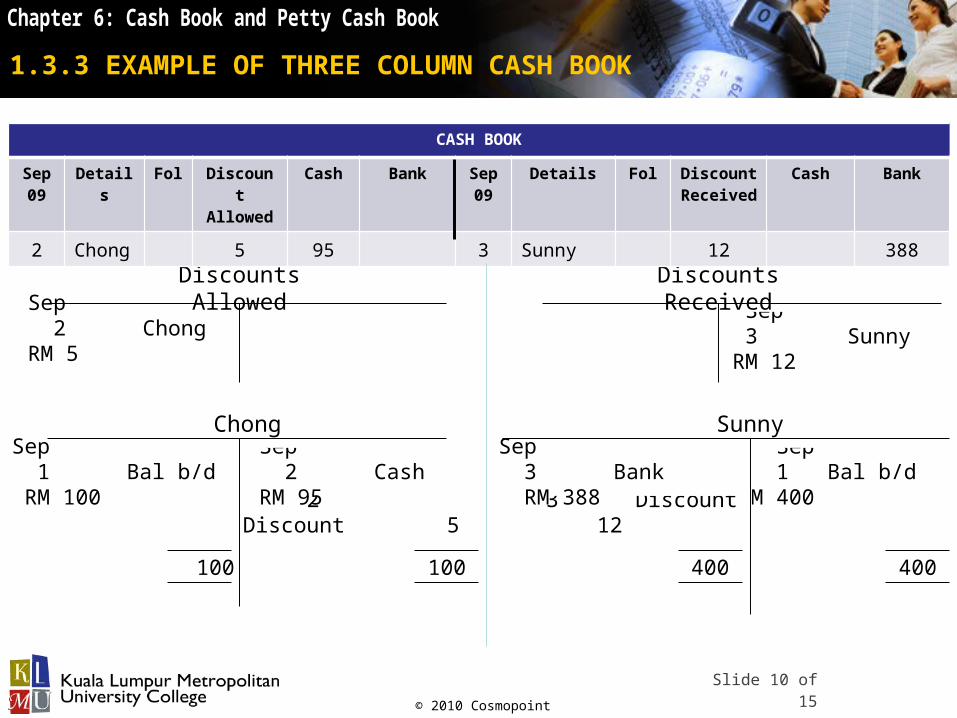

400

Sep 1 Bal b/d RM 400

3 Discount 12

100

2 Discount 5

Sep 2 Cash RM 95

Sep 1 Bal b/d RM 100

SunnyChong

Sep 3 Sunny RM 12

Discounts ReceivedSep 2 Chong RM 5

Discounts Allowed

1.3.3 EXAMPLE OF THREE COLUMN CASH BOOK

CASH BOOK

Sep 09

Details Fol DiscountAllowed

Cash Bank Sep 09

Details Fol Discount Received

Cash Bank

2 Chong 5 95 3 Sunny 12 388

100

Sep 3 Bank RM 388

400

Slide 11 of 15© 2010 Cosmopoint

2.0 PETTY CASH BOOK

• A petty cash book is normally used to record small payments.

• If small cash payments were entered into the main Cash Book, this item would then need posting one by one to the ledgers.

Example:If travelling expenses were paid to staff on a daily basis, thiscould be approximately 250 postings to the staff travelling expenses account during the year.

However, by using a Petty Cash Book, it would be the monthly totals for each period that need posting to General Ledger. If this was done, only 12 entries would be needed in the staff travel expenses account instead of approximately 250.

Slide 12 of 15© 2010 Cosmopoint

3.0 IMPREST SYSTEM

• Is a system for controlling small cash disbursements by establishing a fund at a fixed amount and regularly reimburses the fund by the amount necessary to restore the original cash flow.

Period 1

RM

The cashier gives the petty cashier 100

The petty cashier pays out in the period (78)

Petty cash now in hand 22

The cashier now gives the petty cashier the amount spent 78

Petty cash in hand at the end of Period 1 100

Period 2

The petty cashier pays out in the period (84)

Petty cash now in hand 16

The cashier now gives the petty cashier the amount spent 84

Petty cash in hand at the end of Period 2 100

Slide 13 of 15© 2010 Cosmopoint

4.0 ANALYSE PAYMENT

• The first step in preparing your monthly payments is to write in the cheques that you have written out of your business bank account.

• Enter the total amount of the cheque in the bank column of the Cash Book.

• Next, you will need to tick the cheques that have been presented on your bank statement off on your cashbook listing for that month.

• The cheques that have not been ticked in the Cash Book when you are finished will be the non presented cheque for the month.

• Lastly, write in any other amounts on your bank statement that are not cheques such as bank fee, interest and direct debits.

Slide 14 of 15© 2010 Cosmopoint

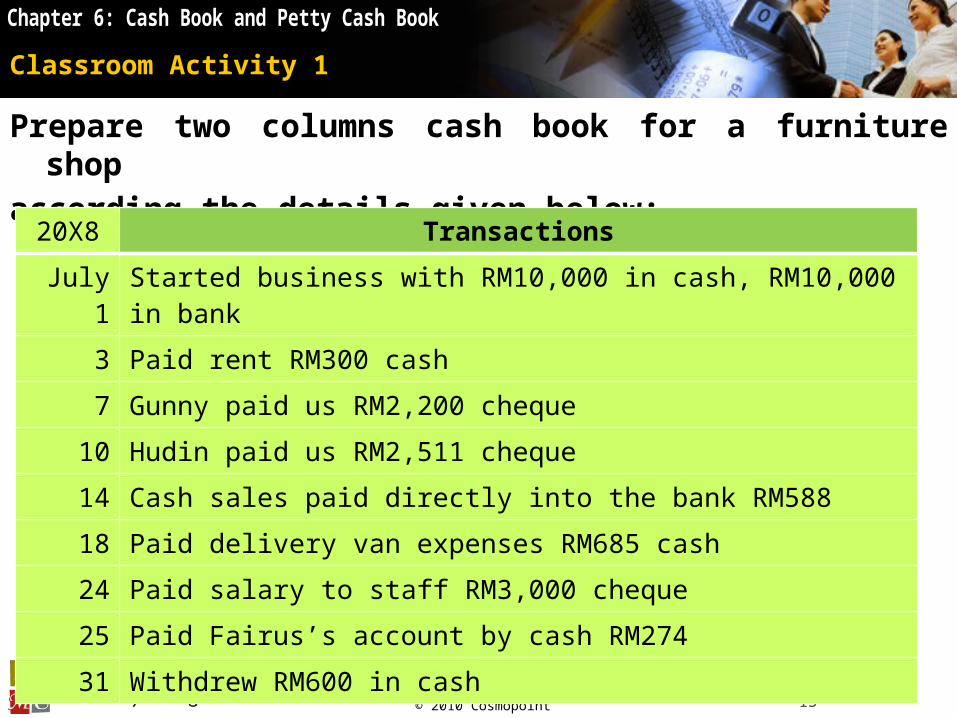

Classroom Activity 1

Prepare two columns cash book for a furniture shop

according the details given below:

20X8 Transactions

July 1 Started business with RM10,000 in cash, RM10,000 in bank

3 Paid rent RM300 cash

7 Gunny paid us RM2,200 cheque

10 Hudin paid us RM2,511 cheque

14 Cash sales paid directly into the bank RM588

18 Paid delivery van expenses RM685 cash

24 Paid salary to staff RM3,000 cheque

25 Paid Fairus’s account by cash RM274

31 Withdrew RM600 in cash

Slide 15 of 15© 2010 Cosmopoint

Cash Book

July 20X8 Details Fol Cash Bank 20X8 Details Fol Cash Bank

1Capital 10,000.00 10,000.00 3Rent 300.00

7Gunny 2,200.00 18Van's Expenses 685.00

10Hudin 2,511.00 24Salary 3,000.00

14Sales 588.00 25Fairus 274.00

31Cash 600.00

31Balance c/d 8,729.00 11,711.00

10,588.00 14,711.00 10,588.00 14,711.00

1-AugBalance b/d 8,729.00 11,711.00

Slide 16 of 15© 2010 Cosmopoint

Classroom Activity 2

Prepare three (3) column cash book

20X9 Transactions

May 1 Balances brought forward Cash RM660, Bank RM7,855

4 Received payment from Shukri RM900, to settle account amounted RM1000 by cheque

9 Cash withdrew RM65

10 Received cheque from Elvin RM550 to settle account amounted RM580

15 Paid rental RM1000 cheque

18 Cash Sales RM840

18 Bought motorbike for business use RM3,000 with cheque

22 Paid Siti RM1,750 with cheque

26 Cash Purchases RM200

28 Bought furniture paying cheque RM200

Slide 17 of 15© 2010 Cosmopoint

Cash Book

May 09 Details FolDiscount Allowed Cash Bank

May 09 Details Fol

Discount Received Cash Bank

1 Capital

660.00

7,855.00 9 Cash 65.00

4 Shukri 100

900.00 15 Rental

1,000.00

10 Elvin 30

550.00 18 Motorbike

3,000.00

18 Sales

840.00 22 Siti

1,750.00

26 Purchases

200.00

28 Furniture

200.00

31 Balance c/d

1,235.00

3,355.00

1,500.00

9,305.00

1,500.00

9,305.00

1-JunBalance b/d

1,235.00

3,355.00