Asset Management Plan - Junee Shire · 4.4 Changes in Technology ... What is an Asset Management...

53

JUNEE SHIRE COUNCIL Sewerage Network Asset Management Plan Version 2 Adopted: 19 November 2013 Minute No: 20.11.13 AM4SRRC JUNEE SHIRE COUNCIL – SEWERAGE ASSET MANAGEMENT PLAN

Transcript of Asset Management Plan - Junee Shire · 4.4 Changes in Technology ... What is an Asset Management...

JUNEE SHIRE COUNCIL

Sewerage Network

Asset Management Plan

Version 2

Adopted: 19 November 2013 Minute No: 20.11.13

AM4SRRC

JUNEE SHIRE COUNCIL – SEWERAGE ASSET MANAGEMENT PLAN

Document Control Asset Management for Small, Rural or Remote Communities

Document ID: sewerage asset management plan.doc

Rev No Date Revision Details Author Reviewer Approver

1 February 2012 Original document DE DES Council

2 September 2013 Update valuations and forecast expenditure DE DES Council

Asset Management for Small, Rural or Remote Communities Practice Note

The Institute of Public Works Engineering Australia.

www.ipwea.org.au/AM4SRRC

© Copyright 2011 – All rights reserved.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- i -

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY ................................................................................................................... iii 2. INTRODUCTION ............................................................................................................................... 1

2.1 Background ............................................................................................................................. 1 2.2 Goals and Objectives of Asset Management .......................................................................... 3 2.3 Plan Framework ...................................................................................................................... 3 2.4 Core and Advanced Asset Management ................................................................................. 5 2.5 Community Consultation ........................................................................................................ 5

3. LEVELS OF SERVICE .......................................................................................................................... 5 3.1 Customer Research and Expectations .................................................................................... 5 3.2 Strategic and Corporate Goals ................................................................................................ 5 3.3 Legislative Requirements ........................................................................................................ 6 3.4 Current Levels of Service......................................................................................................... 7 3.4 Desired Levels of Service ....................................................................................................... 11

4. FUTURE DEMAND ......................................................................................................................... 11 4.1 Demand Drivers .................................................................................................................... 11 4.2 Demand Forecast .................................................................................................................. 11 4.3 Demand Impact on Assets .................................................................................................... 11 4.4 Changes in Technology ......................................................................................................... 12 4.5 Demand Management Plan .................................................................................................. 12 4.4 Asset Programs to meet Demand ......................................................................................... 12

5. LIFECYCLE MANAGEMENT PLAN ................................................................................................... 14 5.1 Background Data ................................................................................................................... 14 5.2 Infrastructure Risk Management Plan .................................................................................. 16 5.3 Routine Maintenance Plan .................................................................................................... 17 5.4 Renewal/Replacement Plan .................................................................................................. 18 5.5 Creation/Acquisition/Upgrade Plan ...................................................................................... 20 5.6 Disposal Plan ......................................................................................................................... 22 5.7 Service Consequences and Risks ........................................................................................... 22

6. FINANCIAL SUMMARY ................................................................................................................... 23 6.1 Financial Statements and Projections ................................................................................... 23 6.2 Funding Strategy ................................................................................................................... 27 6.3 Valuation Forecasts ............................................................................................................... 27 6.4 Key Assumptions made in Financial Forecasts...................................................................... 29 6.5 Forecast Reliability and Confidence ...................................................................................... 30

7. PLAN IMPROVEMENT AND MONITORING .................................................................................... 31 7.1 Status of Asset Management Practices ................................................................................ 31 7.2 Asset Management Systems ................................................................................................. 31 7.3 Improvement Program.......................................................................................................... 32 7.4 Monitoring and Review Procedures ..................................................................................... 32 7.5 Performance Measures ......................................................................................................... 32

REFERENCES .......................................................................................................................................... 33 APPENDICES .......................................................................................................................................... 34

Appendix A Maintenance Response Levels of Service .................................................................... 35 Appendix B Projected 10 year Capital Renewal Works Program .................................................... 36 Appendix C Planned Upgrade/Exp/New 10 year Capital Works Program ...................................... 37 Appendix D Abbreviations ............................................................................................................... 41 Appendix E Glossary ........................................................................................................................ 42

JUNEE SHIRE COUNCIL – SEWERAGE ASSET MANAGEMENT PLAN

- ii -

This page is left intentionally blank.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- iii -

1. EXECUTIVE SUMMARY

Context Junee Shire is located in the south-west slopes of NSW, bordered by Wagga City to its south, Coolamon to its west, Temora and Cootamundra to the north and Gundagai to the east. The Local Government area (LGA) is centred on the township of Junee, population of the shire is approximately 6083.

Agriculture is the dominant industry for the LGA and the pressures of drought, rising input prices and lower commodity prices are shared across the Shire.

The sewerage network provides for the conveyance, treatment and re-use of wastewater for the town of Junee.

The majority of the network was constructed early in the 20th century and, as such, these assets are coming to the end of their useful life. This poses a major challenge for the Council in terms of funding the renewal of these assets whilst maintaining existing levels of service.

As the issue of water security receives more attention and a greater importance is placed on securing water resources, it is expected that mandatory or minimum levels of service – in terms of the quality of wastewater treatment – will be raised.

The Sewerage Service The sewerage network comprises: • Approximately 41km of gravity sewer main • A trickling filter wastewater treatment plant • A Pasveer Channel wastewater treatment plant • Treated-effluent storage ponds • Treated effluent reticulation network comprising

four pumps and approximately 4.5km of pressure main

These infrastructure assets have a replacement value of $20.06 million.

What does it Cost? The projected outlays necessary to provide the services covered by this Asset Management Plan (AM Plan) includes operations, maintenance, renewal and upgrade of existing assets over the 10 year planning period is $9,228,000 or $923,000 on average per year.

Estimated available funding for this period is $7,780,000 or $778,000 on average per year which is 84% of the cost to provide the service. This is a funding shortfall of $145,000 on average per year. Projected expenditure required to provide services in the AM Plan compared with planned expenditure

currently included in the Long Term Financial Plan are shown in the graph below.

The shortfall can be largely attributed to the forecast renewal of the wastewater treatment plant in 2020. To address this, low cost renewal options will be explored, as will the viability of increasing funding for these works.

What we will do Council plans to provide sewerage services for the following: • Operation, maintenance, renewal and upgrade of

sewer mains, treatment facilities and the re-use network to meet service levels set by the Council in annual budgets.

• Construction of a new treatment facility within the 10 year planning period to replace the existing facility.

Managing the Risks There are risks associated with providing the service and not being able to complete all identified activities and projects. We have identified major risks as: • High levels of inflow and infiltration • Increasingly tight restrictions on treatment

standards • Excess loading of treatment works • Blockages and collapse of gravity mains

We will endeavour to manage these risks within available funding by: • Continuing with programmed renewals, focusing

on areas of high inflow and; locating and terminating illegal connections

• Undertaking cost effective improvements to the treatment process

• Record and monitor faults in the network and understand why and when they happen

The Next Steps The actions resulting from this asset management plan are:

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- iv -

• Develop system to link AM with financial services Questions you may have What is this plan about? This asset management plan covers the infrastructure assets that serve the Junee community’s wastewater treatment needs. These assets include sewer mains, man holes, treatment plants and the re-use reticulation network throughout the Council area that provides for the safe and effective treatment of wastewater and its reuse.

What is an Asset Management Plan? Asset management planning is a comprehensive process to ensure delivery of services from infrastructure is provided in a financially sustainable manner.

An asset management plan details information about infrastructure assets including actions required to provide an agreed level of service in the most cost effective manner. The Plan defines the services to be provided, how the services are provided and what funds are required to provide the services.

Is there a funding shortfall? Most of the Council’s sewerage network was constructed from government grants often provided and accepted without consideration of ongoing operations, maintenance and replacement needs.

Many of these assets are approaching the latter years of their life and require replacement; services from the assets are decreasing and maintenance costs are increasing.

The Councils’ present funding levels though are sufficient to continue to provide existing services at current levels in the medium term.

What options do we have? To protect against a funding shortfall several steps are involved: 1. Improving asset knowledge so that data

accurately records the asset inventory, how assets are performing and when assets are not able to provide the required service levels,

2. Improving our efficiency in operating, maintaining, replacing existing and constructing new assets to optimise life cycle costs,

3. Identifying and managing risks associated with providing services from infrastructure,

4. Making tradeoffs between service levels and costs to ensure that the community receives the best return from infrastructure,

5. Indentifying assets surplus to needs for disposal to make saving in future operations and maintenance costs

6. Consulting with the community to ensure that sewerage services and costs meet community needs and are affordable,

7. Developing partnership with other bodies, where available to provide services;

8. Seeking additional funding from governments and other bodies to better reflect a ‘whole of government’ funding approach to infrastructure services.

What happens if we don’t manage the assets? If not managed correctly, we will have a shortfall and it is likely that council will have to reduce service levels in some areas, unless new sources of revenue are found. For sewerage, the service level reduction may include increased response times to more frequent network failures, reduced quality of wastewater treatment or the loss of treated effluent as a resource for the community.

What can we do? Council can develop options and priorities for future sewerage services with costs of providing the services, consult with the community to plan future services to match the community services needs with ability to pay for services and maximise benefit to the community for costs to the community.

What can you do? Council will be pleased to consider your thoughts on the issues raised in this asset management plan and suggestions on how Council may change its sewerage services mix to ensure that the appropriate level of service can be provided to the community.

.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 1 -

2. INTRODUCTION

2.1 Background

This asset management plan is to demonstrate responsive management of assets (and services provided from assets), compliance with regulatory requirements, and to communicate funding needed to provide the required levels of service.

The asset management plan is to be read with Council’s Asset Management Policy, Asset Management Strategy and the following associated planning documents:

• Strategic Business Plan – Sewerage 2011-2030 • Long Term Financial Plan 2013-14 • Delivery Plan 2014 • Operational Plan 2013-14 • Community Strategic Plan 2013-14

The infrastructure assets covered by this asset management plan are shown in Table 2.1.

Table 2.1: Assets covered by this Plan

Asset category Dimension Replacement Value Gravity Sewer Network 41.4km $11,844,333 Wastewater Treatment Plant 4500EP $6,384,469 Effluent Re-Use Plant 262ML p.a. $954,600 Effluent Re-Use Trunk Mains 4.5km $876,375 TOTAL $20,059,777 Key stakeholders in the preparation and implementation of this asset management plane are shown in Table 2.1.1.

Table 2.1.1: Key Stakeholders in the AM Plan Key Stakeholder Role in Asset Management Plan

Councillors • Represent needs of community/shareholders, • Allocate resources to meet the organisation’s objectives in providing services

while managing risks, • Ensure organisation is financially sustainable.

General Manager • Ensure Council’s policies and strategies are implemented

Director of Engineering • Ensure all Sewerage Assets are maintained and renewed in accordance with this Asset Management Plan

Community, Visitors & Tourists • To provide input and feedback on the levels of service that Council provides

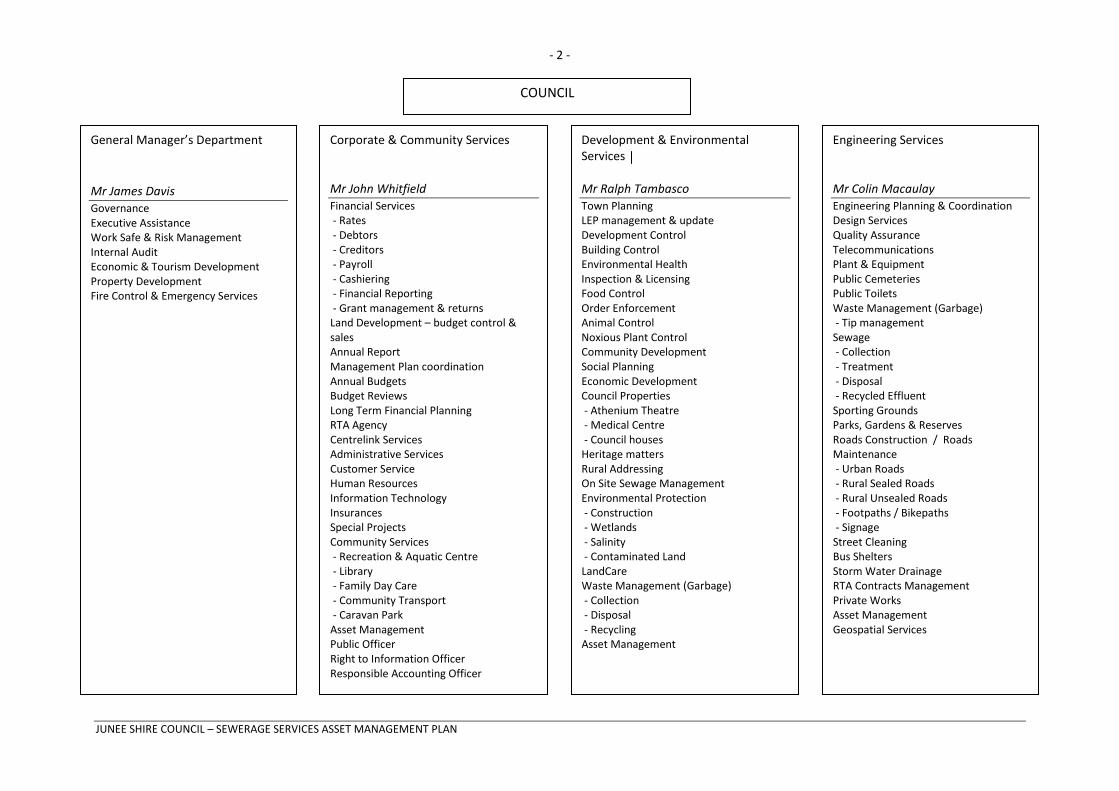

Other Government Bodies • To provide additional grant funding Our organisation’s organisational structure for service delivery from infrastructure assets is detailed below:

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 2 -

General Manager’s Department Mr James Davis Governance Executive Assistance Work Safe & Risk Management Internal Audit Economic & Tourism Development Property Development Fire Control & Emergency Services

Corporate & Community Services Mr John Whitfield Financial Services - Rates - Debtors - Creditors - Payroll - Cashiering - Financial Reporting - Grant management & returns Land Development – budget control & sales Annual Report Management Plan coordination Annual Budgets Budget Reviews Long Term Financial Planning RTA Agency Centrelink Services Administrative Services Customer Service Human Resources Information Technology Insurances Special Projects Community Services - Recreation & Aquatic Centre - Library - Family Day Care - Community Transport - Caravan Park Asset Management Public Officer Right to Information Officer Responsible Accounting Officer

Development & Environmental Services Mr Ralph Tambasco Town Planning LEP management & update Development Control Building Control Environmental Health Inspection & Licensing Food Control Order Enforcement Animal Control Noxious Plant Control Community Development Social Planning Economic Development Council Properties - Athenium Theatre - Medical Centre - Council houses Heritage matters Rural Addressing On Site Sewage Management Environmental Protection - Construction - Wetlands - Salinity - Contaminated Land LandCare Waste Management (Garbage) - Collection - Disposal - Recycling Asset Management

Engineering Services Mr Colin Macaulay Engineering Planning & Coordination Design Services Quality Assurance Telecommunications Plant & Equipment Public Cemeteries Public Toilets Waste Management (Garbage) - Tip management Sewage - Collection - Treatment - Disposal - Recycled Effluent Sporting Grounds Parks, Gardens & Reserves Roads Construction / Roads Maintenance - Urban Roads - Rural Sealed Roads - Rural Unsealed Roads - Footpaths / Bikepaths - Signage Street Cleaning Bus Shelters Storm Water Drainage RTA Contracts Management Private Works Asset Management Geospatial Services

COUNCIL

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 3 -

2.2 Goals and Objectives of Asset Management The organisation exists to provide sewerage services to its community. All of these services are provided by infrastructure assets. We have acquired infrastructure assets from construction by our staff, from government grants and rate income.

Our goal in managing infrastructure assets is to meet the defined level of service (as amended from time to time) in the most cost effective manner for present and future consumers. The key elements of infrastructure asset management are:

• Providing a defined level of service and monitoring performance, • Managing the impact of growth through demand management and infrastructure investment, • Taking a lifecycle approach to developing cost-effective management strategies for the long-term that meet

the defined level of service, • Identifying, assessing and appropriately controlling risks, and • Having a long-term financial plan which identifies required, affordable expenditure and how it will be

financed.

2.3 Plan Framework

Key elements of the plan are

• Levels of service – specifies the services and levels of service to be provided by the organisation, • Future demand – how this will impact on future service delivery and how this is to be met, • Life cycle management – how we will manage our existing and future assets to provide defined levels of

service, • Financial summary – what funds are required to provide the defined services, • Asset management practices, • Monitoring – how the plan will be monitored to ensure it is meeting the organisation’s objectives, • Asset management improvement plan.

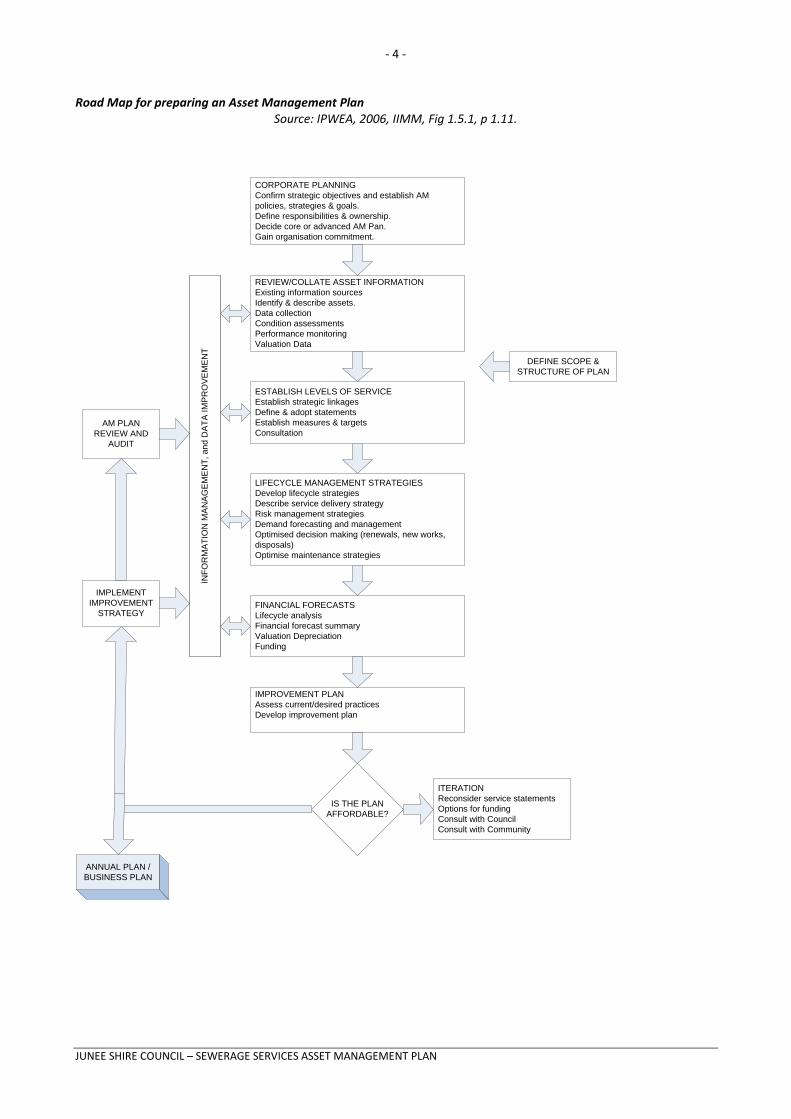

A road map for preparing an asset management plan is shown below.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 4 -

Road Map for preparing an Asset Management Plan Source: IPWEA, 2006, IIMM, Fig 1.5.1, p 1.11.

IS THE PLAN AFFORDABLE?

CORPORATE PLANNINGConfirm strategic objectives and establish AM policies, strategies & goals. Define responsibilities & ownership.Decide core or advanced AM Pan.Gain organisation commitment.

REVIEW/COLLATE ASSET INFORMATIONExisting information sourcesIdentify & describe assets.Data collectionCondition assessmentsPerformance monitoringValuation Data

ESTABLISH LEVELS OF SERVICEEstablish strategic linkagesDefine & adopt statementsEstablish measures & targetsConsultation

LIFECYCLE MANAGEMENT STRATEGIESDevelop lifecycle strategiesDescribe service delivery strategyRisk management strategiesDemand forecasting and managementOptimised decision making (renewals, new works, disposals)Optimise maintenance strategies

FINANCIAL FORECASTSLifecycle analysisFinancial forecast summaryValuation DepreciationFunding

IMPROVEMENT PLANAssess current/desired practicesDevelop improvement plan

ITERATIONReconsider service statementsOptions for fundingConsult with CouncilConsult with Community

DEFINE SCOPE & STRUCTURE OF PLAN

INFO

RM

ATI

ON

MA

NA

GE

ME

NT,

and

DA

TA IM

PR

OV

EM

EN

T

AM PLAN REVIEW AND

AUDIT

IMPLEMENT IMPROVEMENT

STRATEGY

ANNUAL PLAN / BUSINESS PLAN

INFO

RM

ATI

ON

MA

NA

GE

ME

NT,

and

DA

TA IM

PR

OV

EM

EN

T

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 5 -

2.4 Core and Advanced Asset Management

This asset management plan is prepared as a first cut ‘core’ asset management plan in accordance with the International Infrastructure Management Manual1. It is prepared to meet minimum legislative and organisational requirements for sustainable service delivery and long term financial planning and reporting. Core asset management is a ‘top down’ approach where analysis is applied at the ‘system’ or ‘network’ level.

2.5 Community Consultation

This ‘core’ asset management plan is prepared to facilitate community consultation initially through feedback on public display of draft asset management plans prior to adoption by Council. Future revisions of the asset management plan will incorporate community consultation on service levels and costs of providing the service. This will assist Council and the community in matching the level of service needed by the community, service risks and consequences with the community’s ability to pay for the service.

Future revisions of this asset management plan will move towards ‘advanced’ asset management using a ‘bottom up’ approach for gathering asset information for individual assets to support the optimisation of activities and programs to meet agreed service levels.

3. LEVELS OF SERVICE

3.1 Customer Research and Expectations

Junee Shire Council conducted a considerable community survey in 2011. From this survey, satisfaction with sewerage services were rated as being above average when compared to other services provided by council, however the importance of sewerage services were rated as being below average.

3.2 Strategic and Corporate Goals

This asset management plan is prepared under the direction of the organisation’s vision, mission, goals and objectives.

Our vision is:

“Junee will be a great place to live, with a healthy civic pride. That will come about because the amenity of the shire – social, recreational, cultural, environmental and visual – is the best quality possible given our circumstances. There will be an increase in population because of this, with the increase made up of people who are net contributors to the community.” “Junee will be prosperous and existing services and businesses will have been preserved and grown. The shire will have economic development strategies recognising the different circumstances of urban and rural areas.” “Junee will be a place where innovative, responsive leadership and management occurs in all facets of community life.” “It will be an independent Local Government area with a strong sense of identity.”

Our mission is:

“Through effective leadership and management, Junee Shire Council will enable the Shire to advance systematically towards its desired vision.”

Relevant organisation goals and objectives and how these are addressed in this asset management plan are:

1 IPWEA, 2006.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 6 -

Table 3.2: Organisation Goals and how these are addressed in this Plan

Goal Objective How Goal and Objectives are addressed in AM Plan

Theme 1: A Growing Community

1.15: Provide and maintain efficient sewerage systems and allow for required expansion.

This asset management plan has addressed future demand to ensure that there is funding available and capacity within the network to support the objective.

Theme 2: A Liveable Community

2.5: Develop an asset management and renewal programme

This asset management plan directly supports this objective, ensuring public assets are maintained and provided with a level of service matched to community expectations and within the financial resources available for that purpose.

Theme 2: A Liveable Community

2.15: Provide and maintain safe and serviceable public facilities and infrastructure including roads, footpaths and stormwater drains – to maintain public asset to acceptable standards.

The asset management plan identifies what funding is required to achieve this goal and objective.

Theme 2: A Liveable Community

2.17: Implement effective regulation strategies, local policies and compliance programs to manage the impact of development and maximise public and environmental health and safety.

This asset management plan has addressed future demand to ensure that the impacts on public and environmental health and safety are minimised through appropriate investment in sewerage services.

The Council will exercise its duty of care to ensure public safety in accordance with the infrastructure risk management plan prepared in conjunction with this AM Plan. Management of infrastructure risks is covered in Section 5.2

3.3 Legislative Requirements

Council has to meet many legislative requirements including Australian and State legislation and State regulations. Relevant legislation is shown in Table 3.1.

Table 3.1: Legislative Requirements

Legislation Requirement Local Government Act 1993 Sets out role, purpose, responsibilities and powers of local governments

including the preparation of a long term financial plan supported by asset management plans for sustainable service delivery.

Protection of the Environment Operations Act 1997

Governs, via an Environmental Protection Licence, the operations and activities of the sewerage network and sets effluent quality standards in order to protect and preserve the environment.

Occupational, Health and Safety Act 2000

Sets out roles and responsibilities to secure the health, safety and welfare of persons at work.

Protection of Environment (Administration) Act 1991

The objects of this Act is to constitute the Environment Protection Authority, to provide integrated administration for environment protection and to require the Authority to perform particular tasks in relation to the quality of the environment, environmental audit and reports on the state of the environment.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 7 -

Environmental Planning and Assessment Act 1979

Sets out to encourage the proper management, development and conservation of natural and artificial resources for the purpose of promoting the social and economic welfare of the community and a better environment and the protection of the environment, including the protection and conservation of native animals and plants, including threatened species, populations and ecological communities, and their habitats.

National Environmental Protection Measures (Implementation) Act 1998

The objects of this Act are to make provision for the implementation of national environmental protection measures to protect, restore and enhance the quality of the environment and to ensure that the community has access to relevant and meaningful information about pollution in Australia. It is based on an Intergovernmental Agreement on the Environment 1992 (‘the IGAE’), in which the Commonwealth, State and Territory Governments agreed to work together to develop uniform national environment protection standards for the control of air, water, land and noise pollution.

Workers Compensation Act 1987 Sets out to provide for the compensation and rehabilitation of workers in respect of work related injuries.

Public Health Act 1991 The objectives of this Act are to protect the public health of the community.

Waste Avoidance and Resource Recovery Act 2001

The objects of this Act are to encourage the most efficient use of resources, to provide for the continual reduction in waste generation, to minimise the consumption of natural resources, to ensure efficient funding of waste and resource management planning and to assist with the achievement of the objectives of the Protection of Environment Operations Act.

Public Works Act 1912 Sets out to provide the legal framework for an effective and transparent operation of Public Works in NSW.

Civil Liabilities Act 2002 Sets out to make provision in relation to the recovery of damages for death or personal injury caused by the fault or negligent of a person or organisations.

Native Vegetation Conservation Act 1997

The objects of this Act are to provide for the conservation and management of native vegetation, including protection, encouragement and promotion, improving the existing condition, encouraging revegetation and rehabilitation, preventing inappropriate clearing, and promoting the significance of native vegetation, all in accordance with the principles of ecologically sustainable development.

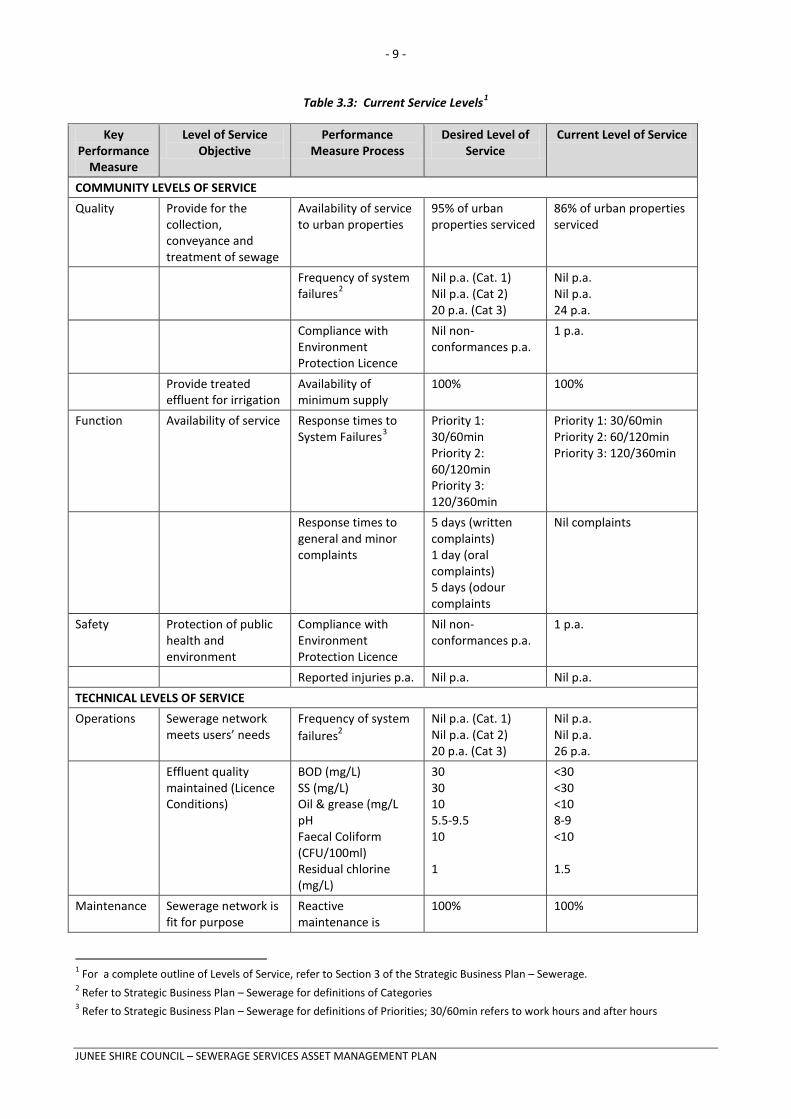

Other relevant Acts and Legislation As required. 3.4 Current Levels of Service Council has defined service levels in two terms.

Community Levels of Service - Relate to the service outcomes that the community wants in terms of safety, quality, quantity, reliability, responsiveness, cost effectiveness and legislative compliance.

Community levels of service measures used in the asset management plan are:

Quality How good is the service? Function Does it meet users’ needs? Safety Is the service safe?

Technical Levels of Service - Supporting the community service levels are operational or technical measures of performance. These technical measures relate to the allocation of resources to service activities that the council undertakes to best achieve the desired community outcomes.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 8 -

Technical service covers:

• Operations – the regular activities to provide services such as opening hours, cleansing frequency, mowing frequency, etc. and licence conditions,

• Maintenance – the activities necessary to retain an assets as near as practicable to its original condition (eg road patching, unsealed road grading, building and structure repairs),

• Renewal – the activities that return the service capability of an asset up to that which it had originally (eg frequency and cost of road resurfacing and pavement reconstruction, pipeline replacement and building component replacement),

• Upgrade – the activities to provide a higher level of service (eg widening a road, sealing an unsealed road, replacing a pipeline with a larger size) or a new service that did not exist previously (eg a new library).

Council’s current service levels are detailed in Table 3.3.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 9 -

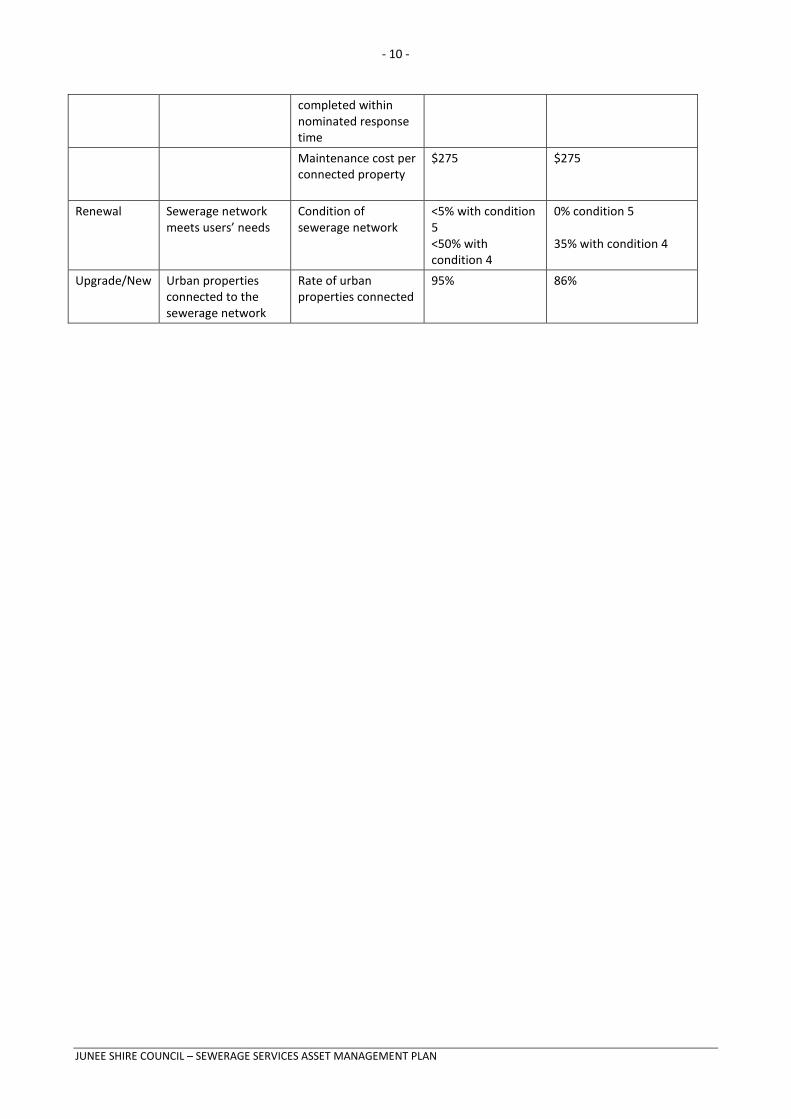

Table 3.3: Current Service Levels1

Key Performance

Measure

Level of Service Objective

Performance Measure Process

Desired Level of Service

Current Level of Service

COMMUNITY LEVELS OF SERVICE Quality Provide for the

collection, conveyance and treatment of sewage

Availability of service to urban properties

95% of urban properties serviced

86% of urban properties serviced

Frequency of system failures2

Nil p.a. (Cat. 1) Nil p.a. (Cat 2) 20 p.a. (Cat 3)

Nil p.a. Nil p.a. 24 p.a.

Compliance with Environment Protection Licence

Nil non-conformances p.a.

1 p.a.

Provide treated effluent for irrigation

Availability of minimum supply

100% 100%

Function Availability of service Response times to System Failures3

Priority 1: 30/60min Priority 2: 60/120min Priority 3: 120/360min

Priority 1: 30/60min Priority 2: 60/120min Priority 3: 120/360min

Response times to general and minor complaints

5 days (written complaints) 1 day (oral complaints) 5 days (odour complaints

Nil complaints

Safety Protection of public health and environment

Compliance with Environment Protection Licence

Nil non-conformances p.a.

1 p.a.

Reported injuries p.a. Nil p.a. Nil p.a. TECHNICAL LEVELS OF SERVICE Operations Sewerage network

meets users’ needs Frequency of system failures2

Nil p.a. (Cat. 1) Nil p.a. (Cat 2) 20 p.a. (Cat 3)

Nil p.a. Nil p.a. 26 p.a.

Effluent quality maintained (Licence Conditions)

BOD (mg/L) SS (mg/L) Oil & grease (mg/L pH Faecal Coliform (CFU/100ml) Residual chlorine (mg/L)

30 30 10 5.5-9.5 10 1

<30 <30 <10 8-9 <10 1.5

Maintenance Sewerage network is fit for purpose

Reactive maintenance is

100% 100%

1 For a complete outline of Levels of Service, refer to Section 3 of the Strategic Business Plan – Sewerage. 2 Refer to Strategic Business Plan – Sewerage for definitions of Categories 3 Refer to Strategic Business Plan – Sewerage for definitions of Priorities; 30/60min refers to work hours and after hours

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 10 -

completed within nominated response time

Maintenance cost per connected property

$275

$275

Renewal Sewerage network meets users’ needs

Condition of sewerage network

<5% with condition 5 <50% with condition 4

0% condition 5 35% with condition 4

Upgrade/New Urban properties connected to the sewerage network

Rate of urban properties connected

95% 86%

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 11 -

3.4 Desired Levels of Service

At present, indications of desired levels of service are obtained from various sources including residents’ feedback to Councillors and staff, service requests and correspondence. Council has yet to quantify desired levels of service. This will be done in future revisions of this asset management plan.

4. FUTURE DEMAND

4.1 Demand Drivers

Factors affecting demand include population change, changes in demographics, seasonal factors, consumer preferences and expectations, economic factors, environmental awareness, etc.

4.2 Demand Forecast

Demand factor trends and impacts on service delivery are summarised in Table 4.1.

4.3 Demand Impact on Assets

The impact of demand drivers that may affect future service delivery and utilisation of assets are shown in Table 4.1.

Table 4.1: Demand Factors, Projections and Impact on Services

Demand factor Present position Projection Impact on services Population The sewerage network serves

approximately 4100 people across 1680 premises.

Population growth is forecast to continue at approximately 1% p.a.

This will increase the loading on the network. By the year 2031 an additional 932 people in 370 new properties will require sewerage services.

Demographics Junee Shire has an age distribution similar to that of the State with a slightly higher proportion of 18-64 year olds. 65+ accounts for approximately 15%

The biggest change will be in the 65+ age category which will see an increase to 23% by 2031 (Dept. Planning projections)

These demographic factors will shape the type of future development the Shire will see. The effect on the network will predominantly relate to the density of premise serviced.

Water security/Climate Change

Presently 100% of average flows are recycled. Recently, wetter than average months have led to unprecedented discharges to the environment.

Forecasts are for increased volatility in rainfall patterns leading to larger, more frequent extreme events, but an overall drying climate.

There will be an increased peak loading on the network based on current inflow and infiltration rates. An overall drying climate will place greater demands for capture and reuse of treated effluent. Effluent storages will require a greater storage capacity to provide effluent during longer periods of dry weather and drought.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 12 -

4.4 Changes in Technology

Technology changes forecast to affect the delivery of services covered by this plan are detailed in Table 4.2.

Table 4.2: Changes in Technology and Forecast effect on Service Delivery

Technology Change Effect on Service Delivery Enhanced/improved communication and automation.

Reduced demand on staff lead to overall resource savings which in turn can be re-invested into bettering service delivery.

4.5 Demand Management Plan

Demand for new services will be managed through a combination of managing existing assets, upgrading of existing assets and providing new assets to meet demand and demand management. Demand management practices include non-asset solutions, insuring against risks and managing failures.

Non-asset solutions focus on providing the required service without the need for the council to own the assets. Examples of non-asset solutions include providing services from existing infrastructure such as aquatic centres and libraries that may be in another council area or public toilets provided in commercial premises.

Opportunities identified to date for demand management are shown in Table 4.3. Further opportunities will be developed in future revisions of this asset management plan.

Table 4.3: Demand Management Plan Summary

Service Activity Demand Management Plan Sewage collection and conveyance

Infiltration and inflow (I&I), if not managed correctly, may lead to localised network failures occurring on a more regular basis. In addressing I & I, a multi-pronged approach is to be taken involving a mains inspection program, monitoring of critical mains and the detection of illegal connections. Increased hydraulic loading may also occur on existing mains due to infill or upstream development. If not managed competently, these increases in hydraulic loading may result in surcharges downstream or costly capital upgrades of existing mains.

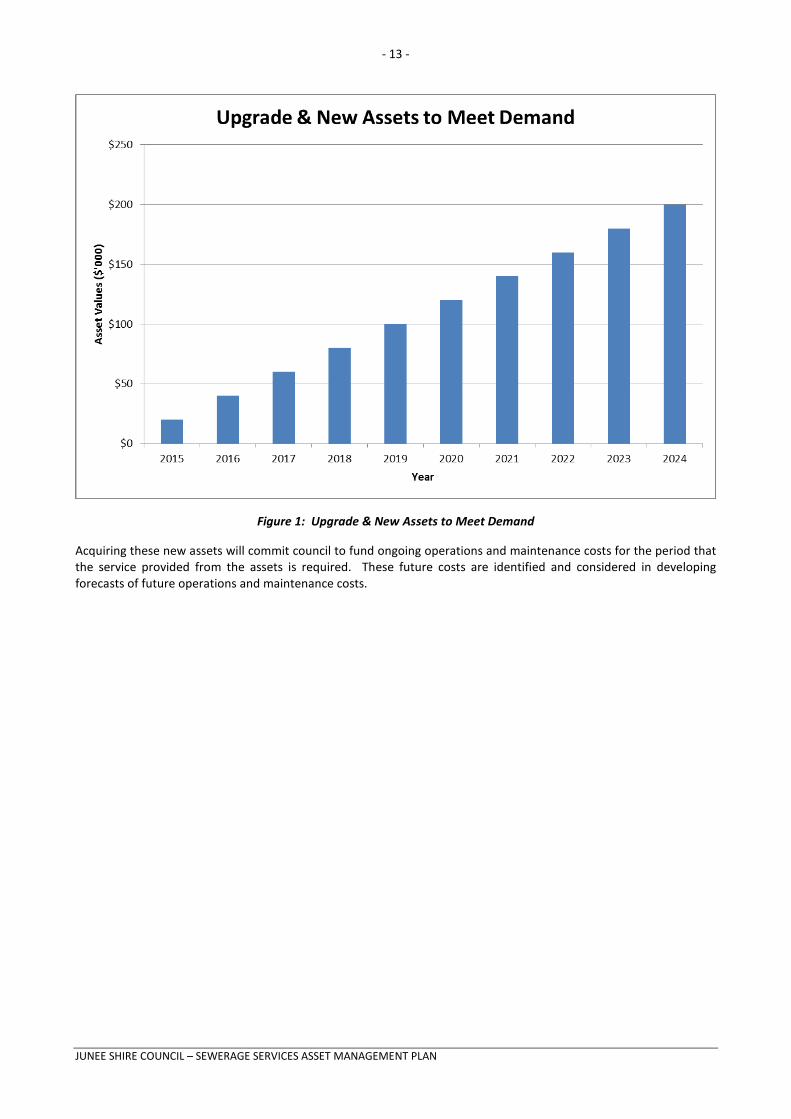

4.4 Asset Programs to meet Demand The new assets required to meet growth will be acquired free of cost from land developments and constructed/acquired by Council. The new contributed and constructed asset values are summarised in Figure 1.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 13 -

Figure 1: Upgrade & New Assets to Meet Demand

Acquiring these new assets will commit council to fund ongoing operations and maintenance costs for the period that the service provided from the assets is required. These future costs are identified and considered in developing forecasts of future operations and maintenance costs.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 14 -

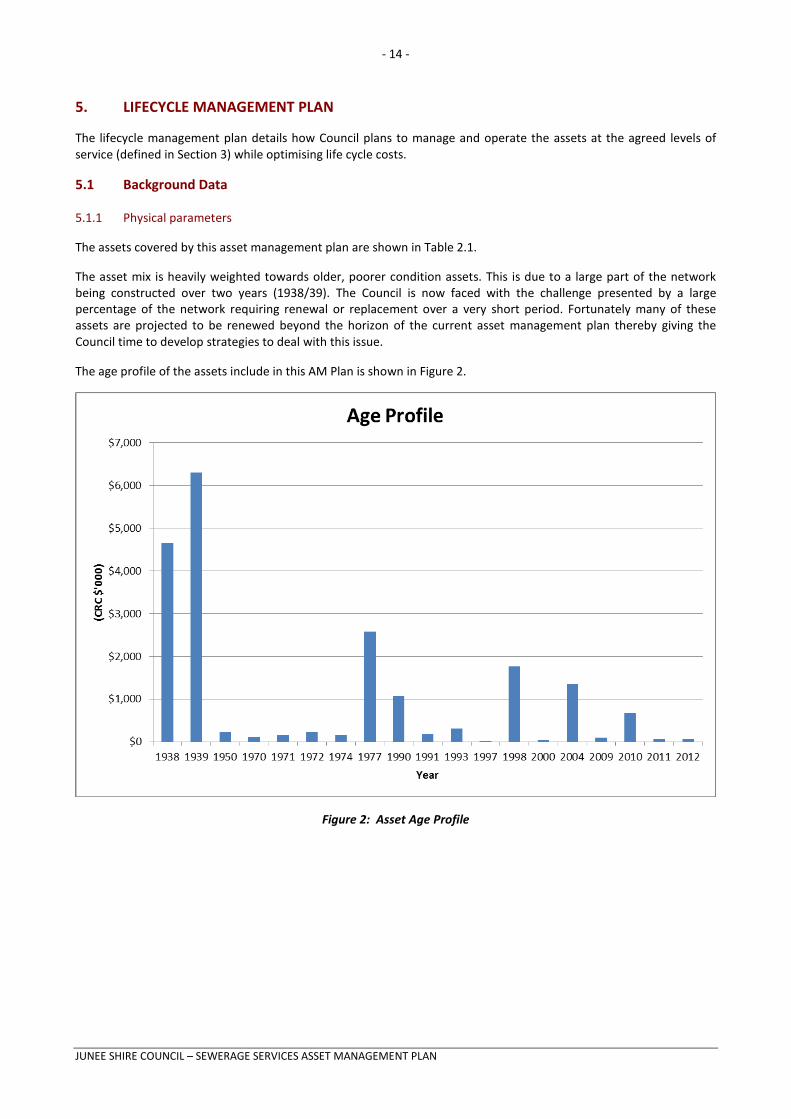

5. LIFECYCLE MANAGEMENT PLAN

The lifecycle management plan details how Council plans to manage and operate the assets at the agreed levels of service (defined in Section 3) while optimising life cycle costs.

5.1 Background Data

5.1.1 Physical parameters

The assets covered by this asset management plan are shown in Table 2.1.

The asset mix is heavily weighted towards older, poorer condition assets. This is due to a large part of the network being constructed over two years (1938/39). The Council is now faced with the challenge presented by a large percentage of the network requiring renewal or replacement over a very short period. Fortunately many of these assets are projected to be renewed beyond the horizon of the current asset management plan thereby giving the Council time to develop strategies to deal with this issue.

The age profile of the assets include in this AM Plan is shown in Figure 2.

Figure 2: Asset Age Profile

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 15 -

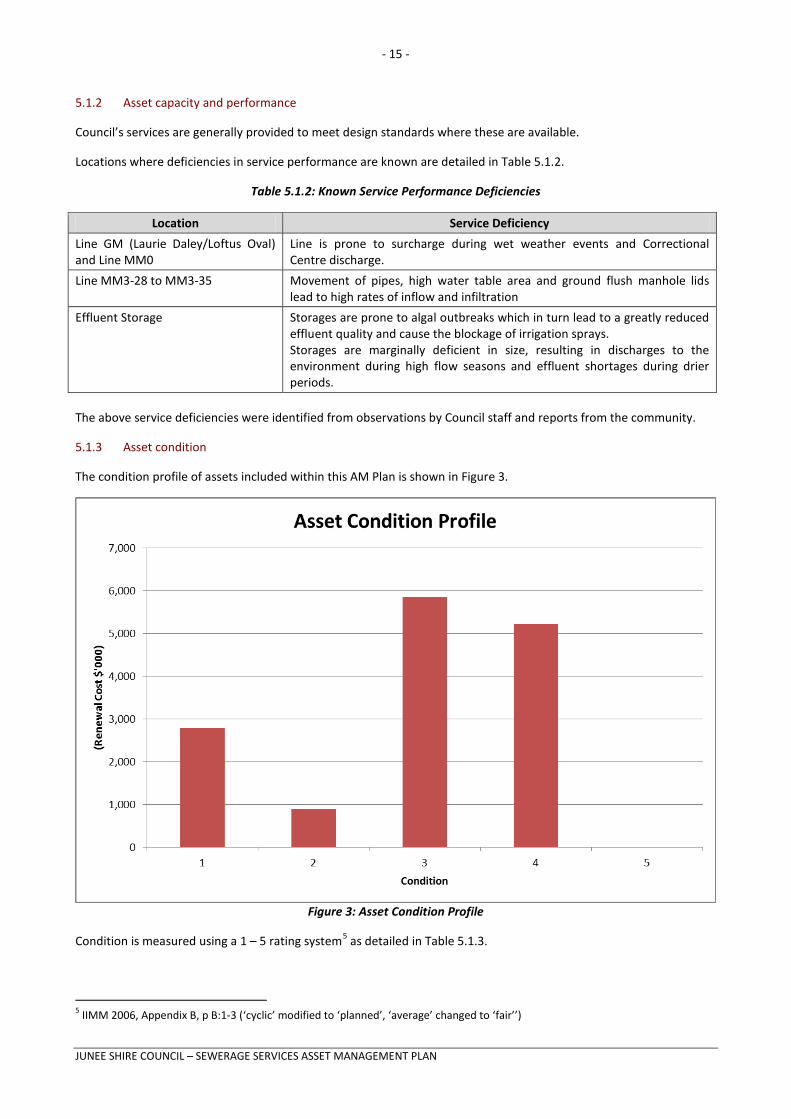

5.1.2 Asset capacity and performance

Council’s services are generally provided to meet design standards where these are available.

Locations where deficiencies in service performance are known are detailed in Table 5.1.2.

Table 5.1.2: Known Service Performance Deficiencies

Location Service Deficiency Line GM (Laurie Daley/Loftus Oval) and Line MM0

Line is prone to surcharge during wet weather events and Correctional Centre discharge.

Line MM3-28 to MM3-35 Movement of pipes, high water table area and ground flush manhole lids lead to high rates of inflow and infiltration

Effluent Storage Storages are prone to algal outbreaks which in turn lead to a greatly reduced effluent quality and cause the blockage of irrigation sprays. Storages are marginally deficient in size, resulting in discharges to the environment during high flow seasons and effluent shortages during drier periods.

The above service deficiencies were identified from observations by Council staff and reports from the community.

5.1.3 Asset condition

The condition profile of assets included within this AM Plan is shown in Figure 3.

Figure 3: Asset Condition Profile

Condition is measured using a 1 – 5 rating system5 as detailed in Table 5.1.3.

5 IIMM 2006, Appendix B, p B:1-3 (‘cyclic’ modified to ‘planned’, ‘average’ changed to ‘fair’’)

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 16 -

Residual Value

Depreciable Amount

Useful Life

Current Replacement

Cost

End of reporting period 1

Annual Depreciation

Expense

End of reporting period 2

Accumulated Depreciation

Depreciated Replacement

Cost

Table 5.1.3: IIMM Description of Condition

Condition Rating Description 1 Excellent condition: Only planned maintenance required. 2 Very good: Minor maintenance required plus planned maintenance. 3 Good: Significant maintenance required. 4 Fair: Significant renewal/upgrade required. 5 Poor: Unserviceable.

5.1.4 Asset valuations

The value of assets recorded in the asset register as at 30 June 2013 covered by this asset management plan is shown below. Assets were last revalued at 2012.

Current Replacement Cost $20,060,000

Depreciable Amount $14,765,000

Depreciated Replacement Cost $10,483,000

Annual Depreciation Expense $219,000

Council’s sustainability reporting reports the rate of annual asset consumption and compares this to asset renewal and asset upgrade and expansion.

Asset Consumption 1.5% (Depreciation/Depreciable Amount)

Asset renewal 0.7% (Capital renewal exp/Depreciable amount)

Annual Upgrade/New 0.1% (Capital upgrade exp/Depreciable amount)

Annual Upgrade/New 0.1% (including contributed assets)

Council is currently renewing assets at 44.2% of the rate they are being consumed and increasing its asset stock by 0.1% each year.

To provide services in a financially sustainable manner, Council will need to ensure that it is renewing assets at the rate they are being consumed over the medium-long term and funding the life cycle costs for all new assets and services in its long term financial plan.

5.1.5 Asset hierarchy

Council does not currently apply an asset hierarchy to its sewerage network. The introduction of such a policy will be reviewed prior to the next review of this plan.

5.2 Infrastructure Risk Management Plan

An assessment of risks6 associated with service delivery from infrastructure assets has identified critical risks that will result in loss or reduction in service from infrastructure assets or a ‘financial shock’ to the organisation. The risk assessment process identifies credible risks, the likelihood of the risk event occurring, the consequences should the event occur, develops a risk rating, evaluates the risk and develops a risk treatment plan for non-acceptable risks.

6 Sewerage Network ‘Core’ Infrastructure Risk Management Plan, 2011

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 17 -

Critical risks, being those assessed as ‘Very High’ - requiring immediate corrective action and ‘High’ – requiring prioritised corrective action identified in the Infrastructure Risk Management Plan are summarised in Table 5.2.

Table 5.2: Critical Risks and Treatment Plans

Service or Asset at Risk

What can Happen Risk Rating (VH, H)

Risk Treatment Plan Associated Costs

Gravity Network High inflows/infiltration

H Raise manholes, replace poor condition mains, terminate illegal connections

$20,000

Gravity Network Overflows to Lower Butlers Gully at Laurie Daley Oval

H Demand management (GEO), construct by-pass

$60,000

Treatment Works Loss of power (transformer failure)

H Review capacity of transformer and likely life

$0

5.3 Routine Maintenance Plan

Routine maintenance is the regular on-going work that is necessary to keep assets operating, including instances where portions of the asset fail and need immediate repair to make the asset operational again.

5.3.1 Maintenance plan

Maintenance includes reactive, planned and specific maintenance work activities.

Reactive maintenance is unplanned repair work carried out in response to service requests and management/supervisory directions.

Planned maintenance is repair work that is identified and managed through a maintenance management system (MMS). MMS activities include inspection, assessing the condition against failure/breakdown experience, prioritising, scheduling, actioning the work and reporting what was done to develop a maintenance history and improve maintenance and service delivery performance.

Specific maintenance is replacement of higher value components/sub-components of assets that is undertaken on a regular cycle including repainting, building roof replacement, etc. This work generally falls below the capital/maintenance threshold but may require a specific budget allocation.

Actual past maintenance expenditure is shown in Table 5.3.1.

Table 5.3.1: Maintenance Expenditure Trends

Year Maintenance Expenditure 2010 $105,000 2011 $120,000 2012 $122,000

Current maintenance expenditure levels are considered to be adequate to meet required service levels. Future revision of this asset management plan will include linking required maintenance expenditures with required service levels.

Assessment and prioritisation of reactive maintenance is undertaken by operational staff using experience and judgement.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 18 -

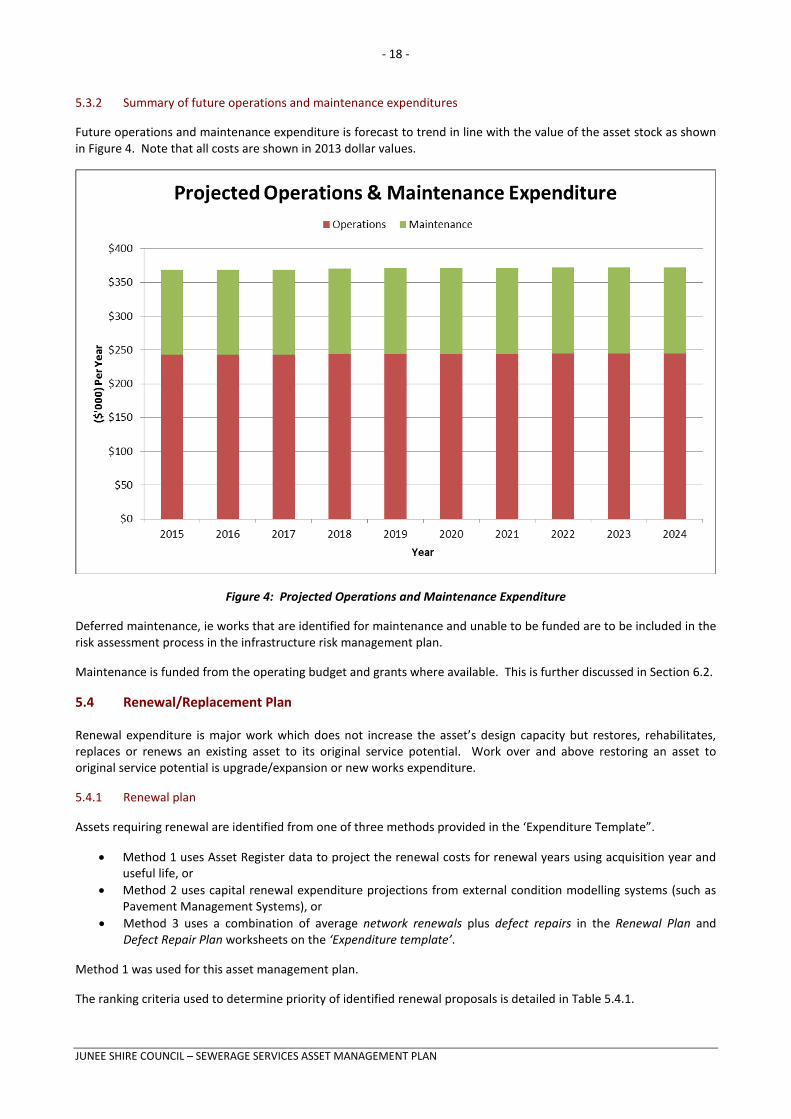

5.3.2 Summary of future operations and maintenance expenditures

Future operations and maintenance expenditure is forecast to trend in line with the value of the asset stock as shown in Figure 4. Note that all costs are shown in 2013 dollar values.

Figure 4: Projected Operations and Maintenance Expenditure

Deferred maintenance, ie works that are identified for maintenance and unable to be funded are to be included in the risk assessment process in the infrastructure risk management plan.

Maintenance is funded from the operating budget and grants where available. This is further discussed in Section 6.2.

5.4 Renewal/Replacement Plan

Renewal expenditure is major work which does not increase the asset’s design capacity but restores, rehabilitates, replaces or renews an existing asset to its original service potential. Work over and above restoring an asset to original service potential is upgrade/expansion or new works expenditure.

5.4.1 Renewal plan

Assets requiring renewal are identified from one of three methods provided in the ‘Expenditure Template”.

• Method 1 uses Asset Register data to project the renewal costs for renewal years using acquisition year and useful life, or

• Method 2 uses capital renewal expenditure projections from external condition modelling systems (such as Pavement Management Systems), or

• Method 3 uses a combination of average network renewals plus defect repairs in the Renewal Plan and Defect Repair Plan worksheets on the ‘Expenditure template’.

Method 1 was used for this asset management plan.

The ranking criteria used to determine priority of identified renewal proposals is detailed in Table 5.4.1.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 19 -

Table 5.4.1: Renewal Priority Ranking Criteria

Criteria Weighting Risk posed by asset failure (including the risk to the public, environment, legal/financial and surrounding infrastructure)

50%

Importance of asset 25% Overall benefit to network operation 25% Total 100%

Renewal will be undertaken using ‘low-cost’ renewal methods where practical. The aim of ‘low-cost’ renewals is to restore the service potential or future economic benefits of the asset by renewing the assets at a cost less than replacement cost.

Examples of low cost renewal include pipe relining or bursting. Either of these methods eliminate the need for excavation of trenches and the former can be completed with a live main.

5.4.2 Renewal standards

Renewal work is carried out in accordance with the following Standards and Specifications.

• Relevant Australian Standards

• Relevant Industry Specifications and Codes of Practice

• Relevant ‘manuals’ provided with specialised equipment (e.g. filters, mixers, screens, pumps, etc)

5.4.3 Summary of projected renewal expenditure

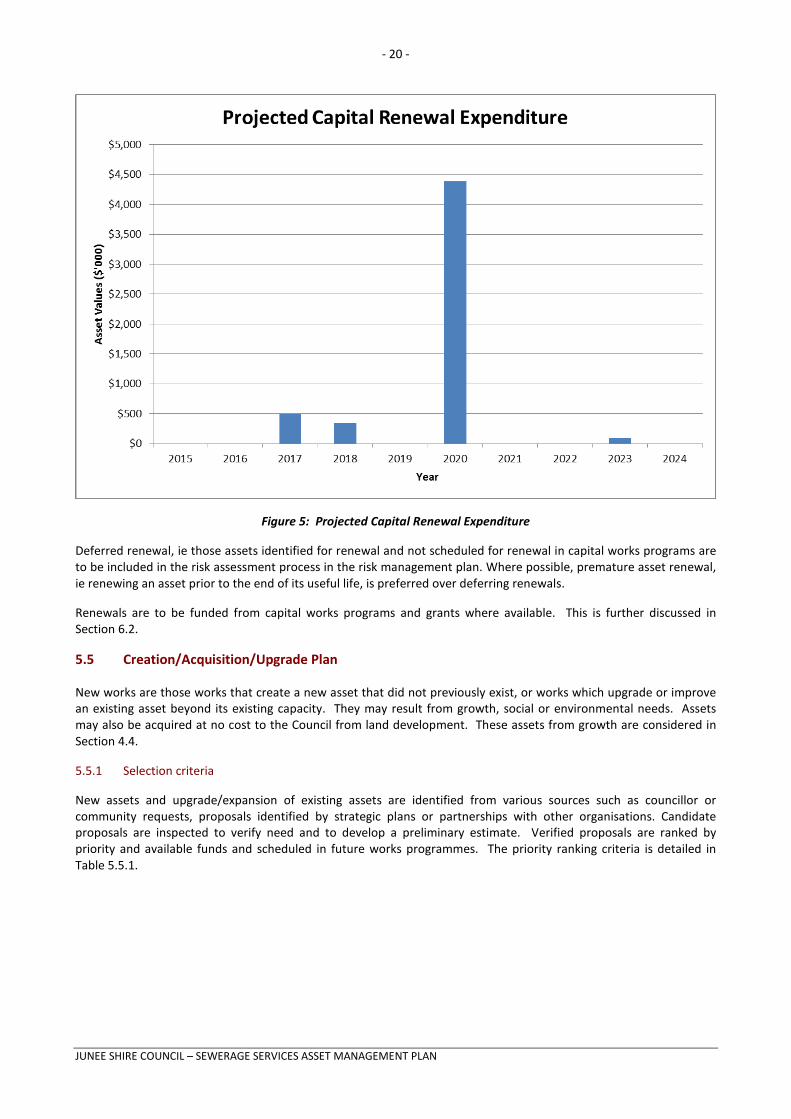

Projected future renewal expenditures are forecast to increase over time as the asset stock ages. The costs are summarised in Figure 5. Note that all costs are shown in 2013 dollar values.

The projected capital renewal program is shown in Appendix B.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 20 -

Figure 5: Projected Capital Renewal Expenditure

Deferred renewal, ie those assets identified for renewal and not scheduled for renewal in capital works programs are to be included in the risk assessment process in the risk management plan. Where possible, premature asset renewal, ie renewing an asset prior to the end of its useful life, is preferred over deferring renewals.

Renewals are to be funded from capital works programs and grants where available. This is further discussed in Section 6.2.

5.5 Creation/Acquisition/Upgrade Plan

New works are those works that create a new asset that did not previously exist, or works which upgrade or improve an existing asset beyond its existing capacity. They may result from growth, social or environmental needs. Assets may also be acquired at no cost to the Council from land development. These assets from growth are considered in Section 4.4.

5.5.1 Selection criteria

New assets and upgrade/expansion of existing assets are identified from various sources such as councillor or community requests, proposals identified by strategic plans or partnerships with other organisations. Candidate proposals are inspected to verify need and to develop a preliminary estimate. Verified proposals are ranked by priority and available funds and scheduled in future works programmes. The priority ranking criteria is detailed in Table 5.5.1.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 21 -

Table 5.5.1: Upgrade/New Assets Priority Ranking Criteria

Criteria Weighting Network benefit 30% User benefit 30% Environmental benefit 20% Economic benefit 20% Total 100% 5.5.2 Standards and specifications

Standards and specifications for new assets and for upgrade/expansion of existing assets are the same as those for renewal shown in Section 5.4.2.

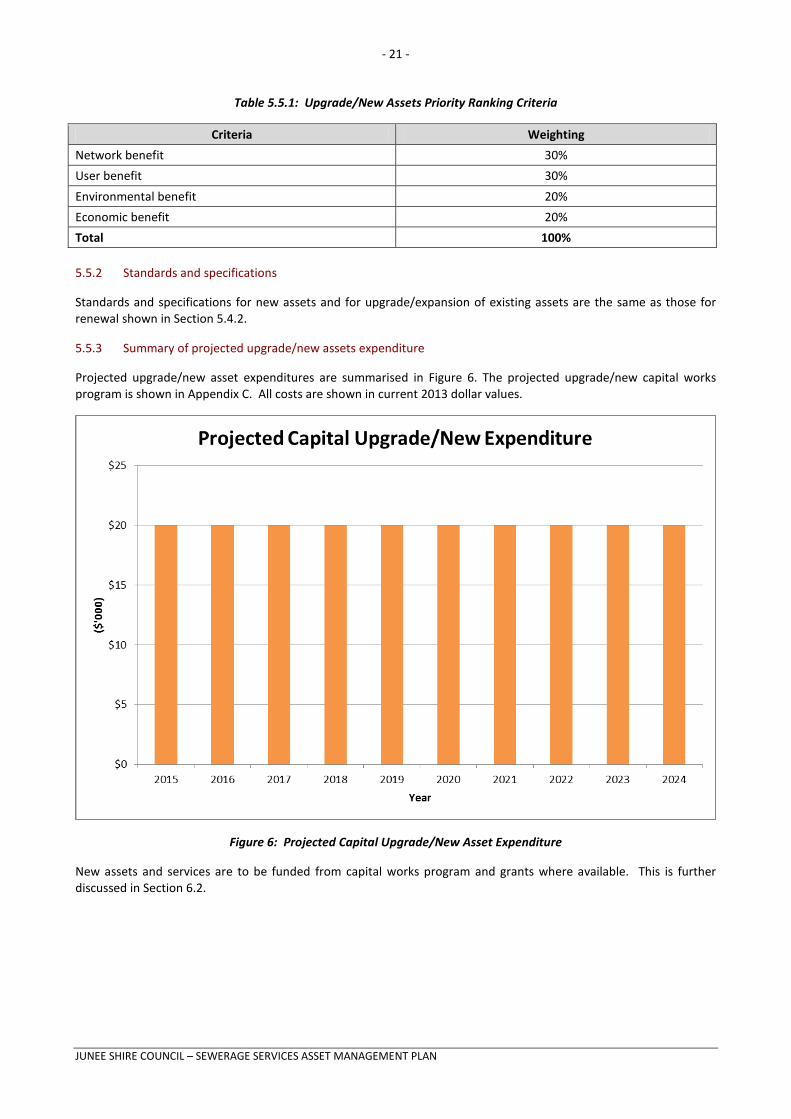

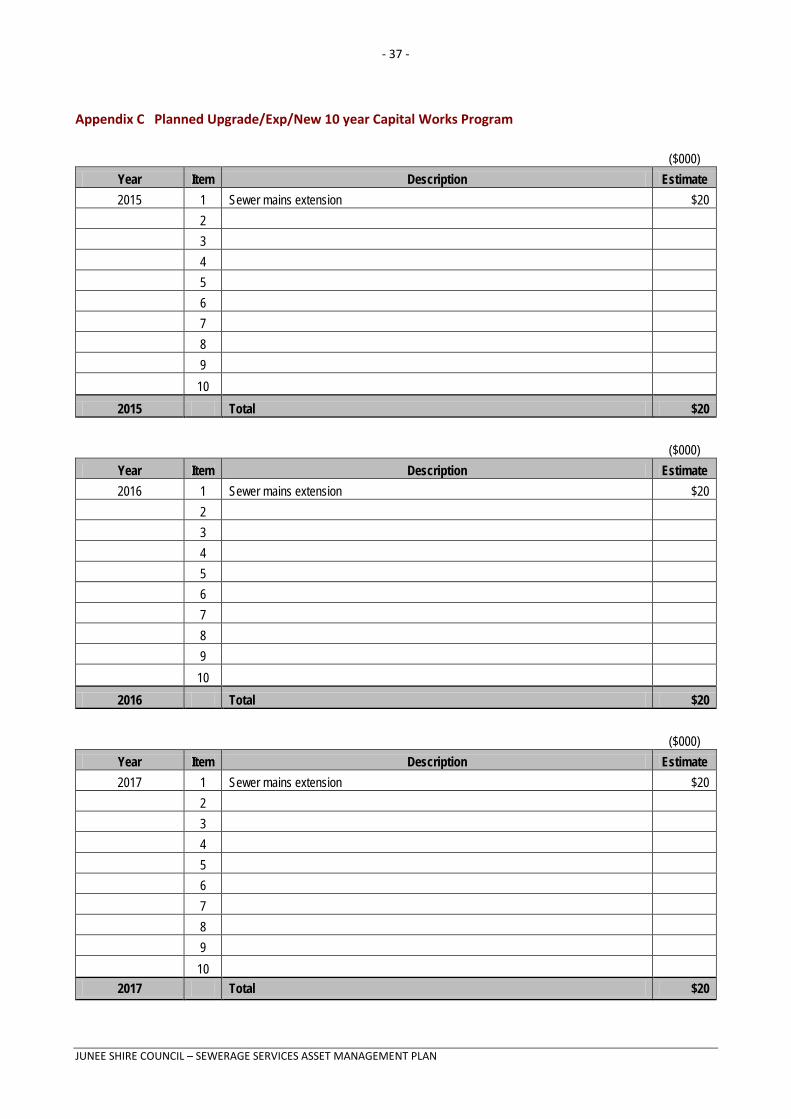

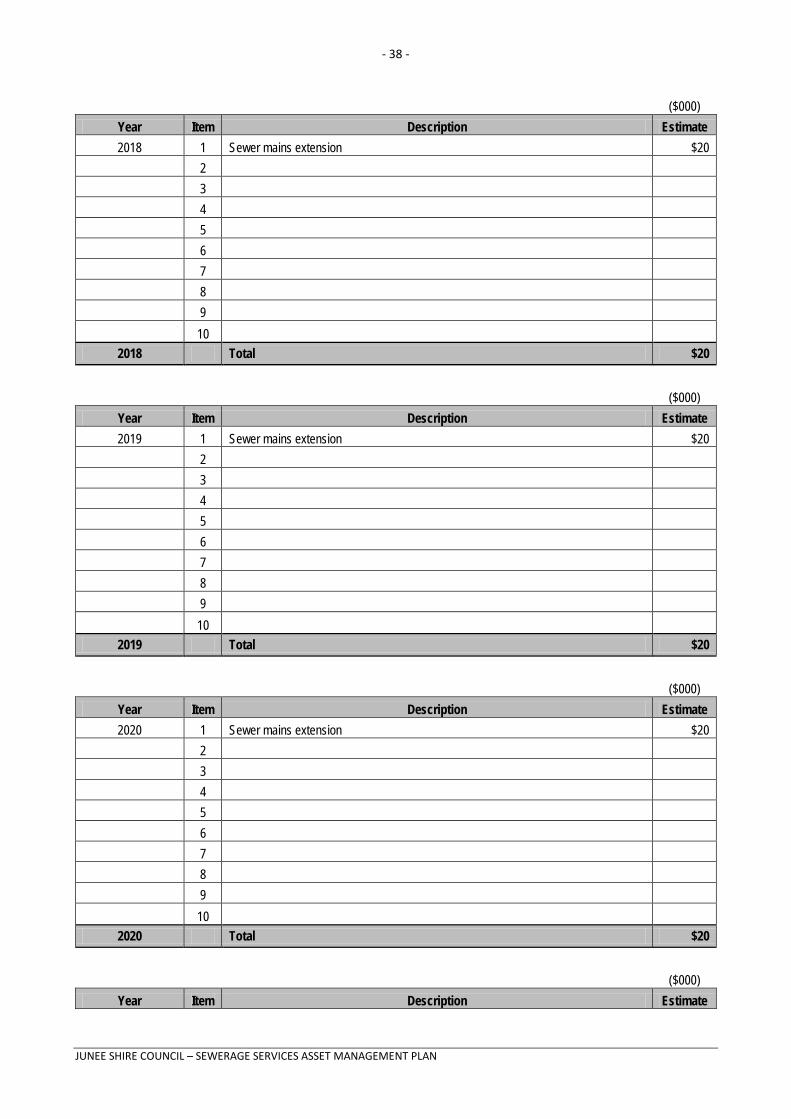

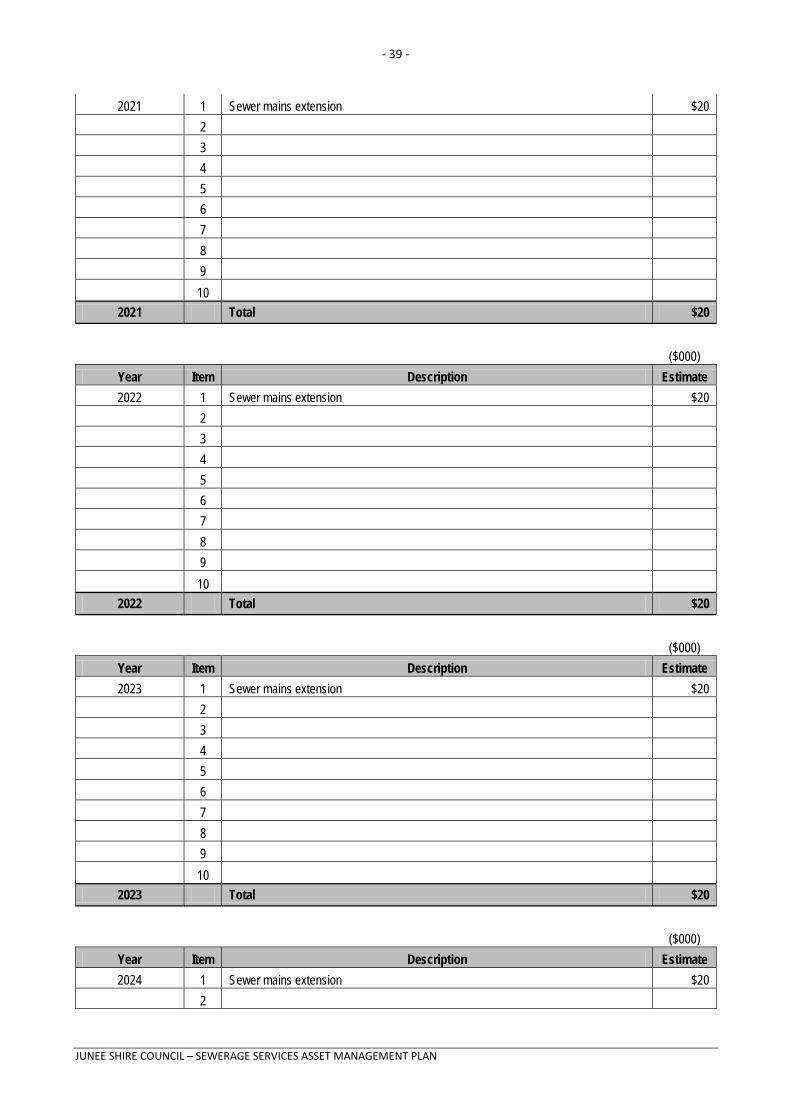

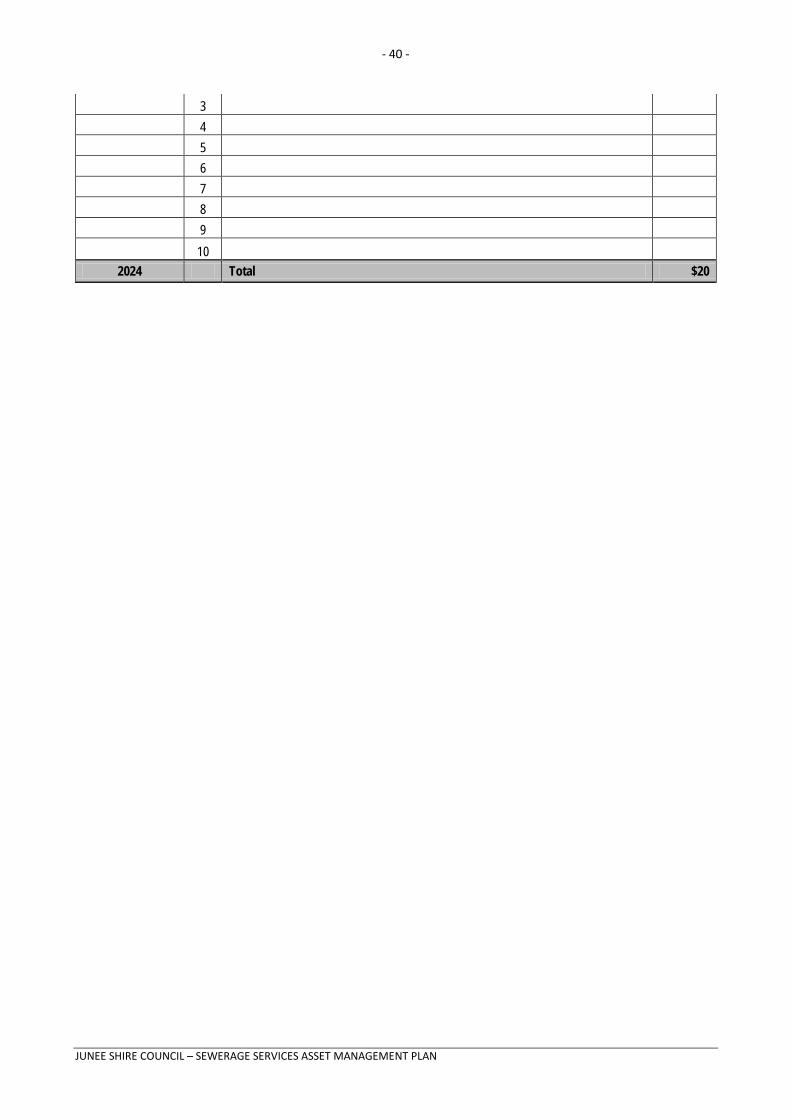

5.5.3 Summary of projected upgrade/new assets expenditure

Projected upgrade/new asset expenditures are summarised in Figure 6. The projected upgrade/new capital works program is shown in Appendix C. All costs are shown in current 2013 dollar values.

Figure 6: Projected Capital Upgrade/New Asset Expenditure

New assets and services are to be funded from capital works program and grants where available. This is further discussed in Section 6.2.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 22 -

5.6 Disposal Plan

Disposal includes any activity associated with disposal of a decommissioned asset including sale, demolition or relocation. Assets identified for possible decommissioning and disposal are shown in Table 5.6, together with estimated annual savings from not having to fund operations and maintenance of the assets. These assets will be further reinvestigated to determine the required levels of service and see what options are available for alternate service delivery, if any.

Where cashflow projections from asset disposals are not available, these will be developed in future revisions of this asset management plan.

Table 5.6: Assets identified for Disposal

Asset Reason for Disposal Timing Net Disposal Expenditure (Expend

+ve, Revenue –ve)

Operations & Maintenance Annual

Savings Nil - - - -

5.7 Service Consequences and Risks

The organisation has prioritised decisions made in adopting this AM Plan to obtain the optimum benefits from its available resources. Decisions were made based on the development of 3 scenarios of AM Plans.

Scenario 1 - What we would like to do based on asset register data

Scenario 2 – What we should do with existing budgets and identifying level of service and risk consequences (i.e. what are the maintenance and capital projects we are unable to do, what is the service and risk consequences associated with this position). This may require several versions of the AM Plan.

Scenario 3 – What we can do and be financially sustainable with AM Plans matching long-term financial plans.

The development of scenario 1 and scenario 2 AM Plans provides the tools for discussion with the Council and community on trade-offs between what we would like to do (scenario 1) and what we should be doing with existing budgets (scenario 2) by balancing changes in services and service levels with affordability and acceptance of the service and risk consequences of the trade-off position (scenario 3).

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 23 -

6. FINANCIAL SUMMARY

This section contains the financial requirements resulting from all the information presented in the previous sections of this asset management plan. The financial projections will be improved as further information becomes available on desired levels of service and current and projected future asset performance.

6.1 Financial Statements and Projections

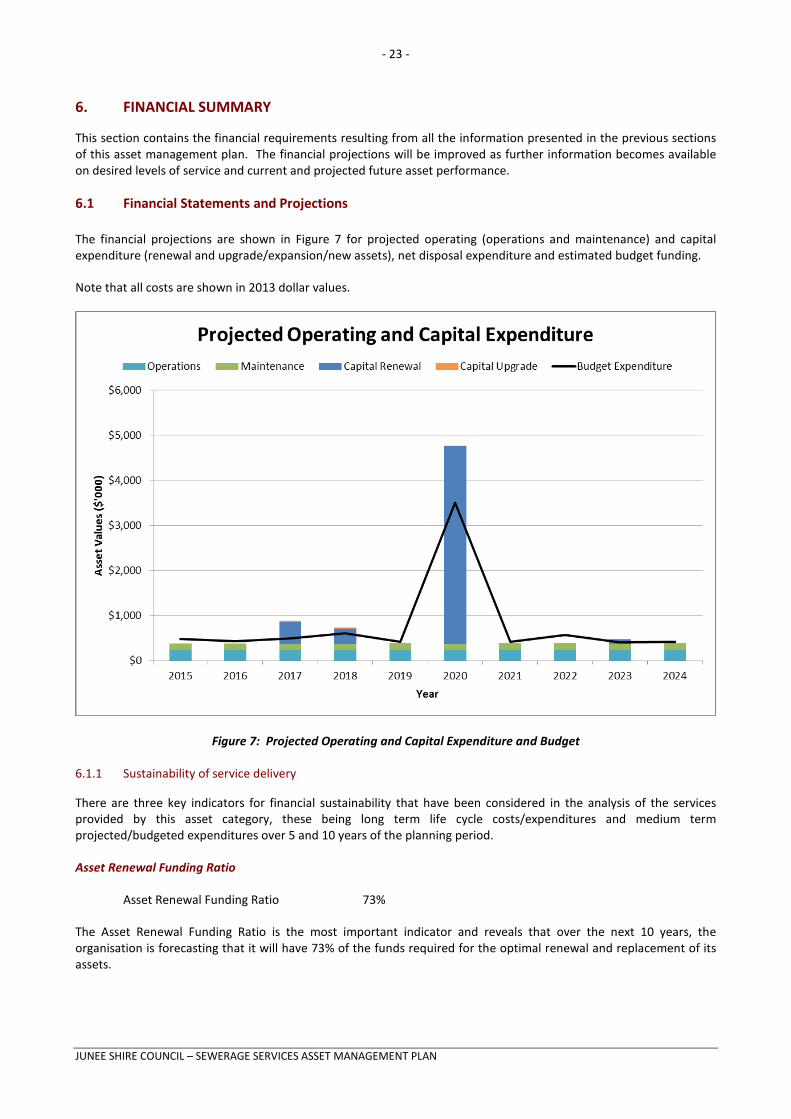

The financial projections are shown in Figure 7 for projected operating (operations and maintenance) and capital expenditure (renewal and upgrade/expansion/new assets), net disposal expenditure and estimated budget funding.

Note that all costs are shown in 2013 dollar values.

Figure 7: Projected Operating and Capital Expenditure and Budget

6.1.1 Sustainability of service delivery

There are three key indicators for financial sustainability that have been considered in the analysis of the services provided by this asset category, these being long term life cycle costs/expenditures and medium term projected/budgeted expenditures over 5 and 10 years of the planning period.

Asset Renewal Funding Ratio

Asset Renewal Funding Ratio 73%

The Asset Renewal Funding Ratio is the most important indicator and reveals that over the next 10 years, the organisation is forecasting that it will have 73% of the funds required for the optimal renewal and replacement of its assets.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 24 -

However, in considering this indicator, it should be noted that it is heavily skewed by the forecast renewal of the wastewater treatment facility in 2020. At the present time, low-cost renewal options are being investigated and until these are better explored, the use of this indicator in assessing the overall sustainability of the service should be guarded.

Long term - Life Cycle Cost

Life cycle costs (or whole of life costs) are the average costs that are required to sustain the service levels over the asset life cycle. Life cycle costs include maintenance expenditure and asset consumption (depreciation expense). The life cycle cost for the services covered in this asset management plan is $590,000 per year (average maintenance expenditure plus depreciation expense projected over 10 years).

Life cycle costs can be compared to life cycle expenditure to give an initial indicator of affordability of projected service levels when considered with age profiles. Life cycle expenditure includes maintenance and capital renewal expenditure. Life cycle expenditure will vary depending on the timing of asset renewals. The life cycle expenditure over the 10 year planning period is $761,000 per year (average maintenance plus capital renewal budgeted expenditure in LTFP over 10 years).

The life cycle gap for services covered by this asset management plan is +$171,000 per year (-ve = gap, +ve = surplus).

Life cycle expenditure is 129% of life cycle costs.

The life cycle costs and life cycle expenditure comparison highlights any difference between present outlays and the average cost of providing the service over the long term. If the life cycle expenditure is less than that life cycle cost, it is most likely that outlays will need to be increased or cuts in services made in the future.

Knowing the extent and timing of any required increase in outlays and the service consequences if funding is not available will assist organisations in providing services to their communities in a financially sustainable manner. This is the purpose of the asset management plans and long term financial plan.

Medium term – 10 year financial planning period

This asset management plan identifies the projected operations, maintenance and capital renewal expenditures required to provide an agreed level of service to the community over a 10 year period. This provides input into 10 year financial and funding plans aimed at providing the required services in a sustainable manner.

These projected expenditures may be compared to budgeted expenditures in the 10 year period to identify any funding shortfall. In a core asset management plan, a gap is generally due to increasing asset renewals for ageing assets.

The projected operations, maintenance and capital renewal expenditure required over the 10 year planning period is $903,000 per year.

Estimated (budget) operations, maintenance and capital renewal funding is $763,000 per year giving a 10 year funding shortfall of $142,000 per year and a 10 year sustainability indicator of 0.84. This indicates that Council has 84% of the projected expenditures needed to provide the services documented in the asset management plan.

Medium Term – 5 year financial planning period

The projected operations, maintenance and capital renewal expenditure required over the first 5 years of the planning period is $538,000 per year.

Estimated (budget) operations, maintenance and capital renewal funding is $471,000 per year giving a 5 year funding shortfall of $66,000. This is 88% of projected expenditures giving a 5 year sustainability indicator of 0.88.

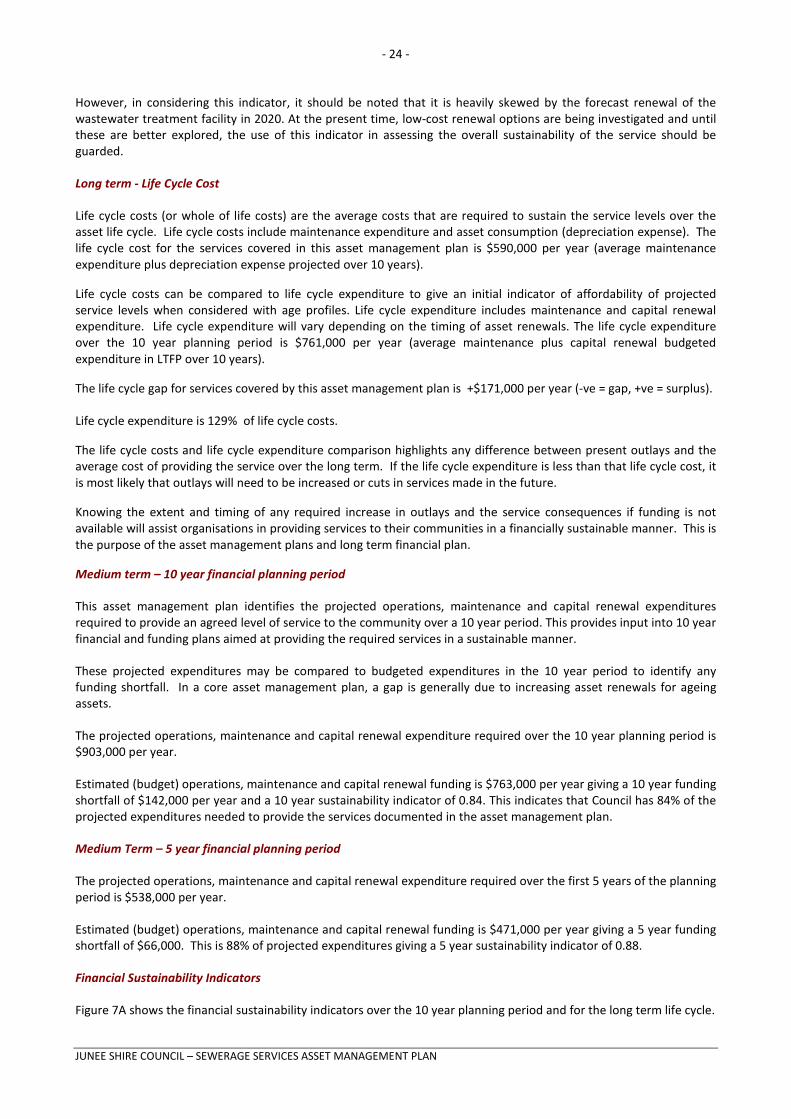

Financial Sustainability Indicators

Figure 7A shows the financial sustainability indicators over the 10 year planning period and for the long term life cycle.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 25 -

Figure 7A: Financial Sustainability Indicators

Providing services from infrastructure in a sustainable manner requires the matching and managing of service levels, risks, projected expenditures and funding to achieve a financial sustainability indicator of 1.0 for the first years of the asset management plan and ideally over the 10 year life of the AM Plan.

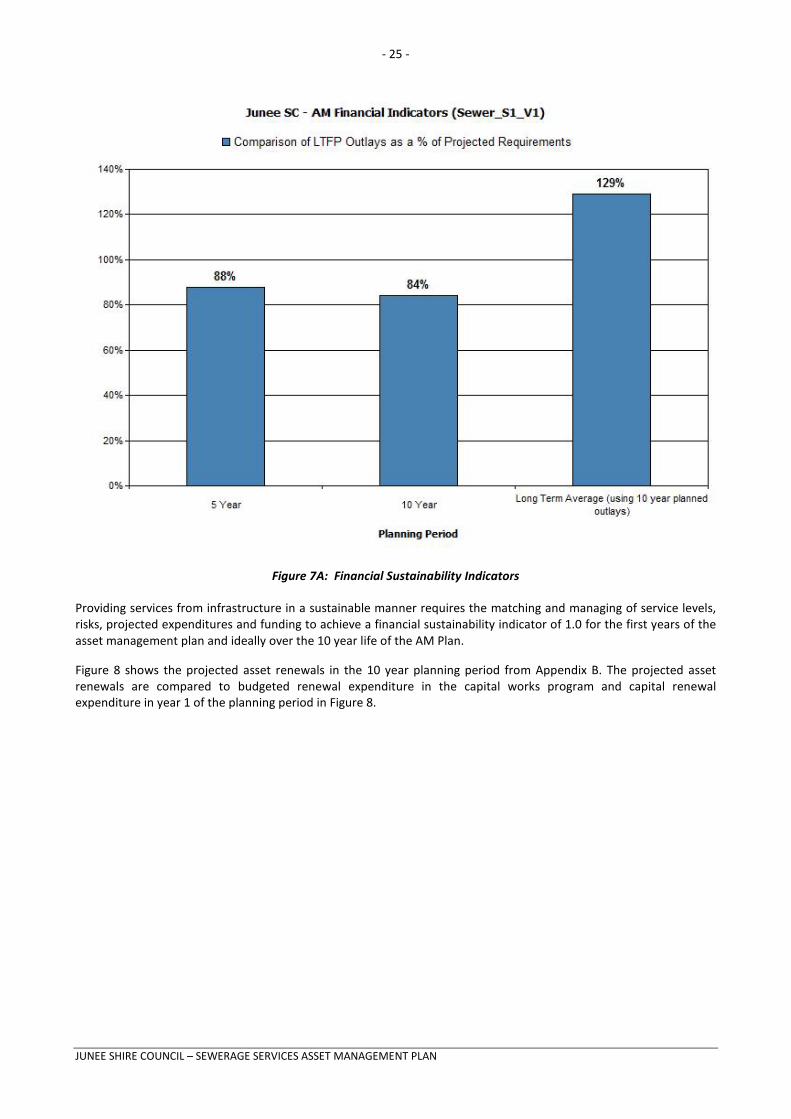

Figure 8 shows the projected asset renewals in the 10 year planning period from Appendix B. The projected asset renewals are compared to budgeted renewal expenditure in the capital works program and capital renewal expenditure in year 1 of the planning period in Figure 8.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 26 -

Figure 8: Projected and Budgeted Renewal Expenditure

Table 6.1.1 shows the shortfall between projected and budgeted renewals

Table 6.1.1: Projected and Budgeted Renewals and Expenditure Shortfall

Year

Projected Renewals ($'000)

Planned Renewal Budget ($'000)

Renewal Funding Shortfall ($'000)

(- ve Gap, +ve Surplus)

Cumulative Difference ($'000)

(- ve Gap, +ve Surplus)

2015 $0 $97 $97 $97 2016 $0 $47 $47 $144 2017 $494 $114 -$380 -$236 2018 $346 $220 -$126 -$362 2019 $0 $34 $34 -$327 2020 $4,386 $3,117 -$1,269 -$1,597 2021 $0 $32 $32 -$1,564 2022 $0 $194 $194 -$1,370 2023 $95 $30 -$64 -$1,435 2024 $0 $36 $36 -$1,398

Note: A negative shortfall indicates a funding gap, a positive shortfall indicates a surplus for that year.

Providing services in a sustainable manner will require matching of projected asset renewals to meet agreed service levels with planned capital works programs and available revenue.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 27 -

A gap between projected asset renewals, planned asset renewals and funding indicates that further work is required to manage required service levels and funding to eliminate any funding gap. As it stands there is a gap due to the projected renewal of the wastewater treatment facility. This gap shall be addressed in future revisions of this asset management plan as low – cost renewal and different funding options are explored.

6.1.2 Expenditure projections for long term financial plan

Table 6.1.2 shows the projected expenditures for the 10 year long term financial plan.

Expenditure projections are in current (non-inflated) values. Disposals are shown as net expenditures (revenues are negative).

Table 6.1.2: Expenditure Projections for Long Term Financial Plan ($000)

Year Operations ($'000)

Maintenance ($'000)

Projected Capital Renewal ($'000)

Capital Upgrade/ New ($'000)

Net Disposals ($'000)

2015 $243.00 $125.90 $0.00 $20.00 $0.00

2016 $243.24 $126.07 $0.00 $20.00 $0.00 2017 $243.49 $126.24 $493.65 $20.00 $0.00 2018 $243.73 $126.41 $345.94 $20.00 $0.00 2019 $243.97 $126.58 $0.00 $20.00 $0.00 2020 $244.21 $126.75 $4,385.98 $20.00 $0.00 2021 $244.45 $126.92 $0.00 $20.00 $0.00 2022 $244.70 $127.09 $0.00 $20.00 $0.00 2023 $244.94 $127.27 $94.61 $20.00 $0.00 2024 $245.18 $127.44 $0.00 $20.00 $0.00

Note: All projected expenditures are in 2013 values

6.2 Funding Strategy

Projected expenditure identified in Section 6.1 is to be funded from future operating and capital budgets. It is Council’s intention to match expenditure in the Long Term Financial Plan to the funding identified in the Asset Management Plan. After reviewing service levels or increasing funding, as appropriate to ensure ongoing financial sustainability projected expenditures identified in Section 6.1.2 will be accommodated in the organisation’s 10 year long term financial plan.

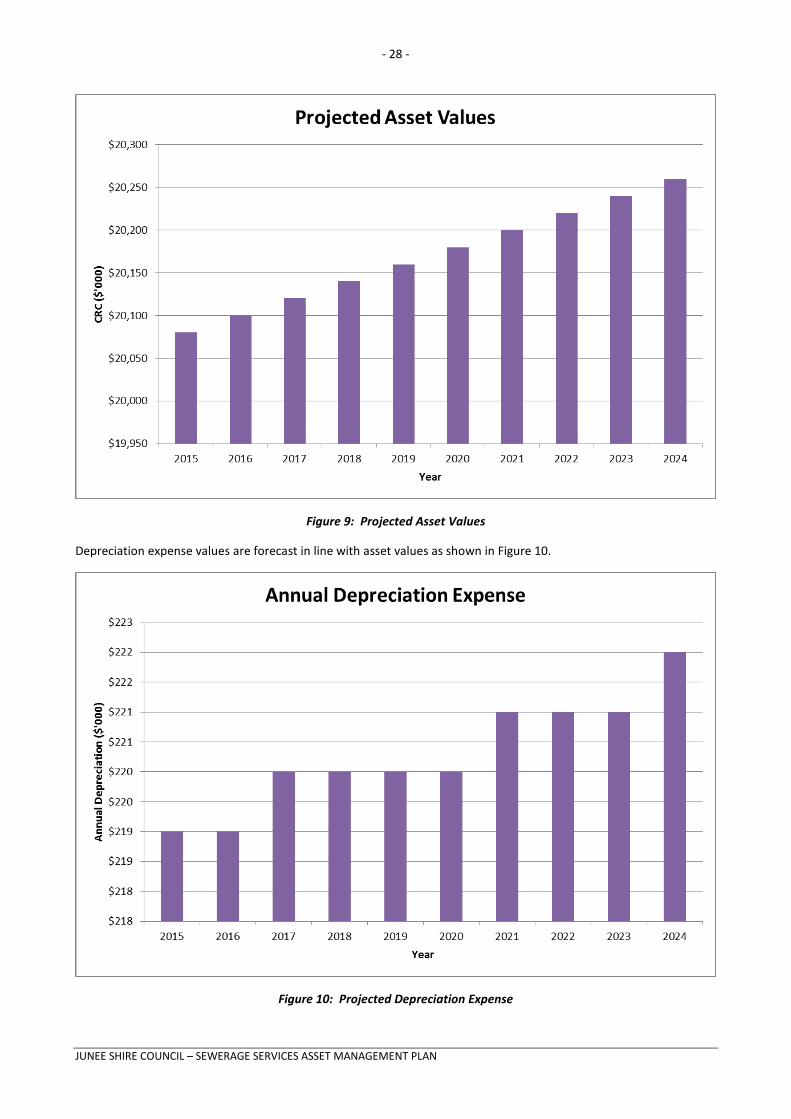

6.3 Valuation Forecasts

Asset values are forecast to increase as additional assets are added to the asset stock from construction and acquisition by Council and from assets constructed by land developers and others and donated to Council. Figure 9 shows the projected replacement cost asset values over the planning period in 2013 dollar values.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 28 -

Figure 9: Projected Asset Values

Depreciation expense values are forecast in line with asset values as shown in Figure 10.

Figure 10: Projected Depreciation Expense

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 29 -

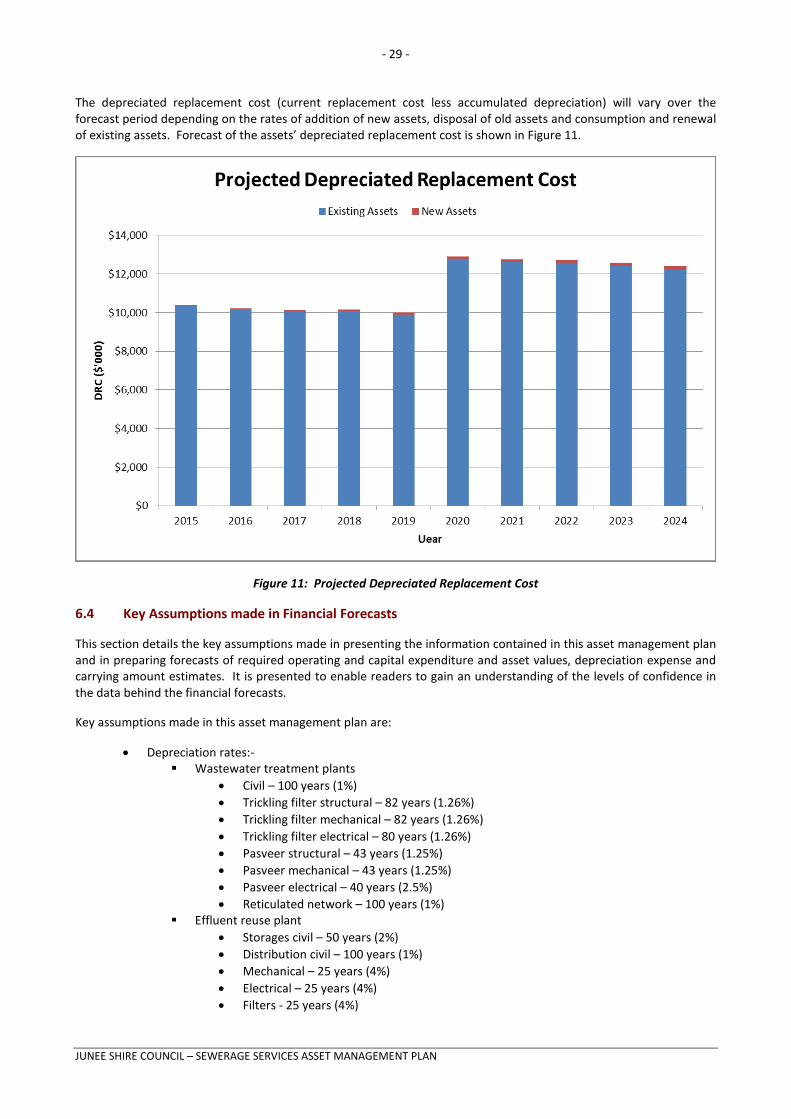

The depreciated replacement cost (current replacement cost less accumulated depreciation) will vary over the forecast period depending on the rates of addition of new assets, disposal of old assets and consumption and renewal of existing assets. Forecast of the assets’ depreciated replacement cost is shown in Figure 11.

Figure 11: Projected Depreciated Replacement Cost

6.4 Key Assumptions made in Financial Forecasts

This section details the key assumptions made in presenting the information contained in this asset management plan and in preparing forecasts of required operating and capital expenditure and asset values, depreciation expense and carrying amount estimates. It is presented to enable readers to gain an understanding of the levels of confidence in the data behind the financial forecasts.

Key assumptions made in this asset management plan are:

• Depreciation rates:- Wastewater treatment plants

• Civil – 100 years (1%) • Trickling filter structural – 82 years (1.26%) • Trickling filter mechanical – 82 years (1.26%) • Trickling filter electrical – 80 years (1.26%) • Pasveer structural – 43 years (1.25%) • Pasveer mechanical – 43 years (1.25%) • Pasveer electrical – 40 years (2.5%) • Reticulated network – 100 years (1%)

Effluent reuse plant • Storages civil – 50 years (2%) • Distribution civil – 100 years (1%) • Mechanical – 25 years (4%) • Electrical – 25 years (4%) • Filters - 25 years (4%)

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 30 -

• Chlorination system – 70 years (2%) • Reticulation – 100 years (1.43%)

It has been necessary to discount budgeted expenditure figures so that the asset management plan can be presented in current dollars. In doing this, figures from the LTFP have been discounted at a rate of 3.2%. 6.5 Forecast Reliability and Confidence

The expenditure and valuations projections in this AM Plan are based on best available data. Currency and accuracy of data is critical to effective asset and financial management. Data confidence is classified on a 5 level scale in accordance with Table 6.5.

Table 6.5: Data Confidence Grading System

Confidence Grade Description A Highly reliable Data based on sound records, procedures, investigations and analysis, documented properly and recognised

as the best method of assessment. Dataset is complete and estimated to be accurate ± 2% B Reliable Data based on sound records, procedures, investigations and analysis, documented properly but has minor

shortcomings, for example some of the data is old, some documentation is missing and/or reliance is placed on unconfirmed reports or some extrapolation. Dataset is complete and estimated to be accurate ± 10%

C Uncertain Data based on sound records, procedures, investigations and analysis which is incomplete or unsupported, or extrapolated from a limited sample for which grade A or B data are available. Dataset is substantially complete but up to 50% is extrapolated data and accuracy estimated ± 25%

D Very Uncertain Data is based on unconfirmed verbal reports and/or cursory inspections and analysis. Dataset may not be fully complete and most data is estimated or extrapolated. Accuracy ± 40%

E Unknown None or very little data held. The estimated confidence level for and reliability of data used in this AM Plan is shown in Table 6.5.1.

Table 6.5.1: Data Confidence Assessment for Data used in AM Plan

Data Confidence Assessment Comment Demand drivers Reliable We have a long, continuous record of the majority of demand

drivers. Forecasts are made on the underlying trends from these records.

Growth projections Reliable Growth of the urban area serviced by the sewerage network is controlled by land zoning. There is a long, continuous record of growth that has remained relatively stable over time.

Operations expenditures Highly reliable Data extracted from Councils accounting system. Maintenance expenditures Highly reliable Data extracted from Councils accounting system. Projected Renewal exps. - Asset values

Reliable Information based on Councils asset register and sound engineering knowledge and history of the sewerage network.

- Asset residual values Reliable Determined from experience with renewal of existing assets. - Asset useful lives Uncertain Many of the sewerage assets are in the last 30% of their

predicted useful lives and few show signs of deteriorating prematurely.

- Condition modelling Uncertain Condition modelling in the past has been completed using only a very small, statistically insignificant sample size. However we have a good record of condition indicators such as blockages.

- Network renewals Reliable Based on assumed useful lives - Defect repairs Highly reliable Projected data based on accurately recorded historical data Upgrade/New expenditures Highly reliable Based on recent expenditure of similar projects Disposal expenditures N/A N/A Over all data sources, the data confidence is assessed as Medium confidence level for data used in the preparation of this AM Plan.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 31 -

7. PLAN IMPROVEMENT AND MONITORING

7.1 Status of Asset Management Practices

7.1.1 Accounting and financial systems

Junee Shire Council utilises Civica’s Authority software package for accounting and reporting services. This software package has the option of an Asset Management module, however Council at present only uses the General Ledger Module.

7.1.2 Accountabilities for financial systems

Financial Services operates within the Corporate Services Department of Council. The Financial Services section is responsible for overseeing Council’s finances and ensuring compliance with the relevant statutory requirements.

7.1.3 Accounting standards and regulations

Council’s financial reporting must comply with Australian equivalents to International Financial Reporting Standards, other authoritative pronouncements of the Australian Accounting Standards Board, Urgent Issues Group Interpretations, the Local Government Act (1993) and Regulations and the Local Government Code of Accounting Practice and Financial Reporting.

7.1.4 Capital/maintenance threshold

Council has not formally adopted a policy to dictate matters relating to capital/maintenance thresholds. The decision to capitalise works/assets is made by the relevant Director on a merits based approach. Assets of a lasting nature (greater than one year) and with a purchase cost of greater than $1000 are generally capitalised.

7.1.5 Required changes to accounting financial systems arising from this AM Plan

No changes have been identified as a result of completing this AM Plan.

7.2 Asset Management Systems

7.2.1 Asset management system

Junee Shire Council utilises Microsoft’s Excel software program for the recording and reporting of its assets. This is supported by, though not directly linked to, Intramaps – Council’s GIS software package.

7.2.2 Asset registers

Asset registers are maintained in Excel. A single sheet serves as the register and the financial record for each asset category. This is updated annually by Financial Services.

7.2.3 Linkage from asset management to financial system

Presently there is no formal link between Council’s financial system and the asset management system. The formalisation of such a link is required.

7.2.4 Accountabilities for asset management system and data

At present Financial Services is responsible for maintaining the asset management system with input from Engineering and Spatial staff.

7.2.5 Required changes to asset management system arising from this AM Plan

At present the management of the asset register is informal. The process for managing the system needs to be formalised with accountabilities, responsibilities and procedures formalised.

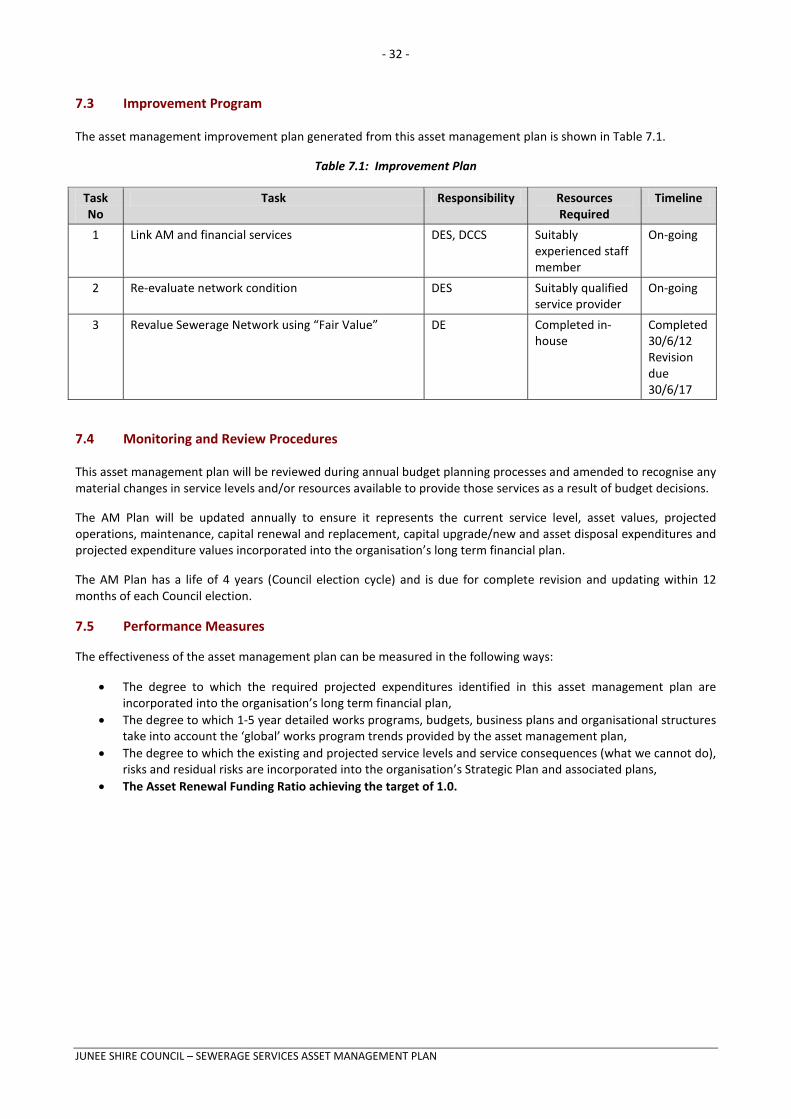

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 32 -

7.3 Improvement Program

The asset management improvement plan generated from this asset management plan is shown in Table 7.1.

Table 7.1: Improvement Plan

Task No

Task Responsibility Resources Required

Timeline

1 Link AM and financial services DES, DCCS Suitably experienced staff member

On-going

2 Re-evaluate network condition DES Suitably qualified service provider

On-going

3 Revalue Sewerage Network using “Fair Value” DE Completed in-house

Completed 30/6/12 Revision due 30/6/17

7.4 Monitoring and Review Procedures

This asset management plan will be reviewed during annual budget planning processes and amended to recognise any material changes in service levels and/or resources available to provide those services as a result of budget decisions.

The AM Plan will be updated annually to ensure it represents the current service level, asset values, projected operations, maintenance, capital renewal and replacement, capital upgrade/new and asset disposal expenditures and projected expenditure values incorporated into the organisation’s long term financial plan.

The AM Plan has a life of 4 years (Council election cycle) and is due for complete revision and updating within 12 months of each Council election.

7.5 Performance Measures

The effectiveness of the asset management plan can be measured in the following ways:

• The degree to which the required projected expenditures identified in this asset management plan are incorporated into the organisation’s long term financial plan,

• The degree to which 1-5 year detailed works programs, budgets, business plans and organisational structures take into account the ‘global’ works program trends provided by the asset management plan,

• The degree to which the existing and projected service levels and service consequences (what we cannot do), risks and residual risks are incorporated into the organisation’s Strategic Plan and associated plans,

• The Asset Renewal Funding Ratio achieving the target of 1.0.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 33 -

REFERENCES

Junee Shire Council, Strategic Business Plan Sewerage – DRAFT, 2012-2031, Junee Shire Council

Junee Shire Council, Management Plan 2011-2015, Junee Shire Council

DVC, 2006, Asset Investment Guidelines, Glossary, Department for Victorian Communities, Local Government Victoria, Melbourne, http://www.dpcd.vic.gov.au/localgovernment/publications-and-research/asset-management-and-financial.

IPWEA, 2006, International Infrastructure Management Manual, Institute of Public Works Engineering Australia, Sydney, www.ipwea.org.au.

IPWEA, 2008, NAMS.PLUS Asset Management Institute of Public Works Engineering Australia, Sydney, www.ipwea.org.au/namsplus

IPWEA, 2009, Australian Infrastructure Financial Management Guidelines, Institute of Public Works Engineering Australia, Sydney, www.ipwea.org.au/AIFMG.

IPWEA, 2011, Asset Management for Small, Rural or Remote Communities Practice Note, Institute of Public Works Engineering Australia, Sydney, www.ipwea.org.au/AM4SRRC.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 34 -

APPENDICES

Appendix A Maintenance Response Levels of Service

Appendix B Projected 10 year Capital Renewal Works Program

Appendix C Planned Upgrade/Exp/New 10 year Capital Works Program

Appendix D Abbreviations

Appendix E Glossary

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 35 -

Appendix A Maintenance Response Levels of Service

To be developed.

JUNEE SHIRE COUNCIL – SEWERAGE SERVICES ASSET MANAGEMENT PLAN

- 36 -

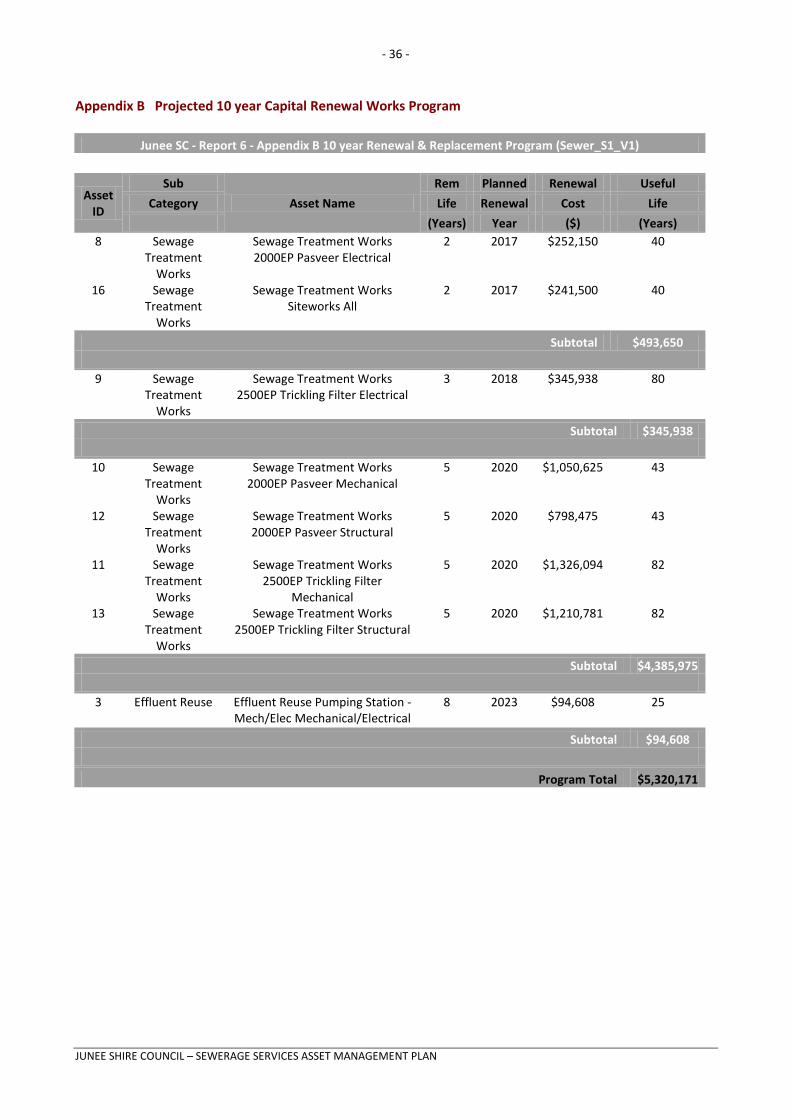

Appendix B Projected 10 year Capital Renewal Works Program

Junee SC - Report 6 - Appendix B 10 year Renewal & Replacement Program (Sewer_S1_V1)

Asset ID

Sub Asset Name

Rem Planned Renewal Useful Category Life Renewal Cost Life

(Years) Year ($) (Years) 8 Sewage

Treatment Works

Sewage Treatment Works 2000EP Pasveer Electrical

2 2017 $252,150 40

16 Sewage Treatment

Works

Sewage Treatment Works Siteworks All

2 2017 $241,500 40

Subtotal $493,650

9 Sewage Treatment

Works

Sewage Treatment Works 2500EP Trickling Filter Electrical

3 2018 $345,938 80

Subtotal $345,938

10 Sewage Treatment

Works

Sewage Treatment Works 2000EP Pasveer Mechanical

5 2020 $1,050,625 43

12 Sewage Treatment

Works

Sewage Treatment Works 2000EP Pasveer Structural

5 2020 $798,475 43

11 Sewage Treatment

Works