AppendiX 145 - Springer978-3-663-10736-1/1.pdf · Kraft Foods lnc .' 26 ,797 34,679 294 , ConAgra...

44

AppendiX 145 Appendix Appendix I Leading U.S. food and beverage companies TOP 25 U.S. FOOO & BEVERAGE' COMPANIES- 2000 (ln millians of dollt"s} PACKAOEO FOOO & BEVERAGE SALES COMPANV 1999 zooo %C HANOE 1. Kraft Foods lnc .' 26 ,797 34,679 29.4 2, ConAgra Foods lnc .' 24,594 25,386 3.2 3. PepsiCo lnc .' 18,666 20,144 7 .9 4. Cargill lnc.* 21,400 22,200 3 .7 5. The Coca - Cola Co. 19,805 20,458 3 .3 6. Mars lnc .* 15,000 15,600 4 .0 7. IBP lnc. 15,122 16,950 12.1 8. H.J. Heinz Co. ' 9,300 9,408 1.2 9. Nestle U.S .A. lnc . 7,986 8,226 3.0 10. Sara Lee Corp .• 7,876 7,915 0 .5 11. Tyson Foods lnc .• 7,363 7,158 (2.8) 12. Kallogg Co. 6,984 6,954 (0 . 4) 13. Oairy Farmers of America• 7,435 6,700 (9. 9) 14. General Mills lnc .' 6,246 6,700 7 .3 15. Campbell Soup Co.• 6,424 6,267 (2 .4) 16. The Plllsbury Co. 3 6,161 6,099 (1.0) 17. Suiza Foods Corp . 4,482 5,756 28.4 18. Smithtield Foods lnc .• 3,775 5,150 36.4 19. The Ouaker Oats Co. 4,725 5,041 6 .7 20. Ftowers lndustries lnc. 4,236 4,937 16.5 21 . Dole Food Co. lnc . 5,061 4,76=i (5.9) 22. Procter & Gambia Co .• 4,655 4,634 (0.5) 23 . Hershey Foods Co . 3,971 4,221 6 .3 24 . Oeen Foods Co.' 3,755 4,066 8 .3 25 . Hormel Foods Cbrp . 3,358' 3,675 9.4 "Prlvately owned. ' Fiacal vear' ended May. 'Pro forme , reflects spinoft of Peps! Bor· tl ing Group end Ulttltory 'Fis cel year ended June. 'fl•c al year ended Sep· tembar. 'Fi scel · vear Ju y, 'Fiacal yelir ended April . ' Pf o forme. l' eflacr. ec:quis l· tlon of Neblsc o Foods. Source: Compeny repo11s; Standard & Poot's estimateil. Source Standard & Poor' s 200 I a. 7

Transcript of AppendiX 145 - Springer978-3-663-10736-1/1.pdf · Kraft Foods lnc .' 26 ,797 34,679 294 , ConAgra...

AppendiX 145

Appendix

Appendix I Leading U.S. food and beverage companies

TOP 25 U.S. FOOO & BEVERAGE' COMPANIES- 2000 (ln millians of dollt"s}

PACKAOEO FOOO & BEVERAGE SALES COMPANV 1999 zooo %CHANOE

1. Kraft Foods lnc .' 26,797 34,679 29.4 2 , ConAgra Foods lnc .' 24,594 25,386 3 .2 3. PepsiCo lnc .' 18,666 20,144 7 .9 4. Cargill lnc.* 21,400 22,200 3 .7 5. The Coca-Cola Co. 19,805 20,458 3 .3 6 . Mars lnc.* 15,000 15,600 4 .0 7. IBP lnc. 15,122 16,950 12.1 8. H.J. Heinz Co. ' 9,300 9,408 1.2 9. Nestle U.S.A . lnc . 7,986 8,226 3.0

10. Sara Lee Corp.• 7,876 7,915 0 .5 11. Tyson Foods lnc .• 7,363 7,158 (2.8) 12. Kallogg Co. 6,984 6,954 (0.4)

13. Oairy Farmers of America• 7,435 6,700 (9.9)

14. General Mills lnc.' 6,246 6,700 7 .3 15. Campbell Soup Co.• 6,424 6,267 (2.4)

16. The Plllsbury Co.3 6,161 6,099 (1.0)

17. Suiza Foods Corp. 4,482 5,756 28.4 18. Smithtield Foods lnc.• 3,775 5,150 36.4 19. The Ouaker Oats Co. 4,725 5,041 6 .7 20. Ftowers lndustries lnc. 4,236 4,937 16.5 21 . Dole Food Co. lnc. 5,061 4,76=i (5.9)

22. Procter & Gambia Co.• 4,655 4,634 (0.5)

23. Hershey Foods Co. 3,971 4,221 6 .3 24. Oeen Foods Co.' 3,755 4,066 8 .3 25. Hormel Foods Cbrp. 3,358' 3,675 9.4

"Prlvately owned. 'Fiacal vear' ended May. 'Pro forme, reflects spinoft of Peps! Bor· tling Group end Ulttltory reell~nmilnt. 'Fiscel year ended June. 'fl•cal year ended Sep· tembar. 'Fiscel ·vear t~nded Ju y, 'Fiacal yelir ended April . ' Pf o forme. l'eflacr. ec:quis l· tlon of Neblsco Foods. Source: Compeny repo11s; Standard & Poot's estimateil.

Source Standard & Poor' s 200 I a. 7

146

Appendix 2.1: Private Iabel volume growth over 52 weeks by category

Fr.••.,_rtc:". ! OryOiaMI'J !

T'llaa -CMDCd !

Popc:oB - ~poppccS i Llll •dt~ · Siio:c4 i

Cai1Up ! Ck~UI · Re..dy4Qe&1 !

· ·h•tlrlD~ !

Oedrn 1

Toutcthluiu i 8t.~1Milu ! - ·""'•!

~«:Oum i PkUu i

Yc,JCIIblu • ().n ll:d i Dott'ood · Doy i

t'nlil · C.Il.cd i YoJ•II i

"'* : I ~llll»t~ :

I A~ ;

I Pol•~-tw- :

I Cookiu :

Sp.Jbc:tti S..cc ~ CMI'ood · Doy! ....

Pl.u• · Dry

Ooatfood - Wc•

CM4y . Qoco~Mc

C..l foo4 · WC4

S!Mip-Caued

s.-. .. ,c SaW ••tl C:O."Ü'IJ (W

~-~· ~· --------~------~--------·" .,. ., 10 ,,

Source: ACNielsen Syndicated Marke! Research Information for Food, Drug, & Mass Channels, and JPMS.

Source: J.P. Morgan 1999a, 53; dataasofNovember 19, 1999.

Appendix

Appendix 147

Appendix 2.2: Split ofU.S. food spending for at home and awayfrom home consumption

Absolute Athome Awayfrom Year expenditure home

ibm. of$) (%) (%)

1999 754.3 54.5 45.5 1998 749.6 52.7 47.3 1997 723.8 53.2 46.8 1996 690.6 53.6 46.4 1995 664.1 53.8 46.2 1994 639.3 53.9 46.1 1993 610.1 54.0 46.0 1992 589.5 55.0 45.0 1991 578.9 55.7 44.3 1990 557.7 55.4 44.6 1980 299.9 59.9 40.1 1970 114.4 65.4 34.6 1960 69.9 72.0 28.0 1950 46.2 73.0 27.0

Source: adapted from Standard & Poor's 2000b, 10; numbers originally from Bureau ofEconomic Analysis.

Appendix 3 .I: Excerpts of exemplary M&A press releases

Note: Key terms are highlighted.

Unilever and Bestfonds Sign Definitive Merger Agreement for Acquisition of Bestfoods At $73 Per Share; Creates Pre--eminent Global Food and Consumer Goods Company (Business Wire, 06/06/2000)

FitzGerald and Burgmans, Chairmen of Unilever, said, "We are very excited about the combination of Unilever and Bestfoods. This transaction creates the pre-eminent global food and consumer goods company. Together we will have a portfolio of powerful worldwide and regional brands, with strong growth prospects.

"This transaction will aceeierate Unilever towards the achievement of our Path-to-Growth objectives- it makes a good plan better. The complementary nature of our geographic coverage and our combined product portfolio together with Bestfoods' strong foodserviee operations, will enable us to further raise our growth ambition," continued the Chairmen.

The complementary natore of Unilevers and Bestfoods' portfolios and geographies uniquely positions the combined companyforthe aceeleration oftop line growth.

Philip Morris Acquires Nabisco for $55.00 Per Share in Cash and Plans for IPO of Kraft (Business Wire, 06/25/2000)

Geoffrey C. Bible, chairman and chief executive ofl:icer, Philip Morris Companies Inc. said, "The acquisition of Nabisco ( ... ) is truly compelling from a strategic, financial and shareholder value perspective."

With this traosaction Kraft will: become the world's most profitable food company; aceeierate its revenue and earuings growth rates by materially strengtherring its presence in the fast growing and dyoamic snack foods category; become the world Ieader in cookies and crackers with a 13% share, and the Ieader in the U.S. cookie and cracker categories, with shares of35% and 47%, respectively, eohanee its scale and add a successful direct store delivery system to its infrastrocture to more effectively meet the needs ofits global trade partoers; increase its brand leadership by adding 18 brands to its existiog 55 brands that each generate more than $100 million in revenue; over 90% of Nabisco's U.S. portfolio of brands are nurober one in the categories in which Nabisco operates

148 Appendix

- double its scale in Latin America and strengthen its presence in Asia and in Europe. In addition, Kraft projects significant revenue synergies resulting from tbe combination of tbe two brand

portfolios. "This acquisition will add such hausehold names as Oreo and Chips Ahoy! cookies, Ritz crackers, Planters nuts and Life Savers candy, to name a few, to our stellar portfolio ofbrands.", Mr. Bible said. "The acquisition of Nabisco will generate attractive returns and will increase our eamings growth rates in tbe future," Mr. Bible said.

General Mills and Diageo to Combine Their Worldwide Consumer Foods Operations (PR Newswire, 07/17/2000)

Paul S. Walsh, Chief Operating Offleer of Diageo, said, "This agreement creates significant long-term value for tbe shareholders of botb Diageo and General Mills. This deal combines two powerful and complementary brand portfolios to create a major force in tbe U.S. food industry. It gives tbe Pillsbury brands tbe right platform from which to achieve tbeir full potential."

Key Competitive Strengths oftbe New General Mills: General Mills' sales will almost double, to nearly $13 billion, and its stronger, more balanced portfolio will be geared for faster growth. Pillsbury's major retail categories have been growing at a significantly faster rate tban General Mills' categories. In addition, General Mills' new business mix has a much stronger convenience profile, with nearly 80 percent of retail sales generated by ready-to-eat or quick-to-prepare foods. Beyond retail, General Mills will have significantly broader scale and capabilities in the fast-growing Foodservice channel, making General Mills one oftbe top U.S. Foodservice manufacturers. Our pro forma sales in fast-growing international markets will double, to $2.3 billion. In combining tbese businesses, General Mills will now have manufucturing, distribution and sales infrastructure in a number of global markets, including the U.K., Western Europe, Latin America and Australia. The company will be the market Ieader in tbe $1.5 billion U.S. refrigerated dough category. This business significantly expands General Mills' participation in refrigeraJ:ed foods, where the company already holds leadership positions in tbe $2 billion yogurt category, and tbe $580 million market for refrigerated entrees. General Mills will compete in two new breakfast food categories, with Hungry Jack frozen waffles and Pillsbury frozen pastries complementing tbe Big G ready-to-eat cerealline. The company will market a broader array of convenient lunch and dinner choices, with Totino's frozen pizza and snacks, Green Giant frozen vegetables and meal starters, Progresse soups, and Old Ei Paso Mexican foods joining tbe Betty Crackerdinner and side dish mix businesses.

Kellogg to Acquire Keebler PR Newswire, 10/26/2000

Revenue synergies should arise from enhanced distribution, marketing, and product development. Considerable cost synergies also are expected.

Kellogg Chairman and Chief Executive Officer Carlos M. Gutierrez and Keebler CEO Sam K. Reed said they expect tha1 benefits from tbe merger will include: • Diversification ofKellogg's portfolio into fuster-growing categories. * Substantial sales growth potential for Kellogg's convenience foods tbrough Keebler's direct store delivery (DSD) system. • New-product, cross branding, and license sharing opportunities. * Greater scale in all U .S. product distribution channels, including retailing, club and mass merchandising, foodservice, and vending. * Cost synergies from combining two grain-based, brand-based packaged food companies. * Greatly expanded opportunities to take advantage of Kellogg's world-class research and development resources.

"We welcome Keebler to tbe Kellogg family," Gutierrez said. "Keebler is an extremely well-run company, with strong brands and a powerful DSD system. We can leam a Iot frcm Keebler, and we believe we can strengthen both companies by bringing them togetber. The result should be better growth for botb."

Reed said, "The fit between these two companies is as natural as you can get. We have complementary strengths in Kellogg's traditional marketing and Keebler's in-store distribution and merchandising. Just think what our elves can do by bringing Kellogg's brands into our DSD system. We couldn't be more excited about tbe prospects for this uncommouly good union."

Appendix 149

Appendix 3.2: Frequencyofjoint occurrence ofdetailed motives

Note: Only code combinations with frequenc1es bigger than 4 are displayed. Values of 10 and bigger are bold. The analysis is based on the complete data sample (n~41 )

150 Appendix

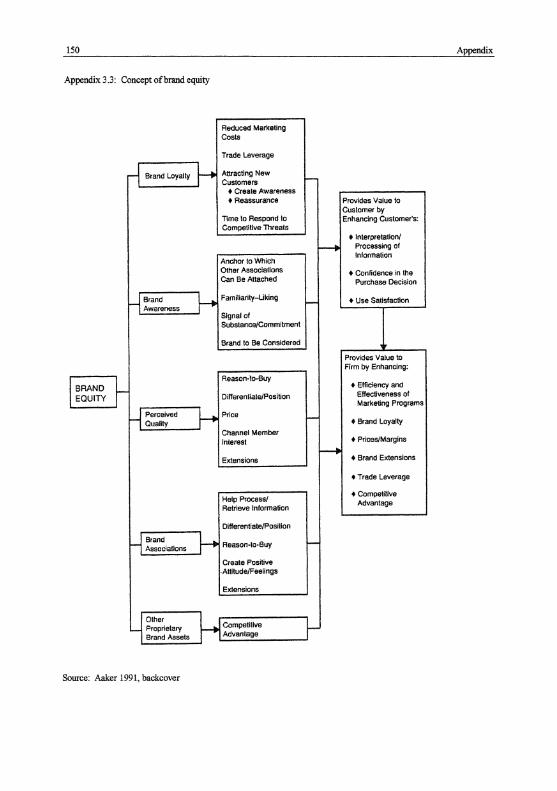

Appendix 3.3: Concept ofbrand equity

Reduced Marketing Costs

Trade Leveraga

-i Brand Loyally ~ Attraeüng New -Customers t Create Awareness t Reassuranca Provides Value to

Customer by Time lo Respond to Enhancing Customer's: Competitive Threals

+ lnterpretalionl

---+ Processing of

Anchor to Which Information

Other Asscciatlons + Confidence in lhe Can Be Altached Purehase Decision

-i Brand ~ Familiarity-Uking - + Use SaUsfaction

Awareness Signal of Substance/Commitment

Brand to Be Considered

Provides Value to Firm by Enhancing:

Reason-lo-Buy

IBAAND ~ + Efficiency and

EQUITY Differentiale/Position Effec1iveness of

~ Marketing Programs -1 Perceived Price -Ouality t Brand Loyalty

Channel Member lnterest • Prices/Marglns

---+ Extensions + Brand Extensions

• Trade Leveraga

Help Process/ + Campeillive

Retrleve Information Advantage

Differentiate/Posilion

-j Brand ~ Reason-lo·Buy -Associatlons

Create Positive .Attitude/Feelings

Extensions

~ Other Proprietary Competillve ~ Brand Assets Advantage

Source: Aaker 1991, backcover

Appendix 151

Appendix 3.4: Measured brand equity forfood manufacturing firms

Company Brand Equity

Measure * Anbeuser Busch 35 Brown-Forman 82 Cadbury-Schweppes 44 Campbell's 31 Dreyers Ice-Cream 151 General Mills 52 Heinz 62 Kellogj~; 61 Pillsbury 30 Quaker 59 Ralston-Purina 40 Sara Lee 57 Seagram 73 Smucker 126 Tootsie Roll 148

• Numbers are in percent offirm replacement value and relate to (average) financial company data as of1985.

Source: Sirnon and Sullivan 1993, 40

152

Appendix 4.1: Questtonnaire of conJoint stud)

CORNELL UNIVERSITY J ohnson Graduate School of Management

Study on Brand Acquisition Decisions

Appendix

Tb.is study is about acquisition decisions on packaged cookie brands. We want to find out which factors contribute most to the brand acquisition decisions of firms and how brands are financially valued in acquisition settings.

You are CEO of a top U.S . food company and make decisions about the acquisition of cookie brands. Piease note that there are no correct or wrang answers. We are interested in your individual perspective.

Pretests ofthis questionnaire showed that the completion will Iake about 35 minutes.

Win $100

In appreciation of your effort we will draw a lottery featuring a prize of $100 for every 25 completed questionnaires returned to us. We therefore ask you to provide your name and email address below. This cover page will be separated from the rest of the questionnaire to keep your responses confidential.

Name and e-mail address:

Piease drop the completed questionnaire in the provided Comell Campus mail envelope in the mailroom downstairs of Sage Hall or in room 304 (faculty support office ). Thank you very much for your cooperation!

Prof. Vithala R. Rao

Denise Dahlhoff

(E-mail: dd65@cornell .edu, Tel: 255-8225)

Ap endix

Acquisidon of Brands

Place yourself in the position ofthe CEO of a major food company. Y our company manufactures and markets ~ food products. Today you leamed that some established cookie brands-national brands seiVing the U.S. market-are being spun offby other food companies. The new situation makes you check out the acquisition possibilities.

Hereis some information on your company.

Your company:

Company2

Focus industries Snacks (crackers, chips)

Customer franchise Mainly young people (20-40 years)

Market position in company's No.2

focus industries

Pricing strategy Mediuntlpremium price Ievel

Company's positioning Convenience products, snack meals

Main distribution channels Grocery stores, convenience stores

Profit/net sales ratio * 10.0% • Profit/net sales rat10: md1cates percentage of profit per dollar of net sales

This company information is attached at the end ofthe questionnaire on the yellow sheet. Piease tear it ofT and have it in front of you when you make your decisions.

153

Now we ask you to make 12 brand acquisition decisions. There are three questions associated with each decision:

I. Which of the brands is more desirable for your company? F or each of the 12 decisions you will be presented two cookie brands which are characterized by several attributes.

2. Would you actually acquire the brand that you chose as more desirable (suppose there are no budget constraints)?

3. Ifyou would, please indicate the offer price that best rejlects the chosen brand's worth to yourcompany. Piease state the offer price as a multiple ofthe brand's current annual earnings. Note that the eamings are expected to continue in the future and that the acquired brand might be extended to other product categories.

~ The two brands change with each decision task. Therefore, please read the characteristics carefully. Piease use the information on both your company (see yellow sheet) and the brands to make your decisions.

154 Appendix

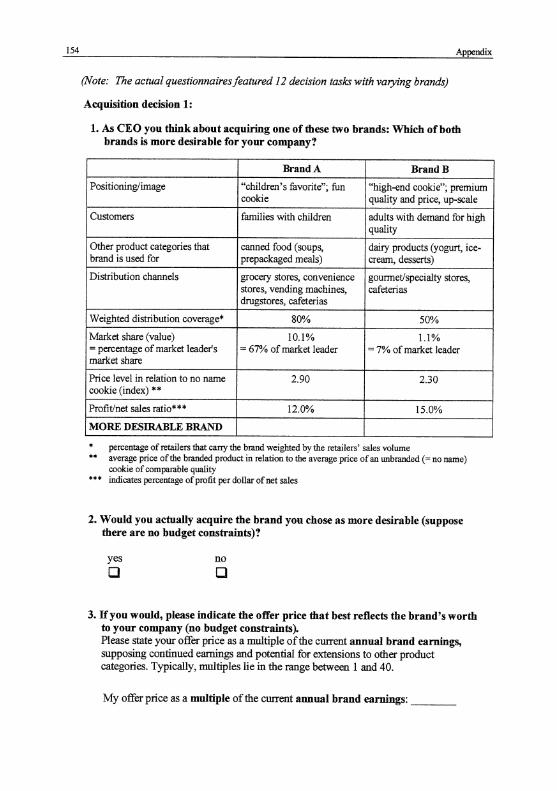

(Note: The actual questionnairesfeatured 12 decision tasks with varying brands)

Acquisition decision 1:

1. As CEO you think about acquiring one of these two brands: Which of both brands is more desirable for your company?

BrandA BrandB

Positionmg/image "children's favorite"; fun "high-end cookie"; premium cookie quality and price, up-scale

Customers families with children adults with demand for high quality

Other product categories that canned food ( soups, dairy products (yogurt, ice-brand is used for prepackaged meals) cream, desserts)

Distribution channels grocery stores, convenience gourmet/specialty stores, stores, vending machines, cafeterias drugstores, cafeterias

Weighted distribution coverage* 80% 50"/o

Market share (value) 10.1% 1.1% = percentage of market leader's = 67% ofmarket Ieader = 7% of market Ieader market share

Price Ievel in relation to no name 2.90 2.30 cookie (index) **

Profit/net sales ratio*** 12.0"/o 15.0"/o

MORE DESIRABLE BRAND

percentage of retailers 1hat cany the brand weighted by the retailers' sales volume •• average price ofthe branded productin relation to the average price ofan unbranded (=noname)

cookie of comparable quality ••• indicates percentage of pro fit per dollar of net sales

2. Would you actually acquire the brand you chose as more desirable (suppose there are no budget constraints)?

yes no

Cl Cl

3. Hyou would, please indicate the offer price that best retlects the brand's worth to your company (no budget constraints). Piease state your offer price as a multiple ofthe current annual brand earnings, supposing continued earnings and potential for extensions to other product categories. Typically, multiples lie in the range between 1 and 40.

My offerprice as a multiple ofthe current annual brand earnings: ___ _

A endix 155

Dec:isioa Maldag

How important were tbe following criteria in your acquisition decisions? very

unimportant important (=1) (=3) (=S)

Characteristics of IDI comJ!&DI Focus industries [J [J [J [J [J

Cuslomer groups [J [J [J [J [J

Market position in focus industries [J [J [J [J [J

Pricing strategy [J [J [J [J [J

Company's positioning [J [J [J [J [J

Main distribution channels [J [J [J [J [J

Profit/net sales ratio [J [J [J [J [J

Characteristics of tbe taaet brand Positionmg/image [J [J [J [J [J

Cuslomers [J [J [J [J [J

Other products that cookie brand is used for [J [J [J [J [J

Distribution channels [J [J [J [J [J

Weighted distribution coverage [J [J [J [J [J

Market share (value) [J [J [J [J [J

Market share as% oflll8ltet leader's market share [J [J [J [J [J

Price Ievel (compared to no name cookie) [J [J [J [J [J

Profit/net sales ratio [J [J [J [J [J

S!neaies/fit between IDI comJ!&DI and taa;et brand Company's and brand's positioning/image [J [J [J [J [J

Company's and brand's distribution channels [J [J [J [J [J

Company's and brand's Ill8ltet positions [J [J [J [J [J

Comp.'s pricing slrategy and brand's price Ievel [J [J [J [J [J

Product categories that brand is currently used for [J [J [J [J [J

Company's and brand's customer franchises [J [J [J [J [J

Profit/net sales ratios of company and target brand [J [J [J [J [J

Others: [J [J [J [J [J

Others: [J [J [J [J [J

!56 Ap ndix

Which criteria bad the strongest influence on your offer price?

onlyweak very strong inßuence inßuence

(=1) (=3) (=5) Market share ofthe brand Cl Cl Cl Cl Cl Profit/net sales ratio of the brand Cl Cl Cl Cl Cl Weighted distribution coverage ofthe brand Cl Cl Cl Cl Cl Synergies in distribution channels between my company and the brand Cl Cl Cl Cl Cl Fit ofmy company's and brand's pricing strategies Cl Cl Cl Cl Cl Access to new customer groups Cl Cl Cl Cl Cl Brand's potential to extend into other product categories Cl Cl Cl Cl Cl Fit ofmy company's and the brand's positioning Cl Cl Cl Cl Cl Others: Cl Cl Cl Cl Cl Others: Cl Cl Cl Cl Cl

Piease indicate how difficult you found the 12 acquisition decisions you made in the previous section.

very easy

(=1)

Cl

(=3)

Cl

very difficult (=5)

Cl

Appendix !57

About Yourself

Are you a 'cookie expert'? never/ some- regu- fre- very rarely tim es larly quently often

I eat packaged cookies .. . [J [J [J [J [J

I !lliy prepackaged cookies ... [J [J [J [J [J

very very weak low average good good

My knowiedge about cookie brands is ... [J [J [J [J [J

My knowledge about the food industry is . .. [J [J [J [J [J

Wbicb oftbe cookie brands bave you tried? How do you like tbem?

tried this cookie brand

yes no Oreo [J [J

Chips Deluxe [J [J

SnackWell's [J [J

Pepperidge Fann [J [J

Wbat is your working and educational background? (Multiple answers possible)

W orkin~: experience

[J Accounting

[J Marketing

[J Finance

[J General management I strategy

[J Management consulting

[J Investment banking

[J Auditing

Others:

do.!!l!!..!i!!! like this this cookie brand cookie brand at an ven: much

(=1) (=3) (=5) [J [J [J [J [J

[J [J [J [J [J

[J [J [J [J [J

[J [J [J [J [J

Focus in your MBA profU3IP

[J EBI

[J MFI

[J SIM

[J Strategie Brand Management

[J Investment Banking

[J Electives

[J Cayuga Fund Manager

158

Have you taken any courses on financial valuation or been involved in real-world mergers & acquisitions?

Courses on financial valuation of companies, assets, etc. Working experience in real-world mergers & acquisitions

What is your gender?

0 Fernale

0 Male

What is your age?

__ years

yes 0 0

no 0 0

Appendix

We appreciate your comments and suggestions concerning this questionnaire very much (understanding of questions, complexity of tasks, etc.).

THANK YOU VERY MUCH

FOR YOUR COOPERATION

Appendix 159

Appendix 4.2: Mruketing-related infonnation on Ieading U.S. cookie bmnd manufacturers

Nabisco Biscuit Keebler Specialty Foods McKeeFoods Pepperidge Fann

Crackers. cookies~ Cookies, sav01y Focus product premium grocery

Cooleies and crackers Cooleies Cookies, cakes, snacks snacks and specialty

categories products (such as and cereals breads condiments)

Position in the U.S. cookie I 2 3 4 5 market TotalUSdollar market share of

37.6% 17.8% 6.3% 6.2% 4.7% company's cookie brands* Companytotal $!,430m sales 1999 ** $3,640m $2,667.8m $900.0m $855.0m

(incl uding Godiva confectionery and overseas business)

~orbrllllds ~: Oreo, Chips ~:Chips Deluxe, Mother's, Archway ~:Little Pepperidge Farm, (selection) Ahoy!, SnackWell's, Cooleie Stix,. Sandies, Cookies, Mrs. Debbie, Mother's Cake Goldfish crackers,

Teddy Graharns; Fudge Shoppe, Vienna Wheatley' s, Bakery &Cookie;~ Godiva chocolate ~:Ritz, Fingers, Rainbow Vanilla Wagon, Marie Lu ~:Sunbelt (candy, biscuits and Premium; .Qtbg;_ A 1. W~rs,etc.~~: ice-cream) steak sauces, Grey Cheez-1~ Club Crackers, Poupon mustard, Life Snax Stix., Keebler Savers confections, Graharn, Zesta, Plantees nuts and Munch'ems, etc.~ .al,sQ: snacks Carr's, Reedy Cru~

Sunshine, Famous Amos, Murray, and Plantation, Girl Scout cookies

Descriptionof Mono brands with the Quality pcsitioning (yet Farnily branding, Farnily branding, good Premium brand, brllllding pclicy corporate name being no premium strategy), value~for-money quality for a positioning: upscale,

used as endorsement convenience orientation positioning, core ressanable price premium quality and on the package (resealable packsging strength are health price, ''indulgence"~ ( comparable to and snack sizes ), mono oriented products mono cookie brand Keebler); pruduct brand strategy in (used in connection variety under brand association with the with product name names (e.g., Oreo Keebler company brand which serves as sub--Dcuble Stut: Fat- as endorsement brlllld, e.g. Popperidge Reduced, Holiday, ( compamble to Nabisco ); Farm Milane, Oreo ice--cream mono brands used as Brussels, Sausalito, cones); SnackWell's · umbrella for product Lake Taboe); clearly, brand positioned as lines ( e.g. Chips DellLxe target group are adults health--conscious Crunchy Waln~ Soft 'n brand for sweet and Chewy, Coconut) savory product categories

Class ofbranding Mixed branding Mixed brllllding 'Hause ofbrands', i.e. 'Hause ofbrands', i.e. Cerparate branding strategy mono brands mono brands Product strategy Premium strategy: Product differentiation Huge product range of Broad coverage of Premium strategy:

top quality and price; strategy, niche lots offlavors and product categories in upscale quality, 'rich' product varieties orientation, growth by variations, substantial the cake, cookie and ingredients and include fat-reduced line extensions number of seasonal pie rnarket segments texture~ two lines: versions and seasonal products and healthy Disti.nctive Line products cookies (sugar~free, (European-style

fat~:free and low- offerings, e.g. Milane, cholesterol), "value .for Brussels) and money" positioning American Collection

(Chocolate Chunk Cookie Classics)

Table continues

160 Appendix

Nabisco Biscuit Keebler Specialty Foods McKeeFoods Pepperidge Farm

Further After establishing a Core strength and Similar to Keebler, Yending machines as Campetiters are not marketing-and completely new competitive advantage: direct store delivery additional distribution only cookie brands

business- product class of national distribution system in 45 states~ channel~ logistics witb lower-profile strategic crackers and cookies system DSD ('direct own Andre Boudin policy: an their way positioning but also information with the SnackWell's store deiivery', i.e. Sotmfough Bakery and back lo the harne base imported premium

brands in the mid- deiivery to stores through Cafe outlets mainly in empty trucks are used brands and in-store 1990s, the entire line own logistical force Califumia; afler years for backhauling goods bakeries~ innovative was refonnulated and rather than through of diversified food for third companies markering activities: repositioned in 1998 wholesalers, almest 3 conglomerate, 'Corporate Cookie

generaring a sales visits per "Week per store ); business focus is now Breaks' in cooperation soar; redesign of direct no. 1 manufucturer of on baired goods, esp. with several corporate store delivery sales private-labei products; cookies; toJrselling headquarters which system in 1999; broad manufactures Kellogg's products are oatmeal hosted sponsored vending machine PoJr Tarts and NutriOrain cookies cookie breaks in order presence; convenience bars; successful "to study impact of focus: snack advertising concept based cookie breaks" sizelsingle-serve on Keebler elves (findings: boost packages and characters employees' creativity, products, variety-pack energy and morale) items

Source: Kalorama Industty Report 1999, ''The US Market for Cookies", original data by Packaged Facts, lnc. 1997 Source: Hoover's On1ine Company Pro:flle (www.hoovezs.com)

Note: The infonnation in the tab1e is as of February 2000 and has been compi1ed from companies' web sites, annual reports, industry reports by investment banks (J.P. Morgan, PaineWebber, Morgan Stanley Dean Witter, among others), Hoover's Online Company Profile data base, and a ranking of the top food companies by Food Processing (1999), the leading U.S. food specialty magazine.

Appendix 161

Appendix 4.3: Comparative overview oftraditional versus choice-based conjoint analysis

Traditional (ratings-/raokings-based) Cboice-based eonjoint analysis eonjoint analysis

Task for respondents Judgment/assessment Decision

Number of objects to be Paired comparison, i.e. two options Usually set of more tban two options evaluated (most common)

Closeness to real decision Remote; evaluation is only pre-decisional Close; actual (albeit experimental) behavior stage; indication: likelihood of purchase, decision rather tban only pre-decisional

acquisition, accepting offer, or according evaluation action

Efficiency of data Profile ratings are more informative, thus Choices are less infmmative, thus less collection more efficient data collection efficient data collection

Method of studying Decompositional; inference of utilities for Decompositional; inference of utilities for preferenceslbehavior individual attribute Ievels from judgments individual attribute Ievels from choices

Featuresnone option? No None option can be entailed

Preference model CO!npensatory trade-off Accounts for lexicographical preference struetures

Level of analysis Individual, i.e. respoodent Ievel (standard) Aggregate, i.e. group Ievel (standard)

Estimated effects Especially suited for estimation of main Weil suited for estimation of interaction effects effects

Analytical tecbniques (Multiple) regression models Binary and multinomiallogit as weil as probit models

Utility function Linear Non-linear (S-shaped)

Ease ofanalysis 'Standard' procedure More complicated

Consideration of context Not considered in utility modeling Considered in utility modeling (by

effects ( e.g., competitive accounting for the specific set of options) situation)

Preferenceslpredicted Deterministic Probabilistic probahility of. choice

162 Appendix

Appendix 4.4: Distribution of samp1e subgroups

Version Company 1 2 3 Total

1 4 (3) 4 6 (2) 14 (9)

2 3 3 4 10

3 4 7 (6) 5 16 (15)

Total 11 (10) 14 (13) 15 (11) 40 (34)

Note: Numbers in parentbeses denote tbe subsamp1e sizes after removing inconsistently responding subjects (see chapter 4.5.3).

Appendix 4.5: Example ofbrand choice set

BrandG BrandH

Positioninglimage "Children's favorite"; fun ''High-end cookie"; premium cookie quality and price, up-scale

Customers Families with children Adults witb demand for high quality

Other product caiegories that brand Cereals Canned food ( soups, is used for prepackaged meals)

Distribution channels Grocery stores, drugstores Convenience stores, vending machirres

Weighted distribution coverage* 70% 60%

Market share ( value) 10.1% 4.3% = percentage of market Ieader's

= 67% of market Ieader = 29% of market Ieader market share

Price Ievel in relation to no name 2.90 3.40 cookie (index) **

Profitirret sales ratio*** 9.5% 7.5%

MORE DESIRABLE BRAND

References 163

References

Aaker, David A. (1991), Managing Brand Equity: Capitalizing on the Value of a Brand Name, New York: The Free Press.

Aaker, David A. (1993), "Are Brand Equity Investments Really Worthwhi1e?," in Brand Equity and Advertising, Aaker, David A. and Alexander L. Bie1, eds., Hillsdale/NJ: Lawrence Erlbaum Associates, 333-341.

Aaker, David A. (1995), Developing Business Strategies, 4th edition, New York: John Wiley &Sons.

Aaker, David A. and Robert Jacobson (1994), "The Financial Information Content of Perceived Quality," Journal ofMarketing Research, 31 (May), 191-201.

Advertising Age (1999), "100 Leaders by U.S. Advertising Spending," Advertising Age, 70, no. 40 (September 27, 1999), S4-S6.

Adweek Online Premium Services, SuperBrand Database, www.adweek.com.

Agins, Teri and Deborah Ball (2000), "Luxmy Match? L VMH Targets Donna Karan," lhe WallStreet Journal, December 19,2000, B1 and B6.

Agres, Stuart J. and Tony M. Dubitsky (1996), "Changing Needs for Brands," Journal of Advertising Research, 36 (January/February), 21-30.

Anderson, Sirnon P., Andre de Palma, and Jacques-Francois Thisse (1992), Discrete Choice Theory of Product Differentiation, Cambridge/MA: The MIT Press.

Atkins, Ralph, Goetz Hamann, and Andrew Edgecliffe-Jobnson (2000), "Wal-Mart at Center ofPrices Probe in Germany," Financial Times, June 28, 2000, 15.

Auty, Susan (1995), "Using Conjoint Analysis in Irrdustrial Marketing," Industrial Marketing Management, 24 (no. 3), 191-206.

Bala, Mohan V., Lisa L. Wood, Sheryl C. Cates, and Suzanne P. Garnbin (1998), "Predicting Participation Intentions for Optional Energy Services," Resources and Energy Economics, 20 (no. 3), 287-301.

Barnes, Julian (2001), "Market Place: Procter & Gamble Wants to Jettison Jif and Crisco," The New York Times on the Web, April26, 2001.

Barth, Mary E., Michael B. Clement, George Foster, and Ron Kasznik (1998), "Brand Values and Capital Market V aluation," Review of Accounting Studies, 3 (no. 1 and 2), 41-68.

Bear, Stearns & Co. (2000), Packaged Foods: An Affordable Harbor, Equity Research Report Consumer, November 2000.

Beck, Emest (1999), "United Biscuits Receives New Bid From Finalrealm," lhe WallStreet Journal Europe, December 17, 1999,3.

164 References

Beck, Emest (2000), "Unilever Renames Cleanser, Tidying Its Brand Portfolio," The Wall Street Journal, December 27,2000, B8.

Ben-Akiva, Moshe E. and Steven R. Lerman (1985), Discrete Choice Analysis- Theory and Application to Travel Demand, Cambridge/MA.: The MIT Press.

Benoit, Bertrand (2000a), "Aiming for More Cash Than Cany," Financial Times, December 20, 2000, 12.

Benoit, Bertrand (2000b), "Metro Keeps Quiet About Tesco's Shopping List," Financial Times, July 5, 2000, 18.

Birkin, Michael (1989), "The Bene:fits ofValuing Brands," in Brand Valuation- Establishing a True andFair View, John Mmphy, ed., London: Hutehinsou Business Books, 12-22.

Bonnot, Sabine, Emma Carr, and Michael J. Reyner (2000), "Fighting Brawn With Brains," The McKinsey Quarterly, No. 2, 76-87.

Branch, Shelly (2000), "Mannnoth Deals Are Expected to Spur More Consolidation in the Food Industry," The WallStreet Journal Interactive Edition, June 27,2000.

Branch, Shelly and Emest Beck (2000), "Unilever Buys Ben & Jeny's, SlimFast for Over $2.5 Billion," The WallStreet Journal Interactive Edition, April13, 2000.

Brewis, Janine (1999), "The Nestle Way to Foreign Expansion," Corporate Finance, October 1999, 14-15.

Brown, Steven P., Pamela M. Homer, and Jeffrey J. Inman (1998), "A Meta-Analysis of Relationships between Ad-Evoked Feelings and Advertising Responses," Journal of Marketing Research, 35 (January), 114-126.

Buchan, Edward and Alastair Brown (1989), "Mergers and Acquisitions," in Brand Valuation - Establishing a True and Fair View, Murphy, John, ed., London: Hutehinsou Business Books, 80-93.

Business Wire (1999), "IBP, Inc. to Acquire Corporate Brand Foods America," December 21, 1999.

Business Wire (2000a), "Bestfoods in Final Negotiations With Brazilian Food Company; Bestfoods' Brazilian BusinesstoBe Doubled," Febnuny 7, 2000.

Business Wire (2000b), "Tyson Foods Speeds Up Bid Process for IBP, Inc. With Hart-ScottRodino Filing and Investor Outreach," December 14,2000.

Business Wire (2000c ), "Unilever to Seil European Bakery Supplies Business for EUR 700 Million," July 11, 2000.

Capron, Laurence, Pierre Dussage, and Will Mitchell (1998), "Resource Redeployment Following Horizontal Acquisitions in Europe and North America, 1988-1992," Strategie Management Journal, 19 (July ), 631-661.

References 165

Capron, Laurence and John Hulland (1999), "Redeployment of Brands, Sales Forces, and General Marketing Management Expertise Following Horizontal Acquisitions: A Resource-Based View," Journal ofMarketing, 63 (April), 41-54.

Carmone, F.J., jr. (1995), "Conjoint Designer-Consurve-Adaptive Conjoint Analysis System (ACA)," Journal ofMarketing Research, 32 (February), 113-121.

Carroll, J. Douglas and Paul E. Green (1995), "Psychometrie Methods in Marketing Research: Part I, Conjoint Analysis," Journal ofMarketing Research, 32 (November), 385-391.

Cattin, Philippe and Dick R. Wittink (1982), "Commercial Use of Conjoint Analysis: A Survey," Journal ofMarketing, 46 (Summer), 44-53.

Chatterjee, Sayan (1986), "Types of Synergy and Economic Value: The Impact of Acquisitions on Merging and Rival Firms," Strategie Management Journal, 7 (March/April), 119-139.

Chen, Kyle D. and Warren H. Hausman (2000), "Technical Note: Mathematical Properlies of the Optimal Product Line Selection Problem Using Choice-Based Conjoint Analysis," Management Science, 46 (no. 2), 327-332.

Churchill, Gilbert A., Jr. (1987), Marketing Research-Methodological Foundations, 4th edition, Chicago/ll.: The Dryden Press.

Clemente, Mark N. and David S. Greenspan (1996), "Getting the Biggest Marketing Bang From the Merger," Mergers and Acquisitions, 31 (July/ August), 19-22.

Cooil, Bruce, Russen S. Winer, and David L. Rados (1987), "Cross-Validation for Prediction," Journal ofMarketing Research, 24 (August), 271-279.

Copeland, Tom, Tim Koller, and Jack Murrin (1996), Valuation-Measuring and Managing the Value ofCompanies, 2nd edition, New York!NY: John Wiley & Sons.

Corstjens, Marcel and Rajiv Lai (2000), "Building Store Loyalty Trough Store Brands," Journal ofMarketing Research, 37 (August), 281-291.

Credit Suisse First Boston (2000a), Equity Research: Europe/Food Manufacturing, worldofood.com, February 7, 2000.

Credit Suisse First Boston (2000b), Equity Research: Europe/Food Manufacturing, worldofood.com, September 18, 2000.

Credit Suisse First Boston (2000c), Equity Research: Europe/Food Manufacturing, worldofood.com, December 4, 2000.

Credit Suisse First Boston (2001), Equity Research Packaged Foods U.S: Food Stocks in Perspective, September 26, 2001.

Darmon, Rene Y. and Domonique Rouzies (1994), "Reliability and Intemal Validity of Conjoint Estimated Utility Functions under Error-Free Versus Error-Full Conditions," International Journal of Research in Marketing, 11 (no. 5), 465-4 76.

166 References

Davidson, Russen and James G. MacKinnon (1999), "Bootstrap Testing in Nonlinear Models," International Economic Review, 40 (May), 487-508.

Day, George (1992), "Marketing's Contribution to tbe Strategy Dialogue," Journal of the Academy ofMarketing Science, 20 (no. 4), 323-329.

Day, George and Liam Fahey (1988), "Valuing Market Strategies," Journal ofMarketing, 52 (July), 45-57.

Deogun, Nikbil and Emest Beck (2000), "Unilever Wins tbe Battle to Buy Bestfoods," The WallStreet Journal Interactive Edition, June 7, 2000.

Deogun, Nikbil and Scott Kilman (2000), "Cargrill Has Deal to Acquire Agribrands After Cuttingin on Ralcorp's Offer," The WallStreet Journal, December 4, 2000, A4.

Deogun, Nikbil and Steven Lipin (2000), "Food Fights? Unilever Bid Could Prompt Merger Binge," The WallStreet Journal Interactive Edition, May 4, 2000.

Doran, Howard E. (1989), Applied Regression Analysis in Econometrics, New York/NY: Dekker.

Dow Jones International News (1998a), "Cadbury/Coca-Cola -2: Dr. Pepper, Canada Dry, Crush Brands," December 11, 1998.

Dow Jones International News (1998b), "Cadbury/Coca-Cola -3: ToSeil Non-U.S. Bottling Activities," December 11, 1998.

Dow Jones Online News (1998), "U.K. Investors Applaud Cadbury's Coca-Cola Bottling Contract," January 15, 1998.

Dow Jones Interactive, http://nrstg1s.djnr.com, link 'Library'.

Eccles, Robert G., Kersten L. Lanes, and Thomas C. Wilson (1999), "Are You Paying too Much fortbat Acquisition?," Harvard Business Review, 77 (July/ August), 136-146.

Edgecliffe-Johnson, Andrew (2000a), "Market Digests Food Merger," Financial Times, July 18,2000, 20.

Edgecliffe-Johnson, Andrew (2000b), "The Feast After tbe Famine," Financial Times, June 30,2000, Financial Times Survey: International Mergers & Acquisitions, 13.

Edgecliffe-Johnson, Andrew (2000c), "U.S. Food Sector Looks to Mergers for Recovery," Financial Times, February 14,2000, 18.

Edgecliffe-Johnson, Andrew (2000d), "Wal-Mart Threat Hits U.S. Retail Stocks," Financial Times, August 24, 2000, 13.

Edgecliffe-Johnson, Andrew (2001a), "Back to Cheap and Cheerful," Financial Times, June 20, 2001, 13.

References 167

Edgecli:ffe-Johnson, Andrew (2001b), "7-Eleven Makes Smaller Numbers Pay," Financial Times, July 25,2001, 15.

Edgecli:ffe-Johnson, Andrew and Adrian Michaels (2001), "P&G to Acquire Clairol for $4.95bn," Financial Times, May 22,2001, 17.

Edgecli:ffe-Johnson, Andrew and Susanna Voy1e (2000), "Waltzing Away With the Prettiest Girl atthe Dance," Financial Times, June 7, 2000,26.

Eig, Jonathan (2000), "Sara Lee Sets Restructuring Plan With an Eye on Global Expansion," The WallStreet Journal Interactive Edition, June 1, 2000.

Elrod, Teny and Keith Chrzan (2000), "The Value of Extent-of-Preference Information in Choice-based Conjoint Analysis," in Conjoint Measurement - Methods and Applications, Gustafsson, Anders, Andreas Herrmann, and Frank Huber, eds., Berlin and New Y ork: Springer, 209-223.

Elrod, Teny, Jordan J. Louviere, and Krishnakumar S. Davey (1992), "An Empirical Comparison of Ratings-Based and Choice-Based Conjoint Models," Journal of Marketing Research, 29, August, 368-377.

Evans, Sirnon (2000), "Upside in Foster's Beringer Buy Despite Share Slip," Australion Financial Review, September 20, 2000, 16.

Farquhar, Peter H. and Vithala R. Rao (1976), "A Balance Model for Evaluating Subsets of Multiattributed Items," Management Science, 22 (no. 5), 528-539.

Fitzgerald Bone, Paula, Subhash Sharma, and Terence A. Shimp (1989), "A Bootstrap Procerlure for Evaluating Goodness-of-Fit Indices of Structural Equation and Confirmatory Factor Models," Mergers and Acquisitions, 26 (F ebruary ), 105-111.

Food Institute (2000), The Food Institute Report, 73 (no. 46), November 20, 2000, www .foodinstitute.com.

Food Processing (1999), The Top 100 Food Companies of 1999, Special Supplement, May, Putman Publishing.

Gaughan, Patrick A. (1999), Mergers, Acquisitions, and Corporate Restructurings, 2nd edition, New Y ork: John Wiley & Sons.

Gelb, Gabriel M. (1988), "Conjoint Analysis Helps Explain the Bid Process," Marketing News, 22 (no. 6), 1-2.

Gillespie, Jeffiey, Gary Taylor, Alvin Schupp, and Ferdinand Wirth (1998), "Opinions of Professional Buyers toward a New, Alternative Red Meat," Agribusiness, 14 (no. 3), 247-256.

Grant, Linda (1996), "Gillette Knows Shaving-and How to Turn out New Products," Fortune, 134, October 14, 1996,207-212.

168 References

Green, Paul E. (2000), "Foreword," in Conjoint Measurement- Methods and Applications, Gustafsson, Anders, Andreas Hemnann, and Frank Huber, eds., Berlin and New Y ork: Springer, 1-3.

Green, Paul E., Abba M. Krieger, and Teny G. Vavra (1997), "Evaluating New Products," Marketing Research, 9 (Winter), 12-21.

Green, Paul E. and V. Srinivasan (1990), "Conjoint Analysis in Marketing: New Developments With Implications for Research and Practice," Journal of Marketing, 54 ( October ), 3-19.

Greene, William H. (1993), Econometric Analysis, 2nd edition, Englewood Cliffs/NJ: Prentice Hall International.

Gregozy, James R. and Jack G. Wieehrnano (1997), Leveraging the Corporate Brand, Lincoinwood (Chicago)!Ill.: NTC Business Books.

Guo, Chuanfa, Lynne R. Wilkens, Mare A. Evans, Christine M. Hansen, and Teny D. Schultz (2000), "Use of Bootstrap Procedure and Monte Car1o Simulation - Response," The Journal ofNutrition, 130 (October), 2618.

Gurdjian, Pierre, George Kerschbaumer, Michael Kliger, and Johanna Waterous (2000), "Bagging Europe's Groceries," The McKinsey Quarterly, 37 (no. 2), special edition, 68-75.

Gustafsson, Anders, Andreas Herrmann, and Frank Huber (2000), "Conjoint Analysis as an Instrument of Market Research Practice, " in Conjoint Measurement - Methods and Applications, Gustafsson, Anders, Andreas Herrmann, and Frank Huber, eds., Berlin and New York: Springer, 5-45.

Haaijer, Rinus and Michel Wedel (2000), "Conjoint Choice Experiments: General Characteristics and Alternative Model Specifications, " in Conjoint Measurement -Methods and Applications, Gustafsson, Anders, Andreas Hemnann, and Frank Huber, eds., Berlin and New York: Springer, 319-360.

Haigh, David (1998), Brand Valuation - Understanding, Exploiting and Communicating Brand Values, London: Financial Times Retail & Consumer Publishing.

Hanes, Kathtyn (1999), "Making Synergies Work," Global Finance, 13 (March), 42-45.

Hansell, Sau! (2000), "Last Noel for Some Dot-Coms," The New York Times, December 23, 2000, C1-C2.

Hays, Constance L. (2001), "Wal-Mart Bulks Up on Private Labels," The New York Times on the Web, July 8, 2001.

Hise, Richard T. (1991), "Evaluating Marketing Assets in Mergers and Acquisitions," The Journal ofBusiness Strategy, 12 (July/August), 46-51.

Hobbs, Jill E. (1996), "Transaction Costs and Slaughter Cattle Procurement: Processors' Selection ofSupply Channels," Agribusiness, 12 (no. 6), 509-523.

References 169

Hollinger, Peggy (2000), "German Retailer in Secret Approach to Rival Groups," Financial Times, July 4, 2000, 1.

Hollinger, Peggy and Bertrand Benoit (2000), "Metro 'Must Boost Its Profitabiljty'," Financial Times, December 20,2000, 18.

Holson, Laura M. and Melody Peterson (2000), "Procter & Gamble Meets in Pursuit of Merger Talks," The New York Times, January 22, 2000, Al.

Hoover's, Inc., Hoover's Online Company Profiles, www.hoovers.com.

Hopkins, H. Donald (1987), "Acquisition Strategy and the Market Position of Acquiring Firms," StrategieManagement Journal, 8 (November/December), 535-547.

Huber, Joel (1999), "The Importance of Multinomial Logit Analysis of Individual Consumer Choices," in CBC User Manual Version 2.0, Sawtooth Software, Fl- FIS.

Huber, Joel, Dick R. Wittink, John A. Fiedler, and Richard Miller (1993), "The Effectiveness of Alternative Preference Elicitation Procedures in Predicting Choice," Journal of Marketing Research, 30 (February), 105-114.

Hussey, Roger and Audra Ong (2000), "Can We Put a Value on a Name: The Problem of Accounting for Goodwill and Brands," Credit Control, 21 (no. 1/2), 32-33.

Ind, Niebolas (1997), The Corporate Brand, New York: New Yorl< Uuiversity Press.

J.P. Morgan (1999a), Market Share Analysis, Food Equity Research, November 19, 1999, NewYork.

J.P. Morgan (1999b), Market Share Analysis, Food Equity Research, December 17, 1999, NewYork.

J.P. Morgan (2000), Mergers & Acquisitions 1999, Company Brochure, New Yorl<.

Jury, Jenuifer (1999), "Food and Drink-Rising to the Bait," European Venture Capital Journal, December 1, 1999, 39-45.

Kalorama Information (1999), The US. Marketfor Cookies, www.bell-howell.com.

Kamakura, Wagner A. and Gary J. Russen (1993), "Measuring Brand Value With Scanner Data," International Journal ofResearch in Marketing, 10 (no. 1), 9-22.

Kamm, Thomas (1999), "Europe Marks a Year of Serious Flirtation With the Free Market," The WallStreet Journal, December 30, 1999, Al-A2.

Keller, Kevin Lane (1998), Strategie Brand Management-Building, Measuring, and Managing Brand Equity, Upper Saddle River/NJ: Prentice Hall.

Kilman, Scott (2000), "ConAgra, International Horne Foods Join Sector's Consolidation Bandwagon," The WallStreet Journallnteractive Edition, June 26, 2000.

170 Refurences

Komobis, Karl-Joerg (1997), "Die Entwicklung von Handelsmarken-Untersuchungen und Zukunftsperspektiven im V erbrauchsgüterbereich," in Handelsmarken-Entwicklungstendenzen und Zukunftsperspektiven der Handelsmarkenpolitik, Bruhn, Manfred, ed., 2nd edition, Stuttgart: Schaeffer-Poesche1 Verlag.

Kotl.er, Philip (2000), Marketing Management-The Millennium Edition, Upper Saddle River/NJ: Prentice Hall.

Kvint, Vladimir L. (1998), "Nature oflntemational JointVenturesand Their Role in Global Business,'' in International M&A, Joint Ventures, and Beyond- Doing the Deal, David J. BenDaniel andArthurH. Rosenbloom, eds., New York: Jobn Wiley & Sons, 295-314.

Lane, Vicki and Robert Jacobsen (1995), "Stock Market Reactions to Brand Extension Announcements: The Effects ofBrand Attitude and Familiarity," Journal ofMarketing, 59 (Janumy), 63-77.

Lazich, Robert S., ed., (1999), Market Share Reporter 2000, Farmington Hills/Ml: The Gale Group.

Lev, Baruch and Theodore Sougiannis (1996), "The Capitalization, Amortization, and ValueRelevance ofR&D," Journal of Accounting and Economics, 21, 107-138.

Li, Hongyi and G. S .. Maddala (1999), "Bootstrap Variance Estimation of NOnlinear Functions ofParameters: An Application to Long-Run Elasticities ofEnergy Demand," The Review ofEconomics and Statistics, 81 (November), 728-733.

Loken, Barbara and Deborah Roedder Jobn (1993), "Diluting Brand Beliefs: When Do Brand Extensions Have a Negative hnpact?," Journal ofMarketing, 51 (July), 71-84.

Louviere, Jordan J. and George Woodworth (1983), "Design and Analysis of Simulated Consumer Choice or Allocation Experiments: An Approach Based on Aggregate Data," Journal ofMarketing Research, 20 (November), 350-367.

Louviere, Jordan J., David A Hensher, and Joffie D. Swait (2000), Stated Choice MethodsAnalysis and Application, Cambridge!UK: University Press.

Mahajan, Vijay, Vithala R. Rao, and Rajendra K. Srivastava (1994), "An Approach to Assess the hnportance of Brand Equity in Acquisition Decisions," Journal of Product Innovation Management, 11 (June), 221-235.

Maler, Kevin (2000), "Hefty Price for Pillsbury May Trim General Mills Earnings per Share," Knight-Ridder Tribune Business News, July 18, 2000.

MarketResearch.com (2000a), Market Looks: The U.S. Health and Natural Food Market, June2000.

MatketResearch.com (2000b ), Market Looks: The U.S. Market for Frazen and Refrigerated Hand-Held Foods, March 2000.

MarketResearch.com (2000c), Market Looks: The U.S. Marketfor Nutraceuticals, September 2000.

References 171

MarketResearch.com (2000d),Market Looks: The U.S. Marketfor lce-Cream, August 2000.

McKay, Betsy (2000), "After Quaker, PepsiCo's Nooyi to Add Top Job," The WallStreet Journal, December 5, 2000, Bl.

McKay, Betsy and Jonathan Eig (2000), "PepsiCo Hopes to Feast on Profits From Quaker Snacks," The WallStreet Journal, December 4, 2000, B4.

Merrill Lynch (2000a), Moody's Food Industry Outlook-Highlights From Moody's Teleconference, U.S. Consumer Goods, February 9, 2000.

Merrill Lynch (2000b), The Food Industry-Brand Power: Separating Fluff From Stuff, Industiy Report, September 13, 2000.

Moorman, Christirre and Roland T. Rust (1999), "The Role of Marketing," Journal of Marketing, 63 (Special Issue), 180-187.

Monotoya-Weiss, Mitzi and Roger J. Calantone (1999), "Development and J:mplementation of a Segment Selection Procedure for Industrial Product Markets," Marketing Science, 18 (no. 3), 373-395.

Morgan Stanley Dean Witter (2000), October 8 IRI Update - Monthly Recap, Equity Research Report Food & Foodservice, November 3, 2000.

Mummalaneni, Venkatapparao, Khalid M. Dubas, and Chiang-Nan Chao (1996), "Chines Purchasing Managers' Preferences and Tmde-offs in Supplier Selection and Performance Evaluation," IndustrialMarketing Management, 25 (no. 2), 115-124.

Mu.rphy, Steven (1999), "M&A Commentary: Wal-Mart Provides Food for Thought," European Venture CapitalJournal, October I, 1999, 54-55.

Naude, Peter and Francis Buttle (2000), "Assessing Relationship Quality," Industrial Marketing Management, 29 (no. 4), 351-361.

Neff, Jack (1999), "The 1999 Top 100 Food Companies," Food Processing, supplement, May, 27-28.

Newman, Laurance R. and Guy F. diCicco (1998), "Strategie Choices," in International M&A, Joint Ventures, and Beyond- Doing the Deal, David J. BenDaniel and Arthur H. Rosenbloom, eds., New York: John Wiley & Sons, 3-25.

Newman, Anne (2000), "Cleaning House at Unilever," Business Week, March 6, 2000, 54.

N.N. (1999a), "Food for Growth," Discount Store News, October, 65-66.

N.N. (1999b), "Kellogg to Acquire Worthington Foods for 1.75 Times Revenue," Weekly Corporate Growth Report, no. 1064, October 11, 1999, 10411.

N.N. (2000), "M&A Roundtable: How M&A Will Navigate the Turn into a New Century," Mergers & Acquisitions, 35 (no. 1 ), 29-35.

172 References

N.N. (2001), "Europe's Food Retailers: Hungry for Credit," The Economist, January 6, 2001, 55-56.

Ohtani, Kazuhiro (2000), "Bootstrapping K and Adjusted K in Regression Analysis," EconomicModelling, 17 (December), 473-483.

Ott, R. Lyman (1993), An Jntroduction to Statistical Methods and Data Analysis, 4th edition, Belmont/CA: W adsworth.

Pretzlik, Charles and William Lewis (2000), "Cross-border Consolidation Gains Pace", Financial Times, Supplement: FT Survey International Mergers & Acquisitions, June 30, 2000, 1-II.

Paine Webher (2000), Packaged Foods Monthly, Equity Research Report Packaged Foods, October 19, 2000.

Pilling, David and Andrew Edgecliffe-Johnson (2000), ''Novartis Joins Quaker to Make Functional Foods," Financial Times, February 10, 2000, l.

PR Newswire (2000), "Kellogg to Acquire Keebler," October 26, 2000.

Priem, Richard L. (1992), "An Application ofMetric Conjoint Analysis for the Evaluation of Top Managers' Individual Strategie Decision Making Processes: A Research Note," Strategie Management Journal, 13 (Summer), special issue, 143-156.

Raghavan, Anita, Nikbil Deogun, and Metthew Eig (2000), "Diageo Holds Talks With General Mills on Merging Pillsbmy With U.S. Firm," The Wall Street Journal Jnteractive Edition, July 13, 2000.

Rangaswamy, Venkatram and Steven H. Cohen (2000), "Latent Class Analysis for Conjoint Analysis, " in Conjoint Measurement- Methods and Applications, Gustafsson, Anders, Andreas Hernnann, and Frank Huber, eds., Berlin and New York: Springer, 361-392.

Rao, Vithala R., Vijay Mahajan, and Nikhil P. Varaiya (1991), "A Balance Model for Evaluating Finns for Acquisition," Management Science, 37 (March), 331-349.

Ratner, Juliana (2000), "Europeans Enjoy U.S. Shopping Spree," Financial Times, August 16, 2000, 13.

Reddy, Srinivas K., Susan L. Holak, and Subodh Bhat (1994), "To Extend or Not to Extend: Success Determinants of Line Extensions," Journal of Marketing Research, 31 (May ), 243-262.

Reibstein, David J., John E. G. Bateson, and William Boulding (1987), Conjoint Analysis Reliability: Empirical Findings, report no. 87-102, February, Cambridge/Mass.: Marketing Science Institute.

Reutterer, Thomas and Herbert W. Kotzab (2000), "The Use of Conjoint Analysis for Measuring Preferences in Supply Chain Design," Industrial Marketing Management, 29 (no. 1), 27-35.

References 173

Rhoads, Cbristopher (2000), "German Markets Gear up for 'BigBang' ifTax Law Passes," The WallStreet Journal, January 31,2000, A24.

Rosenfeld, Irene B. (1980), A Conditional Vector Model of Subset Evaluation: Development and Empirical Test, doctoral dissertation, Comell University, Ithaca/New York.

Sander, Mattbias (1995), "Markenbewertung auf Basis der hedonischen Theorie," Markenartikel, no. 2, 76-80.

Sattler, Henrik (1997), Monetäre Bewertung von Markenstrategien für neue Produkte, Stuttgart: Schaeffer-Poeschel.

Schulz, R. and K. Brandmeyer (1989), "Die Marken-Bilanz: Ein Instrument zur Bestimmung und Steuerung von Markenwerten," Markenartikel, no. 7, 364-370.

Securities Data Company, "SDC Platinum", Mergers & Acquisitions Database, Newark/NJ.

Seth, Anju (1990), "Value Creation in Acquisitions: A Re-Examination of Performance Issues," Strategie Management Journal, 11 (F ebruary ), 99-115.

Shapinker, Michael (2000), "Marrying in Haste," Financial Times, Apri112, 2000, 14.

Simon, Carol J. and Mary W. Sullivan (1993), "The Measurement and Determination of Brand Equity: A Financial Approach," Marketing Science, 12 (Winter), 28-52.

Sirower, Mark L. (1997), The Synergy Trap, New Yorlc The Free Press.

Sorensen, Robert C. (1981), "Marketing Information and the Determination of Value," in Handbook of Mergers, Acquisitions, and Buyouts, Steven James Lee, and Robert Douglas Colman, eds., Englewood Cliffs/NJ: Prentice Hall, 140-146.

Sorkin, Andrew Ross (2000), "General Mills Board Is Said to Be Ready to Vote on Pillsbury Deal," The New York Times, July 15,2000, Cl and C14.

Sorkin, Andrew Ross (2001), "P.&G. Is Said Close to Deal to Acquire Clairol," The New York Times on the Web, May 21, 2001.

Spiegel, Peter (2000), "Old Laws Harnper New Acquisitions," The Financial Times, July 18, 2000,4.

SPSS Inc. (1999a), SPSS Base 10.0 Applications Guide, Chicago/ll.: SPSS.

SPSS Inc. (1999b), SPSS RegressionModels 10.0, Chicago/11.: SPSS.

Srinivasan, V. (1979), "Network Models for Estimating Brand-specific Effects in Multiattribute Marketing Models," Management Science, 25 (January ), 11-21.

Srivastava, Rajendra K. and Allan D. Shocker (1991), Brand Equity: A Perspective on lts Meaning and Measurement, Report no. 91-124, October, Marketing Science Institute.

174 References

Srivastava, Rajendra K., Tasadduq A. Shervani, and Liam Fahey (1998), "Market-Based Assets and Shareholder Value: A Framewerk for Analysis," Journal of Marketing, 62 (January), 2-18.

Srivastava, Rajendra K., Tasadduq A. Shervani, and Liam Fahey (1999), "Marketing, Business Processes, and Shareholder Value: An Organizationally Embedded View of Marketing Activities and the Discipline of Marketing," Journal of Marketing, 63 (Special Issue), 168-179.

Stahl, Michael J. and Thomas W. Zimmerer (1984), "Modeling Strategie Policies: A Simulation ofExecutives' Acquisition Decisions," Academy ofManagement Journal, 27 (no. 2), 369-383.

Standard . & Poor's (1999), Campustat North America-Data Guide, Englewood!CO: McGraw-Hill.

Standard & Poor's (2000a), "Foods & Nonalcoholic Beverages," in Industry Surveys, Standard & Poor's, May 18, 2000, vol. 168, no. 20, section 1, New York: McGrawHill, FNB 1-FNB35.

Standard & Poor's (2000b), "Foods & Nonalcoholic Beverages," in Industry Surveys, Standard & Poor's, November 23, 2000, vol. 168, no. 47, section 1, New York: McGraw-Hill, FNB1-FNB35.

Standard & Poor's (2000c), "Supermarkets & Drugstores," in Industry Surveys, Standard & Poor's, June 8, 2000, vol. 168, no. 23, section 1, New York: McGraw-Hill, SD1-SD28.

Standard & Poor's (2001a), "Foods & Nonalcoholic Beverages," in Industry Surveys, Standard & Poor's, June 7, 2001, vol. 169, no. 23, section 1, New York: McGraw-Hill, FNB1-FNB35.

Standard & Poor's (2001b), S&P's Campustat Within Research Insight, release 7.6, August 23,2001, Englewood/CO: McGraw-Hill.

Strub, Peter J. and Steven J. Herman (1993), "Can the Sales Force Speak for the Customer?," Marketing Research, 5 (Fall), 32-35.

Studer, Margaret and Jennifer Ordonez (2000), "The Golden Arches: Burgers, Fries and 4-Star Rooms," The Wall StreetJournal, November 17,2000, Bland B4.

Sullivan, Ruth (2000), "Adding to the Gucci Handbag," Financial Times, June 5, 2000, 8.

Swait, Joffie, Tulin Erdem, Jordan Louvriere, and Chris Dubelaar (1993), "The Equalization Price: A Measure of Consumer-Perceived Brand Equity," International Journal of Research in Marketing, 10 (no. 1), 23-45.

Swets, John A. (1988), "Measuring the Accuracy ofDiagnostic Systems," Science, 24, June 8, 1988, 1285-1293.

References 175

Sy, Hamath A, Merle D. Faminow, Gazy V. Johnson, and Gazy Crow (1997), "Estimating the Values of Cattle Characteristics Using an Ordered Probit Model," American Journal of Agricultural Economics, 79 (no. 2), 463-476.

Tomkins, Richard (2000a), "Manufacturers Strike Back," Financial Times, June 16,2000, 12.

Tomkins, Richard (2000b), "Selling to the Sated," Financial Times, March 22, 2000, 12.

Tullous, Raydel and Michael J. Munson (1991), "Irade-Offs Under Uncertainty: Implications for Industrial Purchasers," International Journal of Purchasing and Materials Management, 27 (no. 3), 24-31.

UBS Warburg (2000), Packaged Foods Monthly, Equity Research Report Packaged Foods, December 5, 2000.

UBS Warburg (2001), Global Food Analyser-Still Got an Appetite?, Global Equity Research Report Food, September.

Ury, Jennifer (1999), "Focus: Food and Drink-Rising to the Bait", European Venture Capital Journal, December 1, 1999, 39-45.

Vandenbosch, Mark B. and Charles B. Weinberg (1997), "A Value Analysis Model for Farm Equipment Manufucturers," Agribusiness, 13 (no. 4), 409-421.

Varadarajan, P. Rajan (1992), "Marketing's Contribution to Strategy: The View From a Different Looking Glass," Journal of the Academy of Marketing Science, 20 (Fall), 335-343.

Verman, Rohit and Madeleine E. Puliman (1998), "An Analysis of the Supplier Se1ection Process," Omega, 26 (no. 6), 739-750.

Voyle, Susanna and Andrew Edgecliffe-Johnson (2000), "Unilever Wins Bestfoods Prize," Financfal Times, June 7, 2000, 1.

Voyle, Susanna, Andrew Edgecliffe-Johnson, and Christopher Bowe (2000), "General Mills very Close to Pillsbury Deal," Financial Times, July 24, 2000, 23.

Vriens, Marco, Harmen Oppewal, and Michel Wedel (1998), "Ratings-Based versus ChoiceBased Latent Class Conjoint Models - An Empirical Comparison," Journal of the Market Research Society, 40 (July), 237-248.

Walter, Gordon A and Jay B. Barney (1990), "Research Notes and Communications Management Objectives in Mergers and Acquisitions," Strategie Management Journal, 11 (Januazy), 79-86.

Wang, C. Y., Suojin Wang and R. J. Carroll (1997), "Estimation in Choice-Based Sampling With Measurement Error and Bootstrap Analysis," Journal of Econometrics, 77 (March), 65-86.

176 References

Weber, John A. and Utpal M. Dholakia (2000), "Including Marl<eting Synergy In Acquisition Analysis: A Step-Wise Approach," Industrial Marketing Management, 29 (March), 157-177.

Weiner, Jonathan (1994), "Forecasting Demand: Consumer Electronics Marl<eter Uses a Conjoint Approach to Configure Its New Product and Set the Right Price," Marketing Research, 6 (Summer), 6-11.

Weston, John Fred, Kwang S. Chung, and Juan A. Siu (1998), Takeovers, Restructuring, and Corporate Governance, 2nd edition, Upper Saddle River/NJ: Prentice Hall.

Williams, Frances (2000), "Flows of Foreign Investment Surge," Financial Times, December 8, 2000,8.

Willman, John (2000), "Unilever Goes on a Healthy Diet," Financial Times, April 13, 2000, 24.

Wind, Jerry, Paul E. Green, Douglas Shifilet, and Marsha Scarbrough (1989), "Courtyard by Marriott: Desiguing a Hotel Facility With Consumer-Based Marketing Models," Inteifaces, 19 (Janmuy/Februruy), 25-47.

Winter, Greg (2000), "PepsiCo Buys a 90% Stake in South Beach Beverages," The New York Times, October 31, 2000, C2.

Winter, Greg and Andrew Ross Sorkin (2001), "Canada Company Expected to Buy Unilever's Bakeries," The New York Times on the Web, Februruy 19,2001.

Wittink, Dick R., J. Huber, J.A. Fiedler, and R. L. Miller (1991), The Magnitude of and an Explanation/Solution for the Number of Levels E.ffect in Conjoint Analysis, Working Paper, Comell University.

Wittink, Dick R. and Philippe Cattin (1989), "Commercial Use of Conjoint Analysis: An Update," Journal ofMarketing, 53 (July), 91-96.

Wittink, Dick R., David J. Reibstein, William Boulding, John E.G. Bateson, and John W. Walsh (1989), "ConjointReliability Measures," Marketing Science, 8 (Fall), 371-374.

Woodroof, Jon (2000), "Bootstrapping: As Easy As 1-2-3," Journal of Applied Statistics, 27 (May), 509-517.

Wyner, Gordon A. (1996), "Trade-off Techuiques and Marketing Issues," Marketing Research, 7 (Fall/Winter), 32-34.

Zweig, Phillip L., Judy P. Kline, Stephanie A. Forest, and Kevin Gudridge (1995), "The Case Against Mergers," Business Week, October 30, 1995, 122-130.

Zwerina, Klaus (1997), Discrete Choice Experiments in Marketing, Heidelberg!Germany: Physica-V erlag.

References 177

References used for analysis of motives of real-world M&As ( chapter 3):1

Case 1: Unilever - Bestfoods

Business Wire, "Bestfoods Executives Appointed to Top Positions in Unilever's New Foods Division," October 2, 2000.

Business Wire, "Bestfoods Rejects Unsolicited Unilever Proposal," May 2, 2000.

Business Wire, "Unilever and Bestfoods Sign Definitive Merger Agreement for Acquisition of Bestfoods at $73 Per Share; Creates Pre-eminent Global Food and Consumer Goods Company," June 6, 2000.

Case 2: Kraft Foods- Nabisco

Business Wire, "Philip Morris Acquires Nabisco for $55.00 per Share in Cash and Plans for IPO of.Kraft," June 25, 2000.

Business Wire, "Philip Morris Acquisition of Nabisco Approved by U.S. Federal Trade Commission," December 7, 2000.

Business Wire, "Philip Morris Executives Address Morgan Stanley Dean Witter Global Consumer Conference," November 8, 2000.

Dow Jones News Service, "Kraft to Integrate Nabisco Operations into Kraft Foods," December 7, 2000.

Case 3: PepsiCo- Quaker Oats

Associated Press Newswires, "Pepsi Deal Crowns Quaker's Recovery From Snapple Debacle," December4, 2000.

Byrnes, Nanette, "Steven Reinemund: Pepsi's New Generation, Business Week, December 8, 2000,68.

Cappelli, Peter and Harbir Singh, "M&A Mania: Do Soda and Oatmeal Mix?," The Wall Street Journal Europe, December 6, 2000, 9.

Eisenberg, Daniel, "A New-Age Drink War Starts as Soda Flops Pepsi's Purehase ofGatorade and SoBe Takes the Marketing Battle With Coke to a Hot New Segment," Time Magazine, December 18, 2000, 62.

McKay, Betsy, "After Quaker, PepsiCo's Nooyi to Add Top Job," The WallStreet Journal, December 5, 2000, Bl.

1 The short headers of the cases, for instance Unilever -Bestfoods for case 1, state the acquirer first and the target second.

178 References

N.N., "Leaving Drinks: Pepsi Bags Quaker: In acqumng Quaker, Pepsi Has Won an Important Battle in Its War With Coca-Cola," The Economist, December 9, 2000, 54.

Reuters English News Service, "U.S.A: Gatorade Boosts Pepsi's Vaunted Supermarket Arsenal," December 4, 2000.

Case 4: General Mills- Pillsbury

Knight-Ridder Tribune Business News, "Hefty Price for Pillsbury May Trim General Mills Earnings Per Share," July 18, 2000.

PR Newswire, "General Mills and Diageo to Combine Their Worldwide Consumer Foods Operations," July 17,2000.

Case 5: Kellogg- Keebler Foods

PR Newswire, "Definitive Agreements Signed for Sale of Keebler to Kellogg and Spin-Off of Flowers Foods," October 26, 2000.

PR Newswire, "Kellogg Discusses Growth Plans, Keebler Acquisition, Restructuring Charge, and Earnings Outlook," November 28, 2000.

PR Newswire, "Kellogg to Acquire Keebler," October 26, 2000.

Cases 6 and 7: Tyson Foods- illP and Smithfield Foods- illP

Associated Press Newswires, "Farmers, Politicians Mull Possible IBP-Smithfield Consolidation," November 14,2000.

Associated Press Newswires, "Senators Want Review of IBP-Smithfield Merger," November 17,2000.

Associated Press Newswires, "Some Skeptical About Proposed Smithfield-IBP; Smithfield Defends Plan," November 26, 2000.

Barker, Robert, "Just Who Are the Piggies here?," Business Week, December 18, 2000, 242.

Business Wire, "Tyson Foods Speeds Up Bid Process for IBP, Inc. With Hart-Scott-Rodino Filing and Investor Outreach," December 14, 2000.

Dow Jones News Service, "Brandes: Pleased Tyson Bid Nearing IBP's Fair Value," December 4, 2000.

Kilman, Scott and Nikhil Deogun (2000), "Tyson Makes a Move for Meat-Packer lBP-Top U.S. Chicken Company Would Pay $2.8 Billion to Best Smithfield Offer," The Wall Street Journal, December 5, 2000, A3.

References 179

PR Newswire, "Response of Tyson Foods, Inc. to Statement by Smithfield Foods, Inc.," December 4, 2000.

PR Newswire, "Smithfield Issues Statement in Response to Tyson Bid for IBP," December 4, 2000.

Case 8: PepsiCo- Tropicana

Associated Press Newswires, "Pepsi Buys Tropicana Orange Juice Company for $3.3 Billion," July 20, 1998.

Light, Lany, "Tropicana: A Way for Pepsi to Squeeze Coke," Business Week, August 3, 1998,78.

PR Newswire, "PepsiCo to Acquire Tropicana, World Leader in Branded Juices, From Seagram," July 20, 1998.

Case 9: ConAgra- International Horne Foods

PR Newswire, "ConAgra, Inc. Reports Completion of International Horne Foods Acquisition," August 24, 2000.

PR Newswire, "ConAgra to Acquire International Horne Foods in $2.9 Billion Deal," June 23,2000.

Cases 10 and 29: Unilever- Slim-Fast and Unilever-Ben & Jerry's Hornemade

Associated Press Newswires, "Ben & Jerry's, Slim-Fast to Be Acquired by Multinational Unilever," Aprill2, 2000.

Branch, Shelly and Ernest Beck (2000), "For Unilever, It's Sweetness and Light-Company Buys Ben & Jerry's, Famed Ice-Cream Maker, and Slirn-Fast on Same Day," The Wall Street Journal, Aprill3,2000, BI.

N.N., "Ben & Jerry's and Slirn-Fast in Unilever's Cart Deal: Conglomerate Will Pay $326 Million for the Ice-Cream Maker and $2.3 billion for the Weight-loss Products Company," Los Angeles Times, April13, 2000, Cl.

Cases lla and 12: Danone (through Finalrealm) and Nabisco (through Burlington Biscuits)- United Biscuits

Alm, Richard, "Hicks Muse Happy With UK Deal," The Da/las Morning News, March 1, 2000, IOD.

Alm, Richard, "Hicks Muse May Try again for Snack Firm," The Dallas Morning News, January 8, 2000, 1F.

180 References

Associated Press Newswires, "United Biscuits Backs Finalrealm Bid, Rival Group Reviews Options," December 17, 1999.

Beck, Emest, "Fight for United Biscuits Grows After Bid by Danone-led Group," The Wall Street Journal Europe, December 20, 1999, 3.

Beck, Emest, "United Biscuits Receives New Bid From Finalrealm," The WallStreet Journal Europe, December 17, 1999,3.

Beck, Emest and Emily Nelson, "Bid by Nabisco, Hicks MuseIs Topped in Duel for Britain's United Biscuits," The WallStreet Journal, December 17, 1999, B2.

Dow Jones Business News, "Burlington Biscuits Posts Offer Document for United Biscuits," Janruuy 11,2000.

Dow Jones Business News, "United Biscuits Prefers Finalrealm Bid Over Hicks MuseNabisee Offer," January 13, 2000.

Les Echos, "United Biscuits: Danone Raises Its Offer, But Nabisco Increases Its Stake (United Biscuits: Danone releve son offie mais Nabisco rarnasse des titres)," December 17, 1999,21.

Les Echos, "United Biscuits: Final Match between Danone and Nabisco Set for End of February 2000 (United Biscuits : Je matchfinal entre Danone et Nabisco est pour Ia fin du mois)," February 14, 2000, 14.

Murray-West, Rosie, "United Biscuits Recommends Bid From Finalrealm," The Daily Telegraph, December 18, 1999.

Case 13: Cadbury Schweppes- Snapple Beverages

ßusiness Wire, "Triarc Completes Sale of Snapple Beverage Group to Cadbury Schweppes," October 25, 2000.

Business Wire, "Triarc to Seil Snapple Beverage Group to Cadbury Schweppes; Enterprise Value of$1.45 Billion," September 18,2000.

PR Newswire, "Cadbury Schweppes to Acquire Snapple Beverage Group For an Euterprise Value of$1.45 Billion," September 18,2000.

PR Newswire, "Initial Phase of Snapple Beverage Group Integration With Cadbury Schweppes Under Way," November 8, 2000.

Case 14: Foster Brewing Group- Beringer Wine Estates

Business Wire, "Beringer Wine Estates to be Acquired by Foster's Brewing Group of Australia," August 28, 2000.

References 181

Evans, Simon, "Upside in Foster's Beringer Buy Despite Share Slip," Australian Financial Review, September 20,2000, 16.

Case 15: Coca-Cola- Cadbury Schweppes (Soft Drinks)

Dow Jones International News, "Cadbury/Coca-Cola -2: Dr. Pepper, Canada Dry, Crush Brands," December 11, 1998.

Dow Jones International News, "Cadbury/Coca-Cola -3: To Seil Non-U.S. Bottling Activities," Decernber 11, 1998.

Dow Jones Online News, "U.K. Investors Applaud Cadbury's Coca-Cola Bottling Contract," Janmuy 15, 1998.

PR Newswire, "The Coca-Cola Company and Cadbury Schweppes Announce $1.85 Billion Transaction for Cadbury Schweppes Beverage Brands," Decernber 11, 1998.

Case 16: Danone- Mc Kesson Water Products

Dow Jones Business News, "Danone To Acquire McKesson's Bottled-Water Unit For $1.1 Billion," January 11, 2000.

Kamm, Thomas (2000), "French Danone Agrees to Buy Water Unit of McKesson," The WallStreet Journal, January 12, 2000, A16.

PR Newswire, "Groupe Danone to Acquire McKesson Water; Becomes Second Largest U.S. Packaged WaterCompany," January 11,2000.

Case 17: Bestfoods- Arisco

Business Wire, "Bestfoods in Final Negotiations With Brazilian Food Company; Bestfoods' Brazilian BusinesstoBe Doubled," February 7, 2000.

Dow Jones News Service, "Bestfoods Says in Final Stages of Negotiations for Arisco," February 7, 2000.

Case 18: Earthgrains- Metz Baking (Specialty Foods)

Associated Press Newswires, "Earthgrains Agrees to Buy Metz Baking Co.," November 16, 1999.

Deogun, Nikhil, "Earthgrains Agrees to Buy Metz Baking From Specialty Foods for $625 Million," The WallStreet Journal, November 15, 1999, A4.

PR Newswire, "The Earthgrains Company Announces Agreement to Buy Metz Baking Co.," November 15, 1999.

182 References

Case 19: ffiP- Corporate Brand Foods America

Business Wire, "IBP Completes CBFA Transaction," February 8, 2000.

Business Wire, "IBP, Inc. to Acquire Corporate Brand F oods America," December 21, 1999.

Kilman, Scott (1999), "lBP to Buy Corporate Brand Foods in $585 Million Stock-and-Debt Deal," The WallStreet Journal Europe, December 22, 1999, 7.

Case 20: Nabisco- Favorite Brands International

Branch, Shelly, "Nabisco Holdings Plans to Purehase Favorite Brands in $475 Million Deal," The WallStreet Journal, September 30, 1999, A10.

Dow Jones News Service, "Nabisco To Close Favorite Brands Headquarters," January 13, 2000.

Case 21: Keebler Foods- President Baking

Balu, Rekha (1998), "Keebler to Acquire President Baking For $450 Million," The Wall Street Journal, August 25, 1998, B2.

Bonsor, Kevin and Darnon Cline, "Analyst: Keebler Foods Buyout to Have Little Impact on Augusta/Ga., Bakery," The Augusta Chronicle, August 26, 1998.

Business Wire, "Keebler Completes Acquisition of President Baking Company; Hollow Tree Officially Adds New Branch," September 28, 1998.

Business Wire, "Keebler to Acquire President Baking Company," August 24, 1998.

PR Newswire, "Keebler Foods Company Announces New Appointments Following the Purehase ofFresident Baking Company," November 3, 1998.

Case 22: New World Pasta- Hershey Foods (Pasta)

Dochat, Tom, "Pasta Guru Ends Retirement toReturn to Full Plate," February 28, 1999, The Patriot-News, 9.

Dow Jones Business News, "Hershey to Sell Pasta Business to Investment Group for $450 Million," December 15, 1998.

PR Newswire, "Hershey Foods Announces Agreement to Sell U.S. Pasta Business," December 15, 1998.

References 183

Case 23: Ralcorp- Agribrands International

Associated Press Newswires, "Ralcorp, Agribrands to Merge," August 8, 2000.

Deogun, Nikhil and Scott Kilman, "Cargill Has Deal to Acquire Agribrands After Cutting in on Ralcorp's Offer," The WallStreet Journal, December 4, 2000, A4.

Dow Jones Business News, "Former Ralston Purina Units Ralcorp, Agribrands Agree to Merge," August 8, 2000.

Federal Filings Newswires, "FFBN Histocy of the Deal: Agribrands International/Ralcorp," September 29, 2000.

Case 24: ConAgra- Nabisco (Egg Beaters)

PR Newswire, "ConAgra Acquires Egg Beaters and Nabisco Tablespreads Businesses," August 17, 1998.

PR Newswire, "ConAgra Agrees to Buy Egg Beaters and Nabisco Tablespreads Businesses," July 21, 1998.

Case 25: Agrilink Foods- Dean Foods Vegetable

Associated Press Newswires, "Dean Foods to Sell Vegetable Operations to Agrilink," July 28, 1998.

Balu, Rekha, "Dean Agrees to Seil Vegetable Division to Pro-Fac Unit," The Wall Street Journal, July 28, 1998, A6.

Dow Jones News Service, "Dean Foods/Agrilink -2: Vegetable Operations Had '98 Revenues of$553fl.1," July 27, 1998.

Case 26: Hain Food Group- Celestial Seasonings

Dow Jones News Service, "Hain Food, Celestial Seasonings Holders Ok Merger" May 30, 2000.

N.N., "Celestial Seasonings, Hain Food Group Gets Clearance for Purchase," The WallStreet Journal, May 31,2000, C25.

PR Newswire, "The Hain Food Group and Celestial Seasonings Cornplete MergerCombined Company Named the Hain Celestial Group," May 30,2000.

PR Newswire, "The Hain Food Group to Merge With Celestial Seasonings, Inc., the Market Leader in Specialty Teas," March 6, 2000.

184 References

Case 27: ConAgra- Seaboard

PR Newswire, "ConAgra Agrees to Buy Seaboard's Poultry Division," December 6, 1999.

Case 28: PepsiCo- South Beach Beverage

Associated Press Newswires, "PepsiCo Buying Maker of Soße Beverages," October 30, 2000.

Business Wire, "Leapin' Lizards! PepsiCo Agrees to Acquire South Beach Beverage Co.," October 30,2000.

Jenkins, Holman W., "Business World: Big Cola Goes Back to Its Patent-Medicine Roots," The WallStreet Journal, November 8, 2000, A27.

McKay, Betsy, "Juiced Up: Pepsi Edges past Coke, and It Has Nothing to Do With Cola -The Company now Capitalizes on a Growing Thirst for Drinks Without Fizz- Tropicana's Vitamin Punch," The WallStreet Journal, November 6, 2000, Al.

Winter, Greg, "Pepsico Buys a 90% Stake in South Beach Beverage," The New York Times, October 31,2000, 2.

Cases El and E2: Diageo and Pernod- Seagram

Baker, Lucy, "Seagram Swallowed by Diageo and Pernod Ricard for Pounds 5.6bn," The Independent, December 20, 2000, 14.

Deogun, Nikhil and Emest Beck, "Management to Bid for Seagram Unit-Team to Compete With Diageo-Pemod Alliance-Vivendi's Auction ofSpirits Business Shapes up as Hotly Competitive," The WallStreet Journal Europe, August 21,2000, 1.