High force catch bond mechanism of bacterial ... - unibas.ch

advisory

M&A Yearbook 2011 EditionKPMG’s overview of mergers and

acquisitions in switzerland in 2010

Caveat

This study is based on the University of St. Gallen’s M&A DATABASE and KPMG desktop research, focusing on deals announced in 2010 but also providing historical data drawn from previous editions of the Yearbook. The consideration of individual transactions and their allocation to specific industry segments are based on our judgment and are thus subjective. We have not been able to extensively verify all data and cannot be held responsible for the absolute accuracy and completeness thereof. Analysis of different data sources and data sets may yield deviating results. Historical data may differ from earlier editions of this Yearbook as databases are updated retroactively for lapsed deals or for transactions that were not made public at that given time; we have also aligned some of the selection parameters and industry segmentation more closely to those applied by the M&A DATABASE, which can also lead to differences in historical data representation. The following notes pertain to data contained in this M&A Yearbook:

• Deals are included where the deal value is equal to or greater than the equivalent of USD 7 million

• Value data provided in the various charts represents the aggregate value of the deals for which a value was stated. Please note that values are disclosed for approximately 50% of all deals

• Where no deal value was disclosed, deals are included if the turnover of the target is equal to or greater than the equivalent of USD 14 million

• Deals are included where a stake of greater than 30% has been acquired in the target. If the stake acquired is less than 30%, the deal is included if the value is equal to or exceeds the equivalent of USD 140 million

• Deals are included in their respective industry sections based on the industry of the target business

• All deals included have been announced but may not necessarily have closed

• Activities excluded from the data include restructurings where ultimate shareholders’ interests are not affected

The M&A REVIEW and the M&A DATABASE are two valuable sources of merger & acquisition information from the Institute of Management at the University of St. Gallen.

The M&A REVIEW is a professional monthly journal founded in 1990 by Prof. Günter Müller-Stewens and deals with company takeovers and mergers, divestments and strategic alliances in Germany, Austria and Switzerland. The M&A REVIEW has two parts. The first part contains articles from M&A experts. These articles cover a wide range of M&A topics such as Strategy & Visions, Law & Taxes, Valuation & Capital Markets and Industry Specials. In addition, reviews of M&A developments in Switzerland, Austria and worldwide appear regularly. The second part of the M&A REVIEW systematically tracks M&A transactions in 18 sectors, from Energy to Automotive and from Financial Services to Media. The transactions are summarized by sector experts of the University of St. Gallen.

The M&A DATABASE contains more than 70,000 transactions in Germany, Austria and Switzerland since 1985. For each deal data about the buyer, the seller and the target (such as sales and number of employees) is recorded. Additional data about the transactions (size of the investment, purchase price, direction of the transaction, type) is provided. For a better analysis and for the building of sector statistics the University of St. Gallen uses an own industry code parallel to the NACE code. Sources of the M&A DATABASE are press reports, which are screened and entered into the database on a daily basis. Contacts with financial investors and companies allow the database to be completed.

Impressumdesigned and produced by KPMG aG, switzerlandPublication name: M&a yearbook – 2011 EditionPublication date: January 2011order number: [email protected]

M&a yearbook – 2011 Edition | 3

Contents

M&A Yearbook – 2011 EditionKPMG’s overview of mergers & acquisitions in switzerland in 2010

Overview Page Number

1 introduction 4

2 deal Trends / Executive summary 5

Industries

3 Healthcare & Life sciences 10

4 Chemicals & Processing Materials 12

5 Financial services 14

6 industrial Markets 16

7 Consumer Markets 18

8 information, Communication & Entertainment 20

9 other industries 22

Other Aspects

10 Private Equity 24

11 real Estate 26

12 Legislative & regulatory aspects 27

Appendix

13 List of 2010 swiss M&a Transactions 28

Impressumdesigned and produced by KPMG aG, switzerlandPublication name: M&a yearbook – 2011 EditionPublication date: January 2011order number: [email protected]

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2011 KPMG Holding aG/sa, a swiss corporation, is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG international Cooperative (“KPMG international”), a swiss legal entity. all rights reserved. Printed in switzerland. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG international.

4 | M&a yearbook – 2011 Edition

Largely well funded and optimistic about market prospects, swiss industry has emerged from the economic downturn in generally better shape than many of its European counterparts. Boardroom agendas are turning back to talk of sustainable growth and many swiss businesses are in prime position to seize opportunities as they arise. While M&a levels in 2010 remained subdued, there are clear signs of increasing activity, boding well for deal activity in 2011. in the global race for growth, the starting blocks are filling up fast with competitors awaiting the right signals to start.

This fifth edition of KPMG’s annual review of mergers & acquisitions in switzerland is the first to report on a full calendar year following the 2008-2009 economic crisis. Highlighting some of the significant opportunities and the challenges facing the swiss business community as it refocuses on growth, we comment on the trends that have shaped the M&a landscape in 2010 as well as the prospects for 2011. We note which industries appear ripe for consolidation, and where many key players spent 2010 transitioning into acquisition mode.

Following a couple of years when many businesses put their M&a plans on ice, both buyers and sellers are now eagerly awaiting the bang from the starting pistol. The trigger may depend chiefly on when prospective vendors consider conditions to be most conducive to bringing their assets to market.

We believe 2011 will see a significant upturn in M&a activity across almost all sectors in switzerland, with deals being driven by swiss-based businesses rather than foreign investors. Whether or not the year will herald the start of a new wave of mega-deals among the industry giants remains to be seen, but it is a distinct possibility in certain key sectors.

We hope you find our latest yearbook interesting and insightful.

stefan PfisterPartner, Head of Transactions & restructuring, switzerland

1 Introduction

Stefan Pfister T: +41 44 249 26 67E: [email protected]

M&a yearbook – 2011 Edition | 5

Following particularly difficult years in 2008 and 2009, swiss businesses appear to be in an increasingly positive mood. Encouraged by healthier balance sheets and rising confidence in market prospects, and with some significant restructuring and rationalisation programmes behind them, boardroom agendas are again becoming dominated by growth. deal volumes stabilised in 2010, representing an improvement over the steady decline witnessed since 2007. reinvigorated buy-side interest was observed in late 2010, which should combine with progressively easier access to financing to translate into more announced deals in the first part of 2011 and a general upturn in the number of transactions over the coming year.

Finger on the triggerNo matter how ready they might be for the growth race, however, many potential acquirers are frustrated by a lack of available targets. The starter pistol is being controlled to a great extent by prospective vendors, many of whom are struggling to determine the right time to put their assets up for sale. Many are awaiting full year 2010 financial information prior to initiating a sale process on the basis that these figures should demonstrate enhanced performance since the economic downturn, providing a more attractive foundation for the business plan and purchase price. indeed, a major challenge to date has been dealing with the hockey stick effect, with even credible business plans running the risk of looking over-ambitious given the historical dip out of which they are growing.

Private Equity: a strong contender?The Private Equity community may help fuel an M&a recovery on both the supply and demand sides. Many Private Equity houses are sitting on significant funds that they were unable to invest during the downturn due to a lack of attractive opportunities. They are now coming under pressure to demonstrate activity in order to raise future funds, although on the whole new funding is not scarce.

on the supply side, many funds delayed exits due to the economic uncertainty and a generally unfavourable iPo environment. 2011 may see managers looking to realise these investments and show positive returns to investors. This will help bring assets to market which may be of particular interest to corporate bidders or as secondary buyouts if there appears to be potential for further operational improvements.

Looking abroadThis year is likely to present swiss players with a number of interesting opportunities abroad as prices in some regions remain depressed and many foreign groups continue to struggle. such groups may divest business units in order to raise capital and/or to focus on core activities, representing potential for relatively healthy swiss investors. This may be the case particularly in neighbouring countries such as Germany and France, where sizeable mid-markets may be looking at succession issues. in addition to industrial and Consumer manufacturing, sectors such as Chemicals and real Estate may be the ones to watch.

The strong swiss Franc may help swiss-based companies in this regard, though at the same time it continues to hinder sales from the export-led swiss industries. similarly, the currency’s strength is likely to curtail foreign interest in swiss acquisition targets despite the attractiveness of switzerland’s stability, production technology and generally high labour and product qualities.

2 Deal Trends / Executive Summary

Patrik Kerler T: +41 44 249 33 20E: [email protected]

6 | M&a yearbook – 2011 Edition

Return of the mega-deal?Mega-deals were few and far between in 2010 but there are some significant deals out there to be done. The largest transaction in the year was Novartis completing its acquisition of the remaining 75% of alcon shares from Nestlé for Usd 41.2 billion. This represents a significant lead over the second largest deal, being aBB’s acquisition of the Usa’s Baldor Electric Company for Usd 4.2 billion.

The upper end of the market may see further non-core divestments, for instance in Financial services. However, across the board supply is likely to be dominated by small and medium-sized deals, partly fuelled by family-owned businesses looking at succession planning, having been deterred from selling until there are clear signs of an economic recovery.

Healthy prospectssome caution over global macro-economic conditions persists, with a particular eye on what happens to troubled economies within the Eurozone such as ireland, spain, Portugal and Greece, which have the potential to knock business confidence. This may result in M&a activity growing at a more modest pace than otherwise might be expected, at least in the first half of 2011. some export-led industries may continue to suffer due to the strong swiss Franc, which is also deterring inbound acquisition activity into switzerland.

despite such concerns, swiss businesses are generally keen to take to the field and resume M&a activity and are well positioned to do so. The race is on to acquire the best assets, with plenty of competitors ready to chase deals in 2011. The question appears to be not ‘will the race begin?’ but ‘who will be the strongest contenders?’ and ‘which player will get off to the best start?’ if favourable conditions persist, there may be more than one winner.

Patrik KerlerPartner, Head of Mergers & acquisitions

M&a yearbook – 2011 Edition | 7

industry snapshots for 2011

Financially robust Pharmaceutical players are expected to lead M&a activity in the Healthcare & Life Sciences sector in 2011. some smaller deals are likely in Medical Technology and Healthcare service provision, both of which are attracting much interest from investors.

swiss Chemicals groups appear to be in particularly confident mood following a period of reorganisation, and there could be some interesting opportunities for swiss groups abroad. activity is likely to concentrate on building a presence in key regional markets such as asia and in enhancing product portfolios.

one of the sectors hit hardest by the economic downturn, Financial Services is likely to see significant consolidation in Private Banking, where new regulations are prompting fundamental revisions of business and operating models, including on-shore presence. Elsewhere in Financial services more clarity over regulation such as Basel iii should encourage activity.

Export-led Industrial Markets are especially suffering from the strong swiss Franc but cautious optimism prevails as late 2010 saw a significant upturn in order book levels. M&a in 2011 may be modest compared to some other sectors, but global competitive pressures may combine to encourage transformational deals and/or acquisitions along the supply chain.

2011-2012 may see further consolidation within the Consumer Markets sector and some major non-core disposals by the Food & drink giants, which are likely also to remain in highly acquisitive mode. Luxury Goods manufacturers may seek to steal the Consumer Markets M&a crown as they search for potentially large deals outside switzerland.

Technology deals are expected to continue to dominate Information, Communication and Entertainment as many players across industries seek to enhance their capabilities in iT and software solutions, which are increasingly critical to their businesses. a shuffling of Media portfolios is likely to occur as well as a strengthening of the swiss presence in Eastern Europe, but no groundbreaking deals are expected.

The focus on high-grade Real Estate around Geneva, Lausanne, Zurich and Central switzerland is almost certain to continue for the foreseeable future, with prices remaining accordingly high. 2011 may see key players investigating further opportunities in development projects while the residential market continues to boom.

Not to be under-estimated, other industries such as Energy (primarily renewables) and Commodities are likely to see significant M&a activity in 2011 as interest in the swiss scene may continue to grow, with 2010 having seen some major energy traders relocate sizeable teams to Geneva.

8 | M&a yearbook – 2011 Edition

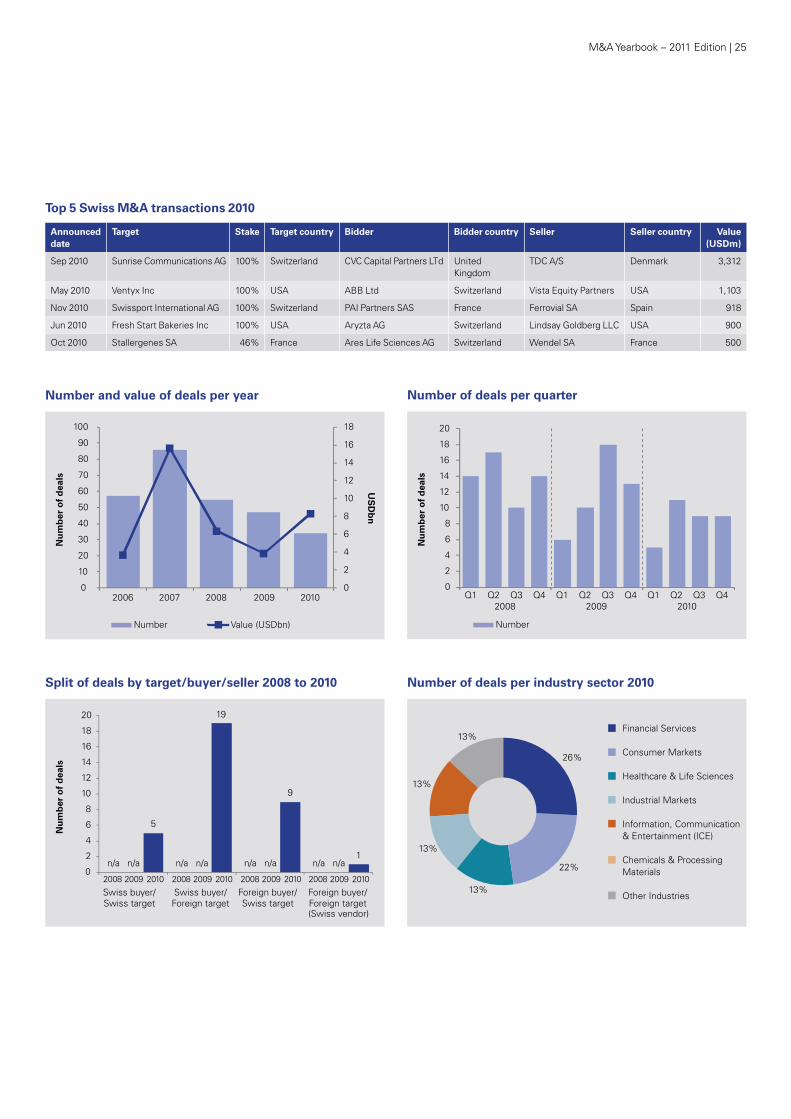

Top 10 Swiss M&A transactions 2010

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

Jan/dec 2010 alcon inc 52%/23% Usa Novartis aG switzerland Nestlé sa switzerland 41,200

Nov 2010 Baldor Electric Co 100% Usa aBB Ltd switzerland 4,188

Jan 2010 Kraft Foods inc (frozen pizza)

100% Usa Nestle sa switzerland Kraft Foods, inc Usa 3,700

sep 2010 sunrise Communications aG 100% switzerland CvC Capital Partners Ltd United Kingdom

TdC a/s denmark 3,312

Mar 2010 Prodeco Mine 100% Colombia Glencore international aG switzerland Xstrata Plc switzerland 2,500

Jun 2010 Fdr Holdings Ltd 100% Usa Noble Corp switzerland 2,160

Feb 2010 Numonyx Bv 100% switzerland Micron Technology inc Usa intel Corp Usa 1,284

Jul 2010 adC Telecommunications inc 100% Usa Tyco Electronics switzerland 1,258

May 2010 ventyx inc 100% Usa aBB Ltd switzerland vista Equity Partners

Usa 1,103

sep 2010 rain and Hail insurance service inc

80% Usa aCE Limited switzerland 1,100

Number and value of deals per year

Number Value (USDbn)

US

Db

n

Nu

mb

er o

f d

eals

0

10

20

30

40

50

60

70

80

90

100

0

50

100

150

200

250

300

350

400

2006 2007 2008 2009 2010

Number and value of deals per quarter

US

Db

n

Nu

mb

er o

f d

eals

Number Value (USDbn)

0

5

10

15

20

25

30

35

40

45

50

0

10

20

30

40

50

60

70

80

90

100

Q1 Q2 Q3 2008

Q4 Q1 Q2 Q3 2009

Q4 Q1 Q2 Q3 2010

Q4

M&a yearbook – 2011 Edition | 9

Number of deals per industry sector 2010

11%

10%

6%

18%

17%

11%

27%

Industrial Markets

Consumer Markets

Healthcare & Life Sciences

Information, Communication & Entertainment (ICE)

Financial Services

Chemicals & Processing Materials

Other Industries

Number of targets of Swiss acquirers by region 2010

Switzerland

Western Europe

North America

Asia-Pacific

Central/Eastern Europe

South America

Middle East/Africa

36%

32%

12%

11%

4%4% 1%

>1 billion

501 million – 1 billion

251 million – 500 million

51 million – 250 million

<50 million

not disclosed

Volume by deal size 2010 (USD)

Nu

mb

er o

f d

eals

0

50

100

150

200

250

300

350

400

2006 2007 2008 2009 2010

329356

320

274262

Split of deals by target/buyer/seller 2008 to 2010

Nu

mb

er o

f d

eals

2008 2009 2010 2008 2009 2010 2008 2009 2010 2008 2009 20100

20

40

6269

147

102

124

73

52 56

3849

13

73

60

80

100

120

140

160

Swiss buyer/ Swiss target

Swiss buyer/ Foreign target

Foreign buyer/ Swiss target

Foreign buyer/ Foreign target (Swiss vendor)

Number of foreign acquirers by region 2010

Western Europe

North America

Asia-Pacific

Central/Eastern Europe

South America

Middle East

67%

22%

5%4% 2%

10 | M&a yearbook – 2011 Edition

The Healthcare industry is approaching a major crossroads. Ever-increasing demand for its products and services is arising from inter alia ageing populations, a rise in obesity and growing purchasing power in less developed nations. However, a large question mark exists over who pays for care – a particularly pertinent issue in the current environment of shrinking government expenditure. in the short term, expiring patents on some blockbuster drugs also pose a threat to future revenues and margins, particularly for those companies with weaker development pipelines or a less diversified revenue base.

despite being dominated by smaller deals, 2010 was punctuated by a couple of major transactions such as Novartis’s Usd 41.2 billion acquisition of the remaining 75% stake in alcon, and Galderma’s Usd 983 million acquisition of Q-MEd. There had been some expectation that 2010 would see a surge of mega-deals. While this did not occur, the relatively unconsolidated state of the sector points towards the possibility of a wave of major transactions in the short to medium-term. The only question appears to be when this will take place, and the extent to which it will gather pace in 2011.

With steady cash flows, the Pharmaceutical sector has been one of the more financially robust sectors through the downturn and has continued to pursue transactions. There appears to be a steady supply of potential acquisition targets, however there is concern around the multiples being commanded and the extent to which it is possible to deliver positive long-term returns on investment.

Biotech has fallen out of favour as a result of the financial crisis, with investors deterred by the scale of investment, high failure rate and lead times in bringing products to market. although classic M&a may remain important in the Biotech field, it is expected that other forms of tie-ups such as partnerships or alliances with larger Pharmaceutical businesses will become more commonplace. such strategies create a potentially powerful proposition between the greater resources and financial firepower of the Pharmaceutical industry and the higher levels of innovation (particularly in more niche specialist drugs) typical of smaller Biotech firms. From the Pharmaceutical perspective this can also represent a more cost-effective and less risky investment than undertaking an acquisition. Many investors are also expressing a preference for Medical Technology investments, which by contrast tend to have lower investment requirements and shorter lead times than Biotech.

Outlook for 20112011 is likely to see continued investment in the providers of Healthcare services within switzerland, although the same question of who pays for the increasing need for care applies. specific to switzerland, the impact of the introduction of the swiss diagnosis related Groups (drG) legislation in 2012 (the national standardisation of hospital tariffs) is still uncertain and may impact the margins Healthcare providers enjoy.

Joshua Martindirector, Transaction services

2010 yielded only a handful of major Healthcare & Life sciences transactions. However, the drivers towards further industry consolidation remain strong and 2011 may well see some larger deals in this relatively unconsolidated sector, particularly among the Pharmaceutical players. Medical technology, generic drug manufacturers and healthcare providers may all represent interesting, albeit smaller, acquisition opportunities

3 Healthcare & Life Sciences

Joshua Martin T: +41 44 249 23 85E: [email protected]

M&a yearbook – 2011 Edition | 11

Top 5 Swiss M&A transactions 2010

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

Jan/dec 2010 alcon inc 52%/23% Usa Novartis aG switzerland Nestlé sa switzerland 41,200

dec 2010 Q-MEd aB 100% sweden Galderma Pharma sa switzerland 983

Feb 2010 Lelystad Biologicals Bv 100% Netherlands Prionics aG switzerland 590

Jul 2010 TargeGen inc 100% Usa sanofi-aventis Group France Consortium of investors switzerland 587

Jan 2010 Mepha aG 100% switzerland Cephalon inc Usa Merckle Germany 560

Number of deals per industry subsector 2010

17%

42%

24%

17%

Pharmaceuticals

Clinical research/laboratories

Biotech

Other

Number and value of deals per year

Number Value (USDbn)

US

Db

n

Nu

mb

er o

f d

eals

2006 2007 2008 2009 20100

10

20

30

40

50

60

0

5

10

15

20

25

30

35

40

45

Number of deals per quarter

Nu

mb

er o

f d

eals

Number

Q1 Q2 2008

Q3 Q4 Q1 Q2 2009

Q3 Q4 Q1 Q2 2010

Q3 Q4 0

2

4

6

8

10

12

Split of deals by target/buyer/seller 2008 to 2010

Nu

mb

er o

f d

eals

2008 2009 2010 2008 2009 2010 2008 2009 2010 2008 2009 2010

1

16

4

1

5

16

4 3

5

10

12

2

0

2

4

6

8

10

12

14

16

18

Swiss buyer/ Swiss target

Swiss buyer/ Foreign target

Foreign buyer/ Swiss target

Foreign buyer/ Foreign target (Swiss vendor)

12 | M&a yearbook – 2011 Edition

The swiss Chemicals industry is facing increasing competition from the Middle East and asia and an increase in regional demand is driving the growth of domestic Chemicals companies.

The larger swiss Chemicals groups such as Clariant have invested much effort and resource in positioning themselves for the post-economic crisis period, with initial indications being that these efforts have paid off. improved earnings, enhanced working capital management and an evidently successful reorganisation of production facilities worldwide are placing them in a much stronger position than one year ago.

This focus on realignment and stabilising the core business may explain the relative lack of acquisition activity in this sector over the course of 2010. However, boardroom agendas are now turning back to the subject of growth as a number of market participants are performing well.

While deal values in 2010 were relatively modest, the year is notable for having seen particular activity in the fertiliser business. The largest and fifth largest deals of the year were an inbound and an outbound deal respectively, the first being the acquisition of a stake in Balderton Fertilisers by Norway’s yara international, and the other being ameropa’s purchase of a stake in the australian impact Fertilisers.

Many major players such as syngenta and sika have fixed an eye on bolt-on acquisitions that will place them in prime position to generate future growth. Both have done deals which focused on penetrating key territories and enhancing product portfolios.

Outlook for 2011While it is unlikely that 2011 will see any mega-deals involving swiss businesses, general deal activity is expected to increase over the course of the year.

More generally across the Chemicals sector, bolt-on acquisitions are likely to continue with a focus on key geographies such as india – interest being driven by a desire to establish a regional hub for East and south East asia, leveraging a low-cost base as well as helping to secure raw material supplies. desire may not necessarily translate into success, however, as experience shows significant difficulty in finding acquisition targets in asia that are attractive and available at a reasonable price.

an option for expansion closer to home may be to acquire business units being divested by groups keen to raise funds. opportunities might exist in certain European countries where the sector was hit harder than its swiss counterpart, and where there are a number of groups that may need to make non-core or forced disposals.

Pablo Ljaskowsky Patrick schaubPartner, Transaction services senior Manager, Transaction services

Having weathered the economic storm, swiss Chemicals groups are in confident mood. With restructuring largely having taken place and balance sheets regaining strength, 2011 may herald a new growth period for the sector. strategic acquisitions look set to top the agenda with a continued focus on key geographies and product portfolio enhancement

4 Chemicals & Processing Materials

Pablo Ljaskowsky T: +41 44 249 45 53E: [email protected]

Patrick Schaub T: +41 44 249 25 67E: [email protected]

M&a yearbook – 2011 Edition | 13

Number and value of deals per year

Number Value (USDbn)

US

Db

n

Nu

mb

er o

f d

eals

0

1

2

3

4

5

6

0

5

10

15

20

25

2006 2007 2008 2009 2010

Number of deals per quarterN

um

ber

of

dea

ls

Number

0

1

2

3

4

5

6

Q1 Q2 2008

Q3 Q4 Q1 Q2 2009

Q3 Q4 Q1 Q2 2010

Q3 Q4

Split of deals by target/buyer/seller 2008 to 2010

Nu

mb

er o

f d

eals

2008 2009 2010 2008 2009 2010 2008 2009 2010 2008 2009 2010

Swiss buyer/ Swiss target

Swiss buyer/ Foreign target

Foreign buyer/ Swiss target

Foreign buyer/ Foreign target (Swiss vendor)

0

1

5

3

1 1 1

5

3

8

2 2

0

1

2

3

4

5

6

7

8

9

Number of deals per industry subsector 2010

7%

20%

73%

Industrial chemicals

Agrochems and seeds

Speciality chemicals

Fine chemicals

Top 5 Swiss M&A transactions 2010

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

Jan 2010 Balderton Fertilisers sa 50% switzerland yara international asa Norway 130

May 2010 Maribo seed international aps

100% denmark syngenta aG switzerland 57

dec 2010 vinythai PCL 9% Thailand solvay vinyls Holding aG switzerland Charoen Pokphand Holding Co

Thailand 49

dec 2010 datacolor aG 67% switzerland Werner dubach switzerland 46

May 2010 impact Fertilisers australia Pty Limited; impact Fertilisers Pty Ltd

50% australia ameropa aG switzerland 45

14 | M&a yearbook – 2011 Edition

The low level of M&a activity in 2010 was driven in part by attention being focused on anticipating and adapting to new and upcoming regulation. Whether capital requirements for Banks and insurance companies or legislation fundamentally impacting the Private Banking business model, the evolving regulatory landscape posed serious challenges and uncertainties across the industry.

While outbound deal activity by swiss institutions almost doubled over 2009 from 8 to 15 deals, foreign players seemed to be deterred from making acquisitions in switzerland, with only one such deal in the year.

Banking transactions were primarily sales-driven with a number of crisis-induced deals. Not strictly distressed sales, they were largely born of a need to focus on core activities and / or reinforce the vendor’s capital position.

The Insurance sector was relatively active, particularly towards the end of the year with aCE completing three transactions including the largest deal in the sector being an acquisition in the Usa valued at Usd 1.1 billion. a number of key players have been actively pursuing opportunities. swiss re appears to be positioning itself for growth in the emerging markets, having undertaken acquisitions in both india and Brazil during the course of the year. its sale of a minority stake in atradius may be seen to bolster its financial position to implement further expansion plans.

Tough market conditions, changing client needs and an increasing regulatory burden are eroding margins in the Private Banking sector. a swathe of new regulation and compliance obligations from the swiss Financial Market supervisory authority (FiNMa) and from non-swiss authorities poses significant additional requirements and raises questions over the sustainability of current service propositions and operating models. indeed, regulatory developments may prompt a degree of consolidation in the industry as some players struggle to adapt.

Outlook for 2011This year’s market may be characterised by strategic realignment and the continued disposal of non-core assets. Banks that do have surplus cash reserves may seek opportunities from among those that continue to struggle. Finalisation of Basel iii in december 2010 may however remove some regulatory uncertainty, positively impacting M&a activity in 2011.

Private Banking is likely to be the hottest sector over the year. significant consolidation may combine with some less profitable players seeking to exit the market, to help drive activity. Larger Private Banks are well positioned to make foreign acquisitions as they seek to build on-shore presences and concentrate on expansion in certain key markets. Western Europe remains the highest priority followed by Latin america and East & south East asia.

Christian HintermannPartner, Transactions & restructuring Financial services

although 2010 experienced the lowest level of Financial services M&a activity since 2005, swiss institutions are getting back into shape following a tough couple of years, with a particular rebound in the number of swiss acquisitions abroad. The insurance sector saw the largest deal of the year, and indeed the only deal to exceed Usd 1 billion. 2011 is likely to experience stronger activity in Private Banking as regulatory challenges and business model considerations encourage long-awaited consolidation

5 Financial Services

Christian Hintermann T: +41 44 249 47 66E: [email protected]

M&a yearbook – 2011 Edition | 15

Number of deals per industry subsector 2010

11%

31%

42%

4%

12%

Banking

Insurance

Financial advisory

Investment companies

Other

Top 5 Swiss M&A transactions 2010

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

sep 2010 rain and Hail insurance service inc

80% Usa aCE Limited switzerland 1,100

Jan 2010 atradius Nv 36% Netherlands investor group spain swiss reinsurance Co Ltd; deutsche Bank aG: sal oppenheim jr & Cie sCa

switzerland 759

May 2010 Marble Bar asset Management (MBaM) LLP

100% United Kingdom

switzerland EFG international switzerland 449

oct 2010 New york Life insurance Company (south Korean subsidiary); New york Life insurance Company (Hong Kong subsidiary)

100% south Korea aCE Limited switzerland New york Life insurance Company

Usa 425

oct 2010 New China Life insurance Co Ltd

n/a China Zurich Financial services Group (ZFs)

switzerland New China Life insurance Co Ltd

China 407

Number and value of deals per year

Number Value (USDbn)

US

Db

n

Nu

mb

er o

f d

eals

2006 2007 2008 2009 20100

2

4

6

8

10

12

14

16

18

0

10

20

30

40

50

60

Number of deals per quarter

Nu

mb

er o

f d

eals

Number

Q1 Q2 2008

Q3 Q4 Q1 Q2 2009

Q3 Q4 Q1 Q2 2010

Q3 Q4 0

2

4

6

8

10

12

14

Split of deals by target/buyer/seller 2008 to 2010

Nu

mb

er o

f d

eals

2008 2009 2010 2008 2009 2010 2008 2009 2010 2008 2009 2010

Swiss buyer/ Swiss target

Swiss buyer/ Foreign target

Foreign buyer/ Swiss target

Foreign buyer/ Foreign target (Swiss vendor)

4

21

14

1

11

8 7

10 8

15

1 2

0

5

10

15

20

25

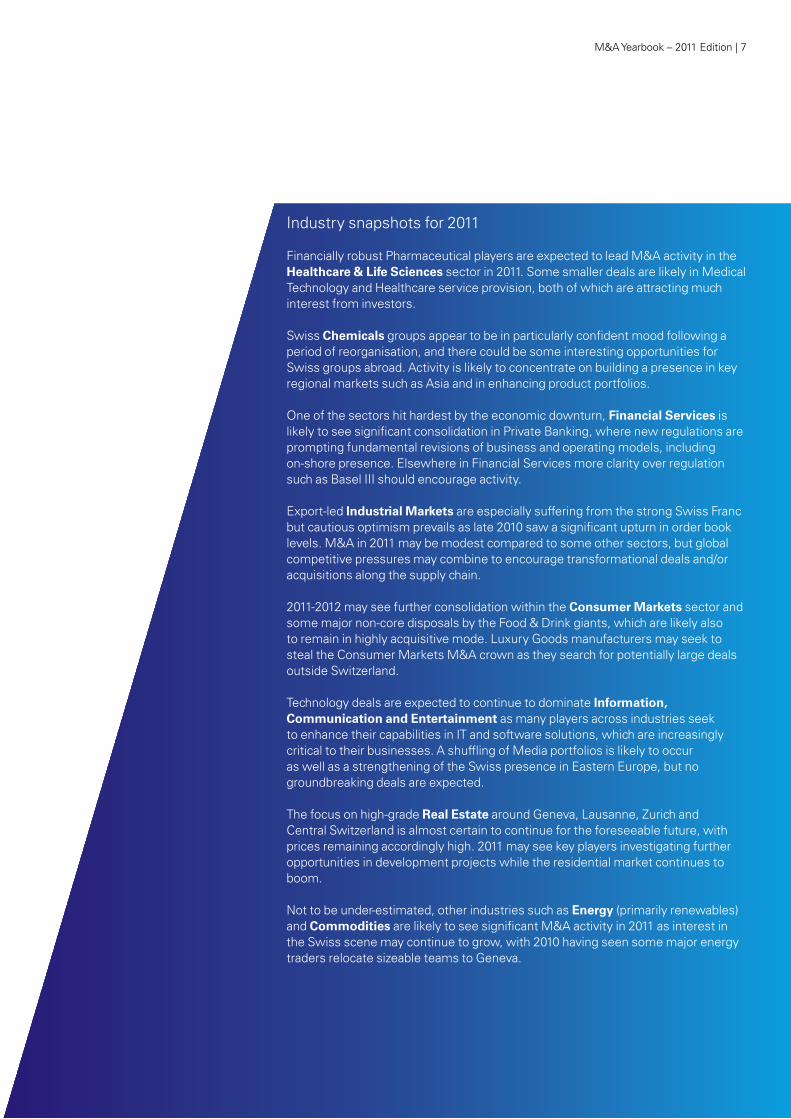

16 | M&a yearbook – 2011 Edition

The swiss industrial sector is seeing a gradual return of confidence after a couple of tough years, with talk around many boardroom tables moving from restructuring to sustainable growth. after a period in which both manufacturers and distributors actively managed down their inventories, the second half of 2010 saw a sales-led restocking as order book levels began to rise. some major businesses have already resumed growth plans in earnest. With a substantial cost-control programme behind it, aBB announced it will spend more than Usd 5 billion combined on two acquisitions alone, bolstering its presence in industrial motors and software solutions respectively through the anticipated purchase of Us-based Baldor Electric Company and the closed acquisition of ventyx.

Many though are cautious about putting into effect significant expansion plans while economic uncertainty remains and there are questions over how the industrial market will develop after the end of stimulus programmes. The continued strengthening of the swiss Franc is a particular issue for the export-led industrial market, challenging its price competitiveness abroad as well as possibly deterring inbound M&a activity. it is also prompting discussions around hedging alternatives and outsourcing production to lower labour cost economies. a further driver negatively impacting M&a activity last year was valuation expectations. although the gap between seller and buyer has narrowed, it is still hindering deal activity.

Outlook for 2011Mounting pressure for businesses to expand abroad in order to remain internationally competitive is likely to help drive M&a activity. This combines with an incentive for larger players to secure strategic assets and supplies, expanding their operations along the value chain. succession planning issues in family-owned businesses may also encourage mid-market disposals. Many owners are presently resisting the temptation to sell until they have (better) full year results for 2010. The consequence is that 2011 could see many more assets coming to market.

in addition to European and North american bidders, expressions of interest are likely to continue from Chinese and indian firms looking for high quality assets and access to production technology. Whether or not this results in M&a is questionable due to the difficulty of concluding deals between such distinct cultures. in terms of outbound deals from switzerland, aBB shows little sign of slowing down and is likely to remain in a highly acquisitive mood in 2011. While few if any mega-deals may be on the menu, a number of bolt-on acquisitions are likely to be in its sights. other groups may also continue screening for assets in strategically important regions.

Corporates should be able to fund acquisitions mainly with internal reserves, operating cash flows and/or divestiture proceeds. However, lower volatility and contracting debt spreads will make debt and equity issues more attractive in the next year. Meanwhile, corporates may wish to look for potential opportunities from the disposal of Private Equity portfolios. industrial Markets has long been popular with Private Equity as it is comparatively straight-forward to drive operational efficiencies. Funds have not generally exited long-term portfolio investments in the last two years and many now feel pressure from investors to do so. They may use the improved market and profitability of disposal assets to start preparing structured disposal processes to take place in 2011.

sean Peyer andreas PoellenPartner, Transaction services senior Manager, Mergers & acquisitions

Cautious optimism prevails as swiss industrial businesses transition into a period of recovery, fuelled by healthier order books. Many cyclical industries grew in 2010, putting M&a appetite back on the agenda for 2011, though perhaps with a focus on less risky transactions such as horizontal consolidation to add scale to core businesses or to add new customers or distribution channels. However, rising global competition may force established players to seriously consider both transformational transactions and acquisitions of key suppliers and/or new technologies

6 Industrial Markets

Sean Peyer T: +41 44 249 21 96E: [email protected]

Andreas Poellen T: +41 44 249 21 08E: [email protected]

M&a yearbook – 2011 Edition | 17

Number of deals per industry subsector 2010

28%

40%

15%

4%

13% Manufacturing & machinery

Industrial products & services

Electronics (industrial types such as robotics)

Automotives

Automation

Other

Top 5 Swiss M&A transactions 2010

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

Nov 2010 Baldor Electric Co 100% Usa aBB Ltd switzerland 4,188

May 2010 aBB indien Ltd 23% india aBB Ltd switzerland 1,092

dec 2010 Winterthur Technologie aG 100% switzerland 3M (schweiz) aG switzerland 371

dec 2010 General de servicios iTv sa

100% spain sGs sa switzerland Fomento de Construcciones y Contratas sa

spain 241

Jun 2010 dowding + Mills Plc 94% United Kingdom

sulzer aG switzerland 208

Number and value of deals per year

Number Value (USDbn)

US

Db

n

Nu

mb

er o

f d

eals

2006 2007 2008 2009 20100

2

4

6

8

10

12

14

16

18

0

10

20

30

40

50

60

70

80

90

Number of deals per quarterN

um

ber

of

dea

ls

Number

Q1 Q2 2008

Q3 Q4 Q1 Q2 2009

Q3 Q4 Q1 Q2 2010

Q3 Q4 0

2

4

6

8

10

12

14

16

18

20

Split of deals by target/buyer/seller 2008 to 2010

Nu

mb

er o

f d

eals

2008 2009 2010 2008 2009 2010 2008 2009 2010 2008 2009 2010

14

27

15

8

15 15 16

9 10

23

13

1 0

5

10

15

20

25

30

Swiss buyer/ Swiss target

Swiss buyer/ Foreign target

Foreign buyer/ Swiss target

Foreign buyer/ Foreign target (Swiss vendor)

18 | M&a yearbook – 2011 Edition

in 2010, M&a started with a bang in switzerland’s Consumer industry with a major transaction. While many businesses took stock of their positions and sought to prepare themselves for a period of renewed market confidence, 2010 saw a healthy level of M&a activity under the lead of Nestlé. still, due to the uncertain economic outlook and attractive acquisition targets remaining scarce the strong start to the year was not sustained. The above factors contributed to a fair degree of caution among prospective dealmakers, though overall a greater disposition towards considering deals was noted, boding well for activity in 2011.

Less impacted by the economic downturn than many other sectors, the Food & Drink giants have been able to remain focused on growth. They are by and large financially stable, well focused on their core segments and possess the necessary war chests to make opportunistic acquisitions as and when such arise. Major deals such as Nestlé’s acquisition of Kraft Foods’ Frozen Pizza business or aryzta’s purchase of the Usa’s Fresh start Bakeries are testimony to the fact that they retain significant financial muscle. also to be noted is the acquisition of the alcon business by Novartis from Nestlé. This transaction impressively demonstrates the closing gap between Consumer and Healthcare, a trend that may further affect both industries and their M&a activity.

Economically stable, the swiss Retail sector is notable for the strong position of its traditional peers Migros and Coop. The foothold recently obtained by German competitors such as aldi and Lidl has undoubtedly brought a new dynamic to the industry, though the dominance of Migros and Coop in the short- and mid-term cannot yet truly be challenged. Coop was the active player on the 2010 retail M&a stage, having bought the remaining stake in TransGourmet from rewe, reinforcing its presence in the swiss foodservices market while at the same time providing new channels and opportunities for future international growth.

The dip in 2009 was righted during the course of 2010, seeing Luxury Goods manufacturers return to form. Businesses such as richemont and swatch remain in fine shape and appear to be in acquisitive mood, looking primarily for smaller, bolt-on acquisitions to enhance or complement their brands and existing portfolios. However, they are struggling in light of a scarcity of attractive targets, which might also drive them to do bigger, more transformational transactions.

Outlook for 2011 The outlook for the Consumer industry appears promising. More transactions should be expected of the Food & drink giants. once Nestlé has digested the recent acquisition of Kraft Foods’ Frozen Pizza, it may once again be hungry. some of the larger international groups may seek to dispose of non-core business units over the next years, which will further shape the industry.

While Food & drink is likely to spearhead swiss Consumer Markets interest abroad, the Luxury Goods players under the lead of richemont and swatch are well positioned to follow or even overtake in 2011 by making large international moves. at the same time the strong interest in smaller swiss luxury brands and companies might trigger certain inbound acquisitions by foreign investors.

Patrik KerlerPartner, Head of Mergers & acquisitions

Financially healthy and well positioned to pursue a growth agenda, switzerland’s Consumer Markets has survived recent economic troubles better than most other sectors. activity may continue to be dominated by the mighty Food & drink players, though manufacturers of Luxury Goods are ready to make interesting acquisitions if opportunities materialise

7 Consumer Markets

Patrik Kerler T: +41 44 249 33 20E: [email protected]

M&a yearbook – 2011 Edition | 19

Top 5 Swiss M&A transactions 2010

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

Jan 2010 Kraft Foods inc (frozen pizza)

100% Usa Nestle sa switzerland Kraft Foods, inc Usa 3,700

Jun 2010 Fresh start Bakeries inc 100% Usa aryzta aG switzerland Lindsay Goldberg LLC Usa 900

Jan 2010 dufry south america Ltd 49% Brazil dufry aG switzerland 527

oct 2010 andreae-Noris Zahn aG 52% Germany alliance Boots GmbH switzerland PHoENiX Pharmahandel GmbH & Co KG; Celesio aG ; sanacorp Pharmaholding aG

Germany 527

aug 2010 Maidstone Bakeries 50% Canada aryzta aG switzerland Tim Hortons inc Canada 456

Number of deals per industry subsector 2010

39%

24%

13%

17%

7%

Food

Retail

Apparel

Luxury goods

Other

Number and value of deals per year

Number Value (USDbn)

US

Db

n

Nu

mb

er o

f d

eals

2006 2007 2008 2009 20100

2

4

6

8

10

12

0

10

20

30

40

50

60

70

Number of deals per quarter

Nu

mb

er o

f d

eals

Number

Q1 Q2 2008

Q3 Q4 Q1 Q2 2009

Q3 Q4 Q1 Q2 2010

Q3 Q4 0

5

10

15

20

25

30

Split of deals by target/buyer/seller 2008 to 2010

Nu

mb

er o

f d

eals

2008 2009 2010 2008 2009 2010 2008 2009 2010 2008 2009 2010

Swiss buyer/ Swiss target

Swiss buyer/ Foreign target

Foreign buyer/ Swiss target

Foreign buyer/ Foreign target (Swiss vendor)

13

30

16

6 6

14

0

8

13

27

6

00

5

10

15

20

25

30

35

20 | M&a yearbook – 2011 Edition

in Technology, the banking software industry in particular has benefited from the economic crisis due to the focus on enhancing risk and reporting systems in Financial services. Many players are actively seeking acquisition opportunities, including Temenos, which continues to scout for targets in key foreign markets.

The largest Telecoms transaction in 2010 was CvC Partners’ acquisition of sunrise following the cancelled merger with orange suisse. Meanwhile, swisscom built on its specialist portfolio in 2010 with acquisitions in network business services, iT solutions, and hospitality (hotel WiFi solutions), but no major deals. in 2011, the focus may be on strengthening its italian subsidiary, Fastweb.

Hard hit by the economic downturn as advertising spend fell, Media appears to be getting back on its feet. of the major players, Tamedia carried out little M&a in 2010 as it progressed with the ongoing merger of swiss media activities with Edipresse.

The traditional Travel business remains in flux, especially due to the internet’s increasing capacity to enable travellers to bypass tour operators and travel agents. some major tour operators are reacting by acquiring destination and specialist travel companies. Kuoni maintained its usual M&a pace through five acquisitions in 2010. Under pressure due to poor financial results, Hotelplan reorganised its structure in 2010, then strengthened its position in the UK ski travel market by buying Enigma Travel.

Outlook for 2011as iT and software solutions become ever more critical across a range of sectors, including Energy and related industries, 2011 may see the start of a wave of M&a or alliances and partnerships. aBB is likely to seek an expansion of its capabilities, especially in the Usa and with a particular interest in managed iT solutions for smart grids. Meanwhile, sGs could also include software-driven solutions in its M&a strategy, where it has been focusing on expansion in developing markets.

The semiconductor industry may see sT Microelectronics return to the M&a scene in 2011 as it develops its portfolio and builds the strength of its intellectual property, while either exiting non-core businesses or merging them with strong partners. Targets are likely to be intellectual property-rich companies in the Usa and Northern Europe, as well as possible partnership opportunities in asia. u-blox may show interest in undertaking acquisitions or may be a target itself.

Logitech will most likely be open to acquiring targets with innovative device solutions in 2011 irrespective of their geographic location. an example could be increasing the depth of its internet Tv product offer on the back of its alliance with Google.

2011 may witness Media companies continuing to try to optimise their portfolios. Goldbach Media and ringier may seek targets to bolster their expansion into Eastern Europe (as ringier did in teaming up with axel springer in 2010), and to bolster their digital services offering, but in 2011 the emphasis is likely to be on portfolio improvement rather than committing to major acquisitions.

James Carterdirector, Transaction services

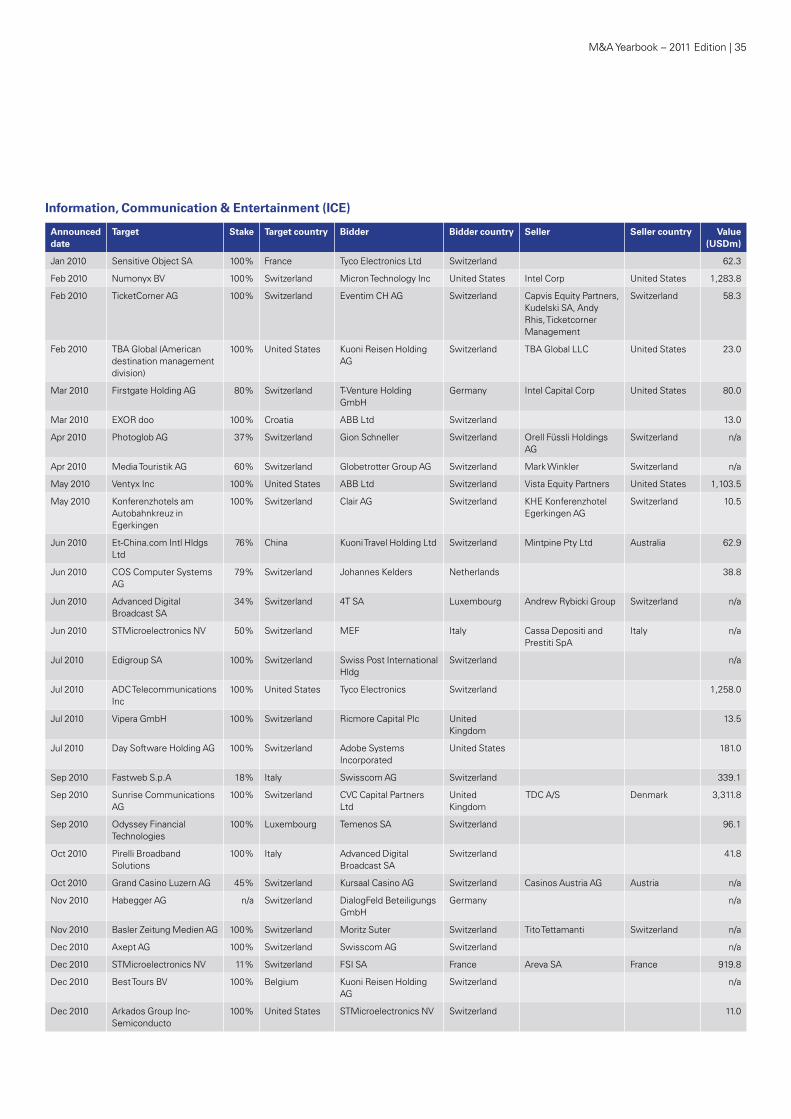

dominated by Technology and Telecoms deals, the sector may see pockets of M&a activity around banking software, semiconductors and energy-related businesses. Media and Travel may continue to focus on portfolio review and consolidation without giving rise to major transformational moves

8 Information, Communication & Entertainment

James Carter T: +41 22 704 15 48E: [email protected]

M&a yearbook – 2011 Edition | 21

Top 5 Swiss M&A transactions 2010

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

sep 2010 sunrise Communications aG 100% switzerland CvC Capital Partners Ltd United Kingdom

TdC a/s denmark 3,312

Feb 2010 Numonyx Bv 100% switzerland Micron Technology inc Usa intel Corp Usa 1,284

Jul 2010 adC Telecommunications inc

100% Usa Tyco Electronics switzerland 1,258

May 2010 ventyx inc 100% Usa aBB Ltd switzerland vista Equity Partners Usa 1,103

dec 2010 sTMicroelectronics Nv 11% switzerland Fsi sa France areva sa France 920

Number of deals per industry subsector 2010

31%

17%

14%

10%

28%

IT (hard and software)

Leisure

Telecoms

Media/internet

Electronics (entertainment related)

Number and value of deals per year

Number Value (USDbn)

US

Db

n

Nu

mb

er o

f d

eals

2006 2007 2008 2009 20100

1

2

3

4

5

6

7

8

9

10

0

10

20

30

40

50

60

Number of deals per quarterN

um

ber

of

dea

ls

Number

Q1 Q2 2008

Q3 Q4 Q1 Q2 2009

Q3 Q4 Q1 Q2 2010

Q3 Q4 0

2

4

6

8

10

12

14

16

18

Split of deals by target/buyer/seller 2008 to 2010

Nu

mb

er o

f d

eals

2008 2009 2010 2008 2009 2010 2008 2009 2010 2008 2009 2010

8

21

6

9 9

20

11

2

8

1110

00

5

10

15

20

25

Swiss buyer/ Swiss target

Swiss buyer/ Foreign target

Foreign buyer/ Swiss target

Foreign buyer/ Foreign target (Swiss vendor)

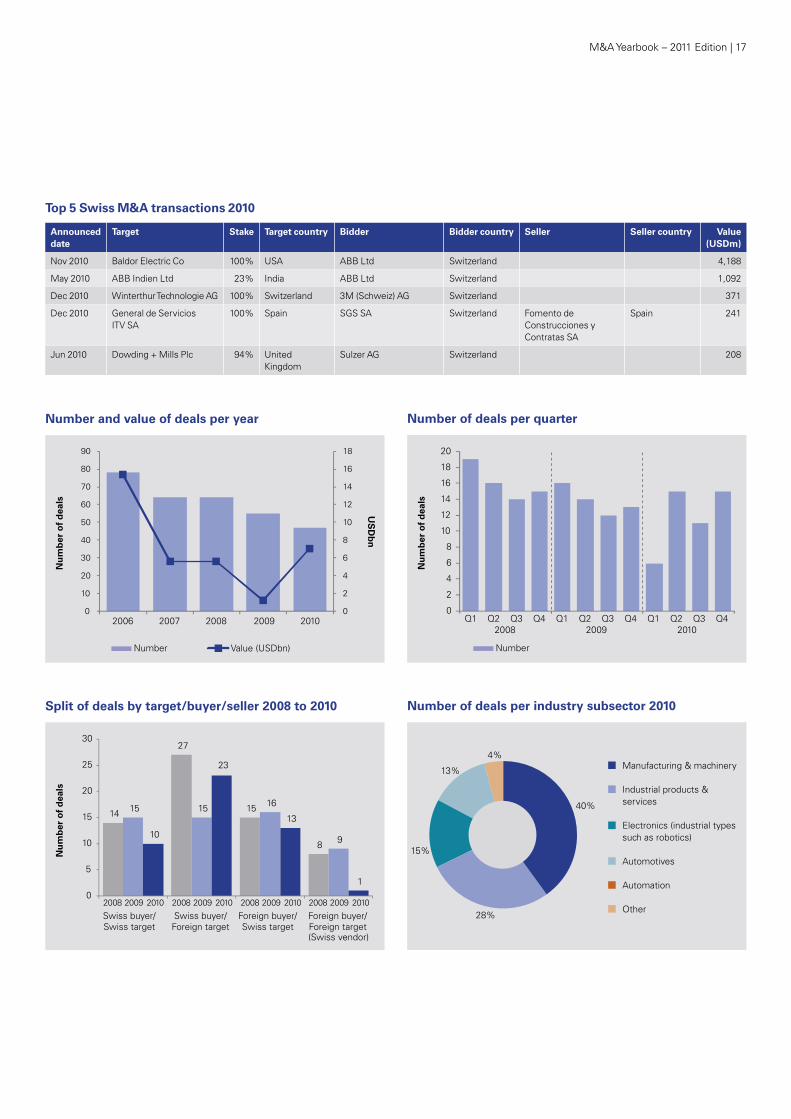

22 | M&a yearbook – 2011 Edition

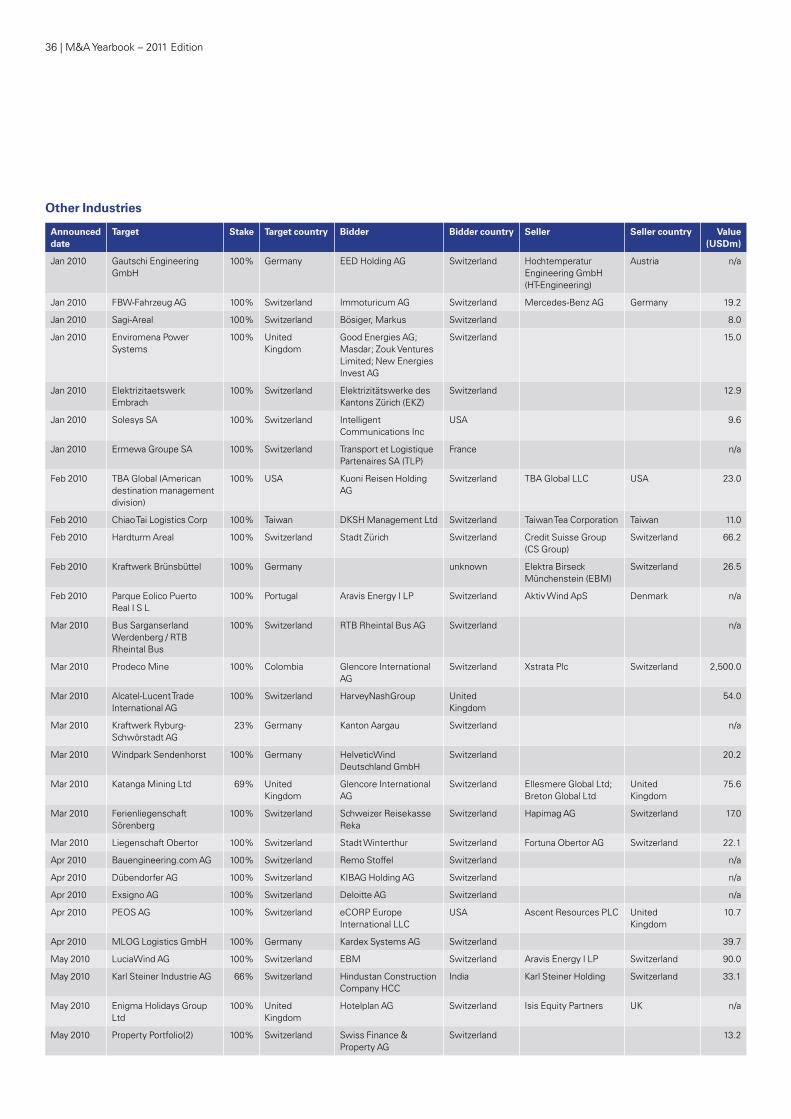

‘other industries’ captures those sectors not specifically covered elsewhere in this publication. For 2010 the most interesting sectors were arguably Energy, Mining and Commodities. This looks set to remain the case in 2011.

2010 showed a notable desire by swiss businesses – particularly utility companies such as those in Zurich and Bern – to invest in Renewable Energy. Primarily in the areas of wind and solar power, there is a feeling that a certain level of ‘catch up’ is required.

The other main focus has been on Mining and Commodities. it is known that Chinese companies are looking globally to acquire land in order to secure access to food and / or raw materials. The battle for such commodities may well intensify over the coming years and will be spearheaded on switzerland’s behalf by groups such as Xstrata and Glencore. due to the nature of the commodities business, acquisitions tend to be few and far between, but when they do take place they tend to be sizeable. it is difficult to predict where and when acquisition targets will become available, and so to an extent a successful growth agenda must be a combination of strategy and opportunism.

a particular development in 2010 was the relocation of a number of oil traders to Geneva, particularly from London. switzerland is noted by some commentators as being about to overtake London as the world’s main trading centre for physical energy commodities. vitol, the world’s largest energy trader, is transferring its European natural gas and power team to Geneva, while the world’s third largest oil trader, Trafigura, is moving one-quarter of its workforce to the city. such moves clearly help to bolster switzerland’s role in global commodity trading and may lead to diverse opportunities.

Outlook for 2011The notable shift into acquisition mode is set to continue in 2011. Many swiss businesses are leaner and more efficient following considerable restructuring or cost control measures and are in excellent positions to actively pursue a growth agenda. on the sale side, many large groups may consider disposing of non-core or problematic businesses they have held on to for a while, in order to enhance shareholder value. These are in the main not distressed sales but rather an opportunity to raise funds to either distribute to shareholders or to spend on acquisitions to reinforce their core businesses.

Energy will remain strongly on the agenda. There is the prospect of the start of a consolidation phase among utility companies, but this is unlikely to be achieved fully until there is greater market liberalisation in switzerland. in the meantime, players may begin laying the groundwork and scouting for attractive assets. acquisitions will chiefly be strategic rather than opportunistic, focused on building a portfolio and / or making bolt-on acquisitions.

rolf Langeneggerdirector, valuation services

Energy and Commodities top the agenda, with swiss companies being in acquisitive mood following a period of restructuring and cost control. disposals are possible with the aim of building shareholder value, representing potential opportunities for Private Equity and corporate investors alike

9 Other Industries

Rolf Langenegger T: +41 44 249 31 16E: [email protected]

M&a yearbook – 2011 Edition | 23

Number and value of deals per year

Number Value (USDbn)

US

Db

n

Nu

mb

er o

f d

eals

2006 2007 2008 2009 20100

5

10

15

20

25

30

35

40

0

10

20

30

40

50

60

70

80

90

100

Number of deals per quarterN

um

ber

of

dea

ls

Number

Q1 Q2 2008

Q3 Q4 Q1 Q2 2009

Q3 Q4 Q1 Q2 2010

Q3 Q4 0

5

10

15

20

25

Split of deals by target/buyer/seller 2008 to 2010

Nu

mb

er o

f d

eals

2008 2009 2010 2008 2009 2010 2008 2009 2010 2008 2009 2010

Swiss buyer/ Swiss target

Swiss buyer/ Foreign target

Foreign buyer/ Swiss target

Foreign buyer/ Foreign target (Swiss vendor)

21

28

13

9

19

26

12 12

22

30

12

6

0

5

10

15

20

25

30

35

Number of deals per industry subsector 2010

10%1%

34%

3%

16%

20%

16%

Energy & utilities

Real estate

Logistics & transportation

Professional services

Minerals & mining

Construction

Commodities

Top 5 Swiss M&A transactions 2010

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

Mar 2010 Prodeco Mine 100% Colombia Glencore international aG

switzerland Xstrata Plc switzerland 2,500

Jun 2010 Fdr Holdings Ltd 100% Usa Noble Corp switzerland 2,160

aug 2010 Gas- und dampfkraftwerk bei szeged

50% Hungary siemens Project ventures GmbH

Germany advanced Power aG switzerland 994

aug 2010 Gas- und dampfkraftwerk bei Wustermark (Havelland)

50% Germany siemens Project ventures GmbH

Germany advanced Power aG switzerland 994

Nov 2010 swissport international aG 100% switzerland Pai Partners sas France Ferrovial sa spain 918

24 | M&a yearbook – 2011 Edition

The Private Equity model so successfully applied prior to the financial crisis faces a number of threats. a decline in cheap financing has eroded a key competitive advantage while a general lack of acquisition targets pushes up prices, making it harder to generate the required returns on investment. some investor classes – notably wealthy individuals and family offices – are also observed to be bypassing funds by making direct investments through shareholdings. Exacerbating the problem is the fact that corporate balance sheets are relatively healthy and boards are becoming more confident to refocus on the growth agenda, giving rise to more intense competition for available assets. on the sale-side, many prospective vendors prefer to wait until a sustained return of confidence and rising prices makes it more conducive to bring assets to market. as switzerland suffered less from the economic crisis than the majority of its European counterparts, there has been a comparative absence of distressed or forced sales. Many Private Equity houses are therefore seeking homes for the often significant funds they hold. This can present a dilemma: invest funds in sub-optimal assets or retain the funds but possibly struggle to demonstrate performance and raise further finance.

various strategies are being pursued to deal with these challenges, notably by investing even more time and patience in sourcing proprietary deals, but also looking outside switzerland. Capvis, for instance, has focused more on the greater number of available targets in the German market, acquiring Kaffee Partner in 2010. on the sell-side, Capvis sold its investment in Ticketcorner to German group CTs Eventim and iPo’d orior, the swiss convenience food group.

Geneva-based argos soditic continues to successfully raise funds with the announcement in december 2010 that it has closed its EuroKnights vi fund of EUr 400 million with the aim of focusing on small and mid-market companies based in Europe, predominantly in France, italy and switzerland.

The most notable new Private Equity investment in switzerland was CvC’s acquisition of sunrise Communications, switzerland’s third largest Telecom provider. Further key exits included Barclays Private Equity’s sale of its 51% stake in schild to the management team, and EGs Beteiligungen and Towerbrook’s sale of odlo, the swiss outdoor apparel company, to Herkules Private Equity.

Outlook for 2011The hottest sector for Private Equity in 2011 is likely to be diversified industrials, where it has typically been easier to drive operational improvements. There may also be interest in small and medium-sized Food businesses. For both, activity may depend on whether sufficient targets come to market and at what price.

despite the challenges, Private Equity continues to be attractive to many vendors, who see benefits over corporate bidders, including: likely longer-term retention of the brand and identity of the acquired business; a willingness to keep the owner and/or management involved; and more flexible and responsive decision-making processes resulting in a potentially more efficient, speedier sale process. The light at the end of the tunnel may thus also be family-owned businesses facing succession issues. Many would-be vendors have held on to their assets during the economic crisis and may be tempted to sell if confidence in business plans grows and prices remain firm or increase. Meanwhile, successful exits may be helped by the presence of well-funded corporates on the look-out for high quality assets to buy or by recovering stock markets encouraging iPo activity.

Tobias valkPartner, Head of Transaction services

2010 saw a reawakening of the swiss Private Equity industry, with deal activity increasing as the year progressed. Fierce competition from resurgent corporates, however, combines with a shortage of available quality assets to present severe challenges to the Private Equity dealmaker, who is pursuing various strategic alternatives such as wider geographic focus and sourcing proprietary deals

10 Private Equity

Tobias Valk T: +41 44 249 33 29E: [email protected]

M&a yearbook – 2011 Edition | 25

Number and value of deals per year

Number Value (USDbn)

US

Db

n

Nu

mb

er o

f d

eals

2006 2007 2008 2009 20100

2

4

6

8

10

12

14

16

18

0

10

20

30

40

50

60

70

80

90

100

Number of deals per quarter

Nu

mb

er o

f d

eals

Number

Q1 Q2 2008

Q3 Q4 Q1 Q2 2009

Q3 Q4 Q1 Q2 2010

Q3 Q4 0

2

4

6

8

10

12

14

16

18

20

Split of deals by target/buyer/seller 2008 to 2010

Nu

mb

er o

f d

eals

2008 2009 2010 2008 2009 2010 2008 2009 2010 2008 2009 2010

Swiss buyer/ Swiss target

Swiss buyer/ Foreign target

Foreign buyer/ Swiss target

Foreign buyer/ Foreign target (Swiss vendor)

n/a n/a n/a n/an/a n/a n/a n/a

5

19

9

1

0

2

4

6

8

10

12

14

16

18

20

Number of deals per industry sector 2010

13%

26%

13%

22%

13%

13%

Financial Services

Consumer Markets

Healthcare & Life Sciences

Industrial Markets

Information, Communication & Entertainment (ICE)

Chemicals & Processing Materials

Other Industries

Top 5 Swiss M&A transactions 2010

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

sep 2010 sunrise Communications aG 100% switzerland CvC Capital Partners LTd United Kingdom

TdC a/s denmark 3,312

May 2010 ventyx inc 100% Usa aBB Ltd switzerland vista Equity Partners Usa 1,103

Nov 2010 swissport international aG 100% switzerland Pai Partners sas France Ferrovial sa spain 918

Jun 2010 Fresh start Bakeries inc 100% Usa aryzta aG switzerland Lindsay Goldberg LLC Usa 900

oct 2010 stallergenes sa 46% France ares Life sciences aG switzerland Wendel sa France 500

26 | M&a yearbook – 2011 Edition

direct real Estate continues to be in demand due to predictable income flows and comparatively high yields (annualised one year total return of 6.67%1), representing enviable returns over other forms of investment. Fund-raising has been active in what was a difficult year for most other sectors. Credit suisse successfully launched a hospitality fund, with raised capital of Usd 1.2 billion, oversubscribed by 33%. These funds will for example flow into the swiss Holiday Park, a hotel and seminar destination acquired by Credit suisse in december 2010.

a hot sector was the privately-owned residential market. demand was so great that the swiss National Bank warned against entering a price bubble, though market players and observers largely discounted this fear. However, the investment residential market recorded a relatively modest price increase of 2.4%1 in 2010.

regional hotspots are a challenge as most investors seek high grade real Estate primarily in Geneva, Lausanne, Zurich and the greater Zurich area. This sustains premium prices and leads to tender processes. Prices are beginning to peak in central switzerland, including Zug, and in holiday destinations such as st Moritz.

investors are responding by moving up the value chain, undertaking development projects with a contractor rather than waiting for completed assets. This reflects in deal activity in the construction and development industry. implenia, the largest swiss-based construction firm, acquired sulzer immobilien, a real estate development company. HiaG immobilien schweiz acquired streiff, a company with a vast land portfolio in Zurich and Basel. Hindustan Construction Company Limited, the listed indian infrastructure company, bought a 66% stake in the construction company Karl steiner for Usd 33 million. despite this latter deal the sector remained overwhelmingly domestic. Foreign investors showed a preference for areas with more depressed market conditions and prices. swiss players showed little appetite for foreign acquisitions. although some pension funds considered investing abroad, plans were revised in light of the impacts of the economic crisis. insurance companies may begin to look at centres such as Paris, Frankfurt or Munich, but activity is likely to be limited.

asset deals tend to dominate over share deals. The largest portfolio transaction in 2010 comprised a residential portfolio, which was sold by the swiss Confederation to the pension fund of F. Hoffmann-La roche. structured as three regional sub-portfolios, it received broad interest among swiss institutional investors and was closed in January 2011. The most prominent single asset transaction was the sale to swiss Life of UBs’s commercial building at Bellevueplatz 5 in Zurich. recently renovated for Usd 52 million, it is a trophy building in a prime location.

Outlook for 2011as interest rates remain low, funds are likely to continue to flow into the sector. regional concentration is set to remain one of the largest challenges. Prices are likely to remain very high compared to other European markets. investors could try to target ‘B’-grade locations, though there is little sign of any of the major players being willing to do so. The medium-term pipeline contains some potential major projects. sBB’s sizeable, centrally located sites are ripe for development and could create interesting opportunities for swiss and foreign investors.

Ulrich PrienPartner, real Estate

regional hotspots and premium pricing continued to define the real Estate sector in 2010. as institutional players tighten their hold on assets, investors are looking to move up the value chain into development projects

11 Real Estate

1 as at 31 december 2010. source: sWX iaZi investment real Estate Performance / Price index

Ulrich Prien T: +41 44 249 21 77E: [email protected]

M&a yearbook – 2011 Edition | 27

2 The swiss Federal act on Cartels and other restraints of Competition

Merger control: Generally of concern only to the largest organisations, merger control in switzerland typically presents few surprises to dealmakers, chiefly due to the high notification thresholds involved. indeed, thresholds in switzerland are much higher than in some of its larger European counterparts, particularly Germany. With the exception of mega-deals, notification requirements would generally be triggered only where one of the parties was characterised as being a market dominant enterprise in a previous legally binding order from the swiss competition authority (in which case it must notify all prospective concentrations). in rare instances the process can derail a merger entirely, such as in 2010 when the authorities denied permission for the proposed merger between sunrise and orange on the grounds that it would create a collective market dominant position.

The possibility of triggering merger control should be considered at an early stage of the transaction planning as it can take up to four to six months to complete, depending on the countries where a notification needs to be filed. Particular attention should be paid when undertaking transactions in Eastern Europe or the Cis, where foreign-to-foreign transactions are also caught by national merger control law. it is not unknown in a deal likely to trigger such notification requirements to split off the relevant part of the transaction in order not to hamper or even block the entire project.

Assessing antitrust risks of targets: Particular attention is drawn to the importance of assessing antitrust risks of targets during a deal process. antitrust risks are often sleeping risks that are extremely difficult, if at all possible, to detect pre-deal. it is highly improbable that a prospective acquirer would be in a position to identify informal, unwritten arrangements between the target management and third parties unless such are specifically disclosed. They can represent major risks if illegal practices remain uncovered by the acquirer or come to light only post-acquisition.

it is important to consider effective means of determining the existence of such risks. Most notably, one may stress-test a target’s compliance programmes: does a formal policy and programme exist? is there a culture of compliance? is the programme enforced, and how? are staff sufficiently aware of it? is regular, formal training provided? do internal sanctions for breaches exist and are they imposed on deviators? often, the target’s corporate culture can be key in assessing hidden risks and it is important that the acquirer gains a sense of it.

Competition Act: The swiss Cartel act2 is presently undergoing revision. While current notification thresholds are expected to remain the same for the foreseeable future it is possible that the material assessment criteria will shift from the current ‘dominant market position’ test to the ‘significant impediment of effective competition’ (siEC) test. as the siEC test is applied in the EU, such a move in switzerland would bring swiss merger control more in line with existing EU standards. Harmonising the two sets of rules, or at least moving them closer together, may yield benefits to the international firm doing business in switzerland in the form of simpler processes. The public consultation as part of the legislative process ended in November 2010.

daniel Lengauer samuel indermühlePartner, attorney-at-law Manager, attorney-at-law

despite being highly stable and predictable, swiss merger control retains the capacity to surprise and to catch dealmakers off-guard, as seen in the denied sunrise / orange merger. However, such surprises are the exception rather than the rule. Meanwhile, a review of the swiss Competition act is underway, which might improve life for many businesses that are active also in the EU

12 Legislative & Regulatory Aspects

Daniel Lengauer T: +41 44 249 23 89E: [email protected]

Samuel Indermühle T: +41 44 249 31 64E: [email protected]

28 | M&a yearbook – 2011 Edition

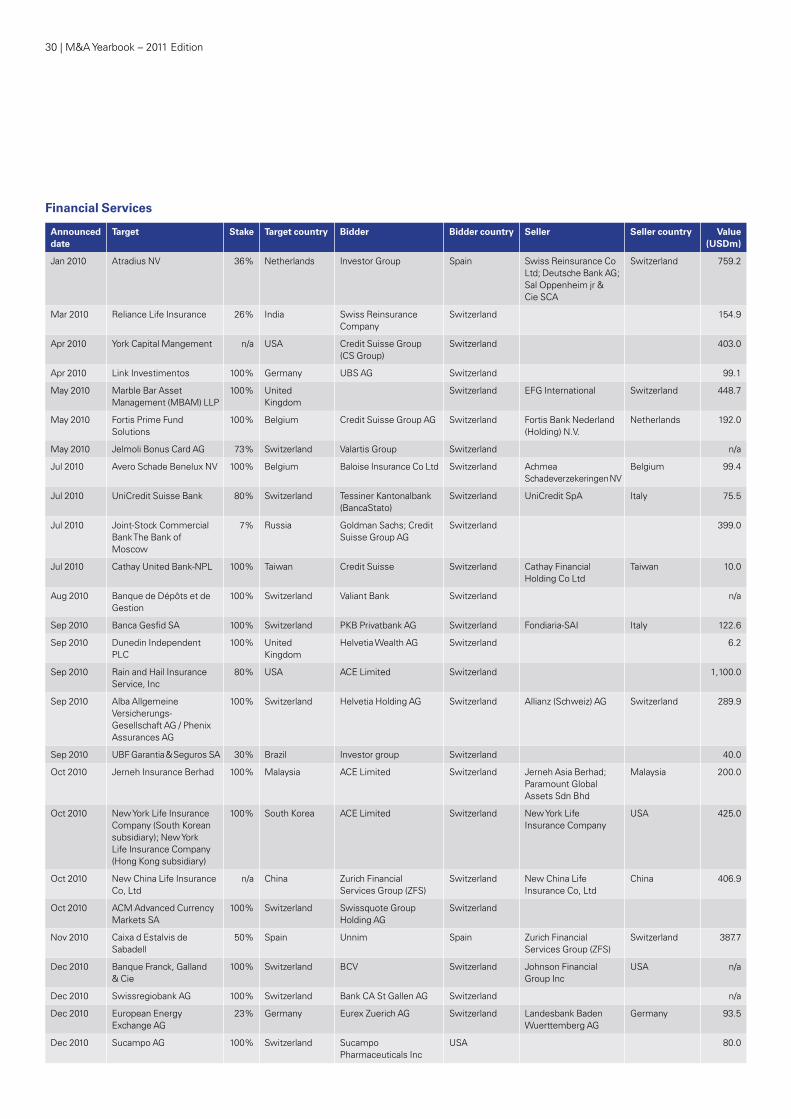

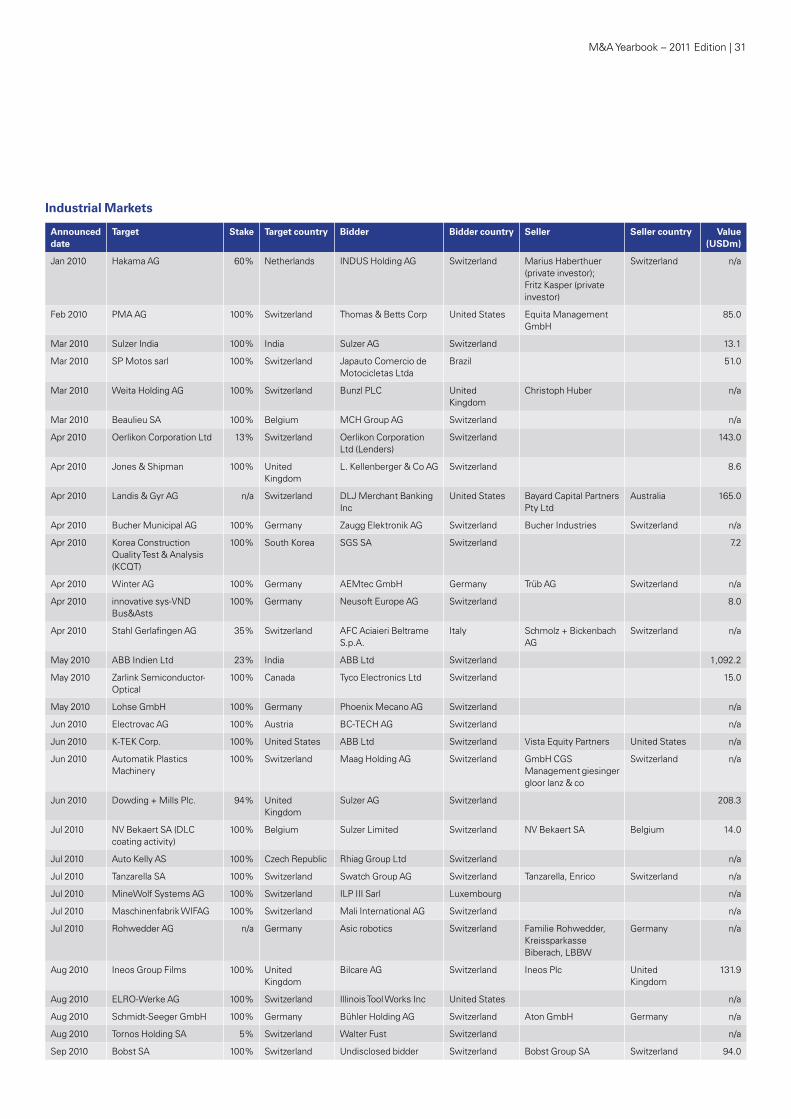

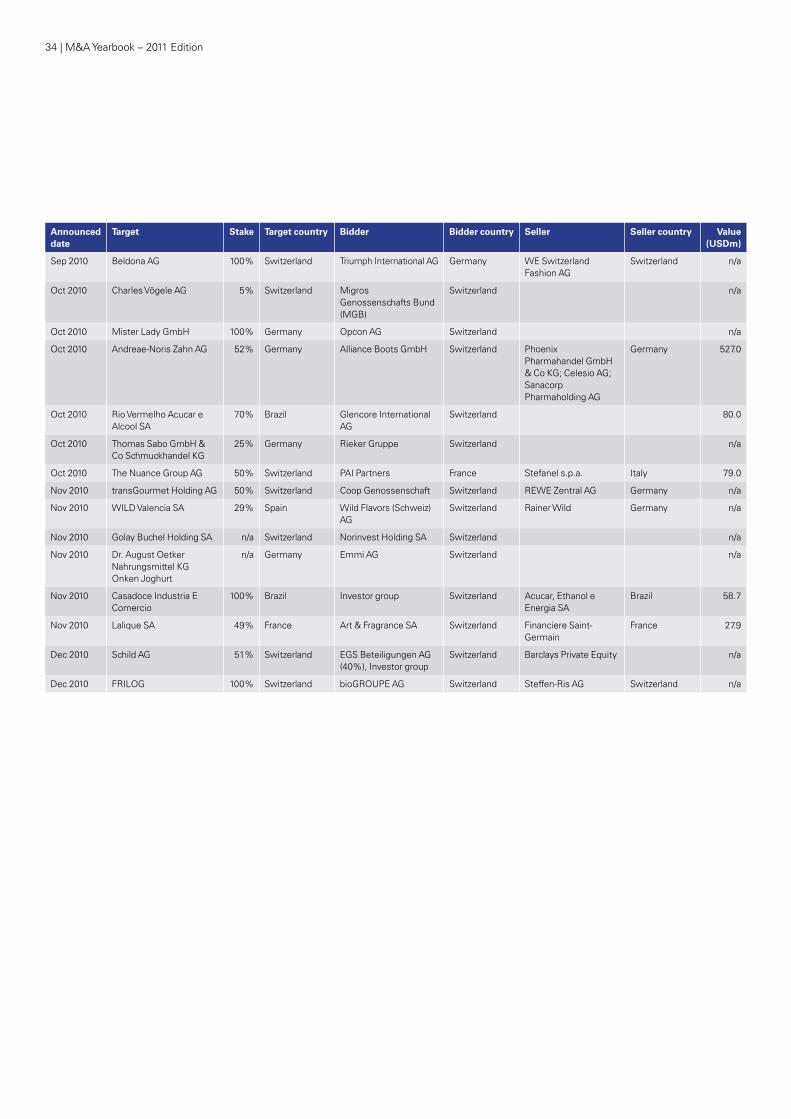

13 List of 2010 Swiss M&A Transactions

Healthcare & Life Sciences

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

Jan 2010 Mepha aG 100% switzerland Cephalon inc Usa Merckle Germany 560.4

Jan 2010 alcon inc 52% Usa Novartis aG switzerland Nestlé sa switzerland 28,300.0

Jan 2010 insound Medical inc 100% Usa sonova Holding aG switzerland 75.0

Feb 2010 Lelystad Biologicals Bv 100% Netherlands Prionics aG switzerland 589.7

Feb 2010 Lonza Group aG n/a switzerland Ehrfeld Mikrotechnik BTs GmbH

Germany n/a

Mar 2010 Bioxell spa 100% switzerland Cosmo Pharmaceuticals spa

italy 9.9

Mar 2010 siegfried Holding aG 33% switzerland investor Group switzerland Camellia investments PLC

United Kingdom

74.2

Mar 2010 Bestewil Holding Bv 100% Netherlands Mymetics Corporation switzerland Norwood immunology Limited

australia 9.5

apr 2010 Medingo Limited 100% Usa roche Holding aG switzerland Elron Electronic industries Ltd

israel 200.0

apr 2010 Bio-analytica Holding aG 85% switzerland Medisupport sa switzerland 23.0

May 2010 spital region oberaargau n/a switzerland dahlia switzerland n/a

May 2010 Lysteda n/a Usa Ferring Pharmaceuticals switzerland Xanodyne Pharmaceuticals, inc

Usa n/a

Jun 2010 Krankenhaus Zimmerberg 100% switzerland sanitas switzerland n/a

Jul 2010 TargeGen inc 100% Usa sanofi-aventis Group France Consortium of investors

switzerland 587.4

Jul 2010 remp aG 100% switzerland NEXUs aG Germany Tecan Holding aG switzerland 18.9

Jul 2010 sperian Welding Protection aG

100% switzerland Marco Koch switzerland n/a

aug 2010 Bioimagene, inc 100% Usa roche Holding aG switzerland 104.7

sep 2010 zahnarztzentrum.ch aG n/a switzerland G square France 19.0

sep 2010 Novartis aG n/a switzerland Warner Chilcott United Kingdom

Novartis aG switzerland 400.0

oct 2010 siegfried aG n/a switzerland sanofi-aventis Group France

oct 2010 PregLem sa 100% switzerland Gedeon richter PLC Hungary sofinnova Partners sa; NeoMed innovation iii LP; sofinnova ventures inc; MvM Life science Partners LLP

France 462.6

oct 2010 stallergenes sa 46% France ares Life sciences aG switzerland Wendel sa France 499.9

oct 2010 Théramex n/a Monaco TEva Pharmaceutical industries Ltd

israel Merck serono sa switzerland 351.0

Nov 2010 Techpool Bio-Pharma Co Limited

51% switzerland Nycomed Pharma as Norway shanghai Pharmaceuticals Company Limited

China 210.2

Nov 2010 Heidelberg Pharma 100% switzerland Wilex aG Germany 25.4

dec 2010 Q-MEd aB 100% sweden Galderma Pharma sa switzerland 983.0

dec 2010 Chiron Behring vaccines Private Limited

49% india Novartis Pharma aG switzerland aventis Pharma Limited

France 22.0

dec 2010 alcon inc 23% Usa Novartis aG switzerland Nestlé sa switzerland 12,900.0

dec 2010 immunotherapeutical Company

100% switzerland Biogen idec inc Usa 427.6

dec 2010 sodem diffusion sa n/a switzerland Zimmer Holdings inc Usa n/a

M&a yearbook – 2011 Edition | 29

Chemicals & Processing Materials

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

Jan 2010 EFTEC aftermarket GmbH

100% Germany Facilitas Bergeyk Bv Netherlands Ems-Chemie Holding aG

switzerland 22.5

Jan 2010 Balderton Fertilisers sa 50% switzerland yara international asa Norway 130.0

Mar 2010 Polartech Ltd 100% United Kingdom

afton Chemical Corp Usa Koras aG switzerland n/a

May 2010 impact Fertilisers australia Pty Limited; impact Fertilisers Pty Ltd

50% australia ameropa aG switzerland 45.0

May 2010 Termoindustriale srl 100% italy argos soditic sa switzerland 10.0

May 2010 Maribo seed international aps

100% denmark syngenta aG switzerland 57.0

May 2010 dyflex Co Ltd n/a Japan sika aG switzerland n/a

Jun 2010 aBB Micafil-resins Business

100% switzerland altana aG Germany n/a

Jul 2010 Greenstreak Group, inc 100% Usa sika aG switzerland n/a

aug 2010 Johnson Matthey Catalysts

100% United Kingdom

dorf Ketal Chemicals aG switzerland Johnson Matthey Plc United Kingdom

7.2

Nov 2010 GreenLeaf Genetics LLC 50% Usa syngenta aG switzerland El du Pont de Nemours & Co

Usa n/a

Nov 2010 Biopetrol industries aG 15% switzerland investor group switzerland n/a

dec 2010 Phonex-Gema aG 100% switzerland investor group switzerland armstrong Metalldecken aG

switzerland n/a

dec 2010 datacolor aG 67% switzerland Werner dubach switzerland 45.8

dec 2010 vinythai PCL 9% Thailand solvay vinyls Holding aG switzerland Charoen Pokphand Holding Co

Thailand 49.2

30 | M&a yearbook – 2011 Edition

Financial Services

Announced date

Target Stake Target country Bidder Bidder country Seller Seller country Value (USDm)

Jan 2010 atradius Nv 36% Netherlands investor Group spain swiss reinsurance Co Ltd; deutsche Bank aG; sal oppenheim jr & Cie sCa

switzerland 759.2

Mar 2010 reliance Life insurance 26% india swiss reinsurance Company

switzerland 154.9

apr 2010 york Capital Mangement n/a Usa Credit suisse Group (Cs Group)

switzerland 403.0

apr 2010 Link investimentos 100% Germany UBs aG switzerland 99.1

May 2010 Marble Bar asset Management (MBaM) LLP

100% United Kingdom

switzerland EFG international switzerland 448.7

May 2010 Fortis Prime Fund solutions

100% Belgium Credit suisse Group aG switzerland Fortis Bank Nederland (Holding) N.v.

Netherlands 192.0

May 2010 Jelmoli Bonus Card aG 73% switzerland valartis Group switzerland n/a

Jul 2010 avero schade Benelux Nv 100% Belgium Baloise insurance Co Ltd switzerland achmea schadeverzekeringen Nv

Belgium 99.4