2017 FULL YEAR RESULTS PRESENTATION - … · 2017 FULL YEAR RESULTS PRESENTATION MEDICLINIC RESULTS...

44

2017 FULL YEAR RESULTS PRESENTATION

Transcript of 2017 FULL YEAR RESULTS PRESENTATION - … · 2017 FULL YEAR RESULTS PRESENTATION MEDICLINIC RESULTS...

2017 FULL YEAR RESULTS

PRESENTATION

2017 FULL YEAR RESULTS PRESENTATION 2

MEDICLINIC RESULTS

DISCLAIMER

This presentation contains certain forward-looking statements relating to the financial condition, theregulatory environment in which we operate, results of operations and businesses of Mediclinic and theGroup, including certain plans and objectives of the Group.

All statements other than statements of historical fact are, or may be deemed to be, forward-lookingstatements. Forward-looking statements are statements of future expectations that are based onmanagement’s current expectations and assumptions and involve known and unknown risks anduncertainties that could cause actual results, performance or events to differ materially from thoseexpressed or implied in these statements.

Forward-looking statements include, among other things, statements concerning the potential exposureof Mediclinic to market risks and statements expressing management’s expectations, beliefs, estimates,forecasts, projections and assumptions, including as to future potential cost savings, synergies, earnings,cash flow, production and prospects. These forward-looking statements are identified by their use ofterms and phrases such as “anticipate”, “believe”, “could”, “estimate”, “expect”, “goals”, “intend”, “may”,“objectives”, “outlook”, “plan”, “probably”, “project”, “risks”, “seek”, “should”, “target”, “will” and similarterms and phrases.

2017 FULL YEAR RESULTS PRESENTATION

MEDICLINIC RESULTS

AGENDA

INTRODUCTION Page 4

FINANCIAL REVIEW Page 6

OPERATIONAL REVIEW Page 19

STRATEGY Page 24

QUESTIONS AND ANSWERS Page 30

APPENDIX Page 31

INTRODUCTION

DANIE MEINTJES

CEO MEDICLINIC INTERNATIONAL

2017 FULL YEAR RESULTS PRESENTATION

MEDICLINIC RESULTS

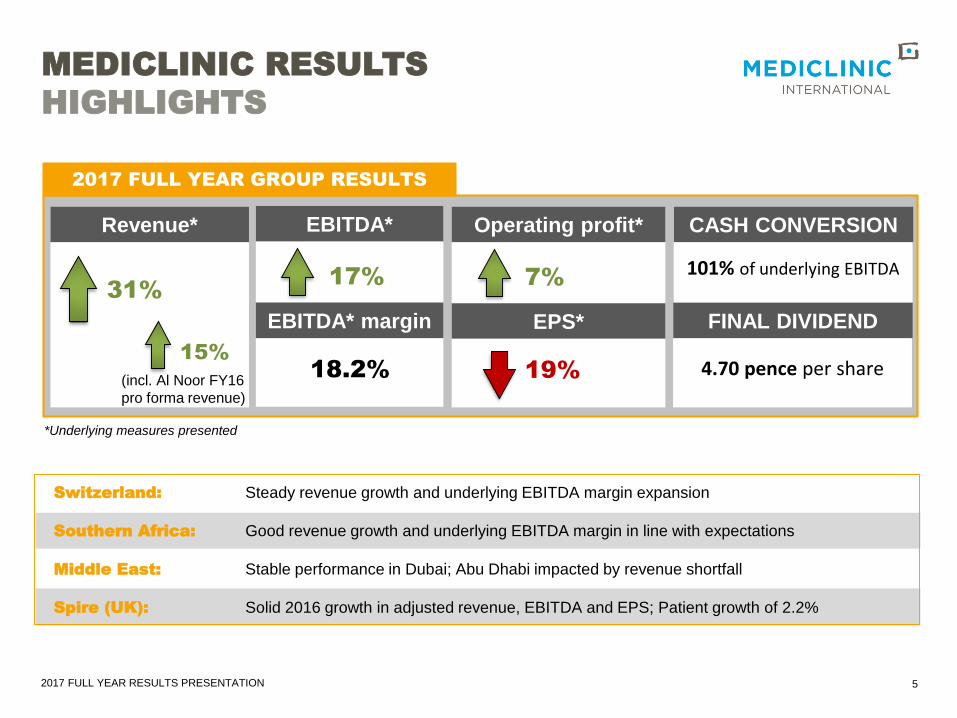

HIGHLIGHTS

2017 FULL YEAR GROUP RESULTS

Revenue*

31%

(incl. Al Noor FY16

pro forma revenue)

15%

Operating profit*

101% of underlying EBITDA7%

19%

EPS*

5

*Underlying measures presented

CASH CONVERSION

Switzerland: Steady revenue growth and underlying EBITDA margin expansion

Southern Africa: Good revenue growth and underlying EBITDA margin in line with expectations

Middle East: Stable performance in Dubai; Abu Dhabi impacted by revenue shortfall

Spire (UK): Solid 2016 growth in adjusted revenue, EBITDA and EPS; Patient growth of 2.2%

EBITDA*

17%

18.2%

EBITDA* margin

4.70 pence per share

FINAL DIVIDEND

2017 FULL YEAR RESULTS PRESENTATION

FINANCIAL

REVIEW

JURGENS MYBURGH

CFO MEDICLINIC INTERNATIONAL

2017 FULL YEAR RESULTS PRESENTATION

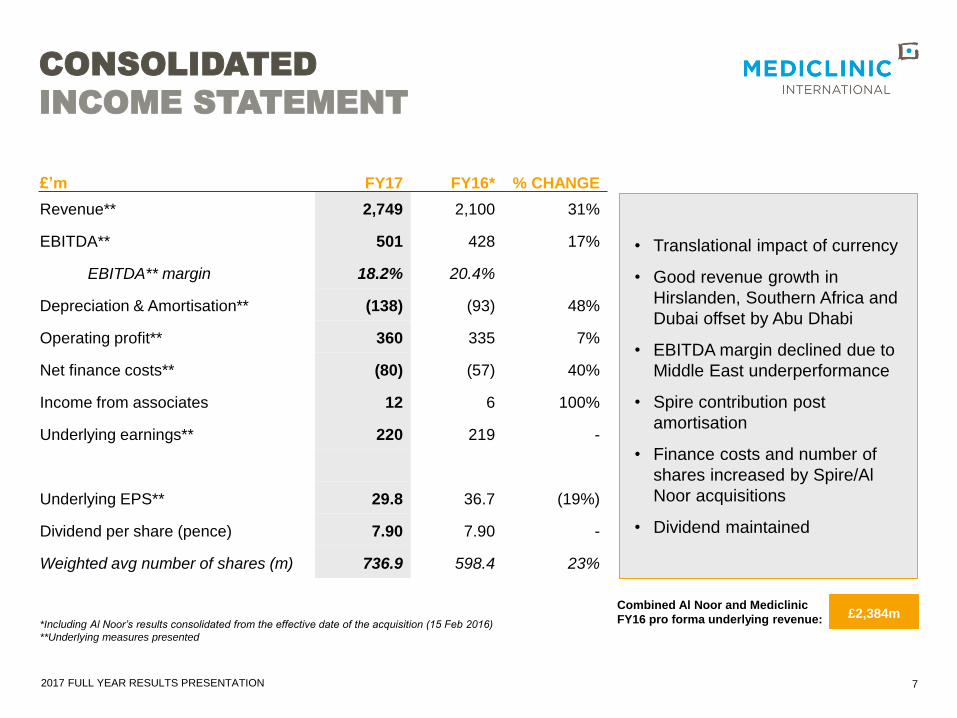

£’m FY17 FY16* % CHANGE

Revenue** 2,749 2,100 31%

EBITDA** 501 428 17%

EBITDA** margin 18.2% 20.4%

Depreciation & Amortisation** (138) (93) 48%

Operating profit** 360 335 7%

Net finance costs** (80) (57) 40%

Income from associates 12 6 100%

Underlying earnings** 220 219 -

Underlying EPS** 29.8 36.7 (19%)

Dividend per share (pence) 7.90 7.90 -

Weighted avg number of shares (m) 736.9 598.4 23%

*Including Al Noor’s results consolidated from the effective date of the acquisition (15 Feb 2016)

**Underlying measures presented

CONSOLIDATED

INCOME STATEMENT

7

£2,384mCombined Al Noor and Mediclinic

FY16 pro forma underlying revenue:

• Translational impact of currency

• Good revenue growth in

Hirslanden, Southern Africa and

Dubai offset by Abu Dhabi

• EBITDA margin declined due to

Middle East underperformance

• Spire contribution post

amortisation

• Finance costs and number of

shares increased by Spire/Al

Noor acquisitions

• Dividend maintained

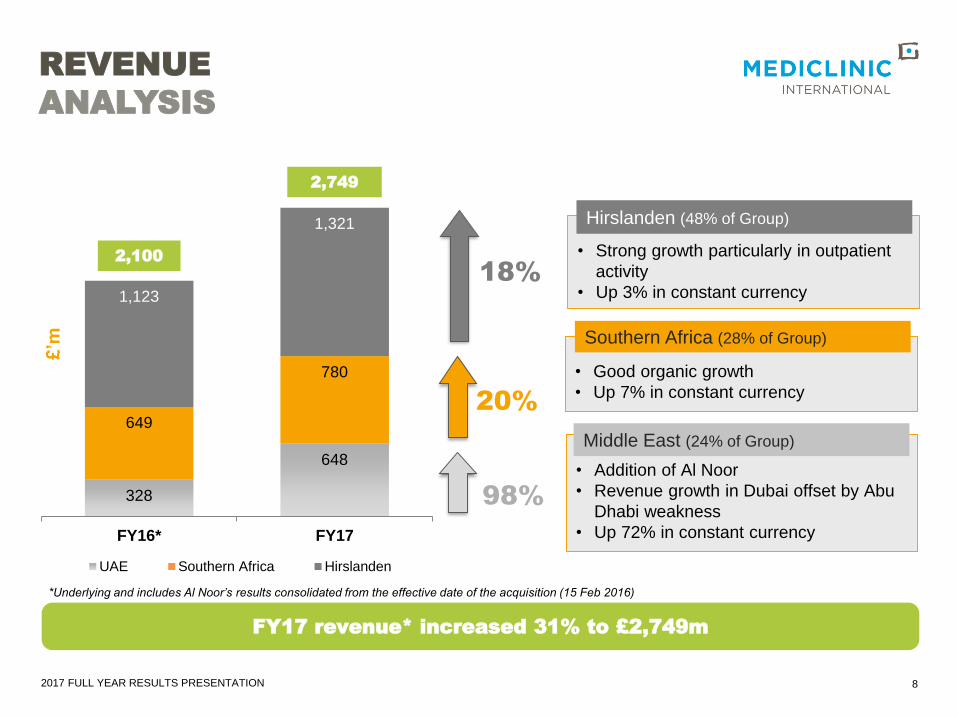

2017 FULL YEAR RESULTS PRESENTATION

328

648

649

780

1,123

1,321

FY16* FY17

UAE Southern Africa Hirslanden

REVENUE

ANALYSIS

8

2,100

20%

18%

98%

• Good organic growth

• Up 7% in constant currency

• Strong growth particularly in outpatient

activity

• Up 3% in constant currency

• Addition of Al Noor

• Revenue growth in Dubai offset by Abu

Dhabi weakness

• Up 72% in constant currency

2,749

Southern Africa (28% of Group)

Hirslanden (48% of Group)

Middle East (24% of Group)

FY17 revenue* increased 31% to £2,749m

£’m

*Underlying and includes Al Noor’s results consolidated from the effective date of the acquisition (15 Feb 2016)

2017 FULL YEAR RESULTS PRESENTATION

FY16 Hirslandenconstantcurrency

SouthernAfrican

constantcurrency

Dubai contantcurrency

Abu Dhabiconstantcurrency

Effect ofreportingcurrency

FY17

9

REVENUE BRIDGE

• Good revenue growth in constant

currency

• Driven by Switzerland and

Southern Africa

• Middle East revenue shortfall:

- Thiqa co-payments

- Doctor vacancies

- Business and operational

alignment

- Increased competition

£’m

MCME

Abu Dhabi

Pro-forma

adjustment

2,100

2,749

284 3944 12

334

-64

2,749

2017 FULL YEAR RESULTS PRESENTATION

UNDERLYING EBITDA

ANALYSIS

10

-4

70 76

139165

221

264

FY16 FY17

Corporate Cost Middle East Southern Africa Hirslanden

FY17 underlying EBITDA increased 17% to £501m

428

19%

19%

9%

• Pharmacy inflation and ongoing investment

in clinical personnel

• Ongoing change in patient mix

• Up 6% in constant currency

• Operating leverage

• Specific cost management measures

• Continued insurance mix change

• Up 5% in constant currency

• Addition of Al Noor

• Affected by revenue shortfall

• Down 5% in constant currency

501

£’m

-2

Southern Africa (33% of Group)

Hirslanden (53% of Group)

Middle East (15% of Group)

2017 FULL YEAR RESULTS PRESENTATION

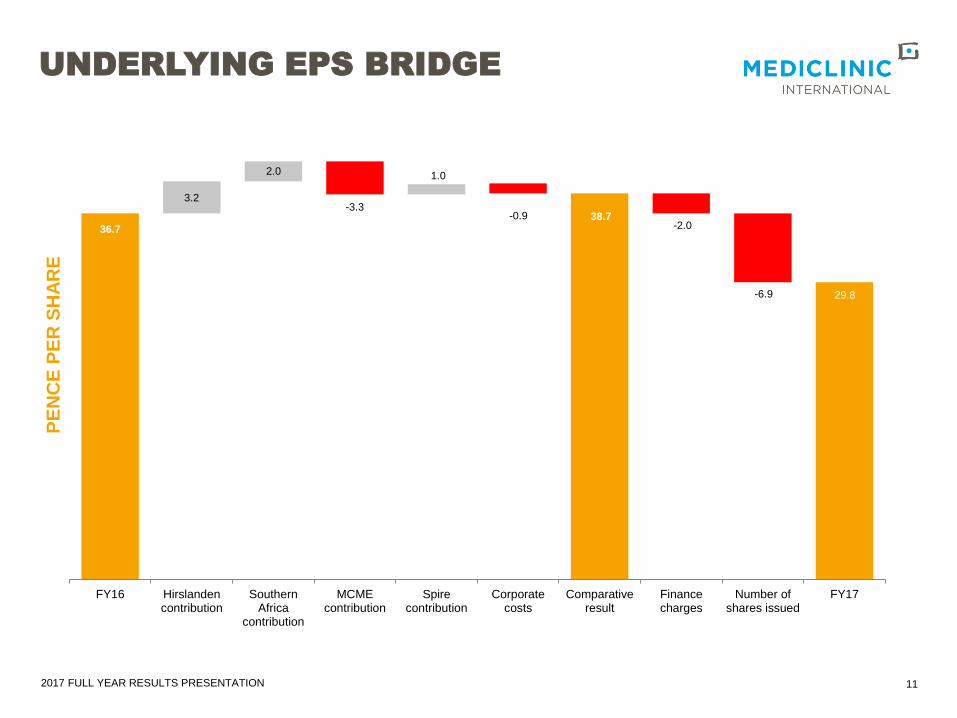

UNDERLYING EPS BRIDGE

FY16 Hirslandencontribution

SouthernAfrica

contribution

MCMEcontribution

Spirecontribution

Corporatecosts

Comparativeresult

Financecharges

Number ofshares issued

FY17

11

PE

NC

E P

ER

SH

AR

E

36.7

29.8

38.7

3.2

2.0

-3.3

1.0

-0.9-2.0

-6.9

2017 FULL YEAR RESULTS PRESENTATION

GROUP

BALANCE SHEET SUMMARY

12

£’m 31 Mar 17 31 Mar 16

Assets 7,422 6,549

Non-current assets:

Property, equipment and vehicles 3,703 3,199

Intangible assets 2,156 1,941

Other non-current assets 494 478

Current assets 1,069 931

Equity and liabilities 7,422 6,549

Shareholders’ funds 4,086 3,509

Non-controlling interests 78 61

Interest-bearing debt 2,030 1,841

Other long-term liabilities 707 668

Current liabilities 521 470

• Borrowings down in constant

currency

• Continued investment in

buildings and equipment

• Strong working capital

management

2017 FULL YEAR RESULTS PRESENTATION

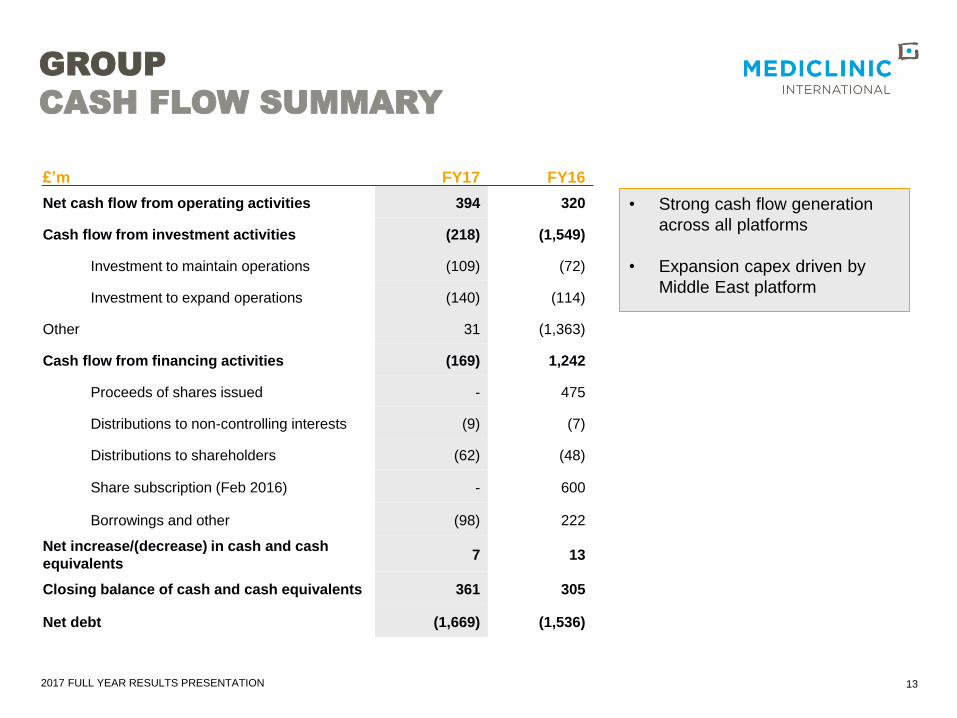

GROUP

CASH FLOW SUMMARY

13

£’m FY17 FY16

Net cash flow from operating activities 394 320

Cash flow from investment activities (218) (1,549)

Investment to maintain operations (109) (72)

Investment to expand operations (140) (114)

Other 31 (1,363)

Cash flow from financing activities (169) 1,242

Proceeds of shares issued - 475

Distributions to non-controlling interests (9) (7)

Distributions to shareholders (62) (48)

Share subscription (Feb 2016) - 600

Borrowings and other (98) 222

Net increase/(decrease) in cash and cash

equivalents7 13

Closing balance of cash and cash equivalents 361 305

Net debt (1,669) (1,536)

• Strong cash flow generation

across all platforms

• Expansion capex driven by

Middle East platform

2017 FULL YEAR RESULTS PRESENTATION

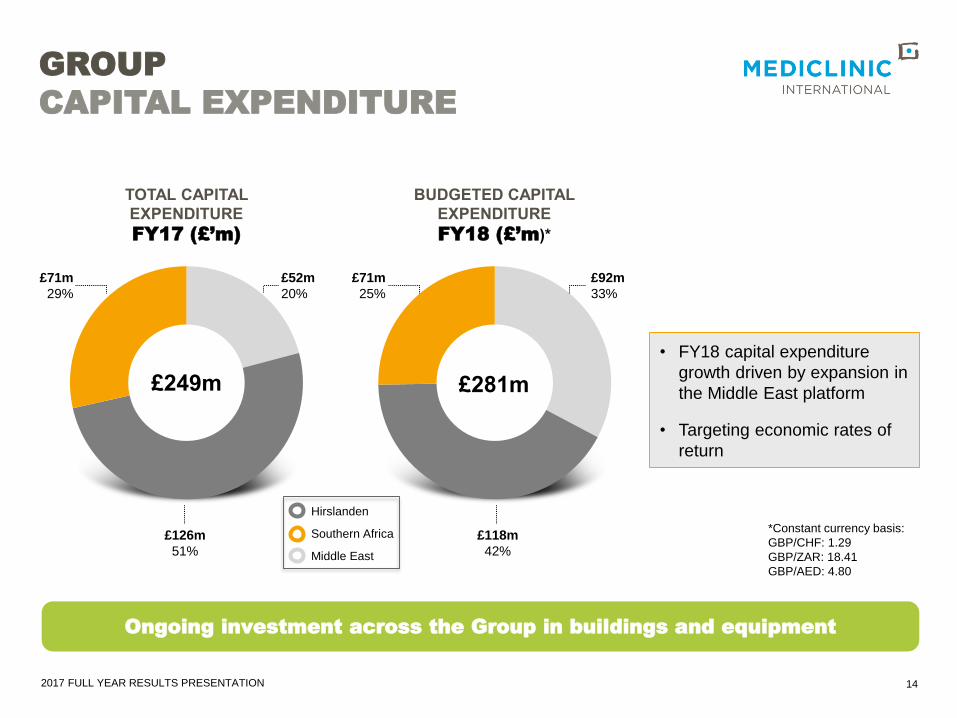

£281m£249m

GROUP

CAPITAL EXPENDITURE

TOTAL CAPITAL

EXPENDITURE

FY17 (£’m)

BUDGETED CAPITAL

EXPENDITURE

FY18 (£’m)*

14

Ongoing investment across the Group in buildings and equipment

• FY18 capital expenditure

growth driven by expansion in

the Middle East platform

• Targeting economic rates of

return

£71m

29%

£126m

51%

£118m

42%

£71m

25%

£92m

33%

£52m

20%

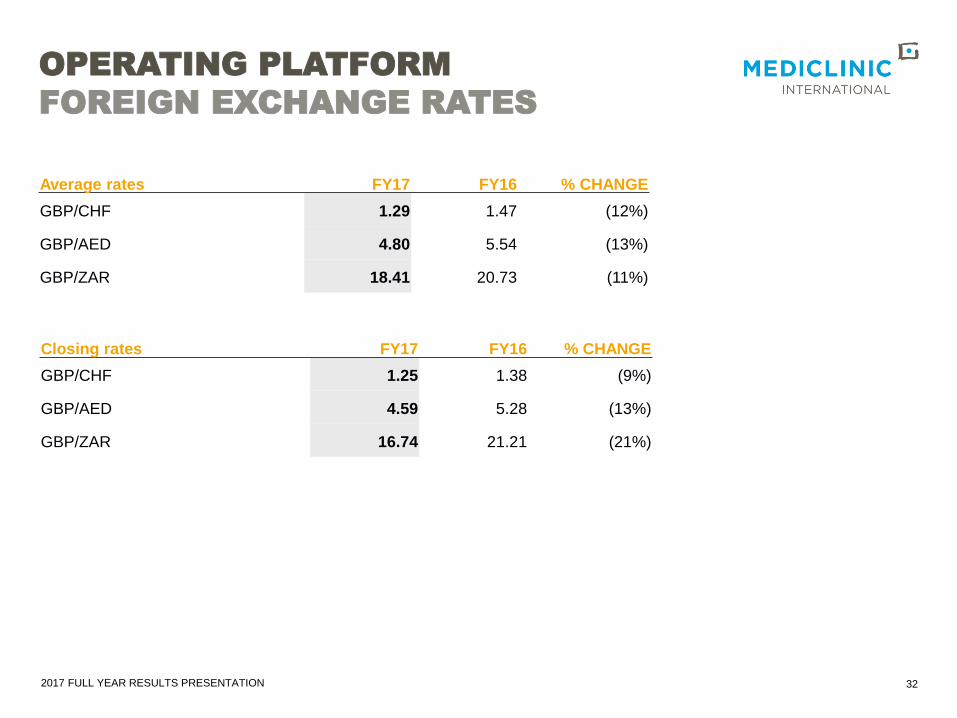

*Constant currency basis:

GBP/CHF: 1.29

GBP/ZAR: 18.41

GBP/AED: 4.80

Hirslanden

Southern Africa

Middle East

2017 FULL YEAR RESULTS PRESENTATION

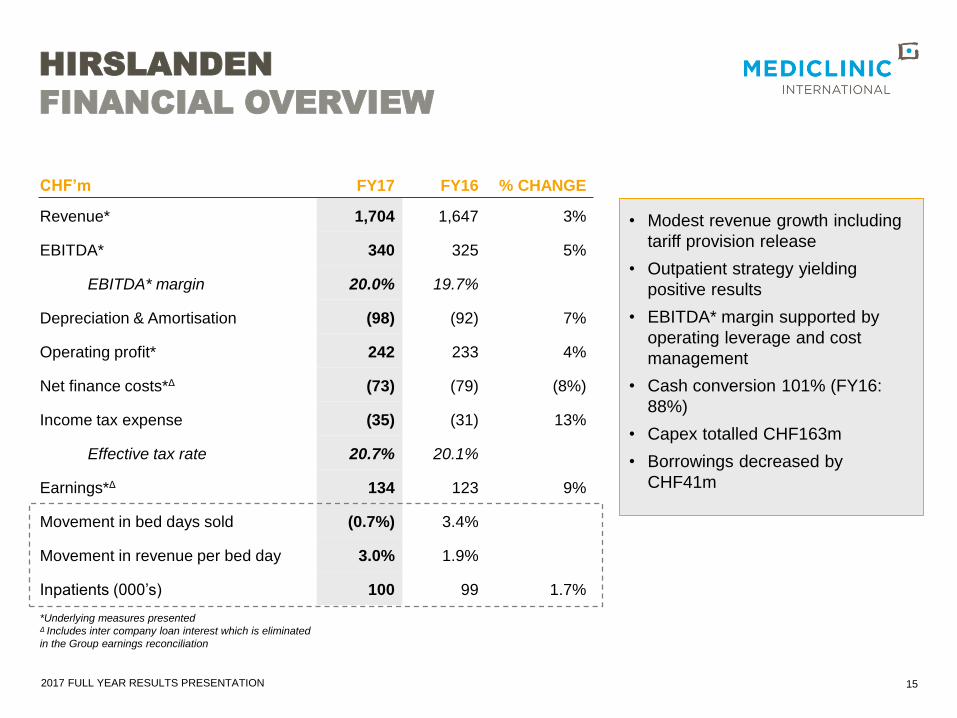

HIRSLANDEN

FINANCIAL OVERVIEW

15

• Modest revenue growth including

tariff provision release

• Outpatient strategy yielding

positive results

• EBITDA* margin supported by

operating leverage and cost

management

• Cash conversion 101% (FY16:

88%)

• Capex totalled CHF163m

• Borrowings decreased by

CHF41m

CHF’m FY17 FY16 % CHANGE

Revenue* 1,704 1,647 3%

EBITDA* 340 325 5%

EBITDA* margin 20.0% 19.7%

Depreciation & Amortisation (98) (92) 7%

Operating profit* 242 233 4%

Net finance costs*Δ (73) (79) (8%)

Income tax expense (35) (31) 13%

Effective tax rate 20.7% 20.1%

Earnings*Δ 134 123 9%

Movement in bed days sold (0.7%) 3.4%

Movement in revenue per bed day 3.0% 1.9%

Inpatients (000’s) 100 99 1.7%

*Underlying measures presentedΔ Includes inter company loan interest which is eliminated

in the Group earnings reconciliation

2017 FULL YEAR RESULTS PRESENTATION

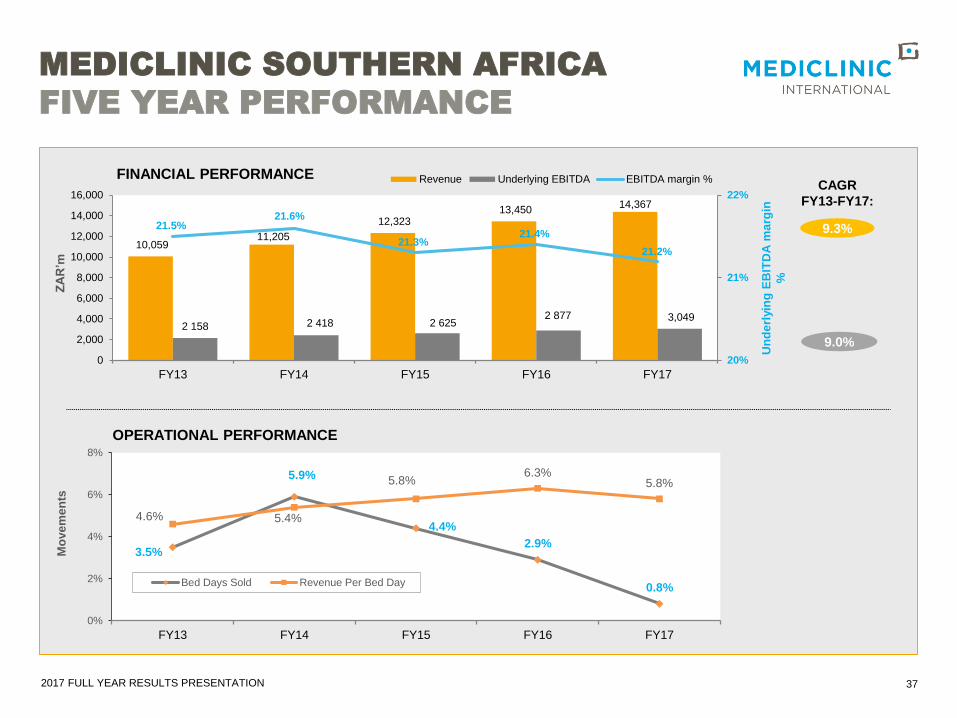

MEDICLINIC SOUTHERN AFRICA

FINANCIAL OVERVIEW

16

• Revenue growth in line with

expectations

• Bed day growth impacted by

weaker macro economic

environment and increased

competition

• EBITDA* margin impacted by

pharmacy inflation, clinical

positions and a continued

change in patient mix

• Cash conversion 104%

(2016: 109%)

• Capex totalled ZAR1,305m

• Borrowings increased by

ZAR2,791m

ZAR’m FY17 FY16 % CHANGE

Revenue 14,367 13,450 7%

EBITDA* 3,049 2,877 6%

EBITDA* margin 21.2% 21.4%

Depreciation & Amortisation (466) (414) 13%

Operating profit* 2,583 2,463 5%

Net finance costs (496) (270) 84%

Income tax expense (582) (637) (9%)

Effective tax rate 27.6% 28.8%

Earnings* 1,239 1,305 (5%)

Movement in bed days sold 0.8% 2.9%

Movement in revenue per bed day 5.8% 6.3%

Admissions (000’s) 579 575 0.6%

*Underlying measures presented

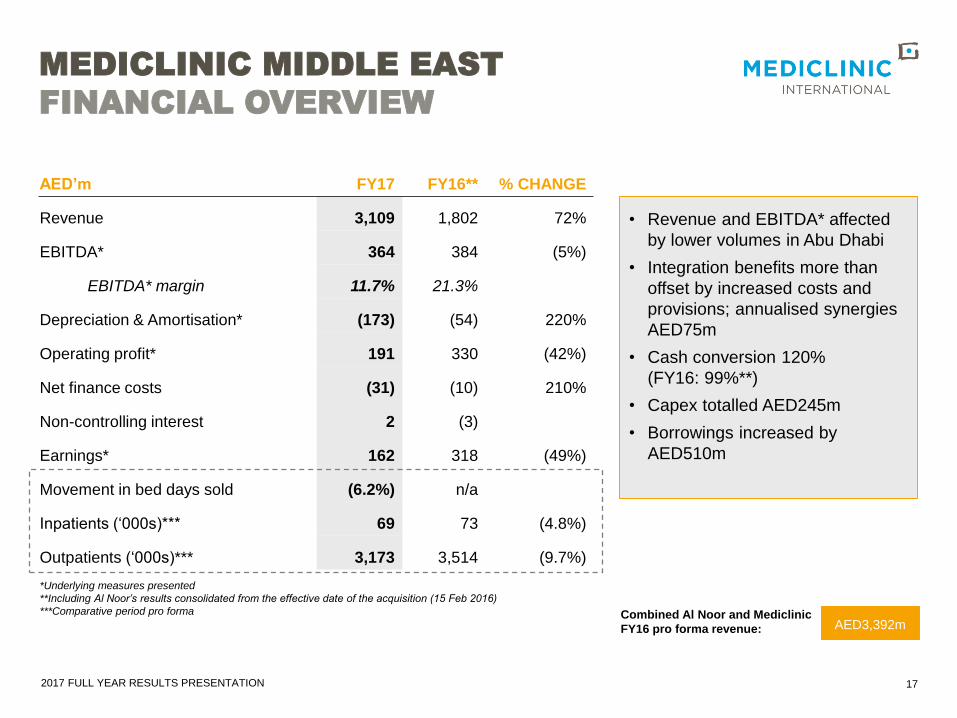

2017 FULL YEAR RESULTS PRESENTATION

AED’m FY17 FY16** % CHANGE

Revenue 3,109 1,802 72%

EBITDA* 364 384 (5%)

EBITDA* margin 11.7% 21.3%

Depreciation & Amortisation* (173) (54) 220%

Operating profit* 191 330 (42%)

Net finance costs (31) (10) 210%

Non-controlling interest 2 (3)

Earnings* 162 318 (49%)

Movement in bed days sold (6.2%) n/a

Inpatients (‘000s)*** 69 73 (4.8%)

Outpatients (‘000s)*** 3,173 3,514 (9.7%)

*Underlying measures presented

**Including Al Noor’s results consolidated from the effective date of the acquisition (15 Feb 2016)

***Comparative period pro forma

MEDICLINIC MIDDLE EAST

FINANCIAL OVERVIEW

17

• Revenue and EBITDA* affected

by lower volumes in Abu Dhabi

• Integration benefits more than

offset by increased costs and

provisions; annualised synergies

AED75m

• Cash conversion 120%

(FY16: 99%**)

• Capex totalled AED245m

• Borrowings increased by

AED510m

AED3,392mCombined Al Noor and Mediclinic

FY16 pro forma revenue:

2017 FULL YEAR RESULTS PRESENTATION

MEDICLINIC INTERNATIONAL

FY18 OUTLOOK

18

HIRSLANDEN

MEDICLINIC

SOUTHERN

AFRICA

MEDICLINIC

MIDDLE

EAST

• Modest revenue growth given already high occupancy rates, stable beds and Easter

impact

• Lower underlying EBITDA margin due to tariff and regulatory environment, increasing

costs and assuming no further net tariff provision benefits; partly offset by ongoing

efficiency gains

• Revenue growth in line with inflation due to challenging macro-economic environment,

greater competition, funder constraints and Easter impact

• Broadly stable underlying EBITDA margin despite cost inflation running above tariff

increases

• Dubai: Performance expected to remain stable despite the competitive landscape

• Abu Dhabi: Gradual improvement over the next couple of years

• MCME: Modest improvement in revenue for the full year

• MCME: Gradual improvement in underlying EBITDA margins over time, including the

impact associated with the opening of new facilities

• MCME: 1H FY18 performance down versus 1H FY17 due to lower patient volumes

and revenues in Abu Dhabi following the Thiqa co-payment introduction, asset sales

and business and operational alignment initiatives

2017 FULL YEAR RESULTS PRESENTATION

OPERATIONAL

REVIEW

DANIE MEINTJES

CEO MEDICLINIC INTERNATIONAL

2017 FULL YEAR RESULTS PRESENTATION

OPERATIONS

HIRSLANDEN

20

Competitive, mature healthcare market

Further increase in productivity through

continued cost focus

High occupancy rates, particularly in

second half of the year

Ongoing investment including outpatient

service development and Hirslanden 2020

Continued change in insurance mix

Ongoing review of regulations at a Federal

and Cantonal level including TARMED and

outmigration

OPERATIONS OPERATIONAL OVERVIEW

HOSPITALS

16

BEDS

1,677

CLINICS

4

EMPLOYEES

9,402

BED NUMBERS AND OCCUPANCY

1,487

1,567

1,655 1,677 1,677

73.3%

75.3%76.2% 76.3% 76.2%

70%

75%

80%

85%

1,000

1,200

1,400

1,600

1,800

FY13 FY14 FY15 FY16 FY17

Operational beds Bed occupancy rate

NU

MB

ER

OF

BE

DS

BE

D O

CC

UP

AN

CY

RA

TE

2017 FULL YEAR RESULTS PRESENTATION

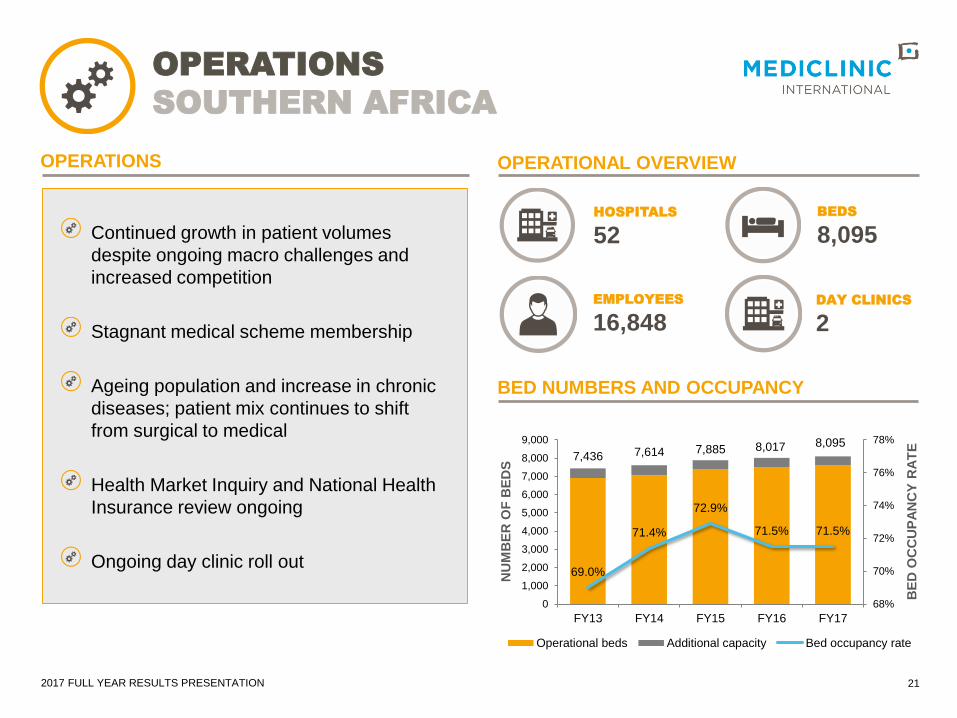

OPERATIONS

SOUTHERN AFRICA

OPERATIONS

Continued growth in patient volumes

despite ongoing macro challenges and

increased competition

Stagnant medical scheme membership

Ageing population and increase in chronic

diseases; patient mix continues to shift

from surgical to medical

Health Market Inquiry and National Health

Insurance review ongoing

Ongoing day clinic roll out

OPERATIONAL OVERVIEW

HOSPITALS

52

EMPLOYEES

16,848

BEDS

8,095

BED NUMBERS AND OCCUPANCY

DAY CLINICS

2

7,436 7,614 7,885 8,017 8,095

69.0%

71.4%

72.9%

71.5% 71.5%

68%

70%

72%

74%

76%

78%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

FY13 FY14 FY15 FY16 FY17

Operational beds Additional capacity Bed occupancy rate

NU

MB

ER

OF

BE

DS

BE

D O

CC

UP

AN

CY

RA

TE

21

2017 FULL YEAR RESULTS PRESENTATION

OPERATIONS

MIDDLE EAST

Long term opportunities in UAE remain

strong; supports expansion strategy

Thiqa co-payments significantly impacted

Abu Dhabi volumes in addition to business

and operational alignment initiatives,

increased competition, doctor vacancies

and the sale of several non-core assets

Focused on doctor recruitment and new

insurance mix and tariff strategy

Encouraging patient activity since opening

the new Mediclinic City Hospital North Wing

and Mediclinic Al Jowhara Hospital

Mediclinic Parkview Hospital project

progressing in Dubai

INPATIENT VOLUMES IN ABU DHABI

OPERATIONS OPERATIONAL OVERVIEW

HOSPITALS

6

BEDS

714

CLINICS

31

EMPLOYEES

6,375

OUTPATIENT VOLUMES* (‘000) IN ABU DHABI

FY16 FY17 Movement

Daman - Basic Plan 15,937 15,823 -1%

Daman - Enhanced 7,671 6,885 -10%

Daman - Thiqa 8,055 5,416 -33%

Others 8,184 6,940 -15%

Total 39,847 35,064 -12%

’000s FY16 FY17 Movement

Daman - Basic Plan 841 772 -8%

Daman - Enhanced 425 356 -16%

Daman - Thiqa 519 360 -31%

Others 568 488 -14%

Total 2,353 1,976 -16%

22

*Outpatient volumes by insurance mix show paid attendances, excluding follow up

visits. Abu Dhabi outpatient attendance including follow up visits declined by 14%.

2017 FULL YEAR RESULTS PRESENTATION

SPIRE HEALTHCARE GROUP PLC

UNITED KINGDOM

23

• Mediclinic’s 29.9% investment in Spire

remained stable and gives the Group

exposure to UK private healthcare market

• Full Year 2016 performance was in line with

expectations, after adjusting for St Anthony’s

• Strong growth in Self-pay and NHS business;

increased market share in the PMI sector

• Investment continued at the new Spire

Manchester and Spire Nottingham hospitals

• Management expects growth in all payor

groups (including the PMI business) over the

medium to long term as a result of an under

funded NHS plus favourable healthcare

demographics

• Spire is ideally positioned to be a leading

player in the independent hospital sector

given its scale, reach and quality of care

STRATEGY

DANIE MEINTJES

CEO MEDICLINIC INTERNATIONAL

2017 FULL YEAR RESULTS PRESENTATION

MEDICLINIC INTERNATIONAL

EVOLVING HEALTHCARE INDUSTRY

25

GLOBAL DEMAND FOR HIGH-

QUALITY HEALTHCARE SERVICES

REMAINS ROBUST

• Underpinned by an ageing population, growing

disease burden and new technology

Mediclinic focusses on high-quality care and optimal patient experience

• Increases the pressure on patients and funders LOWER ECONOMIC GROWTH

• Resulting in changing care delivery models and

greater regulatory oversight

INCREASED FOCUS ON

AFFORDABILITY OF DELIVERING

HEALTHCARE

• Impacts patient choice and service offerings GREATER COMPETITION

2017 FULL YEAR RESULTS PRESENTATION

81.80% 82.90%81.90% 82.10%

April - Sept 2016 October 2016 - March 2017

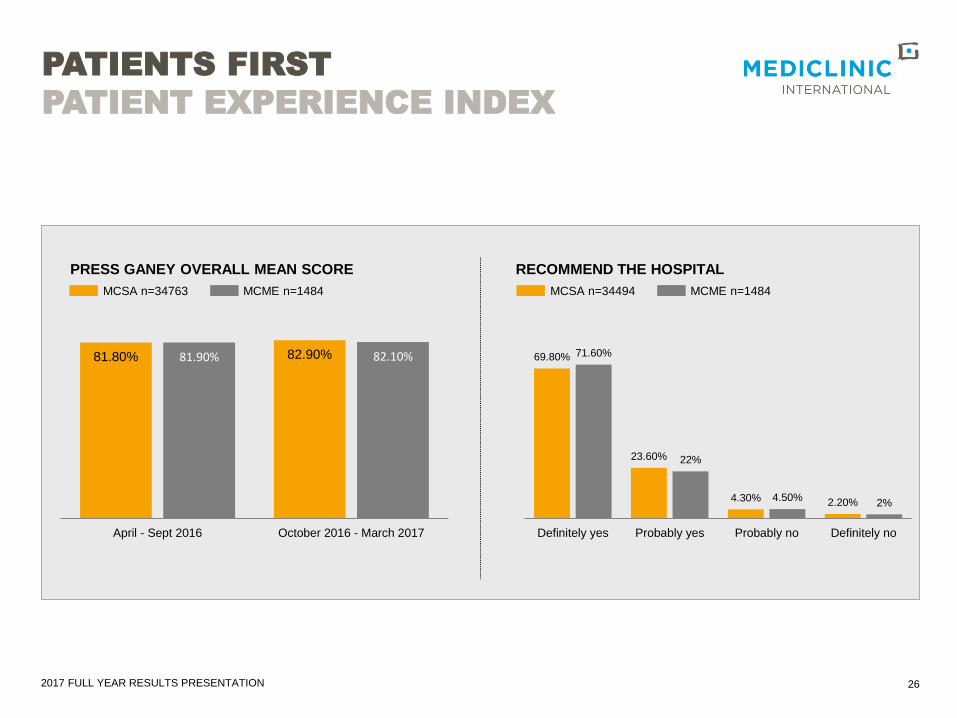

PATIENTS FIRST

PATIENT EXPERIENCE INDEX

PRESS GANEY OVERALL MEAN SCORE RECOMMEND THE HOSPITAL

MCSA n=34763 MCME n=1484

26

69.80%

23.60%

4.30% 2.20%

71.60%

22%

4.50%2%

Definitely yes Probably yes Probably no Definitely no

MCSA n=34494 MCME n=1484

2017 FULL YEAR RESULTS PRESENTATION

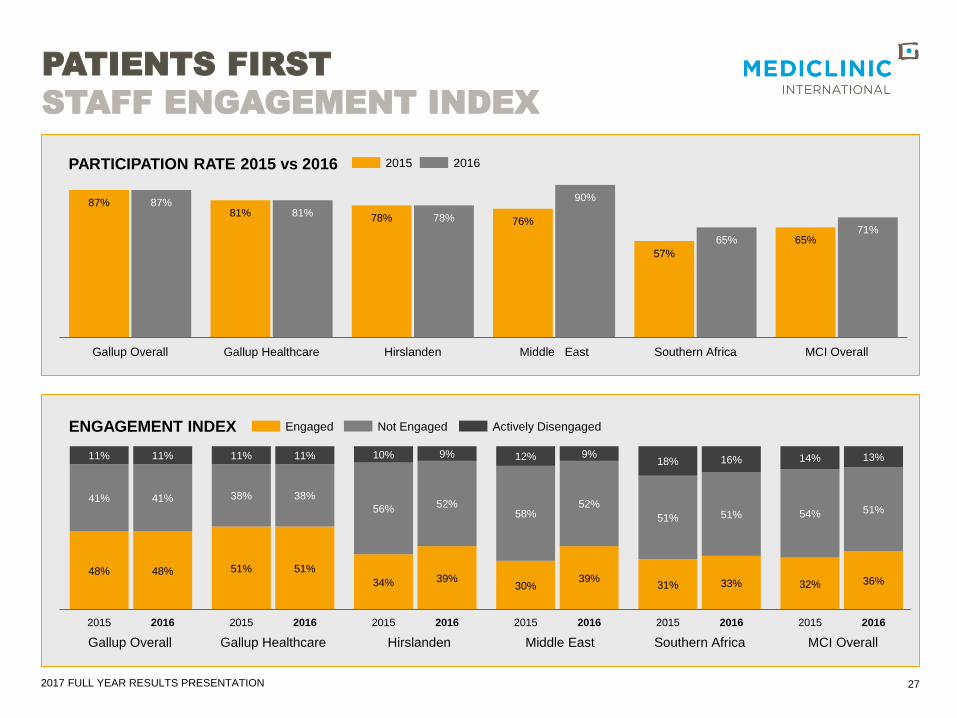

48% 51%

34% 30% 31% 32%

41% 38%

56% 58% 51% 54%

11% 11% 10% 12% 18% 14%

2015 2015 2015 2015 2015 2015

48% 51%39% 39% 33% 36%

41% 38%52% 52%

51% 51%

11% 11% 9% 9%16% 13%

2016 2016 2016 2016 2016 2016

PATIENTS FIRST

STAFF ENGAGEMENT INDEX

87%81%

78% 76%

57%

65%

87%81%

78%

90%

65%71%

Gallup Overall Gallup Healthcare Hirslanden Middle East Southern Africa MCI Overall

27

PARTICIPATION RATE 2015 vs 2016 2015 2016

Engaged Not EngagedENGAGEMENT INDEX Actively Disengaged

Gallup Overall Gallup Healthcare Hirslanden Middle East Southern Africa MCI Overall

2017 FULL YEAR RESULTS PRESENTATION

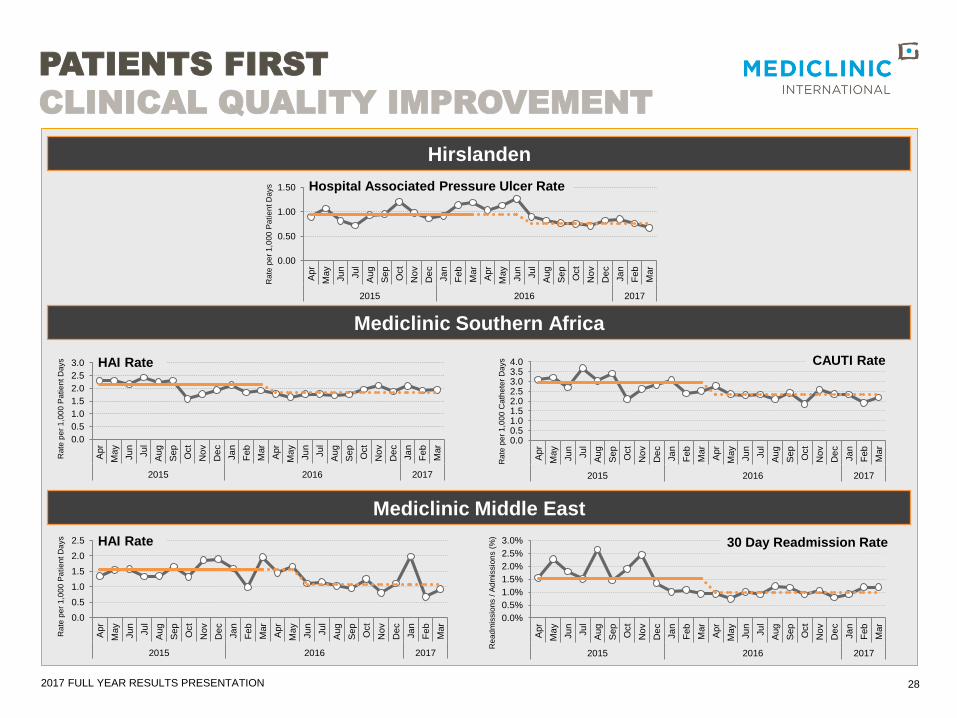

PATIENTS FIRST

CLINICAL QUALITY IMPROVEMENT

28

Mediclinic Southern Africa

Mediclinic Middle East

Hirslanden

0.00

0.50

1.00

1.50

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

No

v

De

c

Ja

n

Feb

Mar

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

No

v

De

c

Ja

n

Feb

Mar

2015 2016 2017

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

No

v

De

c

Ja

n

Feb

Mar

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

No

v

De

c

Ja

n

Feb

Mar

2015 2016 2017

0.00.51.01.52.02.53.03.54.0

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

No

v

De

c

Ja

n

Feb

Mar

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

No

v

De

c

Ja

n

Feb

Mar

2015 2016 2017

0.0

0.5

1.0

1.5

2.0

2.5

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

No

v

De

c

Ja

n

Feb

Mar

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

No

v

De

c

Ja

n

Feb

Mar

2015 2016 2017

HAI Rate CAUTI Rate

Hospital Associated Pressure Ulcer Rate

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%A

pr

May

Ju

n

Ju

l

Aug

Sep

Oct

No

v

De

c

Ja

n

Feb

Mar

Apr

May

Ju

n

Ju

l

Aug

Sep

Oct

No

v

De

c

Ja

n

Feb

Mar

2015 2016 2017

30 Day Readmission Rate

Rea

dm

issio

ns /

Ad

mis

sio

ns (

%)

Rate

pe

r 1

,00

0 C

ath

ete

r D

ays

Rate

pe

r 1

,00

0 P

atie

nt D

ays

Rate

pe

r 1

,00

0 P

atie

nt D

ays

Rate

pe

r 1

,00

0 P

atie

nt D

ays

HAI Rate

2017 FULL YEAR RESULTS PRESENTATION

MEDICLINIC INTERNATIONAL

STRATEGY

29

29

CONTINUING TO GROW

IMPROVING EFFICIENCIES

PUTTING

“PATIENTS FIRST”

• Increased capacity at existing infrastructure

• Acquisitive or organic growth in existing platforms

• Further international acquisitions

• Superior clinical performance in a safe clinical environment

• Improved patient experience

• Integrated and coordinated care

29INVESTING IN EMPLOYEES

• Identifying, attract and retain leading specialists and talented

healthcare professionals

• Improve employee engagement

• Improved operational effectiveness

- Leverage combined international capacity through collaboration and

shared resources

- Pursue initiatives in operating platforms to improve operational efficiency

• Leveraged international group benefits

- Use central resources to achieve Group wide procurement efficiencies

Create long-term shareholder value

QUESTIONS

AND ANSWERS

James Arnold

Head of Investor Relations

MEDICLINIC INTERNATIONAL PLC

14 Curzon Street

London

W1J 5HN

United Kingdom

Tel: +44 (0) 20 3786 8181

www.mediclinic.com

APPENDIX

2017 FULL YEAR RESULTS PRESENTATION

OPERATING PLATFORM

FOREIGN EXCHANGE RATES

32

Average rates FY17 FY16 % CHANGE

GBP/CHF 1.29 1.47 (12%)

GBP/AED 4.80 5.54 (13%)

GBP/ZAR 18.41 20.73 (11%)

Closing rates FY17 FY16 % CHANGE

GBP/CHF 1.25 1.38 (9%)

GBP/AED 4.59 5.28 (13%)

GBP/ZAR 16.74 21.21 (21%)

2017 FULL YEAR RESULTS PRESENTATION

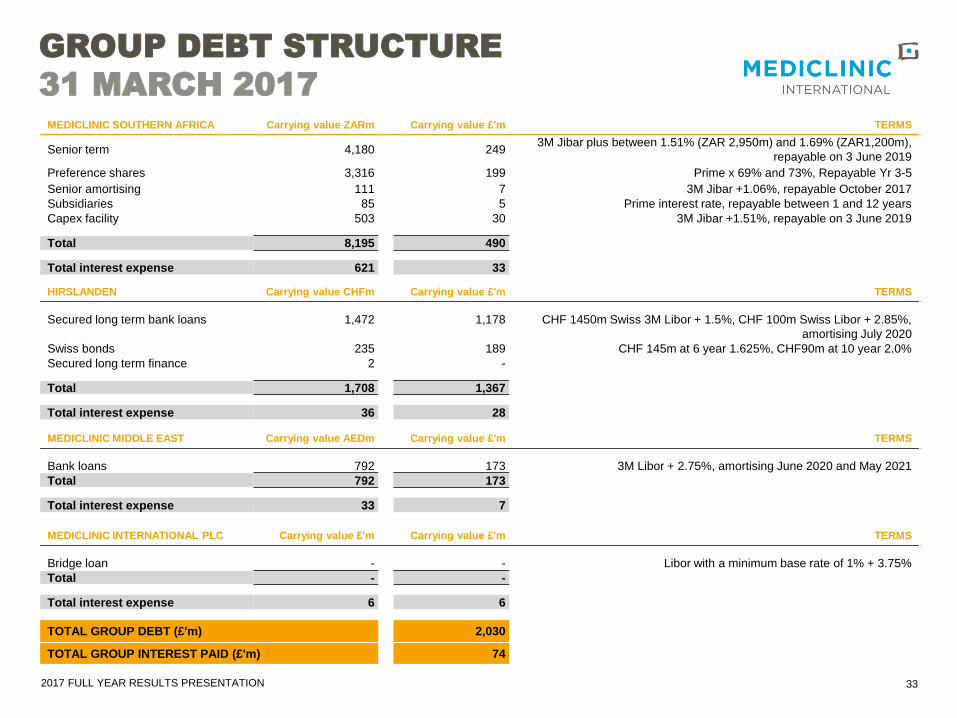

GROUP DEBT STRUCTURE

31 MARCH 2017

MEDICLINIC SOUTHERN AFRICA Carrying value ZARm Carrying value £'m TERMS

Senior term 4,180 249 3M Jibar plus between 1.51% (ZAR 2,950m) and 1.69% (ZAR1,200m),

repayable on 3 June 2019

Preference shares 3,316 199 Prime x 69% and 73%, Repayable Yr 3-5

Senior amortising 111 7 3M Jibar +1.06%, repayable October 2017

Subsidiaries 85 5 Prime interest rate, repayable between 1 and 12 years

Capex facility 503 30 3M Jibar +1.51%, repayable on 3 June 2019

Total 8,195 490

Total interest expense 621 33

HIRSLANDEN Carrying value CHFm Carrying value £'m TERMS

Secured long term bank loans 1,472 1,178 CHF 1450m Swiss 3M Libor + 1.5%, CHF 100m Swiss Libor + 2.85%,

amortising July 2020

Swiss bonds 235 189 CHF 145m at 6 year 1.625%, CHF90m at 10 year 2.0%

Secured long term finance 2 -

Total 1,708 1,367

Total interest expense 36 28

MEDICLINIC MIDDLE EAST Carrying value AEDm Carrying value £'m TERMS

Bank loans 792 173 3M Libor + 2.75%, amortising June 2020 and May 2021

Total 792 173

Total interest expense 33 7

MEDICLINIC INTERNATIONAL PLC Carrying value £'m Carrying value £'m TERMS

Bridge loan - - Libor with a minimum base rate of 1% + 3.75%

Total - -

Total interest expense 6 6

TOTAL GROUP DEBT (£'m) 2,030

TOTAL GROUP INTEREST PAID (£'m) 74

33

2017 FULL YEAR RESULTS PRESENTATION

GROUP

CAPITAL EXPENDITURE

34

FY17 Actual capex (£’m) Hirslanden Southern Africa Middle East Total

To maintain operations 69 28 12 109

To expand operations 57 43 40 140

Total capital expenditure 126 71 52 249

FY18 Budgeted capex (£’m)* Hirslanden Southern Africa Middle East Total

To maintain operations 65 19 16 100

To expand operations 53 52 76 181

Total capital expenditure 118 71 92 281

• Hirslanden: Hirslanden 2020 and HQ relocation. Expansion includes acquisition of building in Bern

• MCSA: Maintaining 52 hospitals. Expansion increased beds by 78 during the year

• MCME: Mediclinic City Hospital North Wing and Parkview Hospitals

• Hirslanden: Ongoing investment projects

• MCSA: Gradual expansion programme continues; excludes Klerksdorp investment awaiting CC approval

• MCME: Mediclinic Parkview Hospital and other expansion

*Constant currency basis: GBP/CHF: 1.29, GBP/ZAR: 4.80, GBP/AED: 18.41

2017 FULL YEAR RESULTS PRESENTATION

2.1%

5.6%

8.4%

3.4%

-0.7%2.5%

4.4%1.2%

1.9%

3.0%

-1%

1%

3%

5%

7%

9%

FY13 FY14 FY15 FY16 FY17

Bed Days Sold Revenue Per Bed Day

35

HIRSLANDEN

FIVE YEAR PERFORMANCE

1,330 1,436

1,563 1,647 1,704

286 298 303325 340

21.5%

20.8%

19.4%19.7%

20.0%

18%

19%

20%

21%

22%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

FY13 FY14 FY15 FY16 FY17

Revenue Underlying EBITDA EBITDA margin %

CH

F’m

Un

de

rlyin

g E

BIT

DA

ma

rgin

%

6.4%

4.4%

FINANCIAL PERFORMANCE CAGR

FY13-FY17:

Mo

ve

me

nts

OPERATIONAL PERFORMANCE

39.6%41.4%

42.7% 43.5%44.8%

34.0% 33.0% 32.3% 31.9% 31.2%

26.4%25.6% 25.0% 24.6% 24.0%

20%

25%

30%

35%

40%

45%

FY13 FY14 FY15 FY16 FY17

Basic Semiprivate Private

PATIENT MIX

2017 FULL YEAR RESULTS PRESENTATION

CAPITAL PROJECTS

HIRSLANDEN

36

Hospital Project Completion

Clinique Cecil Hybrid operating theatre 1H17

Clinique La Colline Doctor’s consulting rooms 1H17

Klinik Stephanshorn Restructuring of radiology 1H17

Klinik Aarau Third cardiac catheterisation laboratory 1H17

Klinik Permanence Restructuring of sterilisation unit 2H17

Klinik St. Anna Modular operating theatres 2H17

Klinik Stephanshorn Modular operating theatres 2H17

Klinik Hirslanden Restructuring of emergency department 2H17

Hospital Project

Expected

Completion

Klinik St. Anna MRI 3 Tesla 1H18

Klinik Stephanshorn Restructuring of entrance 1H18

Klinik Birshof O-arm® Surgical Imaging system 1H18

Klinik St. Anna O-arm® Surgical Imaging system 1H18

Klinik Stephanshorn Operating roboter DaVinci 1H18

Klinik Im Park Outpatient surgery unit “Bellaria” 1H18

Klinik Hirslanden Capacity expansion; MRI, gastroenterology & stroke unit FY18

AndreasKlinik (Cham) Medical centre/physicians house FY18

Klinik Permanence Radiology institute “Cosmos” FY18

Klinik Birshof Medical centre/physicians house FY19

Clinique La Colline Sport medicine centre FY19

Klinik Stephanshorn (Schuppis) Medical centre FY19

Klinik Hirslanden (Seefeldstrasse) Medical centre FY19

CAPITAL PROJECTS DURING 2017

FUTURE PROJECTS

2017 FULL YEAR RESULTS PRESENTATION

3.5%

5.9%

4.4%

2.9%

0.8%

4.6% 5.4%

5.8%6.3%

5.8%

0%

2%

4%

6%

8%

FY13 FY14 FY15 FY16 FY17

Bed Days Sold Revenue Per Bed Day

37

MEDICLINIC SOUTHERN AFRICA

FIVE YEAR PERFORMANCE

10,059 11,205

12,323 13,450

14,367

2 158 2 418 2 6252 877 3,049

21.5%21.6%

21.3%21.4%

21.2%

20%

21%

22%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY13 FY14 FY15 FY16 FY17

Revenue Underlying EBITDA EBITDA margin %

ZA

R’m

Un

de

rlyin

g E

BIT

DA

ma

rgin

%

9.3%

9.0%

FINANCIAL PERFORMANCECAGR

FY13-FY17:

Mo

ve

me

nts

OPERATIONAL PERFORMANCE

2017 FULL YEAR RESULTS PRESENTATION 38

CAPITAL PROJECTS

SOUTHERN AFRICA

Hospital Completion Beds

Growth into existing license

Mediclinic Upington 1H17 26

Mediclinic Emfuleni 2H17 17

Mediclinic Worcester 2H17 20

Mediclinic Bloemfontein 2H17 4

Mediclinic Windhoek 2H17 11

Total licenced beds Year end 2017 8,095

Hospital Expected Completion Beds

Existing licenses

Mediclinic Bloemfontein 1H18 12

Mediclinic Thabazimbi 2H18 12

Mediclinic Newcastle 2H18 30

Mediclinic Midstream 1H19 11

Mediclinic Legae 2H19 23

Mediclinic Vergelegen 2H19 28

Mediclinic Cape Gate 1H20 13

Mediclinic Potchefstroom 1H20 70

Mediclinic Stellenbosch 1H20 70

Mediclinic Medforum 2H20 81

Day clinicsMediclinic Nelspruit Day Clinic 1H20 16

Mediclinic Bloemfontein Day Clinic 2H20 22

Mediclinic Cape Gate Day Clinic 2H20 16

Additional/new facilities

Klerksdorp Awaiting CC approval 256

Life Path Health Completing DD – then requires CC approval 308

*Subject to DOH Approval

CAPITAL PROJECTS DURING 2017

FUTURE PROJECTS*

2017 FULL YEAR RESULTS PRESENTATION 39

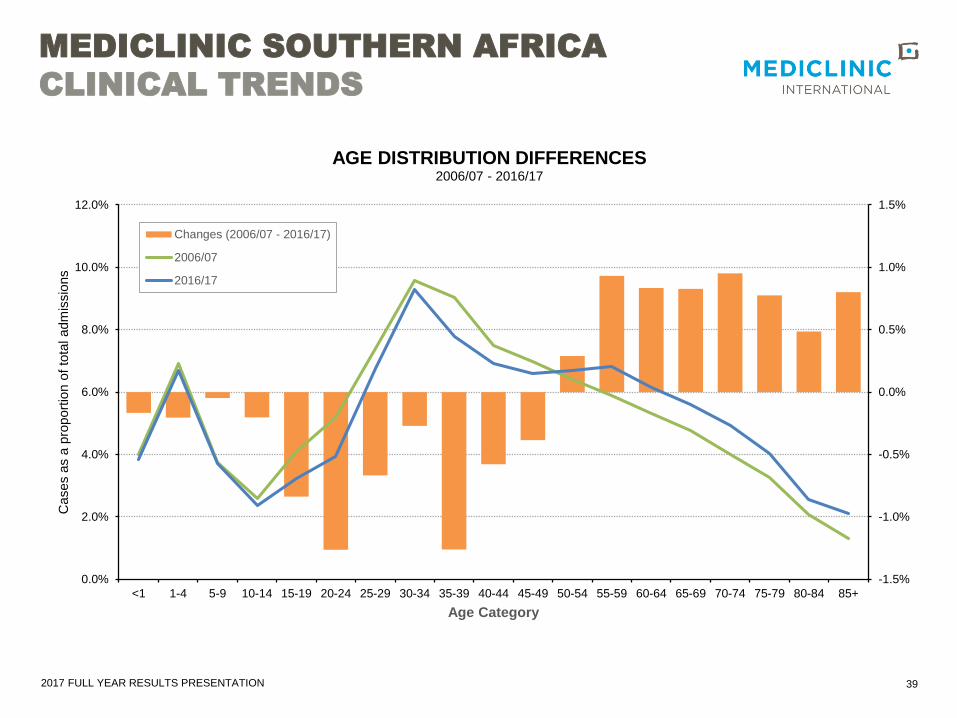

MEDICLINIC SOUTHERN AFRICA

CLINICAL TRENDS

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

<1 1-4 5-9 10-14 15-19 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80-84 85+

Cases a

s a

pro

port

ion o

f to

tal adm

issio

ns

Age Category

AGE DISTRIBUTION DIFFERENCES2006/07 - 2016/17

Changes (2006/07 - 2016/17)

2006/07

2016/17

2017 FULL YEAR RESULTS PRESENTATION 40

MEDICLINIC SOUTHERN AFRICA

CLINICAL TRENDS

6.4%

11.1%

14.4%

15.9%16.8%

16.2%

14.8%15.5%

17.1%

19.0%

24.2%

29.6% 29.7% 29.9%30.6% 30.8%

32.6%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17

Pro

port

ion o

f C

ases w

ith a

Chro

nic

Dis

ease C

ode

Financial Year

CHRONIC DISEASE CODED

Note: Pre 2011/12 data not

comparable with subsequent years

2017 FULL YEAR RESULTS PRESENTATION 41

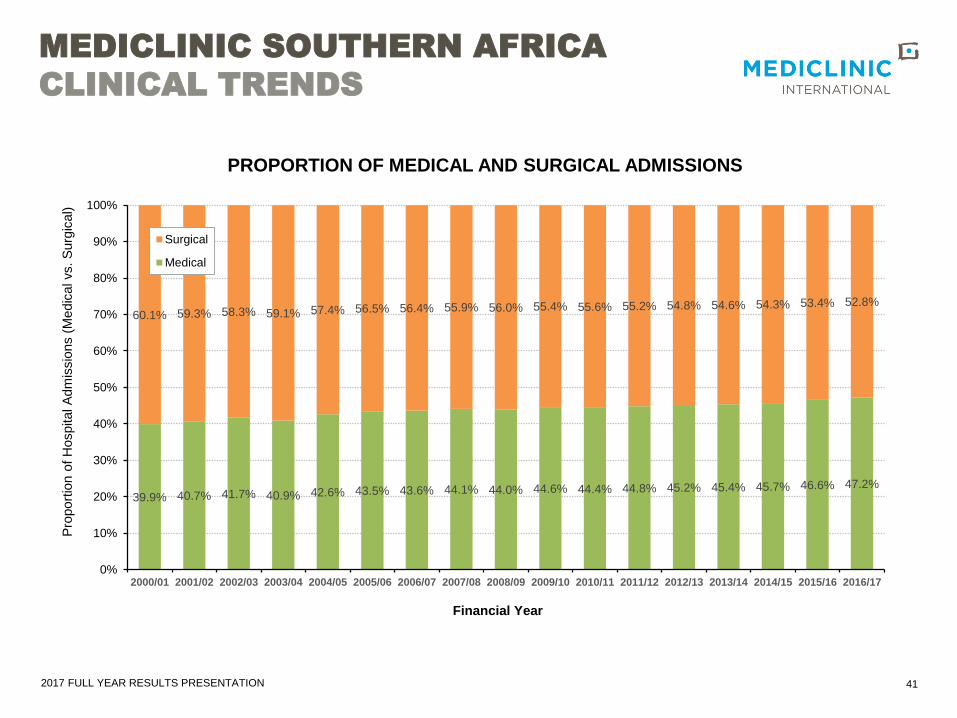

MEDICLINIC SOUTHERN AFRICA

CLINICAL TRENDS

39.9% 40.7% 41.7% 40.9% 42.6% 43.5% 43.6% 44.1% 44.0% 44.6% 44.4% 44.8% 45.2% 45.4% 45.7% 46.6% 47.2%

60.1% 59.3% 58.3% 59.1% 57.4% 56.5% 56.4% 55.9% 56.0% 55.4% 55.6% 55.2% 54.8% 54.6% 54.3% 53.4% 52.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17

Pro

port

ion o

f H

ospital A

dm

issio

ns (

Medic

al vs. S

urg

ical)

Financial Year

PROPORTION OF MEDICAL AND SURGICAL ADMISSIONS

Surgical

Medical

2017 FULL YEAR RESULTS PRESENTATION 42

68.9% 67.9% 69.1% 70.0% 70.9% 71.0% 70.8% 71.2% 71.6% 71.7% 71.8% 72.5% 73.1% 73.7% 74.2% 75.0% 75.5%

31.1% 32.1% 30.9% 30.0% 29.1% 29.0% 29.2% 28.8% 28.4% 28.3% 28.2% 27.5% 26.9% 26.3% 25.8% 25.0% 24.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17

Pro

po

rtio

n o

f H

osp

ita

l A

dm

issio

ns (

Day C

ase

s v

s.

Inp

atie

nts

)

Financial Year

PROPORTION OF DAY CASES AND INPATIENT ADMISSIONS

Daycase

Inpatient

MEDICLINIC SOUTHERN AFRICA

CLINICAL TRENDS

2017 FULL YEAR RESULTS PRESENTATION

• Acquired land on the Umm Suqeim Road Al Barsha in March 2015

• Commenced building in 2016; Projected completion in Q4 FY19

• Creating 188 new beds (phased commissioning period)

• General hospital including cardiology, ER, Maternity and NICU

• Budgeted capex: AED680m (c.75% of total spent over FY18 & FY19)

ARTIST’S IMPRESSION CURRENT PROGRESS• Completed in September 2016

• State of the art Comprehensive Cancer Centre built in collaboration

with Hirslanden

• Construction and commissioning completed within budget at AED255m

• 61 net additional beds created at City Hospital

• 27 in North Wing

• 34 in main hospital (12 commissioned during FY18)

• Strong initial patient volumes

MEDICLINIC CITY HOSPITAL NORTH WING

MEDICLINIC PARKVIEW HOSPITAL

43

CAPITAL PROJECTS

DUBAI

2017 FULL YEAR RESULTS PRESENTATION

• Campus expansion

• Comprehensive Cancer Centre

• Completion expected Q4 FY19

MEDICLINIC AIRPORT ROAD HOSPITAL

MEDICLINIC AL NOOR HOSPITAL (KHALIFA STREET)

• Currently reviewing all expansion and upgrade plans for the hospital

• Finalise plans during 1H FY18

44

• 51 bed hospital (43 beds opened FY17)

• General hospital with a focus on maternity

• Opened Q3 FY17

• Well located to serve Thiqa patients

MEDICLINIC AL JOWHARA HOSPITAL

• Al Yaher Clinic:

Opened in Q2 FY17

• Ghayathi Clinic:

Opened in Q3 FY17

• Aspetar Clinic:

Opened in Q3 FY17

• Khalifa City A Clinic:

Recently opened in Q1 FY18

EXPANDING MEDICAL NETWORKS

CAPITAL PROJECTS

ABU DHABI