Full year results Analyst & Investor presentation -...

51

Full year results Analyst & Investor presentation Tuesday 20 November 2012 1 1

Transcript of Full year results Analyst & Investor presentation -...

Full year results Analyst & Investor

presentation Tuesday 20 November 2012

1 1

2 2

Agenda

1. Review of F’12

2. Financial review

3. Business review

3

Introduction

Carolyn McCall

Chief Executive Officer

4 4

0 .83

3 .36

3 .97

4.81

1.6%

6.3%

7.2%

8.2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

0

1

2

3

4

5

6

2009 2010 2011 2012

PB

T m

arg

in

PB

T /

se

at

PBT / seat PBT Margin

85%

87%

76%

83%

77%

80%

77% 76%

82%

87%

80%

89%

FY'11 FY'12

KLM Lufthansa Air France British Airways Ryanair easyJet

Review of F’12

Excellent customer satisfaction(2) Industry leading on-time performance(1)

Improving returns(3)

(1) On-time performance figures from flight stat.com & reflect average number of arrivals within 15 minutes for period Oct 11 to Sept 12 (2) GfK Customer Satisfaction Tracker. Data updated October 2012 reflecting 12m to end Sept 2012 (3) See appendix for details of calculation; also shows ROCE with leases capitalised on an NPV basis.

FY'11 FY'12 FY'11 FY'12 FY'11 FY'12

Overall

Satisfaction

Satisfaction

with Punctuality

Likelihood to

recommend

79% 80% 82%82%87%

84%

Profit per seat growth

3.6%

8.8%

12.7%

14.5%

3.6%

6.9%

9.8%

11.3%

2009 2010 2011 2012

ROCE excl. operating lease adjustment ROCE incl. operating lease adjustment

5

Financial review

Chris Kennedy

Chief Financial Officer

6 6

4.810.22

4.14

0.123.97

Summary

PBT £ per seat • Returns improved due to:

• management action;

• benign operating environment

• easyJet lean continuing to deliver cost savings

• Tough decisions taken on asset allocation

• Debt levels reduced

• Ordinary and special dividends paid

• Cash generated from operating activities of £457 million exceeds capital expenditure and ordinary dividend

FY 12 Other costs

ex Fuel

(0.69)

Disruption Crew

(0.18)

Fuel (inc FX)

(2.77)

Revenue FX (ex fuel)

FY 11

Increasing level of dividend Level of cover changed from 5x to 3x

7 7

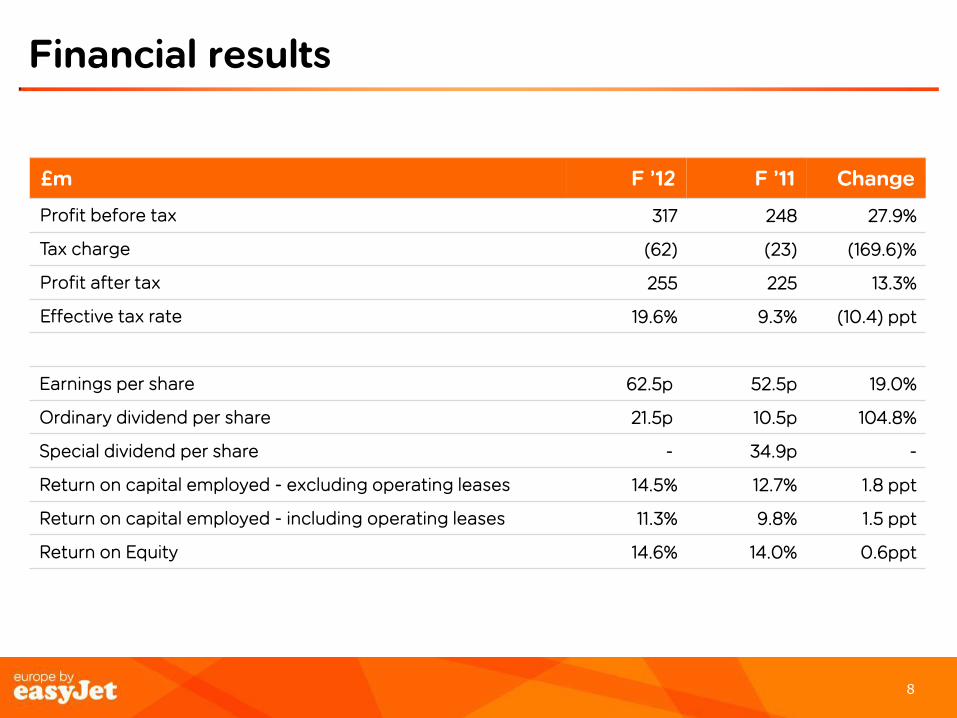

Financial results

£m F ’12 F ’11 Change

Total revenue 3,854 3,452 11.6%

Fuel (1,149) (917) (25.3)%

Operating costs excluding fuel (2,174) (2,067) (5.1)%

EBITDAR 531 468 13.5%

Ownership costs (214) (220) 2.7%

Profit before tax 317 248 27.9%

PBT margin 8.2% 7.2% 1.0 ppt

8 8

Financial results

£m F ’12 F ’11 Change

Profit before tax 317 248 27.9%

Tax charge (62) (23) (169.6)%

Profit after tax 255 225 13.3%

Effective tax rate 19.6% 9.3% (10.4) ppt

Earnings per share 62.5p 52.5p 19.0%

Ordinary dividend per share 21.5p 10.5p 104.8%

Special dividend per share - 34.9p -

Return on capital employed - excluding operating leases 14.5% 12.7% 1.8 ppt

Return on capital employed - including operating leases 11.3% 9.8% 1.5 ppt

Return on Equity 14.6% 14.0% 0.6ppt

9 9

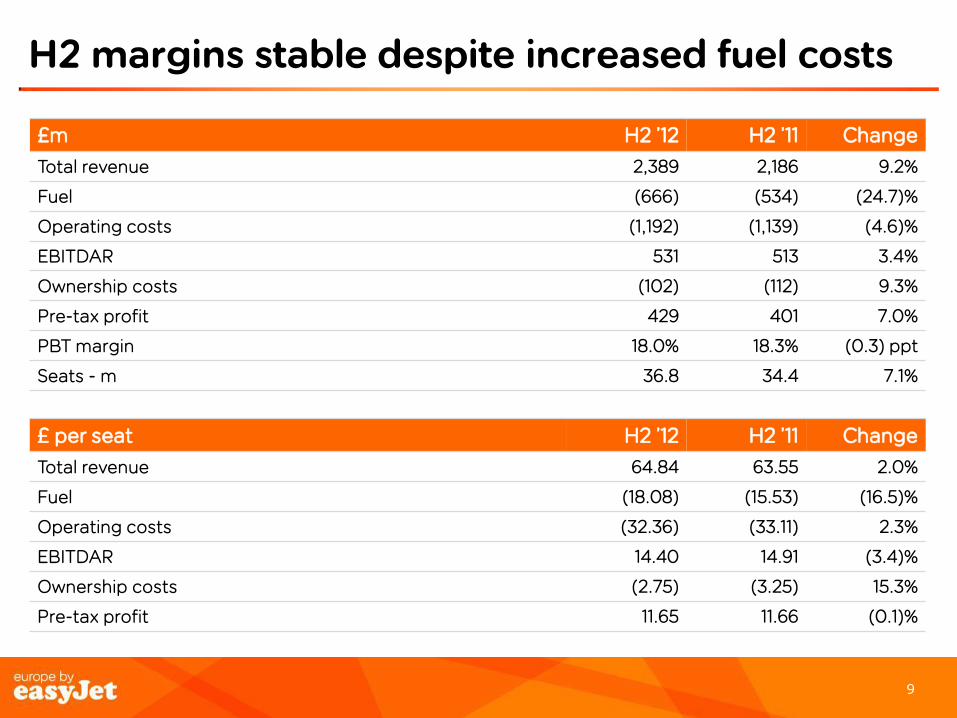

H2 margins stable despite increased fuel costs

£m H2 ’12 H2 ’11 Change

Total revenue 2,389 2,186 9.2%

Fuel (666) (534) (24.7)%

Operating costs (1,192) (1,139) (4.6)%

EBITDAR 531 513 3.4%

Ownership costs (102) (112) 9.3%

Pre-tax profit 429 401 7.0%

PBT margin 18.0% 18.3% (0.3) ppt

Seats - m 36.8 34.4 7.1%

£ per seat H2 ’12 H2 ’11 Change

Total revenue 64.84 63.55 2.0%

Fuel (18.08) (15.53) (16.5)%

Operating costs (32.36) (33.11) 2.3%

EBITDAR 14.40 14.91 (3.4)%

Ownership costs (2.75) (3.25) 15.3%

Pre-tax profit 11.65 11.66 (0.1)%

10 10

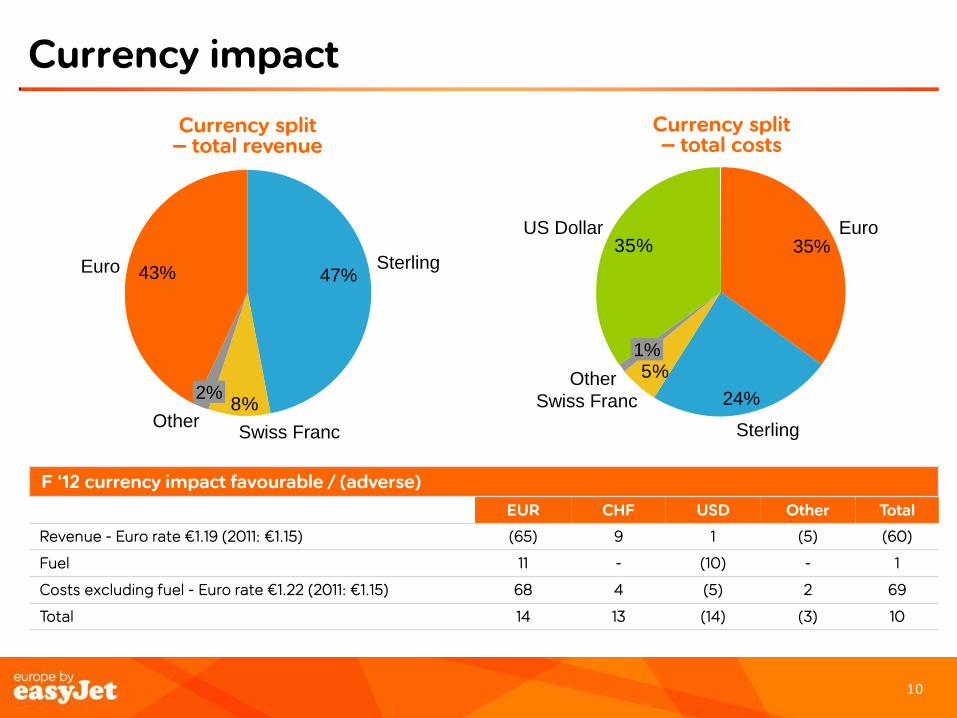

Currency impact

Currency split – total costs

Currency split – total revenue

8%

47% Sterling

Swiss Franc

Euro

2%

Other

43%

35%

5%

Sterling

1%

24%

35%

Other

Euro

Swiss Franc

US Dollar

F ‘12 currency impact favourable / (adverse)

EUR CHF USD Other Total

Revenue - Euro rate €1.19 (2011: €1.15) (65) 9 1 (5) (60)

Fuel 11 - (10) - 1

Costs excluding fuel - Euro rate €1.22 (2011: €1.15) 68 4 (5) 2 69

Total 14 13 (14) (3) 10

11 11

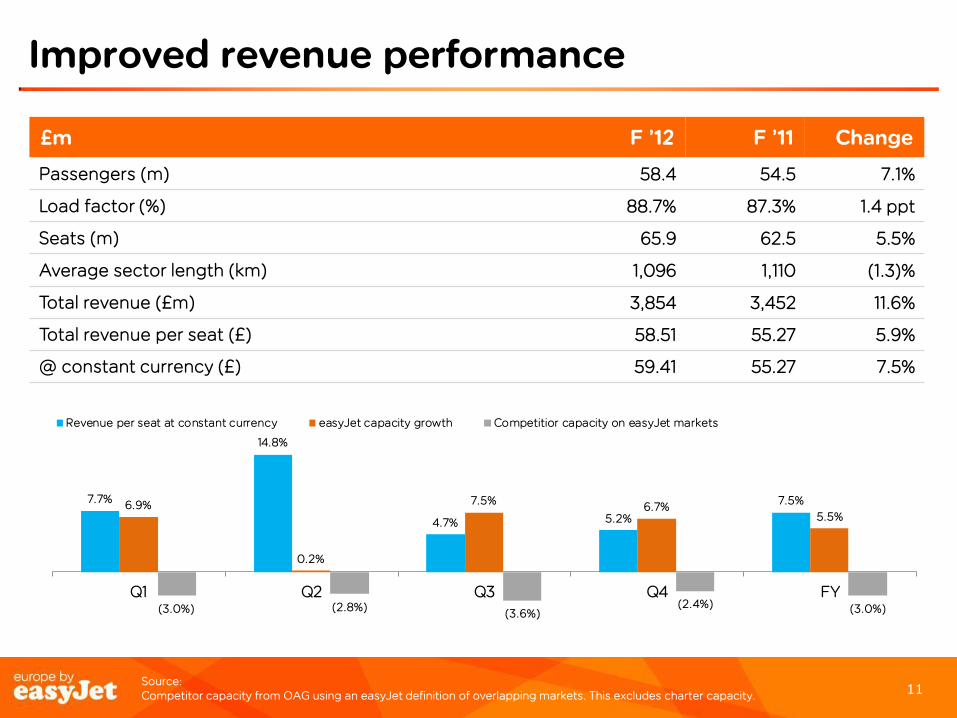

Improved revenue performance

£m F ’12 F ’11 Change

Passengers (m) 58.4 54.5 7.1%

Load factor (%) 88.7% 87.3% 1.4 ppt

Seats (m) 65.9 62.5 5.5%

Average sector length (km) 1,096 1,110 (1.3)%

Total revenue (£m) 3,854 3,452 11.6%

Total revenue per seat (£) 58.51 55.27 5.9%

@ constant currency (£) 59.41 55.27 7.5%

Source: Competitor capacity from OAG using an easyJet definition of overlapping markets. This excludes charter capacity.

7.7%

14.8%

4.7% 5.2%

7.5%6.9%

0.2%

7.5%6.7%

5.5%

(3.0%) (2.8%)(3.6%)

(2.4%) (3.0%)

Q1 Q2 Q3 Q4 FY

Revenue per seat at constant currency easyJet capacity growth Competitior capacity on easyJet markets

12 12

Significant increase in taxes absorbed

£ per seat F ’12 F ’11 Change Change @ CC

Gross seat revenue 64.37 60.51 6.4% 8.1%

Passenger taxes (6.76) (6.26) (8.0)% (10.7)%

Net seat revenue 57.61 54.25 6.2% 7.8%

Non-seat revenue 0.90 1.02 (10.8)% (8.4)%

Total revenue 58.51 55.27 5.9% 7.5%

FY’12

5.5% 6.2%

Q4’12

4.9% 5.4%

Q3’12

2.5% 3.4%

Q2’12

10.6% 10.6%

Q1’12

4.8%

6.0%

Net ticket per seat growth at constant currency

Gross ticket per seat growth at constant currency

13 13

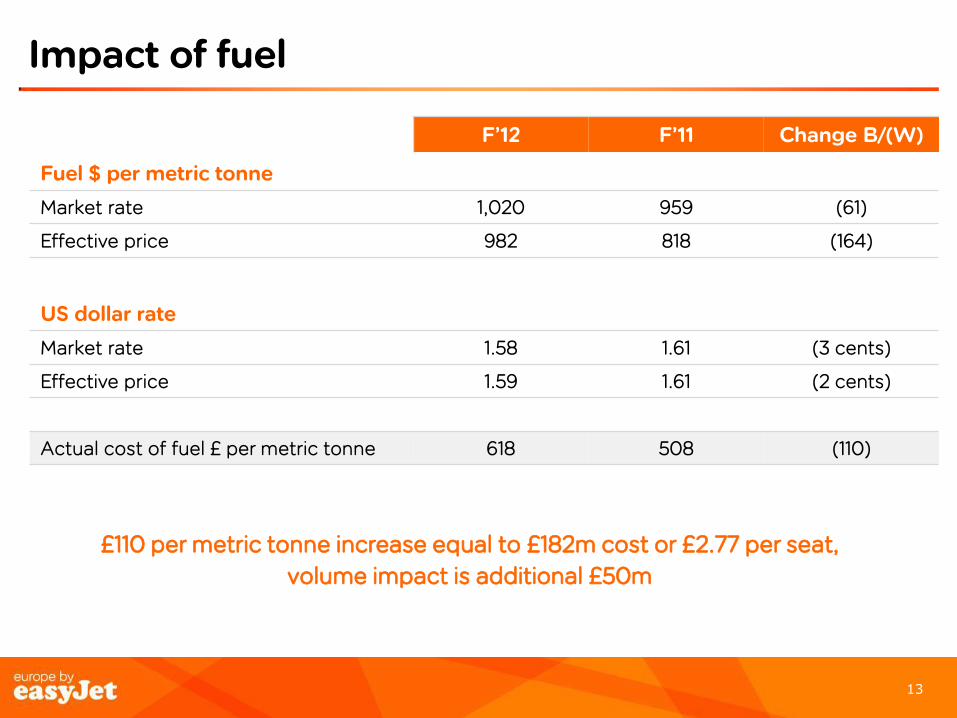

Impact of fuel

F’12 F’11 Change B/(W)

Fuel $ per metric tonne

Market rate 1,020 959 (61)

Effective price 982 818 (164)

US dollar rate

Market rate 1.58 1.61 (3 cents)

Effective price 1.59 1.61 (2 cents)

Actual cost of fuel £ per metric tonne 618 508 (110)

£110 per metric tonne increase equal to £182m cost or £2.77 per seat,

volume impact is additional £50m

14 14

Management action taken to offset headwinds

Profit per seat bridge

£ per seat

3 .97

-0 .19

4.81

-2.77

-1.51

0.12

4.14

0.600.21 0.05

2011 PBT perseat

Fuel Inflation FX (excl fuel) Beforemanagement

action

Revenue IncrementaleasyJet Lean

IncrementalA320 mix

Other 2012 PBT perseat

15 15

Lean Savings

Airports Ground handlingEngineering FuelOther

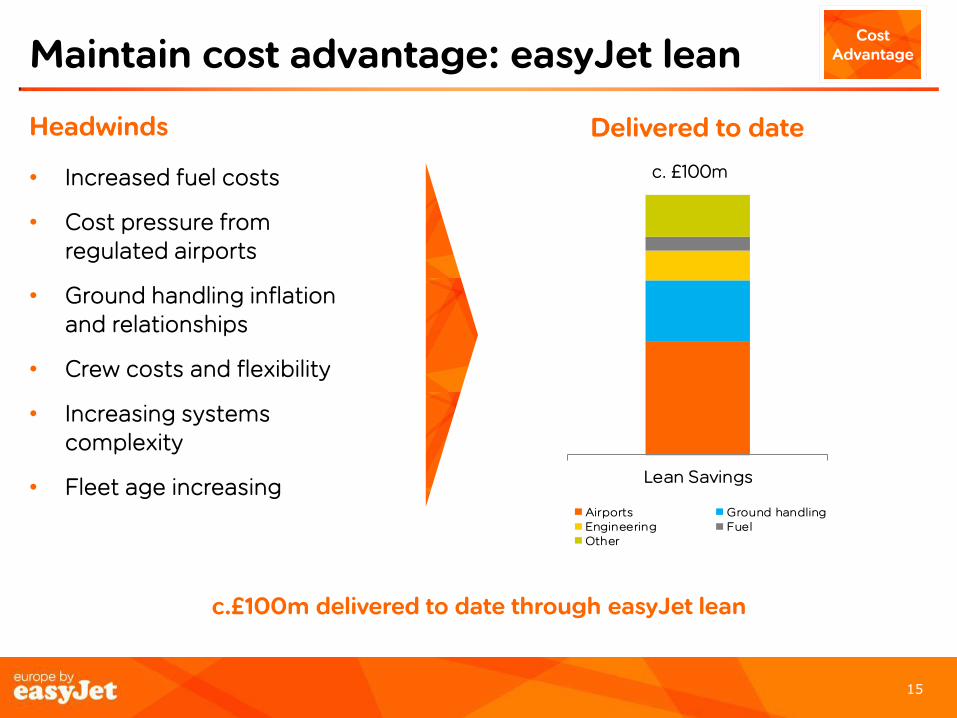

Maintain cost advantage: easyJet lean

Delivered to date Headwinds

• Increased fuel costs

• Cost pressure from regulated airports

• Ground handling inflation and relationships

• Crew costs and flexibility

• Increasing systems complexity

• Fleet age increasing

c.£100m delivered to date through easyJet lean

Cost Advantage

c. £100m

16 16

Cost per seat excluding fuel - key drivers

Movement versus F‘11 Cost per seat (£)

Reported Constant currency

Drivers

Ground Operations 14.49 -2.1% +1.6% • Significant increases in charges in Spain and Italy partially offset by relatively benign winter.

Crew 6.55 +0.6% +2.8% • Average 2% increase in salaries and disciplined winter capacity thinning.

Navigation 4.25 -6.7% -1.2% • Regulated increases of 2% more than offset by higher proportion of A320s and slightly shorter sector length.

Maintenance 3.08 +7.7% +8.1% • Driven by one-offs. Investment in process improvements will partially mitigate increases from the planned aging of the fleet.

Overhead 4.55 +5.9% +7.1% • Investment in IT infrastructure, and performance related employee costs resulting from significantly improved profitability.

Brand licence 0.08 +20.4% +20.4% • Increase in fixed royalty from £3.95m to £4.95m.

Ownership 3.25 -7.8% -7.4% • Leasing costs lower due to the higher proportion of owned aircraft.

Total CPS excluding fuel 36.25 -1.0% +1.8%

17 17

Increasing proportion of A320’s

Sep ‘12 Sep ‘11 Change

A319 (operating lease) 49 56 (7)

A319 (owned / finance lease) 111 111 -

A319 Total 160 167 (7)

A320 (operating lease) 6 6 -

A320 (owned / finance lease) 48 29 19

A320 Total 54 35 19

Main fleet 214 202 12

Sub-fleet (Boeing 737) - 2 (2)

Total fleet 214 204 10

Operating lease 26% 31% (5)ppt

Percentage unencumbered 32% 19% 13ppt

Percentage of A320s in fleet 25% 17% 8ppt

18 18

Flexibility in fleet planning

Maximum fleet - Lease extensions; options exercised

Minimum fleet - Early termination of leases; deferrals of existing orders

Fleet count

210

217220

228

236

244

254 252

213

209

201 199196 194

225223

231 232

241

180

190

200

210

220

230

240

250

260

FY13 H1 FY13 H2 FY14 H1 FY14 H2 FY15 H1 FY15 H2 FY16 H1 FY16 H2

Max fleet

Min fleet

Growth of. c.3% to 5% p.a.

19 19

Strong balance sheet

£m Sep ‘12 Sep ‘11

Property, plant and equipment 2,395 2,149

Goodwill and other intangible assets 456 451

Other assets 561 469

Liabilities (excluding debt) (1,544) (1,464)

1,868 1,605

Debt 957 1,300

Cash and money market deposits (883) (1,400)

Net debt / (cash) 74 (100)

Shareholders’ equity 1,794 1,705

Capital employed 1,868 1,605

Gearing* 29% 28%

*Gearing defined as (debt + 7 x annual lease payments – cash) divided by (shareholders’ equity + debt +7 x

annual lease payments – cash)

20 20

Aircraft cashflows including overhauls

Figures based on contracted fleet commitments

Aircraft 2012 2013

Number of aircraft deliveries 19 10

Capital expenditure (USD) 2012

$m 2013

$m

Final delivery payments 479 268

Pre delivery payments 35 5

Heavy maintenance - owned fleet 14 39

Total $528m $312m

Heavy maintenance - leased fleet 120 93

Total cash flows $648m $405m

Total cash flows (GBP) £410m £257m

21 21

25

150

364

38946

2845109

331

Cashflow

Sep 2012 *

883

Financing CAPEX Ordinary dividend

paid

Tax, net int & other

Net Working Capital

Depn & amort

Special dividend

paid

Operating Profit

FX Sep 2011 *

1,400

* Includes money market deposits but excludes restricted cash

£m

22 22

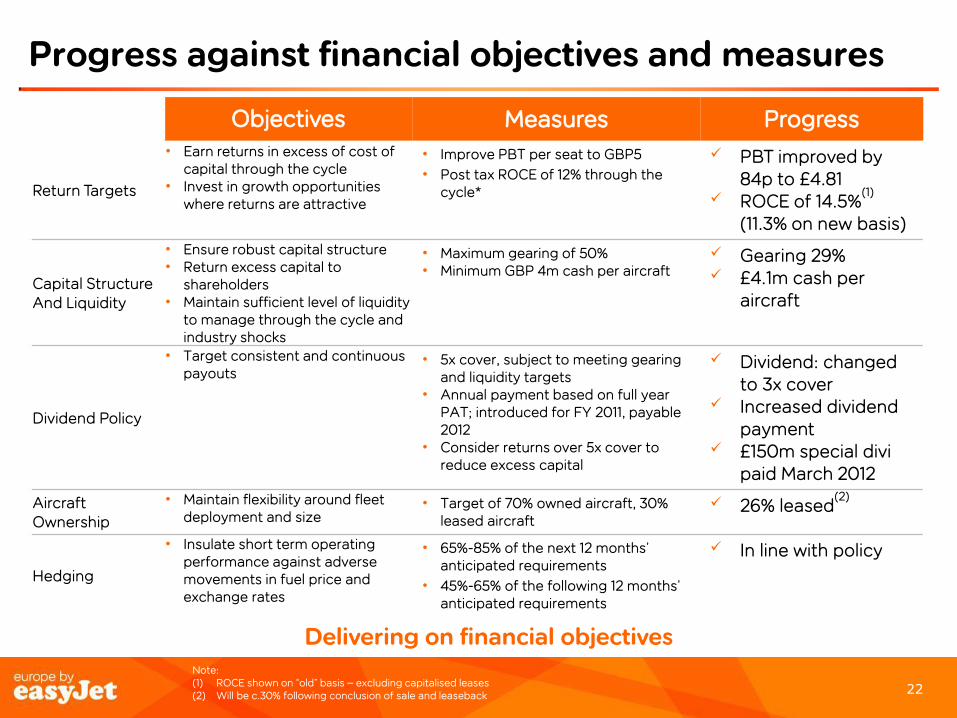

Progress against financial objectives and measures

Objectives Measures Progress

Return Targets

• Earn returns in excess of cost of capital through the cycle

• Invest in growth opportunities where returns are attractive

• Improve PBT per seat to GBP5

• Post tax ROCE of 12% through the cycle*

PBT improved by 84p to £4.81

ROCE of 14.5%(1)

(11.3% on new basis)

Capital Structure And Liquidity

• Ensure robust capital structure • Return excess capital to

shareholders • Maintain sufficient level of liquidity

to manage through the cycle and industry shocks

• Maximum gearing of 50% • Minimum GBP 4m cash per aircraft

Gearing 29% £4.1m cash per

aircraft

Dividend Policy

• Target consistent and continuous payouts

• 5x cover, subject to meeting gearing and liquidity targets

• Annual payment based on full year PAT; introduced for FY 2011, payable 2012

• Consider returns over 5x cover to reduce excess capital

Dividend: changed to 3x cover

Increased dividend payment

£150m special divi paid March 2012

Aircraft Ownership

• Maintain flexibility around fleet deployment and size

• Target of 70% owned aircraft, 30% leased aircraft

26% leased(2)

Hedging

• Insulate short term operating performance against adverse movements in fuel price and exchange rates

• 65%-85% of the next 12 months’ anticipated requirements

• 45%-65% of the following 12 months’ anticipated requirements

In line with policy

Delivering on financial objectives Note: (1) ROCE shown on “old” basis – excluding capitalised leases (2) Will be c.30% following conclusion of sale and leaseback

23 23

Fuel and foreign exchange hedging

Sensitivities

• $10 movement per metric tonne impacts F’13 PBT by $4m

• One cent movement in £/$ impacts F’13 PBT by £1.6m

• One cent movement in £/€ impacts F’13 PBT by £1.2m

Fuel requirement

US dollar requirement

Euro surplus

Half year ending 31 March 2013 86% at $986/tonne 86% at $1.61/£ 76% at €1.18/£

Full year ending 30 September 2013 78% at $985/tonne 81% at $1.60/£ 68% at €1.18/£

Full year ending 30 September 2014 55% at $993/tonne 62% at $1.58/£ 48% at €1.22/£

Table data as of 23rd October

24 24

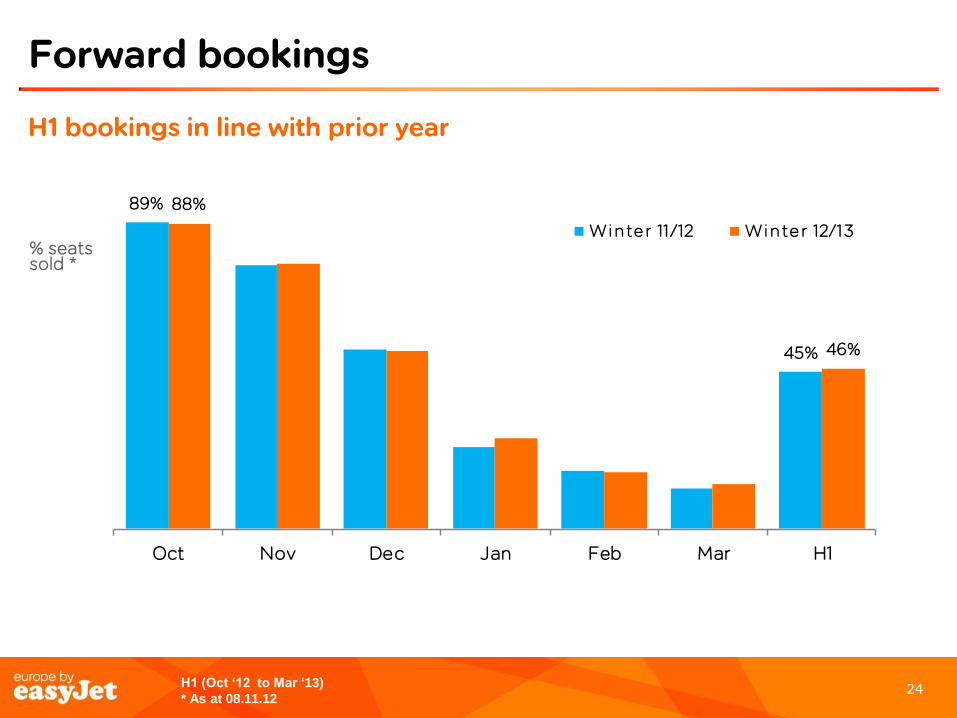

Forward bookings

% seats sold *

H1 (Oct ‘12 to Mar ‘13)

* As at 08.11.12

H1 bookings in line with prior year

89%

45%

88%

46%

Oct Nov Dec Jan Feb Mar H1

Winter 11 /12 Winter 12/13

25 25

Outlook

Capacity (seats flown)

• FY c.+3.5% (before disruption)

• H1 c.+3.5% (before disruption)

Revenue per seat (constant currency)

• H1 up low to mid single digits

Cost per seat ex fuel (constant currency)

• FY c.+3 to 4% (assuming normal disruption levels and constant load factors)

• H1 c.+4 to 5% (assuming normal disruption levels and constant load factors)

• Includes £70m increase in airport costs

Headwinds

• c.£50 million adverse movement from foreign exchange rates

• With fuel remaining within its recent $1,000/MT to $1,100/MT trading range, easyJet’s unit fuel bill for the 2013 financial year would be up to £30m higher

“Whilst there is always the potential for unexpected events to temporarily impact financial results the Board of easyJet is confident that its business model, strategy and people will consistently continue to generate

superior returns and growth for shareholders.”

26

Business review

Carolyn McCall

Chief Executive Officer

26

27 27

7.0

7.5

8.0

8.5

9.0

07 08 09 10 11 12 13 14 15 16 17 18

High

Low

Base

Headwinds for European aviation – but growth expected

Headwinds

• Austerity measures

• Slowing economic growth

• Industrial unrest

• High fuel costs

• Increased taxation on aviation

• Rising costs at regulated airports

Intra-European flying volume(1)

Source: (1) Eurocontrol traffic flow forecast for Europe – ESRA 8 definition (EU + Scandinavia + Turkey + Eastern Europe) Sept’12

Yet

Opportunities for strong airlines such as easyJet to deliver returns and growth

Year

Annual number of flights (m)

28 28

-1%

4%

-1%

-8%

-6%

-2%

3%

9%

11%

6%

-6%

4%

UK France Swiss Italy Spain Market

Competitors - on EZJ routes

easyJet change

Unique structural opportunity for easyJet

Capacity growth H1 ‘ F’13 (OAG)

Key themes

• Legacy carriers incurring significant short haul losses

• Weaker carriers retreating or exiting

• Consolidation

• Capacity discipline in the market

H1 capacity YOY Chg

Competitors on EZJ routes

-1.8%

Competitors in total market

-3.6%

easyJet +3.6%

Source: OAG 6 months to March ’12; based on easyJet city pairs

29 29

Continued structural advantage against legacies

Source:

OAG intra-European travel 2005 vs. .2012

On-going cost advantage against legacies and charter airlines

• Seat density

• Load factors

• Point to point vs. feeder

• Fleet

• Pensions / crew costs

• Overheads

Market share – EZJ vs legacy carriers '05 vs'12

Cost advantage and ability to offer affordable fares allows easyJet to continue to grow profitably and to take share from legacies

UK France Switzerland Italy

vs. BA vs. AF vs. Swiss vs. Alitalia

-3% +6% -13% +8% -1% +8% -5% +8%

21%

15%

61%

5%

35%

12%

34%

2%

18%21%

48%

13%

34%

20%

29%

10%

BA EZJ AF EZJ Swiss EZJ Alitalia EZJ

Market share - EZJvs legacy carriers '05 vs'12

30 30

Winning against low-cost competition

• Strength of network

• Pan-European network and market presence

• No. 1 or 2 positions at primary airports

• Peak slots

• Strong balance sheet

• Scale and purchasing power

• Pan-European brand

• easyJet.com

• Friendly service

Base 36%

Brand 38%

Price 4%

Media 22%

Estimated Seat sale contribution

38% of sales due to the power of the brand

46

24

34 26 23

19 18 17 14 13

3

3

14 2

2

-

10

20

30

40

50

60

Presence in top 100 market pairs

Non primary airports

Primary airports

Source: Market data from OAG: intra-European travel 2005 vs. .2012 Seat sale contribution from Brand Science Big 6 Market Econometrics study, Feb 2012 data

31 31

Strategy to drive growth and returns

1. Build strong number 1 and 2 network positions

2. Maintain cost advantage

3. Drive demand, conversion and yield across Europe

4. Disciplined use of capital

• Sustainable growth • (slightly in excess of market c.

3% to 5% per annum)

• Improved returns

• Tangible and regular cash returns via 3 x cover dividend

Leverage easyJet’s cost advantage, leading market positions and brand to deliver point-to-point low fares with operational efficiency and friendly service for our customers

32 32 (1) Market shares based on OAG capacity shares for 12 months to end September 2012

1. Network positions

Building strong number 1 or 2 positions at major airports(1)

Airport Share Position

London Gatwick 46% No.1

Geneva 38% No.1

Milan Malpensa 37% No.1

Paris Orly 13% No.2

Lisbon 13% No.2

Paris CDG 11% No.2

Amsterdam 10% No.2

Build strong number 1 & 2 network positions

• Highest returns where we have a strong relative market share and cost advantage

• Economies of scale and market presence

33 33

3 to 4%1 to 2%

c.1%

F'13 Cost headwinds Incremental Lean Incremental A320 F'13 cost per seat (excl. fuel)

Cost per seat excluding fuel - at constant currency

Other(Disruption, Crew, Brand

Royalty)c.3%

5 to 6%

Airportsc.3%

Actions planned to offset cost headwinds 2.

Cost Advantage

Actions planned to offset headwinds and increase returns

34 34

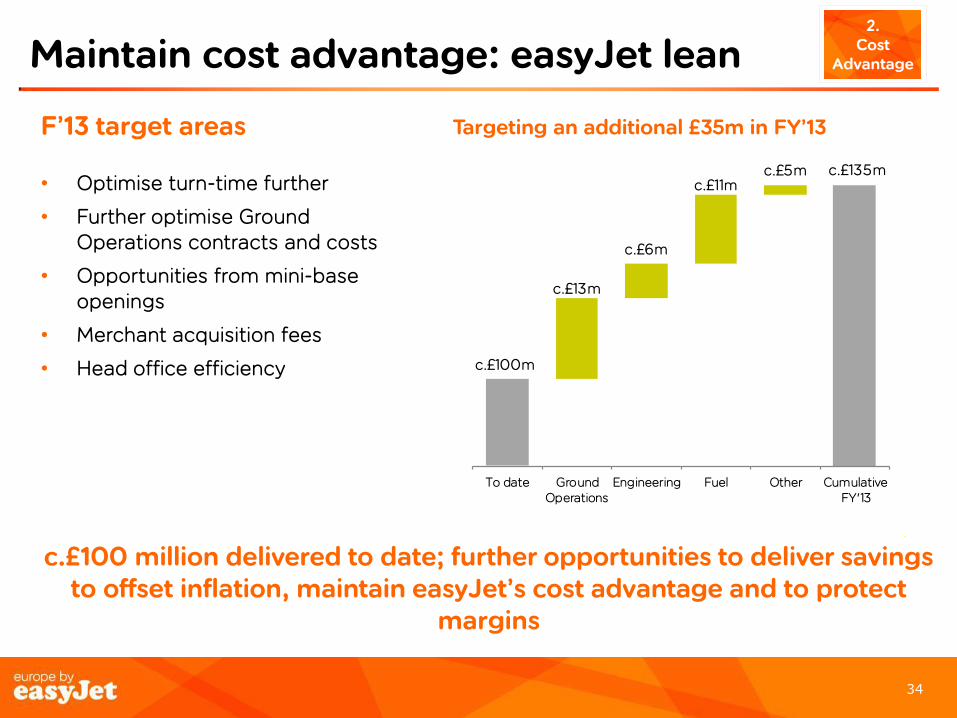

Maintain cost advantage: easyJet lean 2.

Cost Advantage

c.£100m

c.£135m

c.£13m

c.£6m

c.£11mc.£5m

To date GroundOperations

Engineering Fuel Other CumulativeFY'13

F’13 target areas

• Optimise turn-time further

• Further optimise Ground Operations contracts and costs

• Opportunities from mini-base openings

• Merchant acquisition fees

• Head office efficiency

c.£100 million delivered to date; further opportunities to deliver savings to offset inflation, maintain easyJet’s cost advantage and to protect

margins

Targeting an additional £35m in FY’13

35 35

3. Drive

Demand Driving demand, conversion & yield across Europe

• Network optimisation

• Progressing the business initiative

• Allocated seats

• Driving leisure

• Brand

• Digital / Web

• Revenue management

36 36

Network optimisation

United Kingdom 2.7%

France 8.8%

Italy

5.9%

Spain

-5.8%

Switzerland 11.5%

Germany flat

Netherlands flat

Overall 3.6% capacity growth in H1 (adjusting for disruption(1))

Portugal

5.0%

Source : OAG for 6 months to end March 2013

3. Drive

demand

37 37

Progressing Business initiative

Building blocks being put in place

• Business routes added to network

• Partnerships with Global Distribution System providers (GDS)

• Agreements with Travel Management Companies (TMC)

• Large scale customers signed

• In-country Sales teams delivering

Improving functionality & accessibility

• Work with GDS & TMCs to improve technology & functionality (mid-2013)

Drive Demand

3. Drive

Demand

38 38

Allocated seating roll-out is on plan

A320 • ‘Extra Legroom’ = 18

seats • ‘Up front’ = 30 seats • Remaining = 132 seats

A319 • ‘Extra Legroom’ = 18

seats • ‘Up front’ = 24 seats • Remaining = 114 seats

‘Up front’ seats

‘Up front’ seats

to Oct 11th Oct 11th Oct 16th Nov 13th Nov 20th Nov 27th

Route / base description

Existing trial routes

Rolled out to all London airports, and all flights touching Bristol, Glasgow, Edinburgh, Rome, Paris

Rest of Network

Allocating seating roll-out is on track

‘Extra Legroom’ seats

Drive Demand

3. Drive

Demand

39 39

Driving leisure Drive

Demand

3. Drive

Demand

Exciting new destinations

• E.g. Reykjavik

Improved product

• Inflight offer

• Partner offers

• Allocated seating

Innovative distribution

• Inspire Me

• Series seat sales

40 40

Brand: europe by easyJet

Increasingly stronger awareness in our newer markets: 86% Italy, 92% France

Significant growth in consideration, both among business and leisure fliers

New advertising taking effect – high ad recall and recognition

Brand messaging getting stronger

Pan-European campaign

Drive Demand

3. Drive

Demand

41 41

Conversion drivers

US homepage

Swiss homepages

Abandon Basket Email Step 5 Destination Guides

Inspire Me

Drive Demand

3. Drive

Demand

42 42

Revenue management system

• Cutting edge, bespoke revenue management system

• Further benefit from yield managing ancillaries

• Improved effectiveness using latest artificial intelligence techniques

Drive Demand

3. Drive

Demand

Prices as at per 19 November 2012

43 43

Disciplined use of capital 4.

Capital Discipline

Key principles

• Strong balance sheet is a source of competitive advantage

• easyJet committed to covering cost of capital

• easyJet will self fund dividend, fleet replacement and growth

• Rigorous approach to capital allocation embedded throughout easyJet

FY11 FY12 12% ROCE

Improved returns year on year Returns

Routes

44 44

Fleet order framework

• Commercial and technical evaluation progressing well

• New gen offer significant cost saving opportunities

• RFP to five suppliers:

• Engines: Pratt & Whitney, CFMi (GE & Snecma)

• Aircraft: Airbus, Boeing, Bombardier

• No further update expected before the second quarter

• Plan will include details on ‘bridge’ period to next generation

Contracted aircraft @ end Sept'12 @ end Sept'13

A320 family 214 217

% of A320s 25% 29%

4. Capital

Discipline

45 45

Summary

A unique structural opportunity in the market; easyJet to take advantage to deliver sustainable returns and growth

1. Record of delivery

• Financial & operational performance

2. Structural winner

• Against legacies

• Against charters

• Against low cost

3. Opportunity to deliver sustainable returns and growth

Delivery against strategy

Operational resilience

Dividend

Improving network returns

easyjet lean

Driving revenue

Passengers travelling on business

Q & A

46

APPENDIX

47

48 48

ROCE Calculation – including 7x lease adjustment

Reported £m Sep ‘12 Sep ’11

Earnings before interest and tax – reported 331 269

Interest element of operating lease payments 32 36

Earnings before interest and tax - adjusted 363 305

Tax 24% 26%

Normalised operating profit after tax (NOPAT) 276 226

Average shareholders’ equity – reported 1,750 1,603

Average net cash – reported (13) (30)

Opening capitalised leases 763 714

Closing capitalised leases 665 763

Average capitalised leases 714 739

Average capital employed 2,451 2,312

Return on capital employed – 7x basis 11.3% 9.8%

49 49

ROCE Calculation – NPV and Target liquidity

Proforma £m Sep ‘12 Sep ’11

Earnings before interest and tax – reported 331 269

Interest element of operating lease payments 25 27

Earnings before interest and tax – adjusted 356 296

Tax 24% 26%

Normalised operating profit after tax (NOPAT) 270 219

Average shareholders’ equity – reported 1,750 1,603

Adjustment to shareholders’ equity (35) (40)

Average shareholder’s equity – adjusted 1,715 1,563

Average net cash – reported (13) (30)

Increase in debt associated with capitalising leases 355 362

Target liquidity adjustment 836 800

Average net debt – adjusted 1,178 1,132

Average capital employed 2,893 2,695

Return on capital employed – NPV basis 9.3% 8.1%

50 50

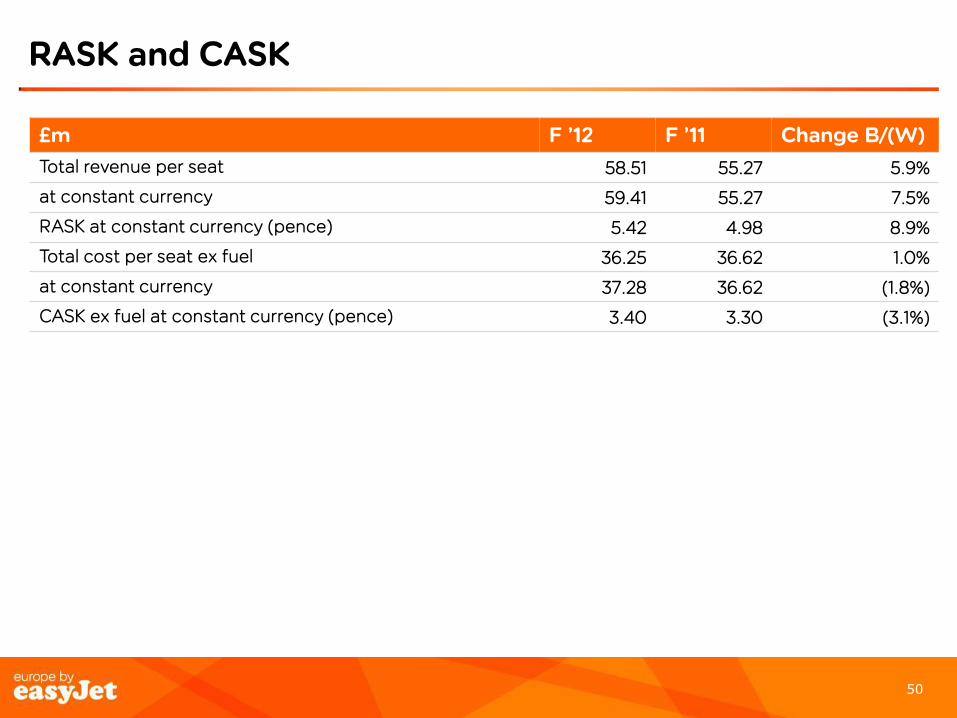

RASK and CASK

£m F ’12 F ’11 Change B/(W)

Total revenue per seat 58.51 55.27 5.9%

at constant currency 59.41 55.27 7.5%

RASK at constant currency (pence) 5.42 4.98 8.9%

Total cost per seat ex fuel 36.25 36.62 1.0%

at constant currency 37.28 36.62 (1.8%)

CASK ex fuel at constant currency (pence) 3.40 3.30 (3.1%)

51 51

This communication is directed only at (i) persons having professional experience in matters relating to investments who fall within the definition of “investment professionals” in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001; or (ii) high net worth bodies corporate, unincorporated associations and partnerships and trustees of high value trusts as described in Article 49(2) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001. Persons within the United Kingdom who receive this communication (other than those falling within (i) and (ii) above) should not rely on or act upon the contents of this communication. Nothing in this presentation is intended to constitute an invitation or inducement to engage in investment activity for the purposes of the prohibition on financial promotion contained in the Financial Services and Markets Act 2000. This presentation has been furnished to you solely for information and may not be reproduced, redistributed or passed on to any other person, nor may it be published in whole or in part, for any other purpose. This presentation does not constitute or form part of, and should not be construed as, an offer for sale or subscription of, or solicitation of any offer to buy or subscribe for, any securities of easyJet plc (“easyJet”) in any jurisdiction nor should it or any part of it form the basis of, or be relied on in connection with, any contract or commitment whatsoever. This presentation does not constitute a recommendation regarding the securities of easyJet. Without limitation to the foregoing, these materials do not constitute an offer of securities for sale in the United States. Securities may not be offered or sold into the United States absent registration under the US Securities Act of 1933 or an exemption there from. easyJet has not verified any of the information set out in this presentation. Without prejudice to the foregoing, neither easyJet nor its associates nor any officer, director, employee or representative of any of them accepts any liability whatsoever for any loss however arising, directly or indirectly, from any reliance on this presentation or its contents. This presentation is not being issued, and is not for distribution in, the United States (with certain limited exceptions in accordance with the US Securities Act of 1933) or in any jurisdiction where such distribution is unlawful and is not for distribution to publications with a general circulation in the United States. By attending or reading this presentation you agree to be bound by the foregoing limitations.

Disclaimer

![3Q21 [ENG] Results Presentation-Analyst](https://static.fdocuments.in/doc/165x107/62059ee21708c43c2d4570d9/3q21-eng-results-presentation-analyst.jpg)