2016 Media Guide ICBA Independent Banker®...

18

INDEPENDENT COMMUNITY BANKERS OF AMERICA independentbanker.org l icba.org 2016 MEDIA GUIDE ICBA INDEPENDENT BANKER® MAGAZINE l e-Newsletters l Websites l Webinars l e-Blasts l Sponsorships ...and more! + Where Community Banking is Always Big Business

Transcript of 2016 Media Guide ICBA Independent Banker®...

independent community bankers of americaindependentbanker.org l icba.org

2016 Media GuideICBA Independent Banker® mAgAzIne

l e-Newslettersl Websitesl Webinarsl e-Blastsl Sponsorships ...and more!

+

Where Community Banking is Always Big Business

2016 Media Information | ICBA Independent Banker®2

We Are Community Banking

ICBA Welcomes You to Community Banking!

The Independent Community Bankers of America®, the nation’s voice for community banks, is the largest banking trade association in the country.

ICBA is the only national association dedicated exclusively to serving and protecting the interests of the community banking industry and the communities and customers they serve. ICBA will connect you with the largest segment of the banking industry, representing community banks of all sizes and charter types throughout the United States.

Readex Research IB magazine Readership Survey, September 2015

l 98% of members believe ICBA positively impacts the community banking industry

l 93% of members believe ICBA Independent Banker® magazine understands and addresses the specific needs of community banks

32016 Media Information | ICBA Independent Banker®

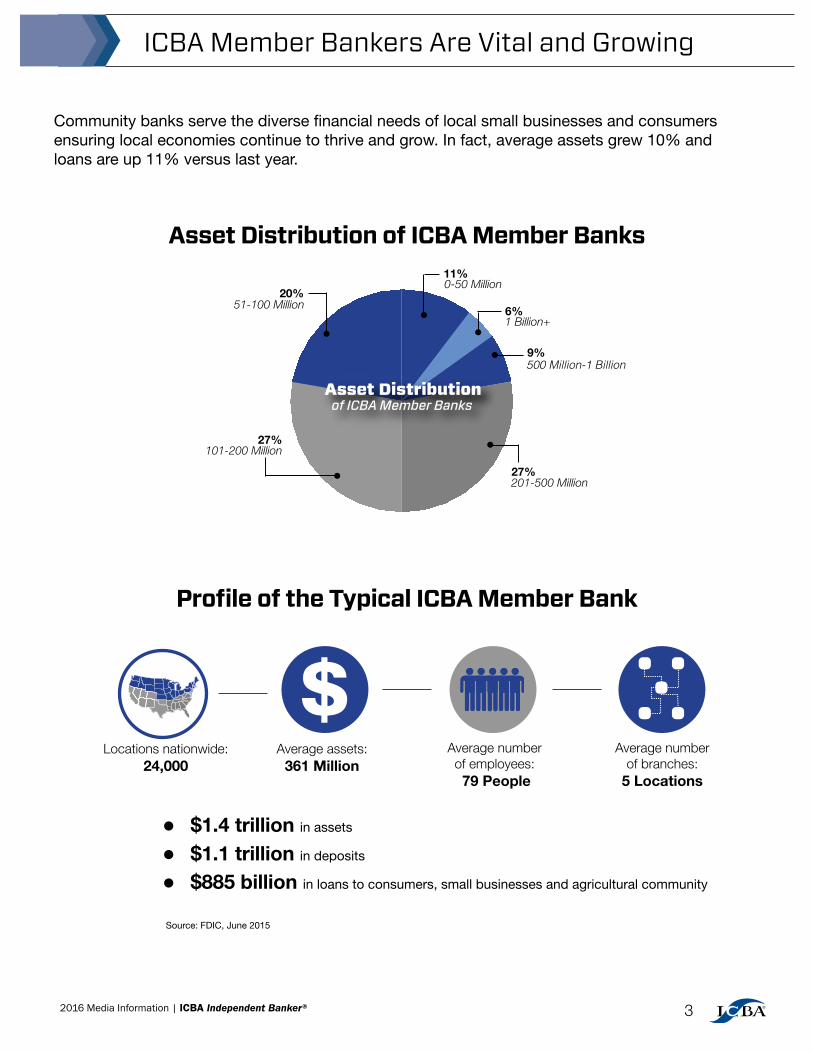

Profile of the Typical ICBA Member Bank

Community banks serve the diverse financial needs of local small businesses and consumers ensuring local economies continue to thrive and grow. In fact, average assets grew 10% and loans are up 11% versus last year.

Asset Distribution of ICBA Member Banks

$Average assets:

303 MillionAverage number

of employees:71 People

Average number of branches:4 Locations

Source: FDIC, June 2015

Average assets:361 Million

Average number of employees: 79 People

l $1.4 trillion in assets

l $1.1 trillion in deposits

l $885 billion in loans to consumers, small businesses and agricultural community

ICBA Member Bankers Are Vital and Growing

11%0-50 Million

9%500 Million-1 Billion

20%51-100 Million

27%101-200 Million

27%201-500 Million

Asset Distributionof ICBA Member Banks

6%1 Billion+

Average number of branches:

5 Locations

Locations nationwide:24,000

2016 Media Information | ICBA Independent Banker®4

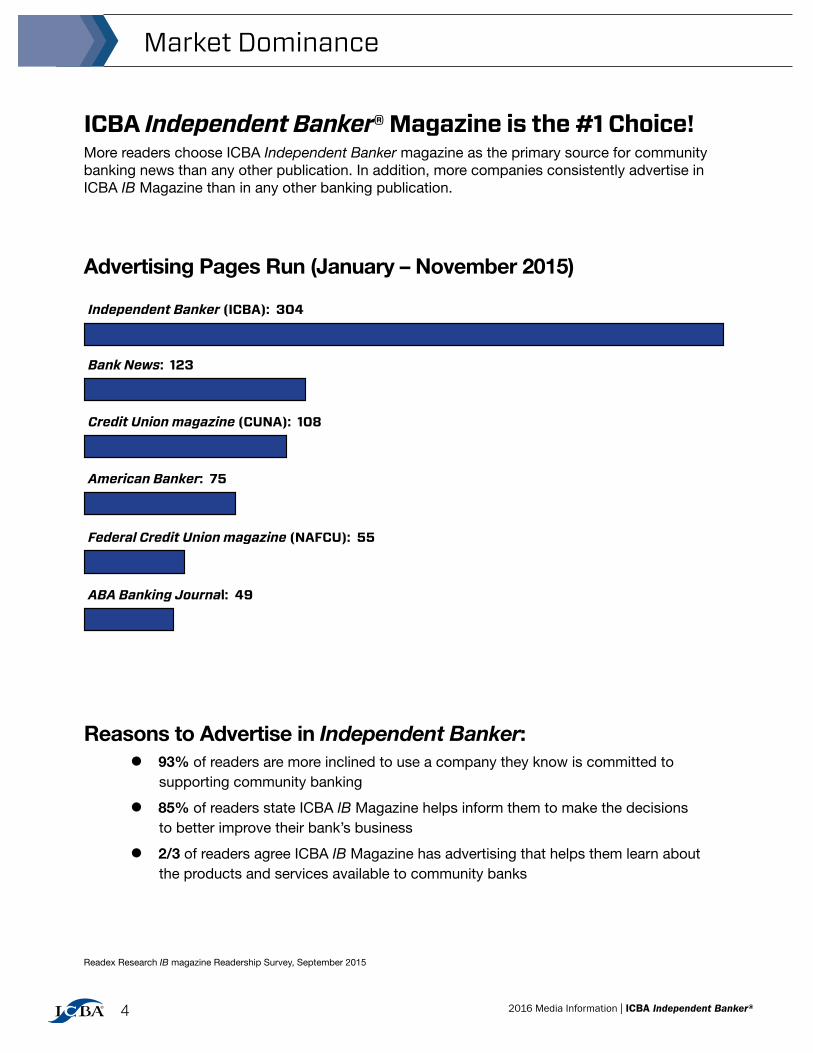

ICBA Independent Banker® Magazine is the #1 Choice!More readers choose ICBA Independent Banker magazine as the primary source for community banking news than any other publication. In addition, more companies consistently advertise in ICBA IB Magazine than in any other banking publication.

Advertising Pages Run (January – November 2015)

Market Dominance

Reasons to Advertise in Independent Banker: l 93% of readers are more inclined to use a company they know is committed to supporting community banking

l 85% of readers state ICBA IB Magazine helps inform them to make the decisions to better improve their bank’s business

l 2/3 of readers agree ICBA IB Magazine has advertising that helps them learn about the products and services available to community banks

Independent Banker (ICBA): 304

Bank News: 123

Credit Union magazine (CUNA): 108

American Banker: 75

Federal Credit Union magazine (NAFCU): 55

ABA Banking Journal: 49

Readex Research IB magazine Readership Survey, September 2015

52016 Media Information | ICBA Independent Banker®

Independent Banker® Readership Breakout by Title:

IB Magazine Readers are Deeply Connected:

NOTABLE ACTIONS TAKEN:

l 71% discussed an article in ICBA IB magazine with others l 61% clipped and saved articles of interest l 47% researched a topic further l 21% discussed or saved an ad for future reference l 19% visited an advertiser’s website after reading ICBA IB magazine l 10% actively sought out and/or requested information on a product or service

Readex Research IB magazine Readership Survey, September 2015

Reader Engagement

20%EVP, SVP, VP

5% Other

62%CEO, President

5%CTO, COO, CIO

Readership Breakoutby title

8%Director/Manager

of ICBA IB Magazine readers have read or looked through three of the last four issuesl 75%

of ICBA IB Magazine readers have taken at least one action as a result of reading the magazine within the last 12 monthsl 94%

l 38 minutes is the average amount of time an ICBA IB Magazine reader spends reading or looking through a typical issue

2016 Media Information | ICBA Independent Banker®6

ICBA Independent Banker Magazine Is:l mailed directly to Presidents, CEOs, and C-level staff of ICBA member community banks who make the decisions to buy.

l circulated nationally, averaging 13,000 printed copies per month with an average monthly pass-along rate of two people per subscriber. Printed copies are seen by more than 39,000 community bank decision-makers monthly.

l distributed digitally to a opt-in subscriber base of over 50k, twice monthly.

ICBA’s flagship publication, Independent Banker, is the only national magazine solely dedicated to addressing the needs of community bank decision-makers, and is consistently ranked the number one benefit of ICBA membership.

National Circulation Breakout by Region/StateICBA works in partnership with state banking associations across the country to secure public policies in Washington D.C. that serve community banks, their customers and communities.

Central . . . . . . . . . . . 45%

Southeast . . . . . . . . .24%

Southwest . . . . . . . . 16%

Northeast . . . . . . . . 11%

Northwest . . . . . . . . . 4%

45%

24%16%

4% 11%

Source: FDIC, June 2015

IB Circulation & Distribution

72016 Media Information | ICBA Independent Banker®

Every Issue Includes:

•ICBAChairman’sPerspective

•ICBAPresident&CEO’sColumn

•ComplianceStrategies

•TechnologyInsights

•BankerCaseStudies

•LendingTrends

•NewProduct&ServiceInfo

•PaymentPlanning

•IndustryUpdates

...and more!

ICBA Touch Points

ICBA Independent Banker® MagazineEvery month, ICBA Independent Banker magazine presents timely information and opportunities for community bankers to learn, grow and effectively compete in the financial services marketplace.

ICBA Corporate Associate Membership Demonstrate your company’s commitment to the community banking industry by joining ICBA as a Corporate Associate Member. ICBA member banks look to our approved Corporate Members to find the best products and services tailored to meet the specific needs of community bankers.

Corporate Associate Member Benefits Include:

l mailing privileges to ICBA members

l free listings in ICBA vendor directories (print and online)

l special discounts in ICBA IB Magazine, convention booths and more . . .

For more information, call Patricia Rajdl, AVP of ICBA Corporate Associate Membership, at (800) 422-7285, or download a brochure of benefits at http://www.icba.org/files/ICBASites/PDFs/cambrochure.pdf.

2016 Media Information | ICBA Independent Banker®8

June is ICBA Independent Banker® magazine’s BIG issue: big names in the industry, big news, and big ideas! This special section will focus on the biggest new products and services in the industry and how they can help community banks be more efficient and effective.

This showcase is specially designed for your company to highlight the solutions your products/services provide to the challenges community bankers face everyday.

Bankers want to stay competitive. Show them how your company’s services can help!

ICBA INDEPENDENT BANKER® MAGAZINE PRESENTS

A NEW PRODUCT AND SERVICE SHOWCASE

1) Provide a concern you know is a challenge for community banks and the solution that your company provides.

2) Expand upon how your company’s new product or service can help community bankers through listing product benefits, case studies and/or testimonials.

BIG IDEASF O R C O M M U N I T Y B A N K S

SPACE & MATERIAL DEADLINES:

Space reservation: 4/15/15Copy & logo due: 4/28/15Proof review: TBDPublication date: June 2015

PDF of your advertorial to host on your website

Big Ideas special section promoted through IBmag eNews

� Hosted Link to Big Ideas in Independent Banker's digital edition

Special section hosted on www.independentbanker.org for three months

ADDED VALUE:

ClickonthepromoimageinthemonthsofJanuary,May,June,July,OctoberandNovemberforSpecialSectionopportunities.

Your company’s success story should demonstrate your commitment to community banks and their customers, as well as the benefits your company provides.

Use this opportunity to:

Discuss how your products and/or services have helped a community bank navigate the ever-changing regulatory landscape.

Describe a customized solution that targets a particular challenge or set of challenges facing community banks today.

Share how you’ve worked with a community bank to help offset the cost of implementing a particular product, service or technological enhancement.

Detail how your products and/or services have helped a community bank remain competitive and profitable in today’s marketplace.

PDF of your advertorial to host on your website

Partnering for Success special section promoted through IBmag eNews

� Hosted Link to Parnerting for Success in Independent Banker's digital edition

Special section hosted on www.independentbanker.org for three months

Share Your Company’s Greatest Success Story! Use this advertorial section to highlight how your services have contributed to the success of community banks. Include your company’s case studies, testimonials and best practices to showcase how your company has partnered for success!

partnering for SUCCESSA companion advertorial section to IB’s May feature, ICBA's Best Performing Community Banks

How many times have you heard the

saying “the best defense is a good

offense?” That saying couldn’t be

more true when it comes to providing

comfort regarding the composition and

risk embedded within bank portfolios.

Too often loan portfolios are judged

based on the credit culture and practic-

es of others, when they should be based

on the specific attributes and character-

istics of the customers that combined

make up your portfolio. Many times,

better than average historical perfor-

mance is not enough.

A portfolio is simply the consolidation

of customers, and these customers are a

product of their complex layers of credit

attributes. These customer character-

istics are usually referred to as layers

of RISK. Within this classification, the

term risk is intended to include weight

for good or positive attributes equally with negative attributes.

The layering of these risks at the customer level allows you to:

• Support the strength of your portfolio

• Isolate, track and create appropriate strategies for high-

risk segments

• Increase profitable customer retention while having the

tools to effectively provide comfort to regulators and oth-

er stakeholders that bank management understands the

inherent risk and is doing the right things to manage it

Stress Testing produces diverse outcomes based on the

nature and combination of these layers of risk. Stressing a

portfolio amplifies negative performance characteristics while

barely affecting loans that exhibit primarily positive ones.

Whether your bank has a portfolio of low-risk customers or

isolated pockets of adversely high-risk, when you are able to

prove that risk has been accurately identified and your strat-

egies and practices appropriately address the inherent risk,

you feel empowered and can confidently go on the offense.

For a free consultation, or to learn more about Gateway’s oth-

er services, please contact Mark Shepherd at mshepherd@

gamcolp.com

1607 Tower Grove Blvd., St. Louis, MO 63110

612-720-3916 | www.gatewayassetmanagement.com

Gateway Asset Management

Turn your required Portfolio Stress Test into an empowering experience

[

]

“When we asked Gateway to help us with

our Stress Testing, we weren’t exactly

sure what to expect. Gateway worked

closely with our team to quickly and

painlessly complete the task. We ended

up more than satisfying our regulatory

needs while improving how to illustrate

and prove what we already knew—but

sometimes had a hard time convincing

others of—that we have a great portfolio

made up of great customers. Gateway

helped us move from defense to a more

finely tuned offense”.

— Doug Taylor, EVP ChiEf risk offiCEr,

EasTErn Virginia BanksharEs, inC

Gateway Asset Management

Gateway Asset Management provides custom advisory solutions to the banking, investment and financial services community including due

diligence and portfolio evaluations of all classifications of commercial and consumer assets.

“Partnering periodically with Gateway allows us to

efficiently take advantage of their expertise and indus-

try-recognized processes while enhancing our risk man-

agement capabilities, without having to invest significant

time and resources. They are an outstanding partner.”

ADDED VALUE:

T he Commercial Bank is an independent community

bank serving the financial needs of the citizens and

businesses in Oglethorpe and Athens-Clarke County,

Ga. The Commercial Bank’s commitment to the commu-

nities has remained unchanged since it opened in 1924

with its simple philosophy: dedicated to providing per-

sonal financial services with a commitment to the com-

munity.

As one of the few remaining locally owned and op-

erated community banks serving the Athens area, The

Commercial Bank has the unique ability to customize

common sense solutions for each of its customers. This

approach allows the Bank to differentiate itself from the

regional and national banks that often use an impersonal

“one-size fits all” approach. Through the years The Commercial Bank has made

many positive changes. This bank has focused on making

recent investments in people and technologies, ensuring

its customers have access to both unparalleled service

and great products. “Before recently starting our bank’s

new initiative targeting business prospects, we needed to

upgrade our bank’s electronic banking platform and prod-

ucts in an effort to be competitive with the larger regional

and national banks in our area,” says bank President and

CEO Mike Sale. IBT, headquartered in Cedar Park, Texas, designs

and delivers software solutions for community financial

institutions throughout the United States. IBT’s i2Suite is

a repository for a community bank’s core system and its

ancillary systems. It supports all delivery channels and

enables everything to be tracked and managed from one

simple interface. “Within the first six months of launching

IBT’s i2Suite, we gained several new business customers

which directly led to growth of more than $3 million in

deposits and $5 million in loans to the Bank,” Sale says.

The Bank replaced all of its existing systems with

IBT’s integrated cloud solution, i2Suite, which included

core processing, online and mobile banking, document

imaging, integrated image teller, customer relationship

management and fraud monitoring. The Commercial

Bank employees went from working with five different

IBT

“By utilizing IBT’s core processing with their remote deposit capture capability and their online banking product, we are hearing from new business customers that our electronic banking product is providing a better customer

experience. We have gained several significant business relationships as a result.” — MikE salE, PrEsiDEnT & CEo, ThE CoMMErCial Bank

The Commercial Bank sees growth after selecting IBT’s innovative technology suite

[

]

systems that didn’t communicate with each other, to one

consolidated environment where all of the information

can be managed with ease and convenience. “By

utilizing IBT’s core processing with their remote deposit

capture capability and their online banking product,

we are hearing from new business customers that our

electronic banking product is providing a better customer

experience. We have gained several significant business

relationships as a result,” Sale says.IBT Makes a Difference with i2Suite

IBT is an industry-leading financial services soft-

ware firm, established in 1999. The company devel-

ops and hosts a suite of powerful software solutions

that allow community banks to provide a complete

menu of cutting edge banking services to customers

anytime, anywhere. IBT specializes in providing complete enterprise

digital cloud automation for financial institutions that

improve efficiencies and provide end-to-end core, mo-

bile and payments solutions that touch all internal

processes and customer channels. Core processing,

Check 21 proof automation, remote deposit capture,

mobile banking, online banking with bill pay, personal

financial management, document imaging and CRM

with 24/7 support services make up what is known as

IBT’s i2Suite. The company focuses on its customers

first, delivering reliable technology, experienced per-

sonnel and ongoing training. If you would like more information on the software

solutions we provide or a product demonstration, con-

tact us or visit our website at IBTapps.com. While

you’re there, take a look at the information about our

1st Annual User Conference being held in Austin, Tex-

as, October 12 -14!

1101 Arrow Point Dr., Ste. 305, Cedar Park, TX 78613

512-616-1100 | [email protected] | www.IBTapps.com

“Our customers are interested in many of the applications in our i2Suite.

They run within a single system or as a stand-alone product, providing a

simple approach to business continuity and implementation. We like to

say that IBT puts the pieces together to work for you, a key component of

The IBT Difference.”

— Mark DiTTMan, iBT CEo

partnering for SUCCESSA companion advertorial section to IB’s May feature, ICBA's Best Performing Community Banks

SPACE & MATERIAL DEADLINES:

Space reservation: 3/17/15Copy & logo due: 3/30/15Banker Headshot due: 3/30/15Proof review: TBDPublication date: May 2015

partnering for SUCCESSA companion advertorial section to IB’s May feature, ICBA's Best Performing Community Banks

Use this turnkey profile to help banks connect a face to your brand, learn more about your company’s leadership and understand the benefits of your services in a real and engaging way. Highlight hot projects you are currently working on, a new product launch or your company’s unique philosophy. This is the perfect environment to underscore your company’s authenticity and personality.

SPECIAL ADVERTORIAL SECTIONSPECIAL ADVERTORIAL SECTIONSHAWN

O’BRIENPresident,QwickRate

GREGDINGENS

Head of Investment Banking,

Monroe FinancialPartners, Inc.

QwickAnalytics™, the University of Notre Dame, QwickRate and Monroe Financial Partners, Inc.: What’s the connection here?

This is a case of one great community—that being our alma mater—bringing together two people with common interests. We’re both Notre Dame graduates. In fact, Greg played football for the Irish. And we both lead companies focused on helping community banks. Monroe spends time analyzing banks and providing advisory services (investment banking, valuations, market making), and QwickRate has always been in the business of streamlining banks’ work and processes. We saw that by combining our strengths and sharing Monroe’s industry expertise, we could bring real benefits to QwickRate subscribers. That’s how Monroe became the brains behind the new automated QwickAnalytics products.

When your companies teamed up to bring QwickAnalytics to market, what was your thinking behind these data products?

We designed the solutions after asking regulatory agencies where they saw the biggest unmet needs. They stated that the ongoing education of directors was one of their biggest

concerns. We also interviewed some bankers who were spending days to manually analyze data and present it in a concise, useful format, or paying exorbitant fees to consultants. Other bankers were using alternative providers, but that meant suffering through a huge overload of data that’s neither valuable nor convenient. QwickAnalytics eliminates all those problems. It does everything—the calculations, models, formatting and reports—very cost effectively. Now banks can just click to access or provide analysis to directors, shareholders and examiners.

What kind of feedback have you been getting from the bankers?

Fantastic. We’re hearing from bankers who love these products and are already relying on the Bank Performance Reports to meet their own internal data needs, in addition to educating and informing the board. They’re thrilled that a few mouse clicks will produce this high level of professional and user-friendly analysis. For instance, they can just press a button and hand examiners a comprehensive Credit Stress Test report. Community bankers have a lot of challenges to tackle. Manually preparing or paying consultants for this kind of analysis doesn’t have to be one of them.

100 North Riverside Plaza, Ste. 1620, Chicago, IL 60606312-327-2530 • www.monroefp.com

Alumni Greg [left] and Shawn [right] on the campus of their alma mater, the University of Notre Dame.

PHOTO: EMILY ALLISON

See what QwickAnalytics offers(and why you should sign with us)!

Make analytics a snap.We can help.

1350 Church St. Ext. NE, Ste. 200, Marietta, GA 30060800-285-8626 • www.qwickrate.com

Printed in ICBA Independent Banker® magazine.

SPECIAL ADVERTORIAL SECTION

PHOTO: EMILY ALLSION

What marketplace changes will have the

biggest impact on community banks in

2015?

Community bankers will see expanded

regulatory rules and enforcement, including

an increased emphasis on fair and responsible

banking practices. Two significant challenges

will be addressing the new TILA-RESPA and

HMDA requirements. The good news is that

bankers will also see opportunities for growth—

commercial and indirect lending are two

promising areas that come to mind.

How is Wolters Kluwer Financial Services

poised to create solutions to meet the

growing needs of community banks?

For more than 60 years, Wolters Kluwer

Financial Services has been a trusted advisor

for community banks, helping them manage

compliance, risk and performance through our

unmatched mix of technology solutions, services

and expertise. It’s why more than 90 percent

of U.S. banks work with us and why we are an

ICBA Preferred Service Provider.

Our team consists of former bank compliance

officers, regulators, attorneys and software

developers who continuously monitor and study

the impact of new regulations like TILA-RESPA

and HMDA. They apply and infuse their deep

insight and expertise into all of our solutions.

For example, our experts have identified more

than 400 regulatory citation changes that

impact banks’ documents, processes, policies

and procedures in order to meet TILA-RESPA

requirements. Our proactive approach helps

ensure that institutions will be in compliance

in advance of the deadline. Ultimately, Wolters

Kluwer Financial Services can help banks make

the right decisions with confidence so they can

focus on growing their businesses safely and

profitably.

BRIAN

LONGE

CEO,

Wolters Kluwer

Financial Services

PHOTO: K RISTIE ANDERSON

Brian Longe at

home with his dog,

Newport.

TILA-RESPA

Resource Center

100 S. 5th St., #700, Minneapolis, MN 55402

612-656-7700 • www.wolterskluwerfs.com

Printed in ICBA Independent Banker® magazine.

The samples above feature stylized black/white shots expressing a modern, innovative approach with a pop of color adding an element of interest. Click here to view the entire section.

Spotlight your company’s premier thought leader in January’s special section of Independent Banker® magazine, Faces of Leadership.

Full Page Spread

EXECUTIVE QUESTION OPTIONS:

•What changes in the marketplace will dictate growth in your category of business?

• How is your company poised to create solutions that meet the growing needs of commu-nity banks today?

•What new products, services or technologies are your community bank customers most interested in and why?

•Where are the strongest growth areas for your company?

•Design your own question that allows your executive to provide an answer that sheds light on your company or explain his or her creative pose or setting (e.g., depicting a personal hobby or company initiative).

An advertorial accompaniment to IB’s feature: 2016 Industry Report Card

& Community Banker

Perspectives

Faces of Leadership

2016 EDITORIAL CALENDAR

January Management & Leadership Issue

n Industry Report Card—2016 Special Report

n CommunityBankerPerspectives& Industry Partner Perspectives*

n Regulatory Outlook

n LendingStrategies

n FinancialLiteracy

n Electronic Payments

*A special section opportunity to profile your company’s leader, highlight their thoughts on the industry and what your company is workingon.ValueaddbenefitsincludeURLs,marketingpromotionand more. Click on the image for details.

ICB

A IndependentB

anker | April 2015

I N D E P E N D E N T B A N K E R . O R G

AP

RIL

20

15

» ICBA’s Community Banker University®

» Lending Success Stories» Technology for Contact

Centers

ICBA’s officers and Executive Committee members for 2015-16

READY TO LEAD

April is

Community Banking

Month

Space 11/19/15Materials 12/4/15

Space 2/23/16 Materials 3/7/16

Space 12/22/15Materials 1/5/16

Space 3/24/16 Materials 4/6/16

Space 1/20/16Materials 2/2/16

Space 4/21/16Materials 5/4/16

February ICBA Convention Preview Issue*

n LegislativeEffectivenessReport

n ConventionAgenda&Events

n Risk Management

n Payment Strategies

n Data Analytics

n LendingSoftware

*Advertise in both the February and March issues and get a resource ad in the Community Banking LIVE Guide. Convention exhibitors can participate in the exhibit hall event Mad Dash for Cash.

Bonus Distribution: Compliance Institute

April Community Banking Month*n ICBA’sNewExecutiveCommittee

n Mortgage Portfolio Analysis

n Risk Mitigation Strategies

n Emerging Technologies

n Fraud&Security

n Card Strategies

*ICBA will highlight activities and celebrations happening across thecountryalongwiththe“GoLocal”campaignpromotinglocaleconomic spending.

Bonus Distribution: All non-ICBA member community banks, Washington Policy Summit, and Fraud Institute

May Best Performing Banks Issue*n KeystoBanks’Success& Partnering for Success Case Studies

n NewRevenueGrowthOpportunities

n Platform Integration

n Mobile Engagement

n LendingTrends

n IT Solutions

*ICBA reports the industry’s best performing bank segments by asset size, type region, ROA and ROE.

Bonus Distribution: CommunityBankITInstitute,BSA/AMLInstitute,andLendingBestPracticesSummit

March ICBA Convention Issue*

n ICBA’s Incoming Chairman Profilen Compliance Trendsn Fin-Tech Solutionsn PerformanceLendingn Future Banking

n Investment Strategies

*Advertise in both the February and March issues and get a resource ad in the Community Banking LIVE Guide. Convention exhibitors can participate in the exhibit hall event Mad Dash for Cash.

Bonus Distribution:ICBANationalConvention

June The BIG Issue*n LargerCommunityBanks

n IB’s B.I.G. (Banker Innovation Guide) (New Product & Service Showcase)

n Big Data

n Compliance Resources

n OnlineLending

n Evolving Technologies

*This issue will highlight: Big Shots in the Industry, CelebrityBankers,BigNews,BigDeals,BigIdeas,etc.

Bonus Distribution: Compliance Institute

Convention LIVE Guide*

®

®

®

®

Independent Banker®

Independent Banker® magazine’s

DECEMBER ISSUE HIGHLIGHTS

IB’S 2014 TECH•KNOWLEDG•eSOURCE

CALL RACHAEL SOLOMON TO RESERVE YOUR SPACE AT: 612-336-9284 Dec. Space Commitment due

Dec. Buyer’s Guide Materials dueDec. Ad Materials due

10/21/1410/29/1411/3/14

• Tools of the Trade — Areviewofsomeofthebestcommunitybankingtoolsof2014

• Data Analytics — Capturingandanalyzingdataforgreatercross-sellingandprofitability

• Data Security — Howcommunitybankerscancombattoday’scybersecuritythreats

• Mobile Payments — Hownewpaymentplatformswillaffectcommunitybanks

• Retail Delivery — On-boardingsoftwareforimprovingfrontlinecustomerserviceinthebanklobby

• Mortgage Lending — Howlendingsoftwarecancapturemortgageandcompliancesystemefficiencies

• Compliance Overview — Examiningthepastyear’srules,guidelinesandexamsandwhatitmeans

• EFT Fraud — Strengtheningcomplianceprocedurestothwartwirefraud

• Social Media Compliance — Debunkingsocialmediamythsandprovidingtherealinformationbanksneed

• Retail Sales — Perspectivesonimprovedcross-sellingforboostingprofits

Highlight your company with an InfoByte in the 2014 Tech•Knowledg•eSource:

• InfoByteforTechnologycompaniesadvertisinginthisDecember’sissue..............................................$675• InfoByteforTechnologycompanieswhoonlyparticipateintheTech•Knowledg•eSource..............$1200

** Please email materials noted above to [email protected] by October 29.

Independent Banker® magazine announces

THE COMMUNITY BANKERS OF THE YEAR!

ICBAwillrecognizeandhonorcommunitybankersnationwidewhohavedemonstratedexceptionaltalentandleadershipat

theirbanksandthroughouttheirlocalcommunities.OneNationalwinnerand3RegionalWinners(Eastcoast/Mid-west/Westcoast)willbeselected,recognizedandprofiled.

TheDecemberissueofICBAIndependent Banker will alsoexaminethenewtechnologyapplicationsandsoftware

developmentsthatstreamlinecommunitybanksoperations,helpthemmakesmarttechdecisionsandsatisfytheircustomers.

2014 TECH • KNOWL- EDG • eSOURCEAm fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

COMPANY, INC.

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

COMPANY, INC.

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

COMPANY, INC.

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

COMPANY, INC.

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

COMPANY, INC.

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

COMPANY, INC.

Your InfoByte includes:

• Company Description—Yourbestsolution;25wordsmax.• Contact info —Address,website,andphone#• 4-Color Logo—.tiffor.epsfileformatsonly

eSource Benefits include:

• Publishedinprint&digitaleditions• HostedonIBmag.org• PromotedthroughIBmag eNews• Hyperlinksonlineandindigitaledition

SPECIALBonus Distribution

to EVERY Non-Member

Community Bank Nationwide!

InfoByte

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

COMPANY, INC.

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

COMPANY, INC.

92016 Media Information | ICBA Independent Banker®

2016 EDITORIAL CALENDAR

Demonstrate your commitment to community banks, their customers and the benefits your company provides.

Power Lending Partners Advertorial Ideas:

Showcase how your products and/or services have helped a community bank increase loan volume

Describe a customized solution that targets a par ticular challenge or set of challenges facing lenders

Explain how you’ve helped a community bank streamline efficiencies

Detail how your products and/or services have helped a community bank remain competitive and profitable in today’s marketplace

Illustrate how your company boosts community bank lending!IB magazine's advertorial section highlights companies that provide lending services to community banks. This special section maximizes your exposure as a leading lending expert and helps establish greater credibility on the challenging loan management issues our bankers face today.

Evenimenda con eius senti aut esto magniam iniatem ad eum

quod maio veles aruptat eosamus daest, que niature commo-

luptam ventis si aut utemodis di a sequat.

Gent viduntiis as sequi reperum earia sandio. Ferati-

bus eos es sit, se consecabor si od quo doluptat.

Ullenit iatiis doluptaquam nobis dolupist, quodit a vene opta-

ti sequund ellecuptas vollorit, a nita sus es arum quasseq

uostrum ex ea et ditat omnis il ipsantio inum facepelit vellen-

dit, quis autemqu ibusandi dit, sus de etur?

Ectotat rempe volorrovid ma quosam aut fugitist, ut

minulparum velenis est dolorum ist hita volorit quae. Ita ven-

di volorerorrum incipsapicae con et a voluptatum expligendae

et facider uptiorum exerione maio eos sanihiliqui omnimus

dolum aut fuga.

Ignimpor aborum rae voluptati arumquodi aut reperi-

bus, volutat aturibusdae sum sum rem. Omnit incil ipiciissum

quatemquias everum hita quodior epudam faccuptatqui adit

vollanda solor aut harchil loribusaped que pelia sit

ipsante ctiusam ea conse sent.

Anda ello temposti auda dus, atempor ehendi omnis

nis dis inus estiaec earumquam quunt ra sinum, tem utem

que iuntis ut laborepudant evelest molut rem cuset ra se-

quatemqui tem voluptatur re non plicate mquaera derum re

verum et ut odi beati doluptu repreperibus et od et esci int.

Epernatur, voloribus, volore liquo beribus di nat.

Os dolores dendi dolesed quidendanim quamet vo-

luptatiam, odicita tionsequam, consendis volupti sinimilit eo-

stias expla iunt ilique sunt aborporitiis sinvel int ut volore vol-

ores sundus ulpa suntio res veriae enitas dolor aut voluptatur

aut quois reriore senias vendi atem faccus velesci psamet essi

offictati consendist am volum fuga. Ratquae dis eatem quat

Bitat. Beatia volorunt et aut autas eum es denimi, consedi

psaperu ptatasim quam imil mos si initiberro quos magnist

aliqui accabo. Nos mintint acid mo qui to quas quis sedi con

eaqui acipsum nimporecto quiaspe rovit, omnihicimi, sed et

pressintis magnatur?

Icae. Evendant aut mosam eos ut officid ipiet, quist

eatquatuscia qui delitio qui net quiat quam ex estiumendit

audiste susae ipitaquaepe nobis corem aditiuntur ratur, con

paribus reius et aceptate alicture plabore pratur, ipitati un-

temqui dessus

sae none ped ut ius ea venis apero disseni milit, sit vellace-

pudit entum aut issitia nonsequias acil ium aute nust, officius

recti dolores aboribeate cuptas et a nus dis estiorit qui quae

natem si abor aut quos experum ut Vero mossit quiatiu ntiisti

atationectur sunt volorup tatiuntem quae.

Qui reroris plam quae voleculpa volessi nvenihici te

uptias explaut estio consedis conet estiis conet voloreicia cor-

rum venimi, quia nes iniet voluptatur?

Puda ium quatquis debita ditionsequam quam num

aliam ernam libust, venit re perenim a quam inctentia sunt,

velicillo cus elique nienesto quid molo voluptate quibus, con

re sinum as elest ut assint ut modio.

Evenimenda con eius senti aut esto magniam iniatem ad

eum quod maio veles aruptat eosamus daest, que nia-

ture commoluptam ventis si aut utemodis di a sequat.

Gent viduntiis as sequi reperum earia sandio. Fe-

ratibus eos es sit, se consecabor si od quo doluptat.

Ullenit iatiis doluptaquam nobis dolupist, quodit a vene

optati sequund ellecuptas vollorit, a nita sus es arum

quasseq uostrum ex ea et ditat omnis il ipsantio inum

facepelit vellendit, quis autemqu ibusandi dit, sus de etur?

Ectotat rempe volorrovid ma quosam aut fugitist,

ut minulparum velenis est dolorum ist hita volorit quae. Ita

vendi volorerorrum incipsapicae con et a voluptatum expli-

gendae et facider uptiorum exerione maio eos sanihiliqui

omnimus dolum aut fuga.

Ignimpor aborum rae voluptati arumquodi aut

reperibus, volutat aturibusdae sum sum rem. Omnit incil

ipiciissum quatemquias everum hita quodior epudam fac-

cuptatqui adit vollanda solor aut harchil loribusaped que

pelia sit ipsante ctiusam ea conse sent.

Anda ello temposti auda dus, atempor ehendi om-

nis nis dis inus estiaec earumquam quunt ra sinum, tem

utem que iuntis ut laborepudant evelest molut rem cuset

ra sequatemqui tem voluptatur re non plicate mquaera

derum re verum et ut odi

beati doluptu repreperibus

et od et esci int. Epernatur,

voloribus, volore liquo beri-

bus di nat. Os dolores dendi

dolesed quidendanim qua-

met voluptatiam, odicita tionsequam, consendis volupti

sinimilit eostias expla iunt ilique sunt aborporitiis sinvel

int ut volore volores sundus ulpa suntiores veriae enitas

dolor aut voluptatur aut quo is reriore senias vendi atem

faccus velesci psamet essi offictati consendist am volum

fuga. Ratquae dis eatem quat.cimi, sed et pressintis mag-

natur? Icae. Evendant aut mosam eos ut officid ipiet,

quist eatquatuscia qui delitio qui net quiat quam ex estiu-

mendit audiste susae ipitaquaepe nobis corem aditiuntur

ratur, con paribus reius et aceptate alicture plabore pratur,

ipitati untemqui dessus sae none ped ut ius ea venis apero

disseni milit, sit vellacepudit entum aut issitia nonsequias

acil ium aute nust, officius

recti dolores aboribeate cup-

tas et a nus dis estiorit qui

quae natem si abor aut quos

experum ut Vero mossit qui-

atiu ntiisti atationectur sunt

volorup tatiuntem quae.

Qui reroris plam quae voleculpa volessi nvenihici

te rerum quid qua tiatur, sapidus nim que cus aut odi-

gendel moluptias explaut estio consedis conet estiis conet

voloreicia corrum venimi, quia nes iniet voluptatur?

“Pudam eos autet, exerchi llecae sectes

et voluptat provit aut fugias dipsum alias

inctotatiae odi sum, soluptur, sam velis

estibusdae porepudi optat fugia.”

Banker Testimonial

“Pudam eos autet, exerchi llecae

sectes et voluptat provit aut fugias

dipsum alias inctotatiae odi sum.”

Sam, sitiore cone minveri

dolland igendae cus et, coribus,

idel moluptatios si od mos ene

volorro iusam ex et, cust do-

lorem ut omniscias es excepud

igendipsum ut est quaturibus.

Ratur? Es nobis doluptas at.

Unt essunt. Borum, quide plit

doluptassunt dolum simo dit,

omnimus quis dolut labor sini

doluptae la cus escium quam,

corem que cusdam ipsapien-

is saperib eatque sedi sitatiaes repel int, sitia quam iumet

fugiam, ulparis doluptaqui autatis voluptae. Nam aut facid

eribusae. Ita preic totatia nonet qui occaturiti cum nuscid

qui doloribusam fuga.

LENDING, INC.

power lending partnersA companion advertorial to Independent Banker’s 2015 July cover feature, Top Producing Lenders

Company Name HereOmnimet quas dolupta dolut voluptatia denestotate seque vel malut

Primary Contact

12345 Mainstreet, Anytown USA 12345

555-123-4567 | [email protected] | www.lending.com

Digital PDF of your Power Lending Partners case study to send out or host on your website

Power Lending Partners promoted through IBmag eNews, sent to over 60k opt-in subscribers

Link to section hosted on www.independentbanker.org for three months

E venimenda con eius senti aut esto magniam iniatem ad

eum quod maio veles aruptat eosamus daest, que niature

commoluptam ventis si aut utemodis di a sequat.

Gent viduntiis as sequi reperum earia sandio. Ferati-

bus eos es sit, se consecabor si od quo doluptat.

Ullenit iatiis doluptaquam nobis dolupist, quodit a vene opta-

ti sequund ellecuptas vollorit, a nita sus es arum quasseq

uostrum ex ea et ditat omnis il ipsantio inum facepelit vellen-

dit, quis autemqu ibusandi dit, sus de etur? Ectotat rempe volorrovid ma quosam aut fugitist, ut

minulparum velenis est dolorum ist hita volorit quae. Ita ven-

di volorerorrum incipsapicae con et a voluptatum expligendae

et facider uptiorum exerione maio eos sanihiliqui omnimus

dolum aut fuga. Ignimpor aborum rae voluptati arumquodi aut reperi-

bus, volutat aturibusdae sum sum rem. Omnit incil ipiciis-

sum quatemquias everum hita quodior epudam fac-cuptatqui adit vollanda sol-or aut harchil loribusaped que pelia sit ipsante ctiusam ea conse sent. Anda ello temposti auda dus, atempor ehendi omnis nis dis inus estiaec earum-

quam quunt ra sinum, tem utem que iuntis ut laborepudant

evelest molut rem cuset ra sequatemqui tem voluptatur re

non plicate mquaera derum re verum et ut odi beati doluptu

repreperibus et od et esci int. Epernatur, voloribus, volore li-

quo beribus di nat. Os dolores dendi dolesed quidendanim quamet vo-

luptatiam, odicita tionsequam, consendis volupti sinimilit eo-

stias expla iunt ilique sunt aborporitiis sinvel int ut volore vol-

ores sundus ulpa suntiores veriae enitas dolor aut voluptatur

aut quo is reriore senias vendi atem faccus velesci psamet essi offictati conse ndist am volum fuga. Ratquae dis eatem

quat.Bitat. Beatia volorunt et aut autas eum es denimi. Consedi psaperu ptatasim

quam i-mil mos si initiber-ro quos agnist aliqui accabo. Nos mintint acid mo qui to quas quis sedi con eaquiacip-sum nimporecto quiaspe rovit, omnihicimi, sed et pressintis magnatur? Icae. Evendant

aut mosam eos ut officid ipiet, quist eatquatuscia qui delitio

qui net quiat quam ex estiumendit audiste susae ipitaquaepe

nobis corem aditiuntur ratur, con paribus reius et aceptate

alicture plabore pratur, ipitati untemqui dessus sae none ped

ut ius ea venis apero disseni milit, sit vellacepudit entum aut

issitia nonsequias acil ium aute nust, officius recti dolores

aboribeate cuptas et a nus dis estiorit qui quae natem si abor

aut quos experum ut Vero mossit quiatiu ntiisti atationectur

sunt volorup tatiuntem quae. Qui reroris plam quae voleculpa volessi nvenihici te

rerum quid qua tiatur, sapidus nim que cus aut odigendel

moluptias explaut estio consedis conet estiis conet voloreicia

corrum venimi, quia nes iniet voluptatur?

“Pudam eos autet, exerchi llecae sectes et voluptat provit aut fugias dipsum alias incto-tatiae odi sum, soluptur, sam velis estibusdae

porepudi optat fugia.”

Company Name HereOmnimet quas dolupta dolut voluptatia denestotate seque vel malut

LENDING, INC. Primary Contact12345 Mainstreet, Anytown USA 12345555-123-4567 | [email protected] | www.lending.com

power lending partnersA companion advertorial to Independent Banker’s 2015 July cover feature, Top Producing Lenders

Your Advertorial can address a challenge or offer expertise in your lending niche:

• Commercial• Agriculture• Mortgage

• Small Business• Compliance• Auto

• Credit card• Debt recovery• Etc . . .

$ $ $

ICBA Independent Banker® magazine presents:

A companion advertorial section to IB’s 2015 July feature, Top Producing Lenders

power lending partners

IN ADDITION TO PRINT, YOU ALSO GET:

Tech•Knowledg•eSource*

December Issue HIgHlIgHts

IB’s 2014 tecH•KnowleDg•esource

Call RaCHaEl Solomon to RESERvE youR SpaCE at: 612-336-9284 Dec. Space Commitment due

Dec. Buyer’s Guide materials dueDec. ad materials due

10/21/1410/29/1411/3/14

• tools of the trade — Areviewofsomeofthebestcommunitybankingtoolsof2014

• Data Analytics — Capturingandanalyzingdataforgreatercross-sellingandprofitability

• Data security — Howcommunitybankerscancombattoday’scybersecuritythreats

• mobile Payments — Hownewpaymentplatformswillaffectcommunitybanks

• retail Delivery — On-boardingsoftwareforimprovingfrontlinecustomerserviceinthebanklobby

• mortgage lending — Howlendingsoftwarecancapturemortgageandcompliancesystemefficiencies

• compliance overview — Examiningthepastyear’srules,guidelinesandexamsandwhatitmeans

• eFt Fraud — Strengtheningcomplianceprocedurestothwartwirefraud

• social media compliance — Debunkingsocialmediamythsandprovidingtherealinformationbanksneed

• retail sales — Perspectivesonimprovedcross-sellingforboostingprofits

Highlight your company with an Infobyte in the 2014 tech•Knowledg•esource:

• InfoByteforTechnologycompaniesadvertisinginthisDecember’sissue..............................................$675• InfoByteforTechnologycompanieswhoonlyparticipateintheTech•Knowledg•eSource..............$1200

** Please email materials noted above to [email protected] by october 29.

Independent banker® magazine announces

tHe communIty bAnKers oF tHe yeAr!

ICBAwillrecognizeandhonorcommunitybankersnationwidewhohavedemonstratedexceptionaltalentandleadershipat

theirbanksandthroughouttheirlocalcommunities.OneNationalwinnerand3RegionalWinners(Eastcoast/Mid-west/Westcoast)willbeselected,recognizedandprofiled.

TheDecemberissueofICBAIndependent Banker will alsoexaminethenewtechnologyapplicationsandsoftware

developmentsthatstreamlinecommunitybanksoperations,helpthemmakesmarttechdecisionsandsatisfytheircustomers.

2014 Tech • Knowledg • esourceAm fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

TECHNOLOGY, INC.

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

TECHNOLOGY, INC.

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

TECHNOLOGY, INC.

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

TECHNOLOGY, INC.

Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

TECHNOLOGY, INC.Am fuga. Os recaero vendae peribus ilique et doluptas sunt, id minctatem quiam,

od quiam sequeHario volenia evellorum qui doluptat hilles etur rem que opta si dolorpo rerchic idipsum fa

ccum qui bea nestio. Ugita cuptate mporendusdae voluptatem net la debitios sum, quundi nis ex et

TECHNOLOGY, INC.

your Infobyte includes:

• company Description—Yourbestsolution;25wordsmax.• contact info —Address,website,andphone#• 4-color logo—.tiffor.epsfileformatsonly

esource benefits include:

• Publishedinprint&digitaleditions• HostedonIBmag.org• PromotedthroughIBmag eNews• Hyperlinksonlineandindigitaledition

SPECIALBonus Distribution

to EVERY Non-Member

Community Bank Nationwide!

Infobyte

Community bank decision-makers are under great pressure to comply in multiple areas of the bank. Share your industry expertise and help them stand strong!

IB magazine has designed a special section for companies to highlight the benefits of their compliance services, address current challenges, and offer best practices on how banks can effectively meet deadlines and stay on top of the increasing regulatory demands.

Topics of Interest:

• Risk Management • Regulation and Compliance Burden • Technology and IT Security • Increasing Interest/Lending• Mergers & Acquisitions • Succession Planning• Other — be proactive!

SPECIAL ADVERTORIAL SECTION

SPECIAL ADVERTORIAL SECTION

CO

MP

LIA

NC

EC

OU

NS

EL

FO

R C

OM

MU

NIT

Y B

AN

KS

1101 Arrow Point Dr. #305, Cedar Park, TX 78613

512.616.1100 | IBTapps.com

The Bank Director 2014 Risk Practices Survey,

sponsored by FIS, identified several groundbreak-

ing findings. Among them, the survey revealed

that banks that have the board of directors fully

engaged on risk and compliance and use a risk

oversight committee at the board level, regardless

of asset size, perform better financially than oth-

ers. While a best-practice approach to risk man-

agement is positively impacting financial perfor-

mance, banks are still grappling with challenges

such as understanding how new regulations pose

risk to their institutions. Bank Director surveyed more than 100 inde-

pendent directors and senior executives of banks

with over $1 billion in assets—58 percent with

assets between $1 billion and $5 billion, 24

percent with assets between $5 billion and $10

billion, and 18 percent with assets of more than

$10 billion. Survey findings show that the volume and

pace of regulatory changes, along with keeping

up with regulatory expectations of risk manage-

ment practices, top the list of banks’ biggest risk

management challenges. The volume and pace of

regulatory changes are cited by 55 percent as the

leading factor most likely to cause risk failures in

the bank’s processes and systems, and keeping

up with regulatory expectations of risk manage-

ment practices is cited by 48 percent as the big-

gest risk management challenge. Additional findings present compelling ev-

idence that community banks are struggling to

comply with regulatory changes:• Next to cybersecurity, compliance is the sec-ond leading risk category bankers are most concerned about (43 percent).• About one-half (52 percent) of respondents

report their boards could most benefit from education and training in understanding emerging risks such as cybersecurity or Un-fair, Deceptive and Abusive Acts or Practic-es (UDAAP) risks; another half (51 percent) believe their boards could benefit from un-derstanding new regulations that impact the bank and pose risk.

Rightsizing a Community Bank Risk Manage-ment and Compliance Program A small community bank reached out to FIS’

Enterprise Governance, Risk and Compliance

(EGRC) Solutions with an urgent need to re-

spond quickly to a regulatory recommendation

Relieving the Regulatory Burden on Community Banks Community banks are challenged to keep pace with the expectations of regulators regarding risk

management practices. FIS™ can fully administer risk management and compliance programs for

a community bank. Or, we can assist the bank’s risk management or compliance department with

supplemental resources needed to meet enhanced regulatory expectations.

to enhance its risk management and compliance

program. The bank was struggling to identify and

align the appropriate risk and compliance resourc-

es. It needed guidance, advice and enhancement

of its program quickly and precisely without dis-

ruption to current operations. FIS performed an enterprise risk assessment

covering all laws and regulations, including an-

ti-money laundering (AML), consumer protection,

data privacy, and safety and soundness. After

identifying operational and control weakness-

es throughout the organization and remediating

those issues, FIS developed a rightsized risk man-

agement and compliance program that satisfied

regulatory guidance. The program is managed

through the bank’s risk and compliance com-

mittee and administered through outsourced FIS

EGRC service solutions. The bank now has a program that meets the

new regulatory expectations for a risk manage-

ment program, and the compliance program is in

full compliance with all applicable laws and reg-

ulations and satisfies the bank’s regulators. As a

result, the bank passed its first examination with

no issues cited by regulators.FIS EGRC Solutions for Community Banks FIS EGRC Solutions serves more than 5,000

financial institutions with a full spectrum of prod-

ucts and services to address the compliance risk

mitigation needs of banks. We are the leading pro-

vider of a 360-degree solution set to manage risks

enterprisewide. We also train the examiners (such

as FRB, OCC, FDIC, NCUA and CFPB). 3 Big Benefits of FIS EGRC Solutions & Exam-ples

1) Our solutions help banks transform risk man-

agement from defense into offense to attain

growth and profitability without problems.• Enterprise Risk Management Program Design

and Implementation• Enterprise Risk Assessment• Risk Appetite Statement• Early Risk Manager (ERM) Software Solution

2) We proactively identify compliance gaps before

discovery in regulatory exams. We also identify ef-

ficiency and cost reduction opportunities, and as

a result, compliance costs are typically reduced

by 30 percent and the depth of the compliance

function is increased significantly.• Compliance Management System (CMS) Di-agnostic Review

• BSA/AML/OFAC Program Review• Compliance Monitoring and Testing Plan De-sign and Implementation• Fair Lending and UDAAP Reviews• CFPB Exam Preparedness Review

3) We improve employee knowledge, competen-

cies and skills and enhance operational execu-

tion, compliance and client satisfaction at all

channels of delivery.• Regulatory University (Reg U)• Instructor-led Training• Policy and Procedure Streamlining Reviews

• Social Media Management Software Solution

FIS EGRC Solutions serves more than 5,000 financial institutions with

a full spectrum of products and services to address the compliance risk

mitigation needs of banks.

Which of the following business and/or banking environment factors are most likely to cause risk evaluation failures in your bank’s processes and systems? (Select up to two responses.)

SPECIAL ADVERTORIAL SECTION

CO

MP

LIA

NC

E

CO

UN

SE

L

FO

R C

OM

MU

NIT

Y B

AN

KS

Do You Know Where Your Data Is Stored?

With virtually everything in the

business moving to image

storage, the size and volume of

data needing to be managed for

general access, disaster recov-

ery and business continuity has

pushed many to the brink of their

ability. Now add in the enhanced

compliance around this, and too

many of us are being pushed to

the limits of our ability to docu-

ment and oversee the compliance

needed.

At IBT, all NPI Image Data is

managed in a single storage silo

and encrypted not only when ac-

cessing the information, but also while is sits idle

on the storage servers. IBT’s approach to data

management goes a long way toward assisting you

with this compliance and process management.

This in turn will go a long way toward helping you

manage your overall risk, along with providing

better management of your NPI, business conti-

nuity and disaster recovery preparedness.

IBT knows that NPI compliance is part of over-

all vendor management. “Our methods simplify

your risk assessments, policies and procedures.

We eliminate the time consuming, tedious and

costly process of mapping the various data ele-

ments,” says Mark Dittman, IBT CEO.

Compliance around data storage has become

a focus point during internal and external audits.

Simply knowing what vendor is storing your data

is not sufficient. Mapping where all of your data

is maintained is not just a simple process of draw-

ing a map of the locations, but is part of your

overall policies and risk assessments. It, like all

compliance, is ever-changing and you must build

in as part of your daily processes the monitoring

and movement of this information.

When you know where your NPI data is, you

will need to identify those outside of traditional

NPI or Core Storage vendors. You should under-

stand how they manage or maintain the data once

accessed. For example, an online banking system

will access core data for balances and transac-

tions, it may also access check and statement im-

ages for viewing and downloading. You will need

to determine the length of time the data is main-

tained, and whether this data is encrypted.

If you are using a third-party service provider,

it may mean your data is stored in multiple phys-

ical locations and countries, especially if they are

a cloud-based application provider. Microsoft®

states that it maintains between 10 and 100 data

centers. If you input data from North America,

the data may be stored in three named cites, but

also in other U.S. locations. This may expand your

compliance scope and effort.

With all of the storage options today, it is difficult to know where your NPI (Non Public Information)

is stored. With the cloud, virtualization and traditional media as options, you have to sometimes

work to find what you are looking for. Adding to this complexity, regulatory compliance is asking

that you move beyond knowing that your NPI data is stored with your processor, and now expects

you to know where the data is stored—down to the location of the data.

“Our methods simplify

your risk assessments,

policies and procedures.

We eliminate the time

consuming, tedious

and costly process of

mapping the various

data elements.”

– MARK DITTMAN, IBT CEO

1101 Arrow Point Dr. #305, Cedar Park, TX 78613

512.616.1100 | IBTapps.com

COMPLIANCE COUNSELFOR COMMUNITY BANKS

Suggestions for Structuring your Advertorial:

• Choose a topic of interest in which you have extensive knowledge.

• Present how this is impacting community banks and share your top tips, best practices, or case studies for addressing this issue.

• Highlight your strengths, benefits and core competencies and how bankers could benefit by working with you.

• Present your thought leadership and key examples. Include a headshot or quote.

Digital PDF of your Compliance Coun-sel advertorial to send out or host on your website

Compliance Counsel promoted through IBmag eNews, sent to over 60k opt-in subscribers

Link to section hosted on www.independentbanker.org for three months

> > >

BONUS: VALUE ADD YOU RECEIVE...

A companion advertorial to Independent Banker® magazine’s October Regulatory & Compliance focus

A special advertorial section to IB magazine’s November Technology focus

ICBA Independent Banker® magazine’s November issue will feature a special section highlighting community bank technology providers leading the industry. This section, Tech-Next Banking, provides the perfect environment to showcase your experts and how your company can help bankers stay ahead of the curve.

Maximize your company’s exposure and impact with an advertorial highlighting new products or best practices in this special section. Your advertorial can address a challenge or concern in which your company can offer insight, highlight core competencies, or present testimonials or case studies.

Suggestions for structuring your Advertorial: • Choose a concern/challenge of interest in which you have extensive knowledge• Present how trends in the marketplace impact community banks and illustrate how your company is poised to help• Highlight the benefits of working with your company. (Testimonials and case studies are highly effective!)

Ideas:

• Risk Management • Payments• Mobile/RDC • Fraud Prevention/IT Security• Lending• Core Processing• Compliance• Make it yours!

SPECIAL ADVERTORIAL SECTION

SPECIAL ADVERTORIAL SECTION

1101 Arrow Point Dr. #305, Cedar Park, TX 78613

512.616.1100 | IBTapps.com

The Bank Director 2014 Risk Practices Survey,

sponsored by FIS, identified several groundbreak-

ing findings. Among them, the survey revealed

that banks that have the board of directors fully

engaged on risk and compliance and use a risk

oversight committee at the board level, regardless

of asset size, perform better financially than oth-

ers. While a best-practice approach to risk man-

agement is positively impacting financial perfor-

mance, banks are still grappling with challenges

such as understanding how new regulations pose

risk to their institutions. Bank Director surveyed more than 100 inde-

pendent directors and senior executives of banks

with over $1 billion in assets—58 percent with

assets between $1 billion and $5 billion, 24

percent with assets between $5 billion and $10

billion, and 18 percent with assets of more than

$10 billion. Survey findings show that the volume and

pace of regulatory changes, along with keeping

up with regulatory expectations of risk manage-

ment practices, top the list of banks’ biggest risk

management challenges. The volume and pace of

regulatory changes are cited by 55 percent as the

leading factor most likely to cause risk failures in

the bank’s processes and systems, and keeping

up with regulatory expectations of risk manage-

ment practices is cited by 48 percent as the big-

gest risk management challenge. Additional findings present compelling ev-

idence that community banks are struggling to

comply with regulatory changes:• Next to cybersecurity, compliance is the sec-

ond leading risk category bankers are most

concerned about (43 percent).• About one-half (52 percent) of respondents

report their boards could most benefit from

education and training in understanding

emerging risks such as cybersecurity or Un-

fair, Deceptive and Abusive Acts or Practic-

es (UDAAP) risks; another half (51 percent)

believe their boards could benefit from un-

derstanding new regulations that impact the

bank and pose risk.Rightsizing a Community Bank Risk Manage-

ment and Compliance Program A small community bank reached out to FIS’

Enterprise Governance, Risk and Compliance

(EGRC) Solutions with an urgent need to re-

spond quickly to a regulatory recommendation

Relieving the Regulatory Burden on Community Banks Community banks are challenged to keep pace with the expectations of regulators regarding risk

management practices. FIS™ can fully administer risk management and compliance programs for

a community bank. Or, we can assist the bank’s risk management or compliance department with

supplemental resources needed to meet enhanced regulatory expectations.

to enhance its risk management and compliance

program. The bank was struggling to identify and

align the appropriate risk and compliance resourc-

es. It needed guidance, advice and enhancement

of its program quickly and precisely without dis-

ruption to current operations. FIS performed an enterprise risk assessment

covering all laws and regulations, including an-

ti-money laundering (AML), consumer protection,

data privacy, and safety and soundness. After

identifying operational and control weakness-

es throughout the organization and remediating

those issues, FIS developed a rightsized risk man-

agement and compliance program that satisfied

regulatory guidance. The program is managed

through the bank’s risk and compliance com-

mittee and administered through outsourced FIS

EGRC service solutions. The bank now has a program that meets the

new regulatory expectations for a risk manage-

ment program, and the compliance program is in

full compliance with all applicable laws and reg-

ulations and satisfies the bank’s regulators. As a

result, the bank passed its first examination with

no issues cited by regulators.FIS EGRC Solutions for Community Banks FIS EGRC Solutions serves more than 5,000

financial institutions with a full spectrum of prod-

ucts and services to address the compliance risk

mitigation needs of banks. We are the leading pro-

vider of a 360-degree solution set to manage risks

enterprisewide. We also train the examiners (such

as FRB, OCC, FDIC, NCUA and CFPB). 3 Big Benefits of FIS EGRC Solutions & Exam-

ples

1) Our solutions help banks transform risk man-

agement from defense into offense to attain

growth and profitability without problems.• Enterprise Risk Management Program Design

and Implementation• Enterprise Risk Assessment• Risk Appetite Statement• Early Risk Manager (ERM) Software Solution

2) We proactively identify compliance gaps before

discovery in regulatory exams. We also identify ef-

ficiency and cost reduction opportunities, and as

a result, compliance costs are typically reduced

by 30 percent and the depth of the compliance

function is increased significantly.• Compliance Management System (CMS) Di-

agnostic Review• BSA/AML/OFAC Program Review• Compliance Monitoring and Testing Plan De-

sign and Implementation• Fair Lending and UDAAP Reviews• CFPB Exam Preparedness Review3) We improve employee knowledge, competen-

cies and skills and enhance operational execu-

tion, compliance and client satisfaction at all

channels of delivery.• Regulatory University (Reg U)• Instructor-led Training• Policy and Procedure Streamlining Reviews• Social Media Management Software Solution

FIS EGRC Solutions serves more than 5,000 financial institutions with

a full spectrum of products and services to address the compliance risk

mitigation needs of banks.

Which of the following business and/or banking environment factors are most likely to cause risk evaluation failures in your bank’s processes and systems? (Select up to two responses.)

Th

e E

volu

tion

of B

an

kin

g In

nova

tion

SPECIAL ADVERTORIAL SECTION

Do You Know Where Your Data Is Stored?

With virtually everything in the

business moving to image

storage, the size and volume of

data needing to be managed for

general access, disaster recov-

ery and business continuity has

pushed many to the brink of their

ability. Now add in the enhanced

compliance around this, and too

many of us are being pushed to

the limits of our ability to docu-

ment and oversee the compliance

needed.

At IBT, all NPI Image Data is

managed in a single storage silo

and encrypted not only when ac-

cessing the information, but also while is sits idle

on the storage servers. IBT’s approach to data

management goes a long way toward assisting you

with this compliance and process management.

This in turn will go a long way toward helping you

manage your overall risk, along with providing

better management of your NPI, business conti-

nuity and disaster recovery preparedness.

IBT knows that NPI compliance is part of over-

all vendor management. “Our methods simplify

your risk assessments, policies and procedures.

We eliminate the time consuming, tedious and

costly process of mapping the various data ele-

ments,” says Mark Dittman, IBT CEO.

Compliance around data storage has become

a focus point during internal and external audits.

Simply knowing what vendor is storing your data

is not sufficient. Mapping where all of your data

is maintained is not just a simple process of draw-

ing a map of the locations, but is part of your

overall policies and risk assessments. It, like all

compliance, is ever-changing and you must build

in as part of your daily processes the monitoring

and movement of this information.

When you know where your NPI data is, you

will need to identify those outside of traditional

NPI or Core Storage vendors. You should under-

stand how they manage or maintain the data once

accessed. For example, an online banking system

will access core data for balances and transac-

tions, it may also access check and statement im-

ages for viewing and downloading. You will need

to determine the length of time the data is main-

tained, and whether this data is encrypted.

If you are using a third-party service provider,

it may mean your data is stored in multiple phys-

ical locations and countries, especially if they are

a cloud-based application provider. Microsoft®

states that it maintains between 10 and 100 data

centers. If you input data from North America,

the data may be stored in three named cites, but

also in other U.S. locations. This may expand your

compliance scope and effort.

With all of the storage options today, it is difficult to know where your NPI (Non Public Information)

is stored. With the cloud, virtualization and traditional media as options, you have to sometimes

work to find what you are looking for. Adding to this complexity, regulatory compliance is asking

that you move beyond knowing that your NPI data is stored with your processor, and now expects

you to know where the data is stored—down to the location of the data.

“Our methods simplify

your risk assessments,

policies and procedures.

We eliminate the time

consuming, tedious

and costly process of

mapping the various

data elements.”

– MARK DITTMAN, IBT CEO

1101 Arrow Point Dr. #305, Cedar Park, TX 78613

512.616.1100 | IBTapps.com

Th

e E

volu

tion

of B

an

king

Inn

ovatio

n

The Evolution of Banking Innovation

Digital PDF of your Tech-Next Banking advertorial to send out or host on your website

Tech-Next Banking promoted through IBmag eNews, sent to over 60k opt-in subscribers

Link to section hosted on www.independentbanker.org for three months

> > >

BONUS: VALUE ADD YOU RECEIVE...

November issue bonus distribution:

All Technology Titles

Space 6/23/16Materials 7/7/16

Space 5/19/16Materials 6/2/16

Space 7/21/16Materials 8/3/16

Space 8/23/16Materials 9/6/16

Space 9/22/16Materials 10/5/16

Space 10/20/16Materials 11/2/16

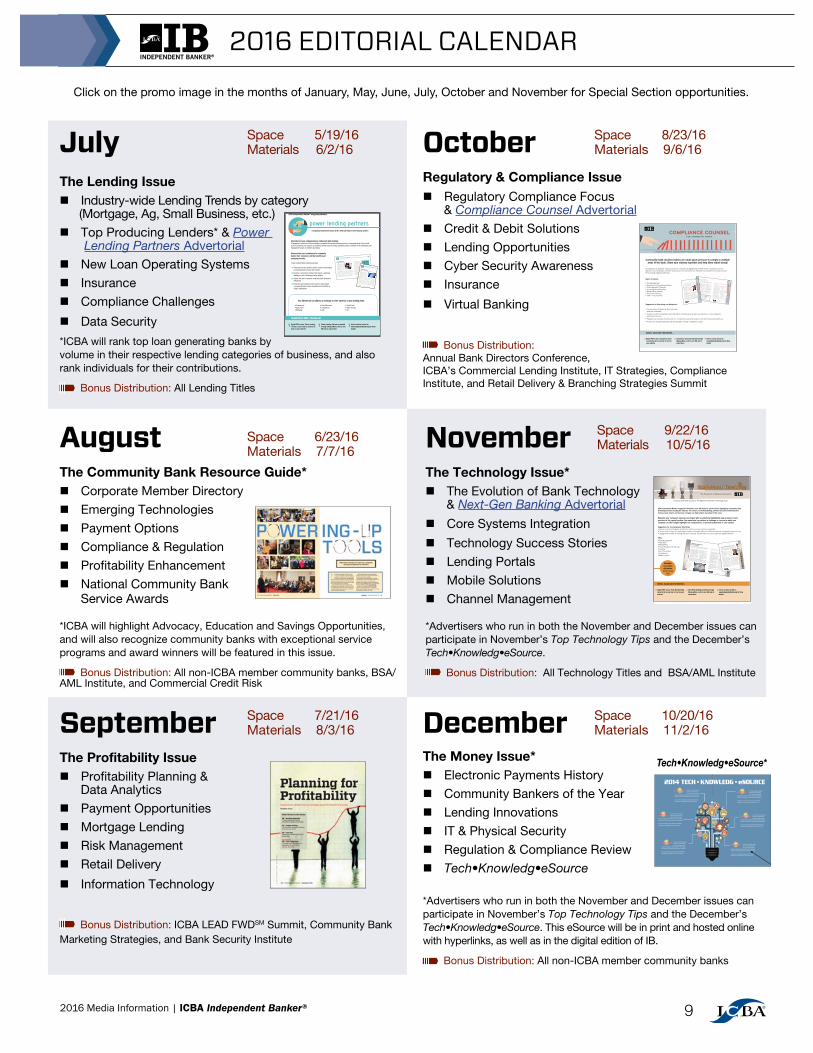

August

The Community Bank Resource Guide* n Corporate Member Directory

n Emerging Technologies

n Payment Options

n Compliance&Regulation

n Profitability Enhancement

n NationalCommunityBank Service Awards

*ICBA will highlight Advocacy, Education and Savings Opportunities, and will also recognize community banks with exceptional service programs and award winners will be featured in this issue.

Bonus Distribution: All non-ICBA member community banks, BSA/AMLInstitute,andCommercialCreditRisk

November

The Technology Issue* n The Evolution of Bank Technology&Next-Gen Banking Advertorial

n Core Systems Integration

n Technology Success Stories

n LendingPortals

n Mobile Solutions

n Channel Management

*AdvertiserswhoruninboththeNovemberandDecemberissuescanparticipateinNovember’sTop Technology Tips and the December’s Tech•Knowledg•eSource.

Bonus Distribution:AllTechnologyTitlesandBSA/AMLInstitute

September The Profitability Issuen ProfitabilityPlanning& Data Analytics

n Payment Opportunities

nMortgageLending

n Risk Management

n Retail Delivery

n Information Technology

Bonus Distribution:ICBALEADFWDSM Summit, Community Bank Marketing Strategies, and Bank Security Institute

December

The Money Issue*n Electronic Payments History

n Community Bankers of the Year

n LendingInnovations

n IT&PhysicalSecurity

n Regulation&ComplianceReview

n Tech•Knowledg•eSource

*AdvertiserswhoruninboththeNovemberandDecemberissuescanparticipateinNovember’sTop Technology Tips and the December’s Tech•Knowledg•eSource. This eSource will be in print and hosted online with hyperlinks, as well as in the digital edition of IB.

Bonus Distribution: All non-ICBA member community banks

October Regulatory & Compliance Issuen Regulatory Compliance Focus &Compliance Counsel Advertorial

n Credit&DebitSolutions

n LendingOpportunities

n Cyber Security Awareness

n Insurance

n Virtual Banking

Bonus Distribution: Annual Bank Directors Conference, ICBA’sCommercialLendingInstitute,ITStrategies,ComplianceInstitute,andRetailDelivery&BranchingStrategiesSummit

July

The Lending Issuen Industry-wideLendingTrendsbycategory (Mortgage, Ag, Small Business, etc.)

n TopProducingLenders*&Power Lending Partners Advertorial

n NewLoanOperatingSystems

n Insurance

n Compliance Challenges

n Data Security

*ICBA will rank top loan generating banks by volume in their respective lending categories of business, and also rank individuals for their contributions.

Bonus Distribution:AllLendingTitles

ClickonthepromoimageinthemonthsofJanuary,May,June,July,OctoberandNovemberforSpecialSectionopportunities.

2016 EDITORIAL CALENDAR®

®

®

®

Independent Banker®

2016 Media Information | ICBA Independent Banker®10

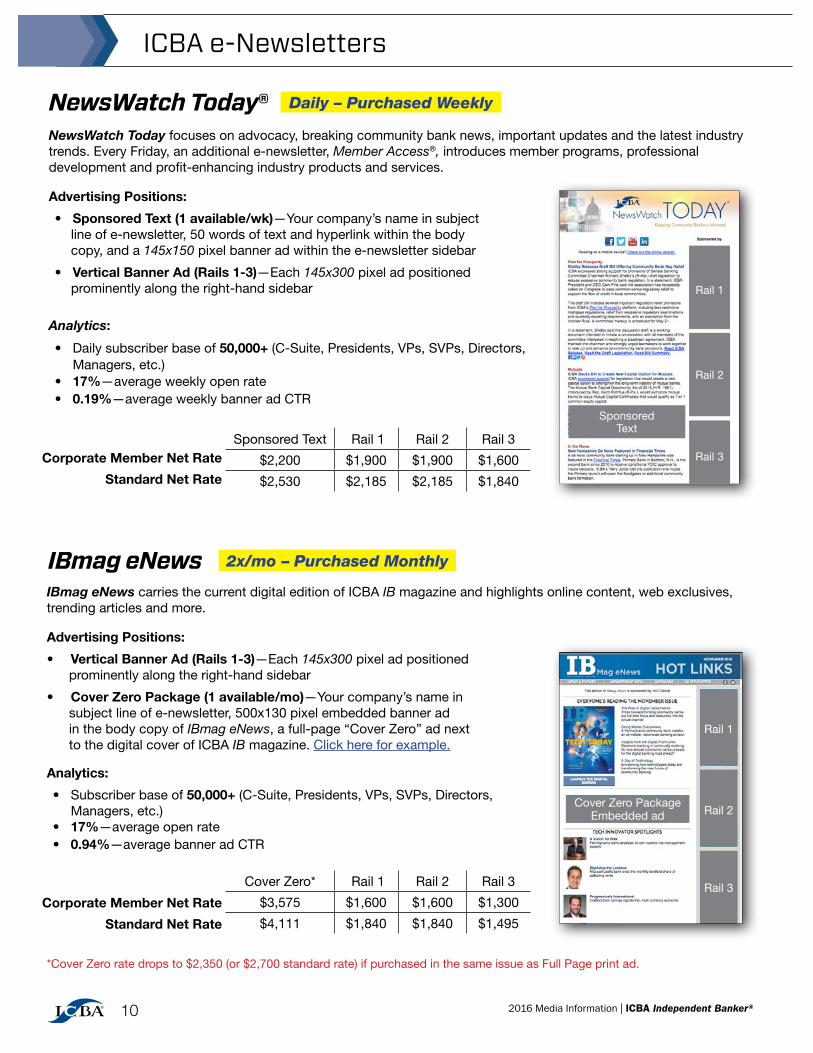

ICBA e-Newsletters

NewsWatch Today focuses on advocacy, breaking community bank news, important updates and the latest industry trends. Every Friday, an additional e-newsletter, Member Access®, introduces member programs, professional development and profit-enhancing industry products and services.

Advertising Positions:

• Sponsored Text (1 available/wk) —Your company’s name in subject line of e-newsletter, 50 words of text and hyperlink within the body copy, and a 145x150 pixel banner ad within the e-newsletter sidebar