Languages

Pages

Legal

Recent Economic Developments in

Singapore

Outline for this Presentation

Structure of the Singapore Economy

Business Cycles in Singapore

Dynamics of the 2001 Recession

Characteristics of the Initial Upturn

Support Provided by Policy

Structure of the Singapore Economy

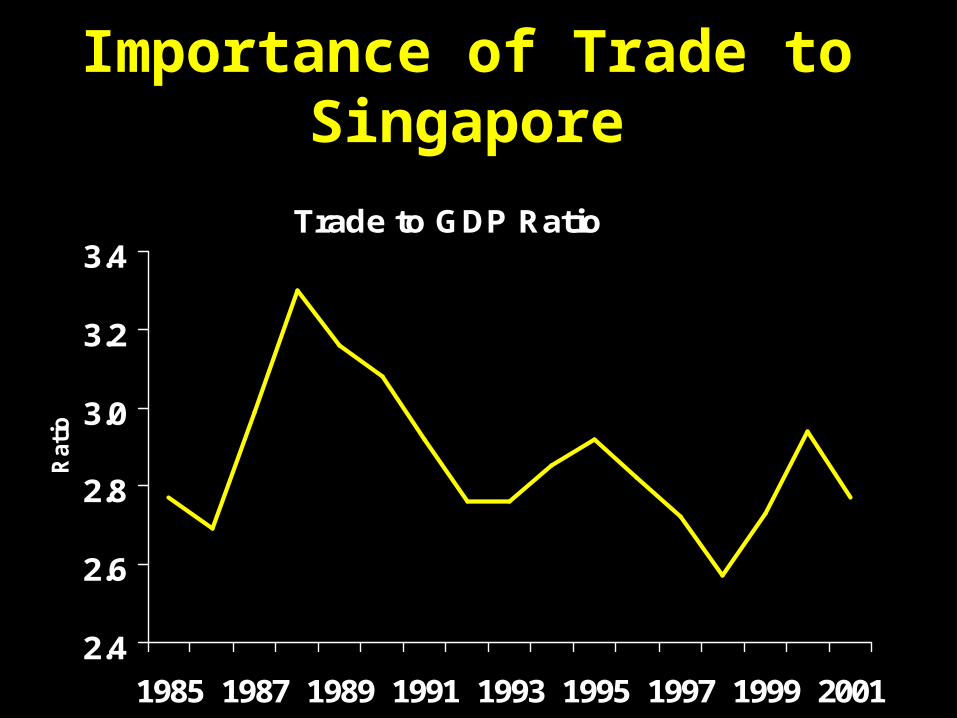

Importance of Trade to Singapore

Trade to GDP Ratio

2.4

2.6

2.8

3.0

3.2

3.4

1985 1987 1989 1991 1993 1995 1997 1999 2001

Rati

o

Structure of the EconomyBy Sector

Manufacturing (22%)

Construction (6%)

Commerce (18%)

Transport & Comm. (11%)

Business Services (14%)

Others (17%)

Key Services Sectors = 67%

Financial Services (12%)

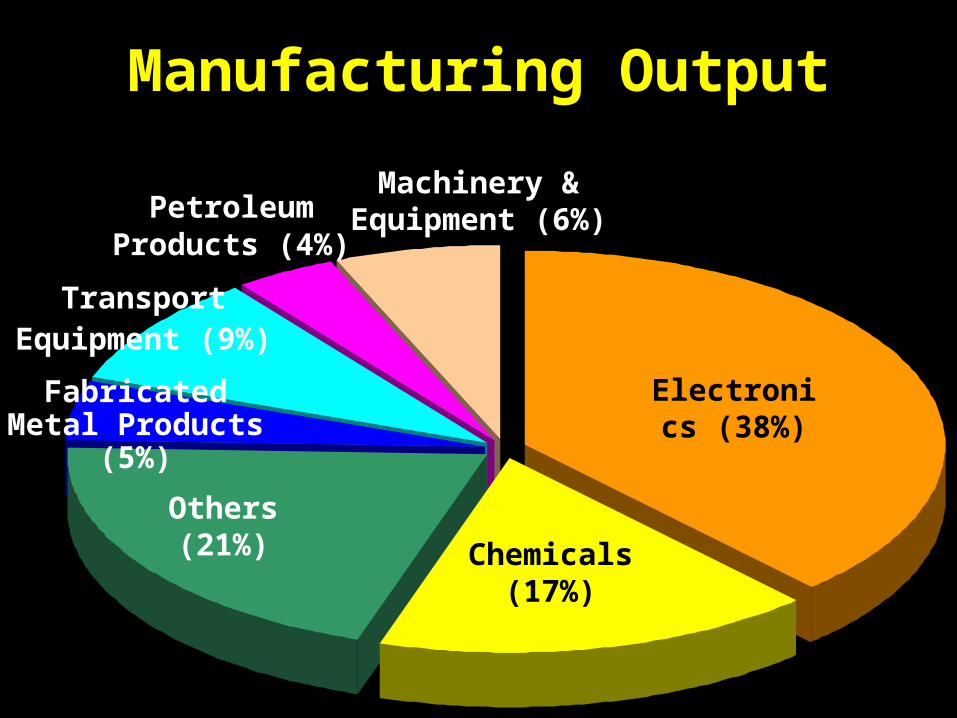

Manufacturing Output

Chemicals (17%)

PetroleumProducts (4%)

Others (21%)

Electronics (38%)

Machinery & Equipment (6%)

TransportEquipment (9%)

Fabricated Metal Products (5%)

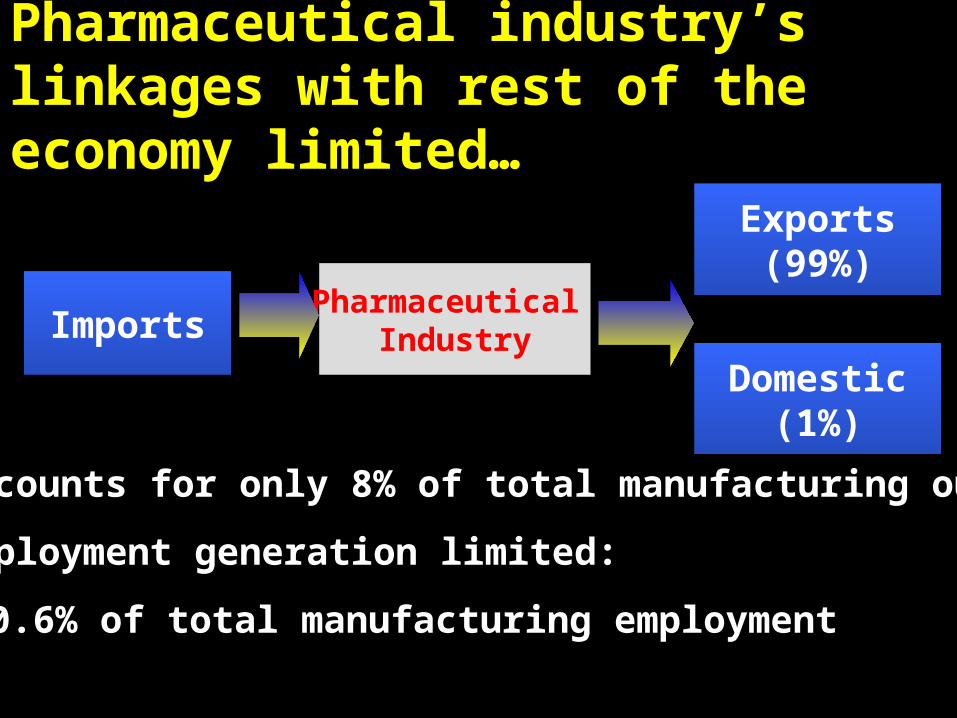

Pharmaceutical industry’s linkages with rest of the economy limited…

Pharmaceutical Industry

Accounts for only 8% of total manufacturing output

Employment generation limited:

0.6% of total manufacturing employment

Imports

Exports(99%)

Domestic(1%)

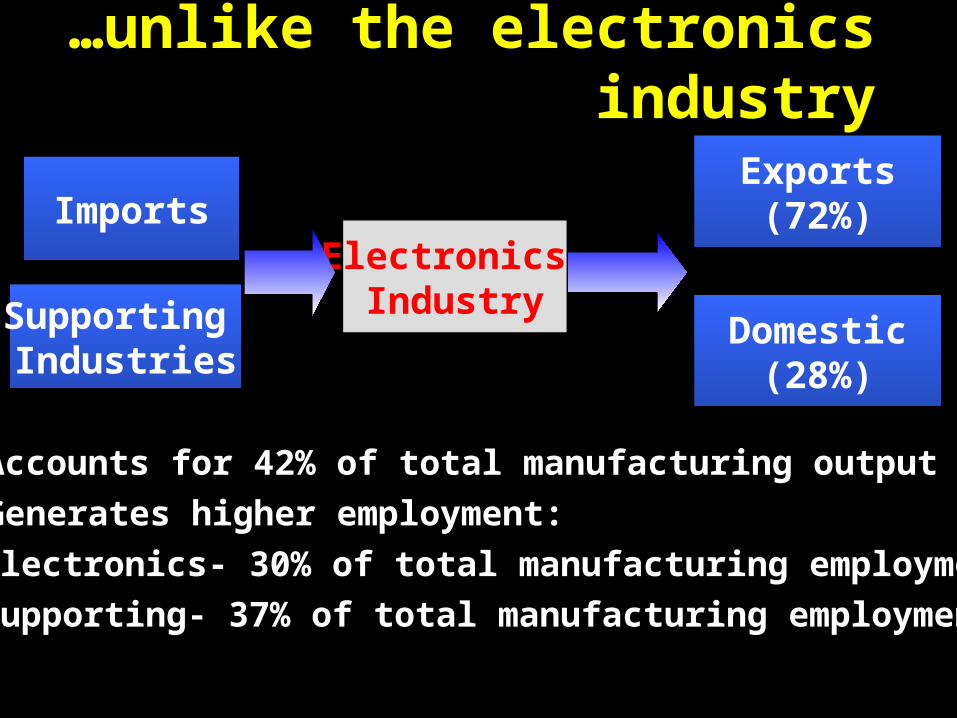

…unlike the electronics industry

Electronics Industry

Accounts for 42% of total manufacturing output Generates higher employment:

Electronics- 30% of total manufacturing employment

Supporting- 37% of total manufacturing employment

ImportsExports(72%)

Supporting Industries

Domestic(28%)

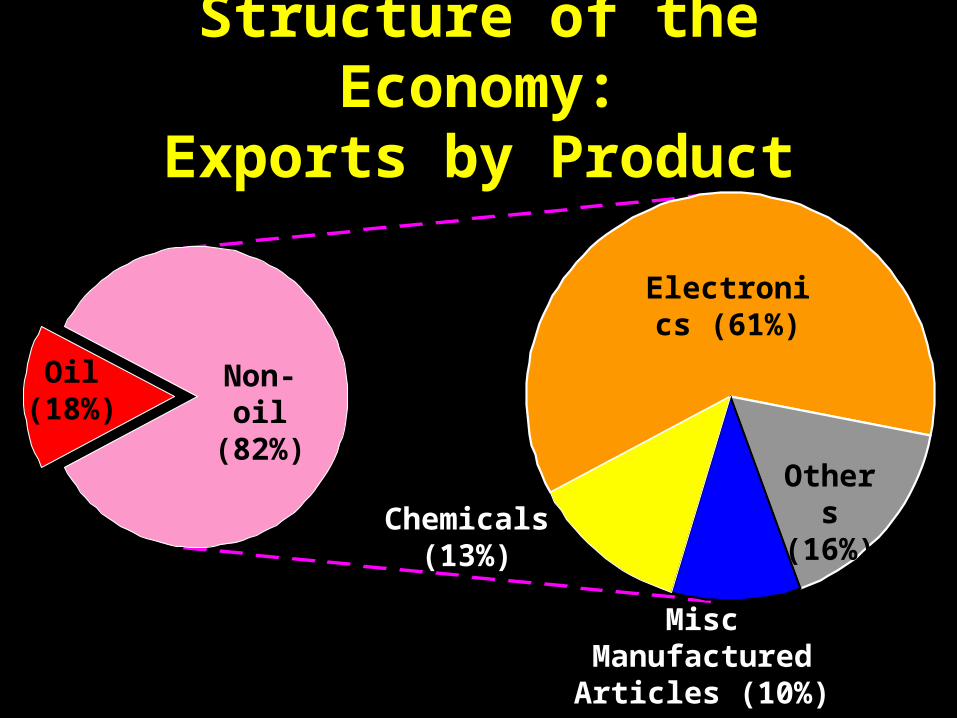

Structure of the Economy:

Exports by Product

Non-oil (82%)

Oil (18%)

Electronics (61%)

Chemicals (13%)

Others (16%)

Misc Manufactured Articles (10%)

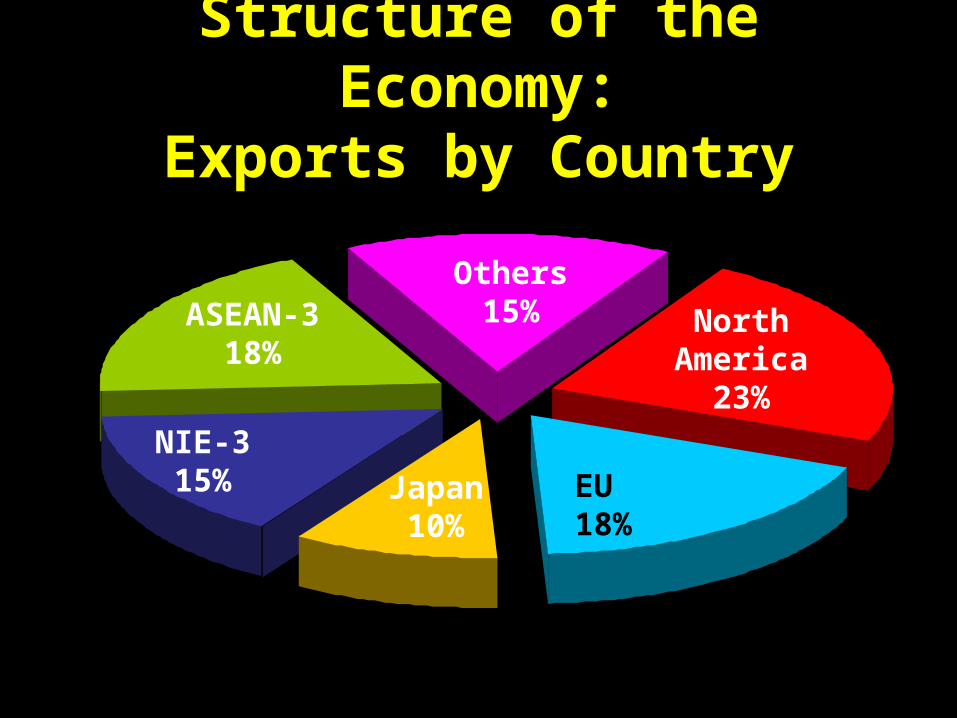

Others 15% North

America 23%

EU 18%

Japan 10%

NIE-3 15%

ASEAN-3 18%

Structure of the Economy:

Exports by Country

Summary I

Ultra Open Economy

Manufacturing & Services as Twin Pillars

Dominance of Electronics in

Manufacturing / Exports

Chemicals Rising But Less Linkages &

Multiplier’s Effects

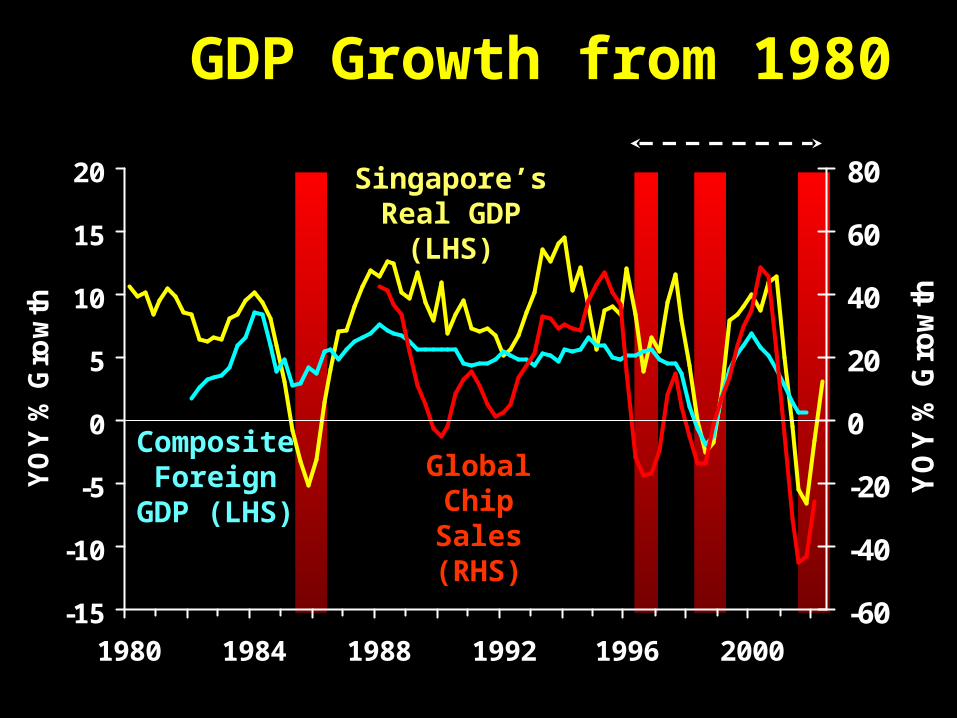

Business Cycles in Singapore

-15

-10

-5

0

5

10

15

20

1980 1984 1988 1992 1996 2000

YO

Y %

Gro

wth

-60

-40

-20

0

20

40

60

80

YO

Y %

Gro

wth

Singapore’sReal GDP

(LHS)

GDP Growth from 1980

Composite Foreign

GDP (LHS)

Global Chip Sales

(RHS)

Dynamics of the 2001 Recession

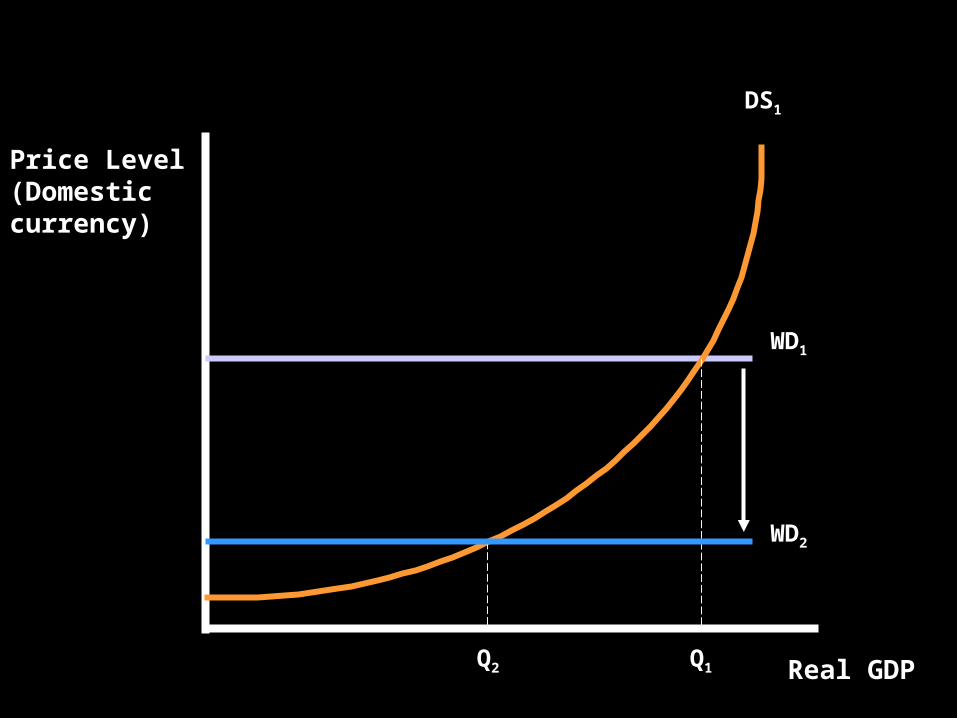

World Demand-Domestic Supply CurveDS1

WD1

WD2

Price Level (Domestic currency)

Real GDPQ1Q2

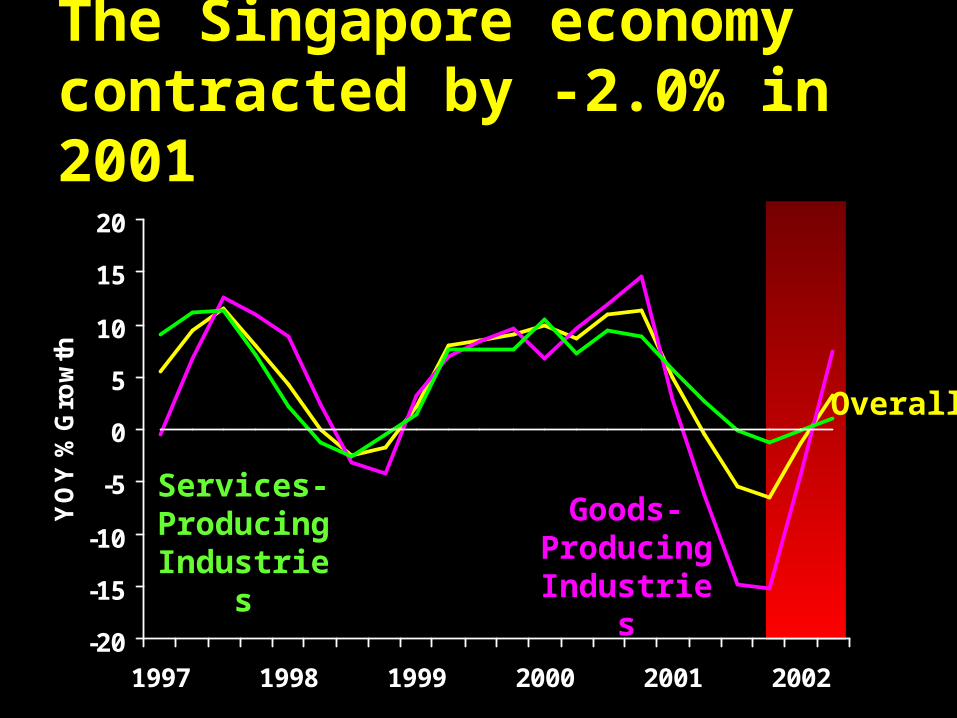

The Singapore economy contracted by -2.0% in 2001

-20

-15

-10

-5

0

5

10

15

20

1997 1998 1999 2000 2001 2002

YO

Y %

Gro

wth

Overall

Goods-Producing Industries

Services-Producing Industries

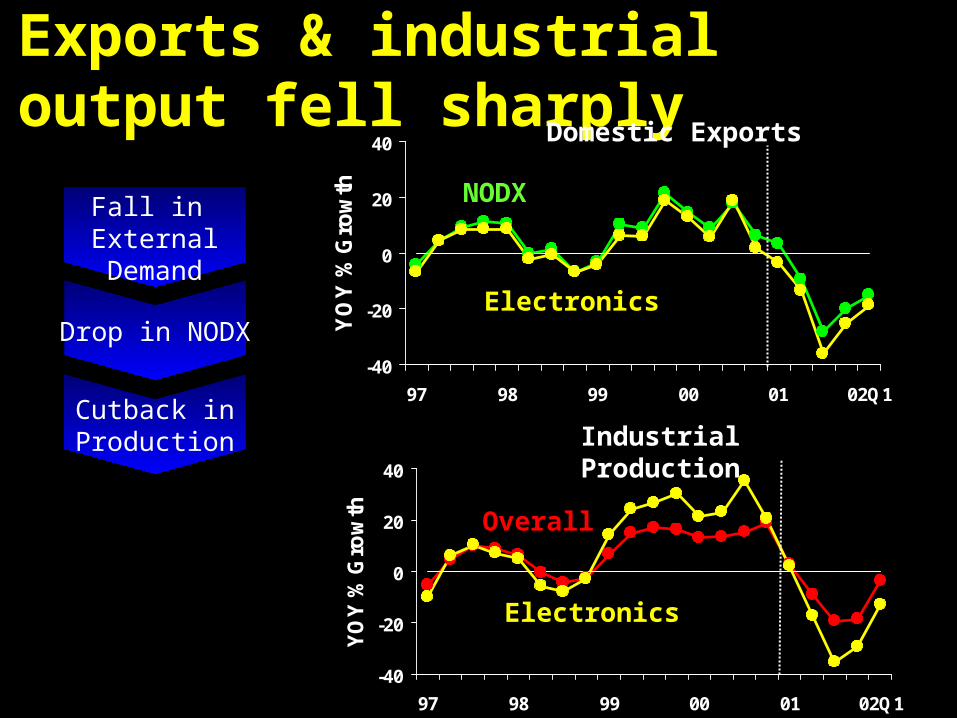

Exports & industrial output fell sharply

-40

-20

0

20

40

97 98 99 00 01 02Q1

YO

Y %

Gro

wth

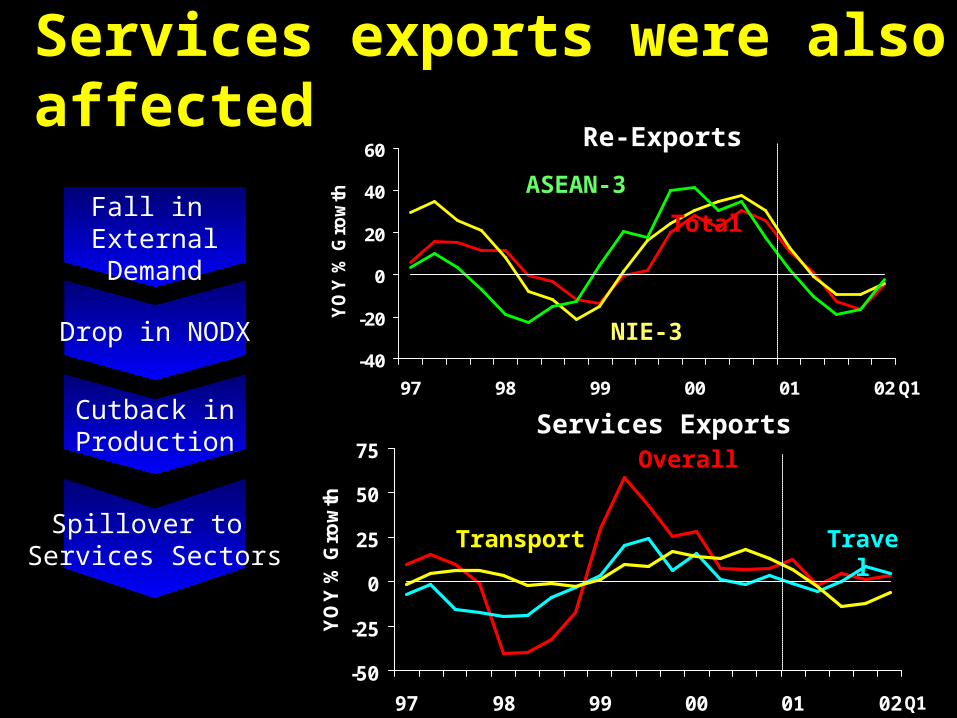

Fall in ExternalDemand

Drop in NODX

NODX

Electronics

Domestic Exports

-40

-20

0

20

40

97 98 99 00 01 02Q1

YO

Y %

Gro

wth

Cutback inProduction

Overall

Electronics

Industrial Production

-40

-20

0

20

40

60

97 98 99 00 01 02

YO

Y %

Gro

wth

Spillover to Services Sectors

Services exports were also affected

Total

ASEAN-3

NIE-3

Re-Exports

-50

-25

0

25

50

75

97 98 99 00 01 02

YO

Y %

Gro

wth

TravelTransport

Overall

Services Exports

Q1Cutback inProduction

Fall in ExternalDemand

Drop in NODX

Q1

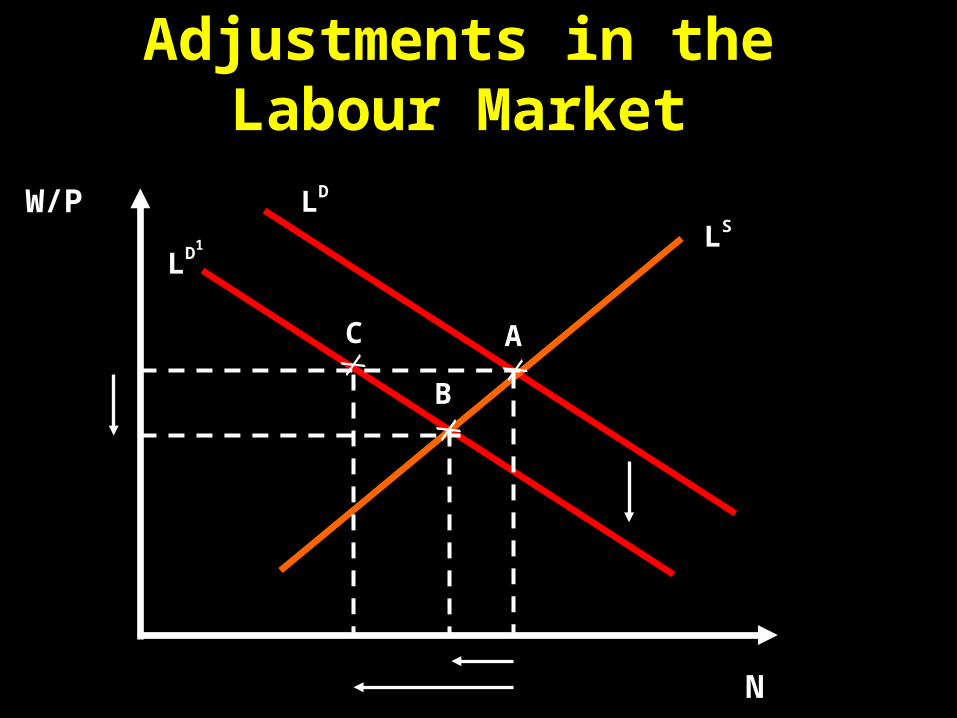

Adjustments in theLabour Market

N

W/PLS

X

A

LD

C

X

B

X

LD1

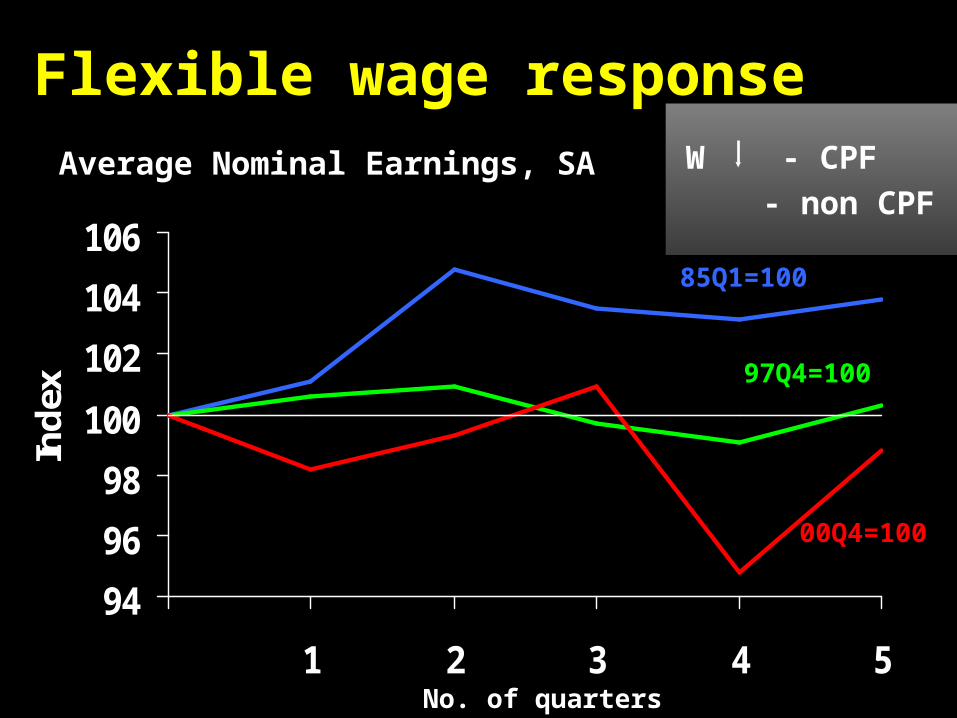

Flexible wage responseAverage Nominal Earnings, SA

94

96

98

100

102

104

106

1 2 3 4 5

Ind

ex

No. of quarters

85Q1=100

97Q4=100

00Q4=100

W - CPF- non CPF

-10

-8

-6

-4

-3-2-10

2

3

4

-40 -20 0Exports CPI

Real GDP

Unemployment Rate

2001

19981985

GDP Downturn in

Summary of Key Indicators : Peak-to-Trough Adjustments

Comparisons Across Downturns

-7.7 (3Q)-3.1 (3Q)-5.3 (3Q)

-0.9 (3Q)-1.6 (4Q)-2.0 (4Q)

2.1 (4Q)2.7 (5Q)3.6 (7Q)

-28.4 (4Q) -7.7 (4Q)-12.9 (2Q)

Summary IIMore volatile environment – 3 shocks in 5 years

Cause shifts in AD curve

Dynamics of Recession :

Exports Output Services Labour Market

Prices

2001: Deepest Recession

2001 : Wages adjusted quickly

Characteristics of the Initial Upturn

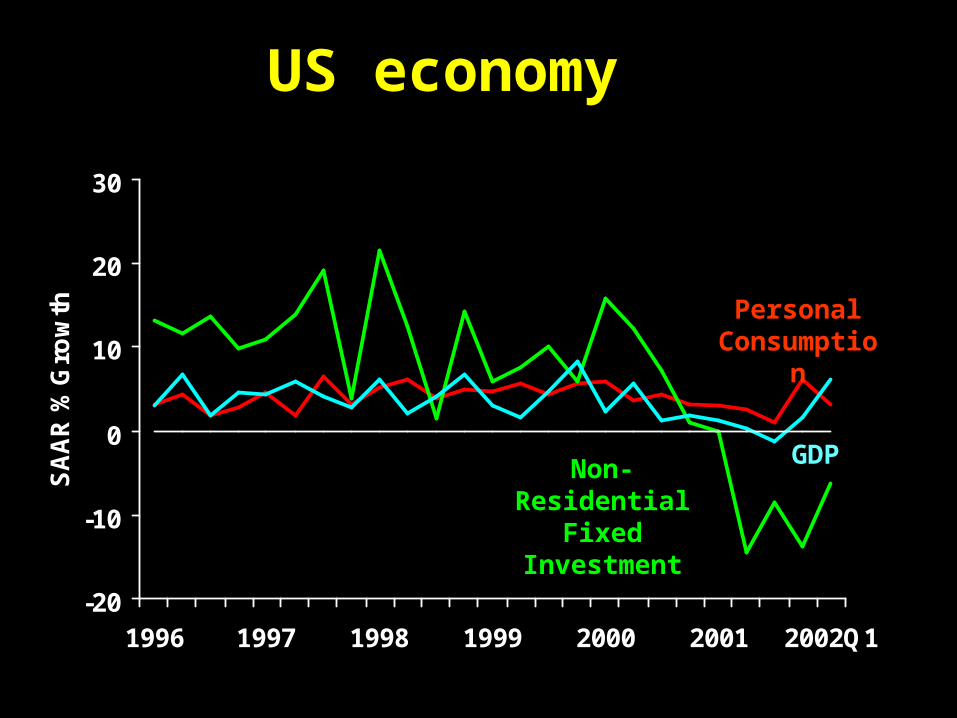

US economy

-20

-10

0

10

20

30

1996 1997 1998 1999 2000 2001 2002Q1

SA

AR

% G

row

th

Non-Residential Fixed

Investment

GDP

Personal Consumption

-15

-10

-5

0

5

10

15

20

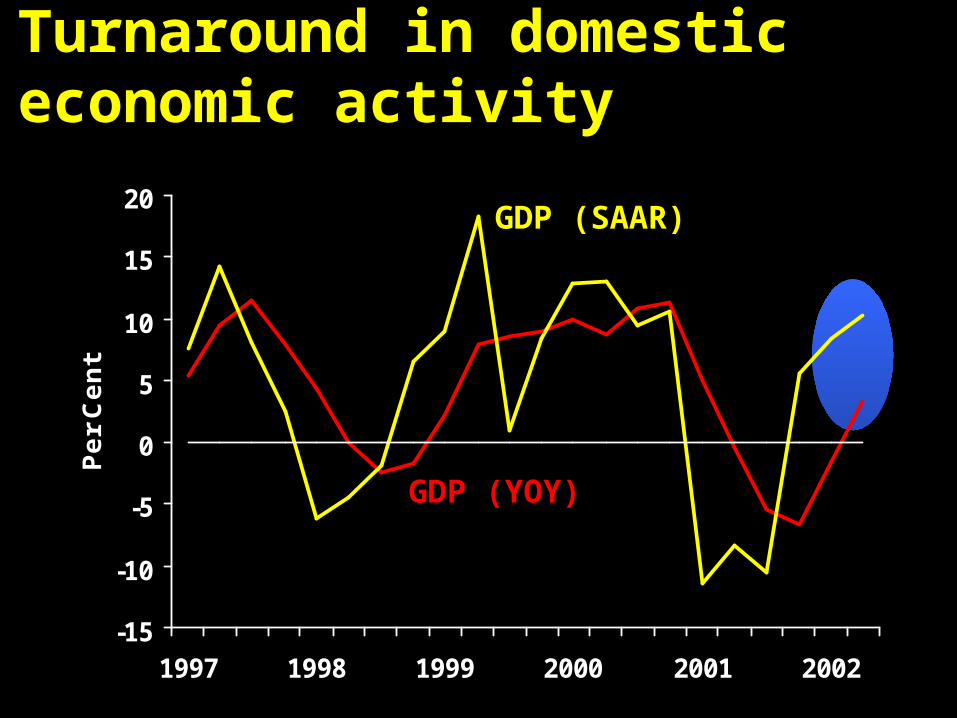

1997 1998 1999 2000 2001 2002

Pe

r C

en

t

GDP (YOY)

GDP (SAAR)

Turnaround in domestic economic activity

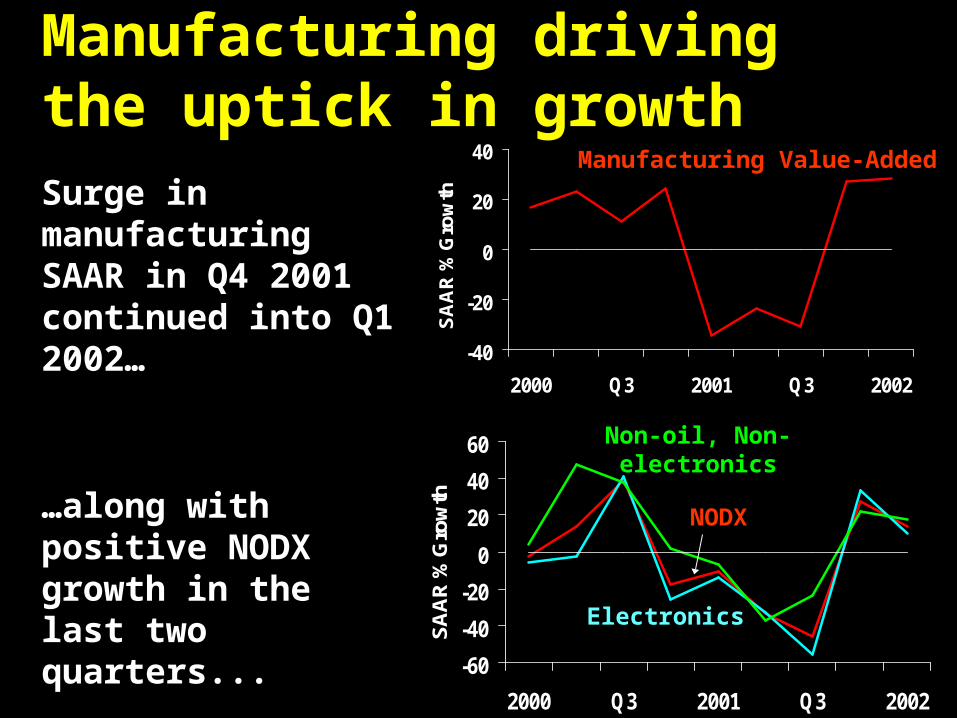

Manufacturing driving the uptick in growthSurge in manufacturing SAAR in Q4 2001 continued into Q1 2002…

…along with positive NODX growth in the last two quarters...

-40

-20

0

20

40

2000 Q3 2001 Q3 2002

SA

AR

% G

row

th

Manufacturing Value-Added

-60

-40

-20

0

20

40

60

2000 Q3 2001 Q3 2002

SA

AR

% G

row

thNon-oil, Non-electronics

NODX

Electronics

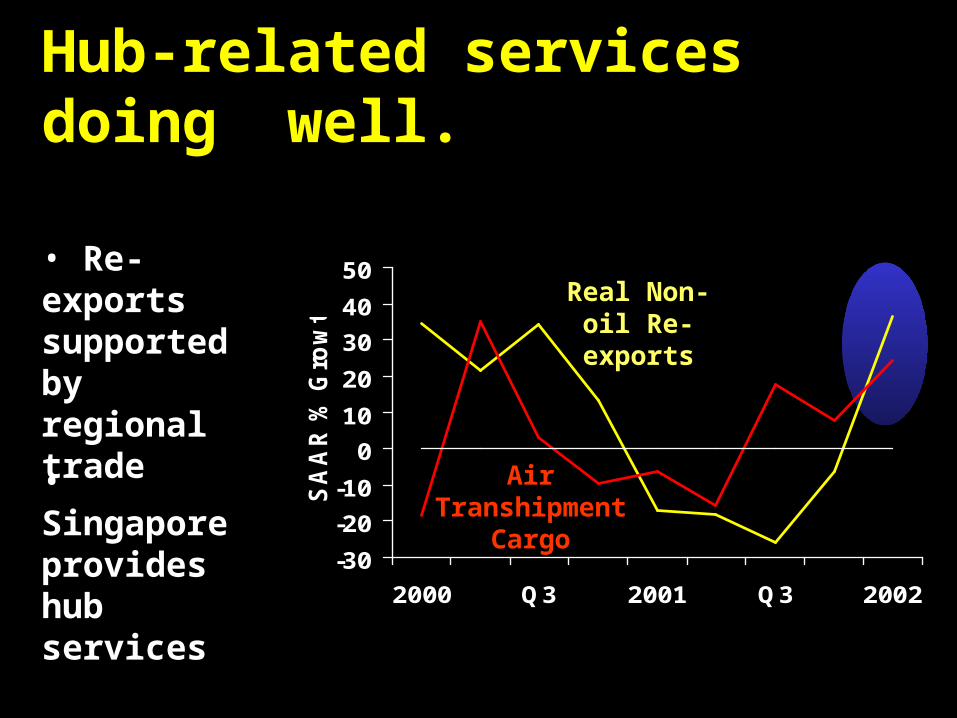

Hub-related services doing well.

-30

-20

-10

0

10

20

30

40

50

2000 Q3 2001 Q3 2002

SA

AR

% G

row

th

Air Transhipment

Cargo

Real Non-oil Re-exports

• Re-exports supported by regional trade

• Singapore provides hub services

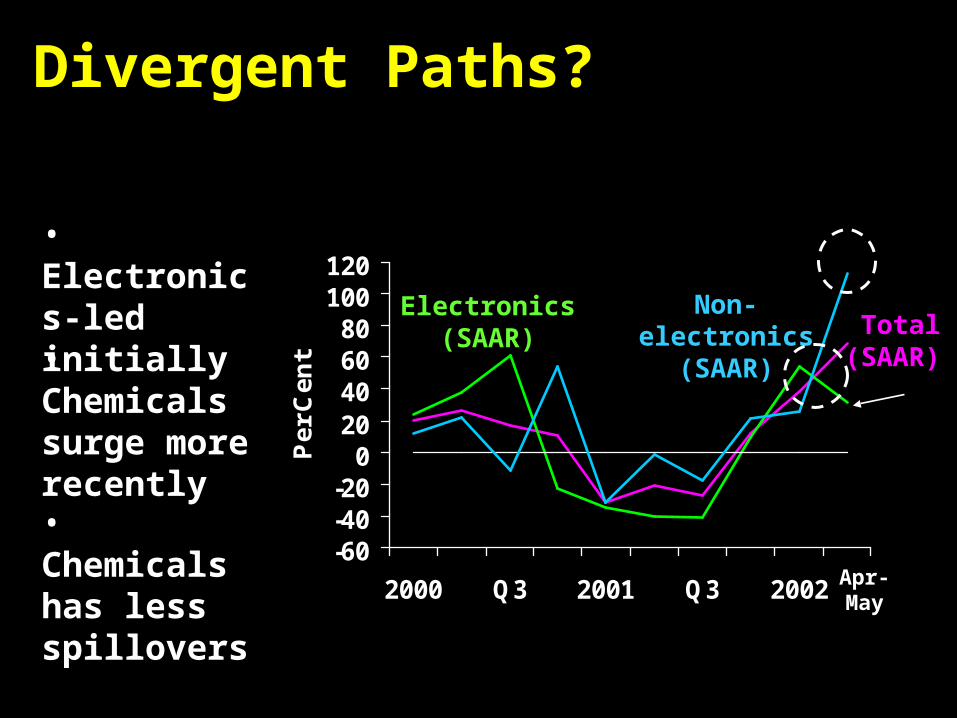

Divergent Paths?

-60-40-20

020406080

100120

2000 Q3 2001 Q3 2002

Pe

r C

en

tTotal

(SAAR)

Electronics(SAAR)

Non-electronics(SAAR)

Apr-May

• Electronics-led initially

• Chemicals has less spillovers

• Chemicals surge more recently

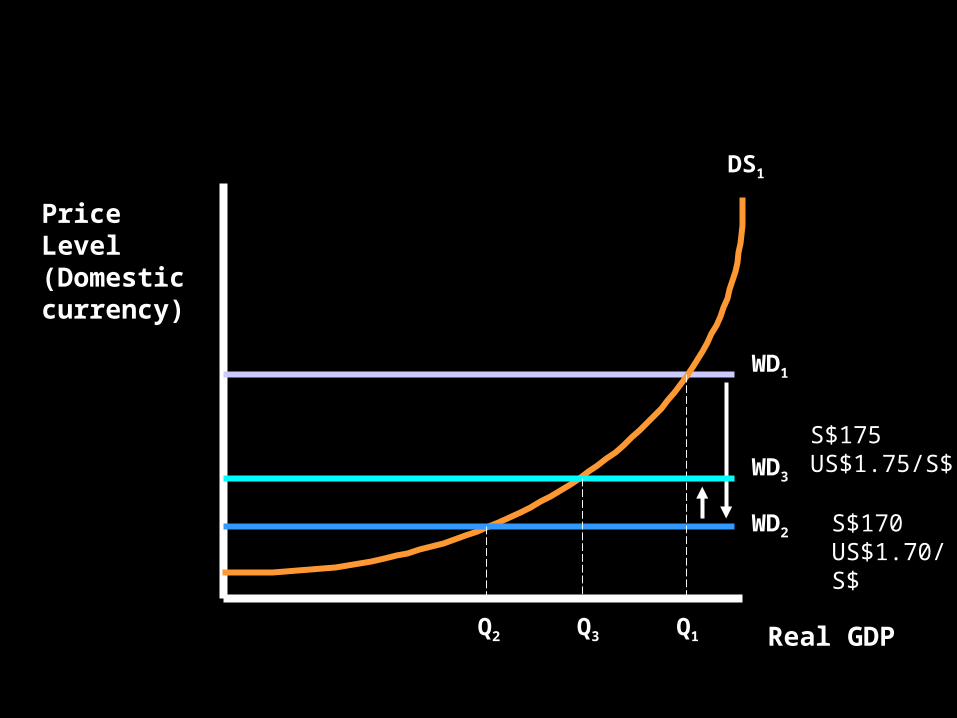

Support Provided by Policy

World Demand-Domestic Supply Curve

Price Level (Domestic currency)

Real GDP

DS1

WD1

WD2

Q1Q2

WD3

Q3

S$175US$1.75/S$

S$170US$1.70/S$

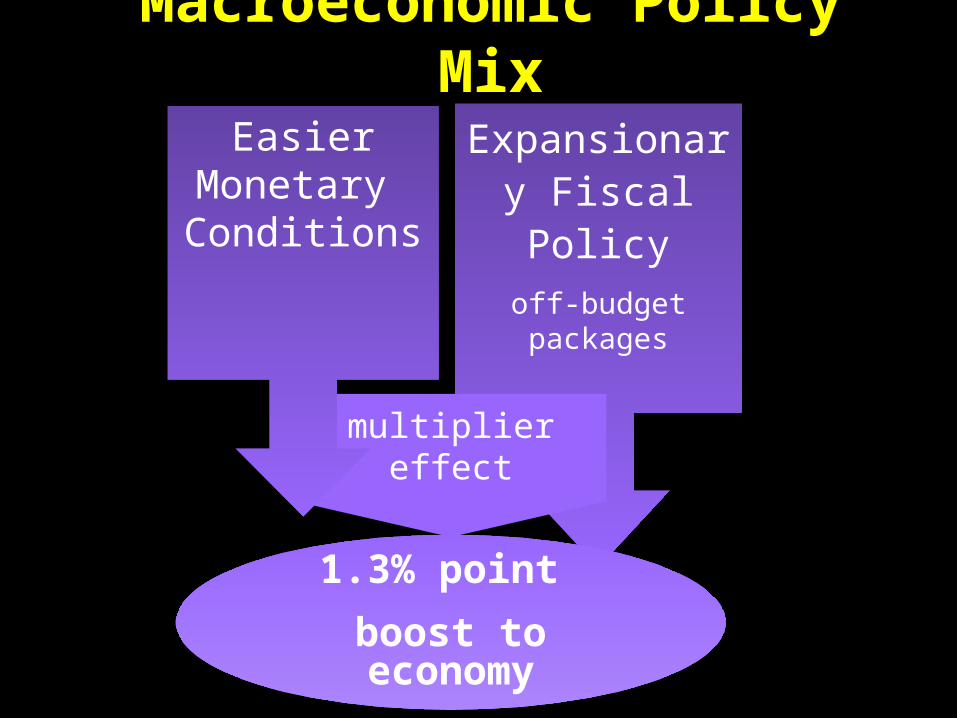

Macroeconomic Policy Mix

Expansionary Fiscal Policy

off-budget packages

multiplier effect

1.3% point

boost to economy

Easier Monetary Conditions

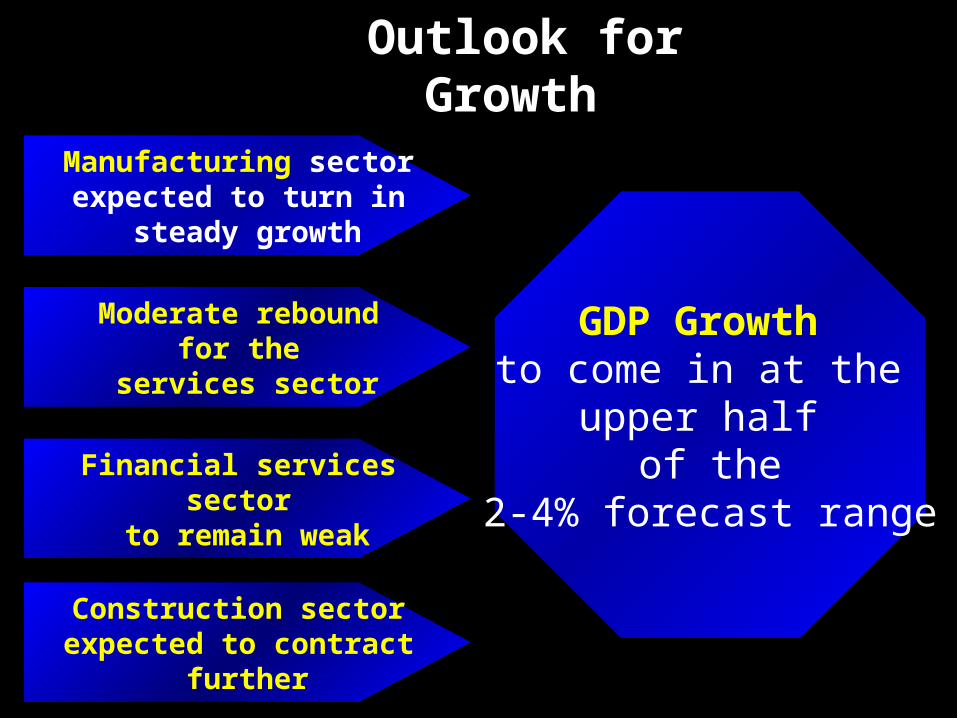

Outlook for Growth

Manufacturing sector expected to turn in

steady growth

Financial services sector

to remain weak

Moderate rebound for the

services sector

Construction sector expected to contract

further

GDP Growth to come in at the

upper half of the

2-4% forecast range

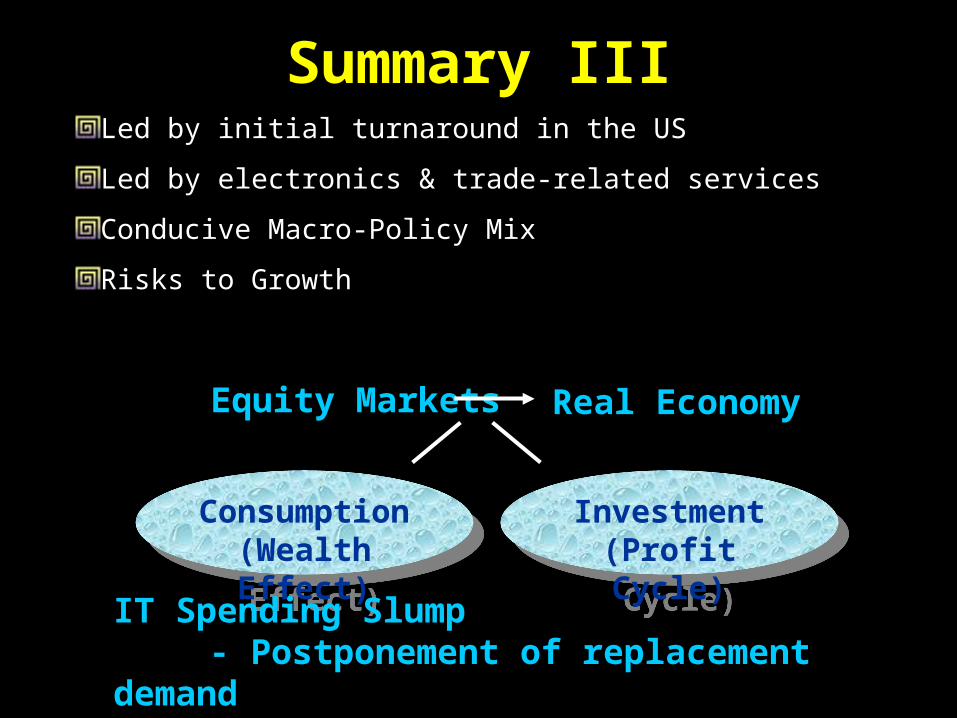

Consumption(Wealth Effect)

Consumption(Wealth Effect)

Equity Markets Real Economy

Investment(Profit Cycle)

Investment(Profit Cycle)

IT Spending Slump- Postponement of replacement demand

Summary IIILed by initial turnaround in the US

Led by electronics & trade-related services

Conducive Macro-Policy Mix

Risks to Growth

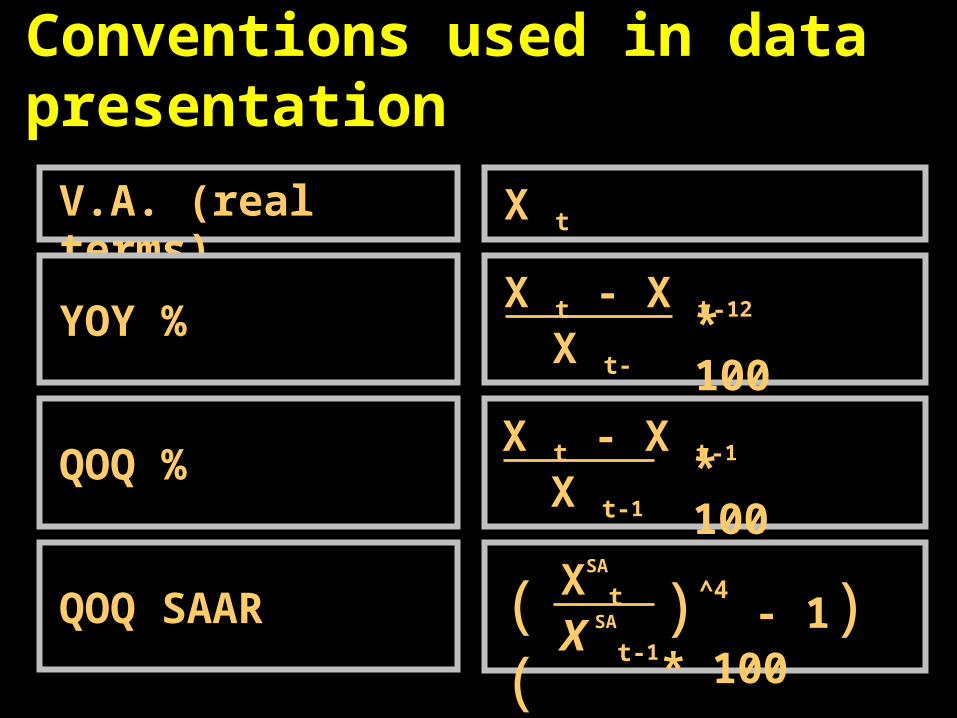

Conventions used in data presentation

V.A. (real terms) X t

YOY %X t - X t-12

X t-12

* 100

QOQ %X t - X t-1

X t-1* 100

QOQ SAARXSA

t

X SA

t-1)^4

- 1) * 100((

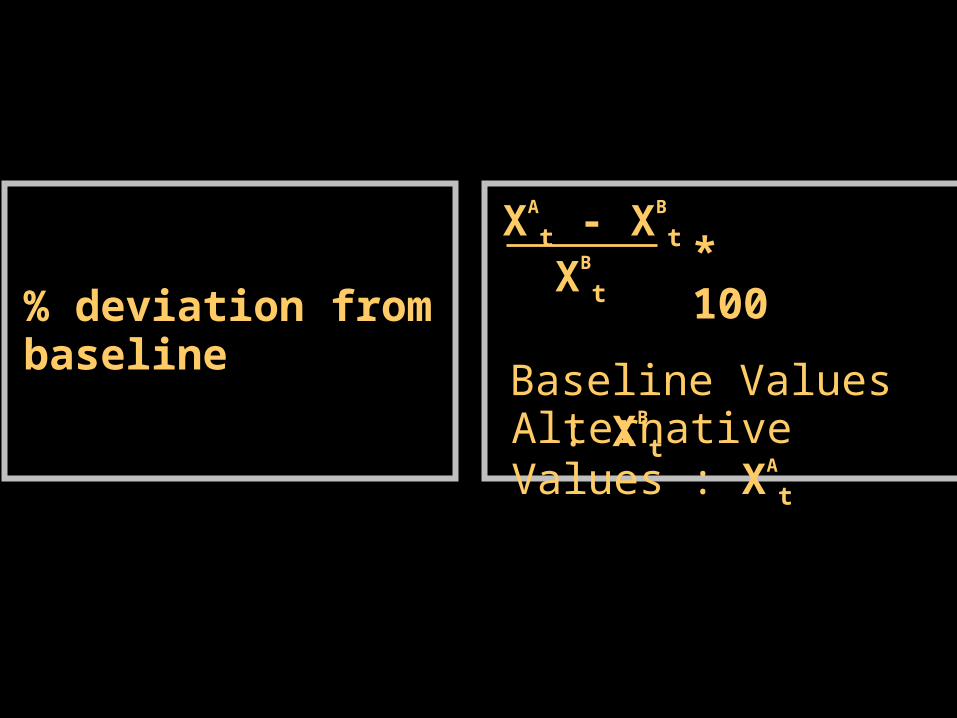

% deviation from baseline

XA

t - XB

t

XB

t

* 100

Baseline Values : XB

t

Alternative Values : XA

t

Top Related