Your Branches - Newcastle Building Society · 221/223 High Street, NE8 1AS. Tel: (0191) 477 2547...

14

Principal Office: Portland House, New Bridge Street, Newcastle upon Tyne, NE1 8AL. Telephone: ( 0191 ) 244 2000. www.newcastle.co.uk England Newcastle upon Tyne 3 Hood Street, NE1 6LZ. Tel: (0191) 232 0505 136 Northumberland Street, NE1 7DQ. Tel: (0191) 261 4940 22 Denton Park Centre, NE5 2RA. Tel: (0191) 267 5038 240 Chillingham Road, NE6 5LP. Tel: (0191) 276 0330 105/107 High Street, Gosforth, NE3 1HA. Tel: (0191) 285 5965 North East ALNWICK 28 Bondgate Within, NE66 1TD. Tel: (01665) 603 344 ASHINGTON 10 Station Road, NE63 9UJ. Tel: (01670) 815 919 BERWICK UPON TWEED 12 Hide Hill, TD15 1AB Tel: (01289) 306 417 CHESTER-LE-STREET 45 Front Street, DH3 3BH. Tel: (0191) 388 5266 CONSETT 19/21 Middle Street, DH8 5QP. Tel: (01207) 502 636 CRAMLINGTON 34/35 Craster Court, NE23 6UT. Tel: (01670) 735 813 DARLINGTON 87/88 Skinnergate, DL3 7LX. Tel: (01325) 383 656 DURHAM 25 Elvet Bridge, DH1 3AA. Tel: (0191) 384 3182 GATESHEAD 221/223 High Street, NE8 1AS. Tel: (0191) 477 2547 HARTLEPOOL 133/135 York Road, TS26 9DR. Tel: (01429) 233 014 HEXHAM 3 Beaumont Street, NE46 3LZ. Tel: (01434) 605 106 LOW FELL 574 Durham Road, NE9 6HX. Tel: (0191) 487 2893 MIDDLESBROUGH 38 Linthorpe Road, TS1 1RD. Tel: (01642) 243 617 MORPETH 14 Market Place, NE61 1HG. Tel: (01670) 514 702 NORTH SHIELDS 76 Bedford Street, NE29 0LD. Tel: (0191) 259 5286 PONTELAND 23 Broadway, Darras Hall, NE20 9PW. Tel: (01661) 821 828 SOUTH SHIELDS 67 Fowler Street, NE33 1NS. Tel: (0191) 454 0407 STOKESLEY 19 High Street, TS9 5AD. Tel: (01642) 711 742 SUNDERLAND 14 Waterloo Place, SR1 3HT. Tel: (0191) 565 0464 WALLSEND 12/14 High Street East, NE28 8PQ. Tel: (0191) 262 3496 WHICKHAM 28 Front Street, NE16 4DT. Tel: (0191) 488 1766 WHITLEY BAY 78/84 Park View, NE26 2TH. Tel: (0191) 252 0642 North West CARLISLE 2/4 English Street, CA3 8HX. Tel: (01228) 524 518 PENRITH 12 Market Square, CA11 7BX. Tel: (01768) 862 888 Scotland DUMFRIES 2/6 Queensberry Square, DG1 1BL. Tel: (01387) 253 815 Overseas Gibraltar 197-201 Main Street. Tel: (00 350) 200 41143 Newcastle Building Society Annual Review and Summary Financial Statement 2010 Your Branches

Transcript of Your Branches - Newcastle Building Society · 221/223 High Street, NE8 1AS. Tel: (0191) 477 2547...

Principal Office: Portland House, New Bridge Street, Newcastle upon Tyne, NE1 8AL.Telephone: (0191) 244 2000. www.newcastle.co.uk

EnglandNewcastle upon Tyne3 Hood Street, NE1 6LZ. Tel: (0191) 232 0505

136 Northumberland Street, NE1 7DQ. Tel: (0191) 261 4940

22 Denton Park Centre, NE5 2RA. Tel: (0191) 267 5038

240 Chillingham Road, NE6 5LP. Tel: (0191) 276 0330

105/107 High Street,Gosforth,NE3 1HA. Tel: (0191) 285 5965

North EastALNWICK

28 Bondgate Within, NE66 1TD. Tel: (01665) 603 344

ASHINGTON

10 Station Road, NE63 9UJ. Tel: (01670) 815 919

BERWICK UPON TWEED

12 Hide Hill, TD15 1AB Tel: (01289) 306 417

CHESTER-LE-STREET

45 Front Street, DH3 3BH. Tel: (0191) 388 5266

CONSETT

19/21 Middle Street, DH8 5QP. Tel: (01207) 502 636

CRAMLINGTON

34/35 Craster Court, NE23 6UT. Tel: (01670) 735 813

DARLINGTON

87/88 Skinnergate, DL3 7LX. Tel: (01325) 383 656

DURHAM

25 Elvet Bridge, DH1 3AA. Tel: (0191) 384 3182

GATESHEAD

221/223 High Street, NE8 1AS. Tel: (0191) 477 2547

HARTLEPOOL

133/135 York Road, TS26 9DR. Tel: (01429) 233 014

HEXHAM

3 Beaumont Street, NE46 3LZ. Tel: (01434) 605 106

LOW FELL

574 Durham Road, NE9 6HX. Tel: (0191) 487 2893

MIDDLESBROUGH

38 Linthorpe Road, TS1 1RD. Tel: (01642) 243 617

MORPETH

14 Market Place, NE61 1HG. Tel: (01670) 514 702

NORTH SHIELDS

76 Bedford Street, NE29 0LD. Tel: (0191) 259 5286

PONTELAND

23 Broadway, Darras Hall, NE20 9PW. Tel: (01661) 821 828

SOUTH SHIELDS

67 Fowler Street, NE33 1NS. Tel: (0191) 454 0407

STOKESLEY

19 High Street, TS9 5AD. Tel: (01642) 711 742

SUNDERLAND

14 Waterloo Place, SR1 3HT. Tel: (0191) 565 0464

WALLSEND

12/14 High Street East, NE28 8PQ. Tel: (0191) 262 3496

WHICKHAM

28 Front Street, NE16 4DT. Tel: (0191) 488 1766

WHITLEY BAY

78/84 Park View, NE26 2TH. Tel: (0191) 252 0642

North WestCARLISLE

2/4 English Street, CA3 8HX. Tel: (01228) 524 518

PENRITH

12 Market Square, CA11 7BX. Tel: (01768) 862 888

ScotlandDUMFRIES

2/6 Queensberry Square, DG1 1BL. Tel: (01387) 253 815

OverseasGibraltar197-201 Main Street. Tel: (00 350) 200 41143

Newcastle Building SocietyAnnual Review andSummary FinancialStatement 2010

Your Branches

excellent and an engagement plan issubsequently in the process of being built,which will be implemented during 2011 andbeyond.

Our new flagship branch on NorthumberlandStreet opened in March, which has been verywell received by our members in Newcastle.We introduced some very popular productsthis year, such as several 90% LTV mortgageproducts, which were aimed at supporting ourfirst time buyers on to the property ladder.

As well as this, our Reward ISA continued tobe a Best Buy product throughout 2010. In2011, we hope to introduce more good valueproducts, while simplifying the product rangewe have, to ensure we continue to offerproducts that meet your - and your family’s -needs in an effective way.

Our Solutions division continues to be a keypart of future strategy offering non-interestincome via diversification, which is built on corebuilding society sector skills. I’m delighted toreport we have launched new contracts with avalue ahead of our plans for 2010. Not only willthis create additional value for the Society andultimately our members, but it has also meant80 new jobs were created. We enter 2011 witha healthy pipeline of new contracts at variousstages of negotiation and I am optimistic thispart of our business will grow and add morevalue over the coming years.

In April 2010 we announced the Society hadreached an innovative agreement with holdersof certain classes of the Society’s existingsubordinated debt and permanent interestbearing shareholders, which would lead to amaterial strengthening of the Society’s capitalposition.

Underlying profitably has significantly improvedand we have found £8m of cost savings,representing 23% of our cost base, withoutnegatively impacting our long-term strategy.

We will continue our drive to become one ofthe most efficient players within the sector andprovide “best value” for our members andcustomers.

Going forward 2010 has been a challengingyear but also one during which the Societyhas made real progress. Our long-term aimcontinues to be focussed on traditionalbuilding society objectives supported bydiversification through our Solutions operation,which combined allow us to provide meaningfulreward to our members. With your continuedsupport, and the support of our staff, we areconfident we will be successful in achievingour aims in 2011.

Yours sincerely

Jim WillensChief Executive

Dear member

2 3

Throughoutthe year we’ve enjoyed

excellent support,from our members

“

”

It is nearly a year since I took over as ChiefExecutive of the Society and I’m extremelypleased with both progress made to date andresults delivered. This has been a year wherethe economy generally continued to present ademanding backdrop, not only for the financialservices sector but many organisations andindividuals too.

While there are signs of a more positive outlookbeginning to emerge I’m very much of the viewthat recovery will be steady, comparatively slowand not without further challenge compared tothat experienced in the past, post recession. Our efforts have therefore been focussed onmaking sure the Society is well placed for thefuture for you, our members.

Everything we have done during the past 12months has been aimed at ensuring long-termdelivery for our members, our third partycustomers, our employees and support for thecommunities in which we operate and indeedour Solutions business customers. Ourstrategy going forward continues to be centredsolely on these key stakeholders.

We entered 2010 knowing the year wouldpresent significant challenge. Our programmeof “Repositioning” the business was therefore developed to guide the Society through ademanding agenda. Excellent progress has

been made as a result of this in 2010, whichnow provides a robust base for the organisationas we move into 2011 and beyond.

Throughout the year we have enjoyed excellentsupport from our membership. In excess of25,000 new members joined the Society during2010 and the average number of products heldby you also increased.

Feedback is critical to any organisation and wehave engaged with our membership regularlythroughout the year looking for ways to furtherimprove both the services offered andproducts delivered. Member engagement isof key importance to us and will be furtherdeveloped over the coming months and years.

We ended 2010 by undertaking an employeeattitude survey, which was built and overseenby employees themselves. Participation was

Welcome

Chief Executive’s Statement

4 5

Financial planning seminarsKen Hines is the Newcastle’s Seminar Manager and has worked at the Society formore than seven years. His role is to engage with local communities and our membersto provide Information Presentations about key aspects of financial services. The freeinformal sessions focus on providing information about savings and investments,inheritance tax planning, protection insurance and estate planning, amongst otherthings. They have the ultimate aim of helping people make the most out of theirmoney but in a non-sales environment that is comfortable, relaxed and usually a littlebit out of the norm!

As Ken said: “I’m sure we’ve all been to presentations where someone stands up, tellsyou everything they think you should know, try to sell and then bid their goodbyes. We’renothing like that. We try to cover important topics during the sessions and make it asfriendly as possible, all while having a cuppa. We do not try any hard sells; we aim toinform, not sell. If people do want to know more we have a Branch Manager andfinancial expert on hand to discuss things on a more personal basis. We also supply abuffet afterwards – most people really enjoy that bit!

“We also try to avoid venues that people would usually associate with the financial sector.For instance, we may have the presentations in an art gallery or a local library, all tomake it as accessible and interesting to people as possible.”

If you’re interested in your local community group hosting one of Ken’sfree seminars then please send Ken an email: [email protected].

Supportingfirst time buyers

The Society demonstrated itscommitment to support aspiring firsttime buyers in 2010 as it launchedseveral new 90% LTV fixed rateproducts especially for newcomers tothe market.

It developed and issued those products specifically tosupport borrowers at a time when people still believe itis difficult to obtain a mortgage.

Steve Urwin, Sales and Marketing Executive said:“Buying a home is one of the most important purchasesyou will ever make and as a first time buyer this can bean intimidating prospect. There are many factors toconsider during this period, with the biggest possiblybeing the level of deposit required. This is why we try to

make getting a mortgage as accessible as possible bymaking them available with only a 10% deposit.

“This hopefully gives first time buyers more spare cashto spend on their new home instead of stretchingbeyond their means trying to do it all. In fact, we lent tofive times more people in 2010 than in 2009 and moreto first time buyers and we’re keen to continue thissupport”.

For information on the latest 90% deals pleasevisit www.newcastle.co.uk/mortgages or call0845 6004 310.

For the last decade many first timebuyers have been locked out of thehousing market, hit by inflated houseprices and a lack of available products.

With the start of 2010, and an extension to the StampDuty Holiday, came a series of new mortgageproducts aimed directly at the first time buyer market.Someone who took advantage of the Society’s firsttime buyer mortgage range was 29 year old, JonathanButterfield, who bought a new home in York:

“I had seen three other mortgage providers when Iwas looking for my home and the Newcastle was oneof those I approached having seen an advert in thenewspaper,” said Jonathan.

He added: “The whole experience with them was verysmooth. I would definitely consider taking out anothermortgage with them if I needed to in the future.”

To download a FREE copy of our mortgage guide‘First Steps’ please visit:www.newcastle.co.uk/mortgages

The Newcastlecan fix-it

for you!The Society urged the country’s homebuyer and remortgage population toconsider locking into low fixed-ratemortgage deals while they were stillavailable.

As the availability of competitive mortgage deals hasincreased steadily since the start of 2010 and into2011, coupled with more affordable housing, it isthought to be encouraging more buyers into thehousing marketplace. This was one of the reasonswhy the Society launched a series of fixed rate dealsbetween one and five years.

“There has been a lot of debate amongstindustry experts as to whether interest ratesare set to rise or not,” said StuartFearn, Head of ProductDevelopment.

“As the housingmarket is hopefullyset to stabilise weanticipate fixedrates, and potentiallylong-term ones, willincrease in popularity,so it’s best to try andbag the best deals while you can.”

Getting ontothe property

ladder

Products & Services

Don’t miss out!Why not join our Priority Register – just for existing customers of the Society. The Register is an email servicethat keeps you up-to-date with our new products and services, so you don’t miss out. It’s easy to join, simplyvisit your local branch or telephone our Newcastle-based Customer Contact Centre on 08457 344 345, provideyour email address and that’s it! We always try to keep the marketing messages to a minimum anyway – onlysending you information on products that we really think could be of interest to you.

We have to remind all our members from time to time that they can choose not to receive marketing mailings,emails or phone calls from the Society. To find out whether you are opted in or out, or to change your preferences,just ask next time you’re in your branch or call our Newcastle-based Customer Contact Centre and our staff willbe happy to help. Remember though, if you choose not to receive marketing messages from the Society, youmay miss out when we launch new products and services.

Savings CAN bemade when we’re

strapped for cash

Geoff Caisley,Newcastle Financial Services Limited Financial Adviser

6 7

With thecountry stillfacing somefinancialuncertaintymany familiesare lookingat tighteningtheir pursestrings.

There are manyways in whichsavings can bemade and ourhomes runsmarter, withoutwholesalechanges.

Products & Services

Make sure you’re

insured!A safety drive targeting the people ofthe North East was launched last yearby the Society.

Branch staff were on hand during the ‘InsuranceAwareness Fortnight’ to share scary statistics aboutpotential dangers facing homes in the UK, all in a bidto get more people to think about the need to makesure their home and contents are properly insured.

Staff were also available to provide advice on ways ofprotecting homes with the right insurance as part of thetwo-week initiative, which ran during Halloween. Thecompany organised the campaign, in partnership withLegal & General, to coincide with the end of BritishSummer Time and the changing of the clocks on thelast Sunday in October.

Ivy Campbell, Branch Manager at the AshingtonBranch said: “People start to think about the safety oftheir homes more as the dark nights draw closer, whichis why we decided to launch our home safety fortnight.

“It’s often the case that after an unwelcome incidentpeople realise their insurance isn’t adequate. It’salways worth checking you are fully covered beforeanything does happen as there are so many insurancecover options available these days.”

Scary Facts...More than one in four (27%) households leavekeys ‘hidden’ outside their house, under doormats,in sheds or under garden gnomes, for example,in case they ever find themselves locked out -Legal & General 2010.

More than 40 customers took up theoffer of a trip, thanks to the Society’spartnership with DFDS.

Customers, who attended an appointment with one ofthe Society’s financial specialists, were given vouchersfor a two-night mini-cruise for two to Amsterdam. Mr andMrs Hankinson, from Berwick, were two of ourcustomers to take advantage of the offer.

“As we walked past the Berwick branch we noticed thecruise offer on a window poster,” said Mr Hankinson.

“We then set up an appointment with one of theirfinancial advisers as we were looking to place somesavings into an account, following which we transferredour cash into a Five Year Bond.

“We also thoroughly enjoyed the trip; it was lots of funand to receive a free trip away is something out of theordinary,” he added.

A chance tohave your say!At the Society, we’re always keen to hearwhat our members think of us and theservice we provide – it is ‘your’ Societyafter all. As part of this, we’re shortly goingto be starting some customer satisfactionresearch amongst people who haverecently transacted with the Society. We’reusing a very reputable North East marketresearch company to carry out the workfor us and they may be calling you in thenext few months.

If you do get a call from the agency, who are calledExplain Research, then we would be really gratefulif you would be as honest as possible about theNewcastle – this way we can find out where ourservice is not coming up to your expectations. Ofcourse, you will not be expected to hand over anyconfidential or personal information to the researchcompany as they are simply asking about customerservice. So this is your chance to get involved!

Sail Away

1. Monitor your mortgage: If you are due to renew your mortgage

you should always shop around for the best deals. Deciding to opt for

a fixed rate or a variable rate deal is a key decision, if in doubt, seek

advice from a qualified adviser.

2. Minimise impact of taxes on your savings: Individual Savings

Accounts or ISAs allow you to save cash or shares without paying

tax on the interest. From 6 April 2011 subscription limits will be

increased each year by the Retail Prices Index (RPI) and limits for

2011 will be upto £5,340 for a cash and £10,680 for a stocks and

shares ISA and the overall combined ISA allowance will stand at

£10,680. The Newcastle’s Reward ISA is still topping the charts so

may be a good option.

3. Household insurance: Have you ever thought about noting the

renewal dates of your cover? If not, then it is recommended you do.

This helps to remind you to review other deals within the marketplace

in time for your policy to be renewed.

4. Mobile bills: By increasing the cost of your monthly tariff to allow

for a larger minute and text allocation you may actually reduce your

monthly bills.

5. Food for thought: Most families probably have left over food in

their fridge at the end of every week so it is wise to always make a

shopping list for specific meals so you aren’t persuaded to buy

unnecessary extras.

6. Downsize your car: It may seem like a big move to downsize

your prize possession but this could save you money in monthly

repayments and in fuel bills and Road Tax.

7. Memberships you don’t remember: It is worth reviewing your

monthly statements to really understand what it is you are paying for

but not benefiting from, such as that gym membership you don’t use.

Some handy tips for keeping costs down...

8 9

Staff graft togetherfor walk

success!More than 200 Society staff and theirfamily and friends put their best footforward to raise more than £1,500 forour charity of the year, as part of a familyfun day.

The Society’s 3rd annual Sponsored Walk andFamily Fun day held at Cobalt Business Park inNorth Tyneside, raised money for The Grafters Club,our Charity of the Year. Staff from the Society weretreated to various activities as part of the day,including face painters, a butterfly hunt, exoticanimals exhibition, arts & crafts stalls and ponytrekking.

Gillian Tiplady, Head of CSR said: “It was fantastic tosee so many staff members taking part. We are luckyenough to have the beautiful country park near to ourCobalt office so we like to take advantage of this andhold our annual walk here. In doing so it helps toraise money and make a valuable contribution to ourcharity of the year, The Grafters Club.

“This charity does an amazing job looking afterchildren and their families in the North East andCumbria who have experienced a burn injury”.

Alison McKenzie, Burns Outreach Nurse at TheGrafters Club, adds: “The money raised will helpmany children affected by a burn injury to attend ournumerous trips and activities.

“We thank everyone at the Newcastle BuildingSociety for their fantastic support. We had a greattime on the day, were made to feel enormouslywelcome by everyone and really enjoy working withthe staff there.”

Newcastle Building Society

take the biscuit andraises hundreds for

MacmillanSociety staff donned their apronsand helped to raise more than £700 for peopleaffected by cancer.

The Society, which has supported the Macmillan Coffee Morning since 2005, saw staff from across its departmentsand branch networks bake dozens of treats, which colleagues donated money for in return. Coffee, cake and eventea lovers raised their cups in support of the charity event, which has been going for 20 years.

Kelly Knighting-Wykes, Fundraising Manager, for Macmillan in Tyneside, Wearside & Northumberland, said: “TheWorlds Biggest Coffee Morning is Macmillan’s flagship event raising close to £8m every year. We really appreciateNewcastle Building Society’s continued support. It makes a huge difference to people affected by cancer.”

Products & Services Community

More peoplesaving in ISAs thanever before

ISAs continue to attractsavers keen to make the

most of their moneyaccording to figuresfrom the Society.

It saw, during 2010, a 10%increase in the number of

people choosing to save inits ISA products for the year to

date, compared with 2009 and a41% increase on 2008 numbers.

Ian Welsh, Product Development Manager, said:“While it has been a relatively uncertain time, it isencouraging that more and more people are choosingto save their money in ISAs which make their moneywork harder for them.

“Cash ISAs are particularly popular, including ourReward ISA which offers a market leading variable rateof 2.75% Gross*/AER**.”

For any information on the investment optionsthe Society has please call our Customer ContactCentre staff on 0845 600 4368 (8am - 6pm Mondayto Friday) or pop into one of our branches.

A special ISA forLoyal Members!From 6 April the Society will introduce aspecial loyalty product called Member ISA.It is available exclusively for UK memberswho have been with the Society for sixmonths or more on 6 April 2011.The five year ISA pays a highly competitive rate of 4.5%(Gross*/AER**) and is available with a minimuminvestment of £500 up to a maximum of £5,340 (2011/12allowance only). It can be opened in our branches or byphone via Newcastle Direct but it will only be available fora limited period.

Ian Welsh, Product Development Manager, said: “It’simportant we recognise the support our membersprovide us and a great way to do this is by an exclusiveproduct, such as our Member ISA.”

Product details are below:Account Name: Newcastle Member ISA (Issue 2)

Interest Rates: Paid on maturity (fixed) 4.5%Gross*/AER**

Tax: Interest will be paid Gross*

Bonus: No bonus is applicable

Withdrawal Arrangements: Withdrawals or transfers arepermitted subject to 120 days’loss of interest

Access: By branch, telephone, post oronline

Maturity: 10 May 2016

Interest Payment: 10 May each year or nextworking day

Minimum Balance: £500

Maximum Balance: £5,340 allowance for 2011/2012tax year. Transfers from other ISAproviders are not permitted.

*’Gross’ interest is the contractual rate of interest payable before the deduction of income tax.**‘AER’ stands for the Annual Equivalent Rate, a notional rate which illustrates what theinterest rate would be if paid and compounded on an annual basis.

Your New CastleIn a 2010 Society survey* more thantwo thirds of people admitted their homeimprovements were not made to addvalue, but to make a nicer homeenvironment. This shows that people’shomes really are their castles. TheNewcastle offers ‘further advances’,which can help pay for those all importanthome improvements, which can be acheaper alternative to a loan.

*The Newcastle’s Home ImprovementSurvey, May 2010.

Important notice regarding ourSavings General Terms & ConditionsA number of amendments have been made to theSavings Terms and Conditions leaflet, which should beread in conjunction with any special conditions for youraccount. Changes include new ISA transfer details andadditional information regarding transacting on youraccount. A copy of this leaflet can be found online atwww.newcastle.co.uk/savings. Alternatively,please visit your local branch.

10 11

Long-serving Earleplanning Aussie visit after

retirementThe second longest-serving Societyemployee, who started working for theorganisation in the same year as Englandwon the World Cup, hung up his calculatorin 2010 and started a well-earnedretirement.

Earle Hodgson started as the office junior in the headoffice of the Grainger & Percy Building Society onHood Street in Newcastle when he left WalkergateSchool in 1966, earning the princely sum of £30 permonth.

Now more than four decades on, Earle is planning atrip to Australia to visit family as the first highlight of hisretirement years. We wish Earle, and all our otherretirees, all the best in their retirement.

Community Staff

A Real surprisetreat for charityStaff at the Society’s Head Office weretreated to a nice surprise when RealRadio’s football pundits visited staff on acharity trip.

Ex-Toon Skipper, Bob Moncur, and his commentarypartner Justin Lockwood visited staff at the Society’sHead Office in Newcastle City Centre. During the visit,in October, the stars interviewed some of the Society’sfootball fans about the Newcastle and Sunderlandderby, talked predictions and what celebratory plansthey had arranged if their chosen football team won.

At the same time generous staff donated to NewcastleUnited Football Club’s (NUFC) charity - NewcastleUnited Foundation. Bob also shook hands with manyof his fans at the Society who were surprised at thespecial visit during their normal working day.

Money donated will be used to help many projectsthroughout the region as part of the football club’ssuccessful Foundation.

“It was great Newcastle Building Society supportedthis charity drive in the build up to the derby game,”says Kate Bradley, Charitable Foundation Manager,Newcastle United Foundation.

“We know that we have fanatical football fans up herein the North East, so it’s fantastic their staff not onlyfound time to talk about the game to Real Radio butalso be so generous and donate money to our charity.”

Society lends ahelping paw to

Children in NeedThe Society’s generous staff pledged tosupport charity once again, this timewith a week-long schedule of activitiesdedicated to Children in Need.

The Society, which has supported the charity forseveral years, played host to a Pudsey treasure huntwhere the iconic bear was lost for a week and staffhad to follow a set of clues, as well as CCTV images,to find him. Each entrant that took part in the huntpaid a donation to the charity.

The hunt built up to a Society-wide Teddy Bear’sPicnic on Children in Need day where employeesbrought in a range of cake and savoury treats, andeven Pudsey shaped cookies, to enjoy and sell.

The organisation also hosted a dress down day forall staff, which enabled the fundraising pot to betopped up.

Gillian Tiplady, Head of CSR said:

We’re delighted that once weadd in the money raised this yearthe total raised over the years forthe charity is more than £6,000.”“

Festive Drawraises cash

for kids!Generous Board directors at the Societyput their hands in their pockets thisfestive season to fund a prize draw thatraised Christmas cash for a local charity.

The Society decided to get its ‘claus’ into a Christmascharity draw, prizes from which were bought followinga donation of more than £1,300 from its Boardmembers.

The draw enabled staff who purchased a raffle ticket toenter and have the chance to win top prizes.

This included an iPAD, theatre trip to London for two,as well as two corporate tickets to see Take That inconcert. The money raised was donated to theSociety’s charity of the year, The Grafter’s Club.

Contact UsWe have experienced staff inour branch network and in ourNewcastle-based Contact Centrewaiting to help you. Whether you needhelp through our financial planningservice or from a trained mortgageadviser, come in and see us or youcan call us on: 0845 609 9292.

i

Celebrating

talent...Newcastle Business School teamed upwith the Society to enable 30 of itsmanagers to complete a work-basedDiploma in Management Development.

The course proved hugely popular with the Society’smanagers involved, with some saying the coursebenefited them in their day-to-day role almost as soonas they commenced it.

Jim Willens, Chief Executive, said: “Nurturing andrewarding talent is something that is important to theSociety and is something we thoroughly endorse.

“We saw this in 2010 with the graduation of 30 of ourown staff who graduated from a Diploma inManagement Development.”

By RoadFrom the A1 North or South take the A184 sliproad. Follow signs for the A189 to cross theRedheugh Bridge, leading onto St. James’Boulevard. Travel all the way to the end of theBoulevard.

Turn left at the traffic lights onto Barrack Road(the Stadium is on the right) and over the nextset of traffic lights move into the right-handlane. Turn right at the next set of traffic lightsinto St. James’ Park.

By RailNewcastle Central Railway Station is only fiveminutes from St. James’ Park by car or taxi. TheTyne & Wear metro system provides a link directto St. James’ Park. For details of the rail serviceplease call National Rail on 08457 484 950.

For details of the Tyne & Wear Metro Systemcall Nexus on 0191 203 3333.

Local Travel InformationIf you would like to find out more about localtransport information you can also contactTraveline on 0871 200 2233.

Venue DetailsUpon arrival, guests travelling by road will beadvised by an attendant where to park. Theattendant will also direct guests to the relevantreception area.

There are a small number of free on-site carparking spaces for members attending ourAnnual General Meeting (some limited disabledcar park spaces are also available).

The free car parking spaces for our membersare on levels 1 and 2 of the multi-storey carpark. The car parking areas can be accessedfrom Barrack Road. Please follow sign for‘Conference and Banqueting Car Parking’.

In the event of levels 1 and 2 of the multi-storeycar park being full, guests may use the nearbylow-level two storey car park. The cost there is40p per hour from 8am - 10pm.

Wheelchair access is available.

ÇÇÇ

1312

Notice is given that the Annual General Meetingof Members of Newcastle Building Society willbe held on Wednesday 27 April 2011 in theBamburgh Suite, Newcastle United FootballClub, St James’ Park, Newcastle upon TyneNE1 4ST at 1.45pm prompt, for the followingpurposes:

Ordinary Resolutions1. To receive the Annual Report and Accounts.2. To re-appoint PricewaterhouseCoopers LLP

as auditors.3. To approve the Report on Directors’

Remuneration.

Election and Re-election of Directors

4. i) To elect David John Buffham

ii) To elect Ann Marie Cairns

iii) To re-elect Ronald Joseph McCormick

iv) To elect Angela May Russell

v) To elect Gillian Tiplady

vi) To elect John Henderson Warden

Agenda:• Registration 1:00pm• AGM 1:45pm prompt• Refreshments 3:20-4:00pm

By Order of the Board

I. Good - Group Secretary3 March 2011

Freepost

1. Complete, sign and detach the Voting Form.2. Post it in the pre-paid envelope provided.

No stamp is required.

Your form must be received by 12 noon Tuesday 26 April 2011.

Online

1. You can also vote online at:agmvote.newcastle.co.uk

2. You must vote online by 12 noon Tuesday26 April 2011. 10p will be donated to ourCharity of the Year, The Grafter’s Club, forevery online vote received.

Annual General Meeting

1. Bring your Voting Form, or other evidence of membership, to the Meeting.

2. To assist us with planning, could you pleaseconfirm your attendance either bycompleting and returning the AGMconfirmation slip on your proxy form orregister to attend on our online site.

How to get there

8

+

Our membersneed our

support evenmore

Notice of AGM How to vote

“

”

14 15

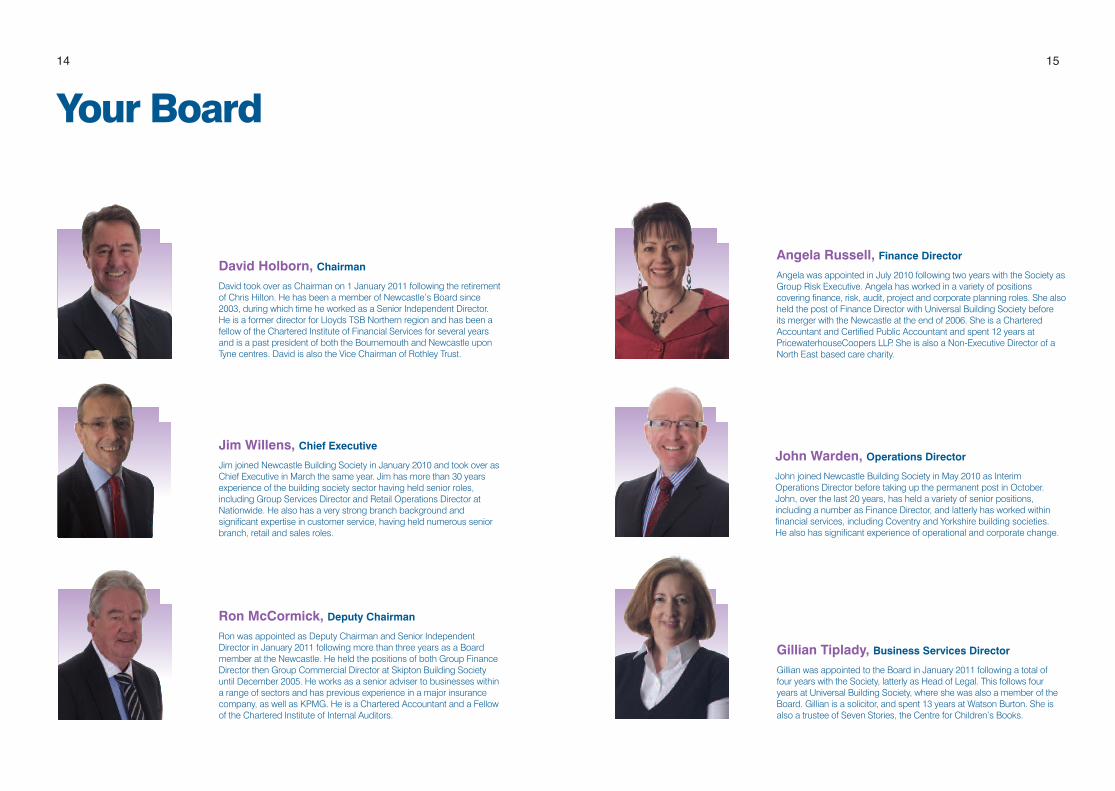

Your Board

Jim Willens, Chief Executive

Jim joined Newcastle Building Society in January 2010 and took over asChief Executive in March the same year. Jim has more than 30 yearsexperience of the building society sector having held senior roles,including Group Services Director and Retail Operations Director atNationwide. He also has a very strong branch background andsignificant expertise in customer service, having held numerous seniorbranch, retail and sales roles.

David Holborn, Chairman

David took over as Chairman on 1 January 2011 following the retirementof Chris Hilton. He has been a member of Newcastle’s Board since2003, during which time he worked as a Senior Independent Director.He is a former director for Lloyds TSB Northern region and has been afellow of the Chartered Institute of Financial Services for several yearsand is a past president of both the Bournemouth and Newcastle uponTyne centres. David is also the Vice Chairman of Rothley Trust.

Angela Russell, Finance Director

Angela was appointed in July 2010 following two years with the Society asGroup Risk Executive. Angela has worked in a variety of positionscovering finance, risk, audit, project and corporate planning roles. She alsoheld the post of Finance Director with Universal Building Society beforeits merger with the Newcastle at the end of 2006. She is a CharteredAccountant and Certified Public Accountant and spent 12 years atPricewaterhouseCoopers LLP. She is also a Non-Executive Director of aNorth East based care charity.

Ron McCormick, Deputy Chairman

Ron was appointed as Deputy Chairman and Senior IndependentDirector in January 2011 following more than three years as a Boardmember at the Newcastle. He held the positions of both Group FinanceDirector then Group Commercial Director at Skipton Building Societyuntil December 2005. He works as a senior adviser to businesses withina range of sectors and has previous experience in a major insurancecompany, as well as KPMG. He is a Chartered Accountant and a Fellowof the Chartered Institute of Internal Auditors.

Gillian Tiplady, Business Services Director

Gillian was appointed to the Board in January 2011 following a total offour years with the Society, latterly as Head of Legal. This follows fouryears at Universal Building Society, where she was also a member of theBoard. Gillian is a solicitor, and spent 13 years at Watson Burton. She isalso a trustee of Seven Stories, the Centre for Children’s Books.

John Warden, Operations Director

John joined Newcastle Building Society in May 2010 as InterimOperations Director before taking up the permanent post in October.John, over the last 20 years, has held a variety of senior positions,including a number as Finance Director, and latterly has worked withinfinancial services, including Coventry and Yorkshire building societies.He also has significant experience of operational and corporate change.

16 17

Ann Cairns, Non-Executive Director

Ann was appointed to Newcastle’s Board in September 2010. She hasmore than 20 years of experience in banking, having worked in seniormanagement positions across Europe and the United States where shehas led global retail and investment banking operations. She is aManaging Director with Alvarez & Marsal in London and Head of theFinancial Industry Advisory Group in Europe. She is also Trustee ofCharity Bank.

Richard Mayland, Non-Executive Director

Richard chairs the Society’s Audit Committee and began his career in1974 in accountancy. He retired as a partner in PricewaterhouseCoopers LLPin 2003, a post that he held for 17 years. He is currently Chief Executive ofNorprime Limited and is a trustee of the locally-based Children’s HeartUnit Fund.

Nigel Westwood, Non-Executive Director

Nigel joined Universal Building Society’s Board in 2000 and he hasbeen a member of the Newcastle’s Board since its merger with theUniversal in December 2006. He is a partner of a regional charteredsurveyors’ practice based in Newcastle and he performs the duties ofthe Consul for Norway.

Catherine Vine-Lott, Non-Executive Director

Catherine joined the Newcastle Board in January 2010. She has spenther entire working life in the financial services industry, which includessignificant experience with Legal and General both at group boardlevel and in running the wealth management division, as well as 18years at Barclays. She is also a Non-Executive Director of OpenworkHoldings Limited, Rathbone Brothers PLC and Cranfield University.

David Buffham, Non-Executive Director

David joined the Newcastle’s Board in May 2010. He chairs the GroupRisk Committee and is also a member of the Remuneration andNomination Committees. He has a wealth of experience gained from acareer spanning more than 30 years in a variety of roles at the Bank ofEngland. He is also a Governor for Northumbria University.

Your Board

Remuneration Committee Report

The Remuneration Committee consists solely of Non-Executive Directors.During the year, David Holborn and Ron McCormick stood down from theCommittee and were replaced by Catherine Vine-Lott and David Buffham.Maxine Pott left the Committee when she retired from the main Board on31 December 2010.

The Committee meets to consider and makerecommendations on the level of remuneration forExecutive and Non-Executive Directors of theBoard, as well as the contractual arrangements forthe Executive Directors and other Executives. Theyalso meet to review the performance of the ChiefExecutive and Executive Directors against theobjectives set by the Board.

Remuneration PolicyBasic SalariesRemuneration packages are set at a level toattract, motivate and retain Executives of thecalibre necessary to oversee the operations of theSociety. Basic salaries are set by taking intoaccount salary levels within similar sized financialservices organisations and the market as a whole,so as to attract and retain the skills levels that areappropriate to operate an organisation as complexas the Society. A general salary increase was notawarded to any staff member, including Executivesand Executive Directors during the year.

Performance Related BonusesIn light of the very difficult trading conditions facingthe Society, the payment of bonuses to ExecutiveDirectors and Executives has been suspendedsince 2007. Sales related incentive and bonusschemes have been operated for some sales staff.

Bonus schemes (when operated) are set in such away as to ensure that they promote the financialstrength of the Society, do not reward failure and

that they do not encourage Executives to takebusiness risks outside of the Society’s risk appetite.In 2011, it is intended to give consideration tore-introducing an appropriate corporate bonusscheme.

PensionsAll staff (including Executive Directors andExecutives) are now only eligible for membershipof the Newcastle Building Society Group PersonalPension Scheme, which is a ‘defined contribution’scheme. Non-Executive Directors appointed since2001 have not been eligible for membership of anyof the Society’s pension schemes.

Three Executive Directors and one Non-ExecutiveDirector had been active members of theNewcastle Building Society Pension & Assurancescheme - a ‘defined benefit’ scheme. The fourDirectors either retired or resigned during thefinancial year and therefore their active membershipof the scheme ended when they left the Society.Following a formal consultation process with allother Executives and staff, there ceased to be anyactive members of the ‘defined benefit’ schemeduring the year. Access to the defined contributionscheme has been provided as an alternative.

Other BenefitsAll Executive Directors and Executives receive arange of taxable benefits which include a motorvehicle or cash equivalent, private health care andthe ability to participate in a concessionary

mortgage scheme. Life cover for a lump sum ondeath in service is also provided.

No Executive participated in the concessionarymortgage scheme during the year although somehad mortgages with the Society on the samecommercial terms as members of the Society.

Service ContractsIt is the Society’s policy to provide six monthsnotice of termination for all Executive Directors. Allof the current Executive Directors therefore havesuch notice periods.

Five of the longer serving Executives have serviceagreements which provide for 12 months notice oftermination from the Society. The remainingExecutives all have notice periods of six months.It is the policy to employ all newly appointedExecutives with notice periods of six months.

There are no contracts for Non-Executive Directorsand no compensatory terms for loss of office.

Policy on Remuneration of Non-ExecutiveDirectorsNon-Executive Directors’ fees are set at a levelappropriate to reflect the skills and time requiredto direct the Society’s operations and progress.Non-Executive Directors receive a base fee andadditional fees depending upon the BoardCommittees on which they sit or chair. Fees arenormally reviewed annually in light of those paid todirectors of other financial services organisations.Fees were not increased in 2010. Non-ExecutiveDirectors do not participate in any bonus scheme.

The performance of Non-Executive Directors isreviewed by the Chairman annually and theperformance of the Chairman is reviewed by theNon-Executive Directors, led by the SeniorIndependent Director.

Financial Services Authority (FSA)Remuneration CodeOn 17 December 2010 the FSA published the finalrules for the FSA Remuneration Code. The Societywill be governed by the new code with effect from1 January 2011 but, in view of the short timescalebetween the announcement and the effective date,the FSA has established a transitional period untilJuly 2011 for organisations such as the Society tocomply fully with the Code.

The Society considers that it already complieswith the spirit of the Code and offers moderatelevels of remuneration in comparison to severalother similar building societies and financialorganisations. We have reviewed the RemunerationCode requirements in significant detail and theSociety will comply fully with all aspects of theCode by July 2011.

Catherine Vine-LottChair – Remuneration Committee

3 March 2011

Remuneration Committee Report

18 19

Overview2010 has been a challenging year but the delivery of theRepositioning Programme has enabled the Society tomake good progress in improving the underlyingprofitability of the Group. Whilst overall reported profitabilityhas reduced from a profit before tax of £0.1m in 2009 to a£4.7m loss in 2010, the underlying profitability of thebusiness has improved with a more stable margin, lowercost base and improving income due to new Solutions’contracts secured in 2010. Excluding Repositioning coststhe first half showed a pre-tax loss of £0.9m and thiscompares to a profit before tax of £0.2m in the second half;this improving trend is expected to continue.

In May 2010, the Society completed an innovative andpro-active Capital Agreement with the majority of itsnon-retail bond holders. This provides the Society with£45m of contingent Core Tier 1 capital, which furtherstrengthens the Society’s capital position. The Groupcapital position improved during 2010 with the overallsolvency ratio increasing from 13.4% to 14.1% and Tier 1capital ratio improving from 10.2% to 10.7%.

The Repositioning Programme announced in May 2010has delivered its primary objectives and was closed off asa project on 31 December 2010. Whilst there was a £4mcost associated with delivering the programme, it hasdelivered underlying cost savings of £8m per annum aswell as other benefits, which will improve underlyingprofitability.

During 2010 good progress was made in reducingexposures to higher risk lending, including an 11%reduction in commercial loans, 20% reduction in loanssecured on traded endowment policies and 5% fall in Buyto Let (BTL) loans. The Society continues to focus on newloans for prime residential borrowers only, particularly firsttime buyers where the Society has had a range ofproducts available at 90% LTV to help customers get onthe housing ladder.

Group results for the yearNet interest incomeThe net interest margin fell from 0.42% in 2009 to 0.40% in2010 due to increased costs of retail funding, a lower returnon liquid assets due to increased holdings of low-riskliquidity buffer eligible assets, including balances in theBank of England reserve account, gilts and supranationalbonds, and the “flooring” of interest rates and savingsaccounts in the low interest rate environment. A full reviewof all aspects of the margin has been completed as partof the Repositioning Programme. The margin has beenstabilised with key targets set for longer-term improvement.

Other income and chargesThe net movement in the income and charges was a£0.6m reduction compared to 2009. Other income remainedbroadly unchanged compared to the prior year. Othercharges increased due to the inclusion of a valuation deficiton the Kings Manor portfolio of £0.5m following a full reviewof the fair value of the investment properties at 31 December2010. Income from the Solutions business reduced from£9.8m to £9.0m due to reduced volumes on one savingsmanagement contract. This reduction had been more thanoffset by the 4th quarter due to a number of new savingsmanagement contracts being delivered during 2010 withthe most significant contract not fully launched until 4thquarter 2010. The full-year impact of the new Solutions’contracts will be seen going forward from 2011 whencontracts implemented in 2010 are fully operational.

Administrative expenses and depreciation

Administration expenses fell by £4.6m in the year to £33.7m(2009: £38.3m) as a result of delivery of the RepositioningProgramme in the second half of the year. The underlyingyear-on-year fall in administration expense, excluding gainsin relation to curtailment of pension benefits was £5.6m.This equates to an annualised saving of £8m in 2011 andrepresents a 23% reduction of the cost base compared tothe start of 2010.

Impairment lossesLoans and advances to customersThe overall net impairment charge for loans and advancesto customers has fallen to £1.8m in 2010 from £8m in2009. The net charge of £0.8m on residential propertiesrelates predominantly to BTL loans within the specialistresidential mortgage book portfolio with only £0.1m ofwrite-offs for the year relating to home-owner residentialproperties. This reflects the quality of the Society’s primeresidential mortgage portfolio. Provisions againstcommercial loans increased overall, reflecting an increasein collective provisions against the backdrop of tougheconomic conditions, although this has not yet fed throughto the Society’s 3 month plus arrears figure. Provisions onother loans have reduced as the underlying loan book hasreduced with redemptions of more than 20% during 2010in relation to loans secured on traded endowment policies.

Remuneration Committee Report Summary Directors’ ReportSummary Financial Statement for theyear ended 31 December 2010

20 21

Continued

Executive Directors

C Greaves (resigned 31 July 2010) 77 - - 5 - 82 - 82 141

W Lee (resigned 31 July 2010) 82 - - 8 - 90 - 90 156

AM Russell (appointed 1 July 2010) 72 - 7 5 - 84 - 84 -

CJ Seccombe (retired 12 March 2010) 54 - - 3 - 57 - 57 286

JH Warden (appointed 7 October 2010) 35 - 3 3 - 41 - 41 -

J Westhoff (resigned 30 April 2009) - - - - - - - - 67

G Wilkinson (resigned 9 April 2010) 11 - 1 - - 12 9 21 85

JH Willens (appointed to the Board 248 - 22 14 - 284 78 362 -4 January 2010 and then toChief Executive on 13 March 2010)

579 - 33 38 - 650 87 737 735

Non-Executive Directors

CJ Hilton (retired 31 December 2010) 63 - - - 1 64 - 64 64

DJ Buffham (appointed 24 May 2010) 20 - - - - 20 - 20 -

AM Cairns (appointed 1 September 2010) 9 - - - - 9 - 9 -

FD Holborn 45 - - - - 45 - 45 46

RD Mayland 40 - - - - 40 - 40 40

RJ McCormick 40 - - 2 - 42 - 42 40

JM Pott (retired 31 December 2010) 33 - - - - 33 - 33 33

CRR Vine-Lott (appointed 1 January 2010) 33 - - 1 - 34 - 34 -

NA Westwood 33 - - - - 33 - 33 33

895 - 33 41 - 970 87 1,057 991

Notes:-1. Ms. W. Lee received compensation for loss of office amounting to £153,000.2. Mr. C.J. Seccombe received compensation for loss of office amounting to £271,260.3. Mr. J.H. Willens was set a relocation allowance of £90,000 inclusive of tax and National Insurance (NI). Mr Willens incurred £42, 519 of costs. An additional £35,222 for tax and NI was paid by the Society.4. Mr. J.H. Willens has elected to take his pension contribution amounting to £22,292 as a cash payment. He is liable for his own Tax and NI contributions on this payment.

Set out below are details of the pension benefits, including unfunded arrangements, payable on retirement, to which each of the Directors is entitledat 31 December 2010. The accrued benefits include any benefits earned as an employee prior to becoming a Director, as well as those earned forqualifying services after becoming a Director.

Salaryor fees

£000

Date ofleaving active

service

£000

Total accruedbenefits as at

31-Dec-10(£ per annum)

£000

Increases inaccrued pensionbenefits over the

year (£ per annum)

£000

Transfer valueof accruedbenefits at31-Dec-10

£000

Transfer valueof accruedbenefits at31-Dec-09

£000

Director’scontributionsduring year

£000

Increase intransfer valueless Director’scontribution

£000

Annualbonus

£000

Pensioncontributions

to definedcontribution

scheme

£000

Otherbenefits

£000

Increase inaccrued pension

benefits earnedin year (excl.

defined benefitscheme)

£000

Total 2010contractual

benefits

£000

‘One off’expenses - relocation

costs

£000

Total 2010including‘One off’expenses

£000

2009total

£000

Directors

C Greaves 31-Jul-10 48 1 1,184 980 7 197

CJ Hilton 31-Dec-10 35 1 744 668 - 76

W Lee 31-Jul-10 17 1 228 181 8 39

CJ Seccombe 05-Mar-10 54 1 1,305 1,200 7 98

Notes:-1. The transfer values have been calculated on the basis of actuarial advice in accordance with regulations 7 to 7e of the Occupational Pension Schemes (Transfer Values) Regulations 1996.2. Mr. C.J. Seccombe retired during the accounting period. The transfer value shown for Mr. C.J. Seccombe as at 31 December 2010 represents the sum of benefits paid during the accountingperiod (approximately £260,000) and the transfer value of his pension in payment as at 31 December 2010. The accrued pension figure shown as at 31 December 2010 is the accrued pension asat Mr. C.J. Seccombe’s date of retirement, before reduction for early payment and exchange of pension for cash at retirement.

Over the course of 2010, loans in arrears of more than 3months improved across all areas of the mortgageportfolio as shown in the table below.

A satisfactory trend is shown in the reduction in residential3 month plus arrears by balance, which has reduced from1.98% to 0.69% following the resolution of paymentdifficulties for several BTL portfolio investors. The level ofpossessions also continued at a low level with onecommercial property with a value of £0.2m, net ofprovisions. Possession properties for residentialhomeowners amounted to 11 cases, with almost half ofthese relating to borrowers that had handed back the keysor where action was being taken by a second chargelender. BTL possessions cases totalled 28 propertiesacross 14 borrowers. The Society continues to operateforbearance measures for homeowners and for theseborrowers possession is only ever a last resort. However,for commercial and BTL cases a rigorous approach isadopted reflecting the commercial nature of thetransactions and the desired reduction targeted in theseportfolios.

Retail savingsCompetition for retail funds continued in 2010 and thiscaused increased funding costs throughout the year; thisis expected to continue over the next 18-24 months. TheSociety continues to attract around a third of its savingsaccounts in the form of ISAs and has offered a range ofattractive products to new and maturing customersthroughout 2010. Savings balances reduced by 5% in2010, reflecting mainly the reduction in mortgage balancesreferred to above.

Wholesale fundingThe Society has maintained a wholesale funding ratiobelow 10% throughout 2010. The main sources of fundingare from local authorities, private companies andrepurchase agreements.

CapitalThroughout the year the Group has operated withinIndividual Capital Guidance set by the FSA and the higherinternal minimum set by the Board. The total solvency ratioimproved to 14.1% (2009:13.4%).

Post Balance Sheet EventsThe Society called the non-recourse finance held in thespecial purpose vehicle, Bamburgh Finance (No1) plc, on1 February 2011. The net funding requirement for the callwas £65m. The non-recourse finance, which consisted ofmortgage-backed floating rate notes secured by firstcharges over commercial property, was redeemed at par.

OutlookFollowing the successful completion of the RepositioningProgramme, the Group now has a more efficient costbase, stable margin, stronger Solutions business pipelineand good progress has been made toward businesssimplification. The Group continues to hold exposures tohigher risk asset classes particularly commercial lendingand a robust strategy will be pursued to wind down theseexposures in order to protect longer-term memberinterests. The Group will maintain its cautious approach tolending, both in terms of risk and volume. Retail savingswill remain as the primary source of funding, although largeadditional volumes will not be required as Balance Sheetgrowth is not planned, protecting capital and liquidity. Weexpect the market for retail savings to remain highlycompetitive and wholesale funding markets to remainsubdued in 2011. The groundwork has been set for animproved financial performance in 2011 and beyond.

Angela RussellFinance Director

3 March 2011

Loans and advances to banks and debt securitiesIn 2008 the Society made impairment provisions totalling£32.6m against exposures to Icelandic banks. Theadministrators of Heritable Bank and Kaupthing Singer &Friedlander provide estimates of the amounts that creditorswill recover from these banks. This information continues tobe revised, enabling the Society to form an increasinglyaccurate estimate of the losses likely to be incurred onthese exposures. A further provision write-back of £2.4mhas been made in 2010 based on improved assessmentsof recovery attributable to the UK-based Icelandic banks.Since the collapse of the Icelandic banking system inOctober 2008 the Society has already recovered £11.5magainst Icelandic Treasury Assets. The overall recovery rateis expected to be circa 50%, with recoveries in the UKappearing higher and more certain than that on directIcelandic exposures.

FSCS LevyThere is no charge for FSCS levy in 2010 as the provisionsmade at the end of 2009 are sufficient to cover liabilitiesincurred as a result of market participation as of 31December 2010.

Repositioning CostsThe Repositioning charge of £4m covers redundancycosts, legal, professional and consultancy fees in relationto business simplification and costs in relation to vacantproperties that the Society has agreed to dispose of. Of the£4m provision established at the half year, £1.7m remainedat 31 December 2010, this related mainly to property costs.

Provisions for liabilities and charges Included within provisions for liabilities and charges areprovisions in relation to trade debtors and settlementliabilities for the pre paid card business. These provisionsare predominantly due to historical exposures on pre paidcard contracts.

Segment reportingThe Member business provides mortgage, savings,investment and insurance products to members andcustomers. The Solutions business provides business-to-business services through people, processes andtechnology. The Board assesses performance based onprofit or loss before tax after the allocation of all centralcosts. The Member business performance improved onan underlying basis in 2010 with a break-even positionbefore Repositioning costs and FSCS levy, compared to aloss of £0.8m in the prior year. This position will continue toimprove in 2011 as the full year impact of the RepositioningProgramme savings become visible. The increase in the

Solutions business loss before tax is due to an increasedprovision for liabilities and charges as previously noted.

Balance sheet reviewLiquid assetsThroughout the year the Society continued to maintainhigh levels of liquidity of excellent quality. Total liquidity was25.2% (2009: 28.2%) with over three quarters of liquidityheld with AAA rated institutions.

At 31 December 2010 the Society had no exposures toPortugal, Italy, Ireland or Greece. Investments with Spanishbanks totalled £8m of which £5m has been repaidsubsequent to the year end. The remaining £3m is heldwith a AA rated Spanish bank with a major UK presence.

Loans and advances to customersThe Society continued to undertake lending only wherefunding was in place in 2010 and where lending could bedone profitably, fully reflecting costs of funding, liquidityand capital. Loans and advances to customers reduced by£135m in 2010 as shown in the table below:

Around 65% of the shrinkage in the mortgage portfoliorelated to higher risk exposures, including commercial(shrinkage of 11%), BTL (down by 5%) and loans securedon traded endowment policies (reduction of 20%). Thisreduction fits with the Society’s business simplificationobjectives and is expected to continue.

Summary Directors’ Report

22 23

Continued

LOANS AND ADVANCES TO CUSTOMERS

2010 2009£m LTV% £m LTV%

Residential Homeowners 1,929 55.8 2,017 49.0

Housing Associations 870 74.7 846 76.7

Commercial 488 78.3 545 74.7

Other 60 62.2 74 64.7

3,347 3,482

Provisions (22) (22)

3,325 3,460

ARREARS PERFORMANCE3+ months arrears

By number of loans By balances2010 2009 2010 2009

Residential 0.75 0.86 0.69 1.98

Commercial - 0.26 - 0.08

Housing Association - - - -

Other 1.29 1.39 0.29 0.60

Total 0.78 0.90 0.40 1.17

Approved by the Board of Directors on 3 March 2011: David Holborn, Chairman Richard Mayland, Chairman of the Audit Committee Jim Willens, Chief Executive.

Group results for the year2010 2009£m £m

Net interest receivable 17.8 20.4

Other income and charges 18.8 19.5

Gains less losses on financial instruments and hedge accounting - (0.1)

Administrative expenses and depreciation (36.9) (41.6)

Impairment (loss) / credit and other provisions (0.4) 0.6

Repositioning Programme (4.0) -

FSCS levy - 1.3

(Loss) / profit for the year before taxation (4.7) 0.1

Taxation credit / (expense) 1.0 (0.1)

(Loss) / profit for the financial year (3.7) -

Group financial position at the end of the year

2010 2009Assets £m £m

Liquid assets 823.9 1,002.5

Mortgages 3,264.7 3,386.2

Fair value adjustments for hedged risk 50.8 43.2

Other loans 60.4 73.6

Derivative financial instruments 34.2 17.9

Fixed and other assets 184.8 96.7

Total assets 4,418.8 4,620.1

Liabilities

Shares 3,593.0 3,787.2

Fair value adjustments for hedged risk 20.8 8.1

Borrowings 457.4 472.7

Derivative financial instruments 54.2 44.4

Other liabilities 29.1 37.6

Subordinated liabilities 58.6 60.8

Subscribed capital 29.6 29.9

Reserves 176.1 179.4

Total liabilities 4,418.8 4,620.1

Summary of key financial ratios2010 2009

% %

Gross capital as a percentage of shares and borrowings 6.65 6.50

Liquid assets as a percentage of shares and borrowings 25.21 28.20

(Loss) / profit for the year as a percentage of mean total assets (0.08) -

Management expenses for the year as a percentage of mean total assets (Excluding Repositioning Programme) 0.82 0.86

Management expenses for the year as a percentage of mean total assets (Including Repositioning Programme) 0.91 0.86

This Summary Financial Statement is a summary of information in theaudited Annual Accounts, the Directors’ Report and the Annual BusinessStatement, all of which will be available to members and depositors, free ofcharge on demand, at every branch of the Newcastle Building Societyfrom 28 March 2011.

Summary Financial Statementfor the year ended 31 December 2010

24 25

Respective responsibilities of Directorsand AuditorsThe Directors are responsible for preparing theSummary Financial Statement in accordancewith applicable United Kingdom law.

Our responsibility is to report to you ouropinion on the consistency of the SummaryFinancial Statement with the full AnnualAccounts, Annual Business Review, Directors’Report and Remuneration Committee Reportand its compliance with the relevantrequirements of Section 76 of the BuildingSocieties Act 1986 and regulations madethereunder.

We also read the other information containedin the Summary Financial Statement andconsider the implications for our statement ifwe become aware of any apparentmisstatements or material inconsistencieswith the Summary Financial Statement.

This statement, including the opinion, hasbeen prepared for and only for the Society’smembers as a body in accordance withSection 76 of the Building Societies Act 1986and for no other purpose. We do not, in givingthis opinion, accept or assume responsibilityfor any other purpose or to any other person towhom this statement is shown or in to whose

hands it may come save where expresslyagreed by our prior consent in writing.

We conducted our work in accordance withthe Bulletin 2008/3 issued by the AuditingPractices Board. Our report on the Society’sfull Annual Accounts describes the basis of ouraudit opinion on those Financial Statements, theAnnual Business Review, the Directors’ Reportand the Remuneration Committee Report.

OpinionIn our opinion the Summary FinancialStatement is consistent with the full AnnualAccounts, Annual Business Review, Directors’Report and Remuneration Committee Reportof the Newcastle Building Society Group for theyear ended 31 December 2010 and complieswith the applicable requirements of Section 76of the Building Societies Act 1986 andregulations made thereunder.

Karyn Lamont (Senior Statutory Auditor)for and on behalf of PricewaterhouseCoopers LLP

Chartered Accountants and Statutory AuditorsNewcastle upon Tyne

3 March 2011

Gross capital as a percentage of shares and borrowingsGross capital represents reserves, plus subordinated liabilities and subscribed capital.The purpose of capital is to provide a bufferagainst any losses arising from a society’s activities, thereby protecting investors’ funds.

The gross capital ratio measures the extent towhich a society’s activities are funded by capital, compared to shares and borrowings.The higher this ratio is, the greater the protection for investors.

Liquid assets as a percentage of shares and borrowingsLiquid assets are assets held by a society,which are in the form of cash or assets whichare readily convertible into cash. NewcastleBuilding Society has a ratio of liquid assets toshares and borrowings which is at a similarlevel to other societies. The ratio is maintainedat a level which the Directors consider appropriate for the activities of the Society.

Profit for the year as a percentage of meantotal assetsA building society needs to make a reasonablelevel of profit each year in order to maintainand strengthen its gross capital ratio. It issimilar to a company’s return on assets.

The Newcastle Building Society operates a policy of ‘profit sufficiency’ and one of the mostappropriate measures of profitability is to express profit as a percentage of mean total assets.

Management expenses for the year as apercentage of mean total assetsManagement expenses are the costs ofrunning a society and comprise administrative expenses, depreciation and amortisation.The lower this ratio is, the greater a society’s efficiency.

Annual re-election of DirectorsIn discharging its responsibilities to beaccountable to the Society’s members for theoperation of the Society, the Board regardsgood corporate governance as extremelyimportant. A revised UK CorporateGovernance Code (formerly the “CombinedCode on Corporate Governance”) was issuedby the Financial Reporting Council in June2010 and applies to all accounting periodsbeginning on or after 29th June 2010. Oneaspect of the new Code provides that allDirectors of FTSE 350 companies should besubject to annual election by shareholders,and the Building Societies Associationconsiders that this new requirement wouldapply to the twelve largest building societies.The FSA states that building societies shouldhave regard to the Code when establishingand reviewing its corporate governancearrangements, something which this Societyis currently doing.

Notes

Summary Financial Statementfor the year ended 31 December 2010

26 27

Independent Auditors’ Statement tothe Members of Newcastle BuildingSociety

We have examined the Summary Financial Statement of Newcastle BuildingSociety for the year ended 31 December 2010, which comprises the ChiefExecutive’s Report, the Remuneration Committee Report, the SummaryDirectors’ Report and the Summary Financial Statement.