World Bank Documentdocuments.worldbank.org/curated/en/658101468740215… · ·...

108

WORLD BANK DISCUSSION PAPER NO. 359 Work in progress for public discussion Fe& b. I The Demand for Oil Products in Developing Countries I)e,,,lot Catvh, tShanel 1S. krtc,it, Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

vuongthien -

Category

Documents

-

view

214 -

download

1

Transcript of World Bank Documentdocuments.worldbank.org/curated/en/658101468740215… · ·...

WORLD BANK DISCUSSION PAPER NO. 359

Work in progress

for public discussion Fe& b. I

The Demand for OilProducts in DevelopingCountries

I)e,,,lot Catvh,tShanel 1S. krtc,it,

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Recent World Bank Discussion Papers

No. 291 Transforming Payment Systems: Meeting the Needs of Emerging Market Economies. Setsuya Sato and David BurrasHumphrey

No. 292 Reguelated Deregutlation of the Financial System in Korea. Ismail Dalla and Deena KhatkhateNo. 293 Design Issutes in Ruiral Finance. Orlando J. Sacay and Bikki K. RandhawaNo. 294 Financing Health Services Throuigh User Fees and Insurance: Case Stuidiesfrom Sub-Saharan Africa. R. Paul Shaw and

Martha Ainsworth

No. 295 The Participation of Nongovernmental Organizations in Poverty Alleviation: The Case Study of the Honduiras SocialInvestment Fund Project. Anna Kathryn Vandever Webb, Kye Woo Lee, and Anna Maria Sant'Anna

No. 296 Reforming the Energy Sector in Transition Economies: Selected Experience and Lessons. Dale Gray

No. 297 Assessing Sector Institutions: Lessons of Experiencefrom Zambia's l dutcation Sector. Rogerio F. Pinto and Angelous J.Mrope

No. 298 Uganda's AIDS Crisis: Its Implicationsfor Development. Jill Armstrong

No. 299 Towards a Payments System Lawfor Developing and Transition Economies. Raj Bhala

No. 300 Africa Can Compete! Export Opporttunities and Challengesfor Garnients and Home Products in the European Market.Tyler Biggs, Margaret Miller, Caroline Otto, and Gerald Tyler

No. 301 Review and Olutlookfor the World Oil Market. Shane S. StreifelNo. 302 The Broad Sector Approach to Investment Lending: Sector Investmenit Programs. Peter Harrold and Associates

No. 303 Institutional Adjuistment and Adjusting to Instituitions. Robert Klitgaard

No. 304 Plutting Institutional Economics to Work: From Participation to Governance. Robert PicciottoNo. 305 Pakistan's Puiblic Agricultutral Enterprises: Inefficiencies, Market Distortions, and Proposalsfor Reform. Rashid Faruqee,

Ridwan Ali, and Yusuf Choudhry

No. 306 Grameen Bank: Performance and Stability. Shahidur R. Khandker, Baqui Khalily, and Zahed Khan

No. 307 The Uruguay Rouend and the Developing Economies. Edited by Will Martin and L. Alan Winters

No. 308 Bank Governance Contracts: Establishing Goals and Accouintability in Bank Restruictuiring. Richard P. RoulierNo. 309 Putblic and Private Secondary Education in Developing Couintries: A Comparative Stuidy. Emmanuel Jimenez and

Marlaine E. Lockheed with contributions by Donald Cox, Eduardo Luna, Vicente Paqueo, M. L. de Vera, andNongnuch Wattanawaha

No. 310 Practical Lessonsfor Africafrom East Asia in Industrial and Trade Plolicies. Peter Harrold, Malathi Jayawickrama, andDeepak Bhattasali

No. 311 The Impact of the Uruiguay Round on Africa. Peter Harrold

No. 312 Procuirement and Disbursement Manutalfor Projects with Community Participation. Gita Gopal

No. 313 Harnessing Information for Development: A Proposalfor a World Bank Grouip Strategy. Eduardo Talero and PhilipGaudette

No. 314 Colombia's Pension Reform: Fiscal and Macroeconomic Effects. Klaus Schmidt-Hebbel

No. 315 Land Quiality Indicators. Christian Pieri, Julian Dumanski, Ann Hamblin, and Anthony YoungNo. 316 Sustainability of a Government Targeted Credit Program: Evidence from Bangladesh. Shahidur R. Khandker, Zahed

Khan, and Baqui Khalily

No. 317 Selected Social Safety Net Programs in the Philippines: Targeting, Cost-Effectiveness, and Optionsfor Reform. KalanidhiSubbarao, Akhter U. Ahmed, and Tesfaye Teklu

No. 318 Private Sector Development During Transition: The Visegrad Couintries. Michael S. Borish and Michel Noel

No. 319 Edutcation Achievements and School Efficiency in Rural Bangladesh. Shahidur R. Khandker

No. 320 Houisehold and Intrahouisehold Impacts of the Grameen Bank and Similar Targeted Credit Programs in Bangladesh. MarkM. Pitt and Shahidur R. Khandker

No. 321 Clearance and Settlement Systemsfor Securities: Critical Design Choices in Emerging Market Economies. Jeff Stehm

No. 322 Selecting Development Projectsfor the World Bank. Jean Baneth

No. 323 Evalu(ating Pueblic Spending: A Frameworkfor Pueblic Expenditure Reviews. Sanjay Pradhan

No. 324 The Bangladesh Rural Advancement Committee's Credit Programs. Performance and Sustainability. Shahidur R.Khandker and Baqui Khalily

No. 325 Institutional and Entrepreneuirial Leadership in the Brazilian Science and Technology Sector:Setting a New Agenda.Edited by Lauritz Holm-Nielsen, Michael Crawford, and Alcyone Saliba

(Continuted on the inside back cover)

WORLD BANK DISCUSSION PAPER NO. 359

The Demand for OilProducts in DevelopingCountries

Dermot GatelyShane S. Streifel

The World BankWashington, D.C.

Copyright (D 1997The International Bank for Reconstructionand Development/THE WORLD BANK1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

All rights reservedManufactured in the United States of AmericaFirst printing February 1997

Discussion Papers present results of country analysis or research that are circulated to encouragediscussion and comment within the development community To present these results with the leastpossible delay, the typescript of this paper has not been prepared in accordance with the proceduresappropriate to formal printed texts, and the World Bank accepts no responsibility for errors. Some sourcescited in this paper may be informal documents that are not readily available.

The findings, interpretations, and conclusions expressed in this paper are entirely those of the author(s)and should not be attributed in any manner to the World Bank, to its affiliated organizations, or tomembers of its Board of Executive Directors or the countries they represent. The World Bank does notguarantee the accuracy of the data included in this publication and accepts no responsibility whatsoeverfor any consequence of their use. The boundaries, colors, denominations, and other information shown onany map in this volume do not imply on the part of the World Bank Group any judgment on the legalstatus of any territory or the endorsement or acceptance of such boundaries.

The material in this publication is copyrighted. Requests for permission to reproduce portions of itshould be sent to the Office of the Publisher at the address shown in the copyright notice above. TheWorld Bank encourages dissemination of its work and will normally give permission promptly and, whenthe reproduction is for noncommercial purposes, without asking a fee. Permission to copy portions forclassroom use is granted through the Copyright Clearance Center, Inc., Suite 910, 222 Rosewood Drive,Danvers, Massachusetts 01923, U.S.A.

ISSN: 0259-210X

Dermot Gately is a professor of economics at New York University. Shane S. Streifel is an energyeconomist in the Commodity Policy and Analysis Unit of the World Bank's International EconomicsDepartment.

Library of Congress Cataloging-in-Publication Data

Gately, Dermot, 1943-The demand for oil products in developing countries / Dermot

Gately, Shane S. Streifel.p. cm. - (World Bank discussion paper ; 359)

Includes bibliographical references, (p. ).ISBN 0-8213-3891-91. Petroleum industry and trade-Developing countries.

I. Streifel, Shane S. II. Title. III. Series: World Bankdiscussion papers ; 359.HD9578.D44G38 1997338.2'7282'091724-dc2l 97-4242

CIP

Contents

FOREWORD . viiABSTRACT . ............................................... ixACKNOWLEDGMENTS ......................................... xiABBREVIATIONS AND ACRONYMS ................................ xii1. Introduction and Summary ........................................... 1

..1 Oil Demand in the Developing Countries 1971-93 .................... l1.2 Econometric Results and Implications ............................ 31.3 Organization of the Paper .................................... 5

2. World Data, by Region: Population, Income, Energy, and Oil Consumption ......... . 63. Data for 37 Developing Countries: Income, Population,

Energy, and Total Oil Consumption ........... .. ................ 123.1 1993 Snapshots: Heterogeneity across Countries ..................... 12

3.1.1 Income and Population: 1993 Snapshot ...................... 143.1.2 Energy Consumption and Population: 1993 Snapshot .... ......... 143.1.3 Oil Consumption and Population: 1993 Snapshot ................ 153.1.4 Oil's Share of Energy Consumption and Electric Power Generation:

1993 Snapshots ...................................... 173.2 Changes from 1971 to 1993: Per-Capita Income, Energy and Oil

Consumption--Heterogeneity across 37 Developing Countries,and in Comparison with OECD Countries .................... 21

3.2.1 Per-Capita Income: Changes from 1971 to 1993 ................ 233.2.2 Per-Capita Energy Consumption: Changes from 1971 to 1993 .... ... 243.2.3 Per-Capita Oil Consumption: Changes from 1971 to 1993 .... ...... 253.2.4 Oil's Share of Energy Consumption and Electric Power Generation ... . 26

3.3 Demand Changes Relative to Income Changes, 1971-93 ...... .......... 293.3.1 Energy Demand Changes vs. Income Changes, 1971-93 .... ....... 313.3.2 Oil Demand Changes vs. Income Changes, 1971-93 .... .......... 32

4. Consumption of Eight Major Oil Products: Data for 37 Developing Countries ... 334.1 1993 Snapshots ............. 33

4.1.1 Oil Products' Shares of Total Oil Consumption: 1993 Snapshots ... ... 334.1.2 Ratios of Oil Product Demand to Income: 1993 Snapshots .... ...... 36

4.2 Oil Products' Shares of Oil Consumption: Changes from 1971 to 1993 .. ..... 394.3 Changes in Individual Oil Product Demand vs. Changes in Income,

1971 to 1993 .......... ............................. 405. Important Phenomena Affecting Oil Demand .... 49

5.1 The Importance of Income Growth . ............ 495.2 Asymmetric Response to Income Decline in Oil-Exporting Countries .. ...... 495.3 Oil Demand Response to Oil Price Increases ........ .. .............. 515.4 Oil Demand Response to Oil Price Cuts ............ ............... 515.5 The Importance of Indigenous Energy Resources ....... .. ............ 545.6 Domestic Energy Policies ................ .................... 555.7 The Transition from Traditional Fuels to Modern Fuels ....... .......... 57

iii

Contents continued

6. Econometric Analysis of Demand for Eight Oil Products ........ .. ............. 606.1 Specifications of Per-Capita Oil Product Demand Equations .... .......... 606.2 Estimated Elasticities of Oil Product Demand with Respect to

Price and Income .................................... 627. Projections of Oil Product Demand .. 748. Conclusions .. 80

Appendix A: Supplementary Tables ...... 84

References ....... 87

List of Figures

1. Population, 1971-93 .............................................. 62. Real Income, Energy and Oil Consumption, 1971-93: Total and Per-Capita .... ...... 83. Energy Consumption vs. Income, Per-Capita, 1971-93 ....................... 94. Oil Consumption vs. Income, Per-Capita, 1971-93 .......................... 105. Energy Consumption by Fuel: 1971-93 ................................. It6. Income vs. Population, 1993 ................ ........................ 147. Energy Consumption vs. Population, 1993 ............................... 148. Oil Consumption vs. Population, 1993 ................................ 159. Oil Consumption, 1993 and 1971 ................................. 1610. Fuel Shares of Modern Energy, 1993 .................................. 1811. Fuel Shares of Energy including Biomass, 1993 ............ ................ 1912. Fuel Shares of Electric Power, 1993 ................................... 2013. Average Annual Growth in Per-Capita Income, 1971-93

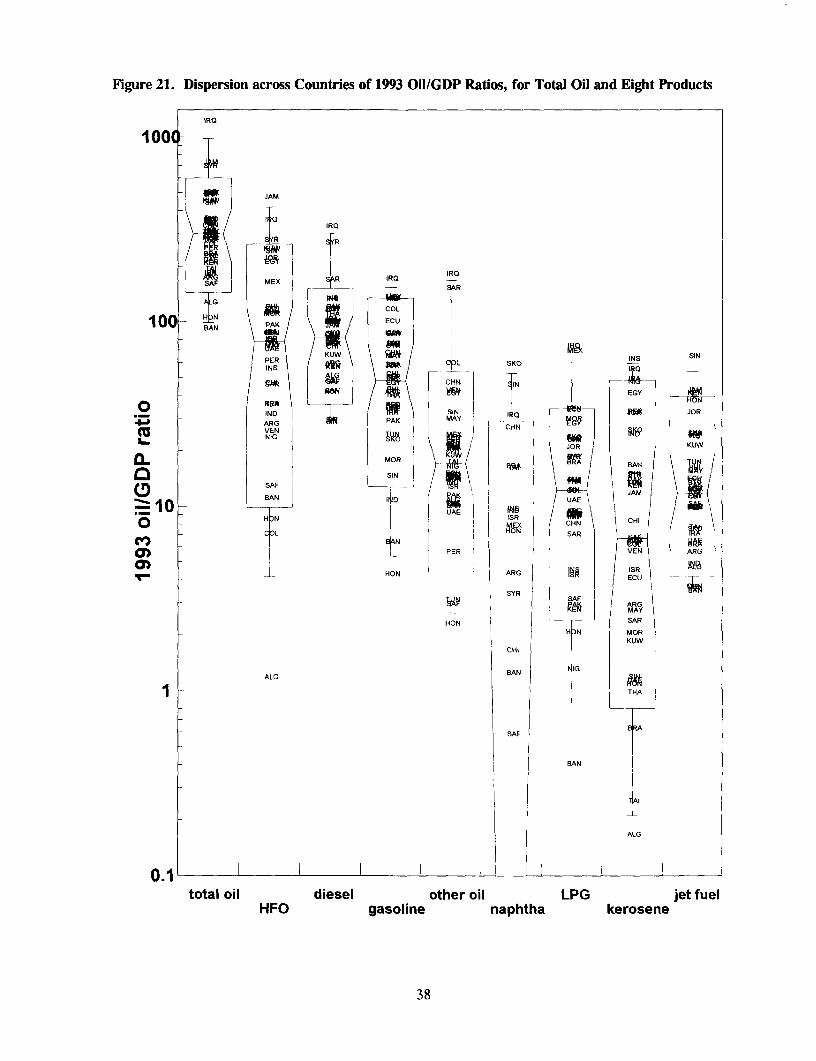

vs. Standard Deviation of Annual Growth ................................ 2314. Per-Capita Energy Consumption, 1993 vs. 1971 ........................... 2415. Per-Capita Oil Consumption, 1993 vs. 1971 .............................. 2516. Oil's Share of Energy Consumption, 1993 vs. 1971 ......................... 2617. Oil's Share of Electric Power Generation, 1993 vs. 1971 ...................... 2718. Ratios, 1993/1971: Per-Capita Energy Demand vs. Per-Capita Income .... ......... 3119. Ratios, 1993/1971: Per-Capita Oil Demand vs. Per-Capita Income ............... 3220. Oil Product Shares of Oil Consumption, 1993 ............................. 3421. Dispersion across Countries of 1993 Oil/GDP Ratios, for Total Oil

and Eight Products ............. .................................. 3822. Shares of Eight Oil Products, 1993 vs. 1971 .............................. 3923. Ratios, 1993/1971: Per-Capita Gasoline Demand vs. Per-Capita Income .... ........ 4024. Ratios, 1993/1971: Per-Capita Diesel Demand vs. Per-Capita Income ... ..... 4125. Ratios, 1993/1971: Per-Capita Jet Fuel Demand vs. Per-Capita Income .... ........ 4226. Ratios, 1993/1971: Per-Capita Heavy Fuel Oil Demand vs. Per-Capita Income ... .... 4327. Ratios, 1993/1971: Per-Capita Kerosene Demand vs. Per-Capita Income .... ....... 4428. Ratios, 1993/1971: Per-Capita LPG Demand vs. Per-Capita Income .... .......... 4529. Ratios, 1993/1971: Per-Capita Naphtha Demand vs. Per-Capita Income .... ........ 47

iv

Figures continued

30. Ratios, 1993/1971: Per-Capita Other Oil Demand vs. Per-Capita Income .... ....... 4831. Oil Demand vs. Income, Per-Capita, 1971-93: India, Peru,

South Korea, and Saudi Arabia ....................................... 5032. World Price of Crude Oil, 1971-93 .................................... 5133. Energy and Oil Demand vs. Income, Per Capita, 1971-93: South Korea and OECD ... . 5234. Oil Price vs. Oil's Fuel Share of Energy, 1971-93: South Korea and OECD .... ..... 5335. Oil's Fuel Share of Modern Energy, 1971-93: South Korea, OECD, and India .. ..... 5436. Indonesia: Energy and Oil Demand vs. Income, Per-Capita, 1971-93 .... .......... 5737. South Korea: Fuel Use in Residential and Commercial Sectors, 1971-93 .... ........ 5838. Indonesia: Fuel Use in Residential and Commercial Sectors, 1971-93 .... .......... 5839. Biomass Share of Energy, 1993 vs. 1971 ................................ 5940. Total Oil Consumption vs Real Income: History 1971-93 and Projections to 2010--

China, Other Asia, Other LDC, OPEC & Mexico .7841. Oil Consumption vs. Income, Per-Capita: History 1971-93 and Projections

to 2010 -- China, Other Asia, Other LDC, OPEC & Mexico ................... 79

List of Tables

1. Levels for Oil and Energy Consumption, Income, and Population for 1993 .... ...... 132. Per-Capita Levels of Oil and Energy Consumption, and of Income,

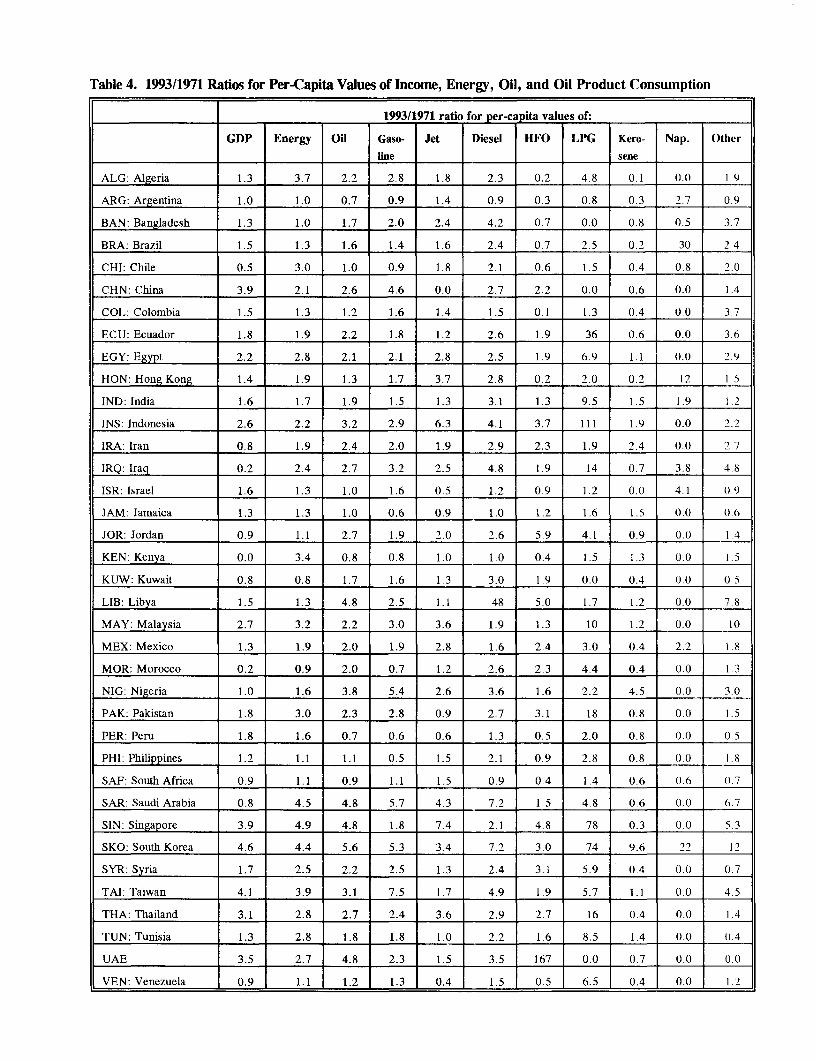

for 1971 and for 1993 ............................................. 223. Oil's Share of Energy and of Electric Power, 1971 and 1993 ................... 284. 1993/1971 Ratios for Per-Capita Values of Income, Energy, Oil, and

Oil Product Consumption . .......................................... 305. Oil Product Consumption, 1993 ..................................... 356. Oil/GDP Ratios for Total Oil and Eight Products, 1993 ....................... 377. Gasoline Demand Equations: Long-run Elasticities ............ ........... 668. Diesel Demand Equations: Long-run Elasticities ........................... 679. Jet Fuel Demand Equations: Long-run Elasticities .......................... 6810. Heavy Fuel Oil Demand Equations: Long-run Elasticities ..................... 6911. LPG Demand Equations: Long-run Elasticities ............................ 7012. Kerosene Demand Equations: Long-run Elasticities ......................... 7113. Naphtha Demand Equations: Long-run Elasticities .......................... 7214. Other Oil Product Demand Equations: Long-run Elasticities ................ 7315. Long-run Elasticities of Regional Oil Product Demand with Respect to

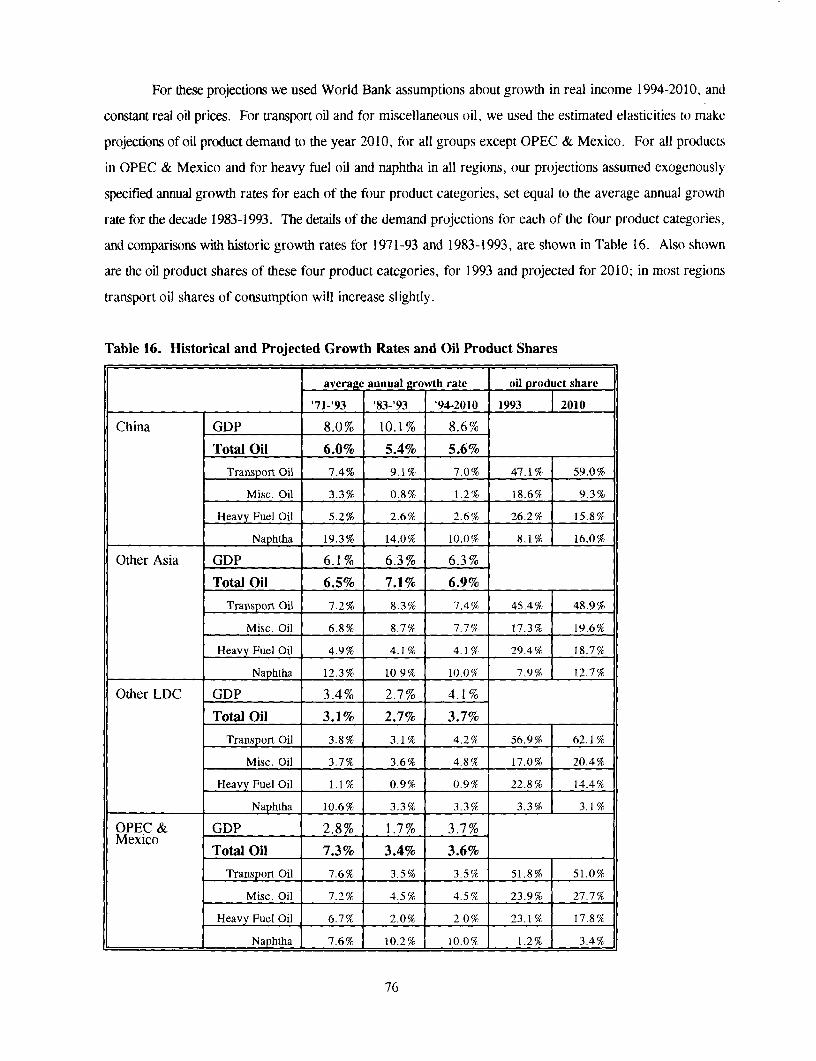

Income and Crude Oil Price .............. .......................... 7516. Historical and Projected Growth Rates and Oil Product Shares .................. 76

Appendix Tables

Table Al. Per-Capita Oil, Energy and Income:Absolute Change 1971-93, and Average Annual Growth .................. 85

Table A2. Average Annual Growth Rate of Oil Consumption, 1971-93 ..... ........... 86

v

FOREWORD

Oil and energy markets have experienced dramatic changes over the past two decades, but there

remains considerable uncertainty about future developments in the world oil market. High prices in the

1970s and 1980s induced significant improvements in energy efficiency and substitution from oil to

alternative fuels. Since the decline in prices in 1986 oil demand growth has rebounded, but at a much

slower rate than prior to the major oil price increases of 1970s. In addition, large declines in the former

Soviet Union and Eastern Europe have reduced the aggregate level of world demand. However, oil

demand is now set to rise in all main regions led by rising incomes, population, industrialization,

investment and trade. Most of the growth is generally expected to occur in the developing countries.

This study examines the growth in demand for eight major oil products for 37 developing countries

over the 1971-1993 period. It analyzes the relationships and changes over time for income, population,

energy and oil product demand for each of these developing countries. The paper shows the extreme

heterogeneity among these countries, not only among themselves but compared with the relative

homogeneity of the developed countries. Some of the important phenomena that affect oil demand are

examined, and income and price elasticities are calculated for each of the products in all countries. Based

on these results, it appears that the medium-term future will be like the past, with oil demand growing

about as fast as income.

Rapidly rising oil demand in the developing countries has significant implications for the petroleum

industry, governments and the world oil market. The increasing concentration of oil demand in the

developing countries could alter crude oil trade flows, requiring more oil from the Middle East. Greater

dependence on oil from the Middle East due to higher demand does not necessarily imply higher oil prices.

Much will depend on trends in non-OPEC supplies, OPEC's share of the world oil market, and the pricing

policies of key oil exporting countries.

This study is part of ongoing efforts of the International Economics Department of the World Bank

to evaluate and project developments in world markets of major commodities. The analysis and

conclusions of this report should provide a basis for further public debate on these issues.

Masood Ahmed

Director

International Economics Department

vii

ABSTRACT

This paper examines the growth in oil product demand over the 1971-1993 period for 37

developing countries (outside the former Soviet Union and Eastern Europe). These countries represent

90% of oil demand for the developing countries, and nearly 70% of the world's population. Relationships

and changes over time for energy and total oil demand with respect to income and population are examined

for each of the countries and presented graphically. The paper then focuses on the 8 major petroleum

products--liquefied petroleum gases (LPG), naphtha, gasoline, jet fuel, kerosene, diesel (gasoil), heavy fuel

oil, and other products--which are similarly examined and presented. Some of the important phenomena

that affect oil demand are analyzed. Income and price elasticities are calculated for each of the eight major

oil products in all 37 countries. Based on these results, projections of oil demand to 2010 are presented.

Over the 1971-1993 period, world oil demand increased by 18.3 million barrels per day or 37%.

Over three quarters of the net growth occurred in the developing countries, rising at an average rate of 5 %

p.a. Oil demand in the developing countries nearly tripled over this period, and its share of world oil

demand rose from 15 % to nearly one third. Despite the growth of per-capita oil demand in the developing

countries, the level is still only about one-tenth as great in the developing countries as in the OECD.

The 37 countries are extremely heterogeneous in many dimensions, not only among themselves

but compared with the relative homogeneity of the developed countries. Oil's share of energy varies

widely, from less than 20% in China and South Africa to more than 90% in Singapore and Jamaica. Over

the 1971-1993 period, oil's share of energy demand declined, as in the developed countries, but for some

countries oil's share has not changed, while in others it has increased, e.g. oil-exporting countries. Oil's

share in power generation is relatively high, varying as widely as possible across countries--from zero in

South Africa to 100% in Singapore. There are also significant differences across countries in the

composition of oil demand, especially for the shares of heavy oil, naphtha and kerosene. The share of

transportation products ranges from one-fourth in Singapore, to one-half in China, two-thirds in Brazil,

and four-fifths in South Africa. Oil/income ratios vary widely across countries for most products, and

changes in demand have also varied widely, both absolutely and relative to changes in income.

OECD oil consumption has been affected more by oil price changes than by income changes, and

more by oil price increases than by price cuts. In the 37 developing countries, there has been a much

greater demand response to income growth than to changes in oii prices. Moreover, there has been greater

demand response to the oil price cuts of the 1980s, in contrast to the OECD where there has been relatively

ix

little demand response to the price cuts. For many oil-exporting countries, oil consumption has responded

asymmetrically to changes in income: increasing rapidly when income is growing, and continuing to

increase--albeit more slowly--even when income is declining.

Although the growth of oil demand is primarily influenced by income growth, there has been

substantial fuel-switching in response to the oil price increases of the 1970s--especially in power

generation. However, since the oil price decline in 1986, there has been a significant rebound in oil-use

to generate electricity in some countries. Other factors affecting oil demand are a country's endowment

of domestic energy resources, and the transition to modern fuels from traditional energy sources.

Overall, the econometric results of the eight major oil products were fairly good for gasoline,

diesel, LPG, and "other oil" products. Results were mixed for jet fuel and heavy oil, and quite

unsatisfactory for naphtha and kerosene. Income was the most important explanatory variable, and the oil-

exporting countries often displayed an asymmetric response to income increases and decreases. In only

about a third of the cases was the price of crude oil significant, and the estimated elasticities were small

relative to the income elasticity. The evidence on whether demand responded symmetrically to oil price

increases and decreases was mixed: some products in some countries appeared to respond symmetrically,

and others asymmetrically.

The econometric results and analysis suggest that the medium term future will be like the past.

With continued growth in real income in the developing countries, oil demand should grow about as fast

as income. This implies a doubling of their oil demand by year 2010, relative to their 1993 levels. The

largest growth will continue to be in Asia. However different oil demand patterns may unfold given many

uncertainties with respect to technology, industrialization, urbanization, penetration of alternative fuels,

macroeconomic and financial performance, and government policies.

Rising oil demand in the developing countries has significant implications for the world oil market,

governments and industry. The increasing concentration of oil demand in the developing countries could

alter all crude oil trade flows, and require more oil from the Middle East. Greater dependence on oil from

the Middle East due to higher demand does not necessarily imply higher oil prices; much will depend on

non-OPEC supplies, OPEC's share of the world oil market, and pricing policies of key oil exporting

countries. Higher demand for petroleum products will necessitate greater refining capacity. Should the

demand barrel become lighter, and the supply barrel heavier as generally expected, greater upgrading

capacity will be required to produce transport fuels and other light products. Much will depend on trends

in heavy fuel oil consumption, especially in power generation. While higher oil demand is associated with

higher incomes and rising standards of living, it can also mean greater emissions, pollution and congestion

from oil use. Government policies can greatly influence these trends through pricing and other initiatives.

x

ACKNOWLEDGMENTS

The views expressed in this paper are solely those of the authors. Critical conmments are gratefully

acknowledged from Taka Akiyama, Clive Armstrong, Douglas Barnes, Carol Dahl, Peter Davies, Thuvara

Nayar, William Porter, Joerg-Uwe Richter, and Jayant Sathaye. Any errors or omissions are the

responsibilities of the authors.

The authors thank Jean Jacobson for assisting in preparation of the final report.

xi

ABBREVIATIONS AND ACRONYMS

FSU & EE Former Soviet Union and Eastern Europe

GDP Gross Domestic Product

HFO Heavy Fuel Oil

I EA Internationial Energy Agency

LDC Less Developed Countries

LPG Liquefied Petroleum Gas

mb/d million barrels per day

MTOE Million Tons of Oil Equivalent

OECD Organization of Economic Cooperation and Development

OPEC Organization of Petroleum Exporting Countries

UAE United Arab Emirates

xii

1. Introduction and Summary

This paper analyzes the growth in oil product demand since 1971 in the developing countries, defined

as those countries outside the Organization for Economic Cooperation and Development (OECD), the former

Soviet Union and Eastern Europe (FSU & EE). Much of the growth in world demand over the past two

decades has occurred in the developing countries. Over the 1971-1993 period, world oil demand increased

by 18.3 million barrels per day (mb/d) or 37%. Of this increase, 14.2 mb/d occurred in the developing

countries, where oil demand grew at an average annual rate of 5 %. OECD oil demand was only moderately

higher, as consumer behavior was severely impacted by the large oil price increases in 1973-74 and 1979-80.

Demand in the FSU & EE also was only modestly higher, having been affected by the enormous economic

and political transformations in recent years.

Oil demand in the developing countries nearly tripled over the 1971-93 period, and its share of world

oil demand more than doubled, from 15 % to nearly one-third. Since most of the future growth in oil demand

is generally expected to occur in the developing countries, it is important to understand where its growth has

occurred, the main driving forces, and what the implications are for future patterns of oil consumption in these

countries. Expected growth in oil demand has significant implications for both oil-importing and oil-exporting

countries, the refining industry, government policies, and for the world oil market, including oil prices.

The analysis focuses on the 37 largest oil-consuming developing countries, which represent 90% of

oil demand for this group, and nearly 70% of the world's population. For each of these countries we analyze

the relationships and changes over time for income, population, energy and oil demand. We then focus on

the 8 major petroleum products -- liquefied petroleum gases (LPG), naphtha, gasoline, jet fuel, kerosene,

diesel (gasoil), heavy fuel oil (HFO), and "other" oil products -- and analyze some of the important

phenomena that explain many of the changes in demand for these products. Income and price elasticities are

calculated for each of the eight major oil products in all 37 countries. Based partly on these econometric

results, projections of future demand are presented. The main conclusions of the paper follow.

1.1 Oil Demand in the Developing Countries 1971-93

The paths of per-capita oil consumption for the different regions of the world have varied widely since

1971. In the OECD, per-capita oil consumption declined after oil prices increased, especially after the

1979-80 price increase, but has remained flat since the early 1980s. In China, it has grown at a slower rate

than income, while in the rest of Asia it risen about as rapidly as income. Consumption in the oil-exporting

countries once surged when their income grew, and it has continued to grow -- albeit more slowly -- even

though per-capita incomes have been stagnant or declining. In the other developing countries and in

I

FSU & EE, per-capita consumption once increased in proportion to income growth but over the last decade

has decreased in proportion to income decline.

The 37 developing countries are extremely heterogeneous in many dimensions, not only among

themselves but compared with the relative homogeneity of the developed countries. For example, the 1993

levels of per-capita income, energy and oil consumption for the 37 countries range across two orders of

magnitude. Oil's share of energy varies widely: from less than 20 % in China and South Africa to more than

90% in Singapore and Jamaica. Over the 1971-1993 period, oil's share of energy demand has declined in most

developing countries, as it has in the OECD countries, but it has increased in a few oil-exporting countries.

Oil's share of power generation is relatively high in the developing countries, although it ranges as widely as

possible -- from zero in South Africa to 100% in Singapore.

There are also significant differences across countries in the composition of the demand barrel

consumed, especially for the shares of heavy fuel oil, naphtha and kerosene. Similarly, there is a wide range

in the share of transportation products: from one-fourth in Singapore, to one-half in China, two-thirds in

Brazil, and four-fifths in South Africa. Oil/income ratios vary widely across countries for most products, and

changes in demand over the 1971-93 period have also varied widely, both absolutely and relative to changes

in income.

Despite the growth of per-capita oil demand in the developing countries and its reduction in the

OECD, the level is still only one-tenth as great (on average) in the developing countries as in the OECD.

Thus there remains enormous potential for large demand growth in these countries, depending on the structure

and pace of economic development.

A number of important phenomena affecting oil demand were analyzed, in an attempt to explain the

changes in consumption over the period. Since 1971, OECD oil consumption has been affected more by oil

price changes than by income changes, and more by oil price increases than by price cuts. In the 37

developing countries, in contrast, there has been a much greater demand response to income growth than to

changes in oil prices. Moreover, there has been greater demand response to the oil price cuts of the 1980s,

in contrast to the OECD where there has been relatively little demand response to the price cuts.

For many oil-exporting countries, oil consumption has responded asymmetrically to changes in

income: increasing rapidly when income is growing, and continuing to increase -- albeit more slowly -- even

when income is declining.

Although the growth of energy and oil demand is primarily influenced by income growth, there has

been substantial fuel-switching away from oil in response to the oil price increases of the 1970s, as well as

some increase in fuel efficiency. The fuel-switching is most obvious in electric power generation. However,

in a few countries there has been a significant rebound in oil-use in power generation since the 1986 collapse

in world oil prices, notably in South Korea, Taiwan and Thailand.

2

A country' s endowment of domestic energy resources is an important factor in understanding some

countries' demand for oil and energy. This is most obvious for the oil-exporting countries, which have

abundant reserves of oil and natural gas. Some oil importing countries have other energy resources, e.g., coal

in China, India, and South Africa, and hydroelectric power in most South American countries, and they

consume large amounts of these resources.

Governments intervene in energy markets in a number of ways but mainly through pricing policies,

access to markets, and import policies. Some governments have subsidies on most or all petroleum products,

particularly in oil-producing countries. At the other extreme, many countries have moved to market prices,

or are nearly there. However, a large number of countries have subsidies on household fuels, notably LPG

and kerosene (and electricity); these are sometimes accompanied by import controls and rationing, which leads

to supply deficiencies and a array of market problems. In many countries these prices are cross-subsidized

with taxes on transport fuels and other oil products. While subsidies are set so as to provide modern fuels to

lower income households and lessen the impact on biomass resources and the environment, governments face

difficult decisions trying to meet diverse objectives simultaneously. Nevertheless, government polices can

greatly affect consumption patterns of all fuels, modern and traditional.

The transition from traditional, biomass fuels to modern fuels has an important influence on the growth

of demand for oil products, especially in the residential sector. During the transition phase, the growth of

modem fuels is driven by income growth and also by substitution for traditional fuels. This transition has been

virtually completed in South Korea which will slow its rapid growth of modern fuel use, but this transition has

a long way to go in many other countries.

1.2 Econometric Results and Implications

For each of the products and each of the countries, we examined several alternative equation

specifications of per-capita oil product demand as a function of per-capita real income and the real price of

crude oil. Overall, the results were fairly good for gasoline, diesel, LPG, and "other" oil products. Results

were mixed for jet fuel and heavy fuel oil, and quite unsatisfactory for naphtha and kerosene. Income was

the most important explanatory variable, and the oil-exporting countries often displayed an asymmetric

response to income increases and decreases. In only about a third of the cases was the price of crude oil

significant, and the estimated elasticities were small relative to the income elasticity. The evidence on whether

demand responded symmetrically to oil price increases and decreases was mixed, at best: some products in

some countries appeared to respond symmetrically, and others asymmetrically.

Analysis based on the econometric results suggests that the medium-term future will be like the past.

With continued growth in real income in the developing countries, oil demand should grow about as fast as

income. This implies a doubling of their oil demand by the year 2010, relative to their 1993 levels. The

3

largest growth will continue to be in Asia.

In developing countries where per-capita income is growing, oil demand should continue growing at

about the same rate as income. But where per-capita income is declining, per-capita oil demand will also

decline -- except in the oil-exporting countries, where oil consumption continues to increase despite declining

per-capita income.

Transportation oil demand (about half of the barrel consumed, on average) ought to grow at least as

fast as income, in virtually all developing countries. The growth of demand for heavy fuel oil and naphtha

are less easily predicted, and are more dependent on government policies regarding electric power generation

and expansion of the petrochemical industry, respectively. Kerosene in most countries appears to be an

inferior good, whose use declines as it is replaced by higher quality fuels as incomes rise, and these fuels

become available or affordable, or both. Government policies and prices can greatly affect demand for this

fuel. For LPG, consumption is also influenced by government policies regarding taxes and subsidies in the

residential sector; its demand could grow at least as rapidly as income, especially in those countries where the

transition to modem fuels is an important phenomenon. Demand for "other" oil products could also grow as

rapidly as income.

However there are many uncertainties that may result in different oil demand patterns unfolding, e.g.,

technology changes, the degree of industrialization, urbanization, penetration of alternative fuels notably

natural gas, macroeconomic performance, and government policies with respect to subsidies, taxation,

traditional fuel use and other issues. At some point there will be saturation effects and a slowdown in energy

demand growth, as already being witnessed in South Korea. Given the extreme heterogeneity of the

developing countries, it is difficult to predict when turning points may occur or how long-term economic and

energy developments will proceed in the various regions.

Rapidly rising oil demand in the developing countries has significant implications for the petroleum

industry, governments and the world oil market. Obviously, greater product demand will require greater

refining capacity. Countries have the choice of building refineries for domestic use or export, or importing

oil products. Should the demand barrel become lighter (and the supply barrel become heavier) as is generally

expected, it means that greater upgrading capacity will be required to supply transport fuels and other light

products. However, much could depend on trends in heavy fuel oil consumption, especially in power

generation.

The increasing concentration of oil demand in developing countries, and in Asia in particular, could

alter trade flows of crude oil. More crude (and possibly products) will be required from the Middle East to

supply growing demand in Asian and other markets. Greater dependence on Middle East oil does not

necessarily imply higher oil prices, although higher demand will add upward pressure, all else equal.

However, much will depend on trends in non-OPEC supplies, OPEC's share of the world oil market, and the

4

pricing policies of key oil-exporting countries.

Higher oil demand has obvious benefits and costs in those countries where demand is rising rapidly.

Greater oil (and energy) demand is associated with higher incomes and raised standards of living. However,

it can also mean greater emissions, pollution and congestion from higher oil use. Government policies can

influence these trends through pricing and other policies. Subsidized prices distort markets and send improper

signals to consumers, causing even greater consumption. On the other hand, excessively taxed products can

adversely affect economic activity and consumer welfare.

1.3 Organization of the Paper

The paper is organized in the following manner. In Section 2 we summarize the world's growth by

main geographical region or grouping over the 1971-1993 period, for population, income, energy and oil

consumption. In Section 3 we focus on these same variables for the 37 developing countries. With so many

countries and variables, we attempt to synthesize the data and changes over time graphically, e.g., 1993

snapshots of the data; per-capita changes over time; and per capita changes versus income changes over the

period. We describe the extreme heterogeneity of these countries, both among themselves, and also compared

with the relative homogeneity of the OECD.

In Section 4, we similarly analyze demand for the 8 major oil products in the 37 countries. Section

5 describes some of the important phenomena that explains some the changes that have occurred in the demand

for the individual petroleum products.

Several specifications of the demand equation are presented in Section 6, and income and price

elasticities are calculated for the 8 products for each of the 37 countries. Based on these results, the

implications for oil demand growth to the year 2010 are projected in Section 7. Finally, the summary and

conclusions are presented in Section 8.

5

2. World Data, by Region:

Population, Income, Energy, and Oil Consumption

First we summarize graphically the world's data since 1971 for population, real income, energy and

oil consumption, both total and per-capita levels. We divide the world into six regions:

* Organization for Economic Cooperation and Development (OECD);'

* the Former Soviet Union and Eastern Europe (FSU & EE);

* OPEC and Mexico2 , the major oil exporters (OPEC & Mexico);

* China;

* Other Asia (excluding Japan, China, and Indonesia); and

* Other Less Developed Countries3 (LDC): excluding all countries already identified.

The source of our energy and oil data is the International Energy Agency (IEA), Energy Statistics and

Balances of Non-OECD Countries. Population data and data on real income are from the World Bank

(income is measured in 1987 US $, using 1987 exchange rates for all years).

In each of these first few graphs, the igure 1. Population (millions), 1971-93

vertical scales are logarithmic, to allow easy 2000 r --

comparison of the slopes of various regions' other 4>ia

curves, which measure their annual growth Ch'

rates. We show first the population of these six .... .°°°.......-.-.

regions in Figure 1. World population grew 0' - _____

from 3.5 billion in 1971 to 5.1 billion in 1993, E 700 -5_600 Othe LD -- ~

at an average rate of 1.74% per year. The X2

fastest growth rate has been in Other LDC 0. , -6' OPEC & Mexico00.400 f - __ __ ,,,, __ _ _ _

(2.71%), followed closely by OPEC & Mexico ,-400

(2.62%), then Other Asia (2.17%) and China 300

(1.54%). Much slower population growth has

been experienced in the OECD (0.76%), and in 200 1 1r1971 1976 1981 186 1991

FSU & EE (0.72%).

Not included in our "OECD" group are three new OECD members, the Czech Republic, Hungary,and Mexico.

2 Mexico was combined with OPEC because of its size as an oil exporter, and because its oilconsumption behavior is similar to that of most OPEC members.

3 The term "LDC" is used only for convenience.

6

In Figure 2 we show:

* Real income (billions 1987$), and real income per capita (1987 $/person)

* Energy consumption (MTOE: million tons oil-equivalent), and energy consumption per capita

(tons of oil-equivalent/person); only modern energy is included: traditional, biomass energy

consumption is not included

* Oil consumption (MT: million tons), and oil consumption per capita (tons/person)4

We see the steady growth of real income in the OECD and Other Asia, and the rapid but irregular growth of

China. In other regions, income has been stagnant, as in OPEC & Mexico after 1978, and in the Other LDC

in the 1980s. In FSU & EE, growth slowed in the early 1980s and total income actually declined since the

late 1980s.

Total energy consumption (modern energy only5) generally has moved together with income, except

in regions such as OPEC & Mexico and Other LDC, where income has been stagnant but energy has continued

to grow. Per-capita energy consumption has also been increasing in most regions, except in Other LDC tor

more than a decade and in FSU & EE since the late 1980s.

Oil consumption has moved closely with income in some regions such as Other Asia and China, but

its growth in the OECD was affected dramatically by the oil price increases of the 1970s. In per-capita terms,

oil consumption has taken several different paths, especially since the 1979-80 oil price increases. It has

increased rapidly in China and Other Asia, but from very low levels. In OPEC & Mexico, its growth has

slowed dramatically. In the other three regions -- the OECD, Other LDC, and FSU & EE -- per-capita oil

consumption has declined substantially.

4 One million tons of oil per year equals approximately 20,000 barrels of oil per day.

5 Traditional biomass fuels such as fuel wood are important in many countries. Their fuel share isincluded in Figure 11, and their importance is discussed in Section 5.7.

7

Figure 2. Real Income, Energy and Oil Consumption, 1971-93: Total and Per-Capita

20000 -- _20000 - j__o__t_Per CReal Income OC12aia(197;

7000 000soo._ seoo _ _ .

.0@0 _ _ . 50004000 4000

3000 3000 _Eastern Europe & Fonrmerovietjnion

2000 2000

Eastern Europe & . .... OPEC & MexicoOPEC & Mexico Former Soviet Union

7O -7 0 - - DC0

s00 500O

400 400 . .............~. 50300 i Other0 LDC 300 Other Asia

200 C 200

70 701971 1976 1981 1986 1991 1971 1976 1981 1986 1991

5o00 Energy Consumption (MTOE) - 5 Energy Per Capita (toe/person) OECD

4000 4

3000 OEasern Europe & Former Soviet Uni

2000 - Eastern Europe & Form n 2

1000 _O_P1 EC & Mexjco900 X00

700 7600 0.6 Other LDC

500~~~~~~~~~~~~~~~~~~~~~~~~.

4004

OPEC & Mexico

100 0.1 '1971 1976 1981 1986 1991 1971 1978 1901 1998 1991

2000 3 Oil Per Capita (tons/person)Oil ConsumptionOECD 2

(million tons)1000900S00700 tEastern Europe & Former Soviet U0

600 07

400 060.5 OPEC & Mexi ------ -.----------'

300 04OPEC&M,xIco- **. . 04o

… -~~~~~~~~0200 Other LD

Other Asia Ch 0.2 OtherAsia

100

70 -0.09

60 = ___ °0.°0°8 . 0.050 007.06

40 0.051971 1976 1981 1906 1991 1971 1976 1901 1906 1991

However, simple comparisons across regions within a single graph in Figure 2 can be misleading.

For example, within the graphs of per-capita energy or oil consumption, two regions may appear to have quite

similar consumption patterns over time. However, relative to income growth, their consumption patterns may

be quite different between regions.

To highlight such differences, we plot in Figure 3 the 1971-93 time-paths of per-capita energy

consumption vs. income, for each of the six regions; the circular marker depicts the 1993 values. Figure 4

is a similar graph for per-capita oil consumption vs. income. The axes are scaled logarithmically, which

allows for the two order-of-magnitude differences among regions. Logarithmic scales also facilitate

percentage comparisons across regions of oil and/or income growth. Movement parallel to the dashed,

diagonal lines indicates equi-proportional changes in oil and income.

In all regions except OPEC & Figure 3. Energy Consumption vs. Income, Per-Capita,

Mexico, energy consumption has 1971-935

increased in rough proportion to 4 OECDin China where ~~E.Eur. OC

income growth, except in China where 3 & FSU

it has increased more slowly than , 2

income. When income declines, '2

energy consumption decreases in rough ' .s)1 ~~~~~~~OIPEC

proportion; this is most obvious in FSU 0 9Mex.

& EE, as well as in Other LDC. In 06 Chfna LDCOtC~~~~LC

OPEC & Mexico, energy consumption J 05 / f /.9 04 other

has increased continuously, almost Asia

regardless of income growth or decline. CL

The effects of the 1973-74 and 1979-80 02

oil price increases are obvious only in

the OECD, where we see the effects of 01

energy conservation after the 1979-80 per-capita income, 1971-93 (1987 S)

oil price increases. __---Relative to their income levels, China and FSU & EE have extremely high levels of energy

consumption, indicating relatively high energy intensity. China's 1993 income equals that of Other Asia in

1971, but its energy consumption is three times as great. Likewise, energy consumption levels in FSU & EE

are comparable to those in the OECD even though their income levels are only one-fifth as large.

9

In Figure 4 the differences Figure 4. Oil Consumption vs. Income, Per-Capita, 1971 93

across regions in the oil consumption 3 . OECD

vs. income relationship are similar to 2-

those in Figure 3 for energy. Oil

consumption in Other Asia has grown , . U7E.Eur. f90 &FSU

about as rapidly as income during _ 0.706 NCOPEC

1971-93. Similarly, in both Other a,> 0.5 &rt &Mex. p0.4~~~~~~1LDC and in FSU & EE there have been h-eC

03 ~~~~LDCyears when oil consumption has 0

~02oteincreased in rough proportion to . Other

income growth; but more recently, 0- Chhina010

there have been periods when oil 0 0 X0.7

conrsumption has declined in proportion 0 06

0 05

to income declines. In contrast to those 004 DN |

reductions in oil consumption when , v /per-capita income, 1971-93 (1987 $)

income declines, OPEC & Mexico __ _ _ _ _ _ ._

have continued to increase oil

consumption in spite of declining income. For the OECD, there has been slow but steady growth in income,

with sharp declines in oil demand after the 1979-80 price increase; these demand reductions were not reversed

by the oil price collapse of the 1980s. At the other extreme, in terms of low income and oil consumption, is

China; its income has grown rapidly for nearly two decades but oil consumption has not increased nearly as

fast.

We next show the fuel composition of modern energy consumption (oil, natural gas, coal, nuclear,

hydro) for each of these six regions (Figure 5). We see that the various regions' energy consumption show

quite different fuel shares. OPEC & Mexico have the highest shares for oil and for natural gas, which is not

surprising given their natural resources. China has the highest share of coal in energy consumption, also

reflecting its resource base. Other regions' energy consumption is more diversified. Nuclear power is

important in the OECD, and hydro power is important in only a few countries, primarily in South America.

10

Figure 5. Energy Consumption by Fuel: 1971-93 (million tons oil equivalent)

5000 2000

hydro hi nuclear OECD 7 hyer EE & FSU

coal * coal4000 g.: gas

oil o1500 oi

3000

w uJ0 . 01000

E~~~~~~~~~~. E .

2000

1000 OIL 5 OIL

I 0~~~~~~~~~~~~~~~~I

ol T| r .| L 1|1971 1976 1981 1986 1991 1971 1976 1981 1986 1991

600 1 - 800 r_

hy hydro

5 nuclear OPEC & Mexico 700uclear5oo E coal Ucoal C in

M gas 9 C igasnoil 600 oil

400 5500

w ul0 300 0 400

200 300[ "

OIL 200

100100

1971 1976 1981 1986 1991 1971 1976 1981 1986 1991

700 400 -- _ __ _ ______ ___

hydro~~~~~~~~~~~~~~~~~~-r6 dr/2 39 h hd; Other LDC<H nu.clear 350 5nuclear

600 M coal c.

gas gas

500 oil Other Asi 300

250

400

0 0 200

300

150

20000 ~~~~~~~~~~~~~~~~~~100 OIL

100 f,,., - OIL so50

0 0 '6 ' '1 '1971 1976 1981 1986 1991 1971 1976 1981 1986 1991

3. Data for 37 Developing Countries:

Income, Population, Energy, and Total Oil Consumption

In this section we describe data for 37 developing countries, for the period 1971-93. We first present

1993 snapshots of income, energy consumption, and oil consumption -- each relative to population. We then

compare changes from 1971 to 1993 in income, energy consumption, oil consumption, and in oil's share of

energy and of electricity generation. Finally we compare across countries the changes in income with the

changes in energy consumption from 1971 to 1993, and then with the changes in oil consumption. We find

that these 37 countries are extremety heterogeneous, especially in comparison with the industrialized countries'

relative homogeneity.

These 37 countries had the largest oil consumption levels in 1993 outside the OECD and FSU & EE.

They represented 69% of the world's population in 1993; the ten largest constituted 58%, and the twenty

largest constituted 66%. Given that future growth of energy and oil demand will be driven primarily by

growth in population and income, and given that these 37 countries have relatively high growth rates for both

variables, it is important to focus on them. Of course, large changes in end-use prices could significantly

affect demand.

3.1 1993 Snapshots: Heterogeneity across Countries

First we present 1993 "snapshots" of the main variables of concern for these 37 countries: income,

population, energy consumption, and oil consumption. The data are presented in Table 1. As we see in the

graphs below, these 37 countries are a very heterogeneous group. Their per-capita levels of the key variables

-- income, energy consumption, and oil consumption -- vary by two orders of magnitude.

12

Table 1. Levels for Oil and Energy Consumption, Income, and Population for 1993

Oil Energy Income Population(million (million tons (billions (millions)

l tons) oil-equivalent) 1987 US $)ALG: Algeria 8 27 66 27

ARG: Argentina 22 49 126 34

BAN: Bangladesh 2 13 22 115

BRA: Brazil 70 155 299 156

CHI: Chile 7 15 32 14

CHN: China 141 785 425 1178

COL: Colombia 12 27 46 36

ECU: Ecuador 5 7 13 11

EGY: Egypt 20 35 40 56

HON: Hong Kong 7 14 63 6

IND: India 63 273 346 898

INS: Indonesia 38 104 112 187

IRA: Iran 56 92 179 64

IRQ: Iraq 20 21 16 19

ISR: Israel 9 14 52 5

JAM: Jamaica 3 3 4 2

JOR: Jordan 4 4 7 4

KEN: Kenya 2 11 9 25

KUW: Kuwait 6 11 14 2

LIB: Libya 7 14 5

MAY: Malaysia 16 34 52 19

MEX: Mexico 82 120 164 90

MOR: Morocco 6 8 22 26

NIG: Nigeria 12 43 38 105

PAK: Pakistan 13 37 46 123

PER: Peru 6 12 23 23

PHI: Philippines 14 27 40 65

SAF: South Africa 14 92 85 41

SAR: Saudi Arabia 48 82 98 17

SIN: Singapore 15 19 33 3

SKO: South Korea 77 124 214 44

SYR: Syria 11 14 15 14

TAI: Taiwan 29 58 149 21

THA: Thailand 25 58 90 58

TUN: Tunisia 4 6 12 9

UAE 7 23 32 2

VEN: Venezuela 17 47 57 21

13

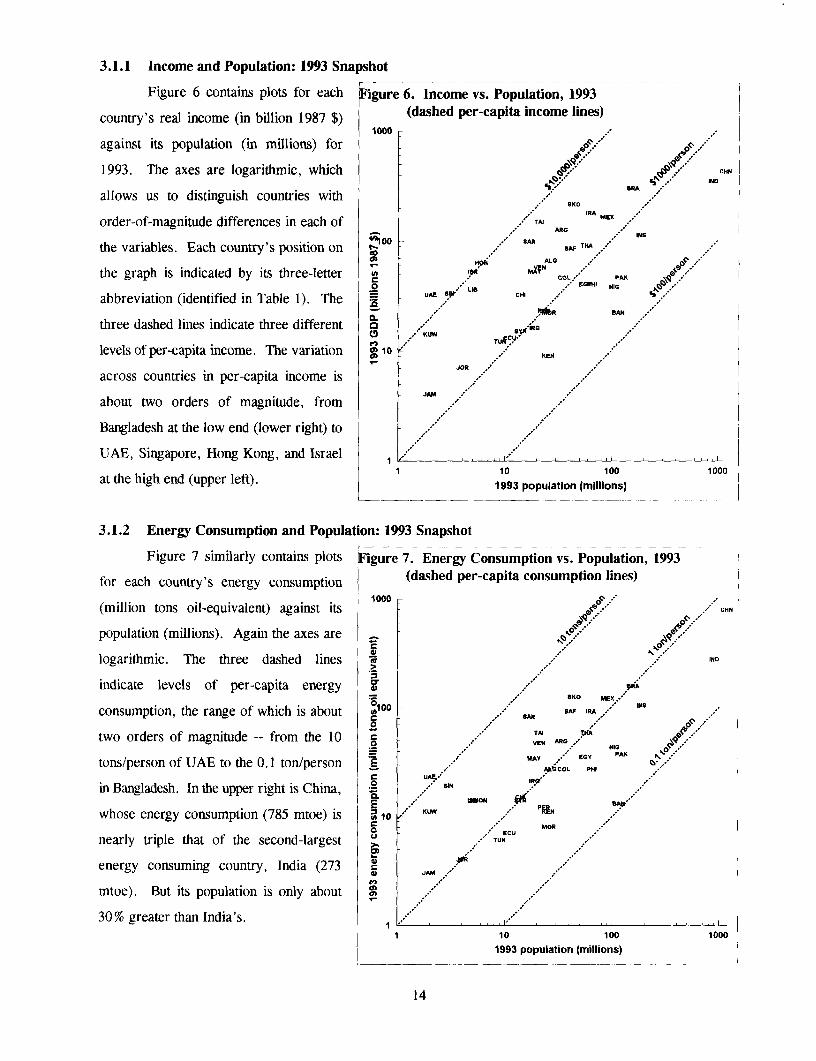

3.1.1 Income and Population: 1993 Snapshot

Figure 6 contains plots for each Figure 6. Income vs. Population, 1993

country's real income (in billion 1987 $) (dashed per-capita income lines)1000 .:.

against its population (in millions) for

1993. The axes are logarithmic, which cirn iBRA

allows us to distinguish countries with SKO HA,

order-of-magnitude differences in each of _A.I ;

'~~~'1O0 . B~~~~AR G

the variables. Each country's position on S A, THmACD ~~~~~~~~~ALG

the graph is indicated by its three-letter to COL. PAK/ IG /

UAE SrLIS CHIi N*.abbreviation (identified in Table 1). The _UAE L

6L R.4k BANthree dashed lines indicate three different A

4., G~~~~~~TIC'

levels of per-capita income. The variation 10 - KEN

JOR

across countries in per-capita income isJAM

about two orders of magnitude, from

Bangladesh at the low end (lower right) to

UAE, Singapore, Hong Kong, and Israel ____*_,_l_,_l__

at the high end (upper left). 1 10 100 10001993 population (millions)

3.1.2 Energy Consumption and Population: 1993 Snapshot

Figure 7 similarly contains plots Figure 7. Energy Consumption vs. Population, 1993

for each country's energy consumption (dashed per-capita consumption lines)

(million tons oil-equivalent) against its 1000 -s, .. CHN

population (millions). Again the axes are

logarithmic. The three dashed lines IND

indicate levels of per-capita energy ,pAe

consumption, the range of which is about IA1 0 0 . S SA IRA INS

two orders of magnitude -- from the 10 C . VEH ARr, NAPVEN R~~~~IG

tons/person of UAE to the 0. 1 ton/person |E .- aklCOL PHI:*

in Bangladesh. In the upper right is China, l SIN

whose energy consumption (785 mtoe) is 10 KUW "INC . MOR

42 ~~~~~~~/ECUnearly triple that of the second-largest

energy consuming country, India (273 X

mtoe). But its population is only about ;

30% greater than India's. ;.1 10 100 1000

1993 population (millions)

14

3.1.3 Oil Consumption and Population: 1993 Snapshot

Figure 8 contains plots for each Figure 8. Oil Consumption vs. Population, 1993

country's 1993 oil demand (in million (dashed per-capita consumption lines)

tons) with its 1993 population (in CHN

millions). Again, the axes are 100 /

logarithmic. The four dashed lines BIRA M IND

indicate four different levels of per- o * /

capita consumption. The variation TAJ / TM

across countries in per-capita oil ES% EGY / \2

.2 SIN IAP A PI

consumption is more than two orders of C. / .P °

magnitude, from Bangladesh at the EIRO UAE LIEl1YP Cl,i

lower right to Singapore at the upper o KLW PNR ,

China, the largest country in

both population and total oil i / .Jam

consumption, has relatively low per- ____ l_lo____ ___

capita oil demand. Bangladesh has 1993 populatIon(millions)

even lower per-capita oil demand; it has

the 7th largest population in this group of 37 countries, but its per-capita oil demand is so low that it ranks 36th

in terms of total oil consumption. At the other extreme, Singapore has a very small population (less than 3

million) but a high level of per-capita oil consumption. Singapore's per-capita oil consumption is more than

twice the average for the OECD; this is due to the fact that oil is the only primary fuel consumed in Singapore

-- they consume no coal, no natural gas, no hydro and no nuclear power.

Another view of these 37 countries' total oil consumption in 1993 is presented in Figure 9. It orders

the countries according to their total oil consumption for 1993. Also shown are the countries' 1971 levels of

oil consumption, which indicates quite varied growth across countries between 1971 and 1993. The top eight

countries stand out, representing nearly two-thirds of total demand for these countries in 1993, and about 18 %

of total world oil demand. The largest growth has been in some Asian countries and in some oil-exporting

countries. The weakest growth has been in Latin American countries and such countries as South Africa and

the Philippines, due to economic and political difficulties.

15

Figure 9. Oil Consumption, 1993 and 1971

(with countries ordered by 1993 oil consumption)

150

125

100

750

E(A 1993 Oi Consu ption

(50

25

0

16

3.1.4 Oil's Share of Energy Consumption and Electric Power Generation: 1993 Snapshots

We now focus on oil's share of energy consumption -- of total modern energy consumption and then

of total energy consumption including biomass -- in the 37 countries, and then oil's share in electric power

generation.

Figure 10 compares the various countries' 1993 fuel-shares of modern energy consumption: coal,

hydro, nuclear, natural gas, and oil. Excluded (until Figure 11) are traditional, biomass fuels such as fuel

wood. The countries are ordered from top to bottom by their oil-share of total modern energy. At the top are

those countries that are the most dependent on oil: Singapore, Jamaica, Jordan, and Ecuador. At the bottom

are those with the lowest oil-share of energy: South Africa, China, Bangladesh, UAE, and India.

It may be surprising that UAE (United Arab Emirates) has such a low oil-share of energy

consumption. However, like many of OPEC's largest oil-producing countries, it consumes substantial amounts

of natural gas, which is not as easily exported as oil, and which helps free-up oil for export. Other such OPEC

members are Algeria, Venezuela, Saudi Arabia, Iran, Kuwait, and Libya.

Several other countries with low oil-shares are heavily dependent on coal, such as South Africa, China

and India; each of these countries have substantial amounts of domestic coal resources. Hydroelectric power

is important in many South American countries, while nuclear power is important in only a few countries, such

as South Korea and Taiwan.

Figure 11 shows an analogous graph of fuel shares of total energy including biomass.6 The countries

are listed in the same order as in Figure 10, which allows us to spot the "outliers". Several of the lowest-

income countries are still heavily reliant on such fuels: Nigeria, Kenya, Bangladesh. China and India are

much less reliant on biomass than are many other low-income countries; they use coal for much of their total

energy: 76% and 60% respectively. Nevertheless, the volume of biomass use in these two countries is

significant.

The third graph of this type, Figure 12, shows 1993 fuel shares of energy used in electric power

generation. The countries are ordered by their 1993 oil-share in electric power. Here we see the special

importance of domestic energy alternatives to oil: coal in South Africa, India, and China; natural gas in

Algeria, Bangladesh, Venezuela; hydro power in Brazil, Venezuela, Colombia, and Chile. In a few coal-

importing countries, such as Hong Kong and Israel, electric power had been generated almost entirely from

oil in 1971, but they shifted to coal-fired electric power generation in the 1980s. Nevertheless, oil is still an

important input for power generation in many developing countries.

6 Given the nature of traditional biomass fuels, the data are only approximated, and are undoubtedlyless accurately measured than the data for modern fuels. Although much biomass consumption bypassesthe market economy, the commercial markets for such fuels can be substantial; for example, their marketsize has been estimated by the World Bank at $5 billion for Africa.

17

Figure 10. Fuel Shares of Modern Energy, 1993

(with countries ordered by 1993 oil share)

* coal 11111 hydro X nuclear E gas II oil

Singapore __ . 7_ Jamaica =_ -- = - _ -=

JordanEcuador

Philippines _________ ________Iraq

Kenya _WIIIIIIIIIIUIIIill -_--1--__--=-Morocco ___ ____= ___7]

Syria _Peru UBUBUIIII U B __ _ = = =

Tunisia . . .

IsraelMexicomi:..

Libya.____ _ ___

Nigeriael ____ _ _ _Egypt .. .... __ __ _____ j

Kuwait iIi......l.lIIlIl.....l.... ___ _ ______

Brazil _111111 Thailand i .=

Iran 1 - ---_ __-- - = ===- -Indonesia 11 __ .-..

Saudi ArabiaChile __

South KoreaMalaysia ..... .................................. ...... .....Colombia ____________________ __ =_ -- 71]

Hong Kong __=__ ___ =Taiwan I _=_ _=

Argentina lIlIX = _ == _ -===177

Pakistan _11111111111; ' * .. = _.________

Aenezuela lIljllljIIllII[._ _:: ::__ -- 11 - -Algeria * ..... .. ......... ..... ..... ... : : ..........

India ; ___=___---__UAE

Bangladesh n lI.. _ _ _China =

South Africa _ I

0 20 40 60 80 1001993 fuel share of modern energy (%)

18

Figure 11. Fuel Shares of Energy including Biomass, 1993

(with countries ordered by 1993 oil share of modern energy)

1 biomass U coal 1111 hydro E nuclear LI gas O oil

Singapore ._ _ _ _ _ ]Jamaica . _ I _

JordanEcuador ____---_--_ - _ ___

Philippines _ - = - -~~ Iraq I _

Kenya I ----_- 7Morocco

Syria 1!1IIPeru flII l__IIIiI LIII .

Tunisia I _ = _Israel fl-I--Zh------ _ _ ]

Mexico 1l -. .=_ _Libya -

NigeriaE-gypt l11[T= _

Kuwait . .. ... ....---.--.-Brazil ll _ ___-= _I

ThailandIra n .. ..... . . ...... ...... .. .. .. f .f .

Indonesia .. 1.17Saudi Arabia ; . ._ =_

Chile =- -------------------

South KoreaMalaysia ii -- - _ - -- == . - 7

Colombia - IIlI-lIlIlI-ILI- ...I1I.....; .___ .--- = -. _ Hong Kong __ __ .i_

Taiwan = - i _i__

ArgentinaPakistan

VenezuelaAlgeria . . -____

IndiaUAE

BangladeshChina

South Africa I __i

0 20 40 60 80 1001993 fuel share of energy including biomass (%)

19

Figure 12. Fuel Shares of Electric Power, 1993

(with countries ordered by 1993 oil share of electric power)

Legend| coal U11 hydro X nuci W gas C oil

Singapore _ _Libya _ I

Jamaica I _ _

Iraq IJordan . =__ J

Philippines lllIlllIlllNlllll 7]Morocco :___

Saudi Arabia , _ _

Mexico EMIDIDIUDlllID, .. ...-Syria iilIlIIIIIiII [____________.__-_ -_ ._ == -

Indonesia -_ _ _ _-Tunisia.._._........

Ecuador _j-l ]Egypt IIIIlIIlI. ::. 1 ... .. !7711i17 .IsraelPeru _ _ _ _ _ _ _ _ _ _ _ _ 7 7 ]Iran .11111 ........ . .... . -=

Pakistan .......................... _____________________________________-__

UE....... ... .. ...... .. .. . . .. ..... ........ ., .... . ...... ...... .. .. . .. _._ . .L

Malaysia . .i . --]Thailand 1 .................. __

Kenya III IIIIIIILIII __Taiwan -- _ X

South Korea o uh wK a i .. . .. . . ... -.-- . .. ..... . ... . .

Nigeria 1.1 .! ... iArgentina IIIIIIIIflIlI lIlIlIlIllH.............. .. ........:

Chile Colombia _l.lluii!ll'll.ii!iiiiiiiiiiiiiiiiiill.ill --

Venezuela .l ..II .....IChina

Bangladesh 11Brazil __ __

AlgeriaHong Kong

India ____________________________X____________

South Africa ',9

0 20 40 60 80 100

1993 fuel share of electric power (%)

20

From these last three graphs, we see the importance of oil in total energy consumption, particularly

with respect to modem fuels. Large amourts of biomass are still consumed in many developing countries, and

the transition to modern fuels is an important consideration for future demand growth. Although oil is less

dominant in power generation, its share is substantially above that for many developed countries.

3.2 Changes from 1971 to 1993: Per-Capita Income, Energy and Oil Consumption --

Heterogeneity across 37 Developing Countries, and in Comparison with OECD Countries

In this section we now focus on the changes over time for these major variables, and observe the

extreme heterogeneity among countries. We summarize the changes between 1971 and 1993 for each of the

37 developing countries in per-capita income, per-capita energy consumption, and per-capita oil consumption.

The data are listed in Table 2, and graphed in several figures below. Each graph plots the 37 countries' 1993

per-capita value against its 1971 per-capita value. Analogous graphs compare the experience of the OECD

countries over this same time period. These graphs -- Figures 13, 14, and 15 -- clearly show the extreme

heterogeneity among developing countries and the relative homogeneity among the OECD countries.

Table Al of Appendix A presents related data for each of the countries: the absolute changes from

1971 to 1993, and the average annual growth rates for per-capita values of income, energy consumption, and

oil consumption.

21

Table 2. Per-Capita Levels of Oil and Enerzy Consumption, and of Income, for 1971 and for 1993

per-capita values of:

Oil (tons/person) EneM. (tons/person) Income ('87$/person)

1971 0 1993 1971 1993 1971 199319711993199

ALG: Algeria 0.14 0 0.31 0.28 0 1.03 1880 0 2456

ARG: Argentina 0.96 0 0.65 1.41 i 1.46 3580 0 3721

BAN: Bangladesh 0.01 0 0.02 0.09 1 0.12 151 i 193I I~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

BRA: Brazil 0.28 0 0.45 0.74 1 0.99 1244 1909

CHI: Chile 0.51 0.52 0.83 1.09 1499 2302

CHN: China 0.05 0 0.12 0.32 0.67 93 I 361I~~~~~~ .

COL: Colombia 0.28 I 0.34 0.59 1 0.77 826 1277

ECU: Ecuador 0.20 0.43 0.38 0.61 692 I 1215

EGY: Egypt 0.17 0.36 0.22 I 0.61 323 713

HON: Honp Kong 0.85 0 1.14 0.86 2.35 3100 10839

IND: India 0.04 0 0.07 0.18 0.30 240 386I. .

INS: Indonesia 0.06 0.21 0.25 0 0.55 232 596

IRA: Iran 0.36 0.87 0.76 1.44 3511 2793

IRQ: Iraq 0.37 0 1.00 0.47 1.10 4644 818

ISR: Israel 1.75 1.82 2.09 2.71 6311 9887

JAM: Jamaica 1.03 I 1.07 1.14 0 1.30 1579 1466

JOR: Jordan 0.32 0 0.86 0.34 i 0.95 1324 i 1714

KEN: Kenya 0.10 I 0.08 0.46 0.44 291 371

KUW: Kuwait 2.14 3.58 7.26 I 6.36 36458 0 7907

LIB: Libya 0.30 1.46 0.80 T 2.70 16411 i 0

MAY: Malaysia 0.39 0 0.84 0.56 I 1.79 1025 0 2752

MEX: Mexico 0.46 0.91 0.72 1.34 1374 1826

MOR: Morocco 0.12 0.24 0.16 ! 0.32 593 857

NIG: Nigeria 0.03 , 0.11 0.26 ! 0.41 378 I 361

PAK: Pakistan 0.05 I 0.11 0.10 i 0.30 202 371

PER: Peru 0.34 0 0.25 0.69 ! 0.53 1231 ! 996

PHI: Philippines 0.20 ! 0.22 0.38 0.42 508 0 610

SAF: South Africa 0.38 0.34 2.10 ! 2.26 2450 0 2097

SAR: Saudi Arabia 0.59 2.80 1.06 4.79 7328 5717

SIN: Singapore 1.10 I 5.29 1.40 i 6.82 3042 11961

SKO: South Korea 0.31 1.74 0.63 2.81 1058 4859

SYR: Syria 0.35 0.78 0.42 ! 1.03 676 1127

TAI: Taiwan 0.45 1.39 0.71 ! 2.76 1744 0 7146

THA: Thailand 0.16 0 0.43 0.36 1.00 497 I 1554

TUN: Tunisia 0.24 ! 0.41 0.35 j 0.67 776 I 1401

UAE 0.80 , 3.85 4.18 r 12.66 35256 17832

VEN: Venezuela 0.71 1 0.83 2.07 i 2.25 3197 2742

22

3.2.1 Per-Capita Income: Changes from 1971 to 1993

For each of the 37 developing Figure 13. Average Annual Growth in Per-Capita Income,countries in Figure 13 we plot on th~e 1971-93, vs. Standard Deviation of Annual Growth

1o% - standard deviation ofhorizontal axis the average annual rate annual growth of

per-capita income of growth in per-capita income from UAE ecA incom

SRY

1971 to 1993, and on the vertical axis BAR 8% JO

ion

the standard deviation of annual growth LDCin per-capita income. A similar graph ECU

PER 8

% cmecontains plots of the same variables for MG

the OECD countries. , mu CHNN

In contrast to the modest but VEN MOR TUNE HON4% v EKO

KEN G

steady income growth of the OECD ItO MAY SIN

countries, the income performance of lamT

the 37 developing countries has been 2% cot Pe

very mixed. Their growth rates and

standard deviation of growth rates are I l l-4% -2% 0% 2% 4% 6% 8%

widely dispersed. One-third of them j average annual growth, per-capita income

have negative growth in per-capita

income. The standard deviation of 10% standard deviation ofannual growth of

their annual growth rates ranges per-capita income

widely, from 2% to 10%.8%

In contrast, the OECD

countries in the bottom graph are

clustered together. The countries have e%

each experienced steady growth in per-

capita income: average annual growth

of about 1-3 %, and a standard deviation 4% ict OECDof the annual growth rate of 2-4%. 2% Tur

SP40SAR ~~Ire2% SVE N?~orJpnl

I [ I II I4% -2% 0% 2% 4% 6% 8%

average annual growth, per-capita income

23

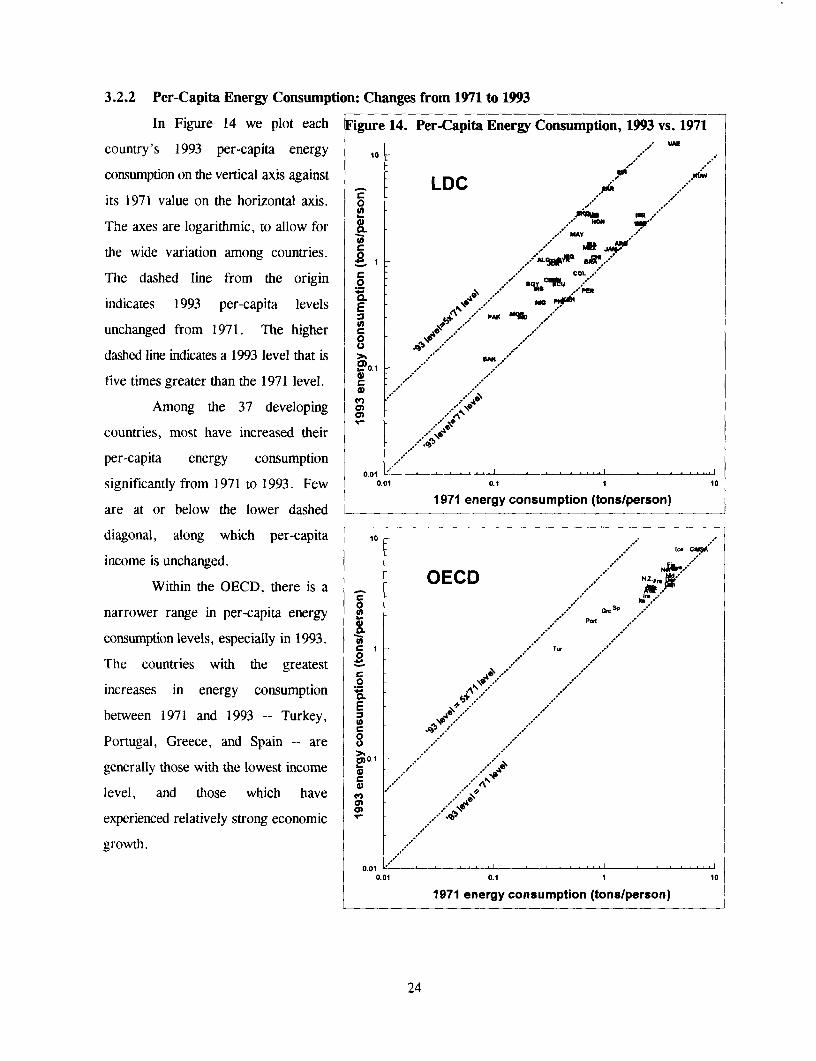

3.2.2 Per-Capita Energy Consumption: Changes from 1971 to 1993

In Figure 14 we plot each Figure 14. Per-Capita Energy Consumption, 1993 vs. 1971

country's 1993 per-capita energy .O : UN

consumption on the vertical axis against LDC .'f

its 1971 value on the horizontal axis. o

The axes are logarithmic, to allow for Wm

the wide variation among countries. A *WM J*JAq

The dashed line from the origin o -C/"

indicates 1993 per-capita levels E

unchanged from 1971. The higher -

dashed line indicates a 1993 level that is c.MM

five times greater than the 1971 level. r_

Among the 37 developing av

countries, most have increased their

per-capita energy consumption001

significantly from 1971 to 1993. Few 0.01 01 1 10are aorblwtelw1971 energy consumption (tons/person)

are at or below the lower dashed l _________ ____ ____________

diagonal, along which per-capita 10 -

income is unchanged. _ ,

Within the OECD, there is a O0.narrower range in per-capita energy G'f ,,3p ff

consumption levels, especially in 1993. o

0The countries with the greatest _ e4i,f

increases in energy consumption tE

between 1971 and 1993 -- Turkey, 0Portugal, Greece, and Spain -- are o

generally those with the lowest income 2' ,4i

level, and those which have

experienced relatively strong economic

growth.

0.01 . .,.0.01 0.1 10

1971 energy consumption (tons/person)

24

3.2.3 Per-Capita Oil Consumption: Changes from 1971 to 1993

Analogously, in Figure 15 we Figure 15. Per-Capita Oil Consumption, 1993 vs. 1971

plot the changes in per-capita oilKIM

consumption (total oil products) from LDC1971 to 1993. For most countries, per- c

capita oil consumption has increased. 2' lqrN.

In several countries, it has increased A .

nearly fivefold. Some of these _ THAEc4uRA,

.2 p. RO c.Acountries are oil exporters, such as E MoR PH ER

ESaudi Arabia and UAE, but others are

oil importing countries that have ° 0.1

0experienced rapid economic growth, o

such as South Korea and Singapore. -

For those countries whose per-

capita demand has not increased0.01

between 1971 and 1993, most have 00.1971 oil consumption (tons/person)

experienced stagnant or declinng per-

capita income: Kenya, Peru, 10

Argentina.

Within the OECD, in contrast, OECDper-capita oil consumption has 0 jin je

generally remained constant or .

declined. Only in Turkey, Portugal, o.",

Greece, and Spain (again, as for C.2~

energy) has per-capita oil consumption EIn~~~C

increased significantly. These are the o001

countries within the OECD where o

incomes are lowest and the economies ,.

less developed.

0.01 .10.01 0.1 1 10

1971 oil consumption (tons/person)

25

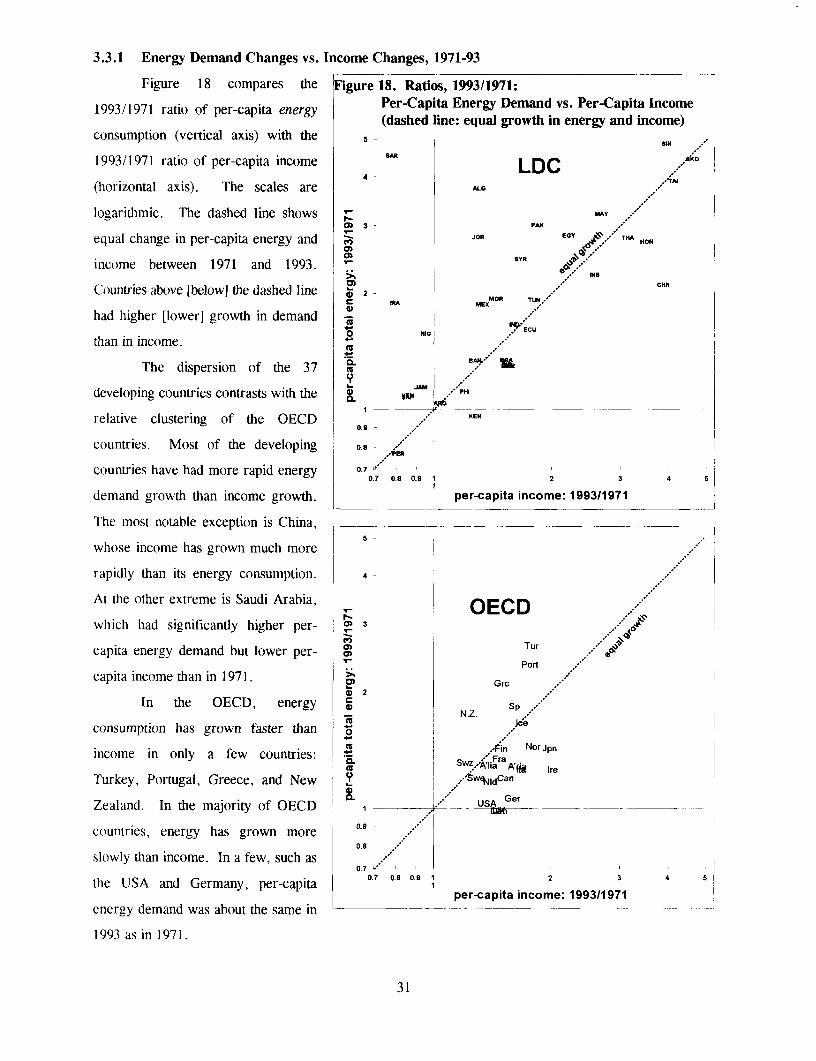

3.2.4 Oil's Share of Energy Consumption and Oil's Share of Electric Power Generation

Figure 16 compares oil's share Figure 16. Oil's Share of Energy Consumption, 1993 vs. 1971

of (modern) energy consumption in 1AOR

1993 vs. 1971, first for the 37 M -R Es MORRQ . KEN

developing countries and then for the

OECD countries. LDC T.N49R

Among the LDC there is > KUW A"' ETy

substantial dispersion, both in oil's 20-.MC6)CO MAY

1971 share and also in the change in o ,/ TAI HON

oil's share from 1971 to 1993. Some XPA

countries were very dependent on oil in EN ALC

1971 but much less dependent by 1993: o5 .A BAN

Hong Kong, Malaysia, Argentina and 0.2

Bangladesh. Some were as dependent

in 1993 as in 1971: Singapore, Jordan,0

Jamaica. In some oil-exporting 0 0o2 0.4 0.8 0.8 I

I ~~~~~oil's share of energy, 1971countries, oil's share of energy [increased (Libya, Kuwait). In others it

declined (Algeria, Venezuela,

Indonesia), perhaps the result of |

OPEC's quotas applying to production

and not exports. In the two most 0. OECDpopulated countries, China and India, C P.a

oil's share was low in 1971 and has z ... t

remained low. S Jp Swz

In contrast, the OECD Tu *'fiN

C) ,,,. A'ria Den

countries are relatively homogeneous, 0.4 USAJK Fra

both in oil's 1971 share of energy, and NZ. Fin Swe

in the reduction of oil's share by 1993.0.2 -

In virtually all these countries, oil's

share was in the range of 40% to 80%

in 1971. By 1993 it was reduced by0 0.2 0.4 0.6 0.8 1

about one-third, to the range of 30% to oil's share of energy, 1971

60%.

26

The LDC thus exhibits greater dispersion across countries, in all dimensions: the shares in 1971, the

shares in 1993, and the changes from 1971 to 1993 -- in both direction and magnitude.

Figure 17 compares oil's share Figure 17. Oil's Share of Electric Power Generation,

of electric power production in 1993 1993 vs. 1971

vs. 1971. There has been, and/ JOR

continues to be, wide variation across