WELCOME - s22.q4cdn.com · 2018. the most exciting time in tech history. nvidia gpu. gaming. pro...

70

2018 Simona Jankowski, March 27, 2018 WELCOME

Transcript of WELCOME - s22.q4cdn.com · 2018. the most exciting time in tech history. nvidia gpu. gaming. pro...

2018

Simona Jankowski, March 27, 2018

WELCOME

20182018

SAFE HARBORForward-Looking Statements Except for the historical information contained herein, certain matters in this presentation including, but not limited to, statements as to: our growth and growth drivers; our market opportunities and TAM; the benefits, impact, and performance of: cinematic games, autonomous vehicles, AI, and our products, technologies, services, and programs; every vehicle being autonomous; the challenges to production of AI cars; our production roadmap and schedules; eSports, social, and the growth of gaming; projected three-year datacenter operating expenses; projected exaflops growth; our intended fiscal 2019 capital return; our strategies; market trends; future financial results, estimates and forecasts; and other predictions and estimates are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements and any other forward-looking statements that go beyond historical facts that are made in this presentation are subject to risks and uncertainties that may cause actual results to differ materially. Important factors that could cause actual results to differ materially include: global economic conditions; our reliance on third parties to manufacture, assemble, package and test our products; the impact of technological development and competition; development of new products and technologies or enhancements to our existing products and technologies; market acceptance of our products or our partners’ products; design, manufacturing or software defects; changes in consumer preferences and demands; changes in industry standards and interfaces; unexpected loss of performance of our products or technologies when integrated into systems and other factors. For a complete discussion of factors that could materially affect our financial results and operations, please refer to the reports we file from time to time with the SEC, including our Form 10-K for the fiscal period ended January 28, 2018. Copies of reports we file with the SEC are posted on our website and are available from NVIDIA without charge. These forward-looking statements are not guarantees of future performance and speak only as of March 27, 2018, based on information currently available to us. Except as required by law, NVIDIA disclaims any obligation to update these forward-looking statements to reflect future events or circumstances.

Financial Measures This presentation contains historical revenue amounts for certain of our market platforms and businesses which provides investors with additional information to supplement the segment reporting information contained in our Form 10-K for the fiscal year ended January 28, 2018. In addition to U.S. GAAP financials, this presentation includes certain non-GAAP financial measures. These non-GAAP financial measures are in addition to, and not a substitute for or superior to, measures of financial performance prepared in accordance with U.S. GAAP. See our website for a reconciliation between each non-GAAP measure and the most comparable GAAP measure. Where we present non-GAAP financial measures, including non-GAAP gross margin, non-GAAP gross margin without IP, non-GAAP operating expense, non-GAAP operating income, non-GAAP operating margin, non-GAAP EPS, and free cash flow we generally exclude stock-based compensation, legal settlement, acquisition-related items, restructuring and other charges, product warranty charge, the associated tax impact, provisional tax benefit from tax reform, and other expense, where applicable.

20182018

AGENDA

Jensen Huang

Shanker Trivedi

Rob Csongor

Jeff Fisher

Colette Kress

All

Rise of GPU Computing

Datacenter

Automotive

Gaming

Financials

Q&A

Questions? Please email [email protected]

2018

Jensen Huang, CEO

NVIDIA

2018

THE MOST EXCITING TIME IN TECH HISTORY

NVIDIA GPU

GAMING PRO VIZ DATACENTER AUTONOMOUS VEHICLES

2018

Shanker Trivedi, March 27, 2018

DATACENTER

20182018

HIGHLIGHTS

Volta chosen by all major server OEM/ODMs and all major public clouds

2,000 customers adopt NVIDIA inference platform

86 of Top 500 Supercomputers NVIDIA Tesla Accelerated

Top 15 HPC Apps Accelerated; 550 accelerated apps

CUDA developers up 75% YoY to 770K

2018: A GREAT YEAR

FY 2018FY 2016

$339M

$1,932M

133%

$830M

145%

FY 2017Source: NVIDIA

$MDATACENTER REVENUE

20182018

BIG GROWTH OPPORTUNITY$50B Total Addressable Market (TAM)

HYPERSCALE & CONSUMER INTERNET

$20B

HIGH PERFORMANCE COMPUTING

$10B $20B

CLOUD COMPUTING& INDUSTRIES

Source: NVIDIA

20182018

NVIDIA PLATFORM EVERY MAJOR CLOUDEVERY MAJOR COMPUTER MAKER

DEVELOPERS

AMBER

ANSYS

ANSYS FLUENT

BLAST

GAMESS

Gaussian

GROMACS

LAMMPS

LS-DYNA

NAMD

OpenFOAM

Quantum Espresso

Simula Abaqus

VASP

WRF

AI FRAMEWORKS DATA ANALYTICS

H20

Kinetica

MapD

MatLab

ENTERPRISE Adobe

ANSYS

Dassault

GE

IBM

SAP

SAS

Schlumberger

APPS & FRAMEWORKS

SOFTWARE

VERTICAL SOLUTIONS

TESLA, DGX

GPU & CUDA

DEVELOPERS

USERS

TOP 15 HPC

NVIDIA DATACENTER STRATEGY

Source: NVIDIA

20182018

APPLICATIONS

NVIDIA AI DRIVE: AUTONOMOUS VEHICLES

METROPOLIS: SMART CITIES

CLARA: HEALTHCARE

SOFTWARE, SDKS, ENGINES, LIBRARIES, OS

CUDA & GPU COMPUTING ARCHITECTURE

DATACENTER PLATFORM

HPC FRAMEWORKS ENTERPRISE DATA ANALYTICS VISUALIZATION

cuDNN TensorRT cuBLAS cuSPARSE OpenACC DCGMcuFFTDeepStream

TESLA DGX

vGPU KONG*

NVIDIA GPU CLOUD

DEEP LEARNING HIGH PERFORMANCE COMPUTING DATA CENTER MGMT

*Kubernetes on NVIDIA GPUs

INDUSTRY VERTICAL SOLUTIONS

20182018

1,200

2,800

FY17 FY18

Inception Startups (Companies)

125

550

FY17 FY18

Enterprise DGX Customers

400

550+

FY17 FY18

GPU Ready Apps (Units)

280K

840K

FY17 FY18

Training – cuDNN (Downloads)

DEVELOPER ECOSYSTEM

HYPERSCALE &CONSUMER INTERNET

CLOUD COMPUTING &INDUSTRIES

HIGH PERFORMANCE COMPUTING

200K

350K

FY17 FY18

Accelerated Computing Developers

70

30K

FY17 FY18

Inferencing – TRT (Downloads)

Mainstream Adoption AI Leadership Rapid Growth

75%

37%

200%

∞

133%

340%

Source: NVIDIA

20182018

GPU ACCELERATED DATACENTER VALUEThe More You Buy, the More You Save

WORKLOAD BASELINECPU-Only

HPC(Amber, LAMMPS,

NAMD, VASP)

AI TRAINING(Caffe2, TensorFlow,

MXNet)

AI INFERENCE (Image, Speech,

Translation)

Speed Up 1X 20X >100X 60X

Servers 5,000 250 <50 84

Capex $45M $11M $7.5M $7M

3 Year Opex(Power + Cooling) $19.5M $2.5M $1M $1.5M

TCO Savings N/A 79% 86% 86%

Note(s): CPU Baselined to 5000 Servers for each workload | Capex Costs: CPU node with 2x Skylake CPU’s ~$9K; GPU node with 4x V100 GPU’s ~$45K | Opex Costs: Power & cooling is $180/kW/month | Power: CPU server + n/w = 0.6 KW; GPU server + n/w = 1.6 KW; DGX-1V/HGX-1 Server = 3.2KW | HPC: GPU node with 4xV100 compared to 2xCPU Server | DL Training: DGX-1V compared to a 2xCPU server | DL Inference: HGX-1 based server (8xV100) Compared to 2x CPU Server |numbers rounded to nearest $0.5M

Source: NVIDIA

20182018

LEADERSHIP MILESTONES$10B TAM

102 Top 500 Systems accelerated, 86 NVIDIA systems

Public sector investment in AI and exascale

Top 15 apps, 70% of top 50 HPC apps accelerated; total 550

2,328 scientific computing papers citing GPUs compared to 1,276 in

FY17

HIGH PERFORMANCE COMPUTINGTo Exascale, and Beyond

0

5

10

15

20

25

30

EXAP

LOPS

Top 500 Rest of HPC

2017 2023

Source: NVIDIA, arXiv, PubMed

20182018

APPLICATIONS LEADERSHIP

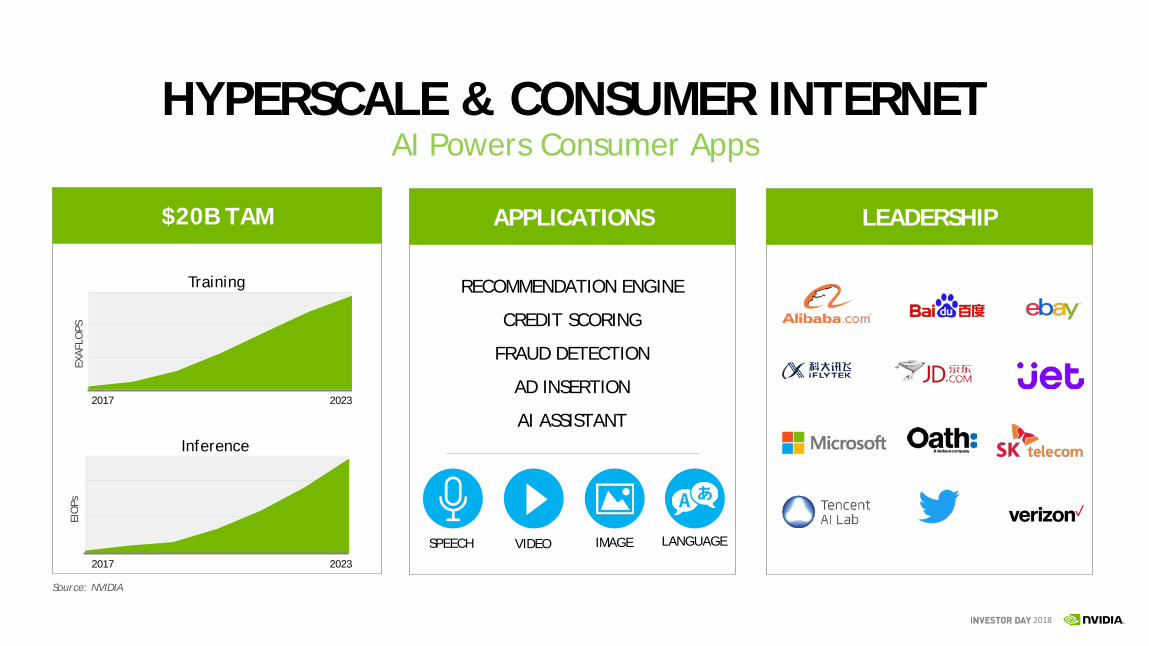

HYPERSCALE & CONSUMER INTERNETAI Powers Consumer Apps

EXAF

LOPS

Training

EIO

Ps

Inference

2017 2023

RECOMMENDATION ENGINE

CREDIT SCORING

FRAUD DETECTION

AD INSERTION

AI ASSISTANT

2017 2023

$20B TAM

Source: NVIDIA

SPEECH VIDEO IMAGE LANGUAGE

2018

HYPERSCALE & CONSUMER INTERNETGPUs Best for Deep Learning Training

Increasing Complexity of DNNs Top 10 Hyperscale/Consumer Internet

0

1

2

2015 2016 2017

ExaF

LOPS

FY 16 FY 17 FY 18

Source: NVIDIA

20182018

HYPERSCALE & CONSUMER INTERNETAI inference opportunity – 30M Hyperscale Servers

190XIMAGE - CNN

ResNet-50 with TensorFlow Integration

50XNLP - RNN

GNMT

45XRECOMMENDER - MLP

Neural Collaborative Filtering

36XSPEECH SYNTH - DGN

WaveNet

60XSPEECH RECOG – RNN++

Deep Speech 2 DNN

Sep ‘16 April ‘16 Sep ‘17 April ‘18

TensorRT 2INT8

TensorRT 3Tensor Core

TensorRTCNNs

TensorRT 4

TensorFlowIntegration

KaldiOptimization

ONNXWinML

Source: NVIDIA

AI Inferencing is a Large Opportunity: 30M+ Hyperscale Servers

20182018

LEADERSHIP MILESTONES$20B TAM

CLOUD COMPUTING & INDUSTRIESAI Transforming Every Industry

Healthcare

Transportation

Manufacturing

Public Sector

Oil & Gas

Future Industries

Startups

Industry BreakdownVolta chosen by all major

public clouds

$5B in funding for 2,800 NVIDIA Inception Startups

Top segments include: Healthcare, Transportation, AI City

Over 2,000 companies using NVIDIA GPU Cloud (NGC)

Source: NVIDIA

20182018

STARTUPS COMPANIESRESEARCH

AI REVOLUTIONIZING MEDICAL IMAGING$100B Market: $35B Instruments, $5B Imaging Software

0%10%20%30%40%50%60%

2014 2015 2016 2017

SPIE ISBI MICCAI

Medical Imaging Papers Using Deep Learning

FDA approved AI for Medical Imaging

Dedicated supercomputer for AI Pathology

300 NVIDIA Inception Members

-

10

20

30

40

50

60

$-

$200

$400

$600

$800

Healthcare AI Financing History

Disclosed Funding ($M) DealsH1 2012 H1 2017

Source: NVIDIA, CB Insights

20182018

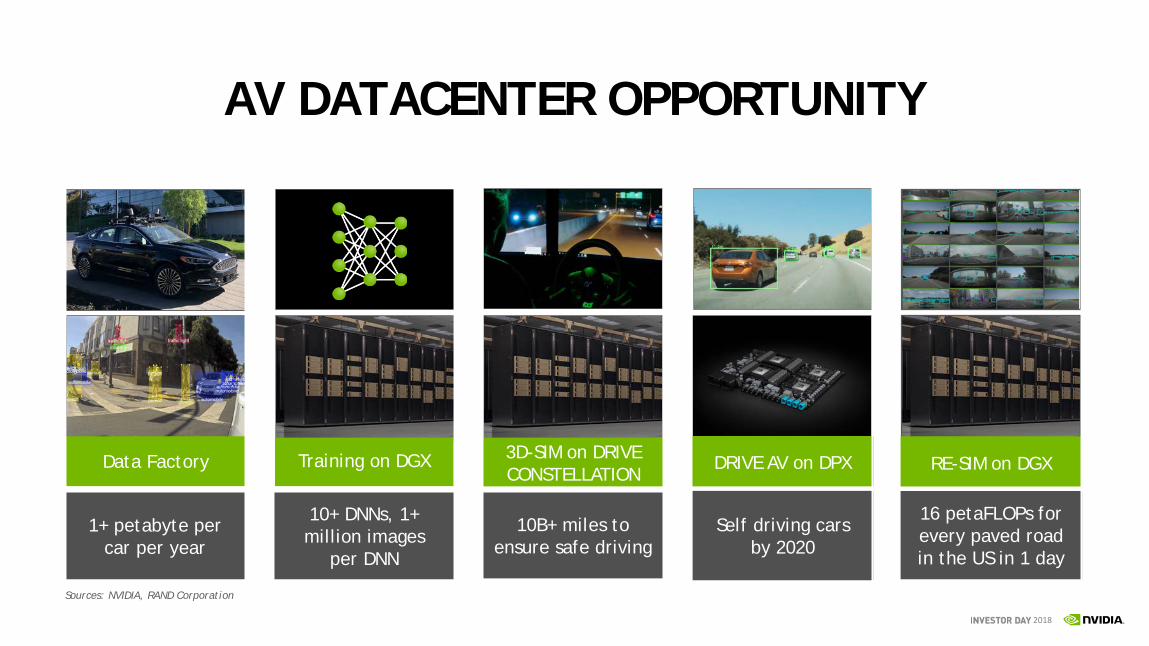

AV DATACENTER OPPORTUNITY

16 petaFLOPs for every paved road in the US in 1 day

RE-SIM on DGX

10B+ miles to ensure safe driving

3D-SIM on DRIVE CONSTELLATION

10+ DNNs, 1+ million images

per DNN

Training on DGX

1+ petabyte per car per year

Data Factory

Self driving cars by 2020

DRIVE AV on DPX

Sources: NVIDIA, RAND Corporation

20182018

DATA CENTER SUMMARY

HYPERSCALE &CONSUMER INTERNET

$20B

HIGH PERFORMANCE COMPUTING

$10B

CLOUD COMPUTING& INDUSTRIES

$20B

Compelling platform strategy

Leadership in HPC and deep learning training

Large AI inference opportunity

Increasing enterprise adoption

Growing developer ecosystem

Extensible flexible architecture

$50B TAM

Source: NVIDIA

2018

Rob Csongor | March 27, 2018

AUTOMOTIVE

2018

AUTOMOTIVE GROWTH

0

100

200

300

400

500

600

700

FY14 FY15 FY16 FY17 FY18

Mill

ions

15%

$558M

0

100

200

300

400

FY17

Q2

FY17

Q3

FY17

Q4

FY18

Q1

FY18

Q2

FY18

Q3

FY18

Q4

Curr

ent

DPX2 DX

0

100

200

300

400

FY17

Q1

FY17

Q2

FY17

Q3

FY17

Q4

FY18

Q1

FY18

Q2

FY18

Q3

FY18

Q4

REVENUE AI ENGAGEMENTSDRIVE PARTNERS

2018

AV REVOLUTIONIZING $10T INDUSTRYEvery Vehicle Will Be Autonomous

DRIVING TRUCKINGMOBILITY SERVICES

$2.4T MARKET

AV will save lives, $Ms in lost productivity

(3000 lives/day, $0.5T/yr)

$5.3T MARKET

AV will reduce parking footprint, lowering cost of ownership

$2T MARKET

AV will extend the range of truckers, help cover shortage of trucker.

(10% decline from ELD, $500B loss due to accidents)

2018Source: ABI Research

AV IS A $60B OPPORTUNITYEvery Vehicle Will Be Autonomous

L5 — Robo-taxi L4 — Full AV L3 — Partial AV L2 — Human backup

2019 2020 20212018 2035

$60B TAM(2035)120M

vehicles

10M Robo-taxis

100MSDC

$20B

$40BL2 – L5

Shipments

AV REVENUE

Development DRIVE Systems

Development NRE

Training, testing &validation systems

2018

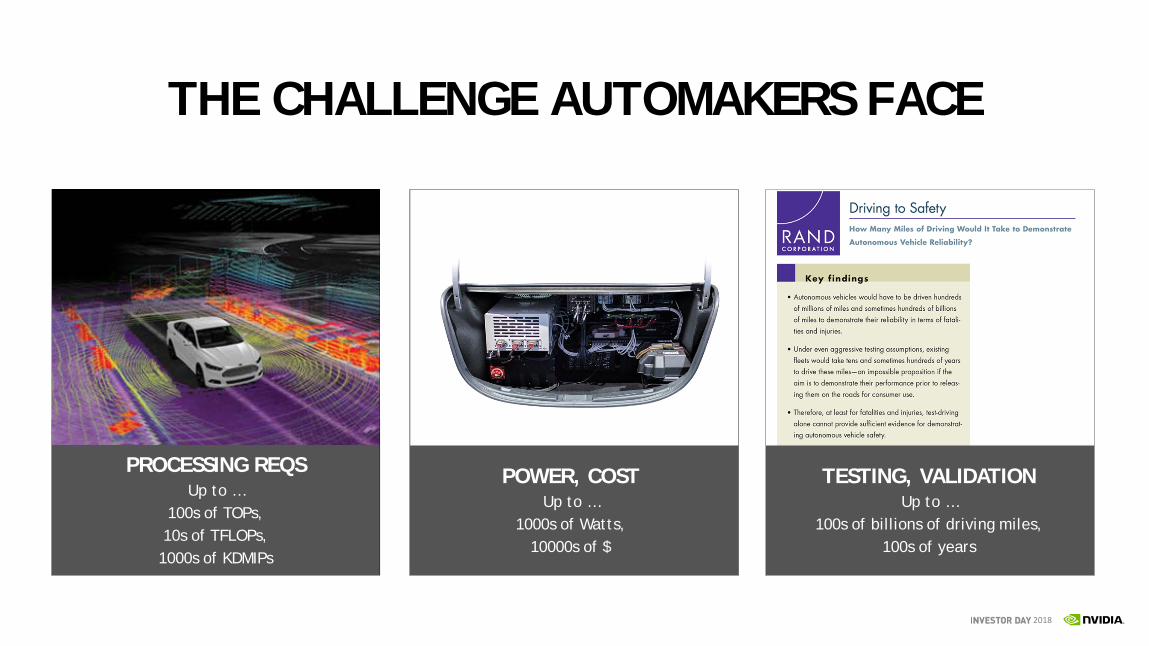

THE CHALLENGE AUTOMAKERS FACE

POWER, COSTUp to …

1000s of Watts, 10000s of $

PROCESSING REQSUp to …

100s of TOPs, 10s of TFLOPs, 1000s of KDMIPs

TESTING, VALIDATIONUp to …

100s of billions of driving miles, 100s of years

2018

AI

The Computing Model for AV

NVIDIA GAME CHANGERSKey Strategies

XAVIER PROCESSOR

One ArchitectureFrom L2 to L5

NVIDIA DRIVEEND-TO-END SYSTEM

Collect DataTrain Models

SimulateDrive

OPEN PLATFORM

370+ PartnerEcosystem

2018

DRIVE Parker

1x Perf

1 Chip

Samples: Now

Production: Now

DRIVE PX 2

20x Perf

4 chips

Samples: Now

Production: Now

DRIVE Xavier

20x Perf

1 chip

Samples: Now

Production: Q1’2019

DRIVE Pegasus

200x Perf

4 chips

Samples: Q3’2018

Production: Q3’2019

ONE SCALABLE ARCHITECTUREL2 through L5 Driving SolutionsONE SW ARCHITECTURE

ORIN

DRIVE Orin

200x Perf

2 chips

2018

DRIVE AV ON XAVIER

2018

FrontRadar

L2 ECU

FrontSurround Camera

SideSurround Camera

SideSurround Camera

SideRadar

ForwardCamera

NCAP ECU

NCAP Camera

SideRadar

Parking ECU

Driving Monitor ECU

Driving Monitor Camera

Rear Radar

RearSurround Camera

TODAY’S ADASFour Separate Computers

Surround ViewECU

2018

FrontRadar

One AI AV Computer

FrontSurround Camera

SideSurround Camera

SideSurround Camera

SideRadar

ForwardCamera

NCAP ECU

NCAP Camera

SideRadar

Driving Monitor Camera

Rear Radar

RearSurround Camera

DRIVE XAVIER VALUEOne Computer — One SW, Lower Cost

2018

ROBO—TAXI DRIVE VALUE

2018

ROBO—TAXI DRIVE VALUE

2018

L5 ROBO-TAXI USE CASE

2x PCs in the Trunk 2x DRIVE PEGASUS

TOPs 330 640

KDMIPs 350 550

GFLOPs 39,000 38,000

Power 3 kw 1/3rd pwr

Size 1x 1/10th size

Cost 1x 1/5th cost

ROBO—TAXI DRIVE VALUE

2018

END-TO-END SYSTEMFrom Training to Testing to Driving

16 petaFLOPs for every paved road in the US in 1 day

RE-SIM on DGX

10B+ miles to ensure safe driving

3D-SIM on DRIVE CONSTELLATION

10+ DNNs, 1+ million images

per DNN

Training on DGX

1+ petabyte per car per year

Data Factory

Self driving cars by 2020

DRIVE AV on DPX

Sources: NVIDIA, RAND Corporation

35

ANNOUNCINGNVIDIA DRIVE SIM AND CONSTELLATIONAV VALIDATION SYSTEM

Virtual Reality AV Simulator

Same Architecture as DRIVE Computer

HIL and PIL Support

Simulate Rare and Difficult Conditions, Recreate Scenarios, Run Regression Tests, Drive Billions of Virtual Miles

10,000 DRIVE Constellations Drive 3B Miles per Year

2018

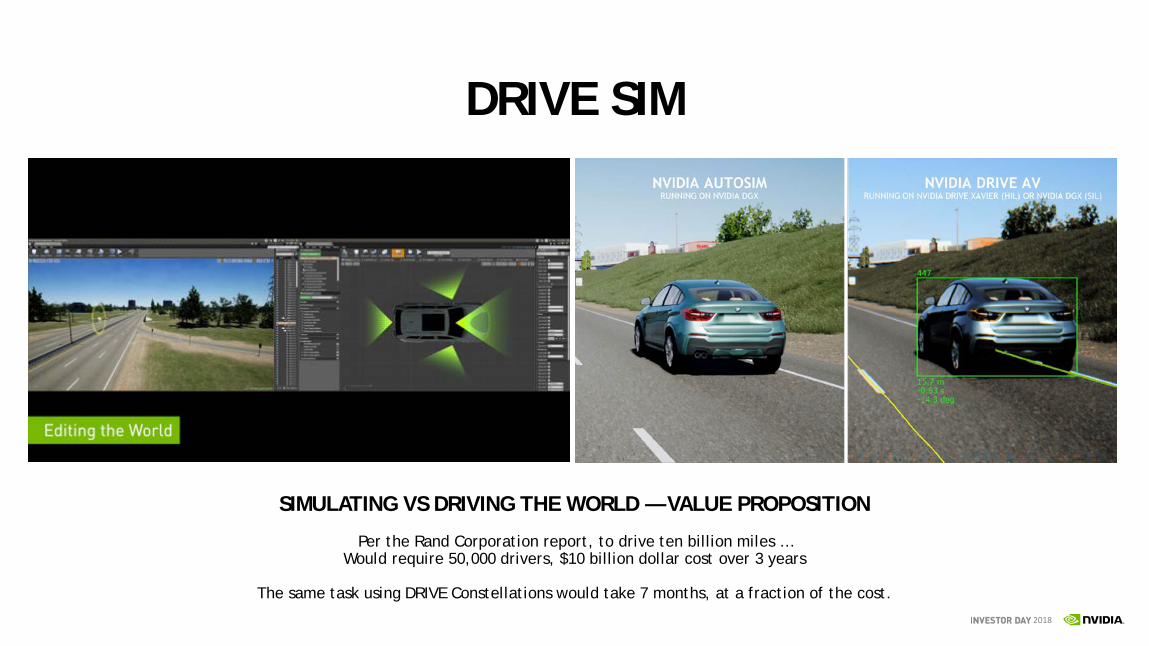

DRIVE SIM

SIMULATING VS DRIVING THE WORLD — VALUE PROPOSITION

Per the Rand Corporation report, to drive ten billion miles …Would require 50,000 drivers, $10 billion dollar cost over 3 years

The same task using DRIVE Constellations would take 7 months, at a fraction of the cost.

2018

THE POWER OF AN OPEN PLATFORM

370+ PARTNERS DEVELOPING ON NVIDIA DRIVE

CARS

TRUCKS

MOBILITY SERVICES

SUPPLIERS

MAPPING

SENSORS

STARTUPS

RESEARCH

2018

KEY ANNOUNCEMENTSProgress This Year

PARTNERSPRODUCTS

VW AI AUDI DEPLOYS ZFASBAIDU APOLLO MERCEDES-BENZ AI

VOLVO / AUTOLIV AURORA CONTINENTAL DEUTSCHE POST DHL

ZF / CHERY TUSIMPLEUBER PACCAR

XAVIER IS HERE DRIVE PEGASUS

DRIVE SIM DRIVE AV

DRIVE IX DRIVE AR

39

SUMMARY

• $0.5B business transitioning to AV – Revenue coming from development systems, NRE, simulating/testing/training systems

• Every vehicle will be autonomous - $60B TAM opportunity by 2035.

• NVIDIA’s Key Strategies - AI, Xavier, end to end system, open platform are game changer strategies for NVIDIA.

• Moment

Every vehicle will be autonomous —$60B opportunity

NVIDIA’s Key Strategies —AI, Xavier, End to End System, Open Platform — are game changers for car makers

Testing & validation for AV —Announcing DRIVE Constellation —AI Validation in the Data Center

The world is building on NVIDIA’s open platform — 370+ partners and growing

2018

2018

Jeff Fisher, March 27, 2018

GAMING

20182018

GAMING HAD A GREAT YEAR

Pascal:1080Ti/1070Ti/Titan Xp

Max-Q Gaming Notebooks

Nintendo Switch Powered by NV

Surpassed 100M GFE Clients

GFN Beta Launched

Crypto Came to Town $0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

FY17 FY18

36% YOY

TOTAL GAMING $M

20182018

WW GAME REVENUE

GAMING IS A HUGE MARKET…AND GROWING

Emerging

GAMERS FOR LIFE

Gam

e Re

venu

e

$B

$20B

$40B

$60B

$80B

$100B

2007 2017

Source: DFC Source: DFC (2007), NewZoo (2017) Source: ESA

2003

2017

3X

0

500

1000

1500

2000

2500

2007 2017

WW GAMERS

3X

Over 35 Yrs OldLess Than 35 Yrs Old

M

2,000M

1,500M

1,000M

500M

Gam

ers

20182018

OPEN PLATFORM DEVELOPERS CHOOSE PC 1000s of GAMES

PC IS WHERE THE ACTION IS

RECORD BREAKING SALES

MOST WATCHED..EVER

0%

10%

20%

30%

40%

50%

60%

PC Phone Console0

2000

4000

6000

8000

2013 2015 2017 PS4

Source: Steam, Twitchstats, SteamSpy, BlueHole Source: GDC Annual Survey 2018 Source: Statista, SteamSpy, GameStop

Gam

es R

elea

sed

on S

team

Eac

h Yr

Gam

e De

velo

pers

Sur

veye

d on

Gam

es in

Dev

elop

men

t

20182018

GEFORCE: WORLD’S LARGEST GAMING PLATFORM

GAMING GPU REVENUE $M

$B

$1B

$2B

$3B

$4B

$5B

FY17 FY18

21% YOY

5Yr CAGR

ASP 11%

UNITS 15%

REV 29%

END MARKET

Emerging+40%

Developed+27%

INSTALLED BASE

Pascal Other

30%

70%

LEADERSHIP

Steam Gamers

VR

GeForce Other

Source: NVIDIA Source: NVIDIA Source: NVIDIA Source: Steam, Oculus

20182018

ESPORTS MOMENTUM FUELS GAMING

Source: Statista, Blizzard & Riot Games

ESPORTS AUDIENCE PRIZE MONEY

86% OF ESPORTS GAMERS PLAY ON GEFORCE

-

50M

100M

150M

200M

250M

300M

350M

400M

2016 2018

eSpo

rts

View

ers

+100M

Tota

l eSp

orts

Tou

rnam

ent

Priz

e M

oney

$M

$20M

$40M

$60M

$80M

$100M

$120M

2015 2017

+70%

M

10M

20M

30M

40M

5/16 8/16 10/16 1/17 4/17 10/17

M

25M

50M

75M

100M

2011 2012 2014 2017

WW

Gam

ers

WW

Gam

ers

Source: NewZoo, esportsearnings.com, NewZoo discrete GPU share of eSports gamers

20182018

SOCIAL EXPANDS GAMING REACH

Source: NVIDIA

GAMES WANT TO SHARE

70% OF GAMERS PLAY GAMES TO BE SOCIAL

Source: Twitchtracker, Discord, Nielsen

0.0M

0.2M

0.4M

0.6M

0.8M

1.0M

Jan 16 Jan 18 CNN

Twitch Concurrent Viewers

GAMERS WANT TO CONNECT

0

20

40

60

80

100

2015 2016 2017

Discord App User Growth

“RISE OF PUBG AND FORTNITE IS GROWING THE GAMING COMMUNITY” - Goldman Sachs

GeForce Weekly Gamers

MOST VIEWED, MOST SHARED GO VIRAL

Total Gamers Playing + 20%

4/17 7/17 10/17 1/18

100M

80M

60M

40M

20M

20182018

GEFORCE EXPERIENCEGAMING PLATFORM

100M Clients WW

Over 1B In-Game Captures in 2017:

800M Game Videos

200M Game Highlights

100M Game Photographs

500M so far in 2018

NVIDIA HIGHLIGHTSNVIDIA ANSEL

2018

CINEMATICS KEEP PUSHING PLATFORM

RAYTRACING GAMES MORE DEMANDING

* Est ASP of Graphics Card (based on Actual GPU ASP)

GAMERS BUY UP

GPU

Per

f Re

quir

ed f

or H

igh

Sett

ings

Source: NVIDIA, Games @ 1080p, High Settings

ASP

$125

$150

$175

$200

$225

$250

$275

$300

FY15 FY16 FY17 FY18

GeForce ASP

$200*

Console ASP

$160*

NVIDIA GPU

NVIDIA® RTX™ Technology

Microsoft DXRNVIDIA GameWorks

Ray Tracing

New Class of Ray Traced Games

0X

1X

2X

3X

4X

5X

2013 2015 2017 2019 2021

RTX4KVR

Console Perf

20182018

Gaming is BIG and Growing

GeForce is Number One Game Platform

Gaming Growth Fueled by Esportsand Social

Cinematic Gaming Needs Bigger GPUs

An Exciting Future

G-SYNC

MAX-Q DESIGNGEFORCE GTX NVIDIA SHIELD

GEFORCE EXPERIENCE

2018

Colette Kress, March 27, 2018

FINANCIALS

2018

RECORDS

Gross Margin, Operating Income and EPS are Non-GAAP measures.

OPERATING INCOME

63%

$2.2B

$3.6B

FY 2017 FY 2018FY 2017 FY 2018

REVENUE

41%

$6.9B

$9.7B

EPS

FY 2017 FY 2018

61%

$3.06

$4.92

GROSS MARGIN

FY 2017 FY 2018

59.2%

60.2%100 BPS

2018

PRO VISUALIZATION3-YEAR CAGR 6%

$ M

illio

ns

$795 $750 $835

0

200

400

600

800

1,000

$934

12%

FY 2015 FY 2017 FY 2018FY 2016

DATACENTER3-YEAR CAGR ~85%

$ M

illio

ns

$317 $339$830

$1,932

0

500

1,000

1,500

2,000

133%

FY 2015 FY 2017 FY 2018FY 2016

AUTO3-YEAR CAGR 45%

$ M

illio

ns

$183 $320$487 $558

0

200

400

600 15%

FY 2015 FY 2017 FY 2018FY 2016

$ Bi

llion

s

FY 2015 FY 2017 FY 2018FY 2016

$2.1 $2.8$4.1

$5.5

0

2

4

636%

GAMING3-YEAR CAGR ~40%

MARKET PLATFORMS

2018

MARKET PLATFORMSDiversified and Growing

PRO VISUALIZATION EMERGING APPLICATIONS

15%

30%

0%

10%

20%

30%

40%

Q4 FY 2018Q4 FY 2017

GAMINGGFE USERS

90M100M

50

70

90

110

FY 2017 FY 2018

Mill

ions

AUTOMOTIVEDRIVE PARTNERS

FY 2017 FY 2018

225

320

100

150

200

250

300

350

DATACENTERHYPERSCALE “7” CUSTOMER REVENUE

$ M

illio

ns

FY 2017 FY 2018

+155%

2018

GROSS MARGIN EXPANSIONValue Added Platforms Expand Margins

Gross Margin excluding IP and Gross Margin are Non-GAAP measures.

52%

54%

56%

58%

60%

62%

64%

0

1

2

3

4

5

6

7

FY 2015 FY 2016 FY 2017 FY 2018

60.2%

59.2%

56.8%55.8%

GM% Value Added Platforms All OtherGM% Excl IP IP

Gro

ss P

rofi

t, $

Bill

ions

2018

GROSS MARGINS BY PLATFORMS

0% 100%

AutoOEM &

Embedded

GPU Gaming

Pro Vis

DataCenter

60.2%

Gross Margin is a Non-GAAP measure.

Company GM% Gross Profit

Gro

ss P

rofi

t, $

Bill

ions

FY 2018 Gross Margin %

2018

$1.7 $1.7

$1.9

$2.2

15%

25%

35%

45%

0.0

1.0

2.0

3.0

FY 2015 FY 2016 FY 2017 FY 2018

19%

OPERATING EXPENSES

Operating Expenses Operating Expenses as a % of Revenue

27%

35%34%

YoY Investments Focused on Gaming, AI, and Auto

Operating Expenses and Operating Expenses as a % of Revenue are Non-GAAP measures.

23%

$ Bi

llion

s

2018

INVESTMENT IN R&DCumulative $15B

0

2

4

6

8

10

12

14

16

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0R&D Investment Cumulative R&D Investment

R&D,

$ B

illio

ns

Cum

ulat

ive

R&D,

$ B

illio

ns

2018

OUR LEVERAGED MODELENGINEERS

HardwareSoftware

BY PLATFORM

Gaming AI Auto

Software ~40%

GPU Architecture ~50%

FY 2018

FY 2018

FY 2013

2018

$1.0 $1.1

$2.2

$3.6

5%

15%

25%

35%

45%

0.0

1.0

2.0

3.0

4.0

FY 2015 FY 2016 FY 2017 FY 2018

OPERATING MARGIN EXPANSION

Operating Income Operating Margin

Operating Income and Operating Margin are Non-GAAP measures.

32%

37%

20%22%

$ Bi

llion

s

2018

CASH AND CASH FLOW

$1.7

$4.0

$6.8

$3.5

$5.1

$7.1

0

2

4

6

8

Cash Flow Net Cash Total Cash

Cash Flow Increased 109%; Net Cash Increased 28%

4.8%

Cash Flow = Cash Flow from Operations; Net Cash = Total Cash – Total Debt; FY 2017 Total Debt = $2.8B; FY 2018 Total Debt = $2.0B; Total Cash = Cash, Cash Equivalents + Marketable Securities

FY 2018 FY 2018 FY 2018FY 2017 FY 2017 FY 2017

10.4%

Cash as a % of Market Capitalization

$ Bi

llion

s

2018

CAPITAL RETURNSince FY 2013: $5B+, 70% FCF

Free Cash Flow is a Non-GAAP measure.

0

400

800

1,200

1,600

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019

$1.25B

Intended Return

$1.0B

Share Repurchase Dividend

$1.0B$1.1B

$147M

$0.8B

$1.25B

$ M

illio

ns

2018OPEX is a Non-GAAP measure.

USES OF CASH

OPEXEngineersSalesInfrastructure

CAPEXDatacentersFacilitiesSoftware license

M&A and Investments

Capital ReturnDividendsShare Repurchases

FY 2018

$ Bi

llion

s

OPEX CAPITAL RETURN

CAPEX

$2.2

$0.6

0.0

0.5

1.0

1.5

2.0

2.5

$1.25

M&A

20182018

Q&A

2018

SILICON VALLEY | MARCH 26-29,2018www.gputechconf.com

#GTC18

2018

RECONCILIATION OF NON-GAAP TO GAAP FINANCIAL MEASURES

2018

RECONCILIATION OF NON-GAAP TO GAAP FINANCIAL MEASURES

GROSS MARGIN ($ IN MILLIONS &MARGIN PERCENTAGE)

NON-GAAP without IP IP NON-GAAP

STOCK-BASED COMPENSATION

(A)

PRODUCT WARRANTY

(B)

OTHER (C) GAAP

FY 2015$2,367 (244) $2,611 (12) — — $2,599

53.6% (2.2) 55.8% (0.3) — — 55.5%

FY 2016$2,602 (244) $2,846 (15) (20) — $2,811

54.8% (2.0) 56.8% (0.3) (0.4) — 56.1%

FY 2017$3,844 (244) $4,088 (15) — (10) $4,063

57.8% (1.4) 59.2% (0.2) — (0.2) 58.8%

FY 2018$5,821 (23) $5,844 (21) — (1) $5,822

60.2% — 60.2% (0.3) — — 59.9%

A. Stock-based compensation charge was allocated to cost of goods sold.B. Consists of warranty charge associated with a product recall.C. Consists of legal settlement and other related costs.

2018

RECONCILIATION OF NON-GAAP TO GAAP FINANCIAL MEASURES (CONTD.)

OPERATING EXPENSES ($ IN MILLIONS & % OF REVENUE)

NON-GAAPSTOCK-BASED

COMPENSATION (A)

ACQUISITION-RELATED ITEMS

(B)

OTHER (C) GAAP

FY 2015$1,657 146 37 — $1,840

35% 3 1 — 39%

FY 2016$1,721 190 22 131 $2,064

34% 4 — 3 41%

FY 2017$1,867 233 16 13 $2,129

27% 4 — — 31%

FY 2018$2,227 370 13 2 $2,612

23% 4 — — 27%

A. Stock-based compensation charge was allocated to research and development expense, and sales, general and administrative expense.B. Consists of amortization of acquisition-related intangible assets, transaction costs, compensation charges, and other credits related to acquisitions.C. Comprises of legal settlement costs, contributions, and restructuring and other charges.

2018

RECONCILIATION OF NON-GAAP TO GAAP FINANCIAL MEASURES (CONTD.)

OPERATING MARGIN ($ IN MILLIONS &MARGIN PERCENTAGE)

NON-GAAPSTOCK-BASED

COMPENSATION (A)

PRODUCT WARRANTY

(B)

ACQUISITION-RELATED ITEMS

(C)

OTHER (D) GAAP

FY 2015$954 (158) — (37) — $759

20% (3) — (1) — 16%

FY 2016$1,125 (205) (20) (22) (131) $747

22% (4) — — (3) 15%

FY 2017$2,221 (248) — (16) (23) $1,934

32% (4) — — — 28%

FY 2018$3,617 (391) — (13) (3) $3,210

37% (4) — — — 33%

A. Stock-based compensation charge was allocated to cost of goods sold, research and development expense, and sales, general and administrative expense.B. Consists of warranty charge associated with a product recall.C. Consists of amortization of acquisition-related intangible assets, transaction costs, compensation charges, and other credits related to acquisitions.D. Comprises of legal settlement costs, contributions, and restructuring and other charges.

2018

RECONCILIATION OF NON-GAAP TO GAAP FINANCIAL MEASURES (CONTD.)

A. Stock-based compensation charge was allocated to cost of goods sold, research and development expense, and sales, general and administrative expense.B. Consists of amortization of acquisition-related intangible assets, transaction costs, compensation charges, and other credits related to acquisitionsC. Other comprises of legal settlements, contributions, restructuring and other charges, gains from non-affiliated investments, interest expense related to amortization of debt discount and loss on early debt

conversions. Other also comprises anti-dilution impact from note hedge that is excluded from GAAP weighted average diluted share calculation.

($ IN MILLIONS, EXCEPT SHARES & EPS) NON-GAAP

STOCK-BASED COMPENSATION

(A)

ACQUISITION-RELATED ITEMS

(B)

OTHER (C)

TAX IMPACT OF ADJUSTMENTS

PROVISIONAL TAX BENEFIT

FROM INCOME TAX REFORM

GAAP

FY 2017

Net income $1,851 (248) (16) (65) 144 — $1,666Shares used in diluted per share calculation 605 — — 44 — — 649

Diluted EPS $3.06 — — — — — $2.57

FY 2018

Net income $3,085 (391) (13) (24) 257 133 $3,047

Shares used in diluted per share calculation 627 — — 5 — — 632

Diluted EPS $4.92 — — — — — $4.82

2018

($ IN MILLIONS) FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY2018

GAAP net cash flow provided by operating activities

$824 $835 $905 $1,175 $1,672 $3,502

Purchase of property and equipment and intangible assets

(183) (255) (122) (86) (176) (593)

Free cash flow $641 $580 $783 $1,089 $1,496 $2,909

RECONCILIATION OF NON-GAAP TO GAAP FINANCIAL MEASURES (CONTD.)