WBG Infrastructure Response to the Crisis

23

1 WBG Infrastructure Response to the Crisis April 2009

-

Upload

preston-blanchard -

Category

Documents

-

view

33 -

download

0

description

WBG Infrastructure Response to the Crisis. April 2009. Outline. Context and Background Infrastructure and the Crisis WBG Response to the Crisis: INFRA. “The Vulnerability Fund” 0.7 Percent of Stimulus Packages. Bilateral Organizations. United Nations Organizations. Non-Governmental - PowerPoint PPT Presentation

Transcript of WBG Infrastructure Response to the Crisis

1

WBG Infrastructure Response to the Crisis

April 2009

2

Outline

I. Context and Background

II. Infrastructure and the Crisis

III. WBG Response to the Crisis: INFRA

3

“The Vulnerability Fund”0.7 Percent of Stimulus Packages

Bilateral Organizations

United Nations Organizations

Non-Governmental Organizations

Multilateral Development Banks

The World Bank Group

Vulnerability Financing Facility (VFF)

Infrastructure Recovery Assets Platform (INFRA)

IFC Private SectorPlatform

GFRPIDAFast

Track Energyfor the

Poor

Trust Funds

Bank Recap

Trade Finance

Infrastructure Facility

Microfinance Facility

Advisory facility

• Direct Finance• Parallel Finance• Concessional finance

Rapid Social

Response

4

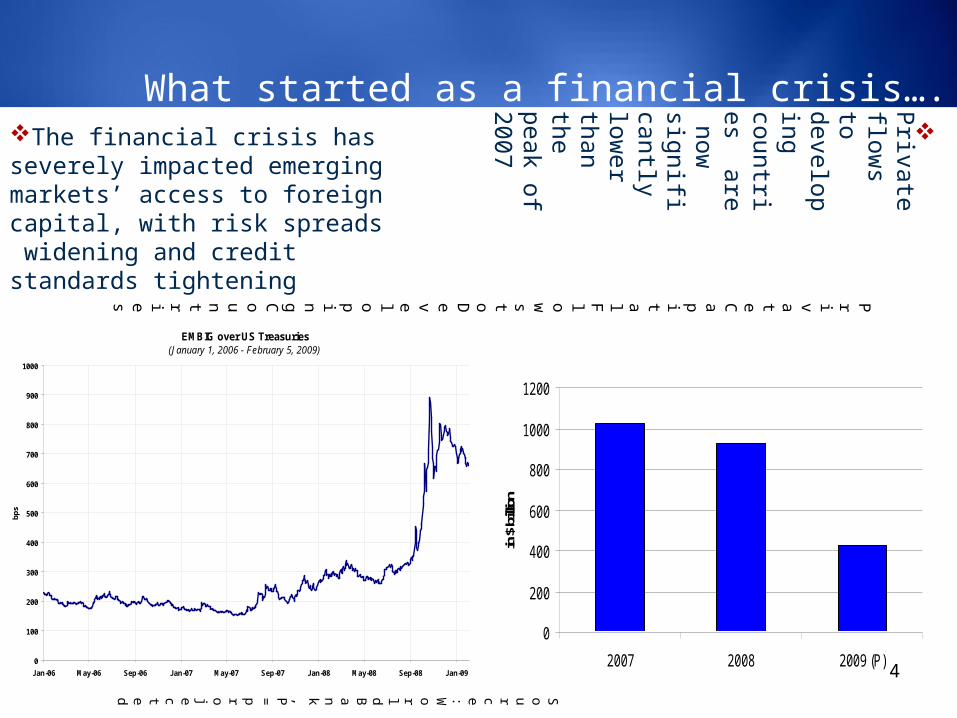

What started as a financial crisis….

EMBIG over US Treasuries(January 1, 2006 - February 5, 2009)

0

100

200

300

400

500

600

700

800

900

1000

Jan-06 May-06 Sep-06 Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09

bps

Private

Capit

al

Flows

to

Developing

Countri

es

Source :

World Bank, P=

projected

The financial crisis has severely impacted emerging markets’ access to foreign capital, with risk spreads widening and credit standards tightening

Private

flows to

developing countries are now

significantly low

er than the peak of 2007

0

200

400

600

800

1000

1200

2007 2008 2009 (P)

in $

billi

on

5

0

1

2

3

4

5

6

7

8

9

2007 2008 2009

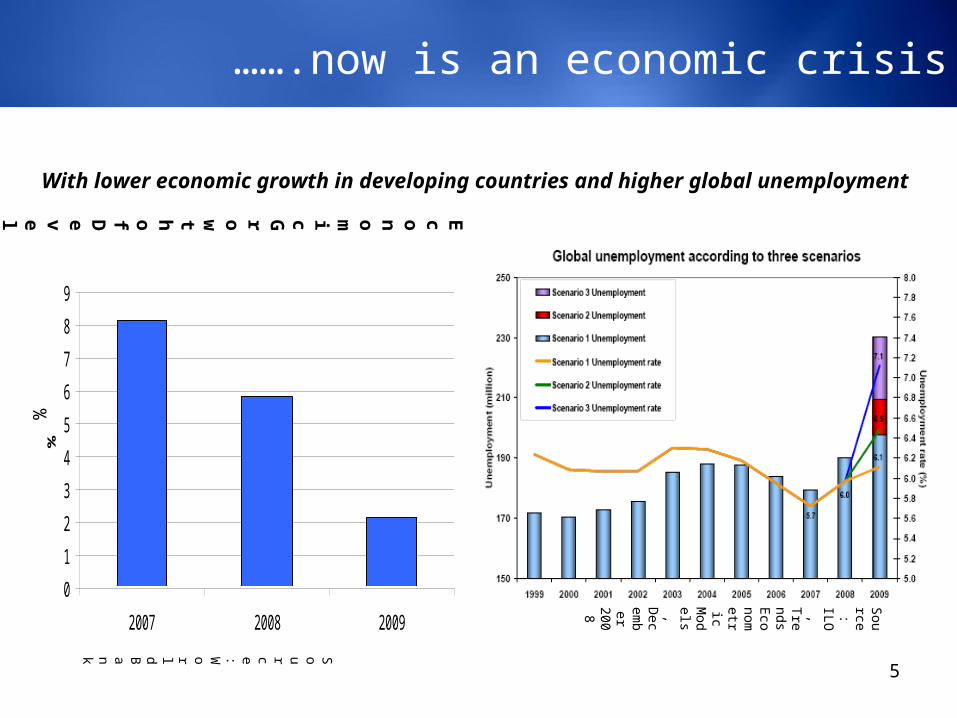

%…….now is an economic crisis

With lower economic growth in developing countries and higher global unemployment

Source: World Bank

Source:

ILO,

Trends

Eco

nometric M

odels, D

ecem

ber

2008

%

Economic Growth

o

f Developing

Countries

6

Financing for infrastructure indeveloping countries is drying up

Capital market financing for developing countries’ infrastructure

0

50

100

150

200

250

in $

bill

ion

Bond issuance

Bank lending

Source: D

ialogic

2007 2008

7

Decline in infrastructure spending leads to decreased growth….

In Indonesia, decline in total infrastructure spending follow

ing the 1997 A

sian crisis w

as accom

panied by declining grow

th

Ind

on

esia

To

tal

Infra

structu

re

Inve

stmen

t(%

o

f G

DP

)

Indonesia Average GDP

Growth

Source: World Bank

76543210

199719981999 2000

%76543210

1988-1997

1998-2007

%8

8

….and decline in infrastructure spending on maintenance has costly consequences

Main

tenance Vs Repl

acement

Costs o

f Roads in

Developing

Countri

es

0

5

10

15

20

25

30

35

40

45

50

in $

bill

ion

Lo

ss

of

roa

d

as

se

t v

alu

e

(19

70

-8

9)

Co

st o

f m

ain

ten

an

ce

to

a

vo

id

los

s in

a

ss

et

va

lue

(1

97

0-

89

)

Source: World Bank

9

…Africa could lose a key source of growth Infrastructure investments are partly

responsible for the recent improved growth performance in Africa

– Infrastructure improvements were aided by surge in external capital flows from $ 4 billion in 2002 to $20 billion in 2007

– Regional integration had become a new focus of recent infrastructure finance helping provide effective linkages to regional and international markets

Additional investments could have yielded further dividends

– $40 billion additional spending necessary to meet economic and social needs over next decade

– Improving infrastructure in all African countries to the level of Mauritius could increase per capital economic growth in the region by 2.2 percent

The crisis threatens recent gains– Reduced private flows and fiscal space

for infrastructure investments and maintenance in African countries

0

0.2

0.4

0.6

0.8

1

1.2

%

Co

ntrib

utio

n to

p

er C

apita

Eco

no

mic

Gro

wth

in

Africa

(1990-

2005)

St

ructural

Poli

cie

s Impr

ovements

in

Infrastructure

Source: World Bank

10

Outline

I. Context and Background

II. Infrastructure and the Crisis

III. WBG Response to the Crisis: INFRA

11

Crisis ResponseInfrastructure spending as a fiscal stimulus measure

Counter-cyclical public spending in infrastructure is an effective tool to create jobs and provide the foundation for economic recovery and sustained growth

Transformational opportunity to invest in “green” Infrastructure

The share of infrastructure spending in announced

fiscal stimulus packages varies substantially across countries:– So far announced infrastructure spending for 2009 represents on

average 64 percent of the total stimulus in emerging market economies and 22 percent of the total stimulus in high income economies

12

Infrastructure and the Crisis: areas of action

1. Stabilize existing infrastructure assets

2. Ensure delivery of projects that remain government priority

3. Support PPPs in infrastructure

4. Support new infrastructure project development and implementation

13

Outline

I. Context and Background

II. Infrastructure and the Crisis

III. WBG Response to the Crisis: INFRA

14

Infrastructure Recovery and Assets (INFRA)

brings priority focus on infrastructure investments and maintenance;

co-ordinates a crisis response for World Bank Group pertaining to infrastructure; and

provides a platform to work with development partners to leverage finance

IBRD/IDA INFRA PlatformOverarching Framework

15

WBG INFRA PlatformPlatform across WBG institutions

FINANCINGINFRA RESPONSE

IFC World

Bank MI

GAPRE-CRISISCURRENT

$2.7 to

3.7 billion/year

up

to $1

5 b

illion

/year

curren

tly b

eing

reasse

ssed

base

d

on

reg

ion

al sca

ns

and

co

un

try p

riorities

$2.1 billio

n

Up

to $0

.3 b

illion

in

Glo

bal

Eq

uity

Fu

nd

u

nd

er the

Infrastru

ctu

re Crisis

Facility (1

)

to b

e ad

justed

d

ow

nw

ard

s reflectin

g

low

er th

an

anticip

ated

FD

I flo

w in

to

INF

$0.7 to $1 billion/year

$11

to $13

billion/year

INSTRUMENTS

(1) Scale up constrained by balance sheet

IFC

Infrastructure C

risis Facility

(over 3 to 5 years)

Sup

port (IDA

/IFC

) pipe

lines

Sub

-national instrum

ents

Sca

led u

p R

espo

nse (o

ver 3 yea

rs):D

irect Fin

ance su

pp

ort

(IDA

/IFC

) pip

eline

s

Parallel fin

anc

e expan

sion

w

ith b

ilaterals/o

the

r IFIs

Co

ncessio

nal w

ind

ow

for

pro

ject prep

aration

pro

ject finan

cing

Sup

port (IDA

/IFC

) pipelines

Early 200

9 Board discussio

n. P

roposed reform

s include:

• N

ew P

roduct – covering

non-honorin

g of sovereign

financial obligations

•E

xpanded co

verage – m

ore

acquisition/restructuring

projects will be elig

ible•

Enh

ance Breach of C

ontract coverage for S

OE

s on selective

basis

16

IBRD/IDA INFRA PlatformAction points to respond to crisis

1.Stabilize existing

infrastructure assets

2.E

nsu

re d

elivery o

f p

rojec

tsthat

are a g

over

nm

ent

prio

rity

3.S

up

po

rt P

PP

s in

in

frastru

ctu

re

4.S

up

po

rt n

ew

in

frastru

ctu

re d

evelop

men

t an

d

imp

lemen

tation

Pro

ject restructu

ring

of

existing

p

ortfo

lio

Su

pp

ort co

un

tries to

m

anag

e curren

cy, in

tere

st rate, an

d

com

mo

dity

risk

Devel

op

me

nt

Po

licy

Op

eratio

ns

and

o

ther

lend

ing

o

perat

ion

s

Acceleratin

g

disb

urse

men

ts o

f exis

ting

p

rojects

Ad

ditio

na

l fin

an

cing

(loan

an

d g

uaran

tee) fo

r on

go

ing

p

rojects

“Green

” in

frastructu

re:

advan

ce clim

ate chan

ge

and

low

carb

on

ag

end

a

Ram

p u

p su

b-

sovereig

n

lend

ing

and

related

ad

visory

services

Deferred

D

raw

do

wn

O

ptio

n (D

DO

); n

on

-IBR

D

hed

gin

g

instru

men

ts

Su

pp

ort to

p

ub

lic co

mm

itme

nts to

PP

P

pro

jects (fin

an

ce

and

ad

visory)

Increa

sed

use o

f g

uaran

tees

Inn

ov

ative in

strum

ents

: OB

A

sub

sidie

s co

mp

lemen

ting

use

r fees

C

oo

rdin

ation

with

IFC

In

frastructu

re Crisis

Facility

Ad

vice to g

overn

me

nts

that la

un

ch g

row

th an

d

job

enh

ancem

ent

pro

gram

s

Su

pp

ort to

PE

Rs

, M

TE

Fs, in

crease g

overn

men

t capa

city to

plan

, prep

are

, im

plem

ent, an

d m

anag

e in

frastructu

re as

sets

Imp

lemen

t En

ergy fo

r th

e Po

or In

itiative

OBJECTIVES ACTIONS

17

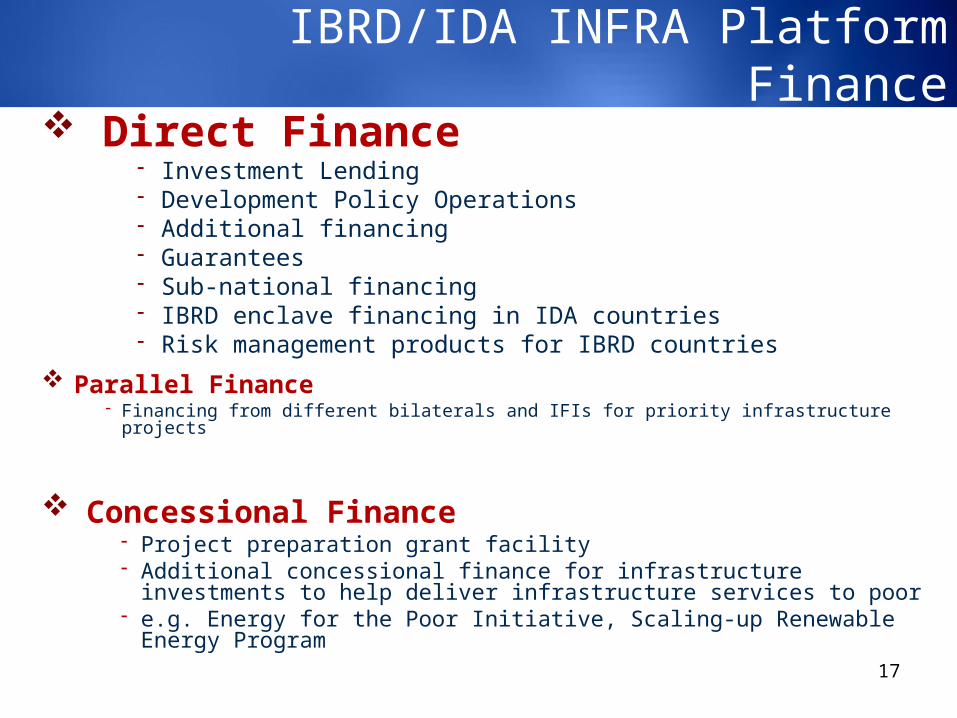

IBRD/IDA INFRA Platform Finance

Direct Finance Investment Lending Development Policy Operations Additional financing Guarantees Sub-national financing IBRD enclave financing in IDA countries Risk management products for IBRD countries

Concessional Finance Project preparation grant facility Additional concessional finance for infrastructure investments to help

deliver infrastructure services to poor e.g. Energy for the Poor Initiative, Scaling-up Renewable Energy Program

Parallel Finance Financing from different bilaterals and IFIs for priority infrastructure projects

18

IBRD/IDA INFRA Platform Energy for the Poor Initiative

Launched in June 2008, EFPI aims at preserving investments to enhance energy access to the poor during a period of changing global environment characterized by the global crisis and increasing volatility of oil prices

EFPI will

in the short term, raise grant financing to develop energy infrastructure programs with greater and direct impact on the poor; and

in the medium term, through co- and parallel financing with donors, scale up public and private sector projects that reduce the longer-term vulnerability of countries to higher oil prices.

19

The specific Africa INFRA focuses on– Regional integration e.g. large scale regional generation and transmission projects,

port facilities and access roads– Asset preservation, ‘saving’ of key projects and maintenance– Urban development e.g. expansion of basic urban services such as drainage, water,

sanitation, street lighting

Africa INFRA funds projects with a mix of short term employment generation and medium term growth impact

It targets countries willing to engage in complementary infrastructure policy reforms

The size of the Africa INFRA would be US $5-6 billion

IBRD/IDA INFRA Platform Africa INFRA

20

IBRD/IDA INFRA PlatformHow it works

REGIONAL MANAGEMENT PRIORITIZED PROJECTS

D

ES

IG

N

DIA

GN

OS

TIC

T

OO

L S

UP

PO

RT

F

RO

M

GP

P

S

EE

K

AD

DIT

IO

NA

L

CO

NC

ES

SIO

NA

L

FU

ND

IN

G S

EE

K

PA

RA

LL

EL

F

UN

DI

NG

SU

PP

OR

T

FR

OM

G

PP

SE

EK

A

DD

IT

ION

AL

C

ON

CE

SS

ION

AL

F

UN

DIN

G

GU

IDA

NC

E

NO

TE

S,

TR

AI

NIN

G, e.g

.. D

PL

, P

PP

, O

BA

MONITORING FRAMEWORK

PROCESSING

COUNTRY

MONITORI

NG

F

INANCE

D

IAGNOSTIC

ASSESSMENT

Re

gio

na

l S

en

ior

Ma

na

ge

me

nt

/Co

un

try

D

irec

tor

HOW

IT

WORKS

PROJECT

PREPARATION

SDN

COORDI

NATING

GROUP

21

IBRD/IDA INFRA Platform Diagnostic Assessment

Strategic Country Reviews Assessment of fiscal space constraints Assessment of actual needs and spending in the infrastructure

sector Assessment of sector policy, regulatory framework and

governance

Country Specific Diagnostics

INFRA Targeted Portfolio Performance Reviews Assessment of analytical gaps Identification of entry points for policy dialogue

To be partially funded through existing GPPs

22

IBRD/IDA INFRA Platform Monitoring and Reporting

INFRA Diagnostic Outcome Indicators (quarterly) At country level– Number of projects identified by RVP to have priority– Expected WBG INFRA intervention–“Green” infrastructure– Expected parallel financing– Expected numbers of jobs created or saved

INFRA Project Indicators (quarterly)– “Green” infrastructure– Status– Amount– Type of instrument: DPO, Investment Loan, Sub-sovereign, other– Amount of parallel financing

INFRA Priority Processing Indicator– Measures how quickly INFRA projects are processed against regional benchmarks

INFRA Concessional Window Indicators (quarterly)– By donor– By type of funding: TA, concessional

SIAP Portfolio Monitoring– Ongoing monitoring through Business Warehouse

COUNTRY

Re

gio

na

l S

en

ior

Ma

na

ge

me

nt

/Co

un

try

Dire

cto

r

23

IBRD/IDA INFRA PlatformNot business as usual

INFRA response will be characterized by:

Timeliness

Targeting

Productivity and growth

Swift response inthe short term e.g. projectsready for implementation

Projects that have employmentgeneration potential and are agovernment priority

Projects that remove infra. bottlenecks and enhancelong term productive capacity