Using Technical Analysis to Augment Performance in … - How technical... · Using Technical...

41

CFA South Africa Investment Conference 10 September 2009 Johannesburg, South Africa Using Technical Analysis to Augment Performance in the Secular Bear Market Philip J. Roth, CMT Chief Technical Market Analyst, Miller Tabak + Co., LLC Director, MTA Educational Foundation

Transcript of Using Technical Analysis to Augment Performance in … - How technical... · Using Technical...

CFA South Africa Investment Conference10 September 2009

Johannesburg, South Africa

Using Technical Analysis to AugmentPerformance in the Secular Bear Market

Philip J. Roth, CMTChief Technical Market Analyst, Miller Tabak + Co., LLCDirector, MTA Educational Foundation

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

2

Technical Analysis Consists of 4 Types of Indicators

1. Trend and Momentum2. Sentiment (Psychology, or what fundamentalists

call Behavioral Finance)3. Supply/Demand (also called Flow of Funds)4. Intermarket Analysis (Equity Alternatives)

This discussion will focus on points 3 and 4

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

3

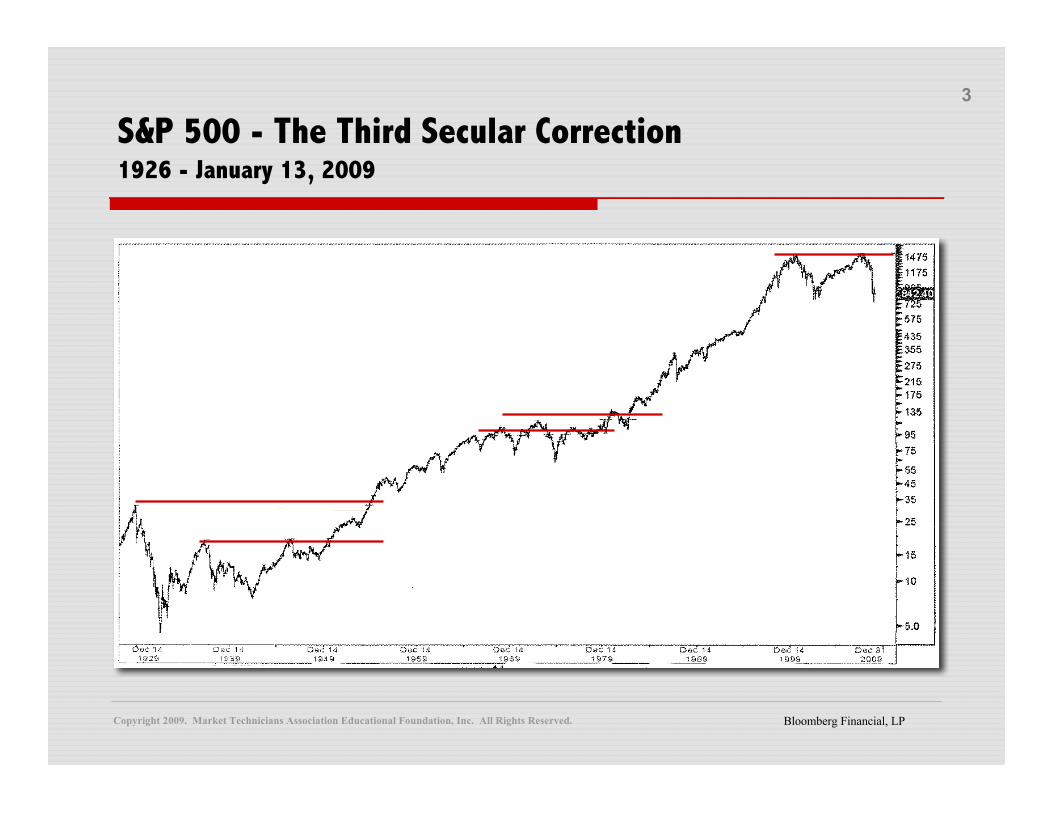

S&P 500 - The Third Secular Correction1926 - January 13, 2009

Bloomberg Financial, LP

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

4

Dow Theory of “Confirmation”Weekly DJIA and DJTA – May 2002-May 2005

StockCharts.com

Confirmationof New High

in Transports

New High

DJ Industrials - Weekly

DJ Transports - Weekly

StockCharts.com

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

5

Viewing the Company versus the Stock

StockCharts.com

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

6

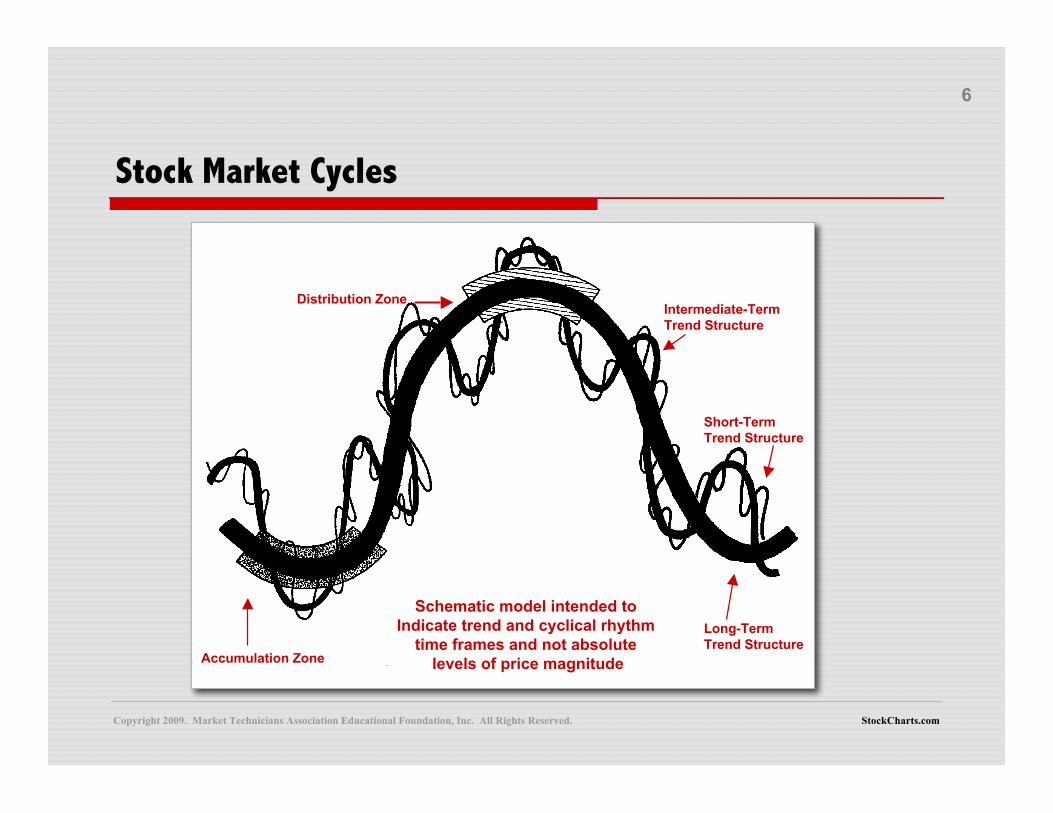

Stock Market Cycles

StockCharts.com

Schematic model intended to Indicate trend and cyclical rhythm

time frames and not absolute levels of price magnitudeAccumulation Zone

Distribution Zone Intermediate-Term Trend Structure

Schematic model intended to Indicate trend and cyclical rhythm

time frames and not absolute levels of price magnitude

Distribution Zone

Long-Term Trend Structure

Short-Term Trend Structure

Intermediate-Term Trend Structure

Accumulation Zone

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

7

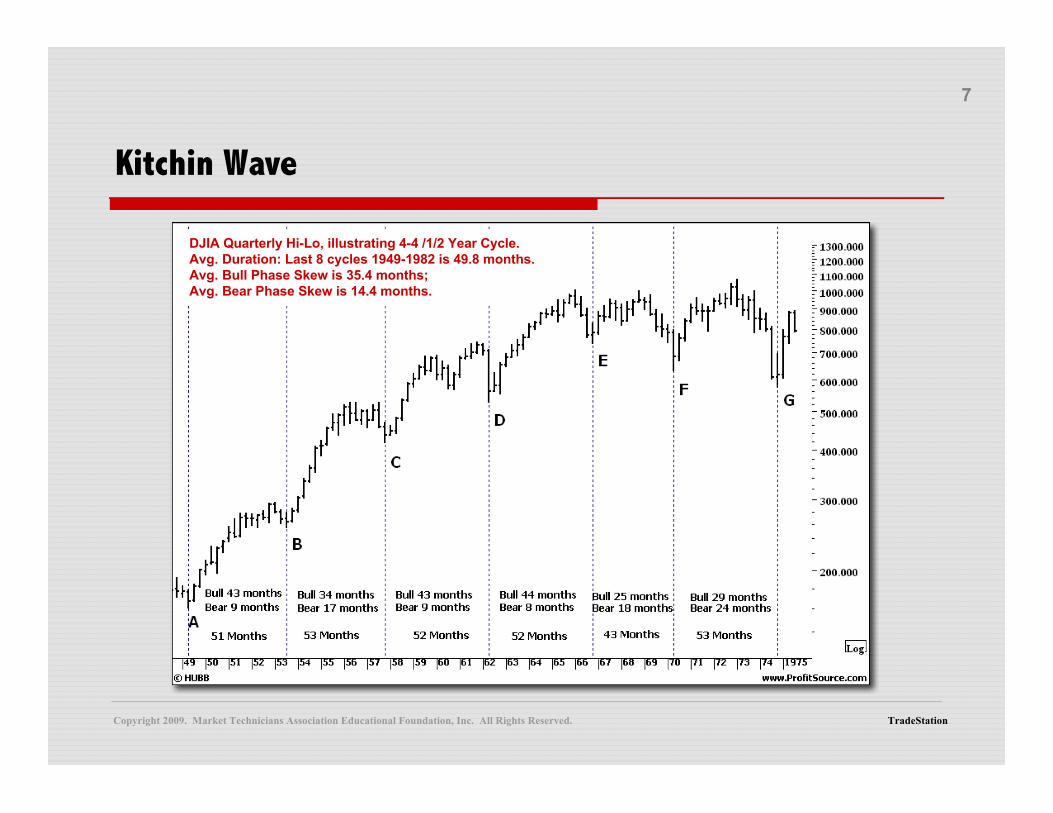

Kitchin Wave

TradeStation

DJIA Quarterly Hi-Lo, illustrating 4-4 /1/2 Year Cycle.Avg. Duration: Last 8 cycles 1949-1982 is 49.8 months.Avg. Bull Phase Skew is 35.4 months;Avg. Bear Phase Skew is 14.4 months.

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

8

StockCharts.com

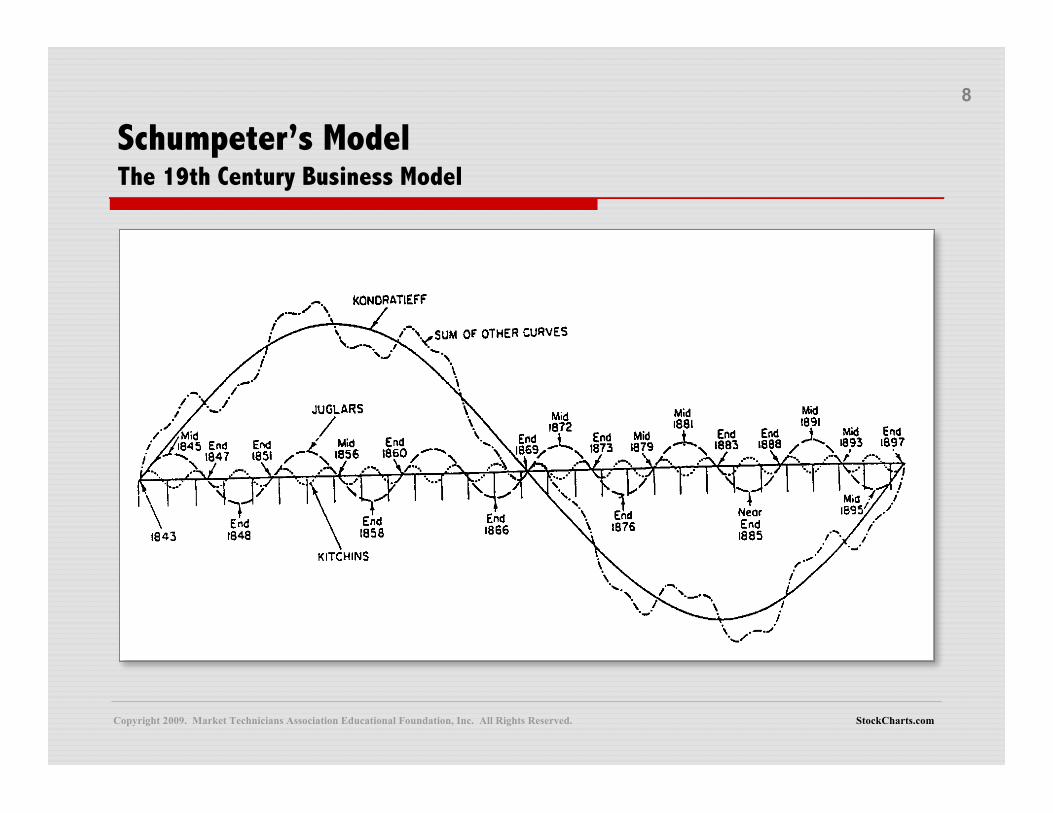

Schumpeter’s ModelThe 19th Century Business Model

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

9

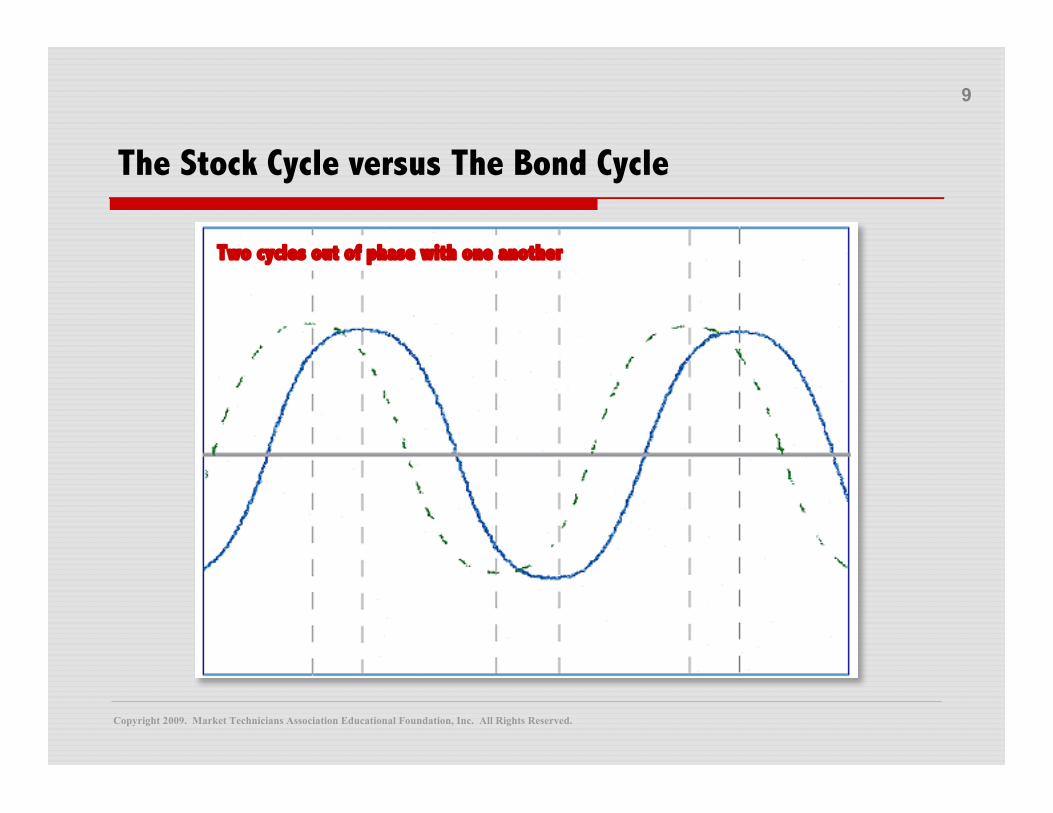

The Stock Cycle versus The Bond Cycle

Two cycles out of phase with one another

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

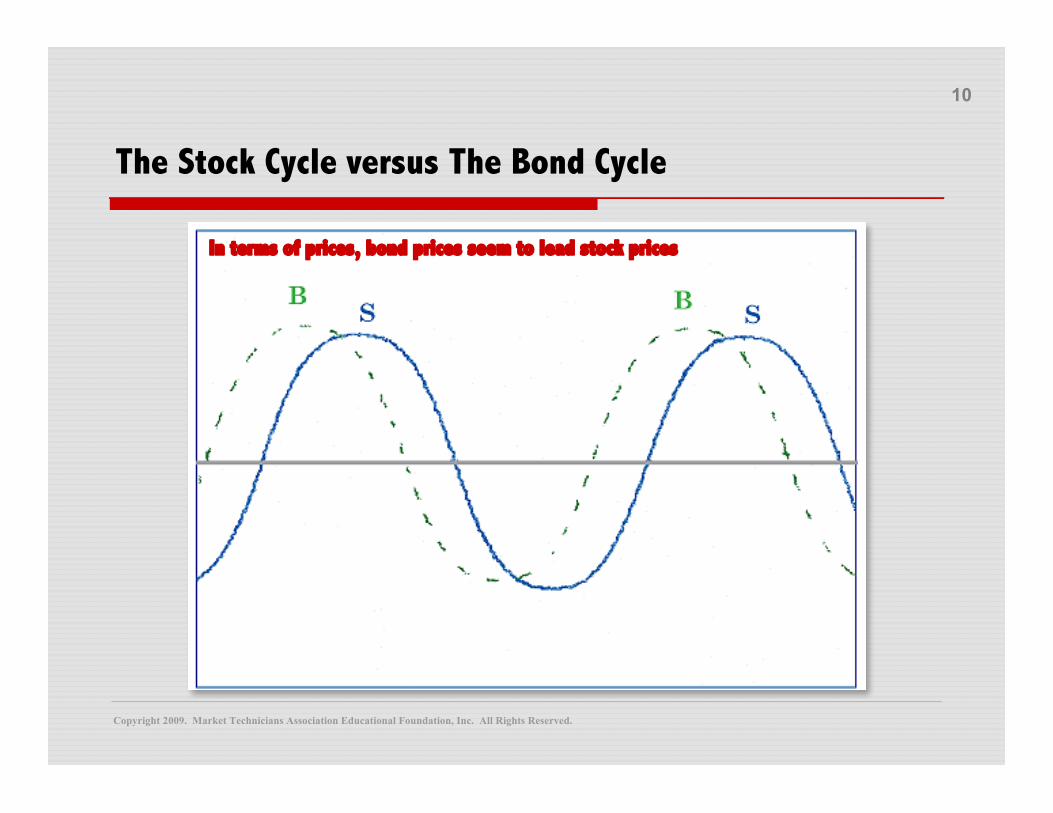

10

The Stock Cycle versus The Bond Cycle

In terms of prices, bond prices seem to lead stock prices

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

11

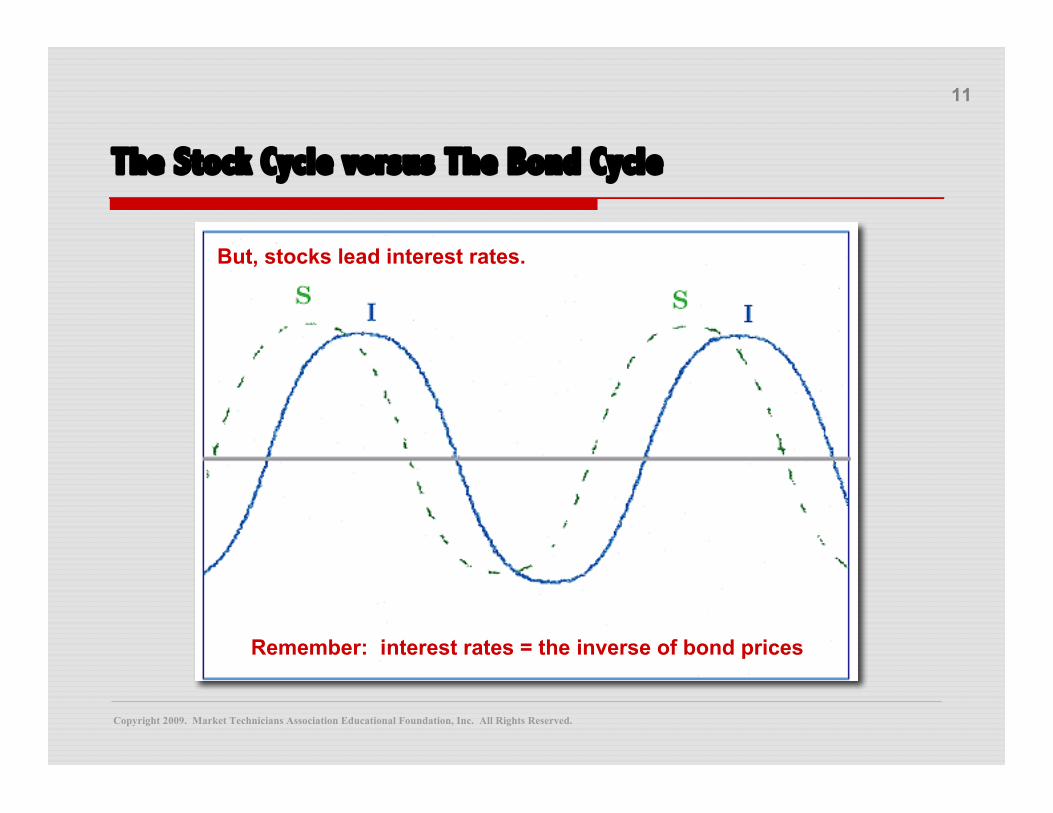

The Stock Cycle versus The Bond Cycle

But, stocks lead interest rates.

Remember: interest rates = the inverse of bond prices

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

12

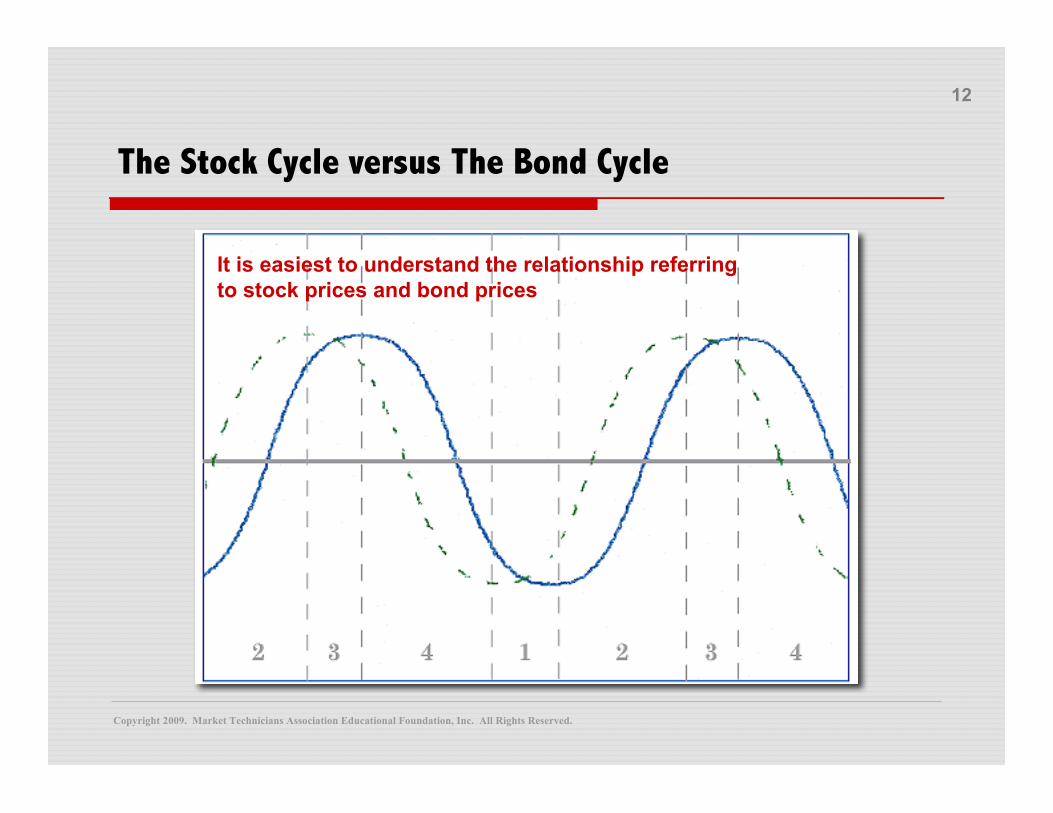

The Stock Cycle versus The Bond Cycle

It is easiest to understand the relationship referringto stock prices and bond prices

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

13

The Stock Cycle versus The Bond Cycle

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

14

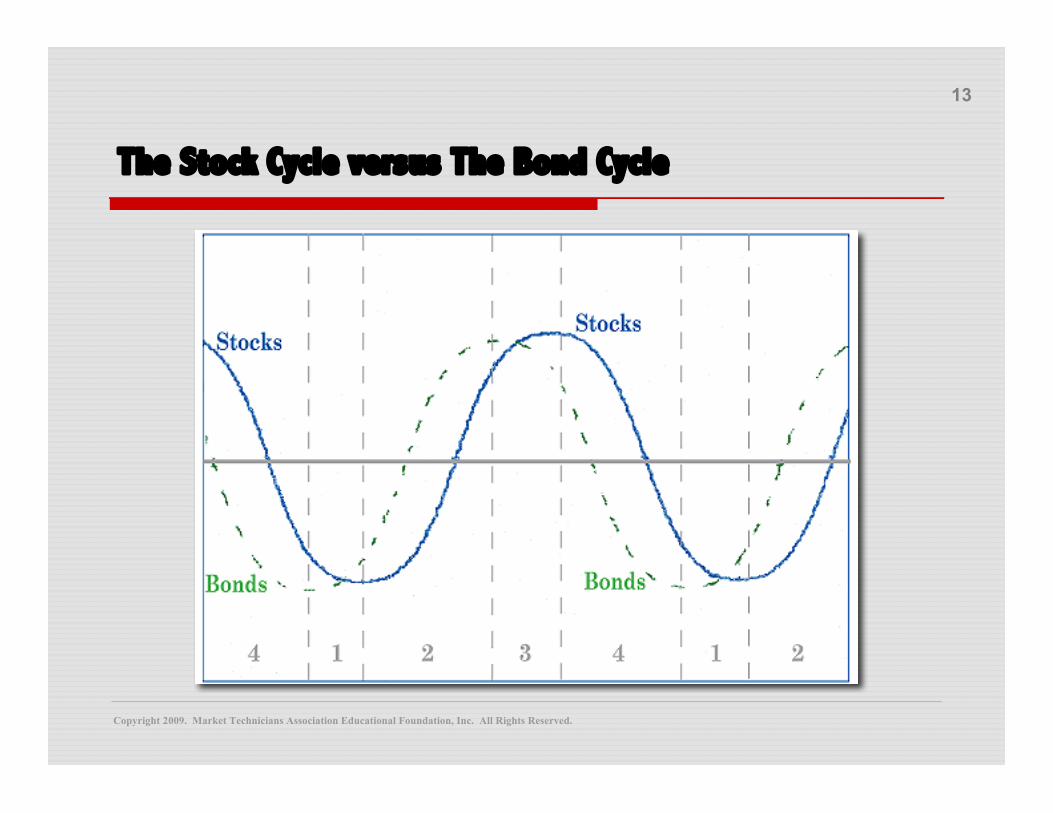

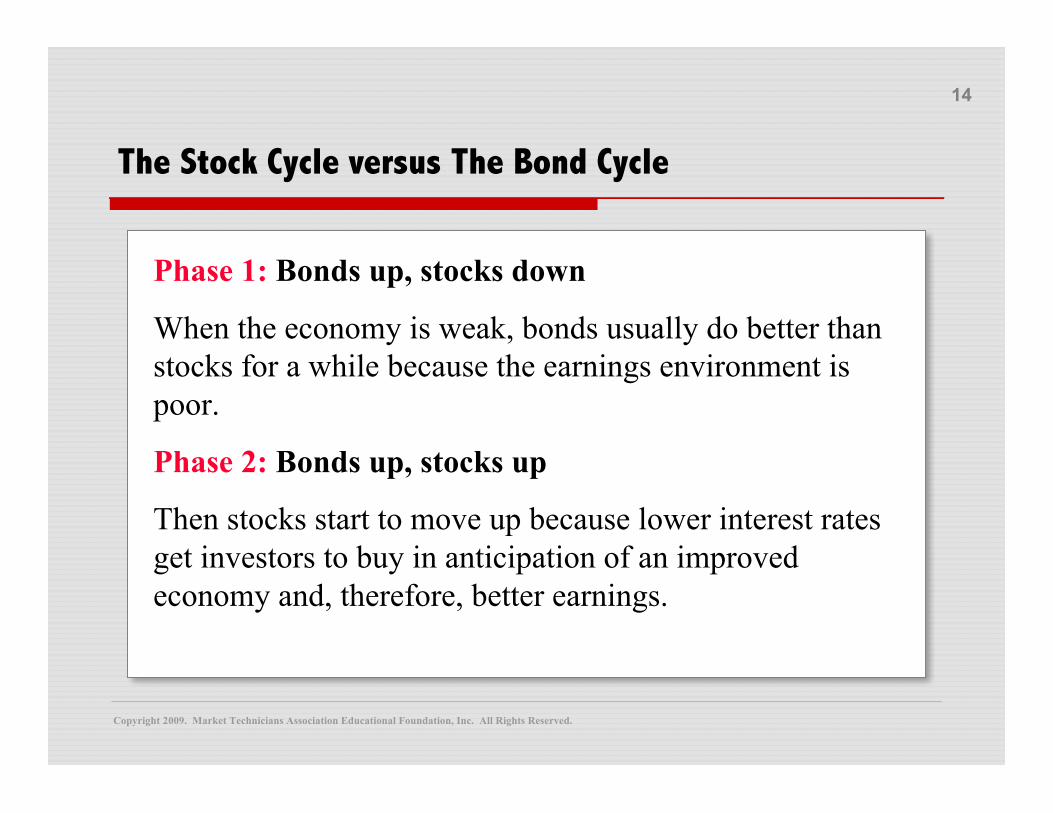

The Stock Cycle versus The Bond Cycle

Phase 1: Bonds up, stocks down

When the economy is weak, bonds usually do better thanstocks for a while because the earnings environment ispoor.

Phase 2: Bonds up, stocks up

Then stocks start to move up because lower interest ratesget investors to buy in anticipation of an improvedeconomy and, therefore, better earnings.

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

15

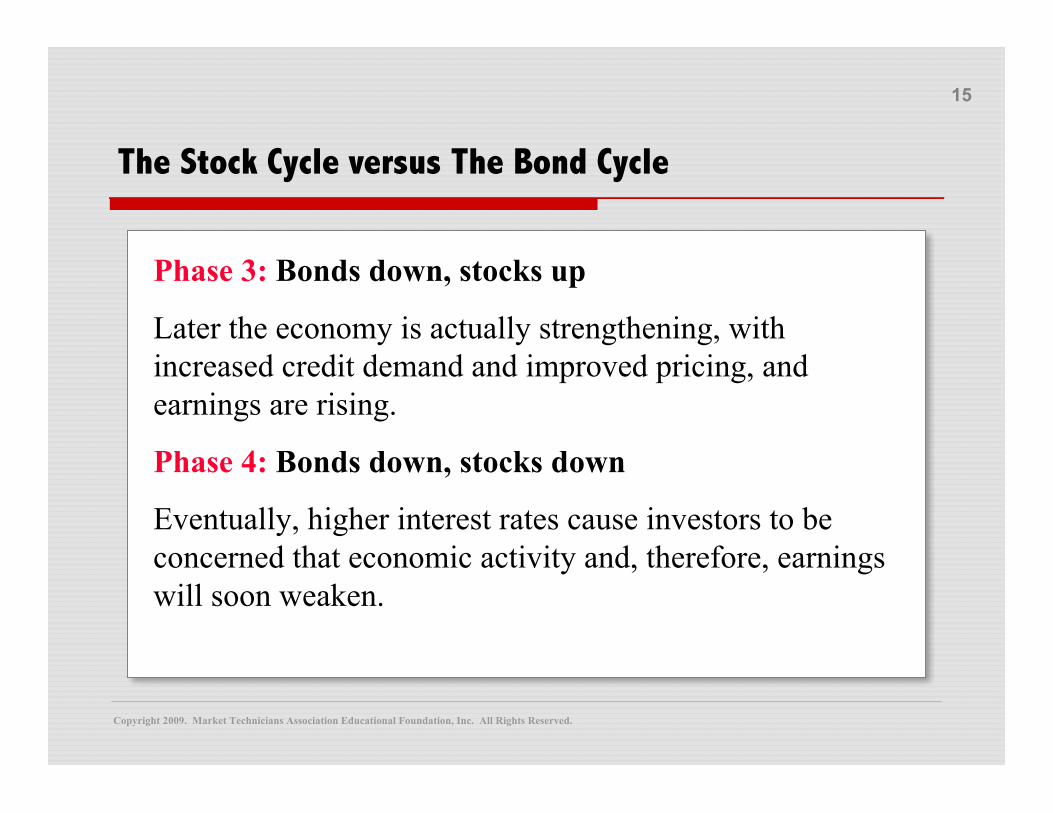

The Stock Cycle versus The Bond Cycle

Phase 3: Bonds down, stocks up

Later the economy is actually strengthening, withincreased credit demand and improved pricing, andearnings are rising.

Phase 4: Bonds down, stocks down

Eventually, higher interest rates cause investors to beconcerned that economic activity and, therefore, earningswill soon weaken.

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

16

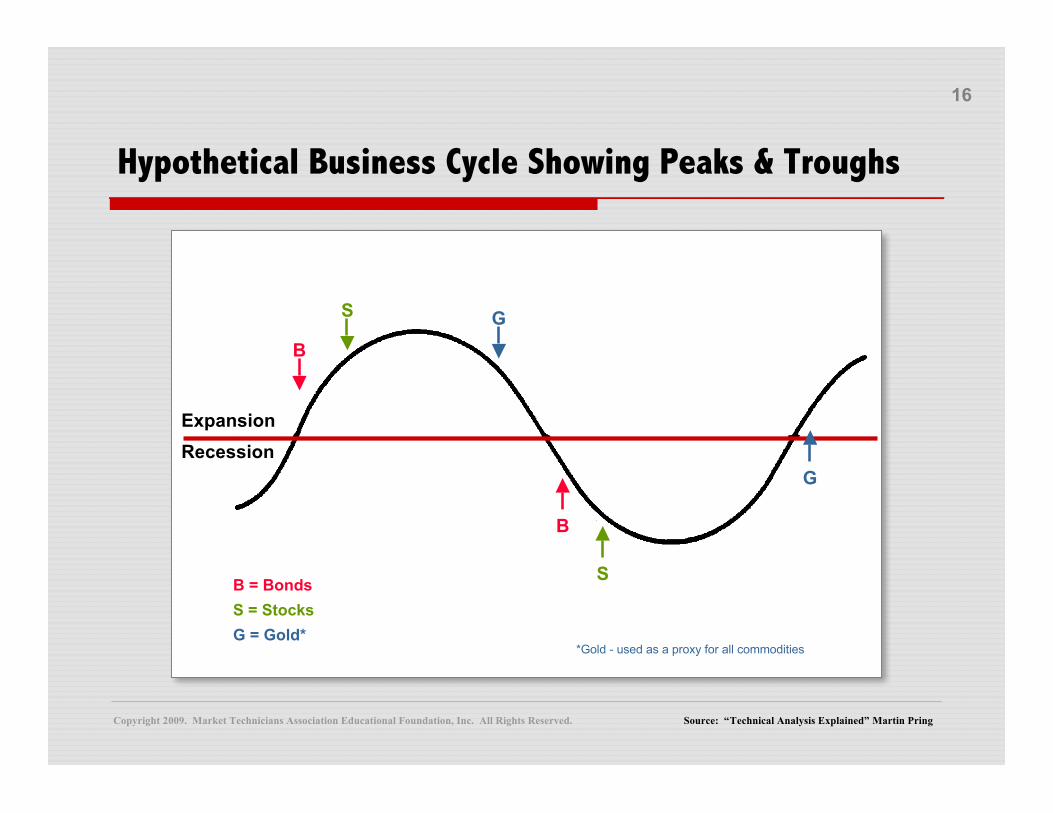

Hypothetical Business Cycle Showing Peaks & Troughs

Source: “Technical Analysis Explained” Martin Pring

*Gold - used as a proxy for all commodities

B

B

S

S

G

G

ExpansionRecession

B = BondsS = StocksG = Gold*

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

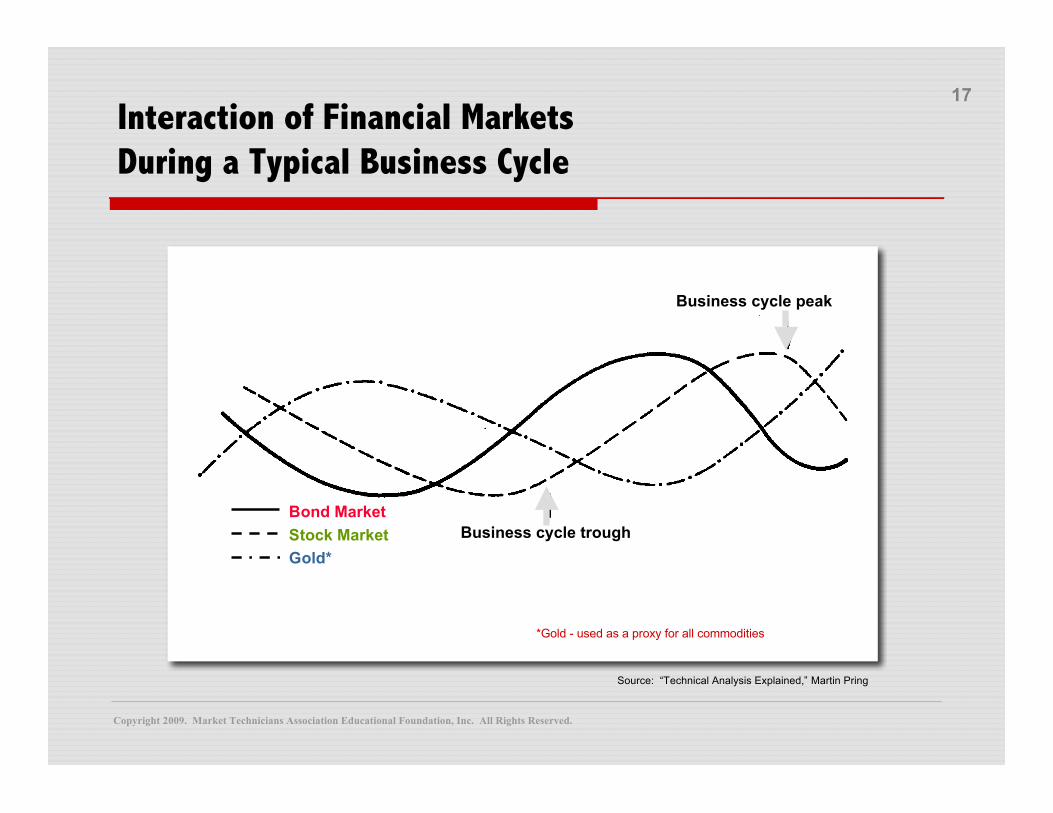

17Interaction of Financial MarketsDuring a Typical Business Cycle

Bond MarketStock MarketGold*

Business cycle trough

Business cycle peak

Source: “Technical Analysis Explained,” Martin Pring

*Gold - used as a proxy for all commodities

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

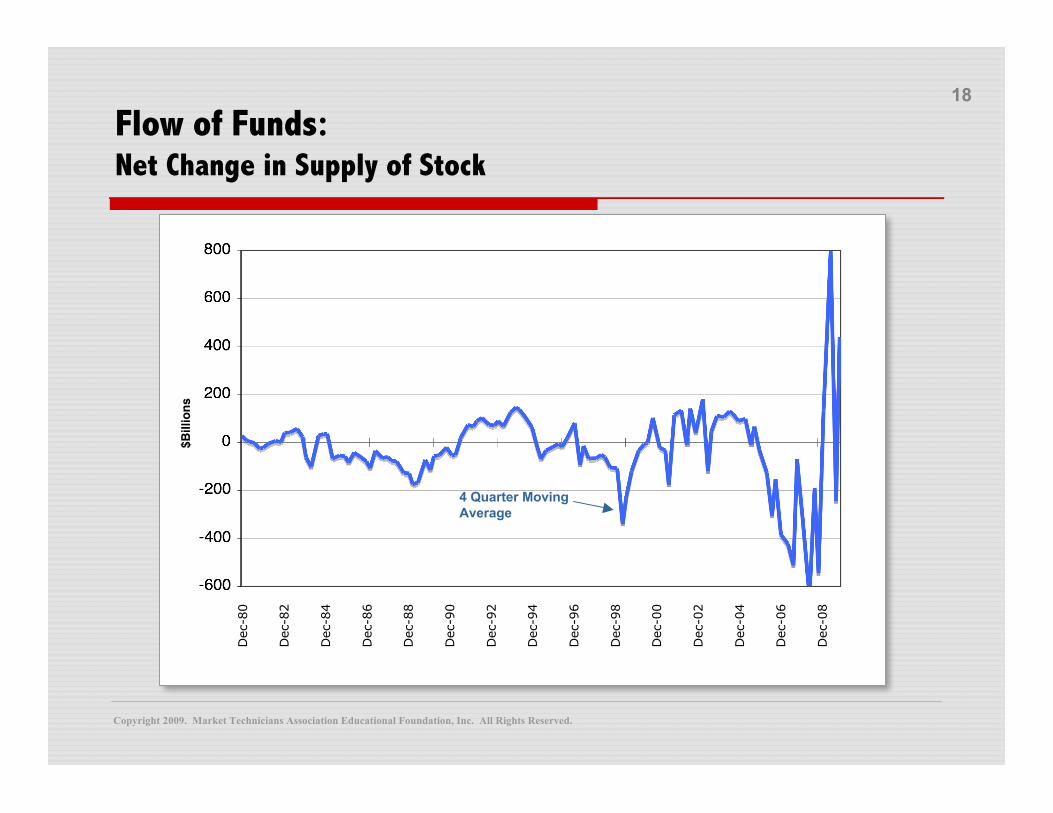

18

Flow of Funds:Net Change in Supply of Stock

Dec-80

Dec-82

Dec-84

Dec-86

Dec-88

Dec-90

Dec-92

Dec-94

Dec-96

Dec-98

Dec-00

Dec-02

Dec-04

Dec-06

Dec-08

4 Quarter MovingAverage

$Bill

ions

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

19

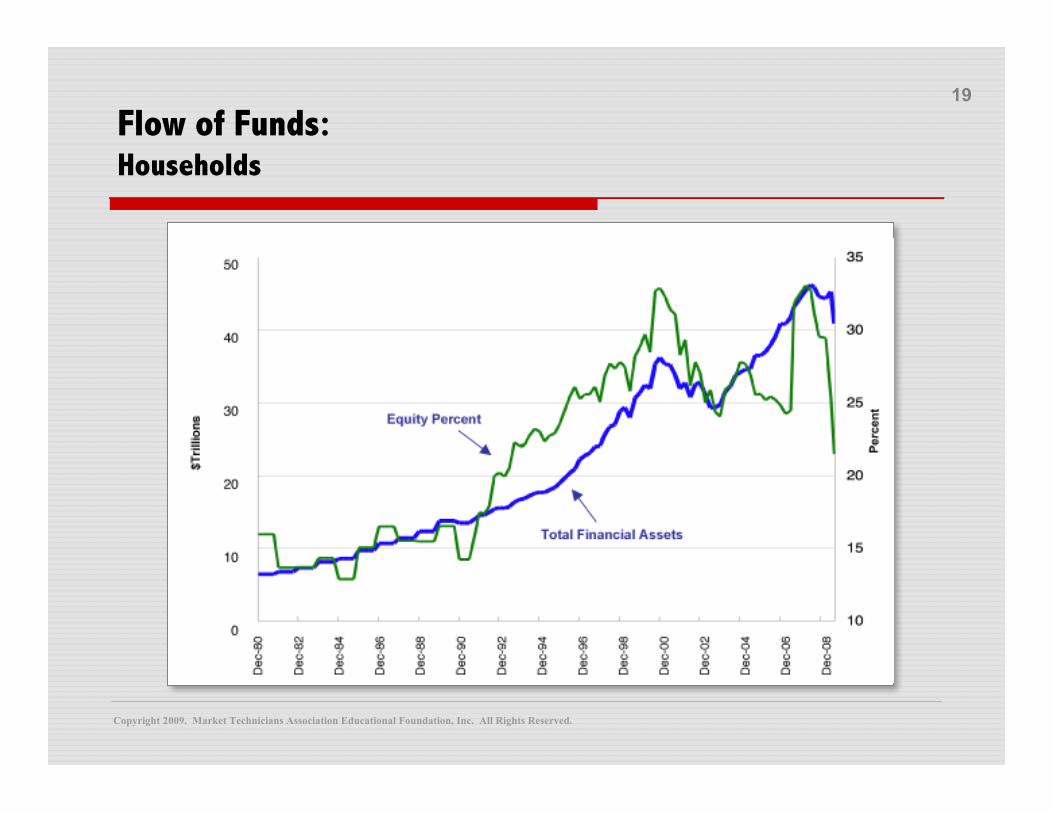

Flow of Funds:Households

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

20

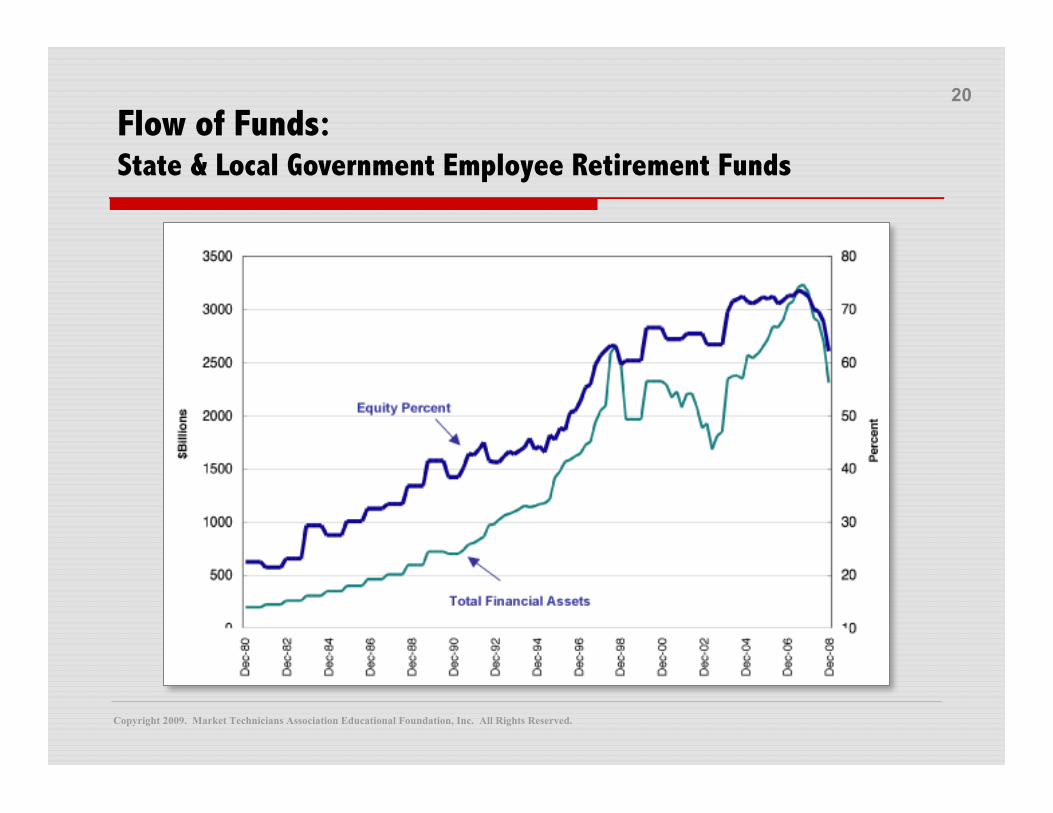

Flow of Funds:State & Local Government Employee Retirement Funds

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

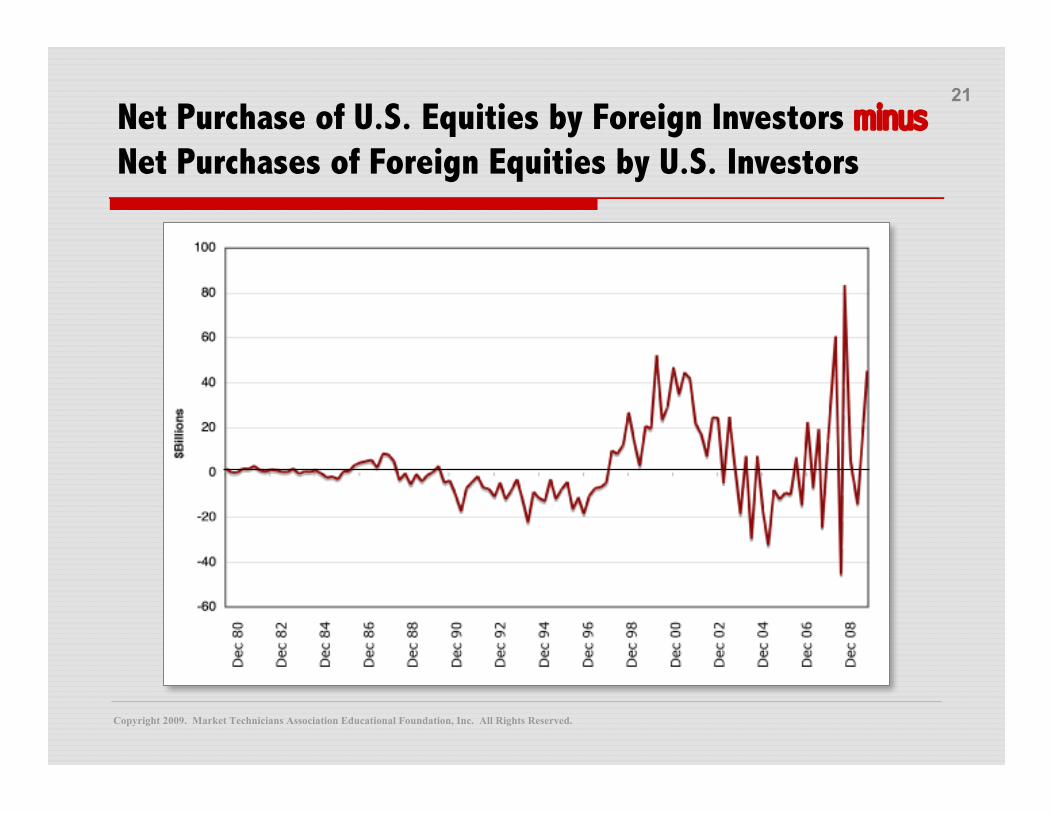

21Net Purchase of U.S. Equities by Foreign Investors minusNet Purchases of Foreign Equities by U.S. Investors

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

22

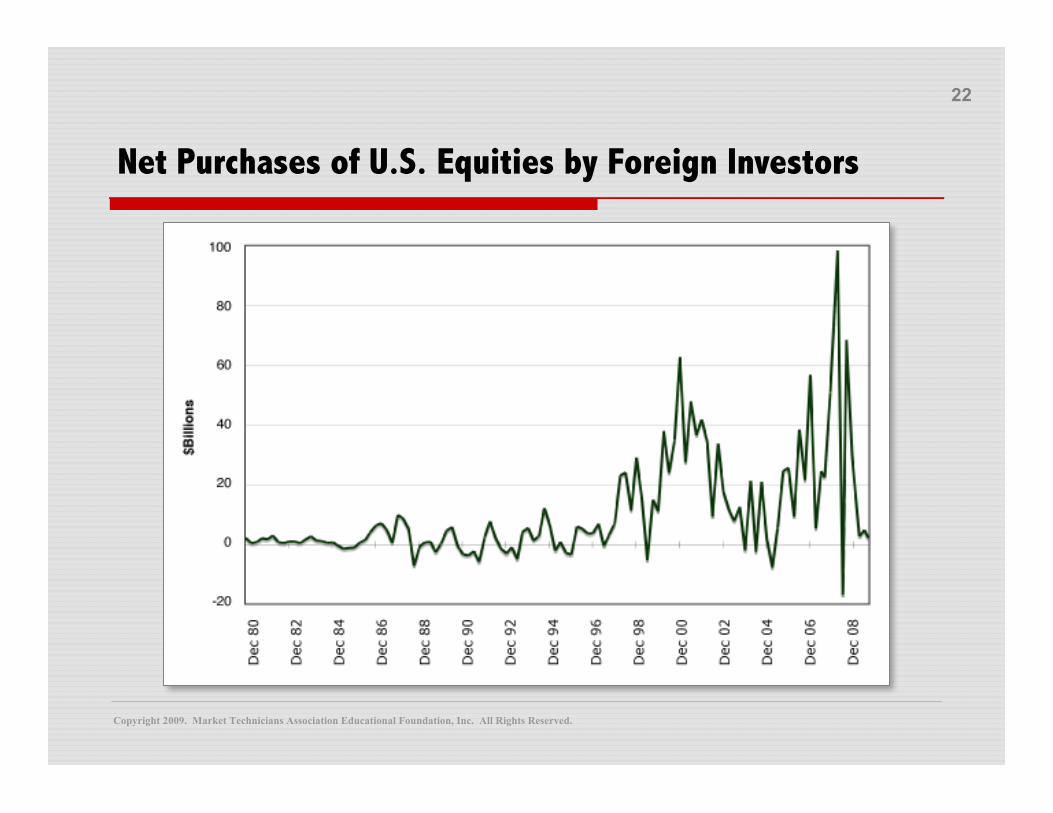

Net Purchases of U.S. Equities by Foreign Investors

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

23

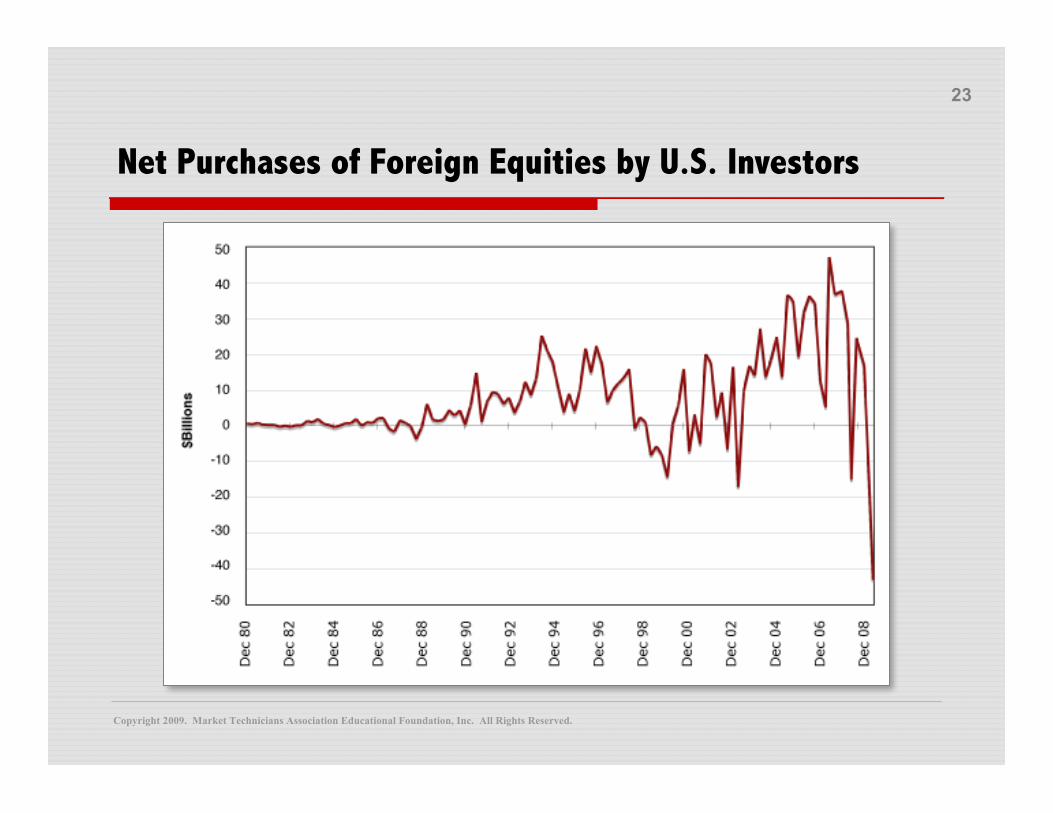

Net Purchases of Foreign Equities by U.S. Investors

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

24

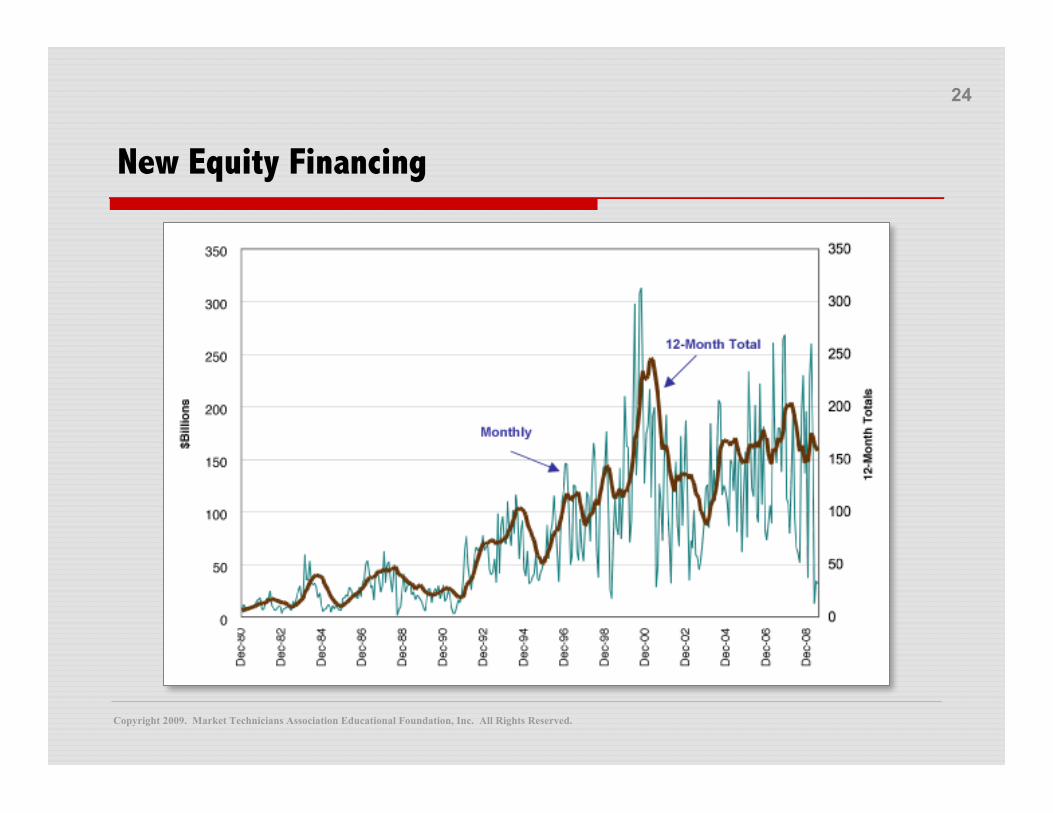

New Equity Financing

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

25

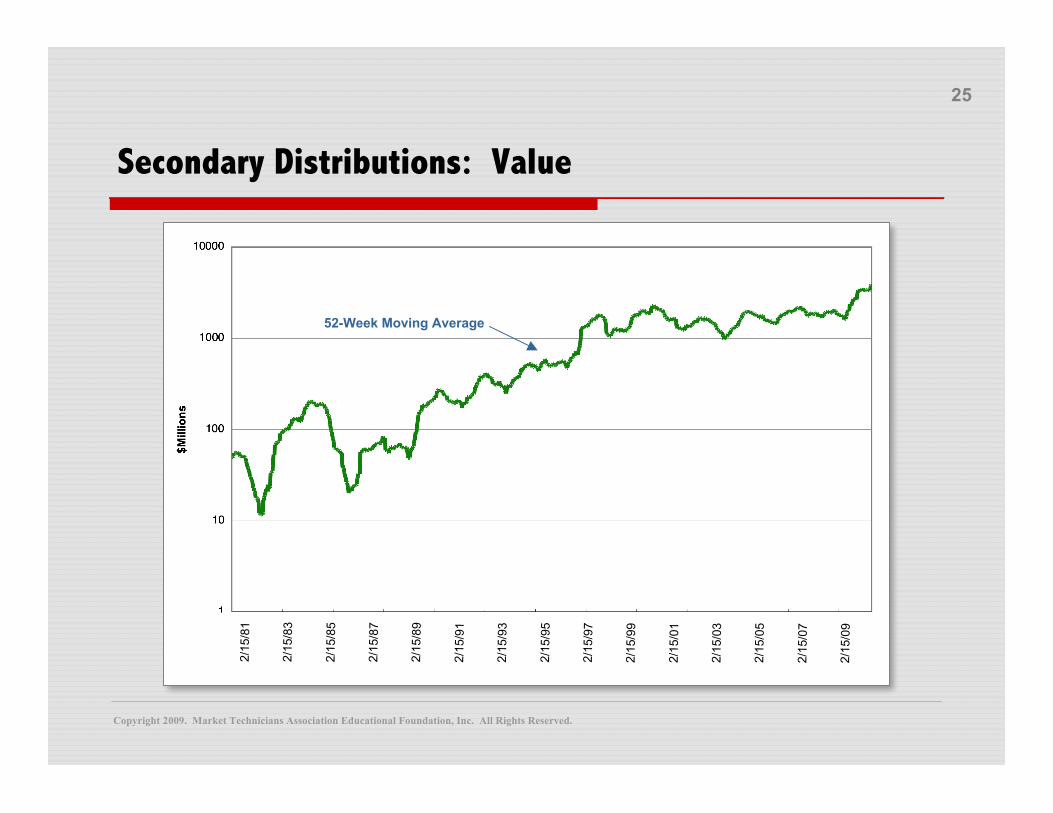

Secondary Distributions: Value

52-Week Moving Average

2/15

/81

2/15

/83

2/15

/85

2/15

/87

2/15

/89

2/15

/91

2/15

/93

2/15

/95

2/15

/97

2/15

/99

2/15

/01

2/15

/03

2/15

/05

2/15

/07

2/15

/09

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

26

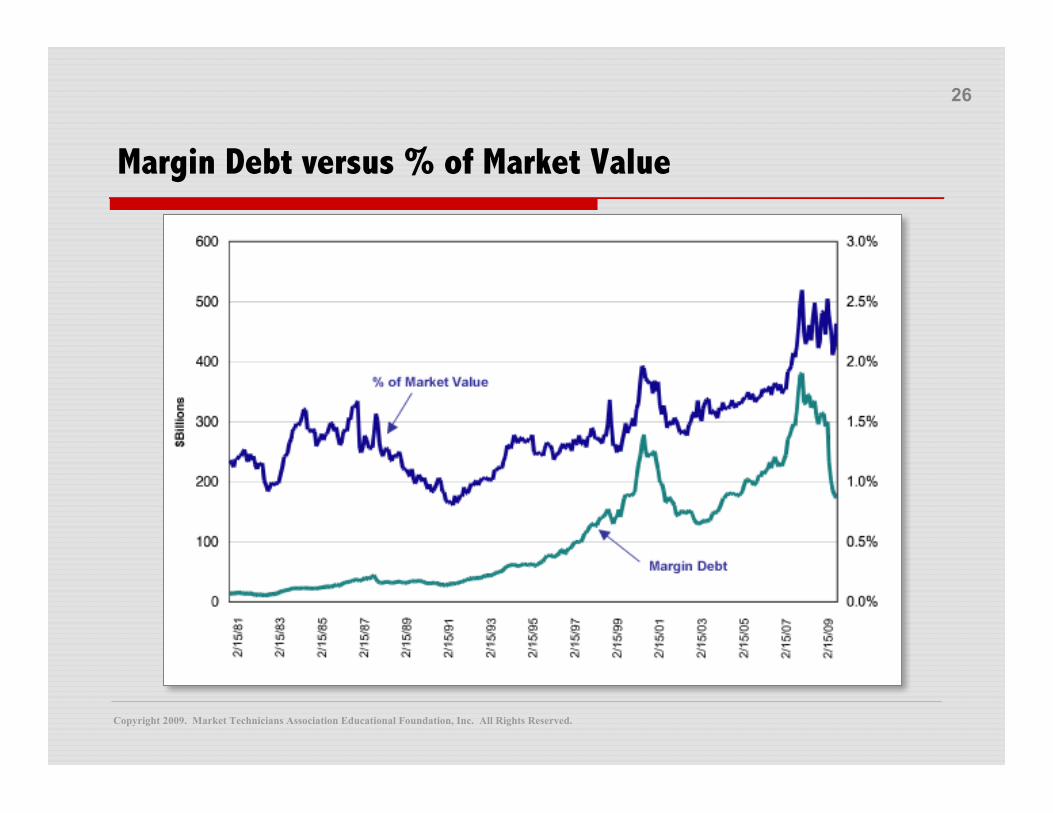

Margin Debt versus % of Market Value

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

27

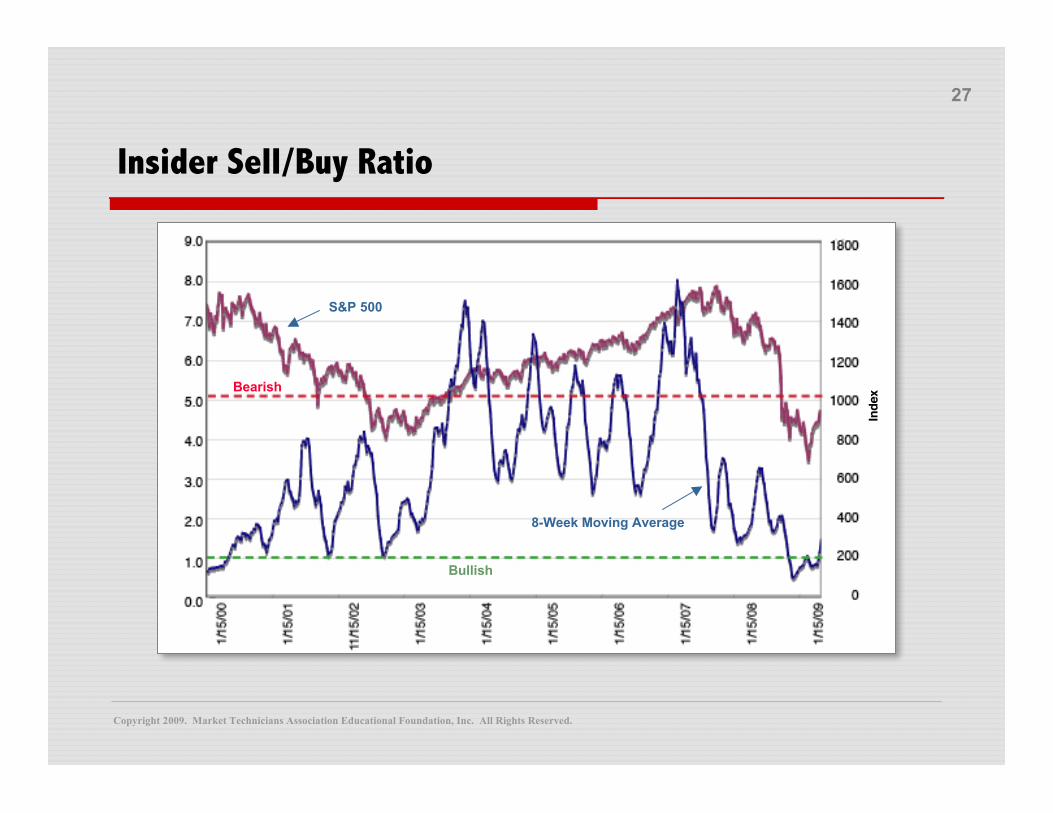

Insider Sell/Buy Ratio

Inde

xBearish

Bullish

8-Week Moving Average

S&P 500

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

28

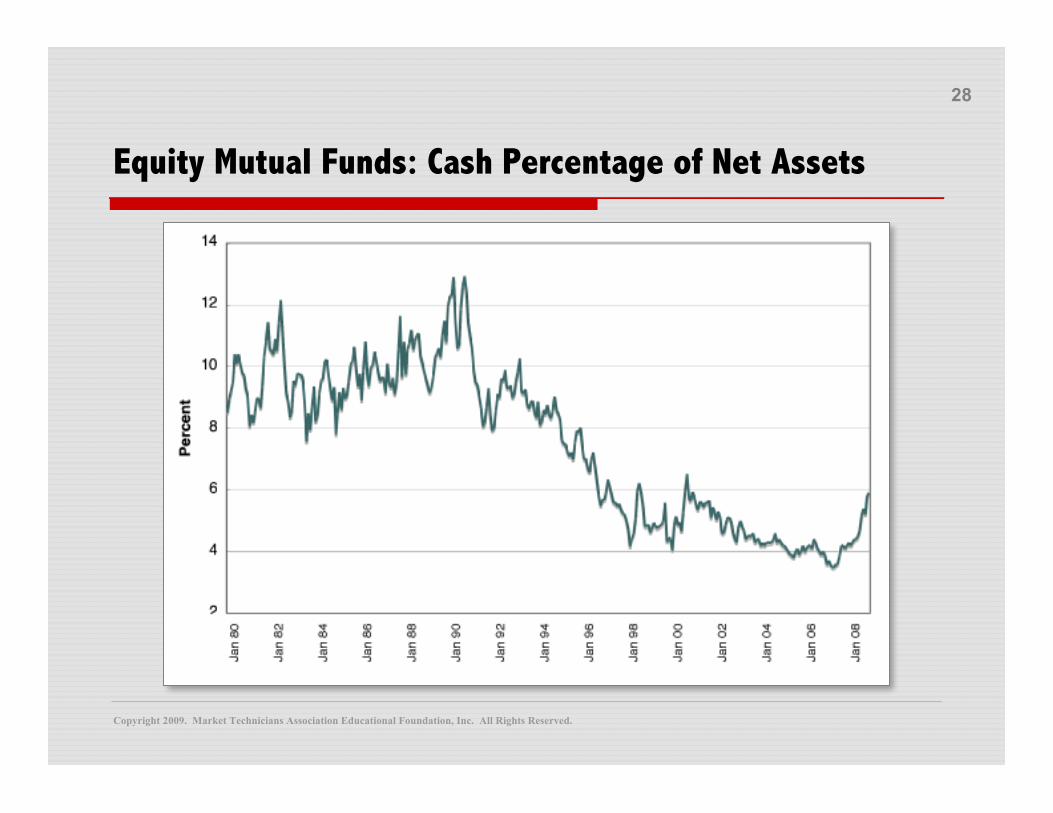

Equity Mutual Funds: Cash Percentage of Net Assets

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

29

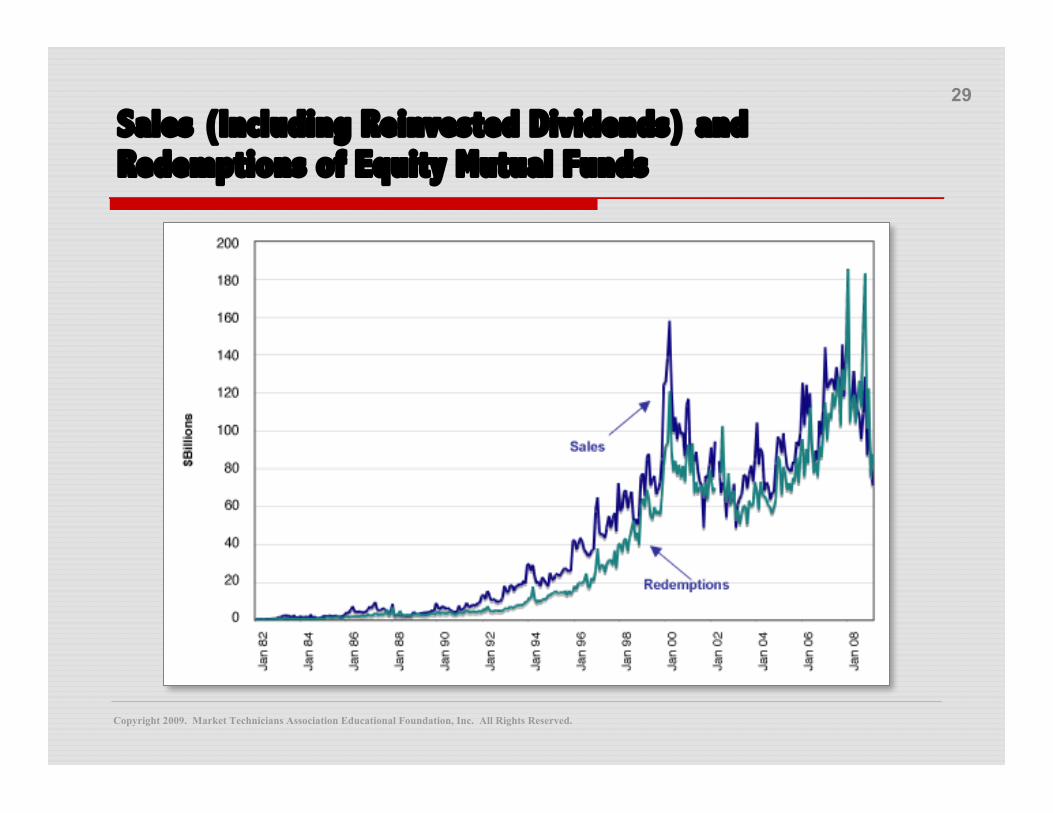

Sales (Including Reinvested Dividends) andRedemptions of Equity Mutual Funds

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

30

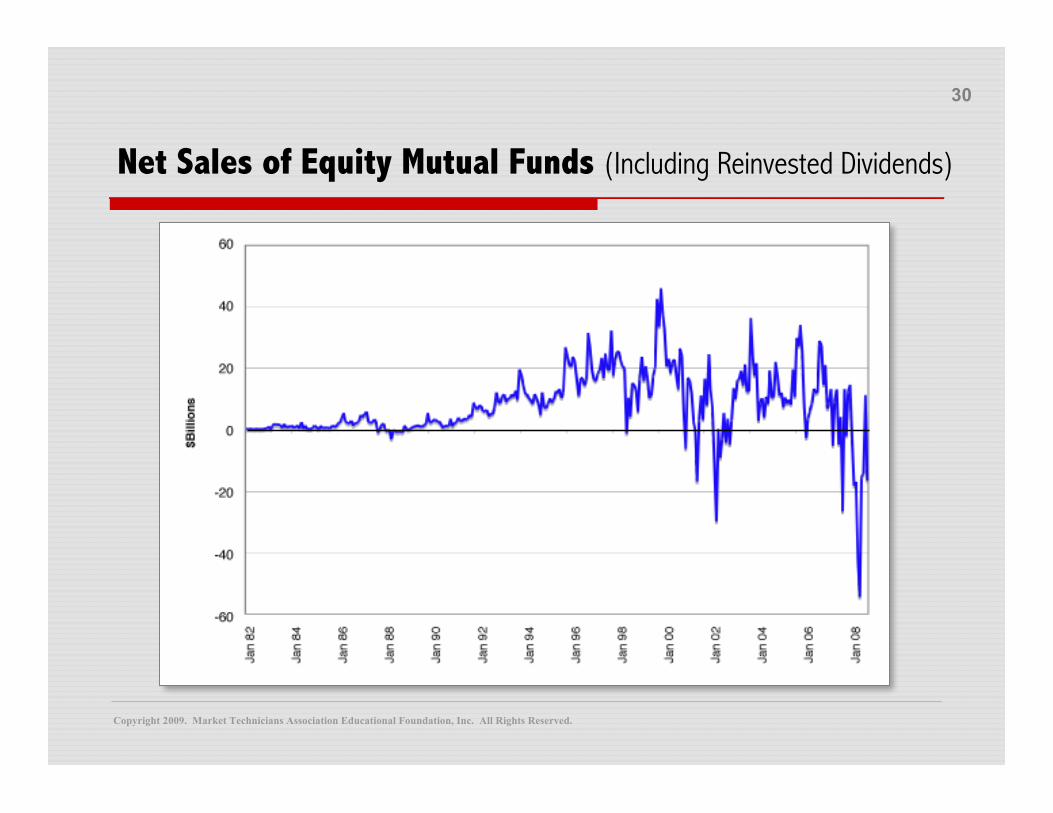

Net Sales of Equity Mutual Funds (Including Reinvested Dividends)

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

31

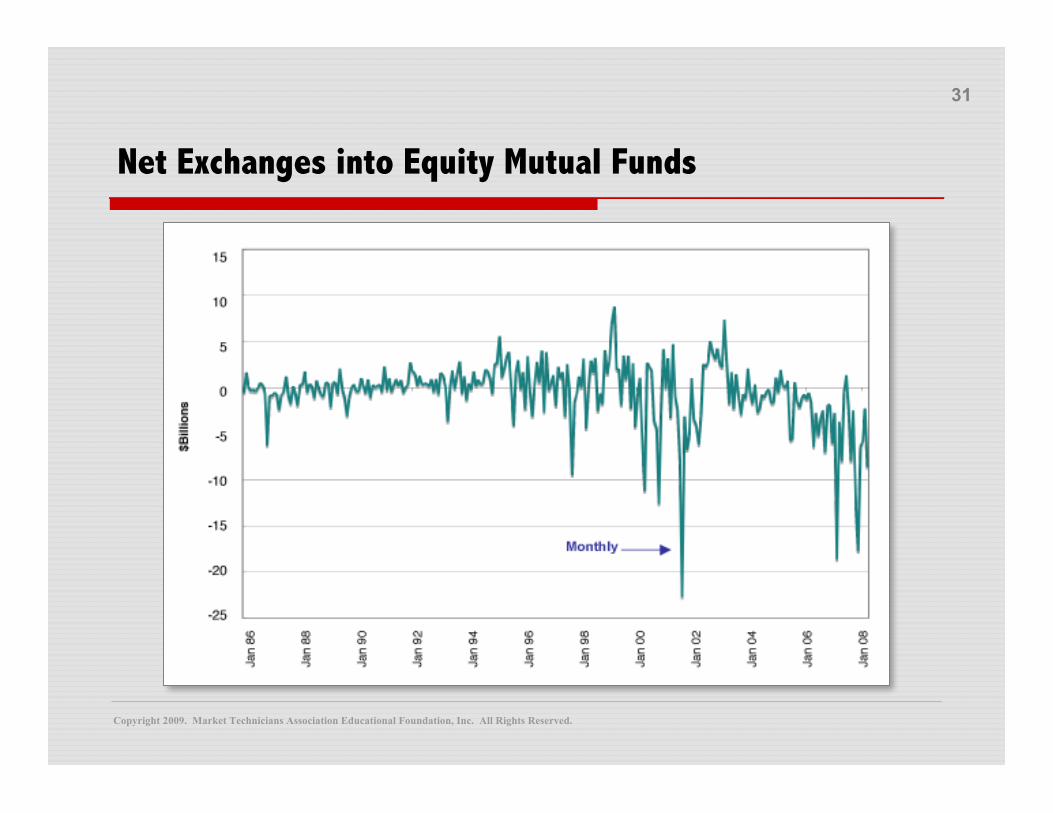

Net Exchanges into Equity Mutual Funds

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

32

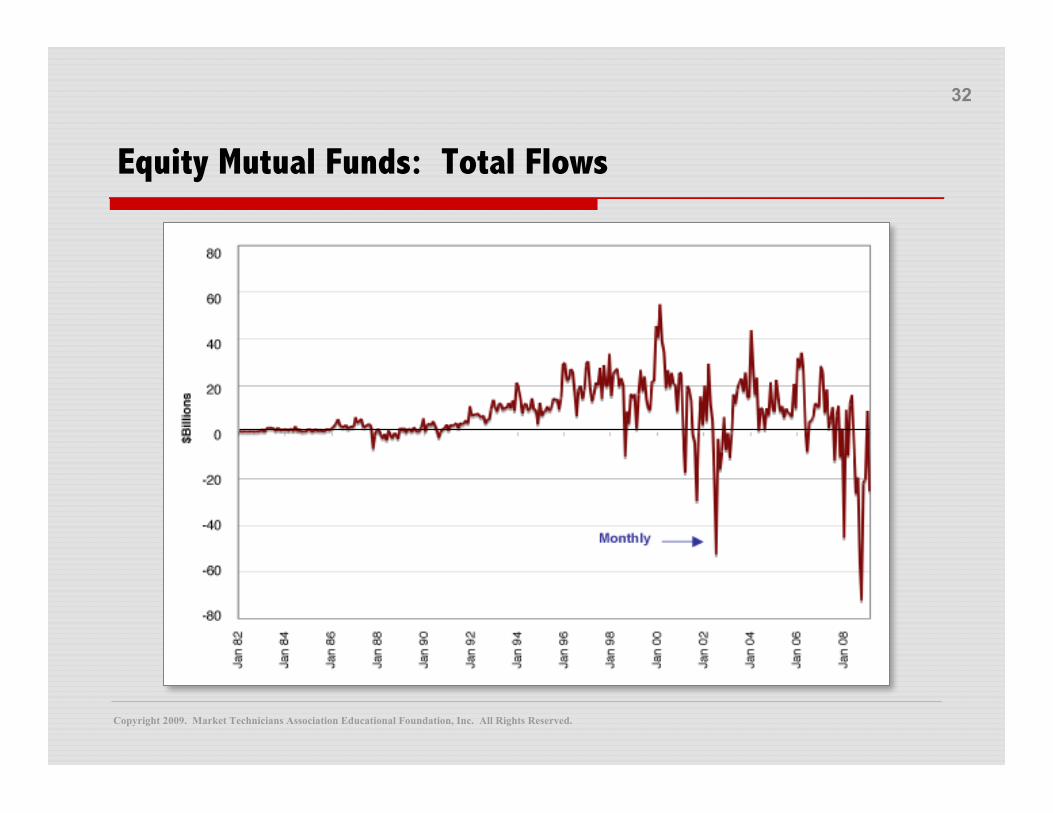

Equity Mutual Funds: Total Flows

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

33

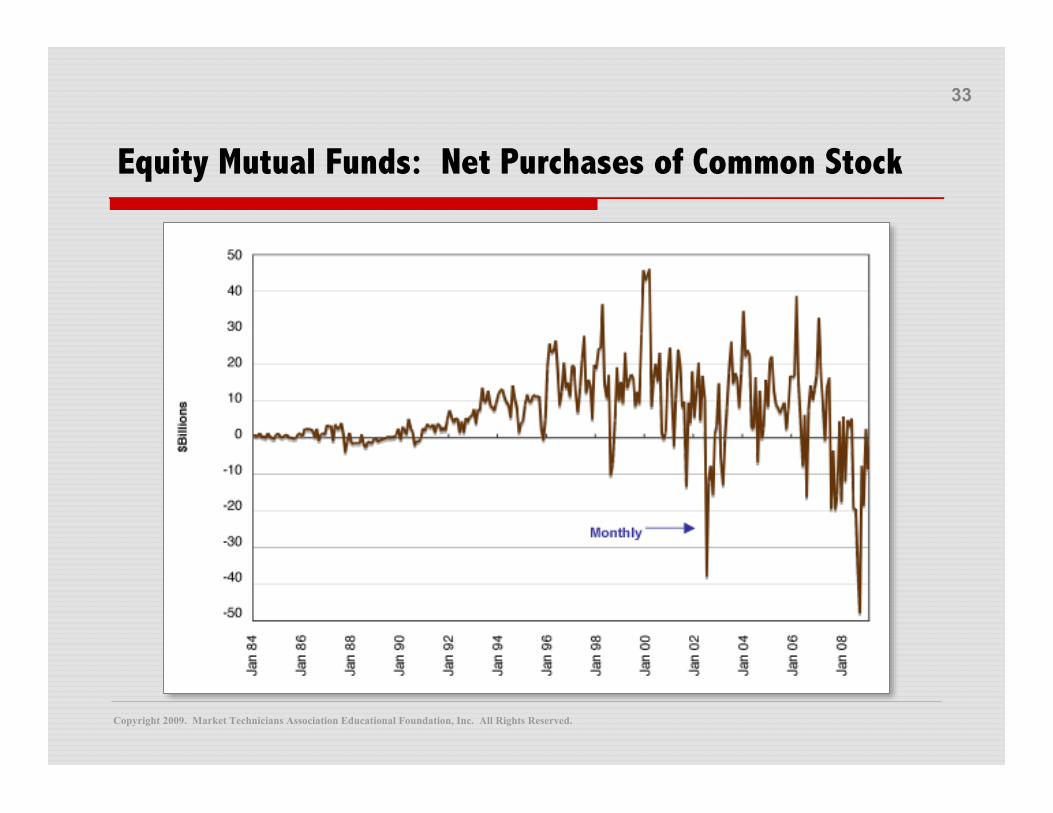

Equity Mutual Funds: Net Purchases of Common Stock

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

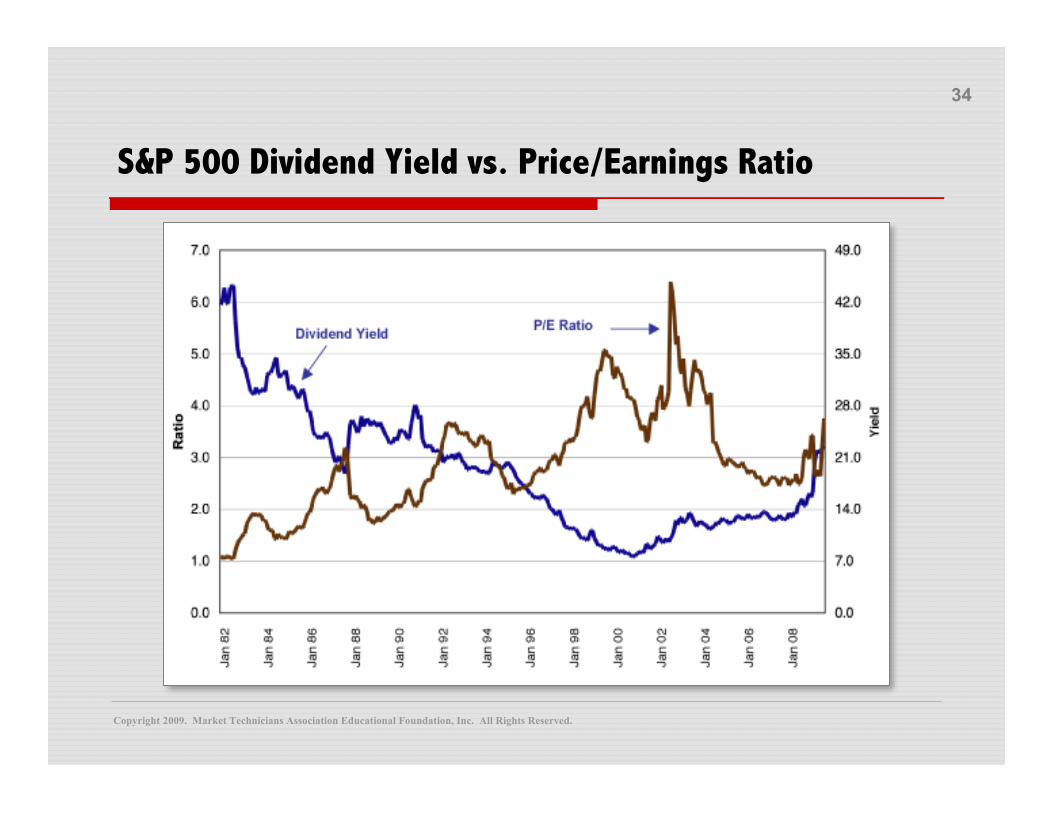

34

S&P 500 Dividend Yield vs. Price/Earnings Ratio

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

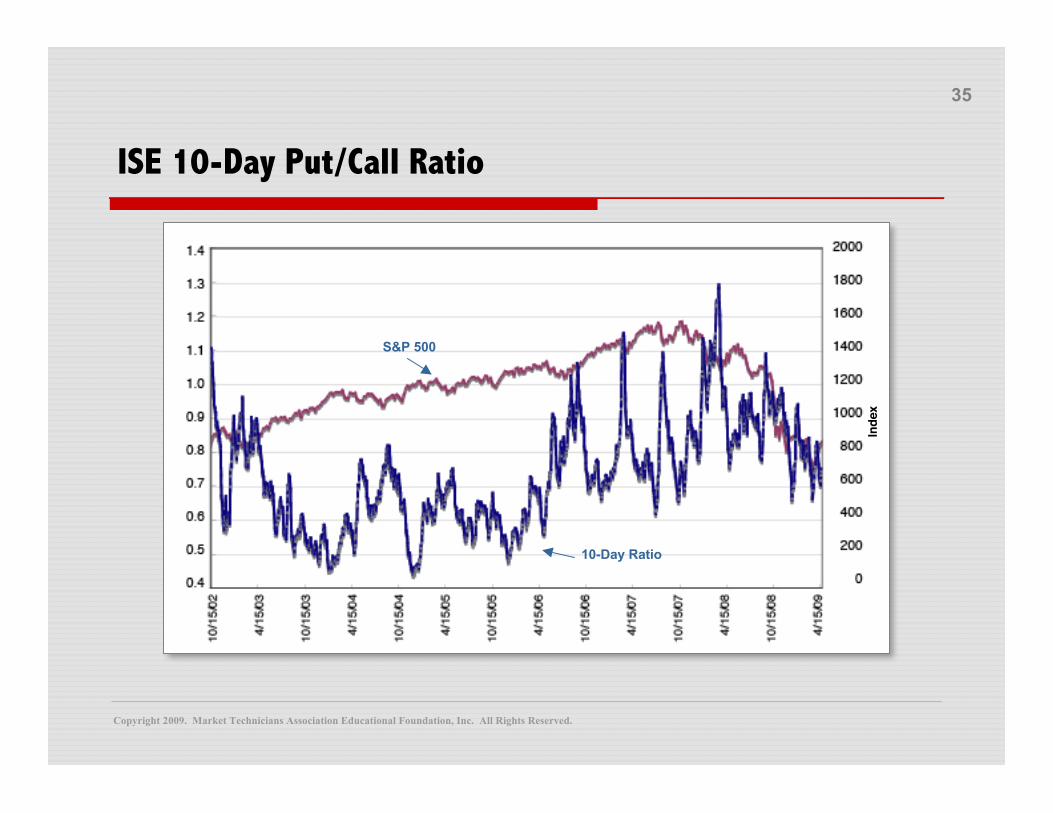

35

ISE 10-Day Put/Call Ratio

Inde

x

S&P 500

10-Day Ratio

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

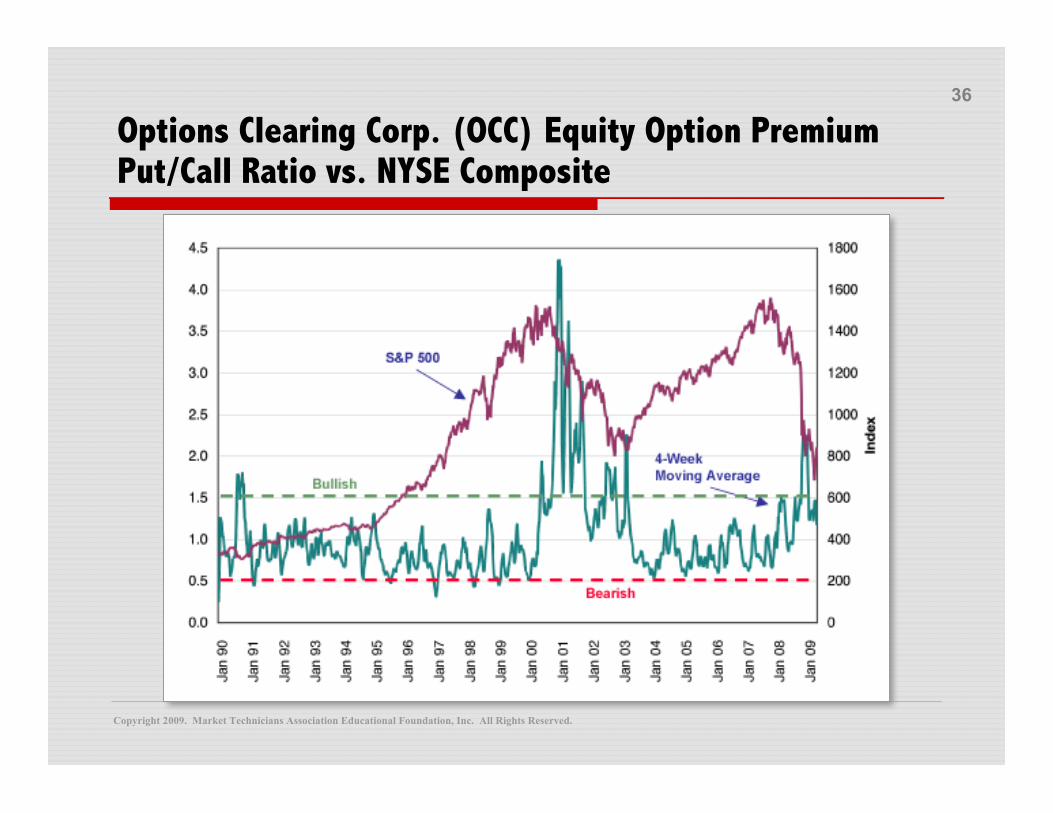

36

Options Clearing Corp. (OCC) Equity Option PremiumPut/Call Ratio vs. NYSE Composite

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

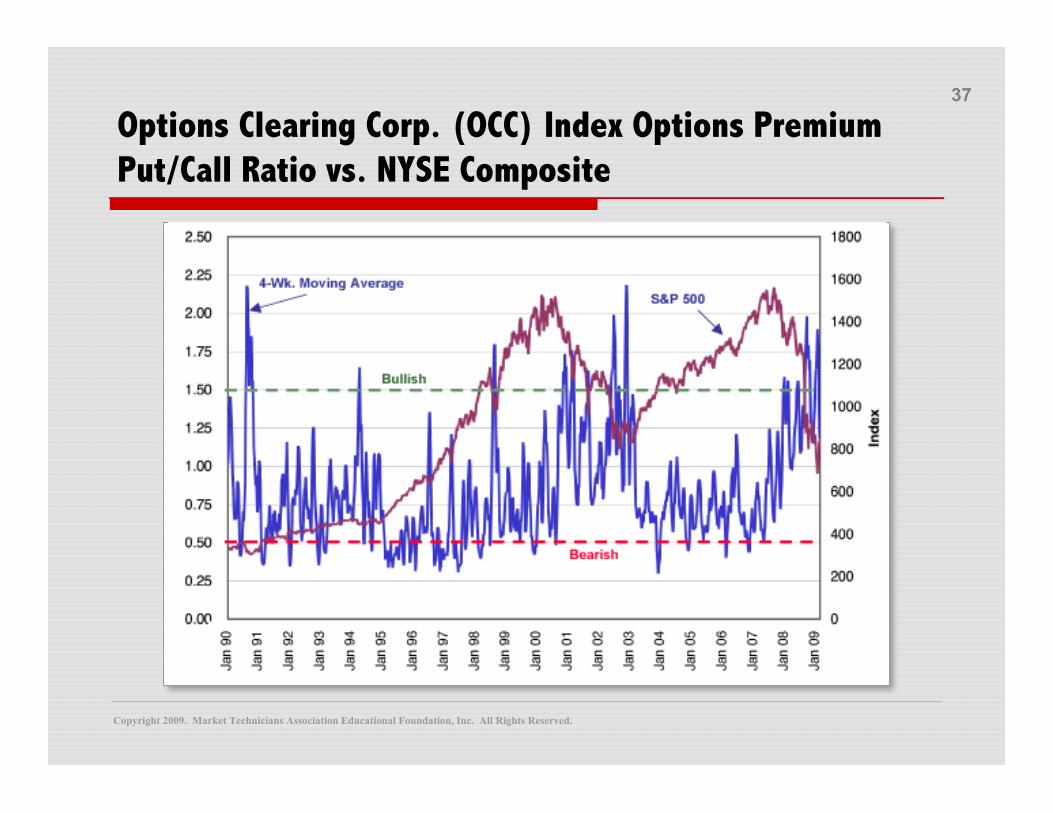

37

Options Clearing Corp. (OCC) Index Options PremiumPut/Call Ratio vs. NYSE Composite

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

38

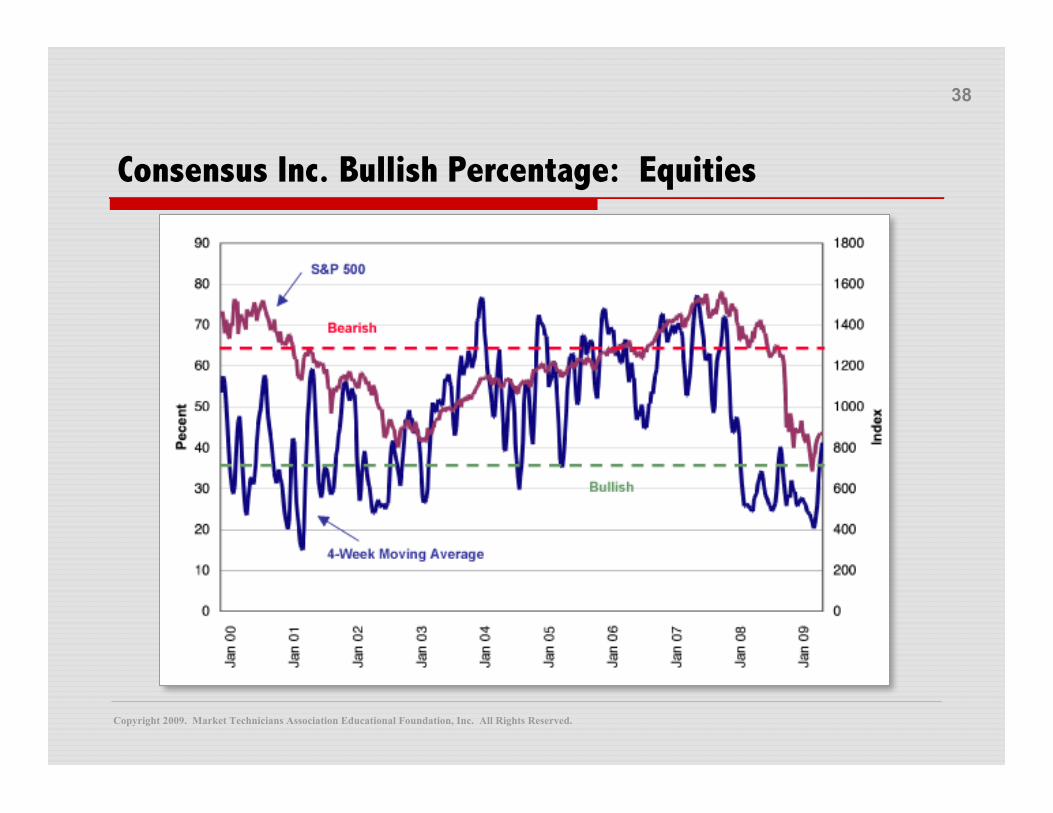

Consensus Inc. Bullish Percentage: Equities

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

39

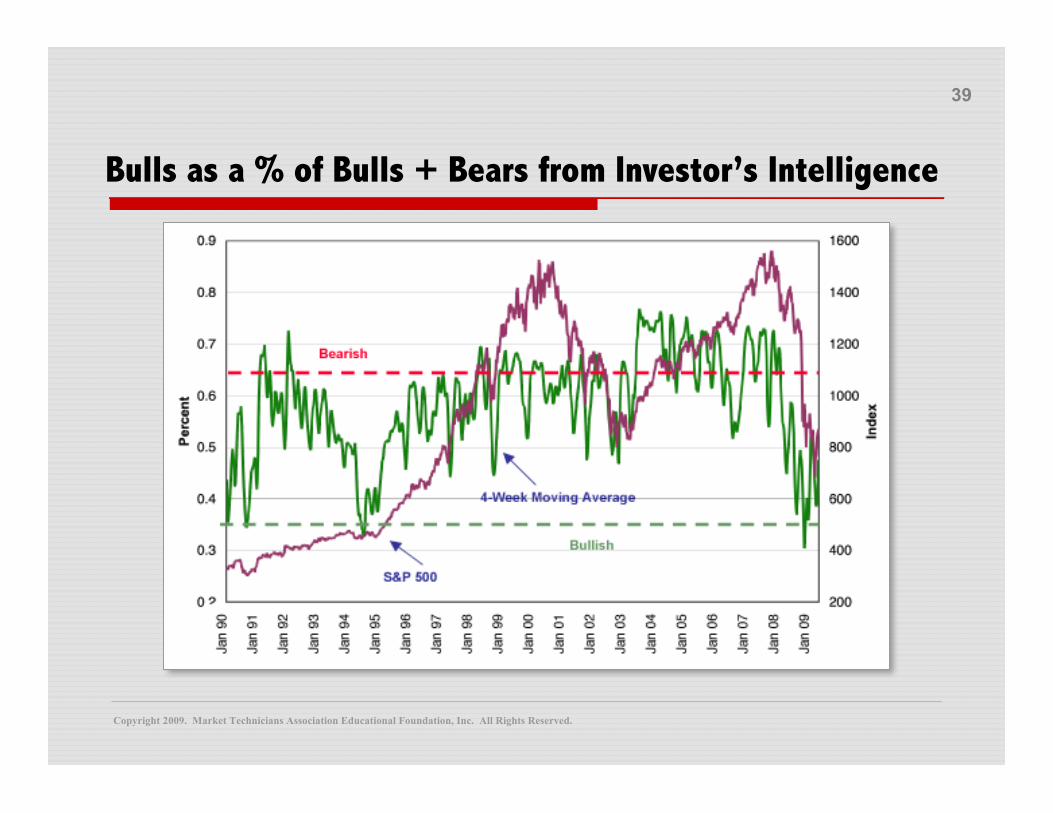

Bulls as a % of Bulls + Bears from Investor’s Intelligence

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

40

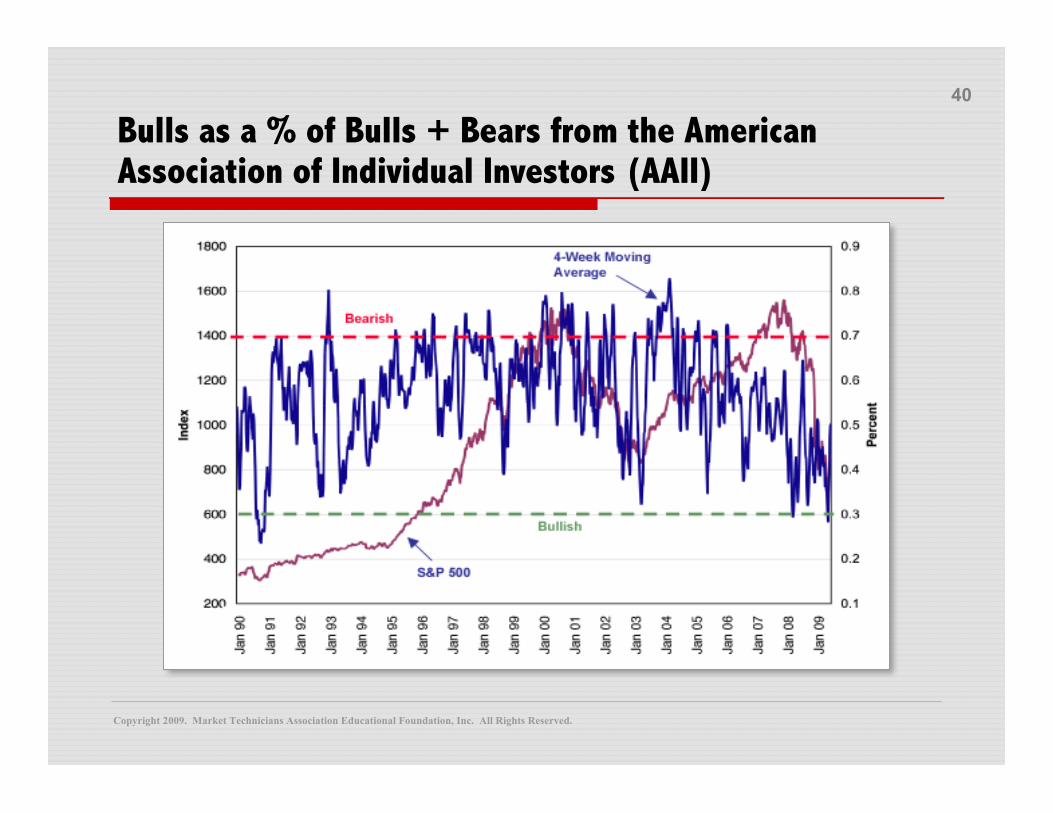

Bulls as a % of Bulls + Bears from the AmericanAssociation of Individual Investors (AAII)

Copyright 2009. Market Technicians Association Educational Foundation, Inc. All Rights Reserved.

41

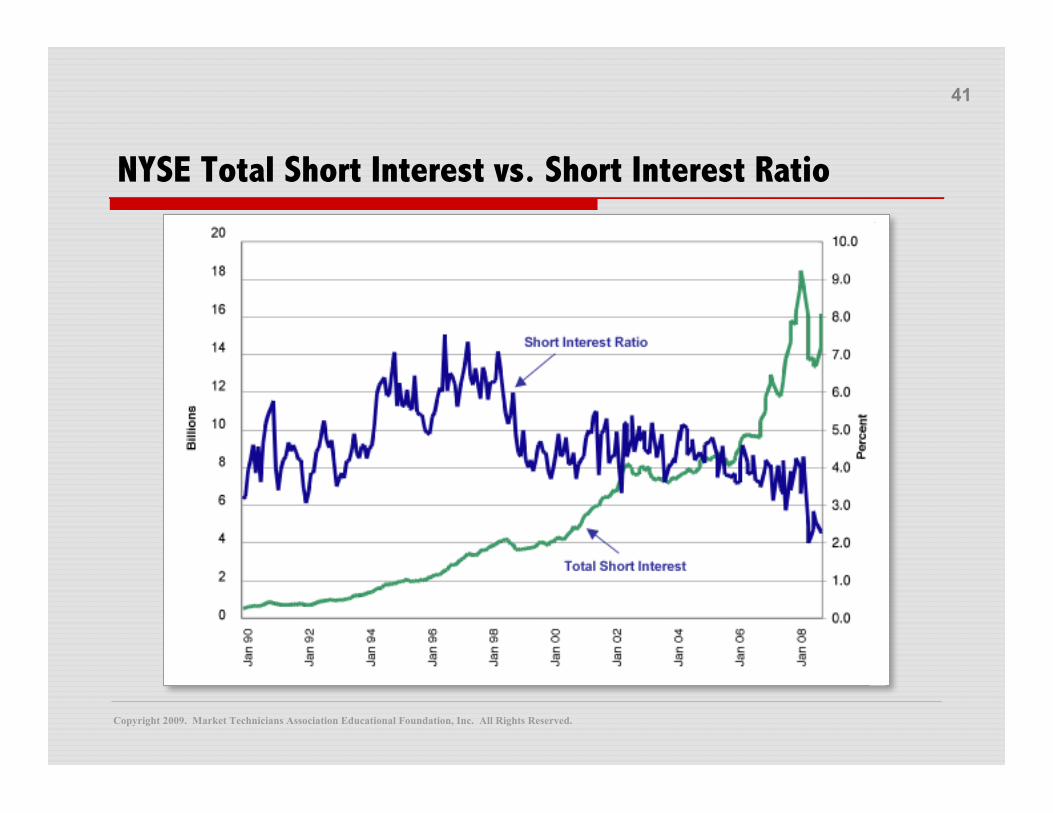

NYSE Total Short Interest vs. Short Interest Ratio