Universal Access and Service Fund (UASF) of Botswana Draft UAS... · Universal Access and Service...

34

In association with Moonstone Capital submitted to Universal Access and Service Fund (UASF) of Botswana First Draft Strategic Plan for the UASF May 2015

Transcript of Universal Access and Service Fund (UASF) of Botswana Draft UAS... · Universal Access and Service...

InassociationwithMoonstoneCapital

submittedto

UniversalAccessandServiceFund(UASF)ofBotswana

FirstDraftStrategicPlanfortheUASF

May2015

TABLEOFCONTENTS

EXECUTIVESUMMARY.......................................................................................I

1 INTRODUCTION..........................................................................................1

2 OBJECTIVES.................................................................................................33 KEYPRINCIPLES...........................................................................................5

4 CURRENTUASSITUATION...........................................................................74.1 VOICECOMMUNICATIONS................................................................................74.2 BROADBANDINTERNET....................................................................................74.2.1 Broadbandnetworkdevelopment.......................................................74.2.2 Broadbandmarket...............................................................................84.2.3 Pricesandaffordability........................................................................84.2.4 Furtherregulatorymeasures...............................................................84.2.5 Institutionalconnectivity.....................................................................9

4.3 BROADCASTING............................................................................................104.3.1 Radio..................................................................................................104.3.2 TV.......................................................................................................10

4.4 POSTALSERVICES..........................................................................................115 AVAILABLEUASFFUNDING.......................................................................13

6 STRATEGICSTREAMS................................................................................156.1 VOICECOMMUNICATIONS..............................................................................156.2 BROADBANDINTERNET..................................................................................166.2.1 Regulatoryenablersandincentivesforfurtherbroadbandroll-out..166.2.2 Connectingschoolsandleveragingfurtherroll-out...........................17

6.3 BROADCASTING............................................................................................266.3.1 Radio..................................................................................................26

6.4 POSTALSERVICES..........................................................................................277 IMPLEMENTATIONPLANQ3/2015TOQ4/2018........................................28

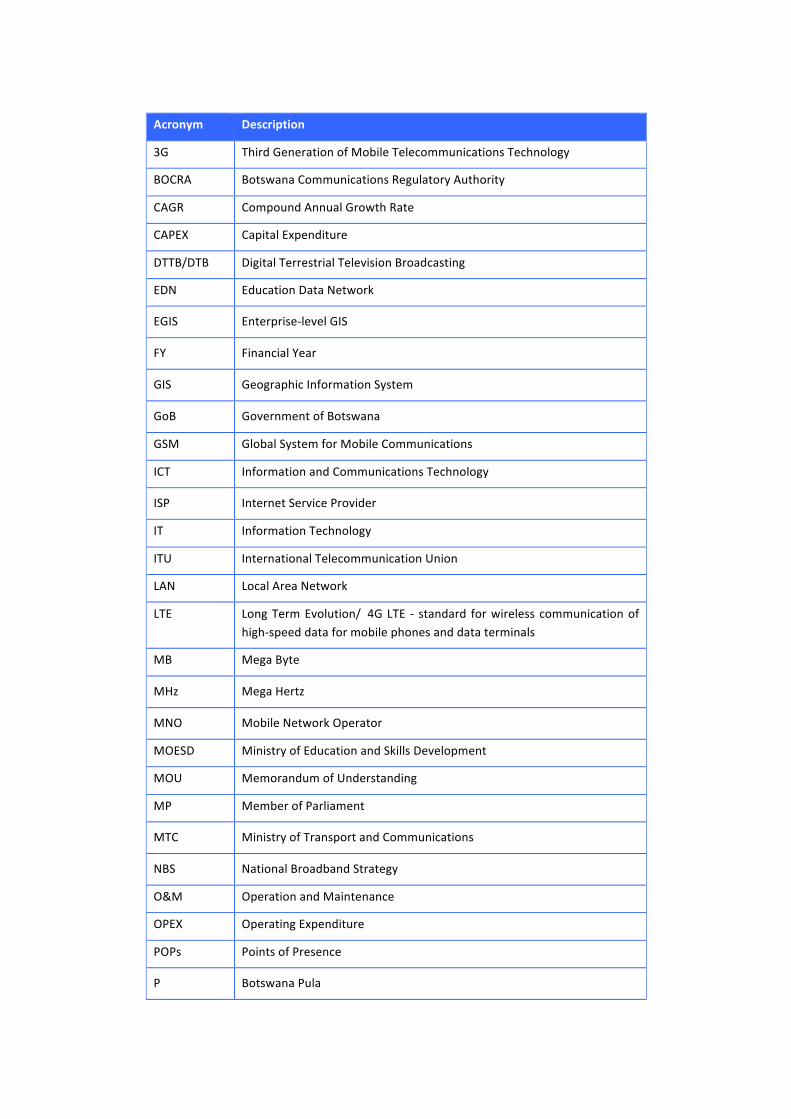

Acronym Description

3G ThirdGenerationofMobileTelecommunicationsTechnology

BOCRA BotswanaCommunicationsRegulatoryAuthority

CAGR CompoundAnnualGrowthRate

CAPEX CapitalExpenditure

DTTB/DTB DigitalTerrestrialTelevisionBroadcasting

EDN EducationDataNetwork

EGIS Enterprise-levelGIS

FY FinancialYear

GIS GeographicInformationSystem

GoB GovernmentofBotswana

GSM GlobalSystemforMobileCommunications

ICT InformationandCommunicationsTechnology

ISP InternetServiceProvider

IT InformationTechnology

ITU InternationalTelecommunicationUnion

LAN LocalAreaNetwork

LTE LongTermEvolution/ 4GLTE - standard forwireless communicationofhigh-speeddataformobilephonesanddataterminals

MB MegaByte

MHz MegaHertz

MNO MobileNetworkOperator

MOESD MinistryofEducationandSkillsDevelopment

MOU MemorandumofUnderstanding

MP MemberofParliament

MTC MinistryofTransportandCommunications

NBS NationalBroadbandStrategy

O&M OperationandMaintenance

OPEX OperatingExpenditure

POPs PointsofPresence

P BotswanaPula

Acronym Description

PPO PublicPostalOperator

PTO PublicTelecommunicationsOperator

RAN RadioAccessNetwork

RFP RequestforProposal

SDH Synchronous Digital Hierarchy - standardized protocols that transfermultipledigitalbitstreamssynchronouslyoveropticalfiber

UAS UniversalAccessandService

UASF UniversalAccessandServiceFund

UN UnitedNations

VAN ValueAddedNetworkprovider

VSAT VerySmallApertureTerminal-atwo-waysatellitegroundstationwithadishantennatypically75cmto1.2minsize

WiFi Local area wireless computer networking technology that allowselectronicdevicestonetwork

WRC World Radio-communications Conference - organized by ITU to review,and,asnecessary,revisetheRadioRegulations, the internationaltreatygoverning the use of the radio-frequency spectrum and thegeostationary-satelliteandnon-geostationary-satelliteorbits

DRAFTSTRATEGICPLANFORTHEUASF Pagei

17May2015

ExecutiveSummaryTheUniversalAccessandServiceFund(UASF)ofBotswanahasthreemainobjectives:

1. To ensure that all Batswana have access to a set of basic yet essentialcommunications services throughout the country at affordable costs – this iscalleduniversalaccessandservice(UAS);

2. To focus its assistance on population groups and areaswhich are beyond thereachofthemarketandtonotdistortthecommunicationsmarket;and

3. Toenablepeopledevelopthecapacitytousecommunicationsservicesandtakeadvantageofitsmanyopportunitiesandbenefits.

In order to fulfill these key objectives the UASF collects a 1% levy of revenues fromdesignatedcommunicationsserviceproviders.TheUASFthendevelopsspecificprogramsand projects to assist in achieving universal access and service, as well as capacitydevelopment.ThisUASstrategysetsoutthespecificstrategicprogramsandtargetsthattheUASFaimstoimplementinthenextthreeyears.The UASF has a starting capital of P90.481.389, a combination of seed funding andsurplus funds fromBOCRA,and the first year levies.Overall accumulated financesoverthenext4yearsareshowninthefigurebelow.

Figure1

Assuming conservative annual revenue growth of 5% per year, the UASF will reachslightly over P230million in FY 2018/2019.However, as the FY 2018/2019 collection isonlycompleteafterthatfinancialyear,theUASFhasatotalofP193millionavailableforthis3yearstrategy.The communications sector comprises the regulated telecommunications, broadcastingandpostalsphereandthustheUASFandUASstrategyalsocomprises

1) Telecommunications,InternetandICT;2) Broadcastingservices;and3) Postalservice.

However,itisimportanttonotethatalmostalloftheUASFfundsarereceivedfromthetelecommunications sector.With the rapiddevelopmentof the Internet, is is themost

DRAFTSTRATEGICPLANFORTHEUASF Pageii

17May2015

dynamicsector,andcapacitybuildingeffortsforthisdigitalinformationage,areurgentlyrequired and promise the highest impact for economic and social development. ThemajorfocusofthisUASstrategyisthereforethebroadbandInternetsector.TheUASFisguidedbythefollowingkeyprinciples:

• Promoting market efficiency and targeting interventions only where marketforcescannotreach;

• Providing smart subsidies that leverage additional investment by serviceproviders,andallowserviceprovisiontobecomesustainableafterUASFfinance;

• Developing market-oriented programs, and subsidise projects that are mostlyimplementedbyoperatorsandserviceproviders;

• Usingcompetitivetenderingforsmartsubsidieswherepossibleandapplytwo-stagebiddingprocess;

• Carefullydecidingifandwhatassistancecanbegivenforthe“trueaccessgap”–areasthatwillneedongoingsubsidies;

• Designingprogramsandprojects in a technologyneutralmanner andallowingserviceproviderstoeinnovativeandchoosethemostcost-effectivetechnology;

• Aiming todesign and implementprojectswith a high impact, especially in theareaofcapacitydevelopment;and

• Workinginatransparentmannerandincloseconsultationwithstakeholders.TheUASF isfairlynewandintheprocessofbecomingfullyoperationalized. Inordertohavebothfastimplementationsuccessandhighimpact, it isrecommendedtofocusforthefirstthreeyearsononemajorflagshipprogram.Afterthesecriticalfirstthreeyears,theUASFcouldincreaseitsprogramsandscopeasrequired.The flagship program of this UAS strategy is computerization of primary schools andprovidingbroadbandconnectivitytoallschoolsthatarelocatedincommunitieswithlessthan 10,000 inhabitants. Therewill be no separate network roll-out project in the firstthree years. Instead increasing broadband coverage will be packaged with the schoolbroadbandconnectivityprogram–i.e.,whereschoolsareoutsideofexistingbroadbandcoverage,theUASFwillprovidefinancenotonlyforthatschool,butassist inupgradingnetworkstoprovidebroadbandcapacityandservicesinthearea.Other UASF activities include providing voice services to around 60,000 unservedinhabitants living in themost remote locationsof thecountry,and increasing radioFMbroadcastingcoverageandavailabilityofthecommercialradiostationstoalmost90%ofthepopulation.Postalservicesremainimportantfortheconveyanceofparcelsandmail,andprovisionofP.O.boxes,amongotherservices.BotswanaPostisthedesignatedPublicPostalOperator(PPO)andrequiredtoprovideuniversalpostalservices.Thissectoristhusfundamentallydifferentasthereisonlyasoleproviderforuniversalservice.Also,severalprovisionsoftheCommunicationsRegulatoryAuthorityAct(CRA)from2012arenotfullyimplementedyet.ThepostalsectoranalysisandpotentialUASFcomponentisconsequentlystillunderdevelopmentandrequiresfurtherengagementwiththerelevantstakeholders.

DRAFTSTRATEGICPLANFORTHEUASF Pageiii

17May2015

Thetablebelowprovidesanoverviewofthe3-yearstrategicgoalsandtargetsofthisUASstrategyandestimatedcosts:

Table1

UASStrategyoverview

Mainprogramactivitypersector

Description Estimatedcosts

(millionPula)

Voicecommunications Provideanestimated60,000inhabitantsinmostremotepartsofthecountrywithvoice

communicationsservices

20

Schoolcomputerization&broadbandInternet

connectivity

Computerization/ITteacherfor234PrimaryschoolsinCluster3and2

81.8

Broadbandconnectivityfor94Secondaryschoolsand234PrimaryschoolsinCluster3and2

76.3

Broadcasting

Increasebroadcastingcoverageofcommercialradiostationsfrom60%ofpopulationupto90%of

population

1.0

Postalservices Thisisstillunderdevelopment

Totalprogramcosts 179.1

Contingency/Reserve 13.9

Est.totalavailableUASFfinance 193

DRAFTSTRATEGICPLANFORTHEUASF Page1

21May2015

1 IntroductionWhyuniversalaccessandservicemattersCommunicationhasalwaysbeen important for societies. In thedigital informationage,communications services – whether they are voice communications or broadbandInternet, the mass media of TV and radio, or postal communications – have becomeindispensibleformodernlife.Theyarecrucialforgovernments,businessandindividualsalike,bothforeconomicgrowthandsocialdevelopment,aswellasforthefunctioningofademocracy.Inaliberalisedcommunicationsmarket,theprivatesectorandcommercialoperatorsarelargely responsible to invest in infrastructure anddeliver communications services to acountry, while the government sets policies and the industry regulator, the BotswanaCommunicationsRegulatoryAuthority(BOCRA),overseesandregulatesthemarket.However,eachcountry, includingBotswana,willhavepopulationgroupsandareas– inparticularlowerincomegroups,disadvantagedpeopleandruralareas–whichcannotbeserved by the market or it will take too long until they are served. Further, with theadvent of broadband Internet and the infinite possibilities it offers for information,content, applications and services, the individual capacity to harness and benefit fromthese opportunities has become critical. As such, capacity building, especially ininstitutionssuchasschools,hasbecomecriticalandurgent,andcannotbepostponed.In recognition of these issues and the importance of communication services,governments intervene to secure universal access and service of a set of minimumcommunicationsservicesforalltheirinhabitants,regardlessoflocation,incomeorotherissues such as disability – this is called Universal Access and Service (UAS). Over 90countriesworld-widehave chosen to set-up specificUAS funds to finance andmanagetheprovisionsofUASandcapacitybuilding,ashasBotswana.Botswana’sUASFIn2006and2007,thethenBTAundertookastudyandconsultationonuniversalaccessand servicepolicies,which resulted in the inclusionof importantUASprovisions in theCommunications Regulatory Authority Act No. 19 of 2012 (CRA Act): Section 5 (1) (b)which gives the Botswana Communications Regulatory Authority Board (The Board)administrative responsibility to promote and ensure universal access with respect toprovisionofCommunicationServicesinBotswana.TheCRAActfurtherprovides,throughsection5 (1) (c), for theBoard to imposeaUniversalAccess andService (UAS) levyonidentified operators for purposes of funding universal access in the communicationssector.In linewith theAct, theBOCRABoardestablishedaUniversalAccess andService Fund(UASFor the Fund) inApril 2014,which ismanagedbyan independentUASFBoardofTrustees.BOCRAservesastheSecretariattotheUASF.TheoverallobjectiveoftheUASFistofacilitateanenablingenvironmentforthedevelopmentanduseofcommunicationinfrastructureandservicesinBotswana,particularlyinunderservedandunservedareas.RelationtootherpoliciesTheTelecommunicationsPolicyof1995andtheICTPolicyforBotswana(Maitlamo2007)identifyexpansionofnetworksandservicestoreachthewholepopulationastheprimary

DRAFTSTRATEGICPLANFORTHEUASF Page2

21May2015

goal of the communications industry in the country. The goal of universal access andservice to communications is closer to realisation in the more urbanised parts ofBotswana, while the provision of services in rural areas is still a challenge. This UASstrategyistoassistinachievingthesenationalgoals.The Botswana National Broadband Strategy (NBS), developed in 2013, sets out theobjectives, targets, principles, and mechanisms to achieve country-wide broadbanddevelopment and penetration, within the market context and priorities of theGovernmentandpeopleofBotswana.Assuch,itcontainsalreadymanydirectivesfortheUASstrategyandthisstrategyhasbeendevelopedinalignmentwiththeNBS.While the NBS has formulated a comprehensive set of measures to achieve nationalbroadbanddevelopment,addressinganenablingbroadbandecosystem,thedemandandsupply-side, this UAS strategy is focused on a very specific sub-part of broadbanddevelopment–theruralandunservedareasandbuildingdigitalliteracy.ScopeofUASstrategyAccording to thedefinitions in theCRAAct2012 thecommunications sector comprisesthe“aggregateregulatedtelecommunications,broadcastingandpostalsphere”andthustheUASFandUASstrategyalsocomprises

4) Telecommunications,InternetandICT;5) Broadcastingservices;and6) Postalservice.

However,itisimportanttonotethat:• Each UAS strategy needs to be seen in very close context to the specific overall

sectorpolicyandmarketsituation;and• UAS,whileacommonconcept, isactuallydefinedquitedifferently ineachofthese

sectors.Therefore the UAS approach for the sectors aredistinct, and each sector is addressedseparatelyinthefollowingUASstrategy.

DRAFTSTRATEGICPLANFORTHEUASF Page3

21May2015

2 ObjectivesThissectionsetsoutthemainobjectivesoftheUASF,aswellasthestrategicgoalsofthisUAS strategy. It also provides a more detailed explanation of universal access anduniversalservice,alsoinlightoflatestinternationaltrends.TheUniversalAccessandServiceFund(UASF)ofBotswanahasthreemainobjectives:

1. To ensure that all Batswana have access to a set of basic yet essentialcommunications services throughout the country at affordable costs – this iscalleduniversalaccessandservice(UAS);

2. To focus its assistance on population groups and areaswhich are beyond thereachofthemarketandtonotdistortthecommunicationsmarket;and

3. Toenablepeopledevelopthecapacitytousecommunicationsservicesandtakeadvantageofitsmanyopportunitiesandbenefits.

ThegoalofUniversalAccessistoensurethat,intheshorterterm,allpeopleineverypartof thecountryhavereasonablemeansofaccess tobasicandessentialcommunicationsservices (including broadcasting, postal, Internet or telecommunications) in theircommunity. Thisdoesnotnecessarilymean individual serviceor service in their home,but instead the minimum required for universal access is shared use, such as publicpayphones or phone shops, postal outlets, broadcasting coverage and various types ofInternetcafes(orKitsongcentres).Basic andessential communications servicesmeans a set ofminimumcommunicationsserviceswhichareconsideredsoessentialthateverybodyshouldhaveaccesstoitortheserviceprovided.Ameasureofhowessentialaserviceis,iswhetherthelargemajorityofthepopulationhasit,andthefewwithoutitwouldbeexcludedanddisadvantaged,andcouldnotparticipateineverydaysocialandeconomicactivities.This is reflected in the term Universal Service: it recognizes that once the marketpenetrationofacommunicationsservice–suchasthetelephone–reachesahighlevelinsocietyandhasdemonstratedsocialandeconomicvalue,thenthatservicehasbecomeessential tovirtuallyeveryhousehold.Asa consequence,exclusion fromhavingprivateaccess to the service would place citizens at a social and economic disadvantage.Universalservicethussetsthetargetoftheprovisionofbasiccommunicationsservicestoeveryhousehold in thecountry.Whereas it is recognized that thisgoalwillbe reachedonlyinstagesandwillberealizedinmoreurbanizedandleastremoteareasfirst,itisthemediumtolongtermgoalforthewholecountry.Further, universal access and universal service have several dimensions and thus theUASFhastheobjectivetosupportandassistintheachievementofthefollowing:

a) Availability-thelevelofthebasicandessentialcommunicationserviceshouldbeavailableforalluserswithoutgeographicaldiscrimination;

b) Accessibility-all inhabitantsshouldbetreatedinanon-discriminatorymanner with respect to being able to access the communicationsservice,inallplaces,withoutdistinctionofrace,sex,religion,disability,etc;and

c) Affordability - the price of the basic communications services shouldnotbeafactorthatlimitsserviceaccessforallusers.

DRAFTSTRATEGICPLANFORTHEUASF Page4

21May2015

With the rise of the Internet, especially the possibilities of broadband Internet, theunderstandingofuniversalaccessandservicehasexpanded.Whileitissufficienttohavetelecomserviceavailable,accessibleandaffordableinordertouseit,broadbandInternetrequiresalsoanindividualscapacitytouseitaswellastheknowledgeaboutitspotentialtangible benefits to be interested to use it. Thus the capacity building function ofuniversal access and service strategies has hugely increased in importance. Also, theimportanceofavailablecontentandapplicationshasincreasedthoughUASFsusuallyplaya lesser role in that area as there are often national programs such as broadbandstrategiesandotherinstitutionswhichaddresscontentandapplications.Theconnectionsamongvariousunderlyingelements – infrastructure, capacity, content&applications –andwhattheyfacilitate–access,usageandbenefits-isshowninthefigurebelow:

Figure2

Specific definitions of universal access and service for the four sub-sectors ofcommunications services - broadcasting, postal, Internet or telecommunications – aredefinedinthecontextofthecurrentsituationandthestrategyinsections4and6.ThisUAS strategy is a high-level three year strategy. Its starts inQ3of 2015, and thencontinues for the three financial years of the UASF: 2016/2017, 2017/2018 and2018/2019.ThisUASstrategyaimsatimplementingprogramsandprojectsearlyandcreatingimpactand benefits. However, there is typically a natural learning curve as a UASF getsoperationalized andmany things have to be developed and done for the first time. Inordertoachieveearlyprojectimplementationandimpact,theUASstrategyhasselectedaclearprogramfocusforthefirstthreeyearsatleast.ThisUAS strategy does not provide detailed individual projects, but instead provides aclear strategic theme and focus, and practical guidelines for developing andimplementingthespecificprojectsinthenextthreeyearsandinsomecasesbeyond.

DRAFTSTRATEGICPLANFORTHEUASF Page5

21May2015

3 KeyprinciplesThe UASF and this UAS strategy is to be implemented according to the following keyprinciples,basedonbestinternationalpractice.MarketefficiencyandtargetedinterventionsThe UAS strategy is implemented within a multi-player, commercial marketplace, inaccordancewith the broader policy objectives of theGovernment. TheGovernment ofBotswana (GoB) continues to be committed to foster efficientmarket operation, a faircompetitiveenvironmentandoverallsectorexpansion,andtoremoveanyregulatoryorother barriers to the operation of an efficient market. Targeted interventions andfinancialaidfromtheUASFwillonlybeusedasameanstoprovidesupportinareasandforusergroupswhereefficientmarketforcesalonecannotprovidethedesiredservices.Thisalsomeans thatUASF fundingwillnotbeused inanenvironmentwherea lackofsectorreformhasresultedinverycostlyservices.SmartsubsidiesandsustainabilityTheconceptofthesmartsubsidy istoencourageoperators,serviceprovidersandtheirinvestors to provide certain communications services with the objective of ultimatelyseeingtheprogrambecomecommerciallyviable.TheFundistodevelopmarket-orientedprograms, and subsidise projects that will be mostly implemented by operators andserviceproviders.Alsoincaseswherecommercialviabilityisnotpossibleorcannotbeimplementedbytheindustry,theUASFistoconsiderandensurelong-termsustainabilityofprojects.TheUASFshallusethesmartsubsidyapproachasmuchaspossible.Smartsubsidiesreferto subsidies given to rural and high cost areas, or low-income population groups andservice targets which will not be reached by the market alone, even in an efficientmarket,oratleastnotforalongtimetocome.Targetedfinancialinterventionisrequiredbeyond normal regulatory measures and incentives to provide services to thesepopulationgroupsandareas.Asmartsubsidy isdesignedtonotdistortthemarket,andencourages cost minimization and growth of the market. It typically is only a part ofrequiredcapitalfortheproject,forexample30-50%,andhelpsto"kickstart"aprojectorservice,andleveragesadditionaloperatorandserviceproviderinvestment.Theultimateobjective of giving a smart subsidy is that the project becomes commercially viable,whereaswithoutthesubsidyoperatorsandserviceprovidersmighthavebeenreluctanttoinvest.Usingthesmartsubsidyapproach,serviceswillthusbecommerciallyviableinthemediumtermwithoutfurther,ongoingfinancialsupport.CompetitivetenderingforsmartsubsidiesThemechanismtoselectanoperatororserviceprovidertoreceiveasmartsubsidyandprovidedefinedservicesinadefinedtargetareaorforspecificcustomersisusuallythatofapublic,transparentandcompetitivetender.TheUASFshoulduseacompetitivetenderingapproachforthe leastamountofsubsidyrequested for service provision from qualified bidders. This does not involve anyweightingbetweenthetechnicalandfinancialproposal,butisatwo-stageprocesswhereasealedtechnicalproposalandasealedfinancialproposalgetsubmitted:

• Firstthetechnicalproposalgetsopened.Herebiddershavetoqualifyfirst.Thisincludesstringentcorporateandfinancialqualification,andsubstantialtechnical

DRAFTSTRATEGICPLANFORTHEUASF Page6

21May2015

andoperationalcompliancewiththeservicespecifications.AgainsttherequiredtechnicalandothercriteriapublishedintheRFP,asimplepassorfailevaluationtakes place. Only bidders that pass the technical evaluation, proceed to thesecondstage.

• Second, qualified bidders have their separately and sealed financial proposalopened.Amongthesequalifiedbidders,thebidderwiththe lowestrequestforsubsidyisawardedtheproject.

Further, a maximum allowable subsidy is to be set so as to avoid unreasonableexpectationsfromtheindustryandincreasecostminimizationeffortsandinnovativeuseoftechnology.Winning bidders will sign a time-bound service agreement, often three to five years,agreeingtoaonce-onlycashsubsidythatwillbedisbursedovertimeastheymeettheirservice installation and/ or build-out requirements, and their service obligations. Theserviceagreementhasstringentpenaltiesifservicestonotmeettherequirements.Anynetworksdeployedforprovidingtheservicesremainownedbytheoperators.ThetrueaccessgapThe true access gap comprises areas or communications targets that are beyond anycommercial viability, even in instances where initial smart subsidies are given.Commercial sector operators or service providers serving these areas would needongoing financial support, possibly in the form of operating subsidies. It is a politicaldecision and one of available financial resources, if and to what extent to subsidiseongoing service provision to areas, institutions such as schools, and population groupsthatarebeyond the limitsof thesmart subsidyzone.TheUASF is tocarefullydecide ifand what assistance can be given for the “true access gap” – considering that theseprojectswillrequireongoingsubsidies.Creatingmaximumsocio-economicimpactTheUASFmustaimtodesignandimplementprojectswithahighsocio-economicimpactandvalue,especiallyintheareaofcapacitydevelopment.Thisincludesconsiderationsofhowmanypeoplecanbeimpacted,andthequalityandlastingeffectsofthatimpact.TheUASFshallaimtomaximiseitsresourcestoprovidehighqualityimpactandbenefitstoasmanyunderservedpeopleaspossible.TechnologyneutralThe UASF mechanisms must enable the most effective, efficient and appropriatetechnologiestobeimplementedforUniversalAccessandUniversalService.Byensuringatechnology neutral approach in the competitive tendering process, theUASFwill allowtheoperators tochoose themostcost-effectiveandappropriate technology toprovidecommunicationsservices.TransparencyandstakeholderconsultationTheUASFwillbeoperatinginanopenandtransparentmannerby

a) invitingstakeholderinputintostrategy,programandprojectdevelopment;andb) publishing,asaminimum,annualreportsthatprovidedetailsoffundscollected,

fundsdisbursed,towhichoperatororserviceprovider,statusandachievementsofprojectsandserviceprovision,successesandproblemsencountered.

DRAFTSTRATEGICPLANFORTHEUASF Page7

21May2015

4 CurrentUASsituation4.1 VoicecommunicationsConsidering its largeterritoryandscatteredruralpopulation,Botswanahasmadegreatstrides in regards to achieving universal service for voice communications. Mobileteledensitystoodat158%attheendofMarch2014.Whilethisincludesbusinessphonesand many Batswana also have multiple SIM cards to take advantage of preferentialtariffs, it is reasonable toassume thathouseholdshave telephoneservice inareas thathaveexistingservice.Mobilecoveragewasestimatedtocover80%ofthepopulationattheendof2006,andthemarkethascoveredsubsequently88%ofthepopulation.Thisleft approximately 12% of the population, i.e., just over 200,000 persons, outside thecoverage range of the mobile operators. The majority of these Batswana lives in 197villageswithapopulationofover130,000.Thesewerethensubsequentlyservedthroughthe implementationof theNteletsa IIprojectwhichstarted in2009/2010andwas fullyimplemented at the end of 2011. Nteletsa II was quite successful in covering thosevillagesbutalsoquite costlybyoffering topay for80%of the costs–average costsofprovidingservicesinall4areaswasP3,143perperson.Thetwomobileoperatorshavingbeen chosen through the competitive tender to implement the Nteletsa II project,Mascom and BeMobile, have benefitted by being able to extend their populationcoverage. Their population coverage is estimated to be today at 95% each, which hasbeenconfirmed.Astheircoveragedoesnotcompletelyoverlap,itisasaveestimatethatapproximately3%orlessofpopulationhasnovoiceservicestoday.Thus,around60,000Batswanahavenovoiceservicestoday.Thisisincommunitieswithlessthan250peopleand can be considered the “true access gap” – meaning these places are chronicallycommerciallyunviabletoserve.Conclusion: To achieve universal service for voice communications in Botswanaapproximately60,000Batswananeedtobeconnected.

4.2 BroadbandInternetThebroadbandInternetmarketisstilldevelopingandexpanding.ManyofthemeasuresrecommendedintheNationalBroadbandStrategy(NBS)haveeitheronlyrecentlybeenimplementedorstillneedtobeimplemented.Timeisneededforthesemeasurestotakeeffect and have an impact in terms of broadband network expansion, price reductionsandsubsequentbroadbanduptake.

4.2.1 BroadbandnetworkdevelopmentBothfixedandwirelessbroadbandnetworksareexpandingsubstantially.BoFiNet, established in 2012, has recently receivedmajor government fundingof P400milliontoexpandandimproveitstransmissionnetworks.Ithas105SDHsitesaroundthecountry, 34 broadband wireless sites and planned 81 more sites by mid-2015. This isrespondingtotheincreasingdemandbytheretailproviders,especiallythethreeMNOs,who require BoFiNet transmission, the upgrade of existing capacity on heavy trafficroutesandimprovedcapillarityofthenetworkthroughoutthecountry.

DRAFTSTRATEGICPLANFORTHEUASF Page8

21May2015

Thereisnow3Gcoverageofat leastonemobileoperator inallvillageswithmorethan5,000 population; population coverage of 3G is at least 70%. In 2015, LTE has beenlaunchedandrolledoutbyatleastoneoperatorsandothersaresoontofollow.However, this means that there is essentially no mobile broadband (3G) coverage inCluster 1 (locations with 500-1,000 inhabitants) and Cluster 2 (locations with 1,000 to5,000 inhabitants) today. The lack of grid-power from BPC in some of these locationsincreasesthecostofrollingoutbroadband.

4.2.2 BroadbandmarketThedevelopmentofthebroadbandmarkethasprogressedinthelastcoupleofyears:

• InMarch 2015, mobile Internet subscriptions surpassed 1 million subscribers,equivalentto30%ofallsubscriptionsandequivalentto49%ofthepopulation.However, as thisalso includesbusiness subscriptionsandmultipleSIMownerswhich also likely include double data subscriptions, individual mobile internetsubscriptionsareverylikelybetweenthosetwofigures,morethan30%butlessthan49%.

• Mobile data revenue as percentage of total revenue of operators has overallroughlydoubledoverthepasttwoyears.

• Mobile Internetgrowth is at least above20%CAGRbetweenendof2012andendof2014,whichis in linewithinternationalmobilebroadbandgrowthratesindevelopingcountries.1

• The fixed mobile broadband has also grown and at a minimum doubled itssubscribernumbersbetween2012andendof2014.

4.2.3 PricesandaffordabilityThe 2014 Affordability Report2 mentions Botswana as one of five countries that havemadeprogressintheireffortstoreduceInternetaccesspricesbetween2013and2014,whilepricesinmanyothercountriesremainedrelativelyconstant.Prices for wholesale national transmission and backbone decreased by around 70% to80%between2011and2014.3While mobile broadband is still considered quite expensive, there are several prepaidbasicentryoptions fromoperatorsthatallow lower-incomeusers toreceive low-pricedInternetaccess,forexample15MBforP9.50,150MBforP20(tobeusedin2days)and20MBforP6(promotion).Amongdeveloping countries, only 23 countrieshaveachieved theUnitedNations (UN)5%entry-level target (i.e.,mobilebroadbandentrypricescost less than5%of income).Botswana is ranked27th and itsmobile broadbandprices (prepaid, handset based, 500MB)represents7.2%ofincome,andthusisgettingquiteclosetotheUNtarget.Among the industry, relatively low mobile broadband (both 3G and LTE) handsetpenetrationisconsideredareasonforslowerthanexpectedtake-up–typicalcostsfora3GenabledmobilehandsetisP700whileanLTEoneisaroundP1500.

4.2.4 FurtherregulatorymeasuresHowever, there are several regulatory enablers and incentives – as identified byoperators during the initial consultation - which could accelerate further mobile

DRAFTSTRATEGICPLANFORTHEUASF Page9

21May2015

broadband up-take, roll-out and reduce prices, thus increasing universal access andservices,asfollows:

• ActiveRadioAccessNetwork(RAN)sharing• 700-800MHzbecomingavailable,possiblyaftertheWRCinNovember2015for

LTEinmoreruralareas• Re-useof900MHzfor3Ginruralareas,and• Improvelandacquisitionprocess–possiblyunifiedcostsorguidelinesforcosts

and specific and formalized application process with reliable timelines to getpermissionorresponse.

Conclusion: The broadbandmarket is still expanding and growing naturally and thusmajor network roll-out projects by theUASF are pre-mature at this stage. It ismoreefficienttostimulatedemandandbuildICTcapacityandre-visitthesupply-sideafter2to3years.TheUASFshallgatherkeydatathoughannuallyandmonitorexpansionofthemarkettodeterminefuturenetworkroll-outprojects.Intheinterim,theUASFshallfocuson

• Lobbyingandfacilitatingforenablingregulatoryincentivesasoutlinedabove;and

• Implementing a major capacity and usage building initiative in schools asdescribedfurtherbelow.

4.2.5 InstitutionalconnectivityThe nearly 1,000 government schools have no broadband Internet connectivity andalmostallprimaryschoolshaveneitheracomputerlaboratories(labs).WhilesomeoftheschoolsinBotswanahaveInternetconnectivity,itisallnarrowbandi.e.,256kbpsorless.Out of the 207 Junior Secondary schools, 26% have some sort of upgraded Internetaccess,while43%of the32SeniorSecondary schoolsalsohave slightlybetter Internetaccess.Mostofthe754primaryschoolshaveeithernoInternetoritissoslow–256kbpsor less – to be virtually useless for a computer labwith around 30 children. Thus, themajorityofschoolsdonothavebroadbandInternettoday.TheMinistryofEducationandSkillsDevelopment(MOESD)issuedatenderinApril2014for the establishment of an Education Data Network (EDN) that is to connect allgovernmentschoolsandprovideserviceforthefirsttwoyears.Thenetworkwastohave6corenodesatstrategiclocationsaroundthecountryandschoolswouldconnecttotheirclosestcorenodethroughleasedlines.Theawardofthetenderiscurrentlystalledduetolackoffunding.BOCRAundertookaneedsassessmentofschoolsintheKgalagadi,GhanziandSoutherndistrictsinNovember2014.Itsreportsummarizessomeofthekeychallengesinschoolsasfollows:

• Noorfewworkingup-to-datecomputersortabletsinprimaryschools• Connectivitytoopoor/slow• Noin-schooltechnicalsupport• NodedicatedICTteacherinprimaryschool• Someschoolslackspecificroomforcomputerlab• Internet access often limited to the computer lab and does not extend to

teachersquarters,and• insomeschoolselectricityisanissue.

DRAFTSTRATEGICPLANFORTHEUASF Page10

21May2015

TheNBShassettargetsforatleast40%broadbandschoolpenetrationby2015-2017,and70%by2018-2021.OneofthemajormeasuresoftheNBSonthedemandsidepoliciesisthe Digital Literacy Programme, which is cognisant of the fact that broadband usagerequires ICT capacity – basic computer skills and the capability of finding, evaluating,ethically using, creating and sharing the information, services, media and applicationsbroadbandInternetmakesavailable.Conclusion:SchoolbroadbandconnectivityshouldbeamaintargetoftheUASF.

4.3 BroadcastingIntermsofuniversalaccessandserviceinbroadcasting,thetwomaincriteriaare

• Availability–whatpercentageofthepopulationhasbroadcastingcoverageandtherequiredend-userdevicetolistentoit?

• Pluralityandchoice–doesthepopulationhaveaccesstoavarietyofdifferentmediawithdifferentcontentandopinions?

4.3.1 RadioThere are currently three commercial radio stations licenced in Botswana, DumaFM,YaronaFMandGabzFM.ThereisalsothestatebroadcasterwithRB1andRB2forradio.However,thestatebroadcasterisoutsideofBOCRA’sjurisdictionandnotpartofthisUASstrategy. Radio household penetration in Botswana is 92%,4 and thus very close touniversalservice.The three commercial radio stations formed the joint venture Kemonokengwhich is acombined signal distribution network with shared FM sites. They have all equalshareholdinginKemonokeng.KemonokenghascurrentlyninetransmissionsitesnamelyLobatse, Gkeomaborone, Mahalapye, Serowe, Selibe Phikwe, Francistown, Maun,TlokwengandMochudi.Thus,allcommercialradiostationsareavailableinmajortownsandvillagesinBotswana,withpopulationcoverageofbetween50-60%.The5yearroll-outplanofthecommercialradio station projected that theywill cover ten districts by end of 2014. In September2014,eightoutoftendistrictshadsignalcover,anachievementof80%rolloutprogress.Kemonokeng is currently planning to deploy 5 new sites which would bring thepopulation coverage to almost 90%. However, they have financing constraints. Theirabilitytoraiseadditionaladvertisingrevenueiscurrentlyhinderedbynothavingnationalcoverage.Conclusion: Radio has very high population penetration but not from all main radiobroadcasters.With Kemonokeng there is an opportunity to increase the coverage ofthethreecommercialradiostations.

4.3.2 TVThe country has one commercial TV station, e-Botswana in addition to the statebroadcaster BTV. However, the latter is not under BOCRA’s jurisdiction and thus alsooutsidethisUASFstrategy.

DRAFTSTRATEGICPLANFORTHEUASF Page11

21May2015

eBotswana covers only Gaborone and surrounding areas within a 60km radius. ThecoveragelicenseconditionforthestationwasamendedtoalloweBotswanatobroadcastnationallyviasatellite.However,whilethestationhadcommittedtobroadcastthroughsatellitebyJuly2014,eBotswanahasnotbeenabletoimplementthisinitiativetodate.There is no data available regarding overall TV household penetration but industryestimatesindicatethisisunder50%ofhouseholds.Botswana is currently in the process ofmigrating to digital terrestrial television (DTT).BOCRA also recently issued a public consultationprocess for a licensing framework forDTT,whichstartedinJanuary2015andisstillongoing.Aconcernistheaffordabilityofnewset-topboxesforthedigitalswitchover,butthereisnoreliableinformationonpotentialpricesandtransitionplansyet.Neitheristhereanyinformationifthereisarealproblemandifso,theextentofthisproblem.Further,thisisno concern of theUASF as TV has not reached 75%of households to be considered abasicservicetobeincludedinUAS.AnyinterventionbytheUASFwouldassistthebetter-off population that can afford a TV, and not bridging the gap for those that needassistance. ThusanyUASFinvolvement inthismatterofdigitalTVset-topboxeswouldnotbeinlinewiththeUASFobjectives.Conclusion:TVhasnotreachedenoughpenetrationtobeincludedinuniversalservice.UASFinvolvementisnotrecommended.

4.4 PostalservicesUniversal Service to postal services is internationally defined as the provision of basicpostalservicestothewholeterritoryofthecountryatthesameprice.UniversalServicealso includesacommonstandardforthosebasicpostalservicesbasedonthefollowingfivecomponents:

a) Provisionofaccesstoservices;b) Levelofcustomersatisfaction;c) Speedandreliabilityofservices;d) Securityofservices;ande) Liabilityandtreatmentofenquiries.

TheCRA2012addressesthepublicpostaloperator(PPO),theuniversalserviceobligationandreservedservicesforthePPO(Section67to71).AccordingtoSection67,BotswanaPosthasbeendesignatedasPublicPostalOperator(PPO).TheActalsodefinesaspecificlistofuniversalpostalservicesforthePPOtodeliver.Otherkeyprovisionsinclude:

• ThePPOhasdetailedreportingrequirementsinregardstouniversalservice;

• The PPO has to provide separate accounting for the costs of the universalservice;and

• universalservicesaretobeprovidedonacost-basedplustariff,assuchallowingBotswanaPosttoraisetariffstocovercostsplus.

Overall, demand for mail is slowly declining with 14.8 mail items per person in 2014compared to 16.9 mail items per person in 2005. BotswanaPost states that it makeslosses due to the requirement to provide universal postal services. The Ministry ofTransportandCommunications (MTC)has secured funding foruniversalpostal servicesfor the financial year 2014/2015 in the amount of P40millionwhich has already been

DRAFTSTRATEGICPLANFORTHEUASF Page12

21May2015

disbursed.MTChasalsosecuredfundingforfinancialyear2015/16andhasaskedBOCRAto develop a contract for delivery of universal postal services and disbursementmodalities.However, while substantial preparations have been made, separate accounting anddetailedreportingonuniversalpostalservicesarenotyetfullyimplemented.TheCRA2012issilentonthedistributionofpostalofficesandpostalagenciesi.e.,whichsizeofvillagerequiresapostalofficeorpostalagencies.Inpractice,thepostalnetworkisdeterminedintermsoftheneedsfordeliveryofthespecifieduniversalpostalservices.BotswanaPosthas124postofficesand86postalagencies.However,as this isa legacypostalnetwork,thesepostofficesandpostalagenciesarenotalwayslocatedintownandvillagesaccordingtodemandforservicesandself-sustainability.TheTablebelowprovidesanoverviewpostalofficesandpostalagenciescategorizedinto5 clusters according to the population size of their location. This is identical to the sixclustersusedfortheNBS,howevercluster4/5werecombined.Based on the information provided, so far 77% of postal offices and 100% of postalagenciescouldbelocatedandcategorizedintothe5clusters.

Table2

Distributionofpostaloutletsacrosspopulationclusters

Clusters #ofpostaloffices #ofpostalagencies #ofcities/towns&villages

Cluster 6 (Cities) 11 3 2Clusters 4/5 (>10,000) 23 9 20Cluster 3 (5001-10,000) 22 6 27Cluster 2 (1001-5000) 36 61 197Cluster 1 (500-1000) 2 7 153Less than 500 pop 1 0 95

Total 95outof124(77%located)

86(100%located) 494

TheTableshowsthatallvillageswithmorethan5,000inhabitantsareserved,eitherbyapostalofficeorpostalagency.Alsoitappearsthatalmost50%ofvillagesbetween1,001and5,000inhabitantshaveapostaloutlet.Thepostalnetworkisthusquitesubstantial,andpossibly in some caseshasmorepostal outlets thanneeded.However, populationsizeisnottheonlycriteriafordemand,butalsoeconomicactivityorsocialimportance.Conclusion: Considering current government funding and the yet to be fullyimplementeduniversalservicecostaccountingandreporting,itiscurrentlyprematuretoconsideraspecificUASFpostalstrategy.Itwillhavetobeanalyzedfurtherintermsof cost-based plus tariff setting for universal postal services, and the demand anduniversalservicecriteria for the locationofapostalofficeoragency inacertaintypeandsizeofvillage.

DRAFTSTRATEGICPLANFORTHEUASF Page13

21May2015

5 AvailableUASFfundingThe first financial year of the UASF started on 1 April 2014 to 31 March 2015 (FY2014/2015).BOCRAprovidedseedfunding for theUASF in theamountofP37.352.734.BOCRA also added its surplus from its financial year 2013/2014 to the UASF in theamountofP16.084.802,asrequiredbytheCommunicationsAct2012.Initsfirstyear,theUASFcollectedP37.043.852,however,somesmallamountsarestilloutstanding.Going intothefinancialyear2015/2016,theUASFhasastartingcapitalofP90.481.389.ToforecastannualUASFcollections,annualtelecommunicationsrevenuegrowthfromFY2011/2012toFY2014/2015wasreviewed(seetheTablebelow).Whilethefirstyearonyeargrowthwashighwithover28%,thetwofollowingyearshadbarelygrowthorevenslightlynegative.TheCompoundAnnualGrowthRate (CAGR)over the last3yearswas8.8%.

Table3–CAGRofTelecomrevenueinpast3years

ThefigurebelowforecaststheUASFindustrylevycollectionof1%grossrevenueoverthenext 4 years. It is assumed thatmarket growthwill pick-up again and there are threescenariosforthe1%UASFlevy,basedon5%,10%and15%annualrevenuegrowthinthemarket.

Figure3

Assumingconservativemarketgrowth,theUASFwillhaveannualcollectionsofbetweenP32millionandP37million.AssumingoptimisticmarketgrowthUASFcollectionscouldrisetoP54millioninFY2018/2019.

DRAFTSTRATEGICPLANFORTHEUASF Page14

21May2015

Overallaccumulatedfinancesoverthenext4yearsareshowninthefigurebelow.

Figure4

Assuming conservativeannual growthof5%per year, theUASFwill reach slightlyoverP230million in FY 2018/2019.With an average growth of 10% per year the fund willaccumulatealmostP250million,andnearlyP270millionunderoptimisticmarketgrowthscenarios.ThisexcludesanyfuturecontributionsofBOCRAsurpluses.It is important tonote though that theUASFcollectionsofFY2018/2019areonly fullyavailable at the end of third financial year, and thus this UAS strategy cannot includethemasfullyavailablefundsforthisthree-yearstrategy.ThisUAS strategy assumes the conservativemarket growth scenario and no additionalsurplusfromBOCRA.AssuchthisprogrammeistailoredtoaconservativeassumptionofUASF funds. This is prudent as there may be unexpected additional expenses orunforeseenprojectopportunities,andtheUASFneedscontingencies.Conclusion:P193millionareavailableforthisUASstrategy,basedontheconservativeassumption.

DRAFTSTRATEGICPLANFORTHEUASF Page15

21May2015

6 Strategicstreams6.1 VoicecommunicationsTheUASFshallclosethevoicecommunicationsgapwithinthreeyearsby:

• Identifyingaccurately thenumberand typeof locationswithout voice servicestoday,thenumberofinhabitantslivingthereandtheirlevelofdemandforvoicecommunications;and

• Designing a project to provide service to these location and offering a smartsubsidyviaacompetitivebidtooperatorswithinthecountry.

Asafirstkeystep, it isrecommendedthatBOCRAdevelopsitsownEnterprise-levelGISorEGIS.EGIS canbedefinedasanaccurateand rich,geographically-based InformationSystemwhich is integratedthroughoutanorganizationtoallowmultipleusers toeasilyaccess and update the same information (or authorized sub-sets) and generate keyreports.ThiswouldbegenerallyusefulforBOCRA,forexampletobeabletoanalyseandreport voice, 3Gand LTE coveragedata throughout the country, butparticularlyusefulfortheUASF.AnadvancedEGIScouldintegratewithotherBOCRAdatabasesystemsandfunctionalitycanbebuiltstep-by-stepinamodularapproachasfundsandresourcesareavailable.TheEGISwouldallowimportantGISanalysesforUASprograming,including:• Baseline GIS map features and statistics including administration boundaries,

villages,terrain,transportationnetworks,population,andothercensusdata;• Ability to generate maps showing areas of operator mobile signal and internet

coverageandlocationsofUASFprojects;• Manipulation of Excel tables, data sets and charts to generate statistics such as

percent change in geographic areawith &without coverage per reporting period,andtotalgeographicareaofcoveragebyadministrationunit;and,

• Aggregate GIS-derived data for use in UASF project cost, revenue and viabilityanalysis.

The EGIS could be used to map a) all villages and localities, and b) all BTS and theircoverage,ifitiscombinedwitharadiofrequencycoveragemappingsoftware.ThiscouldbeaprojectjointlywiththeCentralStatisticOffice(iftheydonotyetalreadyhaveaGIS-basedpopulationdatabase).This would be one option to identify locations without voice coverage today. AnotheroptionwouldbetohaveapublicappealbyBOCRAinvolvingtheParliamentforlocalitiestoregisterthemselveswiththeUASFasnothavingvoicecoverage.Athirdoptionwouldbetoaskthethreemainoperatorstoprovidea listof locationstheyknowtheydonotservewithvoice.Operatorsco-operatedattheendof2014toestablishalistofunservedvillagesandlocalities;theycouldbeaskedtoco-operatewiththeUASF.Inasecondstep, theUASFshall commissionademandstudy ina representativesetofunservedlocalitiestoestablishthelevelandtypeofdemand.Thiscouldalsobeusedasaverificationcheckthatindeedthereisnovoicecoverageandalsonotclose-by.Basedonthenumberoflocationsneedingvoiceserviceandthefindingsofthedemandstudy,thethirdstepistodesignaprojecttocovertheselocations,estimatethecostandcommercial viability of the project, and decide on best approach and whether only asmartsubsidyisneededorpossiblyongoingOPEXsupport.

DRAFTSTRATEGICPLANFORTHEUASF Page16

21May2015

Astheseremaining3%ofpopulationisclearlythemostremoteanddifficulttoserve,itislikely that they represent the “true access gap”, meaning they cannot be served oncommercial terms, even if a smart subsidywere given. Nevertheless, costs to connecttheseremaininglocationscanandshouldbeminimized.Technicaloptions,duetotheremoteness,may includesatelliteservices, likeVSAT.ThiscouldincludeafixedserviceVSATforeachcommunity,i.e.,apublicphone.Oritcouldbeamini-cellconnectedtothemobilenetworkbutwithsatellitebackhaul;thiswouldmeantheinhabitantswouldhavetheirprivatemobilevoice(andbasicdata)service.During project design, it should be investigated if there is demand for internet serviceandwhatthecostfeasibilitywouldbetoaddforexampleapublicWiFispotperlocality(or for the largest localities); as aminimum, the systemput in place for voice servicesshouldbeupgradabletoincludebroadbandInternetatalaterstage.Astherearecurrentlynotenoughinformationtoestimatecostsforthevoiceprogram,itisrecommendedtoreserveP20millionforthiscomponent.

6.2 BroadbandInternetTheUASFstrategywillfocusonthefollowingthreekeystrategiesforbroadbandInternet:

• Advocating for and facilitating of the consideration and implementation ofpotentialregulatoryimprovementsandincentivesforruralbroadbandroll-out;

• Connecting both secondary and primary schools with broadband Internet andalsoprovidingthemwiththeequipment,technicalandtrainingsupporttotakeadvantage of that – and where required, leveraging school connectivity forfurtherbroadbandroll-out;and

• CreatingfurtherpublicaccessthroughaddingpublicWiFitothevillagesinwhichschoolsaregettingbroadbandInternetconnectivityviatheUASF.However,thishasthefollowingtwoconditions:

o ThepublicWiFiwillonlybeestablishedinvillageswhichdonothaveapublic WiFi spot today and are unlikely to have one on commercialgroundsevenin1-2yearstime;

o ThepublicWiFiservicetothepublicwillnotbesubsidized,i.e.,normalpricingwillapply;UASFfundingwillprovideasmartsubsidy.

6.2.1 Regulatoryenablersandincentivesforfurtherbroadbandroll-outAsalreadymentioned insection4, thereareseveral regulatoryenablersand incentiveswhich have the potential to accelerate furthermobile broadband up-take, roll-out andreduceprices,thusincreasinguniversalaccessandservices.TheUASFisafinancinginstrumentandnotaregulatoryinstrument,butitscoreprincipleisthatitisaninstrumentofareformed,liberalizedandwellregulatedmarket,asitwouldotherwise finance the inefficiencies of the market place. No marketplace is perfectlyregulated either, but the UASF should promote and support measures that wouldimproveUAS,especiallyiftheyhavesupportfromasignificantnumberofoperators.RegulatorymeasuresthatcurrentlyareconsideredtoimproveUASinclude:

• Active RAN sharing – there are a number of countries where operators haveimplemented various levels of active RAN sharing, with different business

DRAFTSTRATEGICPLANFORTHEUASF Page17

21May2015

modelsandregulatoryconditions;thisisgenerallyquiteacomplexundertakingand process, but operators can see a large reduction in costs and duplicateinfrastructure and thus some arewilling to explore this.What is required is aposition of the regulator or a regulatory framework that gives operators thecertaintyoverwhatRANsharingandbusinessmodelsareallowedandwhat isnot.

• The“digitaldividend”frequencies-700-800MHz–arebecomingavailable,andpossibly after theWRC inNovember2015 there is a clearer recommendationsforusingthemforLTEinmoreruralareas;

• Re-useof900MHzfor3Ginruralareas,and

• Improvelandacquisitionprocess–possiblyunifiedcostsorguidelinesforcostsand specific and formalized application process with reliable timelines to getpermissionorresponse.

6.2.2 Connectingschoolsandleveragingfurtherroll-outAs outlined earlier, ICT capacity building in schools has potentially the biggest andlongest-term impact on broadband development and the country as a whole. Thusmakingschools Internet readyandconnecting themtobroadband Internet is tobe theflagship program of the UASF. The table below provides an overview of the UASFprogramforschoolcomputerizationandbroadbandconnectivity.Detailsregardingwhichschoolstotarget,theircurrentbroadbandcoverage,thecostsinvolvedandthedetailedimplementationapproacharedescribedinthissection.

Table4

Threeyearschoolcomputerizationandbroadbandconnectivityplan

Mainactivity #ofschools Estimatedcosts(millionPula)

Broadbandconnectivity

94Secondaryschools 22.0

Computerization/ITteacher 234Primaryschools 81.8

Broadbandconnectivity

234Primaryschools 54.3

158.1

SecondaryschoolsAsalreadydescribed inSection4,26%of the207 Junior Secondary schoolshave somesortofupgradedInternetaccess,while43%ofthe32SeniorSecondaryschoolsalsohaveslightlybetterInternetaccess.Basedonthe informationprovided,93%ofthe240secondaryschoolscouldbe locatedandcategorizedinto5clusters.ThisissimilartotheclustersusedfortheNBS,howevercluster 4/5were combined as the population data of the 2011 census did not includepopulationdensitydata.Thetablebelowshowsthedistributionofsecondaryschoolsacross thevarioussizesoflocations.

DRAFTSTRATEGICPLANFORTHEUASF Page18

21May2015

Table5

Distributionofsecondaryschoolsintoclusters

Clusters #ofsecondaryschools

Cluster 6 (Cities) 40Clusters 4/5 (>10,000) 85Cluster 3 (5001-10,000) 31Cluster 2 (1001-5000) 63Cluster 1 (500-1000) 2Less than 500 pop 1

Total 222

56%ofthesecondaryschoolsareeitherincitiesorinlargertownsormajorvillageswithmorethan10,000population,withtheremainderinsmallerplacesandalargeportioninlocalities with less than 5,000 population. While the former are likely already havingInternetaccessandarerelativelyeasytoserve,thelatterareunlikelytohavebroadbandInternetandaresimilarlyunderservedastheprimaryschools.All schools - both secondary and primary, urban or rural - are to be provided withbroadband Internet access, as per theNBS. Even some of the secondary schoolswithbetter Internet accessmight not have the adequate target download speed, and needimprovedInternetservice.The NBS targets are that 40% of schools are provided wit broadband Internet in theperiodof2015-2017,andthatthisincreasesto70%intheperiodof2018-2021.Thereareno specific speed targets for schools in theNBS butminimum speed targets per area:10MBinurbanareasand5MBinruralareasby2014-2017.Itisrecommendedthatthesespeed targets are used as guides for schools at the beginning of the programbut thatquickupgradesormodificationsareplannedfor,basedonanevaluationofactualusagein schools after a year of functioning broadband Internet access. 5MB is a reasonablestartingpointfordownloadspeed,assumingthat30childrenareonlinebrowsingatthesametime,allowingatleast160kbps.ItisrecommendedthattheUASFassistthesecondaryschoolsthatarelocatedinCluster3,2and1.TheroleoftheUASF istoassist inschoolcomputerizationandconnectivity,anditcannotfinancetheentireICTaspect.MOESDcouldfocusonthesecondaryschoolsinthecities(Cluster6)andinlocationswithmorethan10,000inhabitants(Cluster4/5),whichgenerallyhavebetterandlesscostlybroadbandserviceavailable.PrimaryschoolsThetablebelowgivesanoverviewofthedistributionofprimaryschoolsintofiveclustersof cities, town and village size. This is again using the same clusters as for the NBS,howevercluster4/5werecombinedas thepopulationdataof the2011censusdidnotincludepopulationdensitydata.Thetablehasalsousedavailabledatafrom

• BoFiNet’sexistingSDHsites,broadbandwirelesssites,andplannedsitesin2015,

• plannedLTEroll-outdatafromallthreeMNO’s,aswellas

• 3Gcoveragedata.

DRAFTSTRATEGICPLANFORTHEUASF Page19

21May2015

This allowed an identification of the primary schools that have various types ofbroadbandcoverage,andtheprimaryschoolsthathavenobroadbandcoverageforsometimetocome.Note: for the this first draft we have attempted to locate all primary schools (756governmentschoolsand57privateschools),andwereatthisstageonlyabletolocateatotal of 681primary schools. In subsequentdraftswewill eliminate theprivate schoolsandattempttolocatemoreschoolsinthe2011populationdatabase.

Table6–Availabilityofbroadbandcoverageforprimaryschoolsacrosspopulationclusters

Thesituationcanbesummarizedasfollows:

• The98primaryschoolsinthetwocitieshaveachoiceofbroadbandservicebothviafibre-opticandLTE;

• Also, the 173 primary schools in cluster 4 and 5 are covered by BoFinet’stransmission network and LTE, with 54 schools relying solely on LTE asbroadbandoption;

• The 51 primary schools in cluster 3 are again covered by both BoFinet and/orLTE,except15whichwillonlyhave3G,evenattheendof2016(i.e.,thevillagesarenotincludedincurrentLTEroll-outplans);

• Incluster2,40schoolsareinvillageswithBoFiNetpresence–however,thatisall, leaving 143 primary schools outside any broadband coverage today and inthenearfuture;

• For the 113 primary schools in cluster 1, twelve could be served using theBoFiNetinfrastructure–but111arewithoutbroadbandcoverage;and

• 63primaryschoolsresideinlocationswithlessthan500inhabitants(butlargervillagesmaybe closeby) –3haveBoFiNetpresencewhile60arewithoutanybroadbandcoverage.

The table below shows preliminary cost estimates for connecting the 681 schools thathavebeenlocatedsofar.Thesefiguresarelikelytochangeasmoreprimaryschoolsneedtobeincluded;currentlyonly83%arelocated(ontheotherhandsomeprivateschoolsneedtobeexcluded).Further,discussionswithstakeholdersmayyieldslightchangesincost estimates. However, this still gives good ballpark costs for establishing Internet

DRAFTSTRATEGICPLANFORTHEUASF Page20

21May2015

connectivityassumingamixofavailabletechnologyandrequiredadditionalnetworkroll-out.Keyassumptionsinclude:

• Costs were estimated for CAPEX to establish the broadband Internetconnectivityandformonthlycosts(includingmaintenance)for3years;

• Allprimaryschools inFrancistownandGaboronecanbeconnectedusingfibre;costs are likely even lower than currently shown. This is the best solution,consideringthat inthecitiestheLTEnetworkis likelyfacingmoredemandandpotential congestion, and required speeds are more difficult to guaranteecomparedtoruralareaswithlowerdemand;

• Roughcost-estimatesforfibreconnectivityfor10MBobtainedseemquitehighandneedtobe investigated further– for themodel50%ofcostobtainedwasassumed;

• Inlocationswherethereisnobroadbandcoveragetoday,theupgradetoLTEor3G includesonly50%ofCAPEX for theupgradeasoperatorswill benefit fromthesubsidytoprovideservicestothegeneralpublic;

• In places that both have the transmission network from BoFinet present andLTE,weassumedroughlyasplitof50/50amongthetechnologies;and

• The60primaryschoolsinlocationswithlessthan500populationsandwithoutBoFiNetpresencearenotincludedsofarasitneedstobeestablishedwhethertheyareclose to largervillageswithbroadbandconnectivityor invery remotelocations.

Table7–Costsofbroadbandconnectivityforprimaryschoolsdependingonlocation

andavailabebroadbandservice

Findingsfromthemodelareasfollows:

• 50% of overall school connectivity costs is the cost of connecting 37% of theprimary schools to the fibre-optic and transmission network of BoFiNet;However,thiswouldalsobeatahigherandmorereliablespeedof10MB;

• Considering that the UASF starts with over P90 million and will only reachslightly over P230 million at the end of FY 2018/2019, there are insufficientfundstoconnectallschoolsinthethreeyearsofthisstrategicplan.

As there are also additional costs of computerization for the primary schools, first theoverallapproach isoutlinedhere,withamoredetailedphasedactionplan for the firstthreeyearsfurtherbelow.

DRAFTSTRATEGICPLANFORTHEUASF Page21

21May2015

OverallapproachInternet–readyschoolsAnimportantlessonfrominternationalbestpracticeisthatschoolsneedtobe“Internet-ready”before the Internet connectivity isprovided.Otherwise costly Internet service isprovidedwithouttheschoolsbeingabletotakeadvantageofit,wastingUASFfunds.AnInternet-readyschoolconsistsof:

• Existingcomputerlabwiththefollowingfeatureso Safe/secureandsuitableroomo Sufficientpowersupplyandback-upifrequiredo Sufficientandup-to-datecomputerso Recentinstalledsoftware

• ExistingICTcurriculumthatistobetaught• Otherguidelinesofhowto integrate ICT intoteachingvarioussubjectssuchas

mathematics,science,art,etc.• Speciallearningandeducationalsoftware(content)• EspeciallytrainedICTteacher• TrainedorsensitizedotherteachersonhowtointegrateICTintotheirsubjects

Whilealmostallsecondaryschoolshaveacomputerlab,themajorityofprimaryschoolshasnocomputers, safesomedonatedoroldercomputers.So far therehasnotbeenaconsistentstandardordedicatedapproachtothecomputerizationofprimaryschools.InSenior Secondary schools ICT is an examinable subject while Junior Secondary schoolshave ICT awareness courses. There is no ICT curriculum for primary schools. Currently14% of the 28,000 teachers are ICT-trained, and another 2,500 are scheduled to betrainedthisfinancialyear.ThisbasicallymeansthatsecondaryschoolsareInternet-ready,whileprimaryschoolsarenot.AsamatterofpriorityforanycomputerizationandInternetconnectivityprogramforprimaryschoolstogoahead,anICTcurriculum(orawarenesscourse)forprimaryschoolsistobedevelopedbytheMOESD.The Internet readiness will influence the sequencing of which schools get connectedduringthefirstwave,secondwave,thirdwaveandsoon.Flankingmeasures–hiringrecentITgraduatesforprimaryschoolsAnother major lesson learnt from international experience with USF-funded schoolconnectivity is the importance of proper technical support. Many problems can occurwhen there is a lack of proper and timely technical support. This includes outsidetechnical support formajor issues regarding the Internetconnectivitybutalso in-housesupport for typical day-to-day problems such as viruses, required software upgrades,computermaintenance,dealingwithSPAM,trouble-shootingandsoon.Outsidesupportcan be resolved through technical maintenance and support agreements with thesuppliers.For internal support, it is recommended that recent IT graduates are specially hired tolookafterthecomputerlab.Inprimaryschools,theyshouldalsoteachbasicICTskillstobothpupilsandteachers,basedonanapprovedteachingprogram.Thisistoresolvetheproblemthattherearenotenough(orno)trainedICTteachersinprimaryschools,whichiscrucialforsuccess.ThisshouldbeinitiallydoneandfinancedbytheUASFonacontractbasisforaperiodofupto3years,butthereshouldbeanunderstandingwiththeMOESDthattheseITgraduatescouldbecomepermanentemployeesinthelongruniftheywishandhaveproventhemselves.

DRAFTSTRATEGICPLANFORTHEUASF Page22

21May2015

ThisprogrammeofhiringrecentITgraduatesshouldconsiderthefollowing:• JointlywiththeMOESD,aproperjobdescriptionandqualificationcriterianeed

tobeelaborated,aswellasanemploymentcontract;

• Afairandattractivesalaryshouldbeofferedbutwhichalsofitsintotheprimaryteachersalaryculture(i.e.,notsignificantlylowerbutalsonotmuchhigherthanasimilarlyqualifiedentry-levelprimaryteacher);

• Arecruitmentprocessorganized,possiblyoutsourced,butwithmajorinputfromMOESD,UASFandsomerepresentationoftheprimaryschools;

• SometraininginregardstoteachingastheITgraduateshavenoexperienceorqualificationsinteaching;and

• Apropersupervisionprogramofthenew“PrimaryschoolICTteachers”,possiblyinvolvingtheheadteacherbutalsoMOESD’sregionalICTco-ordinators,andtheUASFifrequired.

While themainobjectiveof theUASF is toassistwith ICTcapacitybuildingandserviceprovision which is commercially not viable, this recommendation of hiring recent ITgraduatesallowstheUASFalsotomakeasmallimpactinreducingyouthemployment.CostofgettingschoolsInternetreadyandflankingmeasuresDetailedcostingcannotbeprovidedinthishigh-levelstrategyasmanydetailsandfactorsareunknownatthisstageandneedtobedevelopedinamoredetailedimplementationplan.However,using some informedassumptions shown in the tablebelow,aballparkestimatecanbegainedforapproximateprogramcosts inregardstocomputerizationofprimaryschoolsandcontractingaspecialICTteacherandcomputerlab/ITspecialists.

Table8

CostofgettingprimaryschoolsInternet-ready

Items PerschoolinPula

30 new computers @ 5,000 150.000Computer lab room improvements 20.000IT grad salary @ 5,000/month for 3 years 180.000

Total per school 350.000750 primary schools 262.000.000

Whilethecostofthecomputerlababoveassumesatraditionalcomputerlab,theUASFand MOESD should consider and explore the suitability of alternative and innovativeoptions.Oneconceptincludeshavinga“mobilecomputerlab”forprimaryschoolswherecomputertabletsareused.Insteadofhavingaspecificcomputerroom,thetabletscouldbeonatrolleyandaremovedwithintheschooltotheclassthatneedsthem.OverallprogramcostsRoughcostsforInternetconnectivitywasestimatedatP140million(excludingsecondaryschoolsandnotincludingallprimaryschools).Jointlywiththeapprox.P260milliontogettheprimaryschoolsInternet-ready,this isaboutP400million5.ConsideringthefundsoftheUASFandthevariouscostsshowninthetablebelow, it isclearthatnotallschoolscanbemadeInternetreadyandconnectedinthe3yearperiodofthishigh-levelstrategybytheUASFalone.TheUASFhas57%oftheneededfinanceforthewholeprogram.Soitis crucial that theMOESDuses theiravailable funding toalsoconnectandcomputerizeschools.

DRAFTSTRATEGICPLANFORTHEUASF Page23

21May2015

It is recommended that the MOESD focuses on computerization and broadbandconnectivity for the secondaryandprimary schools in the citiesandclusters4/5,whiletheUASFprovidesthefinanceforsecondaryandprimaryschoolsinclusters3,2and1.Table9–CombinedcostsofmakingprimaryschoolsInternetreadyandconnectivity

costsagainstavailableUASFfinance

Note:Thistablejustincludesthe618primaryschoolsthatcouldbelocatedintheCensusdatabasesofar.Connectingall750primaryschoolswilladdtothecost.

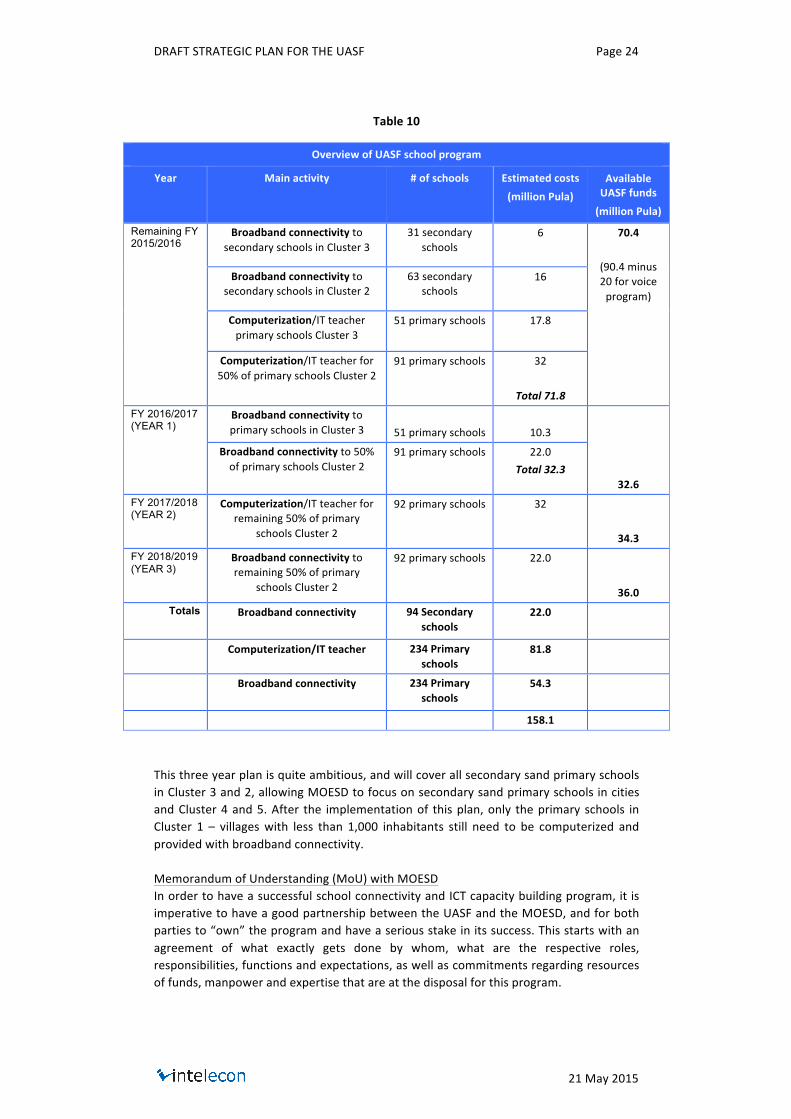

UASFschoolcomputerizationandbroadbandconnectivityplanTheTableothenextpageshowsthedetailedtargetsoftheschoolcomputerizationandbroadbandconnectivityfortheslightlyover3yearsofthisUASStrategicplan.Itmatchesthe costs with available funding and follows a sequence of computerizing the primaryschoolsfirstbeforeprovidingbroadbandInternetconnectivity.Ingeneral,thecomputerlabwouldhavetobeinplaceatleastfor3to6monthsbeforetheInternetconnectivityisprovided.ItalsofocusesontheeasiertoserveCluster3andthenmovestothesmallerlocationsinCluster2.

DRAFTSTRATEGICPLANFORTHEUASF Page24

21May2015

Table10

OverviewofUASFschoolprogram

Year Mainactivity #ofschools Estimatedcosts(millionPula)

AvailableUASFfunds(millionPula)

Remaining FY 2015/2016

BroadbandconnectivitytosecondaryschoolsinCluster3

31secondaryschools

6

70.4

(90.4minus20forvoiceprogram)

BroadbandconnectivitytosecondaryschoolsinCluster2

63secondaryschools

16

Computerization/ITteacherprimaryschoolsCluster3

51primaryschools 17.8

Computerization/ITteacherfor50%ofprimaryschoolsCluster2

91primaryschools 32

Total71.8FY 2016/2017 (YEAR 1)

BroadbandconnectivitytoprimaryschoolsinCluster3

51primaryschools

10.3

32.6

Broadbandconnectivityto50%ofprimaryschoolsCluster2

91primaryschools 22.0Total32.3

FY 2017/2018 (YEAR 2)

Computerization/ITteacherforremaining50%ofprimary

schoolsCluster2

92primaryschools 32

34.3FY 2018/2019 (YEAR 3)

Broadbandconnectivitytoremaining50%ofprimary

schoolsCluster2

92primaryschools 22.0

36.0Totals Broadbandconnectivity

94Secondary

schools22.0

Computerization/ITteacher 234Primaryschools

81.8

Broadbandconnectivity

234Primaryschools

54.3

158.1

Thisthreeyearplanisquiteambitious,andwillcoverallsecondarysandprimaryschoolsinCluster3and2,allowingMOESDtofocusonsecondarysandprimaryschoolsincitiesandCluster4and5.After the implementationof thisplan,only theprimary schools inCluster 1 – villageswith less than 1,000 inhabitants still need to be computerized andprovidedwithbroadbandconnectivity.MemorandumofUnderstanding(MoU)withMOESDInordertohaveasuccessfulschoolconnectivityandICTcapacitybuildingprogram,it isimperativetohaveagoodpartnershipbetweentheUASFandtheMOESD,andforbothpartiesto“own”theprogramandhaveaseriousstakeinitssuccess.Thisstartswithanagreement of what exactly gets done by whom, what are the respective roles,responsibilities,functionsandexpectations,aswellascommitmentsregardingresourcesoffunds,manpowerandexpertisethatareatthedisposalforthisprogram.

DRAFTSTRATEGICPLANFORTHEUASF Page25

21May2015

Co-ordination is also important inorder to avoid anyduplicating efforts, andmaximizeavailablefundsonbothsides,ratherthantheUASFtakingoverallfundingrequirements.ForexampletheMinistryofTransportandCommunicationsissuedatenderinApril2014for the “Design, Implementation andMaintenance of the Education Data network andsupply of high speed Internet service for (all) government schools”. The currentunderstandingisthatithasnotbeenawardedduetoinsufficientfunds.Obviously,ifthisweretogoahead,theUASFwouldnotbeneededanymore.However,bycombiningtheMOESDallocatedfundswiththefundsfromtheUASF,abetterprogramcanbedesigned,reachingmoreschoolsfaster.Further,theMOESDhasplanstoupgradecomputers in177schools,with40zero-clienttechnology.Zeroclient,alsoknownasultrathinclient,isaserver-basedcomputingmodelin which the end user has no local software and very little hardware. Their availablebudgetisP45millionandifpossible,thisshouldbeimplementedinawaythatitsupportsmore schools getting Internet-ready, so the UASF can provide the funds for thebroadbandconnectivity.Amongmanyothertopics,theMoUshouldcoverthefollowing:

• MOESDtogatherandsupplyschool-relevantdataandinformation,

• MOESDdevelopingabasicICTcurriculumforprimaryschools,

• MOESD identifying and purchasing an appropriate e-learning/educationalsoftwaretobeusedinprimaryschools,

• Responsibilityforprovidingthebudgetforgeneralsoftwareupgrades

• Makingsurethattheschoolsalsohaveavoiceandinputintheprogramdesignandimplementationastheirlocalexpertiseandsupportiscrucialforthesuccesstoo

• Developing the job specifications for the recent IT graduate to be hired tomanagethecomputerlabandITresourcesandtrainpupilsandteachers

• Planstomanagetheonlineprotectionoftheschoolchildren

• Commitmentandmechanismtoresolveanydifferencesofopinion

• Sustainability plan – the current UASF funding is for 3 years, Internet serviceprices have likely further decreased; what portion of school connectivity,requiredupgrades,ICTteachersandassociatedcostscantheMOESDtakeover,whichportionneedstobecontinuedbytheUASF?

• MonitoringandevaluationapproachincludingboththeUASFandMOESD

CompetitivebiddingapproachforInternetconnectivityTheUASFshoulduseacompetitivetenderingapproachforthe leastamountofsubsidyrequested for schools from qualified bidders. This does not involve any weightingbetweenthetechnicalandfinancialproposal,butisatwo-stageprocesswhere:

• first the technical proposal gets opened. Against the required technical andothercriteriapublishedintheRFP,asimplepassorfailevaluationtakesplace.Onlybiddersthatpassthetechnicalevaluation,proceedtothesecondstage.

• Second, qualified bidders have their separately and sealed financial proposalopened.Amongthesequalifiedbidders,thebidderwiththe lowestrequestforsubsidyisawardedtheproject.

DRAFTSTRATEGICPLANFORTHEUASF Page26

21May2015

Further, a maximum allowable subsidy should be set so as to avoid unreasonableexpectationsfromtheindustryandincreasecostminimizationeffortsandinnovativeuseoftechnology.Thesecondconsideration ishowtheschools tobeconnectedaregrouped,andvariousoptionshavetheiradvantagesanddisadvantages,asfollows:

Table11

Groupingoptionsofschoolsforcompetitivetendering

Grouping Advantage Disadvantage

Single lot – all schools to be tendered together

- createseconomiesofscale,especiallyiftheoverallnumbersofschoolsinaparticularprojectarenotlarge

- attractsmostly“big”bidders

- easiertoadministrateforUASF

- relianceonsingleprovider- notalwaysattractivefor

industryasonlyoneplayer“wins”

- limitschoiceofindustrytoselectschoolsthatfitwithexistingnetworkcoverageandroll-outplans

Regional tendering (e.g., 4 regions in Botswana)

- stillcreateseconomiesofscale

- attractsmostly“big”bidders

- easiertoadministrateforUASF

- limitschoiceofindustrytoselectschoolsthatfitwithexistingnetworkcoverageandroll-outplans

- excludessmallerplayerswhichmayhaveinnovativeapproaches

Tendering by district - allowssmallerplayerstoparticipate

- increasescompetition

- increasedefforttoevaluateproposals

- increasedefforttoadministrateseveralproviders

School by school tendering (e.g., a list with each school)

- provides maximum competition

- provides maximum choice for bidders in terms of which schools they can serve most cost-effectively

- increasedefforttoevaluateproposals

- increasedefforttoadministrateseveralproviders

Which grouping approach to take will have to be developed during the strategyimplementationinconsultationwiththeindustry.However,regionalordistrict-by-districttenderingtypicallycombinethebestadvantages.ItisrecommendedthatallPTOs,VANsandISPswiththeproperlicencesorregistrationsare eligible to participate in the competitive bidding process. BoFiNet’s role shouldremainasawholesaleprovider.Asagovernment-ownedoperatorthatreceivesgovernmentfunding,itisrecommendedthat BoFiNet offers theirwholesale transmission and Internet capacity at a discountedpricefortheschoolconnectivityprogram.

6.3 Broadcasting6.3.1 RadioIt is very fortunate that the existing three commercial radio broadcasters have alreadycreatedajointsignaldistributioncompany,Kemonokeng.Thereforeacompetitivesmart

DRAFTSTRATEGICPLANFORTHEUASF Page27

21May2015

subsidy tenderwouldnotmakeanysense in this instance,as the radiostationsdonotcompete based on terrestrial broadcasting network coverage, but on broadcastingcontent.Assuch,itwouldbefairandfeasibletoprovideasmartsubsidytoKemonokengdirectly,without any competitive tender, in return for increasing their broadcasting coverage.Further, Kemonokeng is already planning network expansion to five more sites whichwouldbringthepopulationcoveragetobetween80%and90%.CostsareestimatedatP2millionandKemonokengstrugglestofinancethisexpansion.It is recommendedfor theUASFto fundthisexpansionupto50%ofCAPEX,subject toKemonokengprovidingadetailedandcostedroll-outplanforthesesitesandprojectedpopulationcoverage.Due to technical issues the signaldistributionnetworkofKemonokeng couldnoteasilyaccommodate a 4th player as the sites are designed to carry three stations only andequipment has to be ordered and custom-designed for the number of stations to becarried. The UASF shall have to consider if it is feasible to assist in any upgrades andmodifications to allow Kemonokeng to accommodate additional radio stations in thefuture.

6.4 PostalservicesPostalservicesremainimportantfortheconveyanceofparcelsandmail,andprovisionofP.O. boxes, among other services. As discussed in Section 4.4, BotswanaPost is thedesignated Public Postal Operator (PPO) and required to provide universal postalservices. This sector is thus fundamentallydifferent as there is only a soleprovider foruniversal service. Also, several provisions of the Communications Regulatory AuthorityAct (CRA) from 2012 are not fully implemented yet. The postal sector analysis andpotentialUASFcomponentisconsequentlystillunderdevelopmentandrequiresfurtherengagementwiththerelevantstakeholders.