Trade Credit Risk in Turbulent Times RIMS Annual Meeting Boston, MA April 28, 2010 Download at: ...

23

Trade Credit Risk in Turbulent Times RIMS Annual Meeting Boston, MA April 28, 2010 Download at: www.iii.org/presentations Robert P. Hartwig, Ph.D., CPCU, President & Economist Insurance Information Institute 110 William Street New York, NY 10038 Tel: 212.346.5520 Cell: 917.453.1885 [email protected]

-

Upload

lesley-houston -

Category

Documents

-

view

215 -

download

0

Transcript of Trade Credit Risk in Turbulent Times RIMS Annual Meeting Boston, MA April 28, 2010 Download at: ...

Trade Credit Risk in Turbulent Times

RIMS Annual MeetingBoston, MA

April 28, 2010Download at: www.iii.org/presentationsRobert P. Hartwig, Ph.D., CPCU, President & Economist

Insurance Information Institute 110 William Street New York, NY 10038Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

3

Economic Volatility

A Halting Global Recovery is Underway; Volatility Remains

4

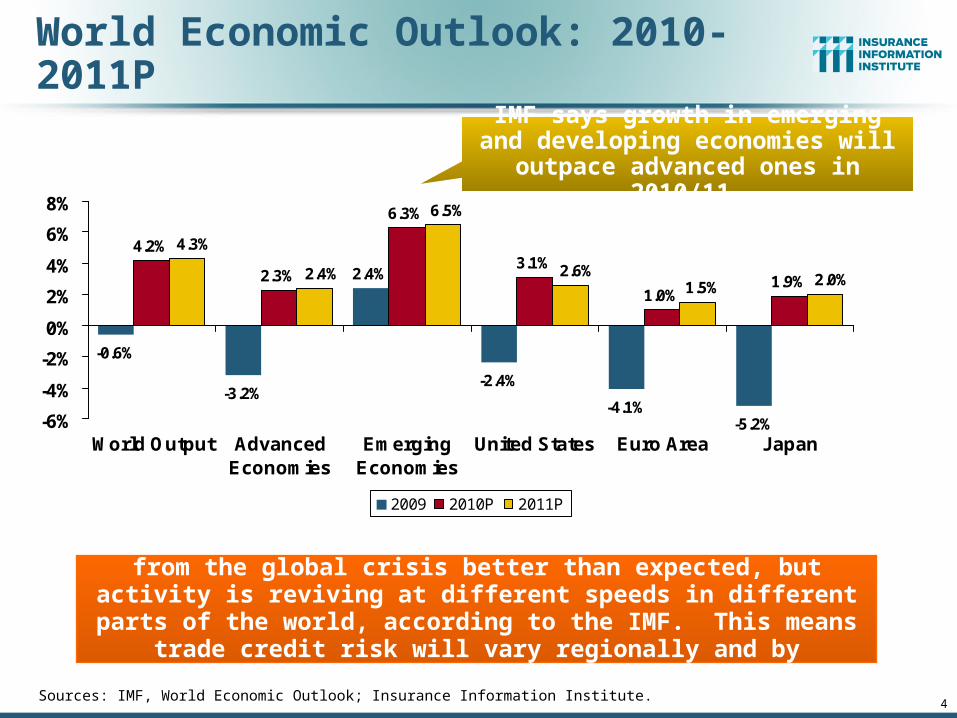

World Economic Outlook: 2010-2011P

Sources: IMF, World Economic Outlook; Insurance Information Institute.

4.2%

2.3%

6.3%

3.1%

1.0%1.9%

-5.2%-4.1%

-2.4%

2.4%

-3.2%

-0.6%

2.0%1.5%2.6%

6.5%

2.4%

4.3%

-6%

-4%

-2%

0%

2%

4%

6%

8%

World Output AdvancedEconomies

EmergingEconomies

United States Euro Area Japan

2009 2010P 2011P

Outlook uncertain: The world economy is recovering from the global crisis better than expected, but activity is reviving at different

speeds in different parts of the world, according to the IMF. This means trade credit risk will vary regionally and by industry.

IMF says growth in emerging and developing economies will outpace

advanced ones in 2010/11.

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

10.0

70

72

74

76

78

80

82

84

86

88

90

92

94

96

98

00

02

04

06

08

10

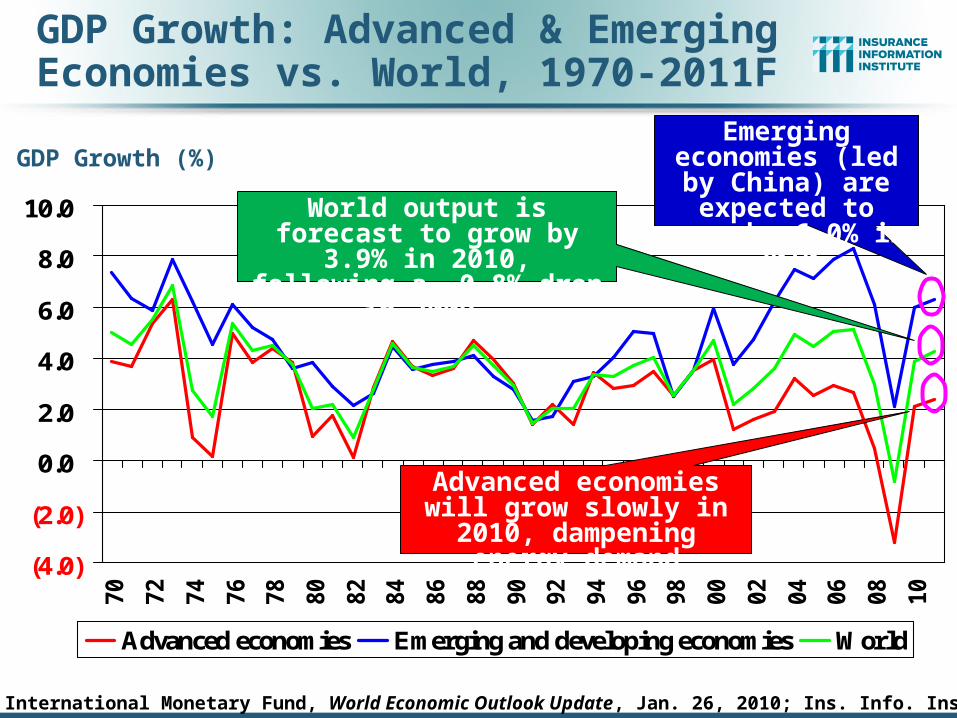

Advanced economies Emerging and developing economies World

Source: International Monetary Fund, World Economic Outlook Update, Jan. 26, 2010; Ins. Info. Institute.

Emerging economies (led by China) are

expected to grow by 6.0% in 2010

GDP Growth: Advanced & Emerging Economies vs. World, 1970-2011F

Advanced economies will grow slowly in 2010,

dampening energy demand

World output is forecast to grow by 3.9% in 2010,

following a -0.8% drop in 2009.

GDP Growth (%)

-30

-25

-20

-15

-10

-5

0

5

10

15

20

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Source: International Monetary Fund, World Economic Outlook Update, Jan. 26, 2010; Ins. Info. Institute.

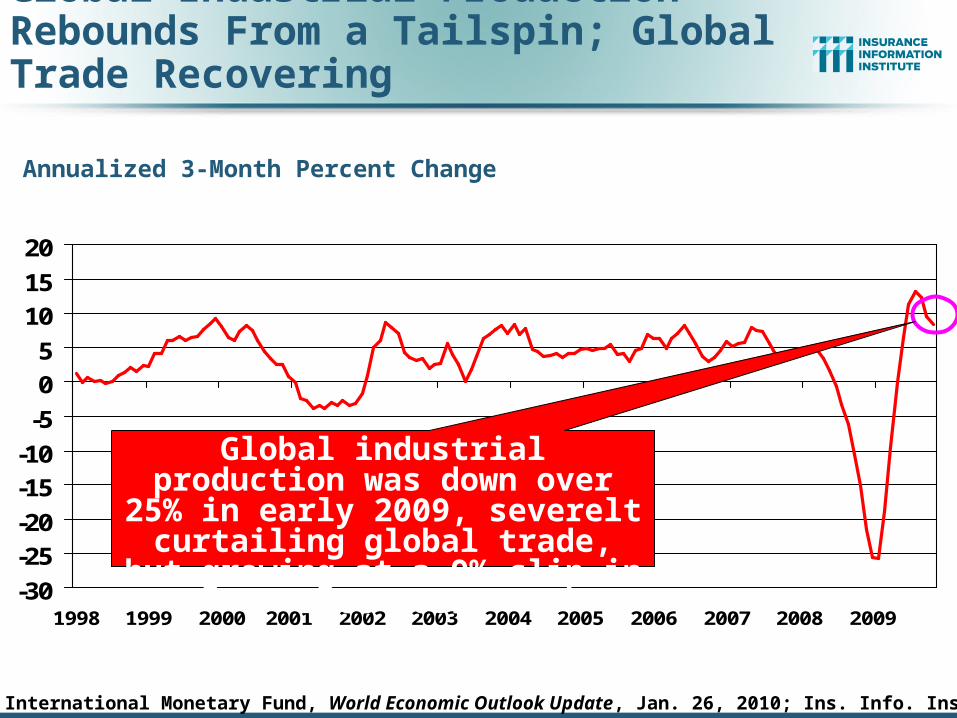

Global Industrial Production Rebounds From a Tailspin; Global Trade Recovering

Global industrial production was down over 25% in early 2009, severelt curtailing global trade, but growing at

a 9% clip in late 2009

Annualized 3-Month Percent Change

7

Merchandise Exports Are Growingat Pre-Crisis Levels Again

-75%

-50%

-25%

0%

25%

50%

75%

Jan

05

Jul 0

5

Jan

06

Jul 0

6

Jan

07

Jul 0

7

Jan

08

Jul 0

8

Jan

09

Jul 0

9

Advanced economies

Emerging economies

Note: data are through November 2009Source: International Monetary Fund World Economic Outlook January 2010 update at http://www.imf.org/external/pubs/ft/weo/2010/update/01/data/figure_2.csv

Annualized % change of 3-month moving average over previous 3-month moving average

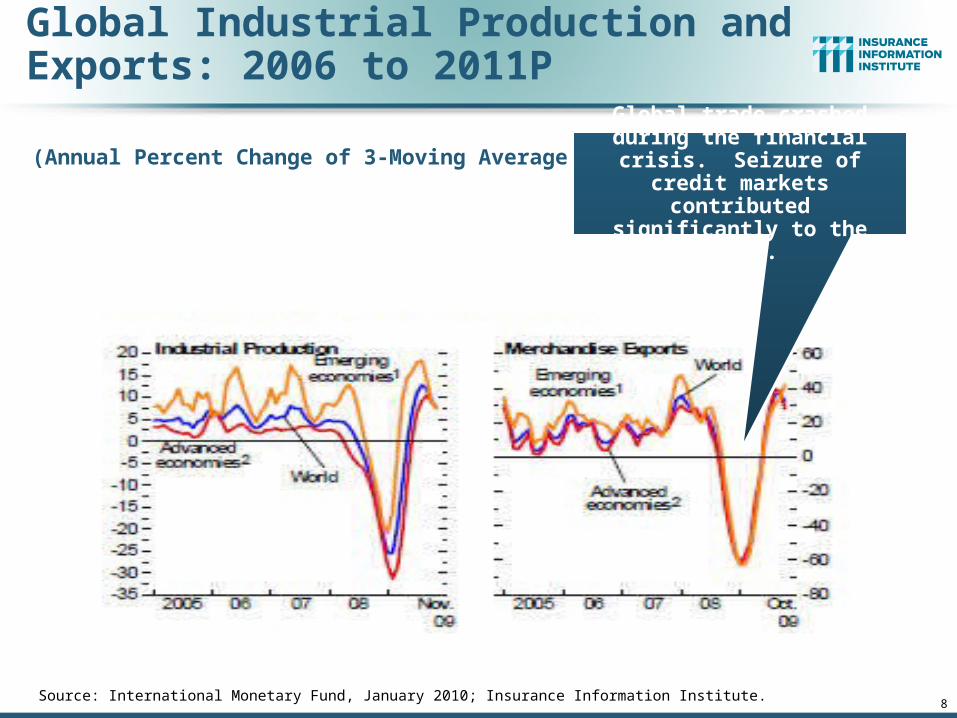

Global trade crashed during the financial crisis. Seizure of

credit markets contributed significantly to the crash.

8

Global Industrial Production and Exports: 2006 to 2011P

Source: International Monetary Fund, January 2010; Insurance Information Institute.

(Annual Percent Change of 3-Moving Average) Global trade crashed during the financial crisis. Seizure of

credit markets contributed significantly to the crash.

9

Exchange Rates, Inflation and Interest Rates

Pace of Recovery and Government Monetary and Fiscal Policies

Influence Exchange and Inflation Rates, Impacting Trade Credit Risk

and Cost

70

75

80

85

90

95

100

105

110

115

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

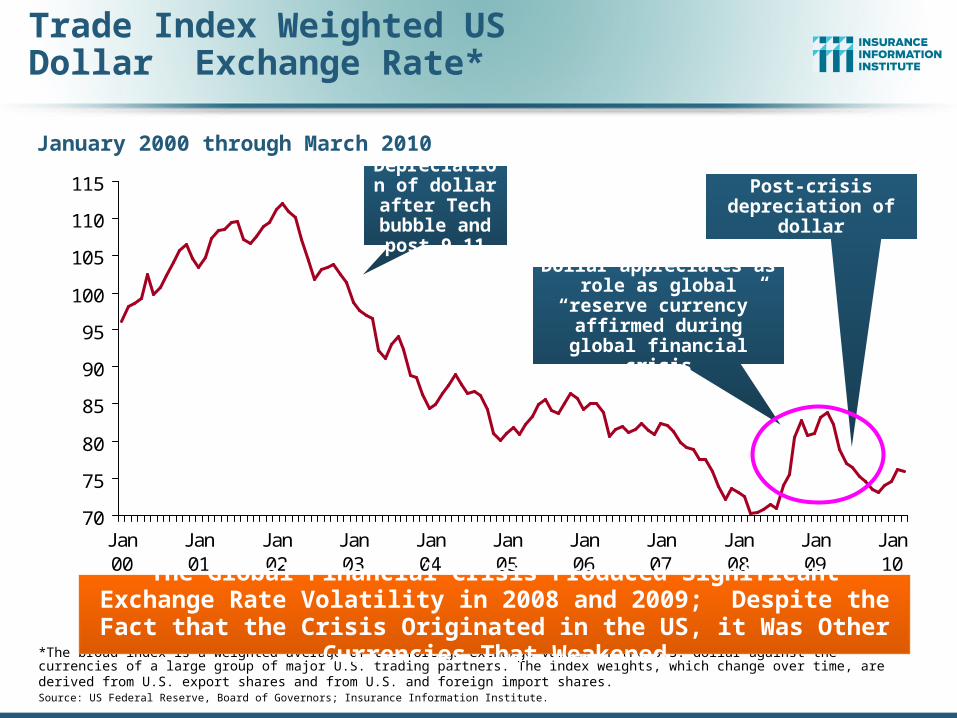

Trade Index Weighted US Dollar Exchange Rate*

*The broad index is a weighted average of the foreign exchange values of the U.S. dollar against the currencies of a large group of major U.S. trading partners. The index weights, which change over time, are derived from U.S. export shares and from U.S. and foreign import shares. Source: US Federal Reserve, Board of Governors; Insurance Information Institute.

The Global Financial Crisis Produced Significant Exchange Rate Volatility in 2008 and 2009; Despite the Fact that the Crisis Originated

in the US, it Was Other Currencies That Weakened

January 2000 through March 2010

Depreciation of dollar after Tech bubble

and post 9-11

Post-crisis depreciation of dollar

Dollar appreciates as role as global “reserve

currency” affirmed during global financial crisis

Inflation Rates for Largest European Economies & Euro Area, 2008-2011F

3.3%

2.6%

3.6%

2.8%

2.5%

0.3%

0.3%

2.2%

0.1%

1.0%

1.3%

1.1%

2.4%

1.4%

1.1%

1.6%

1.6% 1.

8%

1.6%

1.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Euro Area Germany UK France Netherlands

2008 2009

2010F 2010F

Source: Blue Chip Economic Indicators, 3/10/10 edition.

% Change from Prior Year Inflation is below 1.5% across major European economies and

interest rates remain low as a result, obscuring tight conditions

in trade credit markets

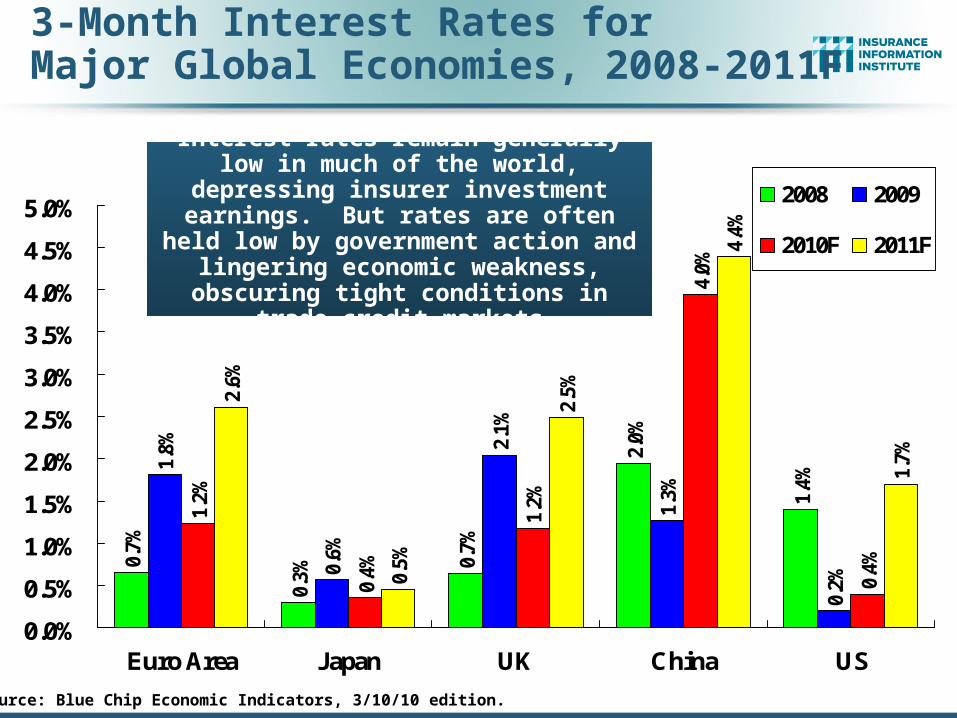

3-Month Interest Rates forMajor Global Economies, 2008-2011F

0.7%

0.3%

0.7%

2.0%

1.4%

1.8%

0.6%

2.1%

1.3%

0.2%

1.2%

0.4%

1.2%

4.0%

0.4%

2.6%

0.5%

2.5%

4.4%

1.7%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Euro Area Japan UK China US

2008 2009

2010F 2011F

Source: Blue Chip Economic Indicators, 3/10/10 edition.

Interest rates remain generally low in much of the world, depressing insurer

investment earnings. But rates are often held low by government action and

lingering economic weakness, obscuring tight conditions in trade credit markets

Internationally, Most Short-termInterest Rates Are Still Quite Low

Central Bank Current Interest Rate

Last Changed

Bank of Canada 0.25% April 21, 2009

Bank of England 0.50% March 5, 2009

Bank of Japan 0.10% Dec 19, 2008

European Central Bank 1.00% May 7, 2009

U.S. Federal Reserve 0.25% Dec 16, 2008

The Reserve Bank of Australia 4.25% April 6, 2010

China 5.31% Dec 22,2008

Hong Kong SAR 0.50% Dec 17, 2008

Korea, Republic of 2.00% Feb 16, 2009

Hungary 5.50%* Mar 29, 2010

*reduced from 5.75%Source: http://www.fxstreet.com/fundamental/interest-rates-table/

14

Political Risk

Many Nations Suffer from Political Instability, Fundamentally

Influencing Trade Credit Risk

15

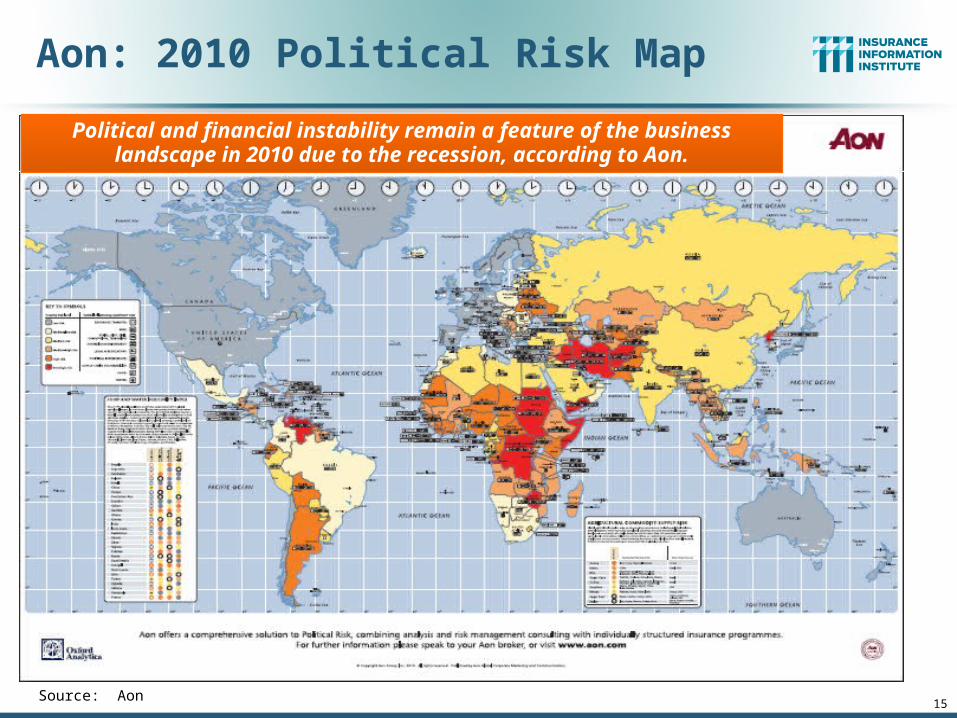

Aon: 2010 Political Risk Map

Source: Aon

Political and financial instability remain a feature of the business landscape in 2010 due to the recession, according to Aon.

16

Aon 2010 Political Risk Map: Findings

Elevated Political Risk Levels to Continue in 2010 Significant volume of credit and political risk claims in international insurance markets

have driven many of the 18 country downgrades in this year’s map. Aon believes 2010 will see elevated political risk levels continue before an overall

tendency for improving global business conditions becomes established. For many companies and across different sectors, including credit and political risk insurance, the business environment remains uncertain when trading with or investing in politically or economically unstable countries.

Movements on the 2010 Map A total of 18 countries have seen conditions worsen leading to a downgrade: Algeria,

Argentina, El Salvador, Equatorial Guinea, Ghana, Honduras, Kazakhstan, Latvia, Madagascar, Mauritania, Philippines, Puerto Rico, Seychelles, Sudan, United Arab Emirates, Ukraine, Venezuela and Yemen.

Sudan, Venezuela and Yemen have been added to the Very High category, joining Afghanistan, Congo DRC, Iran, Iraq, North Korea, Somalia and Zimbabwe.

Eight countries/territories have been upgraded to a lower risk level - Albania, Myanmar/Burma, Colombia, South Africa, Sri Lanka, East Timor, Vanuatu, Vietnam and the Hong Kong Special Administrative Region of the People's Republic of China.

Source: Aon

Bottom Line: Political and financial instability remain a feature of the business landscape in 2010 as a result of the recession.

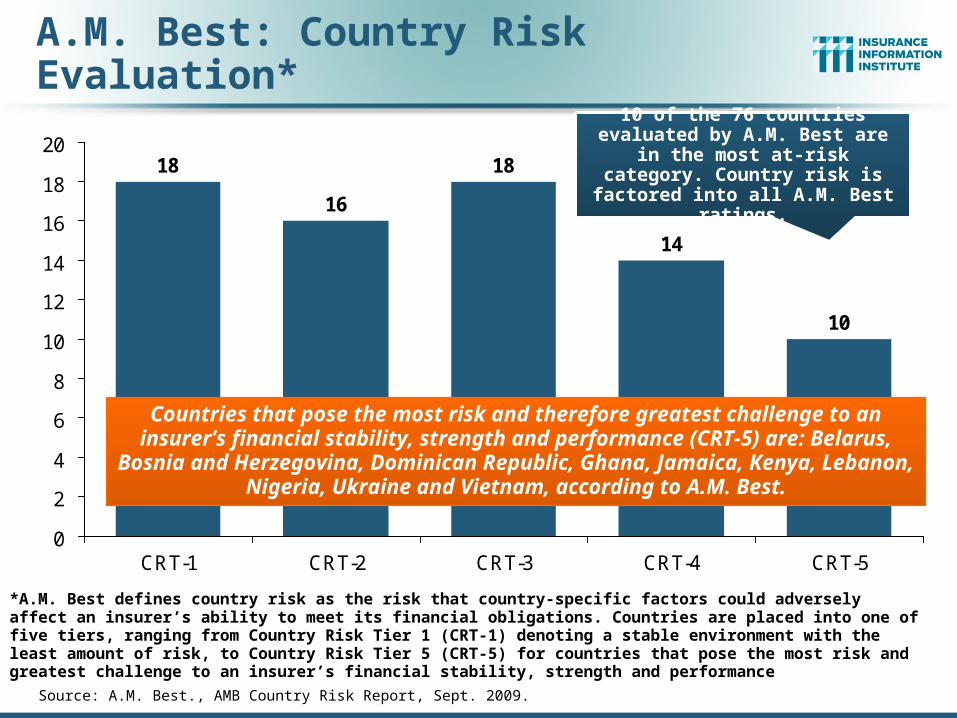

A.M. Best: Country Risk Evaluation*

18

16

18

14

10

0

2

4

6

8

10

12

14

16

18

20

CRT-1 CRT-2 CRT-3 CRT-4 CRT-5

Source: A.M. Best., AMB Country Risk Report, Sept. 2009.

*A.M. Best defines country risk as the risk that country-specific factors could adversely affect an insurer’s ability to meet its financial obligations. Countries are placed into one of five tiers, ranging from Country Risk Tier 1 (CRT-1) denoting a stable environment with the least amount of risk, to Country Risk Tier 5 (CRT-5) for countries that pose the most risk and greatest challenge to an insurer’s financial stability, strength and performance

10 of the 76 countries evaluated by A.M. Best are in the most at-risk

category. Country risk is factored into all A.M. Best ratings.

Countries that pose the most risk and therefore greatest challenge to an insurer’s financial stability, strength and performance (CRT-5) are: Belarus,

Bosnia and Herzegovina, Dominican Republic, Ghana, Jamaica, Kenya, Lebanon, Nigeria, Ukraine and Vietnam, according to A.M. Best.

18

Countries by Risk Tier Rating

*Denotes countries to be considered “Special Cases” by A.M. BestSource: A.M. Best., as of 4/13/10

CRT-2

Barbados*

Belgium

Bermuda

British Virgin Islands*

Cayman Islands*

Hong Kong

Ireland

Italy

Japan

Liechtenstein*

Macau

New Zealand

Slovenia

South Korea

Spain

Taiwan

CRT-1

Australia

Austria

Canada

Denmark

Finland

France

Germany

Gibraltar*

Guernsey*

Isle of Man*

Luxembourg

Netherlands

Norway

Singapore

Sweden

Switzerland

United Kingdom

United States

CRT-3

Bahamas*

Bahrain

China

Cyprus

Israel

Kuwait

Malaysia

Malta

Mexico

Netherlands Antilles*

Oman

Poland

Qatar

Saudi Arabia

South Africa

Thailand

Trinidad and Tobago

United Arab Emirates

CRT-4

Antigua & Barbuda*

Brunei Darussalam

Egypt

India

Indonesia

Jordan

Kazakhstan

Mauritius

Morocco

Panama

Philippines

Russia

Tunisia

Turkey

CRT-5

Belarus

Bosnia and Herzegovina

Dominican Republic

Ghana

Jamaica

Kenya

Lebanon

Nigeria

Ukraine

Vietnam

19

Trade Credit Risk: Summary & Outlook

Complex Array of Economic, Financial and Political Factors Will

Buffet Trade Credit Markets for Years to Come

Top 10 Risks & Reported Readiness and Losses: Many Impact Trade Credit Risk*

Rank Top 10 Risks – All Industries

Reported Readiness – All Industries

Loss of Income in Last 12 Months – All Industries

1 Economic slowdown 60% 57%

2 Regulatory/legislative changes

65% 24%

3 Business interruption 79% 30%

4 Increasing competition 71% 39%

5 Commodity price risk 77% 57%

6 Damage to reputation 58% 9%

7 Cash flow/liquidity risk 75% 25%

8 Distribution or supply chain failure

70% 20%

9 Third party liability 81% 40%

10 Failure to attract or retain top talent

68% 16%

*Yellow shading denotes risks with greater impact to trade credit risk.

Source: Aon Analytics; Global Risk Management Survey; Insurance Information Institute commentary of trade credit risk.

21

Financial Crisis Increases Demand for Trade Credit Insurance

Source: International Credit Insurance & Surety Association, April 2010

Financial crisis has led to significant increased demand for trade credit insurance cover Banks and other trade financiers had to take measures during the crisis which

resulted in increased pressure on suppliers’ credit terms and high risk scenarios Trade credit insurers continued to support their customers during the crisis,

illustrated by: 20 million running credit limits; insured exposures at EUR 1.8 trillion; claims ratio before costs of around 84 percent for 2009 (pre-crisis 40-60 percent)

Available capacity not affected by the crisis, but pre-crisis terms no longer available

Insurers increase information sharing and transparency High policy renewals of around 80-90 percent confirm customer satisfaction with

their insurance partners Increased information sharing and transparency will be provided to customers.

Emphasis on “added value” of insurers’ risk management role and higher transparency re credit limit decisions

Outlook Continued availability of trade credit insurance cover gives confidence and security

during fragile economic recovery Cost of capital and tightened risk environment continues to challenge industry,

leading to higher premium rates and stricter conditions

Bottom Line: Market now stable, but still challenging situation

22

Trade Credit Insurance Marketplace

Trade credit insurance market is concentrated in the hands of a few Total global annual premium income was over $8 billion in 2008 Three major monoline credit insurers account for nearly 90 percent of market: Euler

Hermes (36%); Atradius (31%); Coface (20%). Backed by reinsurers Other companies involved include: Chartis, QBE, various Lloyd’s syndicates and

ACE, as well as govt-backed export credit agencies

Exposures rise, but premium growth lags In past five years exposure levels of major credit insurers saw massive growth as

they competed for market share Premium income has not grown at same rate because of price competition and

increased writing of marginal risks by insurers Risk/reward imbalance

Economic downturn takes its toll Persistent economic downturn with retrenchment of bank credit, drying up of letters

of credit results in significant rise in payment defaults and corporate failures These conditions have led to significant increase in claims and record high loss

ratios for major three insurers in 2009 A capacity problem could follow in 2010 if reinsurance capacity shrinks or becomes

price prohibitive

Source: Marsh: Trade Credit Insurance and the Global Credit Crisis, 2009; Insurance Information Institute (I.I.I.)

23

Trade Credit Insurance Marketplace

Insurers refocus on risk quality Credit insurers review and reduce exposures/limits on certain industry sectors and

countries of concern Industry sectors considered difficult by most credit insurers include: construction,

retail, commodities, electronic consumer goods, automobiles and transport Dramatic premium increases for loss-making policies. Some not renewed at any price. Insurers will not take on risk deemed to be volatile or unprofitable

Alternatives for insurance buyers Top-up cover, other insurers, accounts receivable purchase agreements and govt

support some of the alternatives buyers are exploring Small market for top-up cover, but not in all regions Insureds with strong credit and ability to retain risk exploring increased use of captive

insurers Government-backed options offer limited support in some countries, but at a cost

Source: Marsh: Trade Credit Insurance and the Global Credit Crisis, 2009; Insurance Information Institute (I.I.I.)

Bottom Line: In 2010 challenging conditions remain, but receding recession should improve loss situation for trade credit insurers

www.iii.org

Thank you for your timeand your attention!

Twitter: twitter.com/bob_hartwigDownload at: www.iii.org/presentations

Insurance Information Institute Online: