Financial Crisis, Economic Stimulus & the Future of the P/C Insurance Industry Trends, Challenges &...

79

Economic Stimulus & the Future of the P/C Insurance Industry Trends, Challenges & Opportunities Robert P. Hartwig, Ph.D., CPCU, President Insurance Information Institute 110 William Street New York, NY 10038 Tel: (212) 346-5520 [email protected] www.iii.org Alamo CPCU Society, RIMS & San Antonio Agents Association San Antonio, TX March 5, 2009

-

Upload

joel-simmons -

Category

Documents

-

view

214 -

download

0

Transcript of Financial Crisis, Economic Stimulus & the Future of the P/C Insurance Industry Trends, Challenges &...

Financial Crisis, Economic Stimulus & the Future of the

P/C Insurance Industry Trends, Challenges & Opportunities

Robert P. Hartwig, Ph.D., CPCU, PresidentInsurance Information Institute 110 William Street New York, NY 10038

Tel: (212) 346-5520 [email protected] www.iii.org

Alamo CPCU Society, RIMS & San Antonio Agents Association

San Antonio, TXMarch 5, 2009

Presentation Outline

• Financial Crisis & The Weakening Economy: Insurance Impacts for the P/C Insurance Industry

• Recession, Growth & Insurance

• Economic Stimulus Package• Impacts & Implications for P/C Insurers

• Financial Strength & Ratings• P/C Insurance Industry Overview & Outlook

• Profitability• Premium Growth• Underwriting Performance• Financial Market Impacts

• Capital & Capacity• Regulatory Response to Crisis

• Emerging Blueprint of Regulatory Overhaul

Q & A

THE ECONOMIC STORM

What a Weakening Economy and Financial Crisis Mean for the

Insurance Industry

Exposure & Claim Cost Effects

3.7

%

0.8

% 1.6

% 2.5

% 3.6

%

3.1

%

2.9

%

0.1

%

4.8

%

4.8

%

0.9

%

2.8

%

-0.5

%

-1.5

%

0.8

% 2.0

%

2.4

%

2.9

%

3.1

%

3.1

%

-4.9%

-3.8%

-0.2%

-6%

-4%

-2%

0%

2%

4%

6%

2

00

0

2

00

1

2

00

2

2

00

3

2

00

4

2

00

5

2

00

6

07

:1Q

07

:2Q

07

:3Q

07

:4Q

08

:1Q

08

:2Q

08

:3Q

08

:4Q

09

:1Q

09

:2Q

09

:3Q

09

:4Q

10

:1Q

10

:2Q

10

:3Q

10

:4Q

Real GDP Growth*

*Yellow bars are Estimates/Forecasts from Blue Chip Economic Indicators.Source: US Department of Commerce, Blue Economic Indicators 2/09; Insurance Information Institute.

Recession began in December 2007. Economic toll of credit crunch, housing

slump, labor market contraction is growing

The Q4:2008 decline was the steepest since the

Q1:1982 drop of 6.4%

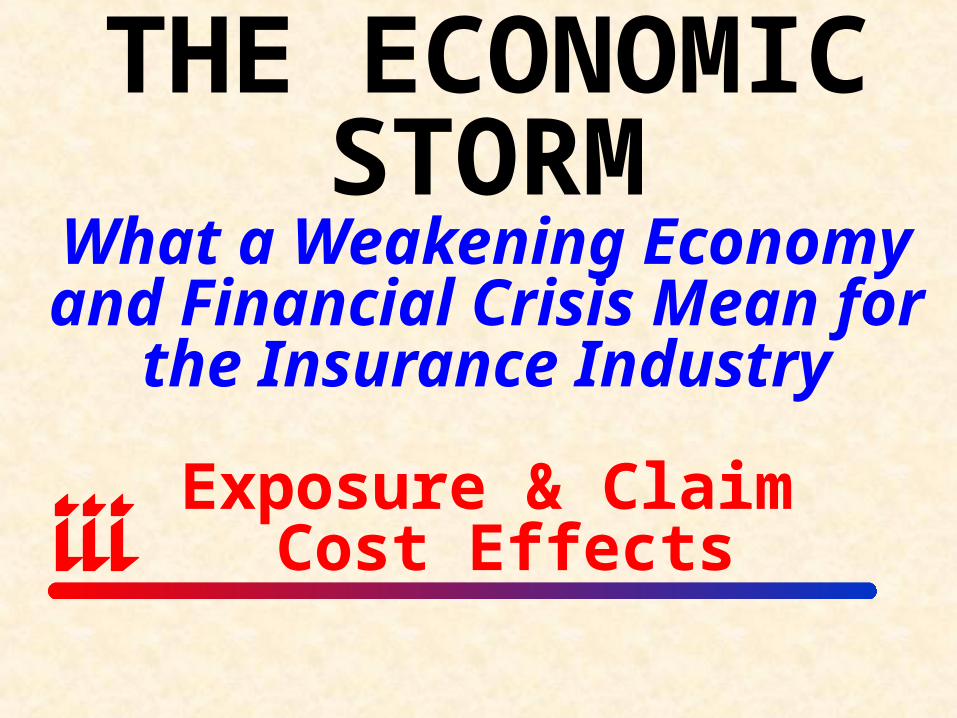

Length of US Recessions,1929-Present*

43

13

811 10

810 11

16

6

16

8 8

14

0

5

10

15

20

25

30

35

40

45

50

Aug.1929

May1937

Feb.1945

Nov.1948

July1953

Aug.1957

Apr.1960

Dec.1969

Nov.1973

Jan.1980

Jul.1981

Jul.1990

Mar.2001

Dec.2007

* As of February 2009

Sources: National Bureau of Economic Research; Insurance Information Institute.

Current recession began in Dec. 2007 and is already the

longest since 1981. If it extends beyond April, it will become the longest recession since the Great Depression.

Months in Duration

“We will rebuild. We will recover.”

--President Barack Obama addressing a joint session

of Congress

February 24, 2009

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

January 2000 through January 2009

Unemployment will likely peak above 8% or 9% during this cycle, impacting payroll

sensitive p/c and non-life exposures

Source: US Bureau of Labor Statistics; Insurance Information Institute.

Jan. 2009 unemployment jumped to 7.6%, exceeding the 6.3% peak during the previous cycle, and is now at it highest

level since Sept. 1992

Unemployment Rate:On the Rise

Average unemployment rate 2000-07 was 5.0%

Previous Peak: 6.3% in June 2003

Trough: 4.4% in March 2007

Jan

-09

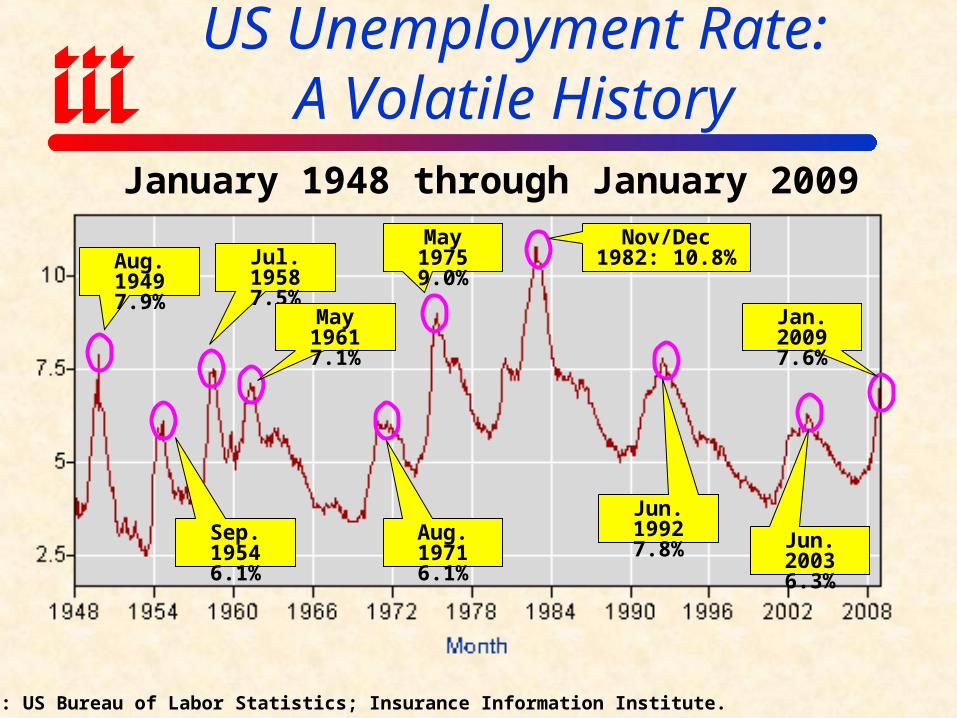

January 1948 through January 2009

Source: US Bureau of Labor Statistics; Insurance Information Institute.

US Unemployment Rate:A Volatile History

Aug. 1949 7.9%

Sep. 1954 6.1%

Jul. 1958 7.5%

May 1961 7.1%

Aug. 1971 6.1%

May 1975 9.0%

Nov/Dec 1982: 10.8%

Jun. 1992 7.8% Jun. 2003

6.3%

Jan. 2009 7.6%

U.S. Unemployment Rate,(2007:Q1 to 2010:Q4F)*

4.5%

4.5% 4.6% 4.

8% 4.9%

5.4%

6.1%

6.9%

7.6%

8.2%

8.6%

8.8%

8.8%

8.8%

8.6%

8.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4 09:Q1 09:Q2 09:Q3 09:Q4 10:Q1 10:Q2 10:Q3 10:Q4

* Blue bars are actual; Yellow bars are forecastsSources: US Bureau of Labor Statistics; Blue Chip Economic Indicators (2/09); Insurance Info. Inst.

Rising unemployment will erode payrolls

and workers comp’s exposure base.

Unemployment is expected to peak at

nearly 9% in late 2009 into 2010.

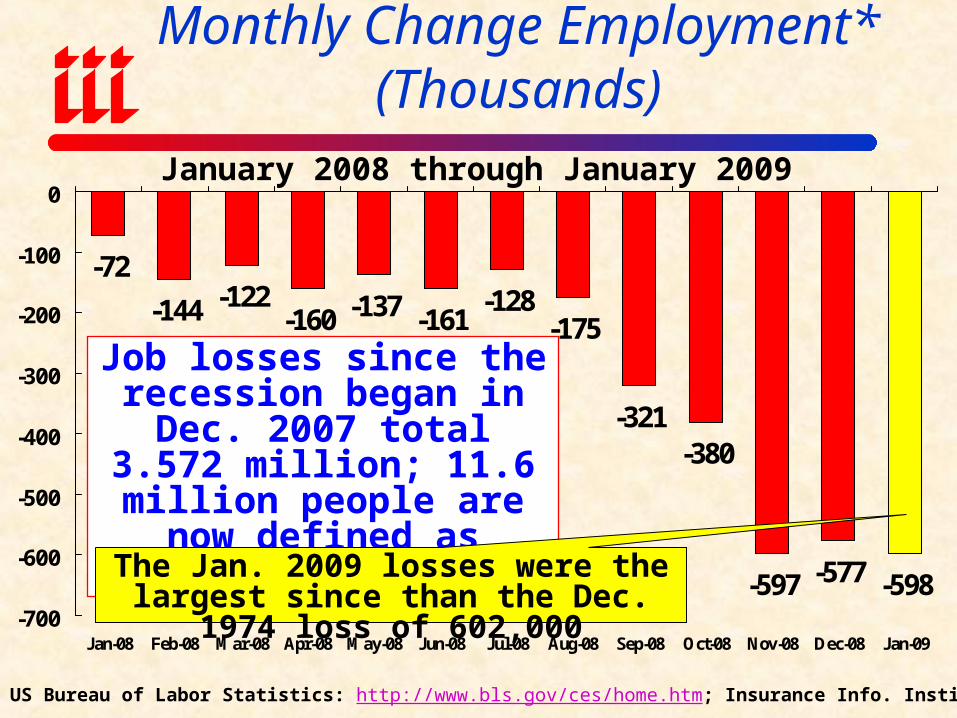

Monthly Change Employment*(Thousands)

-72

-144 -122-160 -137 -161

-128-175

-321-380

-597 -577 -598-700

-600

-500

-400

-300

-200

-100

0

Jan-08 Feb-08 Mar-08 Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 Jan-09

Job losses since the recession began in Dec. 2007

total 3.572 million; 11.6 million people are now defined as unemployed.

Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Info. Institute

The Jan. 2009 losses were the largest since than the Dec. 1974 loss of 602,000

January 2008 through January 2009

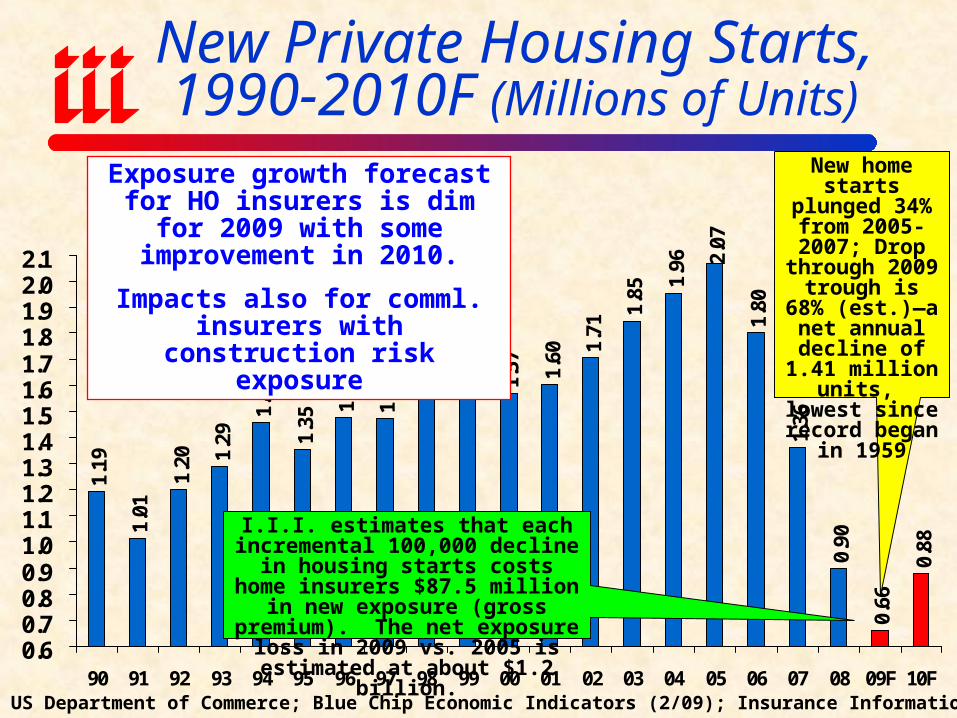

New Private Housing Starts,1990-2010F (Millions of Units)

2.07

1.80

1.36

0.90

0.66

0.88

1.48

1.351.

46

1.29

1.20

1.01

1.19

1.47

1.62 1.64

1.57 1.60 1.

71

1.85

1.96

0.60.70.80.91.01.11.21.31.41.51.61.71.81.92.02.1

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09F 10F

Exposure growth forecast for HO insurers is dim for 2009 with some

improvement in 2010.

Impacts also for comml. insurers with construction risk exposure

New home starts plunged 34%

from 2005-2007; Drop through 2009 trough is 68% (est.)—a

net annual decline of 1.41 million units, lowest since

record began in 1959

I.I.I. estimates that each incremental 100,000 decline in housing starts costs

home insurers $87.5 million in new exposure (gross premium). The net

exposure loss in 2009 vs. 2005 is estimated at about $1.2 billion.

Source: US Department of Commerce; Blue Chip Economic Indicators (2/09); Insurance Information Inst.

14

SD

NDMT

ID

NV

CA

OR

WA

UT

WY

NE

CO

OK

TXLA

FL

MN

IA

IL

ME

AZNM

KS

WI

OH

MINY

VT

IN

MO

AR

KY

TN

NH

PA

RI

MS AL

SC

NC

GA

VAWV

MA

CT

AK

HI

NJ

DE

MD

DC

State Construction Employment, Dec. 2007 – Dec. 2008

0% to 4%

-0.1% to -8.5%

-8.8% to -22%

AK

14

Construction employment declined in

47 of 50 states in

2008

Sources: Associated General Contractors of America from Bureau of Labor Statistics; Insurance Information Institute.

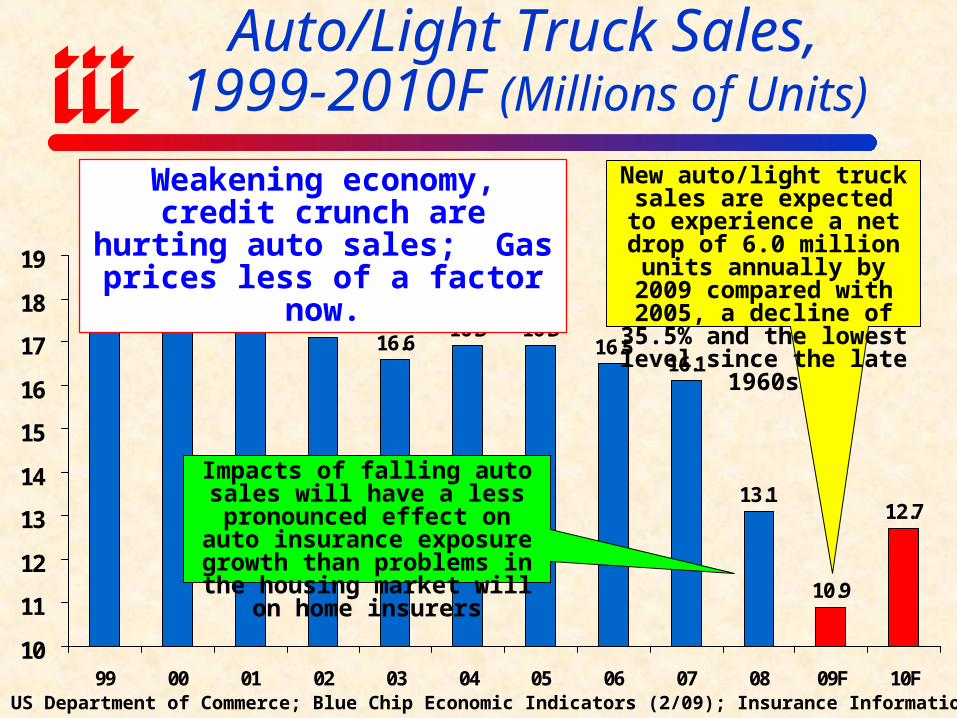

16.916.916.6

17.117.5

17.817.4

16.516.1

13.1

10.9

12.7

10

11

12

13

14

15

16

17

18

19

99 00 01 02 03 04 05 06 07 08 09F 10F

Weakening economy, credit crunch are hurting auto sales; Gas prices less of a factor now.

New auto/light truck sales are expected to experience a net drop of 6.0 million units annually by 2009 compared

with 2005, a decline of 35.5% and the lowest level

since the late 1960s

Impacts of falling auto sales will have a less pronounced effect on auto insurance exposure growth

than problems in the housing market will on home insurers

Auto/Light Truck Sales,1999-2010F (Millions of Units)

Source: US Department of Commerce; Blue Chip Economic Indicators (2/09); Insurance Information Inst.

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08*

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45Wage & SalaryDisbursementsWC NPW

*9-month data for 2008Source: US Bureau of Economic Analysis; Federal Reserve Bank of St. Louis at http://research.stlouisfed.org/fred2/series/WASCUR; I.I.I. Fact Books

Wage & Salary Disbursements (Payroll Base) vs. Workers Comp

Net Written Premiums

7/90-3/91

Shaded areas indicate recessions

3/01-11/01

Wage & Salary Disbursement (Private Employment) vs. WC NWP$ Billions $ Billions

12/07-?

Weakening wage and salary growth is

expected to cause a deceleration in workers comp

exposure growth

5.2%

-0.9

%-7

.4%

-6.5

%-1

.5%

1.8%

4.3%

18.6

%20

.3%

5.8%

0.3%

-1.6

%-1

.0%

-1.8

%-1

.0%

3.1%

1.1%

0.8%

0.4%

0.6%

-0.4

%-0

.3%

1.6%

5.6%

13.7

%7.

7%1.

2%-2

.9% -0

.5%

-3.8

%-4

.2%

1.7%

-10%

-5%

0%

5%

10%

15%

20%

25%7

87

98

08

18

28

38

48

58

68

78

88

99

09

19

29

39

49

59

69

79

89

90

00

10

20

30

40

50

60

70

8E

09

F

Rea

l N

WP

Gro

wth

-4%

-2%

0%

2%

4%

6%

8%

Rea

l G

DP

Gro

wth

Real NWP Growth Real GDP

Real GDP Growth vs. Real P/C Premium Growth: Modest Association

P/C insurance industry’s growth is influenced modestly by growth

in the overall economy

Sources: A.M. Best, US Bureau of Economic Analysis, Blue Chip Economic Indicators, 2/09; Insurance Information Inst.

THE $787 BILLION ECONOMIC STIMULUS

Sectoral Impacts & Implications for P/C

Insurance

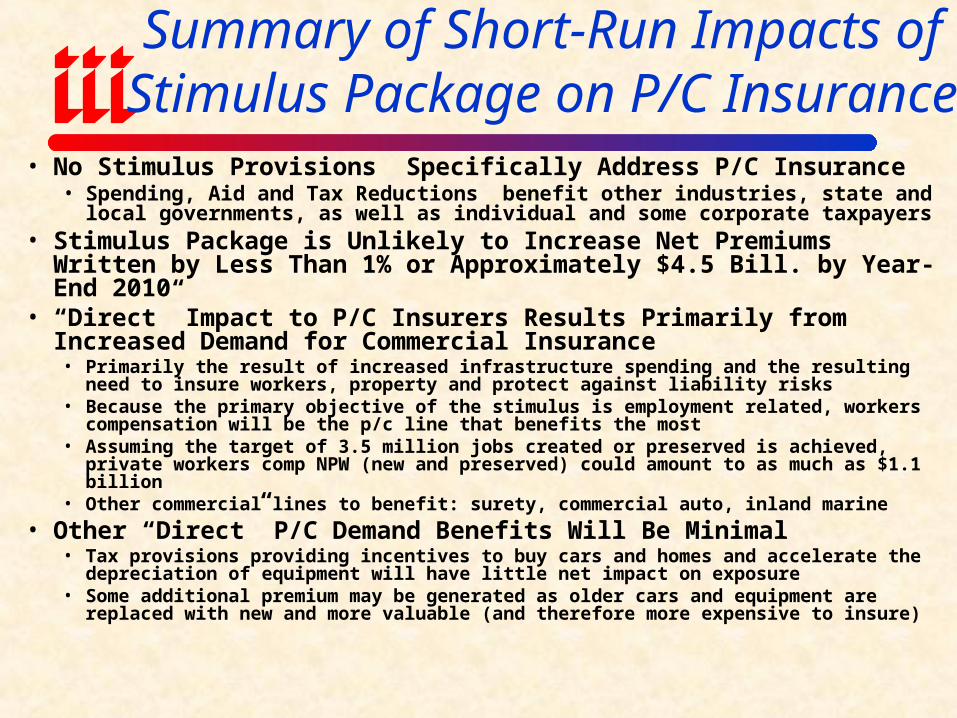

Summary of Short-Run Impacts of Stimulus Package on P/C Insurance

• No Stimulus Provisions Specifically Address P/C Insurance• Spending, Aid and Tax Reductions benefit other industries, state and local

governments, as well as individual and some corporate taxpayers • Stimulus Package is Unlikely to Increase Net Premiums Written by

Less Than 1% or Approximately $4.5 Bill. by Year-End 2010 • “Direct” Impact to P/C Insurers Results Primarily from Increased

Demand for Commercial Insurance• Primarily the result of increased infrastructure spending and the resulting need to insure

workers, property and protect against liability risks• Because the primary objective of the stimulus is employment related, workers

compensation will be the p/c line that benefits the most• Assuming the target of 3.5 million jobs created or preserved is achieved, private workers

comp NPW (new and preserved) could amount to as much as $1.1 billion• Other commercial lines to benefit: surety, commercial auto, inland marine

• Other “Direct” P/C Demand Benefits Will Be Minimal• Tax provisions providing incentives to buy cars and homes and accelerate the

depreciation of equipment will have little net impact on exposure• Some additional premium may be generated as older cars and equipment are replaced

with new and more valuable (and therefore more expensive to insure)

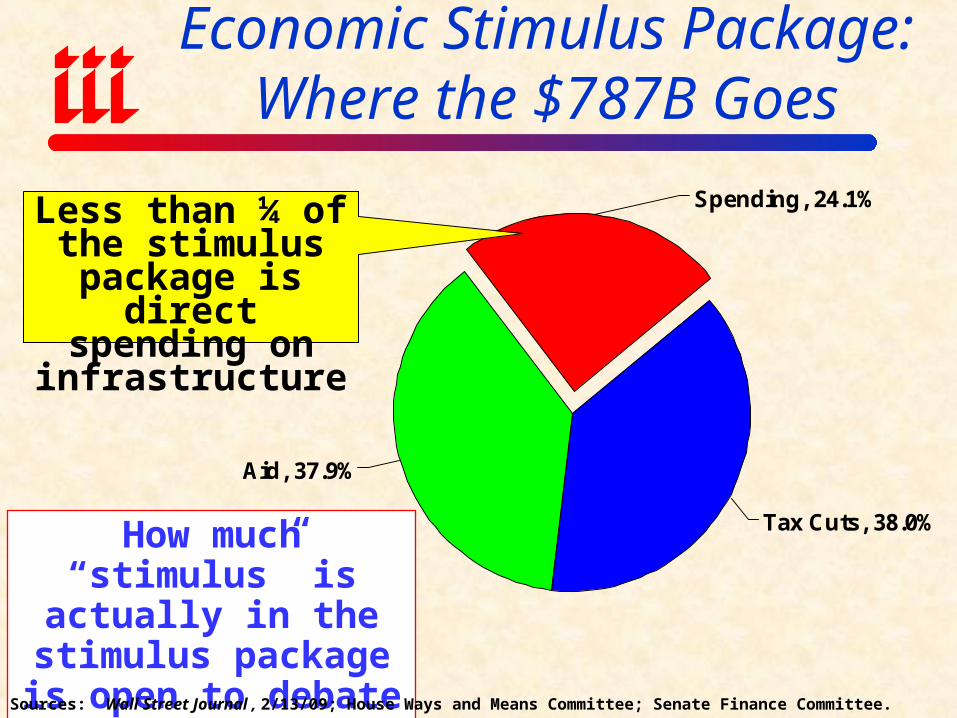

Economic Stimulus Package: Where the $787B Goes

Tax Cuts, 38.0%

Aid, 37.9%

Spending, 24.1%

How much “stimulus” is actually in the stimulus

package is open to debate and dispute

Sources: Wall Street Journal , 2/13/09; House Ways and Means Committee; Senate Finance Committee.

Less than ¼ of the stimulus package is direct spending on

infrastructure

Economic Stimulus Package: Where the $787B Goes

Tax Relief, $288 , 38%

State & Local Fiscal Relief, $144 , 18%

Infrastructure & Science, $111 , 14%

Protecting the Vulnerable, $81 , 10%

Health Care, $59 , 7% Education & Training, $53 , 7%

Energy, $43 , 5%

Other, 8, 1%

Tax relief and aid to state and local

government account for 56% of stimulus. Actual

spending accounts for only about 25%

Source: http://www.recovery.gov/ accessed 2/18/09; Insurance Information Institute.

$ BillionsObjective is to create or preserve 3.5 million jobs

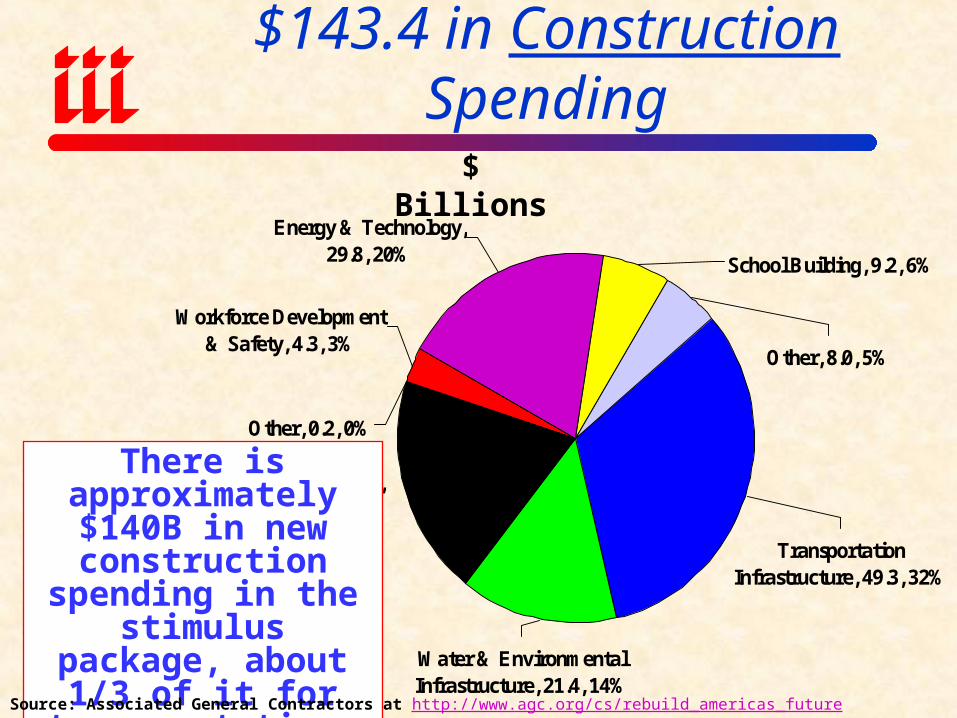

Economic Stimulus Package: $143.4 in Construction Spending

Transportation Infrastructure, 49.3, 32%

Water & Environmental Infrastructure, 21.4, 14%

Building Infrastructure, 29.6, 20%

Other, 0.2, 0%

Workforce Development & Safety, 4.3, 3%

Energy & Technology, 29.8, 20% School Building, 9.2, 6%

Other, 8.0, 5%

There is approximately $140B in new construction

spending in the stimulus package, about 1/3 of it for transportation.

Source: Associated General Contractors at http://www.agc.org/cs/rebuild_americas_future (2/18/09); Insurance Info. Inst..

$ Billions

State-by-State Infrastructure

SpendingBigger States Get More, Should Benefit

Commercial Insurer Exposure

Infrastructure Stimulus Spending by State (Total = $38.1B)

State Allocation State Allocation State AllocationAL $603,871,807 LA $538,575,876 OK $535,407,908

AK $240,495,117 ME $174,285,111 OR $453,788,475

AZ $648,928,995 MD $704,863,248 PA $1,525,011,979

AR $405,531,459 MA $890,333,825 RI $192,902,023

CA $3,917,656,769 MI $1,150,282,308 SC $544,291,398

CO $538,669,174 MN $668,242,481 SD $213,511,174

CT $487,480,166 MS $415,257,720 TN $701,516,776

DE $158,666,838 MO $830,647,063 TX $2,803,249,599

DC $267,617,455 MT $246,599,815 UT $292,231,904

FL $1,794,913,566 NE $278,897,762 VT $150,666,577

GA $1,141,255,941 NV $270,010,945 VA $890,584,959

HI $199,866,172 NH $181,678,856 WA $739,283,923

ID $219,528,313 NJ $1,335,785,100 WV $290,479,108

IL $1,579,965,373 NM $299,589,086 WI $716,457,120

IN $836,483,568 NY $2,774,508,711 WY $186,111,170

IA $447,563,924 NC $909,397,136 U.S. Territories

$238,045,760

KS $413,837,382 ND $200,318,301

KY $521,153,404 OH $1,335,600,553 Total $38,101,898,173

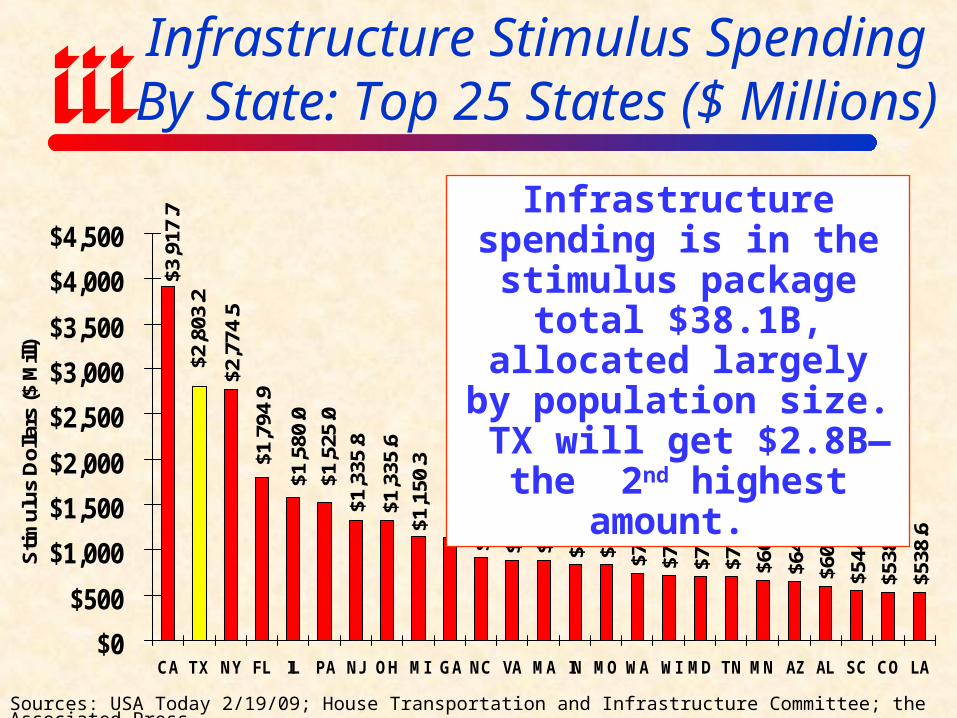

Sources: USA Today, 2/17/09; House Transportation and Infrastructure Committee; the Associated Press.

Infrastructure Stimulus Spending By State: Top 25 States ($ Millions)

$890

.6$8

90.3

$836

.5$8

30.6

$739

.3$7

16.5

$704

.9$7

01.5

$668

.2

$648

.9$6

03.9

$544

.3$5

38.7

$538

.6

$1,3

35.8

$1,5

80.0

$909

.4$1

,141

.3

$1,1

50.3

$1,3

35.6

$1,5

25.0

$2,8

03.2

$2,7

74.5

$1,7

94.9

$3,9

17.7

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

CA TX NY FL IL PA NJ OH MI GA NC VA MA IN MO WA WI MD TN MN AZ AL SC CO LA

Stim

ulus

Dol

lars

($ M

ill)

Sources: USA Today 2/19/09; House Transportation and Infrastructure Committee; the Associated Press.

Infrastructure spending is in the stimulus package total $38.1B, allocated

largely by population size. TX will get $2.8B—the 2nd

highest amount.

Expected Number of Jobs Gained or

Preserved by Stimulus Spending

Larger States = More JobsWorkers Comp Benefits

Estimated Job Effect of Stimulus: Jobs Created/Saved By State = 3.5 Mill Total

State Jobs Created State Jobs Created State Jobs CreatedAL 52,000 LA 50,000 OK 40,000

AK 8,000 ME 15,000 OR 44,000

AZ 70,000 MD 66,000 PA 143,000

AR 32,000 MA 79,000 RI 12,000

CA 396,000 MI 109,000 SC 50,000

CO 60,000 MN 66,000 SD 10,000

CT 41,000 MS 30,000 TN 71,000

DE 11,000 MO 69,000 TX 269,000

DC 12,000 MT 11,000 UT 32,000

FL 207,000 NE 23,000 VT 8,000

GA 107,000 NV 34,000 VA 93,000

HI 16,000 NH 16,000 WA 75,000

ID 17,000 NJ 100,000 WV 20,000

IL 148,000 NM 22,000 WI 70,000

IN 75,000 NY 215,000 WY 8,000

IA 37,000 NC 105,000

KS 33,000 ND 9,000

KY 48,000 OH 133,000 Total 3,467,000

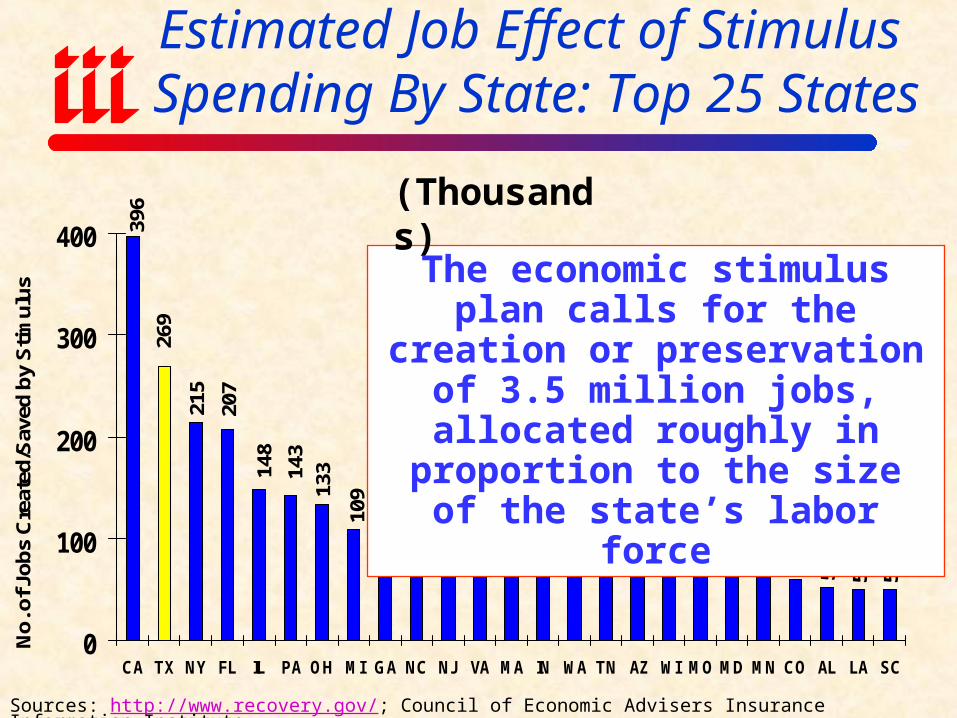

Sources: http://www.recovery.gov/; Council of Economic Advisers; Insurance Information Institute.

Estimated Job Effect of Stimulus Spending By State: Top 25 States

9379 75 75 71 70 70 69 66 66 60 52 50 50

13314

8

100

105

107

109

143

269

215

207

396

0

100

200

300

400

CA TX NY FL IL PA OH MI GA NC NJ VA MA IN WA TN AZ WI MO MD MN CO AL LA SC

No.

of J

obs

Cre

ated

/Sav

ed b

y S

timul

us

Sources: http://www.recovery.gov/; Council of Economic Advisers Insurance Information Institute.

The economic stimulus plan calls for the creation or preservation of 3.5 million jobs, allocated roughly

in proportion to the size of the state’s labor force

(Thousands)

Stimulus: Reading The Economic Tea Leaves for the Next 4 to 8 Years

Source: Insurance Information Institute

• Growing Role of Government: 2009 Stimulus Package and Other Likely Spending Initiatives Guarantee that Government Will Play a Much Larger Role Than at Any Other Time in Recent History Every industry, including insurance, will and must attempt to

maximize direct and indirect benefits from this paradigm shift• Obama Administration Priorities: Stimulus Package

Acts as “Economic Tea Leaf” on the Administration’s Fiscal Priorities for the Next Several Years

• These Include: Alternative Energy Health Care Education Aging/New Infrastructure Aid to States

• Stimulus is Only One Leg of the Stool (1) Stimulus; (2) Housing, and (3) Financial Services Reform

FINANCIAL STRENGTH &

RATINGS Industry Has Weathered

the Storms Well

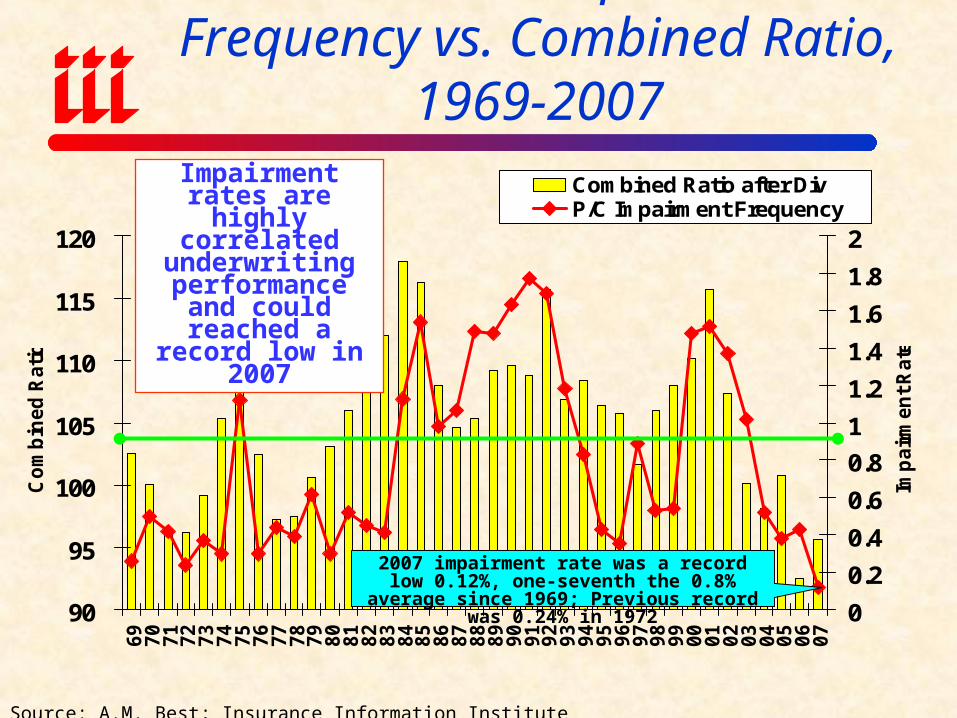

P/C Insurer Impairment Frequency vs. Combined Ratio, 1969-2007

90

95

100

105

110

115

120

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

Co

mb

ined

Ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

Imp

air

men

t R

ate

Combined Ratio after DivP/C Impairment Frequency

Impairment rates are highly correlated

underwriting performance and could reached a

record low in 2007

Source: A.M. Best; Insurance Information Institute

2007 impairment rate was a record low 0.12%, one-seventh the 0.8% average since 1969;

Previous record was 0.24% in 1972

Summary of A.M. Best’s P/C Insurer Ratings Actions in 2008*

Under Review, 63 , 4.3%

Upgraded, 59 , 4.0%

Initial, 41 , 2.8%

Other, 59 , 4.0%

Affirm, 1,183 , 81.0%

Downgraded, 55 , 3.8%

*Through December 19.Source: A.M. Best.

43

Despite financial market turmoil, high cat losses and a soft market in 2008, 81% of ratings actions by A.M. Best

were affirmations; just 3.8% were downgrades

and 4.0% upgrades

P/C insurance is by design a resilient in business. The dual threat of financial

disasters and catastrophic losses are

anticipated in the industry’s risk

management strategy.

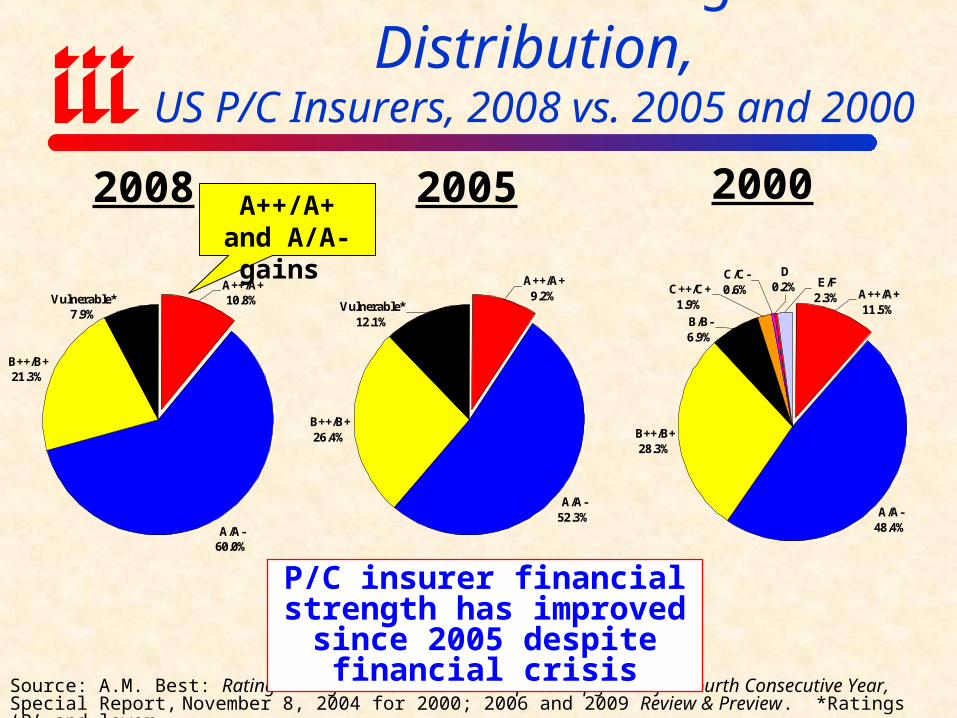

Historical Ratings Distribution,US P/C Insurers, 2008 vs. 2005 and 2000

Source: A.M. Best: Rating Downgrades Slowed but Outpaced Upgrades for Fourth Consecutive Year, Special Report, November 8, 2004 for 2000; 2006 and 2009 Review & Preview. *Ratings ‘B’ and lower.

A/A-48.4%

D0.2%C++/C+

1.9%

E/F2.3% A++/A+

11.5%

C/C-0.6%

B++/B+28.3%

B/B-6.9%

2008 2005

P/C insurer financial strength has improved since 2005 despite financial crisis

A/A-52.3%

A++/A+9.2%

B++/B+26.4%

Vulnerable*12.1%

A/A-60.0%

A++/A+10.8%

B++/B+21.3%

Vulnerable*7.9%

2000A++/A+ and A/A- gains

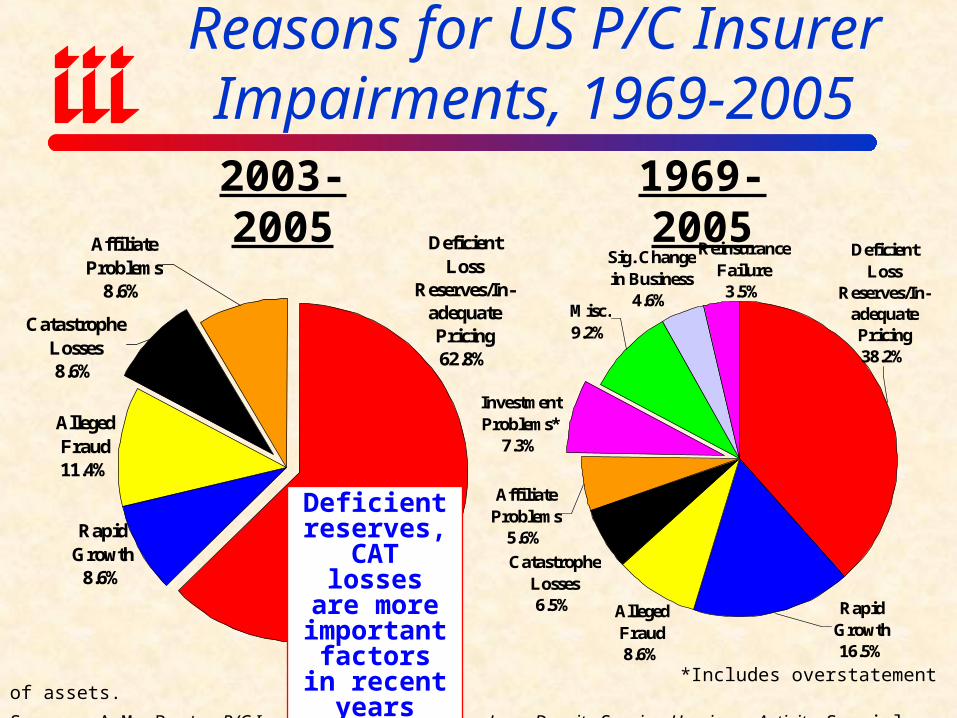

Reasons for US P/C Insurer Impairments, 1969-2005

*Includes overstatement of assets.

Source: A.M. Best: P/C Impairments Hit Near-Term Lows Despite Surging Hurricane Activity, Special Report, Nov. 2005;

Catastrophe Losses8.6%

Alleged Fraud11.4%

Deficient Loss

Reserves/In-adequate Pricing62.8%

Affiliate Problems

8.6%

Rapid Growth

8.6%

2003-2005 1969-2005

Deficient reserves,

CAT losses are more important factors in

recent years

Reinsurance Failure3.5%

Rapid Growth16.5%

Misc.9.2%

Affiliate Problems

5.6%

Sig. Change in Business

4.6%

Deficient Loss

Reserves/In-adequate Pricing38.2%

Investment Problems*

7.3%

Alleged Fraud8.6%

Catastrophe Losses6.5%

Critical Differences Between P/C

Insurers and BanksSuperior Risk Management Model

& Low Leverage Makea Big Difference

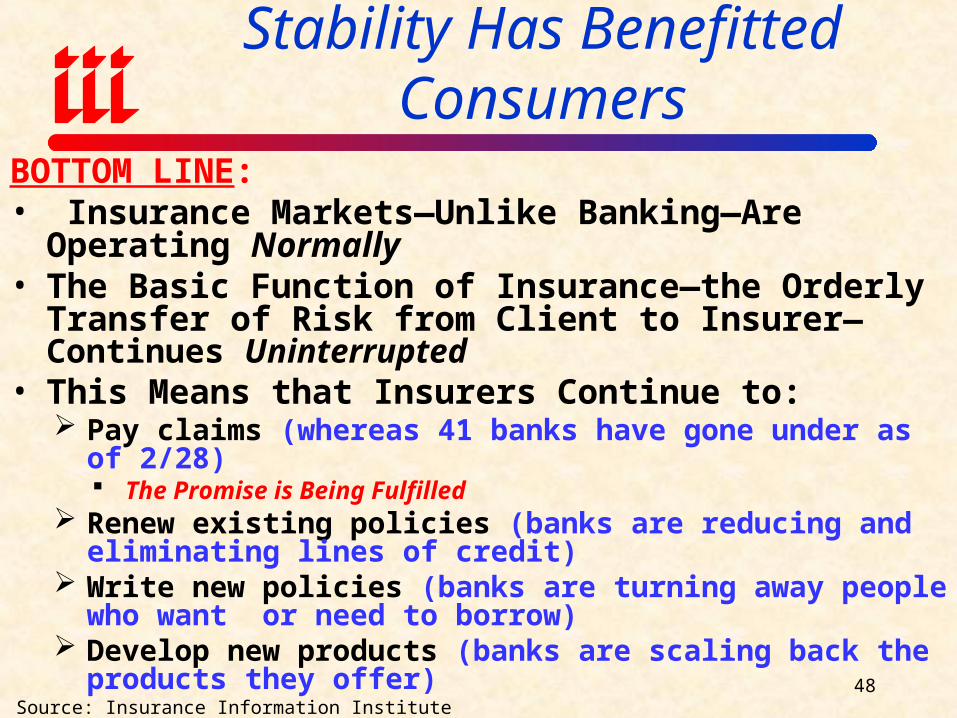

How Insurance Industry Stability Has Benefitted Consumers

BOTTOM LINE:• Insurance Markets—Unlike Banking—Are Operating

Normally• The Basic Function of Insurance—the Orderly Transfer

of Risk from Client to Insurer—Continues Uninterrupted• This Means that Insurers Continue to:

Pay claims (whereas 41 banks have gone under as of 2/28) The Promise is Being Fulfilled

Renew existing policies (banks are reducing and eliminating lines of credit)

Write new policies (banks are turning away people who want or need to borrow)

Develop new products (banks are scaling back the products they offer)

Source: Insurance Information Institute48

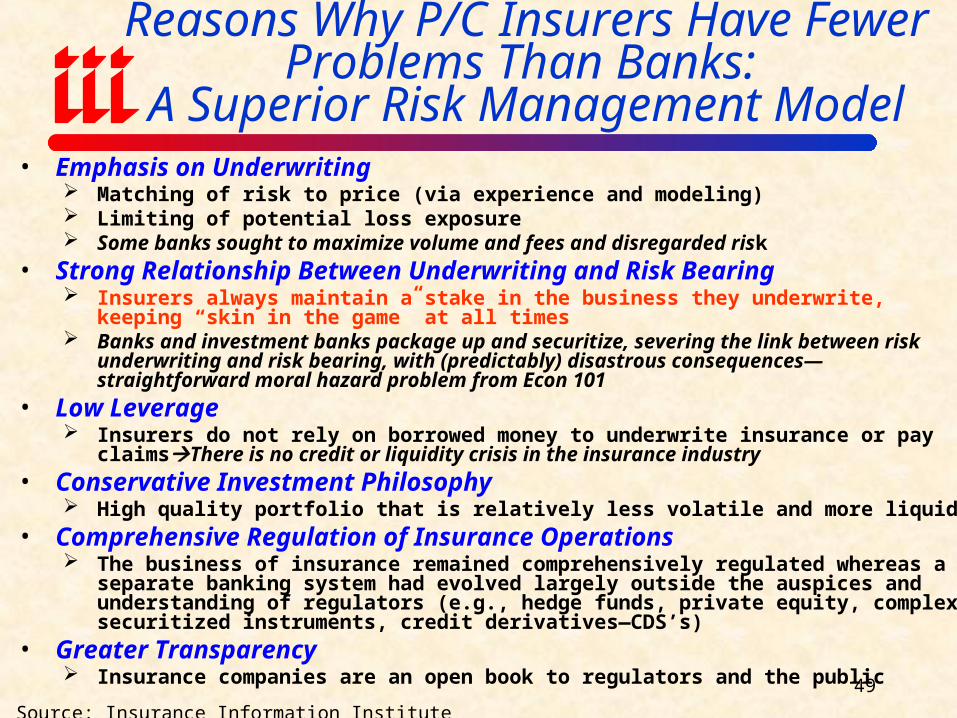

• Emphasis on Underwriting Matching of risk to price (via experience and modeling) Limiting of potential loss exposure Some banks sought to maximize volume and fees and disregarded risk

• Strong Relationship Between Underwriting and Risk Bearing Insurers always maintain a stake in the business they underwrite, keeping “skin in the game”

at all times Banks and investment banks package up and securitize, severing the link between risk

underwriting and risk bearing, with (predictably) disastrous consequences—straightforward moral hazard problem from Econ 101

• Low Leverage Insurers do not rely on borrowed money to underwrite insurance or pay claimsThere is no

credit or liquidity crisis in the insurance industry• Conservative Investment Philosophy

High quality portfolio that is relatively less volatile and more liquid• Comprehensive Regulation of Insurance Operations

The business of insurance remained comprehensively regulated whereas a separate banking system had evolved largely outside the auspices and understanding of regulators (e.g., hedge funds, private equity, complex securitized instruments, credit derivatives—CDS’s)

• Greater Transparency Insurance companies are an open book to regulators and the public

Source: Insurance Information Institute49

Reasons Why P/C Insurers Have Fewer Problems Than Banks:

A Superior Risk Management Model

US Bank Failures:* 1995-2009**

86

13

8 7

4

11

3 4

0 0

3

25

16

0

5

10

15

20

25

30

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09**

Through February 28, 2009

Remarkably, as recently as 2005 and 2006, no

banks failed—the first time this had happened in

FDIC history (dating back to 1934)

*Includes all commercial banking and savings institutions. **Through Feb. 28. Source: FDIC: http://www.fdic.gov/bank/historical/bank/index.html; Insurance Info. Institute

Bank failures are up sharply. 41 banks (but no p/c or life

insurers) failed in 2008/09 due to the financial crisis, including the largest in history—Washington Mutual with $307B in assets.

53

P/C INSURANCE FINANCIAL

PERFORMANCE

A Resilient Industry in Challenging Times

Profitability

Historically Volatile

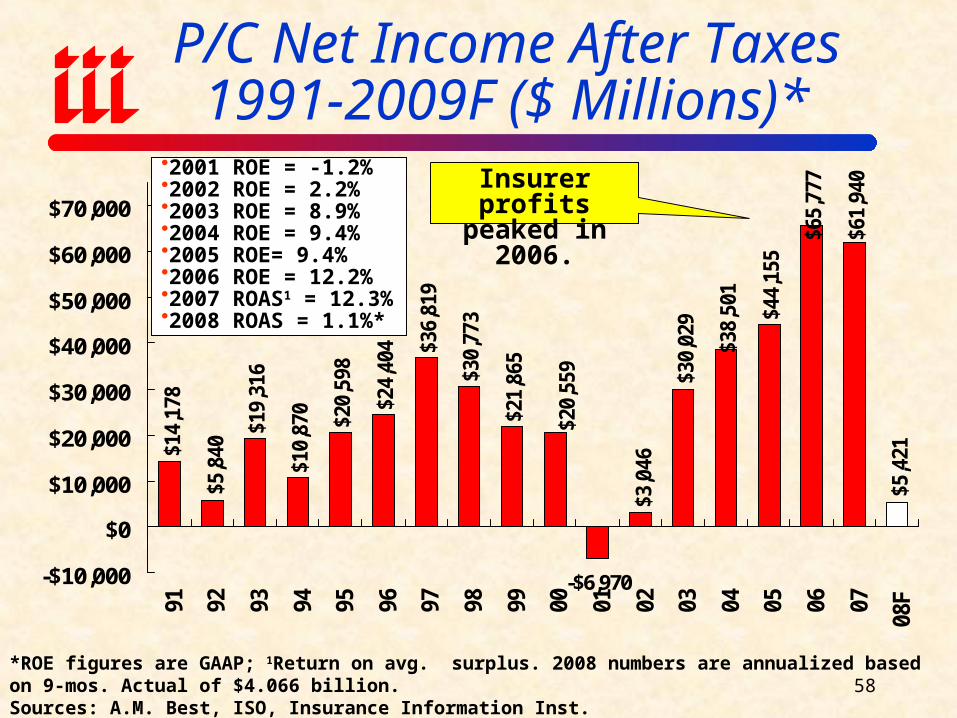

P/C Net Income After Taxes1991-2009F ($ Millions)*

$14,

178

$5,8

40

$19,

316

$10,

870

$20,

598

$24,

404 $3

6,81

9

$30,

773

$21,

865

$3,0

46

$30,

029

$61,

940

$5,4

21

-$6,970

$65,

777

$44,

155

$20,

559

$38,

501

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

08F

*ROE figures are GAAP; 1Return on avg. surplus. 2008 numbers are annualized based on 9-mos. Actual of $4.066 billion.Sources: A.M. Best, ISO, Insurance Information Inst.

2001 ROE = -1.2%2002 ROE = 2.2%2003 ROE = 8.9%2004 ROE = 9.4%2005 ROE= 9.4%2006 ROE = 12.2%2007 ROAS1 = 12.3%2008 ROAS = 1.1%*

Insurer profits peaked in 2006.

58

-5%

0%

5%

10%

15%

20%

25%

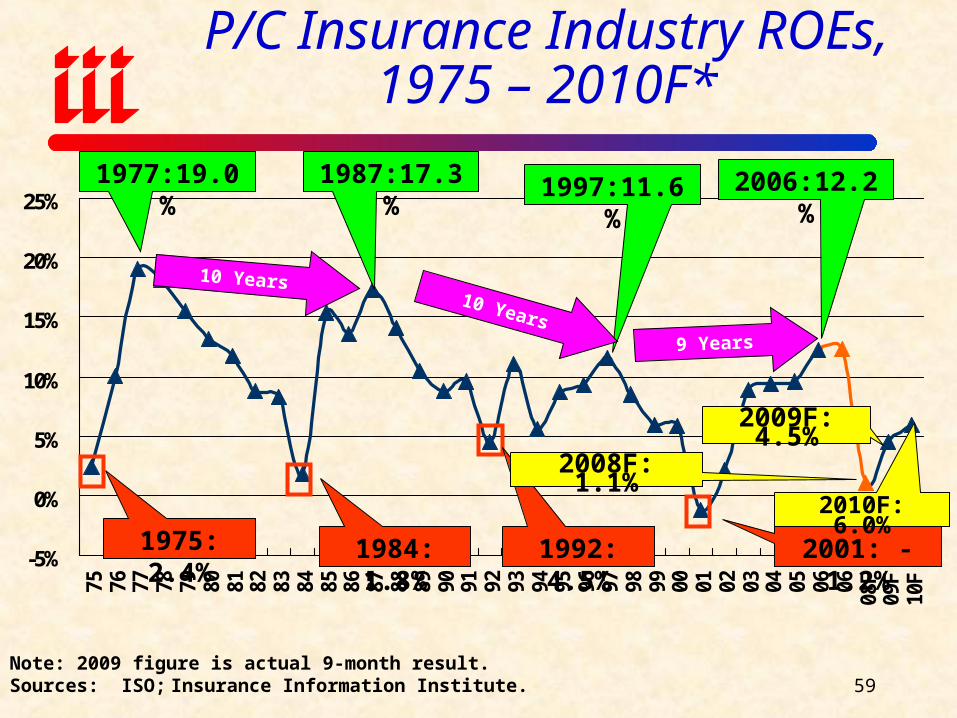

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 0608

F09

F10

F

1975: 2.4%

1977:19.0% 1987:17.3% 1997:11.6% 2006:12.2%

1984: 1.8% 1992: 4.5% 2001: -1.2%

10 Years10 Years

9 Years

Note: 2009 figure is actual 9-month result.Sources: ISO; Insurance Information Institute.

2008F: 1.1%

P/C Insurance Industry ROEs,1975 – 2010F*

2010F: 6.0%

2009F: 4.5%

59

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08*

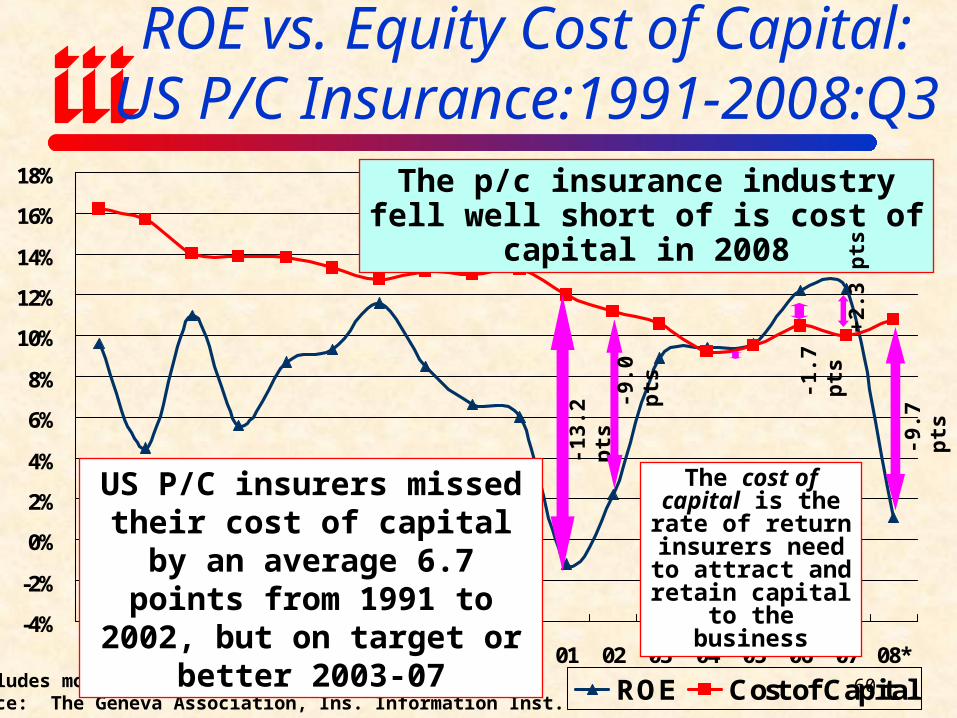

ROE Cost of Capital

ROE vs. Equity Cost of Capital:US P/C Insurance:1991-2008:Q3

*Excludes mortgage and financial guarantee insurers.Source: The Geneva Association, Ins. Information Inst.

The p/c insurance industry fell well short of is cost of capital in 2008

-13.

2 p

ts

US P/C insurers missed their cost of capital by an average 6.7 points from 1991 to 2002, but on

target or better 2003-07

-1.7

pts

+2.

3 p

ts

-9.0

pts

The cost of capital is the rate of return

insurers need to attract and retain

capital to the business

-9.7

pts

60

$ Billions

$1,409 $1,386$1,257

$1,018$919 $894 $878

$804$925$937

$998

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

TX** FL LA OK MS CA MA RI AL CT US

61

Top 10 Most Expensive States for Homeowners Insurance vs. US (2006)*

The average expenditure for home insurance in Texas was $1,409 in 2006, ranking it 1st.

FL has likely overtaken TX.

*Most recent available.**The Texas Dept. of Insurance developed HO policy forms that are similar but not identical to the standard forms.Source: NAIC, Insurance Information Institute

Presidential Politics & P/C Insurance

How is Profitability Affected by the President’s Political Party?

15.10%10.13%

8.93%8.65%

8.35%7.98%

7.68%6.98%6.97%

5.43%5.03%

4.83%4.43%

3.55%

16.43%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Carter

Reagan II

G.W. Bush II

Nixon

Clinton I

G.H.W. Bush

Clinton II

Reagan I

Nixon/Ford

Truman

Eisenhower I

Eisenhower II

G.W. Bush I

Johnson

Kennedy/Johnson

*ROE for 2008 based on H1 data. Truman administration ROE of 6.97% based on 3 years only, 1950-52.Source: Insurance Information Institute

OVERALL RECORD: 1950-2008*

Democrats 8.05%

Republicans 8.02%

Party of President has marginal bearing on profitability of P/C insurance industry

P/C Insurance Industry ROE byPresidential Administration,1950-2008*

P/C Premium Growth

Primarily Driven by the Industry’s Underwriting Cycle, Not the Economy

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

F20

09F

Sources: A.M. Best (historical and forecast), ISO, Insurance Information Institute

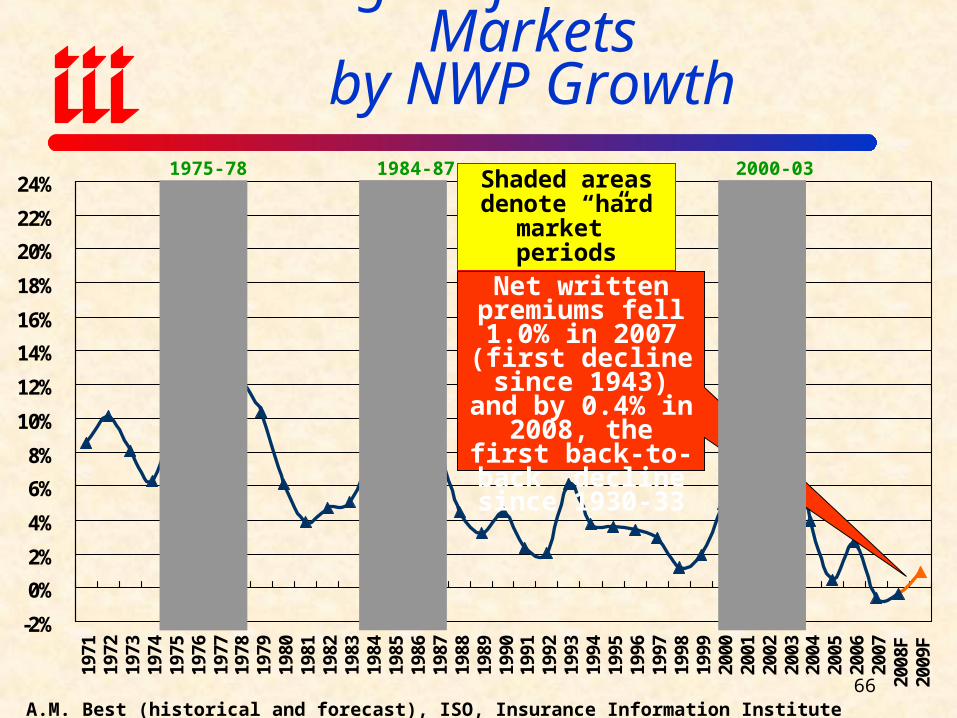

Strength of Recent Hard Marketsby NWP Growth

1975-78 1984-87 2000-03Shaded areas denote “hard

market” periods

Net written premiums fell 1.0%

in 2007 (first decline since 1943)

and by 0.4% in 2008, the first back-

to-back decline since 1930-33

66

Year-to-Year Change in Net Written Premium, 2000-2009F*

*2008 figure is 9-month actual result from ISO.Source: A.M. Best (historical and forecast)

5.0%

8.4%

15.3%

10.0%

3.9%

0.5%

4.2%

-1.0% -0.4%

0.9%

2000 2001 2002 2003 2004 2005 2006 2007 2008F 2009F

P/C insurers are experiencing their

slowest growth rates since 1930-33

Slow growth means retention is critical

Protracted period of

negative or slow growth is possible due to soft

markets and slow

economy

67

Personal/Commercial Lines & Reinsurance NPW Growth, 2006-2009F

2.0% 3.5%

2.5% 5.

0%

28.1%

-0.3

%

0.0%

-11.9%-3.8

%

1.0%

7.6%

-1.4

%-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Personal Commercial Reinsurance

2006 2007 2008E 2009F

Sources: A.M. Best Review & Preview, Feb. 2009

Declines in premium growth began to stabilize in later 2008 and are firming to some extent as we move into 2009, but are partly offset by flat/declining exposures due to the recession

Capital/Policyholder

Surplus

Shrinkage, but Capital is Within Historic Norms

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

$550

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

U.S. Policyholder Surplus: 1975-2008*

Source: A.M. Best, ISO, Insurance Information Institute. *Towers Perrin estimate as of 12/31/08

$ B

illi

ons

“Surplus” is a measure of underwriting capacity. It is analogous to “Owners Equity” or “Net Worth” in non-insurance organizations

Actual capacity as of 9/30/08 was $478.5, down 7.6% from 12/31/07 at $517.9B, but 68% above its 2002

trough. Recent peak was $521.8 as of 9/30/07. Estimate as of 12/31/08 is $438B is 16% below 2007

peak.

The premium-to-surplus ratio stood at $0.94:$1 at year end 2008, up from

near record low of $0.85:$1 at year-end 2007

70

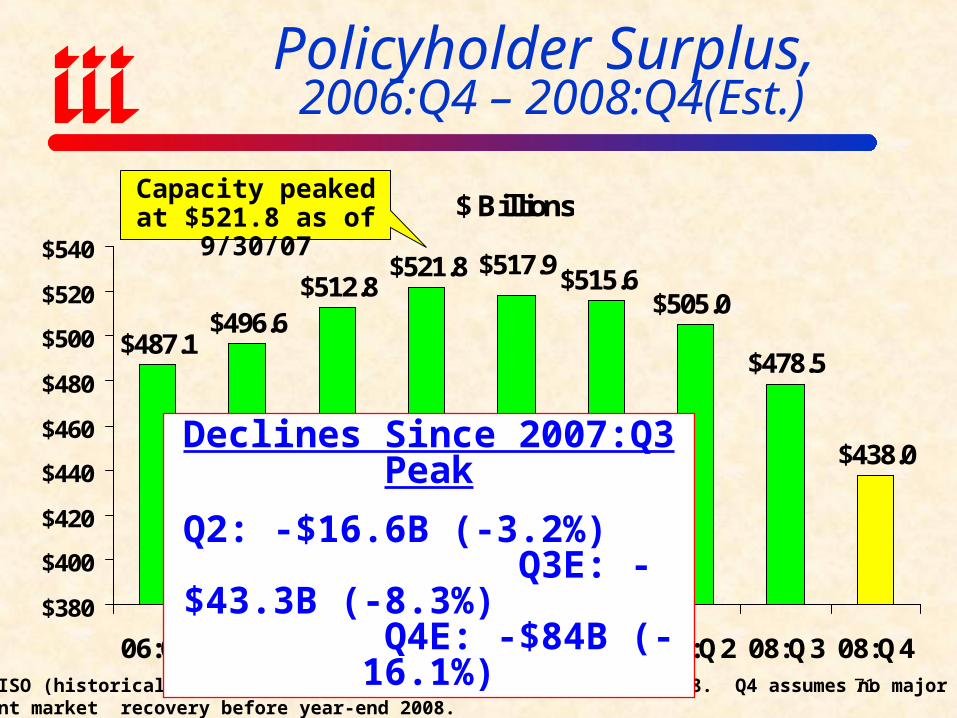

Policyholder Surplus, 2006:Q4 – 2008:Q4(Est.)

$ Billions

$487.1$496.6

$512.8$521.8

$478.5

$438.0

$505.0$515.6

$517.9

$380

$400

$420

$440

$460

$480

$500

$520

$540

06:Q4 07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4

Source: ISO (historical); Towers Perrin (Oct. 21) estimates for Q4 2008. Q4 assumes no major Investment market recovery before year-end 2008.

Declines Since 2007:Q3 Peak

Q2: -$16.6B (-3.2%) Q3E: -$43.3B (-8.3%)

Q4E: -$84B (-16.1%)

Capacity peaked at $521.8 as of 9/30/07

71

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

*

NWP % changeSurplus % change

*Actual 9-month 2008 result.Sources: A.M. Best, ISO, Insurance Information Institute

Historically, Hard Markets Follow When Surplus “Growth” is Negative

Sharp decline in capacity is a necessary but not sufficient

condition for a true hard market

Investment Performance

Investments are the Principle Source of Declining

Profitability

Distribution of P/C Insurance Industry’s Investment Portfolio

Cash & Short-Term Investments

7.2%

Common Stock17.9%

Bonds66.7%

Preferred Stock1.5%

Real Estate0.8%

Other5.9%

Portfolio Facts

•Invested assets totaled $1.3 trillion as of 12/31/07

•Insurers are generally conservatively invested, with 2/3 of assets invested in bonds as of 12/31/07

•Only about 18% of assets were invested in common stock as of 12/31/07

•Even the most conservative of portfolios was hit hard in 2008

Source: NAIC; Insurance Information Institute research;.

As of December 31, 2007

75

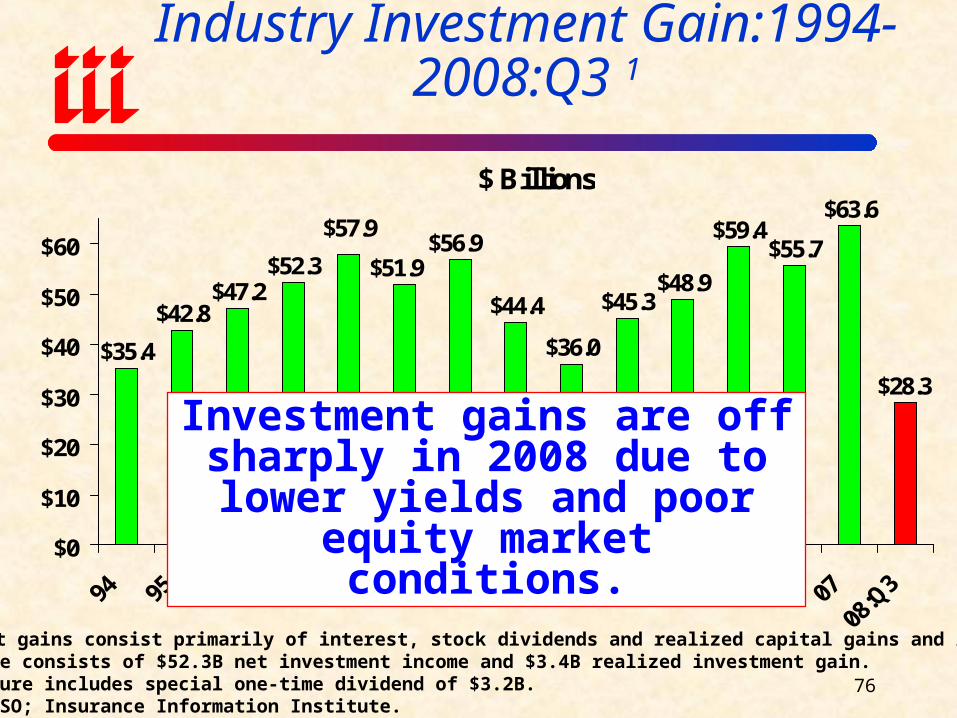

Property/Casualty Insurance Industry Investment Gain:1994- 2008:Q3 1

$ Billions

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7

$63.6

$28.3

$56.9$51.9

$57.9

$0

$10

$20

$30

$40

$50

$60

1Investment gains consist primarily of interest, stock dividends and realized capital gains and losses. 2006 figure consists of $52.3B net investment income and $3.4B realized investment gain. *2005 figure includes special one-time dividend of $3.2B.Sources: ISO; Insurance Information Institute.

Investment gains are off sharply in 2008 due to lower yields and poor equity market conditions.

76

P/C Insurer Net Realized Capital Gains, 1990-2008:Q3

$2.88$4.81

$9.89

$1.66

$6.00

$9.24$10.81

$13.02

$16.21

$6.63

-$1.21

$6.61

$8.97

-$9.71

$18.02

$3.52

$9.70$9.13$9.82

-$10-$8-$6-$4-$2$0$2$4

$6$8

$10$12$14$16$18$20

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

08:Q

3

Sources: A.M. Best, ISO, Insurance Information Institute.

Realized capital gains exceeded $9 billion in 2004/5 but fell sharply in

2006 despite a strong stock market. Nearly $9 billion again in 2007, but

$-9.7 billion in 2008 through Q3.

$ Billions

77

Treasury Bond Yields HaveGenerally Been Falling

-2%

0%

2%

4%

6%

8%

10%

90

91

92

93

94

95

96

97

98

99 00

01

02

03

04

05

06

07

08

09

F

10

F

U.S. Treasury 10-Year Note Yield

Sources: US Bureau of Labor Statistics (history); Blue Chip Economic Indicators, February 2009 issue (forecasts)

ForecastJuly 1990-March 1991

recession

March 2001-November 2001

recession

December 2007 – Present

(Current Recession)

Investment yields on the safest assets

are near multi-decade lows

Underwriting Trends

Financial Crisis Does Not Directly Impact Underwriting

Performance: Cycle, Catastrophes Were 2008’s Drivers

90

95

100

105

110

115

120

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

F

Combined Ratios

1970s: 100.3

1980s: 109.2

1990s: 107.8

2000s: 102.0*

Sources: A.M. Best; ISO, III *A.M. Best year end estimate of 103.2; Actual 9-mos. result was 105.6.

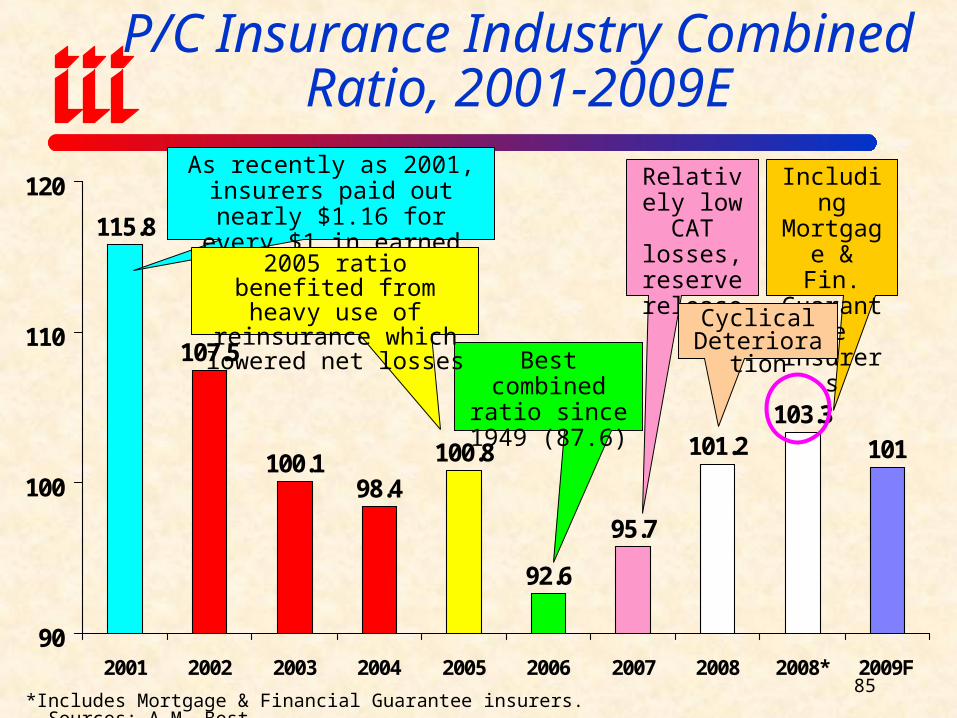

P/C Insurance Combined Ratio, 1970-2008F*

84

115.8

107.5

100.198.4

100.8

92.6

101

103.3101.2

95.7

90

100

110

120

2001 2002 2003 2004 2005 2006 2007 2008 2008* 2009F

P/C Insurance Industry Combined Ratio, 2001-2009E

*Includes Mortgage & Financial Guarantee insurers. Sources: A.M. Best.

Best combined ratio since 1949

(87.6)

As recently as 2001, insurers paid out nearly $1.16 for every

$1 in earned premiums

Relatively low CAT

losses, reserve releases

Including Mortgage

& Fin. Guarantee insurers

Cyclical Deterioration

85

2005 ratio benefited from heavy use of reinsurance which lowered net losses

-55-50-45-40-35-30-25-20-15-10-505

101520253035

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

Source: A.M. Best, ISO; Insurance Information Institute * Includes mortgage & finl. guarantee insurers

$ B

illi

ons

Insurers earned a record underwriting profit of $31.7 billion in 2006, the largest ever but only the

second since 1978. Cumulative underwriting deficit from 1975 through 2007 is $422 billion.

Underwriting Gain (Loss)1975-2008:Q3*

$19.877 Bill underwriting loss in 08:9M incl. mort. & FG insurers

86

Number of Years With Underwriting Profits by Decade, 1920s –2000s

67

10

8

45

0 0

3

0

2

4

6

8

10

1920s 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s*

Note: Data for 1920 – 1934 based on stock companies only.Sources: Insurance Information Institute research from A.M. Best Data. *2000 through 2008.

Number of Years with Underwriting ProfitsUnderwriting profits were common before the 1980s (40 of the 60 years

before 1980 had combined ratios below 100)—but then they vanished. Not a single underwriting profit was recorded in the 25 years from 1979

through 2003.

87

Personal Lines

Auto (~75% of Market)Home (~25%)

103.

9

104.

5

103.

5

104.

9

99.8 10

2.7

104.

5

109.

9

110.

9

105.

3

98.4

94.3 96

.4

93.9

97.6

103.

3

97.6

85

90

95

100

105

110

115

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08E 09FSource: A.M. Best (historical and forecast).

Improvement in 2009 assumes reasonable degree of underwriting

discipline and average CAT activity ($10 B -$12B)

Personal LinesCombined Ratio, 1993-2009F

2008 deterioration due to price

competition and higher CAT

losses. Trends reverse in 2009.

117.7

158.4

113.6118.4

112.7

121.7

101.0

108.2111.4

121.7

109.3

98.394.2

100.1

89.4

95.7

116.5

98

113.0109.4

85

95

105

115

125

135

145

155

165

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08E 09F

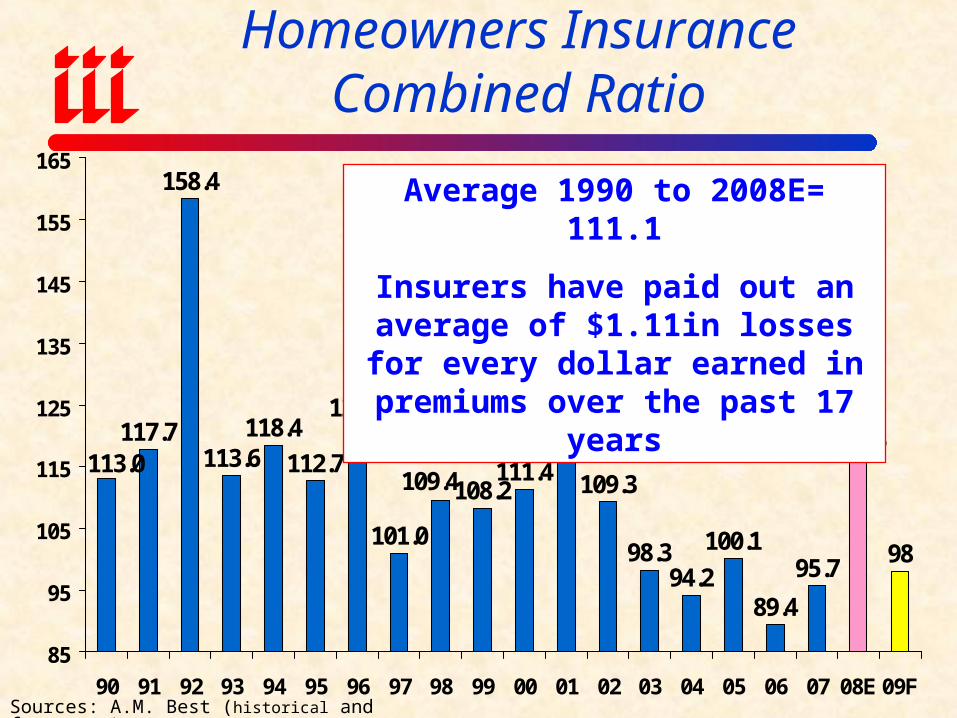

Homeowners Insurance Combined Ratio

Average 1990 to 2008E= 111.1

Insurers have paid out an average of $1.11in losses for every dollar earned in premiums over the past 17 years

Sources: A.M. Best (historical and forecasts)

101.7101.3 101.0

99.5

101.1

103.5

109.5

107.9

104.2

98.4

94.495.1 95.5

98.3 98.597.5

101.3

90

95

100

105

110

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08E 09F

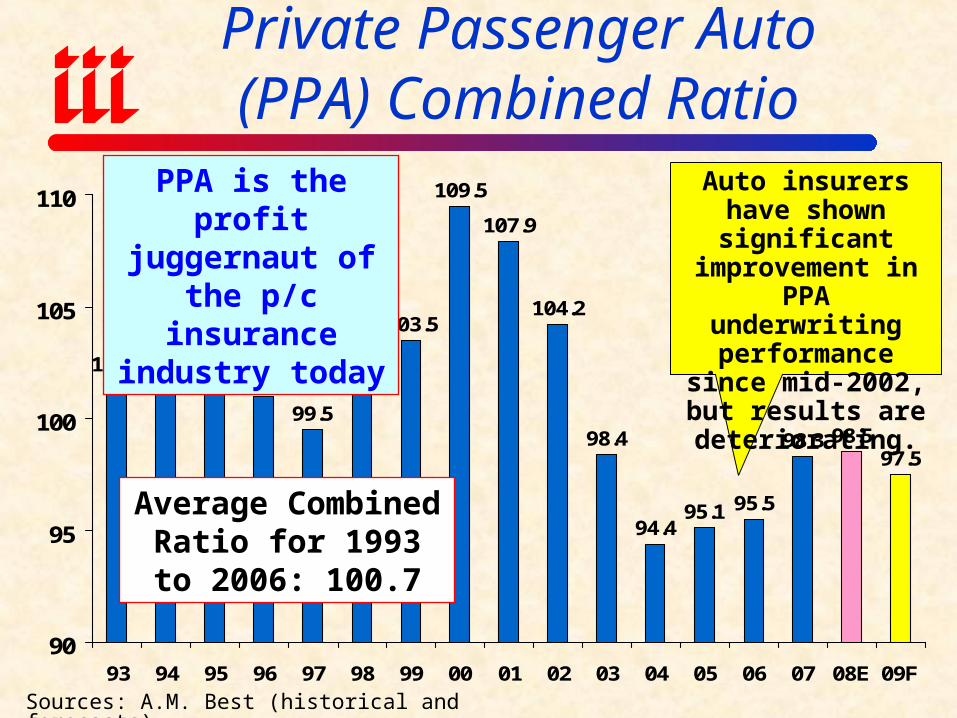

Private Passenger Auto (PPA) Combined Ratio

Average Combined Ratio for 1993 to 2006:

100.7

Sources: A.M. Best (historical and forecasts)

PPA is the profit juggernaut of the

p/c insurance industry today

Auto insurers have shown significant

improvement in PPA underwriting

performance since mid-2002, but results

are deteriorating.

0.8

%

0.8

%

0.5

%

0.4

%

0.3

%

0.3

%

0.5

%

0.6

%

0.5

%

0.1

% 0.5

% 0.9

%

1.1

%

1.3

% 1.7

%

2.6

%

2.6

%

2.7

% 3.0

%

3.1

% 3.4

% 3.7

% 4.0

%

4.0

%

0.2

%

0%

1%

1%

2%

2%

3%

3%

4%

4%

5%

Ja

n-0

7

Fe

b-0

7

Ma

r-0

7

Ap

r-0

7

Ma

y-0

7

Ju

n-0

7

Ju

l-0

7

Au

g-0

7

Se

p-0

7

Oc

t-0

7

No

v-0

7

De

c-0

7

Ja

n-0

8

Fe

b-0

8

Ma

r-0

8

Ap

r-0

8

Ma

y-0

8

Ju

n-0

8

Ju

l-0

8

Au

g-0

8

Se

p-0

8

Oc

t-0

8

No

v-0

8

De

c-0

8

Ja

n-0

9

Monthly Change in Auto Insurance Prices*

*Percentage change from same month in prior year.Source: US Bureau of Labor Statistics

Auto insurance prices have clearly

begun to rise in recent months

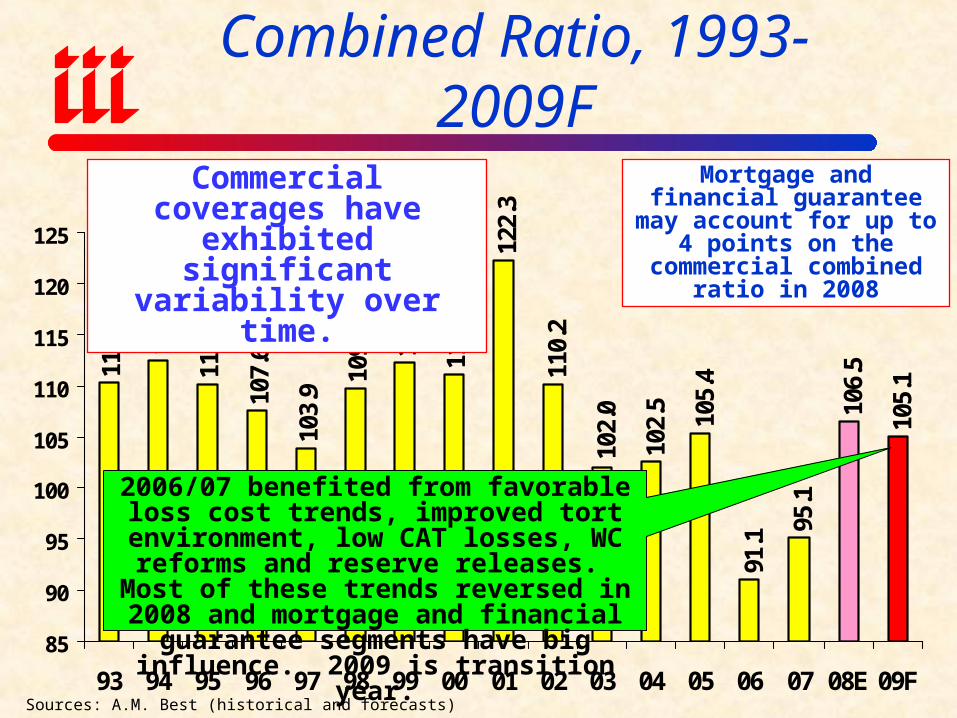

Commercial Lines

110.

3

110.

2

107.

6

103.

9

109.

7

112.

3

111.

1

122.

3

110.

2

102.

5

105.

4

91.1

95.1

106.

5

105.

1

102.

0

112.

5

85

90

95

100

105

110

115

120

125

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08E 09F

2006/07 benefited from favorable loss cost trends, improved tort environment, low CAT

losses, WC reforms and reserve releases. Most of these trends reversed in 2008 and

mortgage and financial guarantee segments have big influence. 2009 is transition year.

Commercial coverages have exhibited significant

variability over time.

Commercial Lines Combined Ratio, 1993-2009F

Mortgage and financial guarantee may account for up to 4 points on the commercial

combined ratio in 2008

Sources: A.M. Best (historical and forecasts)

Advertising

Unlike in Post 9/11 Period, Insurer Advertising Likely to

Remain Strong

Advertising Expenditures by P/C Insurance Industry, 1999-2007

$ Billions

$1.736 $1.737 $1.803 $1.708

$3.426

$4.102

$2.975

$2.111$1.882

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

99 00 01 02 03 04 05 06 07

Source: Insurance Information Institute from consolidated P/C Annual Statement data.

Ad spending by P/C insurers is at a record high, signaling

increased competition

Catastrophe Losses

Impacting Underwriting Results and the Bottom Line

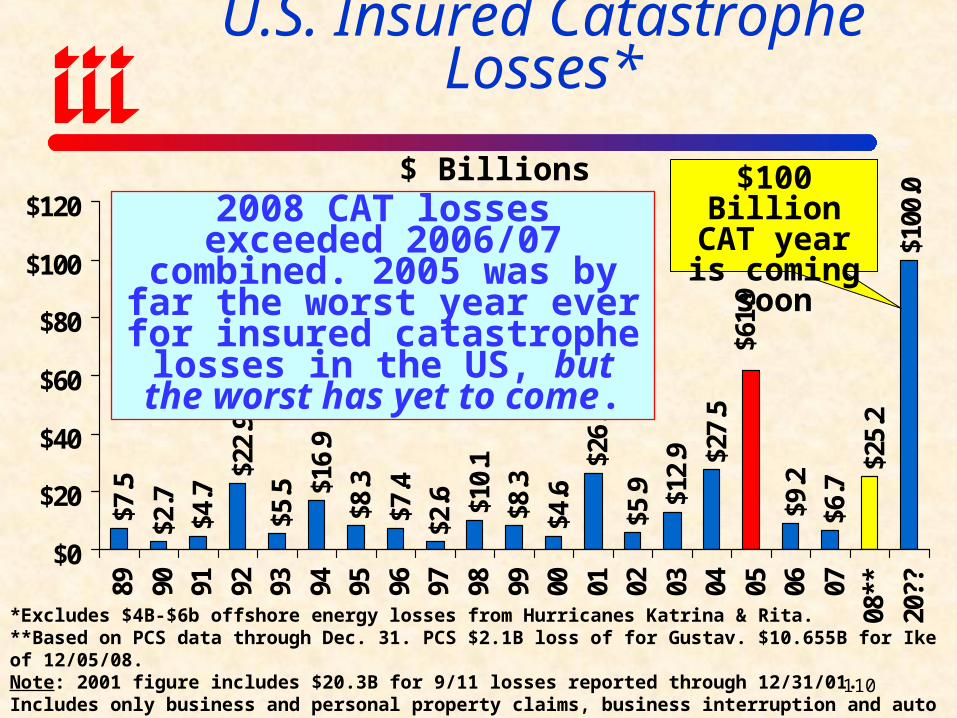

U.S. Insured Catastrophe Losses*$7

.5

$2.7

$4.7

$22.

9

$5.5 $1

6.9

$8.3

$7.4

$2.6 $1

0.1

$8.3

$4.6

$26.

5

$5.9 $1

2.9 $2

7.5

$6.7

$25.

2$1

00.0

$61.

9

$9.2

$0

$20

$40

$60

$80

$100

$120

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

08**

20??

*Excludes $4B-$6b offshore energy losses from Hurricanes Katrina & Rita.**Based on PCS data through Dec. 31. PCS $2.1B loss of for Gustav. $10.655B for Ike of 12/05/08.Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01. Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B.Source: Property Claims Service/ISO; Insurance Information Institute

$ Billions2008 CAT losses exceeded

2006/07 combined. 2005 was by far the worst year ever for

insured catastrophe losses in the US, but the worst has yet to come.

$100 Billion CAT year is coming soon

110

States With Highest Insured Catastrophe Losses in 2008

$ Billions

$10.2

$2.2$1.6 $1.3 $1.0

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

Texas California Minnesota Ohio Georgia

Source: PCS; Insurance Information Institute.

Big catastrophe losses turned up in some surprising states in 2008, due to high tornado, hail and wildfire damage as well as

inland hurricane damage

Top 12 Most Costly Disasters in US History, (Insured Losses, $2007)

$4.0 $5.0 $6.0 $7.0 $7.8 $8.2$10.7 $10.9 $10.9

$22.0 $22.9

$43.6

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

Jeanne(2004)

Frances(2004)

Rita (2005)

Hugo(1989)

Ivan (2004)

Charley(2004)

Ike(2008)*

Wilma(2005)

Northridge(2004)

9/11Attacks(2001)

Andrew(1992)

Katrina(2005)

$ B

illi

ons

*PCS estimate as of 12/15/08.Sources: ISO/PCS; AIR Worldwide, RMS, Eqecat; Insurance Information Institute inflation adjustments.

9 of the 12 most expensive disasters in US history

have occurred since 2004

In 2008, Ike became the 6th most expensive insurance event and 4th most

expensive hurricane in US history

112

AFTERSHOCK: Regulatory Response

Could Be Harsh

All Financial Segments Including InsurersWill Be Impacted

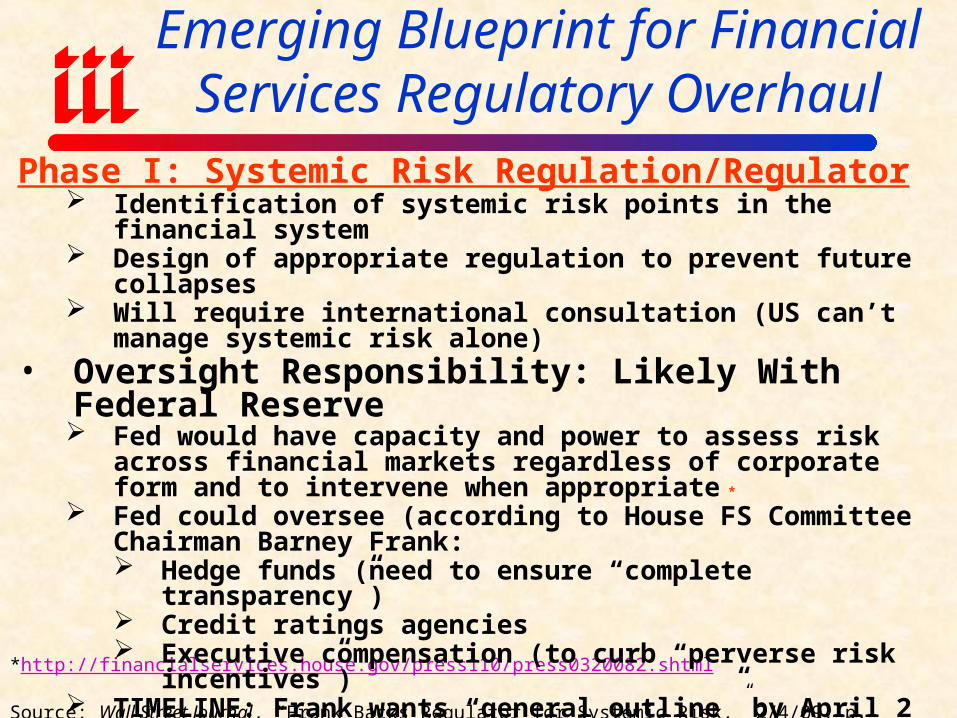

Emerging Blueprint for Financial Services Regulatory Overhaul

*http://financialservices.house.gov/press110/press0320082.shtml

Source: Wall Street Journal, “Frank Backs Regulator for Systemic Risk,” 2/4/09, p. C3; I.I.I. research.

Phase I: Systemic Risk Regulation/Regulator Identification of systemic risk points in the financial system Design of appropriate regulation to prevent future collapses Will require international consultation (US can’t manage systemic risk

alone) • Oversight Responsibility: Likely With Federal Reserve

Fed would have capacity and power to assess risk across financial markets regardless of corporate form and to intervene when appropriate *

Fed could oversee (according to House FS Committee Chairman Barney Frank: Hedge funds (need to ensure “complete transparency”) Credit ratings agencies Executive compensation (to curb “perverse risk incentives”)

TIMELINE: Frank wants “general outline” by April 2 meeting of G20 industrialized and developing nations

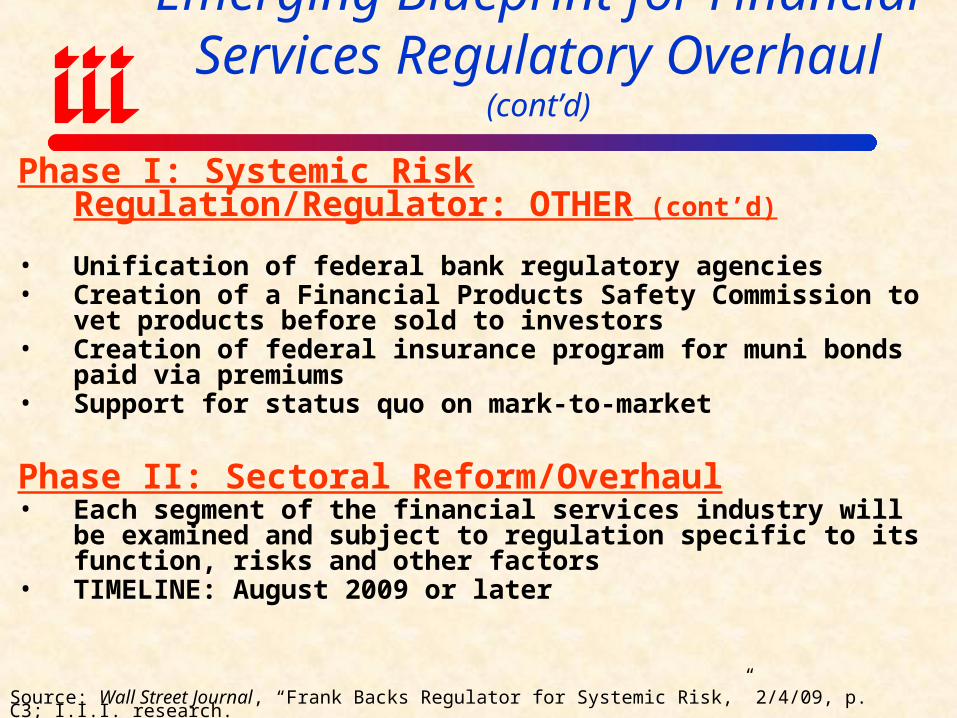

Emerging Blueprint for Financial Services Regulatory Overhaul (cont’d)

Phase I: Systemic Risk Regulation/Regulator: OTHER (cont’d)

• Unification of federal bank regulatory agencies• Creation of a Financial Products Safety Commission to vet products

before sold to investors• Creation of federal insurance program for muni bonds paid via premiums• Support for status quo on mark-to-market

Phase II: Sectoral Reform/Overhaul• Each segment of the financial services industry will be examined and

subject to regulation specific to its function, risks and other factors• TIMELINE: August 2009 or later

Source: Wall Street Journal, “Frank Backs Regulator for Systemic Risk,” 2/4/09, p. C3; I.I.I. research.

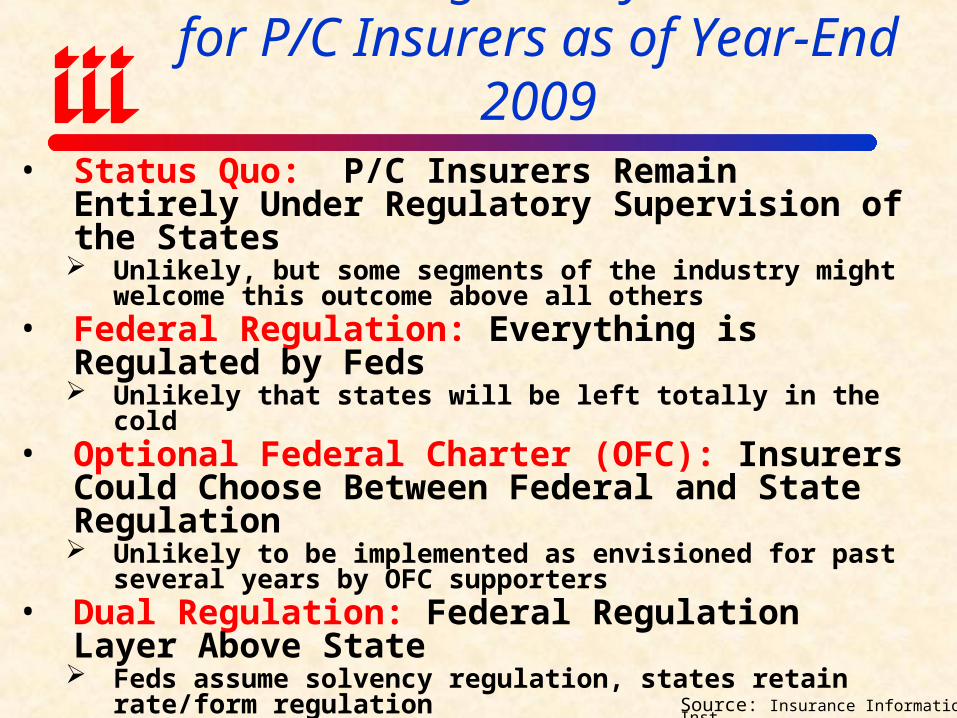

Possible Regulatory Scenarios for P/C Insurers as of Year-End 2009

Source: Insurance Information Inst.

• Status Quo: P/C Insurers Remain Entirely Under Regulatory Supervision of the States Unlikely, but some segments of the industry might welcome this

outcome above all others• Federal Regulation: Everything is Regulated by Feds

Unlikely that states will be left totally in the cold• Optional Federal Charter (OFC): Insurers Could Choose

Between Federal and State Regulation Unlikely to be implemented as envisioned for past several years by

OFC supporters• Dual Regulation: Federal Regulation Layer Above State

Feds assume solvency regulation, states retain rate/form regulation• Hybrid Regulation: Feds Assume Regulation of Large

Insurers at the Holding Company Level• Systemic Risk Regulator: Feds Focus on Regulation of

Systemic Risk Points in Financial Services Sector What are these points for insurers? P/C vs. Life?

Insurance Information Institute On-Line

THANK YOU FOR YOUR TIME AND

YOUR ATTENTION!

127