TNK-BP Presentation to financial community - Credit … Presentation to financial community Credit...

31

TNK-BP Presentation to financial community Credit Suisse Moscow Oil & Gas Day 7 June 2007

Transcript of TNK-BP Presentation to financial community - Credit … Presentation to financial community Credit...

TNK-BP

Presentation to financial communityCredit Suisse Moscow Oil & Gas Day

7 June 2007

2

Cautionary StatementsForward Looking Statements Cautionary Statement

This presentation and the associated slides and discussion contain forward looking statements, particularly those regarding capital expenditure, capital investments, spending on integrity management, annual charges, cost inflation, production and impact of delays in projects on production, expected return to capacity of projects, share buybacks and other distributions to shareholders, group costs, divestment proceeds and their use, effective tax rate, future performance, gearing, growth opportunities, global economic growth, global oil demand growth, oil and gas prices, performance, oil and gas production, production growth, refining margins, refining availability and capacity, outlook for refining environment, the timing of major projects and their contribution to TNK-BP (or TNK-BP Holding) net resources and the application of technology.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that will or may occur in the future. Actual results may differ from those expressed in such statements, dependingon a variety of factors, including the timing of bringing new fields on stream; future levels of industry product supply; demand and pricing; operational problems; general economic conditions; political stability and economic growth in relevant areas of the world; changes in laws and governmental regulations; exchange rate fluctuations; development and use of new technology; changes in public expectations and other changes in business conditions; the actions of competitors; natural disasters and adverse weather conditions; wars and acts of terrorism or sabotage; and other factors discussed elsewhere in this presentation.

June 2007

3

TNK-BP at a glanceUPSTREAM

OilOil GasGas

3% organic oil & gas production growth in 2006 (excl. Slavneft)

1.5 mln bpd liquids production (excluding Slavneft)

7.81 billion barrels total proved liquids reserves (129% replacement)

$250 mln exploration spend; 60% E&A success rate

Growing portfolio of new oil opportunities

0.18 mln boe/day (1.05 bcf/d) of gas sales

Associated gas

Long term options:

Rospan

Kovykta

DOWNSTREAM

Refining & ExportsRefining & Exports Marketing & SalesMarketing & Sales

5 refineries (4 Russia, 1 Ukraine)

0.62 mln bpd refining capacity

Major exporter to Europe –50% of sales as crude, 24% as refined products

Multiple export channels

1,650 retail outlets in Russia and Ukraine

Focused retail expansion in major markets

Operation under BP and TNKbrands

Margin enhancement through building of marketing businesses in lubricants, bitumen

#11 global private oil producer #3 refiner in Russia, with diverse sales channels

4

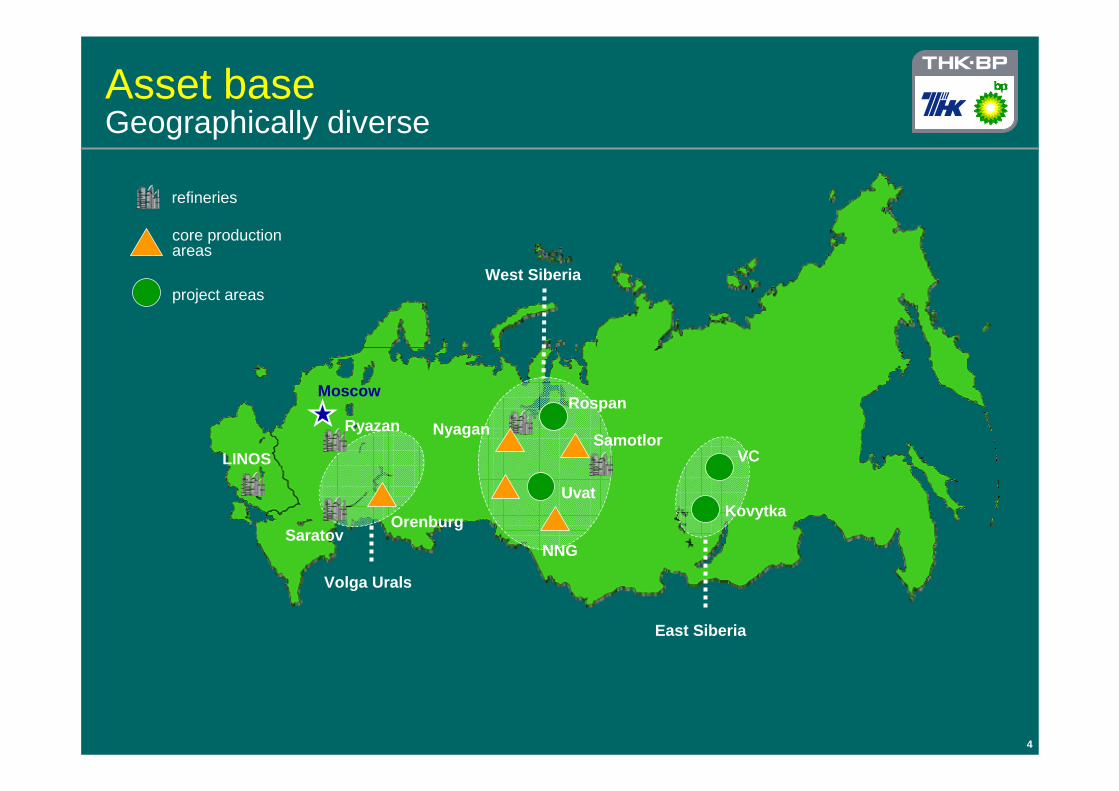

Asset baseGeographically diverse

core production areas

project areas

Volga Urals

West Siberia

Moscow

East Siberia

Samotlor

Orenburg

RospanNyagan

Kovytka

VC

NNG

Uvat

refineries

Ryazan

Saratov

LINOS

5

TNK-BP Corporate Structure

Notes: This year TNK-BP Holding’s US GAAP consolidated financial statements (for 12M2006) are being prepared for the first time

50%

Businesses consolidated into TNK-BP International’s US GAAP financial statements

Businesses recorded as equity investments

Businesses which are not consolidated into TNK-BP International’s US GAAP financial statements but are consolidated into TNK-BP Limited’s US GAAP financial statements0

Upstream Refining Marketing

95%

50%

TNK-BP Ltd (BVI)

50%

63%

TNK Industrial Holdings Ltd(BVI)

STBP Holdings Ltd.

75%

RUSIA Petroleum

TNK-BP Holding

Slavneft(JV with

Gazprom Neft)

TNK-BP Finance S.A. (Luxembourg)

100%

100%

Lisichansk Refinery

(UKRAINE)

68%

Alfa, Access/Renova B P

TNK-BP International Ltd (BVI) 100%

6

Competitive contextRelative ranking of Russian VIOCs in 2006

Russian VIOCs with more refining cover and higher retail exposure enjoy a competitive advantage due to tax incentives to refine in current price environment

Nevertheless, on longer-term performance indicators (like F&D costs, ROACE, capex intensity) TNK-BP leads the industry, as well as maintaining top position in generating of free cash flow per boe production for 3 consecutive years.

Adjusted for assets sale TNK-BP’s production was up 1.0% (liquids) and 0.6% (oil & gas) in 4M07.Rosneft’s 5.0% growth was mainly due to YuganskNG (+7.7% growth y-o-y), while Rosneft's production without YuganskNG decreased by 1.1%; Lukoil’s oil and gas growth (5.3% y-o-y) was mainly due to Nahodkinskoye gas field’s contribution.

112323333Rosneft

223232121Lukoil

331111212TNK-BP

Oil & GasOilF&D costsROACECapex Intensityunit FCFEBITDA

per boeNet

MarginOps Cash

$/boe1 is best

Production organic growth, y-o-yLong-term indicatorsShort-term indicatorsRelative

ranking*;

7

Operating competitive contextProduction, 2006

0.0

0.20.4

0.60.8

1.0

Lukoil Rosneft TNK-BP (incl. Slavneft) Gazprom (incl.Gazprom neft and

Slavneft)

SurgutNG

mln

bpd

Refining Throughput, 2006

Yukos assets Slavneft

0.0

0.5

1.0

1.5

2.0

2.5

Rosneft (incl. YUKOS) Lukoil TNK-BP (incl. Slavneft) SurgutNG Gazprom (incl. Gazpromneft and Slavneft)

mln

bpd

Yukos assets Slavneft

Slavneft

Slavneft

8

Financial competitive context

2006 Dividend Yield, %14.8

1.4 0.7

4.53.0

02468

10121416

TNK-BP Lukoil Rosneft Emg MktOils

SuperMajors

2006 EBITDA, $/boe

11.215.6

11.1

25.4

34.7

0

10

20

30

40

TNK-BP Lukoil Rosneft Emg MktOils

SuperMajors

2006 Capex, $/boe

3.4

8.26.6

13.0 13.8

02468

10121416

TNK-BP Lukoil Rosneft Emg MktOils

SuperMajors

Note: Based on TNK-BP Ltd data (except div. yield computed for TBH)

2006 FCF, $/boe

3.8

0.2

9.6

12.6

-0.2

-2

0

2

4

6

8

10

12

14

TNK-BP Lukoil Rosneft Emg MktOils

SuperMajors

Note: Dividend yield = Dividends paid in 2006 / Year-avg MCap

Note: TNK-BP financials adjusted for gain from assets disposals and tax provisions

9

Financials

26%

17%14%

30%

21%

47%

27%14%

0

5

10

15

20

25

30

35

40

2003 2004 2005 2006

$ bn

0

10

20

30

40

50

60

70$/bbl

Net Revenues Export Duties and Excise taxes Urals CIF

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2003 2004 2005 2006

$ bn

EBITDA Gain from assets disposals

Note:Based on TNK-BP Ltd data

xx% - share of excise taxes and export duties in gross revenues;yy% - Urals CIF price growth (y-o-y 2006)

* - Net income adjusted on tax provisions

Revenues vs. Oil price

EBITDA Net Income

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2003 2004 2005 2006

$ bn

Net Income* Gain from assets disposals

10

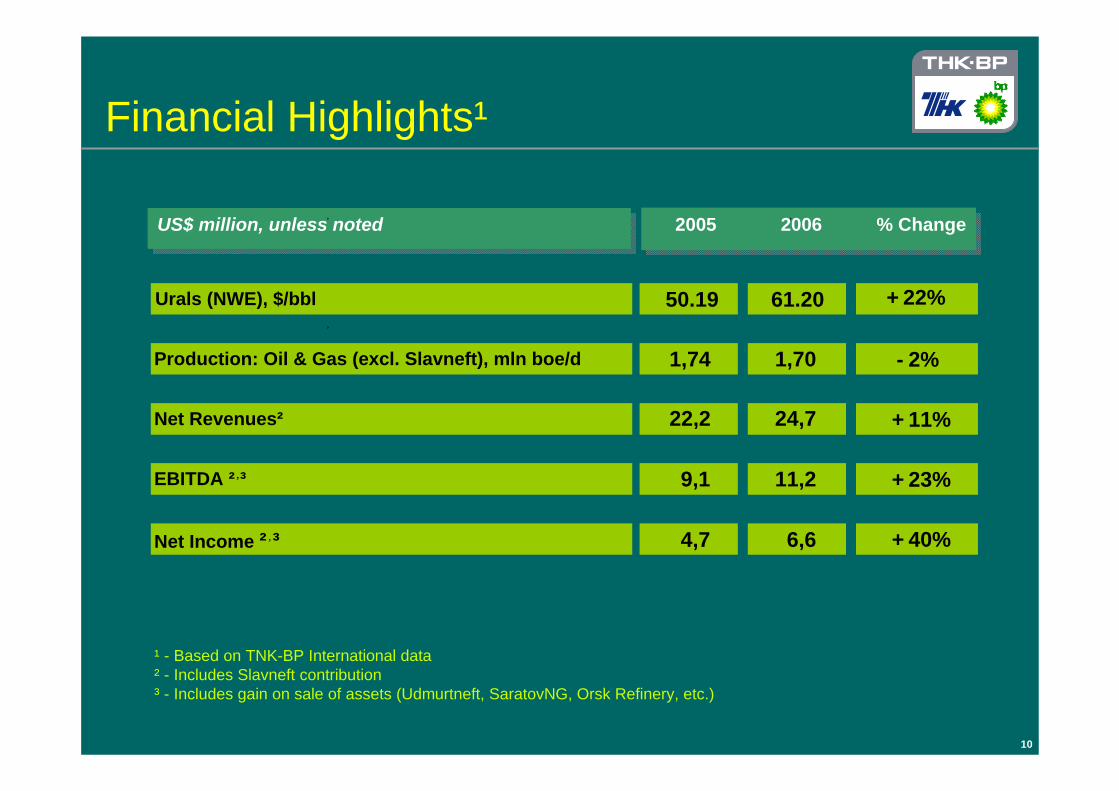

US$ million, unless notedUS$ million, unless noted 2005 2006 % Change

Urals (NWE), $/bbl 50.19 61.20 + 22%

Production: Oil & Gas (excl. Slavneft), mln boe/d 1,74 1,70 - 2%

Net Revenues² 22,2 24,7 + 11%

EBITDA ² ³ 9,1 11,2 + 23%

Net Income ² ³ 4,7 6,6 + 40%

Financial Highlights¹

¹ - Based on TNK-BP International data² - Includes Slavneft contribution³ - Includes gain on sale of assets (Udmurtneft, SaratovNG, Orsk Refinery, etc.)

, ,

,

,

,

11

Financial framework

• Target gearing (net debt / net debt + equity) range: 25-50%

• Credit Ratings: achieve and maintain investment grade ratings. Two out of three rating agencies at investment grade now

• Dividends: minimum 40% of net income and all surplus cash returned to shareholders

• Dividend levels consistent with majority shareholders

• Dividends paid twice yearly at AGM (2Q) and EGM (4Q). Over $8bn declared in 2006 and $0.9bn recommended for AGM in June 2007

TNK-BP Holding:TNK-BP Holding:

TNK-BP Limited:TNK-BP Limited:

12

TNK-BP Transaction

1. Deliver production growth

2. Deliver technology transfer

3. Deliver good corporate governance

4. Deliver socially responsible business conduct

At the time TNK-BP was established, the shareholders made four commitments that would define the Company’s activities going forward:

13

Production growthInitial production growth driven

by optimisation and wellwork:

• Well optimisation

• Frac programme

Improved base management:

• Voidage replacement

• Pattern reconfiguration

Access to additional oil:

• 3D imaging

• Infill drilling

• Sidetracks

• Idle well recovery

Portfolio optimisation:

• Tail disposals (Saratov, Udmurtneft)

• 50% Vanyoganneft acquisition

Oil & Gas ProductionMillion barrels per day

1.0

1.5

2.0

2.5

2003 2004 2005 2006 2007E

mln bpd

0

1

2

3

4

5$bn

Base Slavneft Disposed assets Capex

14

Underpin Brownfield production delivery

• Focus on base waterflood management; optimization of waterflood pattern conversions/target setting

• Waterflood pattern reconfiguration through sidetracking and idle well reactivations

• Putting large 3D seismic programs into use for well identification and planning

• Enhanced Oil recovery, including gas injection

Greenfield developments

• Active appraisal program at Uvat

• TNK-BP approved pilot production project and early oil scheme (EOS) at Verknechonskoye

• Pilot programs initiated for heavy oil project (Russkoye and Vanyoganskoye)

• Pilot designs for Bolshehetsky area in 2008 (Suzun and Tagul)

Reserves management

• Plans to maintain a reserve replacement ratio of at least 100% in the medium term (on a boe basis)

Exploration and Access

• 34 exploration and appraisal wells drilled in 2006 with a 71% success rate.

• Activity in Rospan (oil rim) and East Charsky

• Obtained 35 new licenses during 2006, including 3 in Volga River Delta (Astrakhan)

Technology is a key value driver that underpins brownfield growth and reserve replacement

Technology delivery

15

Refining – key to margin enhancement

• We have invested to improve integrity and product slate of our refineries increasing capacity (34 mtpa, up 15% on 2003) and utilization (to 92%).

• We completed a major upgrade at Ryazan in 2006, enabling production of de-sulphurised high quality fuels (Euro-4 standards)

• We also took advantage of favorable market conditions to restructure the composition of our refining assets through the disposal of the Orsk refinery in order to concentrate on the strategically better positioned plants in Ryazan, Saratov and Yaroslavl (run jointly with Gazprom Neft).

Refining ThroughputThousand barrels per day

Refining netback vs. Transneft export netback

10

20

30

30 40 50 60

Netback, $/bbl

Transneft export netback Simple refining netback

Brent, $/bbl

427 450

75 7172124 132 107

118 125128

130

341 366

120

0

200

400

600

800

2003 2004 2005 2006Russia Disposals Ukraine Slavneft

Due to export duty advantage of products vs. crude even simple refining netbacks exceed Urals export netbacks on Transneft’s core export routes in Brent price range from $50 to $60/bbl. This stimulates oil companies to increase refinery runs.

16

• $2.7 billion in capital and operating costs committed to HSE over next 5 years

• 2,000 hectares of polluted land remediated to end 2006

• 1,400 kilometres of new pipelines (distance equivalent to that between Moscow and Yekaterinburg) installed to replace old worn out lines to end 2006

• PPE equipment issued to all relevant staff, seatbelts fitted, trained inspectors, technical standards and training progressing and performance assessed

• In addition around $1.0 bn over the next 5 years to reduce flaring

HSEHSE

• 150,000 man-days of professional training and development delivered to end 2006

• $370 million worth of social investment programs delivered in 9 regions of Russia in 2005 and 2006

People and Social ProgramsPeople and Social Programs

• Paid over US$ 45 billion of taxes, duties and excise since inception

TaxesTaxes

Samotlor in 2004-2005: polluted acreage before remediation…

…after remediation

Community contribution

17

TNK-BP Vision and Strategy

Possible Winning Formula for Sustained Growth:

Old Oil (Brownfields)

+ New Oil (Greenfields)

+ Gas Development (Organic, influence NOT control)

– Divestments (Tail Assets)

+ Active Inorganics (possible, value additive only)

Vision:To be the leading integrated private Russian Oil and Gas company as measured by profitability and scale

Vision:To be the leading integrated private Russian Oil and Gas company as measured by profitability and scale

Strategy:• Resources to Reserves to Production• Margin Enhancement• Gas• Corporate Governance

Strategy:• Resources to Reserves to Production• Margin Enhancement• Gas• Corporate Governance

Tactics:• Continual Portfolio Management; New

resource access• World-class Health, Safety and Environmental

Standards• World-class Technology Application• World-class Operating Practices• The Best Retail Gasoline Brands in Russia and

the Ukraine• Continual Organizational Capability Growth• World-class Business Practices and Systems• Proactive Regulatory Reform and Competition

Enhancement• Transparency and Corporate Governance

Tactics:• Continual Portfolio Management; New

resource access• World-class Health, Safety and Environmental

Standards• World-class Technology Application• World-class Operating Practices• The Best Retail Gasoline Brands in Russia and

the Ukraine• Continual Organizational Capability Growth• World-class Business Practices and Systems• Proactive Regulatory Reform and Competition

Enhancement• Transparency and Corporate Governance

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2004 2006 2008 2010 2012 2014 2016

mln boed

Major projects, Access, Big GasBase, Waterflood, Wellwork & Drilling

18

TNK-BP strategic priorities• Resources to reserves to production

• Margin enhancement

• Gas

• Value enhancement through improved governance, transparency and performance management

• New Resource Access of 4.7 Bn boe Risked, 70% Exploration Success rate• Organic Reserve Replacement of 2.5 Bn Bo; ~ 125% +• Production growth of 30% since 2003

• $600 mln Ryazan Refinery Modernization, Refining throughputs > 15%• Moscow Retail Expansion & BP Ultimate, St Petersburg / Rostov / Krasnodar New

Entry• $5 Bn + Portfolio Rationalization Program

• Associated Gas Utilization Program• Kovykta Regional Gasification

• TNK-BP Holding (TBH) Restructuring• Accounting Transformation; 10 Day IAS / US GAAP Accounting Close• $45 Bn + in taxes, duties, excise taxes and fees to the state since Day 1• World Economic Forum Principles Against Corruption

19

Resources to reserves

0

10

20

30

40

50

0

1000

2000

3000

4000

5000

6000

7000SP

E pr

oved

Prob

able

Pos

sibl

e

International markets

Infrastructure access

Current production

Infill drilling

Near infrastructureled development

Drilling and re-completions

3P G

as re

sour

ce

Field optimisation

Improved Recovery

Kovykta and Rospan

mln tonnesbn boe 2003-06 Proved SEC Life of Field Reserves Billion barrels of oil equivalent

7.9 8.0 8.2 7.8

0.1 0.6

0.0

2.0

4.0

6.0

8.0

10.0

2003 2004 2005 2006

bn boe

Base Disposals

127%137%

129%

100%

110%

120%

130%

140%

2004 2005 2006

Organic Reserves Replacement Ratio

2006

New

lic

ense

s ac

cess

New licences purchase

Disposals

20

Undeveloped FieldsUndeveloped Fields

Active portfolio management

ExplorationExploration

Tail assets disposalsTail assets disposals

New License AccessNew License Access

Udmurtneft disposal to Sinopec (c. 950 mmbbl 2P reserves for $3.5 bn or $4 bn including Udmurtneft’s pre-sale dividends)

SaratovNG disposal to Russneft (c. 110 mmbbl 2P reserves for $600 mln; total deal amount inc. Orsk Refinery more than $0.8 bn)

In 2004-2006 – 53 new licenses acquired with more than 800 mt of oil and about 500 bcm of gas for about $400 mln

In 2006 alone – 35 new licenses acquired (including 12 Yugansk licenses).

License acreage size of Switzerland (> 40 000 sq km)

Purchase of the remaining 50% of the Vanyoganneft JV from Occidental for $485 mln – this asset has attractive synergies with our core Samotlor area and offers some 1.4 bn boe resource potential

Over 1 billion bbls SPE 2P reserves discovered in 2004-2006 at c. $0.50/bbl

Opportunities for rapid conversion to production in Brownfields (e.g. Orenburg)

SamotlorNG, Orenburgneft, Vanyoganneft, VarieganNG, Nizhnevartovsk, NovosibirskNGKamennoye

etc.

Udm

urtneft, SaratovNG

Uvat, Verkhnechonsk, Bolshekhetsky, Russkoye, new licenses

Astrakhan, new licenses

AcquisitionsAcquisitions

Key to future production growth in 2009 and beyond

Established portfolio with 10+ world scale projects

21

Greenfield Delivery: Uvat• Development of multiple fields across

17 leases stretching 230km

• Estimated reserves in the range of c. 1.3 bln bbls (Kalchenskoye, Urnenskoye,Ust-Tegusskoye, Severo-Demianskoye and Polunyakhskoye)

• Total estimated capex: c. $7-8 bln

• The first stage of commercial development will have production of 3-5 mln tons per annum (or 60 -100 th. bpd) by end of decade

• Active Exploration and Appraisal program continues

• Regional pipeline and road already sanctioned

• Existing Kalchinskoye production 1.5 mln tonnes in 2006

• Potential deeper horizons

• Gas options

,

WestSiberia

Khanti-Mansisk

SouthTyumen Oblast

Samotlor

Khanti Mansisk AOKhanti Mansisk AO

Urnenskoye

Kalchinskoye

South Tyumen OblastSouth Tyumen Oblast

Severo-Demianskoye

Polunyakh

Ust-Teguss

Future road, pipeline & power corridorFuture road, pipeline & power corridorTNK-BP licensesTNK-BP licenses

100 km

22

Greenfield Delivery: VerkhnechonskNG

• TNK-BP, together with a partner Rosneft, is carrying out additional appraisal activity and is progressing an early oil scheme to link the field with the Eastern Siberia Pacific Ocean pipeline now under construction by Transneft.

• In 2008 TNK-BP plans to be one of the first oil company to supply crude to this new pipeline.

• Estimated probable and possible reserves of c. 1.4 bn bbls of oil.

• Total estimated capex: c. $4 bln

• Plateau production: c. 7 -10 mlntons per annum ( 140 – 200 th. bopd)

• Active Appraisal and optimization program continues

23

Greenfield Delivery: Bolshekhetsky

• TNK-BP continues a focused appraisal and pilot production programme in the Bolshekhetsky area in the Krasnoyarsk region

• Seismic analysis and deep drilling have already doubled estimated resources to 100 million tons of oil (over 750 million barrels).

• Total estimated capex: c. $4 bn

• Plateau production: c. 8 - 10 mln tons per annum (or 160 –200 th. bopd)

• Active Exploration and Appraisal Program continues

• Pilot Production 2008Russkoe

TNK-BP licensesTNK-BP licenses

Suzunskoe

Tagulskoe

Russko-Rechenskoe

Vankorskoe

Lodochnoe

,

WestSiberia

Khanti-Mansisk

SouthTyumen Oblast

Samotlor

24

Greenfield Delivery: Kamennoye• The Kamennoye field is part of the

Nyagan group of fields and has estimated resources of 1.1 billion tons.

• These fields were discovered quite some time ago, but were then considered “undevelopable”.

• TNK-BP is using leading technology such as 3D seismic reservoir modeling, horizontal access, water injection and other enhanced recovery methods which has allowed us to revaluate the field’s potential.

• Currently drilling and production is underway in the least complex segments.

• Accelerated / select Phased developed approach being proven and pursued

NovosibirskNovosibirsk

TyumenTyumen

NyaganNyagan

• Total Phase I & Phase II capex: c. $4 bn

• Plateau production Phase I & II: c. 8 - 10 mln tons per annum (or c. 160 – 200 th. bopd)

25

Margin enhancement• Before 2006 key driver was optimisation of crude export routes via scarce pipeline capacity

• Export tax regime now favours refined product exports; refined product sales generated the highest netback in 2006 compared to other channels

• Pipeline export volumes are no longer constrained by Transneft capacity and have also experienced strong growth while rail and river crude export volumes have been reduced and redirected to domestic refining

• Domestic crude sales yield netbacks similar to pipeline exports

Far-abroad pipeline exports

Refined product sales Domestic sales CIS exports (incl. deliveries to LINOS)

Far-abroad rail & river exports

2006 avg $31.6/bbl

2004 avg $19.1/bbl

Netbacks in 2006 vs. 2004 by direction of sales

Notes: Pattern-coloured bars represent 2004 netbacksSource: TNK-BP Estimates

Distribution of Crude Sales, %

Net

back

, US

$/bb

l

2004

2006

30%

32% 8%

8%17%

8%

35%

41% 11%

10%

26

Marketing Strategy• Developing company owned and operated retail network in

high growth markets

• Rationalizing legacy assets in core regions and divesting in low demand regions

• Utilizing our 2 distinct Brands in the highest growth and value metropolitan markets

• Applying fully consistent TNK and BP branded offers, facilities and services

• Strengthen TNK jobber program in advantaged supply regions

• Enhancing existing lubricants business

• Developing offers for growing B2B channel

• Building capabilities to sustain current operations and future business

27

Gas business• Strategic priority: transformation from an oil company into a major oil and gas company

• Resource-rich gas portfolio with two world-class fields in Yamal (Rospan) and in East Siberia (Kovykta)

• With approximately 8-9 bcm sold annually, TNK-BP commercial gas sales in 2006 were 385 billion cubic feet (10.9 bcm), 13% up compared to 2005

• TNK-BP gas business has the potential to produce 50 bcma or more by 2015

• We plan to reach 95% associated gas utilization by 2008-2009

Rospan(100% owned by

TNK-BP)

Rospan(100% owned by

TNK-BP)

2006 Year end SPE reserves (SEC booked annual = production)

• Gas – 18.6 trillion cubic feet (525 bcm, probable and possible)

• Liquids – 1.0 bln bbl of oil (proved, probable and possible)

Commercial gas sales of 98.9 billion cubic feet (2.8 bcm) in 2006

Associatedgas

Associatedgas

• Associated gas utilisation projects on track as a platform to increase gas production and sales and reduce flaring

• JV agreement signed with Sibur in November 2006 to process associated gas produced by TNK-BP in the Nizhnevartovsk region.

28

Governance

• Corporate Restructuring

• Management Information Systems

• Accounting Transformation Project

• Upstream Asset Based Organization

• Strengthening External Audit

• New Policies and Standards

• Enterprise-Wide Risk Management

29

Corporate Policies and Standards

Code ofBusinessPolicies

Corporate Standards

Other normative documentsprocedure, process map; instruction

technical standard

Administrative documentsan order; a directive; a resolution

Organizational documentsorganizational structure; terms of reference; staffing plan job description

Ethical Conduct

• Managing conflict of interest• Principles of business

operations• Business gifts and

entertainment

Employees

• Employees

Security

• Information Security• Assets classification for

security purposes

External relationships

• External corporate relations

Health, Safety & Environment

• Health, Safety & Environment

Control and Finance

• Internal Control and Finance• Internal documents

Operations

• Enterprise-Wide Risk Management

• Procurement of Material and Services

• Purchase and Sale of Hydrocarbon Transportation and Refining Services

• Integrity Management

30

Majors

• Reserves Management• Production Growth• Midstream Options• Value Chain Optimisation

WACC reduction on:• Transparency• Governance

Control• Performance Mgt

Significant value upside

R / P Management

Netback enhancement

Market liberalisation

Gap due to:• Lower

diversification;• Value chain

limitations;• Distance to markets

Emerging Market company valuation ceiling; RF Progressive Tax

Corporate Governance

Country Risk

$2 / boe

Day 1 Sept 04

$12 / boe

$17 / boe

$3 / boe

$5 / boe

2006

TNK-BP

31

Summary

• Quality opportunity set

• High quality skilled workforce

• Resource base confirmed and robust

• Right technology application can deliver

• Focus on margin enhancement via channel optimization

• Gas will become increasingly important

• Governance progressing, more to do