Time-Series Analysis and Forecasting – Part V To read at home.

32

Time-Series Analysis and Forecasting – Part V To read at home

-

Upload

laura-ward -

Category

Documents

-

view

218 -

download

1

Transcript of Time-Series Analysis and Forecasting – Part V To read at home.

Time-Series Analysis and Forecasting – Part V

To read at home

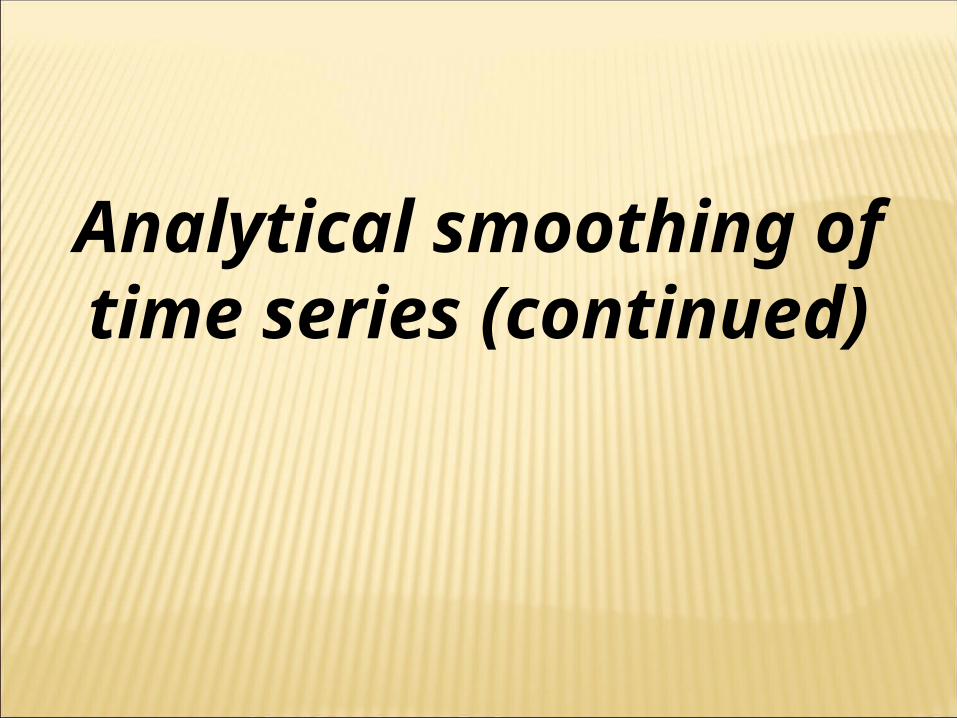

Analytical smoothing of time series (continued)

The second-order parabola smoothing:

where b – speed of change of the levels of time series

c – acceleration

2y a b t c t ,

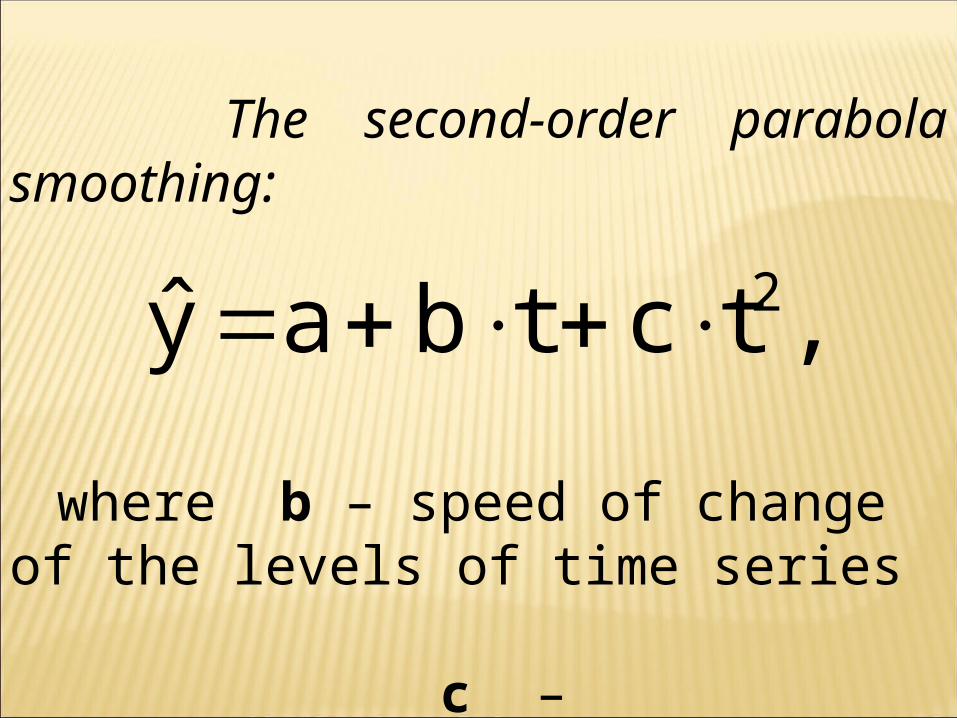

The second-order parabola smoothing is done when the preliminary analysis shows

that the second differences are approximately equal between each other

- the first difference;

- the second difference

1tt(1)t yyΔ

(1)1t

(1)t

(2)t ΔΔΔ

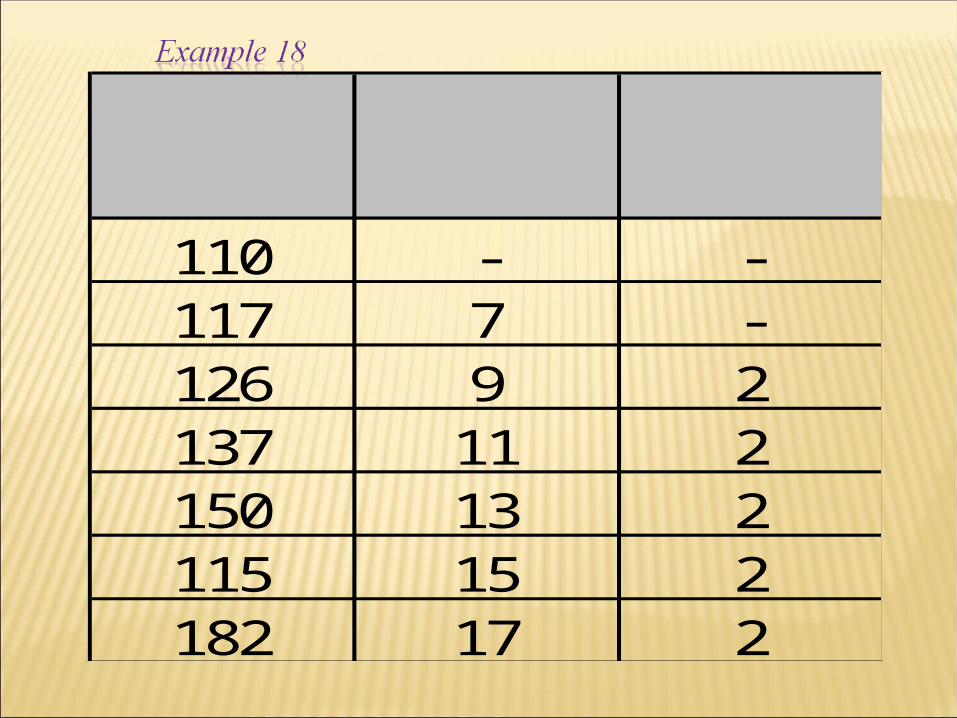

110 - -117 7 -126 9 2137 11 2150 13 2115 15 2182 17 2

ty (1)tΔ

(2)tΔ

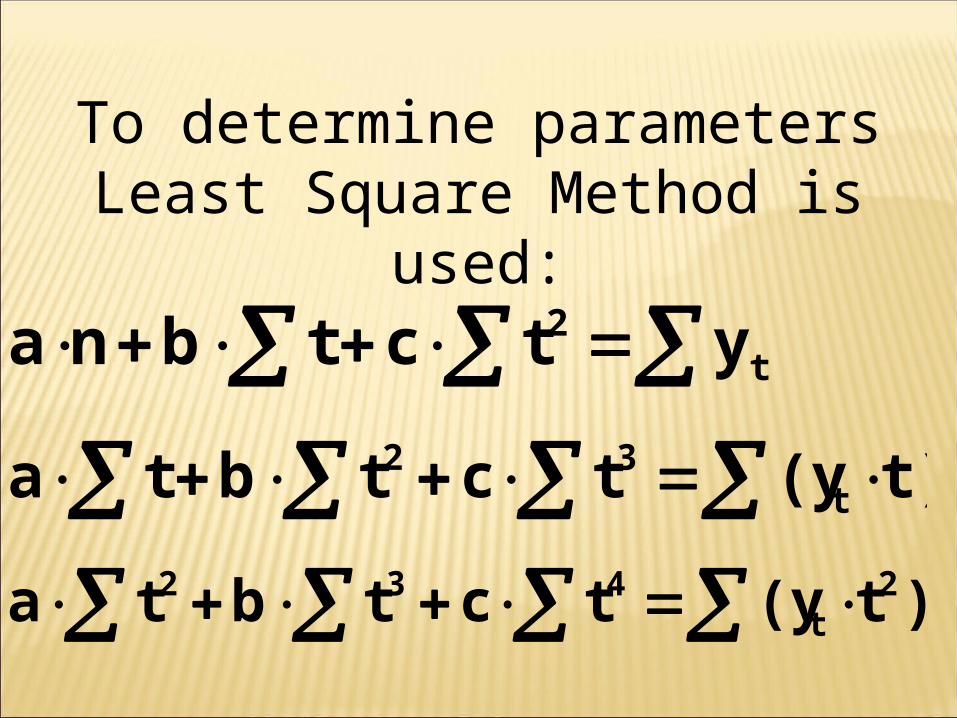

To determine parameters Least Square Method is used:

t2 ytctbna

t)(ytctbta t32

)t(ytctbta 2t

432

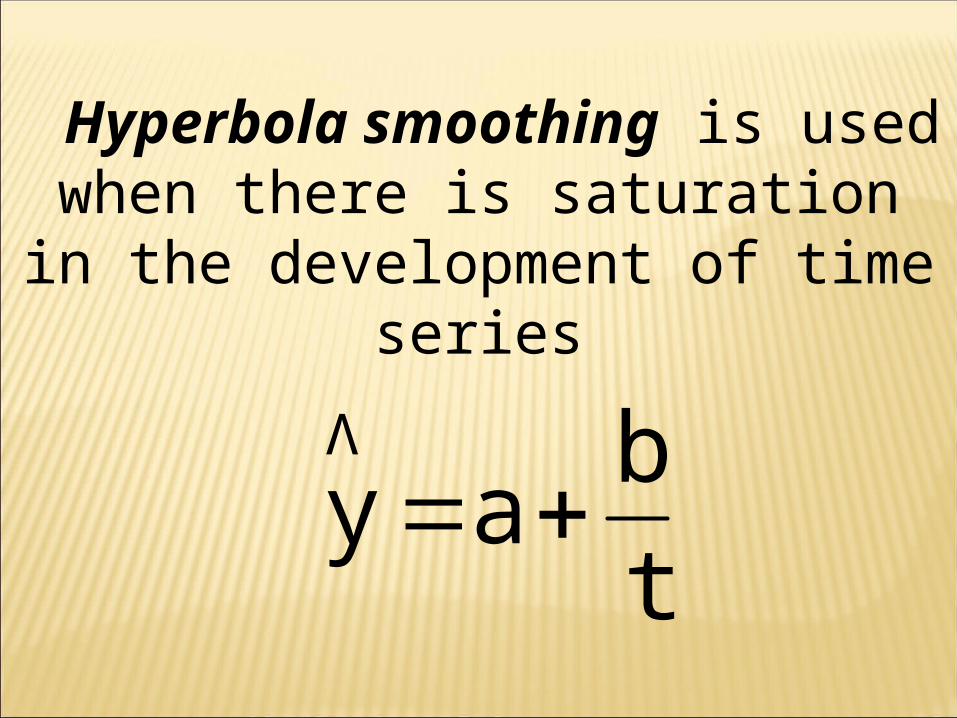

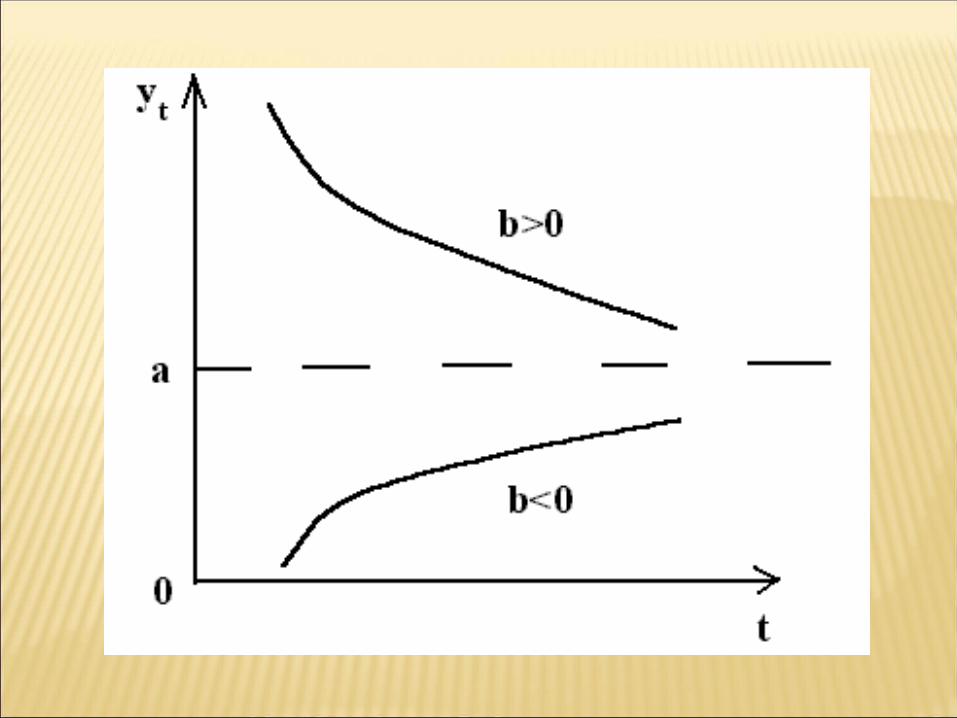

Hyperbola smoothing is used when there is saturation in the development

of time series

t

bay

Λ

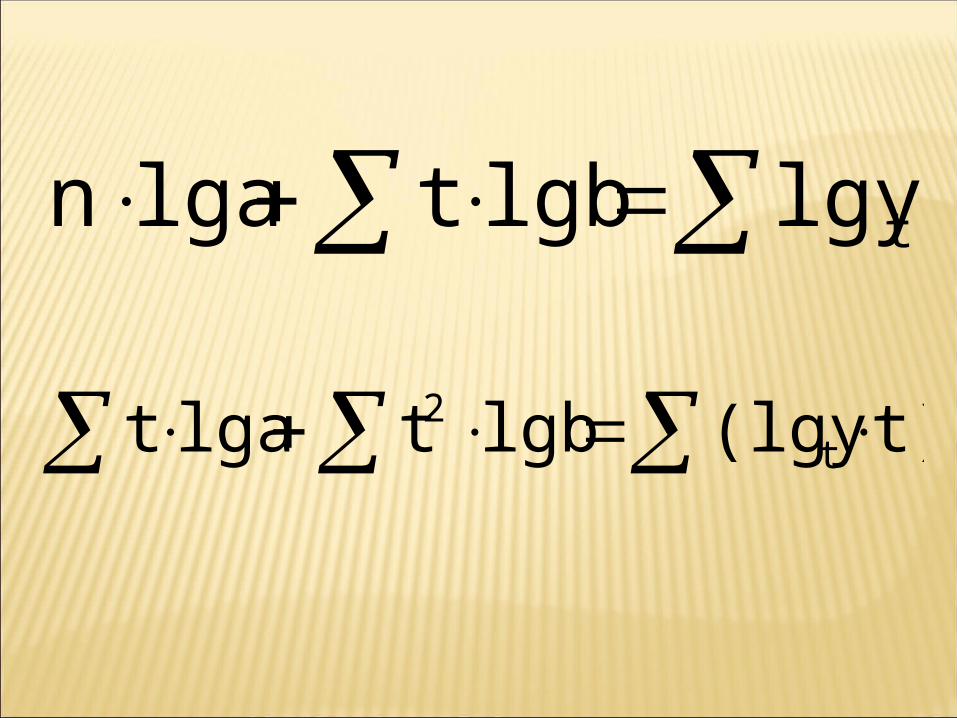

tlgylgbtlgan

t)(lgylgbtlgat t2

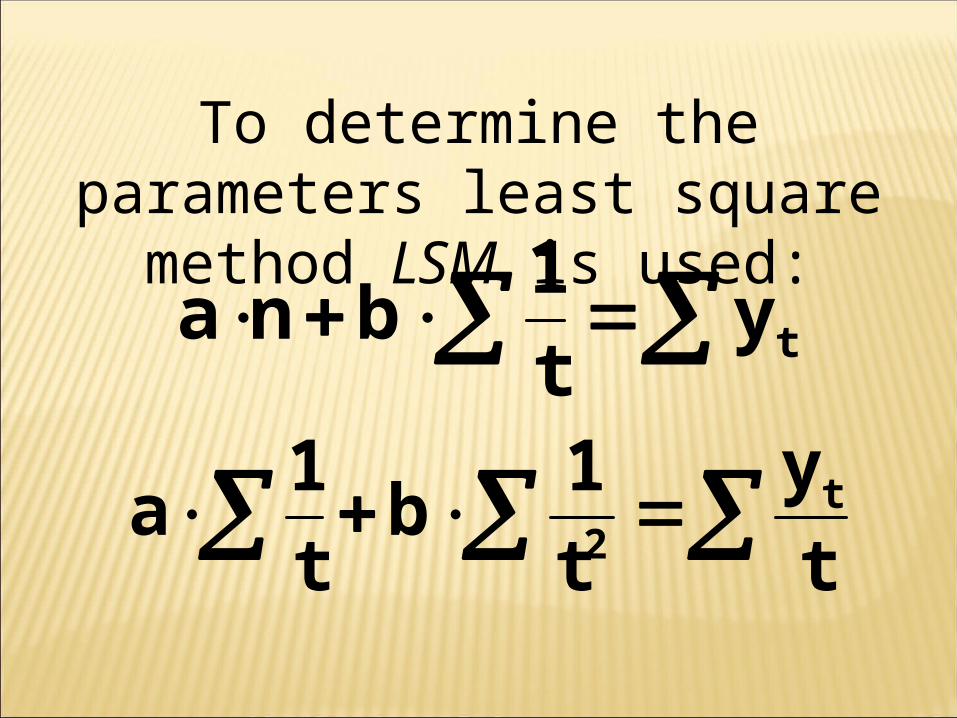

To determine the parameters least square method LSM is used:

tyt

1bna

t

y

t

1b

t

1a t

2

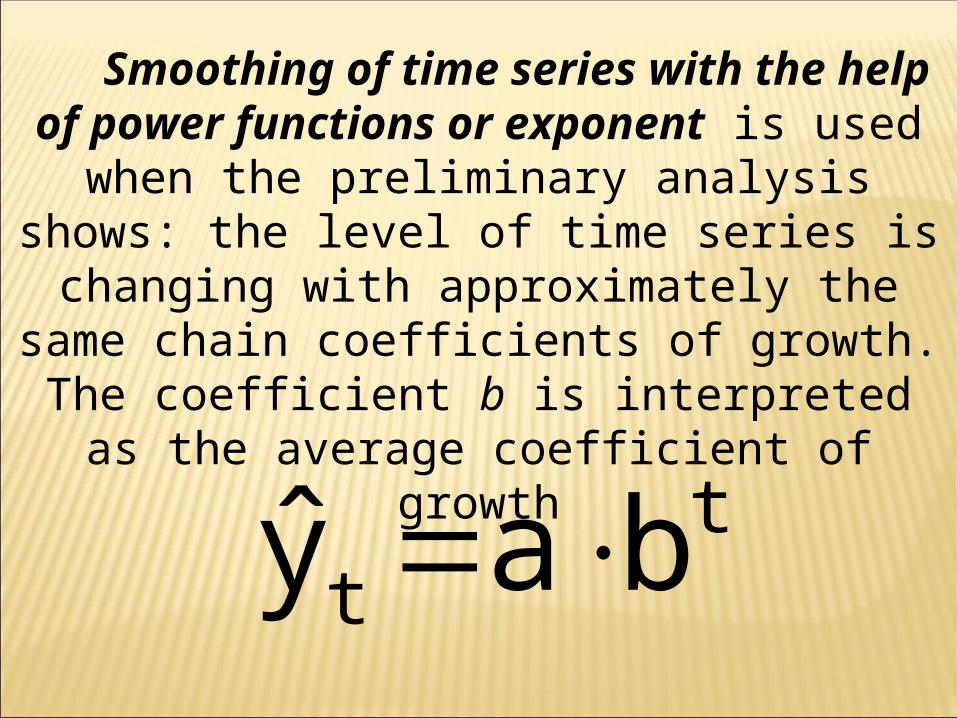

Smoothing of time series with the help of power functions or exponent is used when the

preliminary analysis shows: the level of time series is changing with approximately the same chain

coefficients of growth. The coefficient b is interpreted as the average coefficient of growth

tty a b

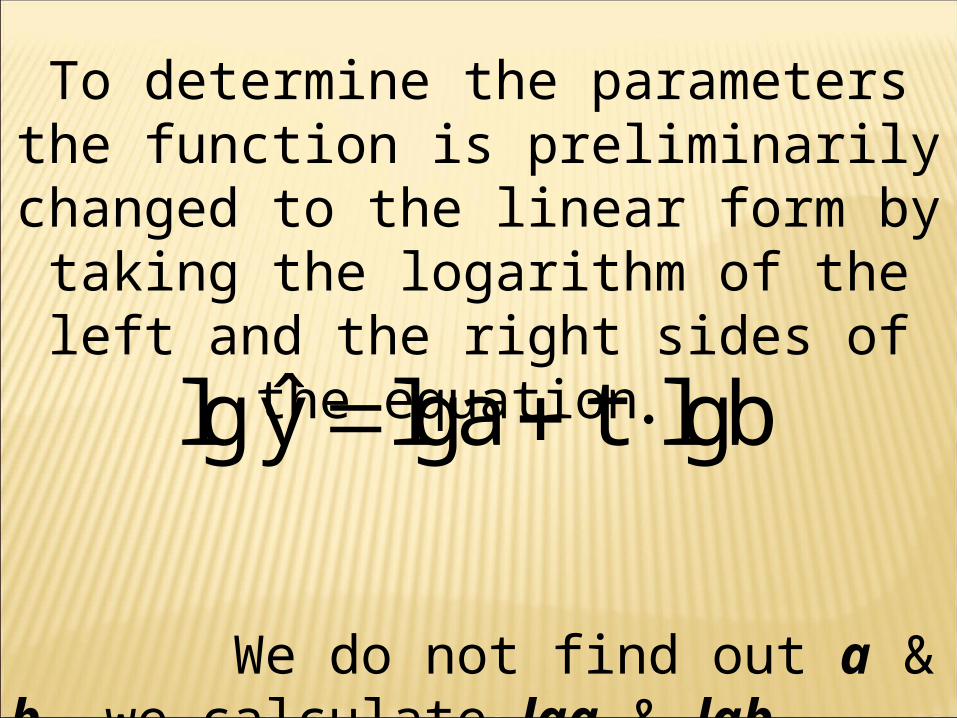

To determine the parameters the function is preliminarily changed to the linear form by taking the logarithm of the left and the right

sides of the equation

We do not find out a & b, we calculate lga & lgb

ˆlg y lga t lgb

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-13

Exponential Smoothing

A weighted moving average Weights decline exponentially

Most recent observation weighted most

Used for smoothing and short term forecasting (often one or two periods into the future)

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-14

Exponential Smoothing

The weight (smoothing coefficient) is Subjectively chosen Range from 0 to 1 Smaller gives more smoothing, larger

gives less smoothing

The weight is: Close to 0 for smoothing out unwanted cyclical

and irregular components Close to 1 for forecasting

(continued)

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-15

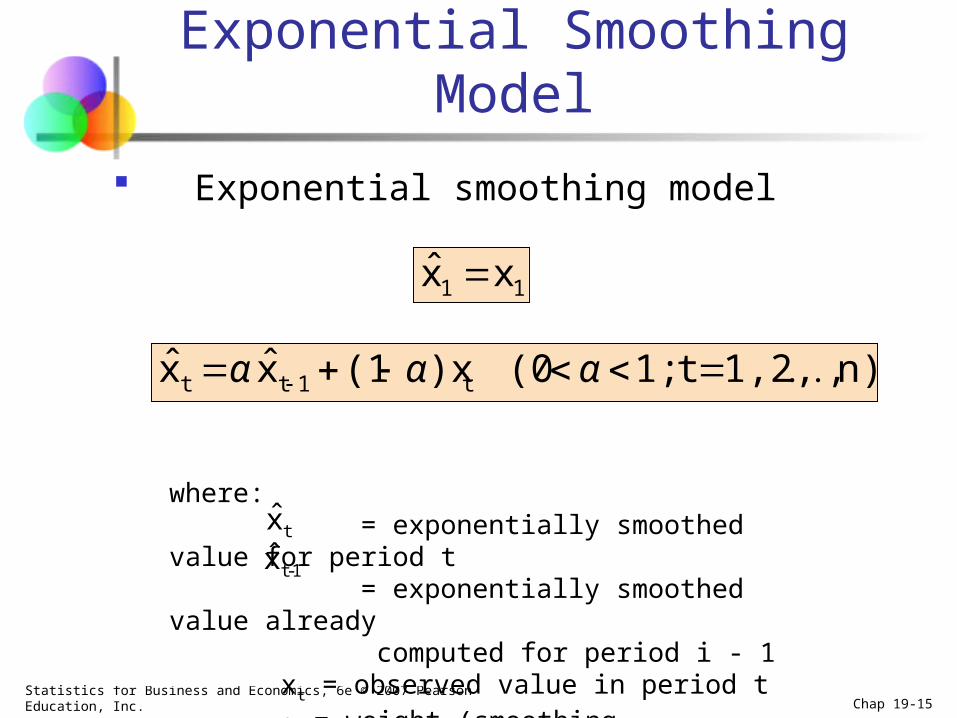

Exponential Smoothing Model

Exponential smoothing model

where: = exponentially smoothed value for period t = exponentially smoothed value already

computed for period i - 1 xt = observed value in period t = weight (smoothing coefficient), 0 < < 1

11 xx ˆ

n),1,2,t1;(0)x(1xx t1tt ααα ˆˆ

tx

1-tx

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-16

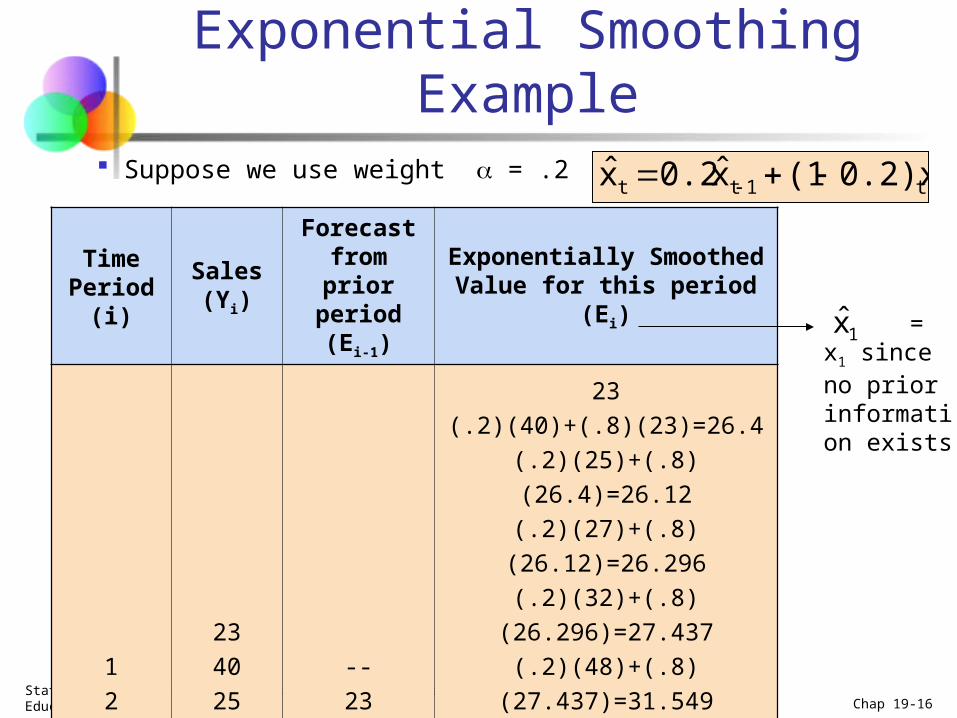

Exponential Smoothing Example Suppose we use weight = .2

Time Period

(i)

Sales(Yi)

Forecast from prior

period (Ei-1)

Exponentially Smoothed Value for this period (Ei)

1

2

3

4

5

6

7

8

9

10

etc.

23

40

25

27

32

48

33

37

37

50

etc.

--

23

26.4

26.12

26.296

27.437

31.549

31.840

32.872

33.697

etc.

23

(.2)(40)+(.8)(23)=26.4

(.2)(25)+(.8)(26.4)=26.12

(.2)(27)+(.8)(26.12)=26.296

(.2)(32)+(.8)(26.296)=27.437

(.2)(48)+(.8)(27.437)=31.549

(.2)(48)+(.8)(31.549)=31.840

(.2)(33)+(.8)(31.840)=32.872

(.2)(37)+(.8)(32.872)=33.697

(.2)(50)+(.8)(33.697)=36.958

etc.

= x1 since no prior information exists

1x

t1tt 0.2)x(1x0.2x ˆˆ

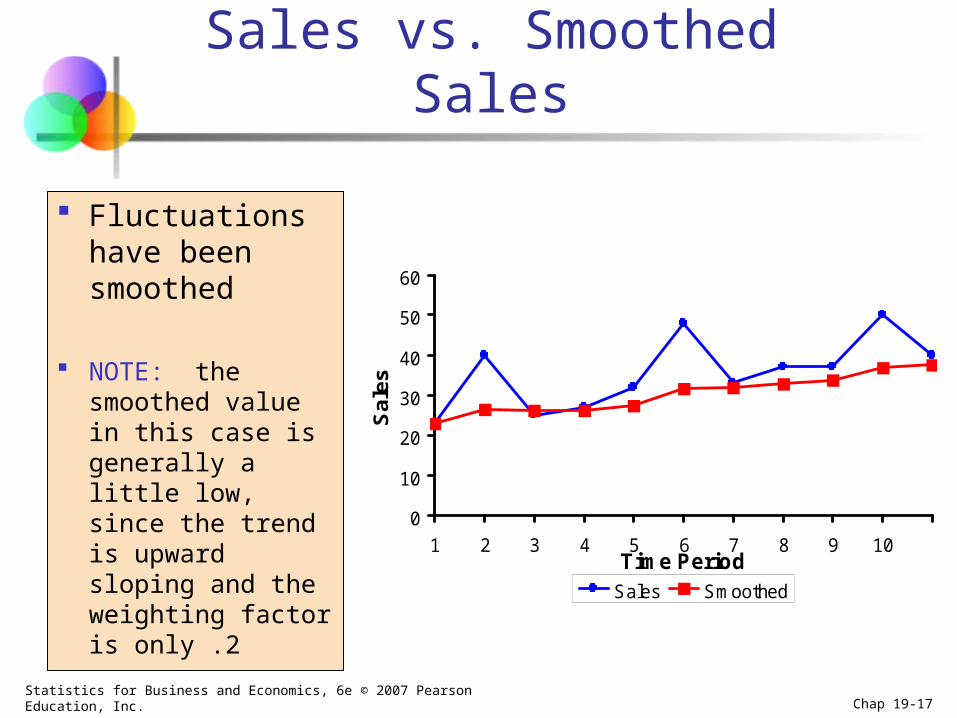

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-17

Sales vs. Smoothed Sales

Fluctuations have been smoothed

NOTE: the smoothed value in this case is generally a little low, since the trend is upward sloping and the weighting factor is only .2

0

10

20

30

40

50

60

1 2 3 4 5 6 7 8 9 10Time Period

Sa

les

Sales Smoothed

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-18

Forecasting Time Period (t + 1)

The smoothed value in the current period (t) is used as the forecast value for next period (t + 1)

At time n, we obtain the forecasts of future values, Xn+h of the series

)1,2,3(hxx nhn ˆˆ

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-19

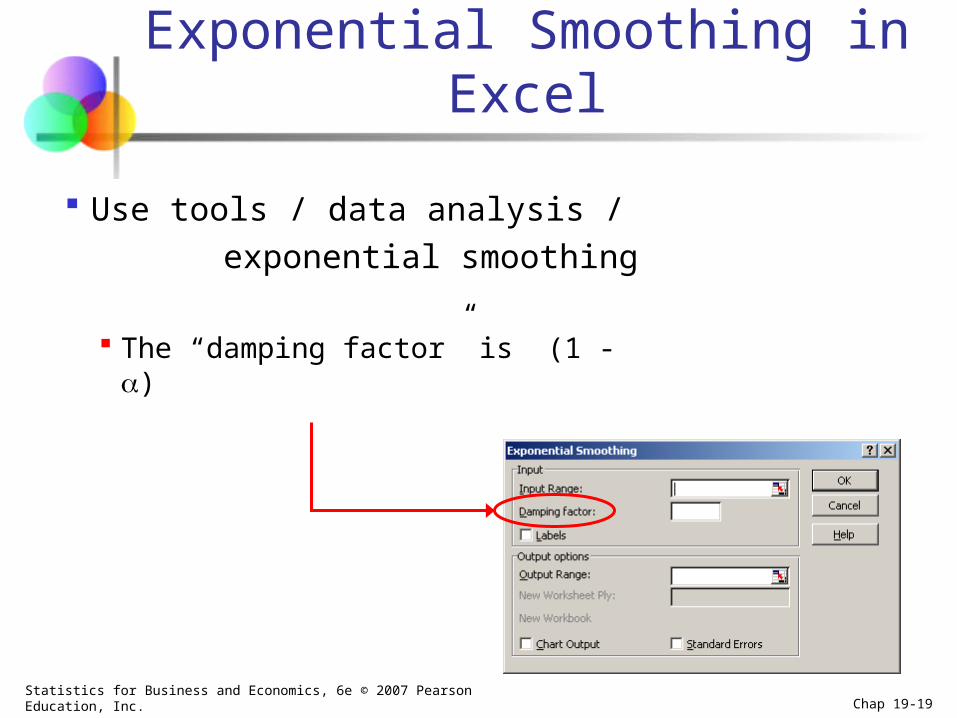

Exponential Smoothing in Excel

Use tools / data analysis /

exponential smoothing

The “damping factor” is (1 - )

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-20

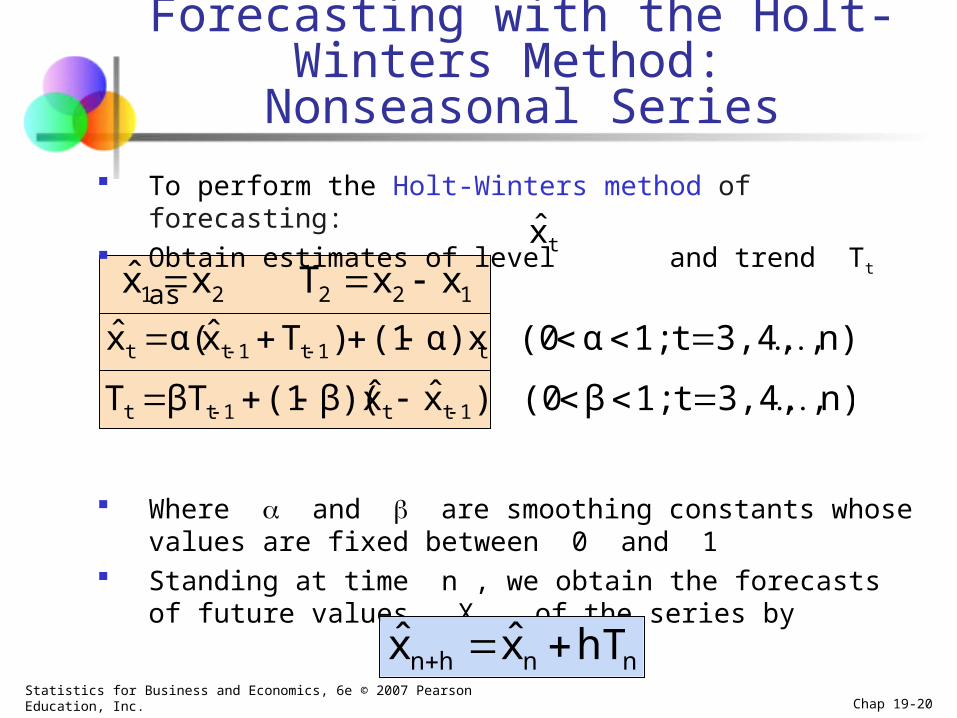

To perform the Holt-Winters method of forecasting: Obtain estimates of level and trend Tt as

Where and are smoothing constants whose values are fixed between 0 and 1

Standing at time n , we obtain the forecasts of future values, Xn+h of the series by

Forecasting with the Holt-Winters Method: Nonseasonal Series

tx

12221 xxTxx ˆ

n),3,4,t1;α(0α)x(1)Txα(x t1t1tt ˆˆ

nnhn hTxx ˆˆ

n),3,4,t1;β(0)xxβ)((1βTT 1tt1tt ˆˆ

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-21

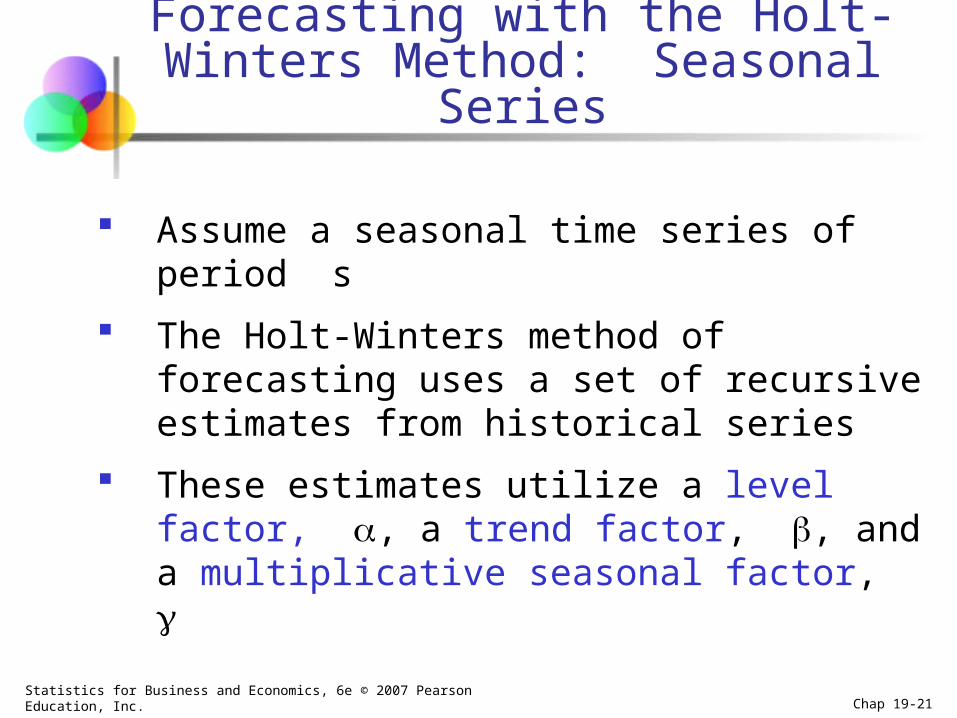

Assume a seasonal time series of period s

The Holt-Winters method of forecasting uses a set of recursive estimates from historical series

These estimates utilize a level factor, , a trend factor, , and a multiplicative seasonal factor,

Forecasting with the Holt-Winters Method: Seasonal Series

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-22

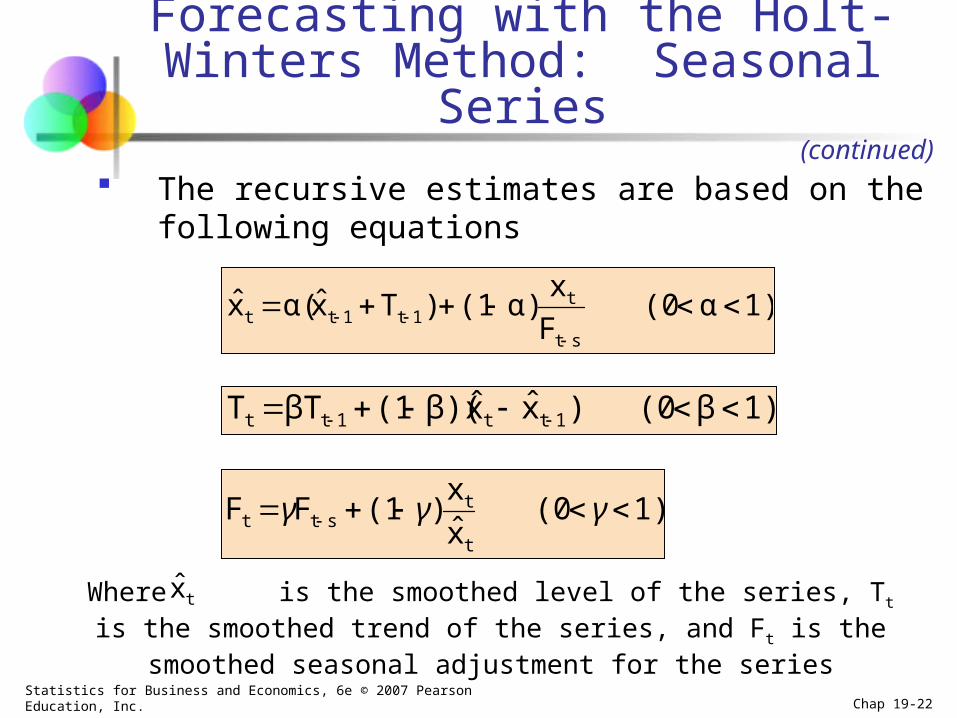

The recursive estimates are based on the following equations

Forecasting with the Holt-Winters Method: Seasonal Series

1)α(0F

xα)(1)Txα(x

st

t1t1tt

ˆˆ

1)(0x

x)(1FF

t

tstt γγγ

ˆ

1)β(0)xxβ)((1βTT 1tt1tt ˆˆ

Where is the smoothed level of the series, Tt is the smoothed trend of the series, and Ft is the smoothed seasonal adjustment for the series

tx

(continued)

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-23

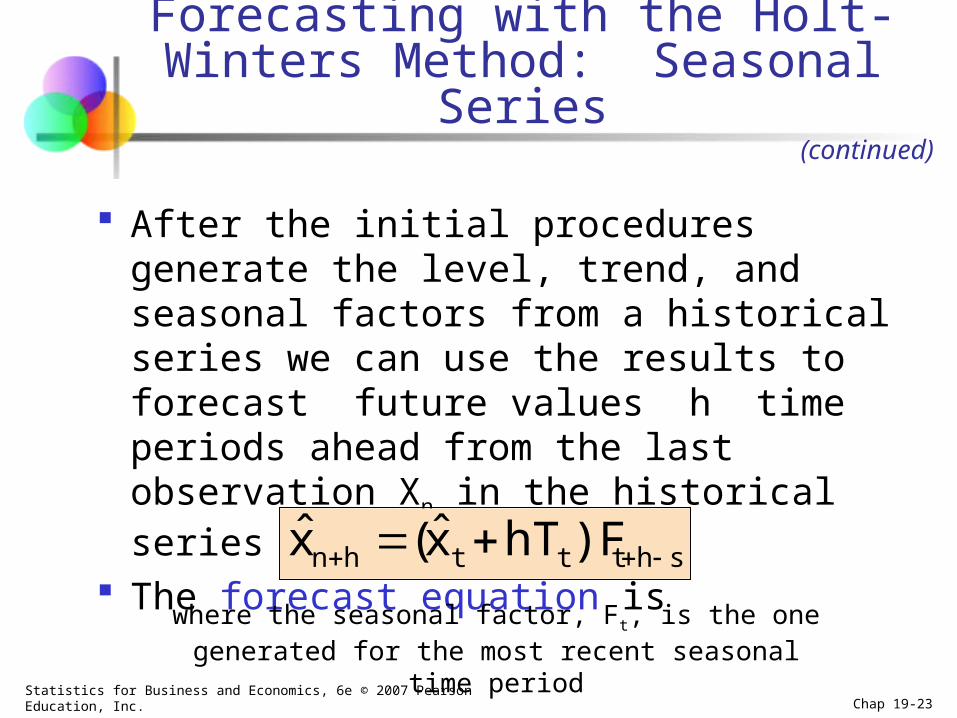

After the initial procedures generate the level, trend, and seasonal factors from a historical series we can use the results to forecast future values h time periods ahead from the last observation Xn in the historical series

The forecast equation is

shttthn )FhTx(x ˆˆ

where the seasonal factor, Ft, is the one generated for the most recent seasonal time period

Forecasting with the Holt-Winters Method: Seasonal Series

(continued)

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-24

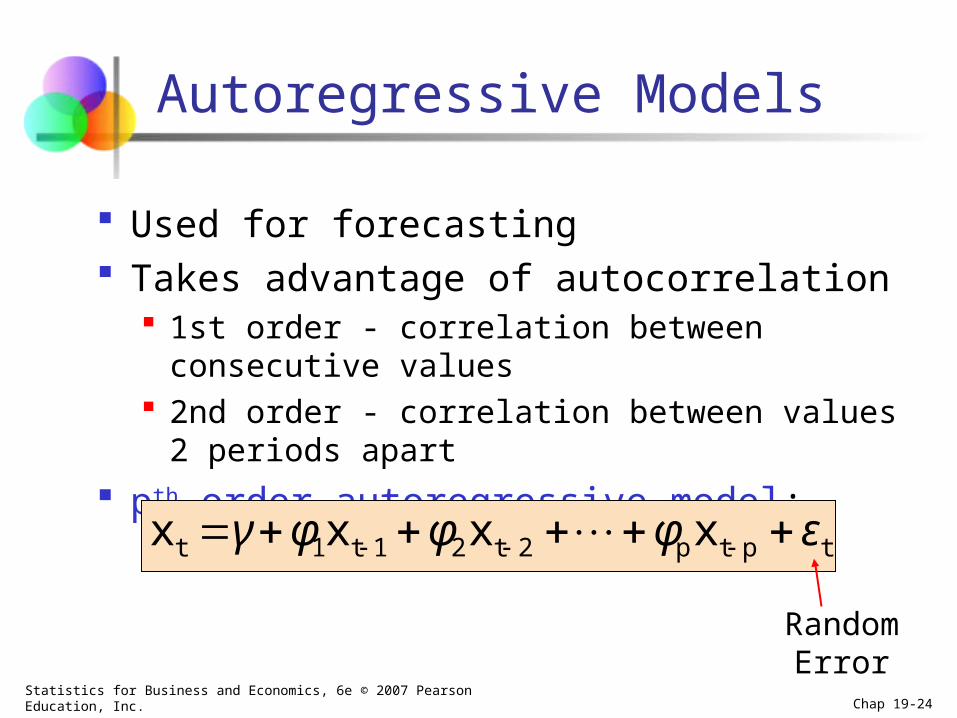

Autoregressive Models

Used for forecasting Takes advantage of autocorrelation

1st order - correlation between consecutive values 2nd order - correlation between values 2 periods

apart

pth order autoregressive model:

Random Error

tptp2t21t1t xxxx εφφφγ

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-25

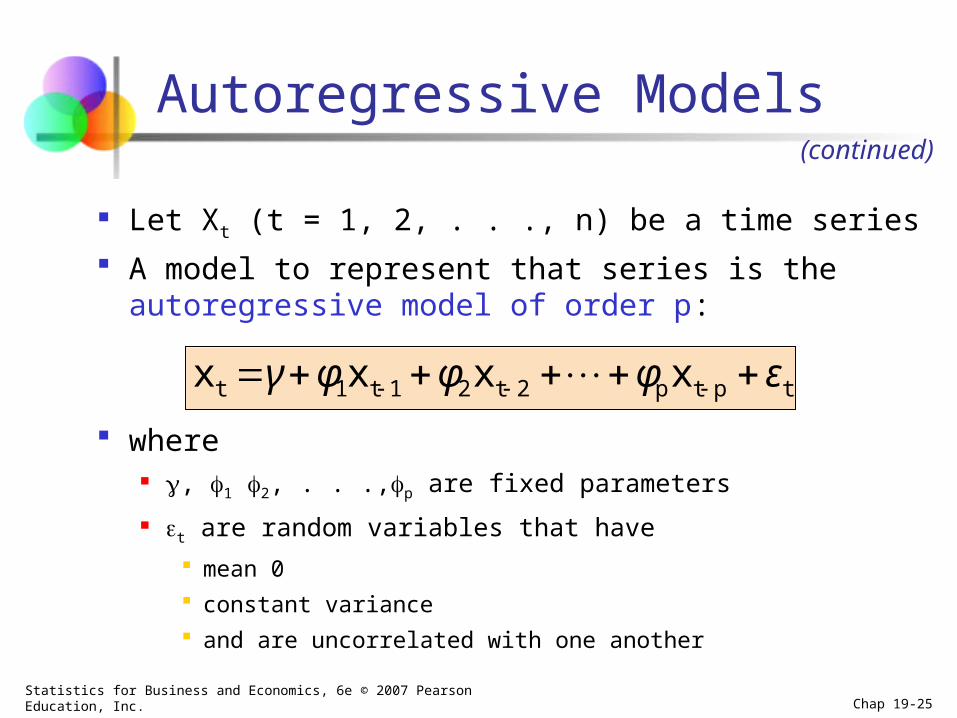

Autoregressive Models

Let Xt (t = 1, 2, . . ., n) be a time series

A model to represent that series is the autoregressive model of order p:

where , 1 2, . . .,p are fixed parameters

t are random variables that have

mean 0

constant variance

and are uncorrelated with one another

tptp2t21t1t xxxx εφφφγ

(continued)

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-26

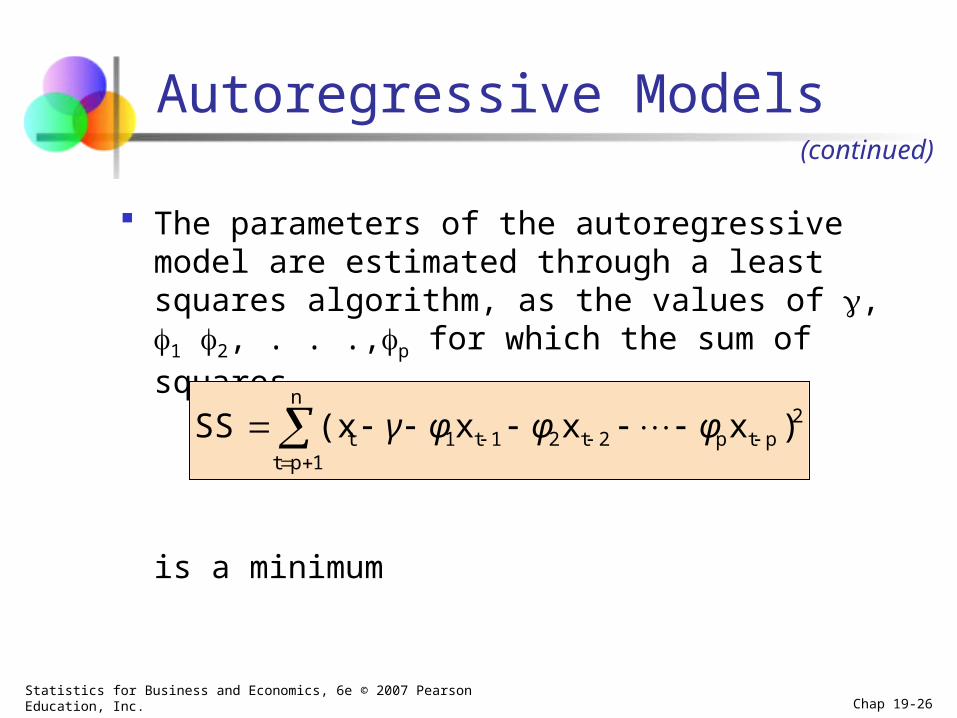

Autoregressive Models

The parameters of the autoregressive model are estimated through a least squares algorithm, as the values of , 1 2, . . .,p for which the sum of squares

is a minimum

2ptp2t21t1

n

1ptt )xxx(xSS

φφφγ

(continued)

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-27

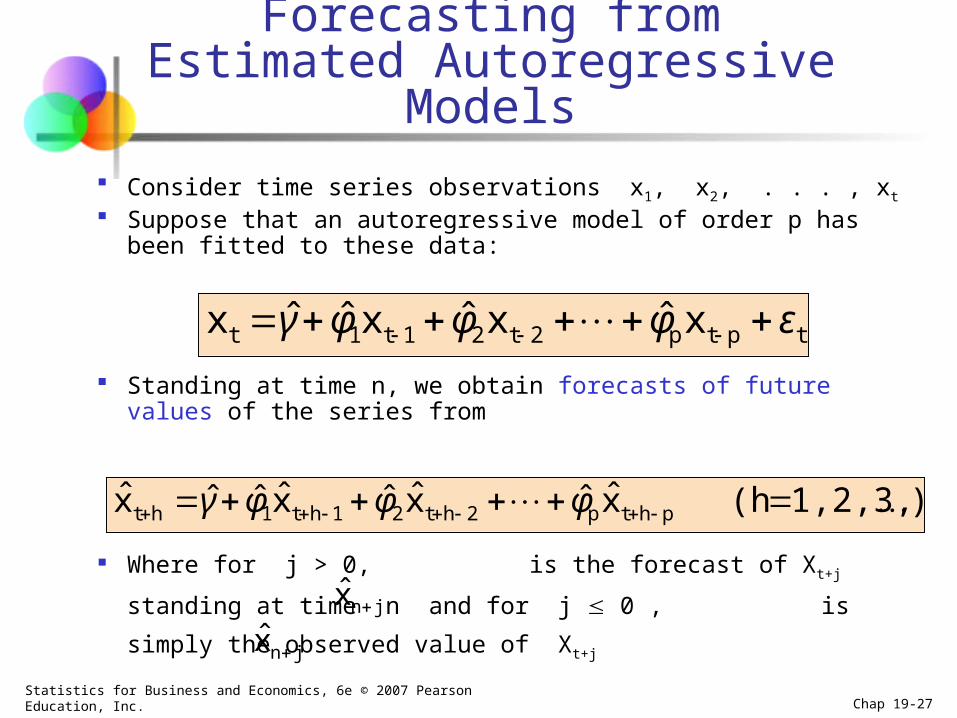

Forecasting from Estimated Autoregressive Models

Consider time series observations x1, x2, . . . , xt Suppose that an autoregressive model of order p has been fitted to

these data:

Standing at time n, we obtain forecasts of future values of the series from

Where for j > 0, is the forecast of Xt+j standing at time n and

for j 0 , is simply the observed value of Xt+j

tptp2t21t1t xxxx εφφφγ ˆˆˆˆ

)1,2,3,(hxxxx phtp2ht21ht1ht ˆˆˆˆˆˆˆˆ φφφγ

jnx ˆ

jnx ˆ

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-28

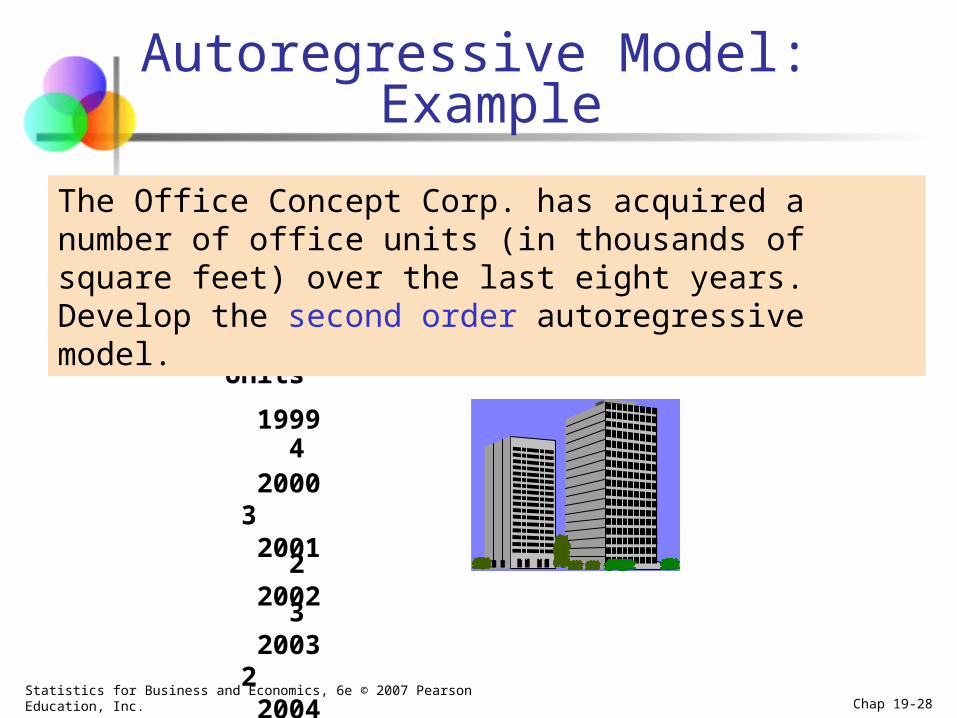

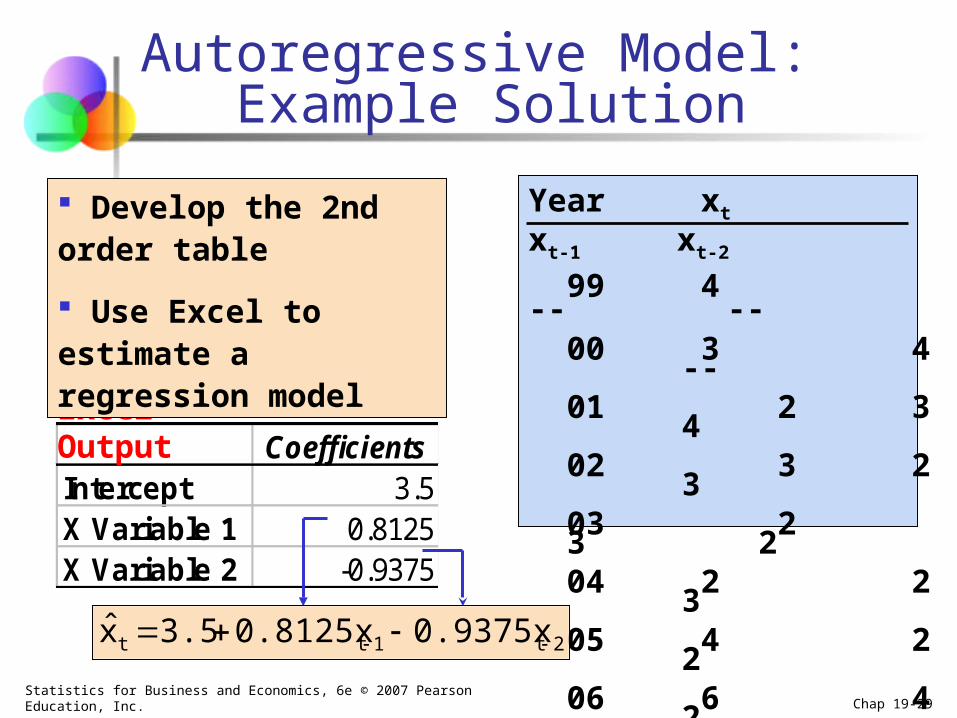

Autoregressive Model: Example

Year Units

1999 4 2000 3 2001 2 2002 3 2003 2 2004 2 2005 4 2006 6

The Office Concept Corp. has acquired a number of office units (in thousands of square feet) over the last eight years. Develop the second order autoregressive model.

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-29

Autoregressive Model: Example Solution

Year xt xt-1 xt-2

99 4 -- -- 00 3 4 -- 01 2 3 4 02 3 2 3 03 2 3 2 04 2 2 3 05 4 2 2 06 6 4 2

CoefficientsIntercept 3.5X Variable 1 0.8125X Variable 2 -0.9375

Excel Output

Develop the 2nd order table

Use Excel to estimate a regression model

2t1tt 0.9375x0.8125x3.5x ˆ

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-30

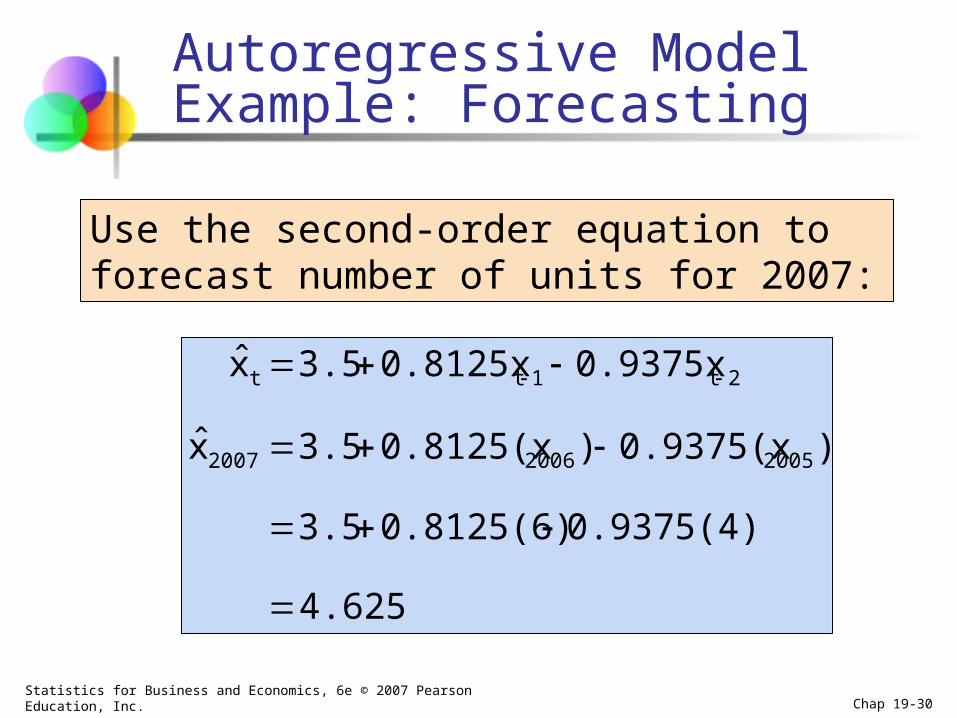

Autoregressive Model Example: Forecasting

Use the second-order equation to forecast number of units for 2007:

4.625

0.9375(4)0.8125(6)3.5

)0.9375(x)0.8125(x3.5x

0.9375x0.8125x3.5x

200520062007

2t1tt

ˆ

ˆ

Statistics for Business and Economics, 6e © 2007 Pearson Education, Inc. Chap 19-31

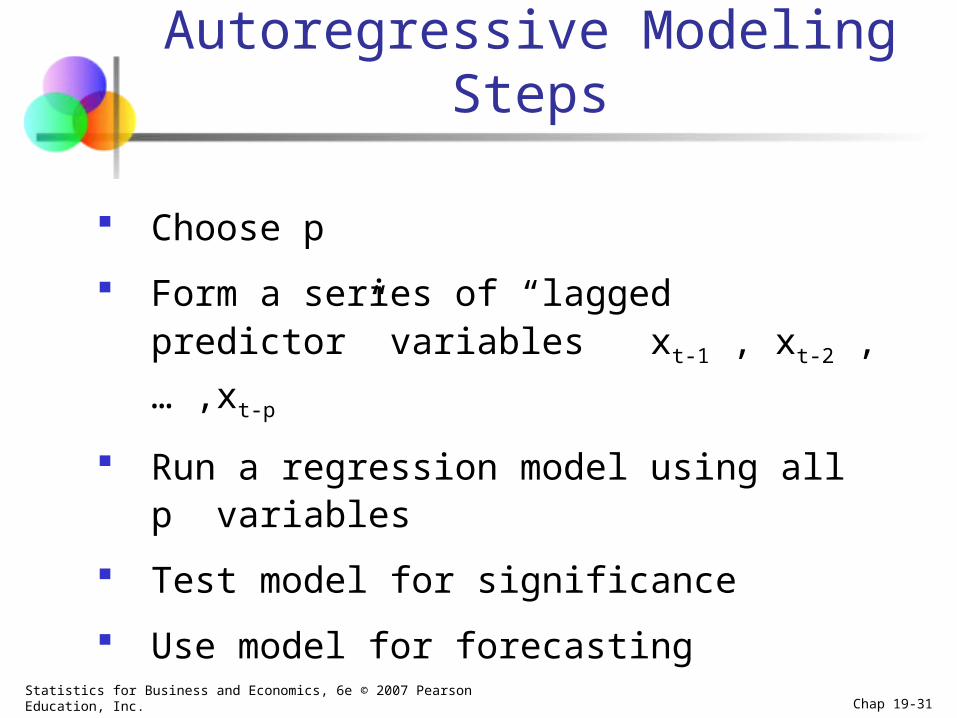

Autoregressive Modeling Steps

Choose p

Form a series of “lagged predictor” variables xt-1 , xt-2 , … ,xt-p

Run a regression model using all p variables

Test model for significance

Use model for forecasting

Merci beaucoup!