The World Economic Outlook

63

Copyright © 2003 Global Insight, Inc. The World Economic Outlook: What Have We Learned in the Last 40 Years and Where Do We Go From Here? Nariman Behravesh Chief Global Economist World Economic Outlook Conference October 21-23, 2003

Transcript of The World Economic Outlook

Copyright © 2003 Global Insight, Inc.

The World Economic Outlook:What Have We Learned in the Last 40 Years

andWhere Do We Go From Here?

Nariman BehraveshChief Global Economist

World Economic Outlook Conference

October 21-23, 2003

Copyright © 2003 Global Insight, Inc.

Welcome!World Economic Outlook Conference 2003

Copyright © 2003 Global Insight, Inc. 310/2003

Outline of Presentation

Global Insight’s short- and medium-term outlook

Four event-filled decades

What have we learned?

Where do we go from here?Looking beyond the horizonA few (of many) plausible scenarios

Copyright © 2003 Global Insight, Inc.

Short- and Medium-TermOutlook

Copyright © 2003 Global Insight, Inc. 510/2003

Overview

The world economy's performance during its current cycle has been a huge disappointment

This year's global growth will enter record books as by far the weakest second-year performance of all post-WWII cyclical recoveries

Key Characteristics of the recovery since the end of the 90s boomSub-par, stop-and-go growth Excessive dependence on the U.S. economyAbsence of pent-up consumer demandPersistent output gap and deflationary pressuresA faltering from the middle of last year that badly scared global capital markets

Nevertheless, all evidence point to a strong U.S. economic rebound being already underway – also in non-Japan Asia

The U.S. rebound should lift the rest of the world, but growth will remain lopsided for some time

Copyright © 2003 Global Insight, Inc. 610/2003

A Global Cyclical Rebound Is Under Way

OECD Leading Indicators(Annualized 6-month rate of change)

-8

-4

0

4

8

12

2000 2001 2002 2003

OECD Total Eurozone Nafta Japan

Copyright © 2003 Global Insight, Inc. 710/2003

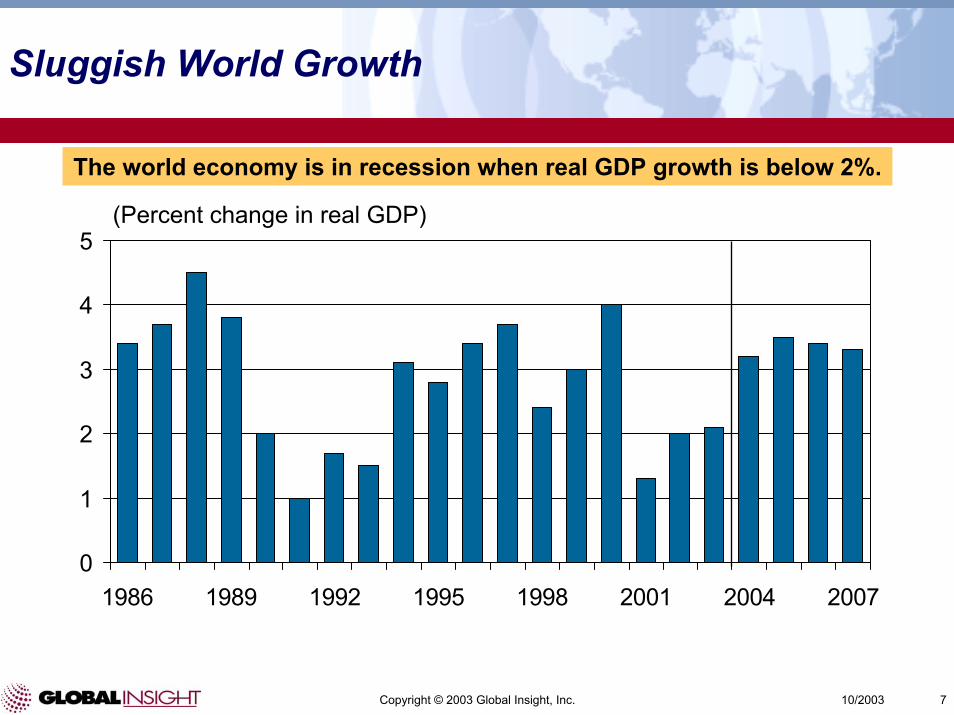

Sluggish World Growth

The world economy is in recession when real GDP growth is below 2%.

0

1

2

3

4

5

1986 1989 1992 1995 1998 2001 2004 2007

(Percent change in real GDP)

Copyright © 2003 Global Insight, Inc. 810/2003

Emerging Markets Achieve the Fastest Growth

-2-10123456

NAFTA OtherAmericas

WesternEurope

EmergingEurope

Japan Other Asia

2001 2002 2003 2004 2005

(Percent change, real GDP)

Copyright © 2003 Global Insight, Inc. 910/2003

Fiscal and Monetary Policy Will Boost Growth Later this Year

Fiscal Balance

(Percentage of GDP, 2003)

Net Cumulative Cut in Policy Rates Since January 2001

(Basis points)

Australia -1.0 150

United Kingdom -2.7 250

Canada 0.5 275

Japan -6.8 25

Sweden 1.3 125

Switzerland -2.2 325

United States -4.0 550

Eurozone -2.5 275

Copyright © 2003 Global Insight, Inc. 1010/2003

Crude Oil Prices Will Retreat

(WTI price, dollars per barrel)

10

15

20

25

30

35

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Copyright © 2003 Global Insight, Inc. 1110/2003

U.S. – Poised to Rebound

Positive Trends

Fiscal and monetary policy still very simulativeInterest rates at 41-year lowUnemployment rate not high relative to past recessionsAfter-tax income growth is strongThe housing sector is holding upCorporate cash flow and balance sheets have strengthenedInventories are lowProductivity growth is strongThe U.S. dollar has fallen

Negative Trends

Job losses continueU.S. corporations are still risk averseCapacity utilization is lowDebt levels are highState and local government are retrenchingNo help from the rest of the world

Copyright © 2003 Global Insight, Inc. 1210/2003

The U.S. Expansion Will Strengthen

-2

0

2

4

6

8

1998 1999 2000 2001 2002 2003 2004 2005 20062

3

4

5

6

7

Real GDP Growth Unemployment Rate

(Percent change, annual rate) (Percent)

Copyright © 2003 Global Insight, Inc. 1310/2003

Price and Wage Inflation Will Stay Mild

(Year-over-year percent change)

-3-2-1012345

1998 1999 2000 2001 2002 2003 2004 2005 2006

CPI Producer Prices Employment Cost Index

Copyright © 2003 Global Insight, Inc. 1410/2003

Federal Reserve Policy Will Be Accommodating: Key Interest Rates

0

2

4

6

8

10

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Federal Funds 10-Year Treasury Yield Mortgage Rate

(Percent)

Copyright © 2003 Global Insight, Inc. 1510/2003

Household Debt Service Burdens Are Manageable

4

5

6

7

8

9

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007

Mortgage Debt Service Other Debt Service

(Percent of disposable income)

Copyright © 2003 Global Insight, Inc. 1610/2003

Ratio of Household Debt to Disposable Income

708090

100110120130140

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

U.S. Japan Germany UK

(Ratio)

Source: OECD

Copyright © 2003 Global Insight, Inc. 1710/2003

House Price Inflation, 1995-2002

Source: National Statistics

Nominal Real Ireland 219 152 Britain 125 89 Netherlands 121 83 Spain 95 58 Sweden 68 56 Australia 83 53 Belgium 57 39 France 45 31 U.S. 51 27 Eurozone 35 19 Italy 29 8 Canada 18 2 Germany -5 -13 Japan -20 -19

Copyright © 2003 Global Insight, Inc. 1810/2003

Employment Will Begin to Recover This Fall

The U.S. lost 2.8 million jobs from February 2001 to August 2003.

-3

-2

-1

0

1

2

3

1998 1999 2000 2001 2002 2003 2004 2005 2006

(Percent change, annual rate)

Copyright © 2003 Global Insight, Inc. 1910/2003

Corporate Profits Are Rebounding

-8-4048

121620

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Before-tax Profits with IVA & CCA GDP

(Percent change, NIPA basis)

Copyright © 2003 Global Insight, Inc. 2010/2003

An Uneven Recovery in Business Investment

-20-10

010203040

Structures Computers Software Communic.Equipment

OtherEquipment

2000 2001 2002 2003 2004

(Percent change, 1996 dollars)

Copyright © 2003 Global Insight, Inc. 2110/2003

U.S. Federal Budget Deficit and Debt

-6.0

-4.5

-3.0

-1.5

0.0

1.5

3.0

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 201320

26

32

38

44

50

56

U.S. Federal Deficit to GDP (LS) U.S. Federal Debt to GDP (RS)

(Ratio) (Ratio)

Copyright © 2003 Global Insight, Inc. 2210/2003

Europe – Still a Drag on Global Growth

Positive Trends

Oil prices and inflation are lowerExpected global recovery will help exportsStock markets have reboundedConfidence is recovering

Negative Trends

Double-dip in GermanyFiscal and monetary policies are still too tightThe euro has appreciatedUnemployment rates are high and risingLittle progress has been made on structural reforms

Copyright © 2003 Global Insight, Inc. 2310/2003

Forecasts for Europe

0.0

0.5

1.0

1.5

2.0

2.5

3.0

France Germany Italy Spain U.K.

2001 2002 2003 2004 2005

(Percent change in real GDP)

Copyright © 2003 Global Insight, Inc. 2410/2003

The Dollar-Euro Exchange Rate

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

(Dollars per euro)

Copyright © 2003 Global Insight, Inc. 2510/2003

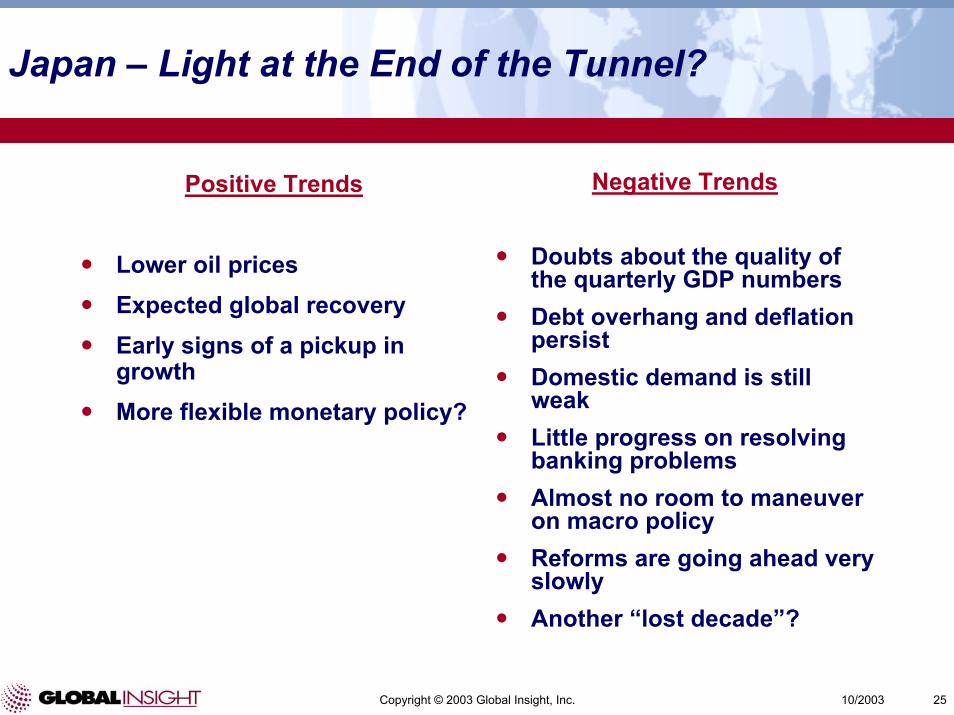

Japan – Light at the End of the Tunnel?

Positive Trends

Lower oil pricesExpected global recoveryEarly signs of a pickup in growthMore flexible monetary policy?

Negative Trends

Doubts about the quality of the quarterly GDP numbersDebt overhang and deflation persistDomestic demand is still weakLittle progress on resolving banking problemsAlmost no room to maneuver on macro policyReforms are going ahead very slowlyAnother “lost decade”?

Copyright © 2003 Global Insight, Inc. 2610/2003

Japan – Another Lost Decade?

-2-101234567

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

(Percent change in real GDP)

Copyright © 2003 Global Insight, Inc. 2710/2003

The Dollar-Yen Exchange Rate

85

95

105

115

125

135

145

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

(Yen per U.S. dollar)

Copyright © 2003 Global Insight, Inc. 2810/2003

Asia: A Bright Spot

Negative Trends

Liquidity explosion could lead to overheating – repeat of 1997?

Attempts to keep exchange rates from appreciating could backfire

Positive Trends

SARS risk has diminished

Exports are booming

High-tech growth is strong

Macro policies have been very accommodative

Chinese deflation is ending

Excess capacity is less of an issue

Copyright © 2003 Global Insight, Inc. 2910/2003

Real GDP Growth in Asian Economies

-4

-2

0

2

4

6

8

China S. Korea India Australia Taiwan

2001 2002 2003 2004 2005

(Percent change)

Copyright © 2003 Global Insight, Inc. 3010/2003

Real GDP Growth in Asian Economies

-4

-2

0

2

4

6

Hong Kong Indonesia Singapore Malaysia Philippines

2001 2002 2003 2004 2005

(Percent change)

Copyright © 2003 Global Insight, Inc. 3110/2003

Latin America: Still Not Out of Danger

Positive Trends

Competitive currencies (except Mexico)

Improving global conditions will help

Argentina is finally growing (from a very low base)

Risk premiums are the lowest in two years

Negative Trends

Brazil’s economy is faltering

Colombia is struggling

Venezuela is in a freefall

High unemployment rates throughout the region

Continued political uncertainty

Copyright © 2003 Global Insight, Inc. 3210/2003

Latin America at a Glance

-12-9-6-3036

LatinAmerica

Argentina Brazil Mexico Venezuela

2001 2002 2003 2004 2005

(Percent change in real GDP)

Copyright © 2003 Global Insight, Inc. 3310/2003

Emerging Europe Is Attracting Investment

Despite weak export markets, economic growth is picking up in Central Europe, Russia, and the Ukraine.

Eastern European countries are attracting foreign investment in anticipation of accession to the European Union.

Falling trade barriers, low costs, and privatization will spark industrial development in Romania, Bulgaria, and Croatia.

Azerbaijan, Kazakhstan, and Turkmenistan will achieve high growth rates as a result of oil and gas development.

Russia, the Ukraine, and Kazakhstan are introducing market reforms, but corruption and weak financial systems will impede non-energy investment.

Copyright © 2003 Global Insight, Inc. 3410/2003

Middle East and Africa Face Several Obstacles

The Iraq war, the Israeli-Palestinian conflict, and fears of terrorism have undermined tourism and investment.

Near-term strength in oil export revenues will support public spending in the Middle East and North Africa.

Iraq’s long-term economic outlook is bright but risky; the country is rich in natural resources.

Oil production—potential to reach 5 mmbd in 5 yearsAgriculture—fertile land, water from Tigris & EuphratesTourism—Shiite holy cities of Najaf and Karbala

Capital flight, the AIDS epidemic, and political instability hinder growth in Sub-Saharan Africa. Demand for Africa’s metals and agricultural exports remains weak.

Copyright © 2003 Global Insight, Inc. 3510/2003

Other Emerging Markets Are Growing

01234567

Eastern Europe Former SovietUnion

Middle East Africa

2001 2002 2003 2004 2005

(Percent change, real GDP)

Copyright © 2003 Global Insight, Inc. 3610/2003

The Biggest Economic Risk In the Next Few Years –A Rapidly Falling U.S. Dollar

Continued lopsided world growth means that, for the U.S. currentaccount deficit to be bought under control, the dollar has to fall further – a lot further

The U.S. CAD is currently twice as big as in the 1980s and dollar has fallen by half as much – and growth in Europe and Japan is much slower

As long as the Asian central banks keep their currencies from appreciating by much, the brunt of the adjustment will be on thefloating currencies, notably the euro

A euro at $1.40 or $1.50 in the next three years is not far-fetched

Without the appropriate policy response to such a shock, the Eurozone will be condemned to sluggish growth for many more years

Depending on how quickly the dollar falls, the impact on U.S. long-term interest rates could be problematic

Copyright © 2003 Global Insight, Inc. 3710/2003

World Growth Will Remain Lopsided

0123456

World NAFTA OtherAmericas

WesternEurope

Japan Other Asia

1992-2002 2002-2012 2012-2022

(Percent change)

Copyright © 2003 Global Insight, Inc. 3810/2003

A Gaping Imbalance

-800

-600

-400

-200

0

200

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010-8

-6

-4

-2

0

2

Current Account Deficit Deficit as % of GDP

(Billions of dollars) (Percent of GDP)

Copyright © 2003 Global Insight, Inc. 3910/2003

The Dollar is Overvalued

0.80.91.01.11.21.31.41.5

1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006

Developing Countries Industrial Countries

(Real trade-weighted dollar index, 1996=1.0)

Copyright © 2003 Global Insight, Inc.

Four Event-Filled Decades

Copyright © 2003 Global Insight, Inc. 4110/2003

1960s

“Supply-side” tax cuts

Booming economy

Guns and butter

Rising inflation

Balance of payments crises

Japan rising

Brazil booms

Copyright © 2003 Global Insight, Inc. 4210/2003

1970s

Collapse of Bretton Woods System

Oil and other supply shocks

Stagflation

Wage and price controls

Petro-recycling

Volcker shock

Early attempts by Europe to limit currency movement (snake-in-the-tunnel and snake-in-the-lake)

Copyright © 2003 Global Insight, Inc. 4310/2003

1980s

Debt crisis – Latin America’s lost decade

Reagonomics and Thatchernomics

High real interest rates

Twin deficits but no hard landing of the dollar

Oil price collapse

Stock market crash

Dollar rise and fall

Japanese bubble

German locomotive

Rise of Asia

Fall of the Berlin Wall and the collapse of Communism

Banking crises (including S&L crisis in the U.S.)

Copyright © 2003 Global Insight, Inc. 4410/2003

1990s

German unification

Gulf-war recession

Job-less recovery

Japanese bubble bursts – Japanese policy mistakes and “lost decade”

ERM crises – Maastricht Treaty

Emerging markets crises – Asia loses some of its luster

Tech boom and productivity “miracle”

U.S. becomes only locomotive of growth

EMU

Most fixed exchange rate regimes are abandoned

Inflation drifts down

Copyright © 2003 Global Insight, Inc. 4510/2003

2000s

Tech bust

Mild downturn followed by lackluster recovery

Wealth destruction does not lead to depression

Synchronized global downturn – the macro consequences of globalization?

Deflation spreads

9/11 and wars in Afghanistan and Iraq

Corporate scandals

U.S. still the growth locomotive – CAD balloons

Double-dips in Europe due to tight policies and structural rigidities

Rise of China

Backlash against globalization

Copyright © 2003 Global Insight, Inc. 4610/2003

Forty-Year Trends

Government’s share of output rose

Growth volatility fell

Globalization accelerated (once again)

Cyclical synchronization increased

Inflation rose then fell

Role of capital markets increased

After steady gains from ’45 to ’95, vis-à-vis the U.S., Japan and Europe lost ground after ’95

Since 1970, manufacturing output in industrial economies doubledwhile employment fell 25%

Asia’s share of world GDP rose

Copyright © 2003 Global Insight, Inc. 4710/2003

Global Per Capital Real GDP Growth

The post-Bretton Woods era:

globalization gathers steam

Industrial countries' "Golden Age"

Two World Wars and the intervening

period: de-globalization

The gold standard triumphant

0.0

1.0

2.0

3.0

4.0

1900-13 1913-50 1950-73 1973-2000

(Average annual percentage change)

Source: Angus Maddison, Monitoring the World Economy 1820-1992.

Copyright © 2003 Global Insight, Inc. 4810/2003

World: Real GDP Growth

0

1

2

3

4

5

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 2020 2024World

(Percent change, annual rate)

Copyright © 2003 Global Insight, Inc. 4910/2003

Real GDP Growth in the U.S.

-4

-2

0

2

4

6

8

1974 1978 1982 1986 1990 1994 1998 2002 2006 2010

GDP

(Percent change)

Copyright © 2003 Global Insight, Inc. 5010/2003

Real Inflation in the U.S.

0

3

6

9

12

15

1974 1978 1982 1986 1990 1994 1998 2002 2006 2010

CPI

(Percent change)

Copyright © 2003 Global Insight, Inc. 5110/2003

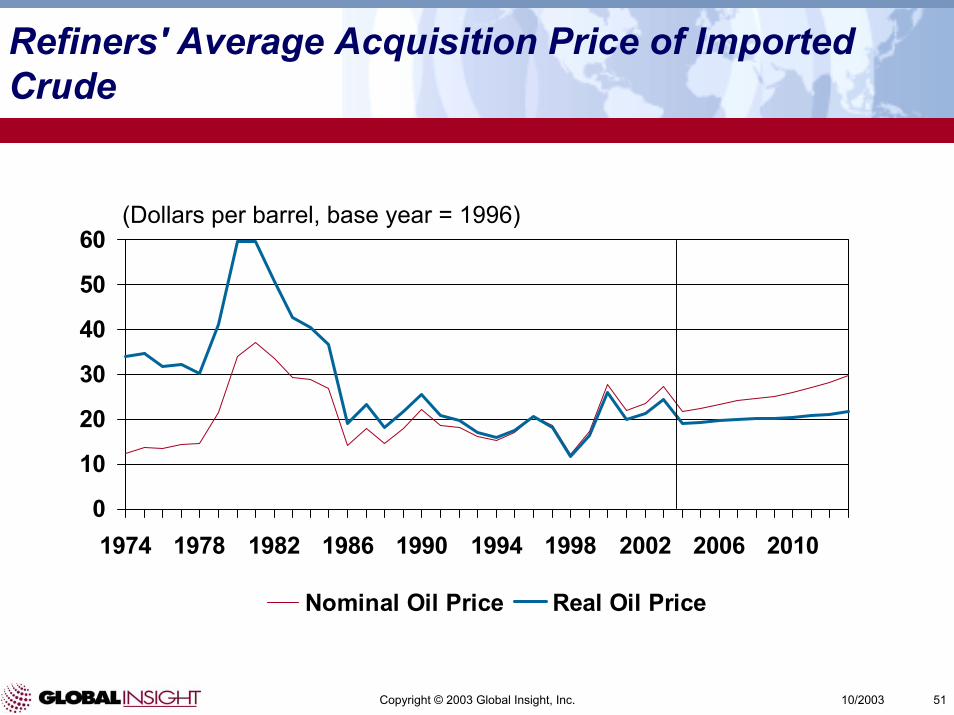

Refiners' Average Acquisition Price of Imported Crude

0

10

20

30

40

50

60

1974 1978 1982 1986 1990 1994 1998 2002 2006 2010

Nominal Oil Price Real Oil Price

(Dollars per barrel, base year = 1996)

Copyright © 2003 Global Insight, Inc. 5210/2003

Economic Volatility

0.75

1.00

1.25

1.50

1.75

2.00

2.25

1961-1970 1971-1980 1981-1990 1991-2000

Japan United Kingdom Euro area* United States

(Standard deviation of output gaps, percent)

* Simple average of Austria, France, Germany, Italy, and Spain.Source: OECD Working Paper no. 315

Copyright © 2003 Global Insight, Inc. 5310/2003

Ratio of Exports to GDP for the World

15

20

25

30

35

40

1979 1983 1987 1991 1995 1999 2003 2007 2011 2015 2019 2023

World Exports

(Percent of GDP)

Copyright © 2003 Global Insight, Inc. 5410/2003

Current Account Deficit

(Percent of GDP)

-6

-4

-2

0

2

4

6

1960 1970 1980 1990 2000 2010 2020

U.S. Europe Japan Asia

Copyright © 2003 Global Insight, Inc. 5510/2003

Comparing the 1980s and the 2000s

World imbalances are bigger

Capital markets are bigger

Inflation is lower

World growth is more fragile – Germany and Japan cannot help

More countries have to be involved in the adjustment process

Little appetite for coordination

Copyright © 2003 Global Insight, Inc. 5610/2003

Net Foreign Debt

Norway (1977)U.S.(1894) U.S. (2003)

Mexico (1980)

Argentina (1980)

Brazil (1980)

U.S. (2007)

New Zealand (1999)

Ireland (1983)Australia (1996)

Finland (1994)Sweden (1994)

Canada (1980)

0

20

40

60

80

100

1999 2004 2009 2014 2019 2024 2029 2034

(Percent of GDP)

Source: IMF; Obstfeld & Rogoff

Copyright © 2003 Global Insight, Inc.

What Have We Learned?

Copyright © 2003 Global Insight, Inc. 5810/2003

Economic Lessons: A Partial List

Markets work

While markets fail, governments fail even more spectacularly – or how governments have turned market dramas into crises

Globalization works (S. Korea, W. Germany, and Taiwan vs. N. Korea, E. Germany, and China)

The business cycle is not dead – but it may have become more benign (and more Austrian)

Boosting domestic demand is more urgent in a synchronized downturn

The combination of aging populations, structural rigidities and poor macro policies in the Eurozone and Japan is a serious threat to the global economy

The U.S. is not like Japan in the 1990s and Japan is not like the U.S. in the 1930s

Copyright © 2003 Global Insight, Inc. 5910/2003

Economic Lessons: A Partial List (Continued)

Deflation may not be a big threat if the banking system is soundand policy makers are vigilant

Bursting asset bubbles don’t necessarily lead to deep recessionsor depressions

No escaping from the trilemma Fixed exchange rates, independent monetary policy, and free flowing capital: a country can have any two but not all three

Fixed exchange rates lead to more pro-cyclical policies than flexible exchange rates – but neither is a substitute for sound macro policies

Labor market flexibility can play an important role in the ability of an economy to respond to positive and negative shocks

Copyright © 2003 Global Insight, Inc. 6010/2003

Forecasting Lessons

Economic forecasters are more like seismologists than weather forecasters

Don’t assume policy makers act rationally

The more frequent the pronouncements about the death of the business cycle, the closer we are to the next downturn

The more frequent the denials about a devaluation, the closer we are to a currency crisis

Avoid the trend line – 1980 headline: $85 a bbl in ’85!

Low probability events can no longer be ignored

Scenarios, scenarios, and more scenarios

Copyright © 2003 Global Insight, Inc.

Where Do We Go From Here?

Copyright © 2003 Global Insight, Inc. 6210/2003

Looking Beyond the Horizon

Will the U.S. dollar crash?

Are we seeing the birth of a new Bretton Woods system?

Are we headed for another emerging market debt crisis?

Is the European Union about to become more rigid or flexible?

Will looming pension “bombs” force Europe and Japan to “privatize” their pension system?

Is “offshore outsourcing” (especially in services and high-tech) the next wave of globalization?

How much (if at all) will the failure at Cancun and terrorism slow globalization?

Are we “one recession away from deflation?”

Copyright © 2003 Global Insight, Inc. 6310/2003

Looking Beyond the Horizon (Continued)

Asia: A million millionaires and a billion boomers?

Will Asia become home to the world’s deepest financial markets?

How sustainable is Chinese growth?

How will China shift the terms of trade?

Will India follow in China’s footsteps or leap-frog manufacturing-led development?