World Economic Outlook, April 2002 -- Chapter 1

60

T here are now increasing signs that the global slowdown, which began in the middle of 2000, has bottomed out. As had been suggested in the October 2001 World Economic Outlook, the events of September 11 had a short-run impact on activity, but—in contrast to the fears that some ex- pressed—have not prevented a recovery in the first half of 2002. 1 Leading indicators have turned up (Figure 1.2); consumer and business confidence have strengthened; and industrial production—including the information technol- ogy (IT) sector—is leveling off. This has been most apparent in the United States and, increas- ingly, the euro area; in Japan, while activity may now be bottoming out, the outlook remains very difficult with few signs of a sustained recovery in domestic demand. In emerging markets, there are signs of recovery in a number of Asian emerging markets—particularly Korea—aided by the nascent improvement in the IT sector, al- though not as yet in most Latin American countries. Growing expectations of recovery have been particularly apparent in financial markets, which recovered strongly after the events of September 11 (Figure 1.3). Equity markets have picked up sharply across the globe, although flattening off in the first quarter of 2002; yield curves have steepened; and risk aversion and spreads—in both mature and emerging markets—have de- clined. Partly reflecting market expectations of the relative pace of recovery, the U.S. dollar has strengthened further, accompanied by a moder- ate weakening of the euro, while the yen has fallen to three-year lows. In emerging markets, contagion from the crisis in Argentina has to date been limited, reflecting the fact that the cri- sis was well anticipated, and that gross interna- tional capital flows were already at low levels (Figure 1.4), as well as a number of technical factors, including the relatively low leverage in the system. 2 Spreads for most emerging market debt have declined sharply since early Novem- ber, and financing conditions for emerging mar- ket borrowers have improved more rapidly than 1 CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES Over recent months, there have been increasing signs that the global slowdown has bottomed out, most clearly in the United States and to a lesser extent in Europe and some countries in Asia. While serious concerns remain in a number of countries, notably Japan and—for different reasons—Argentina, most indicators suggest recovery is now under way, broadly along the lines described in the Interim World Economic Outlook issued last December (Figure 1.1). With confidence stabilizing, uncertainties easing, and emerging market financing conditions improv- ing more quickly than was then anticipated, the risks to the outlook have become more balanced, although the recent volatility in the oil market is a significant concern. While the stance of poli- cies should remain relatively supportive for the time being, there is now—except in Japan—little case for additional easing, and in countries where the recovery is most advanced, attention will need to turn toward reversing earlier monetary policy easing. It will be important to take full ad- vantage of the recovery to reduce remaining economic vulnerabilities, and to pursue a collabora- tive approach designed to promote an orderly resolution of global imbalances—which remain a serious risk to economic stability—over the medium term. 1 See Box 1.1, World Economic Outlook, October 2001. 2 See “Contagion and Its Causes,” Chapter I, Appendix I, World Economic Outlook, December 2001.

Transcript of World Economic Outlook, April 2002 -- Chapter 1

There are now increasing signs that theglobal slowdown, which began in themiddle of 2000, has bottomed out. Ashad been suggested in the October

2001 World Economic Outlook, the events ofSeptember 11 had a short-run impact on activity,but—in contrast to the fears that some ex-pressed—have not prevented a recovery in thefirst half of 2002.1 Leading indicators haveturned up (Figure 1.2); consumer and businessconfidence have strengthened; and industrialproduction—including the information technol-ogy (IT) sector—is leveling off. This has beenmost apparent in the United States and, increas-ingly, the euro area; in Japan, while activity maynow be bottoming out, the outlook remains verydifficult with few signs of a sustained recovery indomestic demand. In emerging markets, thereare signs of recovery in a number of Asianemerging markets—particularly Korea—aided bythe nascent improvement in the IT sector, al-though not as yet in most Latin Americancountries.

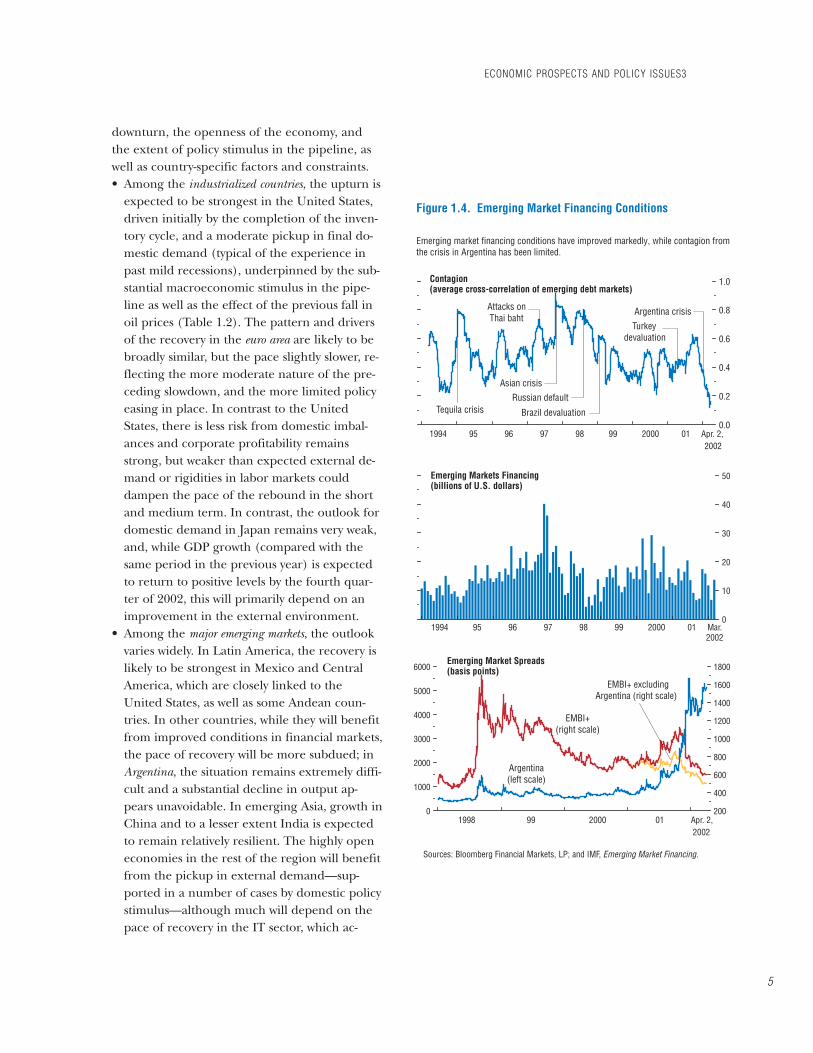

Growing expectations of recovery have beenparticularly apparent in financial markets, whichrecovered strongly after the events of September11 (Figure 1.3). Equity markets have picked upsharply across the globe, although flattening offin the first quarter of 2002; yield curves havesteepened; and risk aversion and spreads—inboth mature and emerging markets—have de-clined. Partly reflecting market expectations ofthe relative pace of recovery, the U.S. dollar hasstrengthened further, accompanied by a moder-ate weakening of the euro, while the yen hasfallen to three-year lows. In emerging markets,contagion from the crisis in Argentina has todate been limited, reflecting the fact that the cri-sis was well anticipated, and that gross interna-tional capital flows were already at low levels(Figure 1.4), as well as a number of technicalfactors, including the relatively low leverage inthe system.2 Spreads for most emerging marketdebt have declined sharply since early Novem-ber, and financing conditions for emerging mar-ket borrowers have improved more rapidly than

1

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

Over recent months, there have been increasing signs that the global slowdown has bottomedout, most clearly in the United States and to a lesser extent in Europe and some countries inAsia. While serious concerns remain in a number of countries, notably Japan and—for differentreasons—Argentina, most indicators suggest recovery is now under way, broadly along the linesdescribed in the Interim World Economic Outlook issued last December (Figure 1.1). Withconfidence stabilizing, uncertainties easing, and emerging market financing conditions improv-ing more quickly than was then anticipated, the risks to the outlook have become more balanced,although the recent volatility in the oil market is a significant concern. While the stance of poli-cies should remain relatively supportive for the time being, there is now—except in Japan—littlecase for additional easing, and in countries where the recovery is most advanced, attention willneed to turn toward reversing earlier monetary policy easing. It will be important to take full ad-vantage of the recovery to reduce remaining economic vulnerabilities, and to pursue a collabora-tive approach designed to promote an orderly resolution of global imbalances—which remain aserious risk to economic stability—over the medium term.

1See Box 1.1, World Economic Outlook, October 2001.2See “Contagion and Its Causes,” Chapter I, Appendix I, World Economic Outlook, December 2001.

earlier anticipated, with high-quality borrowersreaccessing markets toward the end of 2001, fol-lowed increasingly thereafter by non-investment-grade issuers.

The recovery is being underpinned by a num-ber of factors. First, and most important, macro-economic policies in advanced countries havebeen substantially eased over the past year, no-tably in the United States, and—particularly sinceinterest rate cuts were anticipated by markets,and therefore built into asset prices in advance—should now be providing increasing support todemand. Policies in a number of emerging mar-ket countries, especially in Asia, have also beeneased, although in most others the scope hasbeen relatively limited. Second, the completionof ongoing inventory cycles, which appears mostadvanced in the United States but is also underway in Europe, will support economic activity.Finally, activity has also been supported by thedecline in oil prices since late 2000. Since lateFebruary, however, oil prices have risen signifi-cantly, reflecting concerns about possible militaryintervention in the Middle East, the deterioratingsecurity situation in Israel and the West Bank andGaza, as well as the strengthening global recov-ery. At the time the World Economic Outlook wentto press, oil prices had returned to broadly theirmid-2001 level, still well below their fall 2000peak, and prices in futures markets were onlymoderately higher than the oil price assumptionon which the forecasts in this World EconomicOutlook are based (Table 1.1). Nonetheless, thepast fall in oil prices will provide less support torecovery than earlier expected, while the poten-tial for further volatility has become a significantrisk to the outlook.

Inflationary pressures have continued to ease,reflecting weaker global activity. In advancedcountries, inflation is projected to fall to 1.3 per-cent in 2002, the lowest level on record, and—while important wage negotiations in the euroarea are still in train—wage increases have ingeneral been moderate. Indeed, if sustained, in-flation this low could be a concern, since itcould limit the ability of central banks to engi-neer negative real interest rates when neces-

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

2

1970 75 80 85 90 95 2000 05-6

-3

0

3

6

9

1970 75 80 85 90 95 2000 050

5

10

15

20

World Real Long-Term Interest Rate (percent)

1970 75 80 85 90 95 2000 050

100

200

300

400

1970 75 80 85 90 95 2000 050

2

4

6

8

Figure 1.1. Global Indicators

Developing countries (consumer prices,

median)

World Real GDP

Trend,1970–2001

While global growth is expected to increase moderately in 2002, this disguises a sharper pickup in activity during the year (see text). Inflation remains subdued.

2

1

1

3

Inflation

Advanced economies

(consumer prices)

Real Commodity Prices(1990 = 100)

Non-oil commodity

prices

Oil prices

(Annual percent change unless otherwise noted)

2

3

Shaded areas indicate IMF staff projections. Aggregates are computed on the basis of purchasing-power-parity weights unless otherwise indicated. Average growth rates for individual countries, aggregated using purchasing- power-parity weights; these shift over time in favor of faster growing countries, giving the line an upward trend. GDP-weighted average of the 10-year (or nearest maturity) government bond yields less inflation rates for the United States, Japan, Germany, France, Italy, the United Kingdom, and Canada. Excluding Italy prior to 1972.

1970 75 80 85 90 95 2000 05-1

0

1

2

3

4

5

6 World Real Per Capita GDP

Trend,1970–20012

1970 75 80 85 90 95 2000 05-4

0

4

8

12

16

Trend,1970–20012

World Trade Volume (goods and services)

sary.3 Deflation remains a central issue in Japan,where prices appear set to fall for the fourth suc-cessive year. Elsewhere, however, the forces re-straining prices are likely to ease as recovery getsunder way, as excess capacity declines and com-modity prices—especially oil—pickup (seeAppendix 1.1). In emerging and developingcountries, inflation is also projected to fall, al-though it remains of concern in the Common-wealth of Independent States—especially the lessadvanced reformers—some European Union(EU) accession countries, and a few countries inLatin America and Africa.

Assuming that the recovery is sustained, thisglobal slowdown—while seriously affecting manycountries and regions—will have proved to bemore moderate than most previous downturns,and would probably not qualify as a full-fledgedglobal recession (Box 1.1). Global GDP growthand global per capita GDP growth (the bestmeasure of the impact on global welfare) wouldremain above the troughs experienced in thethree major global recessions of the past 30 years(although below the level experienced duringthe Asian crisis in 1997–98). This partly reflectslong-run structural trends, including the ten-dency toward milder recessions in industrialcountries (see Chapter III), and the growingrole of China and India, which—being relativelyclosed—are less affected by global downturns(although these factors are at least partly offsetby countervailing forces, including increasing fi-nancial and corporate sector linkages). However,it clearly also reflects the generally prompt andaggressive response of policymakers to the slow-down, and—linked to that—the progress thathas been made in reducing vulnerabilities andstrengthening economic fundamentals in ad-vanced and developing countries.4 As experi-ence during the past year has shown, managingthe downturn has been considerably easier incountries with the scope for policy flexibility,

ECONOMIC PROSPECTS AND POLICY ISSUES

3

Figure 1.2. Emerging Signs of Recovery

Sources: Haver Analytic. Business confidence for the United States, the National Association of Purchasing Managers; for the euro area, the European Commission; and for Japan, Bank of Japan. Consumer confidence for the United States, the Conference Board; for the euro area, the European Commission; and for Japan, the Economic Planning Agency. Leading indicator for the United States, the Economic Cycle Research Institute; for Japan, the Cabinet Office; for Canada, Statistics Canada; and for Germany, France, Italy, and United Kingdom, OECD Main Economic Indicators. Australia, Canada, Denmark, Euro area, Japan, New Zealand, Norway, Sweden, Switzerland, United Kingdom, and United States. Argentina, Brazil, Chile, China, Colombia, Czech Republic, Hong Kong SAR, Hungary, India, Indonesia, Israel, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Russia, Singapore, South Africa, Taiwan Province of China, Thailand, Turkey, and Venezuela. Seasonally adjusted.

Signs of recovery are suggested by recent improvements in confidence and other leading indicators, particularly in the United States and Europe.

-20

-10

0

10

20

30

40

-10

-5

0

5

10

15 Industrial Production(percent change from a year earlier)

World

Global Trade(percent change from a year earlier)

World

Industrialcountries

Emerging markets

Industrialcountries

Emerging markets

1999 2000 01 Jan. 2002

20

40

60

80

100

120

140

160

-14

-12

-10

-8

-6

-4

-2

0

2

4

32

36

40

44

48

52

56

60

-50

-40

-30

-20

-10

0

10

20Business ConfidenceEuro area

(right scale)

Consumer Confidence

1999 2000 01 Mar. 2002

United States(left scale)

Japan(right scale)

1999 2000 01 Mar. 2002

United States(left scale)

Euro area(right scale)

Japan(left scale)

1999 2000 01 Jan. 2002

1

1

22

1

2

92

96

100

104

108

112

116

90

95

100

105

110

115

120

125 Leading Indicators(January 1999 = 100)

Japan

Leading Indicators(January 1999 = 100)

1999 2000 01 Feb. 2002

United States

Canada

Germany

1999 2000 01 Feb. 2002

FranceItaly

UnitedKingdom

3

3

3See Box 2.2, “Can Inflation Be Too Low?”4See “Statement of the Managing Director on the

Situation of the World Economy and the Fund Response,”IMF News Brief No. 01/98, October 5, 2001.

while others have been forced to follow moreprocyclical policies, deepening the downturnand likely also slowing the ensuing recovery.

The main elements of the IMF’s global fore-cast published in the Interim World EconomicOutlook last December—which projected an up-turn in the first half of 2002—have remainedbroadly unchanged. Global growth in 2002 isprojected at 2.8 percent, somewhat higher thanexpected in December (Table 1.1). Growth inthe United States—and countries with close eco-nomic links—has been revised significantly up-ward, as the pace of recovery has exceeded ex-pectations. Elsewhere, adjustments to the forecastare more modest—with the exception of theWestern Hemisphere, mainly due to the crisis inArgentina; the Middle East, due to lower than ex-pected growth in oil exporters; and theCommonwealth of Independent States, reflectingthe improved outlook for Russia. It is importantto recognize that, while global GDP growth for2002 is projected to be only slightly higher thanin 2001, this disguises a substantial pickup duringthe year. As can be seen from Figure 1.5, globalgrowth is projected to rise from 1!/2 percent inthe last quarter of 2001 to nearly 4 percent bythe end of 2002. As the full impact of this is felt,global growth is expected to rise to 4.0 percent in2003, significantly above the long-run trend.

The global downturn has been more synchro-nized than the one in the early 1990s (although,as discussed in Chapter III, the degree of syn-chronicity has been broadly typical from alonger-term historical perspective). This has pri-marily been due to the commonality of shocks—notably, the bursting of the IT bubble, the run-up in oil prices in 2000, and the tightening ofmonetary policy from mid-1999 to end-2000—but has also reflected the increasing linkagesacross countries, particularly in the corporateand financial sphere. This naturally gives rise tothe question whether the upturn in activity willbe as synchronized. The IMF staff’s projectionssuggest that the recovery in most regions will be-gin in the first half of 2002, with the UnitedStates in the lead, but the nature and pace willvary depending on the depth of the preceding

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

4

60

80

100

120

140

160

180

200

220

240

80

100

120

140

160

180

Figure 1.3. Financial Market Optimism

As expectations of a recovery have increased, financial markets have strengthened in almost all countries, accompanied by steepening yield curves and declining risk premiums and spreads.

DJ Euro Stoxx

Wilshire5000

Mature Equity Markets(September 11, 2001 = 100; national currency)

Eastern Europe and Middle East

Asia

2000 2001 Apr. 3, 2002

LatinAmerica

Sources: Bloomberg Financial Markets, LP; State Street Bank; and IMF staff estimates.

Topix

Emerging Equity Markets(September 11, 2001 = 100; U.S. dollars)

0

2

4

6

8

0

2

4

6

8

Euroarea

United States

Short-Term Interest Rates(3-month LIBOR; percent)

2000 2001 Dec. 2002

Japan

Long-Term Interest Rates(10-year government bond; percent)

2000 2001 Apr. 2, 2002

United States

Euro area

Japan

Futures

Futures

2000 2001 Dec. 2002

0

200

400

600

800

1000

-1.0

-0.5

0.0

0.5

1.0 Monthly Risk Appetite Index(past 6 months)

High yield spread

AAA spread

2000 2001 Apr. 2, 2002

BAA spread

Interest Rate Spreads(basis points)

2000 2001 Apr. 2, 2002

downturn, the openness of the economy, andthe extent of policy stimulus in the pipeline, aswell as country-specific factors and constraints.• Among the industrialized countries, the upturn is

expected to be strongest in the United States,driven initially by the completion of the inven-tory cycle, and a moderate pickup in final do-mestic demand (typical of the experience inpast mild recessions), underpinned by the sub-stantial macroeconomic stimulus in the pipe-line as well as the effect of the previous fall inoil prices (Table 1.2). The pattern and driversof the recovery in the euro area are likely to bebroadly similar, but the pace slightly slower, re-flecting the more moderate nature of the pre-ceding slowdown, and the more limited policyeasing in place. In contrast to the UnitedStates, there is less risk from domestic imbal-ances and corporate profitability remainsstrong, but weaker than expected external de-mand or rigidities in labor markets coulddampen the pace of the rebound in the shortand medium term. In contrast, the outlook fordomestic demand in Japan remains very weak,and, while GDP growth (compared with thesame period in the previous year) is expectedto return to positive levels by the fourth quar-ter of 2002, this will primarily depend on animprovement in the external environment.

• Among the major emerging markets, the outlookvaries widely. In Latin America, the recovery islikely to be strongest in Mexico and CentralAmerica, which are closely linked to theUnited States, as well as some Andean coun-tries. In other countries, while they will benefitfrom improved conditions in financial markets,the pace of recovery will be more subdued; inArgentina, the situation remains extremely diffi-cult and a substantial decline in output ap-pears unavoidable. In emerging Asia, growth inChina and to a lesser extent India is expectedto remain relatively resilient. The highly openeconomies in the rest of the region will benefitfrom the pickup in external demand—sup-ported in a number of cases by domestic policystimulus—although much will depend on thepace of recovery in the IT sector, which ac-

ECONOMIC PROSPECTS AND POLICY ISSUES3

5

0

1000

2000

3000

4000

5000

6000

200

400

600

800

1000

1200

1400

1600

1800

0.0

0.2

0.4

0.6

0.8

1.0

1994 95 96 97 98 99 2000 01 Apr. 2, 2002

0

10

20

30

40

50

Emerging market financing conditions have improved markedly, while contagion from the crisis in Argentina has been limited.

Figure 1.4. Emerging Market Financing Conditions

Tequila crisis

Asian crisisRussian default

Turkeydevaluation

Emerging Markets Financing(billions of U.S. dollars)

Contagion(average cross-correlation of emerging debt markets)

1994 95 96 97 98 99 2000 01 Mar. 2002

1998 99 2000 01 Apr. 2, 2002

Emerging Market Spreads(basis points)

Brazil devaluation

Argentina crisis

Sources: Bloomberg Financial Markets, LP; and IMF, Emerging Market Financing.

EMBI+(right scale)

EMBI+ excludingArgentina (right scale)

Argentina(left scale)

Attacks onThai baht

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

6

Table 1.1. Overview of the World Economic Outlook Projections(Annual percent change unless otherwise noted)

Difference from December

Current Projections 2001 Projections1_________________ ________________2000 2001 2002 2003 2001 2002

World output 4.7 2.5 2.8 4.0 0.1 0.4Advanced economies 3.9 1.2 1.7 3.0 0.1 0.8

Major advanced economies 3.5 1.1 1.5 2.8 0.1 0.9United States 4.1 1.2 2.3 3.4 0.2 1.6Japan 2.2 –0.4 –1.0 0.8 — —Germany 3.0 0.6 0.9 2.7 0.1 0.2France 3.6 2.0 1.4 3.0 –0.1 0.1Italy 2.9 1.8 1.4 2.9 — 0.2United Kingdom 3.0 2.2 2.0 2.8 –0.1 0.2Canada 4.4 1.5 2.5 3.6 0.1 1.7

Other advanced economies 5.3 1.6 2.5 3.7 0.1 0.6MemorandumEuropean Union 3.4 1.7 1.5 2.9 — 0.2

Euro area 3.4 1.5 1.4 2.9 — 0.2Newly industrialized Asian economies 8.5 0.8 3.6 5.1 0.4 1.6Developing countries 5.7 4.0 4.3 5.5 –0.1 –0.2

Africa 3.0 3.7 3.4 4.2 0.1 –0.2Developing Asia 6.7 5.6 5.9 6.4 — 0.2

China 8.0 7.3 7.0 7.4 — 0.2India 5.4 4.3 5.5 5.8 –0.1 0.3ASEAN-42 5.1 2.6 3.3 4.1 0.2 0.4

Middle East and Turkey3 5.8 2.1 3.3 4.5 –0.1 –0.7Western Hemisphere 4.0 0.7 0.7 3.7 –0.3 –1.0

Brazil 4.4 1.5 2.5 3.5 –0.3 0.5Countries in transition 6.6 5.0 3.9 4.4 — 0.2

Central and eastern Europe 3.8 3.1 3.0 4.0 0.1 –0.2Commonwealth of Independent

States and Mongolia 8.3 6.2 4.5 4.6 0.1 0.6Russia 9.0 5.0 4.4 4.9 –0.8 0.8Excluding Russia 7.0 8.8 4.7 4.1 1.9 —

MemorandumWorld growth based on market exchange rates 4.0 1.4 1.8 3.2 — 0.6World trade volume (goods and services) 12.4 –0.2 2.5 6.6 –1.2 0.3Imports

Advanced economies 11.6 –1.5 2.1 6.6 –1.2 0.7Developing countries 16.0 2.9 6.4 7.7 –2.0 –0.1Countries in transition 13.2 10.8 8.0 7.7 –0.5 0.2

ExportsAdvanced economies 11.7 –1.3 0.9 6.3 –1.0 0.3Developing countries 15.0 3.0 4.8 7.0 –0.5 0.2Countries in transition 14.6 6.3 5.2 6.1 –1.5 –1.4

Commodity prices (U.S. dollars)Oil4 57.0 –14.0 –5.3 –4.4 — 18.4Nonfuel (average based on world commodity export weights) 1.8 –5.5 –0.1 7.2 — –1.8Consumer pricesAdvanced economies 2.3 2.2 1.3 1.8 –0.1 —Developing countries 6.1 5.7 5.8 5.1 –0.3 0.5Countries in transition 20.2 15.9 10.8 8.7 –0.3 –0.3Six-month London interbank offered rate (LIBOR, percent)On U.S. dollar deposits 6.6 3.7 2.8 4.5 –0.1 0.1On Japanese yen deposits 0.3 0.2 0.1 0.1 — —On euro deposits 4.6 4.1 3.7 4.5 — 0.8

Note: Real effective exchange rates are assumed to remain constant at the levels prevailing during February 11–March 11, 2002.1Using updated purchasing-power-parity (PPP) weights, summarized in the Statistical Appendix, Table A.2Includes Indonesia, Malaysia, the Philippines, and Thailand.3Includes Malta.4Simple average of spot prices of U.K. Brent, Dubai, and West Texas Intermediate crude oil. The average price of oil in U.S. dollars a barrel

was $24.28 in 2001; the assumed price is $23.00 in 2002, and $22.00 in 2003.

counts for a substantial share of output and ex-ports. In the Middle East, growth has been ad-versely affected by lower oil prices—althoughthe recent rebound will help—as well as thedeterioration in the security situation. Turkeyis gradually recovering from the severe reces-sion of 2001, but the economy remains vulner-able to adverse shocks. In contrast, growth inthe Commonwealth of Independent States hasbeen relatively unaffected by the slowdown,buoyed by solid growth in Russia and Ukraine.Activity in central and eastern Europeaneconomies—except Poland—has also held upwell, aided by robust domestic demand andforeign direct investment.

• While the poorest countries have clearly beenadversely affected by the slowdown, primarilythrough lower commodity prices and fallingexternal demand, growth has in general beensurprisingly well sustained, especially in thosecountries with the strongest domestic policies.This has been aided by the ending of a num-ber of conflicts in Africa, as well as the re-sources released under the Heavily IndebtedPoor Countries Initiative (HIPC). Growth inthe HIPC countries is projected to pick up fur-ther in 2003 and beyond, although it is impor-tant to recognize that in the past the IMF’sforecasts for African countries have provedconsistently optimistic.5

As noted above, the risks to the forecast havebecome more balanced over the past months.There are good reasons to expect a pickup in ac-tivity in the period ahead; indeed it is possiblethat the pace of recovery could exceed expecta-tions, as has generally been the case in the past(Box 1.2). Nonetheless, there are also significantrisks to the sustainability and durability of theupturn, in the United States and elsewhere,which will pose important challenges for policy-makers in the period ahead.• First, the late 1990s saw the cumulative develop-

ment of a number of imbalances in the U.S. and the

ECONOMIC PROSPECTS AND POLICY ISSUES

7

-3

-2

-1

0

1

2

3

4

5

6

-1

0

1

2

3

4

5

6

7

Figure 1.5. Global Recovery(Percent change from four quarters earlier)

Real GDP in most regions is expected to have bottomed out in late 2001, with a recovery beginning in the first half of 2002.

WorldIndustrial

Emerging markets

Euroarea Japan

1996 98 2000 2002

1

United States

Sources: Haver Analytics; and IMF staff estimates. Australia, Canada, Denmark, euro area, Japan, New Zealand, Norway, Sweden, Switzerland, the United Kingdom, and the United States. Hong Kong SAR, Korea, Singapore, and Taiwan Province of China. Indonesia, Malaysia, Philippines, and Thailand. Czech Republic, Hungary, Israel, Poland, Russia, South Africa, and Turkey. Argentina, Brazil, Chile, Colombia, Mexico, Peru, and Venezuela.

1

2345

1996 98 2000 2002

-4

-2

0

2

4

6

8

-12

-8

-4

0

4

8

12 China and India

NIEs

Emerging Asia Other emerging markets

Latin America

1996 98 2000 2002

2

1996 98 2000 2002

ASEAN-43

4

5

5In part reflecting the impact of natural disasters andconflicts. See Box 3.1, Interim World Economic Outlook,December 2001.

global economy—notably, the large U.S. currentaccount deficit and surpluses elsewhere (Table1.3), the low U.S. personal savings rate, the ap-parent overvaluation of the U.S. dollar andundervaluation of the euro, and relativelyhigh levels of corporate and household in-debtedness in a number of countries. As hasbeen discussed extensively in previous issuesof the World Economic Outlook, these imbal-ances have been driven in large part by therelatively rapid growth in the United Statesrelative to other countries. This, in turn, partlyreflected cyclical factors, but also resultedfrom the improvement in U.S. productivity

growth relative to other countries. Partly be-cause the downturn has been so synchronizedand the recession in the United States hasbeen mild, there has been only a moderatecorrection in these imbalances during thedownturn, and the process by which this cor-rection eventually occurs will importantly affectthe outlook. For example, given the substantialstimulus in the pipeline, it is possible U.S.growth could rebound more quickly than ex-pected, which would lead to a further widen-ing of these imbalances. While this would likelybe manageable in the short term, especially ifunderlying U.S. productivity growth remained

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

8

Table 1.2. Advanced Economies: Real GDP, Consumer Prices, and Unemployment(Annual percent change and percent of labor force)

Real GDP Consumer Prices Unemployment____________________________ ____________________________ ____________________________2000 2001 2002 2003 2000 2001 2002 2003 2000 2001 2002 2003

Advanced economies 3.9 1.2 1.7 3.0 2.3 2.2 1.3 1.8 5.9 6.0 6.4 6.2Major advanced economies 3.5 1.1 1.5 2.8 2.3 2.1 1.1 1.7 5.8 6.0 6.5 6.3

United States 4.1 1.2 2.3 3.4 3.4 2.8 1.4 2.4 4.0 4.8 5.5 5.3Japan 2.2 –0.4 –1.0 0.8 –0.8 –0.7 –1.1 –0.5 4.7 5.0 5.8 5.7Germany 3.0 0.6 0.9 2.7 2.1 2.4 1.5 1.2 7.9 7.9 8.2 8.1France 3.6 2.0 1.4 3.0 1.8 1.8 1.5 1.4 9.5 9.0 9.2 8.7Italy 2.9 1.8 1.4 2.9 2.6 2.7 2.2 1.6 10.6 9.5 9.3 8.9United Kingdom1 3.0 2.2 2.0 2.8 2.1 2.1 2.4 2.5 5.6 5.1 5.4 5.4Canada 4.4 1.5 2.5 3.6 2.7 2.5 0.9 1.8 6.8 7.2 7.1 6.7

Other advanced economies 5.3 1.6 2.5 3.7 2.4 2.9 2.0 2.1 6.2 6.1 6.3 5.8Spain 4.1 2.8 2.3 3.2 3.5 3.2 2.3 2.3 14.1 13.0 13.0 12.4Netherlands 3.5 1.1 1.4 2.7 2.3 5.1 3.4 2.3 2.6 2.0 2.5 2.7Belgium 4.0 1.1 0.9 3.2 2.7 2.4 1.1 1.2 6.9 6.6 7.3 7.0Sweden 3.6 1.2 1.6 2.7 1.0 2.6 2.3 2.2 4.7 4.0 4.4 4.3Austria 3.0 1.0 1.3 2.9 2.0 2.3 1.8 1.6 3.7 3.8 4.1 3.8Denmark 3.0 0.9 1.3 2.4 2.9 2.1 2.3 2.2 5.2 5.0 5.2 5.2Finland 5.7 0.7 1.4 3.1 3.0 2.6 1.5 1.6 9.8 9.2 9.8 9.7Greece 4.3 4.1 3.4 2.9 2.9 3.7 3.3 2.7 11.4 10.9 10.9 10.7Portugal 3.2 1.6 0.8 2.0 2.8 4.4 2.9 2.2 4.0 4.1 4.2 4.3Ireland 11.5 6.0 3.2 6.2 5.3 4.0 4.4 3.0 4.3 4.0 4.7 4.7Luxembourg 7.5 5.1 3.0 6.0 3.2 2.7 1.9 1.8 2.6 2.5 2.9 2.7

Switzerland 3.0 1.3 0.8 2.6 1.6 1.0 1.0 1.0 2.0 1.9 2.6 2.3Norway 2.3 1.4 2.3 2.2 3.1 3.0 1.5 2.5 3.4 3.6 3.8 3.7Israel 6.4 –0.6 1.3 3.8 1.1 1.1 3.1 2.1 8.8 9.3 10.5 9.4Iceland 5.0 2.1 –0.9 1.9 5.0 6.7 6.4 3.5 1.3 1.7 2.3 2.6Cyprus 5.1 4.0 3.0 4.2 4.1 2.0 1.8 2.2 3.4 3.6 3.8 4.0

Korea 9.3 3.0 5.0 5.5 2.3 4.1 2.7 2.6 4.1 3.7 3.5 3.5Australia2 3.2 2.4 3.9 4.0 4.5 4.4 2.3 2.3 6.3 6.7 6.7 6.5Taiwan Province of China 5.9 –1.9 2.3 4.8 1.3 — 0.4 1.6 3.0 5.1 5.0 4.9Hong Kong SAR 10.5 0.1 1.5 3.6 –3.7 –1.6 –2.5 — 4.9 5.0 5.6 5.4Singapore 10.3 –2.1 3.2 5.1 1.1 1.0 1.1 1.6 3.1 4.7 4.4 3.7New Zealand2 3.9 2.4 2.6 3.0 2.7 2.7 1.8 1.5 6.0 5.3 5.5 5.6

MemorandumEuropean Union 3.4 1.7 1.5 2.9 2.3 2.6 2.0 1.8 8.2 7.7 7.9 7.7

Euro area 3.4 1.5 1.4 2.9 2.4 2.6 1.9 1.6 8.8 8.3 8.5 8.2

1Consumer prices are based on the retail price index excluding mortgage interest.2Consumer prices excluding interest rate components; for Australia, also excluding other volatile items.

strong, it could adversely affect the sustainabil-ity of recovery later on, particularly if growthin other countries did not pick up, and in-crease the possibility of an eventual disorderlyadjustment.6 It is also possible, however, thatthe recovery in the United States could beweaker than expected, partly because of theimbalances—for instance, if private investmentis held back by weak profitability or excess ca-pacity proves more widespread than presentlybelieved, or if U.S. households and businesses

seek to strengthen savings and balance sheetsearlier. In that case, the imbalances wouldlikely correct sooner, but at the cost of a moresubdued recovery in both the United Statesand the rest of the world.

• Second, as also stressed in the IMF’s GlobalFinancial Stability Report, financial markets maystill embody relatively optimistic expectations for cor-porate profitability and the pace of recovery. Werethese expectations to be disappointed, therewould likely be a downward adjustment in as-set prices, which could adversely affect bothconsumer and business confidence and de-mand more generally. These risks may beheightened by the weaknesses in the account-ing and auditing framework highlighted fol-lowing the recent collapse of Enron, whichhas raised concerns that the financial posi-tions of other firms could also prove weakerthan expected. Beyond this, while the interna-tional financial infrastructure has generallyheld up well in the face of the shocks experi-enced in 2001, a decline in asset prices or de-layed recovery could put pressure on financialinstitutions in countries where the pace ofconsolidation and restructuring has lagged, aswell as the performance of certain financialmarkets, notably for credit derivatives.

• Third, the situation in Japan, which is presently un-dergoing its worst recession in the postwar period, re-mains a source of serious concern. Given the lim-ited macroeconomic policy options, weakactivity in Japan is proving increasingly diffi-cult to offset through policy actions—withnegative consequences, particularly for therest of the region. The financial position ofthe banking system has become increasinglystrained as loan-loss announcements have in-creased, and this is undermining confidence.Further, growing concerns about debt sustain-ability and additional downgrades by ratingagencies make the government bond marketvulnerable to a sharp swing in investor senti-ment and a spike in yields.

ECONOMIC PROSPECTS AND POLICY ISSUES

9

Table 1.3. Selected Economies: Current Account Positions(Percent of GDP)

2000 2001 2002 2003

Advanced economies –1.0 –0.8 –0.8 –0.7 Major advanced economies –1.6 –1.4 –1.4 –1.4

United States –4.5 –4.1 –4.1 –4.0Japan 2.5 2.1 2.9 3.4Germany –1.0 0.5 0.5 0.6France 1.8 2.5 2.5 2.2Italy –0.5 0.4 0.7 1.0United Kingdom –1.8 –1.8 –2.1 –2.3Canada 2.5 2.7 1.8 1.6

Other advanced economies 1.8 2.5 2.4 2.3Spain –3.1 –2.0 –1.7 –1.6Netherlands 3.0 3.1 3.7 3.3Belgium-Luxembourg 4.8 4.9 4.9 4.7Sweden 2.6 3.3 3.0 3.0Austria –2.8 –2.4 –1.6 –1.4Denmark 1.6 2.9 2.5 3.2Finland 7.4 5.4 4.8 4.9Greece –6.8 –6.2 –6.1 –6.0Portugal –10.4 –9.7 –9.3 –8.9Ireland –0.6 –0.6 –1.4 –1.6

Switzerland 12.9 10.2 10.8 11.3Norway 14.3 14.8 13.9 13.1Israel –1.2 –1.5 –1.7 –2.1Iceland –10.3 –6.9 –5.2 –3.9Cyprus –5.2 –4.3 –3.9 –3.7

Korea 2.7 2.0 1.5 0.6Australia –4.0 –2.6 –3.2 –2.7Taiwan Province of China 2.9 6.7 6.6 6.6Hong Kong SAR 5.5 7.4 7.7 7.7Singapore 17.0 23.3 21.4 21.4New Zealand –5.6 –3.2 –4.5 –4.2

MemorandumEuropean Union –0.4 0.4 0.4 0.4

Euro area1 –0.2 0.7 0.8 0.8

1Calculated as the sum of the balances of individual euro areacountries.

6See also “Alternative Scenarios: How Might Medium-Term Productivity Growth Affect the Short-Term Outlook?”Chapter I, Appendix II, World Economic Outlook, October 2001, for a detailed discussion.

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

10

Perhaps the most conventional rule of thumbfor defining a national recession is two straightquarters of negative GDP growth (see ChapterIII on recessions). Unfortunately, this simple ruledoes not translate well to the global context.First, quarterly real GDP data are weak; for anumber of major emerging market countries,quarterly output data do not exist before themid-1990s, and there are still many countriesthat do not report GDP on a quarterly basis.Even among those that do, national methods forseasonally adjusting output data differ to such anextent that meaningful aggregation is difficult.Second, while we cannot measure it exactly, it islikely that quarterly global growth does not turnnegative nearly as often as does GDP within thetypical country. Indeed, annual global growthhas never been negative for any year in recenthistory (see the first figure, which shows globalGDP growth using the IMF’s purchasing-power-parity (PPP) weights to aggregate countryincome.)

The principal reason that global growth israrely negative is that world output is more di-versified than national output. For example, theUnited States, Europe, and Japan do not alwaysexperience downturns at the same time. Data onannual real GDP indicate that this slowdown hasa similar level of synchronization as earlierepisodes in the mid-1970s and early 1980s, eventhough growth in China (in particular) has re-mained relatively robust over this slowdown.The lower level of synchronization in the early1990s was an exception—largely reflecting spe-cific regional events, including the asset pricebubble in Japan and the consequences ofGerman unification activity in continentalEurope. It is also the case that trend growth forthe world is higher than for most advancedeconomies because developing countries growfaster on average, so it takes a steeper dip to hitnegative territory.

While global output may rarely decline, it isuseful to have a simple benchmark for identify-

Box 1.1. Was It a Global Recession?

The main authors are Kenneth Rogoff, DavidRobinson, and Tamim Bayoumi, in consultation withother members of a committee that included CarmenReinhart, Manmohan Kumar, and Aasim Husain.

1970 75 80 85 90 95 20000

2

4

6

8

-15

-10

-5

0

5

10

15

20

25Monthly Indices of Global Activity

Trade1

Industrial production2

Sources: IMF, International Financial Statistics; OECD, Main Economic Indicators; and WEFA-DRI. Weighted average of imports and exports trade volumes, using 1993 trade weights. PPP-weighted average.

1

2

1970 75 80 85 90 95 2000-2

0

2

4

6

Market exchange rate weights

PPP weights

Market exchange rate weights

PPP weights

Measures of Global Activity(Percent change from a year earlier; three-month centered moving average unless otherwise indicated)

1970 75 80 85 90 95 Jan. 2002

Annual Real GDP(percent change)

Annual Real GDP per Capita(percent)

ECONOMIC PROSPECTS AND POLICY ISSUES

11

ing slowdowns that could be labeled as globalrecessions. One reasonable solution to this co-nundrum is to adjust world output growth forgrowth in world population, and declare that asufficient (although not necessary) conditionfor a global recession is any year in which worldper capita growth (on a PPP basis) is negative.In the second figure, the first bars show unad-justed world GDP growth during the major re-cent slowdowns, 1975, 1982, 1991, and 2001.In no case did world growth dip below 1 per-cent, much less turn negative. In 1975, GDPgrowth of 1.9 percent was almost exactly offsetby world population growth, so that per capitaGDP growth was about zero. However, per capitaGDP growth actually turned negative in 1982and, to a lesser extent, in 1991. By contrast, percapita GDP growth in 2001 was over 1 percent,well above zero. Compared with the earlierepisodes, unadjusted growth was stronger at 2.5percent, instead of dipping below 2 percent asin the previous episodes. Also, world populationgrowth is lower today (1.3 percent) than it was a

decade earlier. Thus, the current slowdown hasnot come close to meeting the hurdle of nega-tive per capita annual GDP growth, which wouldautomatically qualify it as a recession. This partlyreflects the relatively high weight of China,which has continued to grow strongly, in theIMF PPP weights. Nonetheless, even going tothe extreme of using market exchange rate-based weights (which substantially reduceChina’s weight), per capita GDP growth wouldstill remain slightly positive in 2001.

Can we declare that the world is not in reces-sion simply because annual global per capitagrowth is positive? No, not necessarily. Whilenegative per capita GDP growth (using IMF PPPweights) is a sufficient condition to identify aglobal recession, by itself it would probably beunduly conservative. As in the case of individualrecessions, one can not rely absolutely on anymechanical rule, but instead some element ofjudgment is required. That is how recessions areidentified in the United States by the NationalBureau of Economic Research (NBER), forexample. The NBER defines a recession as a sig-nificant decline in activity spread across theeconomy and lasting more than a few months,and focuses on economy-wide monthly series(especially nonfarm employment and real per-sonal income less transfers). It also looks atdata from manufacturing (real manufacturingand trade sales and industrial production),although—as the NBER notes—this is a rela-tively small part of the U.S. economy whosemovements often differ from those of other sec-tors. The rule of thumb of two quarters of nega-tive growth often referred to by commentators issimply a useful way of approximating this sys-tem. Indeed, in the recent downturn, the NBERcommittee chose to identify the U.S. slowdownas a recession even though, based on currentinformation, GDP growth was only negative inthe third quarter.

How might one apply these principles to iden-tifying global recessions even when per capitaGDP growth is positive? Given the data inadequa-cies, there is no simple extension of the NBER’smethodology to the global economy. We have al-

Comparison of Global Slowdowns(Percent)

1975 1982 1991 2001-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

GDP growth Per capita GDP growth

• Finally, there are a number of specific risks to theoutlook. Most recently, the volatility in the oilmarket has become a significant potential riskto the recovery, especially if the security situa-tion in the Middle East were to deterioratefurther.7 Were oil prices to rise substantiallyfurther, there could be a significant impact onthe global recovery (see Table 1.12 inAppendix 1.1, which shows the impact ofhigher oil prices on global growth). While oil

exporting countries would clearly benefit,there would be adverse effects on most indus-trial and many emerging market economies,notably in Asia, and many of the heavily in-debted poor countries and several CIS coun-tries could be quite seriously affected. Beyondthis, the war against terrorism has so far gonebetter than expected but setbacks could ad-versely affect confidence; and, although conta-gion from developments in Argentina has so

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

12

ready noted the difficulties in getting satisfactoryquarterly global GDP, and certainly global ver-sions of the main monthly indicators used by theNBER for the United States will not be availablefor the foreseeable future. However, there aremonthly data on global industrial productionand merchandise trade volumes, although—as inthe United States—these focus on the manufac-turing sector, which comprises less than onequarter of global GDP.1 The first figure showsthe change in industrial production and tradevolumes at a global level since 1970. Both seriesclearly identify the global slowdowns after thetwo oil crises that are also clear in the real GDPdata. Subsequently, however, the correspondenceis less close. For example, growth in bothmonthly series remained positive in the recessionof the early 1990s. Moreover, for the Asian crisis,both series suggest a more severe slowdown thandoes real GDP (partly reflecting the large manu-facturing sectors in many Asian economies). Themost recent data show a sharp fall in productionand trade—corresponding to the synchronizedand disruptive decline in manufacturing produc-tion, partly related to the information technol-ogy (IT) sector—but again the picture fromthese series appears more severe than that from

data on real GDP. Cyclical movements in manu-facturing and trade tend to be larger than inoverall activity. In addition, the manufacturingand trade series have been disproportionatelyimpacted by the rapid fall in global IT.

Aside from the global aggregates, it is impor-tant to also look at the extent to which the slow-down is spread across the globe and the speed ofthe decline. If, for example, the United States ex-perienced a sufficiently severe recession, globalaverage numbers could be quite poor even ifthere were positive GDP growth elsewhere. Thisscenario would not, in our definition, qualify as aglobal recession. On the other hand, a particu-larly rapid and generalized fall from a high levelto a much lower level should be an element ofone’s assessment. To ascertain the global natureof the slowdown, we considered, among otherfactors, quarterly GDP where available. Thesedata indicate negative growth for the third quar-ter in some regions of the world, including theUnited States, Germany, Japan, and severalemerging markets. While weakness remained inGermany and Japan in the fourth quarter, theUnited States rebounded. Growth in China andIndia has remained robust throughout.

Overall, therefore, our reading of the dataindicates that the recent slowdown falls some-what short of a global recession, certainly incomparison with earlier episodes that we wouldhave labeled as global recessions. That said, itwas a close call.

Box 1.1 (concluded)

1Manufacturing currently makes up slightly under20 percent of GDP in industrial countries (down fromalmost 30 percent in 1970), and a relatively stable 23percent in developing countries.

7See IMF (2000) for a detailed discussion of the impact of oil price changes on the global economy.

ECONOMIC PROSPECTS AND POLICY ISSUES

13

The consensus among economic forecasters isthat the U.S. recession that started in March2001 will be over during the course of this year.For example, the mean forecast for U.S. growthin 2002 reported by the March survey of Consen-sus Forecasts is 2.1 percent, which would imply arobust recovery in the second half of the year.Given economic forecasters’ poor performancein predicting recessions,1 it is natural to askwhether they are any better at predicting recov-eries. It is difficult to answer this question usingdata for a single country as the number of recov-eries for which consistent growth forecasts arereadily available would be too small to make reli-able inferences. Therefore, this box reviews theexperience from a large sample of industrialcountries to assess how well forecasters havedone.

Cross-Country Evidence on Predicting Recoveries

The publication Consensus Forecasts has pro-vided macroeconomic forecasts for 26 industrial-ized countries on a monthly basis since October1989. Each issue of the publication surveys anumber of prominent financial and economicanalysts, and reports their individual forecasts aswell as the mean forecast (the consensus). Everymonth, Consensus Forecasts contains a new fore-cast of average annual GDP growth in the cur-rent and forthcoming year. Thus, for example,between January 1990 and December 1991 thereare 24 separate forecasts of real GDP growth in1991.2

The behavior of forecasts during the U.S.recession and recovery of 1991–92 provides agood example of the behavior of forecastsaround turning points (see the figure). InJanuary 1990, the forecast for U.S. growth dur-ing 1991 was about 2.5 percent. Following Iraq’s

invasion of Kuwait in August 1990, forecasts forU.S. growth started to be marked down substan-tially. By the start of 1991, the forecast was for amodest recession that year (figure, top panel).

How did the recognition of the recession in1991 affect the forecasts for 1992? Initially, notvery much. The year-ahead forecasts for 1992(the ones made during 1991) remained virtuallyunchanged at about 2.5 percent. The current-year forecasts for 1992 showed somewhat greatervariation but clearly never came close to fore-casting a continuation of the recession of theprevious year (figure, bottom panel). The econ-

Box 1.2. On the Accuracy of Forecasts of Recovery

Consensus Forecasts of U.S. Growth for 1991–92 Recession and Recovery(Percent)

-1.0

-0.5

0

0.5

1.0

1.5

2.0

2.5

3.0

Jan. Apr. Jul. Oct. Jan. Apr. Jul. Oct. 1990 1991

Forecasts for 1991

0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan. Apr. Jul. Oct. Jan. Apr. Jul. Oct. 1991 1992

Forecasts for 1992

Month and year in which forecast was made

Month and year in which forecast was made

Source: Consensus Economics, Inc.

The main author is Prakash Loungani.1See Box 1.1, World Economic Outlook, May 2001, and

Loungani (2001).2The first 12 forecasts—the ones made during

1990—are referred to as year-ahead forecasts; the 12forecasts made during 1991 are called current-yearforecasts.

far been contained, risks remain, particularlyfor the other countries in the region.In setting the stance of policies, policymakers

will need to consider not just the baseline projec-tions, but also the balance of these various risksand the costs associated with each. In making thisassessment, a number of considerations are rele-

vant. First, given the past fall in commodity pricesand substantial excess capacity in most industrialcountries, and increasing evidence that the im-provement in central bank credibility in recentyears is helping to anchor inflationary expecta-tions (Chapter II), long-term inflationary risks re-main limited at this stage. Second, if growth in

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

14

omy did indeed recover and the forecast errorwas small.

The pattern displayed in the figure is quitetypical of forecasts around turning points forthe 25 other episodes of recessions and poten-tial recoveries (in the subsequent year) sinceOctober 1989.3 Recessions typically arrive beforethey are forecast. The recognition that the coun-try is in a recession does not generally lead todrastic markdowns of the forecast for the post-recession year. That is, forecasters act as thoughthe recession is not going to lead to a secondyear of negative growth.

How well does this strategy work in deliveringaccurate forecasts? The simple answer is:“Reasonably well.” In three-fourths of cases overthe 1990s, the recession did not result in a sec-ond year of negative growth.4 Hence, eventhough large forecast errors are made in thecase of multiyear recessions, forecasting a recov-ery in the year following a recession turns out tobe a reasonably good bet on average. Using theApril survey of Consensus Forecasts, the mean ab-solute error of current-year forecasts for the 26episodes of potential recoveries is 1.29 percent-age points. This is only about half as large as themean absolute error from a naive forecastingstrategy of predicting a continuation of the re-cession. While the accuracy of the forecasts isquite good, there is a tendency for forecastsmade at the start of the year of the recovery tounderpredict it. This property was noted in the

case of forecasts of U.S. recoveries over the pe-riod 1972 to 1984 by Zarnowitz (1986). The U.S.recovery of 1992 and recoveries in the cross-country sample studied in this box also tendedto be underpredicted—by about !/2 to #/4 of apercentage point—in forecasts made near thestart of the year.

Comparison with WEO

On average, there is a high degree of similar-ity between forecasts made by the AprilConsensus survey and those reported in the IMF’sMay World Economic Outlook during the years ofpotential recoveries: the mean absolute error ofthe May WEO forecasts is 1.24 percentagepoints, virtually identical to that of ConsensusForecasts. The forecast errors are also highly cor-related at other forecasting horizons as well,such as comparing the October Consensus withthe fall WEO current-year forecasts or compar-ing year-ahead forecasts; hence, the mean ab-solute errors for the two sources of forecasts arevirtually the same at every forecasting horizon.

Conclusion

Conventional wisdom among forecasters isthat the U.S. economy will start to grow againthis year. What these forecasts have going forthem is the fact that multiyear recessions aresomewhat rarer than those that end in about ayear. Over the 1990s, for the set of industrializedcountries studied here, forecasting a recovery inthe year following a recession has thereforeturned out to be a reasonably good bet. So eventhough forecasters are caught flat-footed whenrecessions turn out to be multiyear, the message,broadly speaking, is, most recessions catch fore-casters by surprise; most recoveries do not.

Box 1.2 (concluded)

3See Loungani (2002) for evidence from other in-dustrialized countries.

4Over a longer period, as noted in Chapter III, 60percent of recessions in industrial countries since 1973lasted just one year.

some industrial countries were to disappoint,there could be a significant impact on the rest ofthe world, particularly in emerging market anddeveloping countries. Third, while wider globalimbalances would clearly be of concern, theseshould be addressed primarily through appropri-ate medium-term policies in the United Statesand better growth policies elsewhere. Overall,there appear to be three main policy priorities.• Macroeconomic policies in most industrial countries

should remain broadly supportive of activity, al-though in countries where the recovery is most ad-vanced, attention will need to turn toward reversingearlier monetary policy easing; in Japan, aggressiveaction to address deflation is required. The FederalReserve appropriately left U.S. interest rateson hold in March, while noting that the risksto price stability and growth had becomebroadly balanced. As the recovery progresses,some withdrawal of stimulus is likely to be re-quired, while the focus of fiscal policy shouldshift to medium-term consolidation. In theeuro area, with growing signs of recovery, thepresent stance of monetary policy is broadlyappropriate, while the automatic stabilizersshould be allowed to operate to support activ-ity within the constraints of the Stability andGrowth Pact. In Japan, macroeconomic poli-cies should be as supportive as possible, in-cluding through more aggressive monetaryeasing to address deflation, even if this resultsin some further depreciation of the yen, andthrough an additional supplementary budgetto maintain a broadly neutral fiscal stance in2002 and 2003 (Table 1.4).

• The medium-term policy framework needs to be gearedtoward supporting sustainable growth and an orderlyreduction in the global imbalances. As has been ar-gued in many previous issues of the WorldEconomic Outlook, the global imbalances reflectnot just not the past strong growth in theUnited States—and the excesses that were asso-ciated with it—but also relatively weak growthin other parts of the world. Consequently, deci-sive action to reinvigorate activity in Japan, con-tinued structural reforms to encourage growthin the euro area, building on the progress

made at the Barcelona summit, and continuedcorporate and financial sector reform in someAsian emerging markets with large current ac-count surpluses, are a priority from both na-tional and international perspectives. In theUnited States, in turn, it will be important toavoid exacerbating external imbalances by en-suring that fiscal balance (excluding social se-curity) is restored over the medium term (seeAppendix 1.2 for a detailed discussion).

• As experience during the downturn has shown, it re-mains essential to press ahead with efforts to reducevulnerabilities and maximize the scope for policyflexibility in response to external shocks. In indus-trial countries, this requires accelerated effortsto address the looming problems resultingfrom aging populations, where progress inmany countries falls short of what is required;a sustained effort to use the recovery toachieve broadly balanced budgets in the euroarea within a reasonable time frame, as calledfor under the Stability and Growth Pact; andthe design and publication of a crediblemedium-term fiscal consolidation plan inJapan. In emerging markets, corporate and fi-nancial reforms remain a central priority, par-ticularly in Asia; in Latin America—and insome Asian countries, including India andChina—medium-term efforts to strengthen fis-cal positions are also critical (Chapter II).For many developing countries, an overarch-

ing priority over the longer run remains an en-during reduction in poverty, which in turn willrequire a sustained improvement in growth.From this perspective, it is encouraging that GDPgrowth in China, India, and sub-Saharan Africa,where the bulk of the poorest live, has been rela-tively well sustained during the downturn, and isexpected to pick up in 2002–03. In both Chinaand India, poverty has been on a steady down-ward trend, although in India GDP growth maystill fall short of the level consistent with furthersustained progress, underscoring the need for fis-cal and structural reforms (see below). The mostentrenched problems remain in sub-SaharanAfrica, where GDP growth is well below the levelneeded to make substantial inroads in poverty.

ECONOMIC PROSPECTS AND POLICY ISSUES

15

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

16

Table 1.4. Major Advanced Economies: General Government Fiscal Balances and Debt1(Percent of GDP)

1986–95 1996 1997 1998 1999 2000 2001 2002 2003 2007

Major advanced economies Actual balance –3.9 –3.6 –2.0 –1.6 –1.2 –0.3 –1.7 –2.6 –2.1 –0.6Output gap2 –0.6 –1.9 –1.3 –1.1 –0.7 0.3 –1.0 –1.7 –1.4 —Structural balance –3.5 –2.7 –1.4 –1.0 –0.9 –1.0 –1.5 –2.0 –1.7 –0.6

United StatesActual balance –4.5 –2.4 –1.3 –0.1 0.6 1.5 0.1 –1.4 –1.2 –0.5Output gap2 –1.4 –2.8 –1.6 –0.5 0.4 1.4 –0.4 –0.8 –0.5 —Structural balance –4.0 –1.5 –0.7 0.1 0.5 1.0 0.1 –1.2 –1.0 –0.5Net debt 53.2 59.2 57.0 53.4 48.9 43.7 42.2 42.0 40.9 34.6Gross debt 67.3 72.8 70.3 66.6 63.4 57.4 55.4 54.7 53.0 44.3JapanActual balance –0.4 –4.9 –3.7 –5.6 –7.6 –8.5 –8.5 –8.7 –7.6 –2.3

Excluding social security –3.2 –7.0 –5.8 –7.2 –9.0 –9.2 –8.8 –8.7 –7.4 –2.9Output gap2 0.7 0.8 1.0 –1.6 –2.2 –1.3 –2.7 –4.6 –4.8 —Structural balance –0.6 –5.2 –4.1 –5.0 –6.9 –8.3 –7.8 –7.3 –6.1 –2.1

Excluding social security –3.5 –7.2 –6.0 –6.8 –8.6 –9.2 –8.6 –8.1 –6.8 –2.8Net debt 13.8 21.6 27.9 38.0 44.4 52.7 62.2 72.4 80.2 85.3Gross debt 71.8 91.7 97.4 108.4 120.6 130.8 143.4 157.0 166.4 166.5Euro areaActual balance –4.5 –4.2 –2.5 –2.2 –1.3 0.2 –1.4 –1.6 –1.1 0.2Output gap2 –0.2 –2.1 –2.0 –1.4 –1.1 –0.1 –0.9 –1.9 –1.4 –0.2Structural balance . . . –3.0 –1.4 –1.4 –0.8 –1.1 –1.1 –0.8 –0.5 0.2Net debt 46.2 62.6 62.9 61.4 60.5 58.3 57.6 57.4 56.4 51.4Gross debt 61.0 76.1 75.4 73.7 72.6 70.2 69.1 68.9 67.5 58.4

Germany3

Actual balance4 –2.2 –3.4 –2.7 –2.2 –1.6 1.2 –2.7 –2.7 –2.0 0.2Output gap2 0.1 –0.7 –1.2 –1.1 –1.1 — –1.2 –2.1 –1.4 —Structural balance –1.8 –2.7 –1.6 –1.3 –0.8 –1.3 –2.0 –1.4 –1.1 0.2Net debt 27.6 51.1 52.3 52.2 52.6 51.6 51.1 52.5 52.7 47.9Gross debt 45.1 59.8 61.0 60.9 61.3 60.3 59.8 61.2 61.4 56.6FranceActual balance4 –3.5 –4.1 –3.0 –2.7 –1.8 –1.4 –1.4 –2.1 –1.9 —Output gap2 –0.5 –3.3 –3.1 –1.8 –1.2 –0.2 –0.5 –1.5 –0.9 —Structural balance –3.0 –1.9 –1.0 –1.6 –1.0 –1.2 –1.3 –1.4 –1.3 —Net debt 30.6 48.1 49.6 49.8 48.9 47.8 48.8 48.3 48.0 51.6Gross debt 39.3 57.1 59.3 59.5 58.5 57.5 57.1 58.0 57.7 51.6ItalyActual balance4,5 –10.4 –7.1 –2.7 –2.8 –1.8 –0.5 –1.4 –1.2 –0.2 –0.3Output gap2 –0.1 –2.0 –2.3 –2.4 –2.7 –1.9 –2.0 –2.5 –1.6 —Structural balance –10.4 –6.2 –1.7 –1.7 –0.6 –2.1 –1.2 –0.7 –0.1 –0.3Net debt 97.8 116.1 113.8 110.1 108.4 104.6 103.5 101.9 99.2 86.2Gross debt 103.7 122.7 120.2 116.4 114.5 110.6 109.4 107.7 104.8 91.1

United KingdomActual balance4 –3.4 –4.1 –1.5 0.3 1.5 4.4 0.4 –0.9 –1.2 –1.0Output gap2 0.5 –1.3 –0.5 0.2 –0.5 0.1 –0.1 –0.8 –0.7 —Structural balance –3.0 –3.3 –0.9 0.5 1.6 2.1 0.3 –0.7 –0.8 –1.0Net debt 25.7 46.2 44.6 41.9 39.0 34.5 30.9 28.9 28.6 28.6Gross debt 43.4 51.8 49.6 46.5 43.9 40.9 37.9 35.7 34.6 33.9CanadaActual balance –6.5 –2.8 0.2 0.5 1.6 3.2 2.4 1.7 1.7 1.5Output gap2 –2.5 –6.5 –5.1 –3.7 –1.4 0.3 –0.9 –1.0 –0.2 —Structural balance –5.1 — 2.1 2.4 2.4 3.1 2.9 2.3 1.9 1.5Net debt 69.9 87.8 84.1 81.2 74.9 66.3 61.8 58.7 53.9 38.8Gross debt 101.6 120.3 117.6 115.7 112.3 102.6 97.8 93.9 87.3 66.6

Note: The methodology and specific assumptions for each country are discussed in Box A1.1Debt data refer to end of year; for the United Kingdom they refer to end of March.2Percent of potential.3Data before 1990 refer to west Germany. For net debt, the first column refers to 1988–94. Beginning in 1995, the debt and debt-service obli-

gations of the Treuhandanstalt (and of various other agencies) were taken over by general government. This debt is equivalent to 8 percent ofGDP, and the associated debt service to !/2 to 1 percent of GDP.

4Includes one-off receipts from the sale of mobile telephone licenses equivalent to 2.5 percent of GDP in 2000 for Germany, 0.1 percent ofGDP in 2001 and 2002 for France, 1.2 percent of GDP in 2000 for Italy, and 2.4 percent of GDP in 2000 for the United Kingdom.

5Includes asset sales equivalent to 0.6 percent of GDP in 2001 and 2002, 0.5 percent in 2003, and 0.1 percent in 2004.

The main responsibility, of course, continues tolie with national governments, which must createconditions favorable to domestic savings mobi-lization and private sector investment and ensurethe effective use of both domestic and externalpublic resources—for which good governance isclearly key. The New Partnership for Africa’sDevelopment embodies a concerted and wel-come approach to these issues. However, as theManaging Director has stressed,8 these effortsmust be matched by “stronger, faster, and morecomprehensive” support from the internationalcommunity. Substantial assistance has now beenprovided under the Heavily Indebted PoorCountries Initiative (HIPC), and the progressmade at the Monterrey Conference—includingthe pledges of higher aid by the European Unionand the United States—is encouraging, butmuch more needs to be done to increase aidflows, which are less than one-third of the U.N.target of 0.7 percent of GNP.

The most important issue, however, remainsto further open up industrial country marketsand phase out trade-distorting subsidies—partic-ularly in agriculture—which seriously limit theability of poorer countries to compete in areaswhere they would otherwise have a comparativeadvantage. This would directly support growthand reform efforts in the poorest countries, andwould ultimately also be to the benefit of thericher countries themselves. More generally, therecent decision by the United States to raise tar-iffs on steel products is regrettable, and has al-ready led to the prospect of retaliation fromother countries. It will be essential for all coun-tries to make renewed efforts to resist protec-tionist pressures, and to ensure that substantiveprogress is made with multilateral trade negotia-tions under the Doha round.

North America: A Strengthening RecoveryIn the United States, activity remained weak dur-

ing the second half of 2001, but there are in-

creasingly strong indications that recovery isunder way, as the negative effects of the Septem-ber 11 events have proved more moderate thanearlier feared. Manufacturing output has begunto turn up, including in the high-tech sector; thehousing market has remained strong; retail saleshave remained surprisingly robust, althoughaided by auto incentives; and initial jobless claimshave fallen back, while the unemployment rate,which would generally still be increasing at thisstage of the cycle, remains below its December2001 peak. Forward-looking indicators, includingbusiness and consumer confidence, have pickedup significantly, equity markets have reboundedafter September 11, and the yield curve hassteepened. At the same time, aided by the earlierdecline in oil prices and substantial excess capac-ity, inflationary pressures remain moderate.

With activity expected to accelerate signifi-cantly in the first half of 2002, the recent reces-sion is likely to be the mildest on record. Whilethe decline in fixed investment and inventorieshas been similar to previous downturns (Figure1.6), private consumption has remained surpris-ingly strong. This has been supported by thesubstantial reductions in interest rates, and taxcuts over the past year; strong wage growth;widespread auto incentives, which—after nettingoff the inventory draw down—boosted GDPgrowth by an estimated #/4 percentage point (an-nualized) in the fourth quarter; the strength ofhouse prices (which appears to have offset a sig-nificant portion of the impact on consumptionfrom lower equity prices—see Chapter II); andlower oil prices.

Given signs of a sharp turnaround in inven-tory adjustment in early 2002, as well as the sub-stantial stimulus that is already in the pipeline,the staff’s projections envisage a strong recoveryin activity in the first half of the year, falling backsomewhat thereafter as the effects of these twofactors begin to dissipate. The risks to the pro-jection appear broadly balanced, and are impor-tantly linked to the process by which the various

NORTH AMERICA: A STRENGTHENING RECOVERY

17

8See “Working for a Better Globalization,” address by the Managing Director to the Conference on Humanizing theGlobal Economy, January 28, 2002 (www.imf.org/external/np/speeches/2002/012802.htm).

imbalances in the economy—notably the highcurrent account deficit, low personal savings rate,and relatively large financing requirement in thecorporate sector (Figure 1.6)—are resolved. Onthe one hand, it is certainly possible—given thesize of the stimulus in the pipeline—that activitywill recover more strongly than projected. Whilethis would be welcome in a number of respects,it could—as discussed above—exacerbate theseimbalances, especially if growth in other coun-tries disappoints. On the other hand, there re-main questions about the sustainability of apickup in final domestic demand. In particular,private sector investment could be constrainedby excess capacity and weak profitability (al-though the improvement in the fourth quarterof 2001 is welcome); and private consumptiongrowth could be dampened if consumers seek toincrease savings and rebuild balance sheets,Both of these could be exacerbated by a correc-tion in equity markets, which still appear richlyvalued. This would likely result in an earlier cor-rection in imbalances, but at the cost of a moresubdued U.S. and global recovery. Finally, muchcontinues to depend on external developments,including the speed of recovery in the rest of theworld, oil prices, and geopolitical developments.

In assessing the appropriate stance of policies,policymakers need to take account of the risksand costs related to the uncertainties on bothsides of the forecast, within a longer-term policyframework that is consistent with a gradual re-duction in the imbalances in the economy overtime. With clear evidence that recovery is underway, the Federal Reserve noted in March that therisks to economic growth and price stability hadbecome more evenly balanced. Provided signs ofeconomic strength continue, attention will soonneed to shift to withdrawing the substantial stim-ulus provided last year. On the fiscal side, thecombination of the June 2001 tax cuts and theemergency spending measures passed in the af-termath of the terrorist attacks, along with theoperation of the automatic stabilizers, has pro-vided substantial support to the economy. Thishas come, however, at the cost of a significantdeterioration in the fiscal position; the adminis-

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

18

400

450

500

550

600

650

84

86

88

90

92

94

96

98

50

60

70

80

90

100

10

12

14

16

18

-2

-1

0

1

2

3

4

5

6

-4

-3

-2

-1

0

1

2

3

4

Sources: Haver Analytics; and IMF staff estimates. Shading indicates business cycle from peak to trough. All data for nonfinancial corporate business sector.

Shape of Past Recessions (contribution to GDP growth, peak to trough)

Current recession

Past recession

Shape of Past Recoveries (contribution to GDP growth, year from trough)

1970 75 80 85 90 95 2001: Q4

Corporate Financing(percent of GDP)

The U.S. recession has been remarkably mild compared with previous experience, and the pace of recovery is correspondingly projected to be somewhat moremoderate. The low level of private saving and the high corporate financing requirement remain potential brakes on activity.

Internally generated funds (right scale)

Net exp

orts

Consu

mption

Fixed

inves

tmen

t

Inven

tories

Govern

ment

GDP grow

th

Net exp

orts

Consu

mption

Fixed

inves

tmen

t

Inven

tories

Govern

ment

GDP grow

th

Gross fixedinvestment(right scale)

1970 75 80 85 90 95 2001: Q4

12

Consumption and Wealth(ratio to personal disposable income)

Net worth(left scale)

Personal consumption(right scale)

Corporate debt(left scale)

1

1,2

Past recoveries

Projectedrecovery

Figure 1.6. United States: Recessions and Recoveries(Percent unless otherwise indicated)

tration’s recent budget—adjusted to take ac-count of the latest stimulus package as well asthe faster than expected recovery—provides ad-ditional stimulus in 2002 and would result inbudget deficits (excluding the social security sur-plus) persisting into the medium term.Moreover, with the budget based on relativelyoptimistic assumptions with regard to the con-tainment of non-defense expenditures, even thismay prove difficult to achieve. With economicactivity improving, efforts will now need to focuson returning the budget to broad balance (ex-cluding social security) over the medium term,and to address the longer-term financial prob-lems in the social security system. This wouldhelp manage the pressures associated with theaging population, as well as being supportive ofadjustment in the current account deficit.

Given the strong trade and financial linkages,Canada was strongly affected by the faster thanexpected slowdown in the United States, and ex-perienced a mild downturn in the second half of2001. As activity slowed, and with core inflationat the lower end of the 1–3 percent target band,the authorities eased monetary policy substan-tially during 2001; at the same time, the ex-change rate depreciated to near historically lowlevels in real effective terms, which is helping tocushion the impact of the external slowdownand weak commodity prices. Fiscal policy hasalso provided support through the operation ofthe automatic stabilizers, previous expenditureand tax measures, and a moderate discretionarystimulus in the 2001/02 budget. Aided by thepickup in the United States, growth reboundedin the fourth quarter of 2001, and economic in-dicators suggest that a strong recovery is now un-der way. With the economy expected to reach itspotential output sometime during the next year,the process of withdrawing monetary stimulusalso will likely need to begin in the near term.

Japan: Significant Challenges RemainJapan is experiencing its third—and most se-

vere—recession of the past decade. While theproximate causes of the current downturn in ac-

tivity include a variety of domestic and externalfactors, including falling consumer confidenceand the global slowdown, the inability to achievesustained growth over the past decade reflectsthe failure to deal decisively with deep structuralimpediments (a pattern also seen in other coun-tries, as discussed in Chapter III). This is mosturgent in the case of the banking system, whosedifficulties go back to the bursting of the assetprice bubble in the early 1990s.

Short-term prospects are a source of consider-able concern. Output is expected to fall by 1percent in 2002 after a decline of !/2 percent in2001, as the pronounced weakness in private de-mand seen in 2001 continues through the firsthalf of 2002 even as external demand revives, apath consistent with the results of the MarchTankan survey and the depressed levels of equityprices even after a recent rebound. To date, thefall in activity has been driven by both externaland domestic developments. Exports declined inthe face of the global slowdown and rapid fall indemand for IT goods. Consumption slumpedsince early 2001 as the unemployment rate hasset new records, overtime hours have fallen, andreal earnings have stagnated. Business invest-ment showed some resilience over much of2001, but weakened dramatically late in the year.The government announced a package to com-bat deflation late in February, including a re-statement of its intention to proceed with thedisposal of nonperforming loans (NPLs) and anexplicit commitment to take any necessary meas-ures to ensure the stability of the financial sys-tem. The package also sets out new measuressuch as strengthened regulation of short sellingof equities. While growth in 2002 could be morerapid than projected—most notably if recoverycomes more speedily in the rest of the world andthe IT cycle rebounds more rapidly than cur-rently anticipated—downside risks predominategiven the difficult domestic environment.

Weak growth over the 1990s reflects a failureto deal decisively with structural weaknesses, es-pecially in the banking system. Since the mid-1990s, bank equity prices have been falling rela-tive to the rest of the market (which has also

JAPAN: SIGNIFICANT CHALLENGES REMAIN

19

been on a downward trend, eroding bank capitalheld in the form of equities), and loans to theprivate sector have been declining (Figure 1.7,top panels). Despite past deregulation of the fi-nancial system—most notably the “big bang”completed in 2000—and its accomplishments sofar, the level of direct financing from capitalmarkets remains limited (Bank of Japan, 2001).These bleak trends have in many respects wors-ened since mid-2001, with NPLs remaining athigh levels despite large write-offs, the relativeequity prices of banks falling further (partly as aresult of recent regulatory actions imposinggreater market discipline on banks), increasingreal interest rates on bank loans, and, more re-cently, a significant increase in bank borrowingcosts for debentures and certificates of deposit,especially for weaker banks.

The banking sector will be a significant imped-iment to sustained recovery unless decisive actionis taken. Progress has been made in tacklingbanking sector reform and the allied issue of cor-porate restructuring. In particular, the FinancialServices Agency (FSA) has tightened NPL classifi-cations for banks and strengthened the role ofmarket forces through initiatives such as mark-to-market accounting. However, the FSA should fur-ther its efforts to encourage banking sector re-structuring through more accurate classificationof problem loans (where the FSA’s special auditswill be critical), rapid disposal of a wide range ofsuch loans (which will also help with corporaterestructuring), encouraging banks to raise fur-ther private capital, and, if appropriate, targetedinjections of public money. The basis for effectivecorporate restructuring has been laid through anumber of welcome initiatives, including the in-troduction of consolidated corporate taxationand reform of the commercial code, but rapiddisposal of problem loans and a more aggressiveindustrial deregulation policy are needed to pushthis process forward.

On the macroeconomic front, policymakerscurrently face the difficult task of supporting theimplementation of structural reforms in the faceof very limited room for monetary and fiscal ma-neuver. Monetary policy should be used aggres-

CHAPTER I ECONOMIC PROSPECTS AND POLICY ISSUES

20

30

50

70

90

110

130

150

Figure 1.7. Japanese Policy Dilemmas

Equity Price of Banking Sectorto Entire Market(January 1995 = 100; log scale)

Japan's financial problems are reflected in the falling relative equity price of the banking sector and in the decline in bank lending. Meanwhile, deflation is intensifying and real interest rates are rising. Current fiscal plans involve a significant withdrawal of stimulus later this year, while debt ratios continue to climb.

Sources: CEIC Data Company Limited; Nikkei Telecom; Nomura Security; and IMF staff estimates. Adjusted for changes in indirect taxes in 1997.

0

2

4

6

8

10Funding of the Private Sector (trillions of yen)

1993 95 97 99 Mar. 2002

-1

0

1

2

3

4

1993 95 97 99 Mar. 2002

1993 95 97 99 Dec. 2001

Realshort rate

Nominalshort rate

4

5

6

7

8

9

10

-30

-20

-10

0

10

20

30

40

50

60

1993 95 97 99 2001 03: Q1

Growth of public investment(right scale)

Structural deficit(left scale)

2

4

6

8

10

30

40

50

60

70

80

90

100General government deficit excluding social security

(left scale)