The Nature of Management Control Systems -...

72

The Nature of Management Control Systems

Transcript of The Nature of Management Control Systems -...

The Nature

of Management

Control Systems

Basic Concepts

• What does Control mean?

• Press the accelerator, – and your car goes faster.

• Rotate the steering wheel, – and it changes direction.

• Press the brake pedal, – and the car slows or stops.

• With these devices, – you control speed and direction;

• if any of them is inoperative, – The car does not do what you want it to.

• In other words, it is out of control

Basic Concepts

• An organization must also be controlled;

– that is, devices must be in place

• To ensure that its strategic intentions are

achieved.

– But controlling an organization

• is much more complicated than controlling a car.

• We will begin by describing

– the control process in simpler systems.

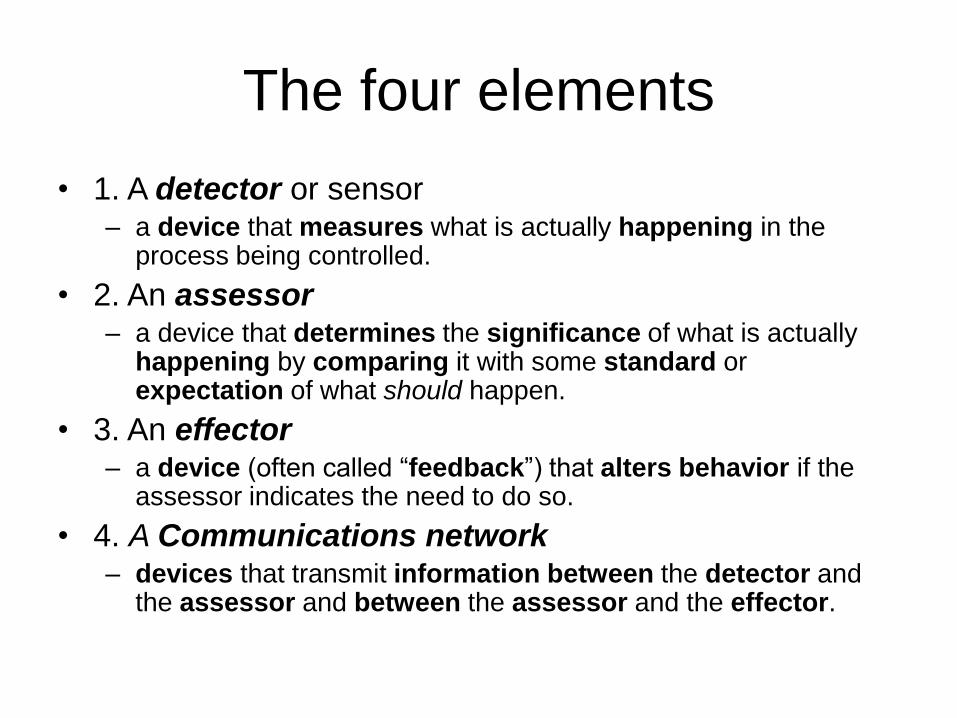

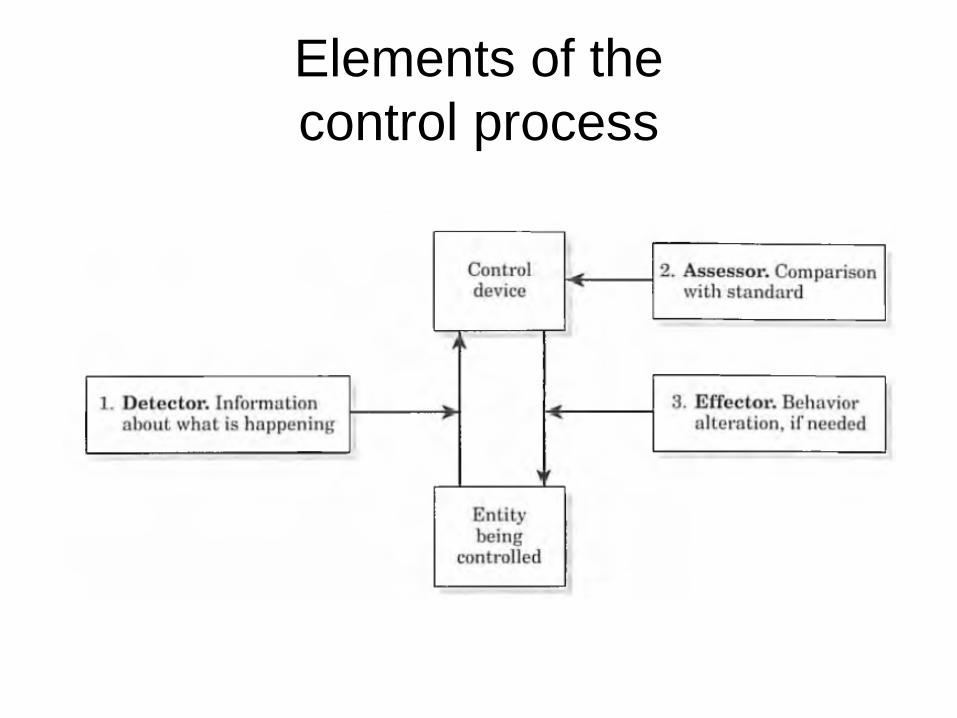

Elements of a Control System

Every control system has at least four

elements:

• 1. A detector

• 2. An assessor

• 3. An effector

• 4. A communications network

The four elements

• 1. A detector or sensor– a device that measures what is actually happening in the

process being controlled.

• 2. An assessor– a device that determines the significance of what is actually

happening by comparing it with some standard or expectation of what should happen.

• 3. An effector– a device (often called “feedback”) that alters behavior if the

assessor indicates the need to do so.

• 4. A Communications network– devices that transmit information between the detector and

the assessor and between the assessor and the effector.

Elements of the

control process

Examples

• Thermostat

• Body Temperature

• Automobile Driver

Management

• An organization consists of a group of

people

• who work together to achieve certain

common goals

– in a business organization a major goal is

to earn a satisfactory profit

hierarchy of managers

• Organizations are led by a hierarchy of

managers,

• with the chief executive officer (CEO) at

the top,

• and the managers of

– business units, departments, functions,

– and other subunits ranked below him or her

in the organizational chart.

Hierarchy in the organization

• The complexity of the organization

determines the number of layers in the

hierarchy.

• All managers other than the CEO are both

superiors and subordinates:

– they supervise the people in their own units,

– and they are supervised by the managers to

whom they report

The management control process

• The CEO– (or, in some organizations, a team of senior managers)

– decides on the overall strategies that will enable the organization to meet its goals.

• Subject to the approval of the CEO, – the various business unit managers formulate additional

strategies that will enable their respective units to further thesegoals.

• The management control process is the process by which managers at all levels – ensure that the people they supervise implement their

intended strategies

Contrast with Simpler Control

Processes

• The control process used by managers

contains

• the same elements as those in

• the simpler control systems described

earlier:

– detectors, assessors, effectors, and a

Communications system

Contrast with Simpler Control

Processes• Detectors

– report what is happening throughout theorganization;

• assessors– compare this information with the desired state;

• effectors– take corrective action once a significant difference

between the actual state

– and the desired state has been perceived;

• Communications system– Tells managers what is happening and how that

compares to the desired state

differences

• There are significant differences

between

• the management control process and

• the simpler processes described earlier:

Differences (1)

• Unlike in the thermostat or body temperature systems, the standard is not preset

• Rather, it is a result of a conscious planning process.

• The management decides what the organizationshould be doing,– and part of the control process is a comparison of actual

accomplishments with these plans.

• the control process in an organization involves planning.

• In many situations, – planning and control can be

• viewed as two separate activities.

• Management control– involves both planning and control.

Differences (2)

• Like controlling an automobile

• management control is not automatic.

• Some detectors in an organization may be

mechanical,

– but the manager often detects important

information

– with her own eyes, ears, and other senses

– because actions intended to alter an organization’s

behavior

– Man. Control involves human beings,

• the manager must internet with at least one other person

to effect change

Differences (3)

• Unlike controlling an automobile,

– a function performed by a single

individual,

– management control requires coordination

among individuals

• An organization consists of many

separate parts,

– management control must ensure that each

part works in harmony with the others

Differences (4)

• The connection from perceiving the need for

action to determining the action required to

obtain the desired result may not be clear.

• A manager

– acting as assessor

• may decide that “costs are too high”

• but see no easy or automatic action

guaranteed to bring costs down

– to what the standard says they should be.

Differences (4)

• The term black box describes

– an operation whose exact nature cannot be

observed

• Unlike the thermostat or the automobile driver,

– a management control system is a black box.

– We cannot know what action a given manager will

take

• when there is a significant difference between actual and

expected performance,

– nor what (she assesses, if any) action others will take

in response to the manager’s signal

Differences (5)

• Much management control is self-

control;

– control is maintained not by

• an external regulating device like the thermostat,

– But by managers

• who are using their own judgment

• rather than following instructions from a

superior.

Systems

Definition

• A system is a prescribed and usually

repetitious way of carrying out

– an activity or a set of activities

• Systems are characterized by a more or less

– rhythmic, coordinated, and recurring

– series of steps

• intended to accomplish a specified purpose.

• Examples:

– The thermostat

– the body temperature

management actions

• Many management actions are unsystematic.

• Managers regularly encounter situations– for which the rules are not well defined

– and thus must use their best judgment in deciding what actions to take.

• The effectiveness of their actions isdetermined– by their skill in dealing with people,

– not by a rule specific to the system

– (though the system may suggest the general nature of the appropriate response)

– If all systems ensured the correct action for all situations,

• there would be no need for human managers

Boundaries of Management

Control

planning and control

• we define management control

• and distinguish it from two

• other systems—or activities—

• that also require both planning and control:

– strategy formulation

– task control

management control

• management control fits between

strategy formulation and task control in

several respects

• Strategy formulation

– is the least systematic of the three,

• task control

– is the most systematic,

• and management control

– lies in between

management control

• Strategy formulation

– focuses on the long run,

• Task control

– focuses on short-run activities,

• and management control is in between.

• Strategy formulation

– uses rough approximations of the future,

• Task control

– uses current accurate data,

• management control is in between.

• Each activity involves

– both planning and control,

• but the emphasis varies with the type of activity

• The planning process

– is much more important in strategy

formulation,

• the control process

– is much more important in task control,

• and planning and control are of

approximately equal importance in

management control.

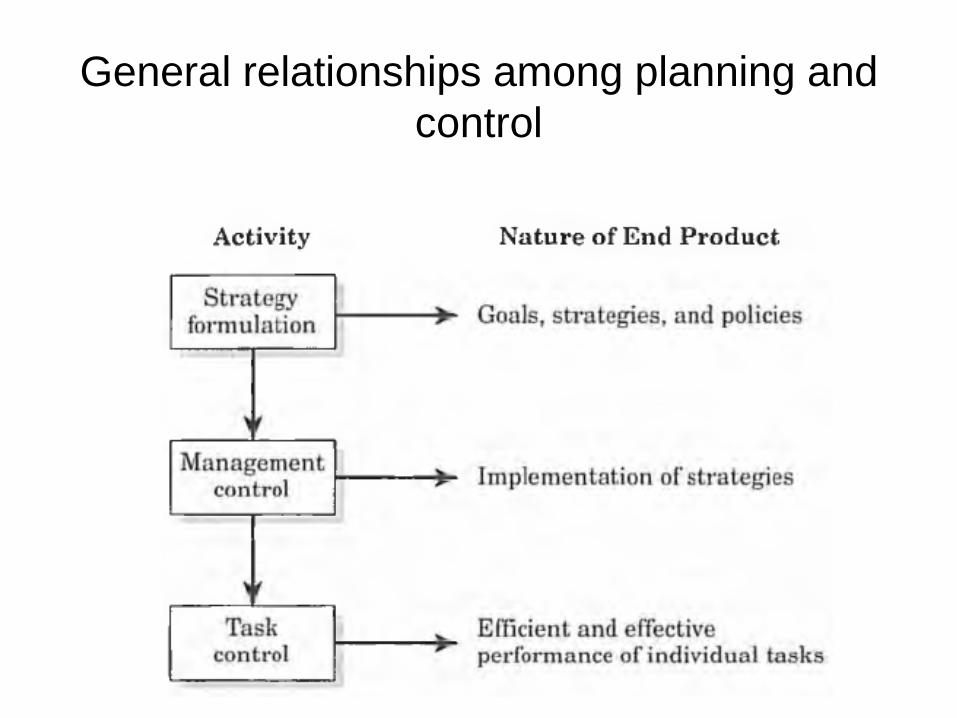

General relationships among planning and

control

Management Control Activities

• Planning what the organization should do.

• Coordinating the activities of several parts of the organization.

• Communicating information.

• Evaluating information.

• Deciding what, if any, action should be taken.

• Influencing people to change their behavior.

• Management control does not necessarily

require that all actions

– correspond to a previously determined plan,

• such as a budget.

• Such plans are based

– on circumstances believed to exist at the time

they were formulated

• If these circumstances have changed at the time of implementation,

• the actions dictated by the plan may no longer be appropriate.

• While a thermostat responds to the actual temperature in a room,

• management control involves

– anticipating future conditions to ensure that the organization’s objectives are attained

• If a manager discovers a better approach

– one more likely than the predetermined plan to

achieve the organization’s goals—

– the management control system should not obstruct

its implementation.

• In other words,

• conforming to a budget is not necessarily good,

• and departure from a budget is not necessarily

bad.

Goal Congruence

• Although systematic, the management

control process is by no means

mechanical;

• it involves interactions among individuals,

which cannot be described in mechanical

ways.

• Managers have personal as well as

organizational goals.

Goal Congruence

• The Central control problem is to induce them to

act in pursuit of their personal goals in ways that

will help attain the organization’s goals as well.

• Goal congruence means that,

– the goals of an organization’s individual members

should be consistent

– with the goals of the organization itself.

• The management control system should be

– designed and operated with the principle of goal

congruence in mind.

Tool for Implementing Strategy

• Management control systems help managers

– move an organization toward its strategic objectives.

• Thus, management control focuses primarily on

strategy execution.

• Management Controls are only one of the tools

– managers use in implementing desired strategies.

• strategies are also implemented

– through the organization’s structure, its management

of human resources, and its particular culture.

Framework for strategy implementation

Framework for strategy implementation

• Organizational structure – specifies the roles, reporting relationships, and

division of responsibilities that shape decision-making within an organization.

• Human resource management – is the selection, training, evaluation, promotion, and

termination of employees so as to develop the knowledge and skills required to execute organizational strategy.

• Culture refers – to the set of common beliefs, attitudes, and norms

that explicitly or implicitly guide managerial actions.

Financial and Nonfinancial

Emphasis

• Management control systems encompass

– both financial and nonfinancial performance

measures.

• The financial dimension focuses on the

monetary “bottom line”—

– net income, return on equity, and so forth.

• virtually all organizational subunits have

nonfinancial objectives—

– product quality, market share, customer satisfaction,

on-time delivery, and employee morale.

Aid in Developing New Strategies -

interactive control

• the primary role of management control is to ensure the execution of chosen strategies.

• In industries that are subject to rapid environmental changes,

– management control information,

– especially of a nonfinancial nature

• can also provide the basis for considering new strategies

Interactive control

Interactive control

• Interactive control calls management’s attention to developments

• both negative– (e.g., loss of market share, customer complaints)

• and positive – (e.g., the opening up of a new market as a result of

the elimination o f certain government regulations)

• that indicate the need for new strategic initiatives.

• Interactive Controls – are an integral part of the management control

system.

Strategy Formulation

• is the process

• of deciding on the goals of the organization

• and the strategies

– for attaining these goals

• Goals are timeless; they exist until they are

changed, and they are changed

• only rarely

Strategy Formulation

• For many businesses, earning a

satisfactory return on investment is an

important goal;

– for others, attaining a large market share is

equally important.

• Nonprofit organizations also have goals;

– they seek to provide the maximum services

possible with available funding.

Strategy

• In the strategy formulation process,

• the goals of the organization are usually

taken as a given,

• although on occasion

• strategic thinking

– can focus on the goals themselves.

Strategies

• Strategies are big plans, important plans.

• They state in a general

– way the direction in which senior

management wants the organization to move.

• A decision by an automobile manufacturer

– to produce and sell an electric automobile

– would be a strategic decision

Strategies

• The need for formulating strategies usually

arises in response to a perceived

• threat (e.g., market inroads by competitors, a

shift in consumer tastes, or new

• government regulations) or opportunity (e.g.,

technological innovations, new

• perceptions of customer behavior, or the

development of new applications for

• existing products).

Strategies

• A new CEO,

– especially one brought in from the outside,

• usually perceives both threats and

opportunities

– differently from how his or her predecessor

did

• Thus, changes in strategies often occur

when a new CEO takes over

Strategies

• Strategies to address a threat or opportunity

– can arise from anywhere in an organization and at

any time

• New ideas do not emanate solely from the

• research and development team or the

headquarters staff.

• Virtually anyone might come up with a “bright

idea,”

– which, after analysis and discussion, can form the

basis for a new strategy.

strategy formulation

• Complete responsibility for strategy

formulation

– should never be assigned to a particular

person or organizational unit.

• Providing a means of bringing worthwhile

ideas directly to the attention of senior

management

– without allowing them to be blocked at lower

levels is important

Distinctions between Strategy

Formulation and Management

Control

• Strategy formulation

– is the process of deciding on new strategies;

• Management control

– Is the process of implementing those strategies.

• From the standpoint of systems design,

– the most important distinction between strategy

formulation and management control

• is that strategy formulation is essentially

unsystematic

strategic decisions

• Threats, opportunities, and new ideas

– do not occur at regular intervals;

• thus,

• strategic decisions may be made at any

time

Strategic analysis

• the analysis of a proposed strategy varies with

the nature of the strategy.

• Strategic analysis involves

– much judgment,

– the numbers used in the process are usually rough

estimates

• the management control process involves

– a series of steps that occur in a predictable sequence

according to a more-or-less fixed timetable

– and with reliable estimates

Strategy vs. management control

• Analysis of a proposed strategy usually

involves relatively few people

• The sponsor of the idea, headquarters

staff, and senior management.

• the management control process involves

– managers and their staffs

– at all levels in the organization

Task Control

• Task control is the process

– of ensuring that specified tasks are carried out

effectively and efficiently

• it is transaction-oriented

– it involves the performance of individual tasks

according to rules established in the

management control process

Task Control

• Task control often consists of seeing that

these rules are followed,

• A function that in some cases does not

– even require the presence of human beings

• Numerically controlled machine tools,

• process control computers,

• and robots

– are mechanical task control devices

Task Control

• Their function involves humans only

– when the latter prove less expensive or more

reliable;

• this is likely to happen only if

– unusual events occur so frequently that

programming a computer

– with rules for dealing with these events is not

worthwhile

Task Control

• Many task control activities are scientific

• the optimal decision or the appropriate action

– for bringing an out-of-control condition back to the desired state is predictable within acceptable limits.

• the rules for economic order quantity

– determine the amount and timing of purchase orders

Task Control

• Most of the information in an organization

is task control information:

– The number of items ordered by customers,

– the pounds of material and units of

components used in the manufacture of

products,

– The number of hours employees work,

– the amount of cash disbursed

Task Control

• Many of an organization’s central activities

– including procurement, scheduling, order

entry, logistics, quality control, and cash

management

• are task control systems

• Some of them, though mechanical, can be

extremely complicated

Distinctions between Task Control

and Management Control

• many task control systems are scientific,

• whereas management control

– can never be reduced to a Science.

• management control involves

• the behavior of managers,

• and this cannot be expressed by

equations

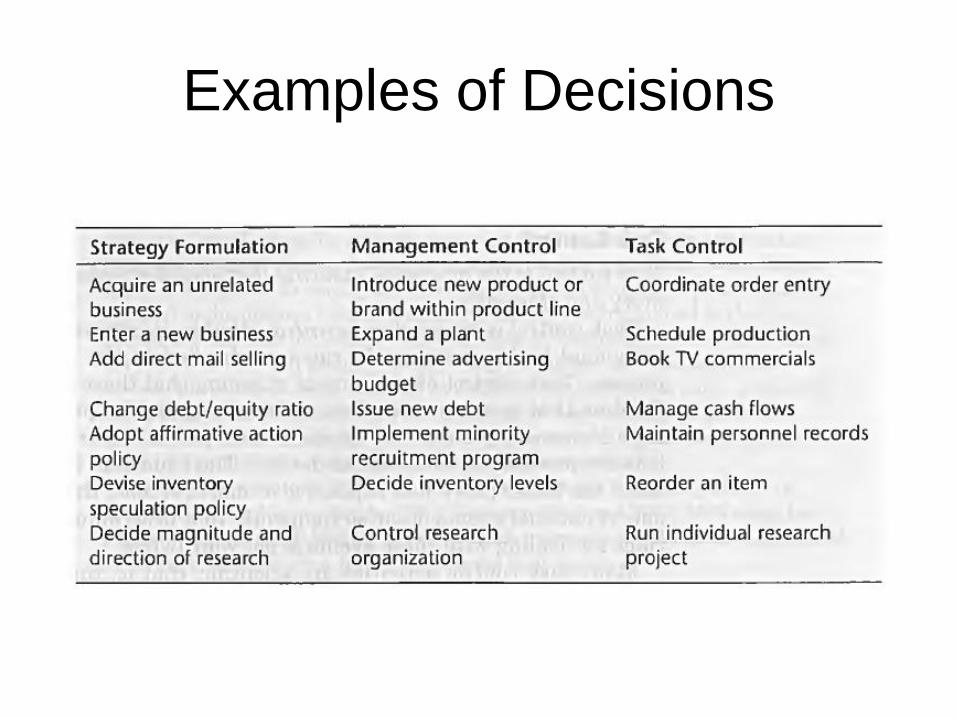

Examples of Decisions

Distinctions between Task Control

and Management Control

• Serious errors may be made when principles developed by management scientists – for task control situations are applied to management

control situations

• In management control,

• managers interact with other managers;

• In task control, – either human beings are not involved at all

– (as in some automated production processes),

• or the interaction is between a manager and anonmanager

Distinctions between Task Control

and Management Control

• In management control

– the focus is on organizational units;

• in task control

– the focus is on specific tasks performed by

these organizational units

– (e.g.,manufacturing Job No. 59268, or

ordering 100 units of Part No. 3642)

Distinctions between Task Control

and Management Control

• Management control is concerned with the

broadly defined activities of managers

deciding

– what is to be done within the general

constraints of strategies.

• Task control relates

– to specified tasks, most of which require little

or no judgment to perform.

Impact of the Internet on

Management Control

• The pace of the information revolution

accelerated

– with the invention of computers,

– gaining tremendous momentum in the 1990s

with the advent of the Internet

The Internet provides major

benefits, such as:

• Instant access

• Multi-targeted communication

• Costless communication

• Ability to display images

• Shifting power and control to the individual

Impact of the Internet

• With these advantages the Internet has

changed the rules of the game in the

business-to-individual consumer sector

• The Internet has also changed business-

to-business commerce

• The impact of the Internet on the world of

business has been significant

the Internet’s impact on

management Controls• Management control systems involve information, and

organizations require an infrastructure to process that information.

• The Internet provides that infrastructure, – making the processing of information easier and faster, with

fewer errors.

• On the Web, a manager can collect huge amounts

• of data, store that data, analyze it in different forms, and send it to anyone in the organization.

• Managers can also use this information – to customize and personalize their reports

the Internet’s impact on

management Controls

• The Internet facilitates coordination and control – through the efficient and effective processing of

information,

• but the Internet cannot substitute for – the fundamental processes that are involved in

management control.

• This is because

• implementing strategies through management Controls – is essentially a social and behavioral process and

thus cannot be fully automated

the Internet’s impact on

management Controls

• although the Internet has vastly improved

information processing,

• the fundamental elements of management

control

– what information to collect and how to use it

• are essentially behavioral in nature and

thus not

• amenable to a formula approach