Working Capital Management - unideb.huoktato.econ.unideb.hu/domician/Downloads/ppt/C18b_new.pdfof...

27

Copyright © 2011 Pearson Prentice Hall. All rights reserved. Working Capital Management Chapter 18

Transcript of Working Capital Management - unideb.huoktato.econ.unideb.hu/domician/Downloads/ppt/C18b_new.pdfof...

Copyright © 2011 Pearson Prentice Hall. All rights reserved.

Working Capital Management

Chapter 18

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-2

Slide Contents

• Learning Objectives

• Principles Used in This Chapter

1. Working Capital Management and the Risk-Return Tradeoff

2. Working Capital Policy

3. Operating and Cash Conversion Cycle

4. Managing Current Liabilities

5. Managing the Firm’s Investment in Current Assets

• Key Terms

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-3

Learning Objectives

1. Describe the risk-return tradeoff involved in managing a firm’s working capital.

2. Explain the principle of self-liquidating debt as a tool for managing firm liquidity.

3. Use the cash conversion cycle to measure the efficiency with which a firm manages its working capital.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-4

Learning Objectives (cont.)

4. Evaluate the cost of financing as a key determinant of the management of a firm’s use of current liabilities.

5. Understand the factors underlying a firm’s investment in cash and marketable securities, accounts receivable, and inventory.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.

18.4 Managing Current Liabilities

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-6

Managing Current Liabilities

Current Liabilities

(debt obligations to be

repaid within one year)

Unsecured current liabilities

(trade credit, unsecured bank loans, commercial

paper)

Secured current liabilities

(loans secured by specific assets like inventories or

accounts receivable)

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-7

Calculating the Cost of Short-term Financing

• When evaluating alternative sources of financing, it is critical to consider the cost. The cost of short-term credit is given by:

• Interest = principal × rate × time

7

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-8

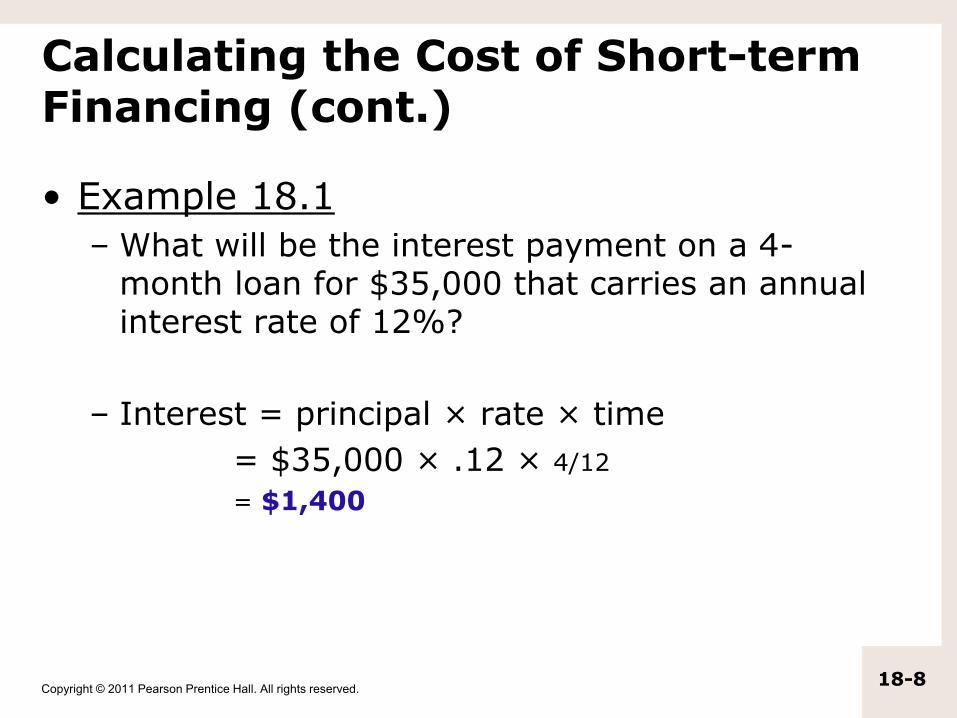

Calculating the Cost of Short-term Financing (cont.)

• Example 18.1

– What will be the interest payment on a 4-month loan for $35,000 that carries an annual interest rate of 12%?

– Interest = principal × rate × time

= $35,000 × .12 × 4/12

= $1,400

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-9

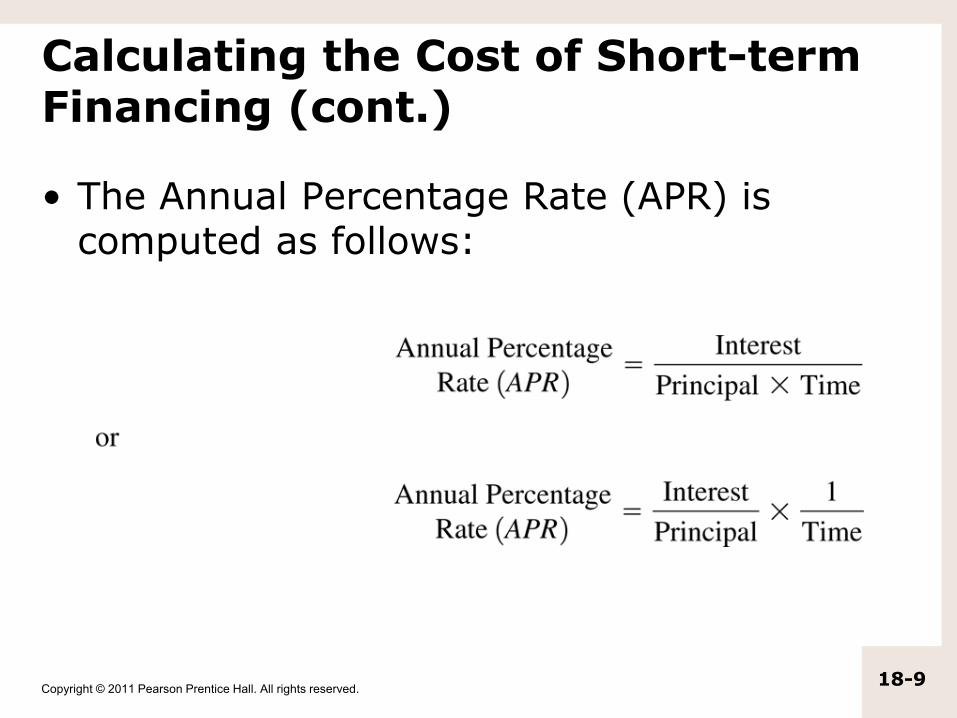

Calculating the Cost of Short-term Financing (cont.)

• The Annual Percentage Rate (APR) is computed as follows:

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-10

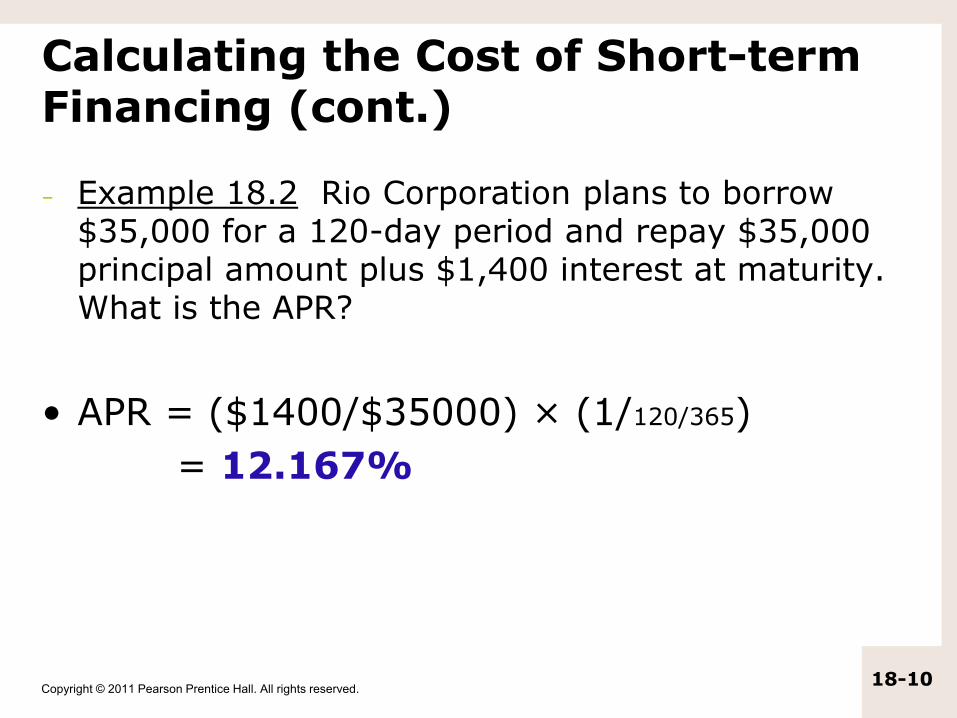

Calculating the Cost of Short-term Financing (cont.)

– Example 18.2 Rio Corporation plans to borrow $35,000 for a 120-day period and repay $35,000 principal amount plus $1,400 interest at maturity. What is the APR?

• APR = ($1400/$35000) × (1/120/365)

= 12.167%

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-11

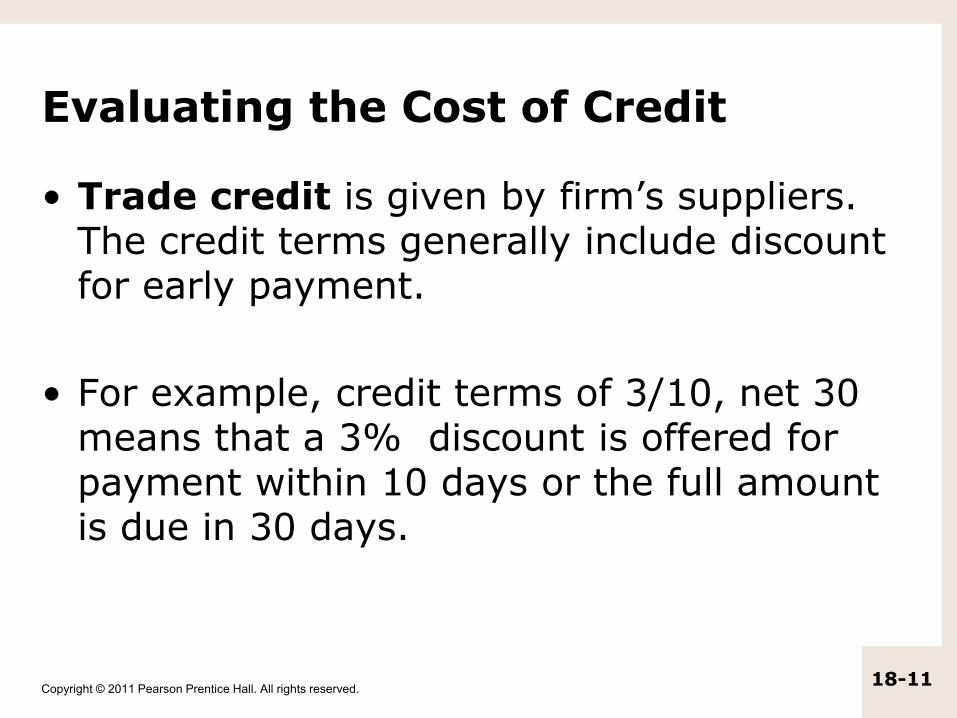

Evaluating the Cost of Credit

• Trade credit is given by firm’s suppliers. The credit terms generally include discount for early payment.

• For example, credit terms of 3/10, net 30 means that a 3% discount is offered for payment within 10 days or the full amount is due in 30 days.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-12

Evaluating the Cost of Bank Loans

• We can apply equation 18-8 (APR) to estimate the cost of bank loans also.

• However, firms generally borrow money from bank by creating a line of credit.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-13

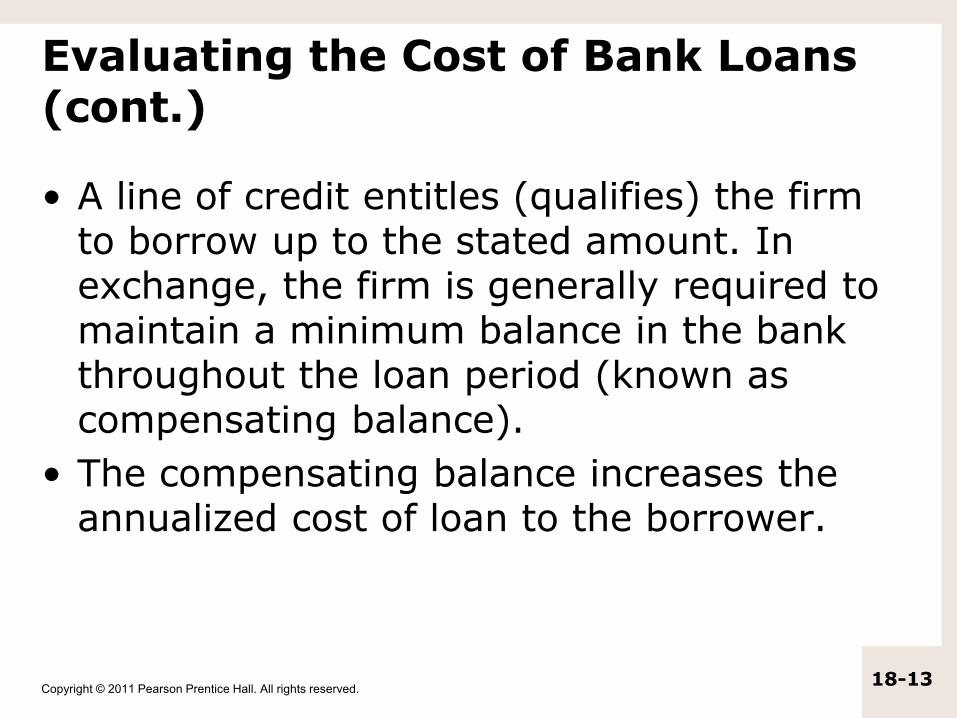

Evaluating the Cost of Bank Loans (cont.)

• A line of credit entitles (qualifies) the firm to borrow up to the stated amount. In exchange, the firm is generally required to maintain a minimum balance in the bank throughout the loan period (known as compensating balance).

• The compensating balance increases the annualized cost of loan to the borrower.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.

18.5 Managing the Firm’s Investment in Current Assets

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-15

Managing the Firm’s Investment in Current Assets

• The primary types of current assets that most firms hold are:

–Cash,

–Marketable securities,

–Accounts receivable, and

–Inventories.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-16

Cash and Marketable Securities

• Cash and marketable securities are held to pay the firm’s bills on a timely basis.

• Holding too little cash and marketable securities could lead to default.

• However, holding excessive (exaggarated)cash and marketable securities is costly since they earn little, or very low rates of return.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-17

Cash and Marketable Securities (cont.)

• There are two fundamental problems of cash management:

1. Keeping enough cash on hand to meet the firm’s cash requirements on a timely basis.

2. Managing the composition of the firm’s marketable securities portfolio.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-18

Cash and Marketable Securities (cont.)

• Problem #1: Maintaining a Sufficient Balance

• To maintain an adequate balance requires an accurate forecast of firm’s cash receipts(income) and disbursements (expenses of amounts paid for goods and services).

This is accomplished through a cash budget.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-19

Cash and Marketable Securities (cont.)

• Problem #2: Managing the composition of the firm’s marketable securities portfolio

• Firms prefer to hold cash reserves in money market securities as it can be easily and quickly converted to cash at little or no loss. These securities mature in less than 1 year, have low or no default probability, and are highly liquid.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-20

Managing Accounts Receivable

• Whenever a sale is made on credit, it increases the firm’s account receivable balance. Cash flow from sales cannot be invested until accounts receivable are collected.

• Efficient collection policies and procedures will improve firm profitability and liquidity.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-21

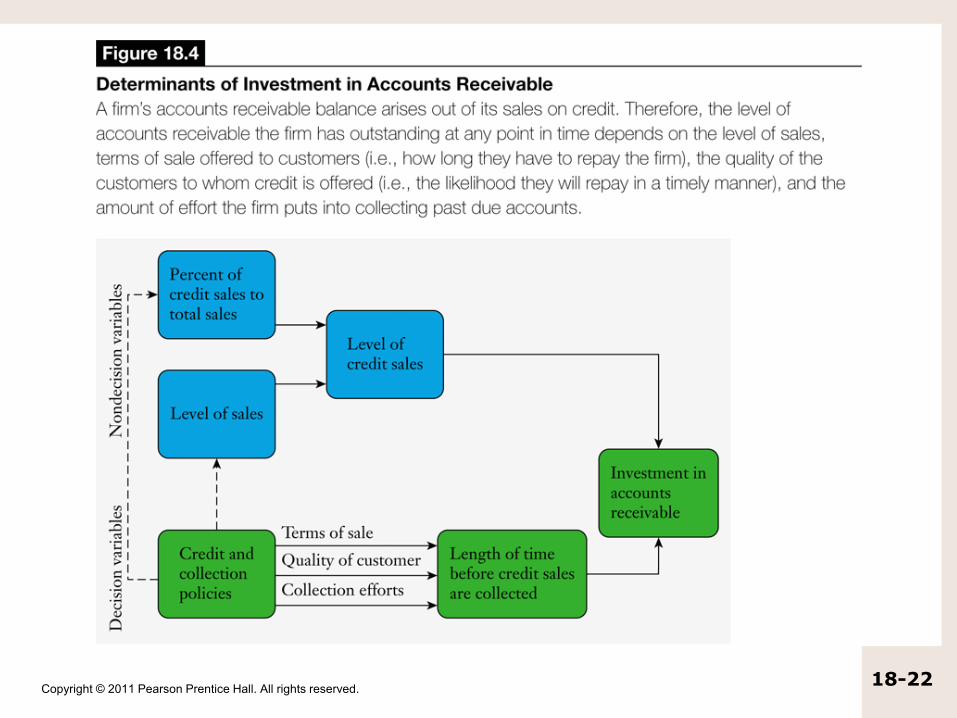

Determinants of the Size of a Firm’s Investment in Accounts Receivable

1. The level of credit sales as a percentage of sales. This percentage will vary with the type of business.

2. The level of sales. Higher the sales, greater the accounts receivable.

3. The credit and collection policy.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-22

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-23

Terms of Sale

• Terms of sale identify the possible discounts for early payment, the discount period, and the total credit period.

• It is generally stated in the form a/b, net c. For example 1/10, net 30, means the customer can deduct 1% if paid within 10 days, otherwise the account must be paid within 30 days.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-24

Customer Quality

• It is important to determine the type of customer who should qualify for trade credit. It is critical to understand the customer’s short-run financial well being.

• As the quality of customer declines, it increases the costs of credit investigation, default costs, and collection costs.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-25

Customer Quality (cont.)

• To determine customer quality, firm can analyze the liquidity ratios, other obligations (liabilities), and overall profitability of the firm.

• The firm can also obtain information from credit rating services such as Dun & Bradstreet that provide information on the financial status, operations, and payment history for most firms.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-26

Customer Quality (cont.)

• Credit score is also a popular way to evaluate the credit risk of individuals and firms.

• Credit score is a numerical evaluation of each applicant based on the applicant’s current debts and history of making payments on a timely basis.

Copyright © 2011 Pearson Prentice Hall. All rights reserved.18-27

Collection Efforts

• Control of accounts receivables focuses on the control and elimination of past-due receivables.

• This can be done by analyzing various ratios such as average collection period, the ratio of receivables to assets, accounts receivable turnover ratio, and the amount of bad debt relative to sales over time.