The Digital Insurer: Accenture 2013 Consumer-Driven Innovation Survey: Playing to win

29

Insurers must raise their game to attract and retain customers, and turn the “switching economy” from a risk into an opportunity— and a pathway to high performance. The Digital Insurer Accenture 2013 Consumer-Driven Innovation Survey Playing to win

-

Upload

accenture-insurance -

Category

Economy & Finance

-

view

1.329 -

download

2

Transcript of The Digital Insurer: Accenture 2013 Consumer-Driven Innovation Survey: Playing to win

Insurers must raise their game to attract and retain customers, and turn the “switching economy” from a risk into an opportunity—and a pathway to high performance.

The Digital InsurerAccenture 2013 Consumer-Driven Innovation Survey

Playing to win

2

Huge opportunity as customers switch to insurers that are playing to win their loyalty

Customers are more demanding than ever. Those who don’t get what they want can switch providers—which is easier than ever. This dynamic represents a huge potential loss of revenue for insurers that fail to retain their customers, and a huge equivalent opportunity for those that can offer dissatisfied customers what they’re looking for. We call it the “switching economy,” and it was worth as much as $400 billion in 2013.

In a market in which most carriers have been playing to avoid losing, a few leaders have adopted a “play to win” strategy. The key features of this strategy are their authentic customer-centricity, the provision of more relevant and personalized products and services, and the exploitation of digital technologies to meet their customers’ rising expectations.

In a volatile and increasingly commoditized market, insurers that play to win will be the ones that benefit from the switching economy—at the expense of their more conservative competitors that persist with a defensive strategy.

3

The 2013 Accenture Consumer-Driven Innovation Survey clearly demonstrates that insurance customers want more relevant, convenient and cost-efficient products and experiences. This research is borne out by the global, cross-industry 2013 Global Consumer Pulse Research (see “About the research” on page 10). These studies also show customers are prepared to switch providers if they don’t get what they’re looking for.

Despite the widely acknowledged upsurge in expectations, Figure 1 shows that most insurers have failed to respond by giving customers what they want.

The fact is that most customers will tolerate sub-standard, impersonal service—until the moment when their provider is called on to do what it is paid to do. This “moment of truth” may be a renewal, a claim, the provision of advice on a new need, or simply the administration of changes to a policy. These are the trigger events which, if not managed efficiently and with sensitivity, may well cause the customer to defect to a new provider.

The likelihood that a poorly managed interaction will trigger a switch is increased by the current high volume of aggressive price-focused advertising designed to erode customers’ confidence in their choice of insurance provider. It has the effect of reducing loyalty (Figures 2 & 3) and downplaying the difficulty of switching providers.

As a result, one of the commanding features of the current insurance landscape is the high proportion of such events likely to occur in the next 12 months (see Figure 4).

How real is the threat? A direct consequence of insurers’ inability to reinforce customer loyalty, according to the Accenture 2013 Consumer-Driven Innovation Survey, is that 40 percent are likely to switch to a new provider for their auto and home insurance in “the next 12 months” (Figure 2).

Figure 2. Customer retention is a major challenge for P&C insurers

Q: How likely are you to stop doing business with one of your auto and home insurance providers and switch to another provider in the next 12 months?

Very likelySomewhat likelyNot very likelyVery unlikely40%

9%

31%

23%

37%

Home and auto insurance

Figure 1. Over the past five years, insurers have been unable to improve customer attitudes

50%

0%2009 2010 2011 2012 2013

Questions:

Percentage of respondents who scored insurers 1 – 3 on a 10-point scale where 1 = “Not at all”

Are you satisfied? Would you recommend to others?Do you feel loyal? Will you buy more?

4

The findings for life insurance (Figure 3) show that this line of business is less volatile; nonetheless, seven percent of customers are very likely to stop doing business with one of their insurance providers in the next 12 months, and 10 percent will take out a new contract with a new provider.

Using the findings of this study, Accenture has calculated1 that there was potentially up to $400 billion in revenue “in play” globally in 2013 as personal-lines P&C and life insurance customers chose to switch providers.

We call it the switching economy, because it represents existing premium income that is up for grabs by those insurers that are best placed to meet customers’ demands. The dramatic success of direct online carriers in increasing their share of the US auto insurance market is one example; others are the rapid ascent to dominance of auto insurance aggregators in the United

Kingdom, the strong interest in usage-based insurance in many parts of the world, and the advent of numerous online businesses that offer innovative services specifically designed to meet customers’ changing needs (see sidebar, “Bold new ventures capture customers”).

In addition to competing for new business, insurers are thus engaged in a fierce battle to prevent their existing customers from being seduced by lower premiums and a wide array of new and appealing offers.

Until now, as the depressingly flat lines in Figure 1 confirm, most insurers have been treading water, essentially playing to avoid losing. This only works as long as all competitors adopt the same strategy. But clearly this isn’t the case. To compete effectively for the switching economy—and to prevent their own customers from defecting—insurers have no choice but to play to win.

Figure 4. A significant proportion of customers are planning to renew or purchase insurance

Q: Do you plan to purchase or renew at least one of your insurance products in the next 12 months?

RenewPurchase a new productI do not plan to purchase or renew insurance products

72%

58%

14%

28%

Figure 3. Churn is lower in life than in P&C insurance, but at least 1 in 10 customers are likely to defect to a new provider

Q: How likely are you, in the next 12 months, to do the following things with regard to life insurance?

Very likelySomewhat likelyNot very likelyVery unlikely

27%

6%

21%

36%

37%

35%

10%

25%

33%

32%

36%

10%

26%

32%

32%

45%

26%

29%

24%

21%

25%

7%

18%

39%

36%

Life insurance

Stop contributing to an existing contract but keep it in force

Take out a new contract with a new provider

Take out a new contract with a current provider

Renew an existing contract which is due to expire

Cancel an existing contract

5

While many insurers persist with a defensive strategy of playing to avoid losing, others have achieved notable success with more aggressive approaches that take advantage of digital innovation to offer customers better prices or more relevant services—or both.

The rapid growth of GEICO, Progressive and USAA’s direct online auto insurance businesses in the United States is well documented, as is the stunning growth of price comparison sites in the United Kingdom, which are estimated to influence more than half of all new motor insurance sales.

Recognizing that price—or value for money—is a key driver of switching, many players have launched radical offers that customers find hard to resist. Progressive’s Name Your Price is an online tool that collects basic information from prospective customers, including their auto insurance “budget.” It recommends a package that matches this budget, and then allows the customer to adjust the price, adding or removing insurance features to create a tailored package that achieves the best balance of suitability and affordability.

A different approach to making auto insurance affordable is the telematics concept offered by the UK online carrier Insurethebox. Customers buy miles of coverage in advance. They then allow their car usage to be monitored by an onboard

device, and top up their insurance when their miles run low. They are rewarded with bonus miles for safe driving, and for purchasing any of a wide variety of goods from the insurer’s ecosystem of retail partners. Retention is strengthened by the customers’ perception that their insurance is priced specifically for them, as well as by the appeal of the loyalty program.

Price matters a great deal in the life sector too, where novel start-ups are using digital technology to lure customers who are loath to pay the fees many advisors charge. FutureAdvisor invites clients to supply all of their financial data and sufficient personal data to create unique investment profiles. Its software program applies investment best practices to its customers’ investment portfolios, sending them regular impartial recommendations for optimizing their portfolios. This service is free. Customers only pay when they commission FutureAdvisor to carry out the changes on their behalf, which they are only likely to do if and when the advice proves to be sound.

While price is a major factor behind switching, it is certainly not the only one—a Datamonitor survey2 found that only 37 percent of respondents who bought auto insurance from a UK comparison site selected the lowest quote. Reputation, flexibility, convenience, personalized advice and innovation are just a few of the factors that influence the choice.

Bold new ventures capture customers

6

Time to play to win

The majority of insurance customers across both P&C and Life are poised to renew an existing product or buy a new one—a moment-of-truth milestone that can often act as a prompt to switch (Figure 4).

As mentioned earlier, four out of 10 are likely to switch P&C providers while one out of 10 will probably turn to a new life provider.

Consumers have certainly shown their propensity to change their behavior in other ways relating to insurance: their use of different channels (Figure 5) and their willingness to buy online (Figure 6) are just two of the more important trends.

In addition, regulatory regimes in many European countries now favor consumer choice (and thus switching) by preventing automatic renewal of policies and standardizing no-penalty cancellations.

In short, insurance customers are predisposed to switch. They will also, over the course of the next year, continue to experience a number of “moments of truth” which will cause them to evaluate their providers against the standards they have set for them. These standards will increasingly be suggested by the experiences they receive from providers in other industries.

In the face of low customer satisfaction and loyalty, and a disinclination to recommend and buy more, few insurers are likely to score well in such an evaluation.

What must never be forgotten in assessing what factors will trigger a customer to switch is the eternal quest for a better price or higher value. In P&C insurance, price and value for money are the stated reason for 45 percent of all switches. These were also the key drivers for switching in life insurance in 2012.3 Increasingly, though, price and value for money are likely to become integrated into how the total customer experience is rated.

In turn, innovation will become increasingly important, not only to help insurers keep pace with customer expectations but also to meet the challenge of providing better value for money. (See the sidebar on page 5, “Bold new ventures capture customers,” for an exploration of how price interacts with other variables in the switching economy.)

Only one conclusion is possible: the time for defensive strategies is over. Insurers now need to take decisive action to retain their existing customers—who are typically more profitable and who are candidates for additional products and services—and to position themselves to attract the disaffected customers of their competitors. The switching economy is thus a great opportunity but also a great risk.

One thing is clear: it’s time to play to win.

Figure 5: In the past two years, more customers have turned to digital channels when buying insurance

Q: When did you first purchase insurance through the following channels?

Less than 2 years agoMore than 2 years ago

Channels used for over 2 years Most recent channels

Your employer OnlineRetailerInsurance companytelephone service

BankInsurance agentIndependent agent / broker

62%

38%

60%

40%

57%

43%

52%

48%

39%

61%

39%

61%

38%

62%

7

of customers are willing to purchase insurance online

Figure 6. To meet customers’ changing expectations, insurers must accommodate their growing preference for digital channels

Q: Which products would you be willing to purchase online?

71% would be interested in buying at least one of theseproducts online

23%

26%

30%

34%

35%

35%

40%

21%

12%

Spectacles and lens insurance

Winter sports insurance

Travel and assistance insurance

Extended warranty

Home insurance

Long-term car insurance

Life insurance

Short-term car insurance

Event ticket cancellation

of insurance premiums are in play in 2013

of P&C customers are likely to stop doing business with a current provider and switch to a new one in the next 12 months

40%$400bn

72% 71%

1 in 10life customers are likely to defect to a new provider in the next 12 months

of insurance customers are planning to renew or purchase insurance in the next year

8

While price continues to play the major role in triggering this switching behavior, as noted above, the massive switching economy in insurance is increasingly being driven also by changing customer dynamics enabled by digital technologies.

Digital is playing a key role in making it easier for customers to research alternative providers’ value propositions, and promoting the “click and change” mentality that already pervades retail.

Today’s customers are empowered by technology and are demanding that the personalization provided by leading companies in one sector be replicated in other sectors, including insurance. They’re looking for a set of experiences that are convenient and relevant to their specific circumstances. Insurance customers, in line with consumers across all industries, regard themselves less and less as purchasers of products, and more and more as architects of the lifestyle to which they aspire.

Figure 7 shows that a high proportion of insurance customers want a more personalized service from their carriers.

It’s also important to understand that while customers move at different speeds, the vast majority of them are using digital channels for at least some transactions. Even “traditional” customers are using online facilities to research their choices. The growth in the convenience and functionality—and the widespread adoption—of mobile devices like smartphones and tablets is driving this trend.

Accenture believes that digital technologies and analytics are now mature enough to permit insurers to deliver relevant, personalized experiences at scale, using the channels preferred by the customer. This channel, for many interactions, is likely to be the agent, so a key part of digital transformation must include enhancing the agent experience.

Customers’ desire for different, more convenient experiences takes various forms: 71 percent are ready to purchase products and services online (Figure 6), and well over one in three of those with mobile devices have used them to deal with their insurer in the past two years—37 percent have used

their phones and 46 percent their tablets (Figure 8). Almost half of all respondents depend on comments on social media to make their insurance-buying decisions (Figure 9).

Now that every customer is a digital customer, a new sales dynamic is developing. Whereas the path to purchase used to be linear—the traditional “sales funnel”—it’s now a dynamic, iterative, reinforcing process, which Accenture represents in its Dynamic Customer Experience Model (Figure 10). As noted above, it’s a process that the customer now largely controls. Companies that are playing to win recognize that today’s customers will define their own experiences based on their personal expectations and the lifestyle they want.

However, as the research makes clear, companies across sectors have fallen short in responding to this challenge, and insurance is no exception (Figure 1).

To respond to this new model, and improve the customer metrics that drive switching, insurers need to become much more customer-centric. Customer-centricity in this dynamic environment is only achievable through digital transformation, Accenture believes.

Every customer is a digital customer

Figure 7. Most customers would switch to an insurer that provided personalized services

Q. How important would a personalized service be in your decision to stop doing business with your current provider or switch to another in the next 12 months?

Very importantSomewhat importantNot very importantNot important at all

80%

30%

50%

14%

6%

Figure 8. Mobile devices are becoming increasingly popular for interacting with insurers

Q: Have you used your mobile device in the past two years to deal online with your insurer?

Base: respondents who own a mobile phone, and own a tablet.

Yes – my mobile phone

To update your personal details

To get information on insurance products & services

To get advice

To apply for/ purchase an insurance product or service

To make a claim

To obtain a quote

37% have used their mobile phone for at least one of these interactions

Yes – my tablet

14%

20%

19%

25%

9%

10%

46% have used their tablet for at least one of these interactions

13%

15%

16%

21%

7%

9%

9

Figure 9. Almost half of all customers rely on comments on social media to make their insurance buying decisions

Q: If you were to consider buying insurance, how important would the comments and recommendations on social media sites be in helping you decide which product and provider to choose?

Very importantSomewhat importantNot very importantNot important at all48%

14%

34%

27%

25%

Figure 10. The customer’s path to purchase used to be linear; now, the journey is dynamic, accessible and continuous

From the traditional sales funnel... ... to the Accenture Dynamic Customer Experience Model

Discover

Evaluate

Purchase

Use

Consider

Evaluate

Discover

Consider

Purchase

Use

Expectation

Promise

Reality

Delivery

Open content & channels Branded content & channels

Influence of “open” content is pervasive and difficult to control

Accessible

Paths are multi-directional at different speeds

Dynamic

Evaluation, not purchase, is central; promise is more important than delivery

Continuous

of customers rely on comments on social media to buy insurance

of insurance customers say that personalized service would play a major role in switching providers

80%

46%

48%

of customers with tablets, and 37% of those with mobile phones, have used these devices to deal with their insurers

Figure 11. The Accenture 2013 Consumer-Driven Innovation Survey

6,135 insurance policy holders were surveyed online in 11 countries in July 2013

Countries

USA1,012 (19%)

Italy520 (9%)

Brazil516 (8%)

Japan512 (8%)

France511 (8%)

UK511 (8%)

Spain511 (8%)

Germany510 (8%)

China510 (8%)

Canada511 (8%)

South Africa511 (8%)

Total: 6,135 (100%)

Respondent age

18-24 years 818 (13%)

(19%)

(23%)

(23%)

(22%)

Respondent gender group

Men3,070

(50%)

Women3,065

(50%)

25-34 years 1,424

1,386

1,316

1,191

35-44 years

45-54 years

Over 54 years

1,869 answered the survey regarding their life insurance

2,098 answered the survey regarding their home insurance

2,168answered the survey regarding their auto insurance

10

About the research

Most of the data is drawn from the Accenture 2013 Consumer-Driven Innovation Survey in which 6,135 insurance policyholders across 11 countries responded online between July 4 and July 25. It covered the automotive, home and life sectors. Salient demographics are depicted in Figure 11.

The Accenture 2013 Global Consumer Pulse Research is used to corroborate the findings. It is the ninth annual survey of the consumer landscape across 10 industry sectors. The 2013 study engaged with 12,867 end-consumers in 32 different

countries via the Internet between May 28 and June 6, 2013. Respondents were asked to evaluate 10 industry sectors (up to four industries per respondent). One of these industries was property and casualty insurance. The Global Consumer Pulse Research provides the broader consumer context plus corroboration for the findings of the Consumer-Driven Innovation Survey. In the 2012 study, life insurance was one of the industries, so these figures are used where appropriate for illustrative purposes.

11

Playing to win: The new business model for the customer-centric digital insurer

Confronted by the reality of a massive potential switching economy, insurers must take the offensive, make some bets and take some calculated risks to retain the customers they already have and attract those who are considering defecting from other, less dynamic providers.

In the quest to create experiences that are valued by customers, insurers must base their customer-experience blueprints on five core elements, described on the next few pages.

12

1. Know me — customer relevance

Figure 12. Four out of five customers would be willing to provide personal information in return for certain benefits

Q: Would you be comfortable for your insurance provider to access information on your usage/behavior in order to optimize your insurance coverage and insurance premium, as well as offer you more personalized products?*

78%

32%

46%

22%

81%

36%

45%

19%

YesIt depends on the informationNo

To optimize your insurance premium

To optimize your insurance coverage

To offer more personalized products

35%

47%

18%

82%

*Question adapted from two separate questions

Figure 13. Customers expect their insurance provider to help them manage their risks

Q: How important is it that your insurance provider, in addition to insuring you against loss, helps you reduce the risks that may result in this loss (e.g., information and advice on how to reduce risks of loss or injury)?

It is something critical for meIt would be good but this is not critical for me I do not see any value for me and my family

92%

44%

48%

8%

Insurance customers are following broader consumer trends—they are empowered and they want relevant advice and offers provided in convenient ways. They expect their provider to know them, and to interact accordingly.

As Figure 12 shows, 82 percent of insurance customers across all lines of business would consider giving access to their personal information if that allowed their carriers to optimize their insurance coverage. Almost as many would consider doing the same to access more personalized products.

In the same vein, insurance customers are starting to expect their insurers to offer risk-management services. Ninety-two percent say it’s important their provider goes beyond merely insuring their risks to helping them reduce risk: a clear indication

that they are looking beyond basic delivery of insurance products (Figure 13).

Insurers that can build a reputation for tailoring valuable services while safeguarding the personal data they collect for this purpose will have a meaningful competitive advantage.

Personalization clearly emerges as a key driver in retaining existing customers and attracting new ones (Figure 7). Perhaps even more important for the future: more than 40 percent of insurance customers are willing to pay more for personalized advice or assistance when purchasing insurance, a number which has increased by 6 percentage points since 2010 (Figure 14).

To be customer-relevant, insurers will have to develop the ability to share customer preferences, interactions, and other customer data across channels; and predict customer behavior and use those predictions to personalize interactions at any point in time and in any channel.

Key take-out: Use analytics effectively to leverage big data (including information mined from social media and other channels), generating the insights needed to stay one step ahead of the customer.

13

of insurance customers would be prepared to pay more to get personalized advice when purchasing automotive, home or life insurance products

10%

31%

19%

40%

Q

5%

30%

17%

48%

Figure 14. Customers are increasingly willing to pay more to get personalized advice or assistance when buying insurance

Q: Would you be willing to pay more to get personalized advice or assistance when buying insurance?

41%35%

2010 2013

Yes, certainlyYes, probably

No, probably notNo, certainly not

of insurance customers would give carriers access to usage/ behavior information to optimize insurance coverage

of insurance customers would like insurers to help them manage risk

82%

92% 41%

81% 78% of insurance customers would give carriers access to usage/ behavior information to optimize premiums

of insurance customers would give carriers access to usage/ behavior information to get more personalized products

14

2. Show me you know me — relationships at scale

The provider-customer relationship is coming full circle. Technology is making it possible to replicate, for today’s mass markets, some of the intimacy of the old-style insurance agent who knew his customers personally.

Accenture believes that this ability to manage relationships at scale will be the difference between winners and losers in the insurance market over the next five years. By seamlessly integrating digital with agent/broker and contact-center channels, insurers can provide even greater degrees of personalization and advice at the point of customer need.

Cloud-based customer relationship management solutions can help insurers develop a single view of the customer across channels and lines of business.

Social media present an opportunity for carriers to listen and learn more about their customers: what they think, what matters to them, and how they act. They also provide a forum to interact and

engage in informed, meaningful ways. In particular, the convergence of social media and mobility can help insurers create new opportunities for increasing customer intimacy by interactions that are both more frequent and relevant through offering context-related advice or offers.

Using analytics and cloud solutions, insurers can now take advantage of real-time data from existing and new sources to gauge and refine risk accurately as they create direct and multi-channel relationships with customers and with partners such as brokers. In time, we believe that insurers will purchase data from third parties or, more likely, share data with new sets of partners to enable them to identify customer life events with purchase, renewal or retention significance, such as moving house or a new child.

Relationships at scale depend on more than simply understanding what individual customers want. They require a sophisticated operating model that includes an automated experience engine that can recommend the “next best action”, enable this action, measure the impact, and feed this result back into the system to continually refine the experience.

Key take out: Provide the tailored service that customers have come to expect, avoid broken promises, and build trust by being responsible with personal data.

15

3. Delight me — seamless experience

Customers’ use of digital channels is increasing in insurance, but traditional channels such as agents and brokers are holding their own—if not for all lines of business and all types of interaction, then certainly for many important ones.4

The key point here is that today’s and tomorrow’s customers expect their experience to be consistent across all channels.

As shown in Figure 15, insurance customers want to be able to use multiple channels to interact with providers, with the percentages changing depending on the type of action contemplated. In all, only half of consumers across multiple industries are satisfied with their ability to access customer service and support using multiple channels.5

Our cross-industry research reveals that significant percentages of consumers become frustrated when companies market the same offers or ask the same questions time and again, when they are presented with inconsistent offers on different channels, and when they cannot access information or buy products or services using the channel of their choice.

Delighting customers by providing a seamless experience across multiple channels requires more than just bolting on new technologies to a traditional model: this will not create the necessary integrated view of the customer or household. Insurers must think not just in terms of channels but of transforming the underlying digital platforms needed to provide seamless experiences across current and future channels.

Insurance customers expect to vary channels based on transaction:

Figure 15. Customers expect to use multiple channels to meet their various needs

Q: How would you prefer to interact with your insurance provider(s) for each of the following actions?

*Only for life insurance

Meet a representative Online (PC, mobile, tablet)Phone a customer service / call center Send / receive a letter

5

10

15

20

25

30

35

40

45

50

55

60

6570

44%43%

46%

13%

49%

34%

11%

52%

34%

43%

12%

54%

33%

45%

13%

60%

45%

11%

50%48%

46%

9%

52%

29%34%

38%47%

68%

31%

27%

7%8%

Update your personal details

Cancel / close a contract*

Make a claimApply for / buy insurance

Change the terms of your

policy

Get information on insurance

products / services

Obtain a quote Get advice

Key take-out: Upgrade the operating model and align the channel mix to meet customer needs, and make sure that customer experiences are consistent and excellent.

would prefer to apply for or purchase insurance online

68%

46%

48%

52%

would prefer to update personal details online

would prefer to meet with a representative to get advice

would prefer to phone in claims

16

4. Enable me — inherently mobile

While Internet access using personal computers or laptops was the first step in enabling customers to use digital channels, the real game-changer has been the growth in mobile.

Now consumers are theoretically connected at all times, and expect the same of their insurance companies. The move to mobile, in particular, opens new opportunities for collaboration—between customers and agents, between customers and the insurance firm, and externally between the firm and the various members of its ecosystem, such as its claims assessors and procurement partners.

The past two years have seen a shift in customer buying patterns across insurance. New channels such as banks, retailers and online have become more prominent (Figure 5). In fact, as Figure 6 shows, a large majority of customers are prepared to buy a

range of insurance products online, among them travel and assistance insurance, extended warranties, home insurance, long-term auto insurance and life insurance.

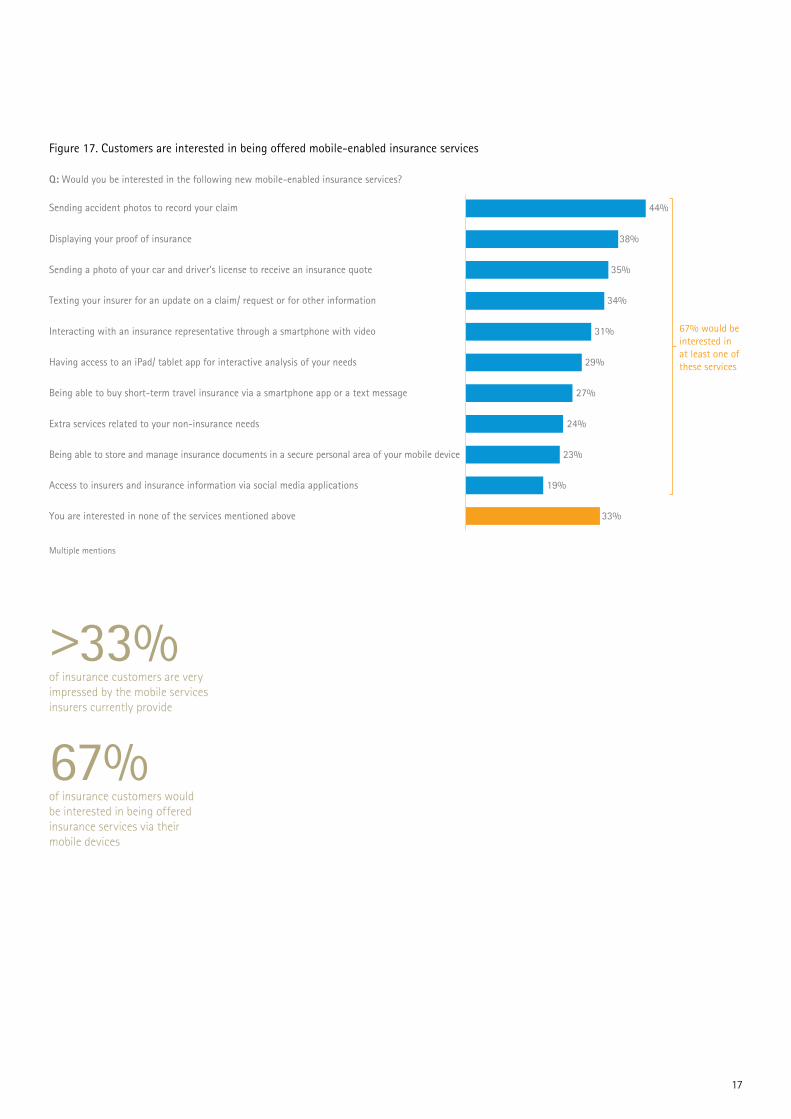

Thirty-seven percent of customers have used their mobile phone to deal with their insurers in the past two years (Figure 8). A little more than one in three are thrilled with the services currently provided on mobile devices (Figure 16). Expanding opportunities for mobile interaction and support should be a key priority in the quest to improve the customer experience.

Figure 17 shows 67 percent of insurance customers are interested in new services being offered on mobile devices, such as the ability to take a photograph with a mobile phone in the case of a car accident, and to send it to the insurance provider.

The mobile channel pre-eminently offers insurers the opportunity to take customer relevance to the next level by tailoring offers and interactions to the physical context. Location-based interaction can be highly relevant in insurance; consider, for

example, injury insurance offered on a ski slope or a claim submitted from an accident scene with supporting photographs. At a less specialized level, the increasing use of mobile devices by customers simply means that insurers must be equipped to interact appropriately on that channel, especially given the expectation of immediacy.

In general, farsighted insurers should be building a variety of new mobile capabilities with which to engage their customers in ways they have not yet imagined.

Figure 16. Slightly more than one in three customers are very impressed by the mobile services insurers currently provide

Q: How would you rate the services provided on mobile channels (smartphone and/or tablet) by your insurance providers?

To apply for/purchase insurance

To cancel/close a contract*

To change the terms of your policy

To get information on insurance

To obtain a quote

To update your details

To make a claim

ExcellentFairPoor

On smartphones On tablets

28% 57% 15% 33% 56% 11%

33% 54% 13% 38% 53% 9%

31% 52% 17% 33% 53% 14%

*Only for life insurance

Base: respondents who own a mobile phone, and own a tablet.

32% 56% 12% 38% 53% 9%

28% 51% 21% 33% 50% 17%

27% 57% 16% 33% 53% 14%

32% 56% 12% 40% 51% 9%

Key take-out: Create compelling mobile interactions that build increasing use of this channel—and that establish your company as mobile-savvy.

17

of insurance customers would be interested in being offered insurance services via their mobile devices

Figure 17. Customers are interested in being offered mobile-enabled insurance services

Q: Would you be interested in the following new mobile-enabled insurance services?

Texting your insurer for an update on a claim/ request or for other information

Sending accident photos to record your claim

Displaying your proof of insurance

Having access to an iPad/ tablet app for interactive analysis of your needs

Being able to store and manage insurance documents in a secure personal area of your mobile device

Access to insurers and insurance information via social media applications

You are interested in none of the services mentioned above

Sending a photo of your car and driver’s license to receive an insurance quote

67% would be interested in at least one of these services

44%

38%

35%

34%

29%

24%

19%

31%

27%

23%

33%

Multiple mentions

Interacting with an insurance representative through a smartphone with video

Extra services related to your non-insurance needs

Being able to buy short-term travel insurance via a smartphone app or a text message

>33%

67%

of insurance customers are very impressed by the mobile services insurers currently provide

18

5. Value me — naturally social

Social media have fundamentally changed the way people interact with each other, and with their service providers.

They are no longer a channel distinctly separated in consumers’ minds. Instead they are the “new normal”—just another way for consumers to communicate, collaborate and get information. Social media have decisively shifted the balance of power from the service provider to the customer: the latter now has a platform from which to broadcast dissatisfaction or pleasure, and to collaborate instantly with other customers.

People generally are using social media sites more and more—and they are using them to make purchase decisions. Almost half of all insurance customers regard comments on social media as very or somewhat important in making their insurance buying decisions (Figure 9). A significant proportion of this group is already using social media for a range of

insurance-related activities, and more plan to do so in the next two years (Figure 18). Most important of all, as shown in Figure 19, over half of insurance customers would be interested in a broad range of services being offered via social media.

Social media thus offer insurers a channel through which to gain a deeper understanding of their customers, to communicate with them and to build trust. This can go a long way to countering the growing commoditization of insurance, giving customers a reason to resist marketing campaigns based mainly on price.

Smart insurers will use the information they glean from social media to create and refine the personalized experiences that customers want. They will also empower their agents to make the most of social networks—to “be where their customers are” and to increase their productivity. They will pass on their customer insights to their agents, equip them with tools such as microsites, and train them to use social media to source, nurture and manage sales leads.

To do all this they may need to think beyond their own capabilities, and create a social network of their own. By partnering with other providers, who offer related services, they could build an ecosystem that goes further toward helping their customers achieve the lifestyles to which they aspire.

A wake-up call for insurers generally is that many of their customers simply don’t know what the firm is doing, or proposing to do, on social media (Figure 20). Insurers must communicate better to ensure that their social media presence and offerings are well understood by customers and consumers in general. This is particularly important in the switching economy, as dissatisfied customers look around for an insurer more in tune with their needs.

Figure 18. A significant proportion of customers are likely to use social networks for their insurance needs in the next two years

Q: Have you used social media sites (e.g. Facebook, Twitter, blogs and consumer review sites) to do any of the following? If not, is it something you may start doing in the next two years?

Share negative comments/ provide feedback on insurance products/ services when you are dissatisfied

Request information on an insurance product or service

Request advice on the best insurance product/ service to meet your needs

Get a quote for an insurance product or service

Submit an insurance claim

Share positive comments/ provide feedback on insurance products/ services when you are satisfied

No, but I am considering doing it in the next two years

Yes, I have already used social media

28% 18% 46%

28% 17% 45%

26% 18% 44%

27% 16% 43%

27% 16% 43%

27% 10% 37%

Key take-out: Use social media as a way to listen to what customers are saying—and then use those insights to engage more meaningfully with customers, crafting better interactions and solutions that ultimately build trust-based relationships.

19

of customers do not know what insurance providers are doing or offering on social media

Figure 19. The majority of customers would be interested in insurance services offered on social media

Q: Would you be interested in any of these services that your insurer may offer on social media?

The use of customer feedback to improve products & services or to create new products

Promotions & discounts

Responses to customers’ service complaints & comments

iPad/ tablet apps for interactive analysis of needs to improve knowledge of insurance and risk mitigation

Interaction with your provider via live chat (text or video) for personalized support or advice

Participation in insurance-related computer games

None of the above – I have no interest in my insurance provider leveraging social media

Information on new products & services

55% would be interested in at least one of these services

Multiple mentions

Customer service assistance

A full “agency” service: all required services via instant messaging, applications, videos

Use of personal data to create personalized products or service recommendations

34%

33%

30%

29%

24%

19%

14%

26%

19%

18%

45%

48%

55%

60% of customers feel that comments posted on social media sites are important in the selection of insurance products and providers

of customers would be interested in insurance products and services offered on social media

Figure 20. Insurers have an opportunity to improve the way they use social media in order to capitalize on them fully

Q: What do you think of the presence and services of insurers on social media?

I am satisfiedI am not satisfiedI don’t know what insurers are doing or offering on social media

23%

17%

60%

20

The youth market is key to future-proofing insurance

Many of the trends noted in this report are even clearer when research results are sorted according to age.

Unsurprisingly, the shift towards digital channels and all of the associated behavior are emphasized in the youth market (ages 18 to 34). Accenture Research concludes that successful digital transformation will be necessary for insurers to realize the opportunities offered by the younger generation.

Key data points from the survey that insurers should consider:

• Theyoungerthecustomer,thegreaterhis or her propensity to switch providers (Figure 21).

• Theyoungerthecustomers,themorelikely they are to want their insurance provider to act as a risk manager (Figure 22). In line with this, younger customers are more willing to pay for personalized advice or assistance when purchasing insurance (Figure 23).

• Youngercustomersaremoredigital,more interested in innovative services like gamification and mobile-enabled services, and they pay more attention to comments posted on social media (Figures 24-27).

However, insurers must be alive to nuance. The greater openness of the younger generations to online channels should not mask the reality that face-to-face channels like agents and brokers remain important, for significant segments within this group as well as others.

This is because younger people, who are less familiar with insurance than their parents, may require more hand-holding. The Accenture 2013 US Personal Lines Consumer Survey bears this contention out, with 32 percent of 18-to-24 year olds wanting an insurance quote delivered to them in person. This is higher than any other age group except those between 65 and 74 years.

Another nuance that should not be missed: the digital generation is made up of consumers of most ages. Large and growing numbers of people from older age cohorts are digital-savvy, something that insurers

of the 18 to 24 age group, and 52% of the 25 to 34 age group, are willing to pay more to get personalized advice or assistance when purchasing insurance

Figure 21. Younger customers are more likely to switch providers than their older counterparts

Q: How likely are you to stop doing business with one of your auto or home insurance providers and to buy from another provider in the next 12 months?

Very likelySomewhat likelyNot very likelyVery unlikely48%

18-24

11%

37%

15%

37%

51%

25-34

12%

39%

18%

31%

40%

35-54

10%

30%

24%

36%

28%

55+

5%

23%

34%

38%

Base: respondents having auto and/or home insurance products

75%

48%

54%

of customers between 18 and 34 will be renewing existing insurance or purchasing new insurance in the next 12 months

of the 18 to 24 age group, and 51% of the 25 to 34 age group, are likely to switch home and auto insurance providers during the next 12 months

21

Figure 22. Younger customers place the highest value on risk management advice

Q: How important is it that your insurance provider, in addition to insuring you against loss, helps you reduce the risks that may result in this loss (e.g., advice on how to prevent loss or injury)?

It is critically important to me

18-24

51%

25-34

49%

35-54

43%

55+

38%

Figure 26: Younger customers are more frequent users of mobile devices to reach their insurers

Q: Have you used your mobile device to interact with your insurer in the past 2 years?

Base: respondents who have a mobile phone/ tablet

18-24

25-34

55+

35-54

49%

48%

21%

33%

% used a smartphone/ mobile phone

56%

60%

28%

40%

% used an iPad/ tablet

Figure 24. Younger customers are more receptive to the idea of buying insurance online

Q: Would you be willing to purchase insurance online?

Yes I would

58%

18-24 25-34 35-54 55+

79%81%

70%

Figure 27. Younger customers pay more attention to recommendations on social media sites

Q: If you were to consider buying insurance, how important would the comments and recommendations on social media sites be in helping you decide which product and provider to choose?

Very importantSomewhat important

18-24 25-34 35-54 55+

20%

43%

63%

19%

42%

61%

13%

32%

45%

7%

20%

27%

23%

44%

24%

42%

Figure 25. Younger customers would be more likely to embrace innovative insurance services such as gamification

Q: Would you be interested in a computer game that your insurance provider offered to help you better manage the risks you face and to optimize your insurance premiums?

Very interestedSomewhat interested

18-24 25-34 35-54 55+

Simulation game could show the impact of your actions & decisions on the risks you face as well as on the cost of your insurance

67%66%

17%

35%

52%

10%

25%

35%

13%

41%

12%

34%

15%

37%

13%

35%

9%

28%

22%

41%

5%

22%

28%

45%

Figure 23. Younger customers are more likely to pay a premium for personalized insurance advice and assistance

Q: Would you be willing to pay more to get personalized advice or assistance when buying insurance?

Yes, certainlyYes, probablyNo, probably notNo, certainly not

18-24 25-34 35-54 55+

22

Creating customer experiences that drive loyalty

All the current research undertaken by Accenture agrees to a remarkable extent. Today’s and tomorrow’s consumers are increasingly moving online, and they are demanding a highly personalized and relevant experience, rather than just products.

Only those insurers with the digital capabilities and flexible operating model to adapt effectively to the changing demands of customers, and the ability to provide the advice they are seeking, will be able to retain and further penetrate their existing customer base and attract the large numbers of dissatisfied customers who are set to leave their less farsighted providers.

At a strategic, conceptual level, insurers need to give careful thought to how they move from simply selling products to providing useful experiences. The importance of personalization for survey respondents, and their willingness to pay more for personalized advice and better cover, are highly significant. Equally significant is the finding that even though most consumers consider their risk profiles average or low, 44 percent regard it as critical that their insurance providers help them manage that risk (Figure 13).

In short, carriers that develop the necessary digital capabilities, and that implement sufficiently flexible business and operating models, can differentiate themselves from competitors. By doing so, they will protect their existing, profitable customer base, and position themselves to attract customers who are switching providers.

Accenture believes that would-be customer-centric digital insurers must bear in mind the two fundamental (and interrelated) drivers:

1. Understand the new customer dynamic.Business has always known that the customer is central, but in the past the impetus was almost entirely from the company out to its clients. Digital technologies have changed that dynamic completely, and customers (and consumers more generally) now have the capability to compare a provider’s products and overall customer experience with those of its competitors, both within the industry and across industries. Control has essentially passed to the customer, and thus the kind of experience the insurer offers its customers is now absolutely critical.

2. Fine-tune business models and use technology to enable the customer experience intelligently.Across industries, the rise of digital channels and the shifting of the center of gravity towards the customer have fuelled a tendency towards simplification of the sales process, a “retailization,” if you will. Many insurers have jumped on this bandwagon, and are spending vast sums of advertising money to convince customers that insurance products are simple and can be bought simply. They are, in essence, trying to move insurance out of the low-frequency, high-complexity category into one that is higher frequency and lower complexity—more like buying a T-shirt or some specialty tea.

The problem with this is that most insurance products are—and remain—inherently complex. By offering a complex product in a retailized environment, insurers are creating a tension that has the potential to rip apart their underlying business models. This type of environment is, by nature, volatile because customers believe that switching providers is simple, and the margins simply do not reflect the costs and operational requirements of a complex product’s back end.

It must also be added here that some customer needs are genuinely simple—insurance for a new cell phone, for example—

and can be met by a simple product sold simply. Insurers that overcomplicate their products and experiences to meet such simple needs will lose out in the end.

However, most insurance products have some level of complexity and need greater expertise on the part of the provider—but the imperative for a simplified customer-facing front end remains. Insurers also need to bear in mind that, over time, education and improved offerings will make even the most complex offerings simple

Insurance companies that recognize this disconnect and put in place technologies to drive a different operating model that can handle the simple front end and complex back end will be the ultimate winners. In other words, the key to high performance for the insurer of the future will be to package and deliver complexity in a way that customers find easy to understand and use, yet which does not downplay the complex nature of the solution. By building their brands and gaining acceptance as trusted advisors, insurers can maintain their differentiation against a tide of commoditization.

Understanding and mastering this tension between complexity and simplicity will be the ultimate barrier to entry protecting carriers against new entrants into the insurance market.

These two drivers, of course, do not operate in isolation but together. It’s thus perhaps worth pointing out that the flexible operating model described in the second driver must be used to innovate and transform continually the customer experience described in the first. This capability also provides the opportunity to build a trust-based relationship with customers, and to become a long-term partner, a risk manager rather than just an insurer. To achieve this, carriers must be prepared to conceptualize their business more broadly, and be willing to create ecosystems of partners who together can provide the total, personalized and convenient experience today’s digital customers want.

23

One can see this playing out in the United Kingdom and Australia, and to some extent in the United States, where the retailization of insurance (particularly automobile insurance) is well under way.

Insurers have a choice as they seek to remain competitive and protect their margins. One option is to become the infrastructure for an aggregator that is offering a suite of financial services products of which insurance is one. This is the indirect model.

A second option would be for the insurer to seize the opportunity of expanding its role to offer a much wider customer experience, one that spans new markets and a range of new products.

A good example of a company that has chosen this latter option is USAA. Originally only an insurance company, it now delivers a full range of financial and other services to its members in the US military. For example, it has become a major vendor of diamond engagement rings in America. By listening to its members, it realized that military personnel on active duty had no way to buy such items for sweethearts back home. By providing that facility, it integrates itself into its members’ lives as a true partner and not just an insurer or a bank.

Another service it offers is buying an automobile, offering a straightforward solution to an inherently complex need. Members simply state what type of car they want and a certified dealer provides a quote which is guaranteed to be lower than any other advertised price. A discounted loan, and insurance, complete the USAA Auto Circle package. This approach implies deep trust and flexible business and operating models that enable the company to keep on innovating the customer experience it offers.

24

Developing a winning game plan

Having defined their strategic intent, carriers confront the pressing question of how to build the digital and other capabilities needed to turn strategy into reality.

Accenture believes that insurers need to seize the first-mover advantage in each of the five elements identified above—customer relevance, relationships at scale, seamless experience, naturally social and inherently mobile—but only within the context of a broad strategy and defined road map.

In creating their own digital strategy and road map for reaching it, insurers need to be aware of the difference between true digital transformation and the mere digitization of existing business processes. The latter may be a first step in certain instances, and may generate marginal improvements in efficiency, but in the end it falls short and simply makes the operating model more complex. Many insurers fall into the trap of trying to provide simplified, digitized front ends to their customers without taking into account the complexity of the back office and, indeed, of the product or solution.

To solve this challenge, insurers need to take an outside-in approach that focuses on the customer, on the kinds of experience

he or she demands, and on growth. This will help them understand the products, services and capabilities they need to achieve growth, and following on from that, the operating model, the systems consolidation and the transformation they need. Ultimately it will define the type of organization they must become.

This transformation will be effected across four primary capabilities: cross-channel excellence, customer-centricity and personalization, operational simplicity, and superior execution agility. Of these, the most important is probably agility, because the only thing one can say about the insurance environment with any degree of certainty, is that it will change. Having adaptable, outward-focused business and operating models gives the insurer a distinct advantage over competitors that are encumbered by product-centric models and offerings that simply reflect their organizational structures.

The progression to digital maturity can take many forms, but there are certain attributes and capabilities that lay a platform for others that follow. In our experience there are four broadly defined stages along this path (Figure 28):

1. The first stage is characterized by the insurer having a few digital systems that are limited in their features and flexibility.

2. At the second stage, the priority is to do the basics right. Some of the channels are integrated and process digitization is underway.

3. Having got the basics right, insurers are now in a position to become interactive. Their integrated multi-channel architecture and the sophisticated use of analytics allow them to enhance the customer experience and sell more effectively across digital as well as traditional channels.

4. The final stage of the journey is the holistic, omni-channel and fully customer-centric insurer that offers consumers insurance “where you are at the precise moment you want it.” At this point, the insurer has moved from defending its position to taking the offensive: playing to win the ongoing loyalty of existing customers and to attract new ones from competitors that have not been as successful in their transformation.

Achieving these capabilities will require profound changes across the entire insurance value chain. The goal will thus not be achieved overnight, nor in the same sequence for each insurer. However, the general trajectory is toward the end goal of becoming an agile, externally-focused insurer with fully digital front and back ends.

Figure 28. The road map to digital excellence is a four-step journey

Innovate and transform, providing leading-edge customer experiences

Do the basics right

Digital objectives, organization and strategy definition

• Insurance where you are, when you want, using the power of mobile• Leveraging of external customer data and social media to create customer intimacy and understand personal interests• One-stop shop• Customer relationships conducted on channels such as social media favored by customers• Leveraging of influencers• Co-creation with customers• Real-time prospective analytics• Collaborative and virtual workplace

Holistic omni-channel insurer

• Integrated multi-channel architecture• Analytics-enabled insurance (event management, etc.)• Advanced digital advisory capability• Needs-based offering optimized by channels• Mobile-enabled salesforce and customers• Extension of self-service offerings• Paperless workflow

Interactive insurer

• Optimized branch network and contact center• Enhanced digital channels• Basic multi-channel integration• Needs-based offering and consistent sales behaviors• Electronic record management

Connected insurer

• Legacy

Standalone insurer

25

26

27

Conclusion: Prepare for the future by listening to customers now

Accenture’s research shows that insurers face a significant risk that is also an immense opportunity.

We estimate this risk/opportunity to be worth anything up to $400 billion in 2013, and it will only be mitigated and/or realized through a thoroughgoing digital transformation that enhances all channels and experiences.

Only companies that transform their technologies as well as their underlying business models will be equipped to deliver the experiences that customers want and demand. Only true digital transformation at this strategic level will enable carriers to let customers define their own experiences rather than simply providing products for them to buy.

One point of interest emerges from the regional results of the survey. These results show that consumers in Brazil and China (and to a lesser extent in South Africa) have the highest level of expectations for the provision of value-added services by their insurance providers as well as the greatest interest in digital services that may be offered online, via the Web, mobile

devices or social media. It must be borne in mind that the research targeted connected consumers in these markets, and therefore these results do not represent the full spectrum of the general population; they do, however, clearly highlight emerging trends in consumers’ attitudes and behaviors.

When it comes to transformation, there is no one size that fits all. Insurers must take a long-term strategic view that assesses the customer landscape and the role the company wishes to play. This role will determine the type of customer experience it must deliver, and so how to mix the five elements of the customer experience outlined above. Having done this, the insurer must develop a detailed plan for achieving the goal.

The future of insurance embraces digital, and only those companies that successfully transform their whole value chain will be able to compete successfully and, in time, become high-performance businesses.

To find out more about Accenture’s Consumer-Driven Innovation Survey or how to embark on digital transformation, please contact one of the authors on the back page or visit our website at www.accenture.com/insurance.

CLICK HERE VISIT OURINTERACTIVETOOL TO LEARNMORE ABOUT SURVEY RESULTS AND HOW IT APPLIES TO YOUR TARGET MARKET

Copyright © 2013 Accenture All rights reserved.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture.

Copyright © 2014 Accenture All rights reserved.

Accenture, its logo, and High Performance Delivered are trademarks of Accenture.

13-4555_lc

References1. The size of the switching economy is estimated as the total of personal-lines property and casualty and life insurance premiums written in a 12-month period multiplied by the percentage of customers who reported they are likely to switch providers in “the next 12 months.” For P&C insurance the definition of switching is cancelling or not renewing a contract with one provider and initiating a new contract with another. For life insurance the definition is cancelling or stopping contributions to a contract with one provider and initiating a new contract with another provider. Investment policies held with life insurers are excluded from the calculation.

2. UK Private Motor Insurance, 2012: Datamonitor.

3. Accenture 2013 Global Consumer Pulse Research.

4. Accenture 2013 Digital Insurance Survey: Europe, Latin America and Africa, p7, available at http://www.accenture.com/us-en/Pages/insight-europe-latin-america-digital-distribution-survey-2013.aspx.

5. Accenture 2013 Global Consumer Pulse Research.

Data sources

Data for the figures is derived from the Accenture 2013 Consumer-Driven Innovation Survey, except Figure 1, which is based on data from the Accenture 2013 Global Consumer Pulse Research. Similarly, data in the text is derived from the Accenture 2013 Consumer-Driven Innovation Survey unless otherwise noted.

About the seriesThe Digital Insurer is an Accenture series that provides insights on how insurers can achieve high performance in the Digital Age. Digital is not simply a new distribution channel—it offers an entirely new way of doing business. Leading insurers are learning how to provide significantly easier access to a wider range of more relevant products and services at a lower cost. With these goals in mind, this series presents pragmatic and visionary discussions on analytics, back-office digitization, marketing, mobility, social media and more. For more information about this series, please visit www.accenture.com/digitalinsurer.

AuthorsJean-François Gasc is the managing director of Accenture Management Consulting for Insurance across Europe and Latin America. He joined Accenture in 1985 and has focused on insurance since 1995. He is leading work at major insurance groups in France, Belgium, the Netherlands and Luxembourg, in the areas of life consolidation and transformation, post-merger integration and industrialization for property and casualty insurers, as well as digital and customer-centric transformation. Gasc holds a degree from the Paris Institute of Political Studies and a Master’s degree in Business Administration from HEC in Paris. Contact him at [email protected].

Erik Sandquist is the managing director of Accenture’s Insurance Distribution and Marketing Business Service in North America. He has helped insurers reinvent their distribution models through strategic transformational change programs. Sandquist holds a degree from Cornell University. Contact him at [email protected].

Mark Halverson is a senior executive in Accenture’s Financial Services practice. He is the lead for Life Insurance Distribution Services and Wealth & Asset Management Services. Halverson has worked with clients in insurance, retail banking, wealth management and brokerage, mutual funds and asset management, and hedge funds and prime brokerage. He specializes in defining strategies and business models, and driving them to successful implementation. Halverson holds a Bachelor of Science in Computer Science Engineering from Southern Methodist University, and is an alumnus of Northwestern University's Kellogg Graduate School of Management. Contact him at [email protected].

Michael Lyman is the Global Managing Director of Accenture’s Management Consulting for Insurance. For over thirty years, he has advised executives and their teams on how to transform their businesses to drive customer-centricity and achieve high performance. Lyman holds a Masters in Business Administration from the Kellogg Graduate School of Management at Northwestern University. Contact him at [email protected].

About Accenture ResearchAccenture Research is Accenture’s global business research team with over 180 professional researchers across 22 countries. The team has experts in industry, technology, financial, survey and economic research.

About AccentureAccenture is a global management consulting, technology services and outsourcing company, with approximately 281,000 people serving clients in more than 120 countries. Combining unparalleled experience, comprehensive capabilities across all industries and business functions, and extensive research on the world’s most successful companies, Accenture collaborates with clients to help them become high-performance businesses and governments. The company generated net revenues of US$28.6 billion for the fiscal year ended Aug. 31, 2013. Its home page is www.accenture.com.