Tax Reform: Reshaping the Code - c.ymcdn.comc.ymcdn.com/sites/ · 2017 NOL enhancement –not...

93

Tax Reform: Reshaping the Code

-

Upload

vuongkhuong -

Category

Documents

-

view

213 -

download

0

Transcript of Tax Reform: Reshaping the Code - c.ymcdn.comc.ymcdn.com/sites/ · 2017 NOL enhancement –not...

Tax Reform:Reshaping the Code

Copyright © 2018 Deloitte Development LLC. All rights reserved. 2Tax Reform Roundtable

Agenda

• Overview

• Key Domestic & International Provisions

• Impact to Employee Related Programs/Expenses

• Building Sustainable Processes

• Multistate Considerations

• Financial Reporting Considerations

• Other Considerations

Copyright © 2018 Deloitte Development LLC. All rights reserved. 3Tax Reform Roundtable

US tax reform overview

US Tax Reform: Implications for US Inbound CompaniesCopyright © 2018 Deloitte Development LLC. All rights reserved. 4

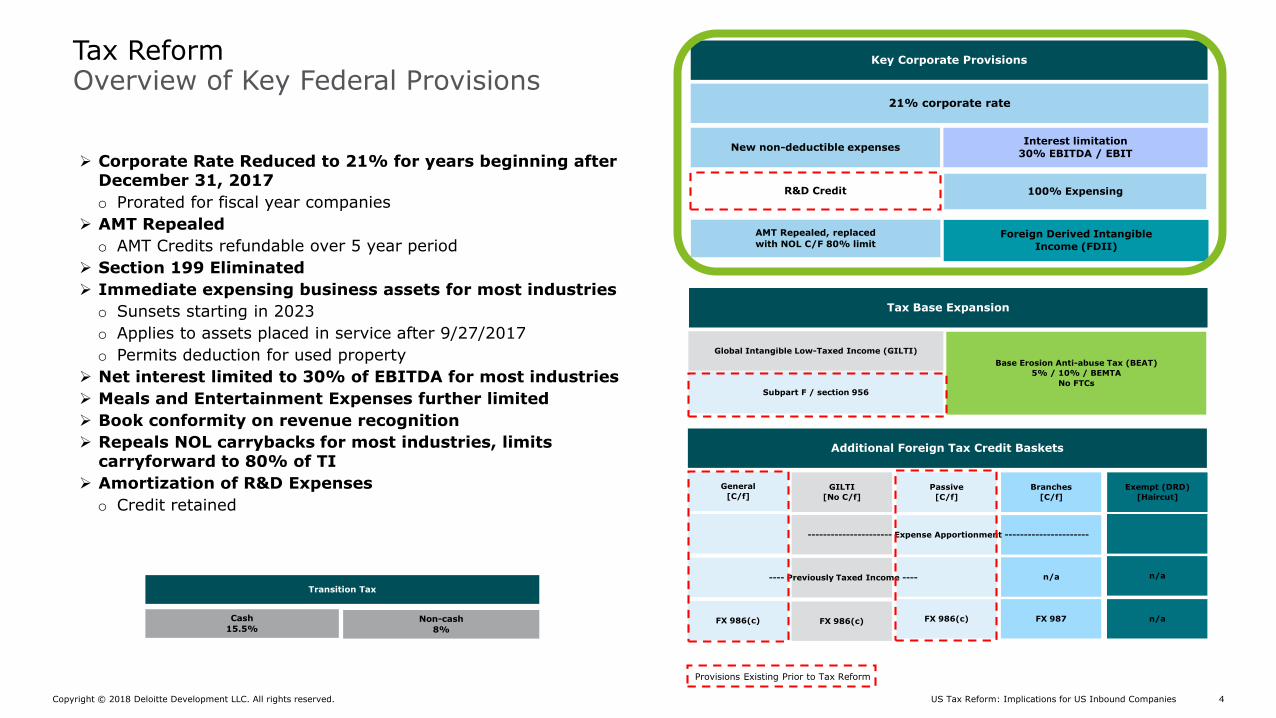

Overview of Key Federal Provisions

➢ Corporate Rate Reduced to 21% for years beginning after December 31, 2017

o Prorated for fiscal year companies

➢ AMT Repealed

o AMT Credits refundable over 5 year period

➢ Section 199 Eliminated

➢ Immediate expensing business assets for most industries

o Sunsets starting in 2023

o Applies to assets placed in service after 9/27/2017

o Permits deduction for used property

➢ Net interest limited to 30% of EBITDA for most industries

➢ Meals and Entertainment Expenses further limited

➢ Book conformity on revenue recognition

➢ Repeals NOL carrybacks for most industries, limits carryforward to 80% of TI

➢ Amortization of R&D Expenses

o Credit retained

Key Corporate Provisions

Tax Base Expansion

Additional Foreign Tax Credit Baskets

21% corporate rate

New non-deductible expensesInterest limitation

30% EBITDA / EBIT

Foreign Derived Intangible

Income (FDII)

Global Intangible Low-Taxed Income (GILTI)

Base Erosion Anti-abuse Tax (BEAT)

5% / 10% / BEMTA

No FTCsSubpart F / section 956

General

[C/f]GILTI

[No C/f]

Passive

[C/f]

Branches

[C/f]

Exempt (DRD)

[Haircut]

---------------------- Expense Apportionment ----------------------

n/a n/a

FX 986(c) FX 986(c) FX 987 n/aFX 986(c)

---- Previously Taxed Income ----

R&D Credit

AMT Repealed, replaced

with NOL C/F 80% limit

100% Expensing

Transition Tax

Cash

15.5% Non-cash

8%

Provisions Existing Prior to Tax Reform

Tax Reform

US Tax Reform: Implications for US Inbound CompaniesCopyright © 2018 Deloitte Development LLC. All rights reserved. 5

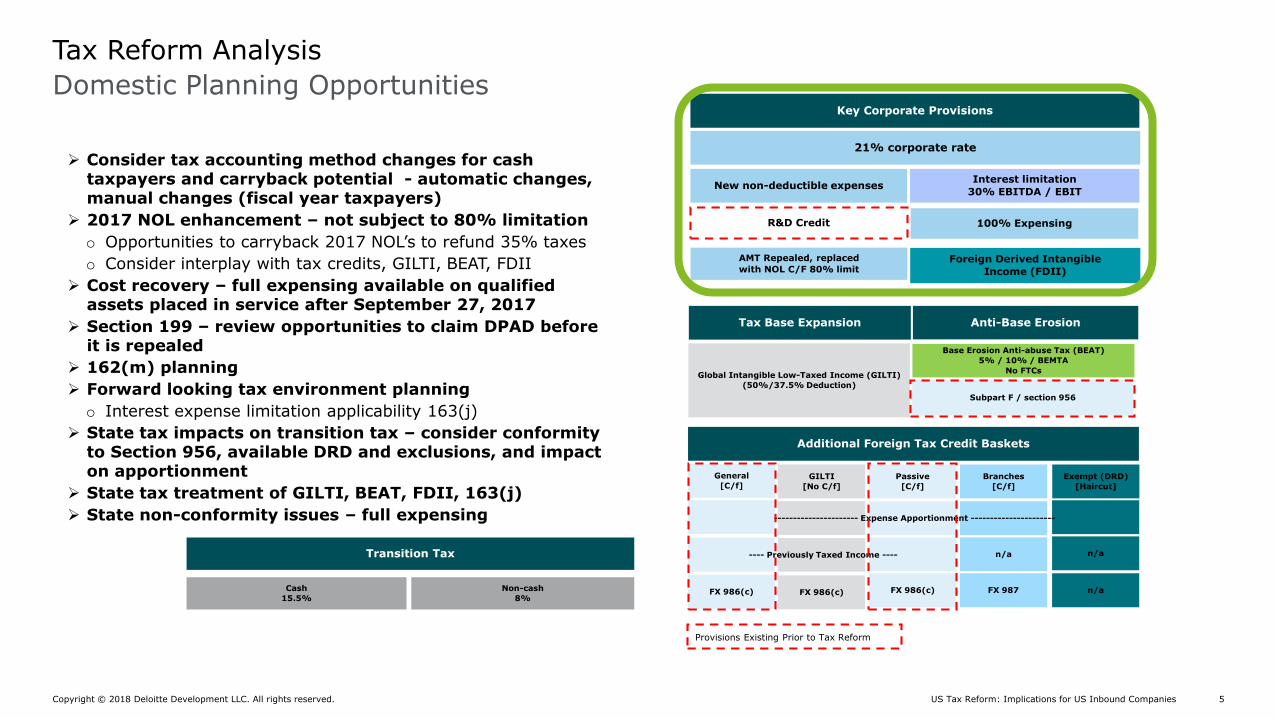

➢ Consider tax accounting method changes for cash taxpayers and carryback potential - automatic changes, manual changes (fiscal year taxpayers)

➢ 2017 NOL enhancement – not subject to 80% limitation

o Opportunities to carryback 2017 NOL’s to refund 35% taxes

o Consider interplay with tax credits, GILTI, BEAT, FDII

➢ Cost recovery – full expensing available on qualified assets placed in service after September 27, 2017

➢ Section 199 – review opportunities to claim DPAD before it is repealed

➢ 162(m) planning

➢ Forward looking tax environment planning

o Interest expense limitation applicability 163(j)

➢ State tax impacts on transition tax – consider conformity to Section 956, available DRD and exclusions, and impact on apportionment

➢ State tax treatment of GILTI, BEAT, FDII, 163(j)

➢ State non-conformity issues – full expensing

Key Corporate Provisions

Tax Base Expansion

Additional Foreign Tax Credit Baskets

21% corporate rate

New non-deductible expensesInterest limitation

30% EBITDA / EBIT

Foreign Derived Intangible

Income (FDII)

Global Intangible Low-Taxed Income (GILTI)

(50%/37.5% Deduction)

Base Erosion Anti-abuse Tax (BEAT)

5% / 10% / BEMTA

No FTCs

Subpart F / section 956

General

[C/f]GILTI

[No C/f]

Passive

[C/f]

Branches

[C/f]

Exempt (DRD)

[Haircut]

---------------------- Expense Apportionment ----------------------

n/a n/a

FX 986(c) FX 986(c) FX 987 n/aFX 986(c)

---- Previously Taxed Income ----

R&D Credit

AMT Repealed, replaced

with NOL C/F 80% limit

100% Expensing

Transition Tax

Cash

15.5%

Non-cash

8%

Provisions Existing Prior to Tax Reform

Anti-Base Erosion

Domestic Planning Opportunities

Tax Reform Analysis

US Tax Reform: Implications for US Inbound CompaniesCopyright © 2018 Deloitte Development LLC. All rights reserved. 6

Provisions Existing Prior to Tax Reform

Additional Foreign Tax Credit Baskets

Global Intangible Low-Taxed Income

(GILTI) (50%/37.5% Deduction)

General

[C/F]

GILTI

[FTC Haircut &

No C/F]

Passive

[C/F]

Branches

[C/F]

Exempt (DRD)

[Hybrid Rules

&FTC Haircut]

---------------------- Expense Apportionment ----------------------

N/A N/A

FX 986(c) FX 986(c) FX 987 N/AFX 986(c)

---- Previously Taxed Income ----

Key Corporate Provisions

21% corporate rate

New non-deductible expensesInterest limitation

30% EBITDA / EBIT

Foreign Derived Intangible

Income (FDII)

R&D Credit

AMT Repealed, replaced

with NOL C/F 80% limit

100% Expensing

Transition Tax

Cash

15.5%

Non-cash

8%

Base Erosion Anti-abuse Tax (BEAT)

5% / 10% / BEMTA

No FTCs

Subpart F / section 956

Tax Base Expansion Anti-Base Erosion

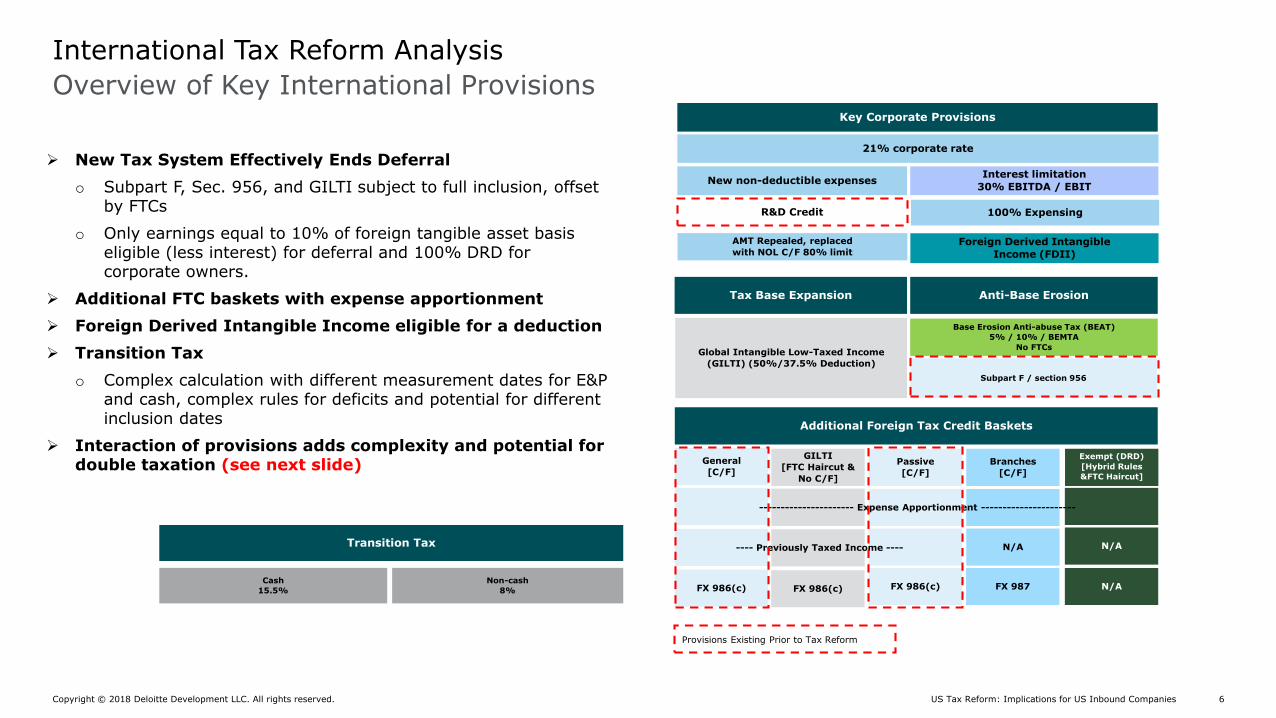

Overview of Key International Provisions

International Tax Reform Analysis

➢ New Tax System Effectively Ends Deferral

o Subpart F, Sec. 956, and GILTI subject to full inclusion, offset by FTCs

o Only earnings equal to 10% of foreign tangible asset basis eligible (less interest) for deferral and 100% DRD for corporate owners.

➢ Additional FTC baskets with expense apportionment

➢ Foreign Derived Intangible Income eligible for a deduction

➢ Transition Tax

o Complex calculation with different measurement dates for E&P and cash, complex rules for deficits and potential for different inclusion dates

➢ Interaction of provisions adds complexity and potential for double taxation (see next slide)

US Tax Reform: Implications for US Inbound CompaniesCopyright © 2018 Deloitte Development LLC. All rights reserved. 7

Cash

15.5%

Non-cash

8%

Global Intangible Low-Taxed Income (GILTI)

(50%/37.5% Deduction)

Base Erosion Anti-abuse Tax (BEAT)

5% / 10% BEMTA

No FTCs

General

[C/F]

GILTI

[FTC Haircut &

No C/F)

Passive

[C/F]

Branches

[C/F]

Exempt (DRD)

[Hybrid Rules & FTC

Haircut]

---------------------- Expense Apportionment ----------------------

N/A N/A

FX 986(c) FX 986(c) FX 987 N/AFX 986(c)

---- Previously Taxed Income ----

Additional FTC Baskets

Subpart F / Section 956

Additional Foreign Tax Credit Baskets

Transition Tax

Provisions Existing Prior to Tax Reform

Key Corporate Provisions

21% corporate rate

New non-deductible expensesInterest limitation

30% EBITDA / EBIT

Foreign Derived Intangible

Income (FDII)

R&D Credit

AMT Repealed, replaced

with NOL C/F 80% limit

100% Expensing

Tax Base Expansion Anti-Base Erosion

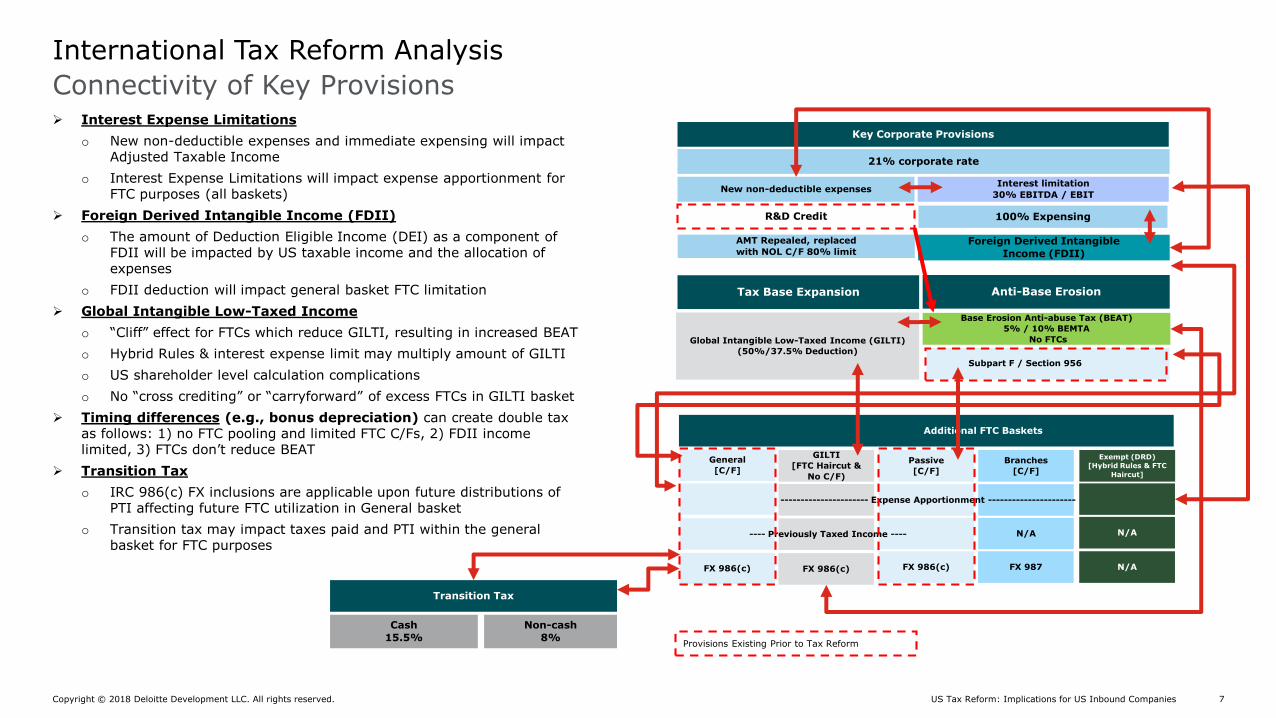

Connectivity of Key Provisions

International Tax Reform Analysis

➢ Interest Expense Limitations

o New non-deductible expenses and immediate expensing will impact Adjusted Taxable Income

o Interest Expense Limitations will impact expense apportionment for FTC purposes (all baskets)

➢ Foreign Derived Intangible Income (FDII)

o The amount of Deduction Eligible Income (DEI) as a component of FDII will be impacted by US taxable income and the allocation of expenses

o FDII deduction will impact general basket FTC limitation

➢ Global Intangible Low-Taxed Income

o “Cliff” effect for FTCs which reduce GILTI, resulting in increased BEAT

o Hybrid Rules & interest expense limit may multiply amount of GILTI

o US shareholder level calculation complications

o No “cross crediting” or “carryforward” of excess FTCs in GILTI basket

➢ Timing differences (e.g., bonus depreciation) can create double tax as follows: 1) no FTC pooling and limited FTC C/Fs, 2) FDII income limited, 3) FTCs don’t reduce BEAT

➢ Transition Tax

o IRC 986(c) FX inclusions are applicable upon future distributions of PTI affecting future FTC utilization in General basket

o Transition tax may impact taxes paid and PTI within the general basket for FTC purposes

US Tax Reform: Implications for US Inbound CompaniesCopyright © 2018 Deloitte Development LLC. All rights reserved. 8

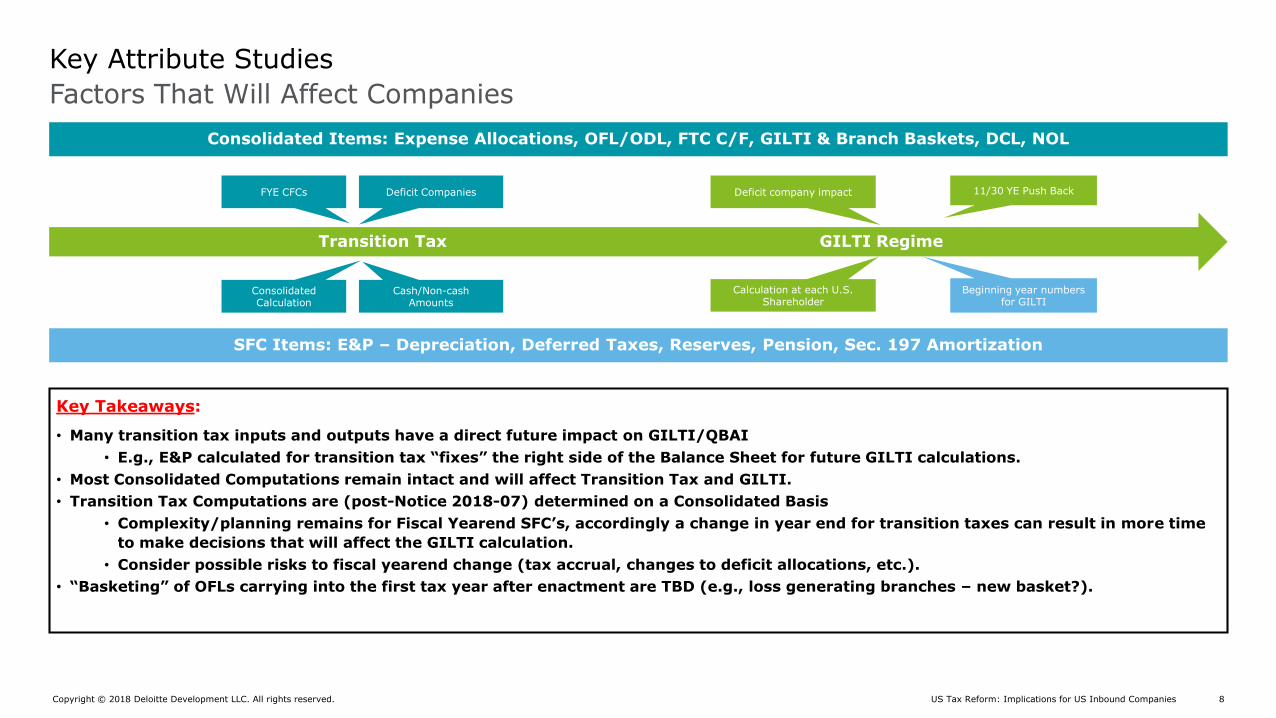

Key Takeaways:

• Many transition tax inputs and outputs have a direct future impact on GILTI/QBAI

• E.g., E&P calculated for transition tax “fixes” the right side of the Balance Sheet for future GILTI calculations.

• Most Consolidated Computations remain intact and will affect Transition Tax and GILTI.

• Transition Tax Computations are (post-Notice 2018-07) determined on a Consolidated Basis

• Complexity/planning remains for Fiscal Yearend SFC’s, accordingly a change in year end for transition taxes can result in more time

to make decisions that will affect the GILTI calculation.

• Consider possible risks to fiscal yearend change (tax accrual, changes to deficit allocations, etc.).

• “Basketing” of OFLs carrying into the first tax year after enactment are TBD (e.g., loss generating branches – new basket?).

Transition Tax GILTI Regime

FYE CFCs

ConsolidatedCalculation

Deficit Companies

Cash/Non-cash Amounts

11/30 YE Push Back

Calculation at each U.S. Shareholder

Deficit company impact

Beginning year numbers for GILTI

Consolidated Items: Expense Allocations, OFL/ODL, FTC C/F, GILTI & Branch Baskets, DCL, NOL

SFC Items: E&P – Depreciation, Deferred Taxes, Reserves, Pension, Sec. 197 Amortization

Factors That Will Affect Companies

Key Attribute Studies

Copyright © 2018 Deloitte Development LLC. All rights reserved. 9Tax Reform Roundtable

Key domestic business tax provisions

Copyright © 2018 Deloitte Development LLC. All rights reserved. 10Tax Reform Roundtable

Corporate Rate

• Prior graduated rates with top rate of 35% now 21% flat rate, effective for tax years after 12/31/17

• Fiscal year taxpayers benefit from rate change starting 1/1/18 by applying a blended rate for the fiscal year based on the number of days of the fiscal year before and after the effective date

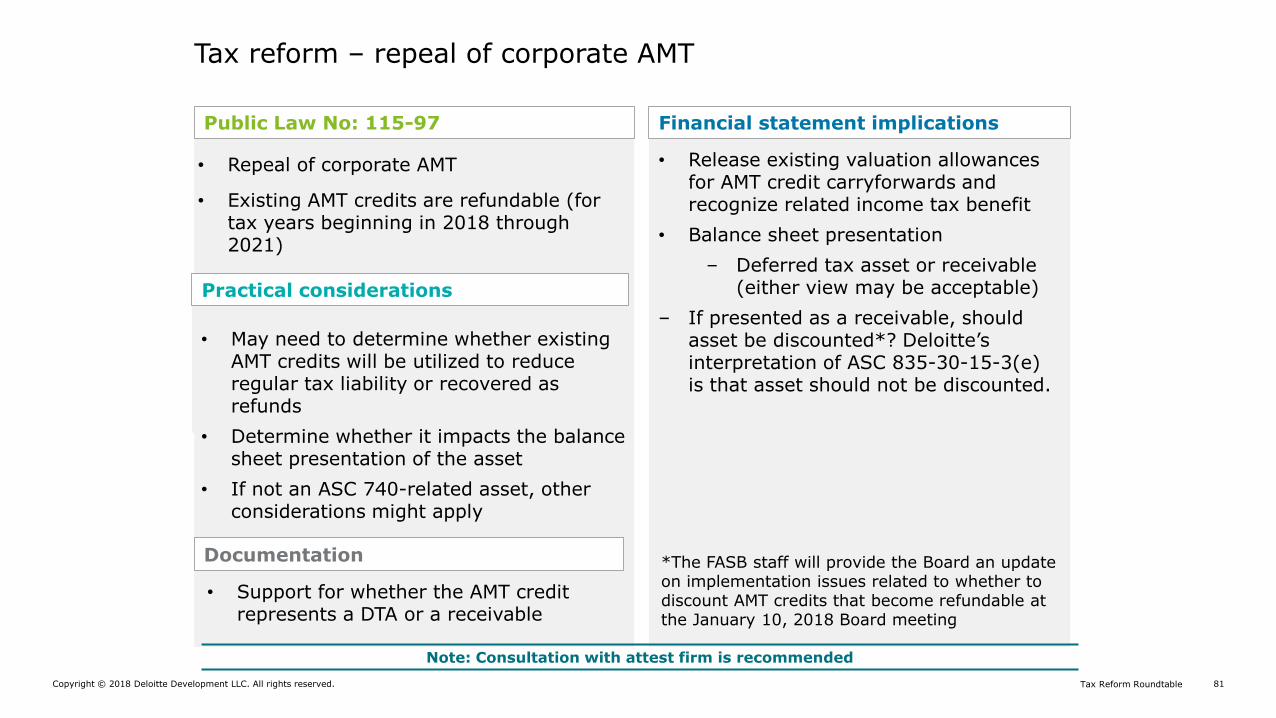

• Corporate alternative minimum tax repealed (final year for taxpayer with fiscal years ending in 2018)

Copyright © 2018 Deloitte Development LLC. All rights reserved. 11Tax Reform Roundtable

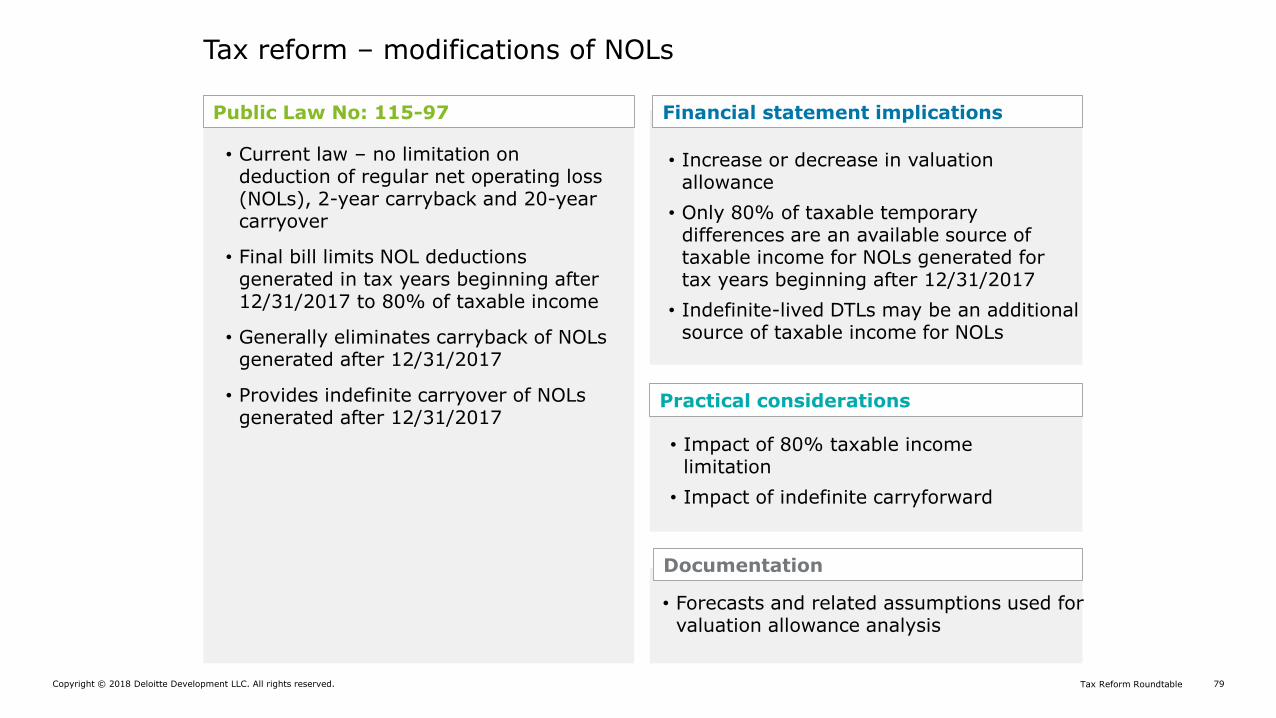

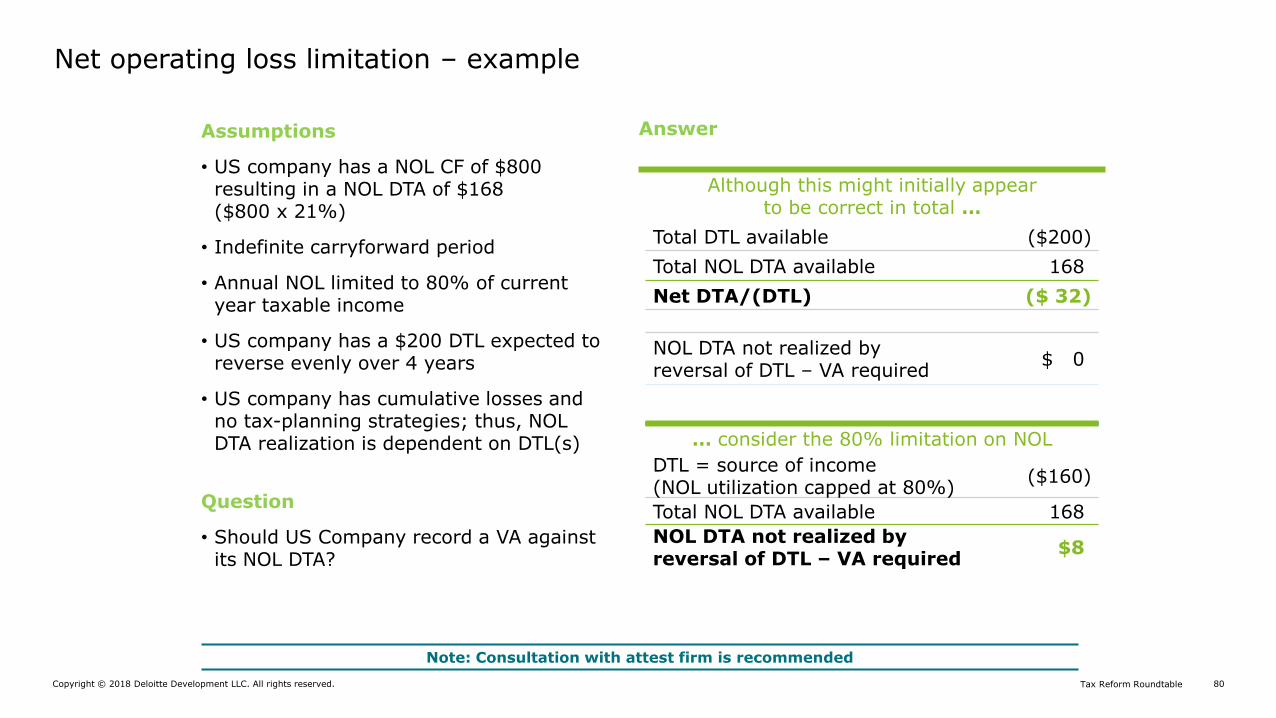

Net operating loss deduction

• Business deductions exceeding gross income result in a carryover tax attribute

• Existing NOLs (generated through 12/31/17) are grandfathered and still may be carried back 2 years and carried over 20 years (note, amount must be determined without regard to increased expensing provision)

• New NOLs (generated in 2018 forward) may be carried forward indefinitely and utilization is limited to 80% of taxable income (80% deduction @ 21% = 4.2% effective tax rate on the use of NOLs)

• Limited carrybacks for new NOLs retained for small businesses and farms in certain casualty and disaster situations and for Property and casualty insurance companies

• No time value of money adjustment on NOLs

− Practical Issue: How is the 80% limitation calculated when pre-2018 NOLs are applied starting in 2019?

− Practical Issue: How is RBIG affected by transaction tax and current expensing?

Copyright © 2018 Deloitte Development LLC. All rights reserved. 12Tax Reform Roundtable

100% expensing of certain tangible property

• New and used qualified property acquired and placed in service after 9/27/17

• Qualified property generally includes tangible property (i.e., intangible assets and goodwill are excluded)

• Bonus deprecation automatically applies to qualified assets unless election out

• Bonus deprecation is not available for assets held outside the US

• Asset acquisitions of “used property” (including IRC § 338(h)(10) and 336(e) transactions) likely eligible with anti-abuse rules that exclude related party acquisitions

• Current view is 100% expensing does not apply to Section 743(b) adjustments (note, guidance on this is still pending)

• Phase down of 100% allowance by 20% per year starting in 2023

Copyright © 2018 Deloitte Development LLC. All rights reserved. 13Tax Reform Roundtable

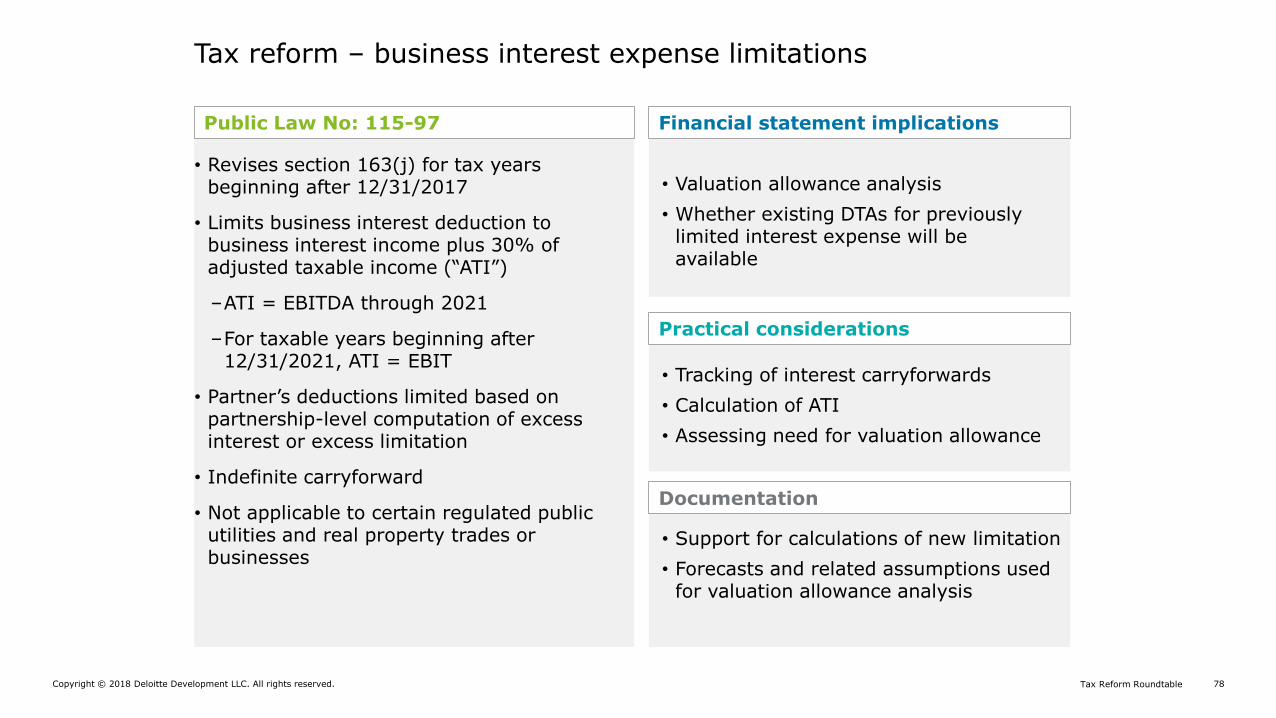

Net business interest expense deduction (IRC § 163(j))

• “Business interest” is defined as interest on indebtedness that is properly allocable to a trade or business; legislative history suggests that all of a corporation’s interest expense is “business interest”

• Business interest expense limited to the sum of business interest income plus 30% of adjusted taxable income (ATI)

• Generally, ATI is the taxable income of the taxpayer without regard to:

−business interest expense or business interest income

−NOLs and

−depreciation and amortization deductions (only through 2021)

• Disallowed business interest expense is treated as paid in the next taxable year

• Disallowed interest carryover is subject to IRC § 382 loss trafficking limitation as pre-change loss in any change in control transaction

• Interest limitation may apply to foreign entities for certain purposes (e.g., computing GILTI and subpart F)

• Exemptions may apply for certain industries (real estate, car dealers, farming, public utilities)

Copyright © 2018 Deloitte Development LLC. All rights reserved. 14Tax Reform Roundtable

Net business interest expense deduction (IRC § 163(j))

• Interest limitation applies at the entity level to limit partnership interest expense deductions (interest allowed is part of non-separately stated partnership income or loss)

• Partner ATI does not include distributive share of partnership income, except for its share of the partnerships unused limitation capacity (so-called “excess taxable income”)

• Disallowed business interest expense is carried forward at the partner level

• Disallowed interest carryforward may only be used to offset income from the partnership generating the carryforward

• A partner may also be subject to limitation with respect to the partner’s own business interest expense

• Similar rules apply to S corporations

Pass-throughs

Copyright © 2018 Deloitte Development LLC. All rights reserved. 15Tax Reform Roundtable

Pass-through business income (IRC § 199A)

• 20% deduction for qualified business income through 2025, subject to certain limitations, including being limited to an amount equal to the greater of:

a) 50% of W-2 wages, or

b) 25% of W-2 wages + 2.5% of qualified property (i.e., certain depreciable property)

• Specified personal services businesses not eligible for the 20% deduction, except for taxpayers with taxable income <$157,500/$315,000 (deduction phased out over next $50k/$100k)

• Personal services businesses include among others healthcare, law, consulting, accounting, athletics, financial services, brokerage services, investing, investment managements, or any business where the principal asset is the reputation or skill of its employees or owners; it does not include engineering or architecture services, as in earlier proposals

Copyright © 2018 Deloitte Development LLC. All rights reserved. 16Tax Reform Roundtable

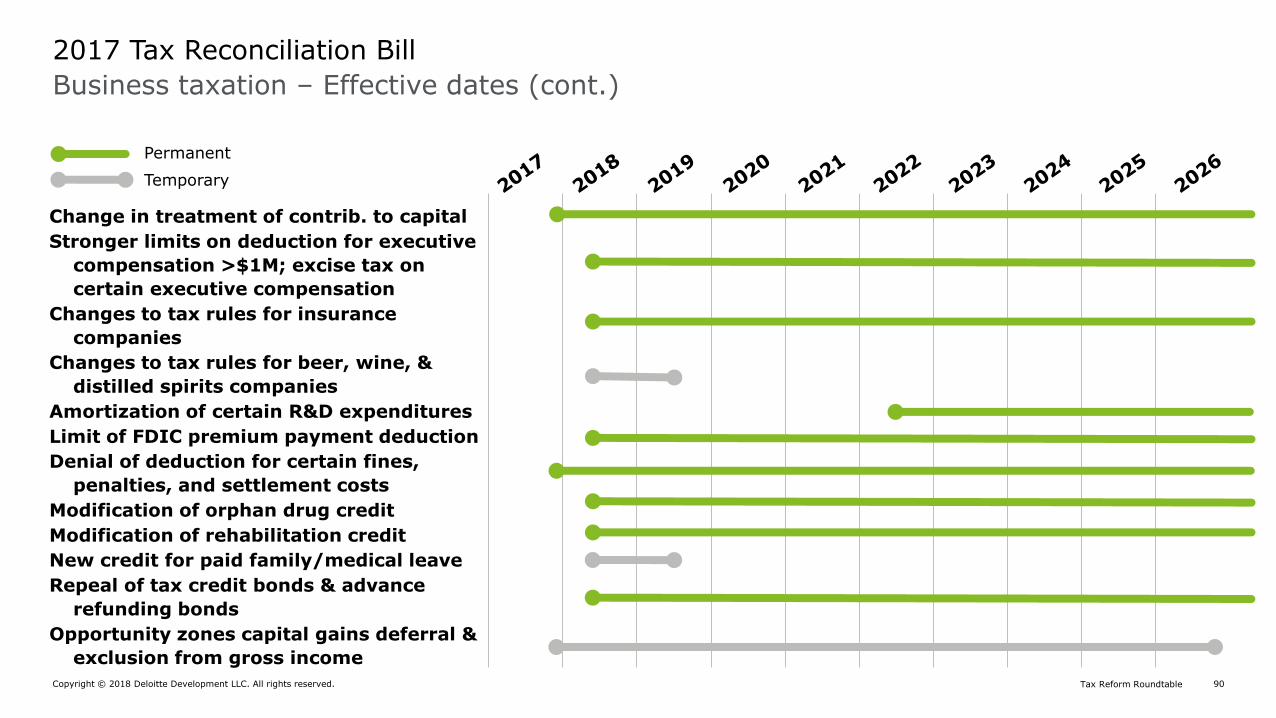

Some other provisions of note:

• Change treatment of contributions to capital1

• Repeal deduction for local lobbying expenses1

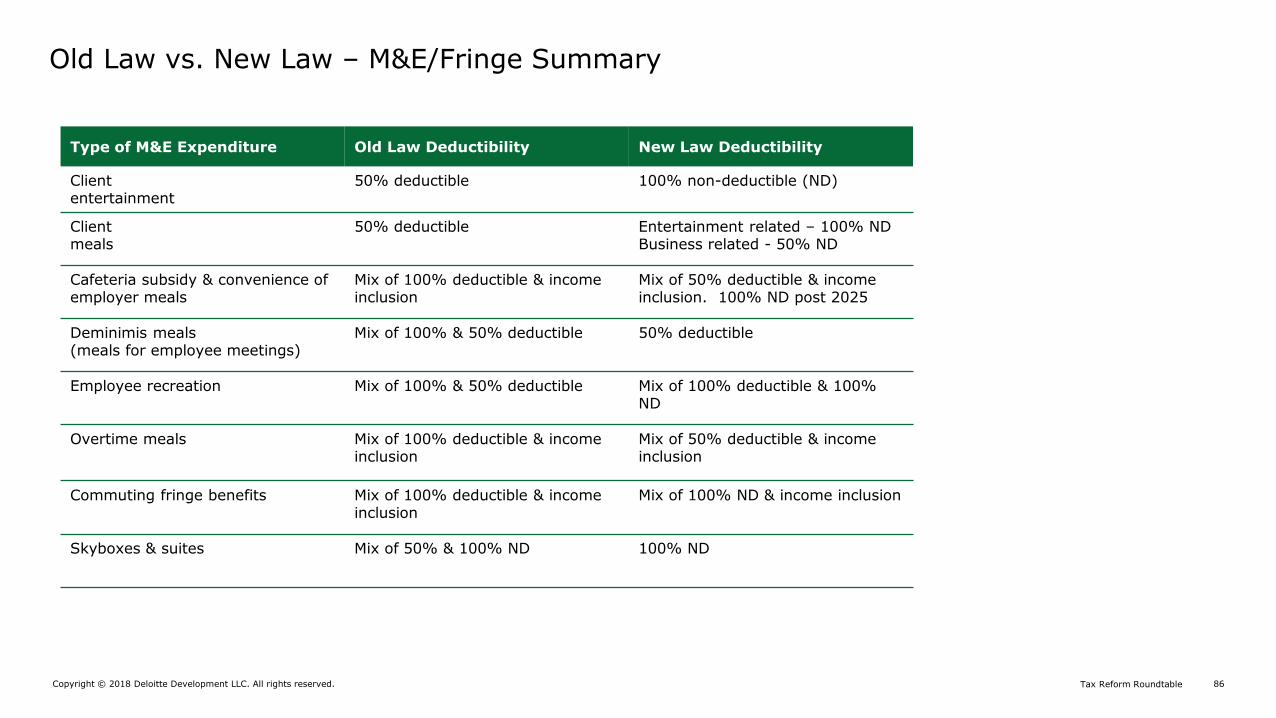

• Repeal deductions for entertainment, amusement or recreation activities, facilities, or membership dues, and most transportation fringe benefits provided to employees; 50% limitation through 2025 on food provided on site for employer’s convenience (then repealed)

• Stronger limits on deduction for executive compensation >$1M; excise tax on certain executive compensation of tax-exempt organizations

• Modify numerous rules specific to insurance companies and to beer, wine and distilled spirits companies

• Require certain R&D expenditures to be amortized over 5 years if done in US; 15 if done abroad2

• Limit deductibility of FDIC premium payments

• Denial of deduction for certain fines, penalties, and settlement costs1

• Modify credit for orphan drug testing, and rehabilitation credit

• Allow temporary tax credit for paid family and medical leave3

• Repeal tax credit bonds and advance refunding bonds

• Create qualified opportunity zones1

1 Effective date of enactment2 Effective for tax years after 12/31/213 Effective for tax years 2018 and 2019

Business taxation

Copyright © 2018 Deloitte Development LLC. All rights reserved. 17Tax Reform Roundtable

Business

• R&D tax credit

• Amortization of advertising expenditures

• LIFO and Lower cost of market accounting methods

• Corporate state and local tax deduction

• Mark to market rules for derivatives

• Entity-level Affordable Care Act (ACA) tax provisions, i.e., medical device tax, “Cadillac tax”

• Tax status of credit unions and cooperatives

Notable current law provisions unchanged

Copyright © 2018 Deloitte Development LLC. All rights reserved. 18Tax Reform Roundtable

Transition tax

Copyright © 2018 Deloitte Development LLC. All rights reserved. 19Tax Reform Roundtable

Transition tax

• Under tax reform, the United States is moving from a system whereby foreign earnings were generally taxed upon receipt of a dividend (deferral) to a system whereby, for most US multi-national corporations (MNCs), a significant portion of foreign earnings will be included on a US tax return currently

• The transition tax is required to transition to the new system. The transition tax requires 10% direct and indirect shareholders to pay tax on the amount of post-1986 untaxed earnings (reduced by certain deficits and offset by a reduced FTC) at a reduced rate of tax

• Corporate transition tax rate:

−15.5 percent on cash and cash-equivalent assets; and

−8 percent on non-cash assets

• There is an election to pay the transition tax in increasing installments over eight years

Copyright © 2018 Deloitte Development LLC. All rights reserved. 20Tax Reform Roundtable

FDII–Foreign-derived intangible income

Copyright © 2018 Deloitte Development LLC. All rights reserved. 21Tax Reform Roundtable

FDII–Foreign-derived intangible income

• FDII is a new type of income category for US corporations

• Many new terms of art have been created for the calculation of FDII, and the calculation itself is complicated

• FDII is income derived from:

−Sales or other dispositions of property to a foreign person for a foreign use;

−A license of IP to a foreign person for a foreign use; and

−Services provided to a person located outside of the United States

• Special rules apply to related-party transactions, but many related-party transactions are likely to qualify if the property or services is for use by a third party outside the United States

Copyright © 2018 Deloitte Development LLC. All rights reserved. 22Tax Reform Roundtable

FDII–Foreign-derived intangible income (cont.)

• US corporations are required to include FDII in gross income but then will be allowed a deduction on the FDII

−From 2018 through 2025, the deduction is 37.5 percent, and starting in 2026 it is 21.875 percent

−When combined with the 21 percent corporate income tax rate, the effective US tax rate on FDII is 13.125 percent for 2018 through 2025 and 16.406 percent starting in 2026

• The deduction is available for US corporations owned by non-US MNCs

Copyright © 2018 Deloitte Development LLC. All rights reserved. 23Tax Reform Roundtable

GILTI–Global intangible low-taxed income

Copyright © 2018 Deloitte Development LLC. All rights reserved. 24Tax Reform Roundtable

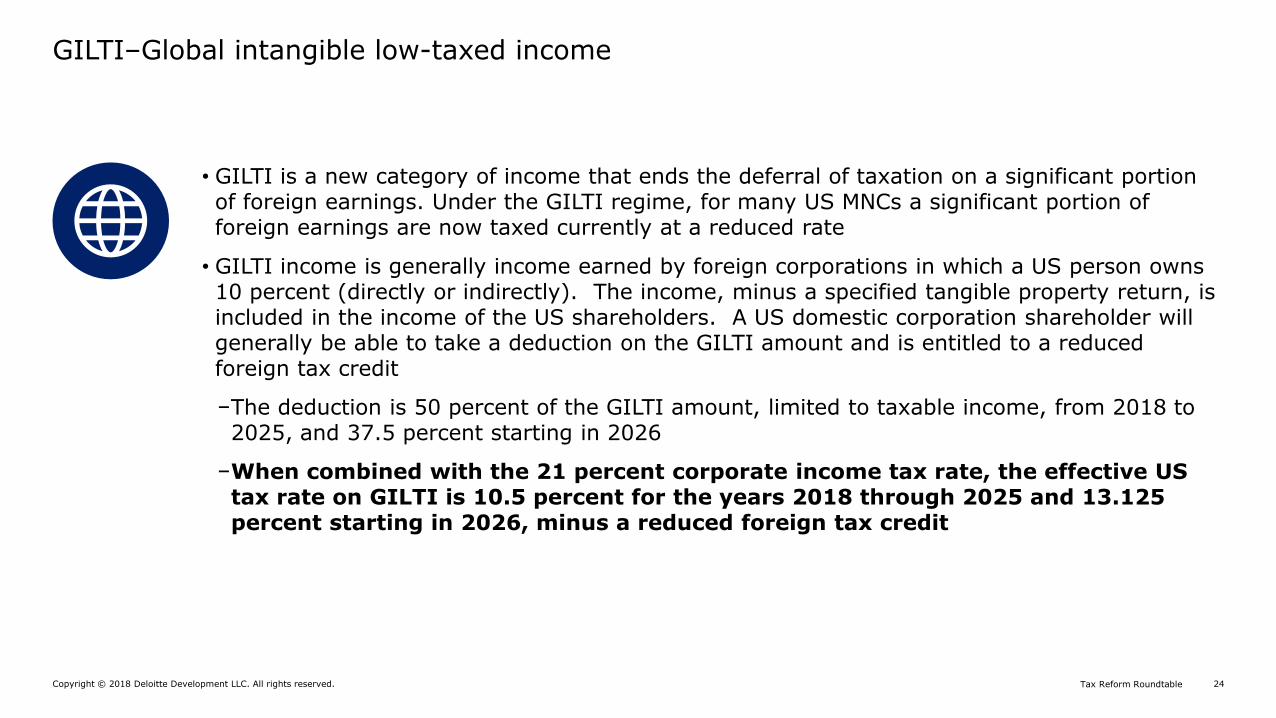

GILTI–Global intangible low-taxed income

• GILTI is a new category of income that ends the deferral of taxation on a significant portion of foreign earnings. Under the GILTI regime, for many US MNCs a significant portion of foreign earnings are now taxed currently at a reduced rate

• GILTI income is generally income earned by foreign corporations in which a US person owns 10 percent (directly or indirectly). The income, minus a specified tangible property return, is included in the income of the US shareholders. A US domestic corporation shareholder will generally be able to take a deduction on the GILTI amount and is entitled to a reduced foreign tax credit

−The deduction is 50 percent of the GILTI amount, limited to taxable income, from 2018 to 2025, and 37.5 percent starting in 2026

−When combined with the 21 percent corporate income tax rate, the effective US tax rate on GILTI is 10.5 percent for the years 2018 through 2025 and 13.125 percent starting in 2026, minus a reduced foreign tax credit

Copyright © 2018 Deloitte Development LLC. All rights reserved. 25Tax Reform Roundtable

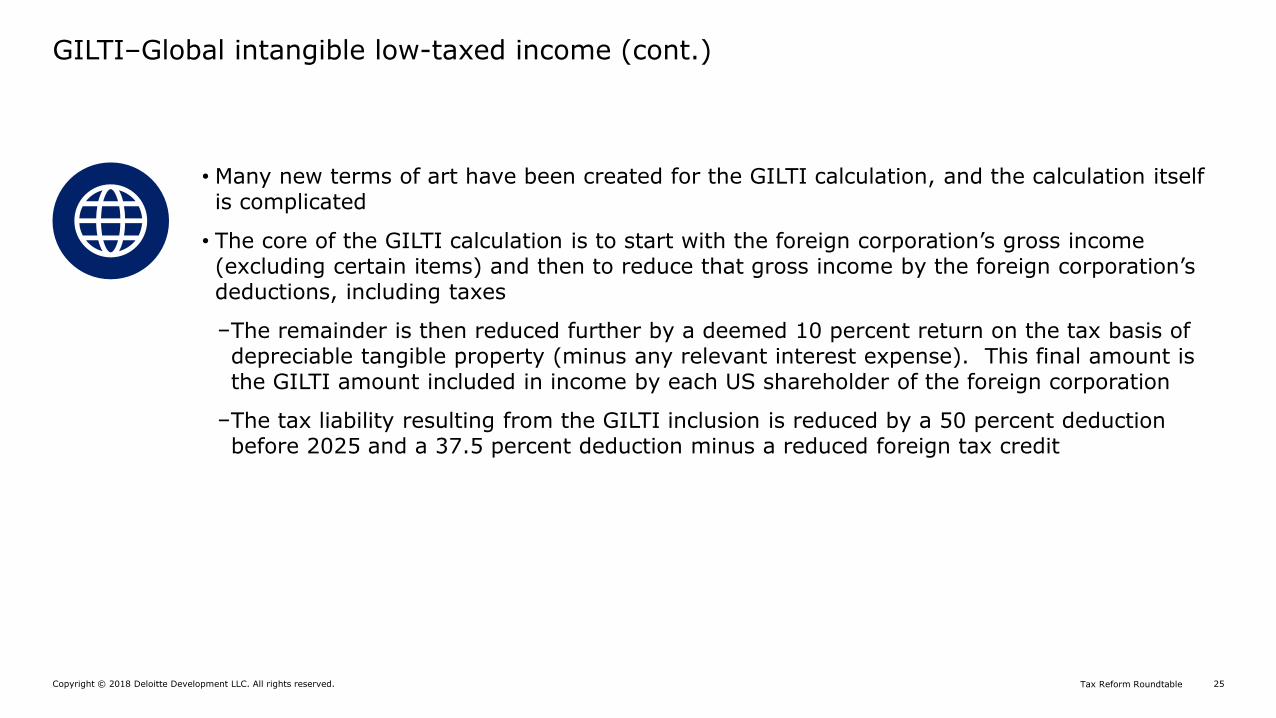

GILTI–Global intangible low-taxed income (cont.)

• Many new terms of art have been created for the GILTI calculation, and the calculation itself is complicated

• The core of the GILTI calculation is to start with the foreign corporation’s gross income (excluding certain items) and then to reduce that gross income by the foreign corporation’s deductions, including taxes

−The remainder is then reduced further by a deemed 10 percent return on the tax basis of depreciable tangible property (minus any relevant interest expense). This final amount is the GILTI amount included in income by each US shareholder of the foreign corporation

−The tax liability resulting from the GILTI inclusion is reduced by a 50 percent deduction before 2025 and a 37.5 percent deduction minus a reduced foreign tax credit

Copyright © 2018 Deloitte Development LLC. All rights reserved. 26Tax Reform Roundtable

BEAT–Base erosion anti-abuse tax

Copyright © 2018 Deloitte Development LLC. All rights reserved. 27Tax Reform Roundtable

BEAT–Base erosion and anti-abuse tax

• BEAT could apply to both US-parented and non-US parented MNCs. BEAT will potentially apply to a US corporation or the US branch of a foreign corporation that makes payments to a foreign related party for which a deduction is allowable (i.e., payments included in SG&A and below). Payments included in COGS are not subject to BEAT

• BEAT is an alternative tax computation. The US company is required to pay the greater of its regular tax liability or its BEAT tax liability

• BEAT applies only if the US corporation or branch has a “base erosion percentage” of 3 percent or more (2 percent for certain banks and securities dealers) and the US corporation or branch has a three-year average annual gross receipts amount of greater than $500 million

−Special aggregation principles are used for these computations, which may eliminate non-US MNCs groups with a US presence of less than $500 million

−Special rules apply to determine the base erosion percentage

Copyright © 2018 Deloitte Development LLC. All rights reserved. 28Tax Reform Roundtable

Big picture changes in the tax system

Copyright © 2018 Deloitte Development LLC. All rights reserved. 29Tax Reform Roundtable

USCo

Foreign Holdco

U.S. Goods

LRDsDistributorsForeign Principal

EU Goods

US Customers

EU Customers

Principal

LRD

Corporation

Disregarded Entity

Legal Flow of Goods

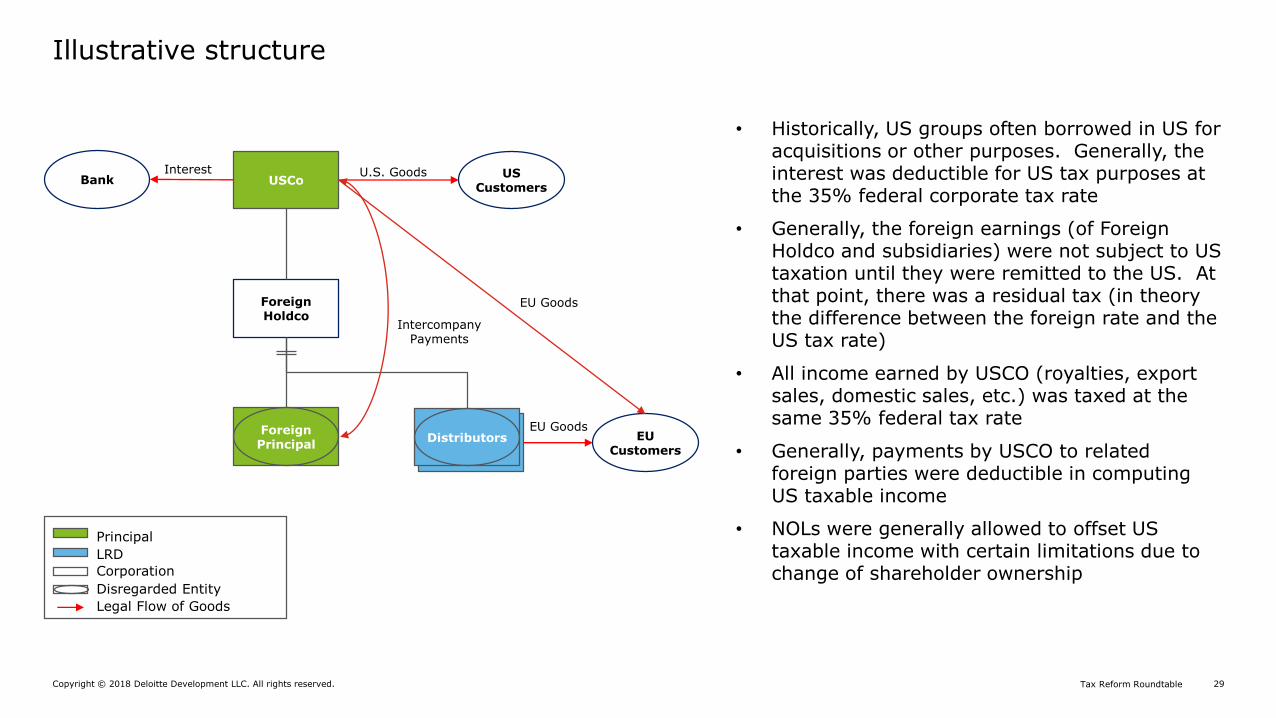

• Historically, US groups often borrowed in US for acquisitions or other purposes. Generally, the interest was deductible for US tax purposes at the 35% federal corporate tax rate

• Generally, the foreign earnings (of Foreign Holdco and subsidiaries) were not subject to US taxation until they were remitted to the US. At that point, there was a residual tax (in theory the difference between the foreign rate and the US tax rate)

• All income earned by USCO (royalties, export sales, domestic sales, etc.) was taxed at the same 35% federal tax rate

• Generally, payments by USCO to related foreign parties were deductible in computing US taxable income

• NOLs were generally allowed to offset US taxable income with certain limitations due to change of shareholder ownership

Intercompany Payments

BankInterest

EU Goods

Illustrative structure

Copyright © 2018 Deloitte Development LLC. All rights reserved. 30Tax Reform Roundtable

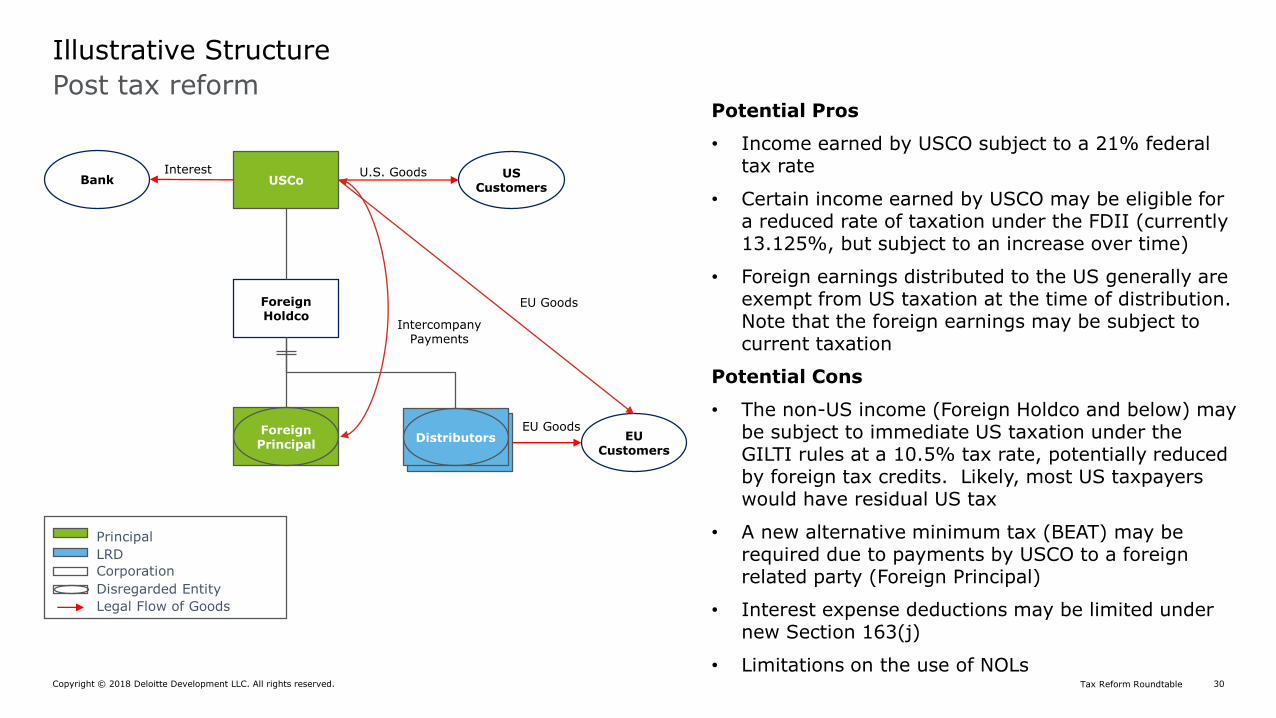

Potential Pros

• Income earned by USCO subject to a 21% federal tax rate

• Certain income earned by USCO may be eligible for a reduced rate of taxation under the FDII (currently 13.125%, but subject to an increase over time)

• Foreign earnings distributed to the US generally are exempt from US taxation at the time of distribution. Note that the foreign earnings may be subject to current taxation

Potential Cons

• The non-US income (Foreign Holdco and below) may be subject to immediate US taxation under the GILTI rules at a 10.5% tax rate, potentially reduced by foreign tax credits. Likely, most US taxpayers would have residual US tax

• A new alternative minimum tax (BEAT) may be required due to payments by USCO to a foreign related party (Foreign Principal)

• Interest expense deductions may be limited under new Section 163(j)

• Limitations on the use of NOLs

Post tax reform

Illustrative Structure

Principal

LRD

Corporation

Disregarded Entity

Legal Flow of Goods

USCo

Foreign Holdco

U.S. Goods

LRDsDistributorsForeign Principal

EU Goods

US Customers

EU Customers

Intercompany Payments

BankInterest

EU Goods

Copyright © 2018 Deloitte Development LLC. All rights reserved. 31Tax Reform Roundtable

Impact to employee related programs/expenses

Copyright © 2018 Deloitte Development LLC. All rights reserved. 32Tax Reform Roundtable

Impact on qualified retirement plan funding

Change in law

• Corporate income tax rate reduced from maximum 35% rate to flat 21% rate for tax years beginning after 2017

• Though not a change, applicable funding rules allow corporate tax deduction for tax year 2017 if funding contribution made in 2018 before extended due date of 2017 return

Considerations

• 2017 corporate deduction generally more valuable than 2018 deduction; allows it to be taken at 35% rate instead of 21% (e.g., $100M contribution results in $35M deduction vs. $21M)

• Additional contribution should be balanced with company’s cash requirements, financing cost, potentially reduced PBGC premiums, and opportunity for pension planning, including:

‒ SERP shift – reduce pension liability under “excess” nonqualified deferred compensation plan by increasing qualified pension benefits for certain employees

‒ Derisking – additional pension funding allows plan to cash out benefits of terminated vested participants, decreasing PBGC liability and reducing volatility

‒ Plan termination – additional pension funding can ease closing of plan, payout of assets to participants

• Additional deductible matching or profit sharing contributions under a defined contribution plan may be possible up to certain IRS limits

Next steps

• Review plan funding levels and cashflow requirements to determine feasibility of additional contribution(s)

• If feasible, determine best use of funding – SERP shift, derisking, termination, or improving funding position of plan

Copyright © 2018 Deloitte Development LLC. All rights reserved. 33Tax Reform Roundtable

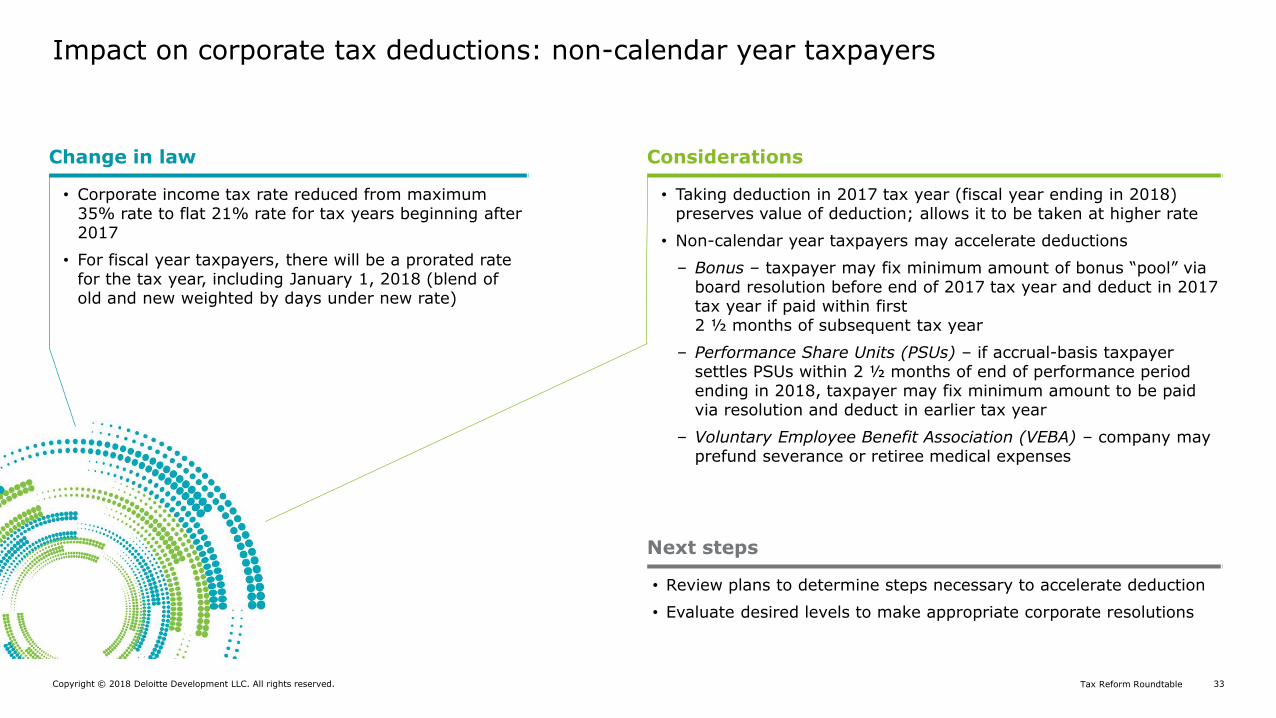

Impact on corporate tax deductions: non-calendar year taxpayers

Change in law

• Corporate income tax rate reduced from maximum 35% rate to flat 21% rate for tax years beginning after 2017

• For fiscal year taxpayers, there will be a prorated rate for the tax year, including January 1, 2018 (blend of old and new weighted by days under new rate)

Considerations

• Taking deduction in 2017 tax year (fiscal year ending in 2018) preserves value of deduction; allows it to be taken at higher rate

• Non-calendar year taxpayers may accelerate deductions

‒ Bonus – taxpayer may fix minimum amount of bonus “pool” via board resolution before end of 2017 tax year and deduct in 2017 tax year if paid within first 2 ½ months of subsequent tax year

‒ Performance Share Units (PSUs) – if accrual-basis taxpayer settles PSUs within 2 ½ months of end of performance period ending in 2018, taxpayer may fix minimum amount to be paid via resolution and deduct in earlier tax year

‒ Voluntary Employee Benefit Association (VEBA) – company may prefund severance or retiree medical expenses

Next steps

• Review plans to determine steps necessary to accelerate deduction

• Evaluate desired levels to make appropriate corporate resolutions

Copyright © 2018 Deloitte Development LLC. All rights reserved. 34Tax Reform Roundtable

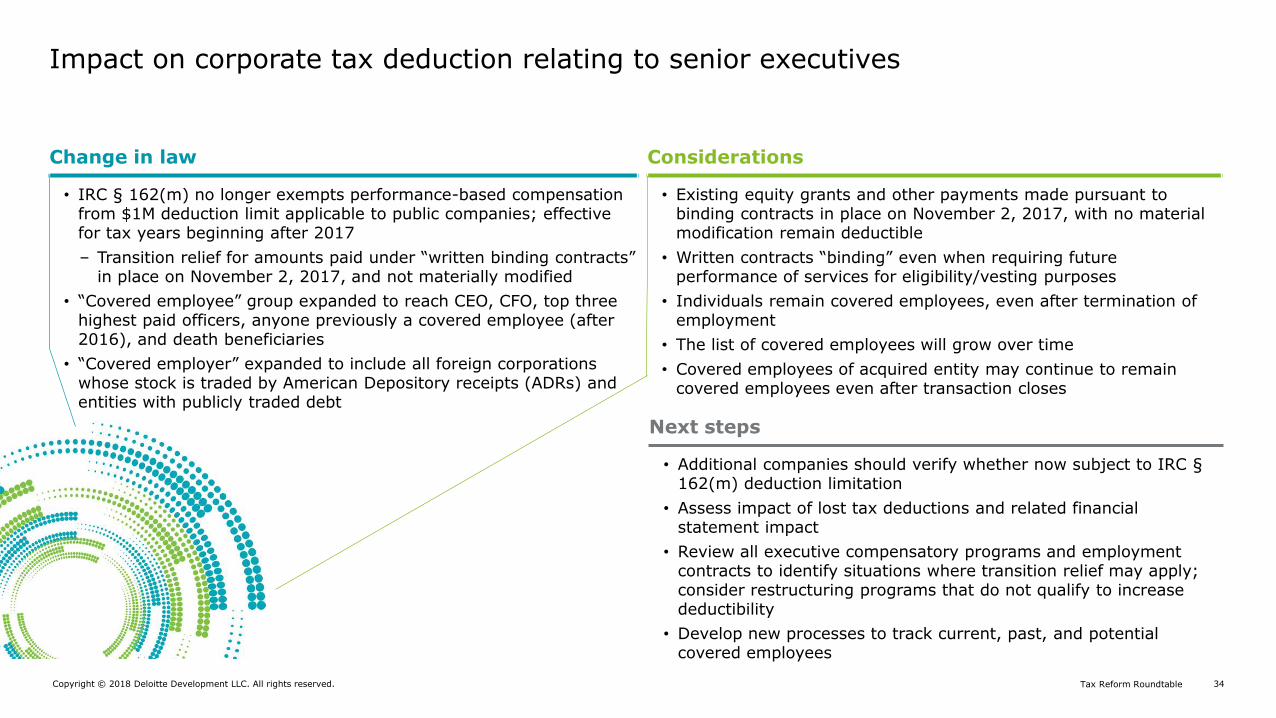

Impact on corporate tax deduction relating to senior executives

Change in law

• IRC § 162(m) no longer exempts performance-based compensation from $1M deduction limit applicable to public companies; effective for tax years beginning after 2017

‒ Transition relief for amounts paid under “written binding contracts” in place on November 2, 2017, and not materially modified

• “Covered employee” group expanded to reach CEO, CFO, top three highest paid officers, anyone previously a covered employee (after 2016), and death beneficiaries

• “Covered employer” expanded to include all foreign corporations whose stock is traded by American Depository receipts (ADRs) and entities with publicly traded debt

Considerations

• Existing equity grants and other payments made pursuant to binding contracts in place on November 2, 2017, with no material modification remain deductible

• Written contracts “binding” even when requiring future performance of services for eligibility/vesting purposes

• Individuals remain covered employees, even after termination of employment

• The list of covered employees will grow over time

• Covered employees of acquired entity may continue to remain covered employees even after transaction closes

Next steps

• Additional companies should verify whether now subject to IRC §162(m) deduction limitation

• Assess impact of lost tax deductions and related financial statement impact

• Review all executive compensatory programs and employment contracts to identify situations where transition relief may apply; consider restructuring programs that do not qualify to increase deductibility

• Develop new processes to track current, past, and potential covered employees

Copyright © 2018 Deloitte Development LLC. All rights reserved. 35Tax Reform Roundtable

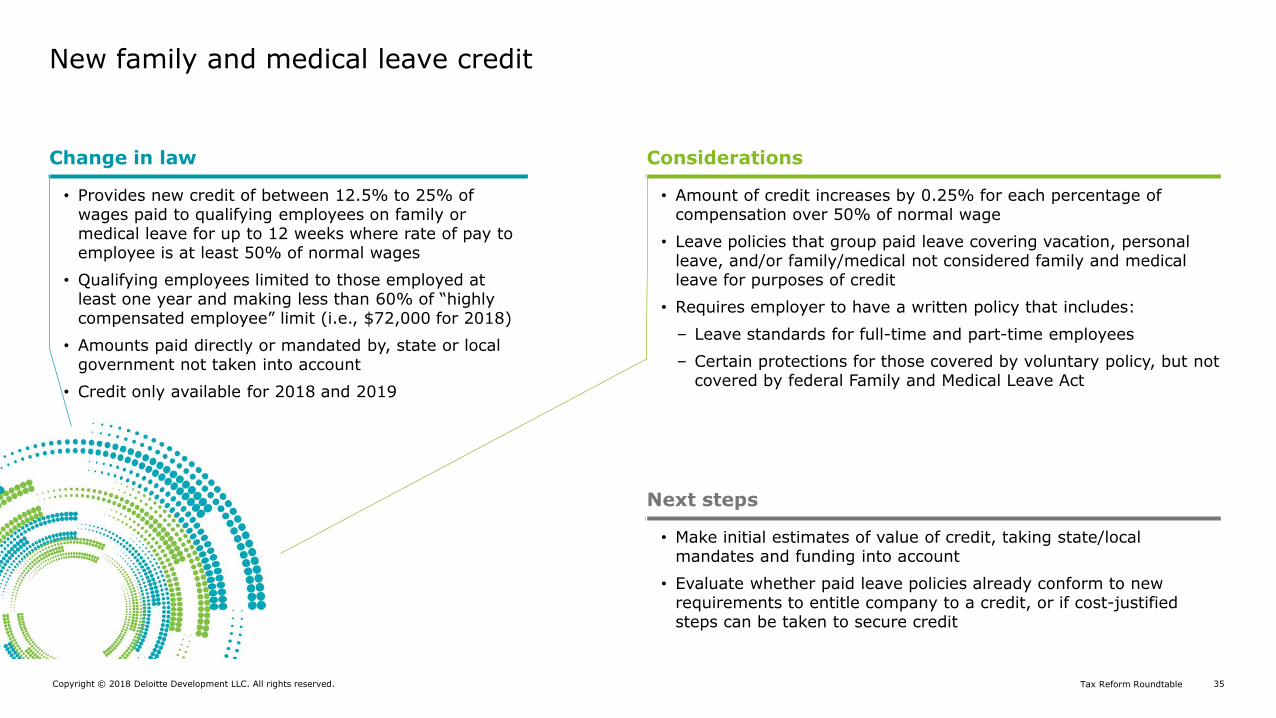

New family and medical leave credit

Change in law

• Provides new credit of between 12.5% to 25% of wages paid to qualifying employees on family or medical leave for up to 12 weeks where rate of pay to employee is at least 50% of normal wages

• Qualifying employees limited to those employed at least one year and making less than 60% of “highly compensated employee” limit (i.e., $72,000 for 2018)

• Amounts paid directly or mandated by, state or local government not taken into account

• Credit only available for 2018 and 2019

Considerations

• Amount of credit increases by 0.25% for each percentage of compensation over 50% of normal wage

• Leave policies that group paid leave covering vacation, personal leave, and/or family/medical not considered family and medical leave for purposes of credit

• Requires employer to have a written policy that includes:

‒ Leave standards for full-time and part-time employees

‒ Certain protections for those covered by voluntary policy, but not covered by federal Family and Medical Leave Act

Next steps

• Make initial estimates of value of credit, taking state/local mandates and funding into account

• Evaluate whether paid leave policies already conform to new requirements to entitle company to a credit, or if cost-justified steps can be taken to secure credit

Copyright © 2018 Deloitte Development LLC. All rights reserved. 36Tax Reform Roundtable

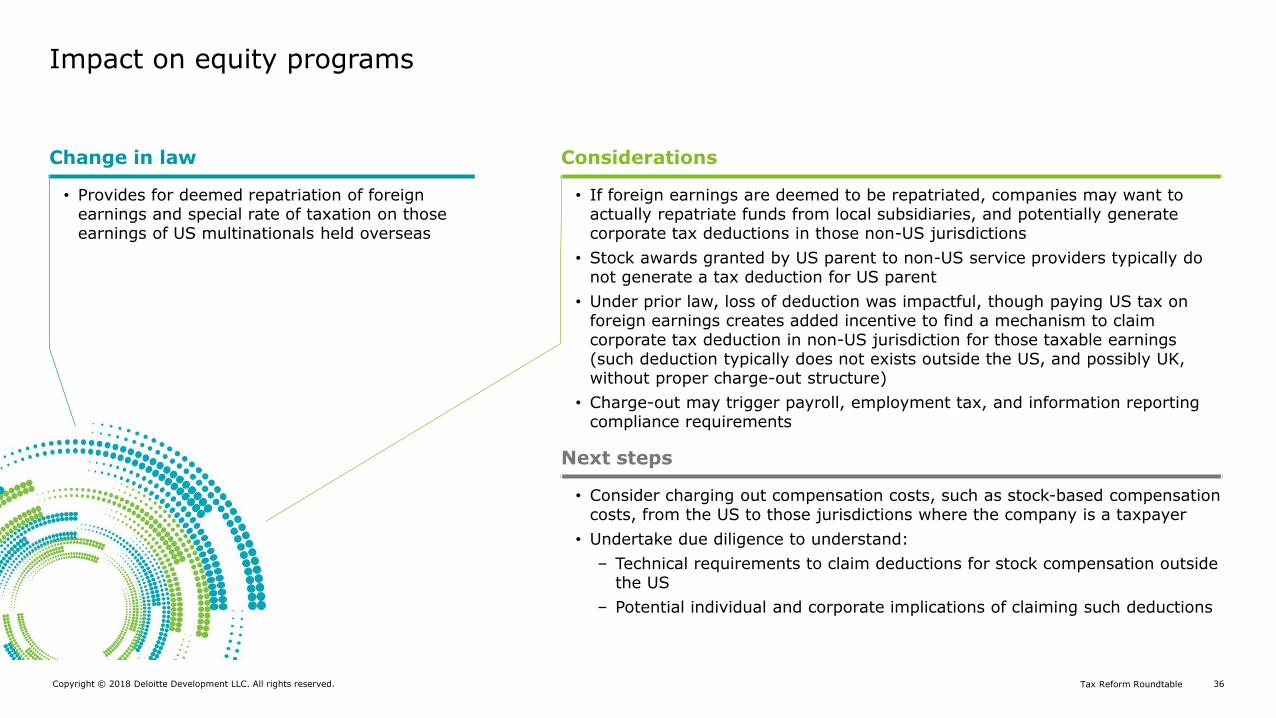

Impact on equity programs

Change in law

• Provides for deemed repatriation of foreign earnings and special rate of taxation on those earnings of US multinationals held overseas

Considerations

• If foreign earnings are deemed to be repatriated, companies may want to actually repatriate funds from local subsidiaries, and potentially generate corporate tax deductions in those non-US jurisdictions

• Stock awards granted by US parent to non-US service providers typically do not generate a tax deduction for US parent

• Under prior law, loss of deduction was impactful, though paying US tax on foreign earnings creates added incentive to find a mechanism to claim corporate tax deduction in non-US jurisdiction for those taxable earnings (such deduction typically does not exists outside the US, and possibly UK, without proper charge-out structure)

• Charge-out may trigger payroll, employment tax, and information reporting compliance requirements

Next steps

• Consider charging out compensation costs, such as stock-based compensation costs, from the US to those jurisdictions where the company is a taxpayer

• Undertake due diligence to understand:

‒ Technical requirements to claim deductions for stock compensation outside the US

‒ Potential individual and corporate implications of claiming such deductions

Copyright © 2018 Deloitte Development LLC. All rights reserved. 37Tax Reform Roundtable

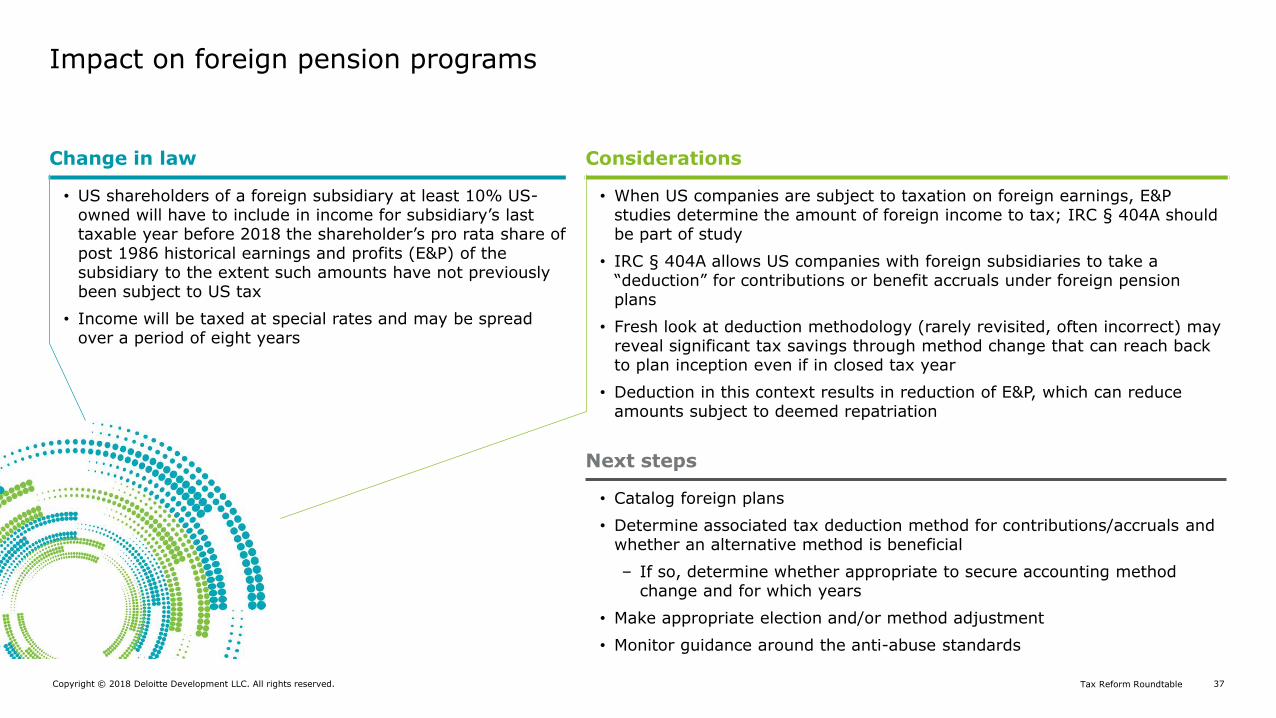

Impact on foreign pension programs

Change in law

• US shareholders of a foreign subsidiary at least 10% US-owned will have to include in income for subsidiary’s last taxable year before 2018 the shareholder’s pro rata share of post 1986 historical earnings and profits (E&P) of the subsidiary to the extent such amounts have not previously been subject to US tax

• Income will be taxed at special rates and may be spread over a period of eight years

Considerations

• When US companies are subject to taxation on foreign earnings, E&P studies determine the amount of foreign income to tax; IRC § 404A should be part of study

• IRC § 404A allows US companies with foreign subsidiaries to take a “deduction” for contributions or benefit accruals under foreign pension plans

• Fresh look at deduction methodology (rarely revisited, often incorrect) may reveal significant tax savings through method change that can reach back to plan inception even if in closed tax year

• Deduction in this context results in reduction of E&P, which can reduce amounts subject to deemed repatriation

Next steps

• Catalog foreign plans

• Determine associated tax deduction method for contributions/accruals and whether an alternative method is beneficial

‒ If so, determine whether appropriate to secure accounting method change and for which years

• Make appropriate election and/or method adjustment

• Monitor guidance around the anti-abuse standards

Copyright © 2018 Deloitte Development LLC. All rights reserved. 38Tax Reform Roundtable

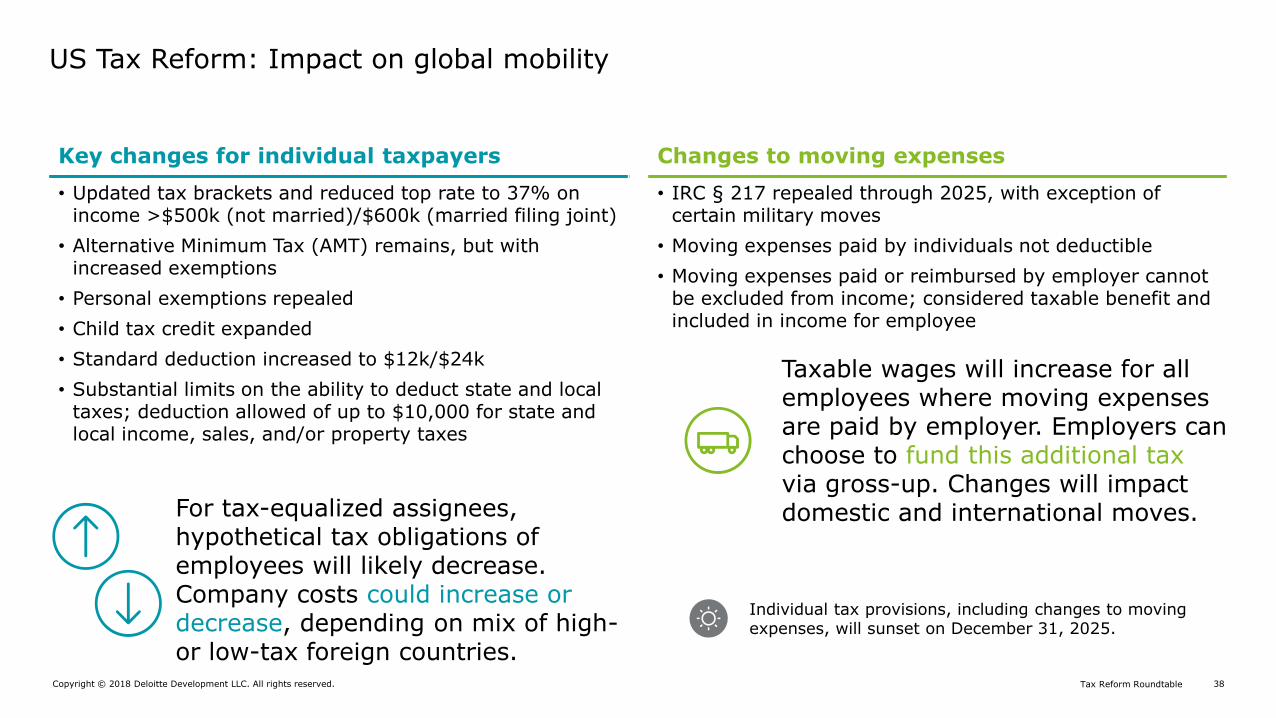

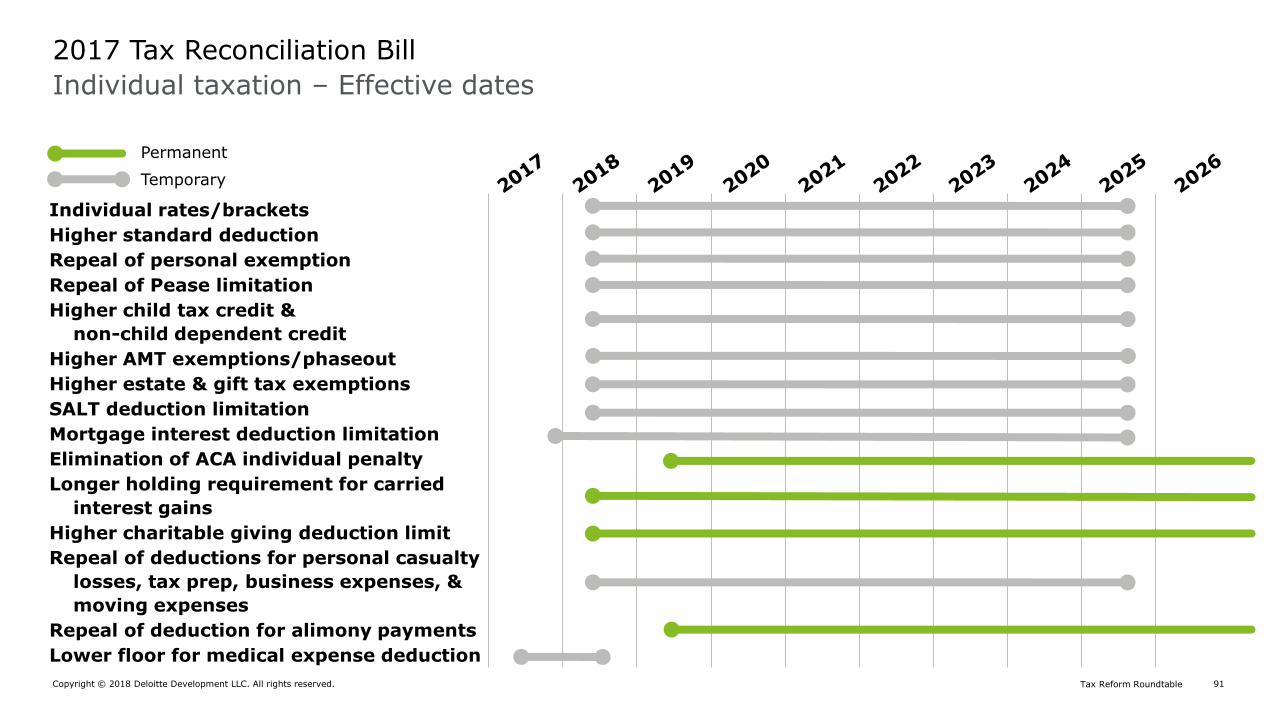

US Tax Reform: Impact on global mobility

Key changes for individual taxpayers

• Updated tax brackets and reduced top rate to 37% on income >$500k (not married)/$600k (married filing joint)

• Alternative Minimum Tax (AMT) remains, but with increased exemptions

• Personal exemptions repealed

• Child tax credit expanded

• Standard deduction increased to $12k/$24k

• Substantial limits on the ability to deduct state and local taxes; deduction allowed of up to $10,000 for state and local income, sales, and/or property taxes

For tax-equalized assignees, hypothetical tax obligations of employees will likely decrease. Company costs could increase or decrease, depending on mix of high-or low-tax foreign countries.

Changes to moving expenses

• IRC § 217 repealed through 2025, with exception of certain military moves

• Moving expenses paid by individuals not deductible

• Moving expenses paid or reimbursed by employer cannot be excluded from income; considered taxable benefit and included in income for employee

Taxable wages will increase for all employees where moving expenses are paid by employer. Employers can choose to fund this additional tax via gross-up. Changes will impact domestic and international moves.

Individual tax provisions, including changes to moving expenses, will sunset on December 31, 2025.

Copyright © 2018 Deloitte Development LLC. All rights reserved. 39Tax Reform Roundtable

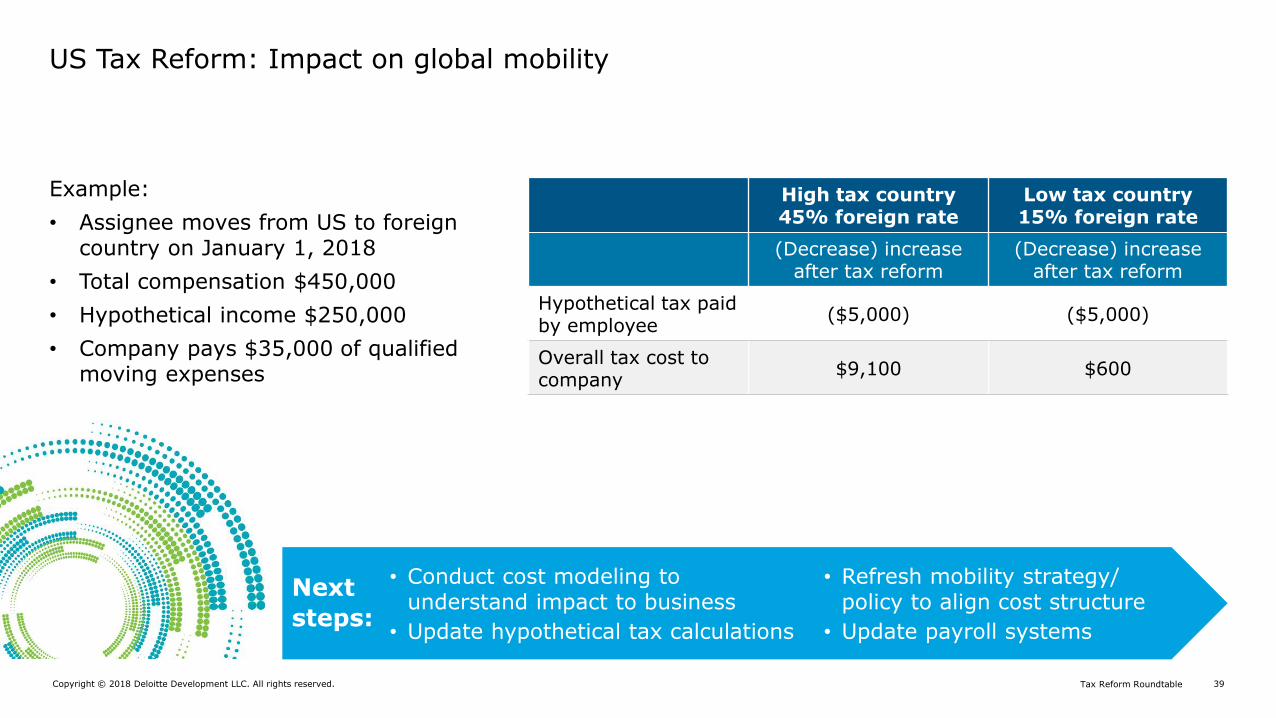

US Tax Reform: Impact on global mobility

Example:

• Assignee moves from US to foreign country on January 1, 2018

• Total compensation $450,000

• Hypothetical income $250,000

• Company pays $35,000 of qualified moving expenses

High tax country 45% foreign rate

Low tax country 15% foreign rate

(Decrease) increase after tax reform

(Decrease) increase after tax reform

Hypothetical tax paid by employee

($5,000) ($5,000)

Overall tax cost to company

$9,100 $600

Next

steps:

• Conduct cost modeling to understand impact to business

• Update hypothetical tax calculations

• Refresh mobility strategy/ policy to align cost structure

• Update payroll systems

Copyright © 2018 Deloitte Development LLC. All rights reserved. 40Tax Reform Roundtable

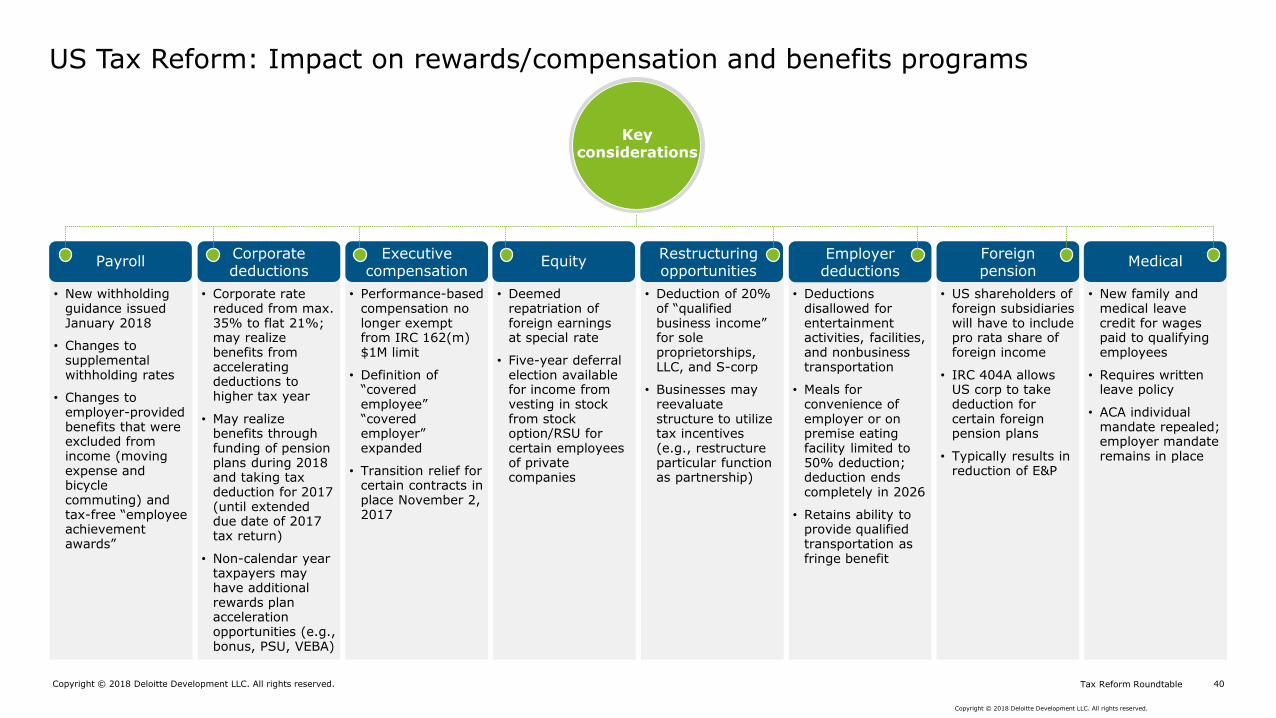

• New withholding guidance issued January 2018

• Changes to supplemental withholding rates

• Changes to employer-provided benefits that were excluded from income (moving expense and bicycle commuting) and tax-free “employee achievement awards”

• Performance-based compensation no longer exempt from IRC 162(m) $1M limit

• Definition of “covered employee” “covered employer” expanded

• Transition relief for certain contracts in place November 2, 2017

• Deemed repatriation of foreign earnings at special rate

• Five-year deferral election available for income from vesting in stock from stock option/RSU for certain employees of private companies

• Deduction of 20% of “qualified business income” for sole proprietorships, LLC, and S-corp

• Businesses may reevaluate structure to utilize tax incentives (e.g., restructure particular function as partnership)

• Deductions disallowed for entertainment activities, facilities, and nonbusiness transportation

• Meals for convenience of employer or on premise eating facility limited to 50% deduction; deduction ends completely in 2026

• Retains ability to provide qualified transportation as fringe benefit

• US shareholders of foreign subsidiaries will have to include pro rata share of foreign income

• IRC 404A allows US corp to take deduction for certain foreign pension plans

• Typically results in reduction of E&P

• New family and medical leave credit for wages paid to qualifying employees

• Requires written leave policy

• ACA individual mandate repealed; employer mandate remains in place

• Corporate rate reduced from max. 35% to flat 21%; may realize benefits from accelerating deductions to higher tax year

• May realize benefits through funding of pension plans during 2018 and taking tax deduction for 2017 (until extended due date of 2017 tax return)

• Non-calendar year taxpayers may have additional rewards plan acceleration opportunities (e.g., bonus, PSU, VEBA)

Copyright © 2018 Deloitte Development LLC. All rights reserved.

PayrollCorporate deductions

Executive compensation

EquityRestructuring opportunities

Employer deductions

Foreign pension

Medical

US Tax Reform: Impact on rewards/compensation and benefits programs

Key considerations

Copyright © 2018 Deloitte Development LLC. All rights reserved. 41Tax Reform Roundtable

Building sustainable processes for new tax law

Copyright © 2018 Deloitte Development LLC. All rights reserved. 42Tax Reform Roundtable

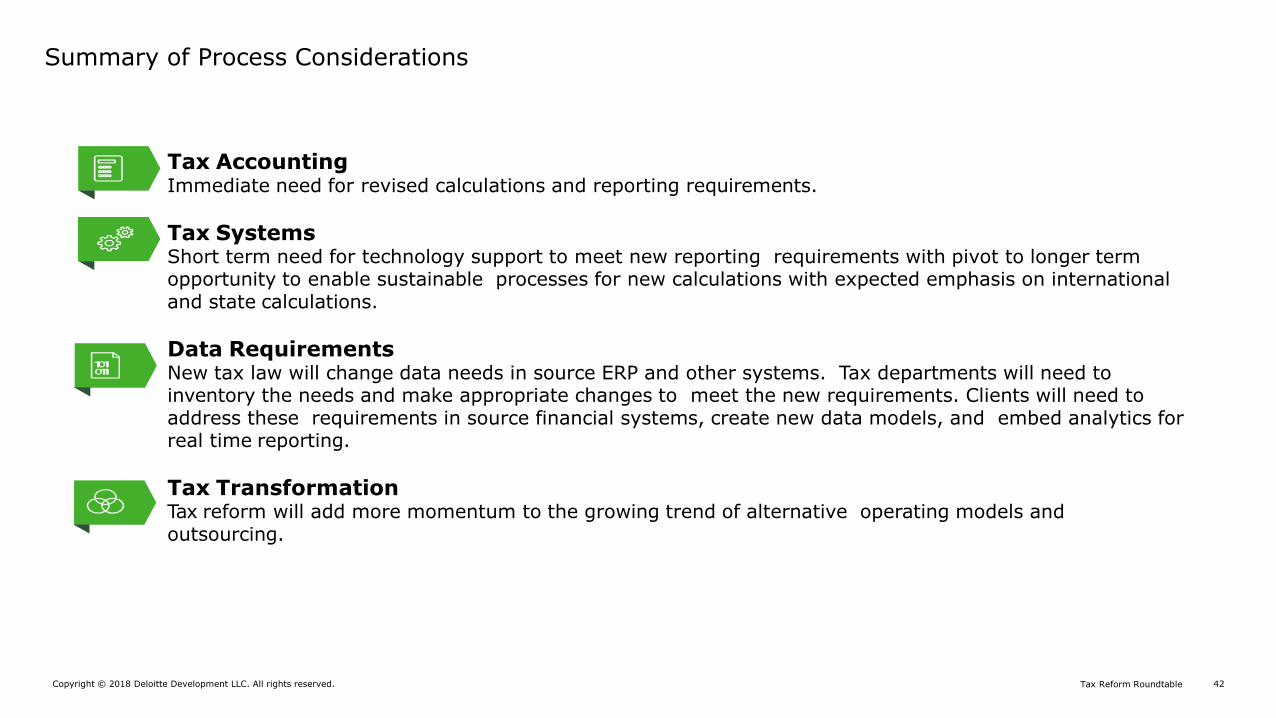

Summary of Process Considerations

Tax AccountingImmediate need for revised calculations and reporting requirements.

Tax SystemsShort term need for technology support to meet new reporting requirements with pivot to longer term opportunity to enable sustainable processes for new calculations with expected emphasis on international and state calculations.

Data RequirementsNew tax law will change data needs in source ERP and other systems. Tax departments will need to inventory the needs and make appropriate changes to meet the new requirements. Clients will need to address these requirements in source financial systems, create new data models, and embed analytics for real time reporting.

Tax TransformationTax reform will add more momentum to the growing trend of alternative operating models andoutsourcing.

Copyright © 2018 Deloitte Development LLC. All rights reserved. 43Tax Reform Roundtable

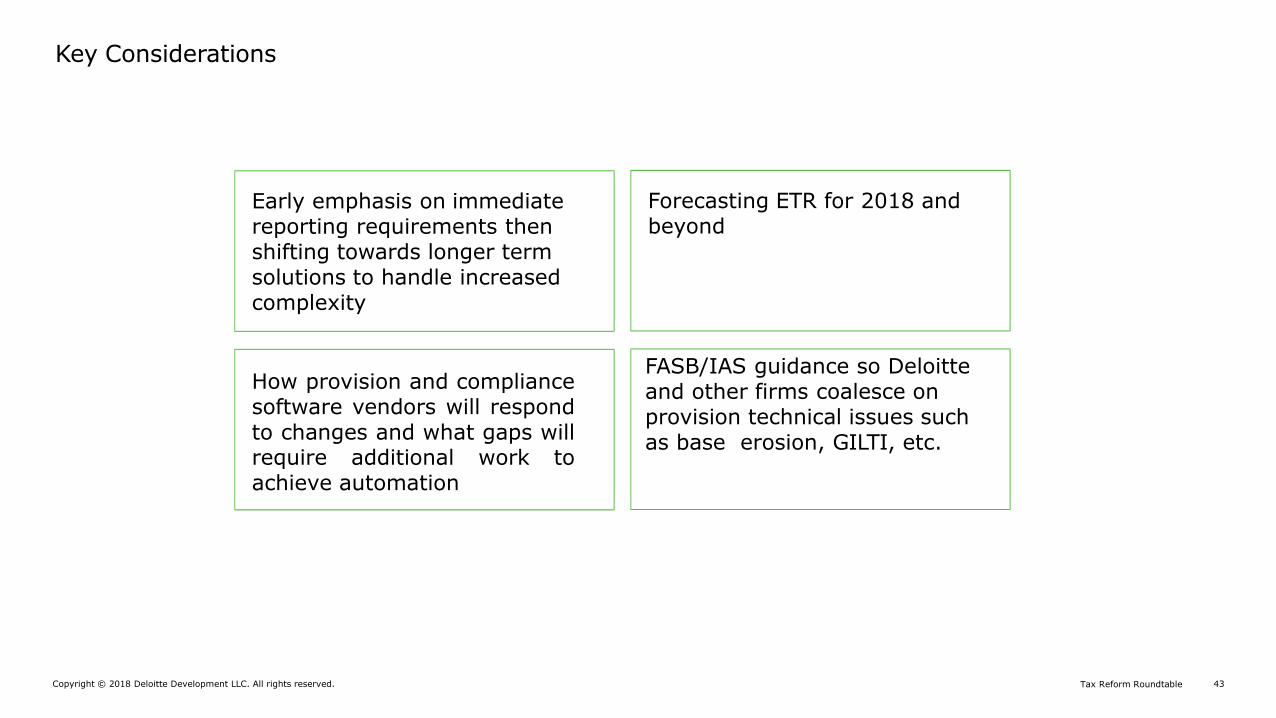

Key Considerations

Forecasting ETR for 2018 and beyond

Early emphasis on immediate reporting requirements then shifting towards longer term solutions to handle increased complexity

How provision and compliancesoftware vendors will respondto changes and what gaps willrequire additional work toachieve automation

FASB/IAS guidance so Deloitte and other firms coalesce on provision technical issues such as base erosion, GILTI, etc.

Copyright © 2018 Deloitte Development LLC. All rights reserved. 44Tax Reform Roundtable

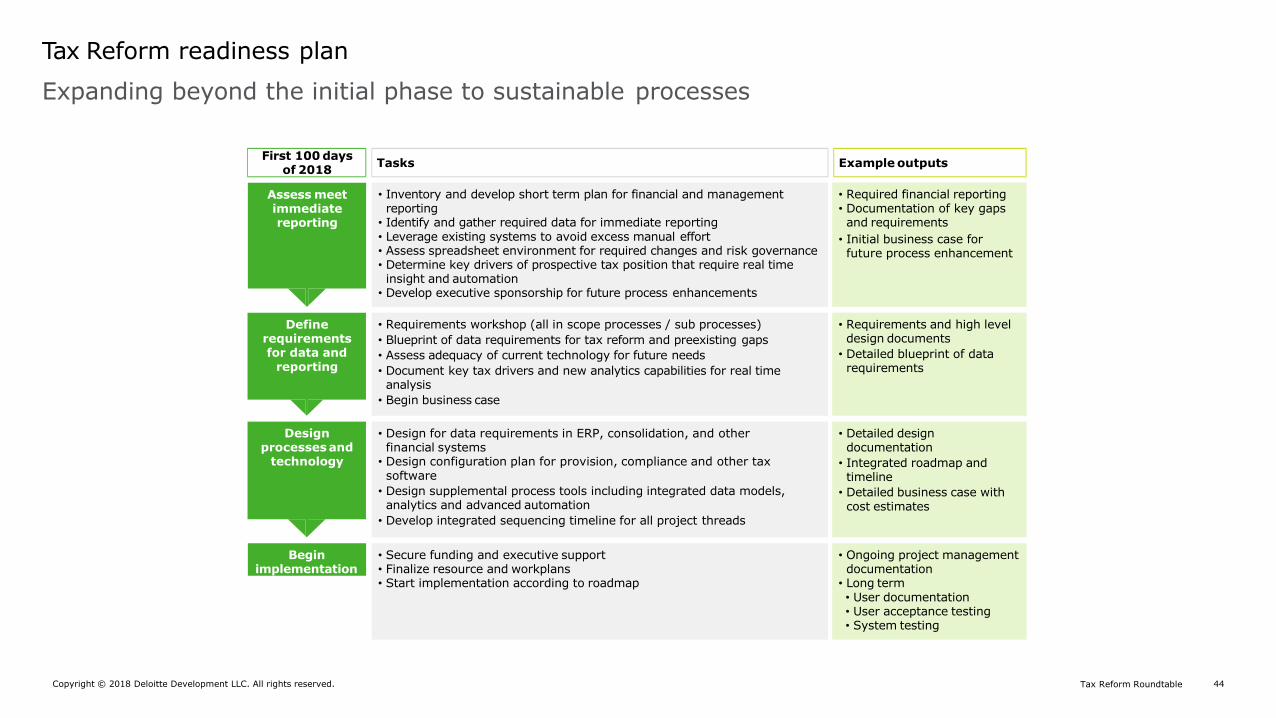

Expanding beyond the initial phase to sustainable processes

Tax Reform readiness plan

• Required financial reporting• Documentation of key gaps and requirements

• Initial business case for future process enhancement

• Requirements and high level design documents

• Detailed blueprint of data requirements

• Detailed design documentation

• Integrated roadmap and timeline

• Detailed business case with cost estimates

• Ongoing project management documentation

• Long term• User documentation• User acceptance testing• System testing

• Inventory and develop short term plan for financial and management reporting

• Identify and gather required data for immediate reporting• Leverage existing systems to avoid excess manual effort• Assess spreadsheet environment for required changes and risk governance• Determine key drivers of prospective tax position that require real time insight and automation

• Develop executive sponsorship for future process enhancements

• Requirements workshop (all in scope processes / sub processes)

• Blueprint of data requirements for tax reform and preexisting gaps

• Assess adequacy of current technology for future needs

• Document key tax drivers and new analytics capabilities for real time analysis

• Begin business case

• Design for data requirements in ERP, consolidation, and other financial systems

• Design configuration plan for provision, compliance and other tax software

• Design supplemental process tools including integrated data models, analytics and advanced automation

• Develop integrated sequencing timeline for all project threads

• Secure funding and executive support• Finalize resource and workplans• Start implementation according to roadmap

Begin implementation

Define requirements for data and

reporting

Design processesand

technology

First 100 daysof 2018

Assess meet immediate reporting

Tasks Example outputs

Copyright © 2018 Deloitte Development LLC. All rights reserved. 45Tax Reform Roundtable

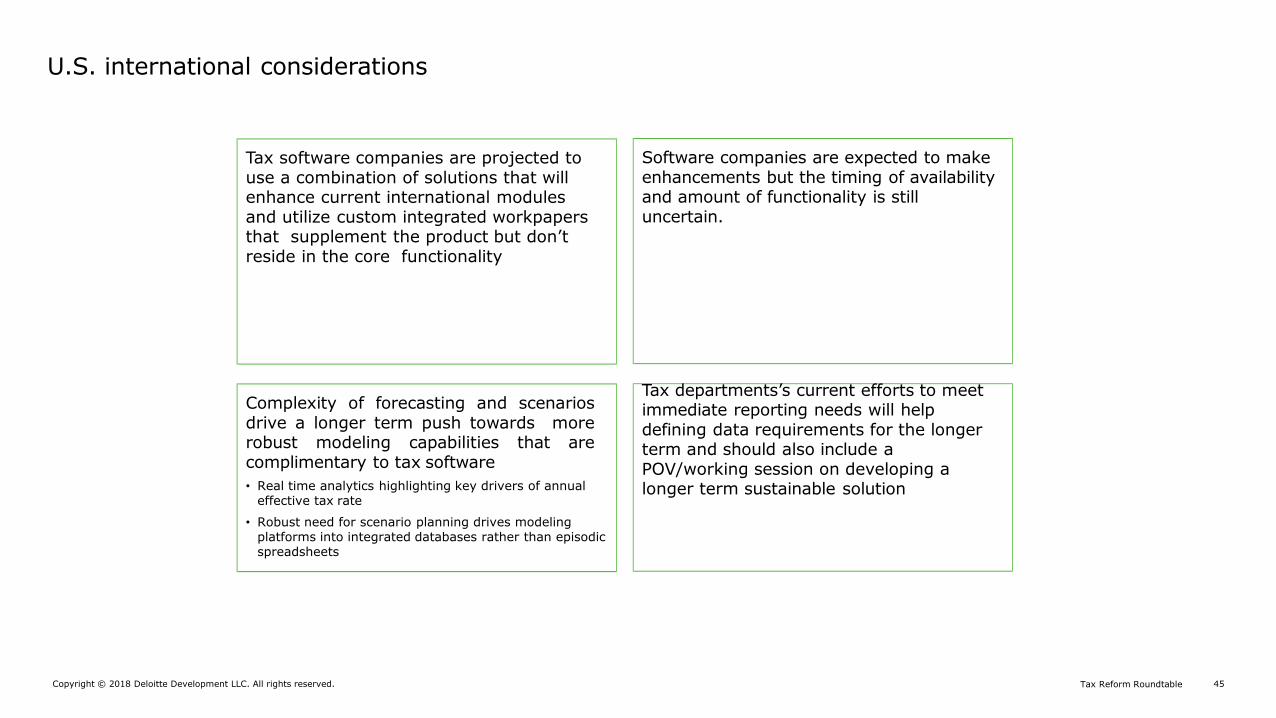

U.S. international considerations

Tax software companies are projected to use a combination of solutions that will enhance current international modules and utilize custom integrated workpapers that supplement the product but don’t reside in the core functionality

Complexity of forecasting and scenariosdrive a longer term push towards morerobust modeling capabilities that arecomplimentary to tax software

• Real time analytics highlighting key drivers of annual effective tax rate

• Robust need for scenario planning drives modeling platforms into integrated databases rather than episodic spreadsheets

Software companies are expected to make enhancements but the timing of availability and amount of functionality is still uncertain.

Tax departments’s current efforts to meet immediate reporting needs will help defining data requirements for the longer term and should also include a POV/working session on developing a longer term sustainable solution

Copyright © 2018 Deloitte Development LLC. All rights reserved. 46Tax Reform Roundtable

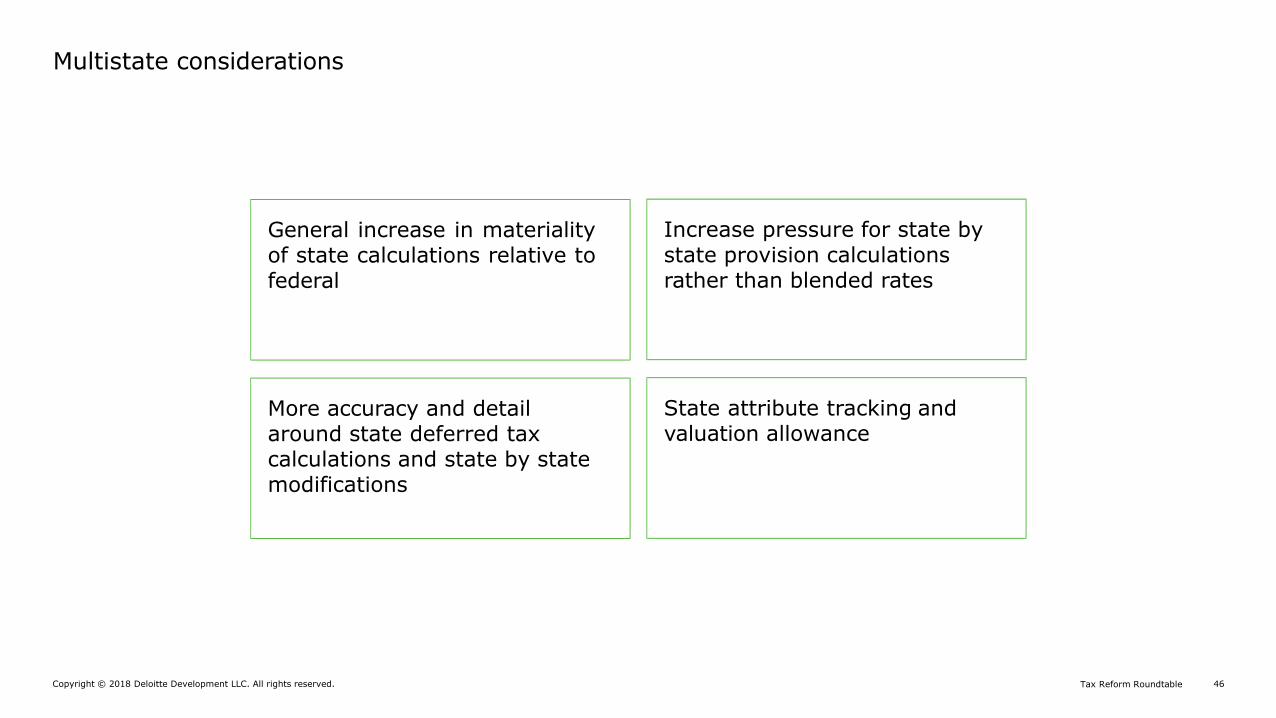

Multistate considerations

General increase in materialityof state calculations relative tofederal

Increase pressure for state by state provision calculations rather than blended rates

More accuracy and detail around state deferred tax calculations and state by state modifications

State attribute tracking and valuation allowance

Copyright © 2018 Deloitte Development LLC. All rights reserved. 47Tax Reform Roundtable

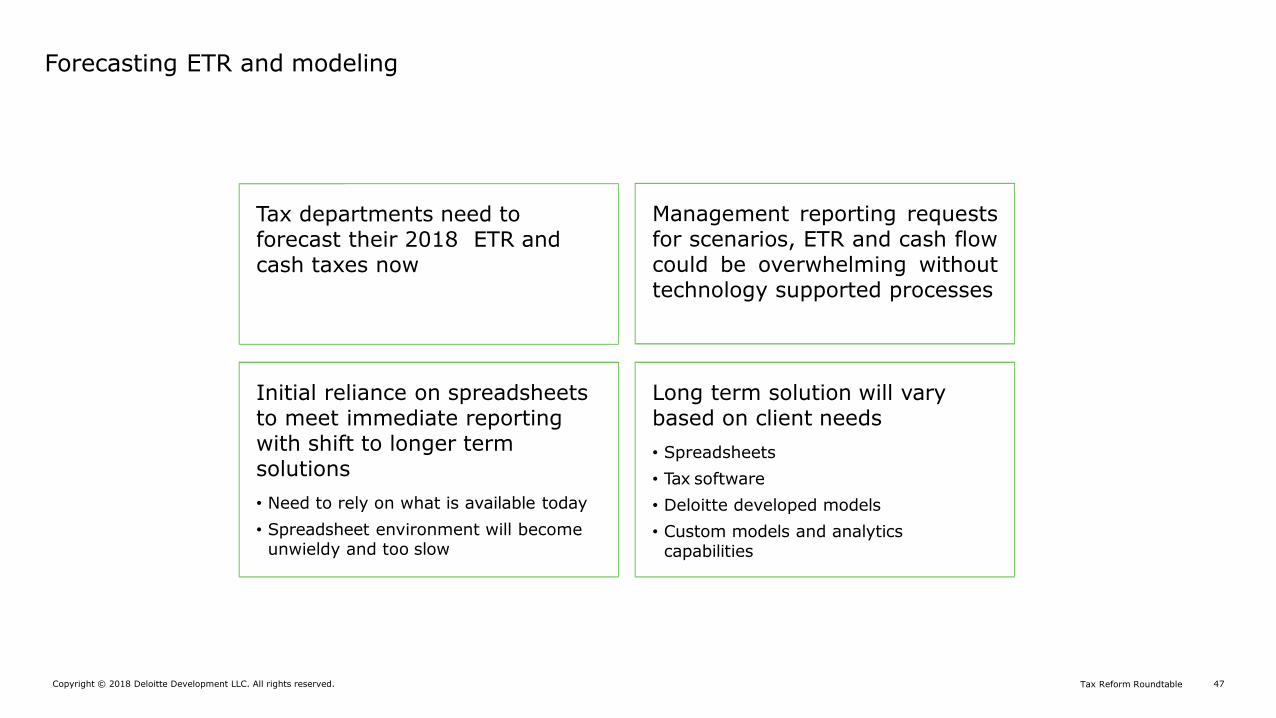

Forecasting ETR and modeling

Tax departments need toforecast their 2018 ETR and cash taxes now

Management reporting requestsfor scenarios, ETR and cash flowcould be overwhelming withouttechnology supported processes

Initial reliance on spreadsheets to meet immediate reporting with shift to longer term solutions

• Need to rely on what is available today

• Spreadsheet environment will become unwieldy and too slow

Long term solution will vary based on client needs

• Spreadsheets

• Tax software

• Deloitte developed models

• Custom models and analytics capabilities

Copyright © 2018 Deloitte Development LLC. All rights reserved. 48Tax Reform Roundtable

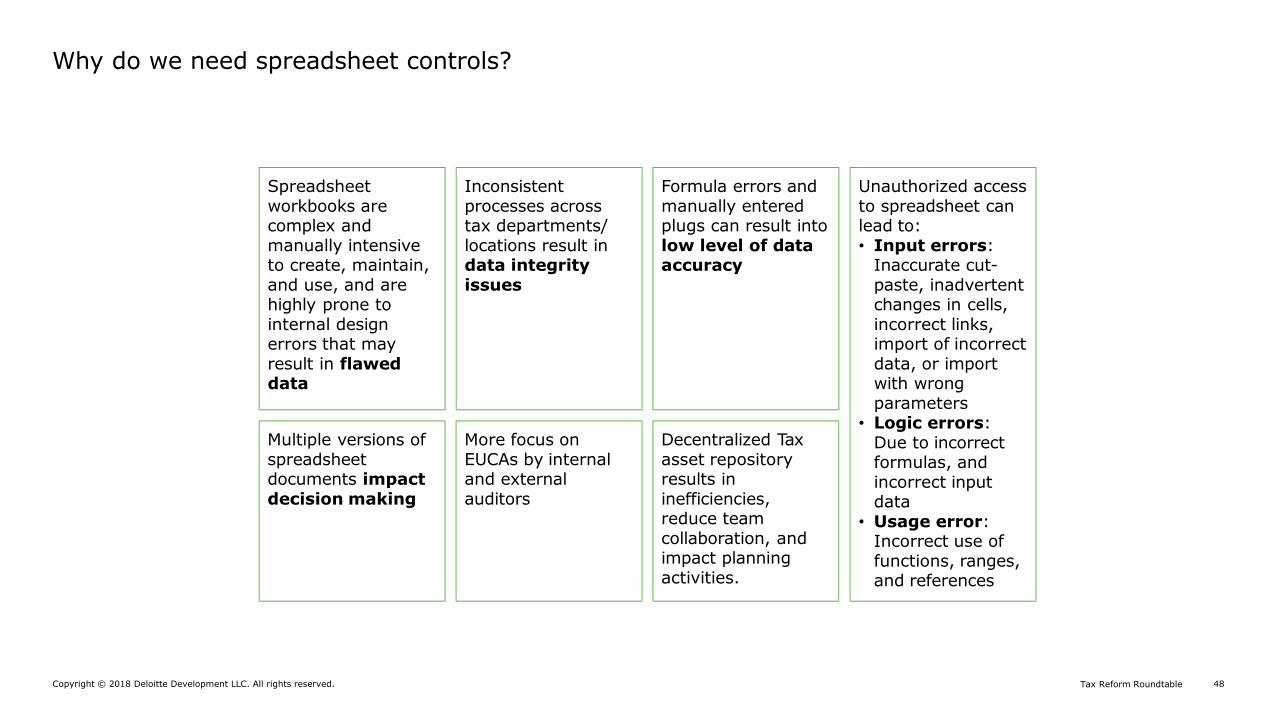

Why do we need spreadsheet controls?

Spreadsheet workbooks are complex and manually intensive to create, maintain, and use, and are highly prone to internal design errors that may result in flawed data

Inconsistent processes across tax departments/ locations result in data integrity issues

Multiple versions of spreadsheet documents impact decision making

More focus on EUCAs by internal and external auditors

Formula errors and manually entered plugs can result into low level of data accuracy

Decentralized Tax asset repository results in inefficiencies, reduce team collaboration, and impact planning activities.

Unauthorized access to spreadsheet can lead to:• Input errors:

Inaccurate cut-paste, inadvertent changes in cells, incorrect links, import of incorrect data, or import with wrong parameters

• Logic errors: Due to incorrect formulas, and incorrect input data

• Usage error: Incorrect use of functions, ranges, and references

Copyright © 2018 Deloitte Development LLC. All rights reserved. 49Tax Reform Roundtable

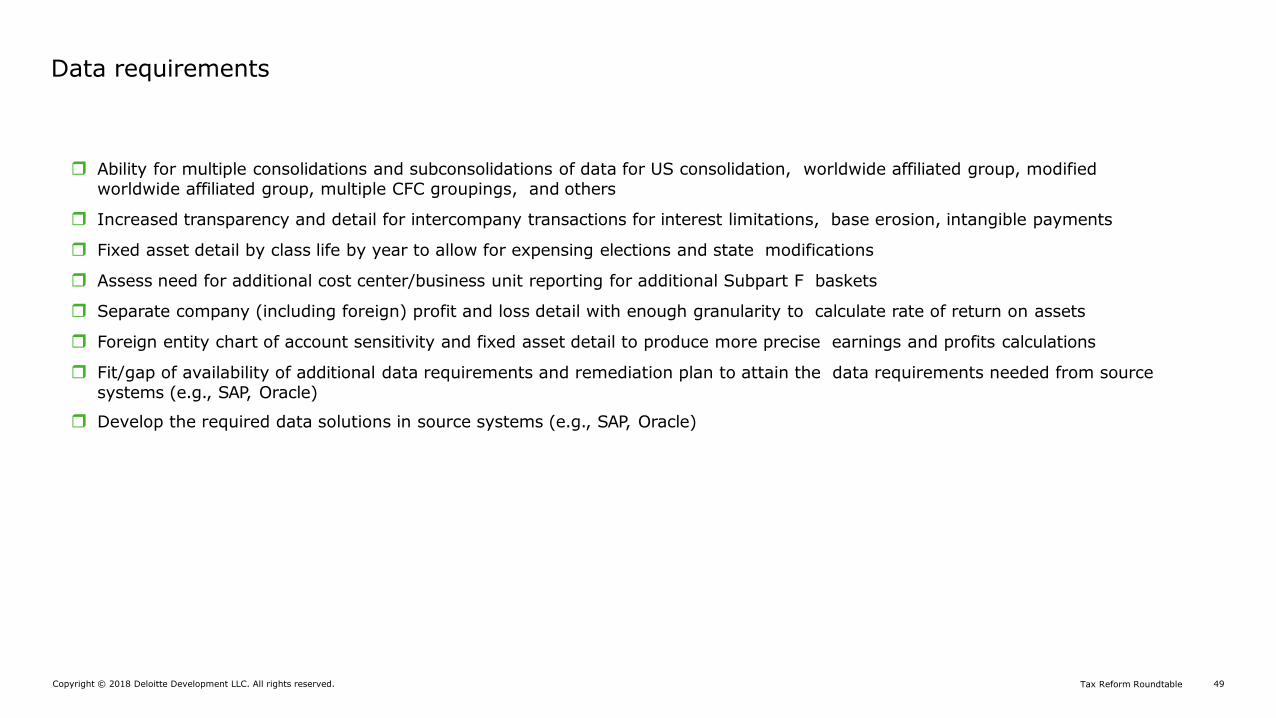

Data requirements

Ability for multiple consolidations and subconsolidations of data for US consolidation, worldwide affiliated group, modified worldwide affiliated group, multiple CFC groupings, and others

Increased transparency and detail for intercompany transactions for interest limitations, base erosion, intangible payments

Fixed asset detail by class life by year to allow for expensing elections and state modifications

Assess need for additional cost center/business unit reporting for additional Subpart F baskets

Separate company (including foreign) profit and loss detail with enough granularity to calculate rate of return on assets

Foreign entity chart of account sensitivity and fixed asset detail to produce more precise earnings and profits calculations

Fit/gap of availability of additional data requirements and remediation plan to attain the data requirements needed from source systems (e.g., SAP, Oracle)

Develop the required data solutions in source systems (e.g., SAP, Oracle)

Copyright © 2018 Deloitte Development LLC. All rights reserved. 50Tax Reform Roundtable

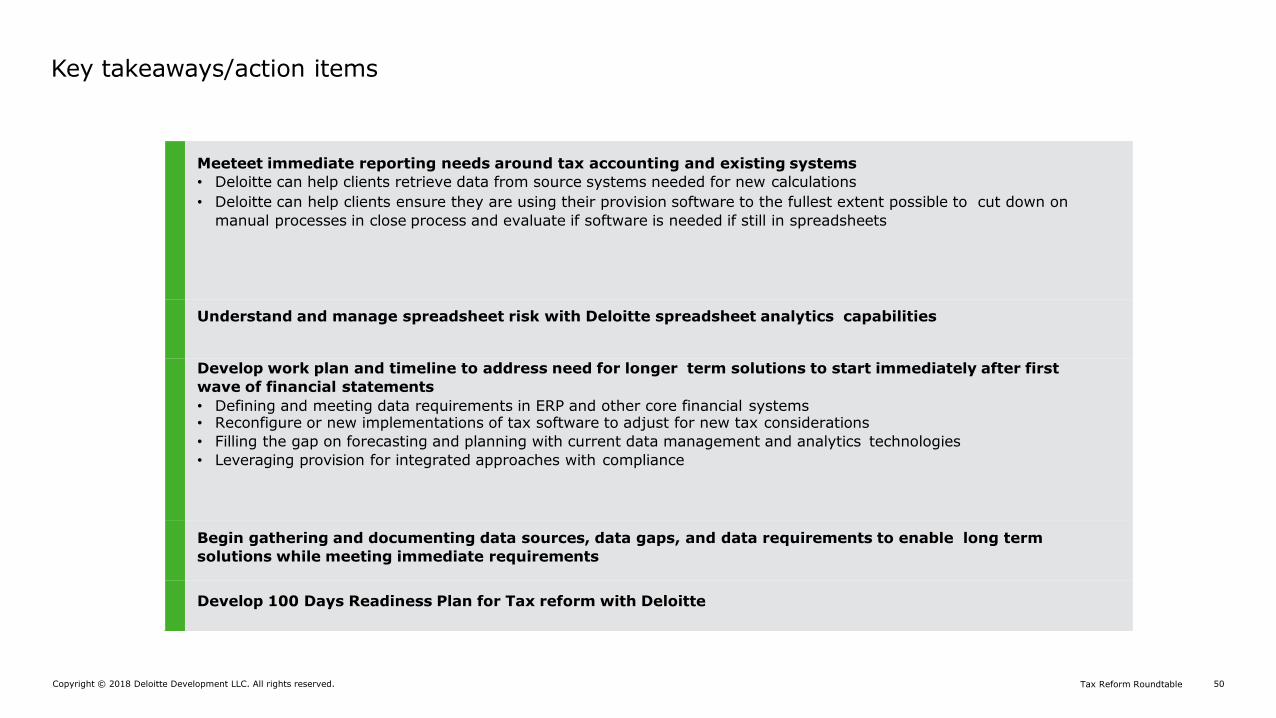

Key takeaways/action items

Meeteet immediate reporting needs around tax accounting and existing systems

• Deloitte can help clients retrieve data from source systems needed for new calculations

• Deloitte can help clients ensure they are using their provision software to the fullest extent possible to cut down on

manual processes in close process and evaluate if software is needed if still in spreadsheets

Understand and manage spreadsheet risk with Deloitte spreadsheet analytics capabilities

Develop work plan and timeline to address need for longer term solutions to start immediately after first

wave of financial statements

• Defining and meeting data requirements in ERP and other core financial systems• Reconfigure or new implementations of tax software to adjust for new tax considerations

• Filling the gap on forecasting and planning with current data management and analytics technologies

• Leveraging provision for integrated approaches with compliance

Begin gathering and documenting data sources, data gaps, and data requirements to enable long term

solutions while meeting immediate requirements

Develop 100 Days Readiness Plan for Tax reform with Deloitte

Copyright © 2018 Deloitte Development LLC. All rights reserved. 51Tax Reform Roundtable

Multistate considerations

Copyright © 2018 Deloitte Development LLC. All rights reserved. 52Tax Reform Roundtable

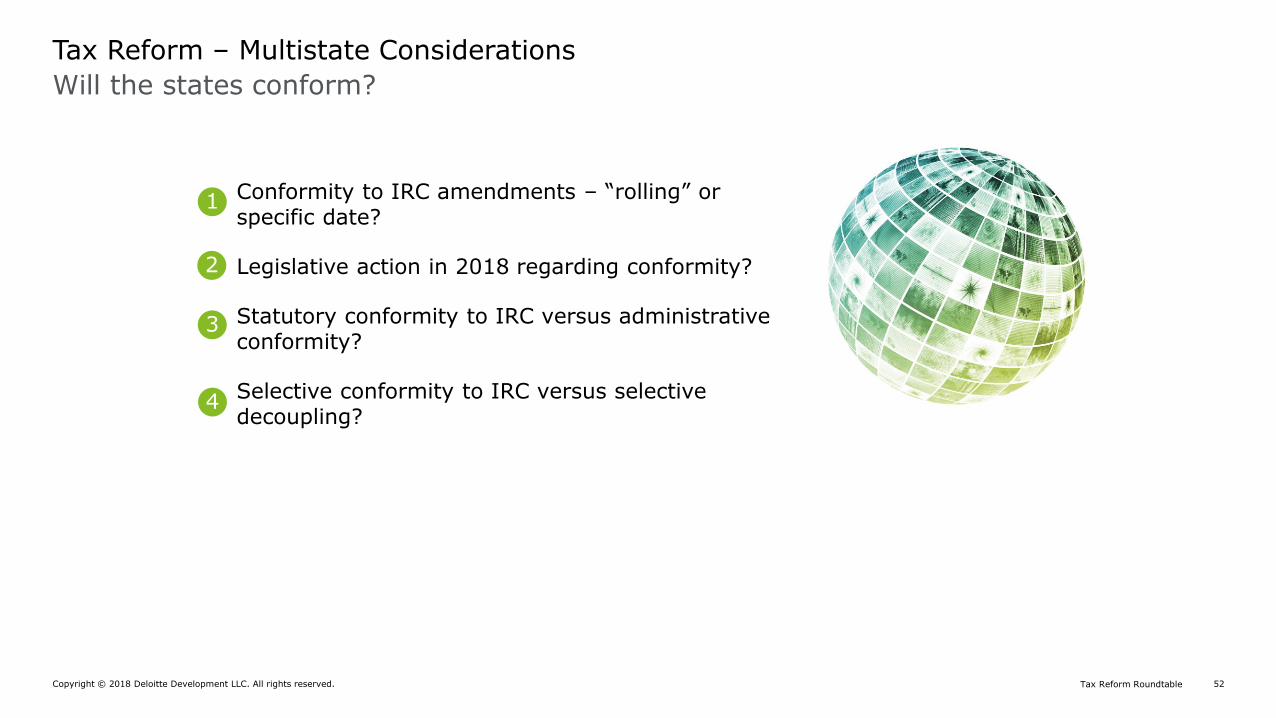

Will the states conform?

Tax Reform – Multistate Considerations

Conformity to IRC amendments – “rolling” or specific date?

Legislative action in 2018 regarding conformity?

Statutory conformity to IRC versus administrative conformity?

Selective conformity to IRC versus selective decoupling?

1

2

3

4

Copyright © 2018 Deloitte Development LLC. All rights reserved. 53Tax Reform Roundtable

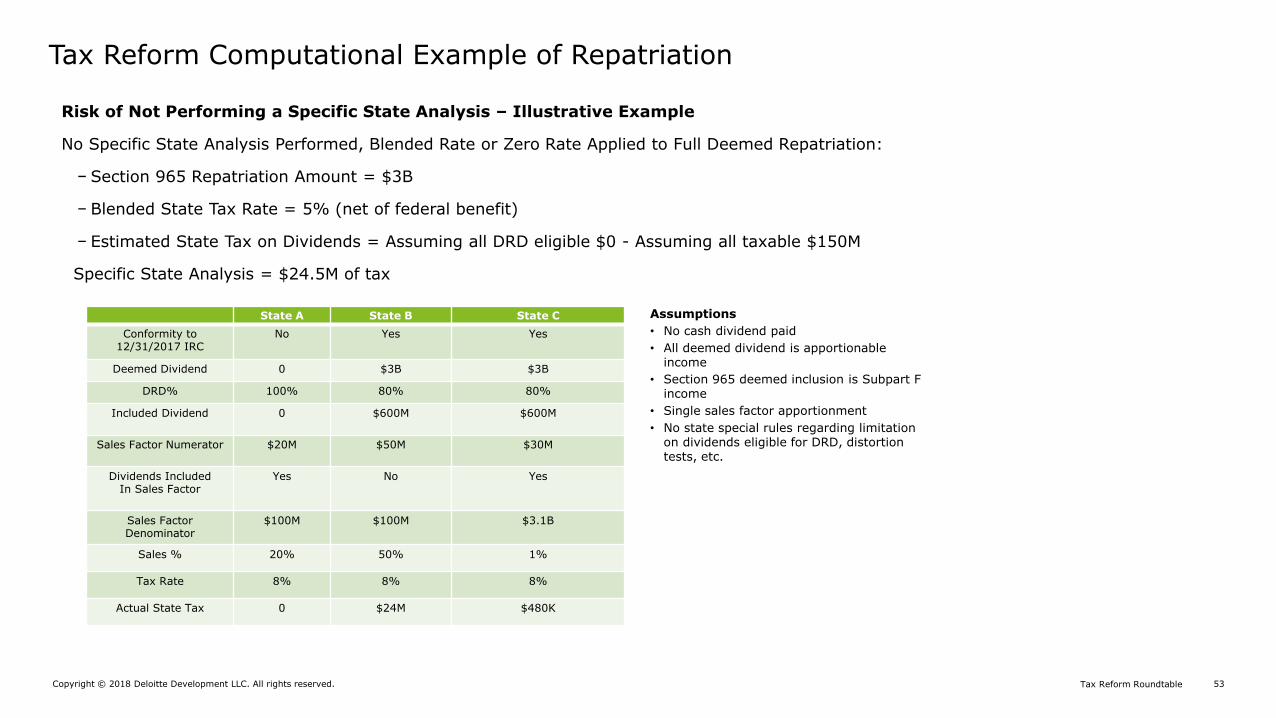

Tax Reform Computational Example of Repatriation

Risk of Not Performing a Specific State Analysis – Illustrative Example

No Specific State Analysis Performed, Blended Rate or Zero Rate Applied to Full Deemed Repatriation:

− Section 965 Repatriation Amount = $3B

− Blended State Tax Rate = 5% (net of federal benefit)

− Estimated State Tax on Dividends = Assuming all DRD eligible $0 - Assuming all taxable $150M

Specific State Analysis = $24.5M of tax

State A State B State C

Conformity to 12/31/2017 IRC

No Yes Yes

Deemed Dividend 0 $3B $3B

DRD% 100% 80% 80%

Included Dividend 0 $600M $600M

Sales Factor Numerator $20M $50M $30M

Dividends IncludedIn Sales Factor

Yes No Yes

Sales Factor Denominator

$100M $100M $3.1B

Sales % 20% 50% 1%

Tax Rate 8% 8% 8%

Actual State Tax 0 $24M $480K

Assumptions

• No cash dividend paid

• All deemed dividend is apportionable income

• Section 965 deemed inclusion is Subpart F income

• Single sales factor apportionment

• No state special rules regarding limitation on dividends eligible for DRD, distortion tests, etc.

Copyright © 2018 Deloitte Development LLC. All rights reserved. 54Tax Reform Roundtable

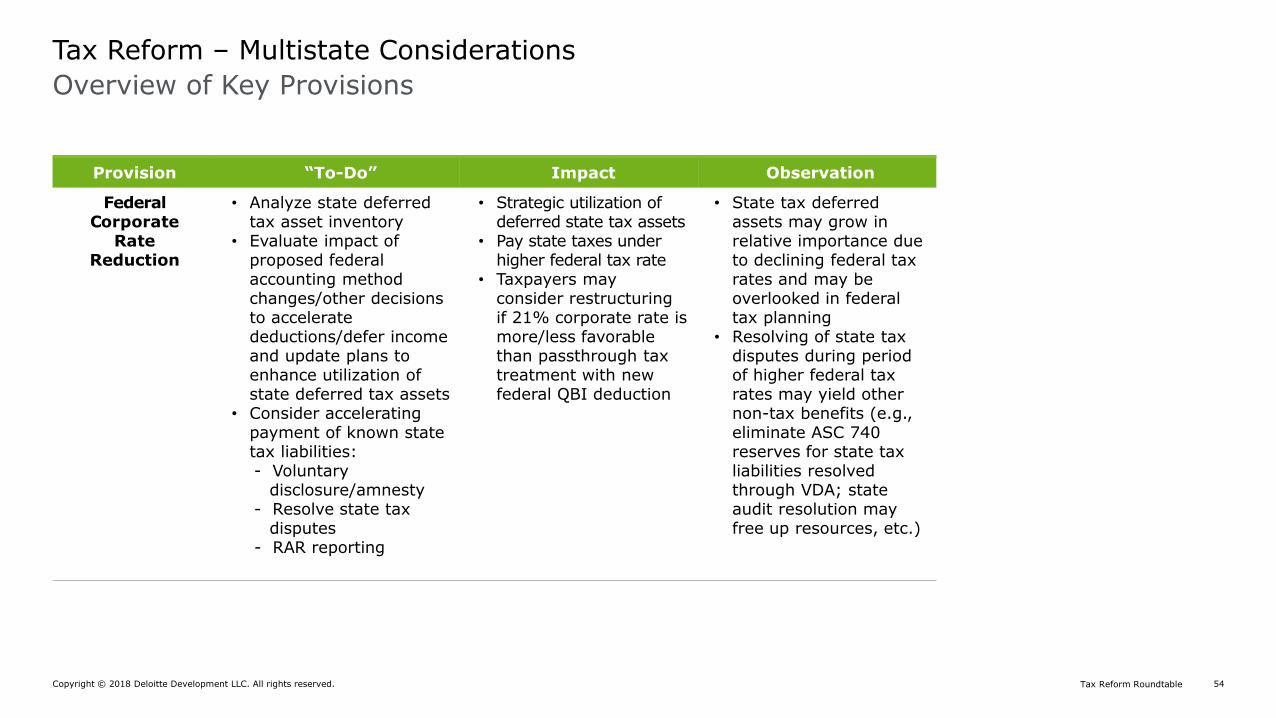

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

Federal Corporate

RateReduction

• Analyze state deferred tax asset inventory

• Evaluate impact of proposed federal accounting method changes/other decisions to accelerate deductions/defer income and update plans to enhance utilization of state deferred tax assets

• Consider accelerating payment of known state tax liabilities:- Voluntary

disclosure/amnesty- Resolve state tax

disputes- RAR reporting

• Strategic utilization of deferred state tax assets

• Pay state taxes under higher federal tax rate

• Taxpayers may consider restructuring if 21% corporate rate is more/less favorable than passthrough tax treatment with new federal QBI deduction

• State tax deferredassets may grow in relative importance due to declining federal tax rates and may be overlooked in federal tax planning

• Resolving of state tax disputes during period of higher federal tax rates may yield other non-tax benefits (e.g., eliminate ASC 740 reserves for state tax liabilities resolved through VDA; state audit resolution may free up resources, etc.)

Copyright © 2018 Deloitte Development LLC. All rights reserved. 55Tax Reform Roundtable

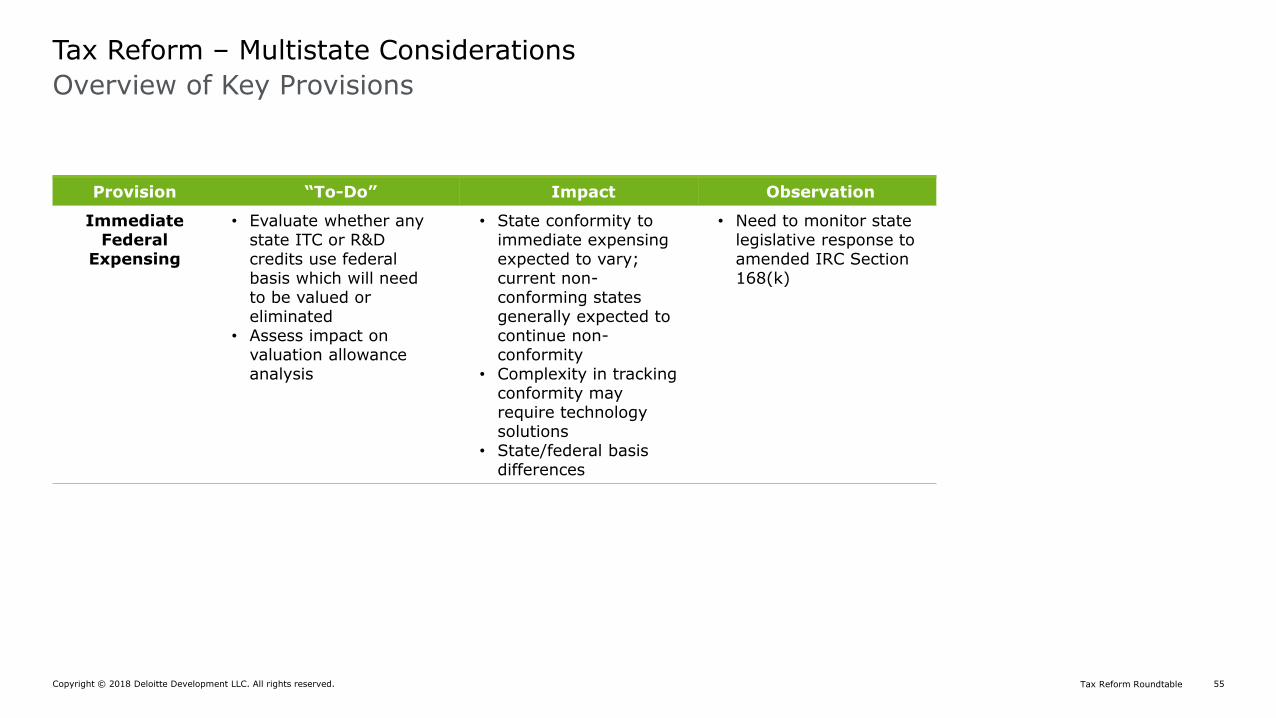

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

Immediate Federal

Expensing

• Evaluate whether any state ITC or R&D credits use federal basis which will need to be valued or eliminated

• Assess impact on valuation allowance analysis

• State conformity to immediate expensing expected to vary; current non-conforming states generally expected to continue non-conformity

• Complexity in tracking conformity may require technology solutions

• State/federal basis differences

• Need to monitor state legislative response to amended IRC Section 168(k)

Copyright © 2018 Deloitte Development LLC. All rights reserved. 56Tax Reform Roundtable

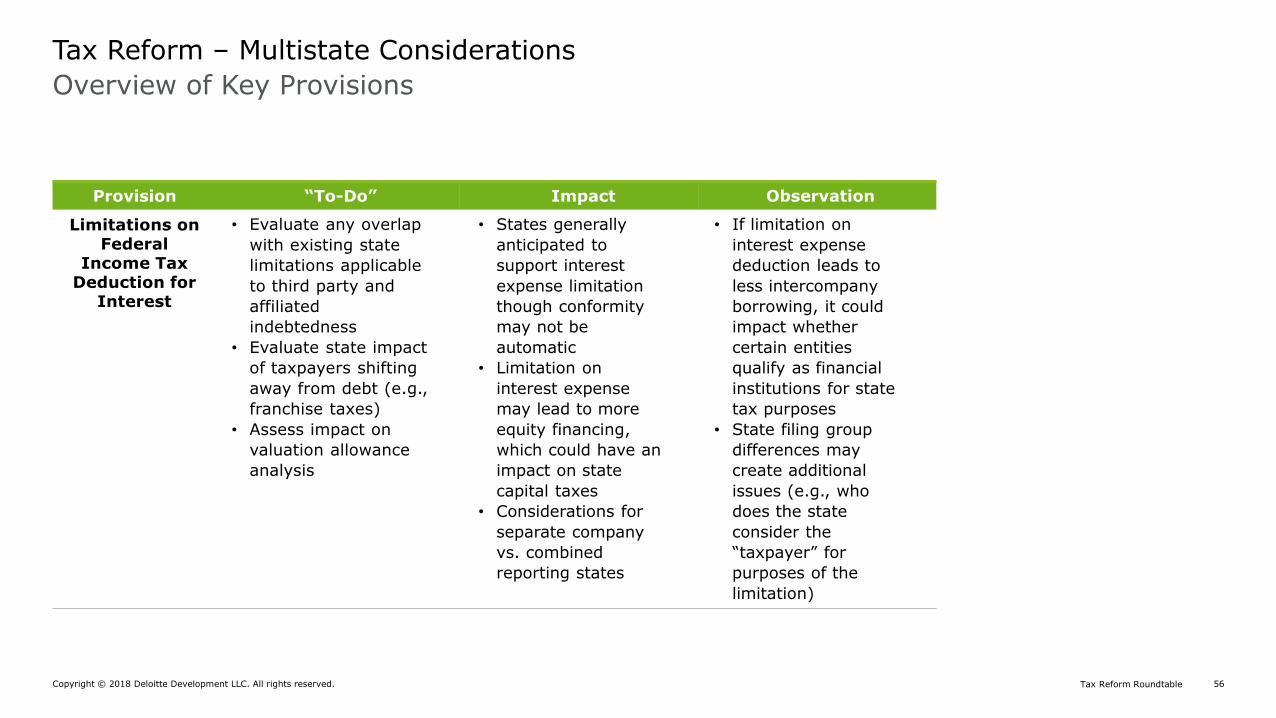

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

Limitations onFederal

Income Tax Deduction for

Interest

• Evaluate any overlap

with existing state

limitations applicable

to third party and

affiliated

indebtedness

• Evaluate state impact

of taxpayers shifting

away from debt (e.g.,

franchise taxes)

• Assess impact on

valuation allowance

analysis

• States generally

anticipated to

support interest

expense limitation

though conformity

may not be

automatic

• Limitation on

interest expense

may lead to more

equity financing,

which could have an

impact on state

capital taxes

• Considerations for

separate company

vs. combined

reporting states

• If limitation on

interest expense

deduction leads to

less intercompany

borrowing, it could

impact whether

certain entities

qualify as financial

institutions for state

tax purposes

• State filing group

differences may

create additional

issues (e.g., who

does the state

consider the

“taxpayer” for

purposes of the

limitation)

Copyright © 2018 Deloitte Development LLC. All rights reserved. 57Tax Reform Roundtable

Overview of Key Provisions

Tax Reform – Multistate Considerations

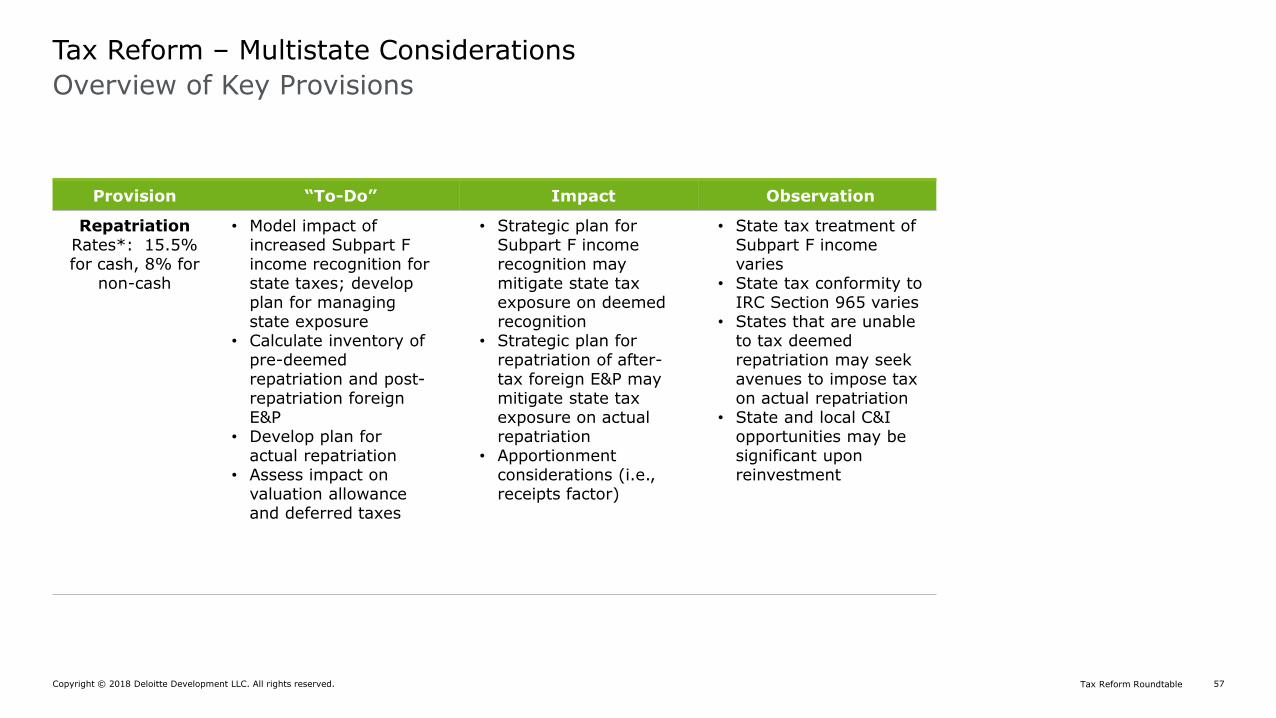

Provision “To-Do” Impact Observation

RepatriationRates*: 15.5% for cash, 8% for

non-cash

• Model impact of increased Subpart F income recognition for state taxes; develop plan for managing state exposure

• Calculate inventory of pre-deemed repatriation and post-repatriation foreign E&P

• Develop plan for actual repatriation

• Assess impact on valuation allowance and deferred taxes

• Strategic plan for Subpart F income recognition may mitigate state tax exposure on deemed recognition

• Strategic plan for repatriation of after-tax foreign E&P may mitigate state tax exposure on actual repatriation

• Apportionment considerations (i.e., receipts factor)

• State tax treatment of Subpart F income varies

• State tax conformity to IRC Section 965 varies

• States that are unable to tax deemed repatriation may seek avenues to impose tax on actual repatriation

• State and local C&I opportunities may be significant upon reinvestment

Copyright © 2018 Deloitte Development LLC. All rights reserved. 58Tax Reform Roundtable

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

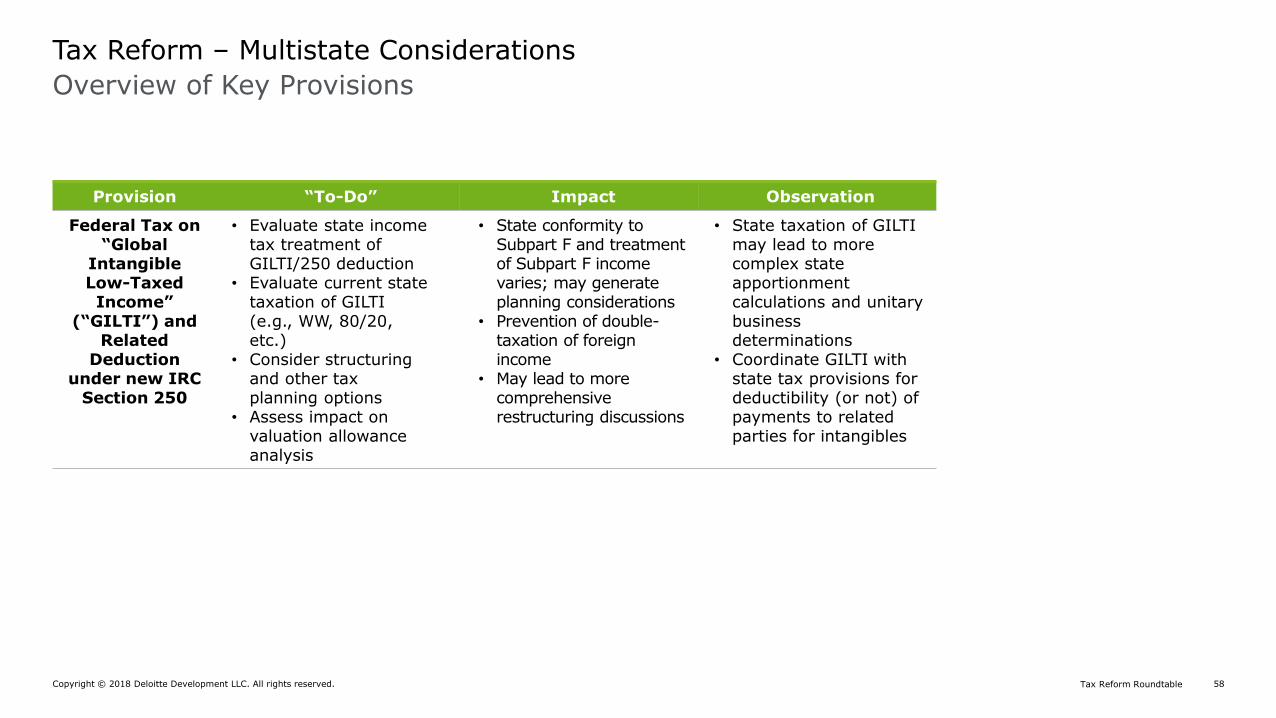

Federal Tax on “Global

Intangible Low-Taxed Income”

(“GILTI”) and Related

Deduction under new IRC

Section 250

• Evaluate state income tax treatment of GILTI/250 deduction

• Evaluate current state taxation of GILTI (e.g., WW, 80/20, etc.)

• Consider structuring and other tax planning options

• Assess impact on valuation allowance analysis

• State conformity to Subpart F and treatment of Subpart F income varies; may generate planning considerations

• Prevention of double-taxation of foreign income

• May lead to more comprehensive restructuring discussions

• State taxation of GILTI may lead to more complex state apportionment calculations and unitary business determinations

• Coordinate GILTI with state tax provisions for deductibility (or not) of payments to related parties for intangibles

Copyright © 2018 Deloitte Development LLC. All rights reserved. 59Tax Reform Roundtable

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

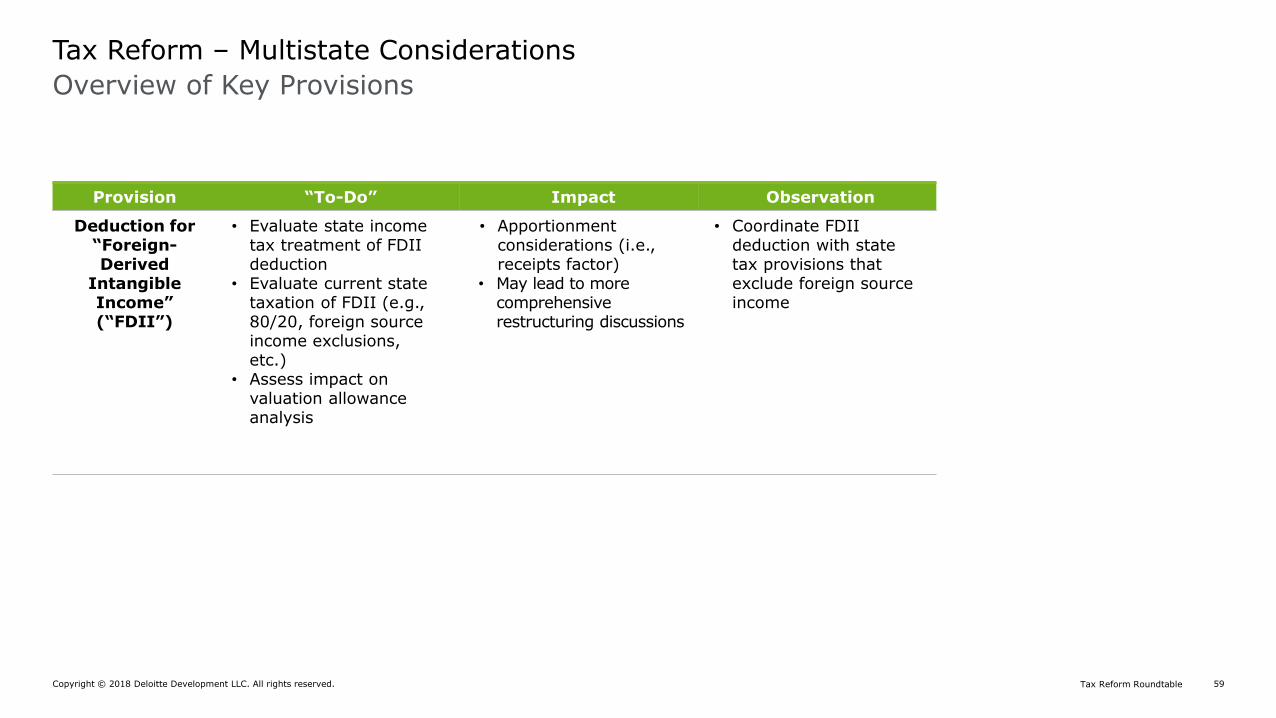

Deduction for “Foreign-Derived

Intangible Income” (“FDII”)

• Evaluate state income tax treatment of FDII deduction

• Evaluate current state taxation of FDII (e.g., 80/20, foreign source income exclusions, etc.)

• Assess impact on valuation allowance analysis

• Apportionment considerations (i.e., receipts factor)

• May lead to more comprehensive restructuring discussions

• Coordinate FDII deduction with state tax provisions that exclude foreign source income

Copyright © 2018 Deloitte Development LLC. All rights reserved. 60Tax Reform Roundtable

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

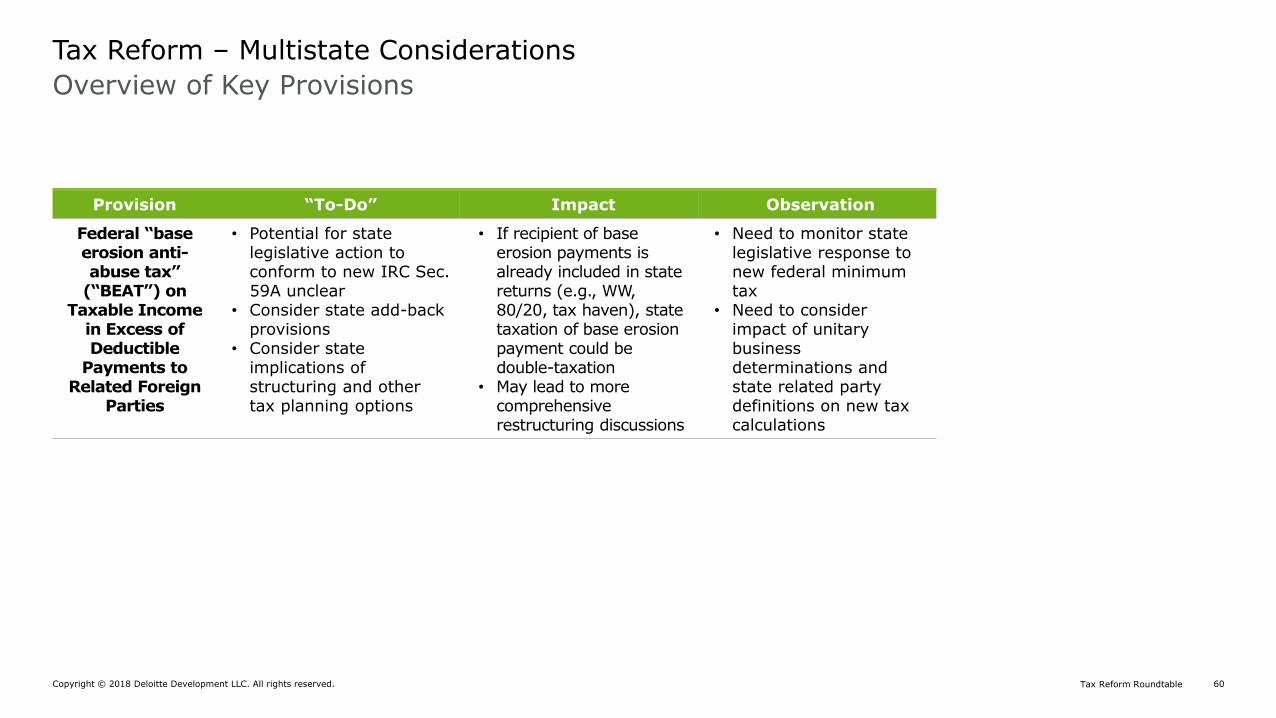

Federal “base erosion anti-abuse tax”

(“BEAT”) on Taxable Income

in Excess of Deductible

Payments to Related Foreign

Parties

• Potential for state legislative action to conform to new IRC Sec. 59A unclear

• Consider state add-back provisions

• Consider state implications of structuring and other tax planning options

• If recipient of base erosion payments is already included in state returns (e.g., WW, 80/20, tax haven), state taxation of base erosion payment could be double-taxation

• May lead to more comprehensive restructuring discussions

• Need to monitor state legislative response to new federal minimum tax

• Need to consider impact of unitary business determinations and state related party definitions on new tax calculations

Copyright © 2018 Deloitte Development LLC. All rights reserved. 61Tax Reform Roundtable

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

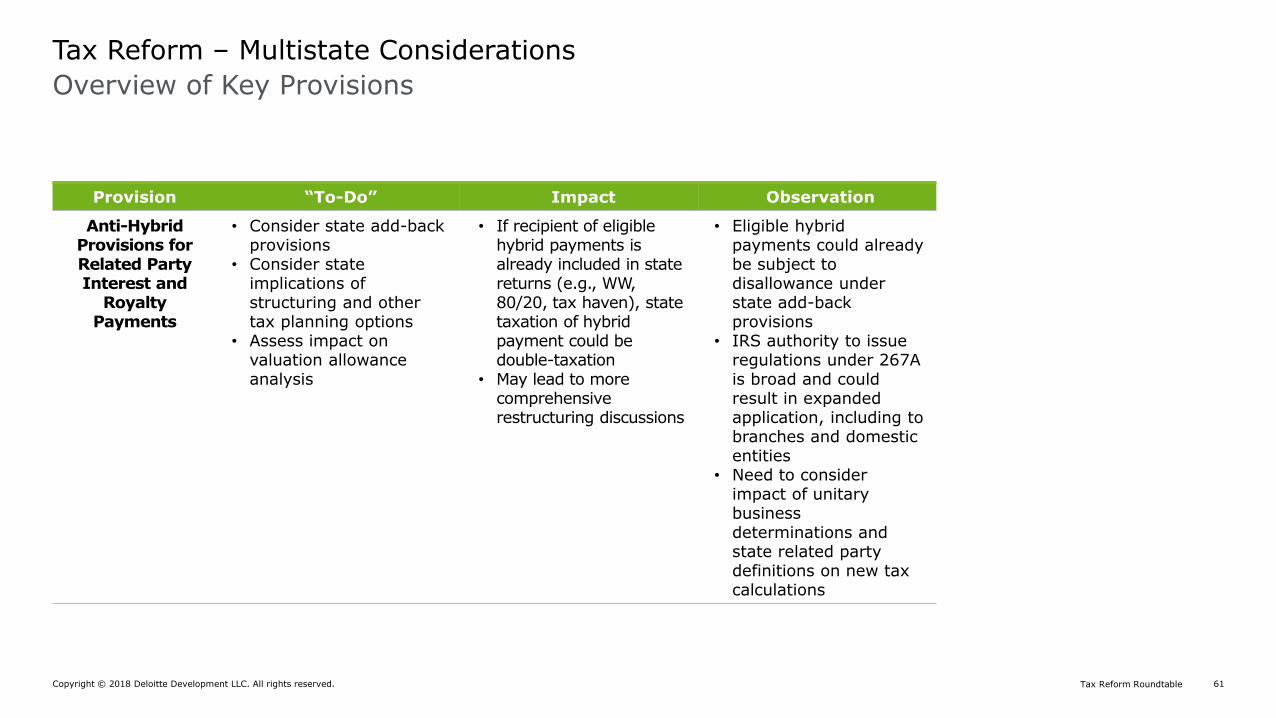

Anti-HybridProvisions for Related Party Interest and

Royalty Payments

• Consider state add-back provisions

• Consider state implications of structuring and other tax planning options

• Assess impact on valuation allowance analysis

• If recipient of eligible hybrid payments is already included in state returns (e.g., WW, 80/20, tax haven), state taxation of hybrid payment could be double-taxation

• May lead to more comprehensive restructuring discussions

• Eligible hybrid payments could already be subject to disallowance under state add-back provisions

• IRS authority to issue regulations under 267A is broad and could result in expanded application, including to branches and domestic entities

• Need to consider impact of unitary business determinations and state related party definitions on new tax calculations

Copyright © 2018 Deloitte Development LLC. All rights reserved. 62Tax Reform Roundtable

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

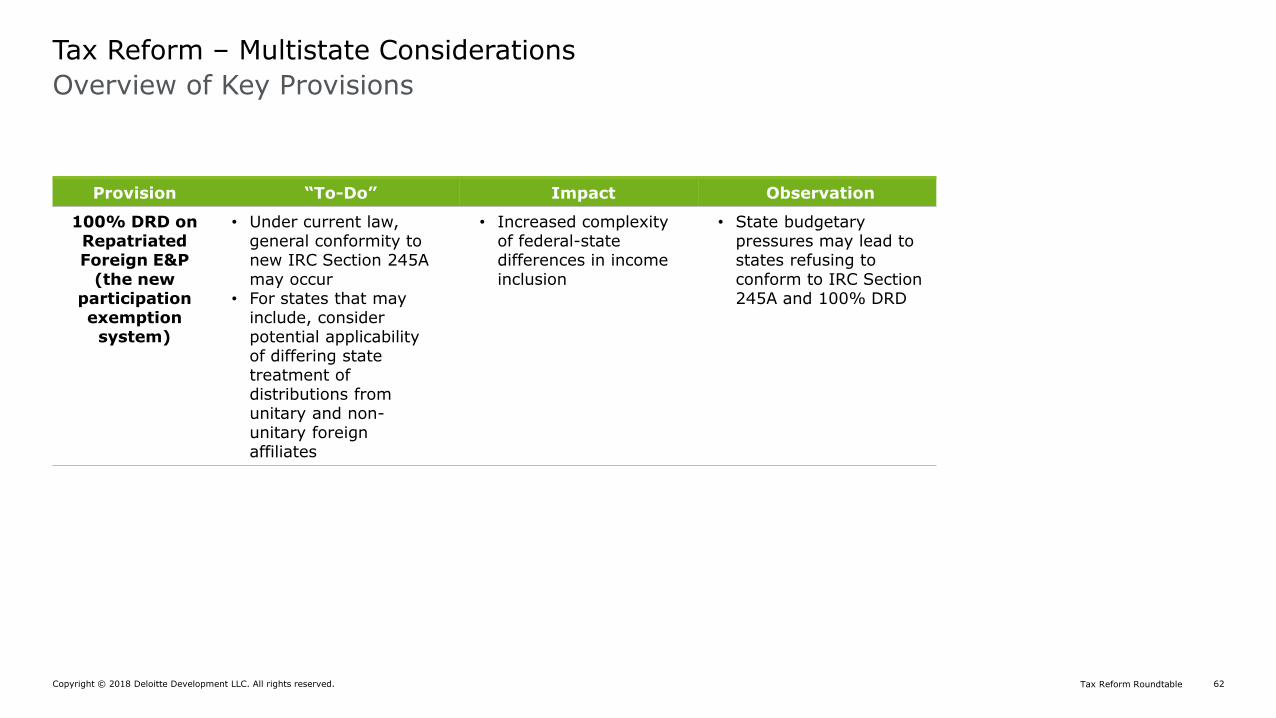

100% DRD on Repatriated Foreign E&P

(the new participation exemption

system)

• Under current law, general conformity to new IRC Section 245A may occur

• For states that may include, consider potential applicability of differing state treatment of distributions from unitary and non-unitary foreign affiliates

• Increased complexity of federal-state differences in income inclusion

• State budgetary pressures may lead to states refusing to conform to IRC Section 245A and 100% DRD

Copyright © 2018 Deloitte Development LLC. All rights reserved. 63Tax Reform Roundtable

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

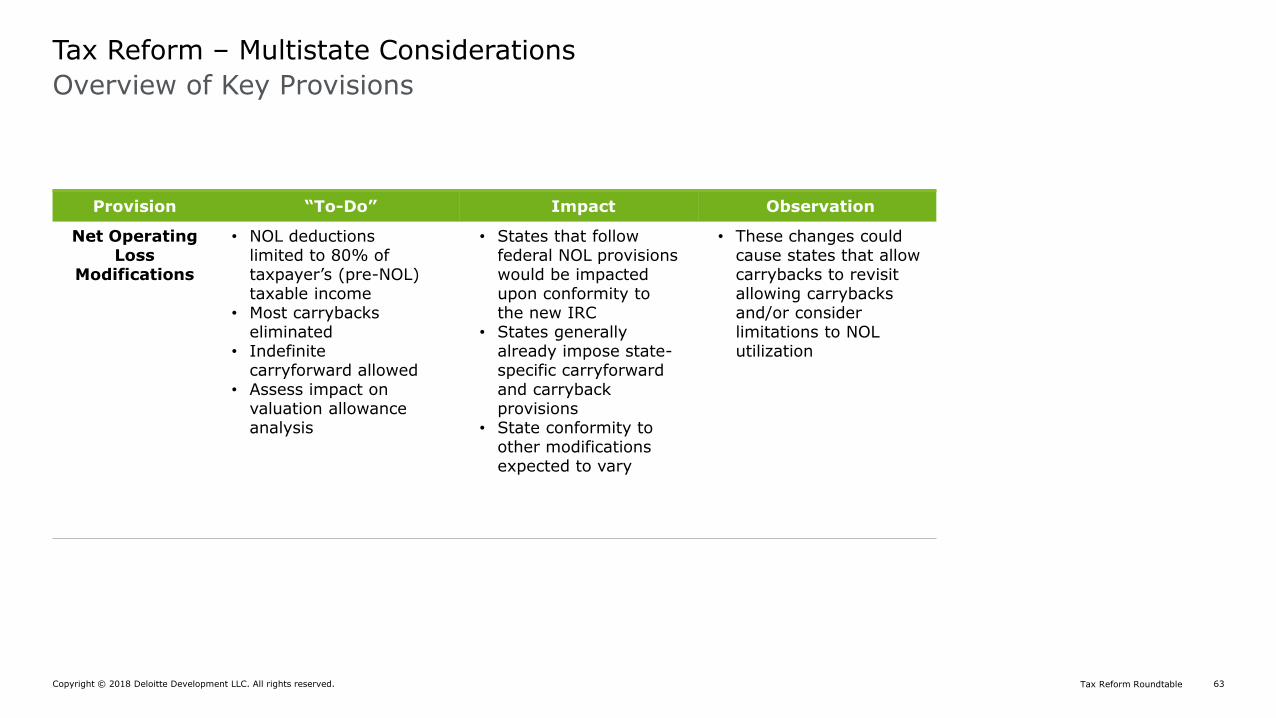

Net Operating Loss

Modifications

• NOL deductions limited to 80% of taxpayer’s (pre-NOL) taxable income

• Most carrybacks eliminated

• Indefinite carryforward allowed

• Assess impact on valuation allowance analysis

• States that follow federal NOL provisions would be impacted upon conformity to the new IRC

• States generally already impose state-specific carryforward and carryback provisions

• State conformity to other modifications expected to vary

• These changes could cause states that allow carrybacks to revisit allowing carrybacks and/or consider limitations to NOL utilization

Copyright © 2018 Deloitte Development LLC. All rights reserved. 64Tax Reform Roundtable

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

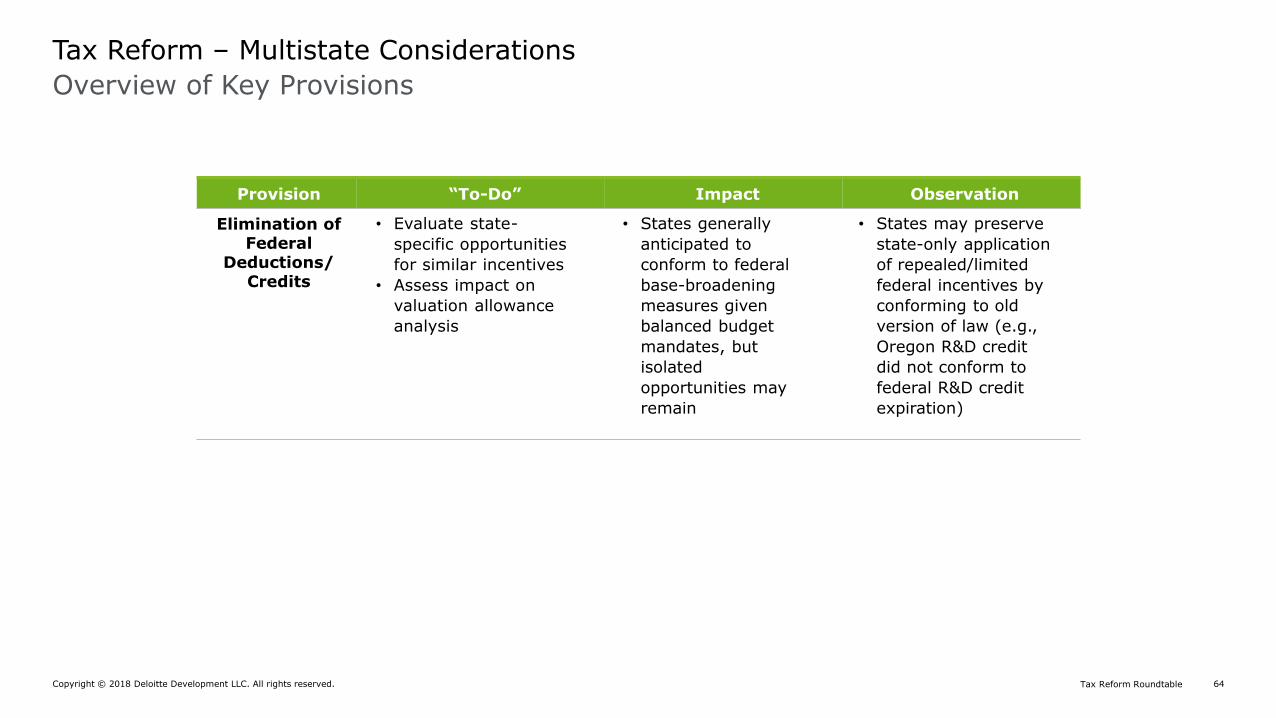

Elimination of Federal

Deductions/Credits

• Evaluate state-

specific opportunities

for similar incentives

• Assess impact on

valuation allowance

analysis

• States generally

anticipated to

conform to federal

base-broadening

measures given

balanced budget

mandates, but

isolated

opportunities may

remain

• States may preserve

state-only application

of repealed/limited

federal incentives by

conforming to old

version of law (e.g.,

Oregon R&D credit

did not conform to

federal R&D credit

expiration)

Copyright © 2018 Deloitte Development LLC. All rights reserved. 65Tax Reform Roundtable

Overview of Key Provisions

Tax Reform – Multistate Considerations

Provision “To-Do” Impact Observation

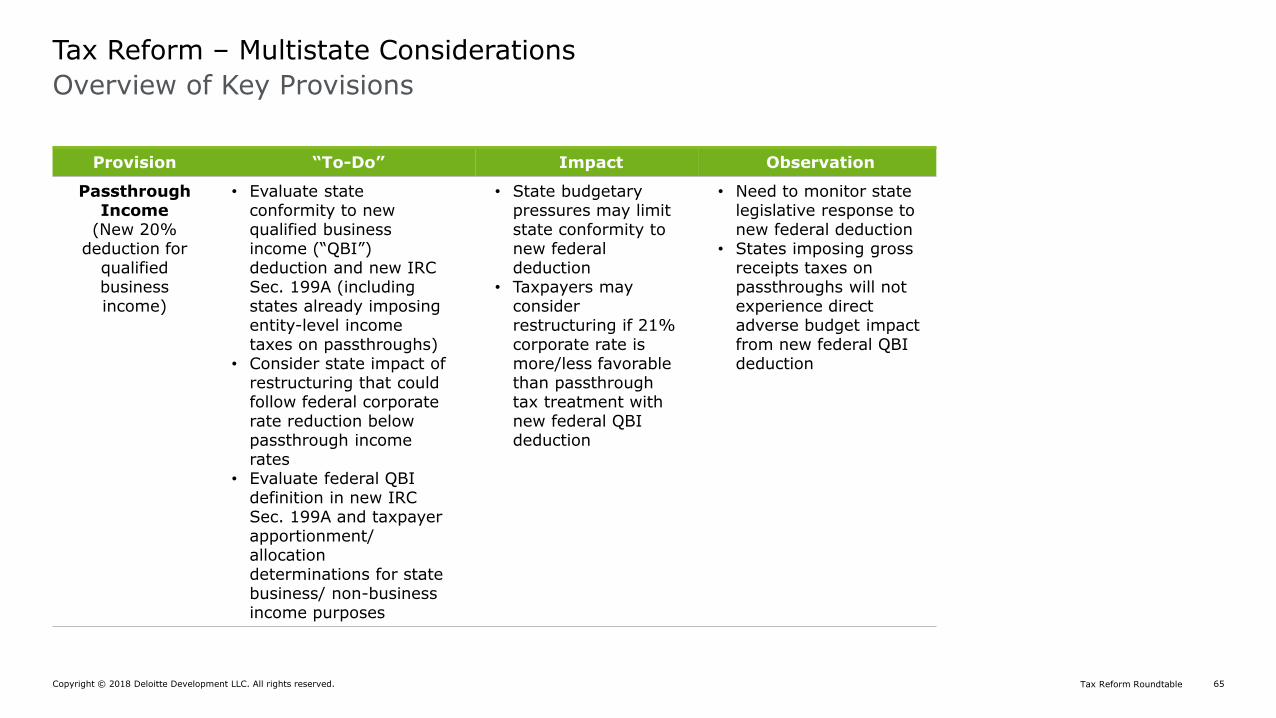

Passthrough Income

(New 20% deduction for

qualified business income)

• Evaluate state conformity to new qualified business income (“QBI”) deduction and new IRC Sec. 199A (including states already imposing entity-level income taxes on passthroughs)

• Consider state impact of restructuring that could follow federal corporate rate reduction below passthrough income rates

• Evaluate federal QBI definition in new IRC Sec. 199A and taxpayer apportionment/ allocation determinations for state business/ non-business income purposes

• State budgetary pressures may limit state conformity to new federal deduction

• Taxpayers may consider restructuring if 21% corporate rate is more/less favorable than passthrough tax treatment with new federal QBI deduction

• Need to monitor state legislative response to new federal deduction

• States imposing gross receipts taxes on passthroughs will not experience direct adverse budget impact from new federal QBI deduction

Copyright © 2018 Deloitte Development LLC. All rights reserved. 66Tax Reform Roundtable

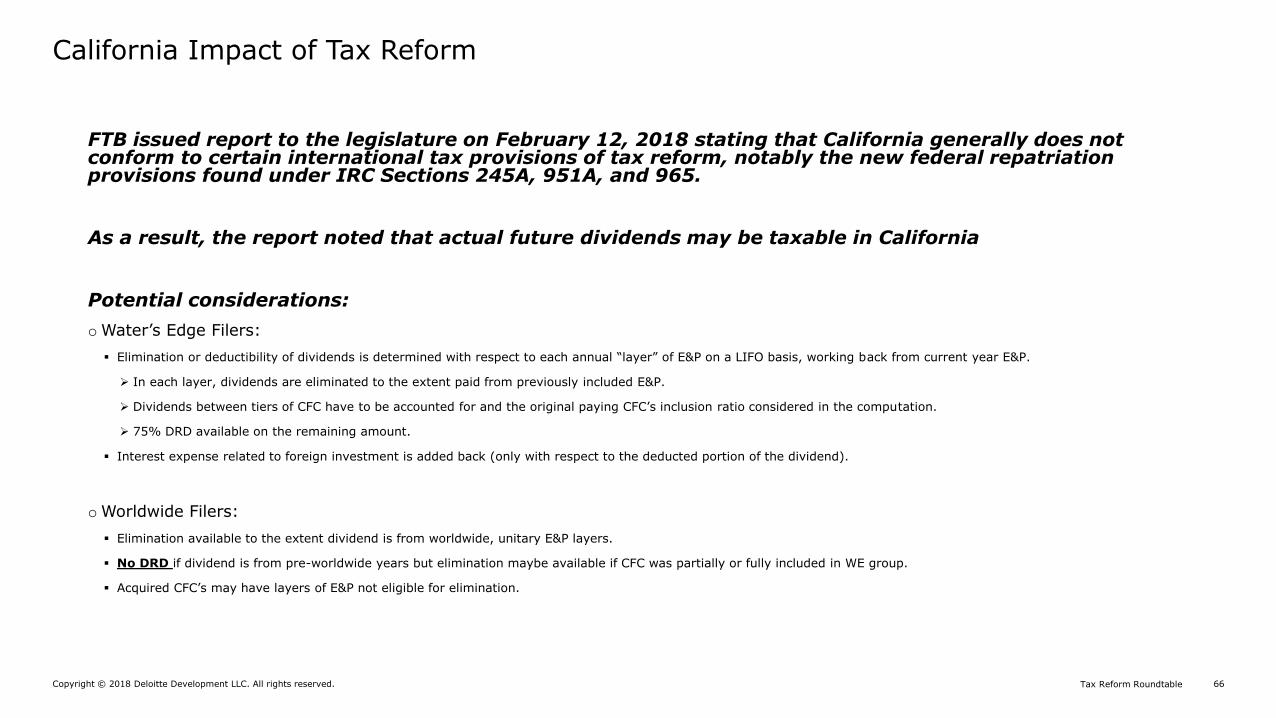

California Impact of Tax Reform

FTB issued report to the legislature on February 12, 2018 stating that California generally does not conform to certain international tax provisions of tax reform, notably the new federal repatriation provisions found under IRC Sections 245A, 951A, and 965.

As a result, the report noted that actual future dividends may be taxable in California

Potential considerations:

oWater’s Edge Filers:

▪ Elimination or deductibility of dividends is determined with respect to each annual “layer” of E&P on a LIFO basis, working back from current year E&P.

➢ In each layer, dividends are eliminated to the extent paid from previously included E&P.

➢ Dividends between tiers of CFC have to be accounted for and the original paying CFC’s inclusion ratio considered in the computation.

➢ 75% DRD available on the remaining amount.

▪ Interest expense related to foreign investment is added back (only with respect to the deducted portion of the dividend).

oWorldwide Filers:

▪ Elimination available to the extent dividend is from worldwide, unitary E&P layers.

▪ No DRD if dividend is from pre-worldwide years but elimination maybe available if CFC was partially or fully included in WE group.

▪ Acquired CFC’s may have layers of E&P not eligible for elimination.

Copyright © 2018 Deloitte Development LLC. All rights reserved. 67Tax Reform Roundtable

Financial reporting

Copyright © 2018 Deloitte Development LLC. All rights reserved. 68Tax Reform Roundtable

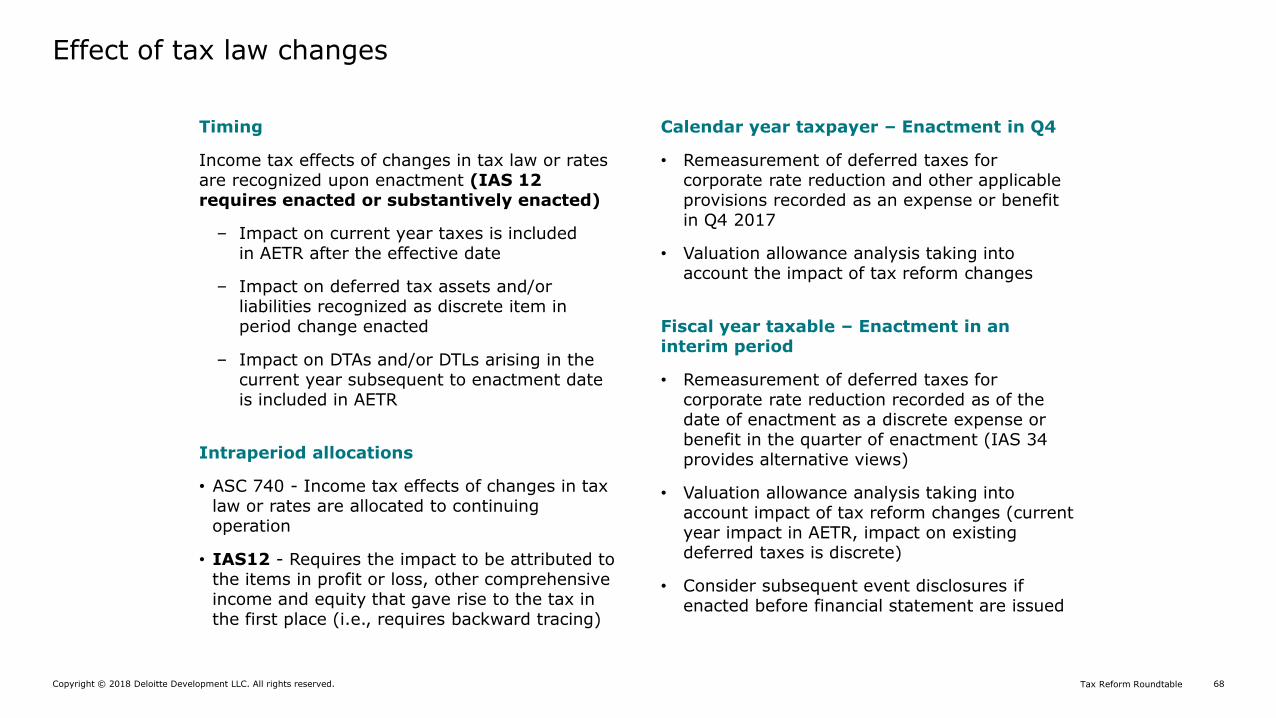

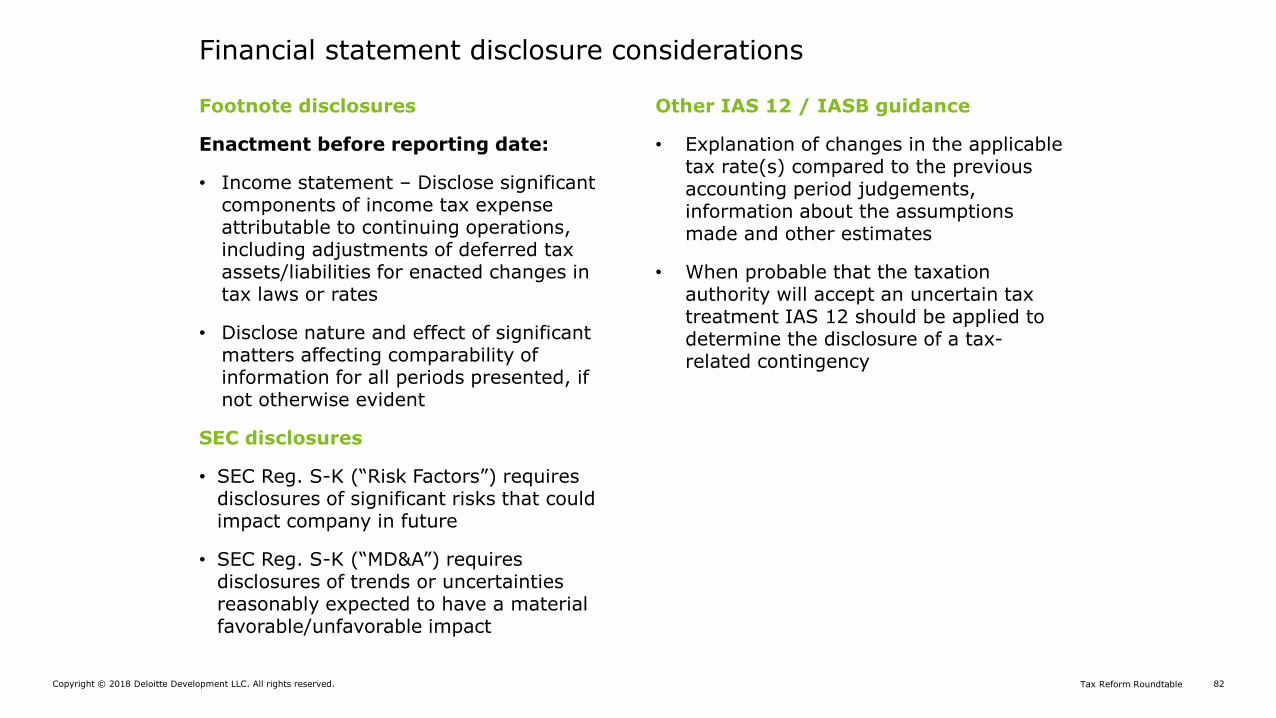

Effect of tax law changes

Timing

Income tax effects of changes in tax law or rates are recognized upon enactment (IAS 12 requires enacted or substantively enacted)

‒ Impact on current year taxes is includedin AETR after the effective date

‒ Impact on deferred tax assets and/or liabilities recognized as discrete item in period change enacted

‒ Impact on DTAs and/or DTLs arising in the current year subsequent to enactment dateis included in AETR

Intraperiod allocations

• ASC 740 - Income tax effects of changes in tax law or rates are allocated to continuing operation

• IAS12 - Requires the impact to be attributed to the items in profit or loss, other comprehensive income and equity that gave rise to the tax in the first place (i.e., requires backward tracing)

Calendar year taxpayer – Enactment in Q4

• Remeasurement of deferred taxes for corporate rate reduction and other applicable provisions recorded as an expense or benefit in Q4 2017

• Valuation allowance analysis taking into account the impact of tax reform changes

Fiscal year taxable – Enactment in an interim period

• Remeasurement of deferred taxes for corporate rate reduction recorded as of the date of enactment as a discrete expense or benefit in the quarter of enactment (IAS 34 provides alternative views)

• Valuation allowance analysis taking into account impact of tax reform changes (current year impact in AETR, impact on existing deferred taxes is discrete)

• Consider subsequent event disclosures if enacted before financial statement are issued

Copyright © 2018 Deloitte Development LLC. All rights reserved. 69Tax Reform Roundtable

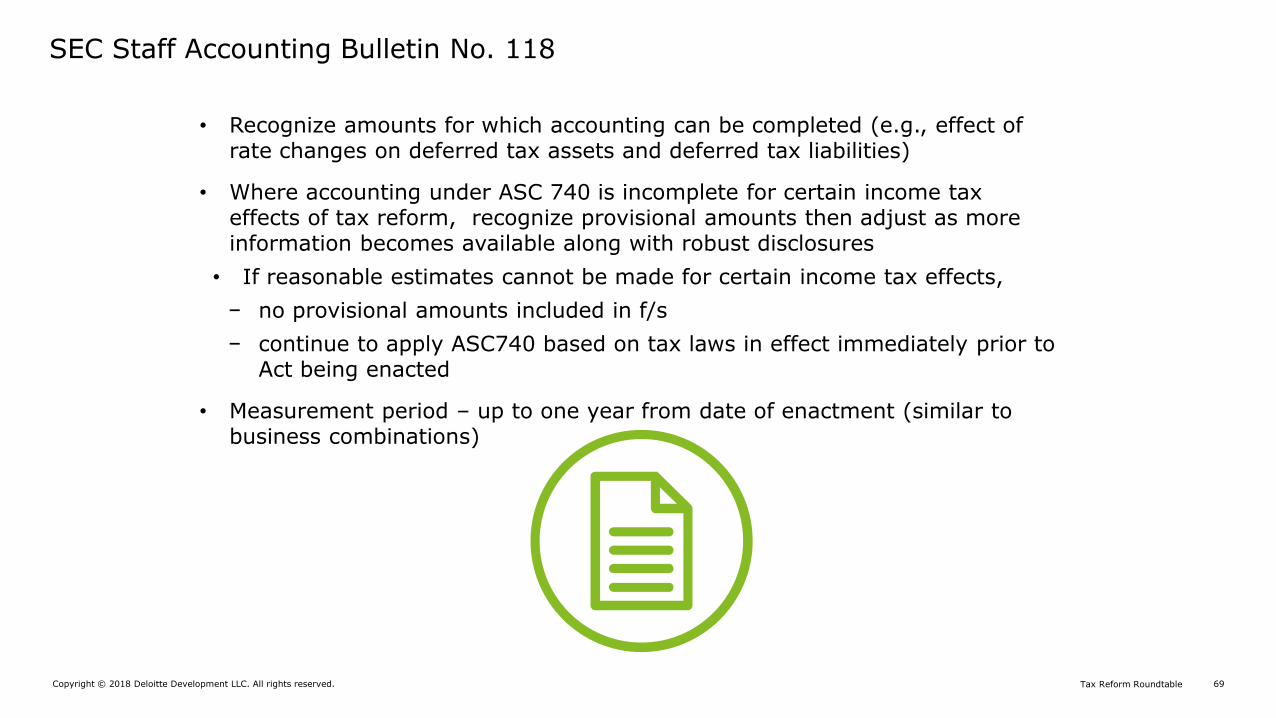

• Recognize amounts for which accounting can be completed (e.g., effect of rate changes on deferred tax assets and deferred tax liabilities)

• Where accounting under ASC 740 is incomplete for certain income tax effects of tax reform, recognize provisional amounts then adjust as more information becomes available along with robust disclosures

• If reasonable estimates cannot be made for certain income tax effects,

− no provisional amounts included in f/s

− continue to apply ASC740 based on tax laws in effect immediately prior to Act being enacted

• Measurement period – up to one year from date of enactment (similar to business combinations)

SEC Staff Accounting Bulletin No. 118

Copyright © 2018 Deloitte Development LLC. All rights reserved. 70Tax Reform Roundtable

SAB 118 (cont.) Disclosures of material impacts:

• Qualitative disclosures of income tax effects for which the accounting is incomplete

• Provisional amounts

• Existing current / deferred tax amounts for which income tax effects of tax reform have not been completed

• Reason why initial accounting is incomplete

• Additional information needed to complete accounting requirements under ASC 740

• Nature and amount of any measurement period adjustments recognized during reporting period

• Effect of measurement period adjustments on effective tax rate; and

• When accounting for income tax effects of tax reform has been completed

At the January 10, 2018 FASB Board Meeting, the FASB staff will provide the Board with an update on implementation issues related to the use of SAB 118 by private companies and not-for-profit entities.

Copyright © 2018 Deloitte Development LLC. All rights reserved. 71Tax Reform Roundtable

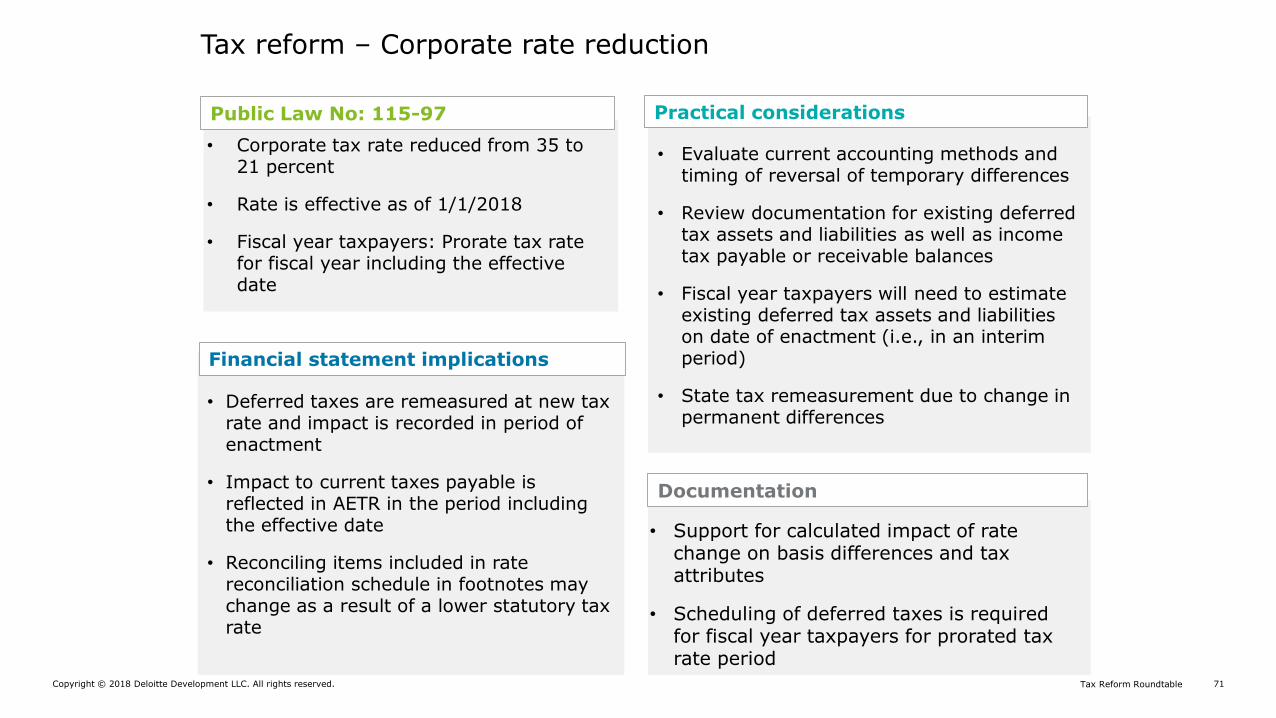

• Deferred taxes are remeasured at new tax rate and impact is recorded in period of enactment

• Impact to current taxes payable is reflected in AETR in the period including the effective date

• Reconciling items included in rate reconciliation schedule in footnotes may change as a result of a lower statutory tax rate

Financial statement implications

Public Law No: 115-97

Tax reform – Corporate rate reduction

• Evaluate current accounting methods and timing of reversal of temporary differences

• Review documentation for existing deferred tax assets and liabilities as well as income tax payable or receivable balances

• Fiscal year taxpayers will need to estimate existing deferred tax assets and liabilities on date of enactment (i.e., in an interim period)

• State tax remeasurement due to change in permanent differences

Practical considerations

Documentation

• Support for calculated impact of rate change on basis differences and tax attributes

• Scheduling of deferred taxes is required for fiscal year taxpayers for prorated tax rate period

• Corporate tax rate reduced from 35 to 21 percent

• Rate is effective as of 1/1/2018

• Fiscal year taxpayers: Prorate tax rate for fiscal year including the effective date

Copyright © 2018 Deloitte Development LLC. All rights reserved. 72Tax Reform Roundtable

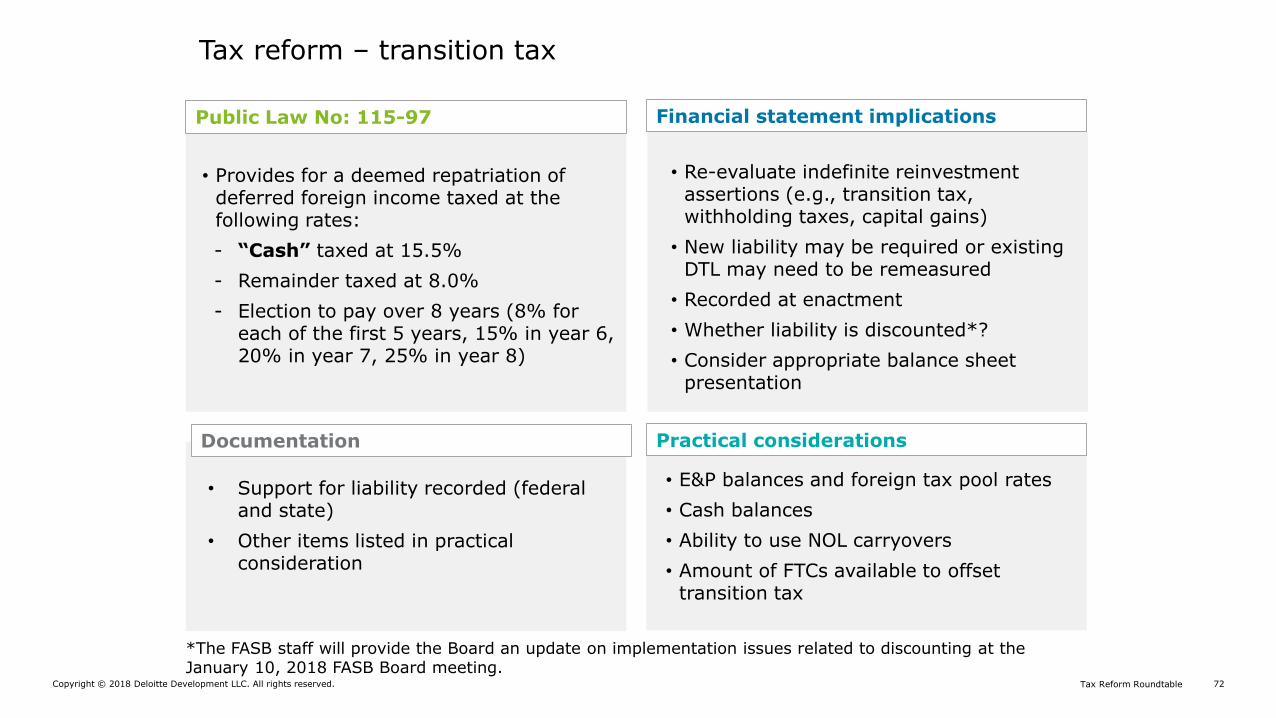

Financial statement implicationsPublic Law No: 115-97

Tax reform – transition tax

Practical considerationsDocumentation

• Provides for a deemed repatriation of deferred foreign income taxed at the following rates:

- “Cash” taxed at 15.5%

- Remainder taxed at 8.0%

- Election to pay over 8 years (8% for each of the first 5 years, 15% in year 6, 20% in year 7, 25% in year 8)

• Re-evaluate indefinite reinvestment assertions (e.g., transition tax, withholding taxes, capital gains)

• New liability may be required or existing DTL may need to be remeasured

• Recorded at enactment

• Whether liability is discounted*?

• Consider appropriate balance sheet presentation

• Support for liability recorded (federal and state)

• Other items listed in practical consideration

• E&P balances and foreign tax pool rates

• Cash balances

• Ability to use NOL carryovers

• Amount of FTCs available to offset transition tax

*The FASB staff will provide the Board an update on implementation issues related to discounting at the January 10, 2018 FASB Board meeting.

Copyright © 2018 Deloitte Development LLC. All rights reserved. 73Tax Reform Roundtable

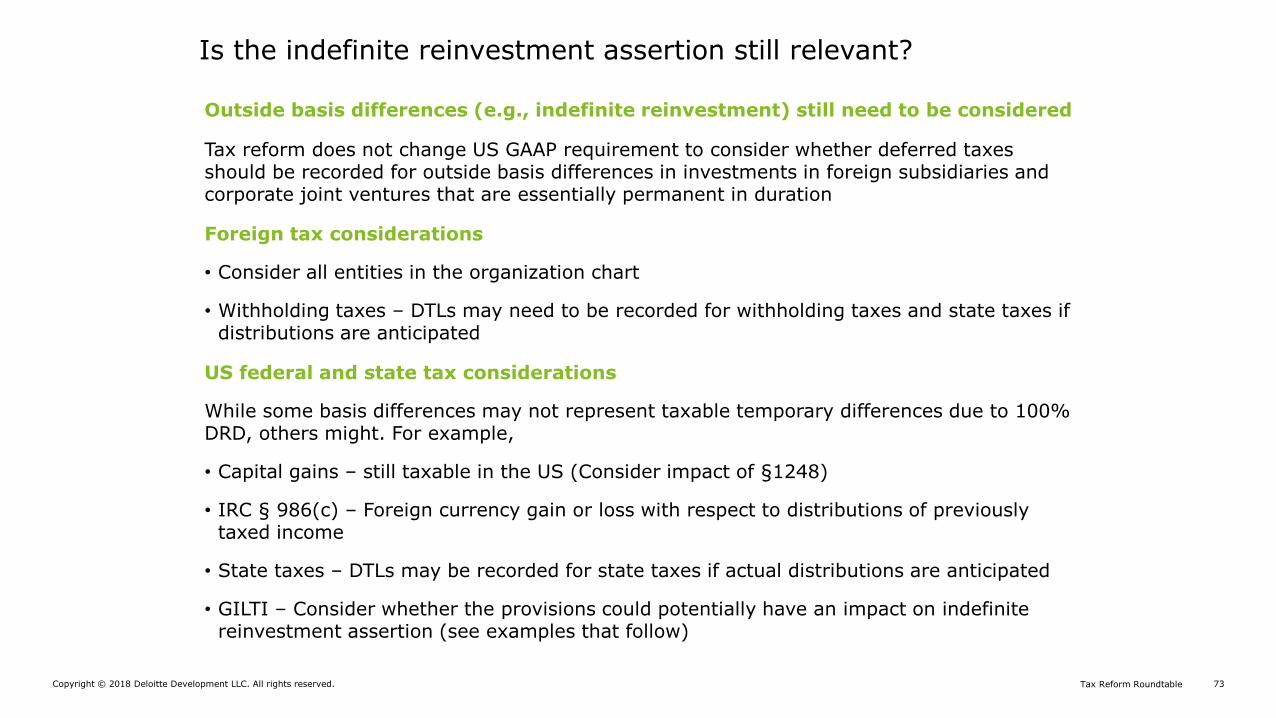

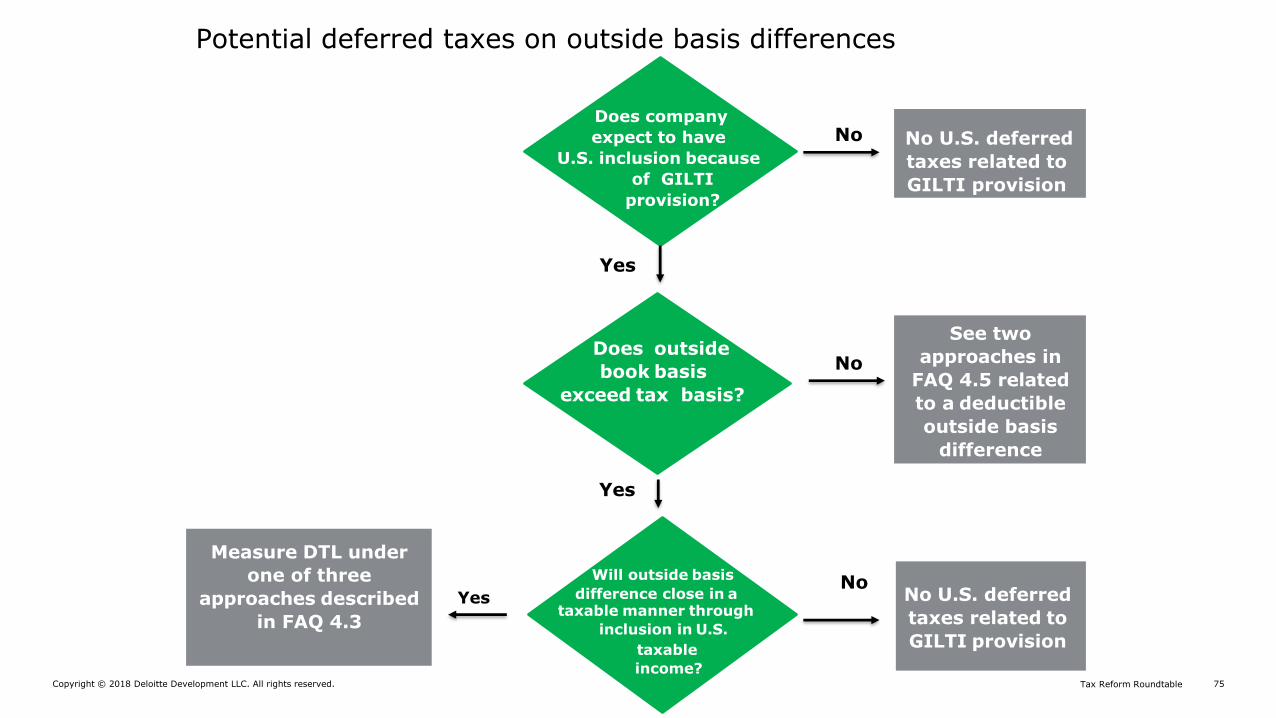

Is the indefinite reinvestment assertion still relevant?

Outside basis differences (e.g., indefinite reinvestment) still need to be considered

Tax reform does not change US GAAP requirement to consider whether deferred taxes should be recorded for outside basis differences in investments in foreign subsidiaries and corporate joint ventures that are essentially permanent in duration

Foreign tax considerations

• Consider all entities in the organization chart

• Withholding taxes – DTLs may need to be recorded for withholding taxes and state taxes if distributions are anticipated

US federal and state tax considerations

While some basis differences may not represent taxable temporary differences due to 100% DRD, others might. For example,

• Capital gains – still taxable in the US (Consider impact of §1248)

• IRC § 986(c) – Foreign currency gain or loss with respect to distributions of previously taxed income

• State taxes – DTLs may be recorded for state taxes if actual distributions are anticipated

• GILTI – Consider whether the provisions could potentially have an impact on indefinite reinvestment assertion (see examples that follow)

Copyright © 2018 Deloitte Development LLC. All rights reserved. 74Tax Reform Roundtable

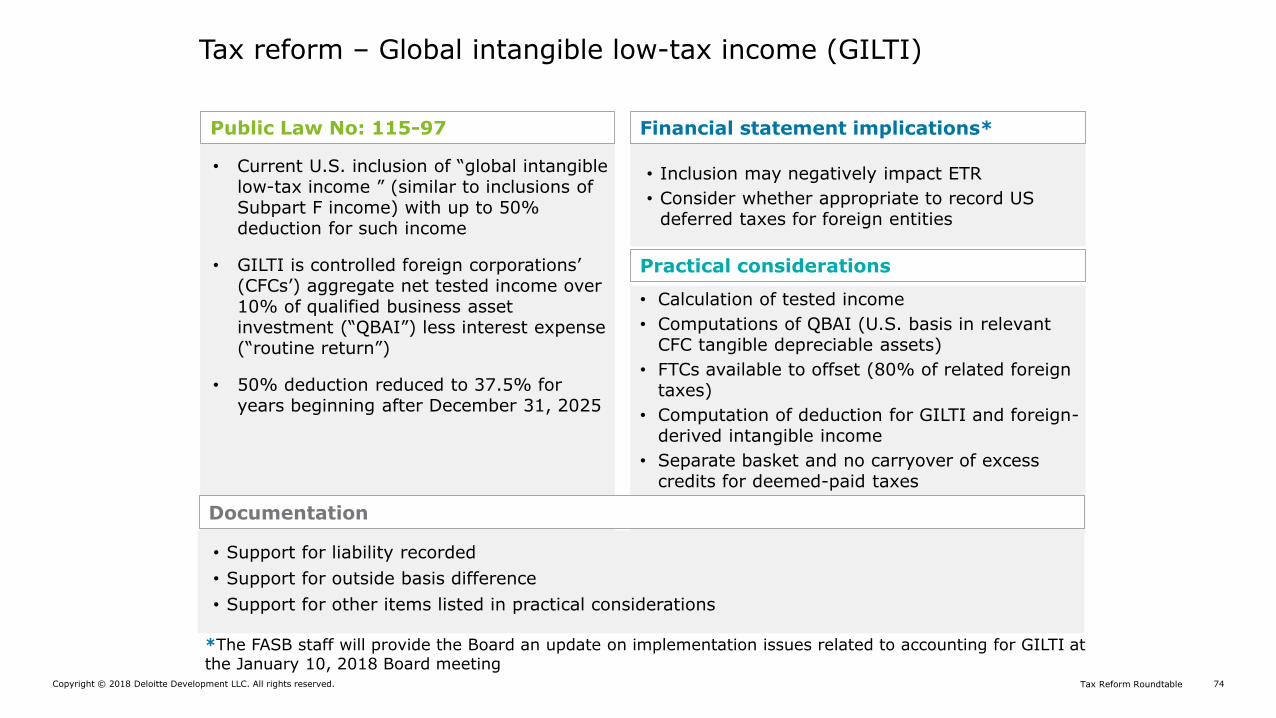

Financial statement implications*Public Law No: 115-97

Tax reform – Global intangible low-tax income (GILTI)

Practical considerations

Documentation

• Inclusion may negatively impact ETR

• Consider whether appropriate to record US deferred taxes for foreign entities

• Calculation of tested income

• Computations of QBAI (U.S. basis in relevant CFC tangible depreciable assets)

• FTCs available to offset (80% of related foreign taxes)

• Computation of deduction for GILTI and foreign-derived intangible income

• Separate basket and no carryover of excess credits for deemed-paid taxes

• Support for liability recorded

• Support for outside basis difference

• Support for other items listed in practical considerations

• Current U.S. inclusion of “global intangible low-tax income ” (similar to inclusions of Subpart F income) with up to 50% deduction for such income

• GILTI is controlled foreign corporations’ (CFCs’) aggregate net tested income over 10% of qualified business asset investment (“QBAI”) less interest expense (“routine return”)

• 50% deduction reduced to 37.5% for years beginning after December 31, 2025

*The FASB staff will provide the Board an update on implementation issues related to accounting for GILTI at the January 10, 2018 Board meeting

Copyright © 2018 Deloitte Development LLC. All rights reserved. 75Tax Reform Roundtable

No U.S. deferred

taxes related to

GILTI provision

See two

approaches in

FAQ 4.5 related

to a deductible

outside basis

difference

No U.S. deferred

taxes related to

GILTI provision

Does company

expect to have

U.S. inclusion because

of GILTI

provision?

Does outside

book basis

exceed tax basis?

Will outside basis

difference close in ataxable manner through

inclusion in U.S.

taxable

income?

Measure DTL under

one of three

approaches described

in FAQ 4.3

No

No

No

Yes

Yes

Yes

Potential deferred taxes on outside basis differences

Copyright © 2018 Deloitte Development LLC. All rights reserved. 76Tax Reform Roundtable

Public Law No: 115-97 Financial statement implications

Documentation

Foreign-derived intangible income (FDII)

• Deduction for 37.5% of FDII (21.875% after 12/31/2025)

• If sum of grossed up GILTI plus FDII exceeds taxable income, GILTI and FDII are reduced proportionately by the excess for purposes of calculating the deduction

• New favorable impact on ETR

• We believe that these deductions are analogous to special deductions cited in ASC 740-10-25-7 and should be accounted for as such

• Support for items listed in practical considerations

Foreign-derived intangible income deduction

Property sold for foreign use (assumption) $ 30.0

Services for foreign use (assumption) 50.0

Total deduction eligible income A $ 80.0

U.S. taxable income (assumption) B $ 200.0

Foreign derived intangible deduction (< of 37.5% of A or B) $ 30.0

Tax-effect of the deduction (assuming 21% rate) $ 6.3

Practical considerations

• Computation of deduction for foreign-derived intangible income

Copyright © 2018 Deloitte Development LLC. All rights reserved. 77Tax Reform Roundtable

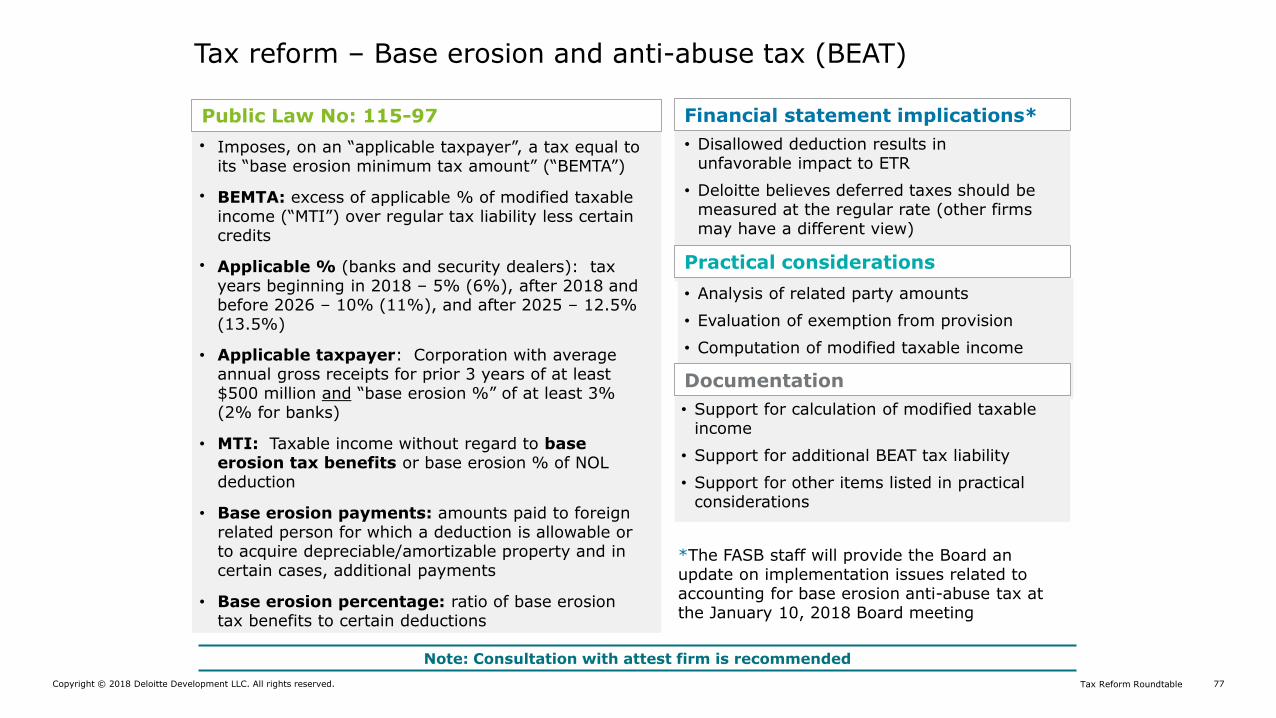

Financial statement implications*Public Law No: 115-97

Tax reform – Base erosion and anti-abuse tax (BEAT)

Practical considerations

Documentation:

• Disallowed deduction results in unfavorable impact to ETR

• Deloitte believes deferred taxes should be measured at the regular rate (other firms may have a different view)

• Analysis of related party amounts

• Evaluation of exemption from provision

• Computation of modified taxable income

• Support for calculation of modified taxable income

• Support for additional BEAT tax liability

• Support for other items listed in practical considerations

• Imposes, on an “applicable taxpayer”, a tax equal to its “base erosion minimum tax amount” (“BEMTA”)

• BEMTA: excess of applicable % of modified taxable income (“MTI”) over regular tax liability less certain credits

• Applicable % (banks and security dealers): tax years beginning in 2018 – 5% (6%), after 2018 and before 2026 – 10% (11%), and after 2025 – 12.5% (13.5%)

• Applicable taxpayer: Corporation with average annual gross receipts for prior 3 years of at least $500 million and “base erosion %” of at least 3% (2% for banks)

• MTI: Taxable income without regard to base erosion tax benefits or base erosion % of NOL deduction

• Base erosion payments: amounts paid to foreign related person for which a deduction is allowable or to acquire depreciable/amortizable property and in certain cases, additional payments