Surgent's Essential Depreciation and Expensing Update

88

Surgent's Essential Depreciation and Expensing Update TDP4/21/W1 Today’s Presenter Loredana Scarlat, CPA, MsA Lori Scarlat is a NY‐licensed CPA with over 14 years of experience in public accounting, providing tax services addressing everything from trust, estate, and gift tax matters to international tax services for individuals. She has worked with small and mid‐size companies and high‐net‐worth individuals. She has co‐authored presentations on introductory courses to 1040, GILTI tax, and U.S. tax treatment of international pensions. Prior to joining Surgent, she was a Tax Manager at BDO USA, LLP. She is a member of the New York State Society of CPAs as well as the AICPA. © Surgent | TDP4/21/W1 2

Transcript of Surgent's Essential Depreciation and Expensing Update

Surgent's Essential Depreciation and Expensing Update

TDP4/21/W1

Today’s Presenter

Loredana Scarlat, CPA, MsA

Lori Scarlat is a NY‐licensed CPA with over 14 years of experience in public accounting, providing tax services addressing everything from trust, estate, and gift tax matters to international tax services for individuals. She has worked with small and mid‐size companies and high‐net‐worth individuals. She has co‐authored presentations on introductory courses to 1040, GILTI tax, and U.S. tax treatment of international pensions. Prior to joining Surgent, she was a Tax Manager at BDO USA, LLP. She is a member of the New York State Society of CPAs as well as the AICPA.

© Surgent | TDP4/21/W12

This Product Is Intended To Serve Solely as an Aid in Continuing Professional Education Due to the constantly changing nature of the subject of the materials, this product is not appropriate to serve as the sole resource for any tax and accounting opinion or return position and must be supplemented for such purposes with other current authoritative materials.

The information in this course has been carefully compiled from sources believed to be reliable, but its accuracy is not guaranteed.

In addition, Surgent McCoy CPE, LLC, its authors, and instructors are not engaged in rendering legal, accounting, or other professional services and will not be held liable for any actions or suits based on this manual or comments made during any presentation.

If legal advice or other expert assistance is required, seek the services of a competent professional.

© Surgent | TDP4/21/W13

Course Objectives

Comprehensive training in tax laws pertaining to property acquisition, depreciation, sale, exchange or disposal

© Surgent | TDP4/21/W14

Course Contents

1) Depreciation Overview – Capitalized Assets

2) Expensing Election §179

3) Depreciation and MACRS Cost Recovery

4) Listed Property, Luxury Auto Limits, Compensation

5) Sale or Exchange of Business and Depreciable Property

6) Miscellaneous Items

© Surgent | TDP4/21/W15

A Quick Word on Policy vs Politics

Many times, when discussing accounting, tax and finance policy issues, it can be difficult to divorce the politics from the policy.

Today, we will discuss the current tax law provisions and the opportunities that exist therein; we will point out the areas where we anticipate changes in policy; however, we will not comment on the merits or righteousness of any of the current/future provisions.

© Surgent | TDP4/21/W16

Depreciation Overview –Capitalized Assets

Chapter 1

© Surgent | TDP4/21/W17

History

Since the Reconstruction Era Income Tax Act of 1870, there has been a deduction limitation that prohibits a taxpayer from deducting amounts paid for new buildings, permanent improvements, or betterments made to increase the value of property

While this concept has been recognized as part of tax law almost from its inception, exactly what must be capitalized and what may be currently deducted has been at issue ever since

© Surgent | TDP4/21/W18

2020 and Beyond ‐‐ Concluding Temporary Permanence ‐‐ Taming Temporary Brevity Congress seems to regularly consider changes to depreciation

Most individuals lack an endlessly long‐term memory

Other individuals utilize the curse of: ‐ or ‐ embrace a convenience of: ‐ the lack of a short‐term memory

However, even those with the shortest of recollections realize the Protecting Americans from Tax Hikes (PATH) Act of 2015 permanently extended §179 In Washington, a “permanent” provision does not mean what one would consider the definitional meaning of the word. Actually in Washington “permanent” is just another way to say “this provision does not have a sunset”

© Surgent | TDP4/21/W19

2020 and Beyond ‐‐ Concluding Temporary Permanence ‐‐ Taming Temporary BrevityWith all the “permanence” of PATH, it took a relatively short time period before TCJA doubled the electable deduction

Bonus depreciation, also known as “Additional First‐Year Depreciation (AFYD) under §168(k), was also doubled by TCJA and extended through the middle of the current decade

Practitioners can rest assured that Congress will feel the need to tinker with all tax provisions, including depreciation

© Surgent | TDP4/21/W110

2021 and Beyond ‐‐ Concluding Temporary Permanence ‐‐ Taming Temporary BrevityOn March 27, 2020, President Trump signed the Coronavirus Aid, Relief, and Economic Security Act (CARES Act)…tax relief for businesses and individuals detrimentally impacted by COVID‐19

The CARES Act did not focus on depreciation; however, it did include a technical correction required by an omission within the TCJA

….a technical correction has been expected for more than 2 years

The CARES Act provides that QIP be included as 15‐year property under §168(e)(3)(E)

With this technical correction QIP is eligible for 100% bonus depreciation. This change is effective for property placed in service after 12/31/17 See Chapter 4 ‐ possible amendment situations ‐ Rev. Proc. 2020‐25

© Surgent | TDP4/21/W111

General Current Law

§263(a)(1) provides that no deduction shall be allowed for any amounts paid out for new buildings or for permanent improvements or betterments made to increase the value of any property or estate

§263A, enacted in 1986, also applies to property produced by the taxpayer for use in its business or an activity conducted for profit (UNICAP)

Capitalization is the proper treatment for expenditures incurred in new construction: Capitalization is also generally required for additions to existing buildings or for installations of material components to buildings or equipment

© Surgent | TDP4/21/W112

General Current Law

Reg. §1.263(a)‐1(b) provides that capital expenditures include amounts paid or incurred to:

• Add to the value, or substantially prolong the useful life of property owned by the taxpayer, such as plant or equipment; or

• Adapt property to a new or different use

© Surgent | TDP4/21/W113

General Current Law

Section 162 provides a deduction for all ordinary and necessary business expenses paid or incurred during the taxable year in carrying on a trade or business: Reg. §1.162‐4 provides that the cost of incidental repairs which neither materially add to the value of the property nor appreciably prolong its life, but keep it in an ordinarily efficient operating condition, may be deducted

However, this regulation also provides that repairs in the nature of replacements, to the extent that they arrest deterioration and appreciably prolong the useful life of the property, shall either be capitalized and depreciated or charged against the depreciation reserve

Additions that are newly installed components are required to be capitalized. This requirement applies to both §1245 and §1250 property

© Surgent | TDP4/21/W114

General Current Law

What may seem intuitive on the surface, may actually pose a lot of questions:

• Does the new roof qualify as a repair that is ordinary and necessary under §162, and therefore fully deductible?

• Is the new roof required to be capitalized, yet qualifies under the new definition of Qualified Real Property for the §179 election?

• Or is the property available for the 100‐percent additional first‐year depreciation deductions of §168(k)?

• Then again could the new roof qualify for full expensing under the safe harbor for small taxpayers detailed in Regulation §1.263(a)‐3(h)?

• Is another option full expensing under the safe harbor for routine maintenance for buildings?

• Perhaps capitalization, not qualifying or electing out of §179 and §168(k), and depreciation covering as MACRS property?

© Surgent | TDP4/21/W115

$50,000 for Roof Repair Northen and Cox TC Sum 2003‐113 8/13/03 Just too much grey area ‐ Why the Capitalization Regs were in need of updating

Tom & Shirley each owned ½ of 23,000 sq. ft. commercial building

Roof leaked (under a/c) and damaged tenants’ materials. Tenants threatened legal action

Shirley hired Armstrong to stop leaks and install foam roofing system. Armstrong said roof basically intact except in one location

The entire $52,880 was deducted Was entire amount deductible? Yes. The expenditure was solely to restore property from one with leaks to one without

© Surgent | TDP4/21/W116

II. Assets That Are Subject to Depreciation

What do we depreciate?

Tangible Personal Property (buildings, machinery, furniture, etc.)

Intangible Property: Copyrights Patents and Computer software

Intangible Assets – §197 assets (in the form of amortization): Goodwill Covenants not to compete

Capital expenditures used in (§168): Taxpayer’s trade or business; or Production of income

Not capital assets

© Surgent | TDP4/21/W117

Basic Requirements

To be depreciable, the property must meet all of the following requirements: Must hold title;

Used in business or income‐producing activity;

Have a determinable useful life (subject to wear and tear);

Expected to last more than one year; and

Not be “excepted property”

© Surgent | TDP4/21/W118

III. What Is the Basis in Depreciable Property?

Cost: Cost plus related amounts:

Sales tax;

Freight;

Installation and testing fees;

Includes amounts paid; or

Liabilities assumed

Other basis: Inheritance

Gift

Transfer or exchange

© Surgent | TDP4/21/W119

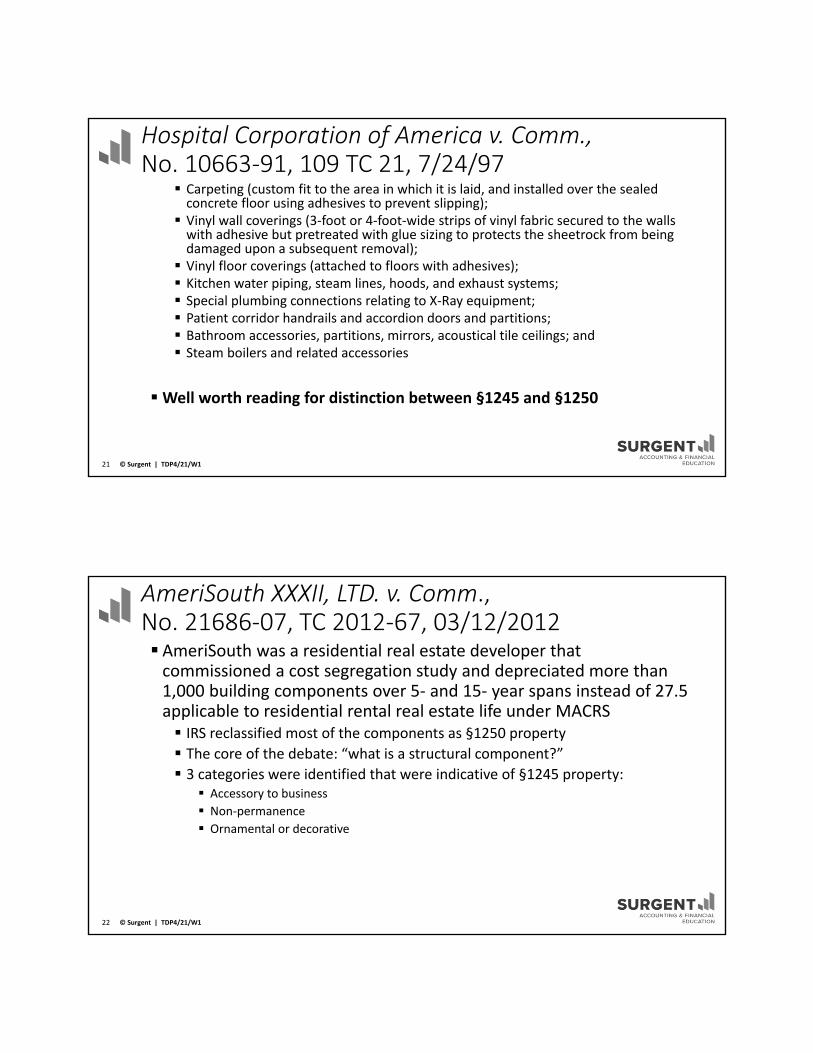

Hospital Corporation of America v. Comm., No. 10663‐91, 109 TC 21, 7/24/97 The Birth of Cost Segregation ‐ Items In Controversy: Part of the primary electrical distribution system used to bring electricity from outside power sources to the main building to the extent the “load” was attributable to HCA’s specialty equipment needs;

Part of the secondary electrical distribution systems, including main switchgears, steel cabinets attached to concrete pillars, conduit, wiring, etc. to the extent attributable to HCA’s specialty equipment needs;

Branch electrical wiring and connections and special electrical equipment which relate to particular items of hospital equipment;

Wiring and related property items relating to: Kitchen equipment

Laboratory and maintenance shop equipment

Television, telephone, communication equipment

© Surgent | TDP4/21/W120

Hospital Corporation of America v. Comm., No. 10663‐91, 109 TC 21, 7/24/97

Carpeting (custom fit to the area in which it is laid, and installed over the sealed concrete floor using adhesives to prevent slipping); Vinyl wall coverings (3‐foot or 4‐foot‐wide strips of vinyl fabric secured to the walls with adhesive but pretreated with glue sizing to protects the sheetrock from being damaged upon a subsequent removal); Vinyl floor coverings (attached to floors with adhesives); Kitchen water piping, steam lines, hoods, and exhaust systems; Special plumbing connections relating to X‐Ray equipment; Patient corridor handrails and accordion doors and partitions; Bathroom accessories, partitions, mirrors, acoustical tile ceilings; and Steam boilers and related accessories

Well worth reading for distinction between §1245 and §1250

© Surgent | TDP4/21/W121

AmeriSouth XXXII, LTD. v. Comm., No. 21686‐07, TC 2012‐67, 03/12/2012 AmeriSouth was a residential real estate developer that commissioned a cost segregation study and depreciated more than 1,000 building components over 5‐ and 15‐ year spans instead of 27.5 applicable to residential rental real estate life under MACRS IRS reclassified most of the components as §1250 property

The core of the debate: “what is a structural component?”

3 categories were identified that were indicative of §1245 property: Accessory to business

Non‐permanence

Ornamental or decorative

© Surgent | TDP4/21/W122

Expensing Election §179Chapter 2

© Surgent | TDP4/21/W123

Review Exercise:The details are included within this chapter, with further discussion at the end of the chapter.

Edging closer to the Boundaries of §179 Limitations

Income (Loss) §179 Amount

Form W‐2 – Pam $600,000 $0

Schedule C – Jim – Net Loss ($30,000) $640,000

Partnership K‐1 Jim – T/B $500,000 $500,000

Totals $1,070,000 $1,140,000

How much of the §179 available can Jim and Pam deduct on their joint tax return, and what happens to any excess?

© Surgent | TDP4/21/W124

§179 Depreciation in 2021: Concluding Temporary Permanence The following discussion of the Section 179 deduction (Form 4562 –Part I) is directed toward tax years 2021, with additional reference to 2020. For nearly 15 years, §179 limitations have been regularly sun‐setting only to be retroactively resurrected. The limitations were finally set and declared “permanent” in 2015.

The Tax Cuts and Jobs Act (TCJA) of 2017 modified §179 by doubling the 2017‐dollar limitation base of $500,000 to $1,000,000. TCJA also increased the “Acquisition Limit” base amount from 2017’s $2,000,000 to $2,500,000.

In addition, TCJA updates the inflation adjustment, resulting in a 2021 limitation base of $1,050,000. Inflation adjustments also increase the 2021 “Acquisition Limit” base amount to $2,620,000.

© Surgent | TDP4/21/W125

II. General Rules ‐ Section 179 Expense Deduction: I.R.C. §179 §179 election to expense

Applies to Qualifying Property acquired during the year and certain other property described

Excludes property: Held for investment; and

Held or used by an estate, trust, tax‐exempt, or passive activity

Property must be purchased

Expensed amount reduces basis for depreciation

Predominant Business Use = More than 50%

© Surgent | TDP4/21/W126

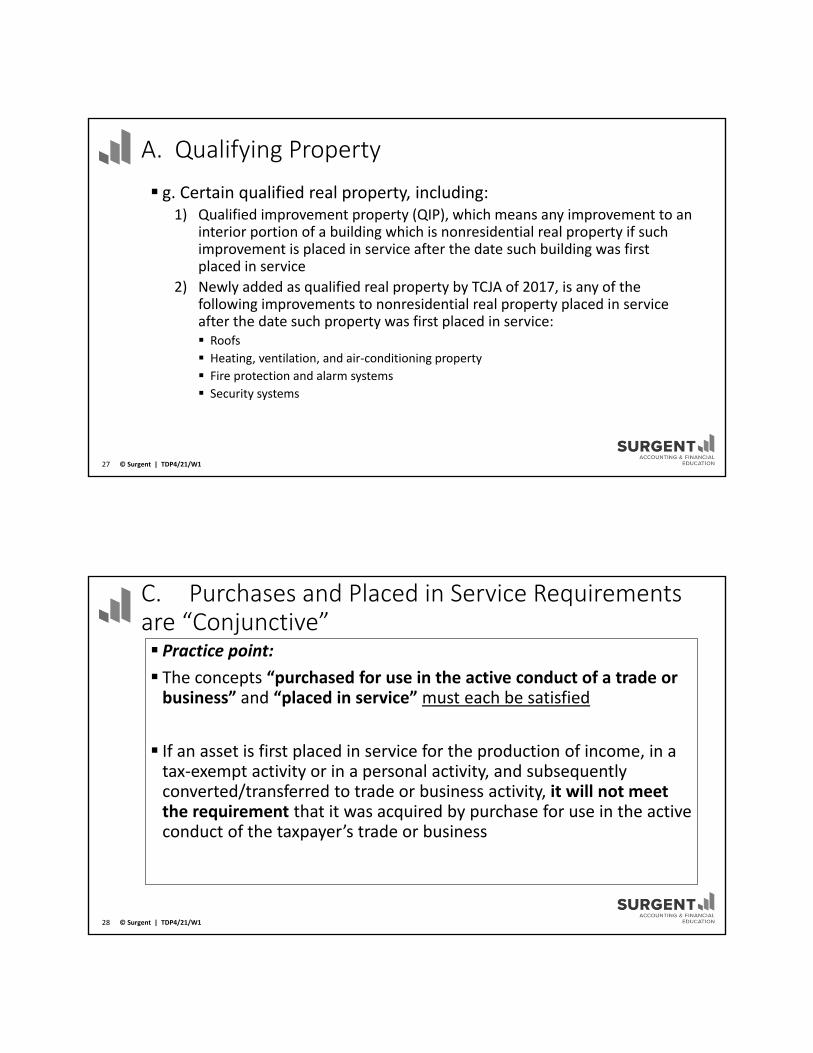

A. Qualifying Property

g. Certain qualified real property, including:1) Qualified improvement property (QIP), which means any improvement to an

interior portion of a building which is nonresidential real property if such improvement is placed in service after the date such building was first placed in service

2) Newly added as qualified real property by TCJA of 2017, is any of the following improvements to nonresidential real property placed in service after the date such property was first placed in service: Roofs

Heating, ventilation, and air‐conditioning property

Fire protection and alarm systems

Security systems

© Surgent | TDP4/21/W127

C. Purchases and Placed in Service Requirements are “Conjunctive” Practice point:

The concepts “purchased for use in the active conduct of a trade or business” and “placed in service” must each be satisfied

If an asset is first placed in service for the production of income, in a tax‐exempt activity or in a personal activity, and subsequently converted/transferred to trade or business activity, it will not meet the requirement that it was acquired by purchase for use in the active conduct of the taxpayer’s trade or business

© Surgent | TDP4/21/W128

III. Section 179 Election Procedures

Election is required on original return (whether or not filed on time) or amended return filed no later than due date (including extensions for year property placed in service)

Election is made in Part I of Form 4562 Property must be listed or scheduled

© Surgent | TDP4/21/W129

III. Section 179 Election Procedures

© Surgent | TDP4/21/W130

III. Section 179 Election Procedures

2. Any election made may be revoked by the taxpayer with respect to any property, and such revocation, once made, shall be irrevocable a. For tax years beginning before 2003, generally any election could not be revoked without IRS consent

C. Manner of making an election or revoking an election under §179 Examples

© Surgent | TDP4/21/W131

Maximum Amount Limitation ‐ §179 Expense Amount A. The maximum §179 expense amount for 2021 is $1,050,000

B. Maximum depreciation deduction for sport utility vehicles (SUVs) to $26,200 Included with TCJA is a new inflationary adjustment commencing for years beginning after 2018

© Surgent | TDP4/21/W132

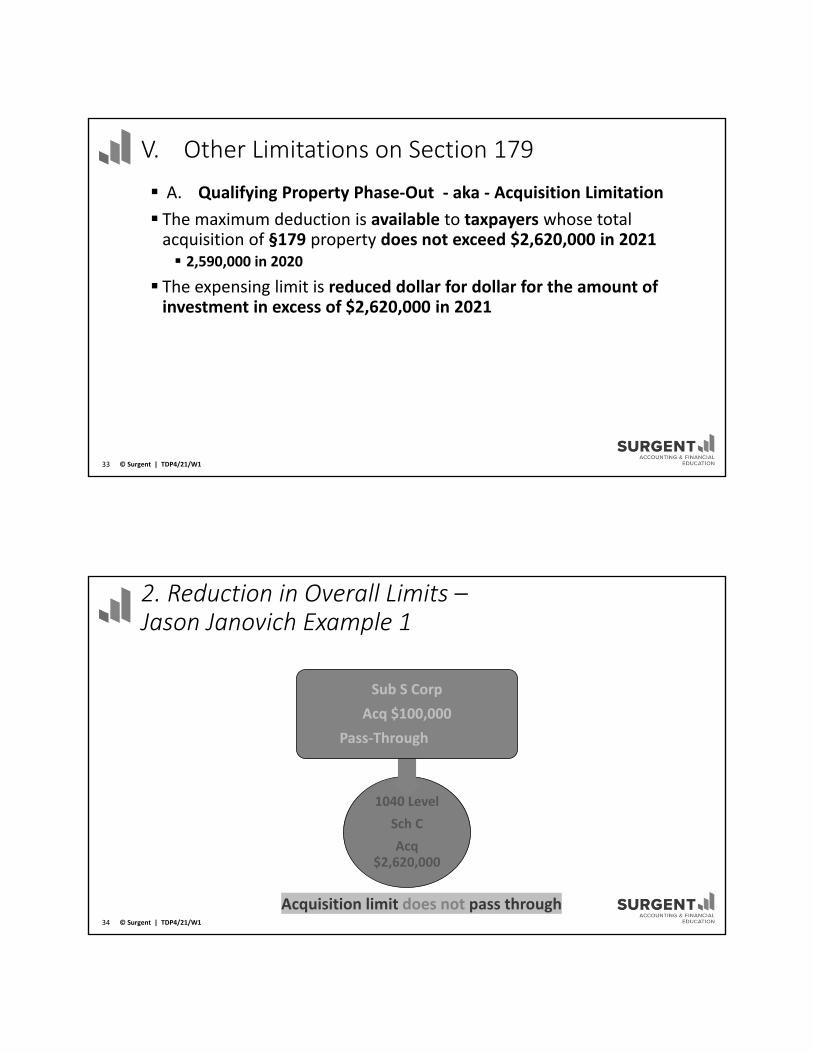

V. Other Limitations on Section 179

A. Qualifying Property Phase‐Out ‐ aka ‐ Acquisition Limitation

The maximum deduction is available to taxpayers whose total acquisition of §179 property does not exceed $2,620,000 in 2021 2,590,000 in 2020

The expensing limit is reduced dollar for dollar for the amount of investment in excess of $2,620,000 in 2021

© Surgent | TDP4/21/W133

2. Reduction in Overall Limits –Jason Janovich Example 1

Acquisition limit does not pass through

1040 Level

Sch C

Acq $2,620,000

Sub S Corp

Acq $100,000

Pass‐Through 50%?

© Surgent | TDP4/21/W134

2. Reduction in Overall Limits –Jason Janovich Example 2 b. Example 2: §179 limited by “Acquisition limit”

Assume the same facts as in example above, except that Jason directly purchased $2,690,000 of equipment.

Cost $ 2,690,000

Less: §179 Expense* ( 980,000)

Depreciable Basis $ 1,710,000

*NOTE: The §179 expense is reduced dollar for dollar by the amount of property purchased in excess of $2,620,000 in 2021.

Statutory §179 Expense Election (2021) $ 1,050,000

Cost of §179 eligible property acquired $2,690,000

§179 Acquisition Limit (2021) ( 2,620,000)

Excess purchases (70,000)

Allowable §179 Expense for year $980,000

© Surgent | TDP4/21/W135

2. Reduction in Overall Limits –Jason Janovich Example 2

© Surgent | TDP4/21/W136

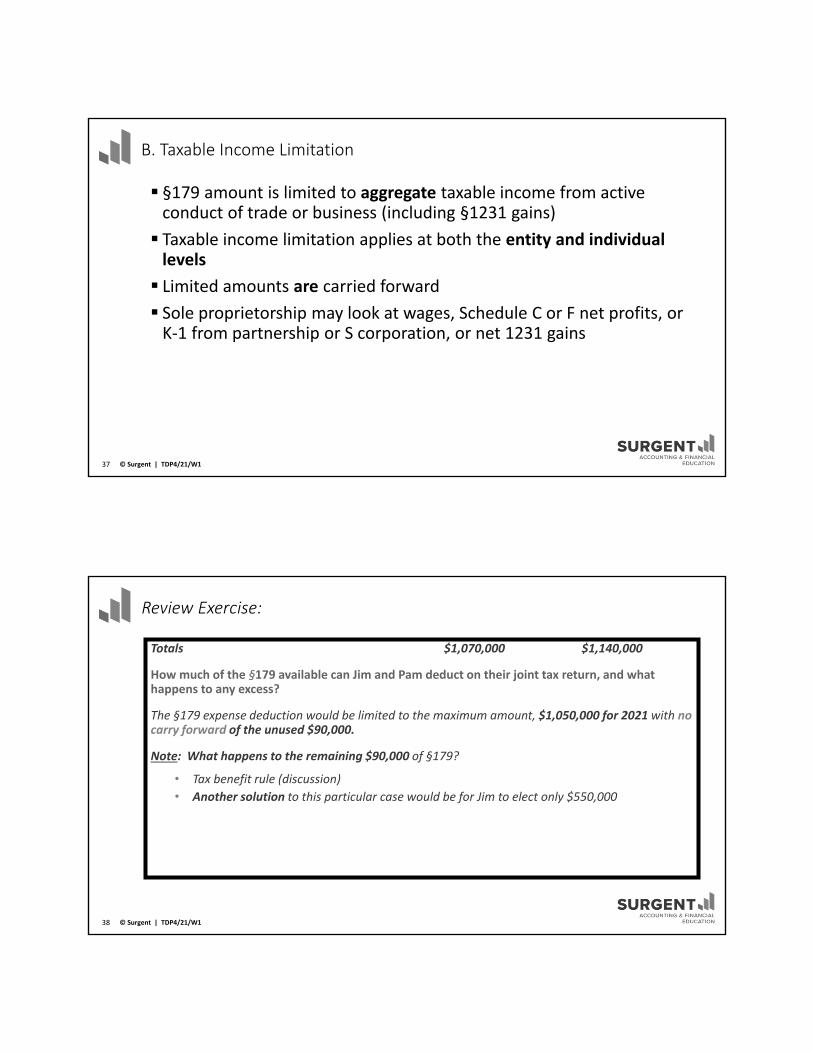

B. Taxable Income Limitation

§179 amount is limited to aggregate taxable income from active conduct of trade or business (including §1231 gains)

Taxable income limitation applies at both the entity and individual levels

Limited amounts are carried forward

Sole proprietorship may look at wages, Schedule C or F net profits, or K‐1 from partnership or S corporation, or net 1231 gains

© Surgent | TDP4/21/W137

Review Exercise:

Totals $1,070,000 $1,140,000

How much of the §179 available can Jim and Pam deduct on their joint tax return, and what happens to any excess?

The §179 expense deduction would be limited to the maximum amount, $1,050,000 for 2021 with no carry forward of the unused $90,000.

Note: What happens to the remaining $90,000 of §179?

• Tax benefit rule (discussion)

• Another solution to this particular case would be for Jim to elect only $550,000

© Surgent | TDP4/21/W138

VII. Section 179 Special Rules for Pass‐Through Entities

Final regulations clearly indicate that the “taxable income limitation” applies at both the entity level and the individual level for S corporations, partnerships, and the owners: Treas. Reg. §1.179‐2(c)(3)

For the §179 deduction for S corporations, net income is income BEFORE shareholders’ salaries

For the §179 deduction for entities taxed as partnerships, net income is income BEFORE guaranteed payments to partners

© Surgent | TDP4/21/W139

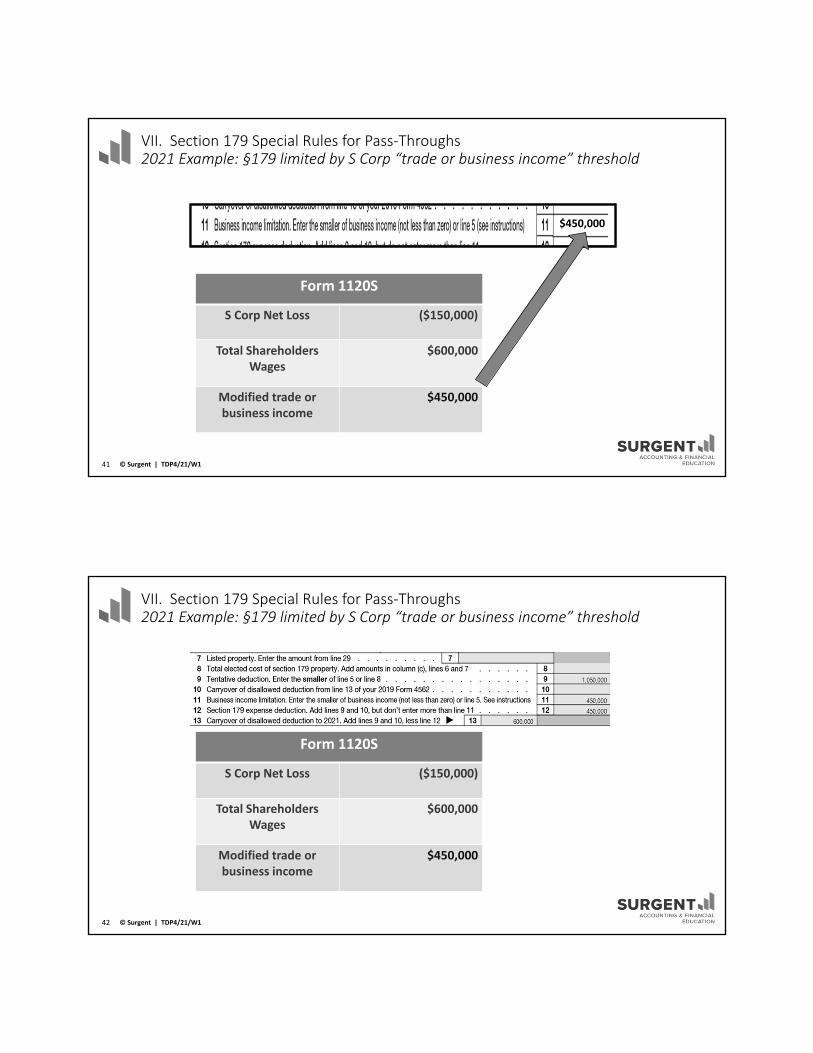

VII. Section 179 Special Rules for Pass‐Throughs2021 Example: §179 limited by S Corp “trade or business income” threshold

Form 1120S

S Corp Net Loss ($150,000)

Total Shareholders Wages

$600,000

Modified trade or business income

$ ????

© Surgent | TDP4/21/W140

VII. Section 179 Special Rules for Pass‐Throughs2021 Example: §179 limited by S Corp “trade or business income” threshold

Form 1120S

S Corp Net Loss ($150,000)

Total Shareholders Wages

$600,000

Modified trade or business income

$450,000

$450,000

© Surgent | TDP4/21/W141

VII. Section 179 Special Rules for Pass‐Throughs2021 Example: §179 limited by S Corp “trade or business income” threshold

Form 1120S

S Corp Net Loss ($150,000)

Total Shareholders Wages

$600,000

Modified trade or business income

$450,000

© Surgent | TDP4/21/W142

VII. Section 179 Special Rules for Pass‐Through Entities B. Special §179 rules with respect to trusts and estates which are S corporation shareholders or partners in partnerships Section 179 election is not available for trusts or estates; a partner or S corporation shareholder that is a trust or estate may not deduct its allocable share of the §179 expense elected by the partnership or S corporation

© Surgent | TDP4/21/W143

VII. Section 179 Special Rules for Pass‐Through Entities C. Special reporting procedures for dispositions of §179 expensed property

1. An S corporation or partnership must provide certain information with respect to the gain or loss on the sale, exchange, or other disposition of property for which a §179 expense deduction was passed through to shareholders or partners rather than reporting the gain or loss on Form 4797

Practice Note: As noted above, certain §179 deductions are limited by the “maximum amount” threshold and carried over at the individual level under the “tax‐benefit” rule. This special reporting is designed as a method to report to the individual shareholders or partners the disposal of property for which they may have a basis adjustment available under the tax benefit rule.

© Surgent | TDP4/21/W144

VIII. Allocation for Married Individuals

Married individuals’ §179 deduction is a function of filing status

1. Taxpayers filing jointly are treated as one taxpayer in determining any reduction to the dollar limit, regardless of who purchased the property or placed it in service

2. Taxpayers filing separate returns are treated as one taxpayer for the dollar limit, including the reduction for costs over $2,620,000 a. Allocate the dollar limit (after any reduction) between the separate returns equally, unless both elect a different allocation

© Surgent | TDP4/21/W145

VIII. Allocation for Married Individuals

Example 1: Facts ... Walter White is married to Skyler. They file separate returns. Walter bought and placed in service $1,500,000 of qualified machinery for his single member LLC (Schedule C) in 2021

Skyler owns a car wash, also a single member LLC (Schedule C) and she bought and placed in service $1,300,000 of qualified business equipment

Conclusion and Analysis … Their combined §179 acquisitions amount to $2,800,000

Their combined §179 deduction dollar limit is $870,000

© Surgent | TDP4/21/W146

VIII. Allocation for Married Individuals

Example 1: Conclusion and Analysis…Their combined §179 deduction dollar limit is $870,000

This is because they must figure the limit as if they were one taxpayer. They reduce the $1,050,000 dollar limit by the $180,000 excess of their costs over $2,620,000

They may elect to allocate the $870,000 dollar limit equally or in any percentage they elect However, if they did not make an election to allocate their costs, or if their allocation did not total 100 percent, they would have to allocate $435,000 ($870,000 × 50%) to each of them

© Surgent | TDP4/21/W147

IX. Controlled Group of Corporations Allocation

All component members of a controlled group shall be treated as one taxpayer in applying the dollar limitations of §179 Controlled group is defined in §1563(a), except that, for such purposes, the “more than 50 percent” test is substituted for the “at least 80 percent” each place it appears

© Surgent | TDP4/21/W148

IX. Controlled Group of Corporations Allocation

Practice note: S Corporation members of a controlled group

An S corporation is treated as an excluded member of a controlled group of corporations. Any member of a controlled group that is treated as an excluded member is not a component member, but is a member of the group

No tax benefit items should be apportioned to an excluded member Thus, an S corporation may make a §179 election up to the maximum election amount, even if it is otherwise a member of a controlled group of corporations for purposes of §1563(a)

© Surgent | TDP4/21/W149

XII. Case ‐ §179 Expense Election

T/B Income

W‐2 ‐ Meredith (not from S corporation) $ 321,000

Schedule C (before §179 deduction) – Derek $( 80,000)

Partnership ‐ K‐1 $ 9,000

S corporation K‐1 $( 90,000)

§179 Exp. Amount

Schedule C ‐ $ 196,000

Partnership ‐ $ 39,000

S corporation $ 36,000

© Surgent | TDP4/21/W150

XII. Case ‐ §179 Expense Election

Apply the Acquisition Limit ($2,620,000 in 2021) – Form 4562, Lines 2‐5

Total acquisitions of §179 property for Derek and Meredith are only the $196,000 acquired on Derek’s Schedule C

The S corporation acquisitions and the partnership acquisitions are each subject to their own $2,620,000 acquisition limitations at the entity level

© Surgent | TDP4/21/W151

XII. Case ‐ §179 Expense Election

Next: Apply the Maximum Amount limitation – Form 4562,Line 9

Total §179 expense elections during the year from all trade or businesses of Derek and Meredith is $271,000

Since the above §179 expense total does not exceed $1,050,000 in 2021, the $271,000 amount potentially qualifies

© Surgent | TDP4/21/W152

XII. Case ‐ §179 Expense Election

Next: Apply the Business Income limitation – Form 4562, Line 11

Total aggregate taxable income derived from any trade or business including W‐2 wages, before any §179 deduction, amounts to $160,000

W‐2 ‐ Meredith $321,000

Schedule C ‐ Derek (80,000)

Partnership ‐ K‐1 Derek 9,000

S corporation K‐1 Meredith ( 90,000)

Total $160,000

© Surgent | TDP4/21/W153

XII. Case ‐ §179 Expense Election

Maximum §179 expense deduction for 2021 and carryover to 2022 ‐Form 4562, Lines 12 & 13

Thus, the §179 expense allowable deduction for the current year is limited to $160,000

The remaining $111,000 of §179 ($271,000 ‐ $160,000) is carried forward to the following year

© Surgent | TDP4/21/W154

Depreciation and MACRS Cost Recovery

Chapter 3

© Surgent | TDP4/21/W155

Review Exercise:The details are included within this chapter, with further discussion at the end of the chapter.

Early in your career you were assigned the task of preparing the tax return for Cervantes Inc. Cervantes had purchased desks and other office furniture.

You input the cost basis into your computer software, but what the heck was the recovery period?

The drop‐down box helps you and you think 7 years may be the answer.

How did you first find “recovery periods?”

© Surgent | TDP4/21/W156

Bonus Depreciation in 2021

Bonus Depreciation and MACRS

The following discussions regarding §168(k) (Form 4562 – Part II) and MACRS (Form 4562 – Part III) depreciation deductions are directed toward tax years 2021. In the previous chapter it was noted the TCJA of 2017 and Protecting Americans from Tax Hikes (PATH) permanently extended §179. The same is not true for bonus depreciation under §168(k)

TCJA both increases and extends for 5 years bonus depreciation (aka ‐AFYD) through 2022. The 4‐year period from 2023 through 2026 of 100% deductions is stepped‐down 20% per year, until the rule sunsets in 2027

MACRS deductions have been in existence since 1987 and had incurred minor changes since. However, on a whole, MACRS remains a constant, steady calculation

© Surgent | TDP4/21/W157

III. TCJA ‐ 100 Percent Additional First‐Year Depreciation Resurrected and Broadened In 2017 Congress, brought back the 100 percent additional first‐year depreciation deduction through 2022

Some changes were made: Most notable is the removal of the previous requirement that qualifying property must be new property, placed into service for the first time

TCJA amends the definition of qualifying property under §168(k)(2)(E)(ii) to allow for NEW and USED property by providing an acquisition of property meets the requirements if: The original use of the property begins with the taxpayer or the property was not used by the taxpayer at any time prior to such acquisition……

© Surgent | TDP4/21/W158

VI. Property Excepted from Additional First‐Year Depreciation TCJA changed the definition of property eligible for bonus depreciation (qualified property) by including used property and removed the requirement that the original use of qualified property must commence with the taxpayer

On September 13, 2019, the IRS and Department of Treasury issued final and proposed regulations regarding the first‐year bonus depreciation deduction under §168(k) The September 2019 proposed regulations created a safe harbor that required taxpayers to look back five years when determining whether property was eligible as used property. Without a safe harbor, taxpayers would need to trace an asset’s history back to when it was first placed in service by any taxpayer in order to determine its prior ownership interests

The September 2019 proposed regulations outlined a Partnership Lookthrough rule to determine the extent to which a partner is deemed to have a depreciable interest in property held by a partnership The Partnership Lookthrough Rule provides that a person is treated as having a depreciable

interest in a portion of property prior to the person’s acquisition of the property if the person was a partner in a partnership at any time the partnership owned the property

© Surgent | TDP4/21/W159

VI. Property Excepted from Additional First‐Year DepreciationOn September 21, 2020, the IRS and Department of Treasury released the second round of final regulations, making further clarifications to §168(k) bonus depreciation under the TCJA The September 2020 final regulations confirm that only the five calendar years immediately prior to the taxpayer's current placed‐in‐service year of the property are taken into account when utilizing the five‐year safe harbor The “placed‐in‐service year” is the current calendar year in which the property is placed in service by the taxpayer

The five calendar years immediately prior to the current calendar year in which the property is placed in service by the taxpayer, as well as the portion of that calendar year up to the placed‐in‐service date of the property, should be considered in determining whether the taxpayer previously had a depreciable interest

The September 2020 final regulations withdrew the Partnership Lookthrough Rule outlined in the September 2019 proposed regulations, stating that it would place a significant administrative burden on both taxpayers and the IRS

© Surgent | TDP4/21/W160

VI. Property Excepted from Additional First‐Year Depreciation The September 2020 final regulations allow taxpayers to choose between applying the proposed regs or the final regs for property acquired between September 27, 2017, and the effective date for the final rule

In November 2020, the IRS released Rev Proc. 2020‐50, providing transition relief for taxpayers with property placed in service after September 27, 2017, and before January 1, 2021

Rev Proc. 2020‐50 allows taxpayers who filed tax returns and relied on prior bonus depreciation guidance to change to either the 2020 final regulations, 2019 final regulations, or both the 2019 final and proposed regulations

© Surgent | TDP4/21/W161

IV. §168(k) ‐ 100 Percent Additional First‐Year Depreciation after TCJAWhen in a Rush – Dotting “I”s and Crossing “T”s

Noticeably missing under the TCJA statutory language…“Qualified Improvement Property” leaving it as nonresidential real property (39 years – MACRS) and not subject to bonus depreciation

Expected for more than 2 years, but eventually was not provided until the passage of the CARES Act in early 2020

In many cases a tax amendment due to this retroactive correction will not be required, as most practitioners realized the technical correction was to be made and considered QIP property as eligible for bonus depreciation in 2018 and 2019

If a taxpayer and their practitioner did not utilize AFYD for qualifying QIP property placed in service in 2018 or 2019, and they desire to change, a proper amendment may be made or Form 3115 may be filed

© Surgent | TDP4/21/W162

IV. §168(k) ‐ 100 Percent Additional First‐Year Depreciation after TCJA F. Qualified Improvement Property (QIP) means any improvement to an interior portion of a building, which is nonresidential real property if such improvement is placed in service after the date such building was first placed in service

Such term shall not include any improvement for which the expenditure is attributable to: “(i) The enlargement of the building;

“(ii) Any elevator or escalator; or “(iii) The internal structural framework of the building”

© Surgent | TDP4/21/W163

IV. §168(k) ‐ 100 Percent Additional First‐Year Depreciation after TCJA Practice Note – QIP Significant difference from Qualified Leasehold Improvement (QLI) Property:

For assets placed in service after Dec. 31, 2015, the phraseology has changed from “Qualified Leasehold Improvement” property to “Qualified Improvement Property” as defined above

Practitioners should note items missing from new phraseology For assets placed in service prior to Jan. 1, 2016, the AFYD was allowed toward “Qualified Leasehold Improvement” (QLI) property. QLI property was also nonresidential, however it included the requirements of a valid non‐related party lease agreement, and that the improvement be placed in service more than three years after the date the building was first placed in service. Neither of those two provisions are included in the definition of QIP

© Surgent | TDP4/21/W164

IV. §168(k) ‐ 100 Percent Additional First‐Year Depreciation after TCJA Practice Note – QIP Significant difference from Qualified Leasehold Improvement (QLI) Property:

Practitioners should also note an item remaining the same In effect prior to and continuing in effect after the 2016 change is the rule that Qualified Restaurant Property, which did not meet the former definition of Qualified Leasehold Improvement Property, was not eligible for the additional first‐year depreciation deduction

A corollary to the phraseology has been consistently applied, that is, Qualified Restaurant Property that does not meet the new definition of Qualified improvement property is not eligible for the additional first‐year depreciation deduction

© Surgent | TDP4/21/W165

I. Depreciation and MACRS Cost Recovery

T. On March 27, 2020, President Trump signed the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) ….it included a technical correction…..that QIP be included as 15‐year property under §168(e)(3)(E) (20‐year for ADS)

With this technical correction QIP is eligible for 100% bonus depreciation

This change is effective for property placed in service after 12/31/17

On April 17, 2020, IRS released Rev. Proc. 2020‐25 Provides guidance allowing a taxpayer to change its depreciation under §168 for QIP placed in service by the taxpayer after December 31, 2017, in its taxable year ending in 2018 (2018 taxable year), 2019 (2019 taxable year), or 2020 (2020 taxable year)

© Surgent | TDP4/21/W166

I. Depreciation and MACRS Cost Recovery

On April 17, 2020, IRS released Rev. Proc. 2020‐25 This revenue procedure also allows a taxpayer to make a late election, or to revoke or withdraw an election, under the following: §168(g)(7) ‐ Election to use alternative depreciation system;

§168(k)(5) ‐ Special rules for certain plants bearing fruits and nuts;

§168(k)(7) ‐ The election out of the special depreciation allowance (aka bonus, or additional first year depreciation)

Without this Rev. Proc. the election out provision could only be revoked with the consent of the Secretary. Rev. Proc. 2020‐25 provides the required consent

§168(k)(10) ‐ Special rule for property placed in service during the first taxable year ending after September 27, 2017, which allowed a taxpayer to elect 50% bonus depreciation in lieu of 100%

© Surgent | TDP4/21/W167

Practice Note: What Is the “Exact” Date Property Is Placed in Service? The TCJA required 100% bonus depreciation for property placed in service after September 27, 2017. For assets placed in service prior to September 28, 2017, the bonus depreciation was 50%

Many tax practitioners are not aware of the “exact” date property is placed in service, and therefore elected under §168(k)(10) – a special rule to apply a 50% special depreciation allowance instead of the 100% allowance for all property placed in service with the year‐end including September 27, 2017

The election merely required a statement attached to a timely filed return (including extensions) indicating the taxpayer was electing to claim a 50% special depreciation allowance for all qualified property

Once made the election could not be revoked without IRS consent. Rev. Proc. 2020‐25 provides the required consent to revoke this election (If needed)……

© Surgent | TDP4/21/W168

I. Depreciation and MACRS Cost Recovery

Under the TCJA proposed and final regulations, certain eligible real property trades or businesses or farming businesses could elect to be an excepted trade or business, meaning they were not subject to the application of the §163(j) limitation An election by a real property trade or business or farming business to be an excepted trade or business was irrevocable and binding on the trade or business for all succeeding tax years Any real property trades or businesses or farming businesses claiming such election were required to depreciate the following assets using the alternative depreciation system (ADS), and were not eligible for a bonus depreciation deduction under §168(k) for: Nonresidential real property; Residential rental property; and Qualified improvement property

© Surgent | TDP4/21/W169

I. Depreciation and MACRS Cost Recovery

If a business made an irrevocable election to be an excepted trade or business prior to the CARES Act being signed into law, it would have been ineligible for the §163(j) relief provisions provided in the CARES Act

Rev. Proc. 2020‐22 addressed recent changes made to §163(j) by the CARES Act, allowing an electing real property trade or business or farming business to withdraw an election made under §163(j)(7) during the 2018 or 2019 tax years If a taxpayer withdraws a previous election made under §163(j)(7), the taxpayer will be treated as if the election were never made

© Surgent | TDP4/21/W170

I. Depreciation and MACRS Cost Recovery

To withdraw a §163(j)(7) election, a taxpayer was required to timely file an amended federal income tax return, or AAR, as applicable, for the taxable year in which the election was made, with an election withdrawal statement The election withdrawal statement should be titled, “Revenue Procedure 2020‐22 Section 163(j)(7) Election Withdrawal” The amended return must include the adjustment to taxable income for the withdrawn §163(j)(7) election and any other adjustments to taxable income or tax liability due to this change (like depreciation)

Except as provided in Rev. Proc. 2020‐23, the amended return was required to have been filed on or before October 15, 2021, but no later than the period of limitations on assessment for the taxable year for which the amended return is being filed

© Surgent | TDP4/21/W171

V. Additional First‐Year Depreciation – Other Guidance B. Elections out of additional first‐year depreciation 1. A taxpayer may elect, for any class of property, to not deduct any special AFYD depreciation allowance for all such in such class. To make an election, the taxpayer must attach a statement to a timely filed return (including extensions) indicating the class of property for which they are making the election and that, for such class they are not to claim any special depreciation allowance. The election must be made separately by each person owning qualified property (for example, by the partnership, by the S corporation, or by the common parent of a consolidated group).

Once made, the election cannot be revoked without IRS consent. See Rev. Proc. 2020‐25 for consent for certain years….noted earlier

© Surgent | TDP4/21/W172

VI. Property Excepted from Additional First‐Year Depreciation A. Qualified property for which §168(k) does not include:Listed property used 50% or less in a qualified business use;

Any property required to be depreciated under the ADS system (that is, not property for which you elected to use ADS);

Property placed in service/ disposed of in the same tax year;

Property converted from business use to personal use in the same tax year acquired. Property converted from personal use to business use in the same or later tax year may qualify

Property for which an election not to claim any special depreciation allowance is made (Elect out)

Any property used in certain trades or business that has had floor plan financing indebtedness

© Surgent | TDP4/21/W173

VI. Property Excepted from Additional First‐Year DepreciationOn September 21, 2020, the IRS and Department of Treasury released the second round of §168(k) bonus depreciation final regulations (T.D. 9916), addressing the CARES Act QIP fix The CARES Act stated that the improvement must be “made by the taxpayer”

The final regulations clarify that an improvement is made by a taxpayer if the taxpayer makes, manufactures, constructs, or produces the improvement for itself, or if the improvement is made, manufactured, constructed, or produced for the taxpayer by another person under a written contract

If a taxpayer acquired nonresidential property in a taxable transaction, and such property had an existing improvement placed in service by the seller, the existing improvement is not considered to have been made by the taxpayer

© Surgent | TDP4/21/W174

Practice Note - Fiscal year taxpayers: Unlike §179 provisions, the 50% AFYD is not based upon the tax year

the item is placed in service; rather it is based upon actual acquisition and placed in service dates

© Surgent | TDP4/21/W175

VII. Modified Accelerated Cost Recovery System (MACRS) ‐ General Rules

A. MACRS applies to property placed in service after December 31, 1986

B. When tangible property is placed in service under MACRS, a number of determinations must be made at the outset: 1. The depreciable basis of the asset 2. The applicable recovery period 3. The applicable depreciation method 4. The applicable convention

• Practice Note: Order for depreciation calculations

• MACRS rules for depreciation deductions have been present in the tax law since 1987. They are applied to depreciate assets AFTER the application of both §179 and §168(k), each previously discussed

© Surgent | TDP4/21/W176

© Surgent | TDP4/21/W177

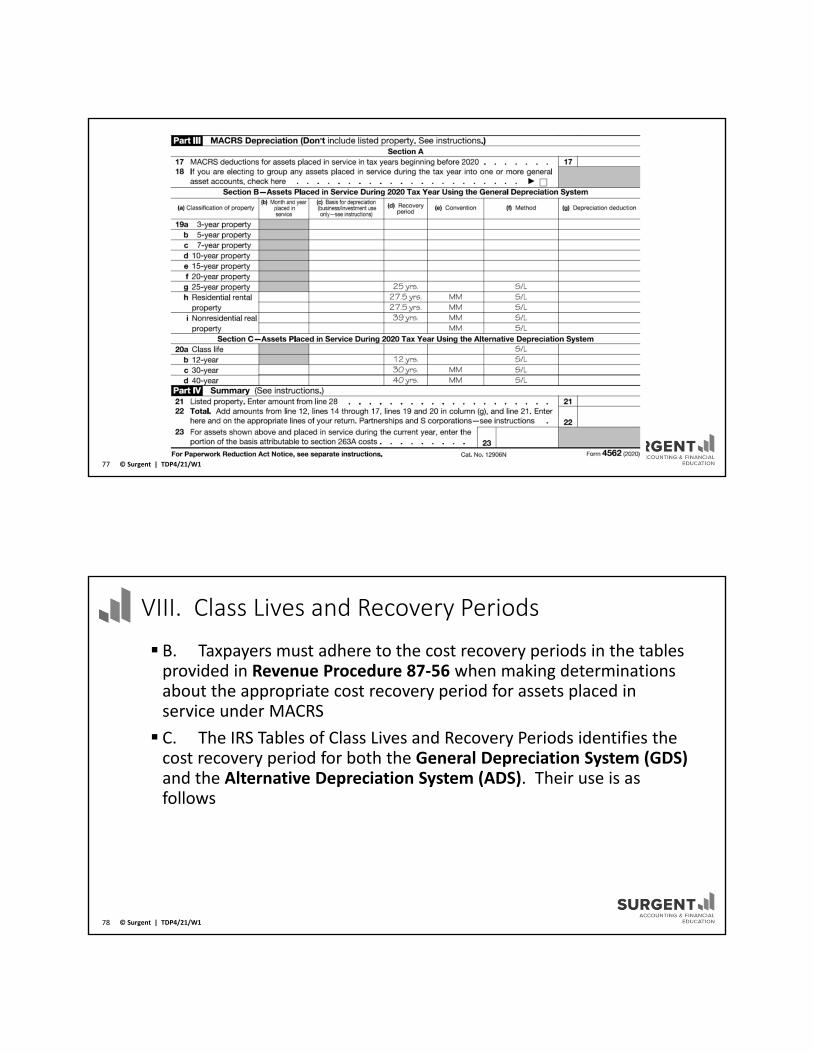

VIII. Class Lives and Recovery Periods

B. Taxpayers must adhere to the cost recovery periods in the tables provided in Revenue Procedure 87‐56 when making determinations about the appropriate cost recovery period for assets placed in service under MACRS

C. The IRS Tables of Class Lives and Recovery Periods identifies the cost recovery period for both the General Depreciation System (GDS) and the Alternative Depreciation System (ADS). Their use is as follows

© Surgent | TDP4/21/W178

B. Rev. Proc. 87‐56

The depreciation bible for MACRS: Find asset description in table Column 1 is ignored (ADR midpoint class life)

Column 2 is generally the recovery period (General Depreciation System)

Column 3 is AMT, ACE, and E&P life (Alternative Depreciation System)

Property not listed: 7‐year GDS, 12‐year ADS

Tables also provided in Appendix B of IRS Pub. 534, “Depreciation”

© Surgent | TDP4/21/W179

Modified Accelerated Cost Recovery System

Four depreciation options are available for MACRS deductions as follows: Option #1 – 200% declining balance over the MACRS recovery period

Option #2 – 150% D.B. method over the MACRS recovery period

Option #3 – Straight‐line method over the MACRS recovery period

Option #4 – Straight‐line over the ADS life

© Surgent | TDP4/21/W180

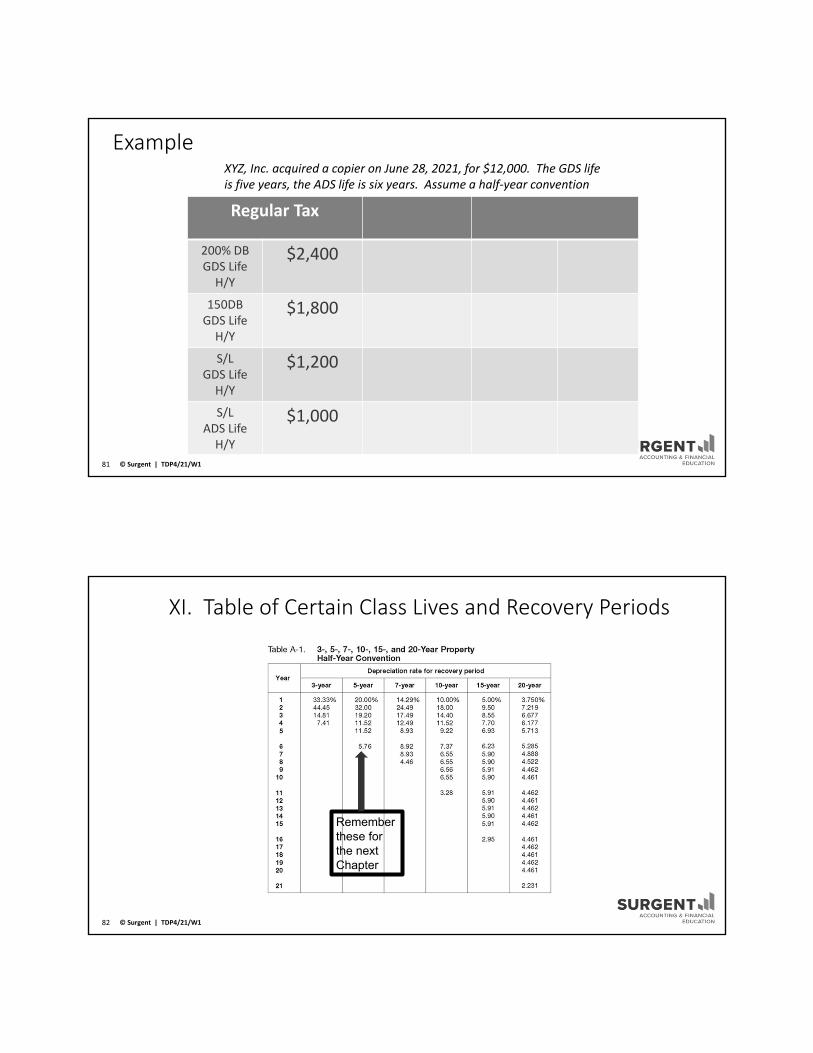

Example

Regular Tax

200% DB GDS LifeH/Y

$2,400

150DBGDS LifeH/Y

$1,800

S/L GDS LifeH/Y

$1,200

S/LADS LifeH/Y

$1,000

XYZ, Inc. acquired a copier on June 28, 2021, for $12,000. The GDS life is five years, the ADS life is six years. Assume a half‐year convention

© Surgent | TDP4/21/W181

XI. Table of Certain Class Lives and Recovery Periods

Rememberthese for the nextChapter

© Surgent | TDP4/21/W182

XI. Table of Certain Class Lives and Recovery Periods Example: After application of §179 and/or §168(k), taxpayer Forty‐Five Sixty‐Two Inc has $100,000 in current year acquisitions to be depreciated under MACRS. In choosing the 200DB method with half‐year convention, the above chart would result in the following depreciation deductions: Year 1 $100,000 x 20% = $20,000 Year 2 $100,000 x 32% = $32,000 Year 3 $100,000 x 19.2% = $19,200 Year 4 $100,000 x 11.52% = $11,520 Year 5 $100,000 x 11.52% = $11,520 Year 6 $100,000 x 5.76% $ 5,760 Total $100,000 The switch to straight line is therefore built into the above table

© Surgent | TDP4/21/W183

XII. Summary and Examples of MACRS Recovery Periods A. The six recovery periods for tangible personal property, the two recovery periods for tangible real property, and the general depreciation method and convention are as follows:‐ 3‐year property ‐ 5‐year property ‐ 7‐year property

‐ 10‐year property ‐ 15‐year property ‐ 20‐year property

‐ 27.5‐year property ‐ 39‐year property

• Practice note: TCJA Change for certain farm property

• In regard to item 8), TCJA shortens the recovery period for machinery and equipment used in a farming business from seven to five years. This shorter recovery period, however, doesn’t apply to grain bins, cotton ginning assets, fences or other land improvements

© Surgent | TDP4/21/W184

XII. Summary and Examples of MACRS Recovery Periods Buildings generally include

The term “building” generally means any structure or edifice enclosing a space within its walls, and usually covered by a roof, the purpose of which is, for example, to provide shelter or housing, or to provide working, office, parking, display, or sales space

The term includes, for example, structures such as apartment houses, factory and office buildings, warehouses, barns, garages, railway or bus stations, and stores

Treas. Regs §1.48‐1(e)(1)

© Surgent | TDP4/21/W185

XII. Summary and Examples of MACRS Recovery Periods Structural Components generally include

The term “structural components” includes such parts of a building as walls, partitions, floors, and ceilings, as well as any permanent coverings therefor such as paneling or tiling, windows and doors;

All components (whether in, on, or adjacent to the building) of a central air conditioning or heating system, including motors, compressors, pipes and ducts;

Plumbing and plumbing fixtures, such as sinks and bathtubs;

Electric wiring and lighting fixtures;

© Surgent | TDP4/21/W186

XII. Summary and Examples of MACRS Recovery Periods Structural Components generally include

Chimneys;

Stairs, escalators, and elevators, including all components thereof;

Sprinkler systems;

Fire escapes;

Other components relating to the operation or maintenance of a building

Treas. Regs §1.48‐1(e)(2)

© Surgent | TDP4/21/W187

XII. Summary and Examples of MACRS Recovery Periods B. Recovery periods for common property utilized in real estate are included in Publication 527, and specifically Table 2‐1 reproduced below

© Surgent | TDP4/21/W188

XIV. Cost Segregation Studies Yield Front Loaded Deductions A. In general, nonresidential real property must be depreciated on a straight‐line basis over 39 years while tangible personal property (§1245) is eligible for accelerated depreciation methods and much shorter lives (5‐7 years) D. The following list (not all inclusive) details some of the assets classified as having shorter recovery periods (generally five or seven years) by IRS Field Directives Signs Drapes, curtains Movable walls, strippable wall paper, and vinyl Canopies and awnings Certain doors Electrical outlets or plumbing specifically associated with particular items of machinery and equipment Etc …

© Surgent | TDP4/21/W189

XIV. Cost Segregation Studies Yield Front Loaded Deductions E. Disputes may arise with IRS over the underlying classification of property. The IRS has issued field directives and other public information regarding certain aspects of cost segregation issues. Practitioners must utilize and monitor all avenues for guidance

1. For example, in a Coordinated Issue Release – The Applicable Recovery Period under I.R.S. §168(a) for Open‐Air Parking Structures, IRS surgically rebutted the argument that such structures are land improvements subject to a 15‐year recovery period The release held that open‐air parking structures are buildings as defined in Treas. Reg. §1.48‐1(e). For depreciation purposes these parking structures are therefore nonresidential real property with a cost recovery period generally of 39 years

© Surgent | TDP4/21/W190

XV. Leasehold Improvements ‐ General Rules I.R.C. §168(i)

A. Generally, leasehold improvements placed in service after December 31, 1986 must be depreciated straight‐line over the assigned life of the real estate improved (i.e., 39 years for non‐residential improvements on or after May 13, 1993)

• Practice Note: Phraseology

• Practitioners must be careful of the phraseology, as leasehold improvements and “qualified improvement property” are afforded differing rules

• Qualified improvement property is eligible for the AFYD under §168(k) discussed above. Leasehold improvements that do not meet the “qualified” status are subject to the MACRS rules

© Surgent | TDP4/21/W191

XVI. Property Qualifying as “15‐Year Property”

Any municipal wastewater treatment plant

Certain improvements made directly to land or added to it (shrubbery, fences, roads, sidewalks)

Any telephone distribution plant and comparable equipment used for 2‐way exchange of voice and data communications

Any §1250 property which is a retail motor fuels outlet (whether or not food or other convenience items are sold at the outlet)

Qualified leasehold improvements – pre‐2018

Qualified restaurant property – pre‐2018 Qualified retail property – pre‐2018Qualified improvement property – post‐2017 (CARES)

© Surgent | TDP4/21/W192

XXIII. Special Rule for Farmers

A. New for years beginning after 2017 the 150% declining balance method is no longer required for 3‐, 5‐, 7‐, or 10‐year property used in a farming business However, the 150% declining balance method will continue to apply to any 15‐ or 20‐year property used in a farming business to which the straight‐line method does not apply or to property for which an election the use of the 150% declining balance method is made

Farming businesses that elect out of the interest deduction limit must use the alternative depreciation system to depreciate any property with a recovery period of 10 years or more, This provision applies to taxable years beginning after Dec. 31, 2017

B. Prior to 2018, must use MACRS 150 percent declining balance method or the straight‐line method

© Surgent | TDP4/21/W193

© Surgent | TDP4/21/W194

XXV. Accounting Conventions for Tangible Property

Mid‐month convention: One‐half month at acquisition or disposal

Half‐year convention: One‐half year at acquisition or disposal

Mid‐quarter convention: Required where 40% of acquisitions are made in final quarter

Use is not elective Must also be used for AMT

Before §168(k) deduction

No depreciation on acquisition and disposal in same year

© Surgent | TDP4/21/W195

XXVII. Alternate Depreciation System

Must be used for:1. All property used predominantly in a farming business and placed in service

in any tax year during which an election not to apply the uniform capitalization rules to certain farming costs

2. A real property trade or business electing out of the interest deduction 3. Listed property used 50% or less in a qualified business use4. Any tax‐exempt use property including:5. Any tax‐exempt bond‐financed property6. Any property imported from a foreign country for which an Executive Order

is in effect because the country maintains trade restrictions or engages in other discriminatory acts

7. Any tangible property used predominantly outside the U.S. during the year8. Earning and profits computations

© Surgent | TDP4/21/W196

XXVII. Depreciation in the Year of Disposal

A. For acquisitions of tangible property January 1, 1987 and subsequent, depreciation is permitted in the year of disposal 1. For tangible personal property acquired January 1, 1981 to December 31, 1986 (ACRS), no depreciation is permitted in the year of disposal

B. For depreciable property acquired January 1, 1987 and subsequent (MACRS), the same convention (i.e., half‐year, mid‐quarter, mid‐month for MACRS real property) must be used in the year of disposal that was used in the year of acquisition

© Surgent | TDP4/21/W197

XXVIII. Calculating MACRS Depreciation in Short Tax Years Rev. Proc. 89‐15

Effective after 12/31/86

Mid‐month applies without regard to length of year (example)

Half‐year is midpoint of short year

Mid‐quarter applies: If year is three months or less

Midpoint is number of days/2

© Surgent | TDP4/21/W198

Listed Property, Luxury Auto Limits, and Taxable Employee Compensation

Chapter 4

© Surgent | TDP4/21/W199

Review Exercise:The details are included within this chapter, with further discussion at the end of the chapter.

You are considering the purchase of a new vehicle and have narrowed your choice to either a 2021 Land Rover Range‐Rover ($100,000 –GVWR 7,055 lbs.) or the 2021 Audi S7 Sedan ($100,000 – GVWR 5,000 lbs)

As a budget‐minded professional, you wonder just how much the depreciation expense will vary in the first 4 years of ownership of each vehicle Of course, it’s 100% business use!

© Surgent | TDP4/21/W1100

I. Listed Property

Any passenger automobile

Any other property used as a “means of transportation”

Property used for purposes of entertainment, recreation or amusement

Computer or peripheral equipment except if used in business location TJCA Removes

© Surgent | TDP4/21/W1101

Listed PropertyB. “Means Of Transportation” … includes trucks, buses, trains, boats, airplanes, motorcycles, and any other vehicles for transporting

persons or goods

“qualified nonpersonal use vehicle” to include the following:

Clearly marked police, fire vehicles and public safety officer vehicles,

Ambulances used as such or hearses used as such,

Any vehicle designed to carry cargo with a loaded gross vehicle weight over 14,000 pounds,

Bucket trucks (“cherry pickers”),

Cement mixers,

Combines,

Cranes and derricks

Any passenger automobile:

GVR <= 6,000 lbs

4‐wheeled vehicle

© Surgent | TDP4/21/W1102

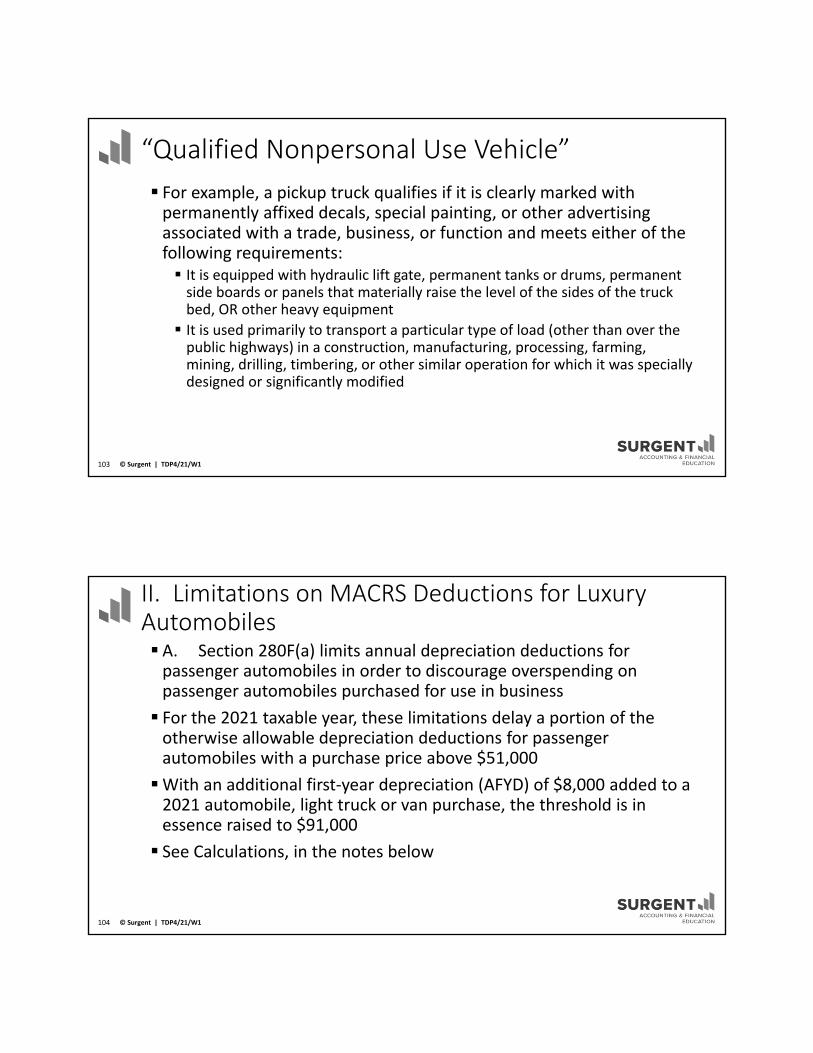

“Qualified Nonpersonal Use Vehicle”

For example, a pickup truck qualifies if it is clearly marked with permanently affixed decals, special painting, or other advertising associated with a trade, business, or function and meets either of the following requirements: It is equipped with hydraulic lift gate, permanent tanks or drums, permanent side boards or panels that materially raise the level of the sides of the truck bed, OR other heavy equipment

It is used primarily to transport a particular type of load (other than over the public highways) in a construction, manufacturing, processing, farming, mining, drilling, timbering, or other similar operation for which it was specially designed or significantly modified

© Surgent | TDP4/21/W1103

II. Limitations on MACRS Deductions for Luxury Automobiles A. Section 280F(a) limits annual depreciation deductions for passenger automobiles in order to discourage overspending on passenger automobiles purchased for use in business

For the 2021 taxable year, these limitations delay a portion of the otherwise allowable depreciation deductions for passenger automobiles with a purchase price above $51,000

With an additional first‐year depreciation (AFYD) of $8,000 added to a 2021 automobile, light truck or van purchase, the threshold is in essence raised to $91,000

See Calculations, in the notes below

© Surgent | TDP4/21/W1104

C. Additional Recordkeeping Requirements

1. The law requires taxpayers to keep “adequate records” to substantiate:a. Travel and meal expenses,

b. Entertainment expenses,

c. Expense for gifts of a business nature, and

d. Deductions and credits claimed for the “listed property” above

Logs are NOT required (but recommended)

© Surgent | TDP4/21/W1105

C. Additional Recordkeeping Requirements

2. For listed property, no deduction is allowed unless the taxpayer adequately substantiates the expense and business usage of the property. The level of substantiation for business or investment use of listed property varies depending on the facts and circumstances. In general, the substantiation must contain sufficient information as to each element of every business or investment use, including: a. The amount (e.g., cost) of each separate expenditure and the amount of business or investment use, based on the appropriate measure (e.g., mileage for automobiles), and the total use of the property for the taxable period,

b . The date of the expenditure or use, and

c. The business purposes for the expenditure or use

© Surgent | TDP4/21/W1106

Luxury Auto Limits for 2021

The law does not define which autos are luxury autos; it merely places a limitation on the depreciation that can be deducted on any auto

1. The maximum depreciation expense allowed on a passenger vehicle placed in service in 2021 is:

2021

With AFYD

2021

No AFYD2022 2023

2024 &

Later

Autos $18,100 $10,100 $16,100 $9,700 $5,760

© Surgent | TDP4/21/W1107

Luxury Auto Limits for 2020

The law does not define which autos are luxury autos; it merely places a limitation on the depreciation that can be deducted on any auto

2. The maximum depreciation expense allowed on a passenger vehicle placed in service in 2020 is:

2020

With AFYD

2020

No AFYD2021 2022

2023 &

Later

Autos $18,100 $10,100 $16,100 $9,700 $5,760

© Surgent | TDP4/21/W1108

Luxury Auto Limits for 2019

D. The law does not define which autos are luxury autos; it merely places a limitation on the depreciation that can be deducted on any auto

3. The maximum depreciation expense allowed on a passenger vehicle placed in service in 2019 is:

2019

With AFYD

2019

No AFYD2020 2021

2022 &

Later

Autos $18,100 $10,100 $16,100 $9,700 $5,760

© Surgent | TDP4/21/W1109

Luxury Auto Limits for 2018 D. The law does not define which autos are luxury autos; it merely places a limitation on the depreciation that can be deducted on any auto

1. The maximum depreciation expense allowed on a passenger vehicle placed in service in 2018 is:

2018

With AFYD

2018

No AFYD2019 2020

2021 &

Later

Autos $18,000 $10,000 $16,000 $9,600 $5,760

• See III below for: TCJA Technical Issue ‐‐ How much depreciation in the following years?

• Due to the interaction of §168(k) 100 percent AFYD (bonus) and the luxury automobile limitations of §280F, a technicality arises in the second year of service for luxury automobiles

• Also see IV below for: TCJA Technical Issue ‐‐ Surgent (correctly) anticipates technical guidance, which discusses relief from the TCJA technicality noted above

© Surgent | TDP4/21/W1110

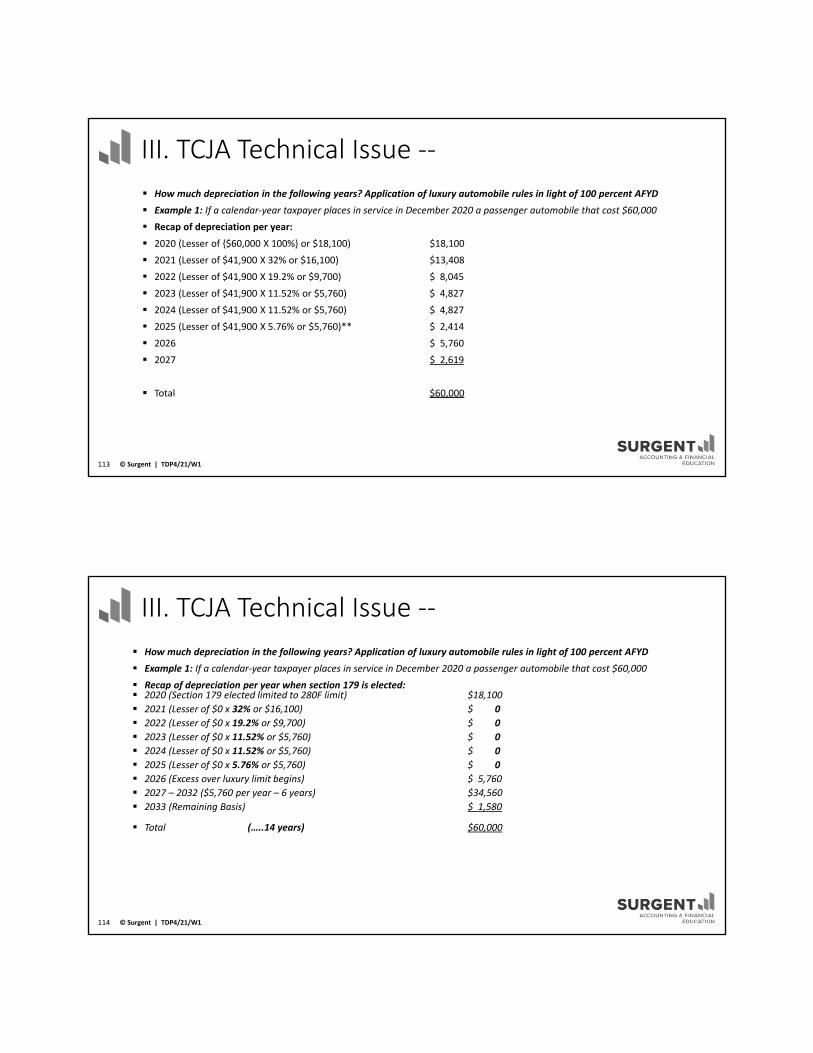

III. TCJA Technical Issue ‐‐

How much depreciation in the following years? Application of luxury automobile rules in light of 100 percent AFYD

A. Due to the interaction of §168(k) 100 percent AFYD (bonus) and the luxury automobile limitations of §280F, a technicality arises in the second year of service for luxury automobiles

1. If the unadjusted depreciable basis of a passenger automobile eligible for the 100 percent AFYD (bonus) deduction exceeds the first‐year limitation amount, the excess amount of unrecovered basis of the passenger automobile is treated as a deductible expense in the first taxable year succeeding the end of the recovery period

© Surgent | TDP4/21/W1111

IV. TCJA Technical Issue ‐‐ Surgent (Correctly) Anticipates Technical Guidance Practice Note: IRS provides a Meaningful Gesture There is no doubt that luxury automobile limits of §280F limit depreciation deductions. However, the doubt occurs when calculating depreciation in the 2nd and subsequent years of service

After release of TCJA Surgent anticipated a technical correction or additional guidance regarding precisely how the luxury automobile limits of §280F will interact with the 100 percent AFYD, to specifically answer the question, “How much depreciation in the following years?”

The issue was addressed in Rev. Proc. 2019‐13, issued February 13, 2019 – it added a safe harbor method of accounting

The guidance is a meaningful gesture; however, it does point out a serious issue if the taxpayer has claimed §179 or elected out of bonus – AFYD. In such cases, the safe harbor described does not apply! (See example with depreciation expense of $0 for years 2019 through 2023 – ouch)

© Surgent | TDP4/21/W1112

III. TCJA Technical Issue ‐‐

How much depreciation in the following years? Application of luxury automobile rules in light of 100 percent AFYD

Example 1: If a calendar‐year taxpayer places in service in December 2020 a passenger automobile that cost $60,000

Recap of depreciation per year:

2020 (Lesser of {$60,000 X 100%} or $18,100) $18,100

2021 (Lesser of $41,900 X 32% or $16,100) $13,408

2022 (Lesser of $41,900 X 19.2% or $9,700) $ 8,045

2023 (Lesser of $41,900 X 11.52% or $5,760) $ 4,827

2024 (Lesser of $41,900 X 11.52% or $5,760) $ 4,827

2025 (Lesser of $41,900 X 5.76% or $5,760)** $ 2,414

2026 $ 5,760

2027 $ 2,619

Total $60,000

© Surgent | TDP4/21/W1113

III. TCJA Technical Issue ‐‐

How much depreciation in the following years? Application of luxury automobile rules in light of 100 percent AFYD

Example 1: If a calendar‐year taxpayer places in service in December 2020 a passenger automobile that cost $60,000

Recap of depreciation per year when section 179 is elected: 2020 (Section 179 elected limited to 280F limit) $18,100

2021 (Lesser of $0 x 32% or $16,100) $ 0

2022 (Lesser of $0 x 19.2% or $9,700) $ 0

2023 (Lesser of $0 x 11.52% or $5,760) $ 0

2024 (Lesser of $0 x 11.52% or $5,760) $ 0

2025 (Lesser of $0 x 5.76% or $5,760) $ 0

2026 (Excess over luxury limit begins) $ 5,760

2027 – 2032 ($5,760 per year – 6 years) $34,560

2033 (Remaining Basis) $ 1,580

Total (…..14 years) $60,000

© Surgent | TDP4/21/W1114

IV. TCJA Technical Issue ‐‐ Surgent (Correctly) Anticipates Technical GuidanceD. Serious issue if §179 is elected and election out of §168(k) has been made

Safe Harbor Example 2: Non‐Application of Rev. Proc. 2019‐13 safe harbor method of accounting when §179 deduction claimed

Total of 14 years to fully depreciate

Therefore, for 2020, Expectation deducts $18,100 for the passenger automobile under §179 and deducts the excess amount of $41,900 beginning in 2026, subject to the annual limitation of $5,760 under §280F

© Surgent | TDP4/21/W1115

IV. TCJA Technical Issue ‐‐ Surgent (Correctly) Anticipates Technical GuidanceD. Serious issue if §179 is elected and election out of §168(k) has been made

Safe Harbor Example 3: Application of Rev. Proc. 2019‐13 safe harbor method of accounting when the taxpayer elects out of §168 Bonus depreciation

For 2020 and subsequent taxable years, Expectation determines the depreciation deductions for the passenger automobile in accordance with the general depreciation system of §168(a), subject to the §280F(a) limitations

© Surgent | TDP4/21/W1116

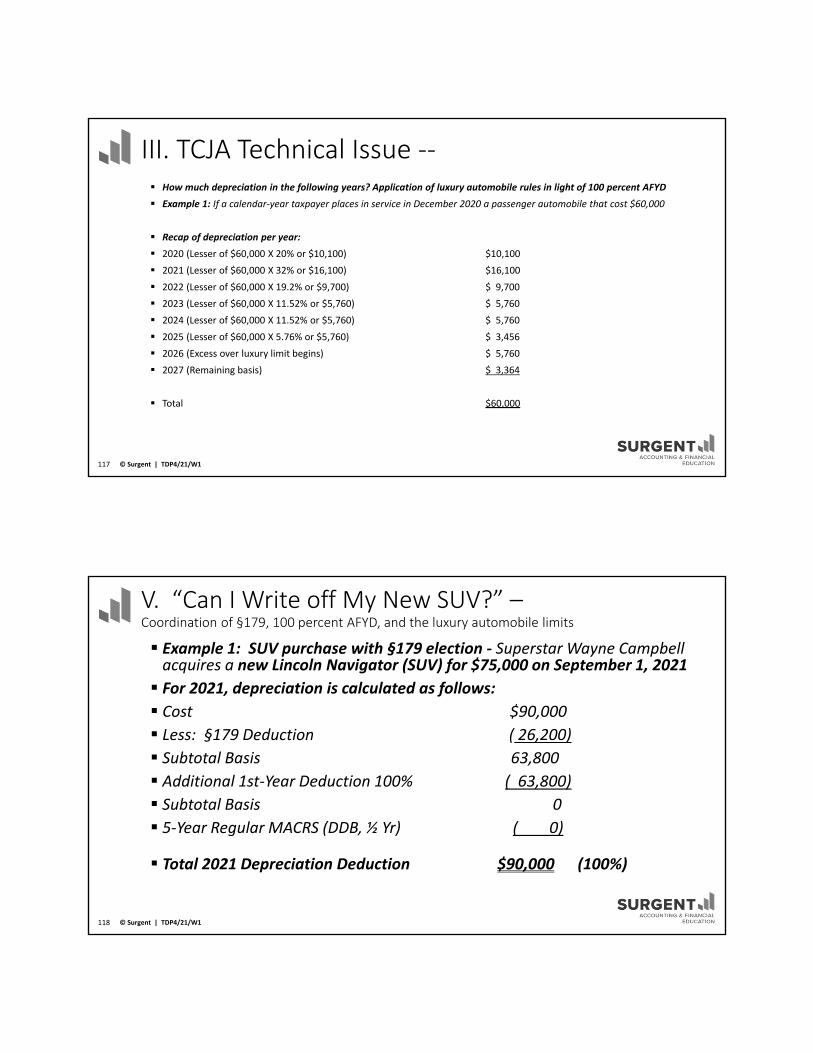

III. TCJA Technical Issue ‐‐ How much depreciation in the following years? Application of luxury automobile rules in light of 100 percent AFYD

Example 1: If a calendar‐year taxpayer places in service in December 2020 a passenger automobile that cost $60,000

Recap of depreciation per year:

2020 (Lesser of $60,000 X 20% or $10,100) $10,100

2021 (Lesser of $60,000 X 32% or $16,100) $16,100

2022 (Lesser of $60,000 X 19.2% or $9,700) $ 9,700

2023 (Lesser of $60,000 X 11.52% or $5,760) $ 5,760

2024 (Lesser of $60,000 X 11.52% or $5,760) $ 5,760

2025 (Lesser of $60,000 X 5.76% or $5,760) $ 3,456

2026 (Excess over luxury limit begins) $ 5,760

2027 (Remaining basis) $ 3,364

Total $60,000

© Surgent | TDP4/21/W1117

V. “Can I Write off My New SUV?” –Coordination of §179, 100 percent AFYD, and the luxury automobile limits

Example 1: SUV purchase with §179 election ‐ Superstar Wayne Campbell acquires a new Lincoln Navigator (SUV) for $75,000 on September 1, 2021

For 2021, depreciation is calculated as follows:

Cost $90,000

Less: §179 Deduction ( 26,200)

Subtotal Basis 63,800

Additional 1st‐Year Deduction 100% ( 63,800)

Subtotal Basis 0

5‐Year Regular MACRS (DDB, ½ Yr) ( 0)

Total 2021 Depreciation Deduction $90,000 (100%)

© Surgent | TDP4/21/W1118

V. “Can I Write off My New SUV?” –Coordination of §179, 100 percent AFYD, and the luxury automobile limits

Example 2: assume example 1 purchase in 2021 without the election to apply §179 For 2021, depreciation is calculated as follows: Cost $90,000 Less: §179 Deduction ( 0) Subtotal Basis 90,000 Additional 1st‐Year Deduction 100% ( 90,000) Subtotal Basis 0 5‐Year Regular MACRS (DDB, ½ Yr) ( 0)

Total 2021 Depreciation Deduction $90,000 (100%)

© Surgent | TDP4/21/W1119

V. “Can I Write off My New SUV?” –Coordination of §179, 100 percent AFYD, and the luxury automobile limits

Example 3: assume example 2 purchase in 2021 was a used vehicle

For 2021, depreciation is calculated as follows:

Cost $90,000

Less: §179 Deduction ( 0)

Subtotal Basis 90,000

Additional 1st‐Year Deduction 100% (90,000)

Subtotal Basis 0

5‐Year Regular MACRS (DDB, ½ Yr) ( 0)

Total 2021 Depreciation Deduction $90,000 (100%)

© Surgent | TDP4/21/W1120

VI. Limitations on Leased Luxury Automobiles

Income inclusion for leased autos with FMV over luxury amount

Business‐use portion only

1. From the following table, select the dollar amount from the appropriate column for the taxable year in which the auto is used under the lease,

a. If a leased auto is transferred from business use to personal use, the dollar amount for the preceding year

b. If a leased auto is transferred from personal use to business use, use the auto’s fair market value on the date of conversion

© Surgent | TDP4/21/W1121

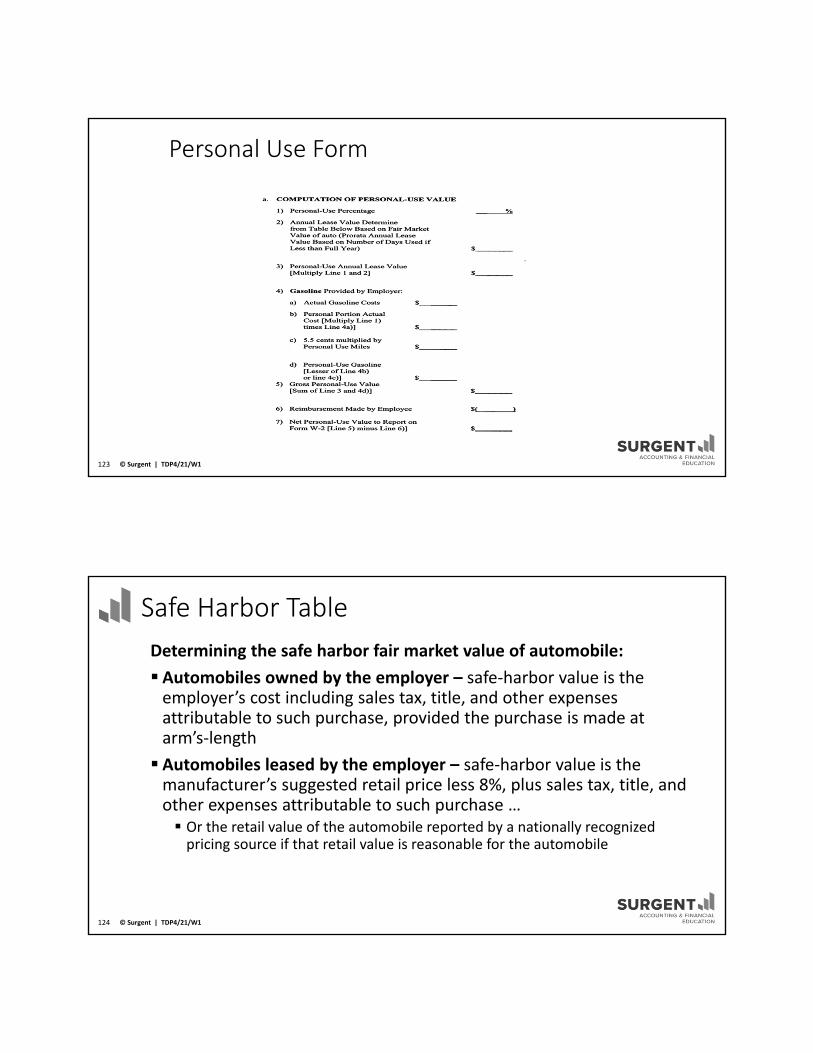

VII. Valuation of Personal Use of Automobile

Include personal use on W‐2 and receive 100% depreciation deduction

Four methods: Facts and circumstances (Actual)

Safe Harbor (Table) Commuting value ($3.00/day)

Cents per mile (56 cents/mile – 2021)

© Surgent | TDP4/21/W1122

Personal Use Form

© Surgent | TDP4/21/W1123

Safe Harbor Table

Determining the safe harbor fair market value of automobile:

Automobiles owned by the employer – safe‐harbor value is the employer’s cost including sales tax, title, and other expenses attributable to such purchase, provided the purchase is made at arm’s‐length

Automobiles leased by the employer – safe‐harbor value is the manufacturer’s suggested retail price less 8%, plus sales tax, title, and other expenses attributable to such purchase … Or the retail value of the automobile reported by a nationally recognized pricing source if that retail value is reasonable for the automobile

© Surgent | TDP4/21/W1124

E. Method #3 ‐ Special Commuting Value

b. For bona fide noncompensatory business reasons, the employerrequires the employee to commute to and/or from work in the vehicle

c. The employer has established a written policy under which neither the employee, nor any individual whose use would be taxable to the employee, may use the vehicle for personal purposes, other than for commuting or de minimis personal use (such as a stop for a personal errand on the way between a business delivery and the employee’s home)

© Surgent | TDP4/21/W1125

F. Method #4 ‐ Special Valuation Cents‐Per‐Mile Method The standard mileage rate is 56 cents per mile for each business mile of use for the year 2021

16 cents for medical or moving purposes

14 cents for charitable purposes

© Surgent | TDP4/21/W1126

Review Exercise:“What’s it going to take to put this car in your garage today?”

……to two opulent and extravagant choices ‐ a new Land Rover Range‐Rover or the Audi S7 Sedan, each $100K

Land Rover Range‐Rover ‐ $100,000 Audi S7 Sedan ‐ $100,000

SUV qualifies for §179, AFYD, MACRS (200DB,H/Y)

depreciation, assumed 100% business use

Passenger vehicle qualifies for 280F limitations,

assumed 100% business use

Year 1 – §179 $26,200 Rev. Proc.

2019-13

Capped by

§280F overall

Year 1 limitYear 1 – AFYD $73,800 $100,000

Year 1 – MACRS 20% = $0 $0 $81,900 Excess $18,100

Year 2 – MACRS 32% = $0 $0 32% = $26,208 §280F limit $16,100

Year 3 – MACRS 19.2% = $0 $0 19.2% = $15,725 §280F limit $9,700

Year 4 ‐ MACRS 11.52% = $0 $0 11.52% = $9,435 §280F limit $5,760

Totals $100,000 $49,660

© Surgent | TDP4/21/W1127

Review Exercise:“It’s not just leather, it’s Corinthian Leather.”

Suppose you lower your sights to less copious but plentiful choices of a new 2020 Range‐Rover Sport or the 2020 Infiniti Q70, each $65,000. (Purchased prior to 1/1/2020)

Range‐Rover Sport ‐ $65,000 Infiniti Q70 ‐ $65,000

SUV qualifies for §179, AFYD, MACRS (200DB, H/Y)

depreciation, assumed 100% business use

Passenger vehicle qualifies for 280F limitations,

assumed 100% business use

Year 1 – §179 $26,200 Rev. Proc.

2019-13

Capped by

§280F

overall Year

1 limit

Year 1 – AFYD $38,800 $65,000

Year 1 – MACRS 20% = $0 $0 $46,900 Excess $18,100

Year 2 – MACRS 32% = $0 $0 32% = $15,008 §280F limit $15,008

Year 3 – MACRS 19.2% = $0 $0 19.2% = $9,005 §280F limit $9,005

Year 4 ‐ MACRS 11.52% = $0 $0 11.52% = $5,403 §280F limit $5,406

Totals $65,000 $47,516

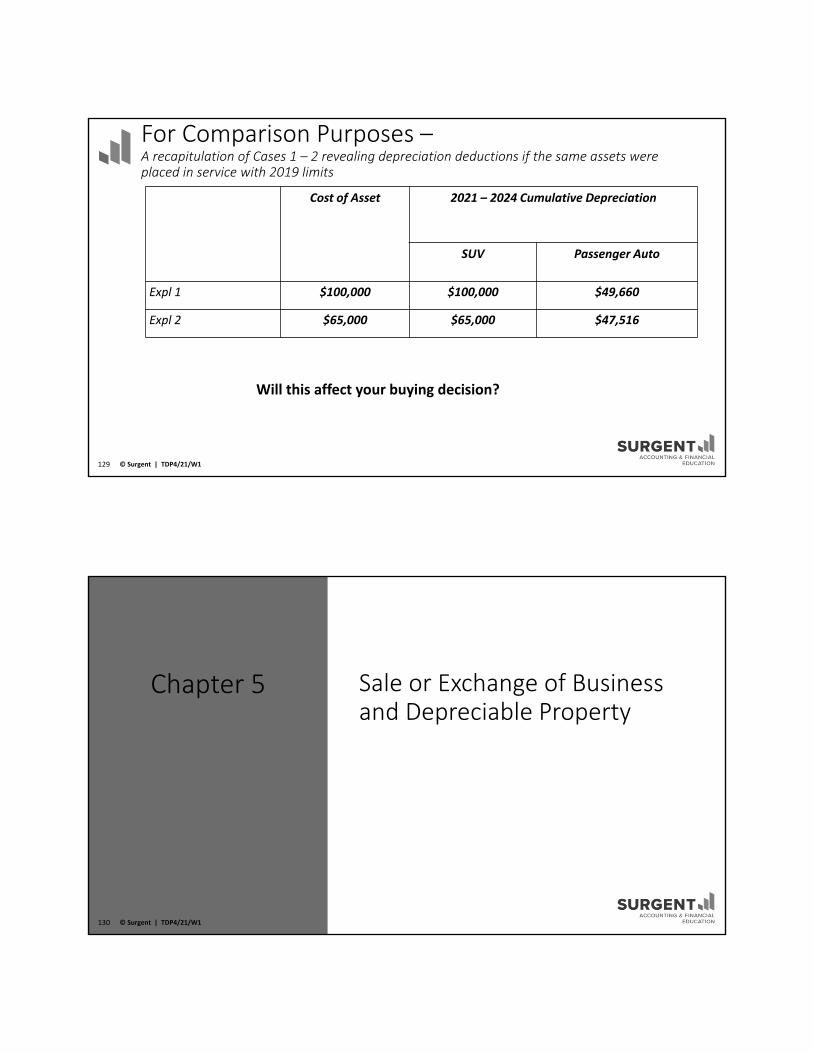

© Surgent | TDP4/21/W1128

For Comparison Purposes –A recapitulation of Cases 1 – 2 revealing depreciation deductions if the same assets were placed in service with 2019 limits

Cost of Asset 2021 – 2024 Cumulative Depreciation

SUV Passenger Auto

Expl 1 $100,000 $100,000 $49,660

Expl 2 $65,000 $65,000 $47,516

Will this affect your buying decision?

© Surgent | TDP4/21/W1129

Sale or Exchange of Business and Depreciable Property

Chapter 5

© Surgent | TDP4/21/W1130

Review Exercise:The details are included within this chapter, with further discussion at the end of the chapter.

You have been assigned to prepare the tax return for Negan Inc. Upon review of the tax trial balance you note the following line item: Gain from Asset Sale $51,000

You delve into the work papers and discover Negan sold one piece of equipment during the year The equipment was sold for $105,000, while its adjusted basis was $54,000 (originally purchased for $90,000, depreciation deducted amounted to $36,000)

On which Section of Form 4797 do you report this gain? Part I or Part II?

© Surgent | TDP4/21/W1131

© Surgent | TDP4/21/W1132

§1231 Family

§1231

§1245 §1250 §1252 §1254 §1255

Capital Gain (Loss)

Ordinary Gain (Loss)

© Surgent | TDP4/21/W1133

§1231 Gains and Losses

§1231 property: Property used in a trade or business held for the required period of time

Includes: Real property and depreciable personal property held > 1 year Timber, domestic iron ore, and coal > 1 year

Livestock for draft, breeding, or sporting Cattle and horses > 2 years

Other > 1 year

Capitalized unharvested crops

© Surgent | TDP4/21/W1134

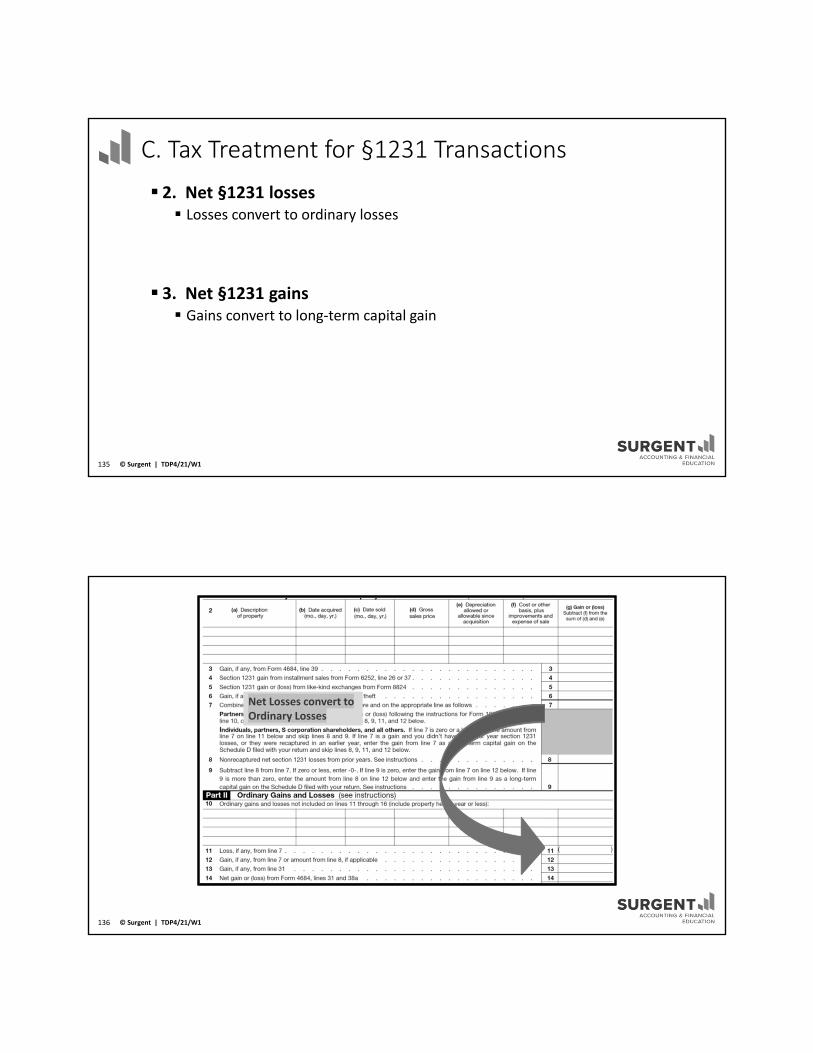

C. Tax Treatment for §1231 Transactions

2. Net §1231 losses Losses convert to ordinary losses

3. Net §1231 gains Gains convert to long‐term capital gain

© Surgent | TDP4/21/W1135

Net Losses convert toOrdinary Losses

© Surgent | TDP4/21/W1136

Net Gains convert toCapital Gains

© Surgent | TDP4/21/W1137

C. Tax Treatment for §1231 Transactions

4. Five‐year lookback rule

a. If §1231 gains exceed §1231 losses, the gain will be recaptured as ordinary income to the extent of the aggregate unrecaptured net §1231 losses for the 5 most recent taxable years

b. Any remaining gain after the ordinary income recapture is §1231 gain

© Surgent | TDP4/21/W1138

C. Tax Treatment for §1231 Transactions

Practice Note: Not Applicable to Partnerships and S Corporations

The “five‐year” look back rule is applied on C Corporation and Individual returns

However, a Partnership or S Corporation does NOT apply the rule. Partnerships and S Corporations summarize sale of business asset information and separately state it prior to the application of the look back rule (Form 4797, line 8) The rule is then applied at the individual partner, member or shareholder level

The look back rule is included in this discussion as it is an integral part of reporting sales and dispositions of business assets for all entities and must be considered

© Surgent | TDP4/21/W1139

Does NOT apply to Partnerships and S Corporations

5 Year Look Back Rule Converts current year §1231 gain to Ordinary

© Surgent | TDP4/21/W1140

II. Section 1245 Ordinary Income Recapture (Gain on Sale of Depreciable Personal Property) Depreciation is recaptured as ordinary income to the extent of the lesser of: Depreciation allowed or allowable Gain

Includes: Depreciable personal property Elevators and escalators Etc.

§179 Amounts are included

© Surgent | TDP4/21/W1141

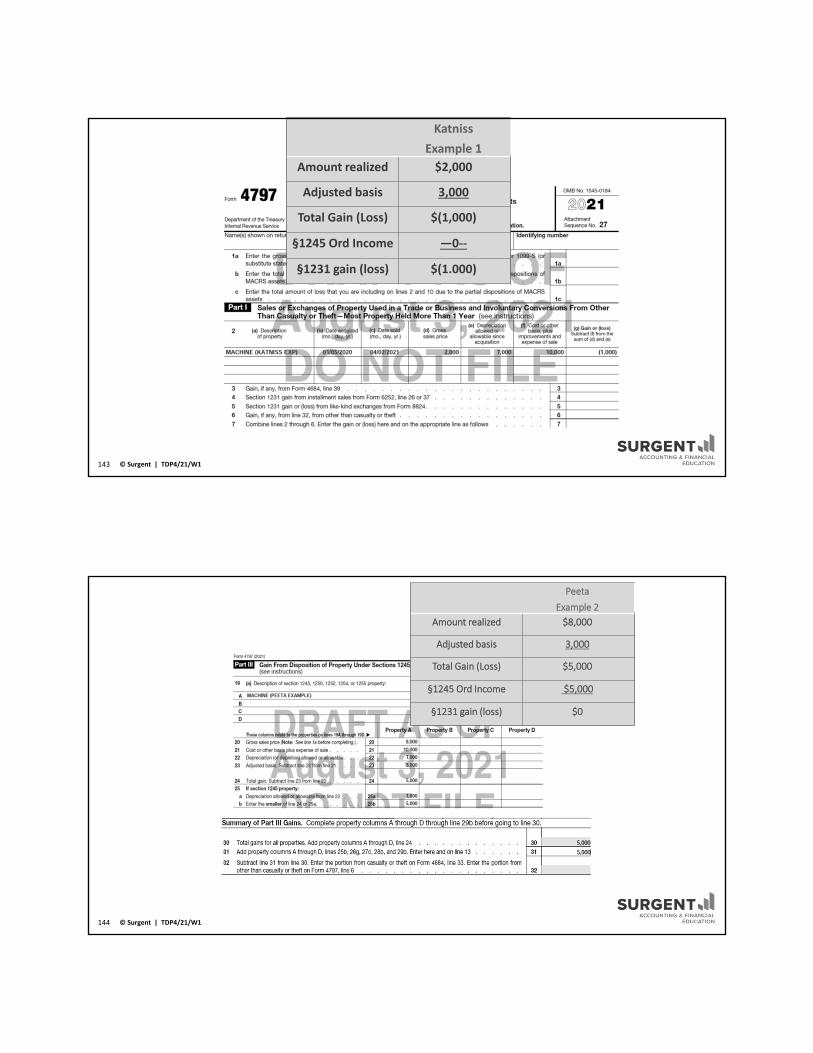

C. Tax Treatment for §1245 (Sale of Depreciable Personal Property at a Gain) Katniss

Example 1

Peeta

Example 2

Haymitch

Example 3

Amount realized $2,000 $8,000 $12,000

Original Cost 10,000 10,000 10,000

Accumulated

Depreciation

7,000 7,000 7,000

Adjusted basis 3,000 3,000 3,000

Total Gain (Loss) $(1,000) 5,000 9,000

§1245 Ord Income 0 $5,000 $7,000

§1231 gain (loss) $(1,000) $0 $2,000

© Surgent | TDP4/21/W1142

Katniss

Example 1

Amount realized $2,000

Adjusted basis 3,000

Total Gain (Loss) $(1,000)

§1245 Ord Income —0‐‐

§1231 gain (loss) $(1.000)

© Surgent | TDP4/21/W1143

Peeta

Example 2

Amount realized $8,000

Adjusted basis 3,000

Total Gain (Loss) $5,000

§1245 Ord Income $5,000

§1231 gain (loss) $0

© Surgent | TDP4/21/W1144

Peeta

Example 2

Amount realized $8,000

Adjusted basis 3,000

Total Gain (Loss) $5,000

§1245 Ord Income $5,000

§1231 gain (loss) $0

© Surgent | TDP4/21/W1145

Haymitch LLC Sold a Business Machine for $12,000

Haymitch LLC sold a business machine for $12,000

2,000

7,000© Surgent | TDP4/21/W1146

Practice Note: Tax enlightenment ‐‐ Favorable tax provision for all businesses Section 1231 must be followed correctly to afford a taxpayer capital gain treatment for gains in excess of recapture and ordinary loss treatment for losses on sales of assets used in a trade or business. This is the best of both worlds. The alternative, ordinary gains (taxed at higher rates) and capital losses (subject to limitations) would both generally be less attractive to taxpayers

Form 4797 is a difficult form in that it provides for many errors. Practitioners must be diligent to secure the proper benefitsof §1231

New preparers should be aware that §1231 provisions are also applicable to corporations, partnerships, trusts, estates, and LLCs to name a few

© Surgent | TDP4/21/W1147

III. Section 1250 Ordinary Income Recapture; §1250 Gain (Gain on Sale of Depreciable Real Estate) Some accelerated depreciation recaptured as ordinary income

Excess of accelerated over straight line Prior to 1981 – SL over number of years of useful life

1/1/81 to 3/15/84 – if ACRS 15 was used, then excess over SL 15 ACRS after 5/8/85 –if ACRS 19 was used, then excess over SL 19 Nonresidential 1/1/81 to 12/31/86 with accelerated = 100% recapture as ordinary