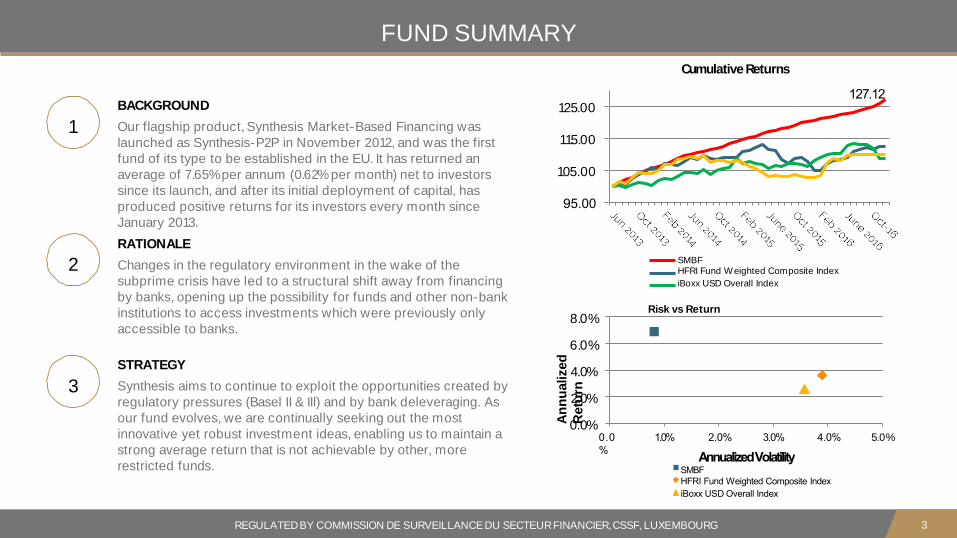

SYNTHESIS MARKET-BASED FINANCING · FUND SUMMARY 1 BACKGROUND Our flagship product,Synthesis...

26

SYNTHESIS MARKET-BASED FINANCING THE NEW EVOLUTION OF THE FIRST SPECIALISED PEER-TO-PEER LENDING FUND LAUNCHED AND REGULATED IN THE EU REGULATED BY COMMISSION DE SURVEILLANCE DU SECTEUR FINANCIER, CSSF, LUXEMBOURG 1

Transcript of SYNTHESIS MARKET-BASED FINANCING · FUND SUMMARY 1 BACKGROUND Our flagship product,Synthesis...

SYNTHESIS MARKET-BASED FINANCING

THE NEW EVOLUTION OF THE FIRST SPECIALISED PEER-TO-PEER LENDING FUND LAUNCHED

AND REGULATED IN THE EU

REGULATEDBYCOMMISSIONDESURVEILLANCEDUSECTEURFINANCIER,CSSF,LUXEMBOURG1

SYNTHESIS’ main objective is to offer uncorrelated and

“ stable returns with low volatility, converting investors’capital into lending facilities grounded in the real economy

and handing back interest earned to our investors.

Spyros Papadopoulos, Founder & CEO ”

REGULATEDBYCOMMISSIONDESURVEILLANCEDUSECTEURFINANCIER,CSSF,LUXEMBOURG 2

FUND SUMMARY

1

BACKGROUND

Our flagship product, Synthesis Market-Based Financing was

launched as Synthesis-P2P in November 2012, and was the first

fund of its type to be established in the EU. It has returned an

average of 7.65%per annum (0.62%per month) net to investors

since its launch, and after its initial deployment of capital, has

produced positive returns for its investors every month since

January 2013.

RATIONALE

Changes in the regulatory environment in the wake of the

subprime crisis have led to a structural shift away from financing

by banks, opening up the possibility for funds and other non-bank

institutions to access investments which were previously only

accessible to banks.

2

3

STRATEGY

Synthesis aims to continue to exploit the opportunities created by

regulatory pressures (Basel II & Ill) and by bank deleveraging. As

our fund evolves, we are continually seeking out the most

innovative yet robust investment ideas, enabling us to maintain a

strong average return that is not achievable by other, more

restricted funds.

127.12

95.00

105.00

115.00

125.00

CumulativeReturns

SMBFHFRI Fund Weighted Composite Index

iBoxx USD Overall Index

8.0%

6.0%

4.0%

2.0%

0.0%0.0

%

1.0% 2.0% 3.0% 4.0%

AnnualizedVolatilitySMBF

HFRI Fund Weighted Composite Index

iBoxx USD Overall Index

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 3

5.0%

An

nu

alized

Retu

rn

Risk vs Return

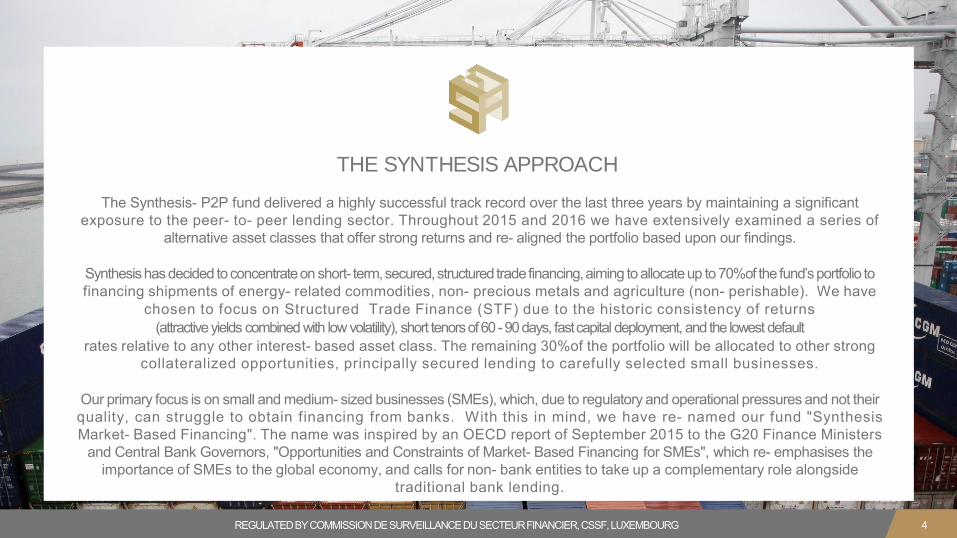

THE SYNTHESIS APPROACH

The Synthesis- P2P fund delivered a highly successful track record over the last three years by maintaining a significant

exposure to the peer- to- peer lending sector. Throughout 2015 and 2016 we have extensively examined a series of

alternative asset classes that offer strong returns and re- aligned the portfolio based upon our findings.

Synthesishas decided to concentrateon short- term,secured,structured tradefinancing,aiming to allocateup to 70%of the fund’sportfolio to

financing shipments of energy- related commodities, non- precious metals and agriculture (non- perishable). We have

chosen to focus on Structured Trade Finance (STF) due to the historic consistency of returns

(attractiveyields combined with low volatility), short tenorsof60 -90days, fastcapital deployment, and the lowest default

rates relative to any other interest- based asset class. The remaining 30%of the portfolio will be allocated to other strong

collateralized opportunities, principally secured lending to carefully selected small businesses.

Our primary focus is on small and medium- sized businesses (SMEs), which, due to regulatory and operational pressures and not their

quality, can struggle to obtain financing from banks. With this in mind, we have re- named our fund "Synthesis

Market- Based Financing". The name was inspired by an OECD report of September 2015 to the G20 Finance Ministers

and Central Bank Governors, "Opportunities and Constraints of Market- Based Financing for SMEs", which re- emphasises the

importance of SMEs to the global economy, and calls for non- bank entities to take up a complementary role alongside

traditional bank lending.

REGULATEDBYCOMMISSIONDESURVEILLANCEDUSECTEURFINANCIER,CSSF,LUXEMBOURG 4

MARKET-BASED FINANCING

STRUCTURED COMMODITY TRADE FINANCE

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 5

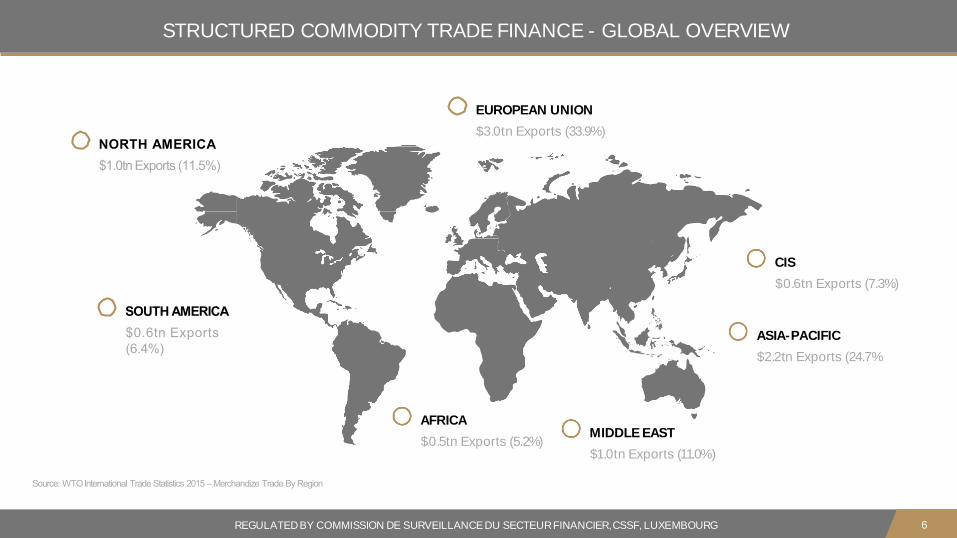

STRUCTURED COMMODITY TRADE FINANCE - GLOBAL OVERVIEW

SOUTH AMERICA

$0.6tn Exports

(6.4%)

NORTH AMERICA

$1.0tn Exports (11.5%)

AFRICA

$0.5tn Exports (5.2%)

ASIA-PACIFIC

$2.2tn Exports (24.7%

CIS

$0.6tn Exports (7.3%)

EUROPEAN UNION

$3.0tn Exports (33.9%)

MIDDLE EAST

$1.0tn Exports (11.0%)

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 6

Source: WTOInternational Trade Statistics 2015 – Merchandize Trade By Region

STRUCTURED COMMODITY TRADE FINANCE - GLOBAL OVERVIEW

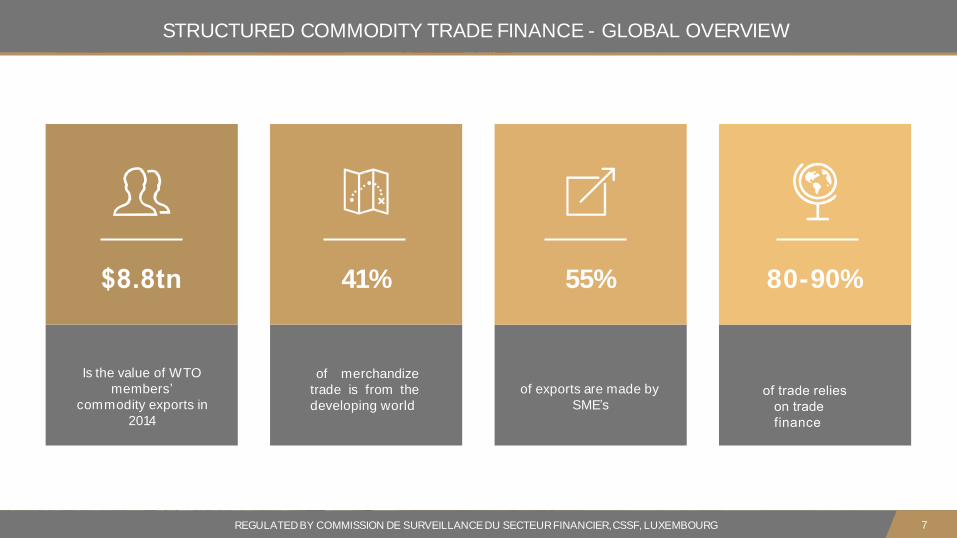

80-90%55%41%

of merchandize

trade is from the

developing world

of exports are made by

SME’sof trade relies

on trade

finance

$8.8tn

Is the value of WTO

members’

commodity exports in

2014

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 7

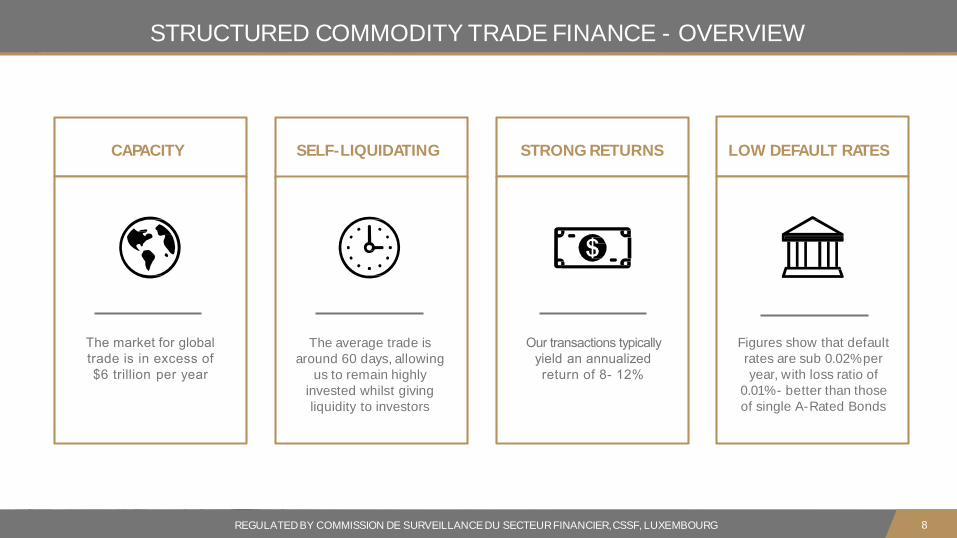

The average trade is

around 60 days, allowing

us to remain highly

invested whilst giving

liquidity to investors

SELF-LIQUIDATINGCAPACITY

The market for global

trade is in excess of

$6 trillion per year

Our transactions typically

yield an annualized

return of 8- 12%

STRONG RETURNS

Figures show that default

rates are sub 0.02%per

year, with loss ratio of

0.01%- better than those

of single A-Rated Bonds

LOW DEFAULT RATES

STRUCTURED COMMODITY TRADE FINANCE - OVERVIEW

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 8

Structured Trade Finance (‘STF’) has been in existence for almost thirty

years. Unlike with "traditional" Trade Finance, where lending is

dependent upon the credit quality of the borrower’s balance sheet, in

Structured Trade Finance, a self-liquidating arrangement is created,

focusing on the underlying transaction itself.

STF has been given many definitions over the years, but we believe the best one is

given by Dr Benedict O. Oramah as ’the art of transferring risks from

parties less able to bear them to those more equipped to manage them, in

a manner that ensures the automatic reimbursement of the financing

through the underlying transaction assets’. With STF, lenders no longer

look to borrowers as direct sources of repayment, but rather to

the underlying assets arising from the financing, namely the goods

financed and the receivables arising therefrom.

Accordingly, Structured Trade Finance makes it possible to isolate certain

risks and convert uncertainty to some certainty (‘predictable cash flow’) due to

the self-liquidating nature of transactions.

REGULATEDBYCOMMISSIONDESURVEILLANCEDUSECTEURFINANCIER,CSSF,LUXEMBOURG 10

STRUCTURED COMMODITY TRADE FINANCE - OVERVIEW

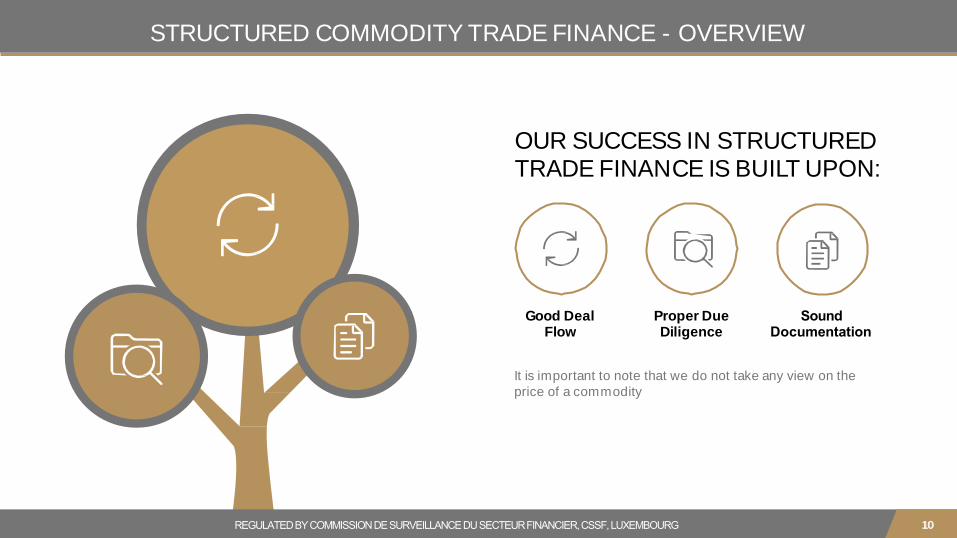

Good Deal Flow

Proper DueDiligence

OUR SUCCESS IN STRUCTURED TRADE FINANCE IS BUILT UPON:

It is important to note that we do not take any view on the

price of a commodity

SoundDocumentation

REGULATEDBYCOMMISSIONDESURVEILLANCEDUSECTEURFINANCIER,CSSF,LUXEMBOURG 1010

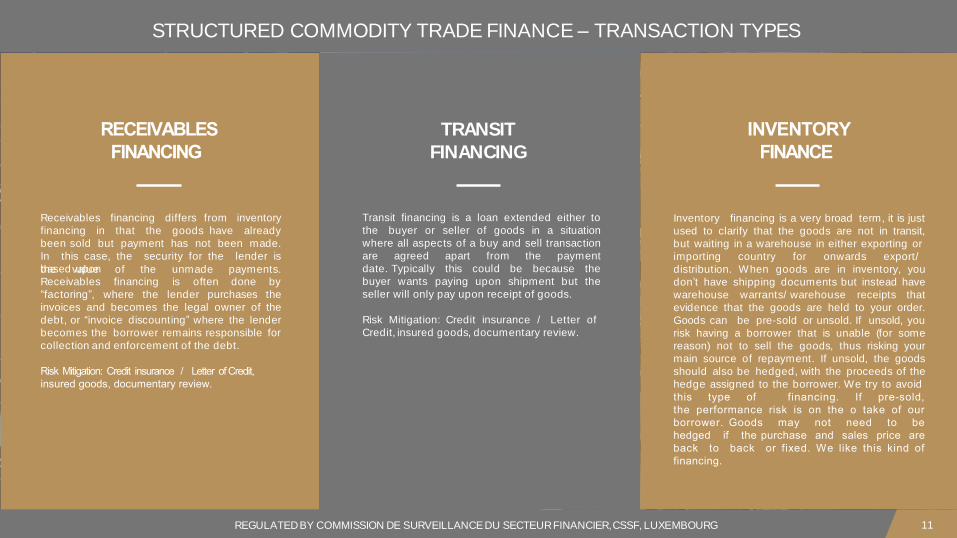

STRUCTURED COMMODITY TRADE FINANCE – TRANSACTION TYPES

Receivables financing differs from inventory

financing in that the goods have already

been sold but payment has not been made.

In this case, the security for the lender is

based uponthe value of the unmade payments.Receivables financing is often done by

“factoring”, where the lender purchases the

invoices and becomes the legal owner of the

debt, or “invoice discounting” where the lender

becomes the borrower remains responsible for

collection and enforcement of the debt.

Risk Mitigation: Credit insurance / Letter of Credit,

insured goods, documentary review.

RECEIVABLES

FINANCING

Transit financing is a loan extended either to

the buyer or seller of goods in a situation

where all aspects of a buy and sell transaction

are agreed apart from the payment

date. Typically this could be because the

buyer wants paying upon shipment but the

seller will only pay upon receipt of goods.

Risk Mitigation: Credit insurance / Letter of

Credit, insured goods, documentary review.

TRANSIT

FINANCING

Inventory financing is a very broad term, it is just

used to clarify that the goods are not in transit,

but waiting in a warehouse in either exporting or

importing country for onwards export/

distribution. When goods are in inventory, you

don’t have shipping documents but instead have

warehouse warrants/ warehouse receipts that

evidence that the goods are held to your order.

Goods can be pre-sold or unsold. If unsold, you

risk having a borrower that is unable (for some

reason) not to sell the goods, thus risking your

main source of repayment. If unsold, the goods

should also be hedged, with the proceeds of the

hedge assigned to the borrower. We try to avoid

this type of financing. If pre-sold,

the performance risk is on the o take of our

borrower. Goods may not need to be

hedged if the purchase and sales price are

back to back or fixed. We like this kind of

financing.

INVENTORY

FINANCE

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 11

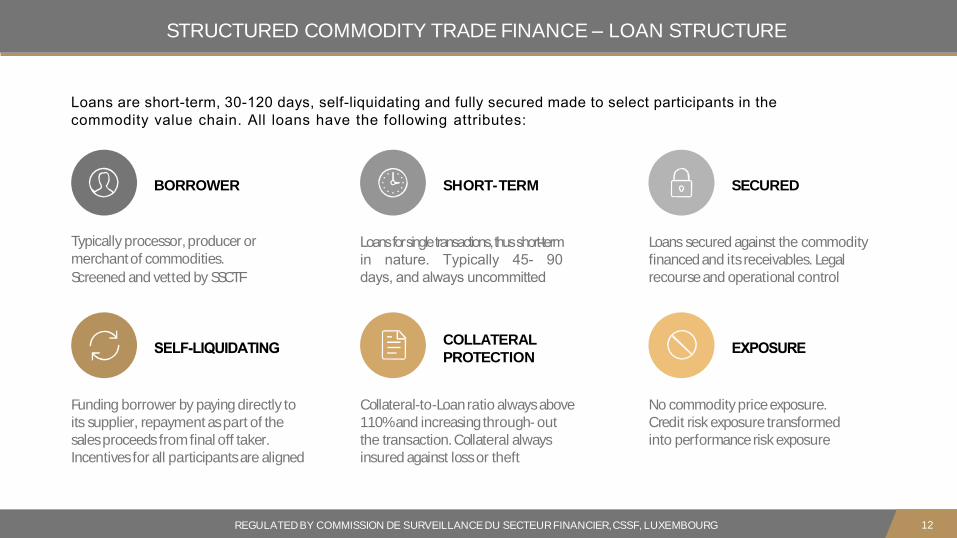

STRUCTURED COMMODITY TRADE FINANCE – LOAN STRUCTURE

Typically processor,producer or

merchantof commodities.

Screened and vetted by SSCTF

BORROWER

Funding borrower by paying directly to

its supplier, repayment aspart of the

salesproceedsfromfinal off taker.

Incentivesfor all participantsare aligned

SELF-LIQUIDATING

Loansforsingletransactions,thusshort-term

in nature. Typically 45- 90

days, and always uncommitted

SHORT-TERM

Collateral-to-Loanratio alwaysabove

110%and increasingthrough- out

the transaction.Collateral always

insured against lossor theft

COLLATERAL

PROTECTION

Loans secured against the commodity

financedand itsreceivables. Legal

recourseand operational control

SECURED

No commoditypriceexposure.

Credit risk exposure transformed

into performanceriskexposure

EXPOSURE

Loans are short-term, 30-120 days, self-liquidating and fully secured made to select participants in the

commodity value chain. All loans have the following attributes:

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 12

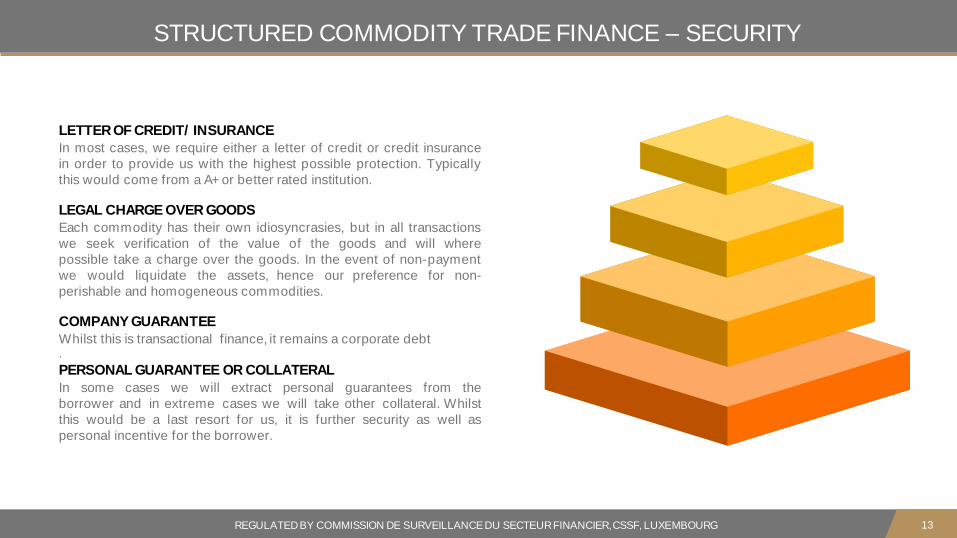

LETTEROF CREDIT/ INSURANCE

In most cases, we require either a letter of credit or credit insurance

in order to provide us with the highest possible protection. Typically

this would come from a A+ or better rated institution.

LEGAL CHARGE OVER GOODS

Each commodity has their own idiosyncrasies, but in all transactions

we seek verification of the value of the goods and will where

possible take a charge over the goods. In the event of non-payment

we would liquidate the assets, hence our preference for non-

perishable and homogeneous commodities.

COMPANY GUARANTEE

Whilst this is transactional finance, it remains a corporate debt.

PERSONAL GUARANTEE OR COLLATERAL

In some cases we will extract personal guarantees from the

borrower and in extreme cases we will take other collateral. Whilst

this would be a last resort for us, it is further security as well as

personal incentive for the borrower.

STRUCTURED COMMODITY TRADE FINANCE – SECURITY

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 13

SMALL BUSINESS

LENDING

REGULATEDBYCOMMISSIONDESURVEILLANCEDUSECTEURFINANCIER,CSSF,LUXEMBOURG 14

Since 2008, small businesses have found it increasingly hard to obtain financing from traditional lenders. At

Synthesis, we focus very particularly on the underlying assets, as well as the strength of the company’s

balance sheet, allowing us to make lending decisions based upon good Fundamentals and the security that

we receive.

Lending to Small Businesses against:

ACCOUNTS

RECEIVABLE

PROPERTY &

EQUIPMENT

PERSONAL & COMPANY

GUARANTEES

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 15

Aircraft Leasing

OTHER COLLATERALIZED OPPORTUNITIES

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 16

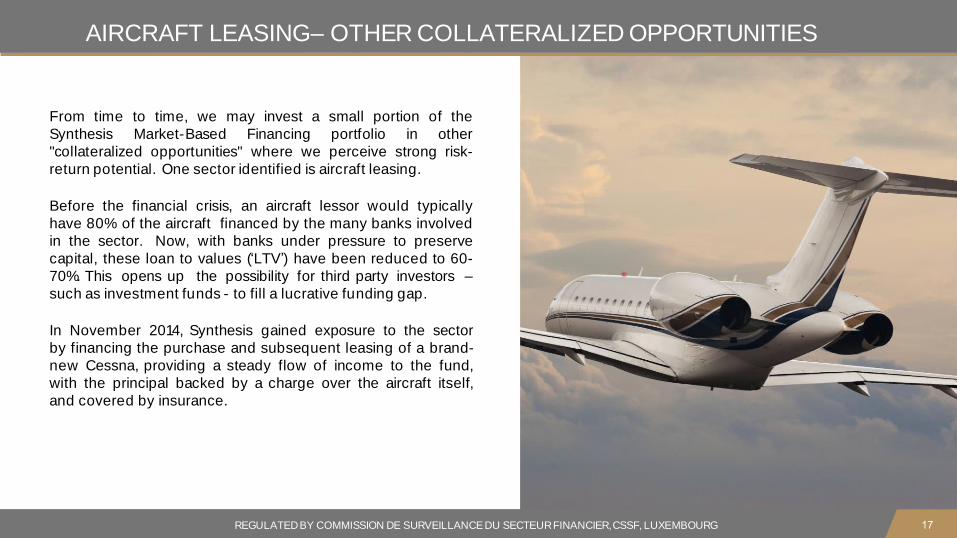

AIRCRAFT LEASING– OTHER COLLATERALIZED OPPORTUNITIES

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG

From time to time, we may invest a small portion of the

Synthesis Market-Based Financing portfolio in other

"collateralized opportunities" where we perceive strong risk-

return potential. One sector identified is aircraft leasing.

Before the financial crisis, an aircraft lessor would typically

have 80% of the aircraft financed by the many banks involved

in the sector. Now, with banks under pressure to preserve

capital, these loan to values (‘LTV’) have been reduced to 60-

70%. This opens up the possibility for third party investors –

such as investment funds - to fill a lucrative funding gap.

In November 2014, Synthesis gained exposure to the sector

by financing the purchase and subsequent leasing of a brand-

new Cessna, providing a steady flow of income to the fund,

with the principal backed by a charge over the aircraft itself,

and covered by insurance.

17

THE SYNTHESISTEAM AN INSIGHT

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 18

Spyros Papadopoulos

Spyros has over 19 years of experience in alternative investments. He began his career in Private Banking, first with Citigroup in London and Geneva,

where he was the key contributor to the development of both the Spanish and Greek Wealth Management Desks, and then with Societe Generale in

Athens, where he was instrumental to the expansion of the Greek Private Banking division. Spyros resigned from Private Banking in 2006 to set up an asset

management company for Deloitte, before returning to London as Director of the hedge fund Absolute Return Partners. He left to found Synthesis in

June 2009. His clients came through unscathed, and indeed pro ted, from the crises of 2000-02 and 2007-present. Spyros holds the Investment

Management Certificate of the CFA-Society of the UK.

Joseph Samuel

With more than 15 years’ broad experience in the legal and financial sectors, Joseph is an experienced management professional, having grown,

re- organised and co-ordinated a number of funds, businesses, teams and departments, with full P&L responsibility and an excellent track record. A key

element of his work has been doing business face to face internationally, having undertaken business trips across five

continents to more than 50 countries, and with clients in more than 150. In 2015, he founded Old Park Lane Consultancy Ltd,

through which he consults on fund structuring, capital raising, product development, international business and communications for a number of

clients.

Aristides Protopapadakis Aristides has a banking background, with a wealth of experience in derivatives, credit, risk analytics, and financial software

systems. Prior to setting up Systemic Risk Management Solutions, he acquired extensive experience in the above areas while holding senior positions at

Citibank, ABN Amro, and Bank of America in Treasury and Risk Management units. Aristides holds an MBA in Commercial Engineering from the

Solvay Business School (Universite Libre de Bruxelles).

THE SYNTHESIS TEAM

REGULATEDBYCOMMISSIONDESURVEILLANCEDUSECTEURFINANCIER,CSSF,LUXEMBOURG 19

Adrian Bell is a UK national fluent in German and Russian, with 20 years' experience in the physical commodity space. Adrian has transformed, traded, hedged,

financed, transported, stored, trans-shipped and insured multifarious physical agri commodities with a focus on vegetable oils and, in particular, the sunflower complex.

Having lived in Germany and Russia as a student, Adrian lived in Odessa, Ukraine for 10 years, where he worked for a major local operator managing a sunflower crush and

importing palms and laurics for distribution throughout the CIS. Resident in Switzerland since 2006, Adrian worked for a while at Bunge Geneva on the MENA desk, for

whom he opened a rep office in Nairobi in 2010. From 2011-2015, Adrian was head of trading for the 2nd largest Ukrainian sunflower and soya bean crusher with a

700kmt annual vegoil book which he ran single-handedly from the group's Swiss office. Under Adrian's aegis, the group graduated from CPT port to FOB and CIF and became

the largest exporter of crude sunflower oil in bulk to China in the 2013-14 campaign.

Natalia Liebiedieva has over 18 years’ experience within the banking industry in Ukraine, with a focus on corporate clients. She has extensive knowledge of complex

financial structures and products in the loan and debt sector, including in-depth experience of structured finance. Natalia started her career at Petrocommerce Bank

Ukraine, where she rose to Head of the Loan Division, Head of Corporate Banking and a Member of the Board. She has since held senior Board positions with BTA Bank,

Bank of Kiev Rus and Ukrgasbank. Natalia holds a diploma in International Affairs from the National Aviation University of Kiev, and a Senior Executive MBA from the

MIM-Kiev Business School.

Mohendra Moodley has over 17 years of experience in investment management and commodities on the buy and sell side in equity research, funds

management, physical commodity trading, trade finance and advisory. He was worked in various capacities in Australia and South Africa as a fund manager and trader

innatural resources. Mohendra has been responsible for allocating capital in commodity assets for banks, family offices, pension funds and multi management

groups in the USA, South Africa, Australia, UK and Germany. He has been an advisor and arranger on various cross border and local trade and supply chain finance

transactions in precious metals, base metals, fertiliser and finished products in Hong Kong, Singapore, Indonesia, South Africa, USA and Australia. Mohendra holds a

Bachelor of Commerce and BCom Honours in Finance (Cum Laude).

THE SYNTHESIS TEAM

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 22

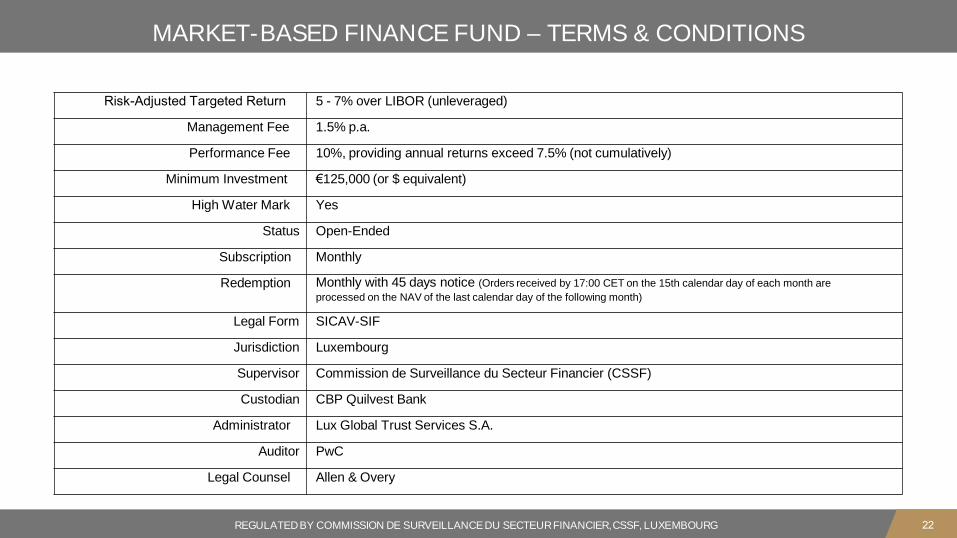

MARKET-BASED FINANCE FUND – TERMS & CONDITIONS

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 22

Risk-Adjusted Targeted Return 5 - 7% over LIBOR (unleveraged)

Management Fee 1.5% p.a.

Performance Fee 10%, providing annual returns exceed 7.5% (not cumulatively)

Minimum Investment €125,000 (or $ equivalent)

High Water Mark Yes

Status Open-Ended

Subscription Monthly

Redemption Monthly with 45 days notice (Orders received by 17:00 CET on the 15th calendar day of each month are

processed on the NAV of the last calendar day of the following month)

Legal Form SICAV-SIF

Jurisdiction Luxembourg

Supervisor Commission de Surveillance du Secteur Financier (CSSF)

Custodian CBP Quilvest Bank

Administrator Lux Global Trust Services S.A.

Auditor PwC

Legal Counsel Allen & Overy

ANNEX

SUPPLEMENTARY INFORMATION

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 23

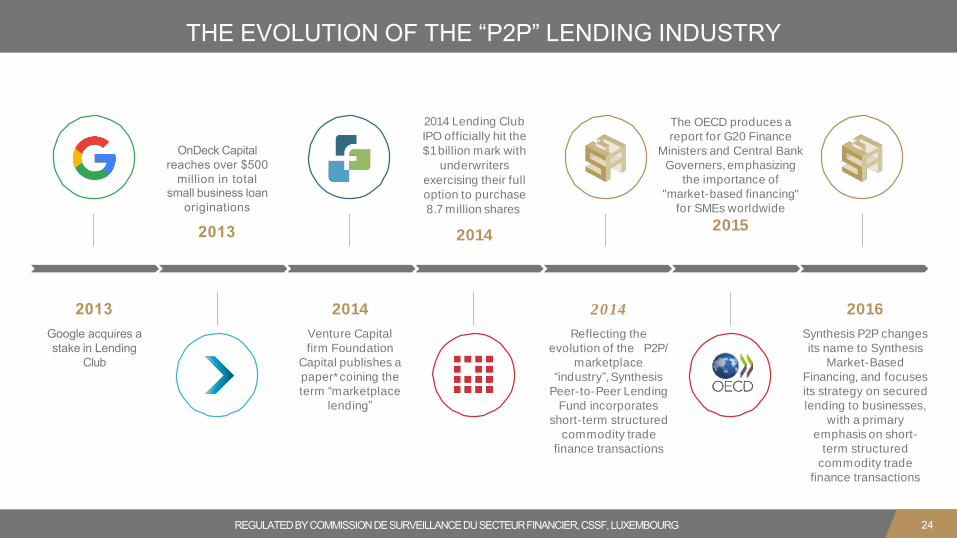

THE EVOLUTION OF THE “P2P” LENDING INDUSTRY

2005

The concept of

peer-to-peer

(consumer) lending

is pioneered in the

UK by Zopa

Founding of

Lending Club and

Prosper in the US.

Lending Club

originates its first

loan in June 2007

2006

2010

MarketInvoice is

incorporated in the UK

for the purpose of

short- term receivables

financing of UK SMEs

Launch of

OnDeck Capital in

the US, providing

small business

loans to SMEs

20 11

2012

Incorporation of

LendInvest in the

UK, and Realty

Mogul in the US, for

short- term bridging

property finance

Lending Club

reaches over $1

billion in total

consumer loan

originations

2012

2012

Launch of

Synthesis Peer-to-

Peer Lending Fund

REGULATEDBYCOMMISSIONDESURVEILLANCEDUSECTEURFINANCIER,CSSF,LUXEMBOURG 2323

2013

Google acquires a

stake in Lending

Club

OnDeck Capital

reaches over $500

million in totalsmall business loan

originations

2013

2014

Venture Capital

firm Foundation

Capital publishes a

paper*coining the

term “marketplace

lending”

2014 Lending Club

IPO officially hit the

$1billion mark with

underwriters

exercising their full

option to purchase

8.7 million shares

2014

2014

Reflecting the

evolution of the P2P/

marketplace

“industry”,Synthesis

Peer-to-Peer Lending

Fund incorporates

short-term structured

commodity trade

finance transactions

THE EVOLUTION OF THE “P2P” LENDING INDUSTRY

The OECD produces a

report for G20 Finance

Ministers and Central Bank

Governers,emphasizing

the importance of

"market-based financing"

for SMEs worldwide

2015

2016

Synthesis P2P changes

its name to Synthesis

Market-Based

Financing, and focuses

its strategy on secured

lending to businesses,

with a primary

emphasis on short-

term structured

commodity trade

finance transactions

REGULATEDBYCOMMISSIONDESURVEILLANCEDUSECTEURFINANCIER,CSSF,LUXEMBOURG 24

This document is not intended for any citizen of the United States or any other person or entity subject to U.S. Securities law.

Without any limitation, this presentation does not constitute an offer, an invitation to offer or a recommendation to enter into any transaction. The

information herein does not constitute the provision of investment advice or a recommendation; its sole purpose is to generate interest for a product

proposal. Changes to this presentation may be made without notice. Opinions expressed may differ from views set out in other documents. Although the

information contained herein has been taken from sources, which the authors believe to be accurate, no warranty or representation is made as to the

correctness, completeness and accuracy of the information or the assessments made on its basis. The authors do not accept liability for any damage

arising from the reliance on this presentation. This presentation may not be distributed by the recipient to any other person without the express written

consent of the authors. Each recipient of this presentation is expected to be sophisticated and capable of independently evaluating the merits and risks

of an investment in the product. If an investor decides to invest in the fund, the investor does so in reliance on his own judgement. Investing in the

product reflects a particular market view the recipient of this presentation has taken independently from the authors. When making an investment

decision the recipient of this presentation should rely solely on his own market and financial research and not the information contained here in. The

product described herein may not suit all investors and before entering into any transaction each investor should take steps to ensure that he fully

understands the product and has made an independent assessment of the suitability of the product, including its possible risks, in light of the investor’s

own objectives and financial situation. In particular, investing in the product may result in the return of less than the investor’s original investment and

even the total loss thereof.Any investor should seek advice from its professional advisors in making such assessment.

DISCLAIMER

REGULATEDBY COMMISSION DE SURVEILLANCEDU SECTEURFINANCIER,CSSF, LUXEMBOURG 25