Market Share Expansion Financing (Msef)Diaporama

28

-

Upload

business-3g -

Category

Documents

-

view

689 -

download

0

Transcript of Market Share Expansion Financing (Msef)Diaporama

Market Share Market Share Expansion Financing Expansion Financing

(MSEF(MSEF®®))

An NFC/ Northern Finance Corporation An NFC/ Northern Finance Corporation ProductProduct

To maximizeTo maximizeYourYour

Financial Performance and ProfitFinancial Performance and Profit

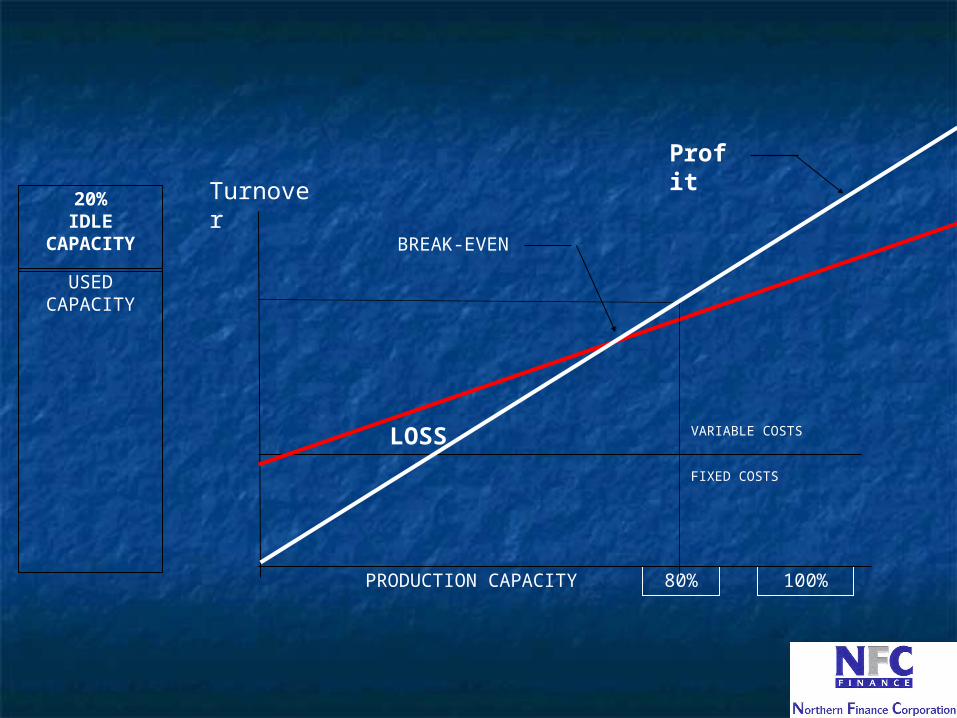

100%80%

USED CAPACITY

20%IDLE

CAPACITY BREAK-EVEN

LOSS

PRODUCTION CAPACITY

FIXED COSTS

VARIABLE COSTS

Profit

Turnover

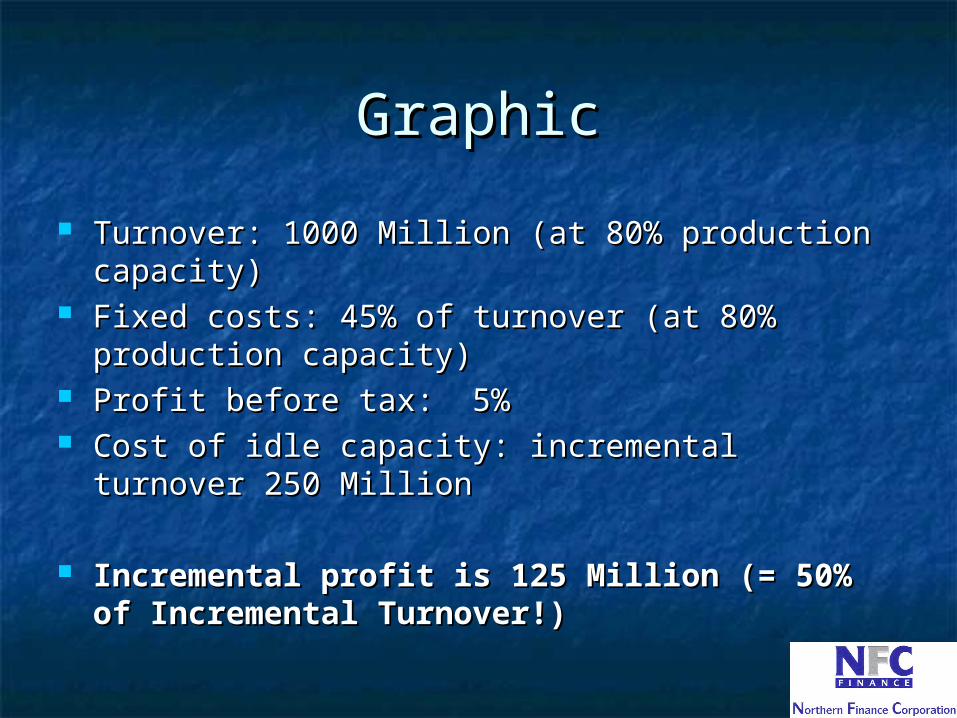

GraphicGraphic

Turnover: 1000 Million (at 80% production Turnover: 1000 Million (at 80% production capacity)capacity)

Fixed costs: 45% of turnover (at 80% production Fixed costs: 45% of turnover (at 80% production capacity)capacity)

Profit before tax:Profit before tax: 5%5% Cost of idle capacity: incremental turnover 250 Cost of idle capacity: incremental turnover 250

MillionMillion

Incremental profit is 125 Million (= 50% of Incremental profit is 125 Million (= 50% of Incremental Turnover!)Incremental Turnover!)

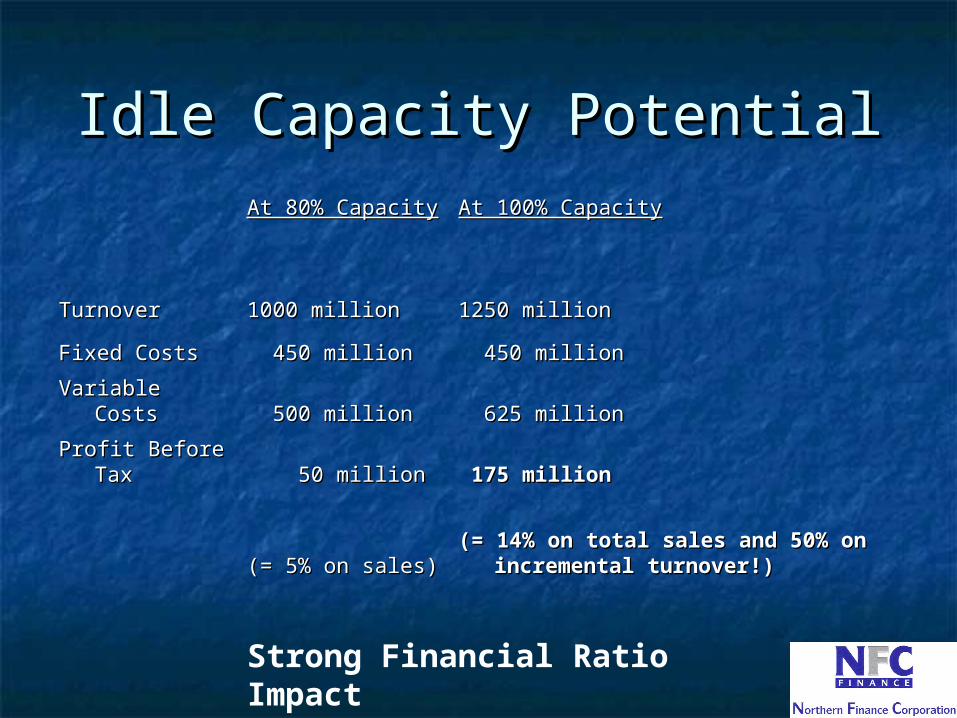

Idle Capacity PotentialIdle Capacity PotentialAt 80% CapacityAt 80% Capacity At 100% CapacityAt 100% Capacity

TurnoverTurnover 1000 million1000 million 1250 million1250 million

Fixed CostsFixed Costs 450 million450 million 450 million450 million

Variable CostsVariable Costs 500 million500 million 625 million625 million

Profit Before Profit Before TaxTax 50 million50 million 175 million175 million

(= 5% on sales)(= 5% on sales)(= 14% on total sales and 50% on (= 14% on total sales and 50% on

incremental turnover!)incremental turnover!)

Strong Financial Ratio Impact

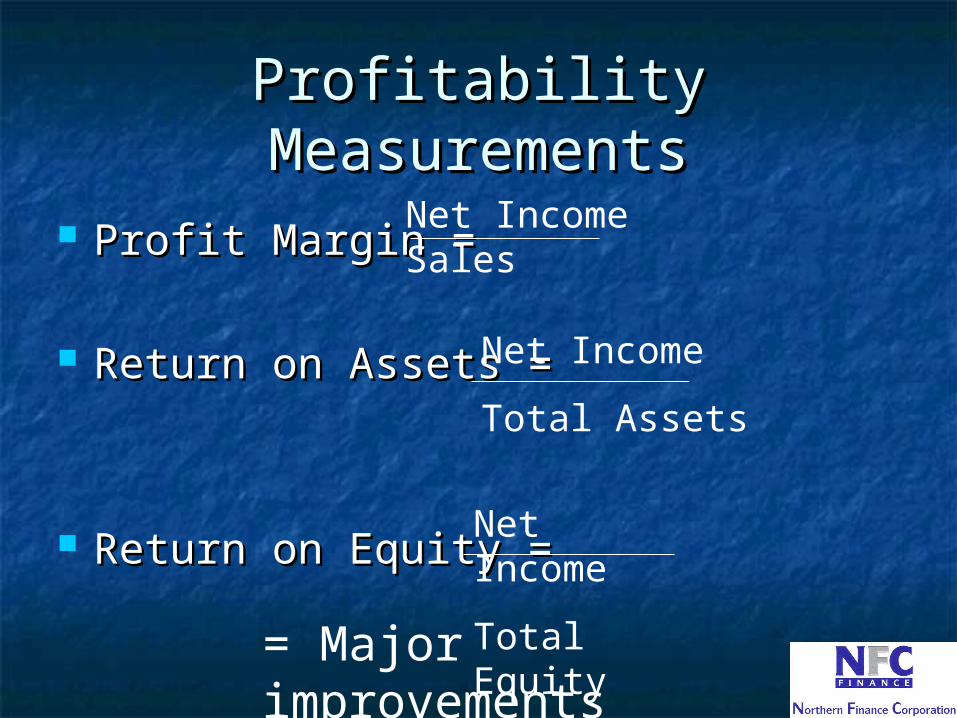

Profitability MeasurementsProfitability Measurements

Profit Margin =Profit Margin =

Return on Assets =Return on Assets =

Return on Equity = Return on Equity =

Net IncomeSales

Net Income

Total Assets

Net Income

Total Equity

= Major improvements

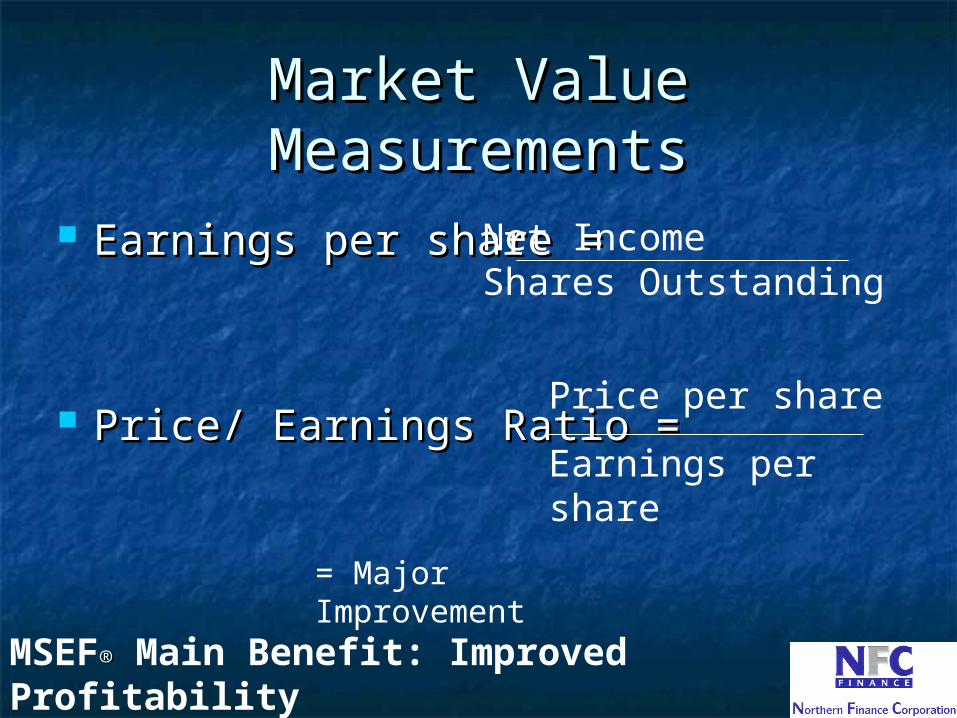

Market Value MeasurementsMarket Value Measurements

Earnings per share = Earnings per share =

Price/ Earnings RatioPrice/ Earnings Ratio = =

Net IncomeShares Outstanding

Price per share

Earnings per share

MSEF®® Main Benefit: Improved Profitability

= Major Improvement

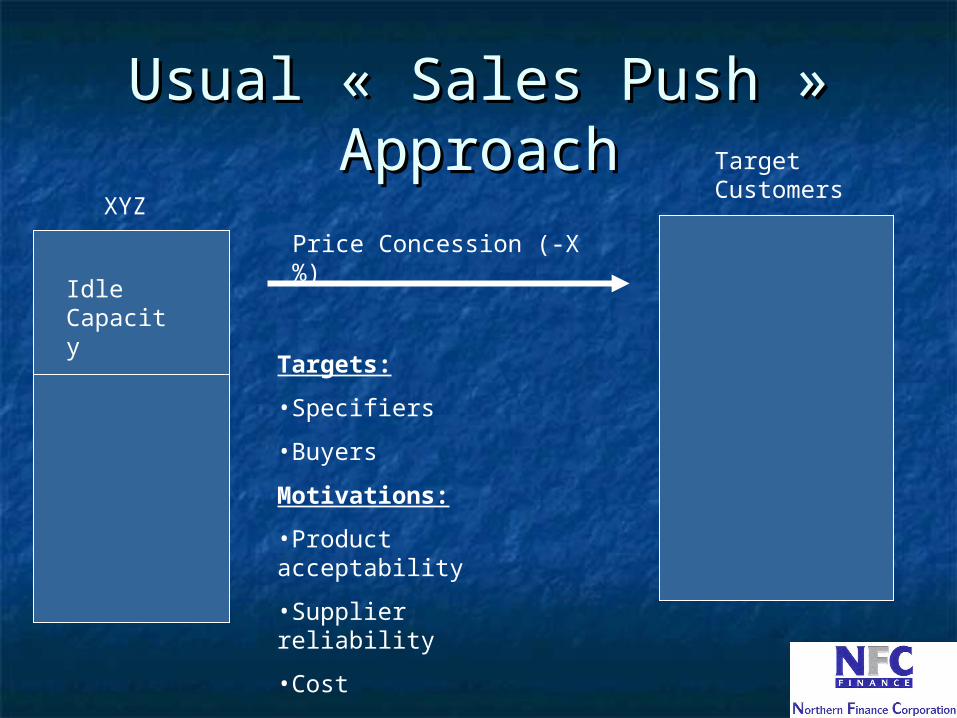

Usual « Sales Push » Usual « Sales Push » ApproachApproach

XYZ

Idle Capacity

Target Customers

Price Concession (-X%)

Targets:

•Specifiers

•Buyers

Motivations:

•Product acceptability

•Supplier reliability

•Cost

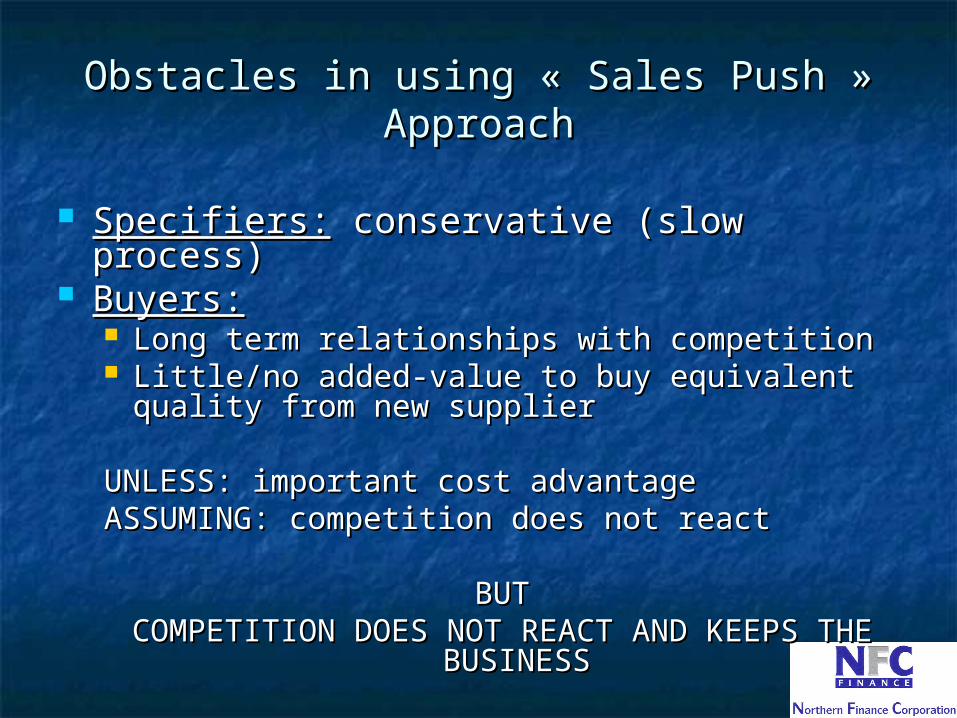

Obstacles in using « Sales Push » Obstacles in using « Sales Push » ApproachApproach

Specifiers:Specifiers: conservative (slow process) conservative (slow process) Buyers:Buyers:

Long term relationships with competitionLong term relationships with competition Little/no added-value to buy equivalent quality Little/no added-value to buy equivalent quality

from new supplierfrom new supplier

UNLESS: important cost advantageUNLESS: important cost advantageASSUMING: competition does not reactASSUMING: competition does not react

BUTBUTCOMPETITION DOES NOT REACT AND KEEPS THE COMPETITION DOES NOT REACT AND KEEPS THE

BUSINESSBUSINESS

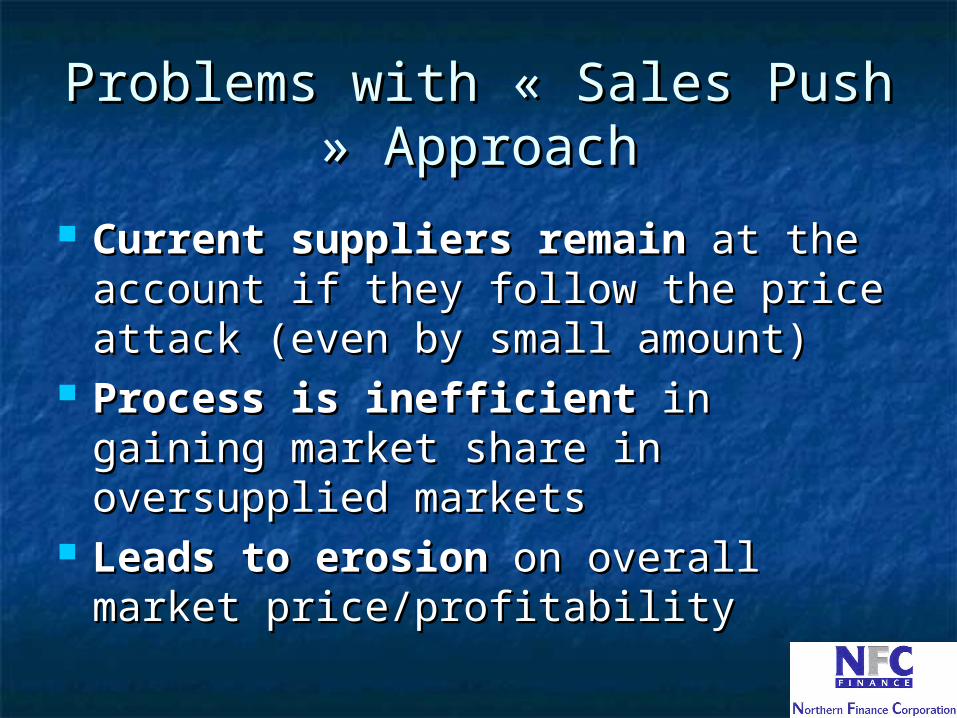

Problems with « Sales Push » Problems with « Sales Push » ApproachApproach

Current suppliers remainCurrent suppliers remain at the at the account if they follow the price account if they follow the price attack (even by small amount)attack (even by small amount)

Process is inefficientProcess is inefficient in gaining in gaining market share in oversupplied market share in oversupplied marketsmarkets

Leads to erosionLeads to erosion on overall market on overall market price/profitabilityprice/profitability

The « Sales Push » ApproachThe « Sales Push » Approachis is

A DEAD END!A DEAD END!

What is the REAL solution?What is the REAL solution?

The MSEF® MethodThe MSEF® Method

What IF….What IF….

Instead of sellingInstead of selling

……We buy?We buy?

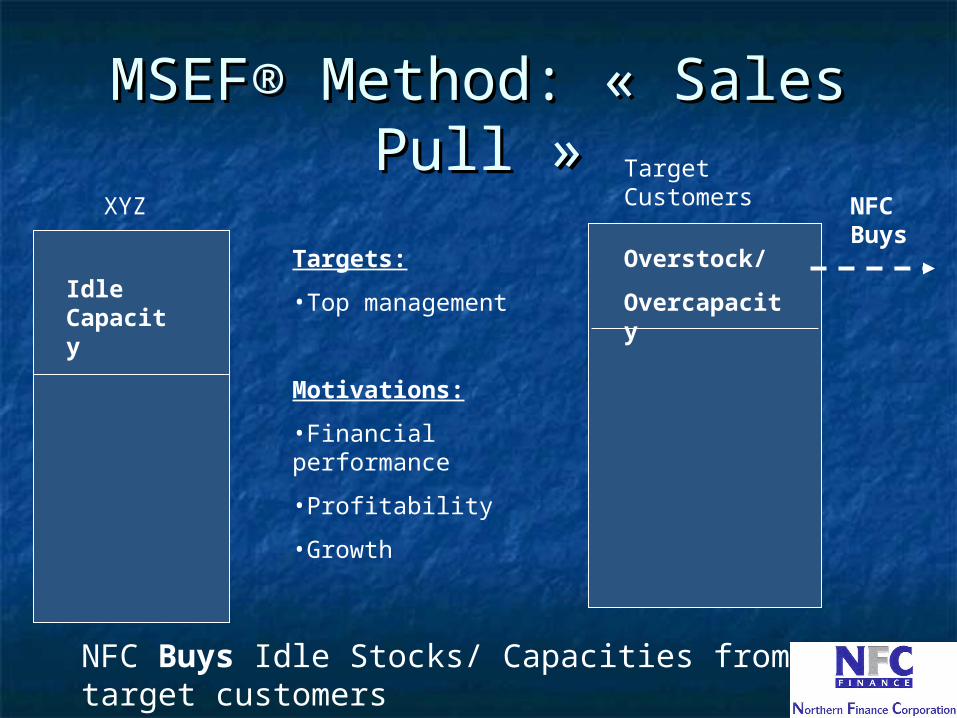

MSEF® Method: « Sales PullMSEF® Method: « Sales Pull »»

XYZ

Idle Capacity

Targets:

•Top management

Motivations:

•Financial performance

•Profitability

•Growth

Target Customers

Overstock/

Overcapacity

NFC Buys

NFC Buys Idle Stocks/ Capacities from target customers

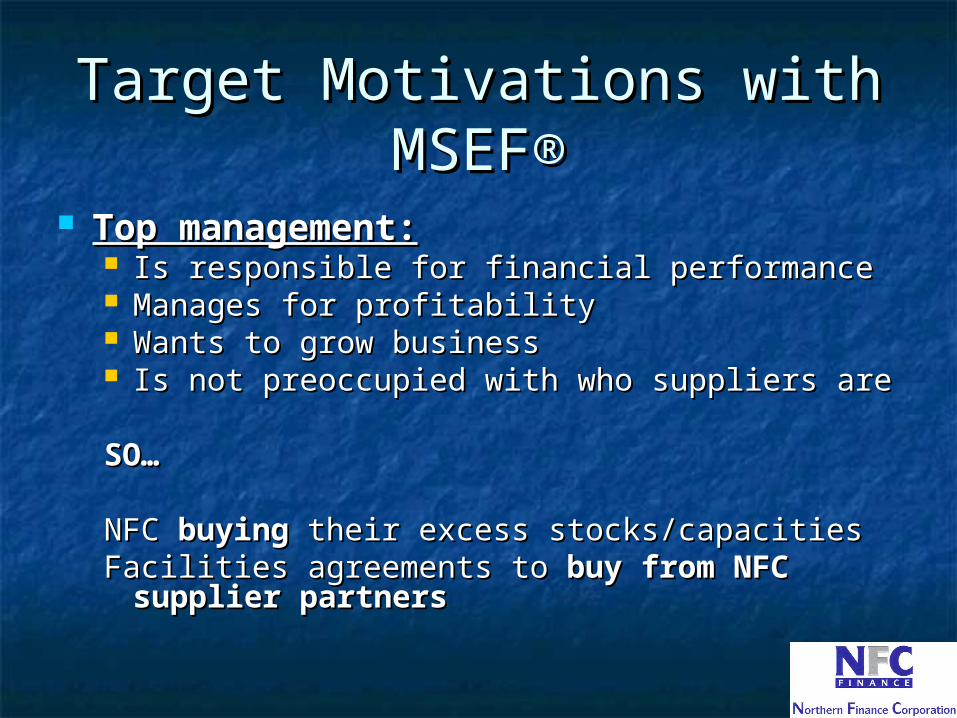

Target Target Motivations withMotivations with MSEFMSEF®®

Top management:Top management: Is responsible for financial performanceIs responsible for financial performance Manages for profitabilityManages for profitability Wants to grow businessWants to grow business Is not preoccupied with who suppliers areIs not preoccupied with who suppliers are

SO…SO…

NFC NFC buyingbuying their excess stocks/capacities their excess stocks/capacitiesFacilities agreements to Facilities agreements to buy from NFC buy from NFC

supplier partnerssupplier partners

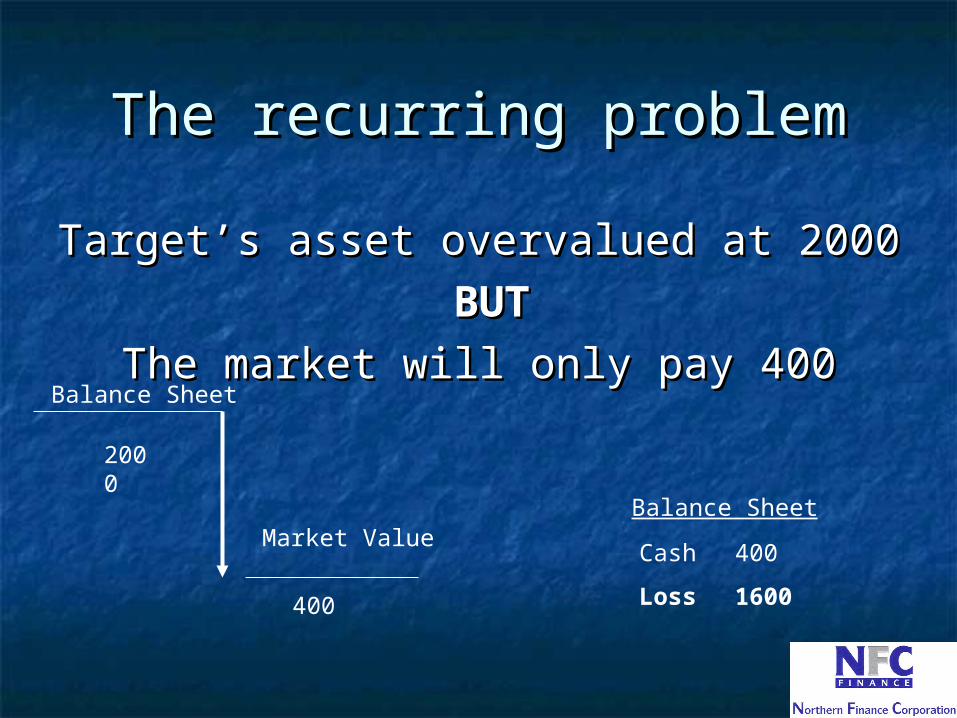

The recurring problemThe recurring problem

Target’s asset overvalued at 2000Target’s asset overvalued at 2000

BUTBUT

The market will only pay 400The market will only pay 400Balance Sheet

Market ValueBalance Sheet

Cash 400

Loss 1600400

2000

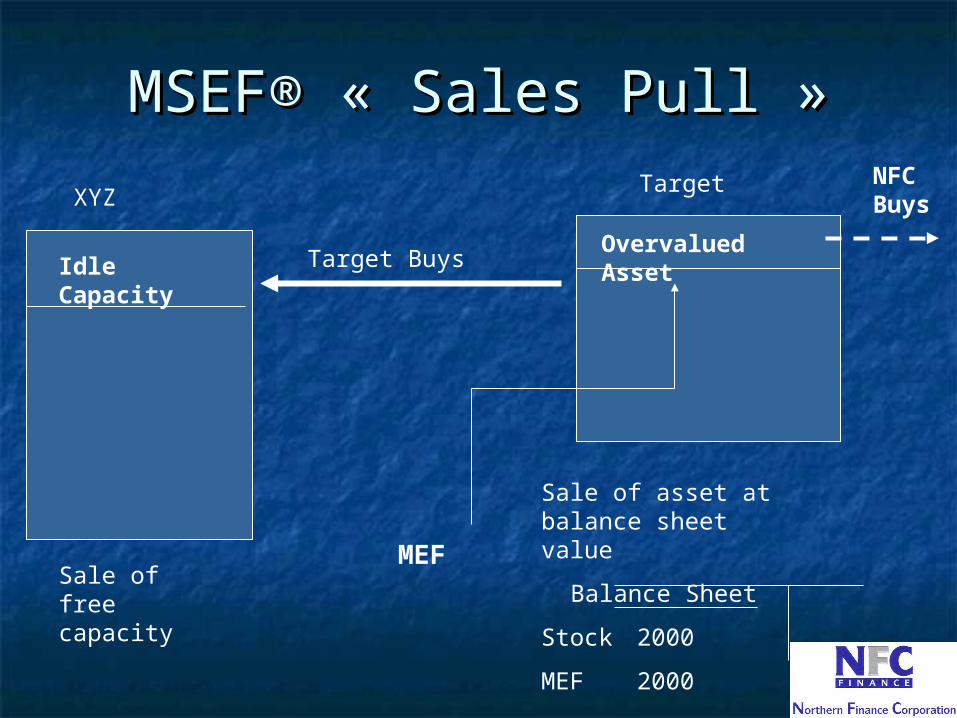

MSEFMSEF®® « Sales Pull » « Sales Pull »

Idle Capacity

XYZ

Overvalued Asset

Target

Target Buys

Sale of free capacity

MEF

Sale of asset at balance sheet value

Balance Sheet

Stock 2000

MEF 2000

NFC Buys

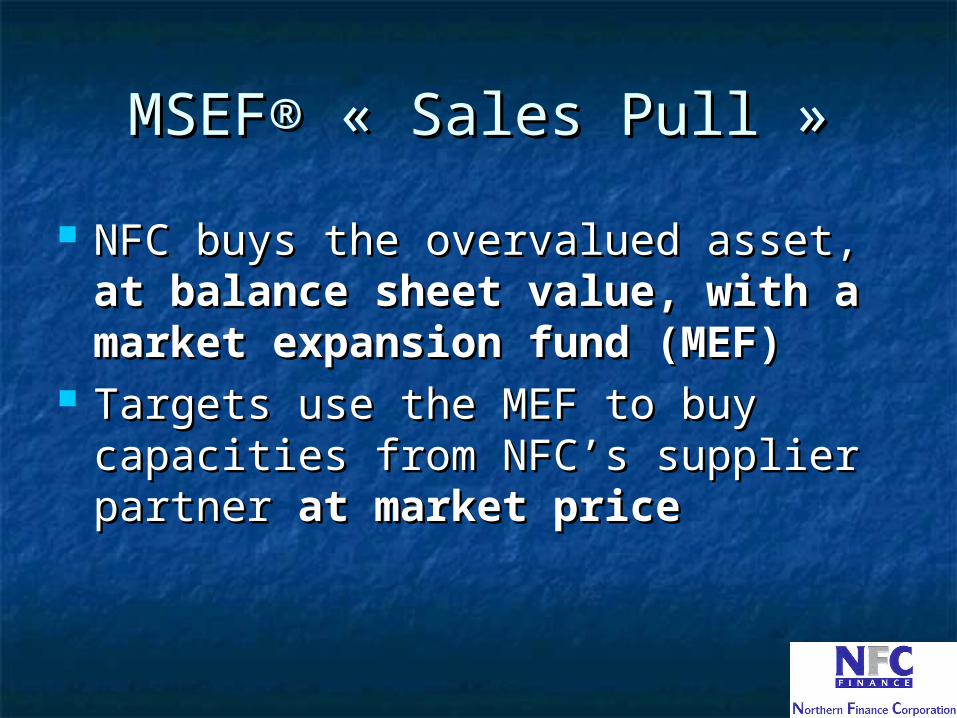

MSEFMSEF®® « Sales Pull » « Sales Pull »

NFC buys the overvalued asset, NFC buys the overvalued asset, at at balance sheet value, with a balance sheet value, with a market expansion fund (MEF)market expansion fund (MEF)

Targets use the MEF to buy Targets use the MEF to buy capacities from NFC’s supplier capacities from NFC’s supplier partner partner at market priceat market price

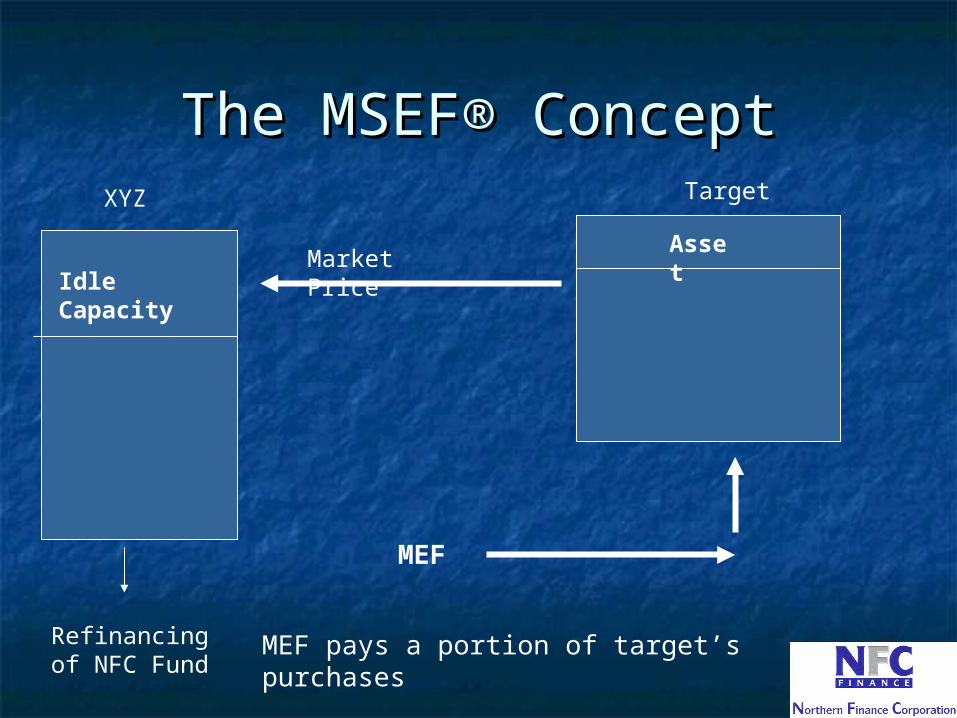

The MSEF® ConceptThe MSEF® ConceptXYZ

Asset

Target

Market Price

Refinancing of NFC Fund

MEF

Idle Capacity

MEF pays a portion of target’s purchases

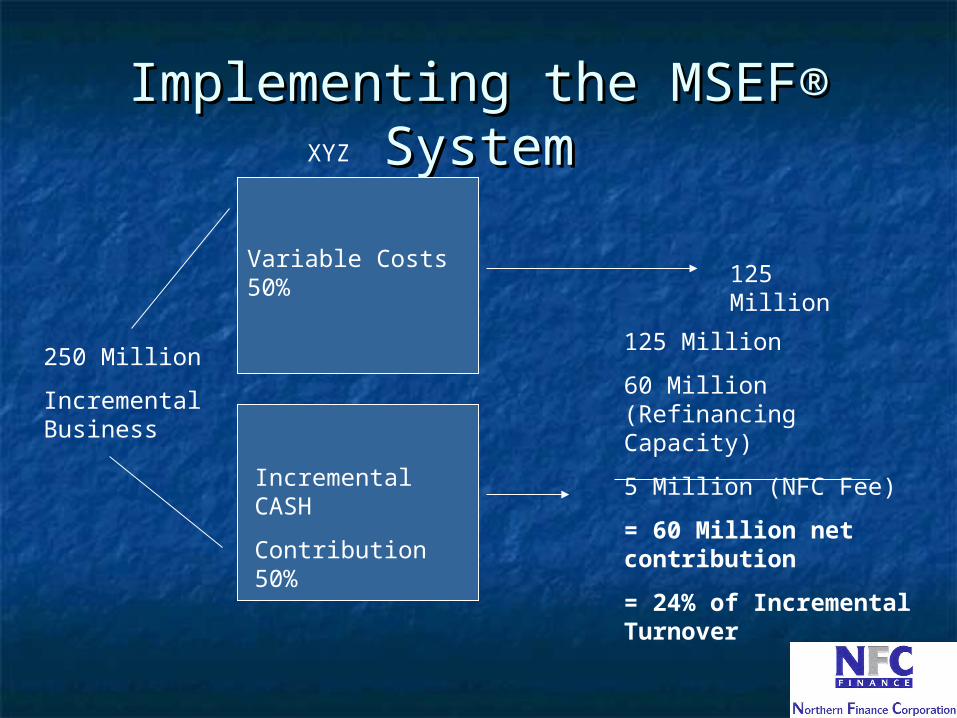

Implementing the MSEF® Implementing the MSEF® SystemSystemXYZ

Variable Costs 50%

Incremental CASH

Contribution 50%

250 Million

Incremental Business

125 Million

125 Million

60 Million (Refinancing Capacity)

5 Million (NFC Fee)

= 60 Million net contribution

= 24% of Incremental Turnover

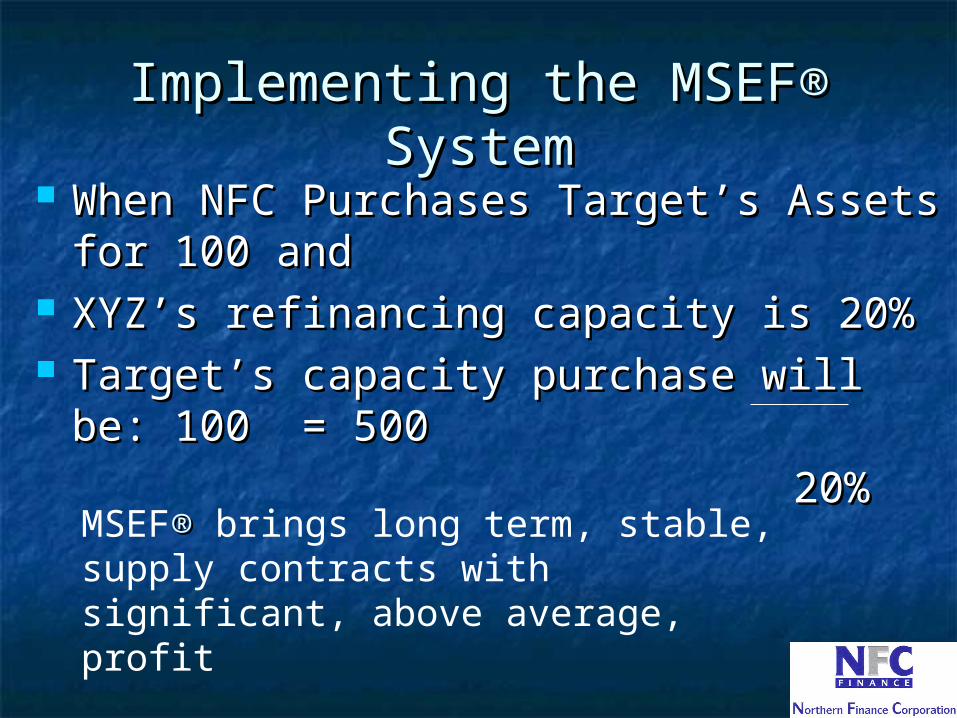

Implementing the MSEF® Implementing the MSEF® SystemSystem

When NFC Purchases Target’s Assets for When NFC Purchases Target’s Assets for 100 and100 and

XYZ’s refinancing capacity is 20%XYZ’s refinancing capacity is 20% Target’s capacity purchase will be: 100 Target’s capacity purchase will be: 100

= 500= 500

20% 20% MSEF®® brings long term, stable, supply contracts with significant, above average, profit

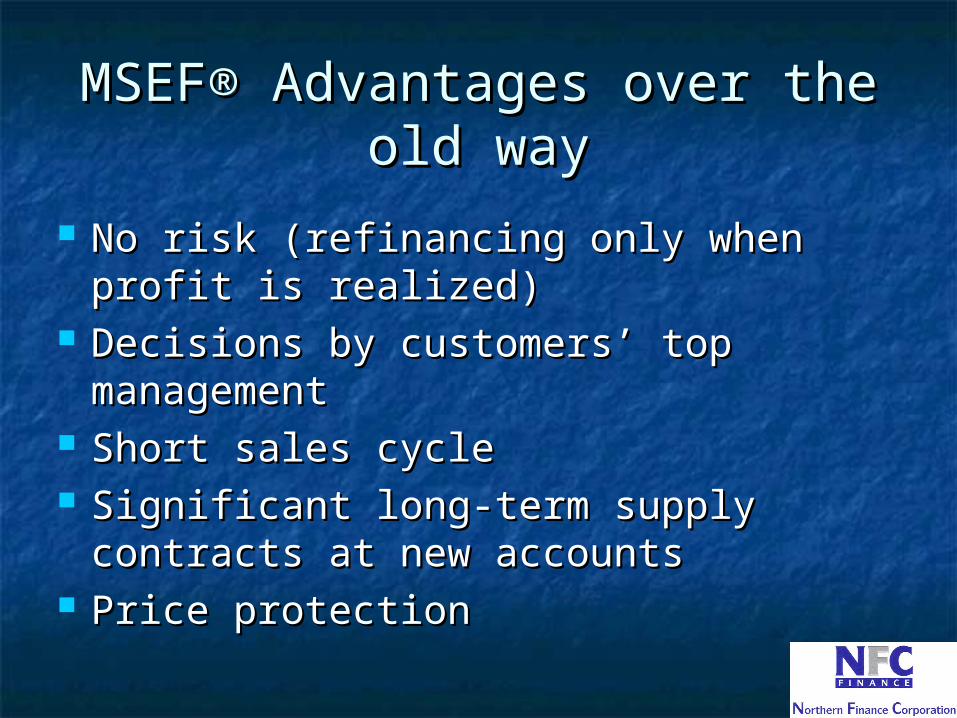

MSEF® Advantages over the MSEF® Advantages over the old wayold way

No risk (refinancing only when profit is No risk (refinancing only when profit is realized)realized)

Decisions by customers’ top Decisions by customers’ top managementmanagement

Short sales cycleShort sales cycle Significant long-term supply contracts Significant long-term supply contracts

at new accountsat new accounts Price protectionPrice protection

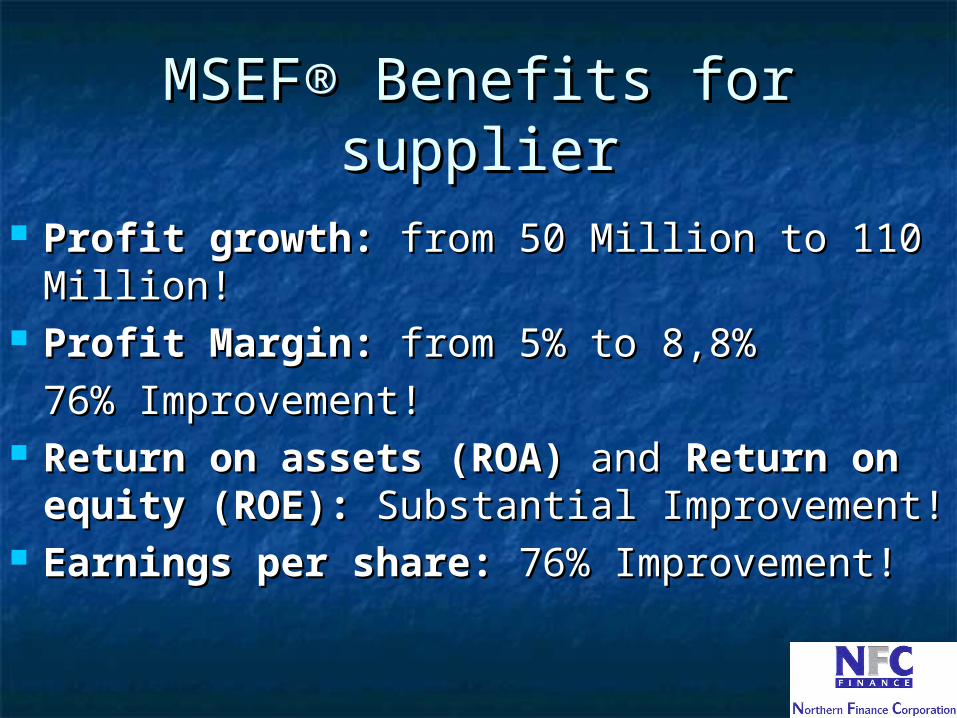

MSEF® Benefits for supplierMSEF® Benefits for supplier

Profit growth:Profit growth: from 50 Million to 110 from 50 Million to 110 Million!Million!

Profit Margin:Profit Margin: from 5% to 8,8% from 5% to 8,8%

76% Improvement!76% Improvement! Return on assets (ROA)Return on assets (ROA) and and Return onReturn on

equity (ROE):equity (ROE): Substantial Improvement! Substantial Improvement! Earnings per share:Earnings per share: 76% Improvement! 76% Improvement!

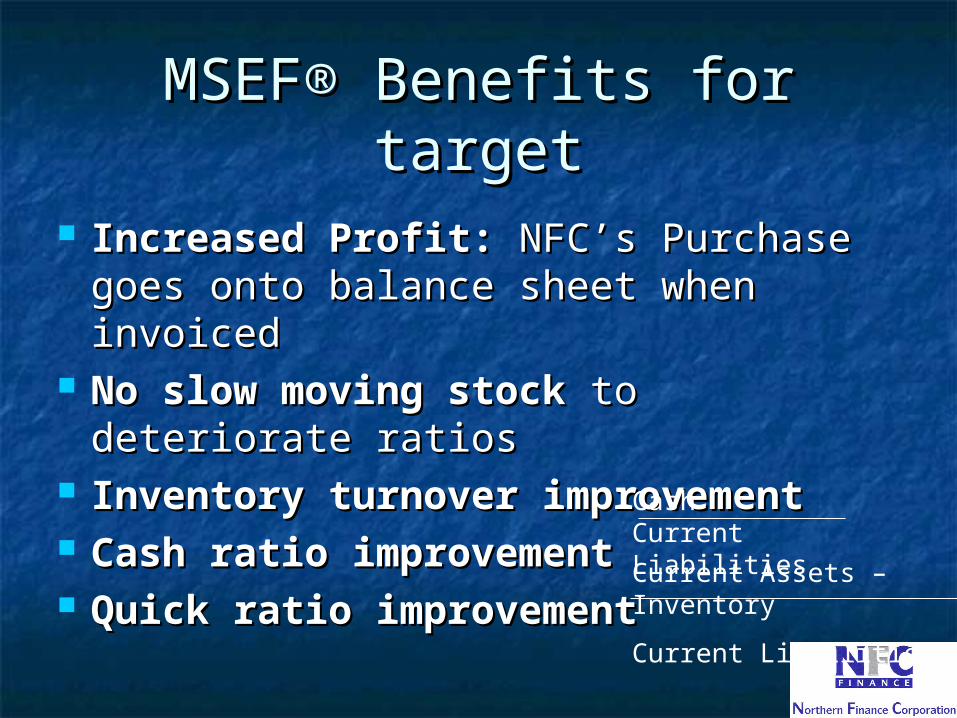

MSEF® Benefits for targetMSEF® Benefits for target

Increased Profit:Increased Profit: NFC’s Purchase NFC’s Purchase goes onto balance sheet when goes onto balance sheet when invoicedinvoiced

No slow moving stockNo slow moving stock to deteriorate to deteriorate ratiosratios

Inventory turnover improvementInventory turnover improvement Cash ratio improvementCash ratio improvement Quick ratio improvementQuick ratio improvement

CashCurrent Liabilities

Current Assets – Inventory

Current Liabilities

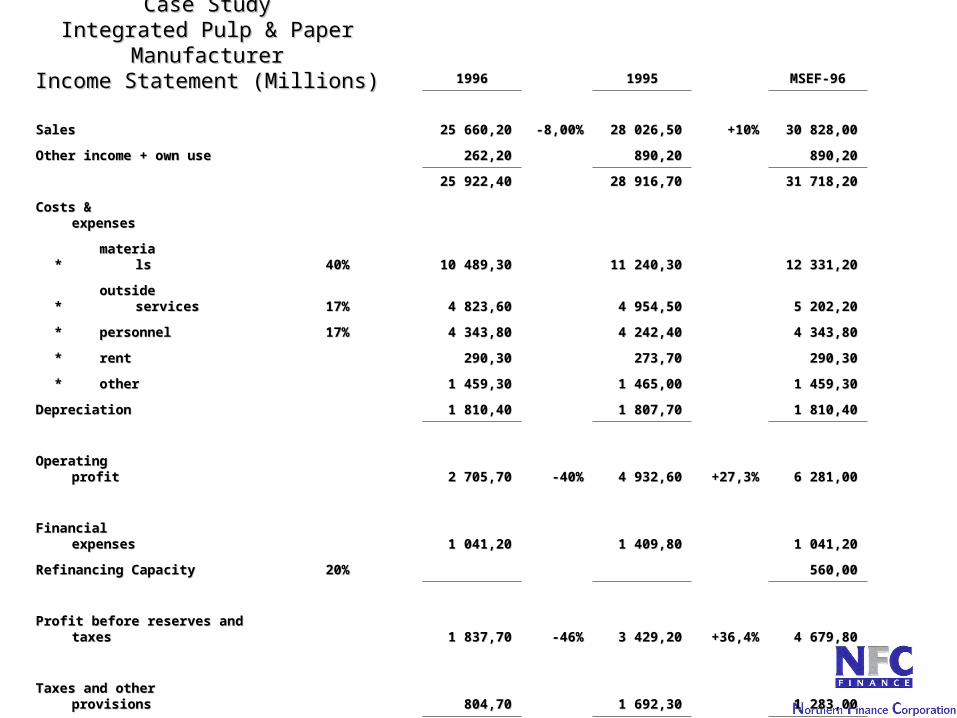

Case StudyCase StudyIntegrated Pulp & Paper Integrated Pulp & Paper

ManufacturerManufacturerIncome Statement (Millions)Income Statement (Millions) 19961996 19951995 MSEF-96MSEF-96

SalesSales 25 660,2025 660,20 -8,00%-8,00% 28 026,5028 026,50 +10%+10% 30 828,0030 828,00

Other income + own useOther income + own use 262,20262,20 890,20890,20 890,20890,20

25 922,4025 922,40 28 916,7028 916,70 31 718,2031 718,20

Costs & Costs & expensesexpenses

**materiamateria

lsls 40%40% 10 489,3010 489,30 11 240,3011 240,30 12 331,2012 331,20

** outside servicesoutside services 17%17% 4 823,604 823,60 4 954,504 954,50 5 202,205 202,20

** personnelpersonnel 17%17% 4 343,804 343,80 4 242,404 242,40 4 343,804 343,80

** rentrent 290,30290,30 273,70273,70 290,30290,30

** otherother 1 459,301 459,30 1 465,001 465,00 1 459,301 459,30

DepreciationDepreciation 1 810,401 810,40 1 807,701 807,70 1 810,401 810,40

Operating profitOperating profit 2 705,702 705,70 -40%-40% 4 932,604 932,60 +27,3%+27,3% 6 281,006 281,00

Financial Financial expensesexpenses 1 041,201 041,20 1 409,801 409,80 1 041,201 041,20

Refinancing CapacityRefinancing Capacity 20%20% 560,00560,00

Profit before reserves and taxesProfit before reserves and taxes 1 837,701 837,70 -46%-46% 3 429,203 429,20 +36,4%+36,4% 4 679,804 679,80

Taxes and other Taxes and other provisionsprovisions 804,70804,70 1 692,301 692,30 1 283,001 283,00

Net ProfitNet Profit 1 033,001 033,00 -40%-40% 1 736,901 736,90 +96%+96% 3 396,803 396,80

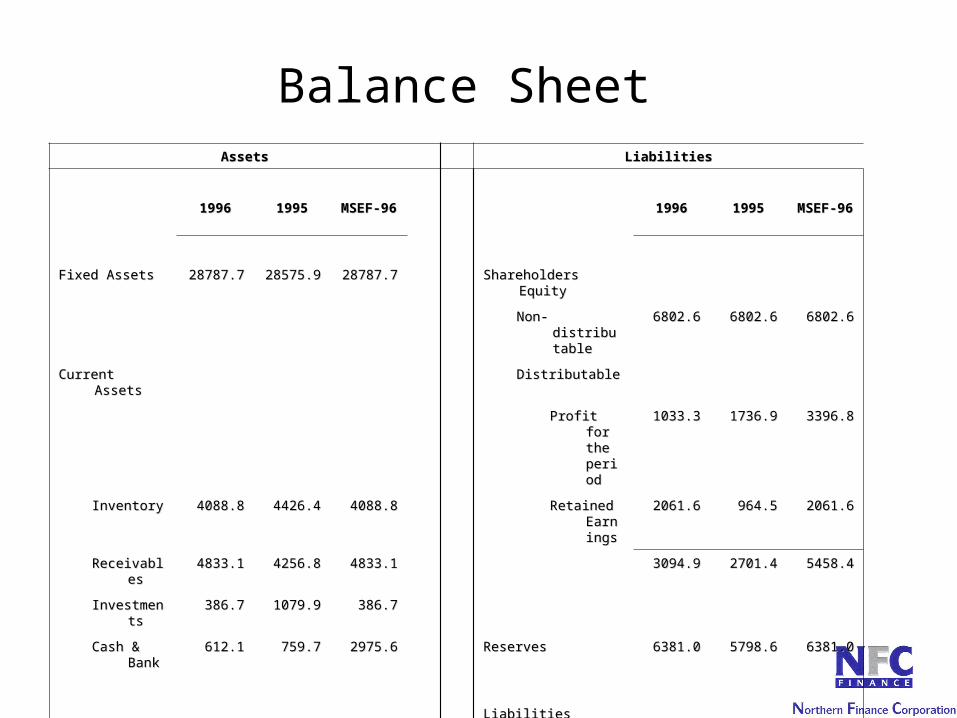

AssetsAssets LiabilitiesLiabilities

19961996 19951995 MSEF-MSEF-9696

19961996 19951995 MSEF-MSEF-9696

Fixed AssetsFixed Assets 28787.728787.7 28575.928575.9 28787.728787.7 Shareholders EquityShareholders Equity

Non-Non-distributadistributableble

6802.66802.6 6802.66802.6 6802.66802.6

Current AssetsCurrent Assets DistributableDistributable

Profit for Profit for the the perioperiodd

1033.31033.3 1736.91736.9 3396.83396.8

InventoryInventory 4088.84088.8 4426.44426.4 4088.84088.8 Retained Retained EarniEarningsngs

2061.62061.6 964.5964.5 2061.62061.6

ReceivableReceivabless

4833.14833.1 4256.84256.8 4833.14833.1 3094.93094.9 2701.42701.4 5458.45458.4

InvestmentInvestmentss

386.7386.7 1079.91079.9 386.7386.7

Cash & Cash & BankBank

612.1612.1 759.7759.7 2975.62975.6 ReservesReserves 6381.06381.0 5798.65798.6 6381.06381.0

LiabilitiesLiabilities

LongLong 12353.712353.7 16355.716355.7 12353.712353.7

CurrentCurrent 10073.210073.2 7440.47440.4 10073.210073.2

TOTALTOTAL 38705.38705.44

39098.39098.77

41068.41068.99

TOTALTOTAL 38705.38705.44

39098.39098.77

41068.41068.99

Balance Sheet

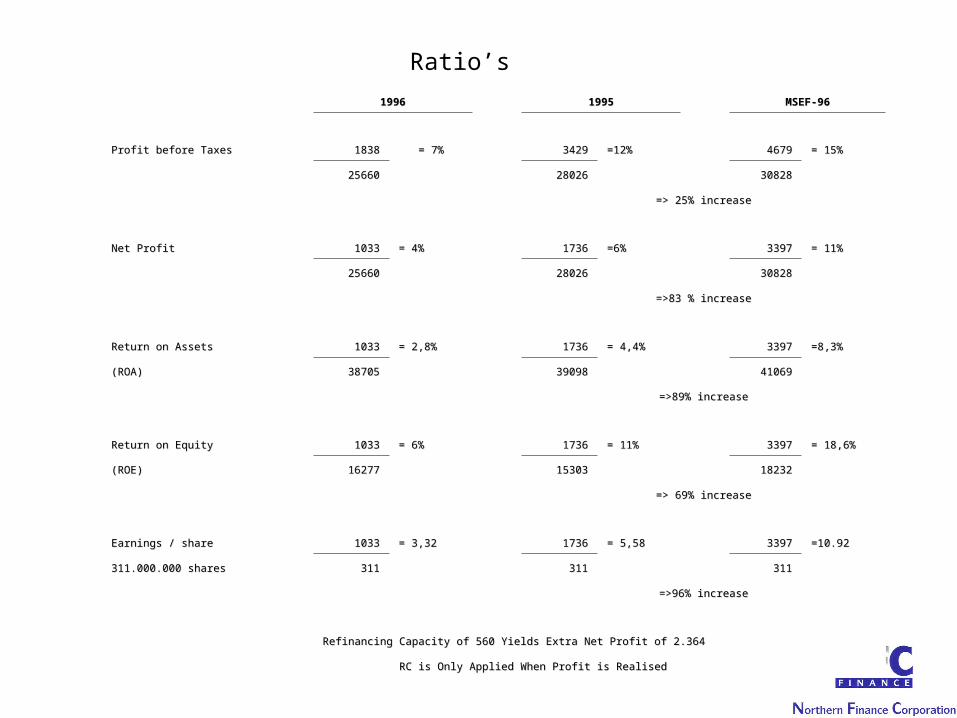

19961996 19951995 MSEF-96MSEF-96

Profit before TaxesProfit before Taxes 18381838 = 7%= 7% 34293429 =12%=12% 46794679 = 15%= 15%

2566025660 2802628026 3082830828

=> 25% increase=> 25% increase

Net ProfitNet Profit 10331033 = 4%= 4% 17361736 =6%=6% 33973397 = 11%= 11%

2566025660 2802628026 3082830828

=>83 % increase=>83 % increase

Return on AssetsReturn on Assets 10331033 = 2,8%= 2,8% 17361736 = 4,4%= 4,4% 33973397 =8,3%=8,3%

(ROA)(ROA) 3870538705 3909839098 4106941069

=>89% increase=>89% increase

Return on EquityReturn on Equity 10331033 = 6%= 6% 17361736 = 11%= 11% 33973397 = 18,6%= 18,6%

(ROE)(ROE) 1627716277 1530315303 1823218232

=> 69% increase=> 69% increase

Earnings / shareEarnings / share 10331033 = 3,32= 3,32 17361736 = 5,58= 5,58 33973397 =10.92=10.92

311.000.000 shares311.000.000 shares 311311 311311 311311

=>96% increase=>96% increase

Refinancing Capacity of 560 Yields Extra Net Profit of 2.364Refinancing Capacity of 560 Yields Extra Net Profit of 2.364

RC is Only Applied When Profit is RealisedRC is Only Applied When Profit is Realised

Ratio’s

How & When you win with How & When you win with MSEF®MSEF®

Available capacityAvailable capacity Desire for growthDesire for growth Accepted in market, offering real Accepted in market, offering real

choice as supplierchoice as supplier Variable cost margin, allows sufficient Variable cost margin, allows sufficient

leverage (Refinancing Capacity)leverage (Refinancing Capacity) Target turnover is significantTarget turnover is significant

MSEFMSEF®®

Cost of Idle CapacityCost of Idle Capacity Traditional « Sales Push » ApproachTraditional « Sales Push » Approach MSEF® MethodMSEF® Method Target customer motivations & Target customer motivations &

advantagesadvantages Financial impact of MSEF®Financial impact of MSEF® How & when you win with MSEF®How & when you win with MSEF®